Embed Size (px)

Citation preview

Florida State Board of Administration

Fiscal Year 1999-2000

Annual Report

Florida Hurricane

Catastrophe Fund

The purpose of the Florida

Hurricane Catastrophe Fund

is to improve the availability

and affordability of property

insurance in Florida by

providing reimbursements to

insurers for a portion of their

catastrophic hurricane losses.

Front cover: Hurricane Floyd

FLORIDA HURRICANE CATASTROPHE FUNDFISCAL YEAR 1999-2000 ANNUAL REPORT

C O N T E N T S

EXECUTIVE MESSAGE 1

OVERVIEW 2

LEGISLATIVE HISTORY 3

1999 - 2000 IN REVIEW 4Operational Activities 4Legislation 4Rulemaking 4Auditing Program 5Bonding Program 6FHCF Bonding Capacity Estimates 6Litigation 6Public Contributions 6

STATISTICAL INFORMATION 82000 Exposure Concentration by County 81999 Exposure Concentration by County 8Participating Insurers by Coverage Option Selection 9Reported Premium by Coverage Option 9Statistical Summary 10Retention Multiples 102000 Tropical Cyclones in the Atlantic Basin 111999 Tropical Cyclones in the Atlantic Basin 11

THE PEOPLE WHO MAKE IT POSSIBLE 12FSBA Trustees 12FSBA Executive Director 12FHCF Staff 12FHCF Advisory Council Members 13FHCF Service Providers 13

APPENDIX: AUDITED FINANCIAL STATEMENTS 14Fiscal Year ended June 30, 2000

Headquarters of the Florida State Board of AdministrationHermitage Centre, Tallahassee, Florida

We hope this report is informative, and we

welcome any thoughts or ideas regarding the

content of future issues. For questions or

additional information, please do not hesitate to

contact our office or visit our website at

www.fsba.state.fl.us/fhcf/.

Jack E. Nicholson, Chief Operating Officer

Florida Hurricane Catastrophe Fund

Florida State Board of Administration

EXECUTIVE MESSAGE

1

The Florida State Board of Administration is

pleased to provide the 1999-2000 Annual Report

of the Florida Hurricane Catastrophe Fund

(FHCF). This report describes the operational

activities of the fund and the legislative changes

enacted during the past fiscal year. Although the

1999 and 2000 hurricane seasons were active,

during this period, only one hurricane in 1999

made landfall in Florida; however, no insurer

losses triggered the payment of FHCF

reimbursements.

FHCF Mission Statement

The mission of the Florida HurricaneCatastrophe Fund (FHCF) is to responsiblyand ethically administer the FHCF by:

1) Understanding the catastrophe financing

needs of our beneficiaries and

stakeholders.

2) Striving to satisfy a portion of the

hurricane catastrophe financing

needs of insurers in order to create

additional insurance capacity for

the state.

3) Protecting the public interest by

maintaining insurance capacity in

the state.

4) Providing exceptional investment,

financial, and administrative services.

2

OVERVIEWOVERVIEW

The Florida Hurricane CatastropheFund (FHCF) is a tax-exempt trustfund created during a SpecialSession of the Legislature inNovember, 1993, in the aftermath ofHurricane Andrew. The purpose ofthe fund is to protect and advancethe State’s interest in maintaininginsurance capacity in Florida byproviding reimbursements toinsurers for a portion of theircatastrophic hurricane losses.Insurers which write residentialproperty insurance on structures ortheir contents are required to enterinto a reimbursement contract withthe Florida State Board of Administration(FSBA), to report their exposures, to pay

premiums, and to report losses by calendar year-end or at other times as required by the FSBA.

The FHCF is a state program administered bythe FSBA. Its trustees are the Governor, theComptroller, and the Treasurer/InsuranceCommissioner. A nine-member advisory councilprovides the FHCF with information and advice.The day-to-day operations are the responsibilityof the FHCF’s chief operating officer. Theseresponsibilities include: proposing legislationand responding to legislative requests;rulemaking; providing information toparticipating insurers; determining bondingcapacity; preparing financial statements andrevenue projections; meeting and interactingwith the FHCF advisory council; implementingand overseeing the audit program; andcoordinating the activities of outside consultants.

LEGISLATIVE HISTORY

The FHCF was created by Section 215.555,Florida Statutes. The law:

• requires certain insurers to participate in the

Fund as a condition of doing business in the

State

• grants rulemaking authority

• establishes the procedures for setting and

collecting the reimbursement premiums

• establishes procedures for paying loss

reimbursements

• authorizes the investment and disbursement

of moneys collected by the Fund

• authorizes the issuance of debt secured by

the premiums and the assessments

• authorizes the imposition and collection of

emergency assessments to retire the bonds

• requires insurers to participate at certain

coverage levels if bonds are outstanding

• limits debt issuance and the amount of the

assessments

• provides for debt security if the Fund is

terminated by operation of law

• establishes an Advisory Council

• provides that a violation of Section 215.555,

Florida Statutes, is a violation of the

Insurance Code

• provides explicit authority to the FSBA for

other legal action

Old and New Capitol Buildings, Tallahassee, Florida

3

LEGISLATIVE HISTORY

1999-2000IN REVIEW

OperationalActivities

Although the 2000hurricane seasonmarked the thirdconsecutive year ofabove-averagehurricane activity, theUnited States escaped adirect hit from ahurricane this year. Two tropical storms, Gordonand Helene, did make landfall striking Florida inSeptember. There have been no hurricanes thathave triggered FHCF coverage since HurricanesErin and Opal in 1995. The major activities forthe past fiscal year include: issuing two Requests

for Information (RFI’s) resulting in the selectionof Paragon Reinsurance Risk ManagementServices, Inc. as the FHCF Administrator andGuy Carpenter/Lehman Risk Advisors as theFund’s Reinsurance Intermediary; consideringreinsurance and financial products; providingassistance to the legislature regarding legislationrelated to insurers’ recovery for the FHCF;developing the 2000 premium formula; issuingbonding capacity estimates in October and May;adopting four rules, and providing staff supportto the Florida Commission on Hurricane LossProjection Methodology. The FHCF also held aloss reimbursement workshop this year andinvited insurers to participate in the discussionand react to various reimbursement approaches.In addition, an audit conference was held withthe FHCF external auditors to familiarize themwith the changes in the audit program.

Legislation

During the 2000Legislative Session, theFHCF offeredamendatory languageto Section 215.555,Florida Statutes, tomodify the prior year’slegislation relating tothe fund’s method for

determining each insurer’s recovery from thefund. In addition, language was added to clarifythat the FHCF may provide coverage to insurersassuming liabilities for policies in the FloridaWindstorm Underwriting Association or theFlorida Residential Property Casualty JointUnderwriting Association.

Rulemaking

During the 1999-2000 contract year, the FSBAadopted the following rules:

19-8.010 Reimbursement Contract Rule –Adopting the annualreimbursement contract

19-8.013 Bonding Rule – Amendments tothe issuance of revenue bonds

19-8.028 Reimbursement Premium Rule –Adopting the annual rates

19-8.029 Insurer Reporting Requirements –Data reporting requirements ofinsurer exposure (Data Call)

Amendments to 19-8.013, F.A.C. were needed toconform the rule with the statutory changes, to

4

1999-2000IN REVIEW

The FSBA has encountered problems withcompanies not being prepared for a scheduledaudit. Often companies have not retained a copyof the exposure data submitted at policy leveldetail. Also, a number of companies haveexperienced difficulty obtaining the actualpolicies for review.

The audits conducted have revealed a numberof common insurer reporting errors. Theseinclude, but are not limited to, the following:

•incorrectly reporting ZIP Codes, and

construction characteristics (e.g., reporting

the mailing ZIP Code rather than the

ZIP Code for the location of the property).

•omitting increased coverages or

endorsements to property coverage.

•reporting policies or coverages not required

to be reported (e.g., builders risk, wind

exclusion, business interruption).

•including policies not in-force as of June 30.

They are reporting canceled policies or those

not yet renewed.

•not able to report percentage deductibles.

Companies are required to retain complete,accurate, and detailed records at the policy levelfor all reported exposure for five years or untilthe FHCF has completed an audit of thecompany records of exposure data and lossreimbursement data in applicable years,whichever is later. Retention of records isimperative since an audit may result in aresubmission, corrective action, or an adjustmentto a company’s FHCF premium or loss recovery.

appropriately define the “balance of the fund asof December 31,” and to remove language whichwould have precluded bonding prior to the endof the calendar year. It should also be noted thatRule 19-8.027, F.A.C. establishing definitions foreach contract year, was eliminated and thecontents of this rule were incorporated into otherexisting rules.

