Embed Size (px)

Citation preview

Cushman & Wakefield

Global Cities Retail Guide

1Cushman & Wakefield | Philippines | 2019

PHILIPPINES

OVERVIEW

The Philippines strong economic

expansion affirmed its position as

one of Asia Pacific’s frontrunners,

with annual GDP growth rate

registered at 6.2% in 2018.

The country’s economic growth is heavily led by the

manufacturing and trade sectors, with 20% and 14%

share of the GDP, respectively. The service sector, which

is the fastest growing sector, is trailed closely by the

industrial sector, particularly by the buoyant construction

segment.

The on-going massive infrastructure programs are seen to

further augment the country’s attractiveness as an

investment destination and deliver sizeable economic

gains as they address the desperate need for better

infrastructures. Factoring in the healthy domestic demand

and investments, which are seen to counterpoise the

global economic pressures, the country is expected to

sustain its robust GDP growth trajectory.

2Cushman & Wakefield | Philippines | 2019

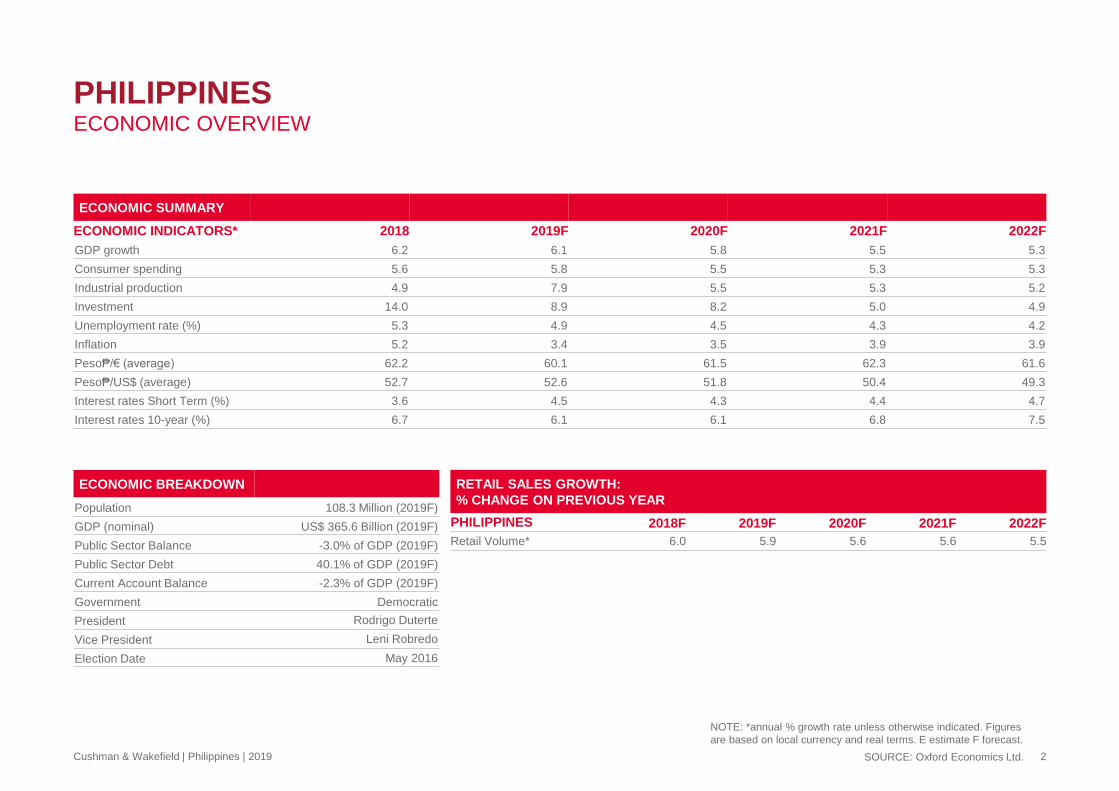

ECONOMIC BREAKDOWN

Population 108.3 Million (2019F)

