Embed Size (px)

Citation preview

RETIREMENT PLANNING GUIDEGetting you on the right track

Table of ContentsWhy is a retirement plan important? 2

How much will you need? 4

How can your retirement plan help? 6

Where should you invest? 8

How can you developan asset allocation strategy? 10

How can you stay involved? 12

GOLDMAN SACHS ASSET MANAGEMENT 1

Retirement

The word means different things to different people. For

some, it conjures up thoughts of travel, relaxation and

recreational activities. For others, it means free time to start

a new hobby, volunteer or take continuing education

classes. No matter what your vision of retirement, there is

one question that many people face:

“Will I have enough money to last throughout myretirement?”

In this guide, we provide a framework to help you develop a

personal retirement plan — one that can help you answer

the question above and many others. We’ll also explain how

your company’s retirement savings plan can help you reach

your retirement goals. By the time you complete this guide,

you should have a clear understanding of the challenges

you’ll face in saving for retirement and an action plan for

meeting them.

1Why is a retirement planimportant?

GOLDMAN SACHS ASSET MANAGEMENT2

2

* Source: Social Security Web Site, www.ssa.gov, Social Security Bulletin vol 68 No 2, 2008

Savings method(30 year time horizon)

This hypothetical example assumes annual contributions of $3,000 at an annual 8% rate of return and does not account for taxes.It is for illustrative purposes only and is not indicative of any actual investment. Your return and principal value may be more orless than your original investment.

THE BENEFITS OF STARTING EARLY

By starting early, youmaximize the power ofcompounding.

Starting Early Procrastinating

Invest $3,000 annually for Do not invest for the first 8 yearsthe first 8 yearsNo additional contributions Invest $3,000 annually for the

next 22 years

Total amount saved $3,000 x 8 years = $24,000 $3,000 x 22 years = $66,000

Value at the end of 30 years

% of end value from savings

$148,268$218,768

11% 45%

Investing enough money to make your retirement dreams a reality doesn’thappen overnight. It takes years of disciplined saving, perseverance and along-term investment plan. With a plan, you can determine how much moneyyou may need throughout retirement and focus on how to achieve yourfinancial goals.

Helps you control your financial future

When it comes to retirement planning, several factors are out of your controlincluding taxes, inflation and the performance of financial markets. But, thereare many elements that you can take charge of, including:

n When to start saving for retirement

n How much to save each year

n Where to invest your savings

n How to diversify your assets

Deciding on the answers to these questions will help you make a seriouscommitment to your retirement future.

Provides you with a disciplined and consistent savings approach

Some people postpone retirement planning because they believe Social Securitywill be enough. However, Social Security is only expected to replace about40% of income for the average wage earner.* The rest will come frompersonal savings — including the money you save in your company'sretirement plan.

The more years you have until retirement, the easier it can be to procrastinate.With housing costs, saving for children’s education expenses and vacations,putting money aside for retirement isn’t a priority for many people. But,starting to save early is one of the most important factors in successfulretirement planning. Consider the following example:

1-Year Per iods 5-Year Per iods 10-Year Per iods 15-Year Per iods

75% 75% 82% 100%

Allows you to remain invested in all market environments

Investing over a longer period of time should also help you ride out theinevitable fluctuations that take place in the financial markets.

Staying invested for thelong term may reduceinvestment volatilityover time.

THE BENEFITS OF LONG-TERM INVESTING

The Percentage of Time Stocks Posted a Positive Return Over Rolling Time Periods From 1989-2009

Source: Goldman Sachs Asset Management.

The returns for Time Tested Principles 2 and 3 are based on the S&P 500 Index. The S&P 500 Index is the Standard & Poor’s 500Composite Stock Prices Index of 500 stocks, an unmanaged index of common stock prices. The Index figures do not reflect anydeduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. Past performance is notindicative of future results.

And staying invested can prove beneficial to your portfolio’s overall outcome.

Invested All5,049 Days

Minus 70 Best Days

Minus40 Best Days

Minus10 Best Days

8.20%

4.52%

-1.80%

-6.52%

Average Annual Total Returns of the S&P 500 Index 1986-2006

Source: Goldman Sachs Asset Management. Calculation is based on 5,049 days, excluding weekends and holidays.

2How much willyou need?

