Embed Size (px)

Citation preview

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 1/106

1

Global Financial Meltdown

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 2/106

2

ACKNOWLEDGMENT

I take the opportunity to express my profound sense of gratitude and respect to all those who

helped me through the duration of the project It was a great opportunity for me to work on

this project and learn about the subject. I would like to thank my project guide Mr. RakeshDahiya, Assistant Manager, Sharekhan Ltd., who has been a constant source of inspiration for

me during the completion of this project. He gave me invaluable inputs during my endeavor

to complete this project.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 3/106

3

Tab l of content

1.

Introduction 5

2.

Causes of Credit Crisis 11

3. Global Transmission of the Crisis 25 4.

International Response 28

5.

Impact of crisis on trade of goods and services, remittance and tourism and FDI 30

6.

Some Facts and Figures 34

7.

Scale of Crises and Bailouts 44

8.

The financial crisis and wealthy countries 50

9.

Asia and the financial crisis 56

10. Global Meltdown and its Impact on the Indian Economy 59

11. Africa and the financial crisis 7012.

Latin America and the financial crisis 72

13. .A crisis in context 74

y

A crisis of poverty for much of humanity

y

A global food crisis affecting the poorest the most

y

Poor nations will get less financing for development

y

Odious third world debt has remained for decades; Banks and military get

money easily

13. A crisis that need not have happened 78

14. Dealing with recession 85

15. Rethinking the international financial system? 89

y

Reforming international banking and finance?

y

Reforming International Trade and the WT O y

Reforming the Bretton Woods Institutions (IMF and World Bank)?

y

Reform and Resistance

16. Rethinking economics? 103

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 4/106

4

I NTRODUCT I ON

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 5/106

5

I ntroduct ion

A year ago, the prospects for Emerging Economies (EE) looked very promising. There were

concerns about the effect of a shallow recession in the United States, but the general perception

was that Asia, the largest regional emerging market group, and Latin America, the second largest,

as well as other regions were doing well. In a wishful way most thought they had ³decoupled´

from the advanced economies, and wealth would grow with few restrictions.

Surely, policies had been conducive to significant improvements in fiscal and external balances,

with a few exceptions, and international reserves were at record levels. Policymakers feltcomfortable. Commodity prices were expected to continue going up, foreign demand, including

among emerging market economies, was strong and there was no serious worry about financing

as creditworthiness was solid. Problems were hitting only the United States and a few other

developed countries.

Since then, the financial crisis which the world is suffering most likely has become the worst in

the last fifty years. Some analysts consider that its intensity is equivalent to that of the Great

Depression of 1929-33. That crisis was the worst of modern times, and reflected previous

excesses and subsequent incompetence. Although the comparison with the Great Depression is anexaggeration unjustified by the facts, the damage caused to the world economy is enormous. The

complex and wide-ranging interaction between the financial world and the real economy as a

result of the present turbulence already has begun to have serious consequences for the emerging

economies, and the prospects for a fast recovery are more remote by the day.

Whereas the conditions in the financial markets have tended to stabilize from the unsustainable

position of September- October of 2008, the real economy is weakening and the prospects for a

recovery can only be envisaged for late 2009 or early 2010. In different ways, Emerging

Economies were initially able to absorb the initial impact of the crisis on account of the

considerable progress in recent years in consolidating economic performance. Nevertheless, this

group of countries is experiencing mounting difficulties. The difficulties are significant in Asia

and Latin America, but more so in Eastern Europe and Russia, as they were even more dependent

on credit and high export prices respectively.

The previous sense of strength and invulnerability is now gone. Commodity prices have declined

by about one half from their peak; demand for manufactured goods is declining sharply all over

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 6/106

6

the world; stock market valuations have declined by about one half or more; and currencies in

many emerging countries have depreciated, as capital flows reversed seeking to find a safe

heaven. Governments were reasonably careful with their policies, but private enterprises held

³toxic´ assets to an unexpectedly large extent, with serious effects for their own financial health

as well as that of their countries. The loss of financial wealth is enormous, and the consequencesfor the economies of the world, will be unfortunately commensurate.

The authorities and economic agents were initially taken by surprise by the collapse. Now they

are responding to the challenges caused by the rapidly deteriorating external environment.

However, there are serious economic and political stumbling blocks that may well cause the

recovery to be costly and slow to consolidate. This paper reviews the origins of the current crisis

and the impact on emerging market economies, but focuses mainly on Developing Asia, the

NICs, and Latin America in the context of the global crisis. While the inclusion of Latin America

may seem extemporaneous to some, it is fitting to include it as the region has a GD P of US$4.4

trillion, somewhat larger than that of China, and about 2/3 of that of developing Asia, which has a

GDP of US$7 trillion, according to IMF data. No other region comes close to these two areas in

terms of size, and common characteristics in terms of development. Furthermore per-capita

income in Latin America is more than double that of Developing Asia both in current and PPP

terms. The paper also discusses what can be realistically expected in the short and medium term,

as financial volatility and recessionary forces may continue to prevail for a while.

The global financial crisis, brewing for a while, really started to show its effects in the middle

of 2007 and into 2008. Around the world stock markets have fallen, large financial

institutions have collapsed or been bought out, and governments in even the wealthiest

nations have had to come up with rescue packages to bail out their financial systems.

On the one hand many people are concerned that those responsible for the financial problems

are the ones being bailed out, while on the other hand, a global financial meltdown will affect

the livelihoods of almost everyone in an increasingly inter-connected world. The problem

could have been avoided, if ideologues supporting the current economics models weren¶t so

vocal, influential and inconsiderate of others¶ viewpoints and concerns.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 7/106

7

Recent evo lut i on of the wor ld econom ic env ironment

Over the last decade, Asian countries were able to emerge from the serious crisis that had brought

many of them down in the late 90s. Helped by the consistent growth of China, and to an

increasing extent India, the Asia region witnessed a stellar performance. Con currently, after a

period of low economic growth, persistent crises, and high volatility that extended through the

1990s, Latin America made a very strong recovery. Inflation declined; the fiscal accounts and

monetary policy showed great strength; international trade boomed; poverty declined; and the

external accounts were much sounder than they had been in decades.

Within this overall positive picture, not all countries acted in a similarly prudent fashion. The

limited initial impact of the financial crisis gave rise to a false sense of security that has now

disappeared. The crisis is now in the open, as the impact on the balance of payments and on

domestic activity becomes very serious. The adverse terms of trade effect will aggravate the

situation, compounded by a massive loss in financial wealth.

Economic growth in 2009 may decline by half among developing and emerging economies

(Table 1). It is likely to be well below 1% in Latin America; a recession among the newly

Industrialized countries of Asia (NICs); and much lower growth rates, even though still in the

order of 5% in Emerging Asia, mainly on account of the resiliency of China, and to a lesser

extent India. Of course, this is shocking for all the regions that had experienced very strong

growth from 2002 onward. Under these conditions, policy makers will need to find a balance

between the needs of economic stimulus and of financial stability.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 8/106

8

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 9/106

9

Genes is of the Present F inanc i a l and Econom ic Cr isis

The reasons for the current crisis are complex, and are linked to the financial market deterioration

of the last 20 months or so, after a period of extraordinary growth but fraught with dangers that

were not anticipated by most even a few months ago. For four years through the summer of 2007,

the global economy boomed. Global GD P rose at an average of about 5 percent a year, its highest

sustained rate since the early 1970s. About three-fourths of this growth was attributable to a

broad-based surge in the emerging and developing economies. Inflation remained generally

contained, even if with some upward pressures. Prosperous stage that using an abused word,

entailed a new economic paradigm. The value of financial and real assets was growing without a

perceptible limit, and commodities had reached new and sustainable heights. Concurrently, the

value of financial assets rose sharply, as described in further detail below.

