Embed Size (px)

DESCRIPTION

CA Final Paper

Citation preview

Financial Reporting for Financial InstitutionsMUTUAL FUNDS & NBFC’s

Financial Reporting for Financial InstitutionsMUTUAL FUNDS & NBFC’s

Question1

»What do you mean by “Net asset value” (NAV) in case of mutual fund units?

2

Answer

»The net asset value (NAV) of a mutual fund indicates the price at which the units of that mutual fund are bought or sold. It represents the fund's market value after subtracting the liabilities. The NAV per unit is derived after dividing the net asset value of the fund by the total number of its outstanding units.

»The formula for calculating NAV:

3

Question 2» Investors Mutual Fund is registered with SEBI and having

its registered office at Pune. The fund is in the process of finalizing the annual statement of accounts of one of its open ended mutual fund schemes. From the information furnished below you are required to prepare a statement showing the movement of unit holders’ funds for the financial year ended 31st March, 2015.

4

Particulars Rs’000

Opening Balance of net assets 12,00,000

Net Income for the year (Audited) 85,000

8,50,200 units issued during 2014-15 96,500

7,52,300 units redeemed during 2014-15The par value per unit is Rs. 100

71,320

Working Note:

Particulars Issued Redeemed

Units

Par value Sale proceeds/Redemption valueProfit transferred to Reserve /Equalisation FundBalance in Reserve/Equalisation Fund (Issued & Redeemed)

8,50,200Rs.’ 000

85,02096,50011,480

7,52,300 Rs ‘000

75,23071,320

3,910

15,390

5

When in the case of an open-ended scheme units are sold, the difference between the sale price and the face value of the unit, if positive, should be credited to reserves and if negative be debited to reserves, the face value being credited to Capital Account. Similarly, when in respect of such a scheme, units are repurchased, the difference between the purchase price and face value of the unit, if positive should be debited to reserves and, if negative, should be credited to reserves, the face value being debited to the capital account.

Statement showing the Movement of Unit Holders’ Fundsfor the year ended 31st March 2015

Particulars (Rs. ’000)

Opening balance of net assets Add: Par value of units issued (8,50,200 × Rs. 100) Net Income for the year Transfer from Reserve/Equalisation fund (Refer working note)

Less: Par value of units redeemed (7,52,300 × Rs. 100)

Closing balance of net assets (as on 31st March, 2015)

12,00,00085,02085,000

15,390

13,85,410

(75,230)

13,10,180

6

Question 3

»On 1.4.2014, a mutual fund scheme had 18 lakh units of face value of Rs. 10 each was outstanding. The scheme earned Rs. 162 lakhs in 2014-15, out of which Rs. 90 lakhs was earned in the first half of the year. On 30.9.2014, 2 lakh units were sold at a “NAV” of Rs. 70.

»Pass Journal entries for sale of units and distribution of dividend at the end of 2014-15.

7

SolutionAllocation of Earnings Old UnitHolders

New Unit

Holders

Total

[18 lakhsunits]

[2 lakhsunits]Rs. in lakhs

Rs. in lakhs

First half year (Rs. 5 per unit) 90.00 90

Second half year (Rs. 3.60 per unit) 64.80 7.20 72

Earning 2014-15 154.80 7.20 162

Add: Equalization payment recovered 10

Total available for distribution 172

Equalization Payment:-Rs. 90 lakhs ÷ 18 lakhs = Rs. 5 per unit.In the case of an open-ended scheme, when units are sold and appropriate part of the sale proceeds should be credited to an Equalisation Account and when units are repurchased an appropriate amount should be debited to Equalisation Account

8

SolutionParticulars Old Unit

HoldersNew Unit

Holders

Dividend distributed8.60 8.60

Less: Equalization payment (5.00)

8.60 3.60

9

The net balance on this account should be credited or debited to the Revenue Account. The balance on the Equalisation Account debited or credited to the Revenue Account should not decrease or increase the net income of the fund but is only an adjustment to the distributable surplus. It should, therefore, be reflected in the Revenue Account only after the net income of the fund is determined