GDP (nominal) US$ 365.6 Billion (2019F)

Public Sector Balance -3.0% of GDP (2019F)

Public Sector Debt 40.1% of GDP (2019F)

Current Account Balance -2.3% of GDP (2019F)

Government Democratic

President Rodrigo Duterte

Vice President Leni Robredo

Election Date May 2016

PHILIPPINESECONOMIC OVERVIEW

ECONOMIC SUMMARY

ECONOMIC INDICATORS* 2018 2019F 2020F 2021F 2022F

GDP growth 6.2 6.1 5.8 5.5 5.3

Consumer spending 5.6 5.8 5.5 5.3 5.3

Industrial production 4.9 7.9 5.5 5.3 5.2

Investment 14.0 8.9 8.2 5.0 4.9

Unemployment rate (%) 5.3 4.9 4.5 4.3 4.2

Inflation 5.2 3.4 3.5 3.9 3.9

Peso₱/€ (average) 62.2 60.1 61.5 62.3 61.6

Peso₱/US$ (average) 52.7 52.6 51.8 50.4 49.3

Interest rates Short Term (%) 3.6 4.5 4.3 4.4 4.7

Interest rates 10-year (%) 6.7 6.1 6.1 6.8 7.5

SOURCE: Oxford Economics Ltd.

RETAIL SALES GROWTH:

% CHANGE ON PREVIOUS YEAR

PHILIPPINES 2018F 2019F 2020F 2021F 2022F

Retail Volume* 6.0 5.9 5.6 5.6 5.5

NOTE: *annual % growth rate unless otherwise indicated. Figures

are based on local currency and real terms. E estimate F forecast.

3Cushman & Wakefield | Philippines | 2019

PHILIPPINES

LARGEST CITIES

CITYPOPULATION

(2015 Census)