The most important factor behind the increasing imbalances was the emergence of growingimbalances among the main economies of the world. The US, with low rates of savings,

embarked in consumption binge and a growing fiscal deficit, experienced growing external

current account deficits. These were financed by the surpluses of oil producing countries, China,

Japan, and to a lesser extent Europe and Latin America. These imbalances grew rapidly, but

markets did not respond significantly before 2007. However, the US dollar started to weaken in

international markets and there were growing signs of impending problems. As stated very

precisely by Jack Boorman, these trends were further complicated by an increasingly integrated

global trading and financial system which magnified and accelerated the transmission process;inadequate regulation and supervision of national financial systems and fragmentation of global

regulation; weak surveillance by the IMF and other multilateral organizations; and aggravated by

weak and uncoordinated policy responses to the initial signs of trouble in the financial system ±

responses that, as noted below, in many instances did more to shake confidence than to instill a

sense that policy was up to the task of dealing with the banking system crisis and the impact on

the real economy.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 10/106

10

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 11/106

11

CAUSES OF CRED I T CR I SES

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 12/106

1 2

Causes of the Cred i t Cr i sis

In the midst of the most serious financial crisis in a generation, some claim that deregulation

is entirely to blame. This is simply not true and more importantly serves to grossly

oversimplify a problem whose roots run deep and involve myriad actors and issues. Thesimple truth is that many share the blame, and pointing to just one person or organization

does a disservice to the American people.

In a time of crisis, the American people cannot afford the same old partisan finger pointing;

they need and deserve real, non-partisan oversight. We need a series of hearings that will

focus on the root causes and how we can fix a system in order to avoid financial meltdowns

in the future. This minority staff analysis attempts to objectively explore the causes of the

financial crisis we are in and how companies like Lehman Brothers and AIG contributed to

this crisis.

The current credit crisis is a complex phenomenon with its roots in a number of places

involving a myriad of people and institutions. Key players and institutions include Members

of Congress, well-respected members of Republican and Democratic administrations, the

Federal Reserve Board, Fannie Mae, Freddie Mac, the Department of Housing and Urban

Development (HUD), the Securities and Exchange Commission (SEC), the major private

sector credit rating agencies, banks, mortgage brokers, and consumers.

There is no single issue or decision one can trace as a cause of the current financial crisis;

rather it was multiple decisions and issues involving many actors over time that led us to

where we are today. However, we can point to organizations that contributed greatly to the

problem and how their role was the catalyst for others to become involved and eventually

fail. Fannie Mae and Freddie Mac fall into this category. They were the central cancer of the

mortgage market, which has now metastasized into the current financial crisis. With the help

of a loose monetary policy at the Federal Reserve, an over-reliance on inaccurate risk

assessment and a fractured regulatory system, this cancer spread throughout the financial

industry.

A few key elements are critical in understanding how we got to where we are today.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 13/106

1 3

.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 14/106

1 4

By 2005, Federal Reserve Chairman Alan Greenspan was so concerned that he characterized

the concentration of systemic risk inherent in the ever-growing portfolios of Fannie and

Freddie as, placing the total financial system of the future at a substantial risk. Recent events

have unfortunately proved him right.

The transformation of Fannie Mae and Freddie Mac into the Affordable Housing Center was

a laudable goal, but to push predatory subprime lending to unspeakable heights and to

encourage questionable lending practices believing housing prices would continue to soar

was beyond reason.

The politicization of Fannie Mae and Freddie Mac over the last decade seriously undermined

the credibility of the organizations and prevented their restructuring and reform, with

Democrats viewing any attempt at curtailing their behavior as an attempt at curtailing

affordable housing. Between 1998 and 2008, Fannie and Freddie combined spent nearly $175

million lobbying Congress, and from 2000 to 2008 their employees contributed nearly $15

million to the campaigns of dozens of Members of Congress on key committees responsible

for oversight of Fannie and Freddie. Those who opposed the restructuring of Fannie Mae and

Freddie Mac were unwittingly helping to build a house of cards on risky mortgage backed

securities.

The motivations for Fannie Mae and Freddie Mac to gamble with taxpayer money on bad

nonprime mortgage bets was not entirely a matter of good intentions gone awry. Greed and

corruption were unfortunately part of the equation as well. The size and growth of Fannie

Mae and Freddie Mac leading up to their collapse were nothing short of astonishing. From

1990 to 2005, Fannie Mae and Freddie Mac grew more than 944% to $1.64 trillion, and their

outstanding liabilities grew 980% to $1.51 trillion. These liabilities were equal to 32.8% of

the total publicly-held debt of the U.S. Government, which in 2005 stood at $4.6 trillion.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 15/106

1 5

.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 16/106

16

Lehman Brothers, A I G and the Cha ll enges of Stat ist ica l R isk Mode lli ng

Lehman Brothers didn¶t cause this mess but it certainly jumped head first into trying to make

money on securitizing mortgage-backed instruments. They followed on the heels of Fannie

Mae and Freddie Mac and for precisely the same reasons. If we understand the initial causeof the cancer at Fannie and Freddie, then we can understand how it metastasized to Lehman

Brothers, Wachovia, Countrywide, and beyond.

AIG is somewhat different; bad management decisions were made in thinking that the

mortgage-backed securities and derivatives could be insured. Yet underlying its bad decisions

was the same mistaken reliance on sophisticated but inaccurate computer models, trusting the

rating agencies were accurate and that Fannie Mae and Freddie Mac couldn¶t possibly fail.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 17/106

1 7

Regu lat i on and the Cred i t Cr isi s

Democrats are wrong in insisting that de-regulation is the primary cause of the financial

crisis. Deregulation is not the problem, rather it is the fractured regulatory system that has

banks, investment institutions, mortgage brokers, and insurance companies all being overseenby different and often competing federal and state agencies. The problem is a lack of coherent

regulatory oversight that has led mortgage brokers and lending institutions to write

questionable loans and investment institutions to play fast and loose with other peoples

money in purchasing bad mortgage-backed assets.