Auditing Program

The FSBA routinely conducts audits of exposuredata submitted by participating companies. Theaudit is limited in scope and is intended to verifythat participating companies are properlyreporting their exposure, as well as, to confirmtheir compliance with the FHCF data reportingrequirements.

Each participating company is required toreport its exposure data annually and to generatean audit file at the same time. All records,including exposure filings, policy files and anyother supporting documentation, must beretained with the audit file. The FSBA notifies acompany at least 60 days prior tocommencement of an audit and includesdetailed instructions to the company onproviding the required records needed for theaudit. All information that supports acompany’s exposure is subject to audit.

It is important for a company noticed for anaudit to follow all instructions given by theFHCF since failure to provide the informationneeded may result in a delay of the audit. Adelay by the company, which causes the FHCF toincur costs in addition to the usual andcustomary costs of the audit, may result in thecompany being charged those additional costs.

5

FHCF Bonding CapacityEstimates

($ billions)

1994 $ 2

1995 4 (a)

MAY OCTOBER1996 5 5

1997 5.5 6

1998 8.5 (b) 8.5

1999 8.7 7.9(c)/3.9(d)

2000 7.4(c)/4.5(d) 7.3(c)/5.5(d)

(a) The requirement to publish bonding estimates twice a year wasinstituted following the 1995 legislative Session.

(b) Reflects a private letter ruling granting tax exempt status to bonds.(c) The 1999 legislative Session resulted in limiting the overall capacity

of the FHCF to $11 billion and provided for subsequent seasoncapacity.

(d) Subsequent season capacity.

Litigation

All previous outstanding litigation andenforcement issues were resolved during thecurrent fiscal year. There is currently no pendinglitigation against the FHCF.

Public Contributions

As part of the private letter ruling issued by theInternal Revenue Service (IRS) granting taxexempt status to the FHCF, the IRS required thata certain amount of the funds in the FHCF bedevoted to hurricane mitigation purposes. The

The FSBA has developed and implemented anaudit program to ensure the proper reporting ofclaims to the FHCF. Again, companies arerequired to retain complete and accurate records,at the policy level, for all reported claims untilthe FHCF has completed an audit of thesespecific records. The FHCF has conducted 18audits related to the losses reported as a result ofHurricane Erin and Hurricane Opal in 1995.These are the only storms resulting inreimbursable claims to date.

Bonding Program

The FHCF is obligated only to the extent of itsaccumulated assets and borrowing capacity.Obligations of the FHCF are not obligations ofthe State. Should current assets be insufficient topay obligations under the reimbursementagreement, the FHCF has the ability to finance adeficit by the issuance of tax exempt revenuebonds. Such revenue bonds are financed by aspecial emergency assessment on all propertyand casualty insurers excluding workerscompensation and accident and health. To datethe FHCF has not issued revenue bonds. TheFHCF staff continues to update the bondingdocuments in preparation for a future eventwhich requires the issuance of bonds.

6

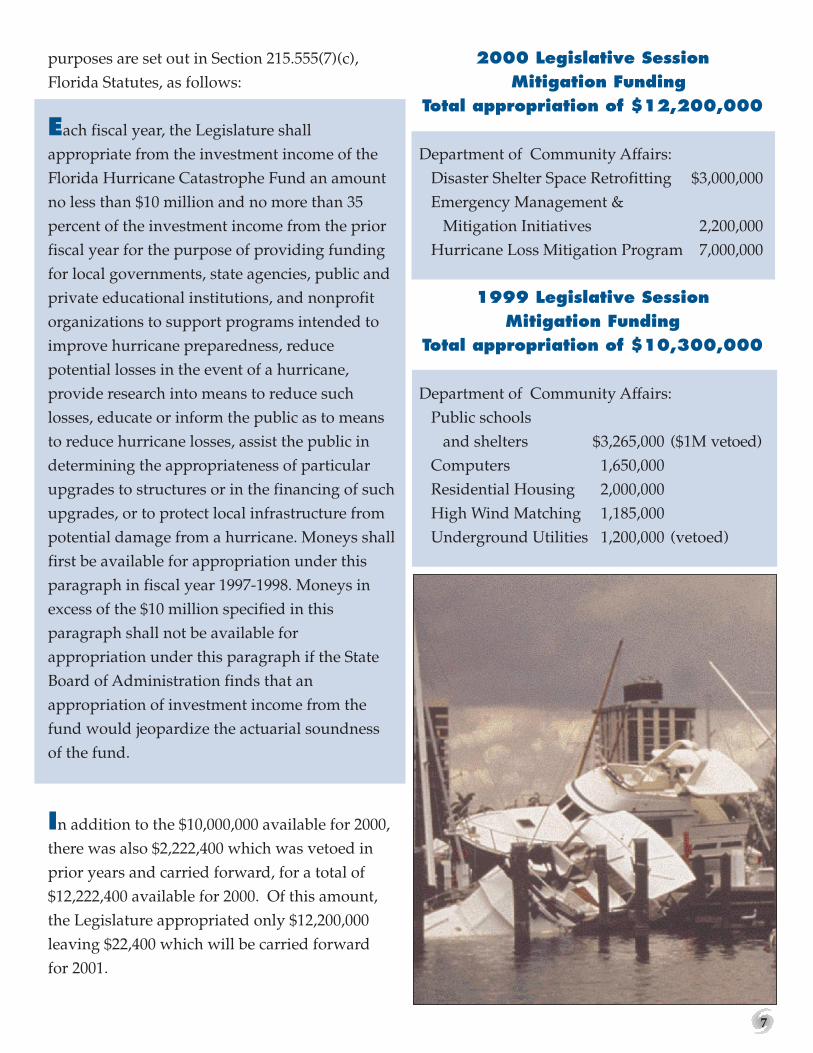

purposes are set out in Section 215.555(7)(c),Florida Statutes, as follows:

Each fiscal year, the Legislature shallappropriate from the investment income of theFlorida Hurricane Catastrophe Fund an amountno less than $10 million and no more than 35percent of the investment income from the priorfiscal year for the purpose of providing fundingfor local governments, state agencies, public andprivate educational institutions, and nonprofitorganizations to support programs intended toimprove hurricane preparedness, reducepotential losses in the event of a hurricane,provide research into means to reduce suchlosses, educate or inform the public as to meansto reduce hurricane losses, assist the public indetermining the appropriateness of particularupgrades to structures or in the financing of suchupgrades, or to protect local infrastructure frompotential damage from a hurricane. Moneys shallfirst be available for appropriation under thisparagraph in fiscal year 1997-1998. Moneys inexcess of the $10 million specified in thisparagraph shall not be available forappropriation under this paragraph if the StateBoard of Administration finds that anappropriation of investment income from thefund would jeopardize the actuarial soundnessof the fund.

In addition to the $10,000,000 available for 2000,there was also $2,222,400 which was vetoed inprior years and carried forward, for a total of$12,222,400 available for 2000. Of this amount,the Legislature appropriated only $12,200,000leaving $22,400 which will be carried forwardfor 2001.

2000 Legislative SessionMitigation Funding

Total appropriation of $12,200,000

Department of Community Affairs:Disaster Shelter Space Retrofitting $3,000,000Emergency Management &

Mitigation Initiatives 2,200,000Hurricane Loss Mitigation Program 7,000,000

1999 Legislative SessionMitigation Funding

Total appropriation of $10,300,000

Department of Community Affairs:Public schools

and shelters $3,265,000 ($1M vetoed)Computers 1,650,000Residential Housing 2,000,000High Wind Matching 1,185,000Underground Utilities 1,200,000 (vetoed)

7

STATISTICAL INFORMATION

2000 ExposureConcentration by County

($ Billions)

Total % of TotalName Exposure ExposurePalm Beach $86.4 10.02%Dade 85.1 9.87Broward 83.6 9.69Pinellas 50.0 5.80Orange 48.5 5.62Hillsborough 46.3 5.37Duval 37.1 4.30Lee 34.1 3.95Sarasota 28.4 3.29Brevard 27.8 3.23Other 335.4 38.86Total $862.7 100.00%

8

1999 ExposureConcentration by County

($ Billions)

Total % of TotalName Exposure ExposurePalm Beach $78.7 9.94%Dade 77.1 9.74Broward 76.1 9.61Pinellas 47.3 5.97Orange 44.8 5.65Hillsborough 42.8 5.40Duval 34.5 4.36Lee 30.0 3.79Brevard 26.2 3.30Sarasota 25.9 3.27Other 308.3 38.97Total $791.7 100.00%