GOLDMAN SACHS ASSET MANAGEMENT4

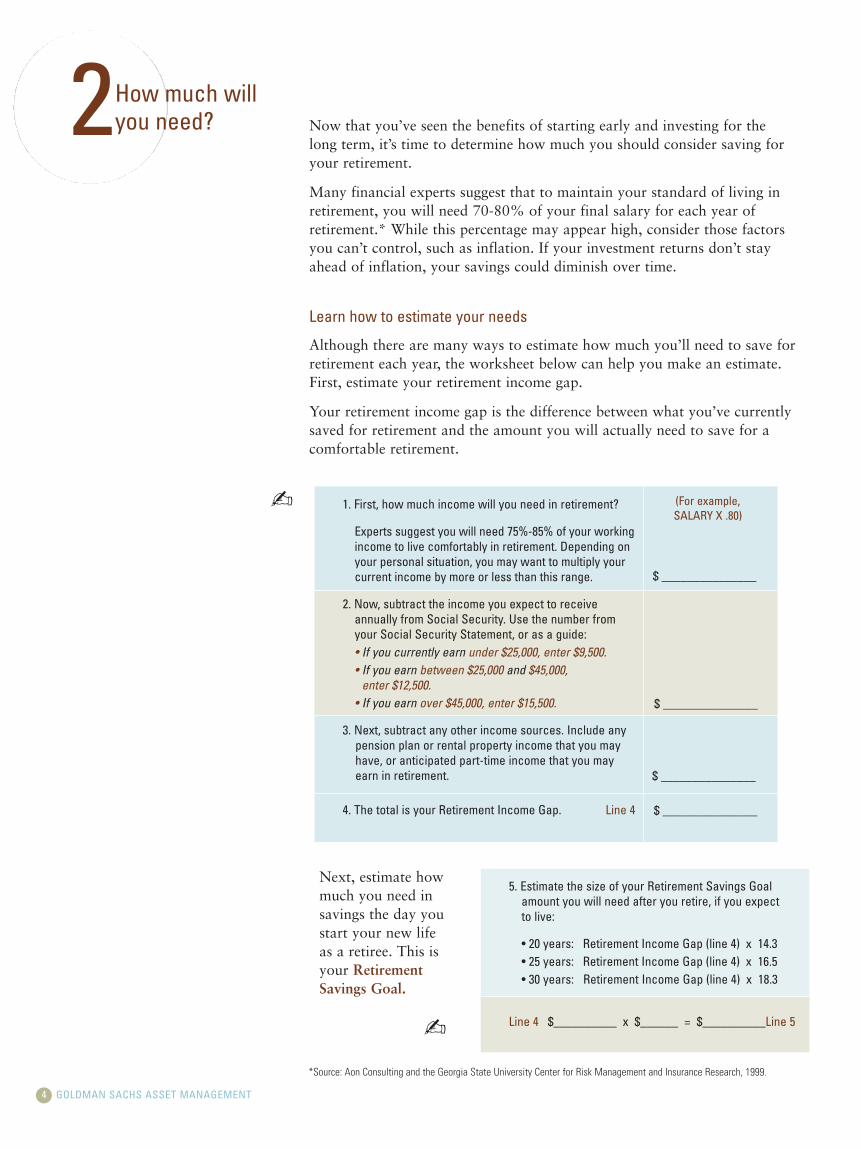

Now that you’ve seen the benefits of starting early and investing for the long term, it’s time to determine how much you should consider saving foryour retirement.

Many financial experts suggest that to maintain your standard of living inretirement, you will need 70-80% of your final salary for each year ofretirement.* While this percentage may appear high, consider those factorsyou can’t control, such as inflation. If your investment returns don’t stayahead of inflation, your savings could diminish over time.

Learn how to estimate your needs

Although there are many ways to estimate how much you’ll need to save forretirement each year, the worksheet below can help you make an estimate.First, estimate your retirement income gap.

Your retirement income gap is the difference between what you’ve currently saved for retirement and the amount you will actually need to save for acomfortable retirement.

1. First, how much income will you need in retirement?

Experts suggest you will need 75%-85% of your workingincome to live comfortably in retirement. Depending onyour personal situation, you may want to multiply yourcurrent income by more or less than this range.

2. Now, subtract the income you expect to receiveannually from Social Security. Use the number fromyour Social Security Statement, or as a guide:• If you currently earn under $25,000, enter $9,500.• If you earn between $25,000 and $45,000,

enter $12,500.• If you earn over $45,000, enter $15,500.

3. Next, subtract any other income sources. Include anypension plan or rental property income that you mayhave, or anticipated part-time income that you mayearn in retirement.

4. The total is your Retirement Income Gap. Line 4

- (For example, SALARY X .80)

$ _______________

$ _______________

$ _______________

$ _______________

Next, estimate howmuch you need insavings the day youstart your new lifeas a retiree. This isyour RetirementSavings Goal.

5. Estimate the size of your Retirement Savings Goalamount you will need after you retire, if you expect to live:

• 20 years: Retirement Income Gap (line 4) x 14.3• 25 years: Retirement Income Gap (line 4) x 16.5• 30 years: Retirement Income Gap (line 4) x 18.3

Line 4 $__________ x $______ = $__________Line 5-

*Source: Aon Consulting and the Georgia State University Center for Risk Management and Insurance Research, 1999.