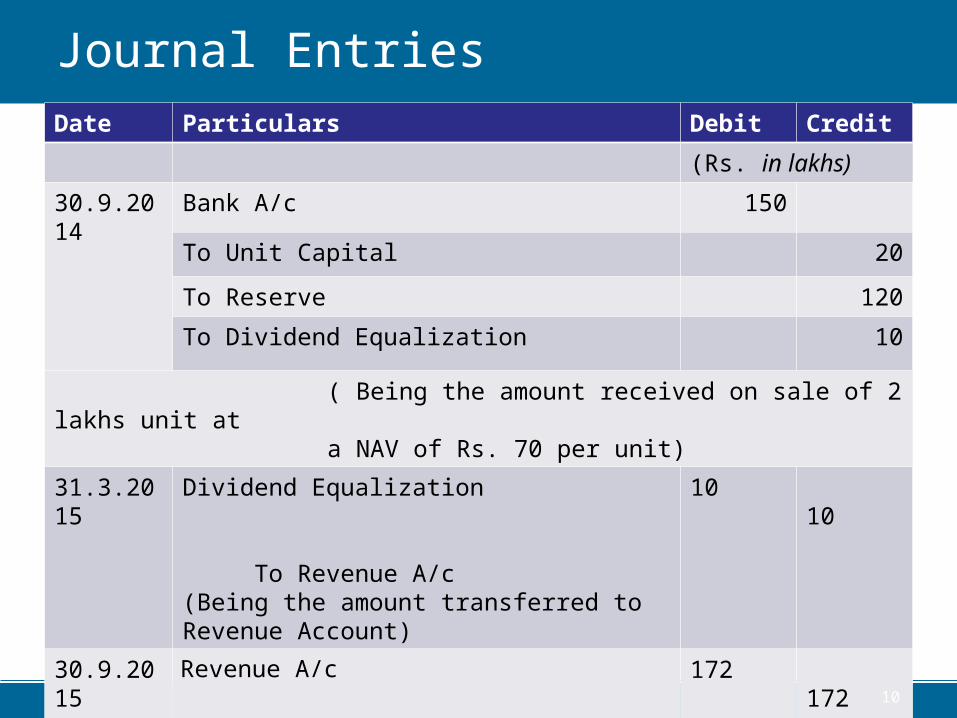

Journal EntriesDate Particulars Debit Credit

(Rs. in lakhs)

30.9.2014 Bank A/c 150

To Unit Capital 20

To Reserve 120

To Dividend Equalization 10

( Being the amount received on sale of 2 lakhs unit at a NAV of Rs. 70 per unit)

31.3.2015 Dividend Equalization To Revenue A/c(Being the amount transferred to Revenue Account)

1010

30.9.2015 Revenue A/c To Bank(Being the amount distributed among 20 lakhs unit holders @ Rs. 8.60 per unit)

172172

10

Question 4

»A Mutual Fund raised 100 lakh on April 1, 2015 by issue of 10 lakh units of Rs. 10 per unit. The fund invested in several capital market instruments to build a portfolio of Rs. 90 lakhs. The initial expenses amounted to Rs. 7 lakh. During April, 2015, the fund sold certain securities of cost Rs. 38 lakhs for Rs. 40 lakhs and purchased certain other securities for Rs. 28.20 lakhs. The fund management expenses for the month amounted to Rs. 4.50 lakhs of which Rs. 0.25 lakh was in arrears.

11

»The dividend earned was Rs. 1.20 lakhs. 75% of the realized earnings were distributed. The market value of the portfolio on 30.04.2015 was Rs. 101.90 lakh.

»Determine NAV per unit.

12

AnswerParticulars Rs. in lakhs Rs. in lakhs Rs. in lakhs

Opening bank balance [Rs. (100- 90-7) lakhs]Add: Proceeds from sale of securities Dividend received

Less: Cost of securities Fund management expenses [ Rs. (4.50–0.25) lakhs] Capital gains distributed [ 75% of Rs. (40.00 – 38.00) lakhs] Dividends distributed (75% of Rs. 1.20lakhs)Closing bank balance Closing market value of portfolio

Less: Arrears of expenses Closing net assets Number of units ( in Lakhs)Closing Net Assets Value (NAV)

3.0040.001.20

28.20

4.25

1.500.90

44.20

(34.85)9.35

101.90111.25

(0.25)111.00

1011.10

13

Question 5

»Ramesh Goyal has invested in three mutual funds. From the details given below, find out effective yield on per annum basis in respect of each of the schemes to Ramesh Goyal upto 31-03-2015.

14

Mutual Fund X Y Z

Date of Investment Amount of investment (Rs.)NAV at the date of investment (Rs.)Dividend received upto 31-3-2015 (Rs.)NAV as on 31-3-2015 (Rs.)

1-12-2014

1,00,000

10.50

1,900

10.40

1-1-2015

2,00,000

10.00

3,000

10.10

1-3-2015

1,00,000

10.00

Nil

9.80

Calculation of effective yield on per annum basis in respect of three mutual fund schemes of Ramesh Goyal upto 31.03.2015

S.No Particulars X Y Z

1 Amount of Investment (Rs.) 1,00,000 2,00,000 1,00,000

2 Date of investment 1.12.2014 1.1.2015 1.3.2015

3 NAV at the date of investment (Rs.)

10.50 10.00 10.00

4 No. of units on date of investment [1/3]

9,523.809 20,000 10,000

5 NAV per unit on 31.03.2015 (Rs.)

10.40 10.10 9.80

6 Total NAV of mutual fund investments on31.03.2015 [4 x 5]

99,047.61 2,02,000 98,000

15

Calculation of effective yield on per annum basis in respect of three mutual fund schemes of Ramesh Goyal upto 31.03.2015

X Y Z

7 Increase/ decrease of NAV [6-1]

(952.39) 2,000 (2,000)

