Embed Size (px)

Citation preview

FACTS &

FIGURES of the

us. PLASTICS INDUSTRY

FACTS &

FIGURES of the

U.S. PLASTICS INDUSTRY

Text printed on recycled paper @ FACTS &I FIGURES is prepared annually by The Society of the Plastics Industry All inquiries regarding its content should be addressed to The Society of the Plastics Industry, Inc., 1801 K Street, N.W , Suite 600K, Washington, D.C. 20006.

0 1997 The Society of the Plastics Industry, Inc. All rights reserved. No part of this publication may be reproduced in any form without permission from SPI.

Released: September 1997

Price: $95.00 (SPI members); $190.00 (non-members)

he Society of the Plastics Industry, rnc. is a trade association of more than 2,000 members T representing all segments of the plastics

industry in the United States. SPl's business units and committees are composed of plastics processors, raw material suppliers, machinevy manufacturers, moldmakers and other industry-related groups and individuals. Founded in 1937, SPf serves as the "voice" ofthe plastics industvy.

SPI's mission is to promote the continued development of the plastics industry and enhance public understanding of plastics' contributions while meeting the needs of society

SPI represents the plastics industry before government bodies, the public and industry groups with which the plastics industry has marketplace relationships. SPI provides forums

Headquarters: 1801 K Street, N.W, Suite 600K Washington, DC 20006 (202) 974-5200

Northeast Regional Office: 400 W Cummings Park, Suite 6900 Woburn, MA 01801

Coleman, Betty

Midwest Regonal Office: 8600 West Bryn Mawr Avenue Suite 960-N Chicago, IL 60631

Faurot, Susan Czizik, Patti

that enable diverse interests within the industry to set policy and develop common goals and objectives, as well as programs to carry them out.

-

-

SPI communicates the value of the plastics industry and its products to various audiences. I t serves as a technical and information resource for the plastics industry, providing expertise, statistical data, publications and general industry information. SPI also sponsors two major industly trade shows: NPE and Plastics USA.

SPI's 36 business units and special committees serve the specialized needs of various industry segments such as materials, manufacturing processes and end markets. In addition, four regional offices serve member needs on a more localized basis.

Southern Regional Ofrice: Nations Bank Building, Suite 606 7 North Laurens Street Greenville, SC 29601

Sturgis, Richard A. Rastatter. Pamela

Westem Regional Office: 2151 Michelson Drive, Suite 240 Irvine, CA 92715

Capolupo, Frank Godwin, Mike Plummer. Debbie

New York Office: 355 Lexington Avenue New York,, NY 10017

he SPI Committee on Resin Statistics is composed of over 100 representatives from T plastics resin producing companies, trade

publications, industry -related professional organizations, and various agencies ofthefederal government. All members of the Committee are quite knowledgeable about the rapidly growing plastics industry and have a special interest in developing marketing and economic data.

The Committee is responsible for developing and maintaining a monthly report on the major plastics materials. This report shows monthly and cumulative data on production and sales &I use (including captive operations), with percent change from the previous year. It is the only detailed monthly report on plastics materials now available. Nearly one hundred producers participate in the monthly program, and are believed to

represent about 95% of total U.S. plastics production. Many of the materials covered reflect 100% industry coverage. The data are compiled by the Association Services Group, LLC, a business of the accounting firm Johnson Lambert & Co. located in Bethesda, Maryland.

The Committee is actively involved with various federal government agencies (International Trade Commission, Department of Commerce, Bureau of the Census, Federal Reserve, etc.), and assists them in developing and improving the plastics segments of their reports.

The Committee also is responsible for monitoring all resin data that appear in FACTS & FIGURES, thus ensuring the most accurate and timely data.

General Statistics Development of Today's Plastics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Introduction of Plastic Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Plastics Monomer Derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

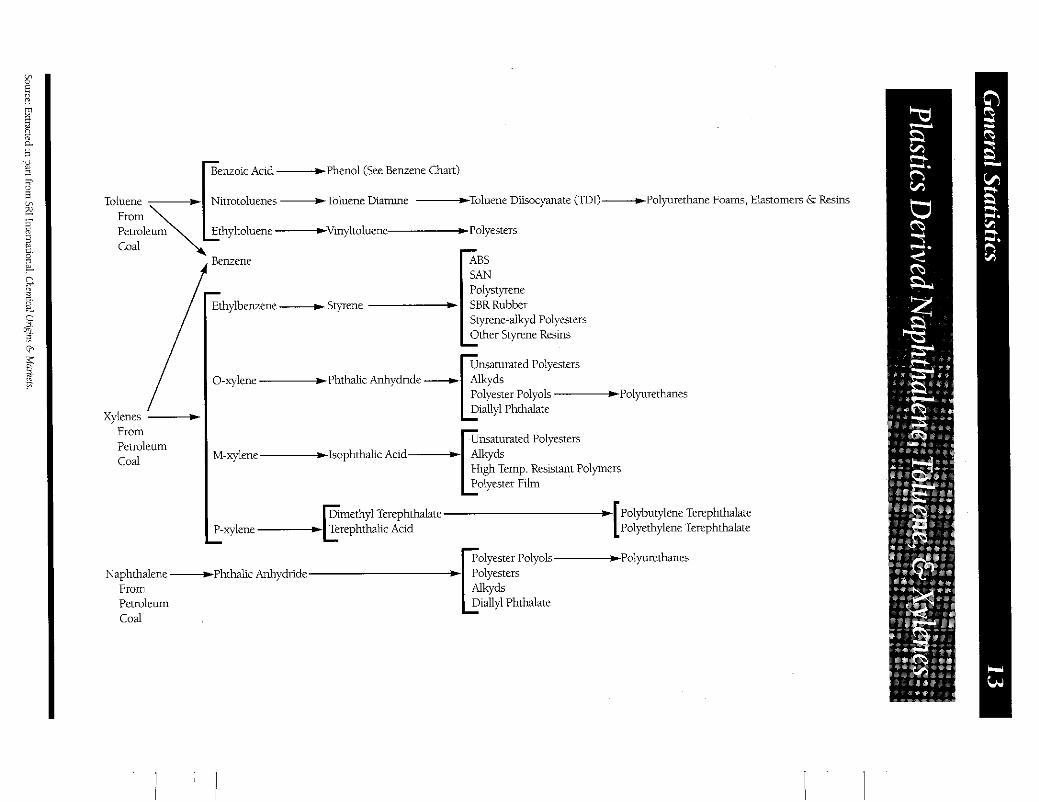

Ethylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Methane . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 Acetylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 Butadiene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Propylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Benzene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 Naphthalene, Toluene and Xylenes . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Plastics SIC Codes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Plastics Materials and Products Industry Trends . . . . . . . . . . . . . . . . . . . . . 16

Plastics Materials and Resins (SIC 2821) . . . . . . . . . . . . . . . . . . . . . . . 16 Miscellaneous Plastics Products (SIC 308) . . . . . . . . . . . . . . . . . . . . . . 16

Plastics Compared to Other Manufacturing Industries . . . . . . . . . . . . . . . . 17 Financial and Operating Ratios - Processing Industry . . . . . . . . . . . . . . . . . 18

Balance Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 Income Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 Statistical Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Major Markets Definitions of Major Market Categories . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Total Sales & Captive Use by Major Market (1992-1996) . . . . . . . . . . . . . 25 Percentage Distribution of Resins by Major Market . . . . . . . . . . . . . . . . . . 26

All Resins (1991-1996) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 Thermoset Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 Thermoplastic Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Major Market Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 Total Thermoset Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 Total Thermoplastic Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 Individual Plastics Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Resin Statistics Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

All Resins (1971-1996) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Individual Plastics Resins (1987-1996) . . . . . . . . . . . . . . . . . . . . . . . . 36

Domestic Merchant Sales by Plastics Resins . . . . . . . . . . . . . . . . . . . . . . . 39 Apparent U.S. Consumption of Selected Plastics Resins . . . . . . . . . . . . . . . 40

.

Resin Statistics Summary Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 46 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 47 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Unsaturated Polyester . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 48 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 49 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50 Production and Sales 6r Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 50 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 52 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Isocyanates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Polyether Polyols . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Polyester Polyols . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Polyurethane . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56 Sales by Material . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Epoxy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

Phenolic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

UreaandMelamine . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Thermodastic Resins 1 . Summary Statlstics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Latex Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61 ABSandSAN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 62 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

...

Engineering Thermoplastic Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 65 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

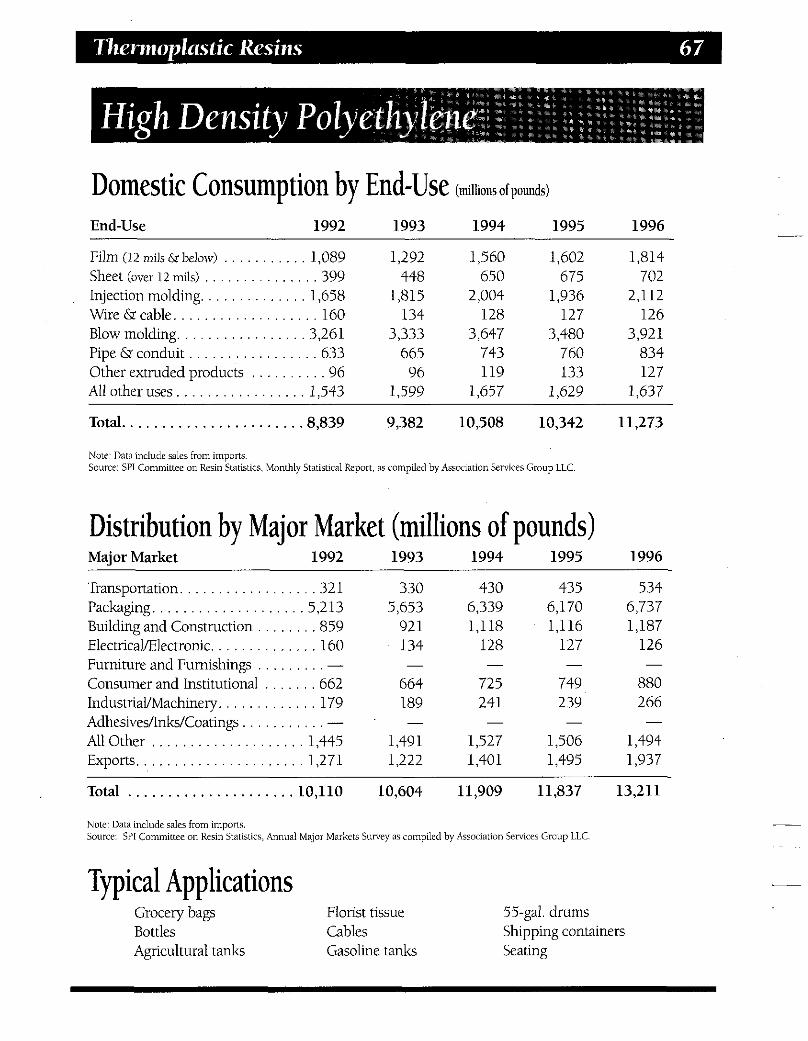

High Density Polyethylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66 Production and Sales 65 Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 66 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 67 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67 Distribution by Selected End-Uses . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