Quezon City, MM 2,919,657

City of Manila, MM 1,763,348

Davao City 1,622,427

Caloocan City, MM 1,581,025

Cebu City 910,678

Zamboanga City 855,418

Taguig City, MM 801,143

Antipolo City 774,734

Pasig City, MM 753,030

Parañaque City, MM 663,733

4Cushman & Wakefield | Philippines | 2019

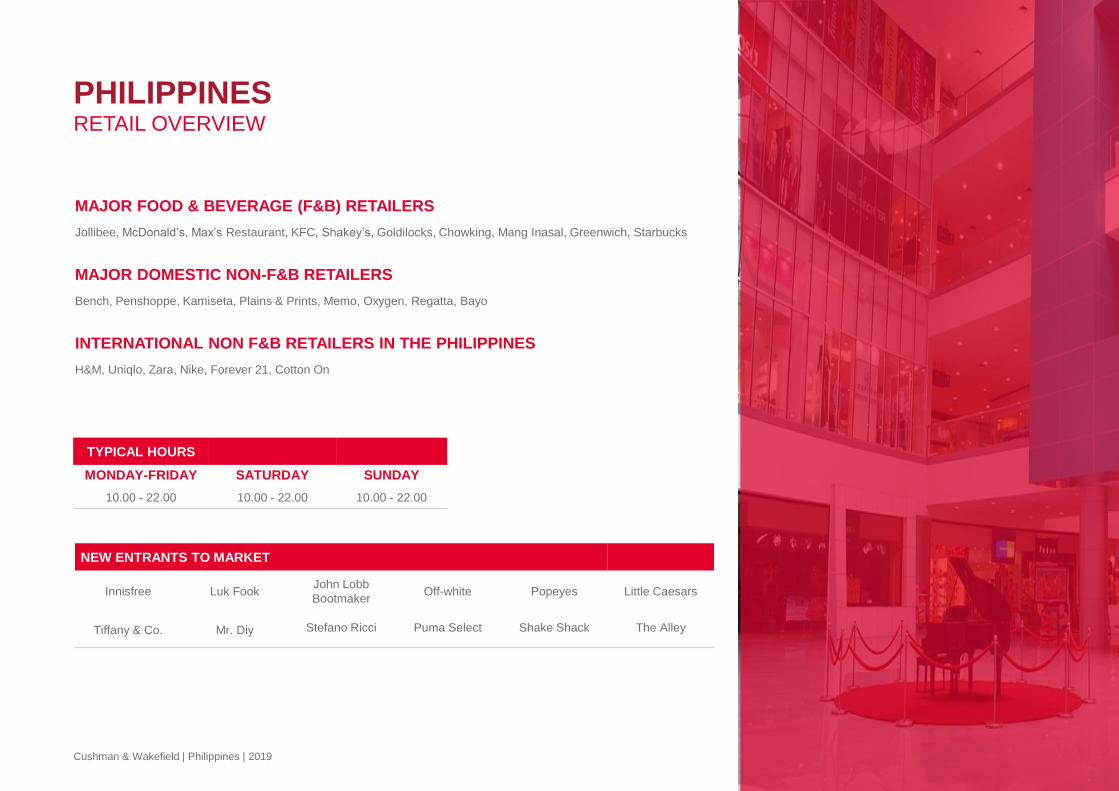

MAJOR FOOD & BEVERAGE (F&B) RETAILERS

Jollibee, McDonald’s, Max’s Restaurant, KFC, Shakey’s, Goldilocks, Chowking, Mang Inasal, Greenwich, Starbucks

MAJOR DOMESTIC NON-F&B RETAILERS

Bench, Penshoppe, Kamiseta, Plains & Prints, Memo, Oxygen, Regatta, Bayo

INTERNATIONAL NON F&B RETAILERS IN THE PHILIPPINES

H&M, Uniqlo, Zara, Nike, Forever 21, Cotton On

PHILIPPINESRETAIL OVERVIEW

TYPICAL HOURS

MONDAY-FRIDAY SATURDAY SUNDAY

10.00 - 22.00 10.00 - 22.00 10.00 - 22.00

NEW ENTRANTS TO MARKET

Innisfree Luk FookJohn Lobb

BootmakerOff-white Popeyes Little Caesars

Tiffany & Co. Mr. Diy Stefano Ricci Puma Select Shake Shack The Alley

5Cushman & Wakefield | Philippines | 2019

The Philippines continue to diverge from

the global trend of dwindling traditional

retail activities as “brick and mortar”

stores continue to thrive and expand,

driven by the sustained increase in per

capita income and purchasing power of

the growing middle-class population.

In 2018 up to mid-2019, the Philippines welcomed at least

43 new foreign retail brands, of which 42% are in the Food

and Beverage (F&B) segment, and 14% are in the

Clothing and Apparel segment. Notable retailers with F&B

concepts include Popeyes, Shake Shack, Little Caesars

and M Bakery. Joining the Clothing and Apparel segment

are Off-White, Puma Select, and Stefano Ricci. Moreover,

the surging consumer demand for the latest healthcare

and beauty trends brought Innisfree and Freyja into the

country’s retail scene. The entry of these foreign brands

cemented Bonifacio Global City in Taguig City as a

premier financial and lifestyle business district, and an

attractive business destination, competing with Makati City

in these aspects, with 40% of these retailers starting their

operations in the area.

PHILIPPINESRETAIL SCENE

The robust demand for retail spaces in the country is

manifested by the healthy occupancy rate currently being

enjoyed by shopping malls and by the continuous

expansions and new developments of retail

establishments. With the Philippines being on track to

upper middle income status, the retail scene is expected

to head towards sustained growth.

While e-commerce does not necessarily translate to a

significant disturbance in the traditional retail situation, its

1% to 2% current share of the total retail value is

projected to upsurge with Filipino consumers spending

more time online and as retailers bet on the recent

evolution labelled as “bricks and clicks”, wherein physical

presence is integrated with online presence in an attempt

to offer an improved shopping experience to customers.