8 Dividend received upto 31.3.2015

1,900 3,000 Nil

9 Total yield [7+8] 947.61 5,000 (2,000)

10 Yield % [9/1] x 100 0.95% 2.5% (2%)

11 Number of days 121 90 31

12 Effective yield p.a. [10/11] x 365 days

2.87% 10.14% (23.55%)

16

Question 6

»The investment portfolio of a mutual fund scheme includes 5,000 shares of X Ltd. and 4,000 shares of Y Ltd. acquired on 31-12-2013. The cost of X Ltd.’s shares is Rs. 40 while that of Y Ltd.’s shares is Rs. 60. The market value of these shares at the end of 2013-14 were Rs. 38 and Rs. 64 respectively. On 30-06-2014, shares of both the companies were disposed off realizing Rs. 37 per X Ltd. shares and Rs. 67 per Y Ltd. shares. Show important accounting entries in the books of the fund for the accounting years 2013-14 and 2014-15.

17

Solution

Date Particulars Debit Rs. Credit Rs.

31.12.2013 Investment in X Ltd.’s shares A/c (5,000 x Rs. 40) Dr. Investment in Y Ltd.’s shares A/c (4,000 x Rs. 60) Dr. To Bank A/c 4,40,000(Being investment made in X Ltd. and Y Ltd.)

2 ,00,000

2,40,0004,40,000

31.3.2014 Revenue A/c [5,000 x Rs. (40-38)] . Dr. To Provision for Depreciation A/c (Being provision created for the reduction in the valueof X Ltd.’s shares)

10,00010,000

18

Date Particulars Debit Rs. Credit Rs.

31.3.2014 Investment in Y Ltd.’s shares A/c

Dr. [4,000 x Rs. (64-60)]To Unrealised Appreciation Reserve A/c (Being appreciation in the market value of Y Ltd.’sshares transferred to Unrealised Appreciation Reserve A/c)

16,000

16,000

01.04.2014 Unrealised Appreciation Reserve A/c Dr. To Investment in Y Ltd.’s shares A/c (Being last year’s unrealised appreciation reservebalance reversed at the beginning of the current year)

16,000

16,000

19

Date Particulars Debit Rs. Credit Rs.30.6.2014 Bank A/c (5,000 x Rs. 37)

Dr. Loss on disposal of Investment A/c Dr. To Investment in X Ltd.’s shares A/c ( 5,000 x Rs. 40)(Being shares of X Ltd. disposed off at a loss ofRs. 15,000)

1,85,000

15,000

2,00,000

30.6.2014 Provision for Depreciation A/c Dr.Revenue A/c Dr. To Loss on disposal of Investment A/c 15,000(Being net loss on disposal of X Ltd.’s shares chargedto revenue account)

10,000

5,000

15,000

20

Date Particulars Debit Rs. Credit Rs.30.6.2014 Bank A/c (4,000 x Rs. 67)

Dr. To Investment in Y Ltd.’s shares A/c (4,000 x Rs. 60) To Revenue A/c (Being shares of Y Ltd. disposed off at a profit ofRs. 28,000)

2,68,000

2,40,000

28,000

21

Question 7

» A Mutual Fund Co has the following assets under it on the close of business as on

Total value of Units 6,00,000

1. Calculate NAV of the Fund

2. Following information is given : Assuming Mr A submits a cheque of Rs 30,00,000 to the mutual fund and the fund manager of this company purchases 8000 shares of M ltd and the balance is held in bank . In such case what would be the position of fund

3. Find the new NAV as 2nd feb 2015

22

Company No of shares 1st February , 2015 Market price per share

2ndFebruary , 2015 Market price per share

L Ltd 20,000 20 20.50

M Ltd 30,000 312.4 360

N Ltd 20,000 361.2 383.10

P Ltd 60,000 505.10 503.90

SOLUTION

COMPANY 1st February , 2015

No of shares Market Price Value

L Ltd 20,000 20 4,00,000

M Ltd 30,000 312.4 93,72,000

N Ltd 20,000 361.2 72,24,000

P Ltd 60,000 505.10 3,03,06,000

4,73,02,000

UNITS 6,00,000

NAV per Unit 78.8367

23

COMPANY 2ndFebruary , 2015

No of shares Market Price Value

L Ltd 20,000 20.50 4,10,000

M Ltd 38,000 360 1,36,80,000

N Ltd 20,000 383.10 76,62,000

P Ltd 60,000 503.90 3,02,34,000

5,19,86000

UNITS Cash= 30,00,000-2499200( 8000* 312.4)=

5,00,800

5,00,800

NAV per Unit 5,24,86,800

UNITS 638053.35

NAV 82.2608

Additional units will be issued to Mr A at Rs 78.8367 = 30,00,000/78.8367= 38053.35

24

COMPANY

1st February , 2015 2ndFebruary , 2015

No of shares

Market Price

Value No of shares

Market Price

Value

L Ltd 20,000 20 4,00,000 20,000 20.50 4,10,000

M Ltd 30,000 312.4 93,72,000 38,000 360 1,36,80,000

N Ltd 20,000 361.2 72,24,000 20,000 383.10 76,62,000

P Ltd 60,000 505.10 3,03,06,000 60,000 503.90 3,02,34,000

4,73,02,000 5,19,86000

UNITS 6,00,000 Cash= 30,00,000-2499200( 8000*

312.4)= 5,00,800

5,00,800

NAV per Unit

78.8367 5,24,86,800

UNITS 638053.35

NAV 82.2608

Additional units will be issued to Mr A at Rs 78.8367 = 30,00,000/78.8367= 38053.35……

25

Question 8

»A Mutual fund has a NAV of 8.5 at the ₹beginning of the year . At the end of the year NAV increase to 9.10. Meanwhile fund distributes ₹ ₹0.90 as dividend and 0.75 as capital gains. ₹

»A) What is the fund’s return during the year ?