GOLDMAN SACHS ASSET MANAGEMENT 5

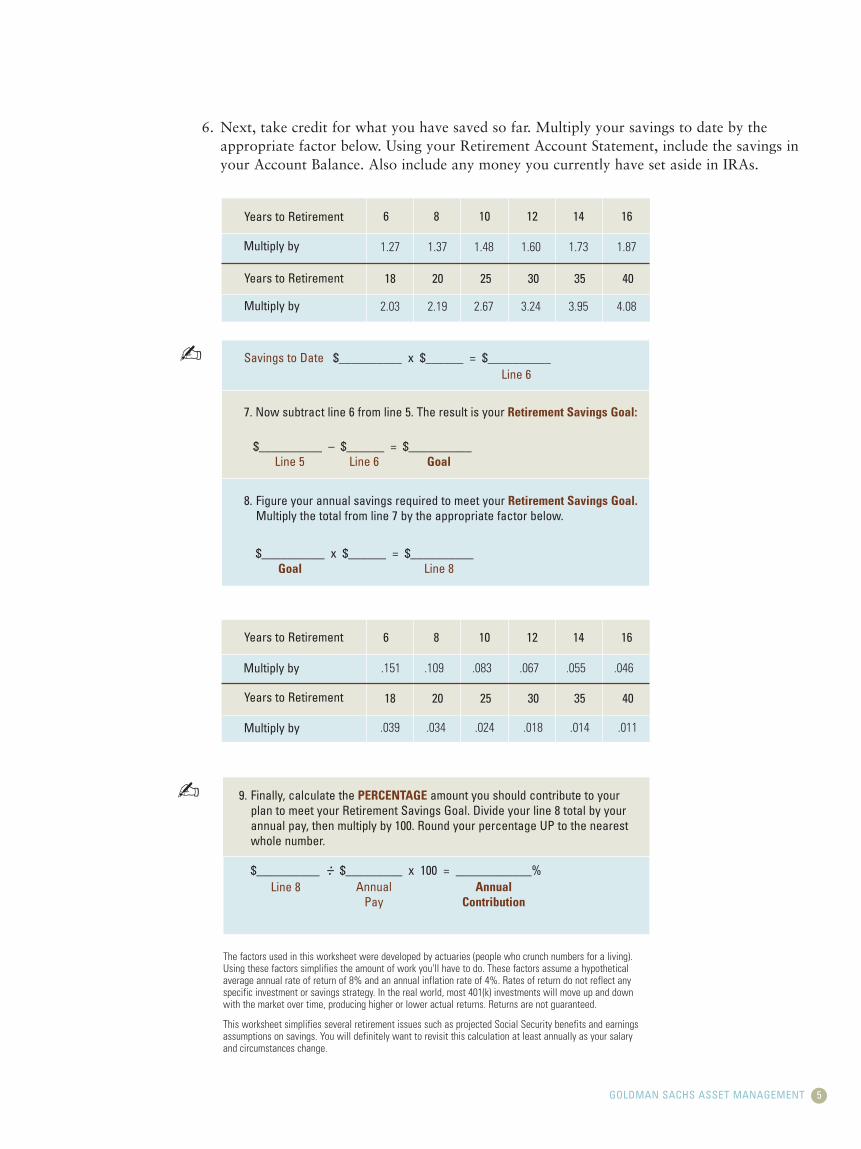

6. Next, take credit for what you have saved so far. Multiply your savings to date by theappropriate factor below. Using your Retirement Account Statement, include the savings inyour Account Balance. Also include any money you currently have set aside in IRAs.

Years to Retirement

Multiply by 1.27 1.37 1.48 1.60 1.73 1.87

6 8 10 12 14 16

Multiply by 2.03 2.19 2.67 3.24 3.95 4.08

18 20 25 30 35 40Years to Retirement

Savings to Date $__________ x $______ = $__________

7. Now subtract line 6 from line 5. The result is your Retirement Savings Goal:

$__________ – $______ = $__________

8. Figure your annual savings required to meet your Retirement Savings Goal.Multiply the total from line 7 by the appropriate factor below.

Line 6

Line 6Line 5 Goal

Years to Retirement

Multiply by .151 .109 .083 .067 .055 .046

6 8 10 12 14 16

Multiply by .039 .034 .024 .018 .014 .011

18 20 25 30 35 40Years to Retirement

-

$__________ x $______ = $__________Goal Line 8

- 9. Finally, calculate the PERCENTAGE amount you should contribute to yourplan to meet your Retirement Savings Goal. Divide your line 8 total by yourannual pay, then multiply by 100. Round your percentage UP to the nearestwhole number.

$__________ ÷ $_________ x 100 = ____________%AnnualPay

Line 8 Annual Contribution

The factors used in this worksheet were developed by actuaries (people who crunch numbers for a living).Using these factors simplifies the amount of work you'll have to do. These factors assume a hypotheticalaverage annual rate of return of 8% and an annual inflation rate of 4%. Rates of return do not reflect anyspecific investment or savings strategy. In the real world, most 401(k) investments will move up and downwith the market over time, producing higher or lower actual returns. Returns are not guaranteed.

This worksheet simplifies several retirement issues such as projected Social Security benefits and earningsassumptions on savings. You will definitely want to revisit this calculation at least annually as your salaryand circumstances change.

3Howcan yourretirement plan help?

GOLDMAN SACHS ASSET MANAGEMENT6

With your estimated savings goal completed, the next step is to determinewhere that money will come from. Fortunately, your company’s retirement plancan help. The plan offers a number of important benefits that can help youmeet your retirement goals.

Every dollar goes to work for you immediately

Contributions to your company’s retirement plan are made on a pre-tax basis.Simply put, that means that 100% of every dollar you contribute is invested inyour account — without first being subject to federal and, in most cases, statetaxes. In contrast, consider your non-plan retirement savings. If you’re in the28% tax bracket, that dollar is whittled down to 72 cents before it can beinvested. Over time, the difference between the $1.00 and 72 cents can besignificant.

Taxes are deferred so you can increase your savings

Contributions to your retirement plan account come out of your paycheckbefore they get taxed. This helps to lower the taxes that are deducted from eachpaycheck. Consider the hypothetical example below:

Your company’sretirement plan can helpyou lower taxes andincrease your savings.

Savings potentially grow faster through compounding

One of the most important investing concepts is the power of compounding.This benefit is even more valuable when your money compounds tax-free.And, when you save through your plan, all the earnings from your investmentsare automatically reinvested into your account. These earnings are not taxeduntil you make a withdrawal. When that time comes, you could be in a lowertax bracket than you were during your working years.