The words regulation and deregulation are not absolute goods and evils, nor are they

meaningful policy prescriptions. They are political cant used to describe complex policy

discussions that defy simplistic categorization. The key to successfully regulating markets is

not to either create more or less regulation in an unthinking way. Government needs to design

smart regulations that align the incentives of consumers, lenders and borrowers to achieve

stable and healthy markets.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 18/106

1 8

Cred i t Rat i ng Agenc ies and the Pract ice of Rat i ng Shopp ing

Some firms that bundled subprime mortgages into securities were engaging in rating

shopping - picking and choosing among each of the three credit rating agencies in order to

find the one willing to give their assets the most favorable rating. Rating agencies willing toinflate their ratings on subprime mortgage-backed securities lobbied Congress to prohibit

notching - the downgrading of assets that incorporate risky, unrated assets - by their

competitors, on the grounds this constituted an anti-competitive practice. Unfortunately, the

Republican Congress was swayed by this argument and codified it in law.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 19/106

1 9

Mortgage Markets: A Pr i mer

Prospective homebuyers apply for mortgages from primary market lenders such as banks,

thrifts, mortgage companies, credit unions, and online lenders. Primary lenders evaluate

borrowers ability to repay the mortgage based on an assessment of risk that combines suchfactors as income, assets and past performance in repaying loans. If a borrower does not meet

the minimum requirement, the borrower is refused a loan.

Prime mortgages are traditionally the gold standard and go to borrowers with good credit who

make down payments and fully document their income and assets. Borrowers with poor

credit and/or uncertain income streams represent a higher risk of default for lenders and

therefore receive subprime loans. Subprime loans have existed for some time but really took

off in popularity around 1995, rising from less than 5% of mortgage originations in 1994 to

more than 20% in 2006. Borrowers who fall in between prime and subprime standards who

may not be able to fully document their income or provide traditional down payments are

sometimes referred to as near-prime borrowers. They generally can apply only for

Alternative-A (Alt-A) mortgages. Starting in 2001, subprime and near-prime mortgages

increased dramatically as a proportion of the total mortgage market. These mortgages

increased from only 9% of newly originated securitized mortgages in 2001 to 40% in 2006.

Subprime borrowers, in addition to being below the standard risk threshold lenders

traditionally deemed creditworthy for mortgages, were increasingly taking advantage of so-

called alternative mortgages that further increased the risk of default. For example, low- or

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 20/106

2 0

zero-down payment mortgages permit borrowers who cannot afford the traditional 20% down

payment on a house to still receive a loan. Instead some mortgages allow them to pay 10%,

5%, or even 3% of the purchase price of the home. The riskiest loans even allow borrowers to

pay no money down at all for 100% financing. Another option is to allow borrowers to take

out a piggyback or silent second loan - a second mortgage to finance the down payment. Thisis possible because the larger first mortgage means some lenders give borrowers a more

favorable rate on the second mortgage. Interest-only mortgages are another alternative type

that allows borrowers to for a time pay back only interest and no principal. However, either

the duration of the mortgage must be extended or the payments amortize the remaining

principal balance over a shorter period of time, increasing the monthly payment, and

ultimately the total size of the loan, a borrower must repay. Negative amortization mortgages

are even riskier, allowing borrowers to pay less than the minimum monthly interest payment,

adding the remaining interest to the loan principal and again increasing the payments and size

of the loan.

Adjustable rate mortgages (ARMs) are the most common of the alternative mortgages. ARMs

offer a low introductory mortgage rate (the cost of borrowing money for a home loan; it is

generally related to the underlying interest rate in the macro economy) which then adjusts in

the future by an amount determined by a pre-arranged formula. There are different formulae

used to determine the new mortgage rate on an ARM, but in general one can think of these

new rates as being related to the performance of the U.S. economy. If interest rates go downduring the introductory period of the ARM, the adjusted mortgage rate will be lower,

meaning the borrowers monthly payment will go down. If interest rates go up, the borrowers

monthly payment will be larger. The prevalence of ARMs as a percentage of the total

mortgage market increased dramatically during the housing bubble, from 12% in 2001 to

34% in 2004.

Unlike other alternative mortgages, however, there are sound reasons for borrowers to take

out ARMs, under certain macroeconomic conditions. In 1984, for example, 61% of newconventional mortgages were ARMs. However, this was a rational response to the very high

interest rates at that time. High interest rates translate into high mortgage rates. This meant

that borrowers at that time were willing to bet that when their mortgage rates adjusted, they

were likely to adjust downward due to falling interest rates. This was a sensible bet and one

that turned out to be correct.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 21/106

2 1

From 2001 to 2004, however, interest rates were abnormally low because the Federal Reserve

led by Chairman Alan Greenspan lowered rates dramatically to pump up the U.S. economy

following the attacks of September 11, 2001. Correspondingly, from 2004 to 2006, mortgage

rates on 30-year fixed-rate mortgages were around 6%, relatively low by historical standards.

Borrowers responding only to these macroeconomic conditions would have been wise to lock in these rates with a traditional 30-year fixed-rate mortgage. The continuing popularity of

ARMs, at least until about 2004, relates in part to the abnormally wide disparity between

short- and long-term interest rates during this period. Since ARMs tend to follow short-term

rates, borrowers could get these mortgages at even lower costs and, as long as they were

confident that housing prices would continue to rise, plan on refinancing before their ARMs

adjusted upward.

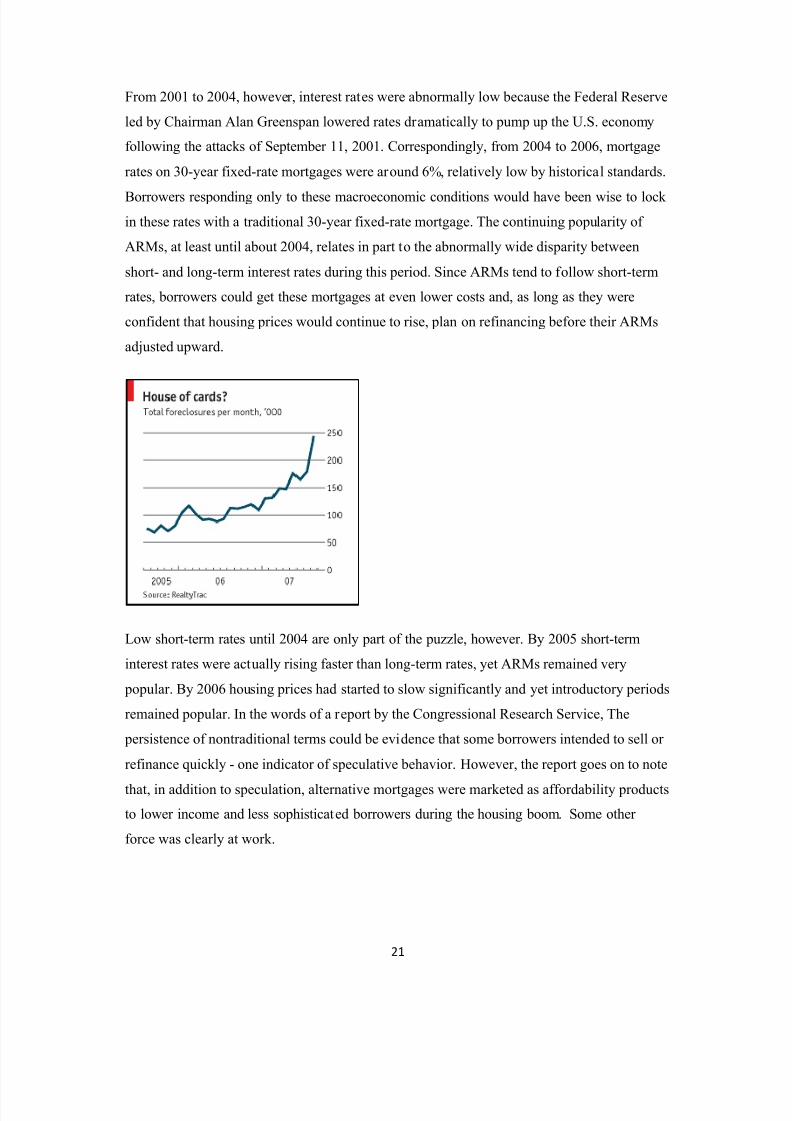

Low short-term rates until 2004 are only part of the puzzle, however. By 2005 short-term

