Embed Size (px)

Citation preview

M.Sc. thesis in Business Administration (Finance and International Business) Århus, December 2009

Family ownership and firm performance Empirical evidence from Denmark

Author: Adiba Kholmurodova Advisor: Jan Bartholdy

Abstract: Families are large shareholders in many countries. Most studies recently have found that family

firms perform better or at least as well as non-family firms. These findings raise the question of

whether the type of a blockholder matters in terms of firm performance. In our analysis we

address this question using a detailed panel dataset of 245 Danish firms using accounting based

performance measures. We find family firms to be younger, smaller and operating in slightly

different industries. Out of total family firms 80% are actively involved in the management and

an unrelated blockholders are present only in 30% of family firms. We do not find strong

evidence of significant negative or positive impact of family firms on accounting measures,

except few cases of significant impact. We conclude that family ownership might not per se be a

cause of positive or negative impact on firm performance, but rather other family firm related

characteristics (e.g. involvement in management) may explain differential performance.

Key words: family ownership, family management, agency theory, firm performance

Table of Contents Introduction………………………………………………………………………………………………...1

1.1 Research questions……………………………………………………………………………………2

1.2 Methodology………………………………………………………………………………………….3

1.3 Data………………………………………………………………………...........................................4

1.4 Limitations……………………………………………………………………………………………4

Chapter 1……………………………………………………………………………………………………5

1.1 Corporate governance………………………………………………………………………………...5

1.2 Agency theory……………………………………………………………………………...................6

1.3 Corporate ownership...........................................................................................................................10

Chapter 2…………………………………………………………………………………………………..15

2.1 Literature review…………………………………………………………………….………………15

2.2 Ownership across the world………………………………………………………………………....22

2.3 Control enhancing mechanisms…………………………………………………………..................26

Chapter 3…………………………………………………………………………………………………..28

3.1 Family ownership and performance (empirical findings)…………………………………………..28

3.2 Family ownership and CEO successions…………………………………………………................32

Chapter 4…………………………………………………………………………………………………..37

4.1 Hypothesis generation……………………………………………………………………….............37

Chapter 5………………………………………………………………………………………………..…40

5.1 Sample……………………………………………………………………………………….............40

5.2 Measuring family ownership………………………………………………………………………..41

5.3 Summary statistics………………………………………………………………………… ………47

5.4 Multivariate analysis…………………………………………………………………………….…..52

Conclusion………………………………………………………...............................................................62 Appendices

M.Sc. thesis 2009 Family ownership and firm performance ______________________________________________________________________________

1 Introduction

Families are large shareholders in many countries. Well known Danish companies such as

Mærsk, Lego, Bang and Olufsen, Danfoss, Grundfoss still have the founding families as the

largest shareholders or the founding families are either present at the board or/and at the

executive level.

Increased interest in the family ownership and its impact on performance appears to have been

motivated after studies by La Porta et al (1999) found that family ownership is as prevalent as

the diffused ownership type at the public firms both in countries with well developed and less

developed capital markets, which is in contrast to the notion of dispersed ownership of public

firms, first suggested by Berle & Means (1932). A couple of studies based on US data (Anderson

and Reeb, 2003, S&P 500; Villalonga and Amit, 2006, Fortune 500; Miller et al, 2007, Fortune

1000) found family firms with superior performance in the US, contrary to the assumptions of

negative impact of family ownership and participation in the management on value creation by

firms and their performance.

‘Whether family firms are more or less valuable than non family firms remains an open

question.’ (Villalonga & Amit, 2006).

From the theoretical perspective there are a number of propositions that discuss the potential

hazards and benefits of family ownership (Jensen & Meckling, 1976; Fama & Jensen, 1983;

Demsetz & Lehn 1985; Shleifer & Vishny, 1986). However, the empirical evidence in the field is

still lacking and often contradicting. National corporate governance characteristics differ across

countries, which might be one of the reasons for contradicting results (e.g. minority shareholders

are well protected in some countries and less in the others1). Difficulty in comparing the results

across the studies could be explained by non existence of a single definition of family firm.

Researchers take each a slightly different approach to defining the family ownership. 1 For example, family firms contribute to performance when minority shareholders are well protected, and vice versa otherwise

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Our interest in the subject starts with the broader question of whether the identity of the the

owner matters for the firm performance. We are interested in what established theories (agency

theory, stewardship theory, signaling, entrenchment and expropriation etc) suggest and test them

in a sample of companies from Denmark. As far as we are aware, there are few studies on family

ownership using the Danish data set (Bennedson et al, 2007).

Foundations are prevalent large shareholders in public companies, as well as families in

Denmark. While CEO duality is not allowed at the boards, minority shareholders have a very

small chance of being elected to the board. Denmark as a country scores low according to

different corporate governance system efficiency indices (e.g. La Porta et al, 1999). Denmark is

also known as one of the few Scandinavian countries where dual class shares are common

practice for the majority of listed companies in the industrial production, service and trade,

which makes the market for corporate control less competitive than in other countries.

We think it would be interesting to investigate family ownership in Denmark under such

conditions.

1.1 Research questions

• Does ownership structure matter? What kinds of ownership structures are spread around

the world?

• What causes different ownership structures across firms? What internal and external

factors (e.g. institutional characteristics such as minority shareholder protection, origins

of legal system, development of equity markets) influence different ownership structures?

• What impact identity of owners has on firm performance (e.g. family firms, institutional

owners, corporate ownership, and state?)

• Families as owners: expected benefits and drawbacks

• What firm characteristics are common for family firms (based on empirical findings)?

• What is relationship link between ownership type and firm performance

- 2 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Empirical study:

• What Danish evidence has to say about the family firms and their performance?

1.2 Methodology

We are going to conduct panel data set regression, based on 10 year performance observations

for a universe of Danish firms. Panel data sets are good to exploit the dynamics that are difficult

to detect with cross-sectional data. Our initial intended sample was 250 Danish joint stock

companies2 (both listed companies at the Copenhagen Stock Exchange (CSE) and unlisted

firms). However due to the small size of CSE and the length of observation period left us with

larger proportion of unlisted companies in the sample. Performance (dependent) variables are

going to be accounting based such as ROE, ROA, EBIDTA.3 Control variables are going to

include firm specific characteristics such as size, industry, firm age and so on.

Tobin’s q is often used as a proxy for firm performance in corporate governance research.

It is a good measure of how a firm employs it’s given assets to make profits. A high q value for a

firm is a sign of strong competitive advantage and the presence of growth opportunities. Rose

(2006) and Himmelberg (1999) are critical about the de-nominator in the q ratio as an

appropriate measure of firms’ replacement costs (e.g. if firms had a large share of their assets in

the form of intangible assets, then the Tobin’s q would be overstated).

Moreover, there is a critic of simple OLS regressions in similar studies that assumes that firm

performance is the only endogenous variable, i.e. ownership by a family in our case, influences

firm performance (Rose, 2006). However, as the relevant literature points out the causation can 2 In Danish ’aktieselskab’ 3Tobin’s q is defined as the sum of equity market value and liability book value divided by the sum of equity book value plus the liability book value. Hence, if q is greater than 1, then the market values the company higher than accounted 3 Financial ratios provided for the firms in both databases and print sources are according to the recommendations of Danish Association of Financial Analysts (DAF). The EBIDTA is calculated by dividing the earnings (before tax and interests, as well as amortization) (‘primært resultat’ in Danish) divided by sales.

