Embed Size (px)

Citation preview

Financial Markets During and After COVID 19

Part Two

State of Play in April

• Uncertainty was coming down:– Policy response will avert a great depression and a financial crisis– Lockdowns are getting the virus under control– Thinking has moved onto how economies will restart

• The Oil Price War had been resolved with a deal between the Opec and non-Opec countries.

• The shape of the recovery remained unknown. But a U shape seemed likely due to Fiscal support

• Market was pricing in a deflationary future as Bonds and Growth stocks were seeing inflows.

• Behaviour post the crises remains unknown:– It is expected that savings rates will stay high for a period – Fiscal Policy will have to step in

to ensure the recovery and is maintained.

2

State of Play Today• Uncertainty has continued to decrease

• Economies have restarted: World has moved from lockdown to living with virus.

• Fiscal and monetary policy has been greater than many expected

• The economic recovery has been stronger than many expected.

• Oil prices have been continuing their recovery

• Equity markets have been recovering

• Markets are starting to think about inflation and longer term consequences of policy action.

• Permanent changes to consumer behaviour are still unknown

3

The Big Questions

➢What is happening in the economy and markets at the moment?

➢What are the long term ramifications for economies from the Coronavirus

➢What are the long term ramifications for markets from the Coronavirus

➢Is the bull market of the last decade over? We think it is and the bull markets of the next decade will be different.