interest rates were actually rising faster than long-term rates, yet ARMs remained very

popular. By 2006 housing prices had started to slow significantly and yet introductory periods

remained popular. In the words of a report by the Congressional Research Service, The

persistence of nontraditional terms could be evidence that some borrowers intended to sell or

refinance quickly - one indicator of speculative behavior. However, the report goes on to note

that, in addition to speculation, alternative mortgages were marketed as affordability products

to lower income and less sophisticated borrowers during the housing boom. Some other

force was clearly at work.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 22/106

22

The Ro le of Fann ie Mae and Fredd ie Mac in Creat i ng the Cred i t Cr isis

Successive Congresses and Administrations have used Fannie Mae and Freddie Mac as tools

in service to a well-intentioned policy to increase the affordability of housing in the United

States. In the process, the U.S. Government created an incentive structure for Fannie andFreddie to facilitate the extension of risky nonprime and alternative mortgages to many

borrowers with a questionable ability to pay these loans back. Ultimately, Fannie and Freddie

may have purchased or guaranteed up to $1 trillion of risky nonprime mortgages. This, along

with a healthy dose of unethical and corrupt behavior by the management of Fannie Mae and

Freddie Mac, has contributed perhaps more than any other single factor to the growth of the

subprime housing bubble from 2005 to 2007, which in turn was the root cause of the current

financial crisis.

In the mortgage market, primary lenders may choose to hold a mortgage until repayment or

they may sell it to the secondary mortgage market. If the primary lender sells the mortgage, it

can use the proceeds from the sale to make additional loans to other homebuyers. This

increase in the funding available to mortgage lenders to lend was the goal behind the creation

of Fannie Mae and Freddie Mac.

Prior to the existence of the secondary mortgage market, there was no national U.S. mortgage

market. Instead, the mortgage industry was mainly concentrated in urban centers, leaving

broad swaths of the country unable to afford home financing. In response, Congress created

the Federal National Mortgage Association, or Fannie Mae, in the National Housing Act of

1934 as a purely public agency. After a number of legislative iterations, Fannie Mae morphed

into a private company, a government-sponsored enterprise (GSE), with no federal funding

by 1970.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 23/106

2 3

Secur i t isat ion and Subpr i me cr isis

The sub prime crisis came about in a large part of financial instruments such as securitisation.

Where bank would pool their various loans into sellable assets, thus off loading risky loans

on to others (For banks, millions can be made in money earning loans, but they are tied up for

decades. So they turned into securities. The security buyer gets regular payments from all those

mortgages; the banker off loads the risk. Securitization was seen as perhaps the greatest financial

innovation in the 20 th century).

As BBC¶s former economic editor and presenter, Evan Davies noted in a documentary called µThe

City Uncovered with Evan Davis: Banks and How to Break Them (January 14,2008)¶, rating agencies

were paid to rate these products (risking a conflict of interest) and invariably got good

ratings,encouraging people to take them up.

Starting in Wall Street, others followed quickly. With soaring profits, all wanted in, even if it

went beyond their expertise. For Example,

y

Banks borrowed even more money to lend out so they could create more

securitization. Some banks didn¶t need to rely on savers as much then, as long as they

could borrow from banks and sell those loans on as securities; bad loans would be the

problem of whoever bought the securities.

y

Some investment banks like Lehman Brothers git into mortgages, buying them in

order to securitize them and then sell them on.y

Some banks loaned even more to have an excuse to securitize those loans.

y

Running out of whom to loan to, banks turned to the poor; the subprime, the riskier

loans. Rising house prices led lenders to think it wasn¶t too riski; bad loans ment

repossessing high-valued property. Subprime and ³ self-certified´ loans (sometimes

dubbed ³liar¶s loans´) became popular, especially in the US.

y

Some banks even started to buy securities from others.

y

Collateralized Debt Obligations, or CD Os, (even more complex forms of

securitization) spread the risk but were very complicated and often hid the bad loans.

While things were good, no one wanted bad news.

High street banks got into a form of investment banking, buying, selling and trading risk.

Investment banks, not content with buying, selling, and trading risk, got into home loans,

mortgages, etc without the right controls and management.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 24/106

2 4

Derivatives didn¶t cause this financial meltdown but they did accelerate it once the subprimemortgage collapsed, because of the interlinked investments. Derivatives revolutionized thefinancial markets and mitigating risk.

This will be very hard to do. Despite the benefits of a market system, as all have admitted for

many years, it is far from perfect. Amongst other things, experts such as economists andpsychologists say that markets suffer from a few human frailties, such as confirmation bias (

always looking for facts that support your view, rather than just facts) and superiority bias (

the belief that one is better than the others, or better than the average and can make good

decisions all the time). Trying to reign in these facets of human nature seems like a tall order

and in the meanwhile the costs are skyrocketing.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 25/106

2 5

G loba l Transm iss ion of the Cr isis

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 26/106

2 6

G loba l Transm iss i on of the Cr isis

The financial crisis that erupted in August 2007 after the collapse of the U.S. subprime mortgage

market entered a tumultuous new phase in September 2008. These developments badly shook

confidence in global financial institutions and markets. Most dramatically, intensifying solvency

concerns triggered a cascading series of bankruptcies, forced mergers, and public interventions in

the United States and Western Europe, which eventually resulted in a drastic reshaping of the

financial landscape.

When the real estate bubble busted in the US and Europe (the UK and Spain come to mind),

investors moved to commodities, where experts expected a continuous increase in prices. The

commodity bubble peaked in mid 2008, with a subsequent collapse, that only decelerated by the

end of the year. In the second half of the year commodity prices declined by some 45%; in

particular losses were large in the case of metals and oil (Chart 1).

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 27/106

2 7

Chart 1: Evo lut ion of commod i ty Pr ices (2005=100 )

Source: IMF: Commodity Prices; .

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 28/106

2 8

I nternat iona l Response

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 29/106

2 9

I nternat i ona l Response

The national rescue operations have been followed by major swap transactions between the

Federal Reserve of the US and a number of other central banks of industrialized economies, in

order to provide sufficient liquidity in response to a steady demand for US dollars. More recently,

this was extended to the Central Banks of Brazil, Korea, Mexico, and Singapore, again to support

the currencies of those countries in the face of continued pressures in foreign exchange markets at

least through end-2008.