- 3 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

go in the opposite direction, which is that firm performance might cause families to hold to their

ownership stakes. To avoid biased OLS parameter estimates, Rose (2006) suggests constructing

a simultaneous equation system where the equations are estimated using instrumental variables.

Himmelberg, Hubbard and Palia (1999) argue that insufficient instruments make it difficult to

establish a robust relation between ownership and performance.

1.3. Data

Our data is based on a sample of both listed (public) and unlisted joint stock Danish companies.

Our data set came from following sources:

‘Navne & Numre’ – is an electronic database of all Danish companies with ownership and

financial information for the latest five years. ‘GreensOnline’4 – is a web based database that

includes Danish companies with ownership and financial information for the last five years. To

be included in the Greens a firm should have more than 45 employees or over DKK 50 million in

sales or DKK 35 million in gross revenues. Additionally the database has background

information on leading people in the corporate world. The database also provided historical

overview over the ownership, management and board composition of the firm. ‘Greens 2004’

and ‘Greens 2006’ – encyclopedic print editions were used for the financial data in the early five

year period (1998-2004).

1.4 Limitations

The biggest limitation of this thesis is the sample size for the empirical results. Due to the limited

amount of time we have to conduct the research and limited access to the information, we

recognize that a different and more extensive sample could be desired for this kind of testing.

The thesis opts for a variety of interesting aspects to be studied, but due to the obvious limits on

the scope and extent of it, we have restricted the study to the research questions discussed in

section 1.1. 4 http://www.greens.dk/

- 4 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Chapter 1 1.1 Corporate Governance This section is devoted to the theory of corporate governance in which we will provide an

overview of it and account for its central problem explained by the agency theory.

An actual definition of corporate governance lacks consensus. Thomsen (2008), points out what

corporate governance is and what it deals with and claims that it is going to differ based on

interests and views of firm stakeholders such as shareholders, employees, banks, NGOs, state

etc. From the discipline of finance, his definition seems to suit best. ‘Corporate governance

deals with control and direction of companies by ownership, boards, incentives, company law

and other mechanisms.5

As managers care about what boards do to control them, investors care about how their rights are

protected and how much value the companies they have invested in, are creating, while at the

other end, politicians, the media, and non profit organizations care about how companies are

contributing to the society or how are they harming the environment to name a few (in general

corporate social responsibility, business ethics etc).

Corporate governance differs among countries originating from differences in the legal systems,

how well the financial markets are developed, country history, cultural differences etc.

Corporate governance is an eye watch over the managers. The board as a central remote control

decides the hiring and firing of senior managers. Corporate governance is an enabling

mechanism to check on firms. Good management is important for good performance. And good

performance is beneficial for all stakeholders and for the whole economy.

5 S. Thomsen, ’Introduction to Corporate Governance’, 2008, p. 15

- 5 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

As discussed in the relevant literature there is not one shoe that fits all solutions to the

governance of all firms. The right solution might differ from firm to firm, industry to industry,

and country to country.

The main task of corporate governance is to ensure good management through employing the

right managers, properly motivating them through different reward systems and giving them

enough freedom to act, and combining such a system with checks that prevent the abuse of

power. Thus, we can conclude that good governance is essential for good economic performance

both at micro and macro level.

1.2 The Agency theory At the heart of the corporate governance is the agency problem (i.e. the agency theory). The

agency theory was first explained by Berly and Means (1932), in their work titled ‘separation of

ownership and control’. Thomsen (2008) argues that it would be less misleading to term it as

separation of ownership and management. The basic idea is that owners (principals) hire the

managers (agents) to manage their wealth or assets on their behalf for a certain promised

compensation (e.g. salary). This relationship gives raise to a problem since both parties have

their own self-interests involved; the agents might not always act on the best interests of the

principal.

Corporate governance thus provides mechanisms that help to eliminate the agency problem. For

example, laws6 and regulations can play a role to ensure that agents act as expected and hold

them responsible for their actions (inactions). Thus, laws are the most fundamental governance

mechanisms. However, there are informal tools such as trust and reputation.

Other mechanisms could be the presence of large owners or owners who are at the same time

managers. Such group of investors are more interested in monitoring management based on the

6 In the US there is fiduciary loyalty.

- 6 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

large amount of wealth that they have invested or based on emotional bonds with a firm in case

of a family firm.

Managers can be motivated to perform well due to incentives (e.g. bonuses or stock options) or

else they can feel threatened by being fired and ruing their reputations.

Agency theory, a main approach to corporate governance, is thus concerned with finding

solutions to the agency problem when both the owners and managers are rational and seek their

self interest. Economic theories of corporate governance include agency theory, transaction cost,

and incomplete contract theory. Sociologists and psychologists argue against the ‘rational

behavior’ of individuals, claiming that people do not always act rationally and on their best self-

interest.

In the real world there are often more than just two actors (principal and agent). A board elected

by shareholders is a sort of intermediary between the owners and managers; however, not all the

firms have boards. It is often a legal requirement to have a board for large firms. The

shareholders can be individuals, founders or members of founding family, institutional investors,

mutual funds or hedge funds. As the interests and stakes of the owners differ, so does their

involvement in a firm. Some of the owners are actively involved in monitoring the management,

while others might just enjoy the ‘free ride’.

Other stakeholders also play an important role to directly or indirectly influence a firm’s

corporate governance (e.g. banks, employees, suppliers, customers, governments, media, and

NGOs). Auditors, analysts, and stock exchanges play a special role by providing information to

shareholders7 and other stakeholders.

7 We use the terms shareholders and stockholders interchangeably

- 7 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Types of agency problems:

1) Owner-manager problems: arises between shareholders and managers. Agents

do not always act in the best interests of the shareholders.

2) Agency problems between majority and minority investors: occurs if there

are conflicts of interest between two groups. For example a founding family in

control of the firm may have different views from those of the minority investors.

The family in charge acts on behalf of the other investors, so in this case the

family is the agent, while minority shareholders are the principals.

3) Agency problems between shareholders and stakeholders: occurs when

shareholders make decisions which influence the welfare of stakeholders. These

kinds of agency problems are mostly associated with corporate social

responsibility.

The owner-manager agency problem begins with separation of ownership and management.

Owners that also manage their companies have a natural tendency to work hard and consume

company resources for their own benefits less, since the performance of the firm have effects to

their private wealth consumption ultimately. If they consume firm resources they are more likely

to do so if the costs of consuming at the firm were less than if they had consumed at home (due

tax advantages and etc). Professional managers are more prone to consume firm resources and

extract private benefits, since they are getting extra value in addition to their assigned salaries.

Since they are not managing their own wealth, they are happy to consume firm resources.

However, they are going to put the necessary effort not to lose their job.

Separation of ownership and management makes specialization possible. From one side we get

owners that are the suppliers of finance and the management, on the other side suppliers of

human capital.