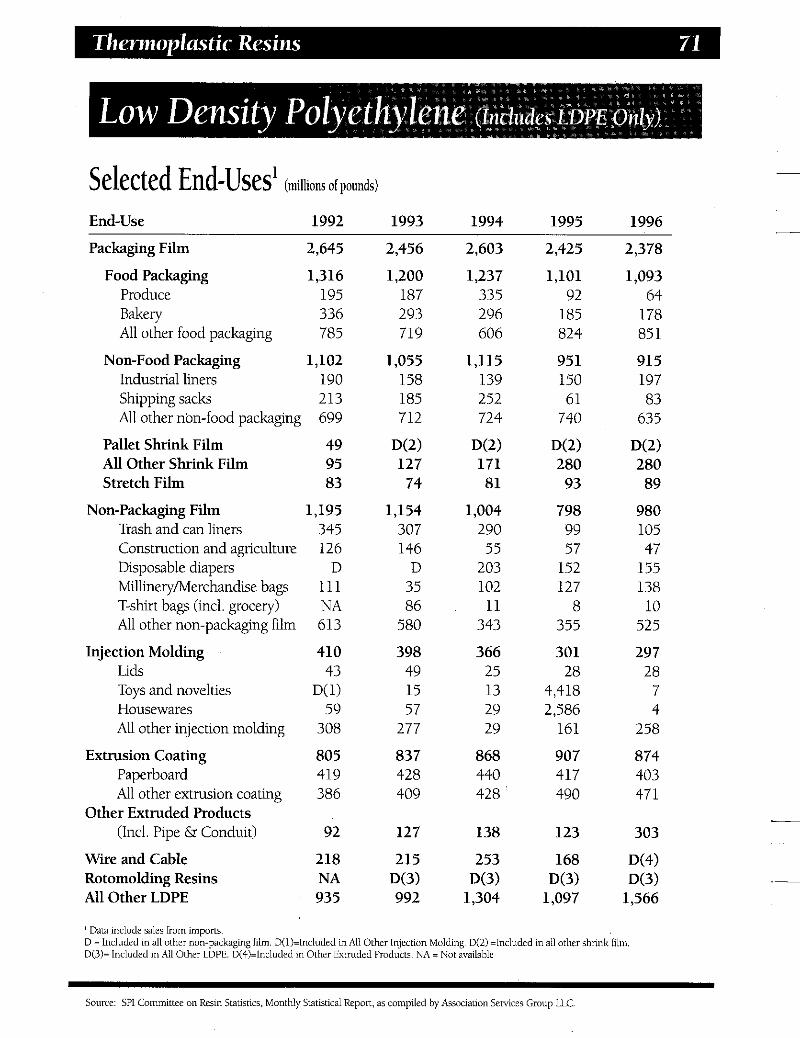

Low Density Polyethylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 70 Distribution by Selected End-Uses . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

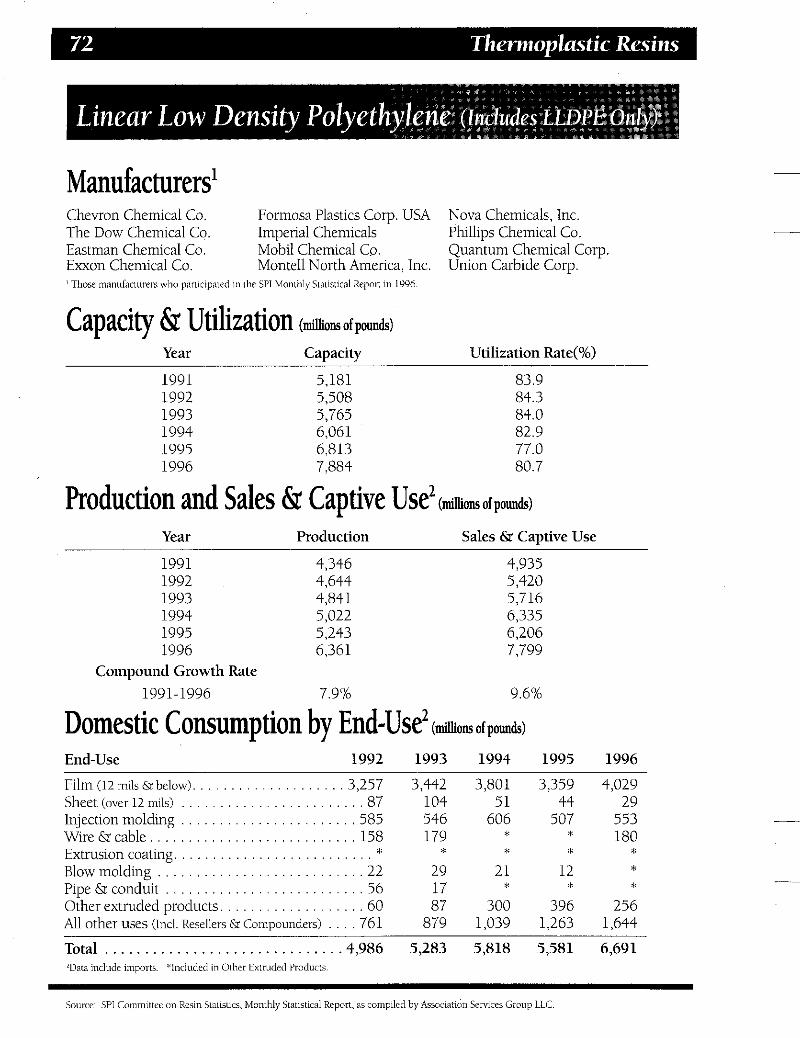

Linear Low Density Polyethylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Nylon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 70

Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Distribution by Selected End-Uses . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

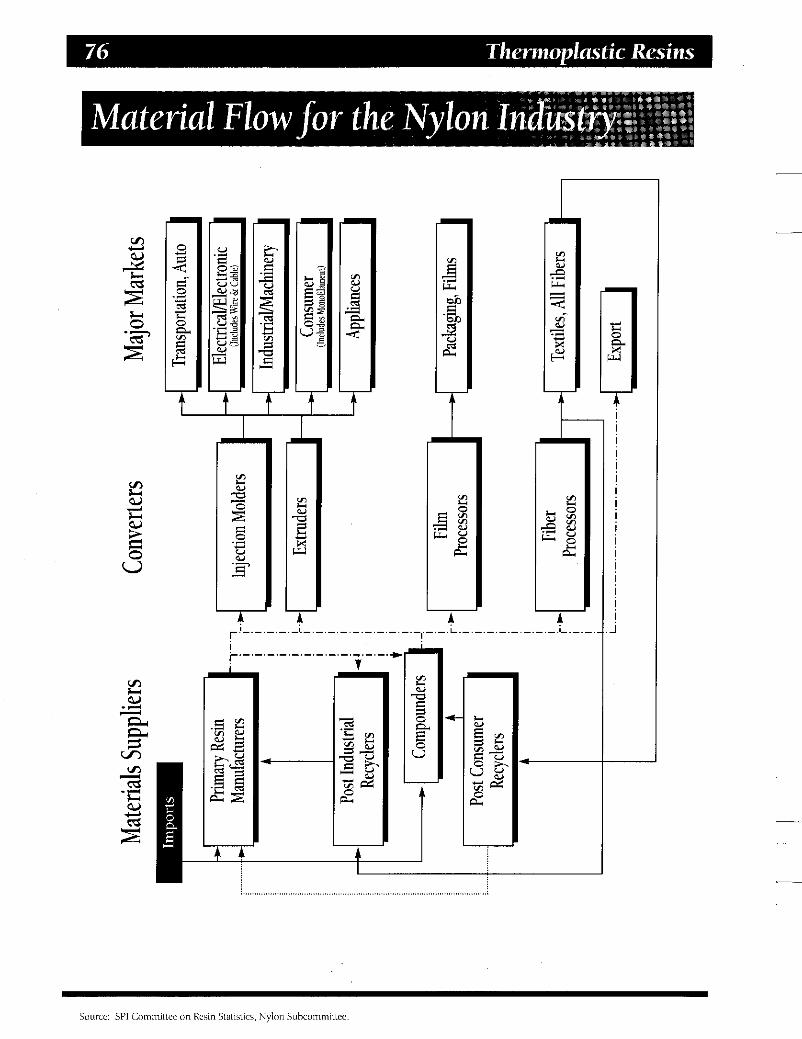

Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 75 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75 Material Flow Chart . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

Polystyrene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77 Material Flow Chart . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 78 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 79 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

.

Polypropylene . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 80 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 81 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Polyvlnyl Chloride . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 83 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

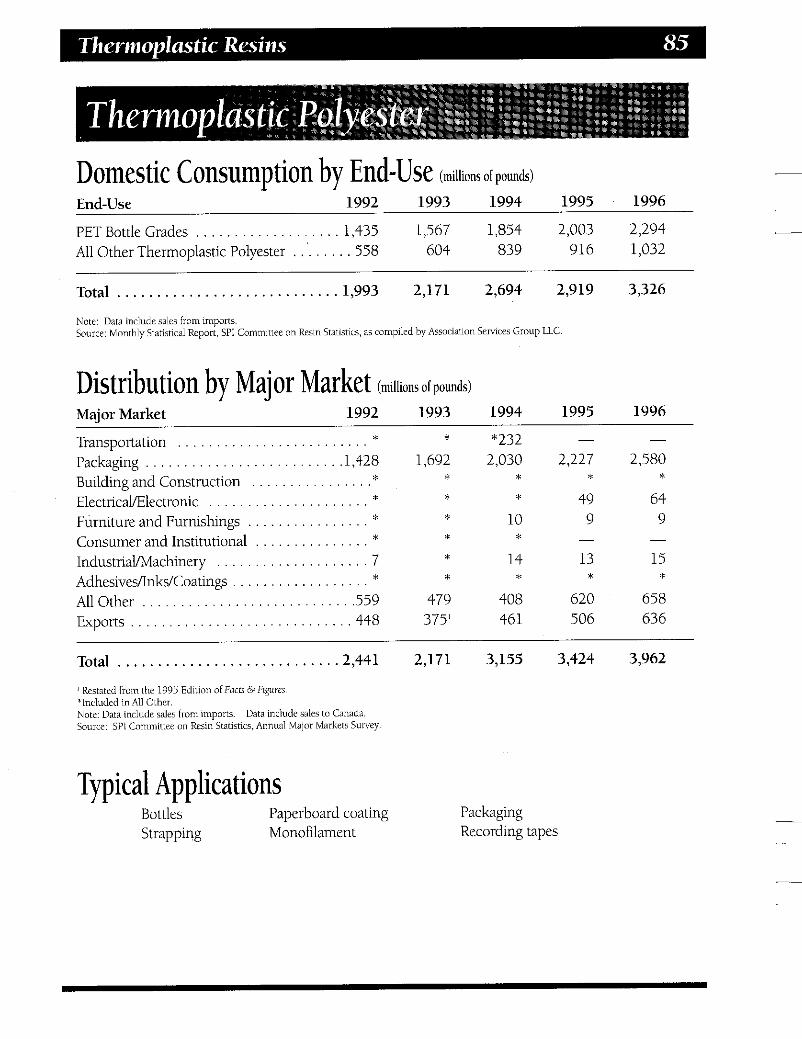

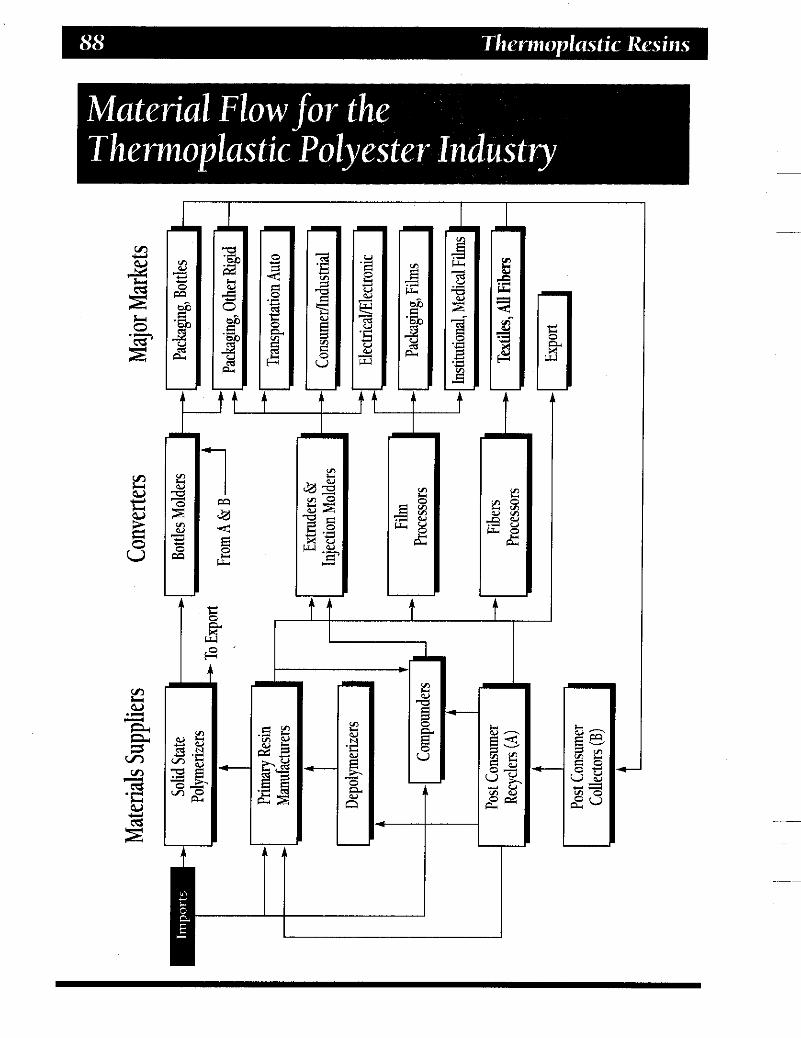

Thermoplastic Polyester . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84 Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84 Capacity and Utilization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84 Production and Sales & Captive Use . . . . . . . . . . . . . . . . . . . . . . . . . . 84 Domestic Consumption by End-Use . . . . . . . . . . . . . . . . . . . . . . . . . . 85 Distribution by Major Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85 Typical Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85 Material Flow Diagram . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

by Process Grade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

Capacity and Utilization . . . . . . 80 . . . . . . . . . . . . . . . . . . . . . . . . . . .