With high financing requirements, access to the International Financial Institutions has also

become imperative. The IMF has already indicated that it will show greater lending flexibility

and can mobilize significant resources. In the past, any borrowing had to be based on what was

seen as burdensome conditions. The IMF would now provide assistance on the basis of fewer

conditions, for countries seen as generally good performers. And conditions would be fewer and

more targeted than in the past. 7

The creation of the G-20 Summits is another noteworthy development. It follows a group formed

in the 1990s to discuss international financial issues, at the ministerial level. Up to now, many

decisions had been taken at the level of the G-7/G-8, the important group formed by the largest

advanced economies, and Russia. The G-20 includes the G-8 and the largest emerging, newly

industrialized economies, including China, India, Korea, South Africa, and in Latin America,

Brazil, Mexico and Argentina. This forum reflects better the growing importance of the emerging

world and may also open the door to a more representative governance system at the internationalfinancial institutions (IFIs). However, over-represented Europe and others will need to accept the

realities of the new world and shift their voting power to the ³new´ countries, and make IFIs

more relevant.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 30/106

3 0

I mpact of cr isis on trade of goods and serv ices, remm itace andtour ism and FD I

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 31/106

3 1

I mpact of cr i sis on trade of goods and serv ices, remm i tace and tour ism and

FD I

Deve lopments in Trade of Goods and Serv ices

As part of the significant slowdown/decline in world activity, trade volumes are expected to

decline for the first time in many years²as a minimum by 3% according to IMF estimates. The

impact will be very different in various areas of the world. Over the last quarter century the

volume of world trade had grown at an average rate of 6%, or about double the rate of world

output. Asian exports have grown at a rate of 10% and those of Latin America and the Caribbean

by some 7%, with a marked transformational impact.

The NICs, which have become highly integrated with the rest of the world, recorded an average

ratio of Exports to GD P of 71% for the period 2002-07. Developing Asia recorded a ratio of 55%,

tempered by the much lower but growing ratios for China (31%) and India (12%) which were

clearly dominated by domestic developments. In Asia the ratio of exports to GD P reflected

increased volumes of trade, but to some extent also some real depreciation of their currencies.

Latin America which had become much more open in the 1990s, registered a stable ratio of

exports to GD P of 21% notwithstanding the impact of a strong real appreciation, as export

volumes increased significantly over the period.

Under these conditions, it would be easy to suggest that the countries that have been most open to

international trade may be subject to the greatest shock on account of reduced world demand,

thus justifying protectionism. However this should be viewed in a broader light.

Countries that opened more vigorously to trade grew the fastest, and benefitted more from global

prosperity. It may be the case that they will experience a significant short term loss, as is being

observed in Taiwan Province and in Korea. But this is taking place from the vantage point of

much higher gains in the past, and with the understanding that the losses, even if large, will be

temporary. More significantly, the more open traders may benefit from a more flexible productive

structure that allows them to adjust more efficiently. More closed economies, adjusted for their

size 8, may be more dependent on a few commodities, and will have more difficulty in correcting

imbalances as their domestic economies may find a lower productive base to provide for their

imports.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 32/106

3 2

Rem i ttances and Tour ism

Two other areas that can be expected to show the impact of the slowdown are remittances and

services, like tourism. Remittances over the last fifteen years have become a major channel of

prosperity. The merits of increased mobility of large numbers of workers to well-paying jobs in

prosperous destinations may be subject to debate. However, the impact of the consequent

remittances to their home countries have helped increase prosperity and reduce poverty,

particularly in Asia and Latin America- India, Mexico and the Philippines being the largest

recipients of workers¶ remittances. Remittances amounted to some US$280 billion in 2008 (some

2% of GD P of the receiving countries), with near US$110 billion to Asia, and US$70 billion to

Latin America. These flows have been very stable, and acted as a countercyclical force in the

receiving countries. 9 However, they are highly sensitive to economic conditions in the countries

of employment. With many emigrants working in the US, Europe, and the Middle East,remittances started to fall in 2008, for the first time in a quarter century. The prospects for 2009

are equally dire, with adverse consequences for the well being of many millions of households

among developing countries.

Tourism is another area of concern. Receipts from tourists are also a significant source of income,

particularly for Thailand, Maldives, India and some other countries in South and South East Asia,

and Mexico, Central America and the Caribbean, and some countries in South America. Even

though transportation costs are declining, tourism from the richer countries has fallen and will

continue to do so. With emerging economies, arguably the most dynamic segment of internationaltourism, also entering into recession the prospects for this segment of economic activity look

particularly grim for the near future.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 33/106

33

Fore ign D irect I nvestment

Foreign Direct Investment (FDI) will also suffer in the short run. FDI stocks and flows grew at a

very fast rate in recent years, reflecting both the emergence of new countries as origin and

destination of capital flows, and rapidly evolving capital markets, which allowed for a sharp

increase in available capital within the private sector, and resulting in a decline in lending by

International Financial Institutions or IFIs. Most interesting was the change in the composition of

these flows. While total FDI directed to developed countries retained the lion¶s share of the total

inflows (70% of the total), both Asia and Latin America became increasingly important, even

with some volatility in the case of Latin America. (Table 2) Also, the countries of the CSIS and

of Eastern and Central Europe began to receive increasing flows. 10 As an illustration of the size of

inflows and outflows, table# 2 presents the cumulative inflows and outflows of FDI and portfolio

investments for Developing Asia and Latin America for the period 1998-2007. The information isparticularly interesting as it shows the large sums of capital outflows from Emerging Economies,

as they became increasingly important investors, as opposed to the previous experience when

these outflows reflected capital flight. By early 2008 capital flows to developing countries had

started to slow down, and these flows fell sharply in the second half of the year reflecting the

financial crisis. In the end, cumulative flows for the year were only about one half of those

registered in 2007, with sharp declines both in Asia and Latin America. The Institute of

International Finance estimates that net private flows to emerging economies declined from a

record US$930 billion in 2007 to below US$470 billion in 2008 and to projected flows of onlyUS$165 billion in 2009. Net flows are projected to decline by 80% from their 2007 peak for

Emerging Asia, and by 75% for Latin America. This will complicate economic management, as

countries deal with weakening external accounts.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 34/106

34

Some Facts and F igures

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 35/106

35

Some Facts and F igures

Chart 1

Growth of GDP in Deve lop ing As ia, Lat in Amer ica and the Wor ld (Annua l percent)

Source: WE O , IMF, ECLAC, .

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 36/106

3 6

Chart 2

I nf lat ion ( in %)

Source: WE O , IMF, ECLAC, .