Some of the generic agency problems: criminal activities on the part of the manager; ‘self-

dealing – using firm money for the activities that benefit themselves (e.g. buying the raw

materials from a company that belongs to his or her family); excess expenditure (e.g. company

- 8 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

jet); empire building (e.g. especially through mergers and acquisitions, buying companies in

unrelated sectors to increase the size of the company); over-investment (same as empire

building); entrenchment (some managers create barriers which makes it difficult for them to fire

them and they then stay on for too long.

Other key elements of agency theory are:

Rationality - both principal and agent are rational and rationally further their own interests.

Asymmetric information - the agent is better informed about his own abilities, his own activities,

and what is going on in the firm than is the principal. If the asymmetric information did not exist

agency problem would disappear, since the principals would be able to perfectly evaluate the

performance of the manager.

Uncertainty (risk) - the existence of ‘other factors’ – weather, bad luck, and unforeseen changes

of any kind – means there is no one-to-one relationship between the activities of the agent and

the outcome.

Risk aversion - Performance pay will usually involve some kind of risk for the agent (either

over-or underpay), and the risk aversion will demand compensation for this. If the agent is

sufficiently risk averse, he will only want to work for a fixed pay to avoid economic uncertainty

all together. Then the principal bears the risk.

There are two problems related to the information asymmetry: moral hazard (i.e. hidden action)

and adverse selection (i.e. hidden knowledge). In adverse selection the events or activities occur

before the principal makes a decision (e.g. hiring a CEO). It happens when one party knows

more than the other party. For example when hiring a CEO, the shareholders might not fully

know how his capabilities. Shareholders can for example check his references from previous

- 9 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

work. The classic example of adverse selection is a used car market (also called lemons

problem). Again monitoring or screening can be a solution to the adverse selection.

Moral hazard occurs after the decision has been made (e.g. the hired CEO expropriates perks). It

is encouraged by the fact that principals can not always know what the manager is doing.

Shareholders can not keep the track of what top management is doing: they might be playing

golf, empire building. Giving incentives to the managers could be a solution, for example, a

yearly bonus for increased revenues or stock options so that managers can benefit from the good

performance of the firm in addition to their fixed salaries8. In this case some of the risk is passed

from the shareholders to the managers and managers receive an incentive to act in the interest of

the stockholders. Monitoring in the form of yearly audit checks could show how the CEO has

performed and how well the company is doing.

Thus, we can conclude that agency theory, a main approach to corporate governance, is

concerned with finding solutions to the agency problem between owners and managers who are

rational and seek their self interests in the presence of asymmetric information.

1.3 Corporate ownership Ownership is a set of rights concerning assets such as: user rights, profit rights, control rights,

transfer rights. With ownership comes the inherit responsibility. These rights can be combined

and de-combined in many different ways to create value (Thomsen, 2008).

Ownership of the firm

While shareholders of a public company cannot consume the assets of the company they do have

the rights to claim profits (e.g. dividends), rights to transfer (e.g. buy and sell their shares), and

rights to control (e.g. decide who is going to manage their firms and etc). However, they don’t

have to manage the firm on a regular basis nor be responsible for the repayment of the debt in the

case of bankruptcy. Jensen and Meckling (1976) suggested that exactly this feature of limited

8 Stock options saw their danger in forms of creative accounting and fraud in the case of Enron scandal in 2001

- 10 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

liability allows for the dispersed ownership. The limited liability perhaps is one of the

foundations of capitalism. The combination of the rights that an owner can have might depend on

the type of a firm. Companies can issue different classes of shares, with voting rights and non-

voting rights (which is well spread in corporate Europe). In cooperatives one can have both

control and profits rights, but might not have the transfer rights9.

Ownership structure

For widely held firms, there are two important features of the ownership structure: who are the

owners and how much do they own. The ownership stakes decide how much of a say an owner

can have over the managers, and the identity of the owners is influences the capital structure,

corporate strategy, growth rates etc based on the objectives and how the influence is executed.

We can measure the ownership concentration by finding the largest shareholder stake. For

example if a largest shareholder owns not more than 5 percent of all shares outstanding, it can be

assumed that ownership structure is dispersed, and if his or her ownership stake is more than 10

or 15 percent, it is a case of a concentrated ownership.

Agency theory suggests that the ownership stake of a single shareholder is a tradeoff between

risk and incentive efficiency. Large owners naturally are more motivated to monitor the

manager’s behavior than small shareholders as they more fortunes invested in the firm, and as a

result the risks borne by the large shareholder increases (Shleifer and Vishny, 1997). The firms

in regulated industries tend to have less concentrated ownership structures due to lower

uncertainty, while firms in more uncertain environments tend to have more concentrated

ownership. Thus the largest stake of ownership is going to differ from firm to firm due to firm

specific risk.

According to Fama and Jensen, (1983), Shleifer and Vishny, (1997) the relationship between

ownership concentration and firm performance is not necessarily uniform (monotonic), but bell 9 Similarly family owned companies can have agreements between each other not to sell their shares to people other than family members.

- 11 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

shaped. They suggest that up to a certain level of concentration, large shareholders are effective

to monitor the management and induce value maximization, however beyond a certain point; the

large owner becomes too powerful and starts to seek private benefits. As well as the risk profile

of the large owner becomes extremely high and undiversified. Once, a full control is reached, the

curve might head up again, as the owner realizes that he or she is going to bear the consequences

of the activities that deviate from the value maximization goal.

Owner identity

The accepted assumption in agency theory is that all individuals act to maximize their

profits/value, which is ultimately to maximize their utility. Many owners, such as banks,

companies and institutional investors act as intermediate agents to final owners. And

theoretically profit maximization is possible when markets are complete, and while they are not

in reality (when all risk in not diversifiable), even profit maximization seeking owners might

disagree about corporate strategy due to different risk preferences and the timing of expected

cash flows.

Thomsen (2008) suggest relative costs and benefits ownership for each owner as a benchmark

for assessing its dominant objectives. There are transaction costs associated with each kind of an

owner (i.e. banks, government etc). As each of them can become owners, they are relieved by the

cost of market contracting. Thus, the opportunity cost of assigning rights to another stakeholder

consists of sum of ownership plus added costs of market contracting. Thus the optimal type of –

j- minimizes transaction costs which consist of ownership costs (CO) and costs of market

contracting (CC):

Min (COj + ΣJ≠ICCi) by j,

‘ I’ is an index of the firm’s stakeholders. Furthermore, regardless of the optimality of the present

owners, the economic behavior of individual ownership types is likely to be influenced by their

ownership costs and benefits.

- 12 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Following tables list the expected advantages and disadvantages associated with each kind of an

owner:

Investor ownership

Investors usually have low risk aversion and long term investment horizons. Institutional

investors are characterized by portfolio investments and easy relationships with the firms.

Their objectives can be described as shareholder value and liquidity. Institutional investor

ownership is expected to have a positive impact, despite their low ownership stakes

which makes is a bit difficult for them to influence managers. Rose (2005) finds negative

impact on performance based on the data set from Denmark.

Family ownership

Families are considered to play a double role for the firm as both owners and managers.

They are seen as risk averse, since they have invested large stakes at the firm, and are

often capital rationed. They are also prone to expropriate minority shareholder wealth.