»B) Assuming that the investor had 200 units and also assuming that the distributions have been reinvested at an average NAV of Rs 8.75 . What is the return

26

»A) What is the fund’s return during the year ?

27

RETURN FOR THE YEAR Amount ₹

Change in price Rs 9.10- Rs 8.50 0.60

Dividend received 0.90

Capital gain distribution 0.75

Total Return 2.25

HOLDING PERIOD RETURN = 2.25/ 8.50= 26.47% 26.47%

» B) Assuming that the investor had 200 units and also assuming that the distributions have been reinvested at an average NAV of Rs 8.75 . What is the return

28

Particulars Amount ₹

Dividend + capital gain per unit 1.65₹ 1.65

Total received from 200 units = 1.65 x 200 ₹ 330

Additional Units acquired 330/ 8.75= 37.7 units₹ ₹

Value of 237.7 units x 9.10 2163

Price paid for 200 units at the beginning of the year = 200x 8.5

1700

Holding period return = (2163-1700)/1700 27.24%

Question 9

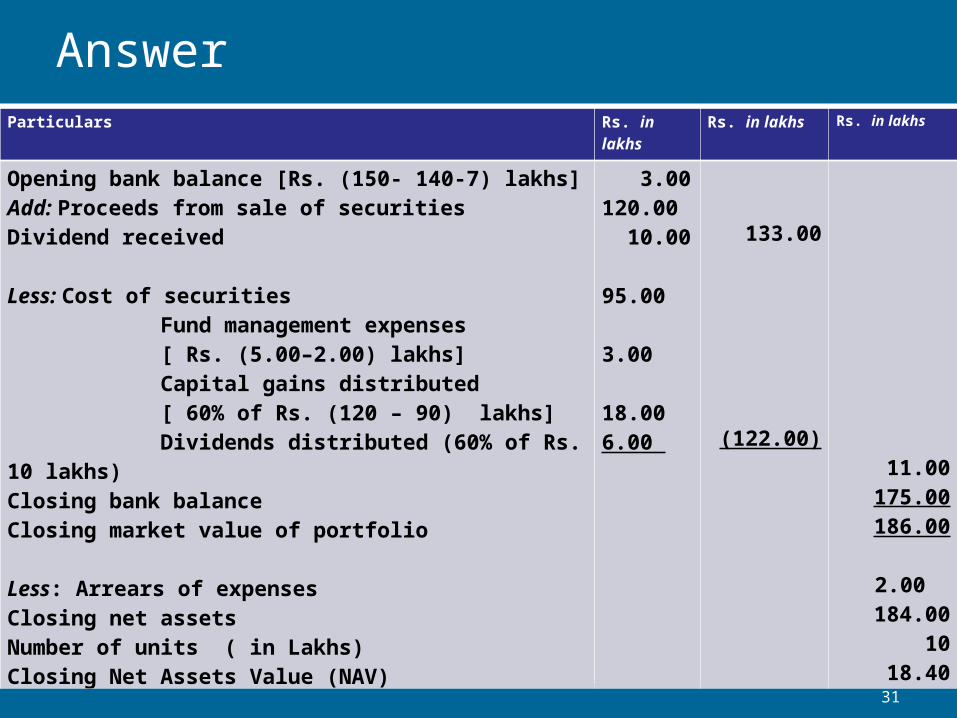

» A Mutual Fund raised funds on 01.04.2014 by issuing 10 lakhs units @ 15.00 per unit. Out of this Fund, Rs. 140 lakhs invested in several capital market instruments. The initial expenses amount to Rs. 7 lakhs. During June, 2014, the Fund sold certain securities worth Rs. 90 lakhs for Rs. 120 lakhs and it bought certain securities for Rs. 95 lakhs. The Fund Management expenses amounting to Rs. 5 lakhs per month out of which 2 lakhs was outstanding on 31.3.2015.

29

»The dividend earned was Rs. 10 lakhs. 60% of the realised earnings were distributed among the unit holders. The market value of the portfolio was Rs. 175 lakhs. Determine Net Asset value (NAV) per unit as on 31.03.2015.