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 37/106

37

Chart 3

Externa l Current Account, Fisca l Ba lance, Exchange Rates and Terms of Trade

Deve lop ing and Emerg ing As ia

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 38/106

38

Chart 4

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 39/106

39

Chart 5

Fore ign D irect I nvestment: Rec ip ient reg ions stocks (US$ b illi ons)

1980 1990 2000 2006

Wor ld 551 1779 5810 11999

Deve loped Econom ies 411 1414 4031 8454

Share in Total 75 80 69 71

Deve lop ing Econom ies 140 365 1708 3156

Share in Total 9 9 17 14

Wor ld FD I Stock 859 2388 7948 11999

MemorandumItems

Cap ita l F lows (US$ b illi on;1998-07)2/ Dev As ia LATAM

FD I I nf lows 841 728

FD I Outf lows -151 -142

Portfo li o I nf lows 127 170

Portfo li o Outf lows -102 -103

1/ Adjusted by wor ld export pr ices

2/2007 va lues for As ia are est imates

Source: UNCTAD, World Investment Report (2007),

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 40/106

4 0

Chart 6

Growth of GDP in Deve lop ing As ia, Lat in Amer ica and the Wor ld

(Annua l percent)

Source IMF, ECLAC

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 41/106

4 1

Chart 7:I nf lat ion ( in %)

Source: WE O , IMF, ECLAC,

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 42/106

4 2

Chart 8

Se lected Countr ies-stock Market and Exchange Rate changes June-Dec 2008

Stock Market Changes % Exchange Rate Changes %

China -48 1

Hong-Kong -40 1

India -41 -13

South Korea -36 -20

Argentina -51 -13

Brazil -49 -31

Mexico -29 -26

Japan -36 18Euro Area -37 -11

USA(S& P500) -36 --Sources: Bloomberg, market data

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 43/106

43

Chart 9

ST I M ULUS PAC K AGES: Se lected Countr ies

Country Announced Amount of St i mu l us Gross Pub li c

Debt

Pub li c Debt, net

of I nternat i ona l

Reserves

US Billion, annual (% of GD P , 2008)

Ch i na 300 (586) 1/ 7.1 18 -30

S ingapore 6.2 3.2 92 2

I ndones i a 6.3 1.3 17 5

South Korea 10.8 1.1 32 11

I nd ia 8.3 0.7 58 37Peru 3.2 2.5 31 1

Ch il e 4.0 2.2 19 6

Argent i na 3.8 1.2 59 46

Mex ico 10.8 1.1 26 18

Braz il 16.0 1.0 57 46

USA 800 (1150) 1/ 5.6 38 38

Japan 250 5.2 153 128

Germany 102 2.7 67 64

Great Br i ta i n 30 1.1 44 41

1/Estimated expenditure in 2009. Number in parenthesis reflects announced total package

Sources: National data; Press Releases; IMF; Eurostat

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 44/106

44

SCALE OF CR I SES

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 45/106

45

The sca le of the cr isis: tr illi ons in taxpayer ba il outs

The extent of the problems has been so severe that some of the world¶s largest financial

institutions have collapsed. Others have been bought out by their competition at low prices

and in other cases, the governments of the wealthiest nations in the world have resorted to

extensive bail-out and rescue packages for the remaining large banks and financial

institutions.

The total amounts that government have spent on bailouts have skyrocketed. From a world

credit loss of $2.8 trillion in October 2009, US taxpayers alone will spend some $9.7 trillion

in bailout packages and plans, according to Bloomberg, $14.5 trillion, or 33%, of the value of

the world¶s companies has been wiped out by this crisis. The UK and other European

countries have also spent some $2 trillion on rescues and bailout packages. More is expected

Many banks were taking on huge risks increasing their exposure to problems.When people

did eventually start to see problems, confidence fell quickly. Some investment banks were

sitting on the riskiest loans that other investors did not want. Assets were plummeting in

value so lenders wanted to take their money back. But some investment banks had little in

deposits; no secure retail funding, so some collapsed quickly and dramatically of criticism for

betting n the things going badly. In the recent crisis they were criticized for shorting on

banks, driving down their prices. Some countries temporarily banned shorting on banks. In

some regards, hedge funds may have been signalling an underlying weakness with banks,

which were encouraging borrowing beyond people¶s means. On the other hand more it

continued the more they could profit.

The market for credit default swaps market (a derivative on insurance on when a business

defaults), for example, was enormous, exceeding the entire world economies output of $50

trillion by summer 2008. It was also poorly regulated. The world¶s largest insurance and

financial services company, AIG alone had credit default swaps of around $400 billion at that

time. A lot of exposure with little regulation. Furthermore , many of AIG¶s credit defaultswaps were mortgages, which of course went downhill, and so did AIG.

The trade in these swaps created a whole web of interlinked dependencies: a chain only as

strong as the weakest link. Any problem, such as risk or actual significant loss could spread

quickly. Hence the eventual bailout (now some $150 billion) of AIG by the US government

to prevent them failing.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 46/106

4 6

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 47/106

47

The effect of this, the United Nation¶s Conference on Trade and Development says in its

Trade and Development Report 2008 is, as summarized by the Thi rd World Network , that

³ The global economy is teetering on the brink of recession. The downturn after four years of

relatively fast growth is due to a number of factors: the global fallout from the financial crisisin the United States, the bursting of the housing bubbles in the US and in other large

economies, soaring commodity prices, increasingly restrictive monetary policies in a number

of countries, and stock market volatility.The fallout from the collapse of the US mortgage

market and the reversal of the housing boom in various important countries has turned out to

be more profound and persistent than expected in 2007 and beginning of 2008. As more and

more evidence is gathered and as the lag effects are showing up, we are seeing more and

more countries around the world being affected by this rather profound and persistent

negative effects from the reversal of housing booms in various countries.´

Kanaga Raja, Econom i c Outlook Gloomy, R is k s to Sout h , s ay UNC TAD , Thi rd World

Network, September 4, 2008

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 48/106

48

A Cr i sis so severe, those respons ib le are ba il ed out

Some of the bail-outs have also been accompanied with charges of hypocrisy due to the

appearance of ³socializing the costs while privatizing the profits.´ The bail-outs appear to

help the financial institutions that got into trouble (many of whom pushed for the kind of laxpolicies that allowed this to happen in the first place).

Some governments have moved to make it harder to manipulate the markets by shorting

during the financial crisis blaming them for worsening an already bad situation.

(It should be noted that during the debilitating Asian financial crisis in the late 1990s, Asian

nations affected by short-selling complained, without success that currency speculators²

operating through hedge funds or through the currency operations of commercial banks and

other financial institutions²were attacking their currencies through short selling and in doing

so, bringing the rates of the local currencies far below their real economic levels. However,

when they complained to the Western governments and International Monetary Fund (IMF),

they dismissed the claims of the Asian governments, blaming it on their own economic

mismanagement instead.)

Other governments have moved to try and reassure investors and savers that their money is

safe. In a number of European countries, for example, governments have tried to increase or

fully guarantee depositors¶ savings. In other cases, banks have been nationalized (socializing

profits as well as costs, potentially.)

In the meanwhile, smaller businesses and poorer people rarely have such options for bail out

and rescue when they find themselves in crisis.

There seems to be little sympathy²and even growing resentment²for workers in the

financial sector, as they are seen as having gambled with other people¶s money, and hence

lives, while getting fat bonuses and pay rises for it in the past. Although in raw dollar terms

the huge pay rises and bonuses are small compared to the magnitude of the problem, the

encouragement such practices have given in the past, as well as the type of culture it creates,

is what has angered so many people.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 49/106

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 50/106

5 0

The f inanc ia l cr isis and wea lthy countr ies

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 51/106

5 1

The f inanc ia l cr isis and wea l thy countr ies

Many blame the greed of Wall Street for causing the problem in the first place because it is in

the US that the most influential banks, institutions and ideologues that pushed for the policies

that caused the problems are found.

The crisis became so severe that after the failure and buyouts of major institutions, the Bush

Administration offered a $700 billion bailout plan for the US financial system.