STATISTICAL INFORMATION

Orange

Palm Beach

Broward

Dade

Hillsborough

Duval

Pinellas

Sarasota

Brevard

Lee

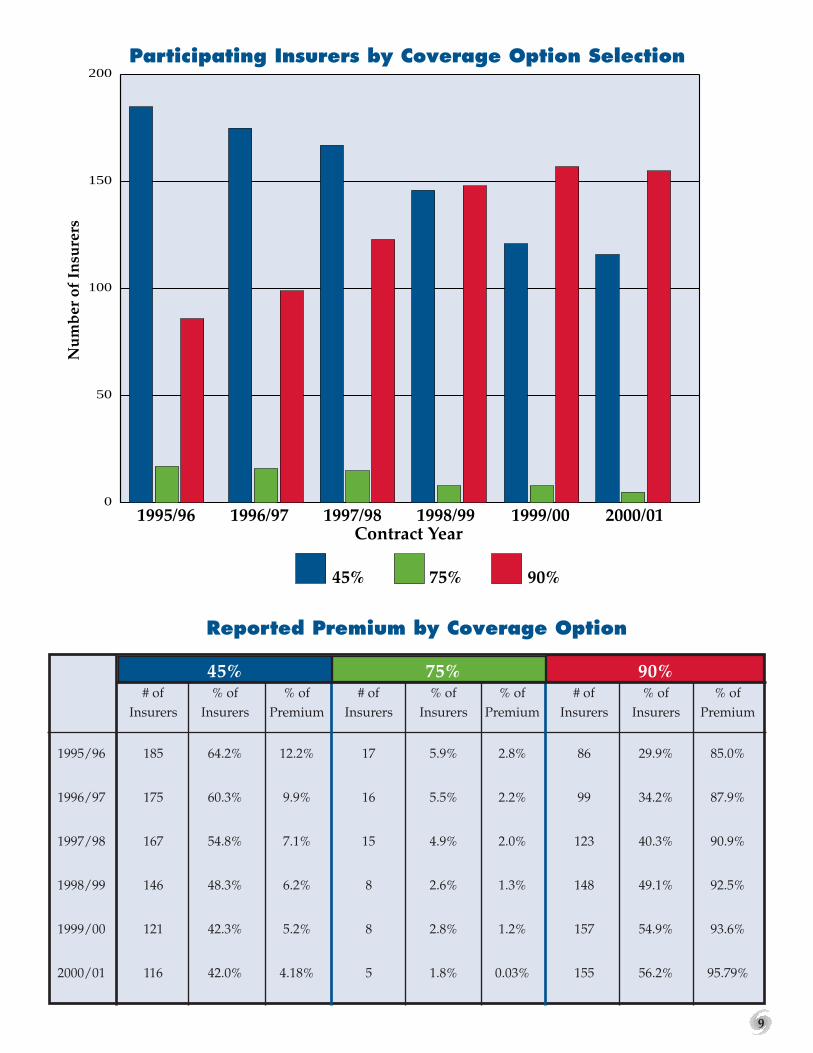

Participating Insurers by Coverage Option Selection

9

Reported Premium by Coverage Option

45% 75% 90%# of % of % of # of % of % of # of % of % of

Insurers Insurers Premium Insurers Insurers Premium Insurers Insurers Premium

1995/96 185 64.2% 12.2% 17 5.9% 2.8% 86 29.9% 85.0%

1996/97 175 60.3% 9.9% 16 5.5% 2.2% 99 34.2% 87.9%

1997/98 167 54.8% 7.1% 15 4.9% 2.0% 123 40.3% 90.9%

1998/99 146 48.3% 6.2% 8 2.6% 1.3% 148 49.1% 92.5%

1999/00 121 42.3% 5.2% 8 2.8% 1.2% 157 54.9% 93.6%

2000/01 116 42.0% 4.18% 5 1.8% 0.03% 155 56.2% 95.79%

0

50

100

150

200N

um

ber

of

Insu

rers

Contract Year1999/001995/96 1996/97 1997/98 1998/99 2000/01

45% 75% 90%

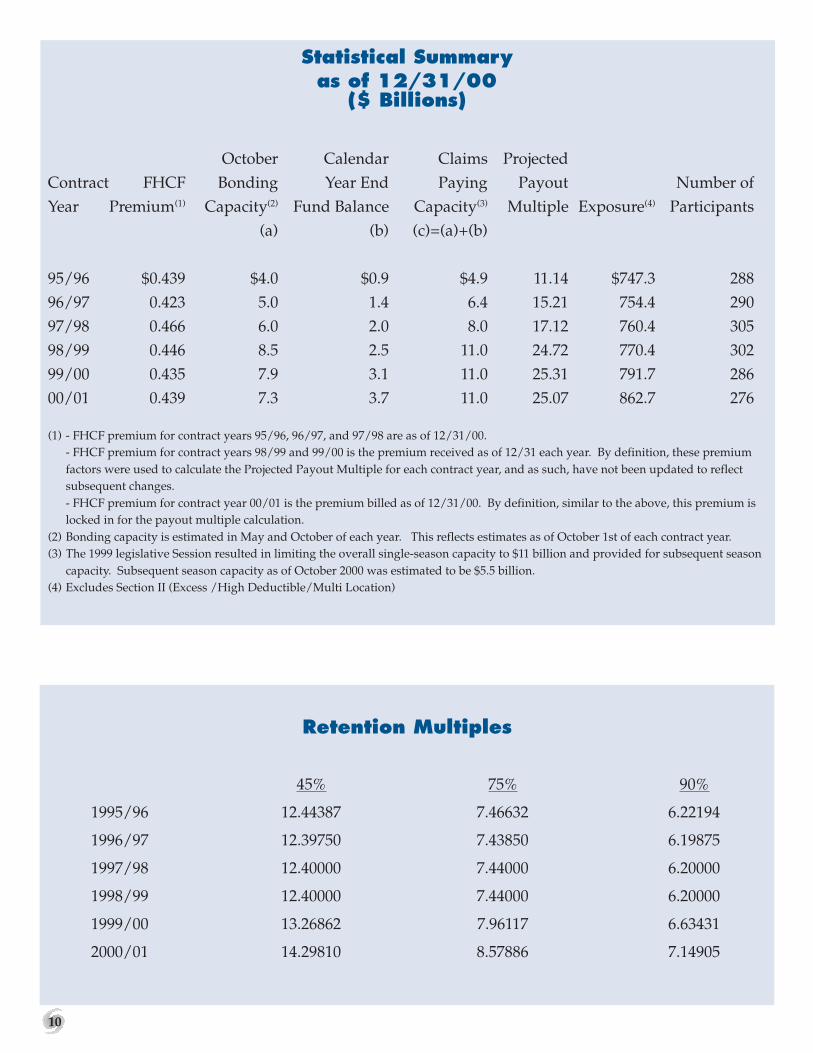

Statistical Summaryas of 12/31/00

($ Billions)

October Calendar Claims ProjectedContract FHCF Bonding Year End Paying Payout Number ofYear Premium(1) Capacity(2) Fund Balance Capacity(3) Multiple Exposure(4) Participants

(a) (b) (c)=(a)+(b)

95/96 $0.439 $4.0 $0.9 $4.9 11.14 $747.3 28896/97 0.423 5.0 1.4 6.4 15.21 754.4 29097/98 0.466 6.0 2.0 8.0 17.12 760.4 30598/99 0.446 8.5 2.5 11.0 24.72 770.4 30299/00 0.435 7.9 3.1 11.0 25.31 791.7 28600/01 0.439 7.3 3.7 11.0 25.07 862.7 276

(1) - FHCF premium for contract years 95/96, 96/97, and 97/98 are as of 12/31/00.- FHCF premium for contract years 98/99 and 99/00 is the premium received as of 12/31 each year. By definition, these premiumfactors were used to calculate the Projected Payout Multiple for each contract year, and as such, have not been updated to reflectsubsequent changes.- FHCF premium for contract year 00/01 is the premium billed as of 12/31/00. By definition, similar to the above, this premium islocked in for the payout multiple calculation.