THE BENEFITS OF TAX-DEFERRAL

** Assumes a 28% income tax rate. Does not take into account any state or local taxes.

Suzanne Melissa

Invests Before Taxes Invests After Taxes

Monthly Income $3,000 $3,000

Plan Contribution $200 0

Taxable Income $2,800 $3,000

Income Tax** -$784 -$840

After Tax Income $2,016 $2,160

After Tax Investment 0 $200

Net Take-Home Pay $2,016 $1,960

GOLDMAN SACHS ASSET MANAGEMENT 7

Investment decisions are in your control

Your company’s retirement plan offers a variety of investment vehicles tochoose from, and you have complete control in deciding how to invest yourcontributions. In addition, your plan allows you to easily change the way youallocate your investment dollars as your needs change. And, since your planassets are invested on a tax-deferred basis, there are no tax consequences whenyou transfer between investments in the plan.

Contributions are automatic

Once you sign up for your retirement plan, you don’t have to remember tomake contributions each pay period — it’s all done for you. Your employerhandles the paperwork and makes sure contributions are deducted from yourpaycheck. That way, you can take advantage of all the benefits of investing inyour plan automatically.

Every little bit counts

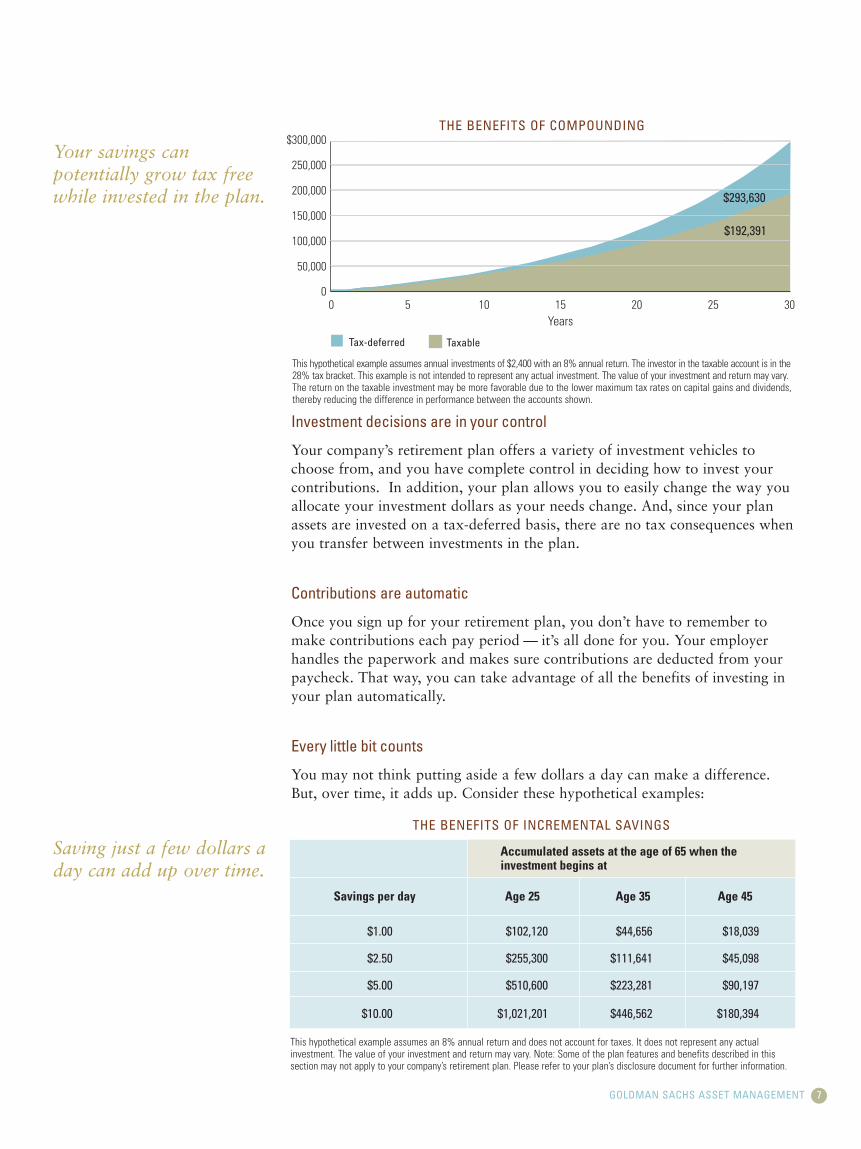

You may not think putting aside a few dollars a day can make a difference. But, over time, it adds up. Consider these hypothetical examples:

Saving just a few dollars a day can add up over time.

This hypothetical example assumes an 8% annual return and does not account for taxes. It does not represent any actualinvestment. The value of your investment and return may vary. Note: Some of the plan features and benefits described in thissection may not apply to your company’s retirement plan. Please refer to your plan’s disclosure document for further information.

Accumulated assets at the age of 65 when the investment begins at

Savings per day Age 25 Age 35 Age 45

$1.00 $102,120 $44,656 $18,039

$2.50 $255,300 $111,641 $45,098

$5.00 $510,600 $223,281 $90,197

$10.00 $1,021,201 $446,562 $180,394

THE BENEFITS OF COMPOUNDING

THE BENEFITS OF INCREMENTAL SAVINGS

This hypothetical example assumes annual investments of $2,400 with an 8% annual return. The investor in the taxable account is in the28% tax bracket. This example is not intended to represent any actual investment. The value of your investment and return may vary. The return on the taxable investment may be more favorable due to the lower maximum tax rates on capital gains and dividends,thereby reducing the difference in performance between the accounts shown.