Bank ownership

Bank ownership is different among countries. In the, US banks are not allowed to have

ownership stakes, and in U.K. banks are not that common either. However, banks play an

important role in German-based models and are crucial as providers of financial services

to industrial companies. Often due to their ownership stakes, banks might have

internalized their relationships with firms providing them with a better access to capital,

information and other services that banks provide. There seems to be a positive effect of

bank ownership on firm performance and firms are less likely to be credit rationed.

Corporate ownership

Corporations can also act as owners. In Japan (e.g. keiretsu system), France (e.g. cross-

holdings), and Sweden (e.g. business groups), in South Korea (e.g. Chaebols) companies

hold large stakes in other companies. Most of the time these companies have some

relation to the firm, for example it could be its supplier of certain inputs or distributing

company, thus a connection in the value chain. Such ownership both have advantages and

disadvantages, while these companies maybe immune during a downfall in the economy,

- 13 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

other times it leads to inflexibility and risk of inefficient monitoring.

Government ownership

Governments often have political goals as owners such as lower prices, employment, or

external effects relative to profitability. In welfare economics, non-profit maximizing

behavior can be a key rationale. Everything else being equal, state-owned companies are

expected to be low performers in terms of conventional performance measures.

Thus, the conclusions are that corporate ownership is important to business strategy and value

creation. The best owner of a company is the one who create most value with it, which involves

weighting costs and benefits of ownership. Some important determinants of ownership are

capital, risk aversion, information, competence, business relations etc.

- 14 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Chapter 2

2.1 Literature review In this chapter we would like to present the main theories and models by different authors as a

framework for our research questions.

Defining a ‘firm’

Coase (1937) is known for his seminal contribution to defining boundaries of a firm as a range of

exchanges over which market system was suppressed and resource allocation was instead

accomplished through authority and direction. He focused on costs of using markets to effect

contracts and exchanges and argued that whenever it was expensive to use the market system,

firms emerged. However, Alchian and Demsetz (1972) questioned this argument, emphasizing

that such exchanges were of voluntary nature on contrary to being enforced by authority.

Monitoring is seen as a way to control joint input or team production. Jensen & Meckling (1976)

in critic of Alchian & Demsetz (1972) point out the narrowness of the joint production notion,

and highlight that contractual relations were not limited to employees but to suppliers,

customers, and so on, that agency and monitoring costs are present in all these contractual

relationships.

Jensen & Meckling (1976) emphasize that agency theory lies at the core of the firm or any

cooperative effort. They define the agency costs as such: the monitoring expenditures by the

principal, the bonding expenditures by the agent, and the residual loss.

They hypothesize that as a firm grows larger, agency costs incurred increase as they become

more costly to monitor. However, they argue that agency costs can decrease as the level of

managerial ownership increases, which leads to decreased monitoring costs. Similarly, lower

agency costs are associated with higher firm values other things being equal.

- 15 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

A simple model10 with a single investment period below explains the agency costs of outside

equity. When the manager is the sole owner he enjoys all the pecuniary benefits and bears all the

costs, as he starts to share the ownership, he continues to consume similar non-pecuniary benefits

however the fraction of the costs are now born buy outside equity providers. As outside equity

providers are aware of these interests of the manager, they evaluate the market value of the firm

accordingly. Thus, the model shows that at the end managers are negatively affected by the

agency costs (i.e. reduction in the value of the firm) and are well off trying to reduce such costs.

It also explains why managers engage in bonding costs (e.g. providing extra information on firm

accounts).

Figure.1. Determination of the optimal scale of the firm in case of where no monitoring takes place. Point C denotes optimum investment, I*, and non-pecuniary benefits, F*, when investment is 100% financed by entrepreneur. Point D denotes optimum investment, I’, and non pecuniary benefits, F, when outside equity financing is used to help finance the investment and the entrepreneur owns a fraction a’ of the firm. The distance A measures the gross agency costs.

The drawbacks of their model lie in the fact that they consider only a single investment financing

decision, instead of multiple investments and long-term horizon, and it also ignores the

relationship between owners/managers and other equity holders.

10 In this case the manager is also the owner with 100 percent stake

- 16 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Demsetz & Lehn (1985) explore the forces that influence and arguably explain the variance of

corporate structure (i.e. the diffused and concentrated ownership) of firms which is consistent

with the value maximization. The main disadvantage of diffused form is shirking11 by owners,

in which case costs of such behavior are shared with other owners (while benefits not always)

and unless other offsetting advantages exist to diffused form, owners are more likely to keep

ownership in a small group of owners, which gives them more control and influence12 in the

outcome of firm success. According to authors following are factors that influence the structure

of ownership form:

Value maximizing size of the firm

A viable size of firms differ for industries and the larger the firm gets, the better for the

value of the firm to have a diffused ownership structure, since concentrated ownership

gets too costly13.

Control potential

In unstable environments14 it is beneficial to have concentrated ownership as owners

believe they can influence the firm-specific risk, and that it would be difficult to evaluate

the performance of the manager.

Systematic regulation

Regulation by government of certain industries (such as utilities) works as of subsidized

monitoring and tight control does not pay off with increased profitability since the

operating environment is more or less stable.

Amenity potential

Extra benefits such as prestige, popularity are characteristic of certain industries such as

sports and media) are argued to influence the structure of ownership form.

11 An example of which could be free riding on other owner’s efforts to monitor management 12 As they believe the outcome of the firm is neither completely random nor completely controllable 13 To keep a concentrated ownership on a large firm would require small group of owners to stake large proportion of their wealth at the firm, which at the end turns out riskier and costlier than the cost of having diffused ownership with shirking costs 14 Where for example price of the products or inputs fluctuate constantly or speed of innovation is rapid

- 17 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

In the empirical test based on 511 US corporations from major industries (inc. utilities and

sports/media), they find that size of a firm is negatively correlated with ownership concentration,

firms from regulated industries tend to have more diffused ownership, and media and sports

firms are positively correlated with ownership concentration possibly due to amenity potential15.

They expect and find no (positive) relationship between ownership concentration and profit

rates, as they argue that decision of owners to switch to diffused ownership is done in awareness

of the consequences of losing control over managers, that higher cost16 and reduced profitability

is offset by lower capital acquisition or other profit enhancing aspects of diffuse ownership, all

consistent with value maximization.

Fama & Jensen (1983) explore the survival of organizations in which agents that make

important decisions do not bear a substantial share of the wealth effects of their decisions.

According to the authors, the central contracts17 in any organization specify 1) the nature of

residual claims and 2) allocation of the steps of the decision process among agents. Two

hypotheses suggested by authors about the relationship between risk-bearing and decision

processes of organization are as such:

• Separation of residual risk18 bearing from management leads to decision systems that

separate decision management (DM - which involves initiation of proposals and

implementation and usually performed by the same agents) from decision control (DC -

which involves ratification of proposals and monitoring the performance usually

performed by the same agents).

• Combination of DM and DC in a few agents leads to residual claims that are largely

restricted to these agents.

15 Which is mostly attributed to family and individual holdings against institutional holdings 16 Meaning costs associated with increased monitoring, shirking etc 17 Firm is seen as a nexus of contracts, both written and unwritten according to Jensen & Meckling (1976) 18 The residual risk is risk of the difference between stochastic inflows of resources and promised payments to agents – is borne by those who contract for the rights to net cash flows. These agents are called the residual claimants or residual risk bearers (e.g. a share (shareholder) of on a public corporation is a residual claim (residual claimant).