30

AnswerParticulars Rs. in lakhs Rs. in lakhs Rs. in lakhs

Opening bank balance [Rs. (150- 140-7) lakhs]Add: Proceeds from sale of securities Dividend received

Less: Cost of securities Fund management expenses [ Rs. (5.00–2.00) lakhs] Capital gains distributed [ 60% of Rs. (120 – 90) lakhs] Dividends distributed (60% of Rs. 10 lakhs)Closing bank balance Closing market value of portfolio

Less: Arrears of expenses Closing net assets Number of units ( in Lakhs)Closing Net Assets Value (NAV)

3.00120.00 10.00

95.00

3.00

18.006.00

133.00

(122.00)11.00

175.00186.00

2.00184.00

1018.40

31

Question 10

»Calculate the NAV of a mutual fund from the following information:

On 1-4-2014 Outstanding units 1 crore of Rs. 10 each = Rs. 10 crores (Market Value Rs. 16 crores) Outstanding liabilities Rs. 5 crores.

Other information:

(i)20 lakhs units were sold during the year at Rs. 24 per unit.

32

»(ii) No additional investments were made during the year and as at the year end 50% of the investments held at the beginning of the year were quoted at 80% of book value.

»(iii) 10% of the investments have declined permanently 10% below cost.

»(iv) At the year end 31-3-15 outstanding liabilities were Rs. 1 crore.

»(v) Remaining investments were quoted at Rs. 13 crores.

33

Solution

Units at the end of the year 2014-2015 Units in crores

Units as on 1/4/2014 1.00

Add units issued during the year 0.20

1.20

34

Net asset Value of the Mutual Fund ₹ crores

Market value of investments

₹10 crores x 50% x80% 4.00

₹ 10 crores x 10% x 90% 0.90

Remaining investment at market value 13.00

Total market value of investments 17.90

Less liabilities 1.00

Net asset value 16.90

NAV per unit 16.90 crores / 1.2 crores = 14.08

Question 11

»Sparrow Holdings is a S.E.B.I. Registered Mutual Fund which made its maiden N.F.O. (New Fund offer) on l0th April, 2014 @ Rs. 10/- Face Value per unit. Subscription was received for 90 lakhs units: An underwriting arrangement was also entered into with Affinity Capital Markets Ltd that agreed to underwrite the entire NFO of 100 lakh units on a commission of 1.5%.Out of the monies received Rs. 892.50 lakhs was invested in various capital market instruments. The marketing expenses for the N.F.O. amounted to Rs. 11.25 1akhs.

35

»During the F.Y. ended March, 2015 the Fund sold securities having cost of Rs. 127.25 lakhs (FV 54.36 lakhs) for Rs. 141.25 lakhs. The fund in turn purchased securities for Rs. 130 lakhs. The management expenses of the fund are regulated by S.E.B.I stipulations which state that the same shall not exceed 0.25% of the average funds invested during the year. The actual amount spent towards management expenses was Rs. 2.47 lakhs of which Rs. 47,000 was in arrear.

36

»The dividends earned on the investments held amounted to Rs. 2.51 Lakhs of which a sum of Rs. 25,000 is yet to be collected. The fund distributed 80% of realized earnings. The closing Market Value of the Port folio was Rs. 1120.23 lakhs.

»You are required to determine the closing per unit NAV of the fund.

37

Computation of Management Expenses chargeable

Actual Expenses incurred (A ) 2.47

Opening investment made 892.50

Closing funds invested (892.50-127.25+130) 895.25

Total 1787.75

Average Funds Invested 1787.75/2 893.875

0.25% of average funds invested (B) 2.23

Lower of A or B 2.23

Less Amount unpaid .47

Management expanses paid 1.76

38

WORKING NOTES ₹ in lakhs

1. Computation of opening cash balance

Proceeds of NFO in full including underwriters commitment

1000.00

less Initial Purchase of securities 892.50

107.50

Less Underwriting Commission 15.00

Marketing Expenses 11.25 26.25

Opening Cash Balance 81.25

39

WORKING NOTES ₹ in lakhs

2 . Computation of closing cash balance

opening bank balance 81.25

Add Proceeds from sale of securities 141.25

Dividend received on investment (2.51—. 25) 2.26 143.51

224.76

Less Cost of securities purchased 130.00

Management expenses 1.76

Capital Gains distributed ( 141.25-127.25) x 80%₹ 11.20

Dividend distributed 2.26 x 80%₹ 1.81 144.77

Closing cash balance 79.99

40

Calculation of closing per unit of NAV of the Fund

Net Assets of Sparrow holdings

Closing Cash balance 79.99

Closing Market value of Investments 1,120.23

Accrued Dividends ( collectable) 0.25

1200.47

Less Current liabilities

Outstanding management fee payable .47

Closing Net Assets A 1200.00

Units outstanding ( in Lakhs) 100

NAV per Unit A/B 12.00

41

Question 12

» Calculate the year-end NAV of the mutual fund scheme on the basis of the information

» (i) UTI launched a new fund scheme for 6,000 ₹crore.

»(ii) Underwriting commission is 1% of the fund shared equally by SBI, PNB,Syndicate Bank and UTI Bank.

