Embed Size (px)

Citation preview

FINANCE FOR LAWYERS

READING & INTERPRETING

FINANCIAL STATEMENTS

MARK HUNT,

TIM NEATHERCOAT,

JONATHAN COMPTON &

JAMES BARRACLOUGH

13 NOVEMBER 2013

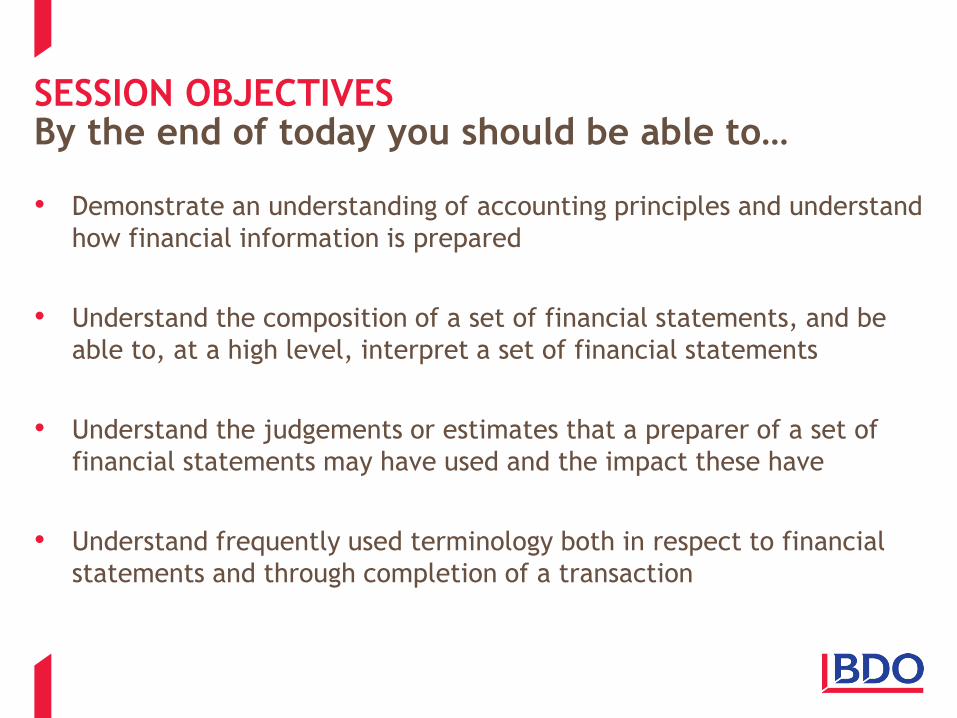

SESSION OBJECTIVES

• Demonstrate an understanding of accounting principles and understand

how financial information is prepared

• Understand the composition of a set of financial statements, and be

able to, at a high level, interpret a set of financial statements

• Understand the judgements or estimates that a preparer of a set of

financial statements may have used and the impact these have

• Understand frequently used terminology both in respect to financial

statements and through completion of a transaction

By the end of today you should be able to…

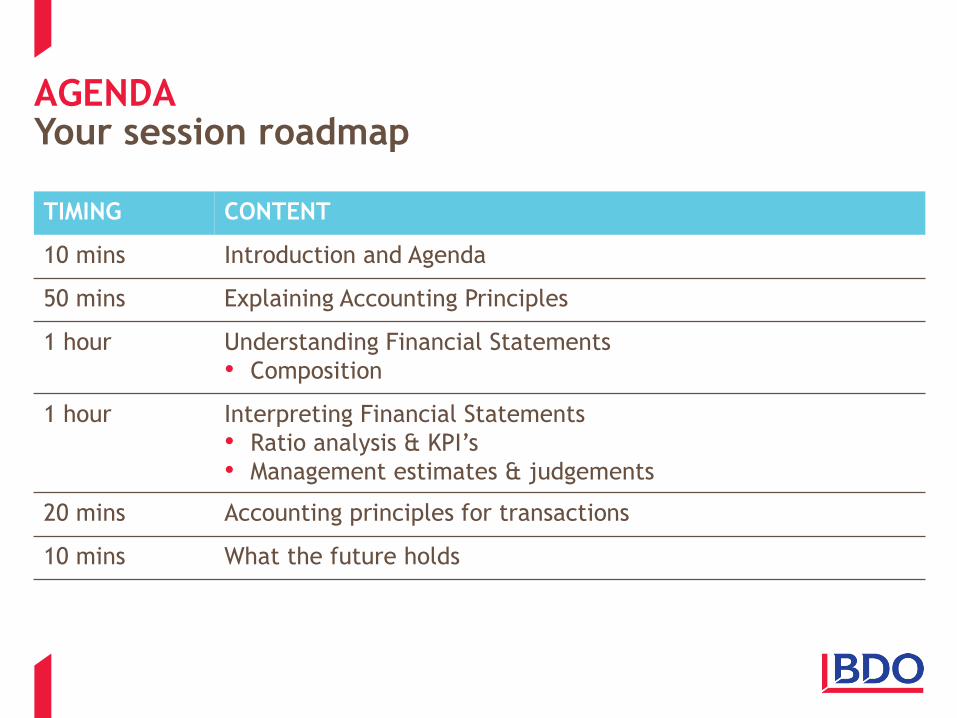

AGENDA Your session roadmap

TIMING CONTENT

10 mins Introduction and Agenda

50 mins Explaining Accounting Principles

1 hour Understanding Financial Statements

• Composition

1 hour Interpreting Financial Statements

• Ratio analysis & KPI’s

• Management estimates & judgements

20 mins Accounting principles for transactions

10 mins What the future holds

FINANCE FOR LAWYERS EVENT

EXPLAINING ACCOUNTING PRINCIPLES

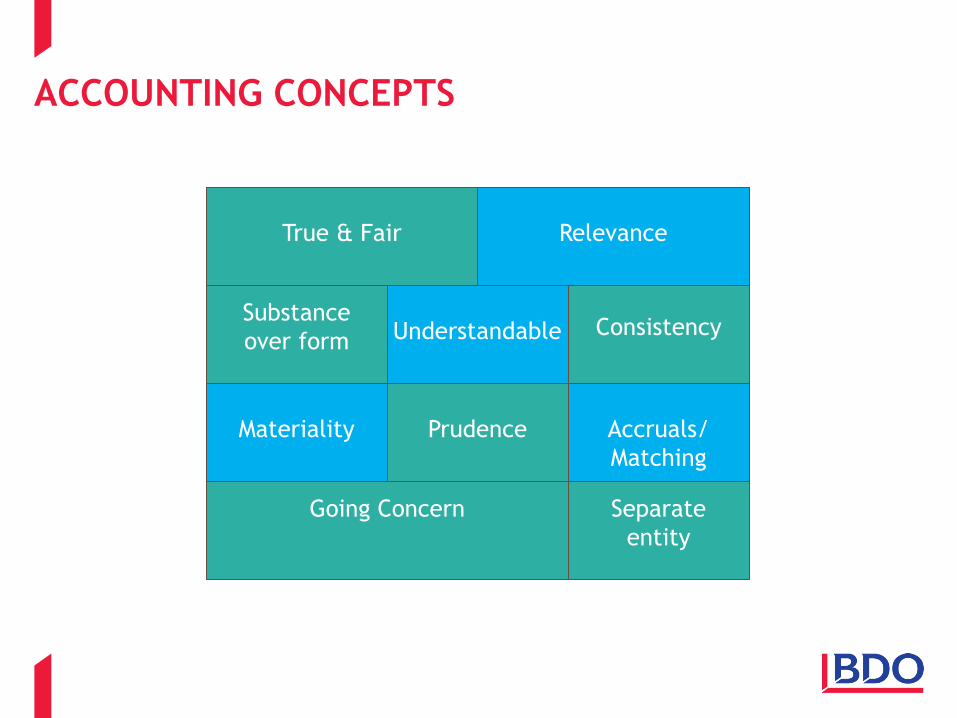

ACCOUNTING CONCEPTS

Going Concern

Prudence

Separate

entity

Materiality Accruals/

Matching

Relevance True & Fair

Understandable Consistency Substance

over form

CONCEPTS QUIZ

Working in your teams, work through the 10 accounting concept

definitions shown on the handout and create a definition for each of the

concepts.

You have 10 minutes for this activity.

Accounting concepts

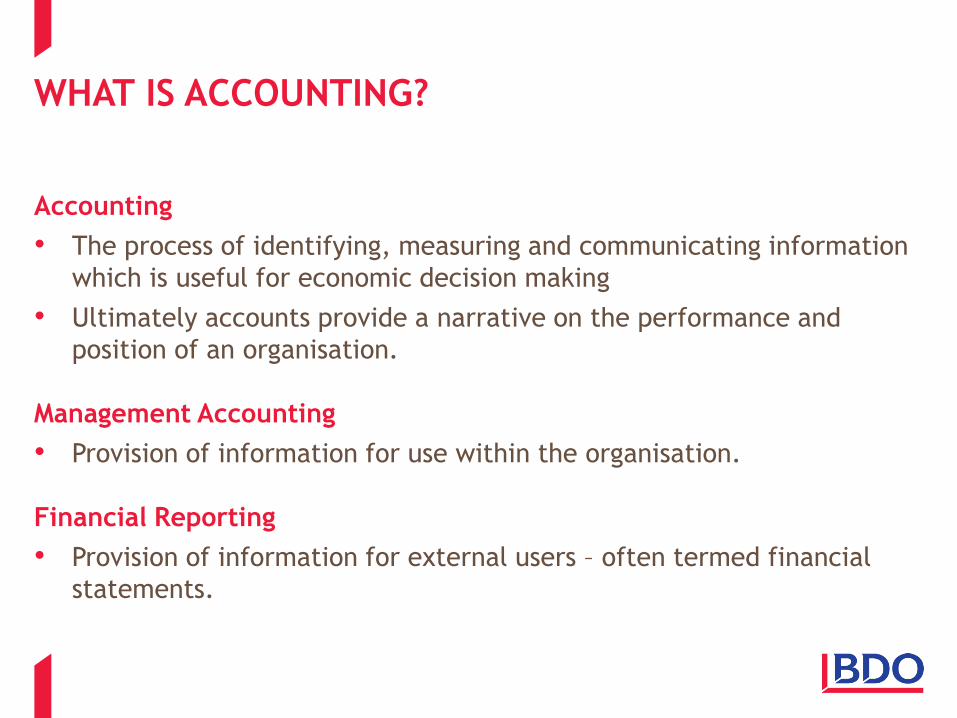

WHAT IS ACCOUNTING?

Accounting

• The process of identifying, measuring and communicating information

which is useful for economic decision making

• Ultimately accounts provide a narrative on the performance and

position of an organisation.

Management Accounting

• Provision of information for use within the organisation.

Financial Reporting

• Provision of information for external users – often termed financial

statements.