- 18 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

In certain organizational forms it is efficient to combine the DM and DC functions in one or few

agents19, in such cases an efficient way to control for agency problem would be restricting

residual claims to the decision makers, supported by the examples of proprietorships, small

partnerships, and closed corporations in small-scale production activities. On the other hand,

organizations (with separation of risk-bearing from decision management) which are complex in

a way that specific information valuable for decisions is spread among many agents throughout

the organizations so it becomes beneficial to delegate decision functions at all levels to the

agents who have the relevant information, instead of allocation all decision management and

control to the residual claimants. In such cases, the agency problem is addressed by separating

the DM from DC. The efficiency of such systems then can be supported by incentive structures

that reward the agents both for initiating and implementing decisions and for ratifying and

monitoring the decision management of other agents.

Moreover in complex organizations, residual claims are diffused among many agents (e.g. large

public companies), where it is costly for all of them to take part in DC. This creates agency

problems between residual claimants and decision agents. Separation of DM and DC at all levels

of organization helps to control these agency problems by limiting the power of individual agents

to expropriate the ‘wealth’ of residual claimants.

Central hypothesis is that major mechanisms for separating decision management and decision

control are similar across organizations such as formal decision hierarchies20.

They are further supported by less formal mutual monitoring systems that are a by-product of

interaction that takes place to produce outputs and develop human capital.

19 A noncomplex organization where specific information relevant to decisions is concentrated in one or few agents 20 in which the decision initiatives of lower level agents are passed on to higher level of agents, first for the ratification and then for monitoring (found in large open corporations, large professional partnerships, large financial mutuals, and large nonprofits.

- 19 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Board of directors21 is one mechanism for decision control systems of organizations both for

large and small organizations that ratifies and monitors important decisions and chooses,

dismisses, and rewards important decision agents. Boards make it difficult for the top-level

decision management and control agents to agree effortlessly, and are a mechanism that allows

separation of the management and control of organization’s most important decisions.

Shleifer and Vishny (1986) explain and model the value increasing benefits the presence of a

large shareholder in a diffused ownership company can bring. They argue that a large

shareholder can work as a partial solution to the free rider problem. Large shareholders are

interested even in small increases in the value of their stakes, and seek the improvements at the

firm that could materialize that, which sometimes might require the change of management. As a

large shareholders tries to accumulate more shares he sends a signal to minority shareholders that

the improvements he wants to implemented (via change in management brought by takeover) are

profitable, thus making them to demand higher premium price.22

The choice of how a large shareholder is going to implement changes in the management, for

example through tender offer, proxy fight, or jawboning23, signals the expected increase in the

firm value. Moreover, dividends are seen as premiums to keep large shareholders, since small

shareholders (mostly private) prefer capital gains, while large shareholders prefer dividends due

to tax preferences and this can possible explain why dividends are widely spread, as small

shareholders might see it as a way to keep large

shareholders who provide ‘monitoring and check up’ services at their own costs.

Himmelberg et al (1999) try to give a balanced view on observed differences in firm structures

across the firms24. In their analysis of the determinants of firm value they argue that unobserved

21 As well trustees, managing partners etc depending on type of organization 22 Proposition I: An increase in the proportion of shares held by large shareholder results in a decrease in the takeover premium but an increase in the market value of the firm. Proposition II: An increase in the legal and administrative costs of a takeover will result in the takeover premium but a fall in the market value of the firm. 23 Informal negotiations with the existing management 24 for example, low levels of managerial ownership could be an optimal incentive arrangement for the firms where the scope of perquisite consumption (i.e. moral hazard problem) is already low

- 20 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

heterogeneity generates a false correlation25 between ownership and performance. They argue

that studies, which interpret the positive relation (of firm value or performance) at low levels of

managerial ownership as evidence of incentive alignment, and the negative relation at high levels

of managerial ownership as evidence for managerial entrenchment (high moral hazard), lack to

address the endogeneity problem that opposes the use of managerial ownership as an explanatory

variable. Extending the studies of Demsetz & Lehn (1985), authors use panel data26 to

investigate the hypothesis that managerial ownership is related to observable27 and

unobservable28 firm characteristics influencing firm contracts29 30.

Their results show that proxies for the contracting environment (observable firm characteristics)

faced by the firm strongly predict the structure of managerial ownership. Moreover, they report

that the coefficient on managerial ownership is not robust to the inclusion of fixed effects31 in

the regression for Tobin’s Q, thus in support of view that managerial ownership is endogenous in

Q regressions. Thus, managerial ownership and firm performance are determined by common

characteristics some of which are observable and others are not (to the econometrician).

Instrumental variables used to control for the endogeneity of managerial ownership to

performance (as an alternative to fixed effects), show some evidence for causal link, but authors

underline that this is uncertain evidence due to the weaknesses of the instruments.

25 for example, if some of the determinants of Tobin’s Q are also determinants of managerial ownership 26 helps to address the endogeneity problem 27 e.g. firm size, industry, R&D spending etc 28 examples of unobservable characteristics could be intangible assets, firm market power etc 29 If unobserved sources of heterogeneity are relatively constant over time, they can be treated these as fixed effects and panel data techniques can be used to obtain consistent estimates of the parameter coefficients. This approach provides consistent estimates of the residuals in the Q regression, which can be used to construct a test of correlation between managerial ownership and unobserved firm heterogeneity. 30 for example, in case of two identical firms, where one operates with a higher fraction of intangible assets, it would be best to assign higher ownership levels to managers to align their interests, since intangible assets are harder to monitor, and are subject to managerial discretion. This firm will have higher Q values, because the market will value intangibles in the numerator and, and the book value of assets in the denominator. Thus, in this example unobserved level of intangibles leads to a positive correlation between managerial ownership and Tobin’s q, but this relation is spurious, not causal. 31 Unobserved heterogeneity is assumed as a ‘firm fixed effect’

- 21 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

2.2 Ownership across the world One of the studies of ownership structures and types around the world was conducted by La

Porta et al (1999) reports evidence contrary to the well accepted image of ‘modern corporation’

by Berle & Means (1932)32. In their study of 27 ‘richest’ countries, they examine the ultimate

ownership33 of top 20 companies.34

For a sample of large firms35 at 20 (10) percent control level36, 36 (24) percent of the firms in the

world are widely held, 30 (35) percent are family-controlled, 18 (29) percent are State-

controlled, and the remaining 15 (19) percent are divided between residual categories. Selected

for their large size and using the stiff 20% percent chain definition of control, slightly more than

one third widely held firms cast doubt to the dominance of ‘Berle and Means’s corporation.37

As authors argue, these results point out why we should care about countries with less diffused

ownership structures (despite their insignificant role at the world stock market). It is beneficial to

understand corporate governance across the countries in the world, to appreciate what is essential

in countries where widely held firms are common, and to examine how corporate governance is

changing or can be changed, as well as to recognize the extension of widely held firms to other

countries.