This bailout package was controversial because it was unpopular with the public, seen as a

bailout for the culprits while the ordinary person would be left to pay for their folly. The US

House of Representatives initial rejected the package as a result, sending shock waves around

the world.

It took a second attempt to pass the plan, but with add-ons to the bill to get the additional

congressmen and women to accept the plan.

However, as former Nobel prize winner for Economics, former Chief Economist of the

World Bank and university professor at Columbia University, Joseph Stiglitz, argued, the

plan ³remains a very bad bill:´

In Europe, starting with Britain, a number of nations decided to nationalize, or part-

nationalize some failing banks to try and restore confidence. The US resisted this approach at

first, as it goes against the rigid free market view the US has taken for a few decades now.

Eventually, the US capitulated and the Bush Administration announced that the US

government would buy shares in troubled banks.

This illustrates how serious this problem is for such an ardent follower of free market

ideology to do this (although free market theories were not originally intended to be applied

to finance, which could be part of a deeper root cause of the problem).

Perhaps fearing an ideological backlash, Bush was quick to say that buying stakes in banks

³is not intended to take over the free market, but to preserve it.´ Professor Ha-Joon Chang of

Cambridge University suggests that historically America has been more pragmatic about free

markets than their recent ideological rhetoric suggests, a charge by many in developing

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 52/106

5 2

countries that rich countries are often quite protectionist themselves but demand free markets

from others at all times.

While the US move was eventually welcomed by many, others echo Stieglitz¶s concern

above. For example, former Assistant Secretary of the Treasury Department in the Reaganadministration and a former associate editor of the Wall Street Journal , Paul Craig Roberts

also argues that the bailout should have been to help people with failing mortgages, not

banks: ³The problem, according to the government, is the defaulting mortgages, so the money

should be directed at refinancing the mortgages and paying off the foreclosed ones. And that

would restore the value of the mortgage-backed securities that are threatening the financial

institutions [and] the crisis would be over. So there¶s no connection between the

government¶s explanation of the crisis and its solution to the crisis.´

(Interestingly, and perhaps the sign of the times, while Europe and US consider more

socialist-like policies, such as some form of nationalization, China seems to be contemplating

more capitalist ideas, such as some notion of land reform, to stimulate and develop its

internal market. This, China hopes, could be one way to try and help insulate the country

from some of the impacts of the global financial crisis.)

Despite the large $700 billion US plan, banks have still been reluctant to lend. This led to the

US Fed announcing anot h er $800 billion stimulus package at the end of November. About

$600bn is marked to buy up mortgage-backed securities while $200bn will be aimed at

unfreezing the consumer credit market. This also reflects how the crisis has spread from the

financial markets to the ³real economy´ and consumer spending.

By February 2009, according to Bloomberg , the total US bailout is $9.7 trillion. Enough to

pay off more than 90 percent of America¶s home mortgages (although this bailout barely

helps homeowners).

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 53/106

53

A cr isis s igna li ng the dec li ne of US¶s superpower status?

Even before this global financial crisis took hold, some commentators were writing that the

US was in decline, evidenced by its challenges in Iraq and Afghanistan, and its declining

image in Europe, Asia and elsewhere.

The BBC also asked if the US¶s superpower status was shaken by this financial crisis:

The financial crisis is likely to diminish the status of the United States as the world¶s only

superpower. On the practical level, the US is already stretched militarily, in Afghanistan and

Iraq, and is now stretched financially. On the philosophical level, it will be harder for it to

argue in favor of its free market ideas, if its own markets have collapsed.

Some see this as a pivotal moment.

The political philosopher John Gray, who recently retired as a professor at the London School

of Economics, wrote in the London paper The Observer: ³Here is a historic geopolitical shift,

in which the balance of power in the world is being altered irrevocably.

³The era of American global leadership, reaching back to the Second World War, is over«

The American free-market creed has self-destructed while countries that retained overall

control of markets have been vindicated.´

³How symbolic that Chinese astronauts take a spacewalk while the US Treasury Secretary is

on his knees.´

² Paul Reynold s , US s uperpower s tatu s is sh aken, BBC, October 1, 2008

Yet, others argue that it may be too early to write of the US:

The director of a leading British think-tank Chatham House, Dr Robin Niblett « argues that

we should wait a bit before coming to a judgment and that structurally the United States is

still strong.

³America is still immensely attractive to skilled immigrants and is still capable of producing

a Microsoft or a Google,´ he went on. ³Even its debt can be overcome. It has enormous

resilience economically at a local and entrepreneurial level.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 54/106

54

³And one must ask, decline relative to who? China is in a desperate race for growth to feed

its population and avert unrest in 15 to 20 years. Russia is not exactly a paper tiger but it is

stretching its own limits with a new strategy built on a flimsy base. India has huge internal

contradictions. Europe has usually proved unable to jump out of the doldrums as dynamically

as the US.

³But the US must regain its financial footing and the extent to which it does so will also

determine its military capacity. If it has less money, it will have fewer forces.´

² Paul Reynold s , US s uperpower s tatu s is sh aken, BBC, October 1, 2008

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 55/106

55

Europe and the f inanc ia l cr isis

In Europe, a number of major financial institutions failed. Others needed rescuing.

In Iceland, where the economy was very dependent on finance sector, economic problems

have hit them hard. The banking system virtually collapsed and the government had to

borrow from the IMF and other neighbors to try and rescue the economy. In the end, public

dissatisfaction at the way the government was handling the crisis meant the Iceland

government fell

A number of European countries have attempted different measures (as they seemed to have

failed to come up with a united response).

For example, some nations have stepped in to nationalize or in some way attempt to provideassurance for people. This may include guaranteeing 100% of people¶s savings or helping

broker deals between large banks to ensure there isn¶t a failure.

The EU is also considering spending increases and tax cuts to be worth ¼200 billion over two

years. The plan is supposed to help restore consumer and business confidence, Shore up

employment, getting the banks lending again, and promoting green technologies.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 56/106

5 6

As ia and the f inanc ia l cr isis

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 57/106

57

As ia and the f inanc i a l cr isis

Countries in Asia are increasingly worried about what is happening in the West. A number of

nations urged the US to provide meaningful assurances and bailout packages for the US

economy, as that would have a knock-on effect of reassuring foreign investors and helping

ease concerns in other parts of the world.

Many believed Asia was sufficiently decoupled from the Western financial systems. Asia has

not had a subprime mortgage crisis like many nations in the West have, for example. Many

Asian nations have witnessed rapid growth and wealth creation in recent years. This lead to

enormous investment in Western countries. In addition, there was increased foreign

investment in Asia, mostly from the West.

However, this crisis has shown that in an increasingly inter-connected world means there arealways knock-on effects and as a result, Asia has had more exposure to problems stemming

from the West. Many Asian countries have seen their stock markets suffer and currency

values going on a downward trend. Asian products and services are also global, and a

slowdown in wealthy countries means increased chances of a slowdown in Asia and the risk

of job losses and associated problems such as social unrest.

India and China are the among the world¶s fastest growing nations and after Japan, are the

largest economies in Asia. From 2007 to 2008 India¶s economy grew by a whopping 9%.