Domestic Sales and Captive Use of Selected Thermoplastics

Integrated Solid Waste Management v .

The American Plastics Council. . . . . . . . . . . . . . 90 PlasticsRecycling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91 Municipal Solid Waste . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

Flow Chart: Raw Material to Finished Product . . . . . . . . . . . . . . . . . . . . . 94

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

Fabricated Plastic Products Composites . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

Shipments by Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95 Vinyl Siding and Soffit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

U.S. Shipments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96 Participating Producers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

.

Processing & Machinery Description of Processing Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98 Shipments of Plastics Machinery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Injection Molding Machinery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101 Single Screw Extrusion Machinery . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Glossary

Other Sources of Plastics Information

Additives for Plastics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105 Definitions of Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107 Definitions of Selected Plastics Properties . . . . . . . . . . . . . . . . . . . . . . . . . 114

Business Consulting Groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121 Government Publications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121 Newspapers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122 Trade Associations and Professional Organizations . . . . . . . . . . . . . . . . . 122

. . . . . . . . . . . . . . 122 Trade Publications . . . . . . . . . . . . . . . .

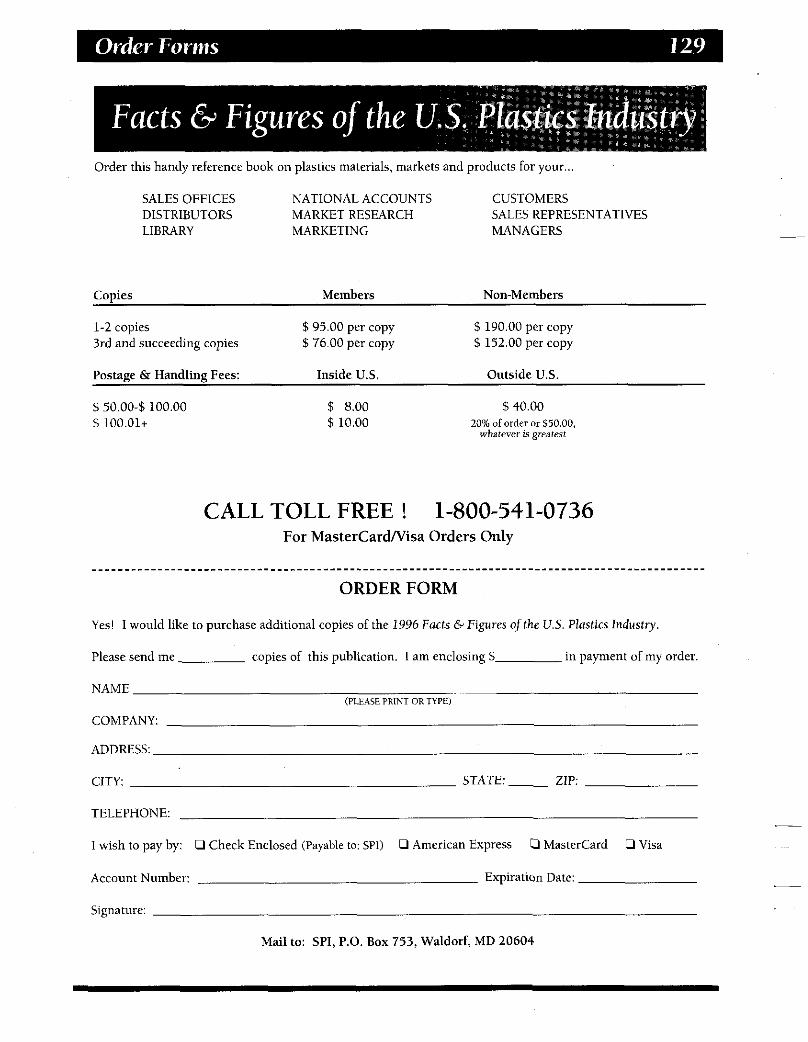

Order Forms Monthly Statistical Report . Resins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125 Facts & Figures of the U.S. Plastics Industry . . . . . . . . . . . . . . . . . . . . . . 129

Index Index . . . . . . . . . . . . . . . 133

!

i

i

day’s plastics are one of the most used materials on a volume basis in U.S. T industrial and commercial life. Plastics are

broadly integrated into today’s lifestyle and make a majol; irreplaceable contribution to virtually all product areas. Although the plastics industvy in the United States is now in its second centuvy, the most important developments have occurred since 1910. However; the roots ofthese modern developmentsgo back not only to the research of cellulose nitrate byJohn Wesley Hyatt in the 1860s, but also to the plastic-like compositions used by man through the centuries.

Following work by Pelouze, Schonbein established conditions of controlled nitration of cellulose. The product soon became of interest as an explosive and in the manufacture of collodion, a cellulose solution in an alcohol-ether mixture. In the 1850s, the English inventor Alexander Parkes observed that the solid residue left after the evaporation of the solvent of photographic collodion was a “hard, horny elastic and waterproof substance.” In 1856, he patented the process of waterproofing woven fabrics by the use of such materials.

Origin of Plastics One can go as far back as the Old Testament to find references about natural materials used as fillers, adhesives, coatings, and the like. These materials were the precursors of modem plastic materials. Historians continue to differ as to the exact year or decade that the plastics industry began because the definition of “plastic” is a matter of interpretation.

Certainly, the history of the rubber industry has a bearing on plastics. This is because ebonite, or hard rubber, discovered in 1851, was the first thermosetting material to be prepared and the first material that involved a distinct chemical modification of a natural material. But ebonite was not exploited commercially for some years after its discovery; for that reason, its historical importance has become somewhat blurred.

European Developments While the basic processes of rubber technology were developing, other important discoveries were taking place in Europe.

In 1862, at the Great Exhibition in London, Parkes introduced a new material named for himself- Parkesine. Parkesine was obtained by dissolving cellulose nitrate in a minimum of solvent. The mixture was then put on a heated rolling machine from which some of the solvent was then removed. While still in the plastic state the material was then shaped by dies or pressure. In 1866, Parkes organized the Parkesine Company to manufacture products from his new material, but the company failed in 1868. This appears to be due, in part, to Parkes’ attempt to reduce production costs that resulted in the production of inferior items.

One year after the failure of the Parkesine Company, an associate of Parkes, Daniel Spill, formed the Xylonite Company to manufacture products similar to Parkesine. Once again, economic failure resulted and Spill’s company went bankrupt in 1874. Undaunted, Spill moved to a new site, established the Daniel Spill Company, and continued production of his material, Xylonite.

First Plastics in the U.S. n the United States during the I860sJohn Wesley Hyatt experimented with cellulose I nitrate. In 1865, Hyatt became involved in

devising a methodfor producing billiard balls from materials other than ivory. Originally using mixtures ojcloth, ivory dust, and shellac, he patented in 1869 the use of collodionfor coating billiard balls. The patent came one year after his collodion material was introduced commercially.

John W Hyatt and his brother Isaiah took out U.S. Patent 105,338 in 1870 for a process of producing a horn-like material using cellulose nitrate and camphor. Although Parkes and Spill had mentioned camphor in their work, the Hyatt brothers recognized the value of camphor as a plasticizer for cellulose nitrate. In 1872, the term “celluloid was coined by Isaiah Hyatt to describe the Hyatts’ commercially successful product.

The validity of Hyatts’ patents was challenged by Spill, and a number of court actions took place between 1877 and 1884. In the final action, it was found that Spill had no claim on the Hyatt brothers’ patents, the judge ruling that Parkes was the true inventor of the process because he had mentioned the use of camphor in his patents. Thus, there was no restriction on the use of these processes and any company, including the Hyatts’ Celluloid Manufacturing Company, was free to use them. After that decision, the Celluloid Manufacturing Company prospered, changed its name to the American Cellulose Chemical Corporation, and eventually was absorbed by the Celanese Corporation.

Formaldehyde Resins ext to cellulose nitrate, the most important material in the early history ofplastics was Nf ormaldehyde. Around 1897 there was a

demand in German schoolsfor a white chalkboard. Efforts to obtain such a product resulted in the discovery of casein plastics, produced by reacting casein (milk protein) with formaldehyde. The material soon became established under the trade names of Galalith and Erinoid. Today, casein still is used by the button industry

In 1899, Arthur Smith took out British Patent 16,275, the first dealing with phenol- formaldehyde resins for use as an ebonite substitute in electrical insulation. During the next decade, the phenol-formaldehyde reaction was investigated mainly for academic interest. In 1907, however, Leo Hendrik Baekeland discovered techniques to control and modify the reaction so that useful products could be made from it. Thus, phenolics were the first fully synthetic resins to become commercially successful.

Prompted by the success of phenolic moldings, research began on reacting other materials, such as urea and thiourea, with formaldehyde. These materials were used to manufacture molding powders. Unlike phenolics, they could be molded into light- colored articles and rapidly achieved commercial success. Today, these urea-based resins are used for molding powders, adhesives, and textile and paper finishing, while the related melamine-formaldehyde resins are used in decorative laminates.

Growth of Modern Plastics ellulose acetate, a themoplastic, was developed about the same time as the urea- C based resins. Similar in structure to cellulose

nitrate, it wasJuund tu be safer to process and use. Cellulose acetate was introduced as a molding compound in 1927.

The period 1930-1940 saw the initial commercial development of today's major thermoplastics: polyvinyl chloride, low density polyethylene, polystyrene, and polymethyl methacrylate. The advent of World War I1 in 1939 brought plastics into great demand, largely as substitutes for materials in short supply, such as natural rubber. In the United States, the crash program leading to large-scale production of synthetic rubbers resulted in extensive research into the chemistry of polymer formation and, eventually, to the development of more plastic materials.

The first decade after World War I1 saw the development of polypropylene and high density polyethylene and the growth of the new plastics in many applications. Linear low

density polyethylene was introduced in 1978 and made it possible to produce polyethylenes with densities ranging from 0.90 to 0.96. Large-scale production of these materials reduced their cost dramatically, The new materials began to compete with the older plastics and even with the more traditional materials such as wood, paper, metal, glass, and leather. The introduction of alloys and blends of various polymers made it possible to tailor properties to fit certain performance requirements that a single resin could not provide. The demand for plastics has increased steadily; plastics are now accepted by designers and engineers as basic materials along with the more traditional materials. The automotive industry, for instance, relies on plastics to reduce weight and thus increase energy efficiency

YEAR MATERIAL EXAMPLE 1868 . . . . . . . . . . . . . . . . . . . Eyeglass Frames 1909 . . . . . . . . . . . . . . . Phenol-Formaldehyde . . . . . . . . . . . . . . . . . . . Telephone Handset

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Electrical Bases . . . . . . . . . . . . . . Toothbrushes

1929 . . . . . . . . . . . . . . . Urea-Formaldehyde. . . . . . . . . . . . . . . . . . . . . Lighting Fixtures

1936 . . . . . . . . . . . . . . . Acrylic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Brush Backs 1935 . . . . . . Ethyl Cellulose . . . . Flashlight Cases

1936 . . . . . . . . . . . . . . . Polyvinyl Acetate. . . .

1938 . . . . . . . . . . . . . . .

1939 . . . . . . . . . . . . . . . Polyvinylidene Chloride . . . . . . . . . . . . . . . . . Packaging Film . . . . . . . Melamine-Formaldehyde . . . . . . . . . . . . . Unsaturated Polyester

. . . . . . . . . . Low Density Polyethylene . . . . . . . Fluoropolymers . . . . .

Epoxy . . . . . . . . . . . .