6Cushman & Wakefield | Philippines | 2019

PHILIPPINESSHOPPING CENTERS

TOP SHOPPING CENTERS BY SIZE

NAME CITYSIZE*

(GFA SQM)

YEAR

OPENED

SM City North EDSA Quezon City 498,000 1985

SM Megamall Mandaluyong City 474,000 1991

SM Seaside City Cebu Cebu City 470,000 2015

SM Mall of Asia Pasay City 432,819 2006

SM City Fairview Quezon City 282,681 1997

SM City Cebu Cebu City 273,804 1993

SM Aura Premier Taguig City 249,862 2013

Robinsons Place Manila City of Manila 241,000 1997

Robinsons Galleria Quezon City 220,000 1990

TriNoma Quezon City 224,502 2007

*Does not include the GFA of ongoing and proposed expansion plans

7Cushman & Wakefield | Philippines | 2019

SUB-HEADING

PHILIPPINESKEY FEATURES OF LEASE STRUCTURE

KEY FEATURES OF LEASE

ITEM COMMENT

Lease Terms Typical lease terms for retail outlets in the Philippines run for 1-2 years. Anchor tenants may get a lease term of up to 5 years.

Rental Payment

Rents are usually payable with a month’s deposit and a quarter advance payable on the start of the lease, followed by monthly payments for the

remaining months. However, these terms are usually negotiable with the landlord and usually depend on the length of the lease contract and

the size of the property.

Rent ReviewIt is rather difficult to track and index rent growth in the market as developers usually keep rents confidential. However, developers in recent

years have been increasing rents by 5-10% annually.

Service Charges, Repairs and

Insurance

Service charges, or most commonly known as Common Use Service Area or CUSA fees in the Philippines, are usually payable in tenanted

buildings which covers management fees, security, cleaning, repair and landscaping of common parts and areas of the development. This is

usually excluded from rent and is calculated on a per square meter basis. The landlord is responsible for the repair of external or structural

matters in shopping centers and developments, while the tenants are responsible for internal repairs. Insurance for common parts of the

shopping center is also paid by the landlord but it is usually charged back to the tenant. The tenant is usually responsible for internal insurance.

Property Taxes and other costsVAT of 12% is payable on lease rentals in the Philippines and landlords shoulder the annual property taxes. In addition to the monthly rental, it

is common for mall operators to take a percentage of the retail tenant’s gross monthly revenues. This normally runs at about 3-10%.

Disposal of a LeaseRetail landlords, particularly those in the malls are hesitant to allow subleasing and normally keep strict control of retail tenants in their facilities.

In situations where suitable replacement tenants can be found then landlords will allow the lease to be assigned to the incoming tenants. Incases of pre-termination, penalties will apply.

Valuation Methods

Shops are usually valued on a zoning basis. Shops located on the ground floor are usually charged higher rents compared to those shops on

the upper floors. There will occasionally be local variations to these rates, which will also depend on the quality and functionality of the

accommodation, relative to the market norm.

LegislationA mandatory standard form of lease does not exist and each mall operator will have their own template. In addition, Documentary Stamps are

payable on notarized lease contracts in order to register lease contracts.

No warranty or representation, express or implied, is made to the

accuracy or completeness of the information contained herein, and the

same is submitted subject to errors, omissions, change of price, rental

or other conditions, withdrawal without notice, and to any special

listing conditions imposed by our principals.

© 2019 Cushman & Wakefield LLP. All rights reserved.

TETET CASTRO

Director, Tenant Advisory Group

Cushman & Wakefield Philippines, Inc.

9th Floor Ecotower

32nd Street corner 9th Avenue

Bonifacio Global City, Taguig City

Metro Manila, Philippines

Tel: +63 2 554-2927

Email: [email protected]