»(iii) The fund was launched on 1.4.2014 with face value of 1,000 per unit(As per SEBI rules Face ₹value must be 10)₹

42

»(iv) Underwriting commission was paid in full.

» (v) Management expense was allowed by SEBI @ 1% of the fund raised. However during the year management expense was 45 crore only. ₹The management decided to defer the payment of 5 crore to the next financial year. ₹

»(vi) On 1.5.2014,the total fund received was invested after deduction of underwriting commission And 100 cr to meet day to day ₹management expenses.

43

»The investment fund received Yielded 10% interest per annum. The interest was received for 3 quarters and the interest of Last quarter is yet to receive. The interest realized in cash has been distributed to the unit holders @ 80%. The financial year runs from April to March. The quarter starts from the date of investment i.e.,1.5.2014.

44

Solution Working Notes

Calculation of year end cash balance

Sale of units 6000

Add interest for 3 quarters of investment 5840 x 10% x 9/12

438

Investments = (6000-60-100)= 5840 6438

Less underwriting commission 60

Management expenses paid in cash 40

Investment 5840

Dividend paid 438 x 80% 350.40 6290.40

Closing cash balance 147.60

45

Calculation of Net Asset Value of a Fund ₹ in crore

Total Assets

Investments (6000-60-100) 5840

Add : Closing Cash balance 147.60

Add : Interest for two months due to be received 97.33 6084.93

( 5,840 x 10% 2/12 )

Less : Outstanding management expenses 5.00

Total value of the fund 6079.93

No of Units 6,000 crore / 1000= 6 crore units₹

NAV per unit 6079.93 / 6 crore units₹ ₹ 1013.32

46

Question 13

»The investment portfolio for a mutual fund scheme includes 10,000 shares of A Ltd and 8,000 shares of B Ltd acquired on 30/10/2014.

»The cost of A ltd shares is 20 while that of B ltd ₹is 30 . The market values of these shares at ₹the end of 2014-15 were 19 and 32 ₹ ₹respectively .

»Show important accounting entries in books of the fund in the accounting year 2014-15

47

solution

Date ₹ 000 ₹ 000

31/10/2014 Investment in A ltd Shares Dr 200

Investment in B Ltd shares Dr 240

To Bank 440

( Being purchase of A ltd 10,000 shares @ 20 ₹and 8,000 shares of B ltd @ 30 each)₹

31/03/2015 Revenue a/c 10

To Provision for Depreciation 10

(Being market value of A ltd depreciated for 1 ₹each for 10,000 shares

31/03/2015 Investment in B ltd shares Dr 16

To Unrealised appreciation reserve 16

( Being 8000 shares of B ltd appreciated @ 2 ₹each per share on the closing date

48

Question 14

»A fund purchased 10,000 debentures of a company on June 1, 2012 for 10.7 lakh and further 5,000 debentures on November 1, 2012 for 5.45 Lakh . The debenture carry fixed ₹annual coupon of 12% payable on every 31st March and 30th September . On Feburary 28, 2013 the fund sold 6,000 of these debentures for

6.78 lakh . Nominal value per debenture is ₹ ₹100

»Show investment in Debentures A/c in books of the Fund

49

Working Note

Note 1 10,000 x 100 x 12/100 x 2/12 = 0.20 Lakhs₹

Note 2 5000 x 100x 12/100x 1/12= .05 lakhs ₹

Note 3 6000 x 100x 12/100x 5/12 = 0.30 lakhs₹

Note 4 = Cost of investments per unit (10,70,000 – 20,000 ) + 5,45,000-5000) / 15000 units

= 10,50,000+ 5,40,000 )/ 15000 = 106₹

COST OF INVESTMENTS SOLD = 106 x 6000 = 6,36,000₹ ₹

6,000 x 100 x 12/100 x 5/12 = 30,000₹

SALE PROCEEDS = 6,78,000- 30,000 ( interest ) = 6,48,000₹

PROFIT 6,48,000- 6,36,000= 12,000₹

50

solution

Date Particulars ₹ lakhs Date Particulars ₹ lakhs

June 1 2012

To Bank 10.70 June 1 2012

By interest recoverable

.20

Nov 1 2012

To Bank 5.45 Nov 1 2012

By interest recoverable

.05

Feb 28 2013

To Interest Recoverable

.30 Feb 28 2013

By bank 6.78

Feb 28 2013

Profit on disposal

.12 March 31 2013

By balance c/d 9.54

16.57 16.57

51

INVESTMENT IN DEBENTURES ACCOUNT :

Question 15

»On April 1, 2012 a Mutual Fund scheme had 9 Lakhs units of the face value of 10 outstanding. ₹The scheme earned 81 lakh in 2012-13 out ₹which 45 lakh was earned in the first half year . ₹1 lakh units were sold on 30/09/12 at NAV of ₹60 .