(2) Bonding capacity is estimated in May and October of each year. This reflects estimates as of October 1st of each contract year.(3) The 1999 legislative Session resulted in limiting the overall single-season capacity to $11 billion and provided for subsequent season

capacity. Subsequent season capacity as of October 2000 was estimated to be $5.5 billion.(4) Excludes Section II (Excess /High Deductible/Multi Location)

Retention Multiples

45% 75% 90%

1995/96 12.44387 7.46632 6.22194

1996/97 12.39750 7.43850 6.19875

1997/98 12.40000 7.44000 6.20000

1998/99 12.40000 7.44000 6.20000

1999/00 13.26862 7.96117 6.63431

2000/01 14.29810 8.57886 7.14905

10

2030405060708090

40

30

20

10

Hur. CINDY8/19 - 8/31140 mph

Hur. GERT9/11 - 9/23150 mph

Hur. FLOYD9/7 - 9/17155 mph

Hur. JOSE10/17 - 10/25100 mph

T.S. EMILY8/24 - 8/2850 mph

Hur. LENNY11/13 - 11/22155 mphT.S. KATRINA

10/28 - 11/140 mph

Hur. BRET8/18 - 8/25140 mph

Hur. IRENE10/13 - 10/19110 mph

T.S. HARVEY9/19 - 9/2260 mph

Hur. DENNIS8/24 - 9/5105 mph

T.S. ARLENE6/11 - 6/1860 mph

2030405060708090

40

30

20

10

T.S. HELENE9/15 - 9/2265 mph

T.S. BER YL8/13 - 8/1550 mph

Hur . ISAAC9/21 - 10/1140 mph

T.S. LESLIE10/4 - 10/740 mph

Hur . ALBER TO8/4 - 8/23125 mph

Hur . MICHAEL10/16 - 10/20100 mph

Hur . GORDON9/14 - 9/1875 mph

Hur . DEBBIE8/19 - 8/2475 mph

T.S. ERNESTO9/2- 9/340 mph

Hur . KEITH9/28 - 10/6135 mph

Hur . FLORENCE9/11 - 9/1780 mph

T.S. NADINE10/19 - 10/2160 mph

Hur . JOYCE9/25 - 10/290 mph

T.S. CHRIS8/17 - 8/1940 mph

2000 TROPICAL CYCLONES IN THE A TLANTIC BASIN

H AlbertoTS BerylTS ChrisH DebbieTS ErnestoH FlorenceH Gordon*TS HeleneH IsaacH JoyceH KeithTS LeslieH MichaelTS Nadine

TS Tropical StormH Hurricane

Storms makinglandfall in Florida

* hit Florida as a Tropical Storm

The FHCF was not required to pay losses for the 2000 hurricane season.

1999 TROPICAL CYCLONES IN THE A TLANTIC BASIN

TS ArleneH BretH CindyH DennisTS EmilyH FloydH GertTS HarveyH IreneH JoseTS KatrinaH Lenny

TS Tropical StormH Hurricane

Storms makinglandfall in Florida

The FHCF was not required to pay losses for the 1999 hurricane season.11

FLORIDA STATE BOARD OF ADMINISTRATION

TRUSTEES

The Honorable Jeb BushGovernor, State of FloridaPL 05, The CapitolTallahassee, FL 32301Ph: (850) 488-4441

The Honorable Robert F. MilliganComptroller, State of FloridaPL 09, The CapitolTallahassee, FL 32301Ph: (850) 410-9370

The Honorable Tom GallagherTreasurer and Insurance CommissionerState of FloridaPL 11, The CapitolTallahassee, FL 32301Ph: (850) 922-3100

EXECUTIVE DIRECTOR

Tom HerndonFlorida State Board of Administration1801 Hermitage BoulevardTallahassee, FL 32308Ph: (850) 488-4406

FLORIDA HURRICANECATASTROPHE FUND STAFF

Jack E. Nicholson, Ph.D, CLU, CPCUChief Operating Officer1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1340e-mail: [email protected]

Anne T. BertAssistant Chief of Operations1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1342e-mail: [email protected]

THE PEOPLE WHO MAKE IT POSSIBLE

Tracy L. Allen, EsquireSenior Attorney1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1341e-mail: [email protected]

Gina Wilson, CPA (GA), CPMAudit Program Field Coordinator1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1348e-mail: [email protected]

Donna SirmonsManagement Review Analyst1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1349e-mail: [email protected]

Ramona A. WorleyBudget Analyst1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1343e-mail: [email protected]

Marcie VernonAdministrative Assistant-Audit Program1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1345e-mail: [email protected]

Patti ElsberndManagement Assistant1801 Hermitage Boulevard, Suite 100Tallahassee, FL 32308Ph: (850) 413-1346e-mail: [email protected]

(as of 1/31/01)12

THE PEOPLE WHO MAKE IT POSSIBLE

FHCF ADVISORYCOUNCIL MEMBERS

Barney T. Bishop IIIThe Windsor Group501 East Tennessee Street,Suite ATallahassee, FL 32308

Larry Johnson, FCAS, MAAAAllstate Insurance Company2775 Sanders Road, Suite C09Northbrook, IL 60062

Jim W. Henderson, CPA, CPCUBrown & Brown, Inc.P. O. Box 2412Daytona Beach, FL 32115-2412

William HuffcutOffice of the ComptrollerThe Capitol, Plaza LevelTallahassee, FL 32399

Yolanda Cash Jackson, Esquire (Chair)Becker & Poliakfoff3111 Stirling RoadFt. Lauderdale, FL 33312

Rade Musulin, ACAS, MAAAFlorida Farm Bureau5700 S.W. 34th StreetGainesville, FL 32608

Robert M. PedutoEmployers Reinsurance CorporationP. O. Box 2991Overland Park, KS 66201-1391

Michael RuckerWTXL TV277927 Thomasville RoadTallahassee, FL 32312

Joseph Varon, P.E.The Haskell CompanyP. O. Box 44100Jacksonville, FL 32231

FHCF SERVICE PROVIDERS

Legal Services:

Office of the Attorney GeneralDepartment of Legal AffairsThe CapitolTallahassee, FL 32399-1050Ph: (850) 487-1963

Brown & Wood, LLPOne World Trade CenterNew York, NY 10048Ph: (212) 839-5300

Lewis, Longman &Walker, P.A.125 South Gadsden Street,Suite 300P. O. Box 10788Tallahassee, FL 32302Ph: (850) 222-5702

Ausley & McMullen, P.A.P. O. Box 391227 South Calhoun StreetTallahassee, FL 32302Ph: (850) 224-9115

Financial Services:

Raymond James & AssociatesP. O. Box 12749St. Petersburg, FL 33733-2749Ph: (727) 573-8189

Administrator Services:

Paragon Risk Management Reinsurance Services, Inc.3600 West 80th StreetMinneapolis, MN 55431Ph: (612) 844-9752

Actuarial ConsultingServices:

Paragon Risk Management Reinsurance Services, Inc.3600 West 80th StreetMinneapolis, MN 55431Ph: (612) 844-9752

Auditing Services:

Wendell K. McDavid, AIE3933 Kings CoveEllenwood, GA 30294

Regulatory Insurance Consulting Services, Inc.3613 Londerry DriveTallahassee, FL 32308

Donald KoelkerP. O. Box 250783Daytona Beach, FL 32125-0783

James E. Salter, CPA, AFE7500 Old Georgetown RoadSuite 700Bethesda, MD 20814-6133

Harold S. Tattershall, AIE13780 Sea Mist DriveJacksonville, FL 32224

Terri Shealy2217 Tuscaville RoadTallahassee, FL 32312

Ernst & Young LLP1400 Pillsbury CenterMinneapolis, MN 55402-1491Ph: (612) 343-1000

Hurricane ModelingAnalytical ConsultingServices:

Willis Faber North America, Inc.7900 Xerxes Avenue SouthSuite 2000Minneapolis, MN 55431Ph: (612) 820-0088

13

Financial Statements and Additional InformationFlorida Hurricane Catastrophe Fund(a Fund of the State of Florida)Years ended June 30, 2000 and 1999 with Report of Independent Auditors

CONTENTS

Report of Independent Auditors ............................................................................................................ 1

Audited Financial Statements

Balance Sheets ........................................................................................................................................... 2

Statements of Revenues, Expenditures, and Changes in Fund Balance ........................................... 3

Notes to Financial Statements ................................................................................................................. 4

Additional Information

Report of Independent Auditors on Other Financial Information ................................................... 10

Supplemental Revenues, Expenditures, and Claim Development Information ............................ 11

Report on Compliance and on Internal Control Over Financial Reporting Based on an Audit of

Financial Statements Performed in Accordance With Government Auditing Standards ............ 12

APPENDIX: AUDITED FINANCIAL STATEMENTS

Ernst & Young LLP is a member of Ernst & Young International, Ltd.

14

APPENDIX: AUDITED FINANCIAL STATEMENTS

Report of Independent Auditors

Trustees of the Florida State Board of AdministrationFlorida Hurricane Catastrophe Fund

We have audited the accompanying financial statements of the Florida Hurricane Catastrophe Fundof the State of Florida as of and for the years ended June 30, 2000 and 1999. These financial statementsare the responsibility of the Florida Hurricane Catastrophe Fund’s management. Our responsibility isto express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United Statesand the standards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States. Those standards require that we plan and perform the audit toobtain reasonable assurance about whether the financial statements are free of material misstatement. Anaudit includes examining, on a test basis, evidence supporting the amounts and disclosures in the finan-cial statements. An audit also includes assessing the accounting principles used and significant estimatesmade by management, as well as evaluating the overall financial statement presentation. We believe thatour audits provide a reasonable basis for our opinion.