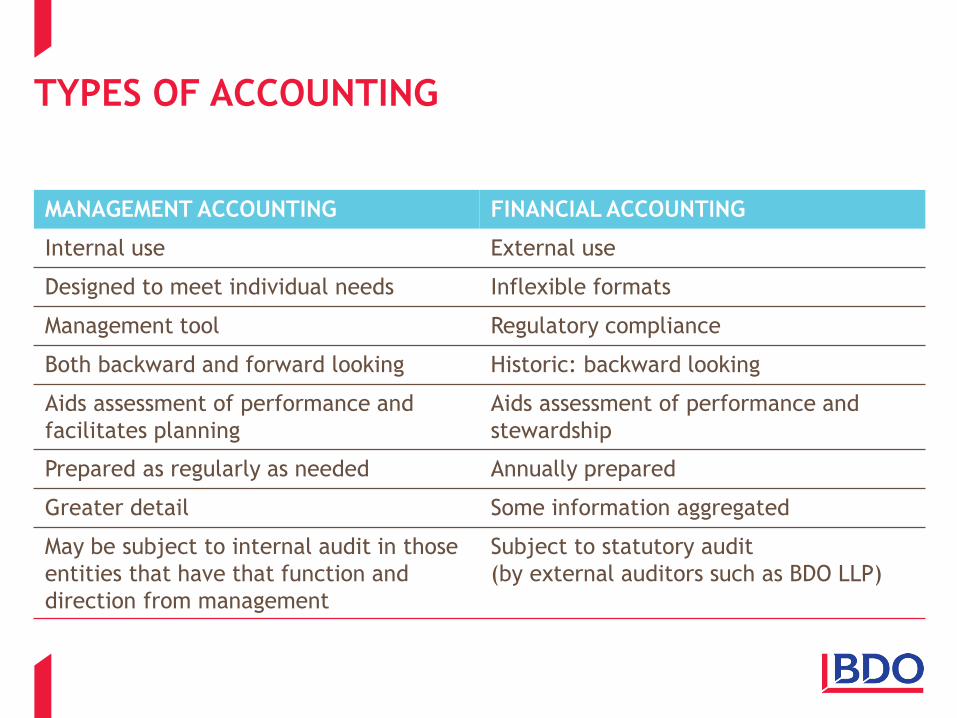

TYPES OF ACCOUNTING

MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

Internal use External use

Designed to meet individual needs Inflexible formats

Management tool Regulatory compliance

Both backward and forward looking Historic: backward looking

Aids assessment of performance and

facilitates planning

Aids assessment of performance and

stewardship

Prepared as regularly as needed Annually prepared

Greater detail Some information aggregated

May be subject to internal audit in those

entities that have that function and

direction from management

Subject to statutory audit

(by external auditors such as BDO LLP)

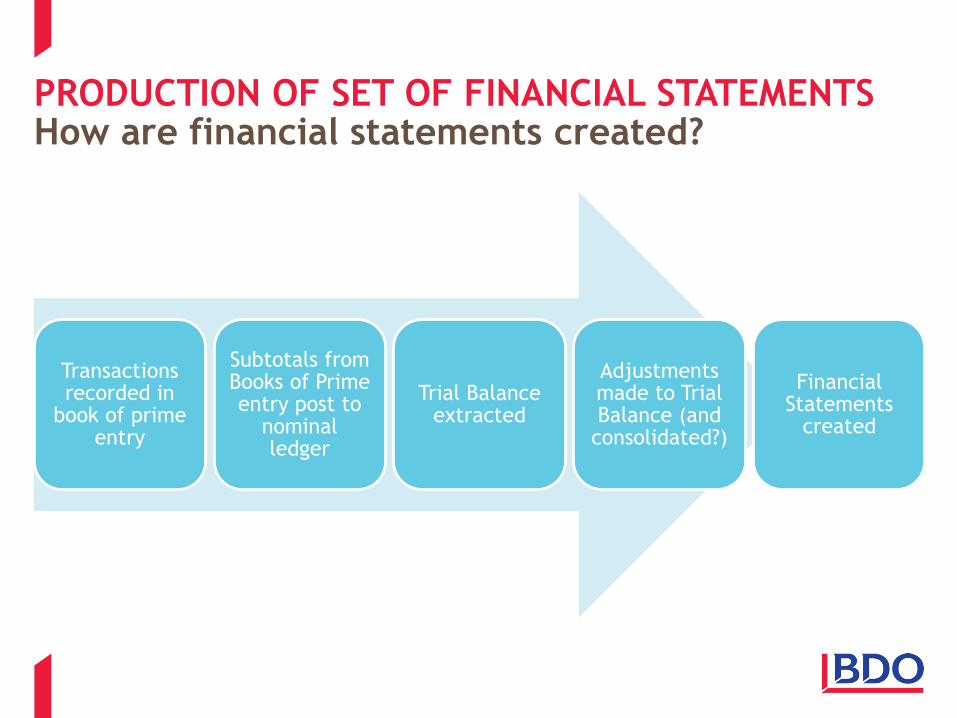

PRODUCTION OF SET OF FINANCIAL STATEMENTS How are financial statements created?

Transactions recorded in

book of prime entry

Subtotals from Books of Prime entry post to

nominal ledger

Trial Balance extracted

Adjustments made to Trial Balance (and

consolidated?)

Financial Statements

created

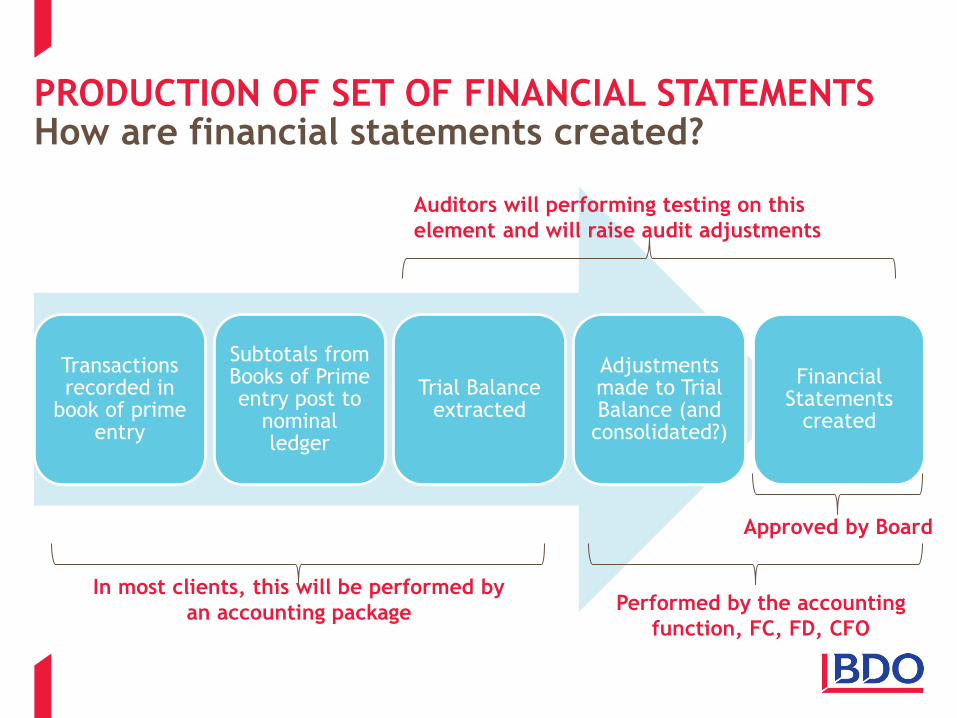

PRODUCTION OF SET OF FINANCIAL STATEMENTS How are financial statements created?

Transactions recorded in

book of prime entry

Subtotals from Books of Prime entry post to

nominal ledger

Trial Balance extracted

Adjustments made to Trial Balance (and

consolidated?)

Financial Statements

created

In most clients, this will be performed by

an accounting package

Auditors will performing testing on this

element and will raise audit adjustments

Performed by the accounting

function, FC, FD, CFO

Approved by Board

FINANCE FOR LAWYERS EVENT

FINANCIAL STATEMENTS COMPONENTS

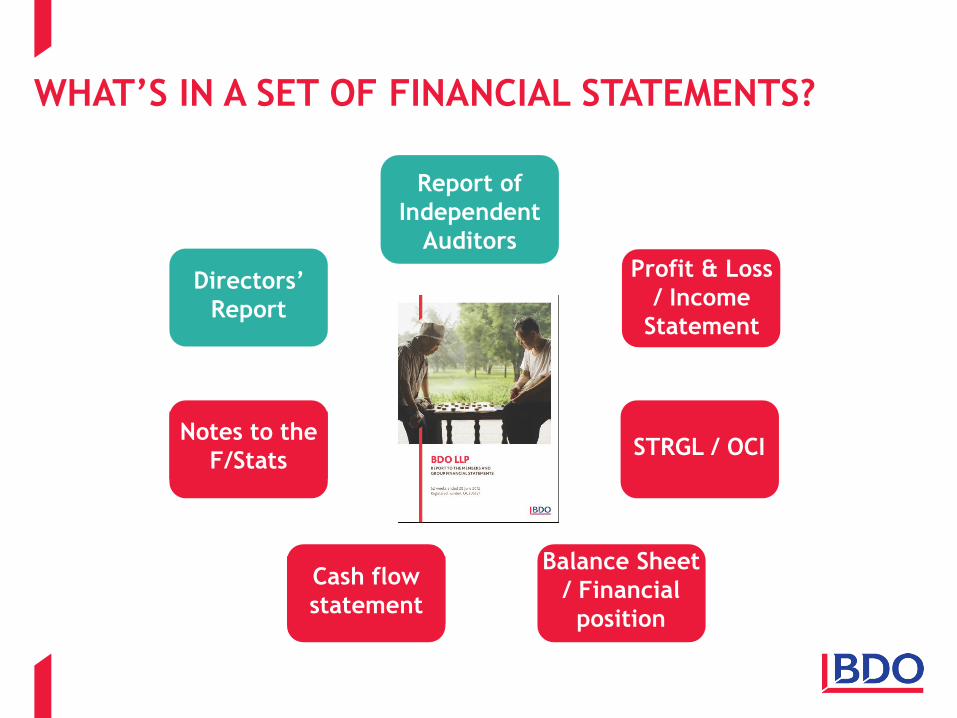

WHAT’S IN A SET OF FINANCIAL STATEMENTS?