»Show important entries for sale of units and distribution of dividend at the end of 2012-13

52

SolutionAllocation of Earnings Old UnitHolders

New Unit

Holders

Total

[9 lakhsunits]

[1 lakhsunits]Rs. in lakhs

Rs. in lakhs

First half year (Rs. 5 per unit) 45.00 Nil 45

Second half year (Rs. 3.60 per unit) 32.40 3.60 36

Earning 2012-13 77.40 3.60 81

Add: Equalization payment recovered 5

Total available for distribution 86

Equalization Payment:-Rs. 45 lakhs ÷ 9 lakhs = Rs. 5 per unit.In the case of an open-ended scheme, when units are sold and appropriate part of the sale proceeds should be credited to an Equalisation Account and when units are repurchased an appropriate amount should be debited to Equalisation Account

53

SolutionParticulars Old Unit

HoldersNew Unit

Holders

Dividend distributed8.60 8.60

Less: Equalization payment (5.00)

8.60 3.60

54

The net balance on this account should be credited or debited to the Revenue Account. The balance on the Equalisation Account debited or credited to the Revenue Account should not decrease or increase the net income of the fund but is only an adjustment to the distributable surplus. It should, therefore, be reflected in the Revenue Account only after the net income of the fund is determined

Journal EntriesDate Particulars Debit Credit

(Rs. in lakhs)

30.9.2012 Bank A/c 65

To Unit Capital 10

To Reserve 50

To Dividend Equalization 5

( Being the amount received on sale of 1 lakhs unit at a NAV of Rs. 60 per unit)

31.3.2013 Dividend Equalization To Revenue A/c(Being the amount transferred to Revenue Account)

55

30.9.2013 Revenue A/c To Bank(Being the amount distributed among 10 lakhs unit holders @ Rs. 8.60 per unit)

8686

55

Question 16

»A Mutual Fund raised 250 lakh on May 1, 2014 by issue of 25 lakh units of Rs. 10 per unit. The fund invested in several capital market instruments to build a portfolio of Rs. 231 lakhs. The initial expenses amounted to Rs. 10 lakh. During September, 2014, the fund sold certain securities of cost Rs. 83.75 lakhs for Rs. 105 lakhs and purchased certain other securities for Rs. 78.20 lakhs. The fund management expenses for the month amounted to Rs. 7.50 lakhs of which Rs. 0.55 lakh was in arrears.

56

»The dividend earned was Rs. 2.70 lakhs. 80% of the realized earnings were distributed. The market value of the portfolio on 30.05.2014 was Rs. 259.70 lakh.

»Determine NAV per unit.

57

AnswerParticulars Rs. in lakhs Rs. in lakhs Rs. in lakhs

Opening bank balance [Rs. (250- 231-10) lakhs]Add: Proceeds from sale of securities Dividend received

Less: Cost of securities Fund management expenses [ Rs. (7.50–0.55) lakhs] Capital gains distributed [ 80% of Rs. (105.00 – 83.75) lakhs] Dividends distributed (80% of Rs. 2.70lakhs)Closing bank balance Closing market value of portfolio

Less: Arrears of expenses Closing net assets Number of units ( in Lakhs)Closing Net Assets Value (NAV)

9.00105.00

2.70

78.20

6.95

17.00 2.16

116.7

104.31)12.39

259.70272.09

(0.55)271.54

2510.86

58

Question 17

»Ms Vrinda has invested in three mutual funds. From the details given below, find out effective yield on per annum basis in respect of each of the schemes to Ms Vrinda upto 31-03-2015.

59

Mutual Fund P Q R

Date of Investment Amount of investment (Rs.)NAV at the date of investment (Rs.)Dividend received upto 31-3-2015 (Rs.)NAV as on 31-3-2015 (Rs.)

1-11-2014

1,50,000

10.42

Nil

10.70

1-10-2014

2,70,000

10.11

4600

10.25

12-9-2014

1,25,000

9.50

1200

9.46

Calculation of effective yield on per annum basis in respect of three mutual fund schemes of Ms Vrinda upto 31.03.2015

S.No Particulars P Q R

1 Amount of Investment (Rs.) 1,50,000 2,70,000 1,25,000

2 Date of investment 1.11.2014 1.10.2014 12.9.2014

3 NAV at the date of investment (Rs.)

10.42 10.11 9.50

4 No. of units on date of investment [1/3]

14395.3934 26706.2314 13157.894

5 NAV per unit on 31.03.2015 (Rs.)

10.70 10.25 9.46

6 Total NAV of mutual fund investments on

31.03.2015 [4 x 5]

1,54,031 2,73,739 1,24,474

60

Calculation of effective yield on per annum basis in respect of three mutual fund schemes of Vrinda upto 31.03.2015

P Q R

7 Increase/ decrease of NAV [6-1]

4,031 3,739 -526

8 Dividend received upto 31.3.2015

Nil 4600 1200

9 Total yield [7+8] 4031 8,339 674

10 Yield % [9/1] x 100 2.69% 3.09% .54%

11 Number of days 151 182 201

12 Effective yield p.a. [10/11] x 365 days

6.50% 6.19% .98%

61

Question 18

»A Mutual Fund has launched a new scheme “All Purpose Scheme“. The Mutual Fund's Asset management company wishes to invest 25% of the NAV of the Scheme in an unrated debt instrument of a company Y Ltd. which has been paying above average returns for the past many years. The promoters of the company seek your professional advice in light of the Regulations of SEBI. Will the position change in case the debt instruments of the company Y Ltd., is a rated.