Prevalence of concentrated ownership with state38 and families as more frequent ultimate owners

than financial institutions (as expected by the German-bank oriented model) is surprising. For

32 Of atomistic shareholders and influential managers 33 Defined in terms of voting rights 34 We reconstruct the results of La Porta et al (1999) in a new table, Table II and III 35 For each country they select two samples: 1) top 20 companies ranked by the market capitalization of common equity at the end of 1995 (large sample) 2) smallest 10 firms with market capitalization of common equity at least $500 million at the end of 1995 (medium firms). 36 20% cutoff is usually enough for efficient control of the firm 37 While 20 firms in U.K., 18 in Japan, and 16 in the US fit the widely held description (out of 20), 0 in Argentina, 2 in Greece, 1 in Austria, 2 in Hong Kong, 2 in Portugal, 1 in Israel, or 1 in Belgium (out of 20) show the rarity of widely held firms. 38 Authors explain high percentage of companies with state control in the sample as the result of sample content of largest firms and the continuing privatization in most countries. High stakes by State in Austria 70%), in Singapore (45%), and in Israel (40%) and Italy (40%) is explained by massive post-war State ownership around the world.

- 22 -

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

medium firms, the percentage of firms controlled by families rises to a world average of 45

percent, making it the dominant ownership pattern.

A comparison of countries with good and poor shareholder protection shows that widely held

firms are more common in the former countries than in the latter (48% vs. 27%)39. Countries

with poor shareholder protection have more of other kind of principle owners such as families

(34% vs. 25%) and state (22% vs. 14%). Interestingly, firms in good shareholder protection

countries are more commonly controlled by a widely held corporation (8% vs. 2%). The results

lead to associate dispersed ownership with a good shareholder protection country, which allows

the owners to diversify.

The difference between one-share one-vote and shares with differential voting rights seems to be

small for large firms. In the sample, it takes on average 18.6 percent of capital to control 20

percent of the votes (17.7 percent on average in countries with poor shareholder protection),

which suggest that multiple classes of shares are not important mechanisms for separating

ownership and control.

On the other hand, 26 percent of firms with ultimate owners are controlled via pyramids. That

fraction is 18 and 31 percent respectively for countries with good and poor shareholder

protection. Thus, pyramidal ownership appears to be more important means of separating cash

flow rights and control rights than multiple class shares. Pyramids are used by controlling

shareholders to make existing shareholders to pay the costs, but leave them out in the benefits of

new ventures specifically in the poor shareholder protection countries.

With exception of Sweden and Germany, cross-shareholdings by sample of firms in the firms

that control them or in the controlling chain are few and interestingly appear to be common

where they are restricted (e.g. Spain, Korea, Germany, Italy and etc).

39 The difference is statistically significant (- 1.95).

- 23 -

M.Sc. thesis 2009 ________________________________________________________________________

Family ownership and firm performance

- 24 -

Significant ownership by banks seems to be rare. In the results only 5 percent of large firms are

controlled by financial institutions, and the number is higher for countries with poor protection

countries (7 % vs. 2%). Even in countries with poor protection, bank ownership of equity is

small outside Belgium and Germany. It is interesting to note that where banks are controlling

shareholders they often control several of the largest firms (in cases of Belgium, Portugal and

Sweden).

The results also show that in an average country, the ultimate family owners control on average

25 percent of the value of the top 20 firms. Moreover, a controlling family on average controls

1.33 of the top 20 firms (for Israel and Sweden 2.5). This is evidence of very significant control

of productive resources by the largest shareholding families.

In terms of participation of families in the management of the firm they control (as e.g. CEO, the

Chairman) for all the firms (at least) 69 percent of the time. It is often argued that controlling

shareholders are often monitored by other large shareholder. But authors do not have find

another large shareholders in 75 percent of the firms in total (71 percent in families), which

suggest that controlling shareholders are not monitored by other large shareholders.

M.Sc. thesis 2009 ________________________________________________________________________

Family ownership and firm performance

25

Source: Reconstructed by author from La Porta et al, 1999

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________ 2.3 Control enhancing mechanisms (CEM) Large shareholders have more influence over the firm’s activities than smaller

shareholders due to larger voting rights their ownership stakes entitles to – which is a

case when there is one class shares. However, controlling shareholders around the world

are also found to have excess control over their ownership stakes through different

control enhancing mechanisms, or through active participation in the management.

Multiple class shares, pyramids, crossholdings – all give this extra influence, protection

to large shareholders.

Families as large shareholders are found to use more frequently control enhancing

mechanisms than other type of owners such as for example financial institutions. They

can exercise excess control over their ownership stakes in a number of ways. For

example they can hold top management positions, they can sit in the boards, they can

issue two class shares, and they can use pyramids and cross-holdings.

Multiple class shares

It is quite common for Continental European companies to issue two class shares, where

one class is superior than other in terms of how much voting rights it gives to the

shareholder. Divergence can be as much as 10 times voting rights for the superior share

class. Shareholders do not see dual class shares as a good thing and shares of such

companies are found to trade at discount in stock markets.

Pyramids and cross-holdings

Pyramids are found often in Europe than in North America, but also in many emerging

and East Asian countries. Pyramids can have as much as ten layers with a company

having 51% ownership at each layer (Morck et al, 2001). For example, Wallenberg

family in Sweden controls more than 40 % of total value of Swedish Stock Exchange,

though the value of their wealth would not get them into 1000 world’s richest people list.

26

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________ Cross-holdings are another way of keeping control in hands of all related companies.

Disentangling cross-holdings can be problematic. The difference between two methods

could be seen as pyramids used to get control over more assets, while cross-holding are

used to keep control. Crossholdings seem to be used in Japan as an antitakeover device

(La Porta et al. 1999).

Some of the researchers argue that it is not per se the family ownership of the firm that

affects value or firm performance, but the use of CEM or the lack of them (King &

Santor, 2008).

27

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________ Chapter 3

3.1 Family ownership and performance (empirical findings and discussion) In this section we discuss the empirical findings on family ownership and its impact on

firm performance. Table 3.1 gives the discussed benefits and costs of family ownership

by different researchers. Table 3.1

Source: author Despite the growing empirical evidence, the theoretical development in the area is still

lacking, which could be due to the fact that evidences are contradicting and

incomparable. A single definition of a family firms itself is not in the place.

Villalonga & Amit (2006) point out that in regard to family firm ownership and

performance the ultimate question is what agency problem is more damaging: Minority

shareholders versus large shareholders; or owner-manager conflict.

28

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________ Anderson & Reeb, 2003 empirical study on S&P500 sample was one of the early studies

that increased the interest into the area (and was an inspirational paper for our research).

They find that family firms performing better than non family firms based on both

measures: accounting measures (i.e. ROA being 6.5 % higher in family firms) and market

measures (i.e. Tobin’s q being 10% higher). Both ‘young’ and ‘old’ family firms

outperformed all other firms, against the assumption that family firms are usually young

entrepreneurial firms. Active family involvement was positively associated with better

performance (e.g. family member as a CEO instead of an outsider). They also detect a

nonlinear relationship between performance and ownership levels, the former declining

roughly after 33% of ownership threshold. They suggest that in well regulated and

transparent markets family ownership of public firms might be beneficial to reduce

agency problems.

Miller et al. (2007) conduct an empirical study on a US sample, Fortune 1000 and a

random sample of 100 small companies for the period of 1996-2000. According to them

it is difficult to attribute a superior performance to a single governance variable. They

find that only family firms with a lone founder (no other relatives being present)

outperform other ownership type of firms. They argue that ‘founder effect’ which is often

found to have positive impact on firm performance in many studies, could be due to a

single member being present at the firm. It is suggested that a presence of more than one

family members leads to the inefficiency of decision making due to squabbles among the

members.