Profit & Loss

/ Income

Statement

Directors’

Report

Report of

Independent

Auditors

Balance Sheet

/ Financial

position

STRGL / OCI

Cash flow

statement

Notes to the

F/Stats

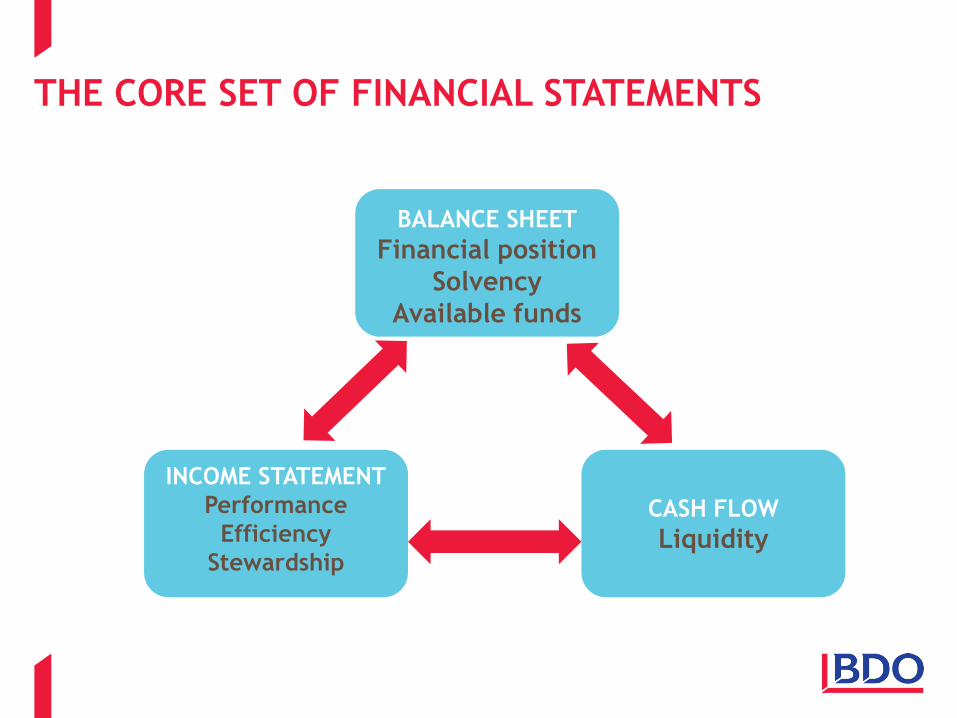

THE CORE SET OF FINANCIAL STATEMENTS

BALANCE SHEET

Financial position

Solvency

Available funds

INCOME STATEMENT

Performance

Efficiency

Stewardship

CASH FLOW

Liquidity

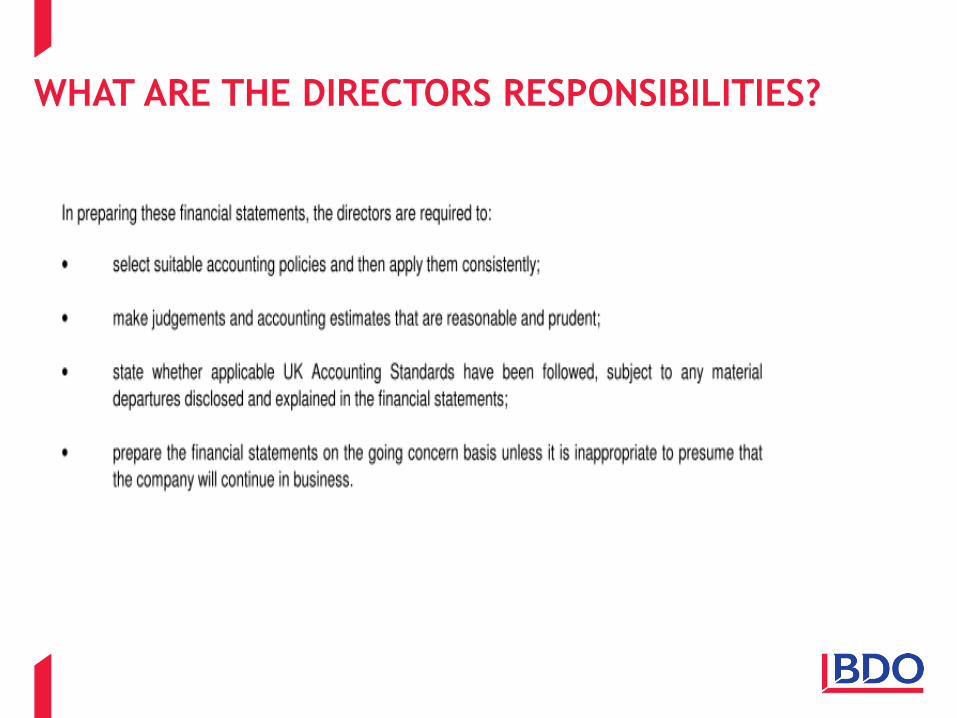

WHAT ARE THE DIRECTORS RESPONSIBILITIES?

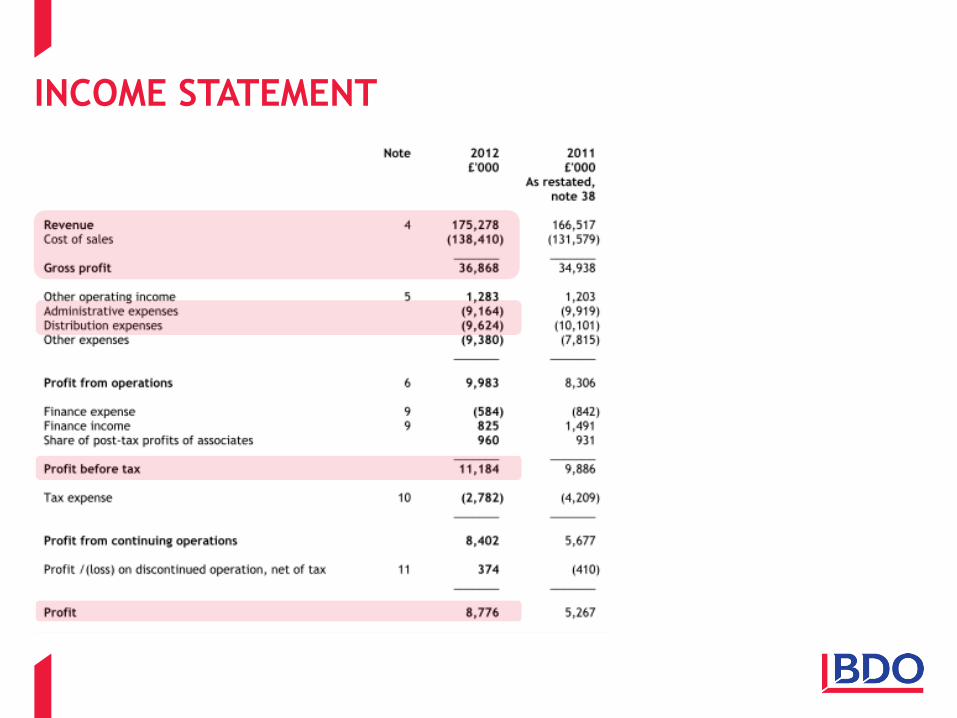

INCOME STATEMENT

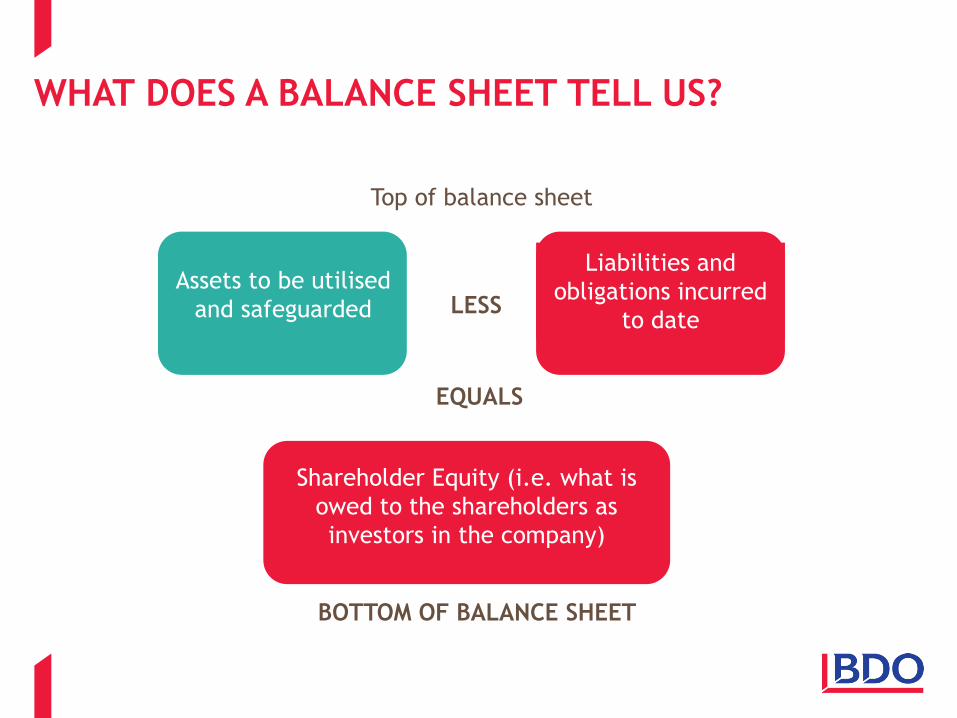

WHAT DOES A BALANCE SHEET TELL US?

Shareholder Equity (i.e. what is

owed to the shareholders as

investors in the company)

Assets to be utilised

and safeguarded

Liabilities and

obligations incurred

to date LESS

BOTTOM OF BALANCE SHEET

Top of balance sheet

EQUALS

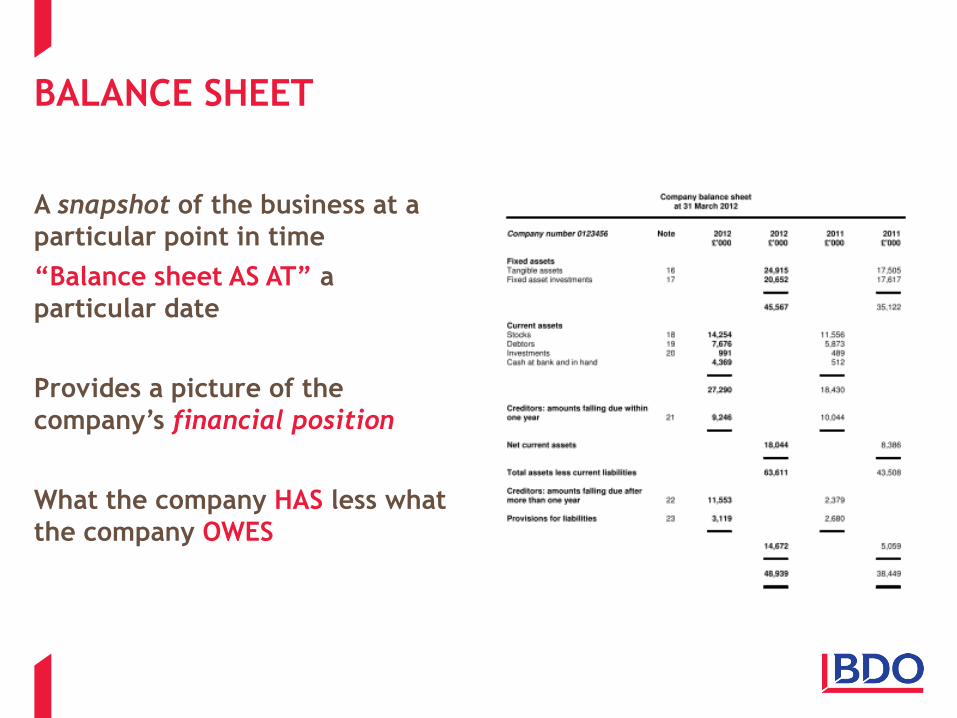

BALANCE SHEET

A snapshot of the business at a

particular point in time

“Balance sheet AS AT” a

particular date

Provides a picture of the

company’s financial position

What the company HAS less what

the company OWES

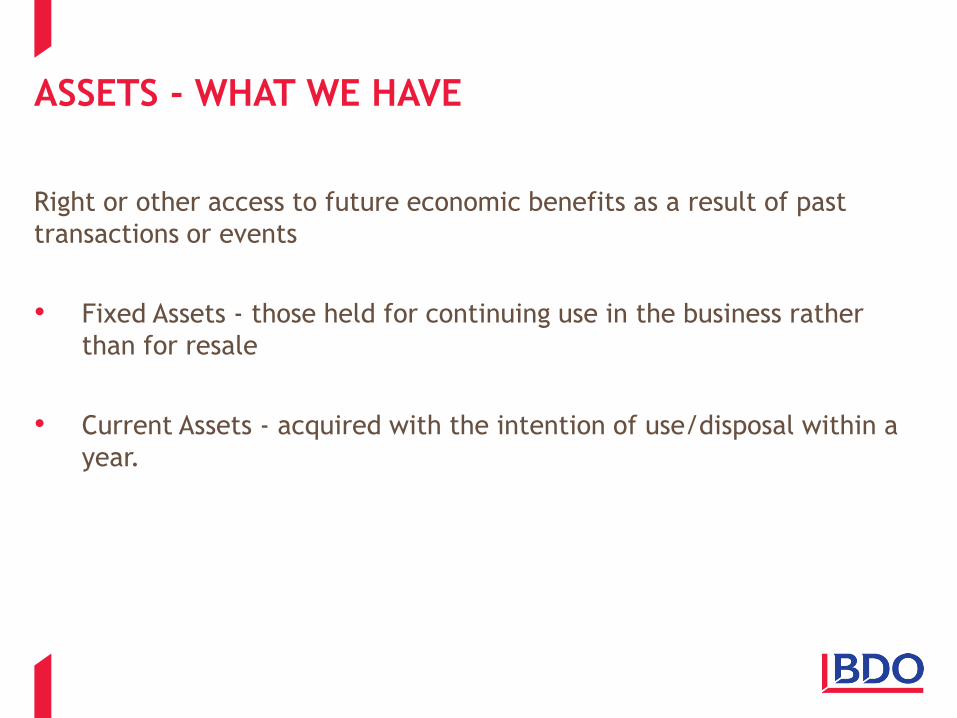

ASSETS - WHAT WE HAVE

Right or other access to future economic benefits as a result of past

transactions or events

• Fixed Assets - those held for continuing use in the business rather

than for resale

• Current Assets - acquired with the intention of use/disposal within a

year.