4

Economies Have Restarted

5

Back Spending Money But Not GOING to Work

Source: Wilmot, Opportunity insights 5th August 2020

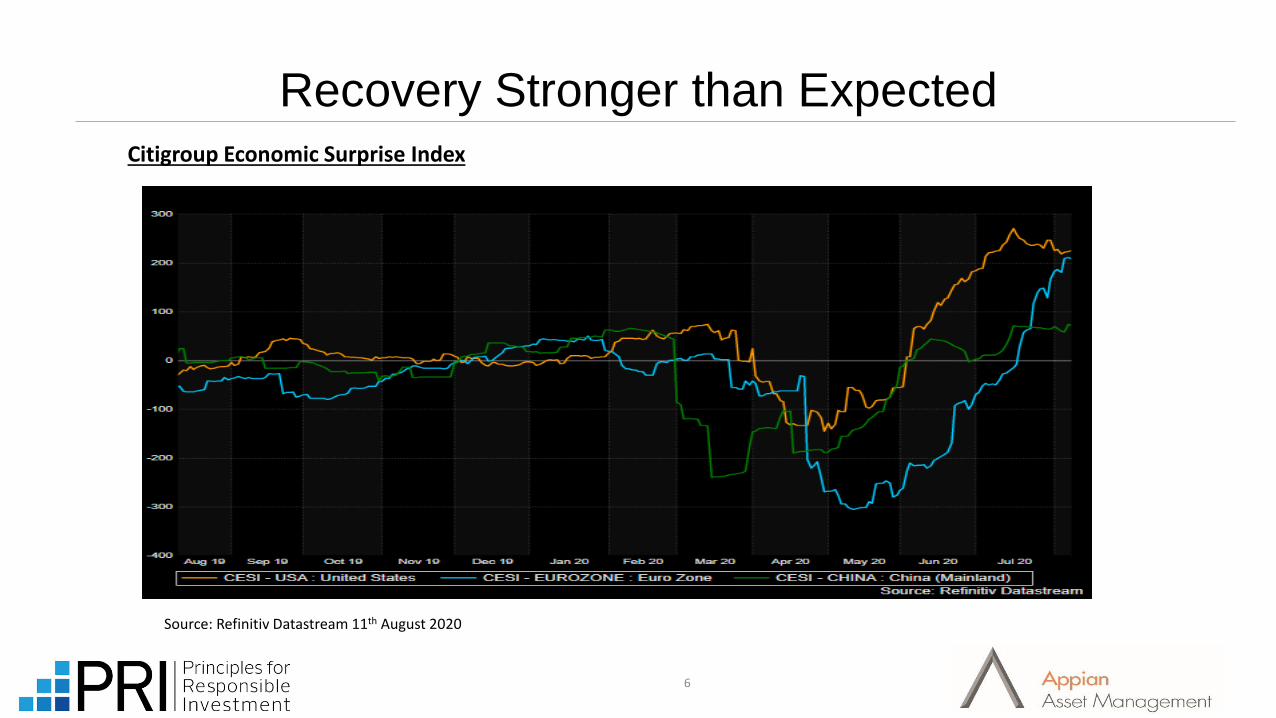

Recovery Stronger than Expected

6

Citigroup Economic Surprise Index

Source: Refinitiv Datastream 11th August 2020

Fiscal and Monetary Policy Support

Central Banks are Supporting

7

Governments are Spending

Source: Refinitiv Datastream 10th August 2020Source: Macrostrategy 2nd August 2020

It’s a Global Response: Everyone is on Board

8

Source: IMF 1st August 2020

Big Shocks Can Change Markets for Decades

• Global Financial Crisis • Post Pandemic

9

▪ Austerity

▪ Money Supply didn’t reach main street

▪ Asset bubbles favoured Wall Street over the main street

▪ Low Inflation

▪ US Dominance

• Austerity is Dead

• Focus is on getting money to main street

• Different assets will work for the next decade

• Inflation is being encouraged

• US Dominance is under threat

The Pandemics Lasting Legacy?

10

• Rising inflation expectations have sent US Real Rates Negative:

Source: Refinitiv Datastream 11th August 2020

The Bond Market is Still Under Attack

11

➢ Negative Real Rates Doesn’t mean Rates Cant go Up:

Source: Exane BNP Paribas April 2020

The Big Difference from the GFC is Who Pays

12

Paying for the GFC Paying for the Pandemic

What this Means for Financial Markets

13

There is Such thing as Flat Earthers

14

➢ If your interested, they have an annual conference in Birmingham

No Surprise to see Equity Markets Recovering

• The conditions were in place for a recovery.

➢Monetary and Fiscal Policy was being put in place to restore economic growth.

➢ After falling 35%, Equity Markets were pricing in a lost decade, not a lost year

➢The question was then timing/speed of a recovery and what would lead the recovery?

15

Not Everything has Recovered Equally

16

Word Technology index and World ex US equity Index

Source: Refinitiv Datastream 9th August 2020

Market Psychology Today

• Bonds becoming not investible due to low rates

• Uncertainty over the economy

17

• Technology stocks are safe like bonds as even when things are bad we need technology

• Technology stocks benefit if the economy improves or if the economy gets worse and we all stay at home