1943 . . . . . . . . . . . . . . . Silicone Motor Insulation Cellulose Propionate . . . . . . . . . . . . . . . . . . . . Pens and Pencils

Acrylonitrile-Butadiene-Styrene (ABS) . . . . . . Luggage Styrene-Acrylonitrile (SAN) . . . . . . . . . . . . . . . Housewares Polyurethane . . . . . . . . . . . . . . . . . . Foam Cushions

. . . . Tools and Jigs

1956 . . . . . . . . . . . . . . . Acetal. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Automotive Parts 1957 1957 . . . . . . . . . . . . . . . Polypropylene . . . . . . . . . . . . . . . . . . . . . . . . . Safety Helmets

. . . High Density Polyethylene . . . . . . . . . . . .

. . . . . Polycarbonate . . . . . . . . Appliance Parts

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Skin Packaging

Valves and Fittings Bottles

Battery Cases

Adhesives and Coatings

1964 . . . . . . . . . . . . . . . Polyphenylene Oxide Polymide. . . . . . . . . . . . . . . . . . . . . . . . . . . . . Bearings

. . . . . . . . . . . . . . . . . . ElectricaVElectronic Parts r . . . . . . . . . . . . . . . . . ElectricaVElectronic Parts

. . . . . . Polybutylene . . . . . . . . . Piping 1973 . . . . . . . . . . . . . . . Polyphenylene Sulfide . . . . . . . . . . . . . . . . . . . Telecommunications

1975 . . . . . . . . . . . . . . . . . . . . . Polyethersulfone . . . . . Printed Circuit Boards

Nitrile Barrier Resins . . . . . . . . . . . . . . . . . . . . Non-food Packaging

Polyetherimide . . . . . . . . . . . . . . . . . . ElectricaVElectronic Parts Linear Low Density Polyethylene . . . . . . . . . . Extruded Film

1983 . . . . . . . . . . . . . . . Polyetheretherketone. . . . . . . . . . . . . . . . . . . . Wire and Cable 1984 . . . . . . . . Aromatic Copolyester . . . . ElectricaVElectronic Parts 1985 . . . . . . . . . . . . . . . Liquid Crystal Polymers ElectricaVElectronic Parts 1988 . . . . . . . . . . . . . . . Polymethylpentene . . . High Temp.mransparent

Polyethylene Naphthala Films,Containers, Bamer Resin

rE thylene From Refinery Gas Liquefied Petroleum Gases Liquid Hydrocarbons

__

E SBR Rubber Styrene-butadiene Copolymers Styrene-alkyd Polyesters Polystyrene -I Other Styrene Resins

Ethylbenzene --f Styrene

High Density Polyethylene + Law Density

EthyleneNinyl Acetate Copolymers

I Linear Low Density

Ethylene Glycol - Polyethylene Terephthalate

Tnethylene Glycol }+{ Polyesters Diethylene Glycol

Ethylene Oxide +

Propylene Copolymers Linear Alpha-olefins + Linear Low-density Polyethylene

Ethylene-propylene Elastomers

Polyester Polyols -Polyurethanes { Propionic Acid - Cellulose Acetate Propionate Trimethylolethane -Alkyds

Propionaldehyde +

{ Trichloroethane---bVinylidene Chloride -Polpnylidene Chloride Ethylene Dichloride -+ Vinyl Chloride- Polynnyl Chloride & Copolymers

Polyvinyl Butyral Polyvinyl Formal

Acetic Acid Cellulose Acetate+ Copolymers Acetaldehyde - Vinyl Acetate {Polyvinyl Acetate+Polyvinyl Alcohol-