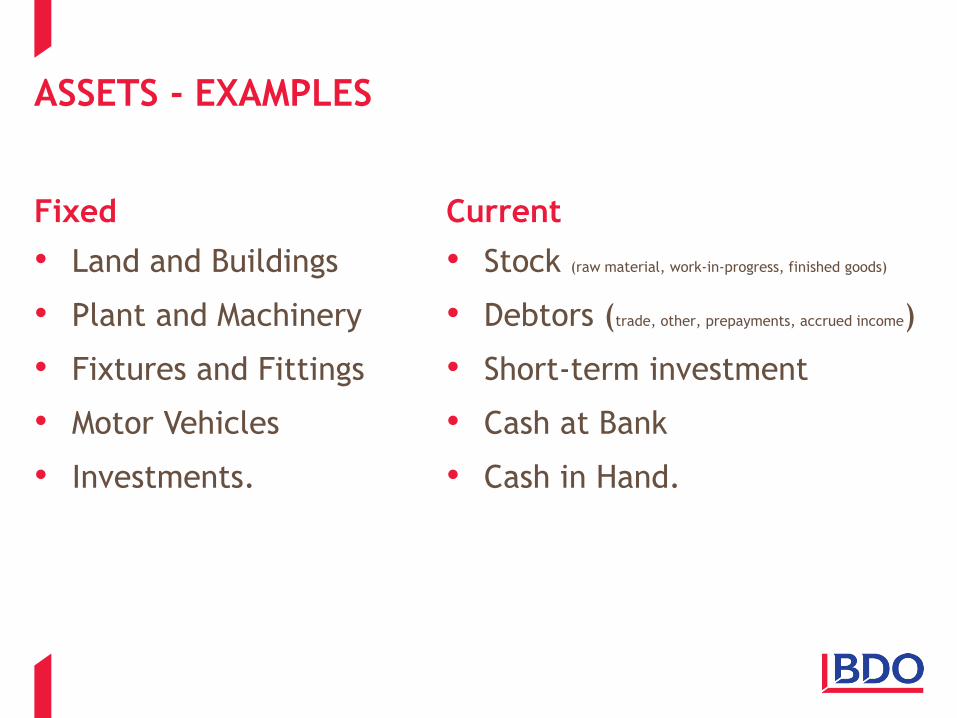

ASSETS - EXAMPLES

Fixed

• Land and Buildings

• Plant and Machinery

• Fixtures and Fittings

• Motor Vehicles

• Investments.

Current

• Stock (raw material, work-in-progress, finished goods)

• Debtors (trade, other, prepayments, accrued income)

• Short-term investment

• Cash at Bank

• Cash in Hand.

LIABILITIES - WHAT WE OWE

An obligation to transfer economic benefits as a result of past

transactions

• Current liabilities - amounts due for payment within one year

• Long-term liabilities - amounts due for payment after more than one

year

• Categorised by the Companies Act as “Creditors”.

LIABILITIES - EXAMPLES

Current

• Bank overdraft

• Trade creditors

(Owed for purchases)

• Accruals

• Lease payments/loan

repayments due within

one year.

Long-term

• Debenture loan stock

• Mortgages

• Lease payment/loan

repayments due after more

than one year.

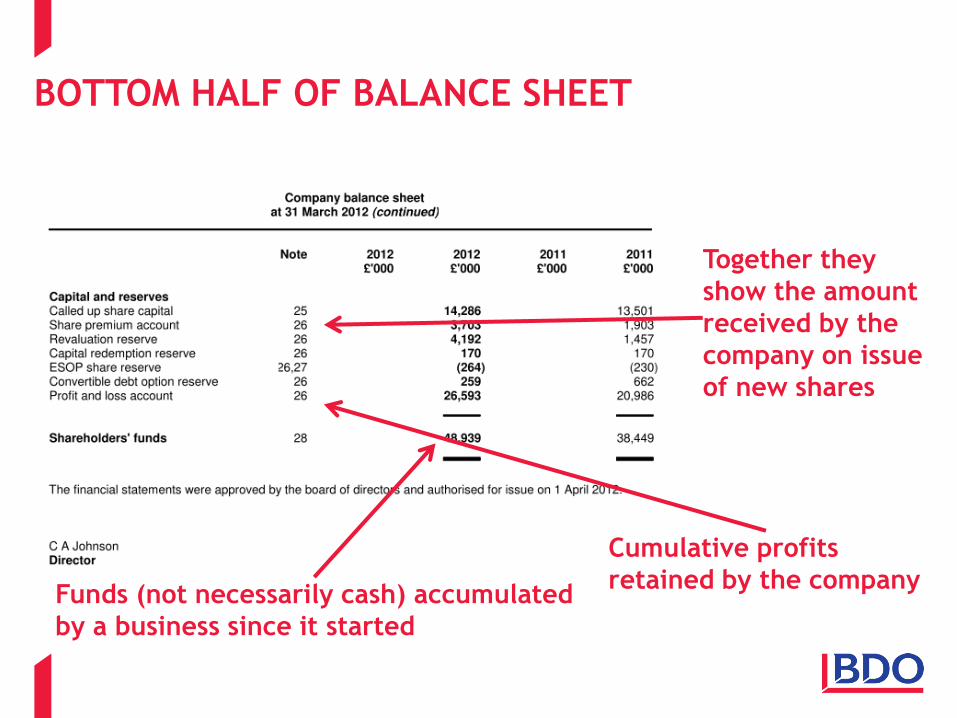

BOTTOM HALF OF BALANCE SHEET

Funds (not necessarily cash) accumulated

by a business since it started

Together they

show the amount

received by the

company on issue

of new shares

Cumulative profits

retained by the company

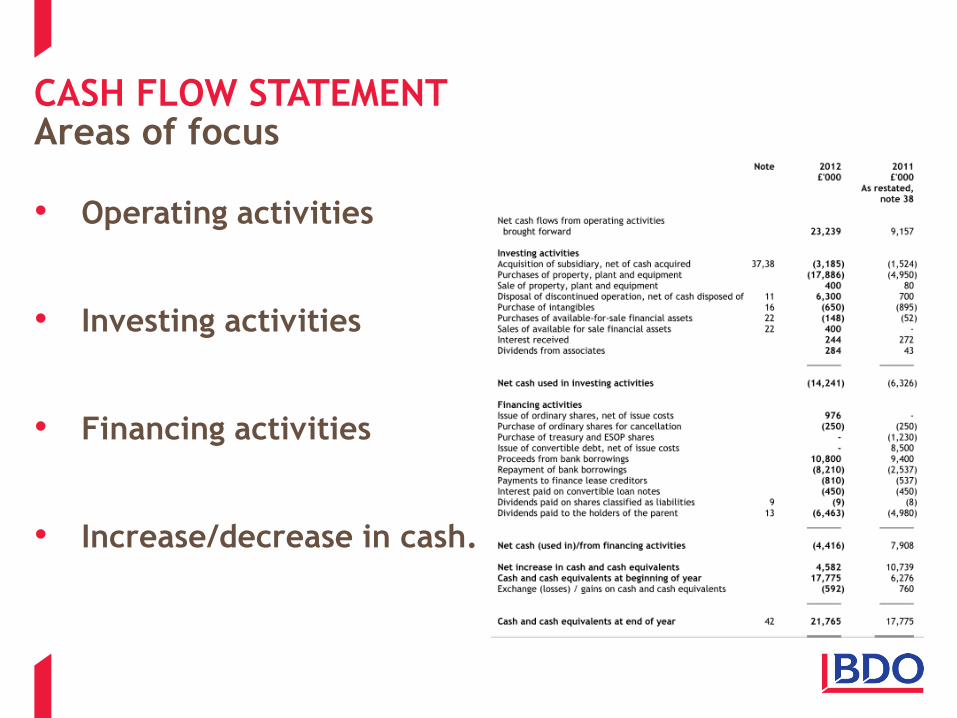

CASH FLOW STATEMENT

• Operating activities

• Investing activities

• Financing activities

• Increase/decrease in cash.

Areas of focus

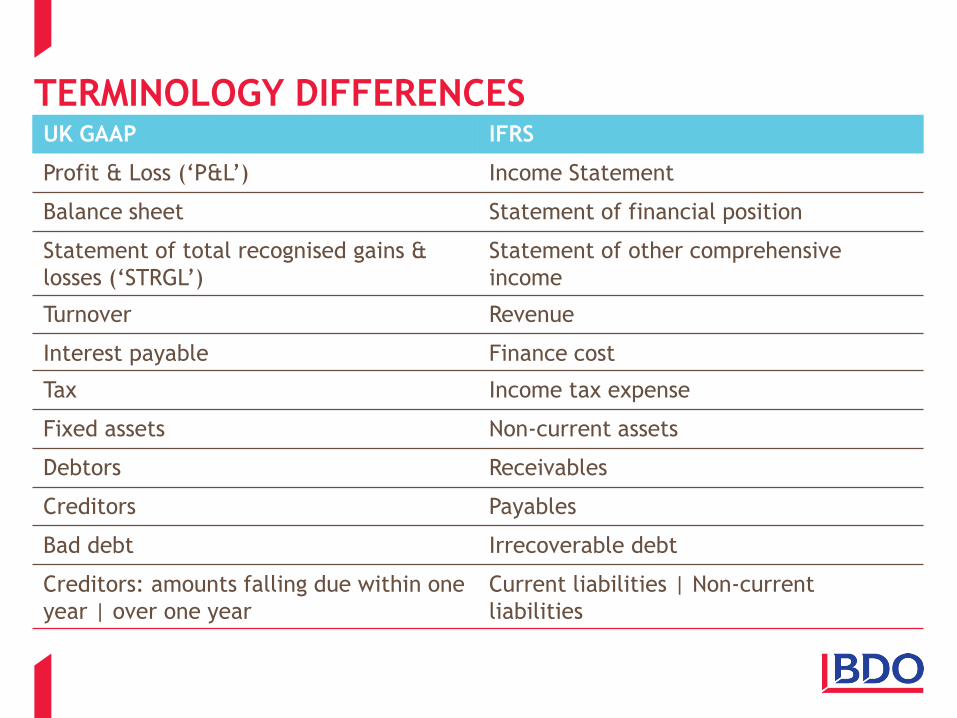

TERMINOLOGY DIFFERENCES UK GAAP IFRS

Profit & Loss (‘P&L’) Income Statement

Balance sheet Statement of financial position

Statement of total recognised gains &

losses (‘STRGL’)

Statement of other comprehensive

income

Turnover Revenue

Interest payable Finance cost

Tax Income tax expense

Fixed assets Non-current assets

Debtors Receivables

Creditors Payables

Bad debt Irrecoverable debt

Creditors: amounts falling due within one

year | over one year

Current liabilities | Non-current

liabilities

FINANCE FOR LAWYERS EVENT

INTERPRETING FINANCIAL STATEMENTS

WHO MIGHT READ THE ANNUAL REPORT AND WHY?