➢ Lets All Buy more Amazon, Google, Apple, Microsoft and Facebook

The Elephant in the Room Hasn’t Gone Away

18

Source: Bank of America 26th July 2020

19

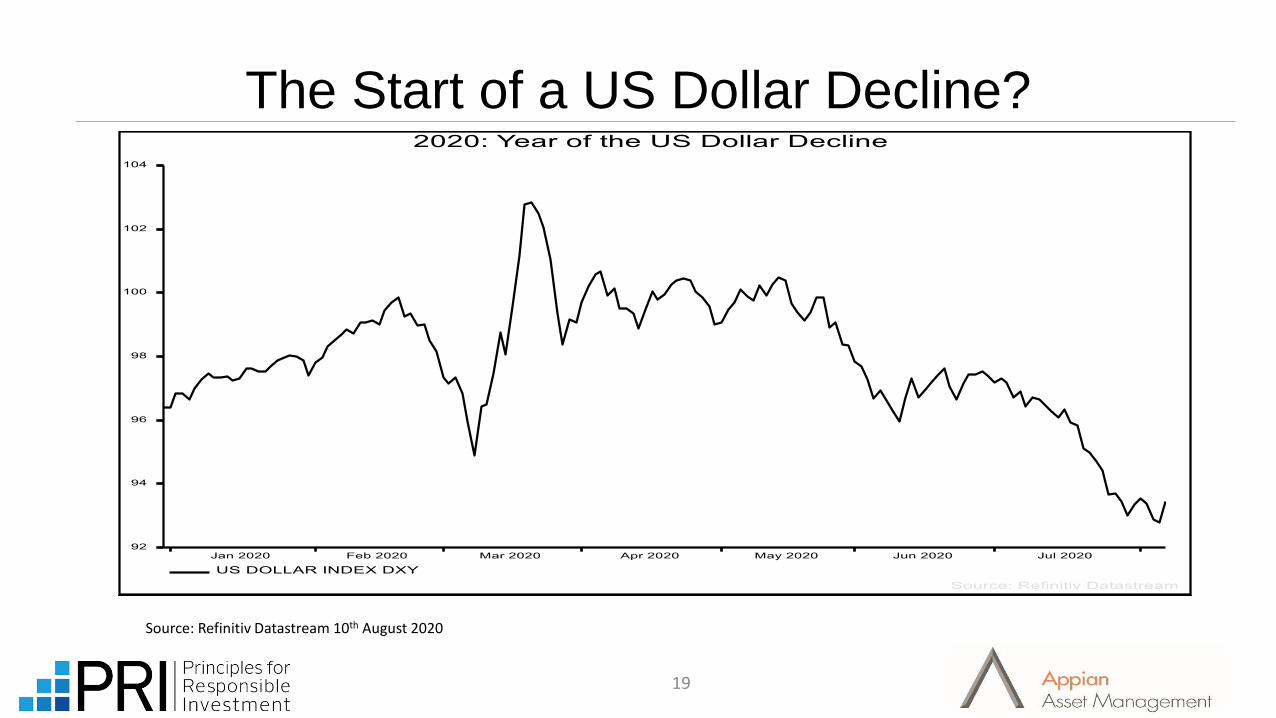

The Start of a US Dollar Decline?