Polyvinyl Butyral Polyinyl Formal Polyvinyl Acetate -Polyvinyl Alcohol

Other Copolymers Vinyl Acetate --r, EthyleneNinyl Acetate Copolymers

Vinyl Toluene -Polyesters

- ~~~~~

Source: Extracted in pan irom SRI Intemational, Chemical Origins G Markets.

Source. Exrracted in part from SRI Intemationsl, Chumical Origins & Markcti

3 0

L L 2 1 i 0 a

i

8 3 c7

_-

Source: Exlrmed ~n part tmni SRI Intematv". Chrmical Ongins 0 Murkeh.

Butadiene D From:

Olefin Coproduct Butylene Dehydrogenation

I I

- ABS

Styrene-butadiene Latexes

Adiponitnle P H e x a m e t h y I e n e d i a m e - Bamer Resins

MBS (Impact Modifien)

SBR Rubber

Polybutadiene Rubber

Thermoplastic Elastomers

Cyclododecatnne - 1, 12 - Dodecanedioic Acid

- Nylon 66

Nylon 612

Hexmethylem -

Nylon 612

: Diisocyanate -Polyurethanes

Source: Extracted in part from SRI Intemational. Chemical O@inr 0 Markets.

-r

I

Source. Extracted in pan Iron? SRI Imcmmonal, Chemical Ongm DMarkeli .

Benzoic Acid -Phenol (See Benzene Chart)

Toluene - Nitrotoluenes -Toluene Diamine -Toluene Dilsocyanate (TDI)-Polyurethane Foams, Elastomers 6s Resins From \[ Petroleum Ethyltoluene -Vinyltoluene-Polyesters Coal

/i:b:mene - Styrene - PoIystFene

Styrene-alkyd Polyesters

Polyester Polyols -Polyurethanes Diallyl Phthalate

0-xylene -Phthalic Anhydride

Xvlenes - Unsaturated Polyesters I M-xvlene-Isoohthalic Acid-Lkds

From Petroleum ,.,

I coal High Temp. Ramant Polymers

Polybutylene Terephthalate Polyethylene Terephthalate

Dimethyl Terephthalate P-xylene - Terephthalic Acid

Polyester Polyols -Polyurethanes * Polyesters

I C L W s

Naphthalene -Phthalic Anhydride From Petroleum Diallyl Phthalate Coal

I 1 I ' I

The Plastics Industrv I

and SIC Codes he Standard Industrial Classijcation (SIC) is a numerical system developed by thefederal T government to classiJy the total economy

into different industry segments. It is a classijcation of establishments’ by type of economic activity in which they are engaged. Its puyposes are (1) to facilitate the collection, tabulation, presentation, and analysis of data relating to establishments and (21 to promote unformity and comparability in the presentation of statistical data collected by various agencies of thefederal government, state agencies, trade associations, and private research organizations.

Among the uses for the SIC system, the two- and four-digit SIC codes are the basis for agencies such as EPA and OSHA to target certain industry segments for regulatory activity

The History of SICS The SIC system was inaugurated in 1945 and at first covered only manufacturing industries. Four years later, the program was revised and enlarged to include all sectors of economic activity

Periodically since then the program has been refined further to reflect changes in the composition and structure of the U.S.

economy The incorporation of these changes and updates takes place about every five years. Changes may include refinements in industry detail or coverage, improvements in industry definitions, or clarification of industry classifications.

Major revisions, such as the addition of new industry codes, occur only once every 10 years. The 1987 edition of the Standard Industrial Classification Manual that was released in May 1989 reflects such a major revision that affects the plastics industiy

What’s New According to the Office of Management and Budget, the 1987 SIC revision has taken into account technological changes; institutional changes such as deregulation in the banking, communications, and transportation industries; and the tremendous expansion in the service sector.

For the plastics industry this revision includes the division of “miscellaneous plastics products” into nine separate SIC industry codes as opposed to the single listing for that category (3079) that had been in existence since 1947. The breakdown reflects the tremendous growth of the plastics industry and was intended to allow the industry to keep track of more detailed statistics.

‘An establishment is a single location at which economic actwily (i E . manufacturing) t a l e place. 11 is s)monymous with ‘‘plani;

How It Works 1987 Census of In most of these publications, each project or service is identified by a seven-digit code. This classification system operates so that the industrial coverage is progressively narrower with the successive addition of digits.

Classification of Major Industries

SIC Code Economic Division 01,02,07-09 Agriculture, Forestry, Fishing

10-14 Mining 15-17 Construction 20-39 Manufacturing* 40-49 Transportation, Public Utilities 50-51 Wholesale Trade 52-59 Retail Trade 60-67 Finance, Insurance, Real Estate 70-89 Services 91-97 Public Administration

Manufactures and the Plastics Industry New industry data include the addition of the nine new codes that have now replaced the single four-digit listing (3079) for "miscellaneous plastics products."

Industry Code 3081

3082

3083

3084 3085 3086 3087

3088 3089

Description

Unsupported plastics film &

Unsupported plastics profile

Laminated plastics plate, sheet &

Plastics pipe Plastics bottles Plastics foam products Custom compounding of

purchased resins Plastics plumbing fixtures Plastics products, not elsewhere

sheet

shapes

profile shapes

classified

* Plasacs fall under "Manufactunng".

Plastic Materials & Resins (SIC 2821) (millionsofdollars)

1994

Percent Change

1995 1994-95

Industry Data Value of shipment9 37,305 43,529 Total employment (000) 68.9 69.7 Production workers (000) 40.4 41.5 Average hourly eamings ($) 19.39 19.96 Capital expenditures 2,536 2,337

16.7 1.2 2.7 2.9

-7.7

Miscellaneous Plastics Products (SIC 308) (millions of dollars )

Percent Change

1994 1995 1994-95

Industry Data Value of shipmentsi 100,837 Total employment (000) 730.2 Production workers (000) 572.8 Average hourly eamings ($) 10.36 Capital expenditures 4,597.8

108,555 763.4 599.4 10.47

5,433.3

' Value of all products and S ~ M C C S sold by establishments in the plastics material and resin industry 'Value of all produas and seMccs sold by establishments in the mix plastics products.

7.7 4.5 4.6 1.1

18.2

Source: U.S. Department of Commerce. Bureau of the Census, Economics & Sratisucs Administration

Relative 1995Rank SIC Industry

1995' Industry

Shipments (Mil. Dollars)

1 2 3 4

* 5

6 7 8 9 10

11

13 14 15

* 12

16 17 18 19 20

3711 26

2911 367 308

3714 331 3674 275 2834

3721 2821 2711 3812 3663

2015 2653 281 3577 3761

Motor vehicles & car bodies Paper & allied products Petroleum refining Electronic components 6s accessories Misc. plastics products, n.e.c.

Automotive parts & accessories Steel mill products Semiconductors Commercial printing Pharmaceutical preparations

Aircraft Plastics materials & resins Newspapers Search and navigation equipment Radio and TV communications equipment

Poultry slaughtering and processing Corrugated and solid fiber boxes Industrial inorganic chemicals, exc. pigments Computer peripheral equipment Guided missiles and space vehicles

' Most rccent actual data available from the Orpartmen1 n i Commerce ~ .

$200,939 172,638 136,023 119,288 108,555

107,417 74,547 65,623 65,093 57.943

49,504 43,529 37,732 29,435 29,360

28,887 27,521 26,722 14,719 14,315

Source U 5. Depailment of Commcrce, Rurcau ofthe Census, Economics & Statistics Administration

- -~

Plastics Processing Industry - 1996 BALANCE SHEET‘ TOTAL

Cash and Marketable Securities . . . . . . . . . . . . . . 3.4 Accounts Receivable . . . . . . . . . . . . . . . . .21.8

. . . . . . . . . . . . . . . . -0.8

TOTAL CURRENT ASSETS . . . . . . . . . . . . . . . . . ,43.3 12.4

Other Currenl Ass . . . . . . . .

Land and Buildings (net of depreciation) Machinery, Equipment and Tooling (net o

depreciation) . . . . . . . . . . .27.0 Other Long Term Assets . . . . . . . . . . . . . . . . . . . . . . . 17.3 TOTAL ASSETS .......................... 100.0

Accounts Payable . . . . . . . . . . . . . . Other Current Liabilities . . . . . . . . . Current Portion of Long Term Debt

Deferred Income Taxes . . . . . . . TOTAL CURRENT LIABILITIES . . . . . . . . . . . . . .21.1

. . . . 1.1

TOTAL LIABILITIES . . . . . . . . . . . . . . . . . . .45.4 EQUITY (NET WORTH) .................... .54.6 TOTAL LIABILITIES and NET WORTH , . , . . , . 100.0 INCOME STATEMENT’

Long Term Liabilities (less current portion) . . . . 22.5

$5MM

7.0 28.3 14.3 7.1 1.0 5.3

-0.2 2.5

52.1 18.9

26.6 2.4

100.0 9.5 9.5 5.5

24.5 0.4

40.1 66.4 33.7

100.0

S. ,LES 5-10MM

7.1 27.0 23.4 11.5 6.3 6.5

-0.6 1.9

59.3 7.7

32.0 1.0

100.0 13.9 11.5 5.4

30.7 0.1

10.9 41.7 58.3

100.0

~

__

~

ILUME 10-25Mk

6.2 23.4 14.6 7.5 1.2 6.3

-1.4 2.0

46.3 14.4

31.9 7.4

100.0 10.3 13.8 4.4

28.5 1.8

20.1 51.3 48.7

100.0

NET SALES (1) ........................... 100.0 Direct Materials . . . . . . . . . . . . . . . . . . . . . . . . .45.8 Direct Labor . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8.7 Indirect Labor . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.2

Depreciation Expense . . . . . . . . . . . . . . . . . . . . . .3 .5 Other Manufacturing Expense . . . . . . . . . . . . . . 10.1

Inventory Revaluations &LIFO Adjustments . . . . . . . -0.1 Total Production Related Expenses (COGS) . . . . . 78.1 GROSS MARGIN ......................... .21.9

Sales Salaries, Commissions, Fringe Benefits , , , . 2.9 Other Selling Expense . . . . . . . . . . . . . . . . . . . . . 1.9 Administrative Expense . . . . . . . . . . . . . . . . . . . : 7.3 (includes Engineering & R&D Salaries)

Total Non-Production Related Expenses . , . . , . , . 12.1

Manufacturing Personnel Fringe Benefits . . . . . . . 3.9

100.0 36.4 13.2 5.3 3.1 4.0

14.7 -0.1 76.6 23.4

4.0 1.2

14.4

19.6

100.0 39.0 14.0 6.8 4.6 2.6

13.2 -0.1

80.1 19.9 2.6 0.8

10.6

14.0

(1) Not all companies surveyed responded to every question; therefore. some details may not sum to totals. ‘Average as a percent of Total h e & . I Average as 8 percent of Net Sales.

100.0 40.9 8.8 7.0 4.7 4.2

13.3 -0.1 79.0 21.0

3.3 1.7 9.7

14.7

4 2 5 M M

2.0 19.7 12.8 5.1 0.8 5.3

-0.9 5.6

40.0 10.6

25.5 23.9

100.0 11.4 4.0 2.2

17.5 1.0

28.7 48.0 52.0

100.0

100.0 48.6 7.6 5.4 3.2 3.1 8.1

-0.1 76.9 23.1

2.7 2.3 5.0

10.0

Income Statement' (continued from page 17) Total

OPERATING PROFITRBIT Interest Expense (Income) Other Expense (Income)

PROFIT BEFORE INCOME TAXES Income Taxes

PROFIT AFTER INCOME TAXES

Under $5MM- $10MM- $5MM $10MM 525MM

-

Statistical Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Net SaIedAverage I

Number Employees

Value Added per Employee . . . . . . . . . . . .

Net Sales per Employee Hour. . . . . . . . . . . .

Value Added per Employee

Net Sales per Production Worker Hour. . , .

Value Added per Production Worker

Total Employment CosWNet Sales. . . . . . . .

Production Worker Emp. CosWNet Sales . .

Production Worker Emp. CostsRbs. Proc.. ,

Total Employment CostsRbs. Processed . . .

Total Production Related ExpenseiLb. Proc.

Productive Machine HrdAvail. Mach. Hrs.. ,

Inventory Tumover (times) . . . . . . . . . . . . .

Average Collection Period (days) . . . . . . . . .

Asset Turnover (times) , , , , , , , , , , , , . , , , ,

Return on Equity (after tax) . . . . . . . . . . . . .

Retum on Invested Capital (before tax) . . . .

Percent Change in Net Sales (1995-1996) . . . . . . . . . . . . . . . . . . .

- -

N

98

98

90

90

89

89

98

38

79

79

79

90

96

98

97

34

26

-

28 -

- -

Total

133,353

672,216

$64

$34

$85

$46

25.9%

18.8%

$0.31

$0.43

$1.34

54.0%

9.0

48

1.6

15.9%

16.5%

~

9.2%

9.9 1.4 0.3 8.2 2.7 5.5

- -

N

28

24

19

19

19

19

24

24

20

20

20

22

23

24

23

22

23

-

24 -

4.1 2.0 0.3 3.6 1.5 2.1

Under $5MM

b81,377

651,463

$45

$29

$60

$38

32.5%

21.5%

$0.63

$0.94

$2.26

41.5%

8.0

47

1.3

8.3X

6.6%

8.4%

- -

N

16

16

15

15

15

15

16

16

11

11

__

11 13

15

16

16

15

15

L6 -

6.3 0.7

-0.4 6.0 1.6 4.4

$5MM- $10MM

;86,950

i52,929

$42

$26

$51

$31

34 8%

25.3%

$0.81

$1.14

$2.75

51.9%

8.4

38

1.2

17.5%

18.4%

11.1%

- -

N

2 i

27

2:

25

24 24

27

27

21

2 1

-

21 25

27

27

17

17

27

27 -

6.4 1.4

-0.4 5.4 2.2 3.2

$10MM- 25MM

i118,187

$69,833

$56

$33

$73

$43

30.0%

20.5%

$0.36

$0.53

$1.46

54.3%

8.5

54

1.6

10.3%

11.5%

8.8%

N = Number or operating plants included m calculation. 2 Each avcragc LS calculated using only those companies providing data necessary for the spcciiled calcuisticr.

Source: SP1 Financial & Operaling Ratios Survey.

______

Plastics Processing Companies by Percent

Factory Overhead 25.2 ' Includes CUSlOl" processors and propric,ary pr"CfsS0".

L

he primary product groupsfor each Major Market category are listed below: T

Transportation Motor Vehicles and Parts: including autos, trucks, buses, motorcycles, and bicycles All Other: including railroad equipment, travel trailers, campers, golf carts, snowmobiles, aircraft, military vehicles, ships, boats, and recreational vehicles.

Packaging Bottles, Jars, Vials Food Containers: excluding disposable cups Flexible Packaging: including household and institutional refuse bags and film All Other: including tubes, tape, strapping, drums, caps, baskets, trays, boxes, pallets, shipping crates, pails, buckets, shipping cases, and blister and bubble containers.

Building and Construction Pipe, Conduit and Fittings: including drainage, irrigation, plumbing fixtures, and septic tanks Building Material for All Structures: including siding, flooring, and insulation materials All Other: including panels, doors, windows, skylights, bathroom units, gratings, and railings.

ElectricaVElectronic Home and Industrial Appliances: including electrical industrial equipment, wire and cable coverings, communications equipment Electronic Components: including resistors, magnetic tape, records, and batteries.

Furniture and Furnishings Rigid and Flexible Types: including household and office furniture, bedding, carpets, rugs, backing, curtains, blinds, awnings, lamps, picture frames, and wall coverings.