As discussed in Note 1, the financial statements present only the Florida Hurricane Catastrophe Fundand are not intended to present fairly the financial position of the Florida State Board of Administrationand the results of its operations and cash flows of its proprietary fund types and nonexpendable trustfunds in conformity with accounting principles generally accepted in the United States.

In our opinion, the financial statements referred to above present fairly, in all material respects, thefinancial position of the Florida Hurricane Catastrophe Fund as of June 30, 2000 and 1999, and theresults of its operations for the years then ended in conformity with accounting principles generallyaccepted in the United States.

In accordance with Government Auditing Standards, we have also issued our report for the year endedJune 30, 2000, dated July 28, 2000, on our consideration of the Florida Hurricane Catastrophe Fund’sinternal control over financial reporting and our tests of its compliance with certain provisions oflaws, regulations, contracts, and grants.

July 28, 2000

1

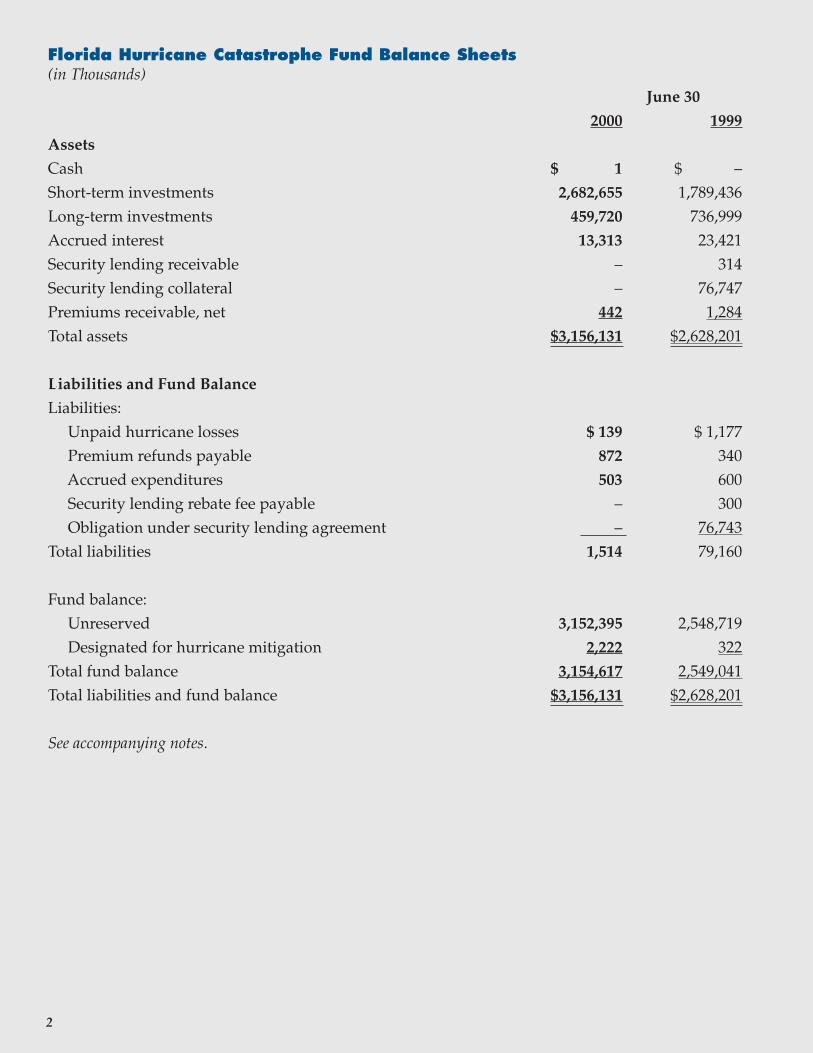

Florida Hurricane Catastrophe Fund Balance Sheets(in Thousands) June 30

2000 1999

Assets

Cash $ 1 $ –Short-term investments 2,682,655 1,789,436Long-term investments 459,720 736,999Accrued interest 13,313 23,421Security lending receivable – 314Security lending collateral – 76,747Premiums receivable, net 442 1,284Total assets $3,156,131 $2,628,201

Liabilities and Fund Balance

Liabilities: Unpaid hurricane losses $ 139 $ 1,177 Premium refunds payable 872 340 Accrued expenditures 503 600 Security lending rebate fee payable – 300 Obligation under security lending agreement – 76,743Total liabilities 1,514 79,160

Fund balance: Unreserved 3,152,395 2,548,719 Designated for hurricane mitigation 2,222 322Total fund balance 3,154,617 2,549,041Total liabilities and fund balance $3,156,131 $2,628,201

See accompanying notes.

2

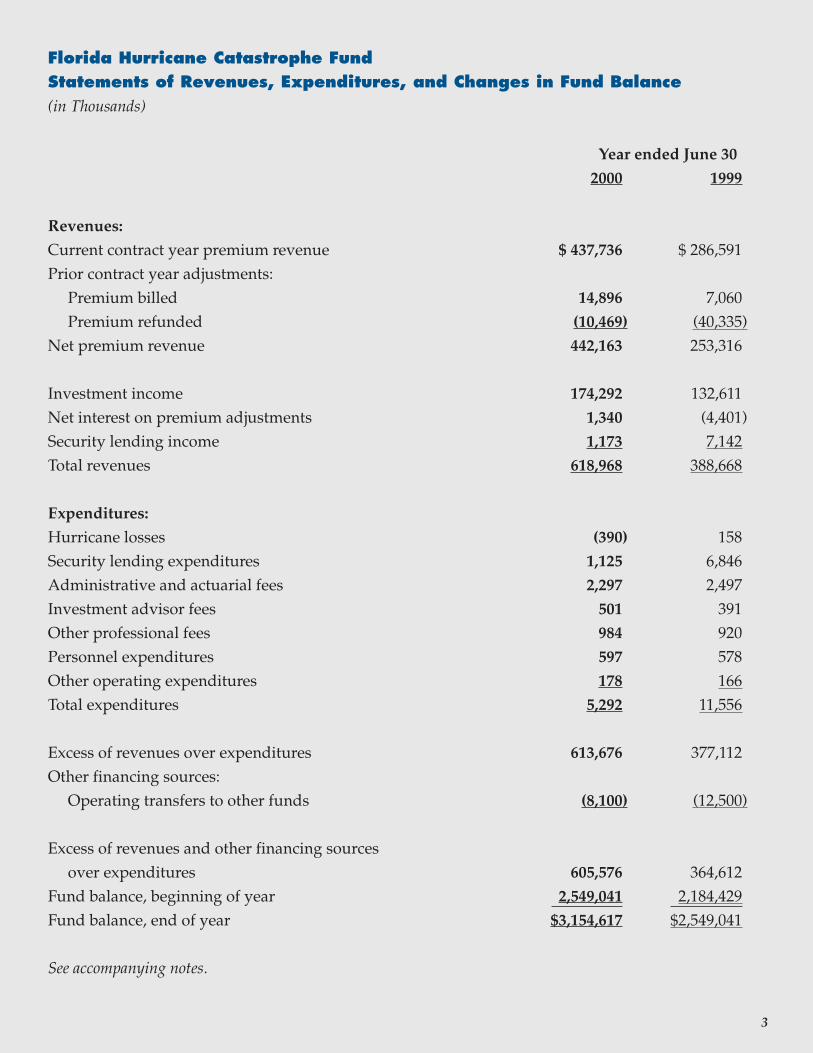

Florida Hurricane Catastrophe FundStatements of Revenues, Expenditures, and Changes in Fund Balance(in Thousands)

Year ended June 30

2000 1999

Revenues:

Current contract year premium revenue $ 437,736 $ 286,591Prior contract year adjustments: Premium billed 14,896 7,060 Premium refunded (10,469) (40,335)Net premium revenue 442,163 253,316

Investment income 174,292 132,611Net interest on premium adjustments 1,340 (4,401)Security lending income 1,173 7,142Total revenues 618,968 388,668

Expenditures:

Hurricane losses (390) 158Security lending expenditures 1,125 6,846Administrative and actuarial fees 2,297 2,497Investment advisor fees 501 391Other professional fees 984 920Personnel expenditures 597 578Other operating expenditures 178 166Total expenditures 5,292 11,556

Excess of revenues over expenditures 613,676 377,112Other financing sources: Operating transfers to other funds (8,100) (12,500)

Excess of revenues and other financing sources over expenditures 605,576 364,612Fund balance, beginning of year 2,549,041 2,184,429Fund balance, end of year $3,154,617 $2,549,041

See accompanying notes.