King & Santor (2008) take a sample of 613 listed Canadian firms for the period of 1998-

2005. They see Canada having a similar regulatory system as in US, but find differences

in the frequency of family firms (more frequent in Canada), and more spread use of

control enhancing mechanisms (from here and forth ‘CEM’). Their findings confirm that

family firms without CEMs have similar Tobin’s q values as non family firms, but

superior ROA and more debt. Family firms that use CEM seems to have 17% lower

Tobin’s q ratios than other firms. They argue that it is not the family firms per se but the

use of CEMs by family firms affects negatively the firm value.

29

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________ Maury, (2006) takes a more of a cross country study. His sample includes 13 Western

European countries. Their results are insightful in terms of showing if the county level

differences matter for the performance of family firms. Their results are consistent with

the notion that family control reduces the classical agency problem, but gives rise to the

conflicts with the minority shareholders, especially when the control level is tight.

According to them, family control increases value for the firms in well regulated

economies, whereas it might turn harmful due to risks of expropriation when the

transparency is low. They find that active family participation (i.e. being involved in the

management) increased the profitability. However, the value creation was positive in

lower control levels.

Andres, 2008 conduct an empirical study on 275 listed German companies for the period

of 1998-2004. They find family firms being more profitable than both companies with

dispersed ownership structure and other firms with a controlling shareholder. They find

small number of family firms in capital intensive industries. They argue that family

ownership might not be the optimal structure for all companies and that family ownership

can have positive effects depending on what roles families play at the firms.

Villalonga & Amit, 2006 further contribute to studies conducted using the US sample.

Authors try to test all Fortune 500 companies for the period of 1994-2000, and at the

same time to separate the family effect on three parameters such as ownership,

management and control, which they think other authors failed to address in previous

studies. They find differential contribution of each element. According to them family

firms create value under certain forms of control and management. For example, family

control in excess of ownership reduces shareholder value. Family management creates

value when a founder is a CEO or the Chairman, but destroys value in all other

generations.

Barontini & Caprio, 2006 conduct a cross country empirical study of the effects of

family control on firm performance and value. What is notable of their research is that

they try to separate founder and descendants effect from that of general family control in

30

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________ 11 countries of Continental Europe. The interesting part of their findings is that how

countries with the same legal system origin (e.g. French origin: France, Spain, Italy,

Belgium) show similar patterns and results. They find more CEO roles occupied by

families in firms from Scandinavian origin countries (e.g. Denmark, Finland, Norway,

and Sweden). However, family control in these countries seems to have negative effect

on valuation and performance.

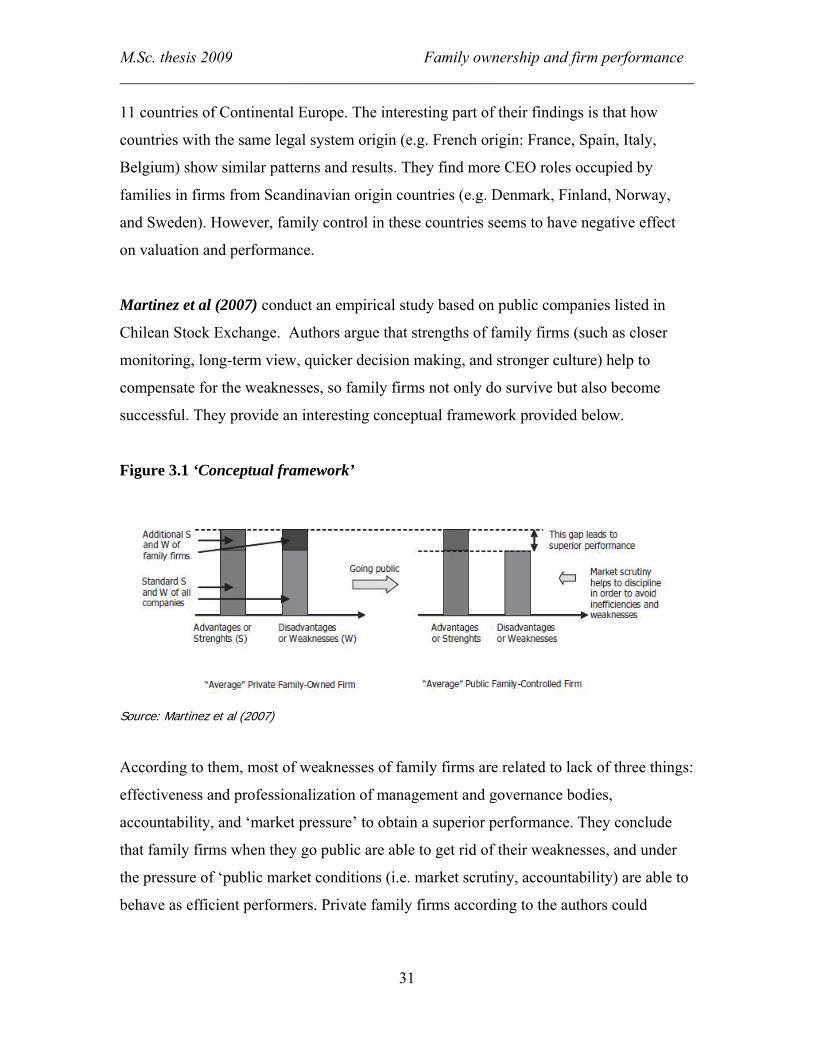

Martinez et al (2007) conduct an empirical study based on public companies listed in

Chilean Stock Exchange. Authors argue that strengths of family firms (such as closer

monitoring, long-term view, quicker decision making, and stronger culture) help to

compensate for the weaknesses, so family firms not only do survive but also become

successful. They provide an interesting conceptual framework provided below.

Figure 3.1 ‘Conceptual framework’

Source: Martinez et al (2007)

According to them, most of weaknesses of family firms are related to lack of three things:

effectiveness and professionalization of management and governance bodies,

accountability, and ‘market pressure’ to obtain a superior performance. They conclude

that family firms when they go public are able to get rid of their weaknesses, and under

the pressure of ‘public market conditions (i.e. market scrutiny, accountability) are able to

behave as efficient performers. Private family firms according to the authors could

31

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

actually improve their performance by acting as if they were under ‘public market

conditions’.

3.2 Family ownership and CEO successions

‘One of the most contentious issues surrounding family firms relates to chief executive

officer (CEO) succession decisions’, (Bennedson et al, 2007).

‘To use Warren Buffett’s analogy, those firms that pick executives from the small pool of

family heirs would be “choosing the 2020 Olympic team by picking the eldest sons of the

gold-medal winners of the 2000 Olympics.’(Perez-Gonzalez, 2006)

There are arguments for both sides of a coin as why should family CEOs perform better

or worse. Non pecuniary benefits associated with the success of a firm, might drive

family CEOs to work harder, and they might have acquired firm specific knowledge

passed down from generations, as well as longstanding loyalty and trust from different

stakeholders. Not the last, the characteristic of families - attribute of long-term

perspective about the firm prospects. Cons range from tensions between the family

members that affect negatively firm decisions, clashes of firm interests against family

interests etc. And one of the possible important impacts of families on firm performance

is their choice of succeeding CEO. If families decide to recruit from within, then the pool

to choose from is like a drop in an ocean in comparison to what markets can supply.