Consumer and Institutional Products Disposable Food Serviceware: including disposable cups Dinner and Kitchenware: including picnicware Toys and Sportings Goods Health Care and Medical Products: including laboratory supplies Hobby and Graphic Arts Supplies: including photographic equipment and supplies All Other: including footwear, luggage, buttons, lawn & garden tools, signs & displays, and credit cards.

Indus triamachiner y All Types: including engine and turbine parts, farm and garden machinery, construction and related equipment, machine tools, ordnance and firearms, and chemical process equipment.

Ad hesiveshn kslC oa t ings Adhesives and Sealants All Other: including printing ink, magnet wire enamels, core binders, foundry facings, paper coating and glazing, paints, varnishes, and enamels.

All Other Sales of Resins Sold to Resellers and Compounders Other sales of resins which cannot be classified under any of the Major Market categories previously listed.

Exports Sales of Plastic Resin Exported from the U.S

ajor market volumes are derived from plastic resins sales and captive use data as M compiled by Association Services Group

LLC. This study reflects data collectedfor the following individual resin categories:

Thermosets Epoxy Polyester, Unsaturated Urea and Melamine Phenolic

Thermoplastics Low Density Polyethylene Linear Low Density Polyethylene High Density Polyethylene Polypropylene Acrylonitrile-Butadiene-Styrene (ABS),

Styrene-Acrylonitrile (SAN) E3 Other Styrene Based Polymers (OSBP)

Polystyrene Styrene Butadiene Latexes (SBL) Nylon Polyvlnyl Chloride Thermoplastic Polyester Engineering Resins

Total Resin Sales & Captive Use by Major Market (millions of pounds, dry weight basis)

Major Market 1992 1993 1994 1995 1996

Transportation Packaging Building and Construction ElectricaElectronic Furniture and Furnishings Consumer and Institutional Industrialhlachinery AdhesiveshksKoatings All Other Exuorts

2,817 3,221 3,795 18,284 19,569 19,551 11,876 12,885 14,715 2,766 2,98 1 3,325 2,559 2,759 3,118 6,093 6,015 9,266

617 768 836 1,723 1,572 1,789 6,877 7,234 7,515 6.950 6.632 6,889

3,916 19,334 14,321 2,966 3,198 9,054

818 1,795 8,050 7.742

3,964 21,271 16,199 3,137 3,477 9.804

980 1,833 9.361 8.722

Total 60,562 63,636 70,799 71,194 78,748

Major Markets - All Resins Major Market 1992 1993 1994 1995 1996

Transportation Packaging Building and Construction ElectricaVElectronic Furniture and Furnishings Consumer and Institutional IndustriaUMachinery Adhesives/Inks/Coatings All Other Exports

4.7 5.1 5.4 5.5 5.0 30.2 30.8 27.6 27.2 27.0 19.6 20.2 20.8 20.1 20.6 4.6 4.7 4.7 4.2 4.0 4.2 4.3 4.4 4.5 4.4

10.1 9.4 13.1 12.7 12.5 1.0 1.2 1.2 1.1 1.2 2.8 2.5 2.5 2.5 2.3

11.3 11.4 10.6 11.3 11.9 11.5 10.4 9.7 10.9 11.1

Total 100.0 100.0 100.0 100.0 100.0

Major Markets - All Resins Major Market 1991/92 1992/93 1993194 1994/95 1995/96

Transportation Packaging Building and Construction Electrical/Electronic Furniture and Furnishings Consumer and Institutional IndustriaVMachinery AdhesiveslInkslCoatings All Other Exports

Total

21.0 14.3 17.8 3.2 1.2 9.3 7.0 -0.1 -1.1 10.0

11.5 8.5 14.2 -2.7 13.1 -4.5 7.8 11.5 -10.8 5.8 13.5 7.8 13.0 2.6 8.7 7.1 -1.3 54.0 -2.3 8.3 5.1 24.5 8.9 -2.2 19.7

23.9 -8.8 13.8 0.3 2.1 3.9 5.2 3.9 7.1 16.3

-6.3 -4.6 3.9 12.4 12.7

7.1 5.1 11.3 0.6 10.6

All Resins -

Transuortation 5.0%

AdhesivesLnks Coatings 2.3 o r / /o

/ A \

/ 4- IndustriaVMachinery

1.2% Consumer & Institutional 12.5%

Electrical/ Electronic

4.0%

Furniture & Furnishings 4.4%

Packaging 0.7% Thermoset Resins ~

Transportation 8.4%

All Others & Exoorts 11.9%

Adhesiveshnks Coatings 4.0%

IndustriaVMachinery 2.5%

Consumer & Institutional 3.5%

Furniture & Furnishings 6.1%

ElectricaVElectronic 3.1%

Thermoplastic Resins

IndustriaVMachinery 1.1% L-h

Consumer & / Institutional 13.5%

f Transportation 4.6%

Construction 15.4% Furniture & Furnishings 4.2% ElectricaVElectronic 4.1%

Total Thermosets & Thermoplastics (thousands of pounds, dry weight basis)'

Major Market

Transportation . . . . . . . . . . . . . . . .

Packaging, . . . . . . . . . . . . . . . . . . .

Building & Construction . . . . . . .

ElectricaElectronic . . . . . . . . . . . .

Furniture & Furnishings . . . . . . . .

Consumer & Institutional Products

Industrial/Machiner y . . . . . . . . . . .

AdhesivesLnWCoatings . . . . . . . .

All Other '. . . . . . . . . . . . . . . . . . . .

Exports. . . . . . . . . . . . . . . . . . . . . .

Total

I

Total Thermosets

Quantity

680,966

54,746

5,341,894

253,563

496,452

283,474

205,014

326,593

215,676

278,348

8,136,726

~

Percent 3f Total

8.4

0.7

65.6

3.1

6.1

3.5

2.5

4.0

2.7

3.4

100.0

Total Thermoplastics

Quantity

3,282,541

!1,216,492

10,856,632

2,883,666

2,980,468

9,520,894

774,483

1,506,562

9,145,658

8,443,550

'0,610,946

~

Perceni If Tota

4.6

30.0

15.4

4.1

4.2

13.5

1.1

2.1

13.0

12.0

-00.0

Grand Total

__

Quantity

3,963,507

21,271,238

16,198,526

3,137,229

3,476,920

9,804,368

979,497

1,833,155

9,361,334

8,721,898

78,747,672

'ercent f Total

5.0

27.0

20.6

4.0

4.4

12.5

1.2

2.3

11.9

11.1

LOO.0

' Phenolic is an a gross waghi baas. All Other totals do nut include disclosure data; therefore. these to& may not equal the sum of their repcctive components.

Source SPI Cammiltee on Resin Statistics; Annual Major Markets Survey as compiled by Associauon Semccs Group LLC

Thermosets & Thermodastics Resins (thousands of pounds, dry weight basis)'

Packaging.. . . . . . . . . . . . . . . . . . .31,000

Building & Construction . . . . . . . . 74,771

Electrical/Electronic . . . . . . . . . . . . 78,953

Fumiture & Furnishings . . . . . . . . .3,798

Consumer & Institutional . . . . . . .53,820

1ndustriaVMachinei-y . . . . . . . . . . .95,125

AdhesiveflnMCoatings . . . . . . . . . . . . . 0

AllOther . . . . . . . . . . . . . . . . . . . .85,117

Exports . . . . . . . . . . . . . . . . . . . . 154,336

1

EPOXY

Transportation . . . . . . . . . . . . . . . .

4.8

11.6

12.3

0.6

8.4

14.8

0.0

13.2

24.0

Total.. . . . . . . . . . . . . . . . . .

Unsaturated Polye

Quantity

494,983

0

786,217

51,145

0

141,665

0

0

1,429

89,661

565,100

____

-

__

-

r - trcent Total -

31.6

0.0

50.2

3.3

0.0

9.1

0.0

0.0

0.1

5.7

10.0

-

-

Urea Melam

Quantity

D

D

L,576,685

D

D

D

D

D

8,37,184

17,982

,43 1,851

'Phenolic is on a Gross Weight Basis. 'Includes total ofU.S.A. and Canada. D= Disclosure. Amount is included in All Other. NIR= Not reported in order to mask disclosure m another c a t e g q Amount E included in ALL OTHER,

Phenolics - 2uantity

NII

t

,904,221

Nfi

I:

NiF

c

NiE

575,853

16,369

496,443

-

Low Density PE

Quantity

56,678

3,073,762

167,212

51,948

30,269

1,141,881

227,748

624,613

1,023,762

.,475,926

7,873,799

- 'b1Ce"I fTorsl - 0.7

59.0

2.1

0.7

0.4

4.5

2.9

7.9

3.0

8.8

10.0

-

-

Source: SPI Commmee on Resin Statistics: Annual Major Markets Survey as campiled.by Associarmn Services Group LLC.

Thermoplastics (thousands of pounds, dry weight basis)

Polystyrene Linear Low Density PE

Major Market

I Styrene Based -

'kKC"1 f T d

0.0

23.5

8.1

12.9

1.4

31.5

0.0

0.0

15.8

6.8

00.0 Total.. . . . . . . . . . . . . . . . . . .7,7!18,8851100.0

Latex

Quantity o,T,,tal

D

D

D

D

473,481 34.4

D

0 0.0

720,084 52.4

181,840 13.2

D

1,375,405 100.0

Percent

' Sales to Canada included in Exports. * Includes total of U S.A. and Canada. D= Disclosure. Amount is included m All Other.

Transportation . . . . . . . . . . . . . . . . 13,715

Packaging . . . . . . . . . . . . . . . . .3,817,756

Building & Construction , . . , , , . .53,535

ElectricaVElectronic . . . . . . . . . . ,257,146

Fumiture & Furnishings . . . . . . . .23,699

Consumer & Institutional. . . . . 1,286,154

IndustriaVMachinery . . . . . . . . . . . . . . . . 0

Adhesives/lnks/Coatings . . . . . . . . 57,153

AUOther . . . . . . . . . . . . . . . . . 1,182,265

Exports.. . . . . . . . . . . . . . . . . . 1,107,462

High Density PF

0.2

48.9

0.7

3.3

0.3

16.5

0.0

0.7

15.2

14.2

_I

Quantity

533,505

5,787,429

L,187,462

125,586

0

879,744

265,998

0

.,493,540

.,937,445

3,210,705

- :Tc" Total - 4.0

51.4

9.0

0.9

0.0

6.7

2.0

0.0

11.3

14.7

00.0

-

-

Polypropylene

Quantity

724,535

2,435,235

D

396,583

2,066,054

2,829,437

0

0

2,647,224

1,021,878

12,120,946

- " 1 ' Total -

6.0

20.1

3.3

17.1

23.3

0.0

0.0

21.8

8.4

00.0

- -

- Juantity

(

,427,89:

491,36:

782,395

84,825

,912,49C

C

C

962,551

409,928

,071,445

Source: SPI Committee on Resin Statistics; Annual Major Markets Survey as compiled by Association Semcer Group LLC

Thermoplastics (thousands of pounds, dry weight basis)

Orcent Tom1

55.1

1.6

0.2

0.4

16.6

L6.1

10.0

Quantity

678,303

D

156,467

D

28,817

218,142

102,041

D

578,887

331,168

2,093,825

Major Market Quantity

Transportation . . . . . . . . . . . . . . . 349,872

Packaging.. . . . . . . . . . . . . . . . . . 103,323

Building & Construction. . . . . . . . . . . . . 0

Electrical & Electronic . . . . . . . . . 164,032

Fumiture &Furnishing . . . . . . . .52,162

Consumer 6s Institutional . . . . . . .96,304

Industriaiflvlachinery . . . . . . . . . . .78,156

AdhesivesflnMCoatings . . . . . . . . . . . . . 0

All Other . . . . . . . . . . . . . . . . . . . .78,244

Exports.. . . . . . . . . . . . . . . . . . . . 183,335

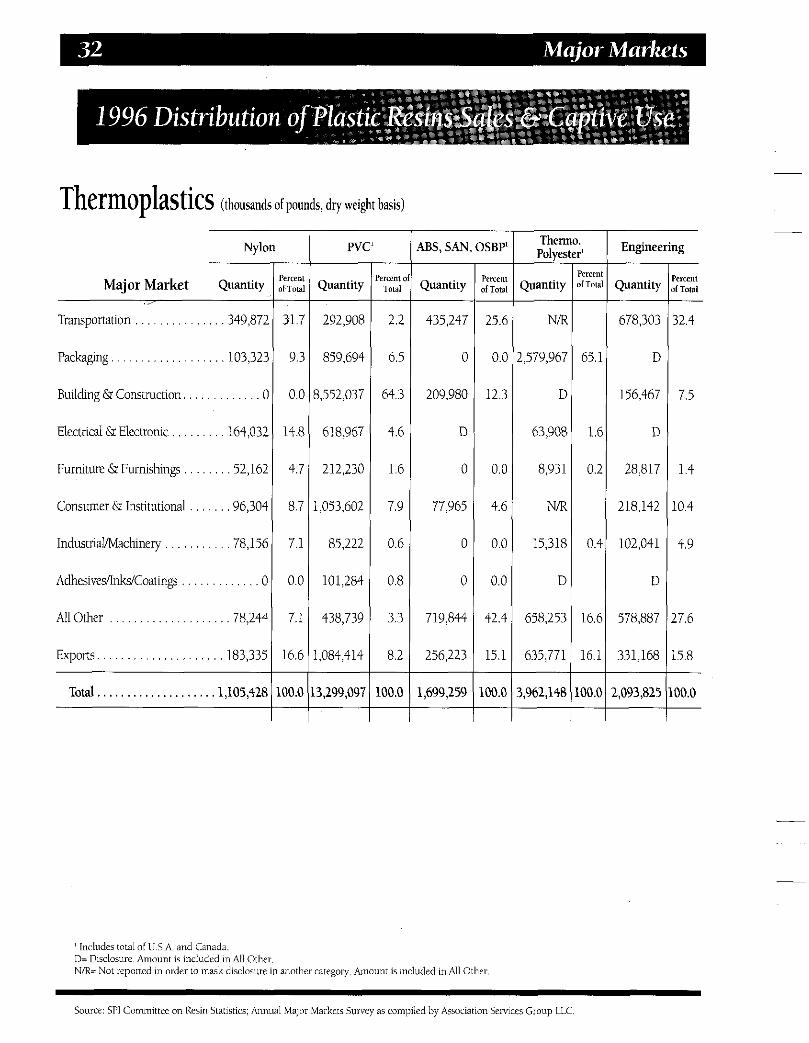

J

PVC' 1 ABS, SAN, OSBP

zy:t 31.7

9.:

O.C

14.E

4.7

8.7

7.1

0.0

7.1

16.6

- Quantity

6.5

292,908

859,694

;,552,037

618,967

212,230

,053,602

85,222

101,284

438,739

,084,414

0

5,299,097 __

4.6

1.6

I

D

0

2.2 1 435,247

0.6

0.8

0

0

Total.. . . . . . . . . . . . . . . . . . .1,105,428

7.9 1 77,965

100.0

:::I ::::: 00.0 1,699,259

- PWCC",

fTlofa -

25.f

0.C

12.3

0.c

4.t

0.c

0.0

42.4

15.1

00.0 -

-

' Includes total of U S.A. and Canada. D= Disclosure Amount is includcd in All Other N/R= Not reported in order IO inask disclosure in another category. Amount i s included in All Other,

Them Polyes

Quantity

~

NB

.,579,967

D

63,908

8,931

N R

15,318

D

658,253

635,771

8,961,148 -

1 I Engineering - .we", TOtd - 2.4

7.5

1.4

0.4

4.9

7.6

5.8

10.0 -

-

~~ ____

Source: SPI Committee on Resin Siaiistics; Annual Major Mailiers Survey as compiled by Asociatmn Services Group LLC.

Total U.S. Production and Sales & Captive Use' (millionsofpounds)

Year Production Sales & Captive Use2 1971" 21,161 19,813 1972 26,475 25,504 1973 29,213 28,719 1974 29,274 27,890 1975 22,828 22,278 1976 29,196 28,379 1977 33,948 32,771 1978 37,605 36,818 1979 41,577 40,607 1980 37,347 36,896 1981 39,867 38,801 1982 36,607 36,639 1983 42,777 42,212 1984 46,336 45,221 1985 47,946 47,470 198@ 50,849 50,452 1987 55,751 55,818 1988 59,762 58,554 1989 58,529 59,676 1990 61,960 63,039 1991 62,786 63,369 1992 66,371 67,675 1993 68,854 71,094 1994 75,971 78,744 1995 78,684 79,240 1996 84,295 86,426

I Includes polyurethane. Sales and Captive Use is defined as Merchant Sales plus Intra-Company Captive Use.

" 1971-1996 includes cellulosics. SPI data used for 1971-1996.

'1986-1996 include SPI Estimates.

Compound Growth Rates (%) YEARS PRODUCTION SALES & CAPTIVE USE

1971-1996 1981-1996 1986-1996 1991-1996 1995-1996

5.6 5.1 5.2 6.0 7.1

6.2 5.7 5.5 6.5 9.0

Production and Sales & Captive Use (millionsofpounds)

1987 RESIN - P

Epoxy . . . . . . . . . . . . . . . . 433 Phenolic. . . . . . . . . . . . .2.869 Polyester (Unsaturated) . . 1,367 Urea., . . . . . . . . . . . . . 1,382 Melamine . . . . . . . . . . . . 212

Total Selected . . . . . . . . 6,263 Thermosets

ABS . . . . . . . . . . . . . . . . 1,175 SAN . . . . . . . . . . . . . . . . 126 HDPE.. . . . . . . . . . . . . .7,995 LDPE.. . . . . . . . . . . . . .9,599 LDPE, . . . . . . . . . . . . . . . NA LLDPE . . . . . . . . . . . . . . . NA

Nylon. . . . . . . . . . . . . . . . 507 Polypropylene . . . . . . . .6,647 Polystyrene . . . . . . . . . .4,780 PVC.. . . . . . . . . . . . . . . 7,971 Thermoplastic . . . . . . . . 1.394 Polyester

Total Selected . . . . . . . 40,194

Total Selected Plastics . 46,457

All Other Plastics. . . . . . 9,294

Grand Total.. . . . . . .55,751

Thermoplastics

;&a 419

2,871 1,362 1,368

198

__

6,218

1,208 127

8.155 9,611

NA NA 499

6,720 4,860 8,081 1,410

0,671

6.889

8,929

5,818 ~

1988

P 486

3,066 1,404 1,425

207

~

6,588

1,277 148

8,400 0,397

NA NA 566

7,274 5,187 8,350 1,652

.3,251

,9339

9,923

9,762 ~

i&CL 468

3,073 1,393 1,350

203

~

6,487

1,279 146

8,084 0,177

NA NA 574

7,088 5,027 8,287 1,643

2,305

8.792

9.762

3.554

1989

P 510

2,879 1,319 1.477

222

~

6,407

1.260 113

8,102 9,695 6,575 3,120

569 7,238 5,104 8,478 1.630

.2,189

8,596

9,933

8.529

i&CL 482

2,863 1,302 1,465

213

~

6.325

1,217 108

8,173 0,803 6,916 3.887

580 7,303 5,131 8,493 1,707

3,515

1,840

1,836

2.676

1990

P 49 9

2,946 1.221 1,496

202

~

6,364

1,162 135

8,337 1,148 7,255 3,893

558 8,310 5,021 9,096 1,879

5,646

2,010

9,950

1,960 ~

i&CU 484

2,938 1,211 1,498

176

~

6,307

1,161 134

8,838 1,963 7,202 4,761

581 8,239 5,049 8,996 1.905

5,866

3,173

1,866

3.039

1991

P 497

2,658 1,075 1.483 2.196

~

5,909

1.103 109

9,213 1,148 7,236 4,346

576 8,330 4,954 9,164 2.115

7,146

3,055

9,731

2,786 ~

i&CU 491

2,663 1,078 1,485

172

5,889

__

1.125 114

3,345 1,963 7,397 4,935

627 3,327 4,896 3,086 2,113

7,963

3,852

3,517

1.369

P = Production

Notes: - 1987.1996 data include SPI estimates. All Other Plastics include Polyurethane

5 & CU = Sales &Captive Use NA = Not Available

-Imports are included in S&CU beginning in ( )year for rhe followingresins Epoxy (1995); ABS (1994), SAN (1994); HDPE (1991). LDPE (1989); LLDPE (1989); Polypropylene (1991). Polystyrene (1992); Nylon (1989): Thermoplasac Pniyesler (1989).

and Melamine began m 1996. Beginning m 1994, Production data include U S and Canadian rotals for ABS, SAN and PVC. Polypropylene began in 1995, Phenolic, Urea