3

Florida Hurricane Catastrophe FundNotes to Financial StatementsJune 30, 2000

1. ORGANIZATIONBusinessThe Florida Hurricane Catastrophe Fund (the Fund), which was created in November 1993 during aspecial legislative session after Hurricane Andrew, provides catastrophic reinsurance coverage to allprimary insurers of habitational structures with wind/hurricane coverage in the State of Florida.Premiums are calculated for each of the approximately 300 insurers using rates developed based onhurricane modeling of the trended data from the prior year. The modeling takes into considerationfactors such as historical records of hurricane strength and landfall patterns, geographic location, typeof business, construction, and deductible. The Fund is administered by the Florida State Board ofAdministration (SBA), which has contracted administrative and actuarial services.Basis of PresentationThe Fund is a state trust fund and has been accounted for as an expendable trust fund of the State ofFlorida using the modified accrual basis of accounting. The financial statements presented hereinrelate solely to the financial position and results of operations of the Fund and are not intended topresent the financial position of the SBA or the results of its operations and cash flows. The Fundfollows GASB pronouncements and only FASB pronouncements issued before December 1, 1989, thatdo not conflict with or contradict GASB pronouncements.Limited Liability of the FundThe Fund’s obligation to participating insurers, in the event of a hurricane(s) that causes reimbursablelosses, is limited to the claims paying capacity of the Fund, which is the sum of the balance of theFund as of December 31 of a contract year, plus any reinsurance purchased by the Fund, plus theamount the SBA is able to raise through the issuance of revenue bonds. If revenue bonds are issuedunder authorization of Section 215.555(6) of the Florida Statutes, and the SBA determines that theamount of revenue produced under Section 215.555(5) of the Florida Statutes is insufficient to fundthe obligations, costs, and expenses of the Fund, including repayment of revenue bonds, the SBAshall direct the Florida Department of Insurance to levy an emergency assessment on each insurerwriting property and casualty business in this state. The Fund, therefore, has no risk that it will beunable to meet its contractual obligations to participating insurers because its obligation is limited toits ability to pay. Participating insurers are at risk as to whether the Fund would have sufficientclaims paying capacity in the event of a large or several moderate hurricanes in a given contract year.Factors that mitigate this risk include (1) the use of modeling software to analyze exposure datasubmitted by participating insurers, which have been trended and aggregated, in conjunction withhistorical hurricane data to develop actuarially determined rates for the reimbursement premiums;(2) a $3.2 billion aggregate industry retention level, which is adjusted to reflect the percentage growthin exposure to the Fund for covered policies since 1998; and (3) the ability of the Fund, through itsbonding authority, to generate up to $8.5 billion in capital.

4

If bonds are issued on behalf of the Fund, the State of Florida assumes no liability for the repaymentof the bonds. Additionally, the State of Florida has no legal responsibility to make any contribution tothe Fund should its obligations exceed available resources.Use of EstimatesThe preparation of financial statements in conformity with generally accepted accounting principlesrequires management to make estimates and assumptions that affect the reported amounts of assetsand liabilities at the date of the financial statements. Estimates also affect the reported amounts ofrevenues and expenditures during the reporting period. Although estimates are considered to befairly stated at the time that the estimates are made, actual results could differ from those estimates.

2. SIGNIFICANT ACCOUNTING POLICIESMeasurement FocusThe Fund uses the flow of current financial resources as a measurement focus. Under the modifiedaccrual basis of accounting, premium revenues are recognized when susceptible to accrual (i.e., whenthey are “measurable and available”). “Measurable” means the amount of the transaction can bedetermined and “available” means collectible within the current period or soon enough thereafter topay liabilities of the current period. Expenditures are recorded when the related fund liability isincurred.InvestmentsThe Fund invests all funds in relatively low-risk, highly liquid fixed-maturity securities. These in-vestments are recorded at fair value and the fair values are obtained from independent quoted mar-ket prices. No investments were recorded at amortized cost as of June 30, 2000 and 1999. The Fundconsiders all investments with maturity dates of less than one year to be short-term investments.Investments with maturity dates in excess of one year are included in long-term investments. Invest-ment advisory services are provided by the SBA.Security Lending ReceivableThe Fund, under authorization of Section 215.455 of the Florida Statutes, participated in a securitylending program in fiscal years 2000 and 1999. In a security lending program, a lender (the Fund)loans various securities to a borrower for collateral with a simultaneous agreement to return thecollateral for the same securities in the future. Collateral received from borrowers may be cash or U.S.government securities. Interest earned on short-term investments purchased with the cash collateralheld is recognized as revenue. Lending agent costs and borrower rebate fees are recognized as expen-ditures when incurred. As of June 30, 2000, the Fund had no security lending receivable. Due tocurrent market conditions, the FHCF is not actively participating in the security lending program.The Fund’s security lending program only accepts U.S. Treasuries, and these securities have had alower yield than other investment options.Premiums ReceivablePremiums receivable represent amounts from previous billings that have not yet been collected andare net of any allowances management has established to anticipate uncollectible billings.

5

Premiums PayablePremiums payable represent amounts due to participating insurers where provisional or estimatedpremium payments are in excess of amounts actually owed based upon the current exposure data.Also included are premium amounts received from companies pending exemption. These amountsare returned once an exemption is granted.Unpaid Losses LiabilityThe unpaid losses liability represents the estimated ultimate net cost of all reported, including paid, out-standing, and incurred but not reported, losses in excess of participating company retention levels throughJune 30. Such estimates are based on case-basis estimates of losses reported by June 30, estimates of lossesincurred but not reported, and a provision for loss adjustment expenses. Given the inherent degree ofvariability in any such estimates, the liabilities reported at June 30, 2000 and 1999, are a reasonable esti-mate of the Fund’s ultimate losses and loss adjustment costs to be incurred to discharge the Fund’s obliga-tions. Liabilities are continually reviewed and adjusted as participating insurers update their loss reportsto the Fund or new information becomes known; such adjustments are included in current operations.Current Contract Year Premium RevenuePremium revenue is recognized when billed. Coverage is provided to the participating insurers on acontract year basis which runs from June 1 to May 31. Premiums are billed in three installments withprovisional payments due August 1 and October 1, and a final payment due December 1.Current contract year premium revenue for the fiscal year ended 2000 includes the revenue of the July1999, September 1999, and November 1999 contract year billings. In 1999, the SBA moved the first billingdate of the three installments from May 1 to July 1. As a result, contract year premium revenue for thefiscal year ended 1999 included only the August 1998 and November 1998 contract year billings.Prior Contract Year AdjustmentsParticipating insurers remit premium to the Fund based upon current policyholder exposure informa-tion. When insurers provide updated or corrected exposure information, the Fund may bill andreceive additional premium relating to a prior contract year; the Fund may also be required to refundamounts to insurers relating to a prior contract year.Net Interest on Premium AdjustmentsParticipating insurers have the option of paying the billed provisional premium or estimating pre-mium for the July and September installments. If the estimated payments were too high, interest isreturned to the insurer on the overpayment. Likewise, if estimated premiums were underpaid, inter-est is charged to the insurer with the November installment. For the contract year ended May 31,2000, the interest rate was 5.46% for overpayments of premium and 8.46% for underestimated pay-ments. For the contract year ended May 31, 1999, the interest rate applied to overpayments of pre-mium was 5.73% and the interest rate charged for underestimated payments was 8.73%.Hurricane ExpendituresLosses include amounts paid during the fiscal year for hurricane losses from the current and priorcontract years that exceeded the participating insurers’ individual company retention levels. In addi-tion, a provision for future payments on hurricanes that occurred prior to the end of the fiscal year isincluded in losses.

6

Operating TransfersPursuant to Section 215.555(7)(c) of the Florida Statutes, beginning in fiscal year 1998, the Floridalegislature will appropriate from the Fund an amount no less than $10,000,000 and no more than 35%of the investment income from the prior fiscal year, providing that the actuarial soundness of theFund is not jeopardized, for the purpose of providing funding for governments, agencies, and educa-tional institutions to support programs intended to improve hurricane preparedness or reduce poten-tial losses in the event of a hurricane. In fiscal year 2000, $10,000,000 was appropriated from the Fundfor these purposes. $8,100,000 was transferred on September 28, 1999. The remaining $1,900,000of the fiscal year 2000 appropriation, and the $322,000 available for transfer from fiscal year 1999,have been designated in the June 30, 2000 ending fund balance for future transfer. In fiscal year 1999,approximately $12,500,000 was appropriated from the Fund for these purposes. The transfers weremade on October 27, 1998 and November 25, 1998. The remaining $322,000 of the $12,822,000 avail-able for transfer in fiscal year 1999 has been designated in the June 30, 1999 ending fund balance forfuture transfer.Income TaxesThe Fund is exempt from federal and state income taxes. This tax-exempt status was affirmed by aprivate letter ruling obtained from the Internal Revenue Service in November 1994.