Directors /

Management

Competitors

Regulators

(FRRP)

Providers of

finance

Employees

Shareholders

Government

(Tax)

Lawyers

Suppliers

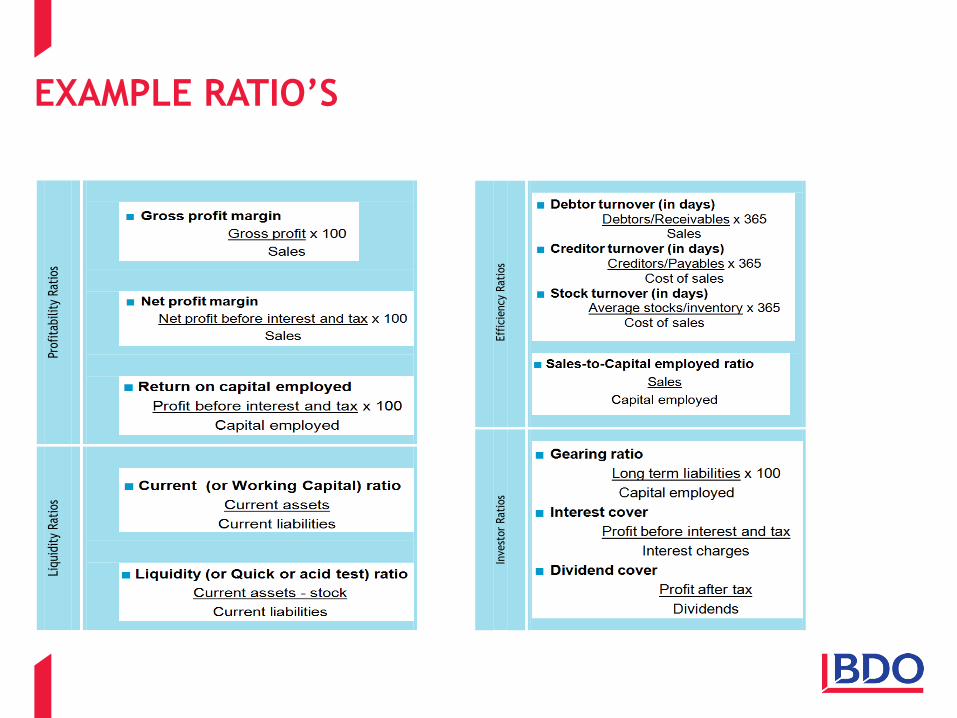

USING RATIOS Types of ratios WHY ARE RATIOS USEFUL? TYPES OF RATIOS

1. Identification of trends

2. Quick measurement

3. Overcomes problems of scale

4. Easy to calculate

5. Used with sector knowledge.

• Profitability

• Efficiency

• Liquidity

• Investment/Gearing.

EXAMPLE RATIO’S

Prof

itab

ility

Rat

ios

Liqu

idit

y Rat

ios

Eff

icie

ncy

Rat

ios

Inve

stor

Rat

ios

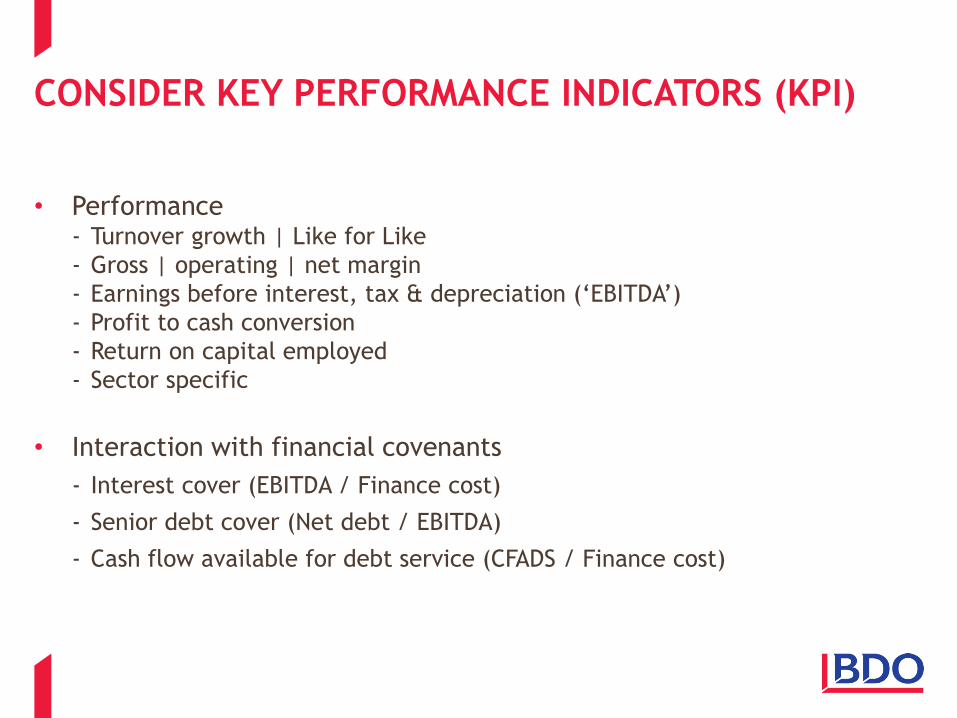

CONSIDER KEY PERFORMANCE INDICATORS (KPI)

• Performance - Turnover growth | Like for Like

- Gross | operating | net margin

- Earnings before interest, tax & depreciation (‘EBITDA’)

- Profit to cash conversion

- Return on capital employed

- Sector specific

• Interaction with financial covenants

- Interest cover (EBITDA / Finance cost)

- Senior debt cover (Net debt / EBITDA)

- Cash flow available for debt service (CFADS / Finance cost)

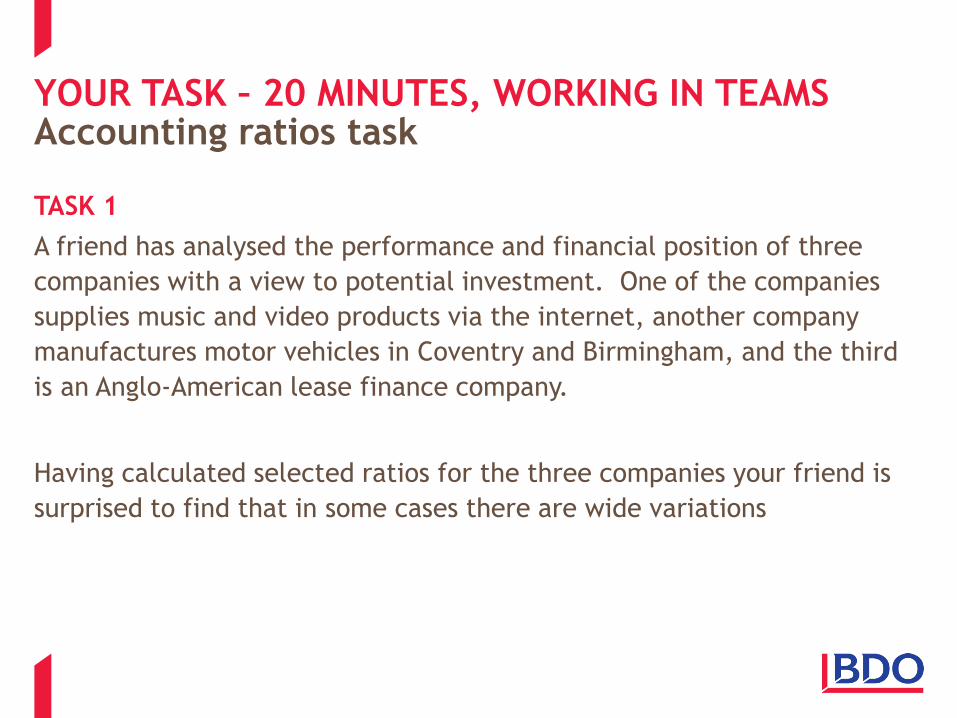

YOUR TASK – 20 MINUTES, WORKING IN TEAMS Accounting ratios task

TASK 1

A friend has analysed the performance and financial position of three

companies with a view to potential investment. One of the companies

supplies music and video products via the internet, another company

manufactures motor vehicles in Coventry and Birmingham, and the third

is an Anglo-American lease finance company.