~~~~ ~

Source: SPI Committee on Resin Statistics, Monthly Staustical Report, as compiled by Associauon Scrmces Group LLC.

Production and Sales & Captive Use cont. (millionsofpounds)

1992 RESIN ~ P

Epoxy . . . . . . . . . . . . . . ,457 Phenolic. . . . . . . . . . . . .2,923 Polyester (Unsaturated) . . 1,175 Urea. . . . . . . . . . . . . . . 1.548 Melamine . . . . . . . . . . . . ,232

Total SelecLed . . . . . . . . 6,335 Thermosets

ABS . . . . . . . . . . . . . . . 1.326 SAN . . . . . . . . . . . . . . . . . 1 13 HDPE. . . . . . . . . . . . . . .9,808 LDPE . . . . . . . . . . . . . 11,9 17 LDPE, . . . . . . . . . . . . .7,273 LLDPE . . . . . . . . . . . .4,644

Nylon . . . . . . . . . . . . . . ,668 Polypropylene . . . . . . . .8,42 1 Polystyrene . . . . . . . . . . 5.096 PVC.. . . . . . . . . . . . . . .9,989 Thermoplastic . . . . . . 2,413

Polyester

Total Selected . . . . . . . 49,751

Total Selected Plastics . 56,086 Thermoplastics

All Other Plastics 10,285

Grand Total. . . . . . . .66,371

512 2,926 1,185 1,548

148

6,319

1,277 u n

10,110 12,919 7,499 5,420

725 8,468 5,213

10,003 2,441

51,266

57,585

10,090

57,675

~

P 1993

512 3,078 1,264 1.744

270

6,868

1.462 105

9,941 2,067 7,226 4,841

768 8,628 5,382 0,257 2,549

1,159

8,027

3.777

3,854

535 3,081 1.280 1,743

261

6,900

1,373 118

10.604 13,140 7,424 5,716

794 8,938 5,494

10,549 2,546

53.556

50,456

10,650

71,094

1994

P 601

3,229 1,468 1.915

300

7,513

1.701 138

1,117 2,600 7,578 5,022

943 9,539 5,848 1.712 3,196

5,794

4,307

1,664

j,971

~

S&CU 606

3,230 1.493 1,910

283

~

7,522

1,583 162

11,910 14,239 7,904 6,335

942 9,946 6.000

11,761 3,154

59,697

57,219

11,525

78,744

Compound Growth Rates 1987-1996 ( O h ) I

P sdrcu P S&CU

1995

P 632

3,204 1,577 1.816

290

7,519

__

1,458 130

1,211 2,886 7,643 5,243 1,020 0,890 5,656 2,295 3.785

3,331

5,850

1,834

3,684

j&CI 620

3,201 1,569 1,810

286

~

7,486

1,463 150

1,837 3,730 7,524 6,206 1,031 0,710 5,799 2,033 3,425

0.178

7,664

1,576

9,240

1996

P 662

3,476 1,557 2.147

287

~

8,129

1,477 121

2.373 4,145 7,784 5,361 1,103 1,991 5,065 3,220 %,031

+,526

2,655

1,640

1,295

S&CU 643

3,496 1,565 2,139

293

-

8,136&--

1,433

5,bG 7,874 7,799 8

1.105 2,121 v

6071 I 3,299 3 962

6.999

5,135

1,291 c-

P S&CU

2.6 2.0 Total Selected Plastics 5.1 5.3 E P O V 4.9 4.9 ABS Phenolic 2.1 2.2 SAN 0.4 0.2

LDPE N/A N/A All Other Plastics 2.5 2.6 Urea 5.0 5.0 LLDPE NIA N I A 4.4 Nylon 9.0

Melamine 3.4

Total Selected 3.0 3.0 Polvurouvlene 6.8 6.8

Palyester (Unsat.) 1 5 1.6 HDPE 5.0 5.5

Grand Total 4.7 5.0

Thermosets 2.1 2.5 5.8 5.7

Thermoplastic Polyester 12.5 12.2 Total Selected 5.4 5.7 Thermoplastics

Source: SPI Commntee on R e m SlatisLics. Monthly Statistical Repon, 8s compilcd by Association Scrviccs Group LLC.

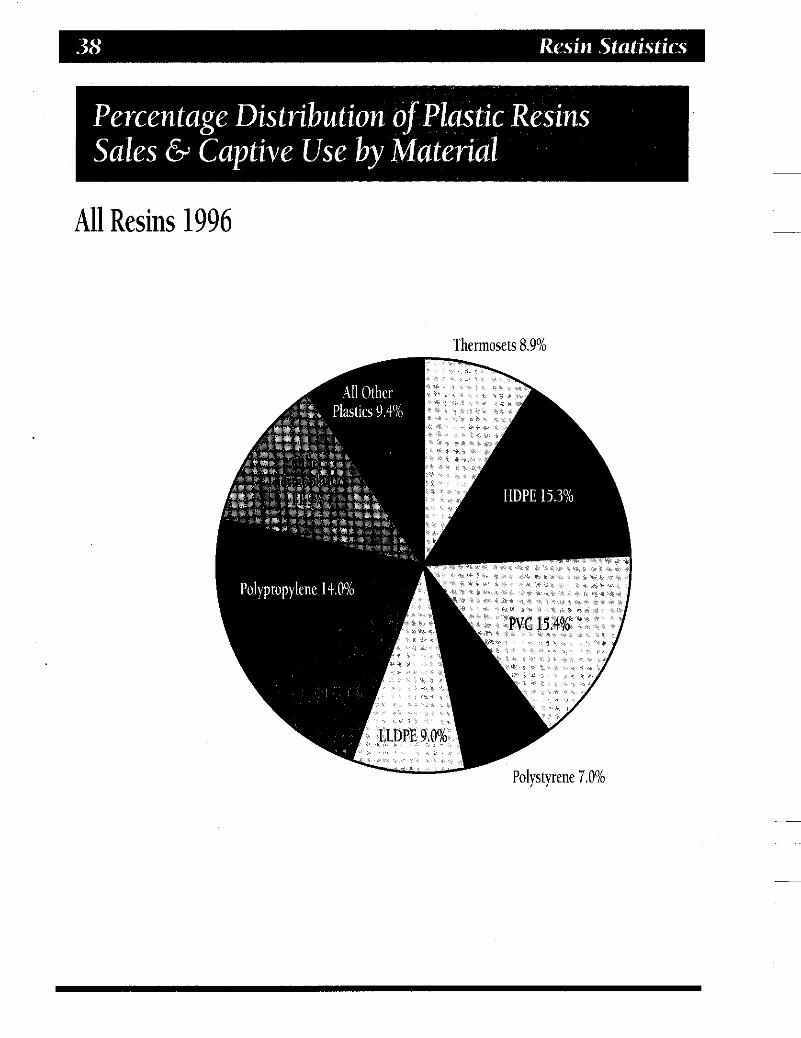

All Resins 1996 __

Thermosets 8.9%

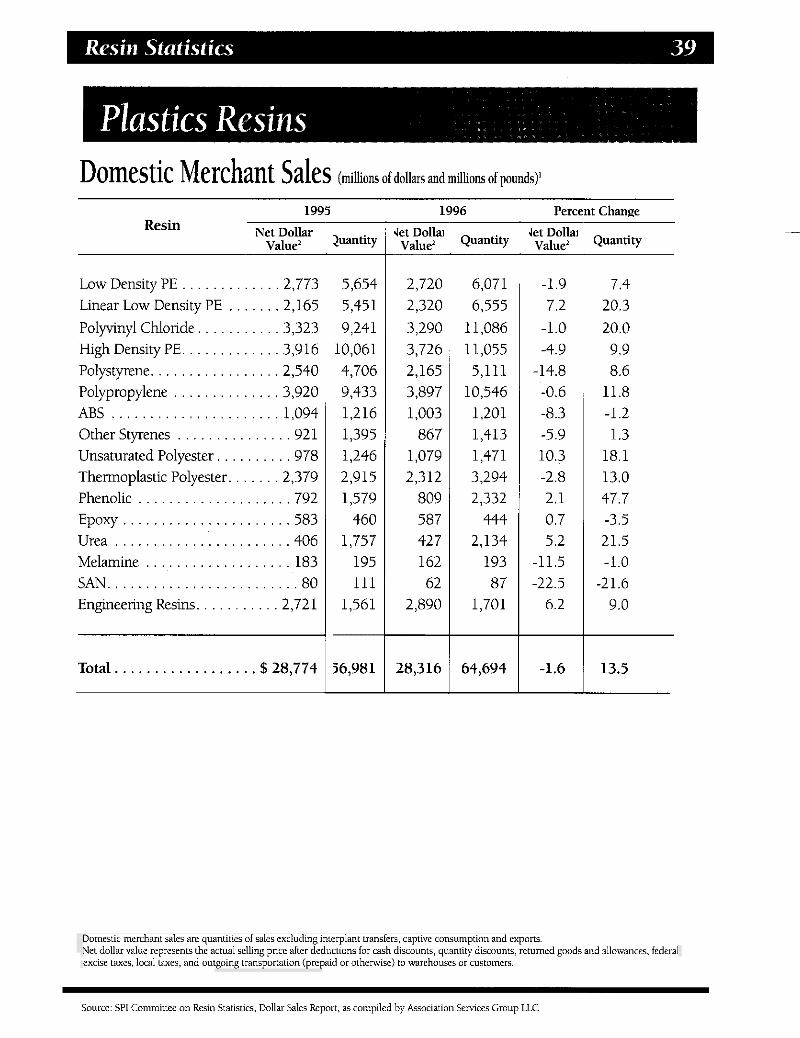

Domestic Merchant Sales (millions of dollars and millions of pounds)'

1995

Net Dollar Value'