3. INVESTMENTSThe Fund is authorized to invest in accordance with Section 215.47 of the Florida Statutes, whichincludes, but is not limited to, certificates of deposit, commercial paper, U.S. government agencynotes, U.S. Treasury bills, repurchase agreements, and variable rate notes that enhance the Fund’sinvestment income while maintaining liquidity.As of June 30, 2000 and 1999, the Fund’s deposits are entirely insured or collateralized with securitiesheld by the Fund or by its agent in the SBA’s name. The Fund’s investments are classified by level ofrisk assumed by the Fund at year-end. Custodial credit risk is defined as the risk that the Fund maynot recover securities held by another party. The level of custodial credit risk assumed by the Fund iscategorized as follows:Category A includes investments that are insured or registered, or securities held by the Fund or itsagent in the Fund’s name. Category B includes uninsured and unregistered investments for whichsecurities are held by the counterparty’s trust department or agent in the Fund’s name. Category Cincludes uninsured and unregistered investments for which securities are held by the counterparty orby its trust department or agent, but not in the Fund’s name.

7

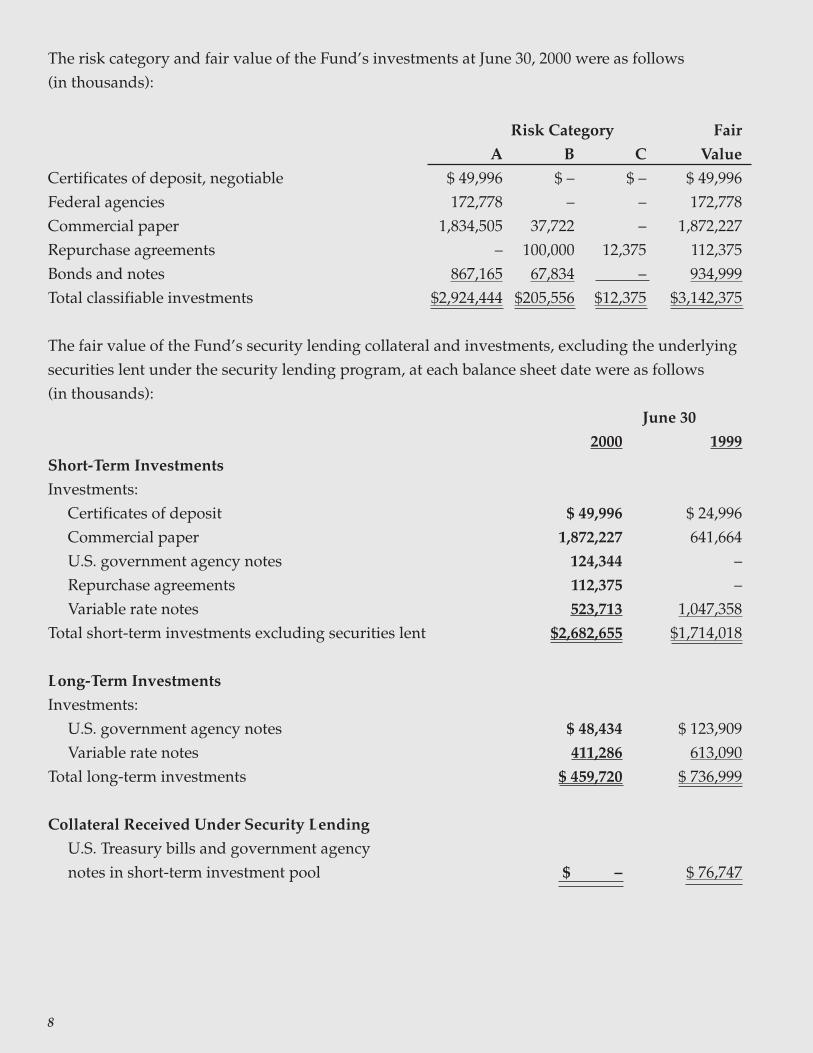

The risk category and fair value of the Fund’s investments at June 30, 2000 were as follows(in thousands):

Risk Category Fair

A B C Value

Certificates of deposit, negotiable $ 49,996 $ – $ – $ 49,996Federal agencies 172,778 – – 172,778Commercial paper 1,834,505 37,722 – 1,872,227Repurchase agreements – 100,000 12,375 112,375Bonds and notes 867,165 67,834 – 934,999Total classifiable investments $2,924,444 $205,556 $12,375 $3,142,375

The fair value of the Fund’s security lending collateral and investments, excluding the underlyingsecurities lent under the security lending program, at each balance sheet date were as follows(in thousands): June 30

2000 1999

Short-Term Investments

Investments: Certificates of deposit $ 49,996 $ 24,996 Commercial paper 1,872,227 641,664 U.S. government agency notes 124,344 – Repurchase agreements 112,375 – Variable rate notes 523,713 1,047,358Total short-term investments excluding securities lent $2,682,655 $1,714,018

Long-Term Investments

Investments: U.S. government agency notes $ 48,434 $ 123,909 Variable rate notes 411,286 613,090Total long-term investments $ 459,720 $ 736,999

Collateral Received Under Security Lending

U.S. Treasury bills and government agency notes in short-term investment pool $ – $ 76,747

8

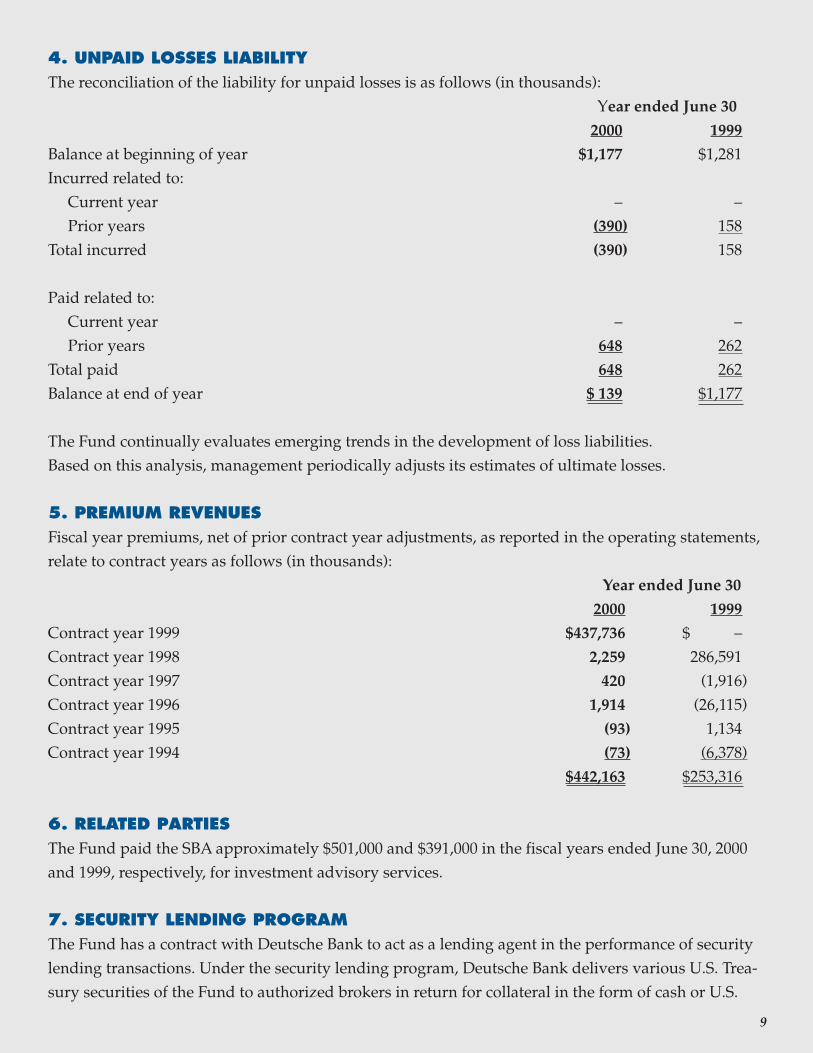

4. UNPAID LOSSES LIABILITYThe reconciliation of the liability for unpaid losses is as follows (in thousands): Year ended June 30

2000 1999

Balance at beginning of year $1,177 $1,281Incurred related to: Current year – – Prior years (390) 158Total incurred (390) 158

Paid related to: Current year – – Prior years 648 262Total paid 648 262Balance at end of year $ 139 $1,177

The Fund continually evaluates emerging trends in the development of loss liabilities.Based on this analysis, management periodically adjusts its estimates of ultimate losses.

5. PREMIUM REVENUESFiscal year premiums, net of prior contract year adjustments, as reported in the operating statements,relate to contract years as follows (in thousands): Year ended June 30

2000 1999

Contract year 1999 $437,736 $ –Contract year 1998 2,259 286,591Contract year 1997 420 (1,916)Contract year 1996 1,914 (26,115)Contract year 1995 (93) 1,134Contract year 1994 (73) (6,378)

$442,163 $253,316

6. RELATED PARTIESThe Fund paid the SBA approximately $501,000 and $391,000 in the fiscal years ended June 30, 2000and 1999, respectively, for investment advisory services.