Having calculated selected ratios for the three companies your friend is

surprised to find that in some cases there are wide variations

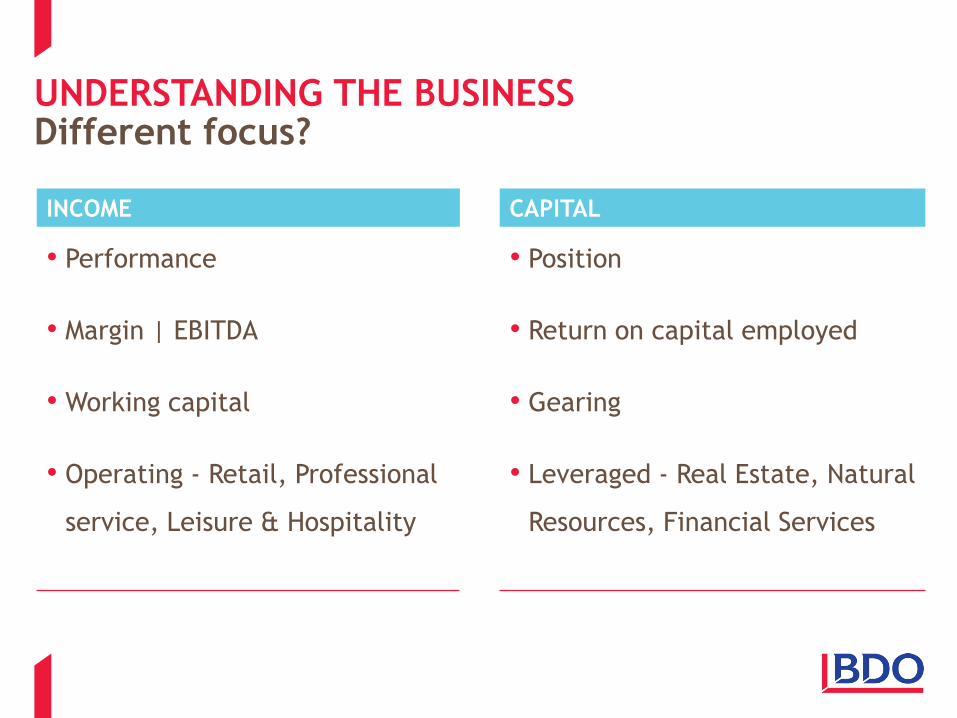

UNDERSTANDING THE BUSINESS Different focus? INCOME CAPITAL

• Performance

• Margin | EBITDA

• Working capital

• Operating - Retail, Professional

service, Leisure & Hospitality

• Position

• Return on capital employed

• Gearing

• Leveraged - Real Estate, Natural

Resources, Financial Services

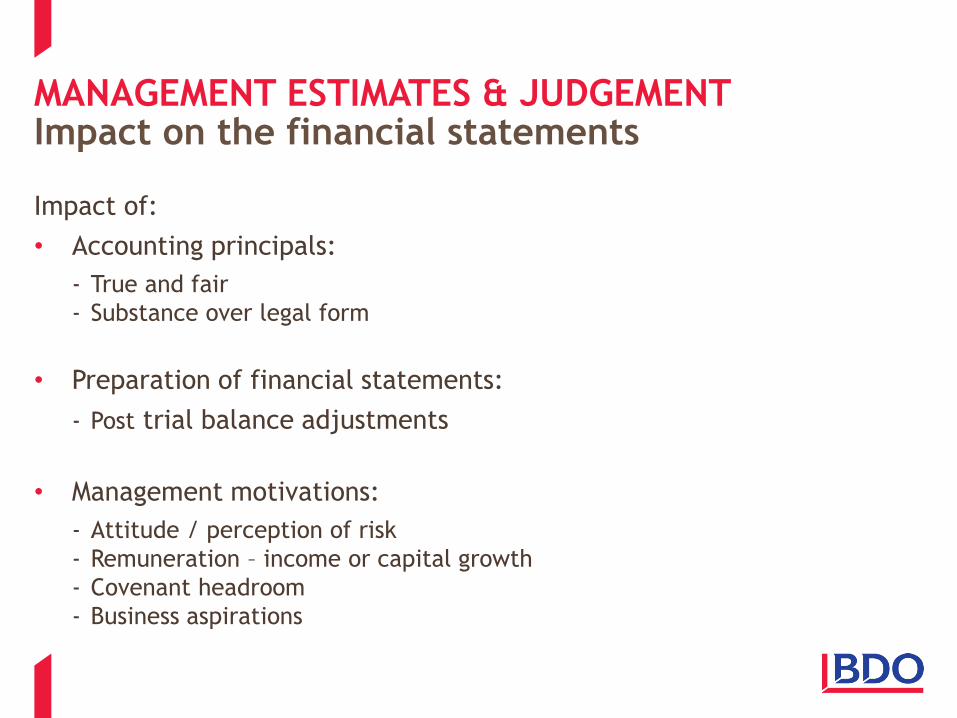

MANAGEMENT ESTIMATES & JUDGEMENT

Impact of:

• Accounting principals:

- True and fair

- Substance over legal form

• Preparation of financial statements:

- Post trial balance adjustments

• Management motivations:

- Attitude / perception of risk

- Remuneration – income or capital growth

- Covenant headroom

- Business aspirations

Impact on the financial statements

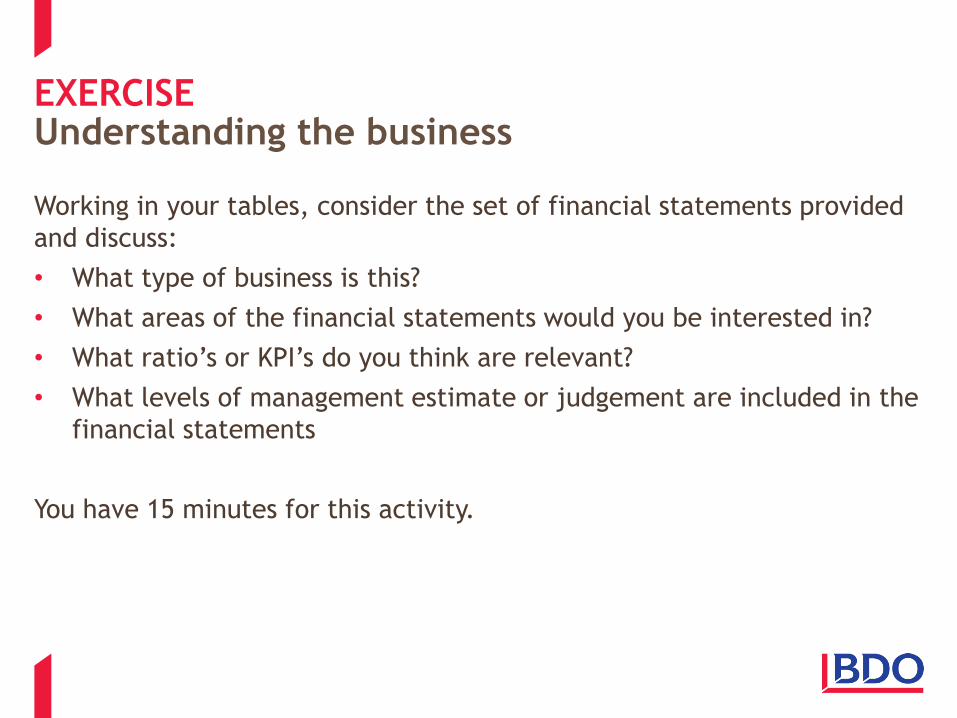

EXERCISE

Working in your tables, consider the set of financial statements provided

and discuss:

• What type of business is this?

• What areas of the financial statements would you be interested in?

• What ratio’s or KPI’s do you think are relevant?

• What levels of management estimate or judgement are included in the

financial statements

You have 15 minutes for this activity.

Understanding the business

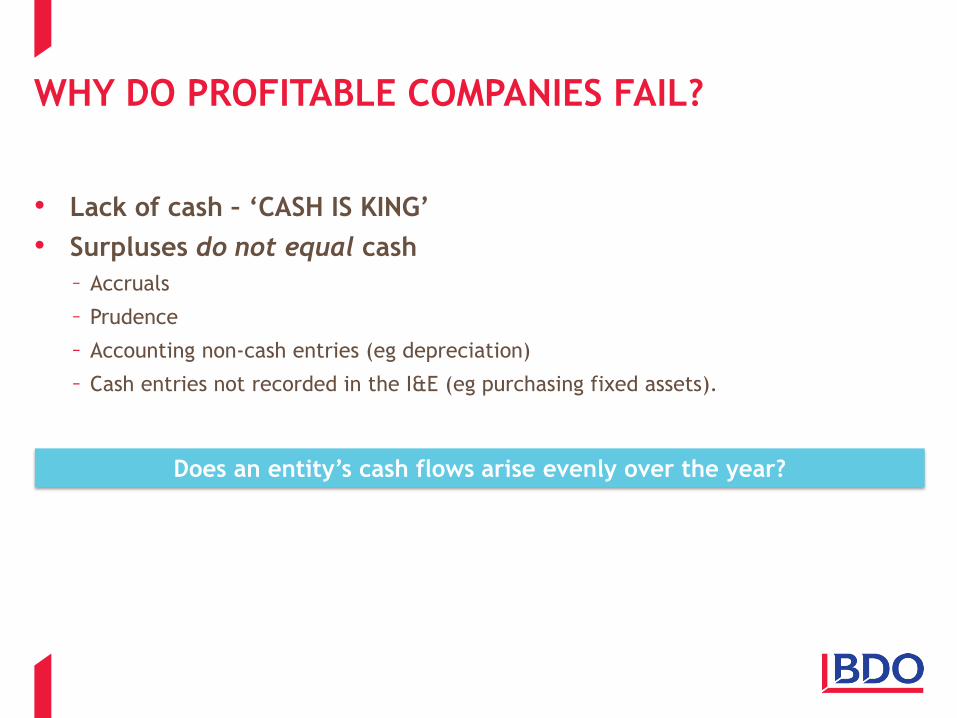

WHY DO PROFITABLE COMPANIES FAIL?

• Lack of cash – ‘CASH IS KING’

• Surpluses do not equal cash

– Accruals

– Prudence

– Accounting non-cash entries (eg depreciation)

– Cash entries not recorded in the I&E (eg purchasing fixed assets).

Does an entity’s cash flows arise evenly over the year?