Your savings canpotentially grow tax freewhile invested in the plan.

3010 15Years

20 2550

$293,630

$192,391

0

50,000

100,000

150,000

200,000

250,000

$300,000

Tax-deferred Taxable

GOLDMAN SACHS ASSET MANAGEMENT8

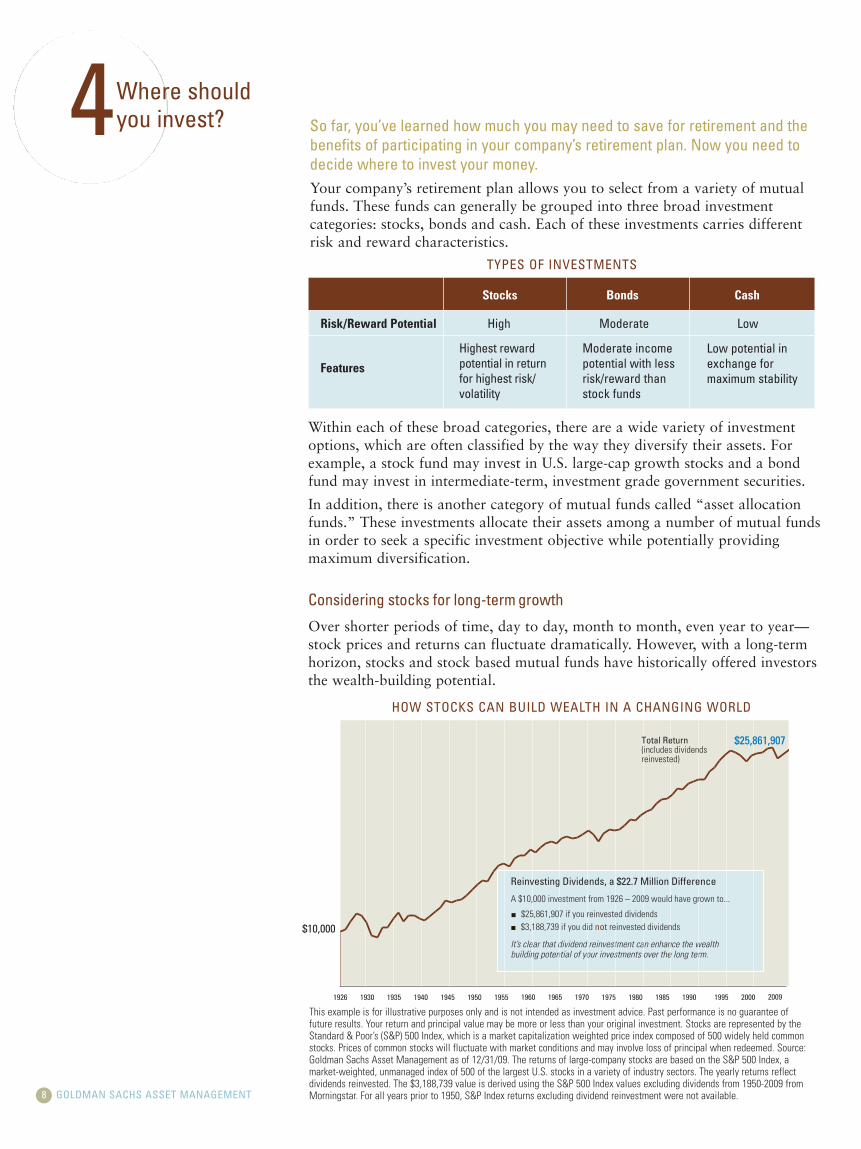

So far, you’ve learned how much you may need to save for retirement and thebenefits of participating in your company’s retirement plan. Now you need todecide where to invest your money.Your company’s retirement plan allows you to select from a variety of mutualfunds. These funds can generally be grouped into three broad investmentcategories: stocks, bonds and cash. Each of these investments carries differentrisk and reward characteristics.

TYPES OF INVESTMENTS

Stocks Bonds Cash

Risk/Reward Potential High Moderate Low

Features

Within each of these broad categories, there are a wide variety of investmentoptions, which are often classified by the way they diversify their assets. Forexample, a stock fund may invest in U.S. large-cap growth stocks and a bondfund may invest in intermediate-term, investment grade government securities.

In addition, there is another category of mutual funds called “asset allocationfunds.” These investments allocate their assets among a number of mutual fundsin order to seek a specific investment objective while potentially providingmaximum diversification.

Considering stocks for long-termgrowth

Over shorter periods of time, day to day, month to month, even year to year—stock prices and returns can fluctuate dramatically. However, with a long-termhorizon, stocks and stock based mutual funds have historically offered investorsthe wealth-building potential.

Highest rewardpotential in returnfor highest risk/volatility

Moderate incomepotential with lessrisk/reward thanstock funds

Low potential inexchange for maximum stability

This example is for illustrative purposes only and is not intended as investment advice. Past performance is no guarantee offuture results. Your return and principal value may be more or less than your original investment. Stocks are represented by theStandard & Poor’s (S&P) 500 Index, which is a market capitalization weighted price index composed of 500 widely held commonstocks. Prices of common stocks will fluctuate with market conditions and may involve loss of principal when redeemed. Source:Goldman Sachs Asset Management as of 12/31/09. The returns of large-company stocks are based on the S&P 500 Index, amarket-weighted, unmanaged index of 500 of the largest U.S. stocks in a variety of industry sectors. The yearly returns reflectdividends reinvested. The $3,188,739 value is derived using the S&P 500 Index values excluding dividends from 1950-2009 fromMorningstar. For all years prior to 1950, S&P Index returns excluding dividend reinvestment were not available.