Resin

Low Density PE . . . . . . . . . . . . . 2 . 773 Linear Low Density PE . . . . . . . 2. 165 Polyvinyl Chloride . . . . . . . . . . . 3 . 323 High Density PE . . . . . . . . . . . . . 3 . 9 16 Polystyrene . . . . . . . . . . . . . . . . . 2. 540 Polypropylene . . . . . . . . . . . . . . 3. 920 ABS . . . . . . . . . . . . . . . . . . . . . . 1. 094 Other Styrenes . . . . . . . . . . . . . . . 921 Unsaturated Polyester . . . . . . . . . . 978 Thermoplastic Polyester . . . . . . . 2. 379 Phenolic . . . . . . . . . . . . . . . . . . . . 792 Epoxy . . . . . . . . . . . . . . . . . . . . . . 583 Urea . . . . . . . . . . . . . . . . . . . . . . . 406 Melamine . . . . . . . . . . . . . . . . . . . 183 SAN . . . . . . . . . . . . . . . . . . . . . . . . . 80 Engineering Resins . . . . . . . . . . . 2 . 72 1

Total . . . . . . . . . . . . . . . . . . $28, 774

2uantity

5. 654 5. 45 1 9. 241

10. 061 4. 706 9. 433 1. 216 1. 395 1. 246 2. 915 1. 579

460 1. 757

195 111

1. 561

~

56. 981

1996

get Dollai Value'

2. 720 2. 320 3. 290 3. 726 2. 165 3. 897 1. 003

867 1. 079 2. 312

809 587 42 7 162 62

2. 890

28. 316

Quantity

6. 071 6. 555

11. 086 11. 055 5. 111

10. 546 1. 201 1. 413 1. 471 3. 294 2. 332

444 2. 134

193 87

1. 701

64. 694

Percent Change

Jet Dollai Value'

-1.9 7.2

-1.0 -4.9

-14.8 -0.6 -8.3 -5.9 10.3 -2.8 2.1 0.7 5.2

-11.5 -22.5

6.2

-1.6

Quantity

7.4 20.3 20.0 9.9 8.6

11.8 -1.2 1.3

18.1 13.0 47.7 -3.5 21.5 -1.0

-21.6 9.0

13.5

Source: SPI Committee on Resin Statistics. Dollar Sales Report. as compiled by Association Semices Group LLC

pparent consumption is calculated by adding For PUToses O f t h e below the Production .

imports to production, then subtracting xports . It is a measure ofthe quantity of

figures were takenfrom SPl's Monthly Statistical Report, as compiled by Association Services Group

tahenfrom Bureau of the Census reports . material actually consumed in the United States . . Both the and exPortfiWes Were -

A, 1996 (millions of pounds)

c Resin Production

Low Density Polyethylene . . . . . . . 7. 784 Linear Low Density Polyethylene . 6. 361 High Density Polyethylene . . . . . 12. 373

Polypropylene* . . . . . . . . . . . . . . 11. 991 Polystyrene . . . . . . . . . . . . . . . . . . 6. 065 Phenolic* . . . . . . . . . . . . . . . . . . . . 3. 476 ABS* . . . . . . . . . . . . . . . . . . . . . . . 1. 477 Thermoplastic Polyester'l). . . . . . . . 2. 294* * Urea* . . . . . . . . . . . . . . . . . . . . . . . 2 . 147 Unsaturated Polyester . . . . . . . . . . 1. 577 Nylon . . . . . . . . . . . . . . . . . . . . . . . 1. 103 Epoxy* . . . . . . . . . . . . . . . . . . . . . . . 662 Melamine* . . . . . . . . . . . . . . . . . . . . 287

1996 Total . . . . . . . . . . . . . . . . .70. 797

PVC* . . . . . . . . . . . . . . . . . . . . . .13. 220

1995 . . . . . . . . . . . . . . . . . . . . . . 66. 720 1994 . . . . . . . . . . . . . . . . . . . . . . 62. 107 1993 . . . . . . . . . . . . . . . . . . . . . .56. 942 1992 . . . . . . . . . . . . . . . . . . . . . . 54. 995 1991 . . . . . . . . . . . . . . . . . . . . . . 52. 061 1990 . . . . . . . . . . . . . . . . . . . . . . 49. 071

J L

Imports

201 1. 532 1. 192

119 105 232 97

167 95 33 61

155 42 12

4. 043

3. 509 3. 972 3. 236 2. 453 1. 950 2. 112

Exports

m a74

1. 793 1. 102 1. 217

583 125 255 396

52 156 314 154"' 44

8. 688

7. 624 7. 526 7. 496 7. 539 8. 167 6. 260

1 Apparent :onsumption

6. 362 7. 019

11. 772 12. 237 10. 879 5. 714 3. 448 1. 389 1. 993 2. 128 1. 462

944 550 255

66. 152

62. 605 58. 553 52. 682 49. 909 45. 844 46. 923

Import Oh Of Apparent Ionsumption

3.2 21.8 10.1 1.0 1.0 4.1 2.8

12.0 4.8 1.6 4.2

16.4 7.6 4.7

6.1

5.6 6.8 6.1 4.9 4.3 4.5

* Pioduciion. Tiadc &Apparent consumption arc bascd on U.S. and Canadian data m 1996 .

* * Rcpresenls Bottle Grade PET resin sales . no production data available ('I Biiiile Grade only .

comparable .

Data for Lhox and other resins in prior years reflect U S . only

Rcpresenls SPI primary data Epoxide exports as reported m U.S. Census report EM 545 cunlorm to a different specification and arc noi

Sources: Production-SPI Monihly Siaiisucal Repori . as coml?iled hy Associalion Scrvrei Group LLC Imports-Bureau ofrhe Census . IM 146 E n ~ o n c B u r e a u ofthe Census . EM 545

and may be cured by heat, catalysts, or other chemical means. After beingfully cured, thermosets cannot be resoftened by heat.

- hermoset plastics in theirfinal state as mished articles are substantially infusible Ti and insoluble. They are ofen in liquidform at some point in their manufacture or processing,

-

Material

Maior Markets J

AdhesivesllnksKoati

Consumer & Institut

Note: Includes

Pack rtation

aging 0.7% 8.4%

Sources: SPI Commiwee on Resin Statistics. SPI Major Market Report. as compiled by Asrociaoon Services Group LLC.

Manufacturers' Ciba-Geigy Corp The Dow Chemical Co. Reichhold Chemicals, Inc Shell Chemical Co. Union Carbide Corp.

1 Those manufdcturers who participated in the SPI Monthly Swtisncal Report m 1996,

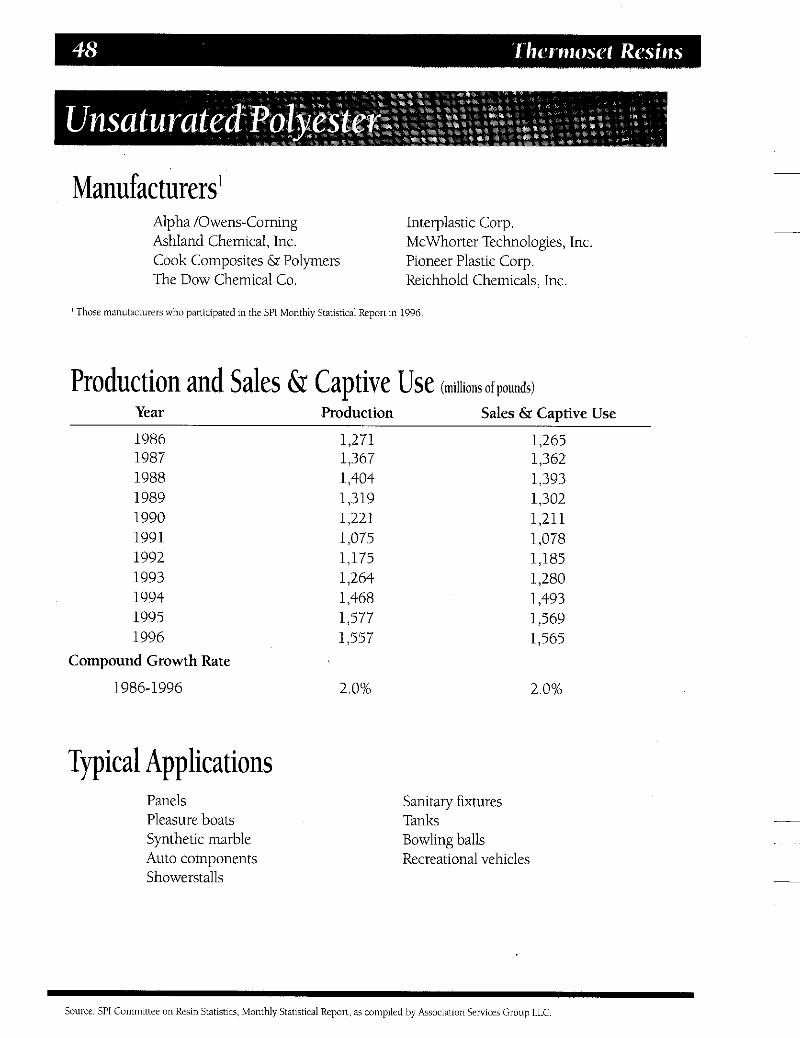

Production and Sales & Captive Use (millions ofpounds)

Year Production Sales & Captive Use'

1986 1987 1988

1990 1991 1992 1993 1994 1995 1996

1989

398 433 486 509 499 497 457 512 60 1 632 662

Compound Growth Rate 1986-1996 5.2%

'Begmnmg m 1995. Imports included m Domestic Sales & Use

Domestic Consumption By End-Use (millions of pounds)

376 419 468 482 484 49 1 512 535 606 620 643

5.5%

End-Use 1992 1993 1994 1995

33 39 44

Protective coatings 245

Tooling, casting, and molding resins, . . , . . 24 17 15 17 All other uses. . . . . . . . . . . . , . . . . . . , . . . . 3 6 29 26

Bonding & adhesives. . . . . . . . . . . . . . . . . . 31 Flooring, paving and exposed aggregates . . 31 34 38 34

Fiber reinforced laminates & composites . . 73 81 90 95 . . . . . , . . . . . . . . . . . 206 218 24 1

31

1996

51 40

263 89 17 29

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . 401 414 452 461 489

Source: SPI Committee on Resin Staustics. Monthly Statisrical Report. as compiled by Association Services Group LLC

Distribution by Major Market (millionsofpounds)

Major Market 1992 1993 1994 1995 1996

Transportation. . . . . . . . . . . . . . . . . . * 52 58 61 66 Packaging . . . . . . . . . . . . . . . . . . . . . * 25 28 29 31 Building and Construction . . . . . . . 52 61 68 66 75 ElectricaVElectronic. . . . . . . . . . . . . 63 71 79 84 79 Furniture and Furnishings . . . . . . . . * 3 3 3 4 Consumer and Institutional . . . . . . . * 44 49 50 54 Industrial/Machinery. . . . . . . . . . . . . * 81 86 90 95 Adhesives/Inks/ Coatings . . . . . . . 235 - - - - All Other. . . . . . . . . . . . . . . . . . . . . 51 77 80 78 85 Exports'. . . . . . . . . . . . . . . . . . . . . 111 121 155 158 154

Total.. . . . . . . . . . . . . . . . . . . . , 5 1 2 535 606 619 643

* Included in All Other. ' Sales to Canada included in Enporls, Source: SPI Committee an Resin SLatistics, Annual Major Markcis Survey.

Typical Applications Coatings Reinforced composites Adhesives Electrical laminates ElectricaVElectronic casting and molding FloorRaving aggregates Industrial equipment Sealants

Manufac turersl Ashland Chemical, Inc. Borden, Inc. Owens Corning Capital Resins COT. Plaslok Corp. Georgia-Pacific Resin, Inc. Plastics Engineering Co. Lockport Thermosets, Inc. (Valite Div.) Rogers Corp. Monsanto Co. Spurlock Adhesives, Inc. Neste Resins Corp.

Occidental Chemical COT.

' Those manufacturers who participated in the SPI Monthly Statistical Report in 1996.

Production and Sales & Captive Use (millionsofpounds)

Year Production Sales & Captive Use lY86 2 , 1 3 2,111 1987 2,869 2,871 1988 3,066 3,073 1989 2,879 2,863 1990 2.946 2,938 1991 1992 1993 1994 1995 1996

2,658 2,923 3,078 3,229 3,204 3,476

Compound Growth Rate

1986-1996 2.4%

' Beginning in 1996, data includes U.S.A. and Canada.

Typical Applications Wiring devices Connectors Transmission parts Pulleys Electrical switch gear Closures

2,663 2,926 3,081 3,230 3,201 3,496