7. SECURITY LENDING PROGRAMThe Fund has a contract with Deutsche Bank to act as a lending agent in the performance of securitylending transactions. Under the security lending program, Deutsche Bank delivers various U.S. Trea-sury securities of the Fund to authorized brokers in return for collateral in the form of cash or U.S.

9

government securities. Borrowers under the transactions must be approved by Deutsche Bank’scredit department and Deutsche Bank is required to indemnify the Fund if the borrower fails toreturn the underlying securities or fails to pay income distributions on them. The Fund is contractu-ally limited from pledging or selling collateral represented by U.S. Treasury securities except in theevent of borrower default. No violations of legal or contractual provisions occurred and no losseswere incurred due to borrower or lending agent defaults in 2000. As of June 30, 2000, the Fund had nosecurity lending activity.

8. YEAR 2000 (UNAUDITED)The Year 2000 issue is the result of shortcomings in many electronic data processing systems andother electronic equipment that had the potential to adversely affect the SBA’s operations. No signifi-cant Year 2000 problems were encountered with respect to the SBA’s internal computer hardware andsoftware, key business partners and vendors, and insurance policy exposure. Additionally, the SBAdid not encounter any disruption in the financial services it provides to its constituency.

ADDITIONAL INFORMATION

Report of Independent Auditors on Other Financial Information

Trustees of the Florida State Board of AdministrationFlorida Hurricane Catastrophe Fund

Our audits were conducted for the purpose of forming an opinion on the financial statements takenas a whole. The accompanying supplemental revenues, expenditures, and claim development infor-mation of the Florida Hurricane Catastrophe Fund (the Fund) is presented for purposes of additionalanalysis and is not a required part of the Fund’s financial statements. Such information has beensubjected to the auditing procedures applied in our audit of the Fund’s financial statements and, inour opinion, is fairly stated, in all material respects, in relation to the Fund’s financial statementstaken as a whole.

July 28, 2000

10

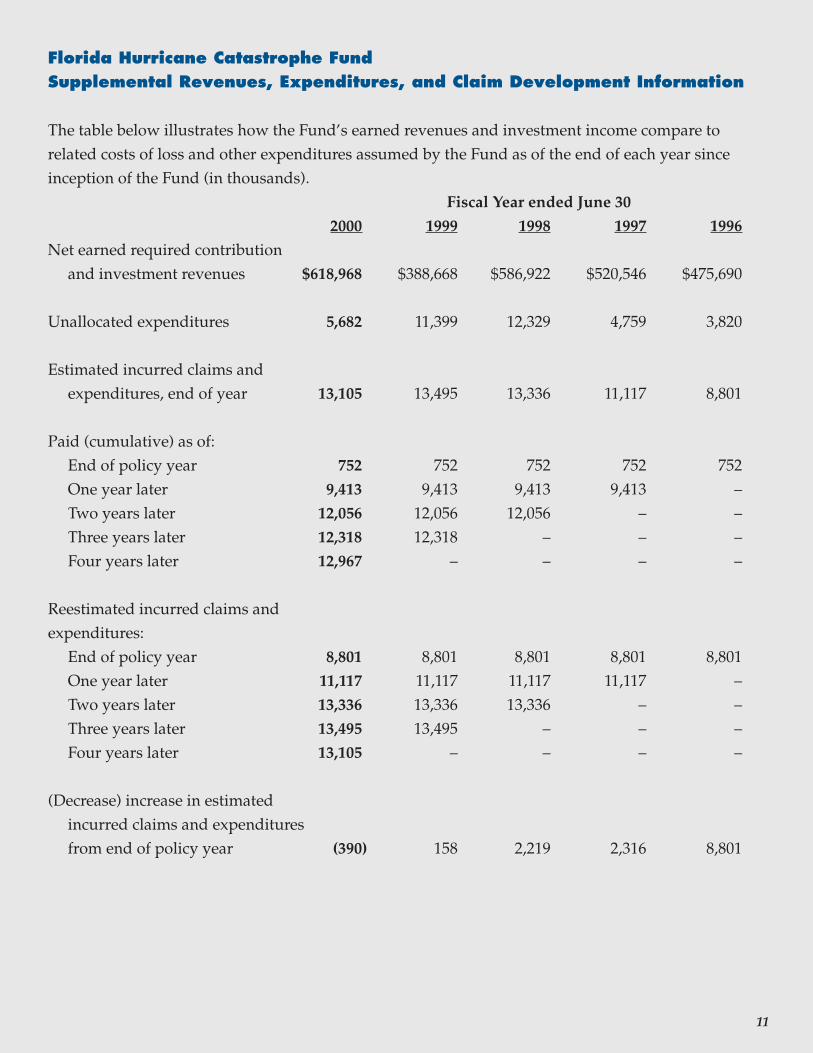

Florida Hurricane Catastrophe FundSupplemental Revenues, Expenditures, and Claim Development Information

The table below illustrates how the Fund’s earned revenues and investment income compare torelated costs of loss and other expenditures assumed by the Fund as of the end of each year sinceinception of the Fund (in thousands). Fiscal Year ended June 30

2000 1999 1998 1997 1996

Net earned required contribution and investment revenues $618,968 $388,668 $586,922 $520,546 $475,690

Unallocated expenditures 5,682 11,399 12,329 4,759 3,820

Estimated incurred claims and expenditures, end of year 13,105 13,495 13,336 11,117 8,801

Paid (cumulative) as of: End of policy year 752 752 752 752 752 One year later 9,413 9,413 9,413 9,413 – Two years later 12,056 12,056 12,056 – – Three years later 12,318 12,318 – – – Four years later 12,967 – – – –

Reestimated incurred claims andexpenditures: End of policy year 8,801 8,801 8,801 8,801 8,801 One year later 11,117 11,117 11,117 11,117 – Two years later 13,336 13,336 13,336 – – Three years later 13,495 13,495 – – – Four years later 13,105 – – – –

(Decrease) increase in estimated incurred claims and expenditures from end of policy year (390) 158 2,219 2,316 8,801

11

Report on Compliance and on Internal Control Over Financial ReportingBased on an Audit of Financial Statements Performed in Accordance WithGovernment Auditing Standards

Trustees of the Florida State Board of AdministrationFlorida Hurricane Catastrophe Fund

We have audited the financial statements of the Florida Hurricane Catastrophe Fund (the Fund) asof and for the year ended June 30, 2000, and have issued our report thereon dated July 28, 2000. Weconducted our audit in accordance with generally accepted auditing standards and the standardsapplicable to financial audits contained in Government Auditing Standards, issued by the ComptrollerGeneral of the United States.

Compliance

As part of obtaining reasonable assurance about whether the Fund’s financial statements are free ofmaterial misstatement, we performed tests of its compliance with certain provisions of laws, regula-tions, contracts, and grants, noncompliance with which could have a direct and material effect on thedetermination of financial statement amounts. However, providing an opinion on compliance withthose provisions was not an objective of our audit and, accordingly, we do not express such opinion.The results of our tests disclosed no instances of noncompliance that are required to be reportedunder Government Auditing Standards.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the Fund’s internal control over financial reportingin order to determine our auditing procedures for the purpose of expressing our opinion on the financialstatements and not to provide assurance on the internal control over financial reporting. Our consider-ation of the internal control over financial reporting would not necessarily disclose all matters in theinternal control over financial reporting that might be material weaknesses. A material weakness is acondition in which the design or operation of one or more of the internal control components does notreduce to a relatively low level the risk that misstatements in amounts that would be material in relation tothe financial statements being audited may occur and not be detected within a timely period by employ-ees in the normal course of performing their assigned functions. We noted no matters involving the inter-nal control over financial reporting and its operation that we consider to be material weaknesses. Thisreport, Report on Compliance and on Internal Control Over Financial Reporting Based on an Audit ofFinancial Statements Performed in Accordance With Governmental Auditing Standards, is intended solelyfor the information and use of the Florida Auditor General and the management of the Florida State Boardof Administration, and is not intended to be and should not be used by anyone other than these specifiedparties. However, this report is a matter of public record and its distribution is not limited.

July 28, 2000

12

PHOTO CREDITS:Florida Department of Commerce

Florida Department of Environmental ProtectionGoddard Space Institute/NASA

National Oceanic and Atmospheric Administration

FLORIDA HURRICANE CATASTROPHE FUND

FLORIDA STATE BOARD OF ADMINISTRATION

HERMITAGE CENTRE, SUITE 1001801 HERMITAGE BOULEVARD

TALLAHASSEE, FL 32308850.413.1349 FAX 850.413.1344

http://www.fsba.state.fl.us/fhcf/