2009

$10,000

20001970 1980197519601955 19951965 1985 1990 195019451940193519301926

It’s clear that dividend reinvestment can enhance the wealth building potential of your investments over the long term.

$25,861,907$25,861,907Total Return (includes dividends reinvested)

Reinvesting Dividends, a $22.7 Million Difference

A $10,000 investment from 1926 – 2009 would have grown to...

J $25,861,907 if you reinvested dividendsJ $3,188,739 if you did not reinvested dividends

HOW STOCKS CAN BUILD WEALTH IN A CHANGING WORLD

4Where shouldyou invest?

-50

-40

-30

-20

-10

0

10

20

30

40

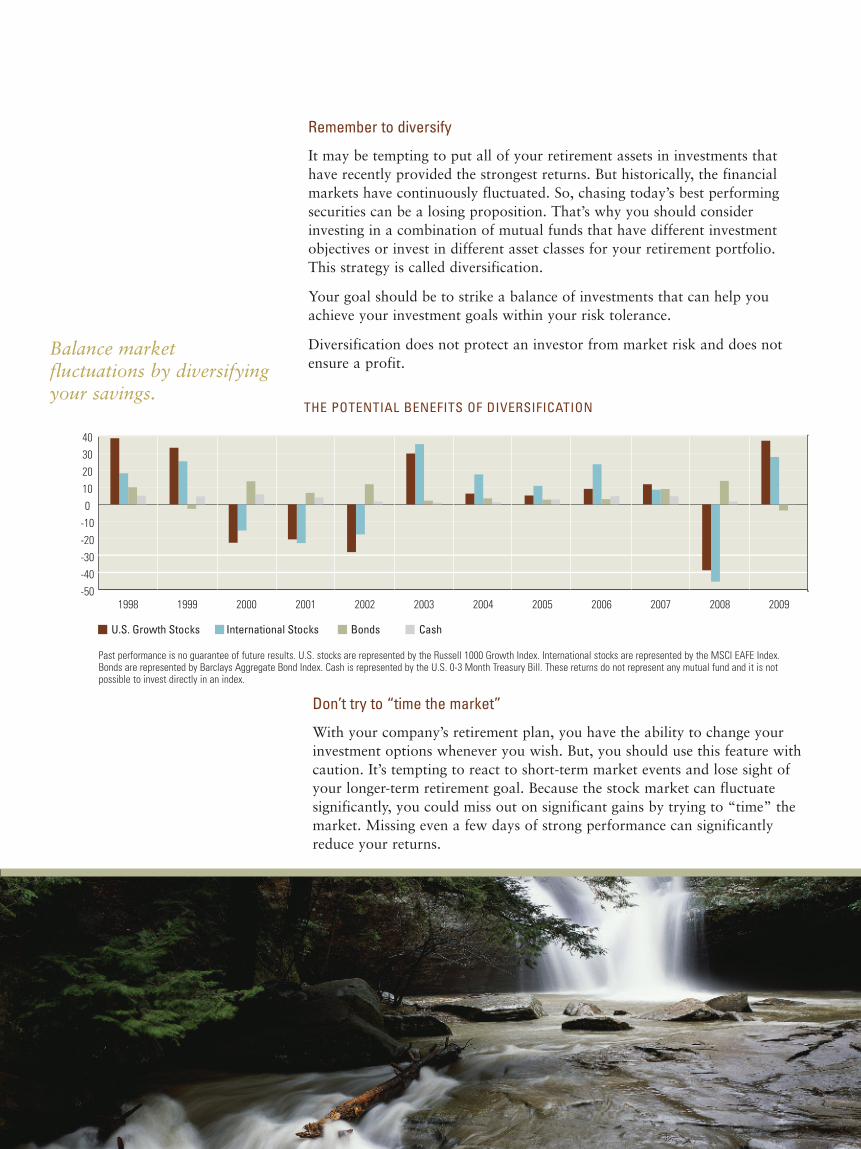

200920082007200620052004200320022001200019991998

U.S. Growth Stocks International Stocks Bonds Cash

Remember to diversify

It may be tempting to put all of your retirement assets in investments thathave recently provided the strongest returns. But historically, the financialmarkets have continuously fluctuated. So, chasing today’s best performingsecurities can be a losing proposition. That’s why you should considerinvesting in a combination of mutual funds that have different investmentobjectives or invest in different asset classes for your retirement portfolio.This strategy is called diversification.

Your goal should be to strike a balance of investments that can help youachieve your investment goals within your risk tolerance.

Diversification does not protect an investor from market risk and does notensure a profit.

Don’t try to “time the market”

With your company’s retirement plan, you have the ability to change yourinvestment options whenever you wish. But, you should use this feature withcaution. It’s tempting to react to short-term market events and lose sight ofyour longer-term retirement goal. Because the stock market can fluctuatesignificantly, you could miss out on significant gains by trying to “time” themarket. Missing even a few days of strong performance can significantlyreduce your returns.