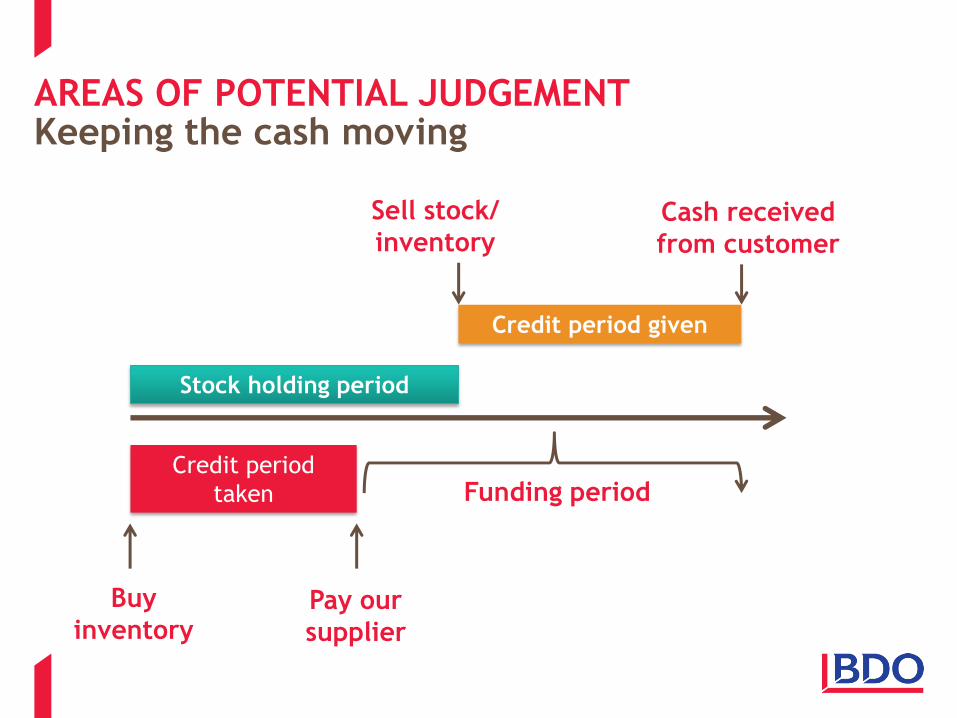

AREAS OF POTENTIAL JUDGEMENT Keeping the cash moving

Stock holding period

Credit period given

Credit period

taken

Buy

inventory Pay our

supplier

Sell stock/

inventory Cash received

from customer

Funding period

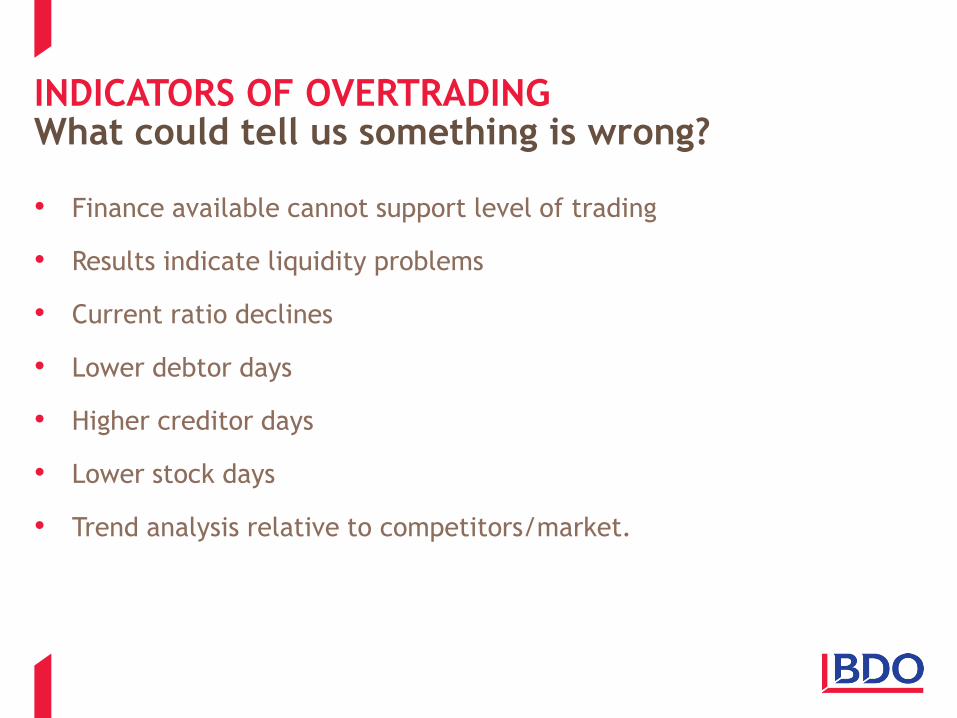

INDICATORS OF OVERTRADING

• Finance available cannot support level of trading

• Results indicate liquidity problems

• Current ratio declines

• Lower debtor days

• Higher creditor days

• Lower stock days

• Trend analysis relative to competitors/market.

What could tell us something is wrong?

ACCOUNTING PRINCIPLES FOR TRANSACTIONS

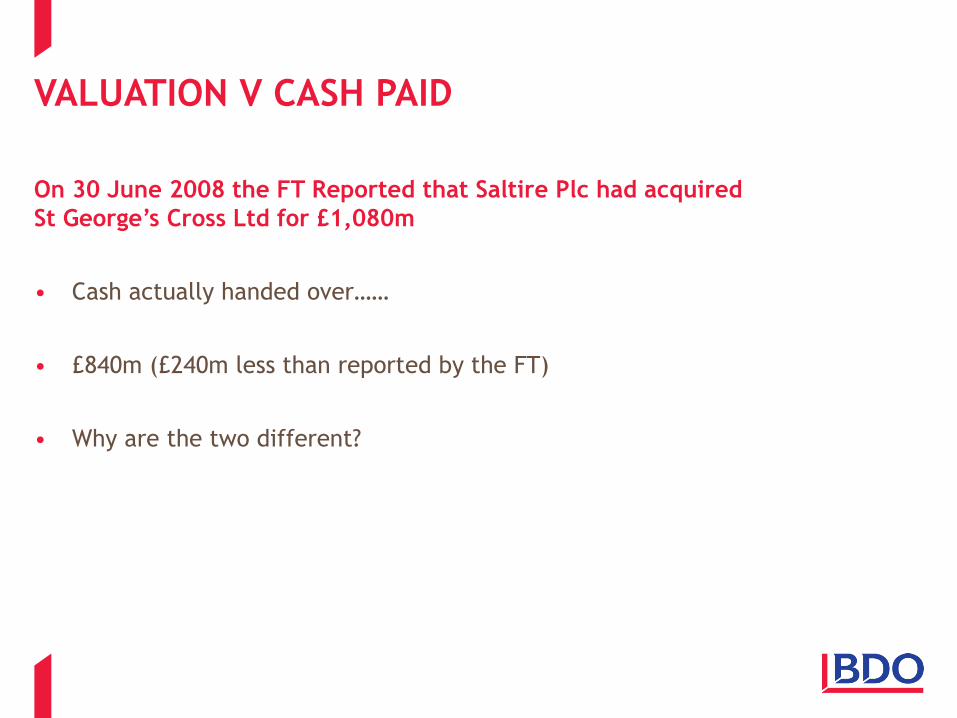

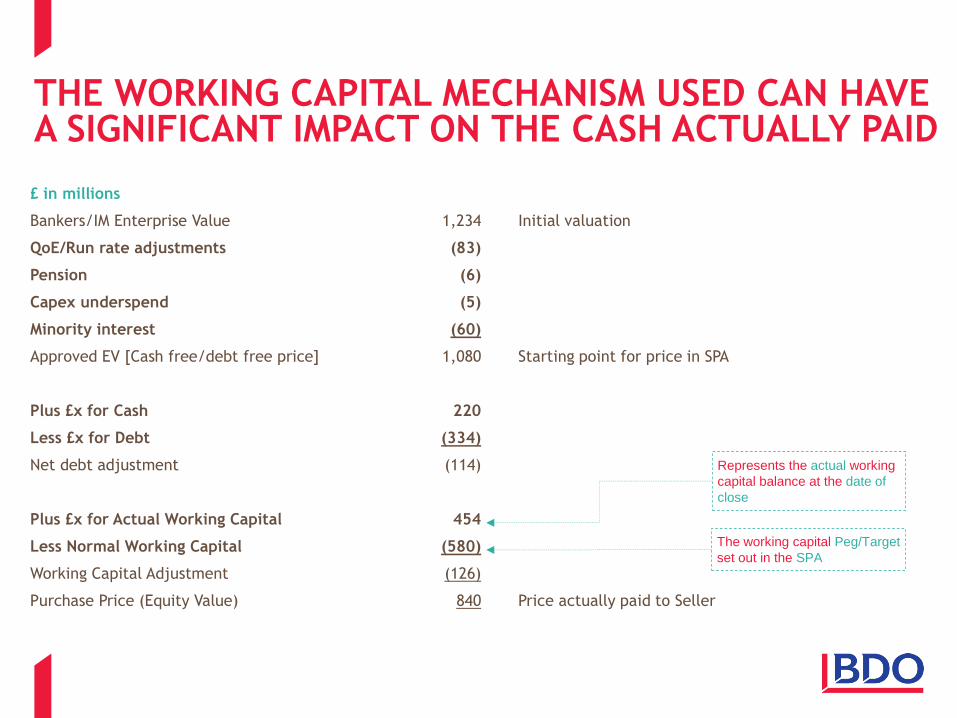

VALUATION V CASH PAID

On 30 June 2008 the FT Reported that Saltire Plc had acquired

St George’s Cross Ltd for £1,080m

• Cash actually handed over……

• £840m (£240m less than reported by the FT)

• Why are the two different?

THE WORKING CAPITAL MECHANISM USED CAN HAVE A SIGNIFICANT IMPACT ON THE CASH ACTUALLY PAID

£ in millions

Bankers/IM Enterprise Value 1,234 Initial valuation

QoE/Run rate adjustments (83)

Pension (6)

Capex underspend (5)

Minority interest (60)

Approved EV [Cash free/debt free price] 1,080 Starting point for price in SPA

Plus £x for Cash 220

Less £x for Debt (334)

Net debt adjustment (114)

Plus £x for Actual Working Capital 454

Less Normal Working Capital (580)

Working Capital Adjustment (126)

Purchase Price (Equity Value) 840 Price actually paid to Seller

Represents the actual working

capital balance at the date of

close

The working capital Peg/Target

set out in the SPA

WE THEREFORE NEED ADJUSTMENTS IN THE SPA TO HELP US……

Get from Enterprise value to Equity value

• ‘Headline’ price to actual value extracted by shareholders.

Balance sheet adjustments to P&L valuation

• Cash free debt free basis.

Normalising working capital, stopping manipulation

• Relevant to both buy and sell side.

Direct and potentially significant effect on value realised / price paid

• Guideline treatments are starting point for negotiations.

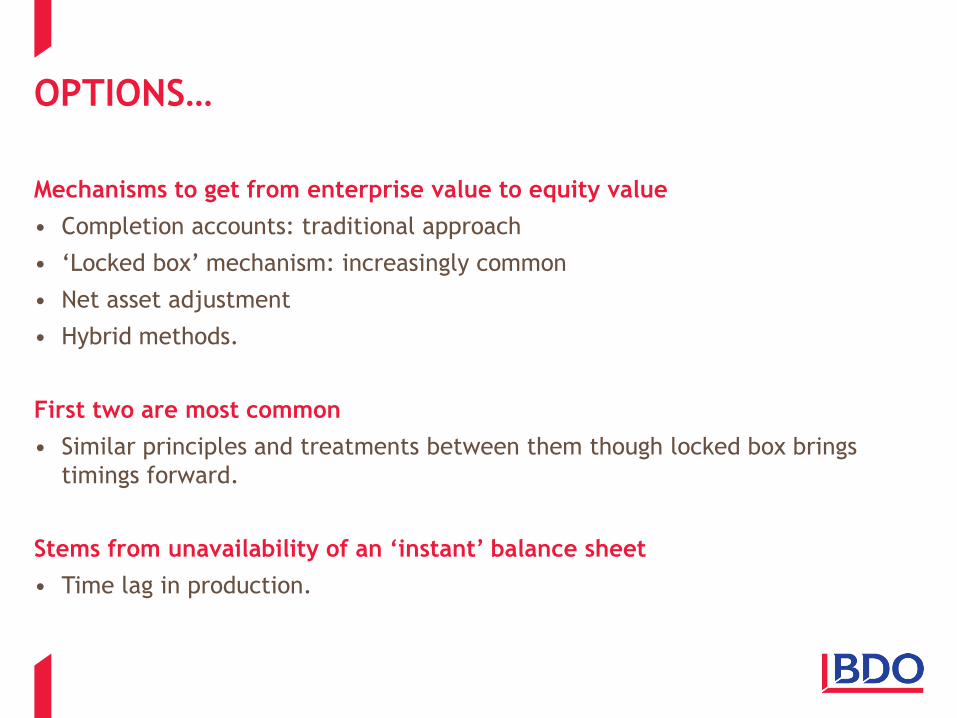

COMPLETION METHODOLOGIES AVAILABLE

OPTIONS…

Mechanisms to get from enterprise value to equity value

• Completion accounts: traditional approach

• ‘Locked box’ mechanism: increasingly common

• Net asset adjustment

• Hybrid methods.

First two are most common

• Similar principles and treatments between them though locked box brings

timings forward.

Stems from unavailability of an ‘instant’ balance sheet

• Time lag in production.