62

solution

»The Seventh Schedule of SEBI (Mutual funds) Regulations, 1996 states that a mutual fund scheme shall not invest more than 10% of its NAV in unrated debt instruments issued by a single issuer and the total investment in such instruments shall not exceed 25% of the NAV of the scheme. All such investments shall be made with the prior approval of the Board of Trustees and the Board of Asset Management Company.

63

Solution...Contd

»It also states that a mutual fund scheme shall not invest more than 15% of its NAV in debt instruments issued by a single issuer which are rated not below investment grade by an authorised credit rating agency. Such investment limit may be extended to 20% of the NAV of the scheme with the prior approval of the Board of Trustees and the Board of Asset Management Company.

64

» Accordingly,

» (i) If the debts instruments of Y Ltd. unrated then Mutual fund’s Asset Management Company (AMC) cannot invest more than 10% of its NAV in it.

» (ii) If the debts instruments of Y Ltd are rated, then also, Mutual Fund’s AMC cannot invest more than 20% of its NAV in it. Therefore, investment of 25% of its NAV of the scheme in debts instrument of Y Ltd. by Mutual Fund’s AMC is not permissible as per the SEBI (Mutual Fund) Regulation 1996.

65

Question 19

» While closing its books of account on 31st March, 2015 a Non-Banking Finance Company has its advances classified as follows:

» Calculate the amount of provision, which must be made against the Advances.

66

Particulars Amount Rs Lakhs

Standard assets Sub-standard assets Secured portions of doubtful debts:− upto one year − one year to three years− more than three years Unsecured portions of doubtful debts Loss assets

16,8001,340

32090

30

97

48

Solution

Calculation of provision required on advances as on 31st March, 2015:

AmountRs. in lakhs

Percentageof provision

ProvisionRs. in lakhs

Standard assets 16,800 0.25 42

Sub-standard assets 1,340 10 134

Secured portions of doubtful debts−

− upto one year 320 20 64

− one year to three years

90 30 27

− more than three years

30 50 15

Unsecured portions of doubtful debts

97 100 97

Loss assets 48 100 48427

67

Question 20

»Anischit Finance Ltd. is a non-banking finance company. It makes available to you the costs and market price of various investments held by it as on 31.3.2015:

68

69

Scripts: Cost Market Price

A.

B

C

Equity Shares-ABCDEFGMutual funds-MF-1 MF-2 MF-3Government securities-GV-1 GV-2

60.0031.5060.0060.0090.0075.0030.00

39.0030.006.00

60.0075.00

61.2024.0036.00120.0105.0090.00 6.00

24.0021.009.00

66.0072.00

»(i) Can the company adjust depreciation of a particular item of investment within a category?

»(ii) What should be the value of investments as on 31.3.2015?

»(iii) Is it possible to off-set depreciation in investment in mutual funds against appreciation of the value of investment in equity shares and government securities?

70

Solution

»(i) Quoted current investments for each category shall be valued at cost or market value, whichever is lower. For this purpose, the investments in each category shall be considered scrip-wise and the cost and market value aggregated for all investments in each category. If the aggregate market value for the category is less than the aggregate cost for that category, the net depreciation shall be provided for or charged to the profit and loss account.

71

»If the aggregate market value for the category exceeds the aggregate cost for the category, the net appreciation shall be ignored. Therefore, depreciation of a particular item of investments can be adjusted within the same category of investments.

72

Category Security COST Market valueA. Equity Shares-

A 60 61.2

B 31.5 24

C 60 36

D 60 120

E 90 105

F 75 90

G 30 6

Total 406.5 442.2

73

Category Security COST Market value B Mutual funds-

MF-1 39 24

MF-2 30 21

MF-3 6 9

Total 75 54

Investment in units of mutual funds shall be valued at NAV declared By the mutual fund in respect each particular scheme

C Government securities-

GV-1 60 66

GV-2 75 72Total 135 138

Investments in Gsecs shall be valued at carrying cost

74

Type of Investment Valuation

Valuation Principle Value

ValueRs. in lakhs

Equity Shares (Aggregated)

Mutual Funds

Government securities

Lower of cost or market Value

NAV (Market value, assumed) Cost

406.50

54.00

135.00

595.50

75

Investment in units of mutual funds shall be valued at NAV declared By the mutual fund in respect each particular scheme

»As per para 14 of AS 13 “Accounting for Investments”, the carrying amount for current investments is the lower of cost and market price. Sometimes, the concern of an enterprise may be with the value of a category of related current investments and not with each individual investment, and accordingly, the investments may be computed at the lower of cost and market value computed category-wise.

76

»(iii) Inter category adjustments of appreciation and depreciation in values of investments cannot be done. It is not possible to offset depreciation in investment in mutual funds against appreciation of the value of investments in equity shares and Government securities

77