THE POTENTIAL BENEFITS OF DIVERSIFICATION

Past performance is no guarantee of future results. U.S. stocks are represented by the Russell 1000 Growth Index. International stocks are represented by the MSCI EAFE Index.Bonds are represented by Barclays Aggregate Bond Index. Cash is represented by the U.S. 0-3 Month Treasury Bill. These returns do not represent any mutual fund and it is notpossible to invest directly in an index.

Balance marketfluctuations by diversifyingyour savings.

GOLDMAN SACHS ASSET MANAGEMENT10

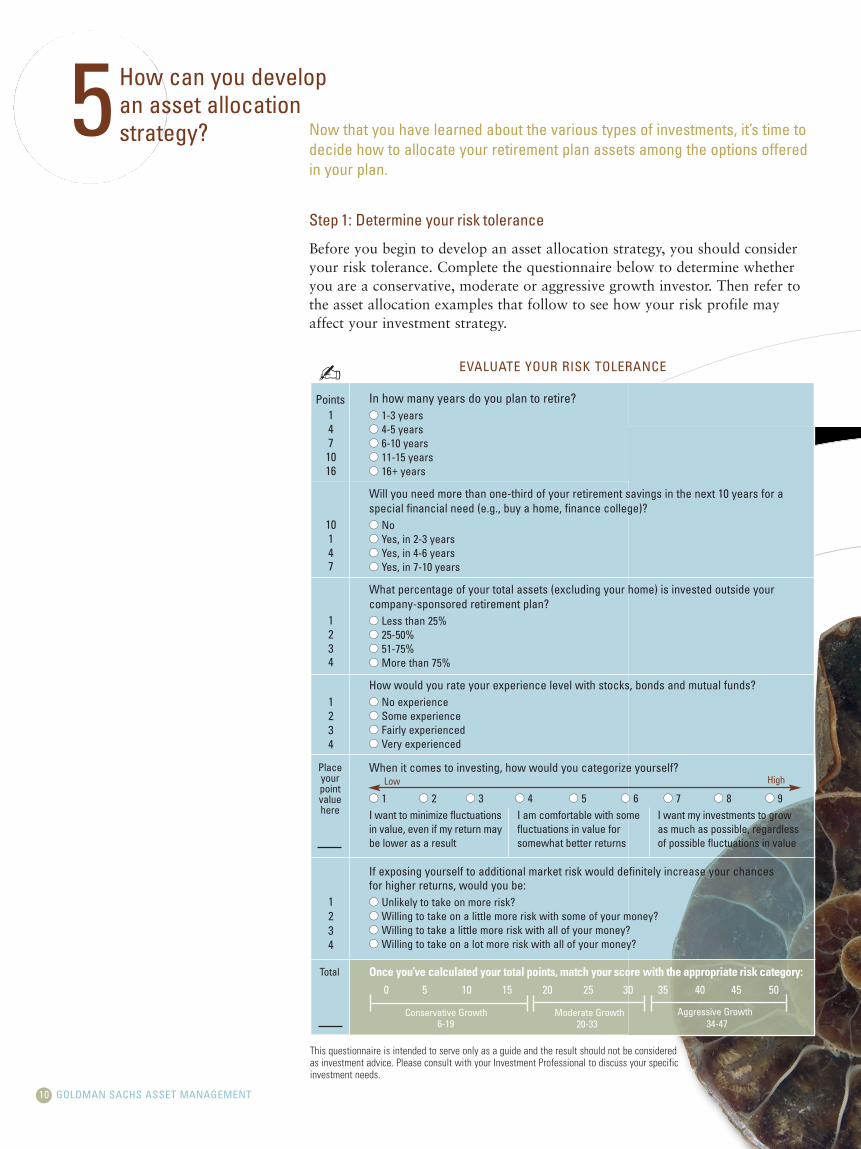

In how many years do you plan to retire?l 1-3 yearsl 4-5 yearsl 6-10 yearsl 11-15 yearsl 16+ years

Will you need more than one-third of your retirement savings in the next 10 years for aspecial financial need (e.g., buy a home, finance college)?l Nol Yes, in 2-3 yearsl Yes, in 4-6 yearsl Yes, in 7-10 years

What percentage of your total assets (excluding your home) is invested outside your company-sponsored retirement plan?l Less than 25%l 25-50%l 51-75%l More than 75%

How would you rate your experience level with stocks, bonds and mutual funds?l No experiencel Some experiencel Fairly experiencedl Very experienced

When it comes to investing, how would you categorize yourself?

l 1 l 2 l 3 l 4 l 5 l 6 l 7 l 8 l 9I want to minimize fluctuations I am comfortable with some I want my investments to growin value, even if my return may fluctuations in value for as much as possible, regardlessbe lower as a result somewhat better returns of possible fluctuations in value

If exposing yourself to additional market risk would definitely increase your chances for higher returns, would you be:l Unlikely to take on more risk?l Willing to take on a little more risk with some of your money?l Willing to take a little more risk with all of your money?l Willing to take on a lot more risk with all of your money?

1471016

10147

1234

1234

1234

This questionnaire is intended to serve only as a guide and the result should not be consideredas investment advice. Please consult with your Investment Professional to discuss your specificinvestment needs.

EVALUATE YOUR RISK TOLERANCE-Points

Placeyourpointvaluehere

Total Once you’ve calculated your total points, match your score with the appropriate risk category:

Conservative Growth Moderate Growth Aggressive Growth

0 5 10 15 20 25 30 35 40 45 50

6-19 20-33 34-47

Low High

5How can you developan asset allocationstrategy? Now that you have learned about the various types of investments, it’s time to

decide how to allocate your retirement plan assets among the options offeredin your plan.