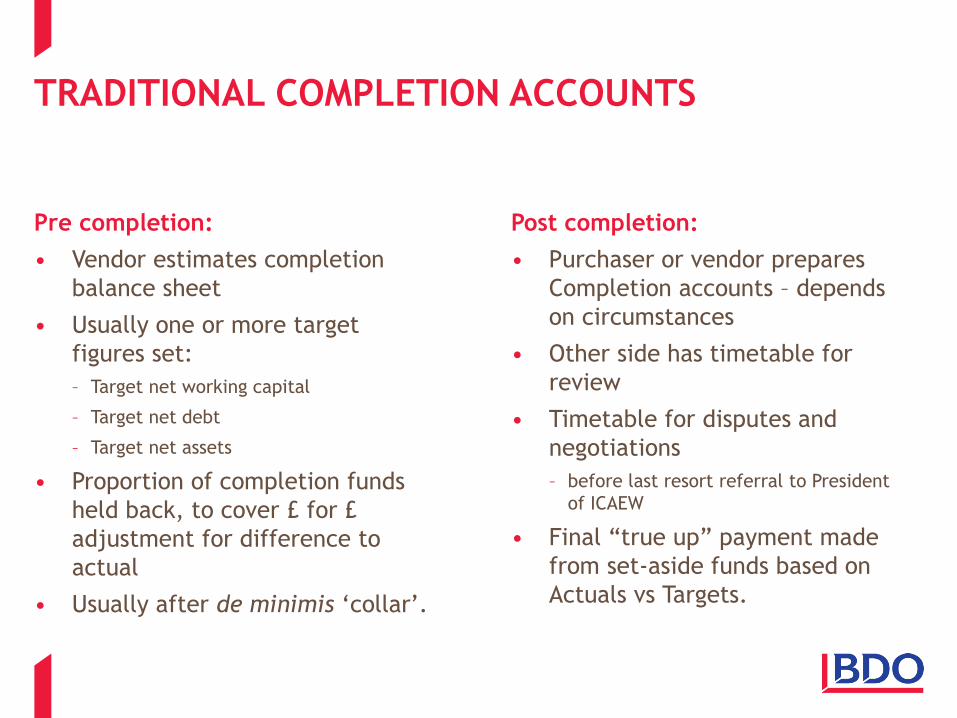

TRADITIONAL COMPLETION ACCOUNTS

Pre completion:

• Vendor estimates completion

balance sheet

• Usually one or more target

figures set:

– Target net working capital

– Target net debt

– Target net assets

• Proportion of completion funds

held back, to cover £ for £

adjustment for difference to

actual

• Usually after de minimis ‘collar’.

Post completion:

• Purchaser or vendor prepares

Completion accounts – depends

on circumstances

• Other side has timetable for

review

• Timetable for disputes and

negotiations

– before last resort referral to President

of ICAEW

• Final “true up” payment made

from set-aside funds based on

Actuals vs Targets.

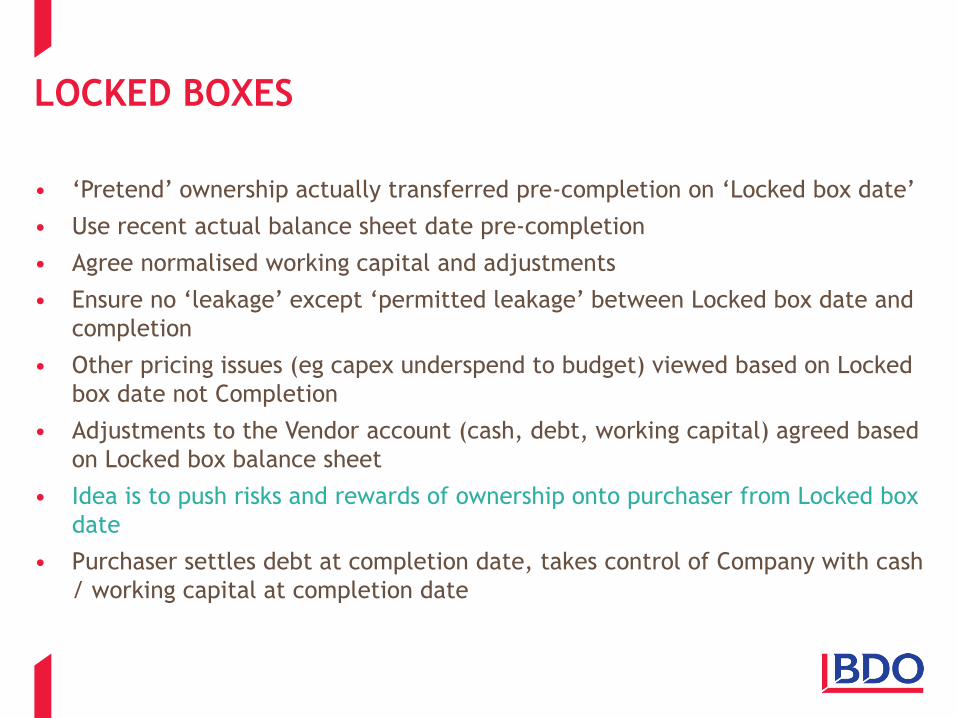

LOCKED BOXES

• ‘Pretend’ ownership actually transferred pre-completion on ‘Locked box date’

• Use recent actual balance sheet date pre-completion

• Agree normalised working capital and adjustments

• Ensure no ‘leakage’ except ‘permitted leakage’ between Locked box date and

completion

• Other pricing issues (eg capex underspend to budget) viewed based on Locked

box date not Completion

• Adjustments to the Vendor account (cash, debt, working capital) agreed based

on Locked box balance sheet

• Idea is to push risks and rewards of ownership onto purchaser from Locked box

date

• Purchaser settles debt at completion date, takes control of Company with cash

/ working capital at completion date

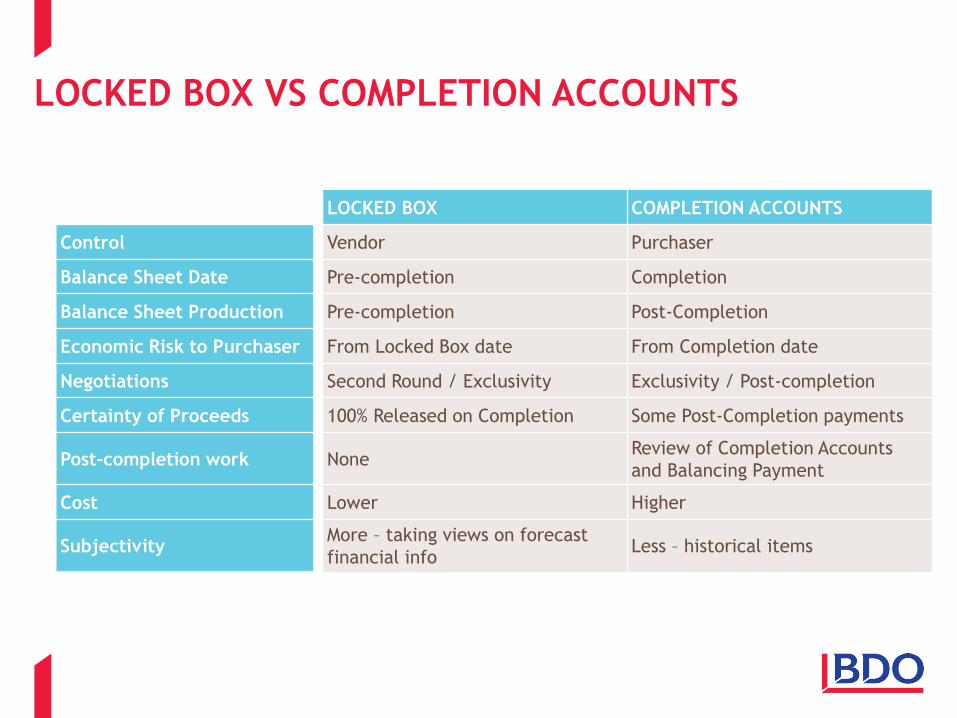

LOCKED BOX VS COMPLETION ACCOUNTS

LOCKED BOX COMPLETION ACCOUNTS

Control Vendor Purchaser

Balance Sheet Date Pre-completion Completion

Balance Sheet Production Pre-completion Post-Completion

Economic Risk to Purchaser From Locked Box date From Completion date

Negotiations Second Round / Exclusivity Exclusivity / Post-completion

Certainty of Proceeds 100% Released on Completion Some Post-Completion payments

Post-completion work None Review of Completion Accounts

and Balancing Payment

Cost Lower Higher

Subjectivity More – taking views on forecast

financial info Less – historical items

LOCKED BOX: PRO’S & CON’S

• Locked Box mechanics perceived to favour Vendors

• In reality simpler and cheaper to produce

• Sustainability in bear market?

Vendor Purchaser

Pro

s

• Control over process

• Maintain competitive tension

• Simplicity

• Cost savings

• Transfer risk pre-completion

• Simplicity

• Cost savings

• Certainty

Cons

• PE house using LB as Vendor will have difficulty

avoiding it as Purchaser

• Used aggressively can alienate potential

purchasers

• Loss of trading upside

• Lose “chip” potential of completion accounts

and exclusive negotiations

• Information disadvantage, need DD and access

to management

• Extra business risk pre-completion

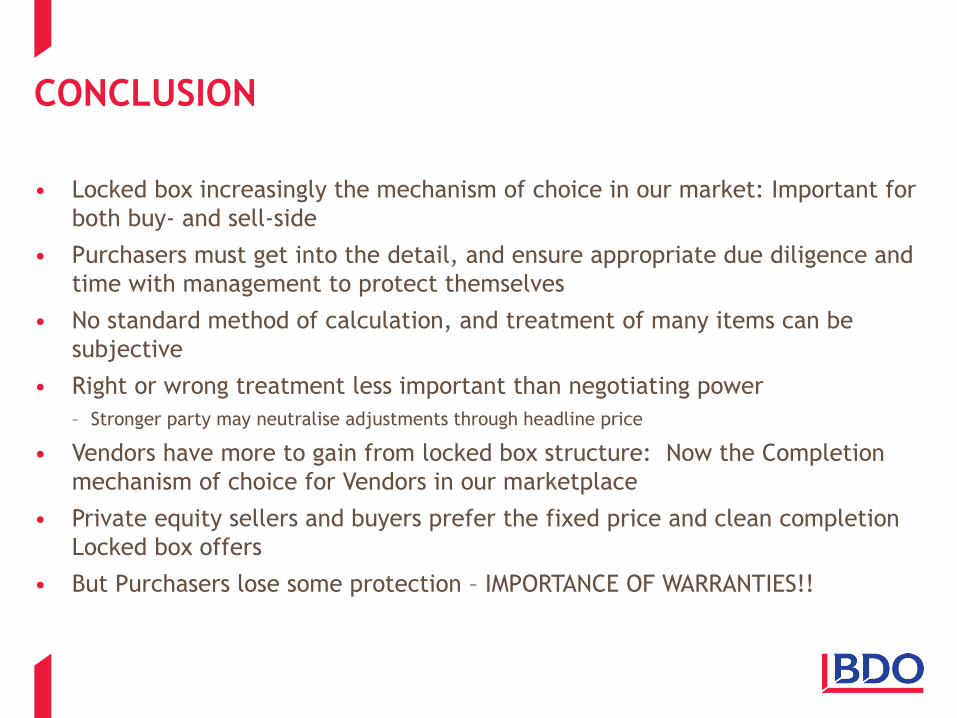

CONCLUSION

• Locked box increasingly the mechanism of choice in our market: Important for

both buy- and sell-side

• Purchasers must get into the detail, and ensure appropriate due diligence and

time with management to protect themselves

• No standard method of calculation, and treatment of many items can be

subjective

• Right or wrong treatment less important than negotiating power

– Stronger party may neutralise adjustments through headline price

• Vendors have more to gain from locked box structure: Now the Completion

mechanism of choice for Vendors in our marketplace

• Private equity sellers and buyers prefer the fixed price and clean completion

Locked box offers

• But Purchasers lose some protection – IMPORTANCE OF WARRANTIES!!

FINANCE FOR LAWYERS EVENT

WHAT DOES THE FUTURE HOLD?

THE SHAPE OF THINGS TO COME…

• Audit report formats

• Directors’ reports

• Changes to accounting standards (FRS 102, Accounting for leases).

What will be different?