Source: Refinitiv Datastream 10th August 2020

20

Source: Refinitiv Datastream 11th August 2020

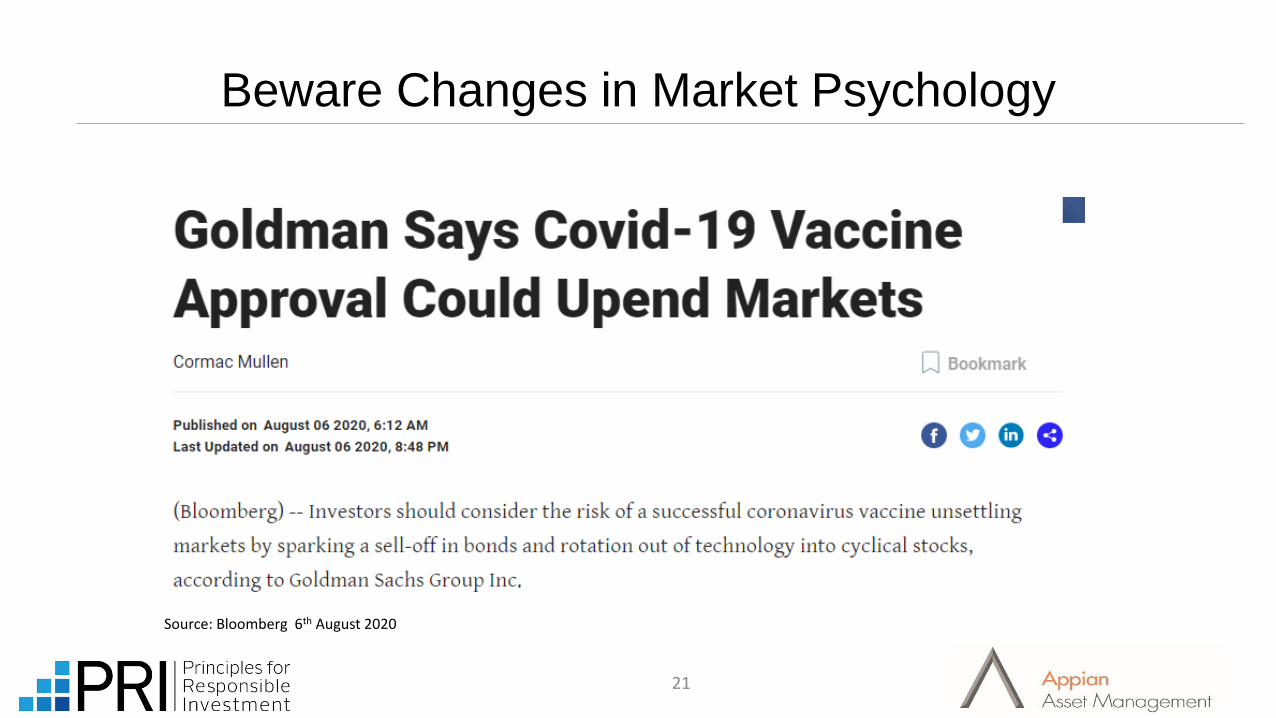

Beware Changes in Market Psychology

21

Source: Bloomberg 6th August 2020

The Virus Impacted Markets so will the Vaccines

22

Source: Mckinsey 29th July 2020

The Battle within the Market

Deflationary Shock Versus Inflationary Response

23

The Bull Markets of the Last Decade May be Over:

24

Deflation Assets:

❑ Government Bonds❑ US Investment Grade❑ US High Yield❑ S+P 500❑ US Growth Stocks❑ US Consumer Discretionary

Stocks

Inflation Assets:

❑ Commodities❑ Real Estate❑ TIPS❑ Equities in World ex US❑ US Banks❑ Value❑ CashNew Ones will Emerge

Source: Bank of America 13th May 2020

Global Equities Have not Been in a Bull Market

• The money has flowed into the United States, Particularly Technology

25

Source: Refinitiv Datastream 11th August 2020

World Technology Price and World ex US Market

Equities Outside the US Continue to Offer Value

26

World ex US Market Price Index and World ex US Book Value

Source: Refinitiv Datastream 11th August 2020

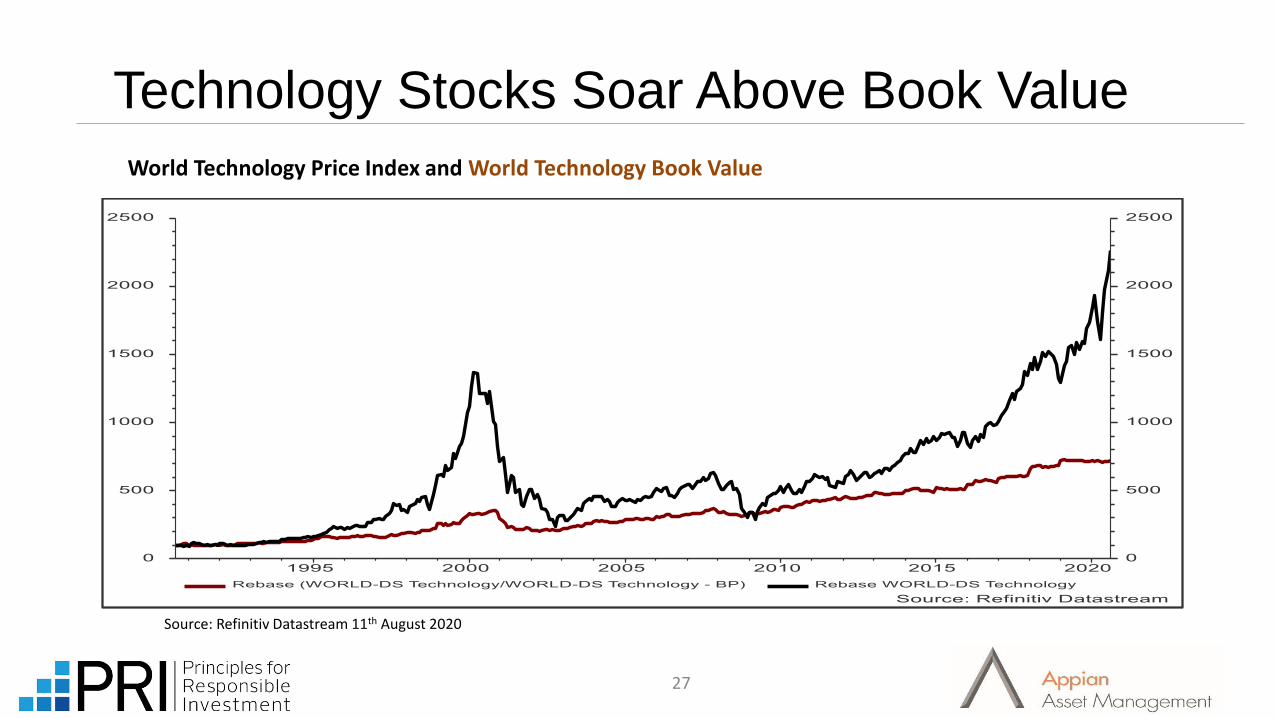

Technology Stocks Soar Above Book Value

27

Source: Refinitiv Datastream 11th August 2020

World Technology Price Index and World Technology Book Value

Asset Class Implications of a Negative Yield World

• Cash:

➢ Guaranteed to Lose Purchasing Power

• Bonds:

➢ Guaranteed to Lose Purchasing Power and Also nominal value if inflation pushes yields higher➢ Inflation Protected Bonds may offer protection

• Equities:

➢ Can Protect Against inflation but not all are equal➢ Equities with high fixed costs and the ability to get revenue increases are the real beneficiaries:

• Alternatives

➢ Commodities- Can be stores of value➢ Property – Can grow rental income➢ Infrastructure - If inflation protected

28

Short term: Fear Continues to Dominate

29

Source: Evercore 7th August 2020 Source: Bloomberg ICI 28th July 2020

Are investors looking far enough into the Future?

30

Risks

• Short Term Risks:

➢ Policy Support is withdrawn bringing down asset prices

➢ A vaccine takes longer than expected

➢ Political instability in the developed world.

• Long Term Risks:

➢ Not Being invested as inflation WILL destroy savings

➢ Being invested in the wrong assets

➢ Stagflation

➢ Reversal of Globalisation

31

What it Means for Multi Asset Fund Investing

32

Running into Deflationary Assets Like Bonds and the US Dollar is tempting but doesn’t make sense.

Equities represent a hedge against inflation providing you own the right ones.

Real Assets such as Forestry, Gold, Infrastructure and Property will gain in importance post the crisis.

Cash can be used to avail of Opportunities in the Equity market or elsewhere

Appian Asset Management

33

• Polite Notice Re GDPR Requirements

• By attending this presentation we are assuming your

permission for Appian to contact you in the future. If you

would rather not please let us know on the contact

details provided

Appian Asset Management-Sales/Distribution Contacts

34

[email protected]+353 (1) [email protected]+353 (1) [email protected]+353 (1) [email protected]+353 (1) [email protected]+353 87 180 6784

Disclaimer

Please note that any target return noted in this material is not guaranteed.

The Appian Multi-Asset Fund, Appian Impact Fund, Appian Global Dividend Growth Fund, Appian Global Small Companies Fund and the Appian Euro Liquidity Fund are Retail

Investment Alternative Investment Funds and are sub-funds of the Appian Unit Trust.

The Appian Burlington Property Fund is a limited Liquidity fund and is only open to Qualifying Investors. A minimum investment threshold of €100,000 applies. Redemptions are at the

discretion of the directors and minimum investment term prior to any redemption request being considered is two years from investment.

Further information in relation to all risks for each fund is provided in the relevant Fund Prospectus and supplements available on request.

The information contained in this material is not financial advice. Nor does it constitute an offer for the purchase or sale of any financial instruments, trading strategy, product or service.

No one receiving this material should treat any of its contents as constituting advice. It does not take into account the investment objectives, knowledge, experience or financial situation

of any particular person. You should seek advice in the context of your own personal circumstances prior to investing or taking out any product from your own independent adviser.

This material has been prepared and issued by Appian Asset Management Limited on the basis of publicly available information, internally developed data and other sources believed to

be reliable. While all reasonable care has been given to the preparation of the information, no warranties or representation, express or implied are given or liability accepted by Appian

Asset Management Limited or its affiliates or any directors or employees in relation to the accuracy, fairness or completeness of the information contained herein. Any opinion expressed

(including estimates and forecasts) may be subject to change without notice.

The above disclaimer and limitations of liability are applicable to the fullest extent permitted by law, whether in Contract, Statute, Tort (including without limitation, negligence) or

otherwise.

Appian Asset Management Limited is regulated by the Central Bank of Ireland.

35

Warning• If you invest in any of the funds you may lose some or all of the money you invest• Past performance is not a reliable guide to future performance• Appian Funds may be affected by changes in currency exchange rates• The value of your investment may go down as well as up