Step 1: Determine your risk tolerance

Before you begin to develop an asset allocation strategy, you should consideryour risk tolerance. Complete the questionnaire below to determine whetheryou are a conservative, moderate or aggressive growth investor. Then refer tothe asset allocation examples that follow to see how your risk profile mayaffect your investment strategy.

GOLDMAN SACHS ASSET MANAGEMENT 11

Step 2: Diversify your assets

When it comes to financial goals and investment selection, no two people arealike. And, neither are their asset allocation strategies. However, there aresome general guidelines to consider when you decide which approach to take.

n Generally speaking, the closer you move toward retirement, the lessaggressive your overall portfolio may need to become.

n Even during retirement, most financial experts recommend that youcontinue to include some growth investments in your portfolio to help youstay ahead of inflation.

n If you’re investing for the long term, be careful not to overemphasize cashinvestments in your portfolio.

Because stocks and bonds generally do not react identically to the sameeconomic, geographic or market events, combining these assets in differentways can produce more attractive risk-adjusted returns for different types ofinvestors. Refer to the charts below to see some sample asset allocationstrategies based on various risk tolerance levels.

Cash

SAMPLE ASSET ALLOCATIONS

Fixed Income

Step 3: Begin the allocation process

At this point, you are ready to begin developing your personalized assetallocation strategy. To learn which investments are being offered in yourcompany’s retirement plan, refer to the listing contained in the accompanyingenrollment materials. If you need further assistance in developing your assetallocation strategy, you may wish to consult with your InvestmentProfessional.

These examples are for illustrative purposes only and are not intended as investment advice. The asset allocation strategy you useshould reflect your individual goals and risk tolerance.

Conservative Moderate Aggressive

Non-U.S. Equity U.S. Equity

70%20%

10%

60%25%

15% 20%40%

40%

55%25%

20%

65%

35%

6

GOLDMAN SACHS ASSET MANAGEMENT12

How can youstay involved?

Track your performanceThere are many ways to track theinvestments in your plan account:

Quarterly account statementsCheck your account balance,portfolio composition and otherinvestment information.

Web siteAccess your savings and reviewinvestment performance. You can also revise your investmentallocation and change your contribution amount.

Interactive voice response systemUse the telephone to access thesame information provided on the Web site.

NewspaperReview fund performanceinformation in the business section.

Start today

You’ve learned about the importance of developing

a retirement plan and how starting early can help

you to achieve your goals. Now, take the first step

by enrolling in your retirement savings program.

Enclosed you will find complete information on the

plan, including details on your investment options.

As you review these materials, speak with your

Investment Professional if you have questions.

After you have enrolled in your retirement plan, you should monitor your investments and periodically make adjustments if needed.

Conduct annual check-ups

Over time, you may want to adjust your retirement plan portfolio. This maybe necessary for reasons including:

n New retirement goals and objectives

n A lifestyle change, such as the birth of a child, marriage or divorce

n A shift in your retirement time frame

n A change in your sensitivity to market risk

n The performance of your investments

n A shift in your portfolio’s asset allocation mix due to market movements

Consider getting help

As you’ve seen, deciding how to invest your retirement savings requires yourtime and knowledge. Many investors choose to work with an experiencedInvestment Professional who can help analyze their needs and develop apersonalized investment plan. An Investment Professional can also help youadjust your plan as needed and, in some cases, offer comprehensive servicessuch as estate and tax planning.

A prospectus for the Goldman Sachs Funds containing more complete information may be obtained from yourinvestment representative or from Goldman, Sachs & Co. by calling 800-526-7384. Please consider a Fund’sobjectives, risks, and charges and expenses, and read the prospectus carefully before investing. The prospectuscontains this and other information about the Fund.

IRS Circular 230 Disclosure: Goldman Sachs does not provide legal, tax or accounting advice. Any statement contained in this communication (including anyattachments) concerning U.S. tax matters is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties imposed on the relevanttaxpayer. Clients of Goldman Sachs should obtain their own independent tax advice based on their particular circumstances.

The S&P 500 Index is the Standard & Poor’s 500 Composite Index of 500 stocks, an unmanaged index of common stock prices. The Index is unmanaged and the figures forthe Index do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

The Russell 1000 Growth Index is an unmanaged market capitalization weighted index of the 1000 largest U.S. companies with higher price-to-book ratios and higherforecasted growth values. The Index is unmanaged and the figures for the Index do not include any deduction for fees, expenses or taxes. It is not possible to investdirectly in an unmanaged index.

The unmanaged MSCI EAFE Index (unhedged) is a market capitalization-weighted composite of securities in 21 developed markets. The Index is unmanaged and thefigures for the Index do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

The Barclays Aggregate Bond Index represents an unmanaged diversified portfolio of fixed-income securities, including U.S. Treasuries, investment-grade corporatebonds, and mortgage-backed and asset-backed securities. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly inan unmanaged index.

Goldman, Sachs & Co. is the distributor of the Goldman Sachs Funds.

Copyright © 2010 Goldman, Sachs & Co. All Rights Reserved. Date of First Use: April 1, 2010 10-33454.MF.TMPL RETIMGUIDE/2.5K/04-10

NOT FDIC-INSURED May Lose Value No Bank Guarantee