Few studies give that further insight to the family characteristics (Bennedson et al, 2007;

Pérez-Gonzaléz, 2006; Lin et al, 2007; Braun & Sharma, 2007).

Bennedson et al (2007) using Danish dataset40 and employing heterogeneity41 in

departing CEOs family characteristics try to explain the variation in the CEO succession

decisions (i.e. who succeeds as a CEO a family member or unrelated professional CEO).

40 CEO successions at the limited liability companies (both private and public) for the period of 1994-2002 41 They use a gender of a first born child at the departing CEO family, as a plausible instrumental variable, since the gender of a firstborn is less likely related to the firm outcome.

32

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Family successions occur in 1,776 out of 5,334 CEO successions (33.3 percent)42, and

out of family CEO successions 48.6 percent involve the children of the departing CEO.

Their results suggest that professional CEOs provide invaluable services to the

companies they lead.43 The interesting results of their study is that the gender of a first

born child in a departing CEO family is strongly correlated with a decision to appoint a

family CEO with a frequency of 29.4 (39) percent for a female (male) firstborn. Negative

impact of family CEO are detected as more damaging in fast-growing, innovative, and

highly skilled labour force industries44. Moreover, authors fail to find support for the

assumption that family CEOs engage in significantly larger investments45 relative to

unrelated CEOs. They also find that unrelated CEOs are going to be more likely to have

been a seasoned CEO, have attended college and so on, thus more qualified. Thus,

strengthening support for the CEOs with competitive managerial skills.

A concern Bennedson et al (2007) try to address with their study is that when testing the

impact of family or family-heir status on firm performance studies use cross-sectional

variation in the family-CEO status, or changes in family-CEO status around management

turnover, both of which they argue are unlikely to be random, which makes it difficult to

establish if a family CEO damages firm performance. And as authors explain further

family status and low performance ex-post could be the result of for example

endogenously determined board46 that is optimally weak relative to the CEO, and by

mean-reversion. Moreover, omitted variables, such as, antitakeover provisions could

explain both results.

A study of CEO successions at the U.S corporations by Pérez-Gonzaléz (2006) yields

comparable results. Out of 335 management transitions, 36.4 percent are identified as

42 Authors own explanation for seemingly small percentage of family successions is that strength of ‘rule of law’ in the country makes expropriation by outside managers less likely, and thus ‘safer’ to appoint unrelated CEO 43 OROA (operating profitability on assets) is found to be four percentage points lower in case of family CEO succession 44 Conversely, there seems to be no big gap in firm performance in industries where family CEOs are common 45 In attempt to diversify their tied up wealth in a single firm 46 Authors find that family CEOs underperform relative to unrelated managers even when the departing CEO’s family remains on the board of directors after transition

33

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

family successions, where incoming CEO is related to the departing CEO47 either by

blood or marriage. Overall they find that family CEOs are on average eight years younger

than unrelated CEOs at the time of appointment and secondly that firms that appoint a

family member significantly underperform relative to firms that promote a professional

CEO48: operating return on assets (Market to Book ratios) is 14 (16) percent lower within

three years of transition.

The interesting results of their study are that firms with a family CEO who did not attend

a selective college49, which occurred in (i.e. 45 percent of family CEO successions),

dramatically underperformed, operating return on assets and M-B ratios are around 25

percent lower within three years of the succession relative to firms that promote unrelated

CEO. These statistically significant results are not observed in firm where family CEO

attended a selective college.

Both studies (Bennedson et al, 2007; Pérez-Gonzaléz, 2006) do not show significant

differences in firm characteristics between the firms who select family CEO and those

who prefer an unrelated CEO in terms of size, industries they represent, profitability

ratios such as ROA prior to the transition. In general, it is not so much that professional

CEOs are overperforming, but family CEO is negatively impacting firm performance.

In the bigger picture, Bennedson et al (2007) points out that inferior managerial talent can

potentially extend beyond family firms, hurting aggregate total factor productivity, and

economic growth. These findings indicate nepotism costs dearly to firms and might be

borne by minority investors who do not share in private benefits of control.

47 Or the founder, largest shareholer 48 Firms with a professional CEO show positive abnormal returns both upon announcement and after the succession 49 ‘A “selective” college is an undergraduate institution classified as “very competitive” or better in Barron’s (1980) profiles. In 1980, a total of 189 colleges that primarily considered applicants who ranked in the top 50 percent of their graduating high school class were classified as “very competitive” or better.’(Perez-Gonzalez, 2006)

34

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Another interesting study on choice of CEO at the family firms is by Lin et al (2007),

who take a sample of listed family firms from Taiwan which has similar corporate

governance environment to emerging countries.50 An argument, authors suggest, that

perhaps operational characteristics of firms51 are to influence a certain choice of CEO

(family or unrelated) and accordingly best suited for the firm performance.

They report that presence of a family member as a CEO shows a strong relationship to

low levels of R&D, small firm size, and high advertising spending52 53. Further they find

that family firms in need of high managerial skills could improve their performance with

a professional CEO54, particularly if controlling family allows them to use their expertise

freely (in case of weak control and low cash flow rights). On the other hand, when the

risk of expropriation by an outsider (CEO) is high, firms might be well of with a family

member as a CEO, and when the family has high cash flow rights55.

Thus, the main conclusions are that family firms do perform better or worse in

combination with certain family firm characteristics (and definitions) such as

management role, presence of a founder, use of control enhancing mechanisms, or in

relation to different corporate governance environments and etc.

50 Such as concentrated ownership; spread out family ownerships, pyramids and cross-holdings; and low protection for minority shareholders 51 Emerging argument that family firms are not the same, and need to be categorized (Dyer, 2007) 52 The coefficient estimates for firm size and R&D intensity are negative: it is less likely that there will be family-member CEO for large and high R&D firms 53 For Family (Professional) CEO R&D spending is 0.67% (0.92%) of book value of assets; Advertisement spending for Family (Professional) CEO 0.69% (0.35 %) to total assets 54 The coefficient of family CEO is negative both for ROA and Tobin’s Q measures for the firms in need of high skilled managerial skills 55 The coefficient for both ROA (significant at 5%) and Tobin’s q is positive

35

M.Sc. thesis 2009 Family ownership and firm performance ________________________________________________________________________

Chapter 4

4.1 Hypothesis generation Three aspects of family ownership Amit & Villalonga (2006) advise to pay attention are

the ownership, management and control. Authors argue that without identifying these

three ways families are able to impact firm performance or value creation, it would be

difficult to separate family influence on firm performance in comparison to non family

owned firms.

Ownership

Based on literature review and empirical findings that point out the positive impact of

families on firm performance, we test the following hypotheses:

• Do family firms perform better than non family owned firms (positive or

negative effect, or no effect)?

Hypotheses 1: There is a relationship between a family ownership and

firm performance.

We are not able to test the hypothesis of if the founder-present family firms perform

better in comparison to family firms without a founder and other non family owned firms,