Much of it is fueled by its domestic market. However, even that has not been enough to

shield it from the effect of the global financial crisis, and it is expected that in data will show

that by March 2009 that India¶s growth will have slowed quickly to 7.1%. Although this is a

very impressive growth figure even in good times, the speed at which it has dropped²the

sharp slowdown²is what is concerning.

China, similarly has also experienced a sharp slowdown and its growth is expected to slow

down to 8% (still a good growth figure in normal conditions). However, China also has a

growing crisis of unrest over job losses. Both have poured billions into recovery packages.

Japan, which has suffered its own crisis in the 1990s also faces trouble now. While their

banks seem more secure compared to their Western counterparts, it is very dependent on

exports. Japan is so exposed that in January alone, Japan¶s industrial production fell by 10%,

the biggest monthly drop since their records began.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 58/106

58

Towards the end of October 2008, a major meeting between the EU and a number of Asian

nations resulted in a joint statement pledging a coordinated response to the global financial

crisis. However, as Inter Press Service (I PS) reported, this coordinated response is dependent

on the entry of Asia¶s emerging economies into global policy-setting institutions.

This is very significant because Asian and other developing countries have often been treated

as second-class citizens when it comes to international trade, finance and investment talks.

This time, however, Asian countries are potentially trying to flex their muscle, maybe

because they see an opportunity in this crisis, which at the moment mostly affects the rich

West.

Asian leaders had called for ³effective and comprehensive reform of the international

monetary and financial systems.´ For example, as I PS also noted in the same report, one of

the Chinese state-controlled media outlets demanded that ³We want the U.S. to give up its

veto power at the International Monetary Fund and European countries to give up some more

of their voting rights in order to make room for emerging and developing countries.´ They

also added, ³And we want America to lower its protectionist barriers allowing an easier

access to its markets for Chinese and other developing countries¶ goods.´

Whether this will happen is hard to know. Similar calls by other developing countries and

civil society around the world, for years, have come to no avail. This time however, the

financial crisis could mean the US is less influential than before. A side-story of the emergingChinese superpower versus the declining US superpower will be interesting to watch.

It would of course be too early to see China somehow using this opportunity to decimate the

US, economically, as it has its own internal issues. While the Western mainstream media has

often hyped up a ³threat´ posed by a growing China, the World Bank¶s chief economist (Lin

Yifu, a well respected Chinese academic) notes ³Relatively speaking, China is a country with

scarce capital funds and it is hardly the time for us to export these funds and pour them into a

country profuse with capital like the U.S.´

Asian nations are mulling over the creation of an alternative Asia foreign exchange fund, but

market shocks are making some Asian countries nervous and it is not clear if all will be able

to commit.

What seems to be emerging is that Asian nations may have an opportunity to demand more

fairness in the international arena, which would be good for other developing regions, too.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 59/106

59

G loba l Me ltdown and i ts I mpact on the I nd ian Economy

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 60/106

60

G loba l Me l tdown and i ts I mpact on the I nd ian Economy

With the collapse of Lehman Brothers and other Wall Street icons, there was growing

recession which affected the US, the European Union (EU) and Japan. This was the result of

large scale defaults in the US housing market as the banks went on providing risky loans

without adequate security and the repaying capacity of the borrower. The principal source of

transmission of the crisis has been the real sector, generally referred to as the µMain Street¶.

This crisis engulfed the United States in the form of creeping recession and this worsened the

situation. As a consequence, US demand for imports from other countries indicated a decline.

The basic cause of the crisis was largely an unregulated environment, mortgage lending to

subprime borrowers. Since the borrowers did not have adequate repaying capacity and also

because subprime borrowing had to pay two-to-three percentage points higher rate of interest

and they have a history of default, the situation became worse. But once the housing market

collapsed, the lender institutions saw their balance-sheets go into red.

Although at one time it was thought that this crisis would not affect the Indian economy, later

it was found that the Foreign Direct Investment (FDI) started drying up and this affected

investment in the Indian economy. It was, therefore, felt that the Indian economy will grow at

about seven per cent in 2008-09 and at six per cent in 2009-10. The lesson of this experience

is that India must exercise caution while liberalising its financial sector.

A redeeming feature of the current crisis is that its magnitude is much lesser than that of the

Great Depression of the 1930s when unemploy-ment rate in the United States exceeded 25

per cent. Currently, it stands at 6.5 per cent and is predicted to remain around eight per cent

in 2009.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 61/106

61

The industries most affected by weakening demand were airlines, hotels, real estate. Besides

this, Indian exports suffered a setback and there was a setback in the production of export-

oriented sectors. The government advised the sectors of weakening demand to reduce prices.

It provided some relief by cutting down excise duties, but such simplistic solutions were

doomed to failure. Weakening demand led to producers cutting production. To reduce theimpact of the crisis, firms reduced their workforce, to reduce costs. This led to increase in

unemployment but the total impact on the economy was not very large. Industrial production

and manufacturing output declined to five per cent in the last quarter of 2008-09.

Consequently, a vicious cycle of weak demand and falling output developed in the Indian

economy.

A weakening of demand in the US affected our IT and Business Process Outsourcing (B PO )

sector and the loss of opportunities for young persons seeking employment at lucrativesalaries abroad. India¶s famous IT sector, which earned about $ 50 billion as annual revenue,

is expected to fall by 50 per cent of its total revenues. This would reduce the cushion to set

off the deficit in balance of trade and thus enlarge our balance of payments deficit. It has now

been estimated that sluggish demand for exports would result in a loss of 10 million jobs in

the export sector alone.

To lift the economy out of the recession the Government announced a package of Rs 35,000

crores in the first instance on December 7, 2008. The main areas to benefit were the

following:

(a) Housing²A refinance facility of Rs 4000 crores was provided to the National Housing

Bank. Following this, public sector banks announced to provide small home loans seekers

loans at reduced rates to step up demand in retail housing sector.

(i) Loans up to Rs 5 lakhs: Maximum interest rate fixed at 8.5 per cent.

(ii) Loans from Rs 5-20 lakhs: Maximum interest rate at 9.25 per cent.

(iii) No processing charges to be levied on borrowers.

(iv) No penalty to be charged in case of pre-payment.

(v) Free life insurance cover for the entire outstanding amount.

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 62/106

6 2

This means a borrower can get a loan up to 90 per cent of the value of the house. The

government hopes to disburse Rs 15,000 to 20,000 crores under the new package.

The housing package is the core of the government¶s new fiscal policy. It will give a fillip to

other sectors such as steel, cement, brick kilns etc. Besides, the small and medium industries(SMEs) too get a boost by manufacturing all kinds of fittings and furnishings.

The success of the housing package will, however, depend on the State governments efforts

to free up surplus land so that land prices come down and the cost of housing becomes

reasonable.

(b) Textiles²Due to declining orders from the world¶s largest market the United States, the

textile sector has been seriously affected. An allocation of Rs 1400 crores has been made to

clear the entire backlog in the Technology Upgradation Fund (TUF) scheme.

The Apparel Export Promotion Council (AE PC) Chairman, however, said: ³It is a

disappointing package. The allocation of Rs. 1,400 crores has been pending for many years

and thus, it is the payment of arrears only. There is nothing new in it. It would have been

much better if more concrete measures have been taken to reverse the downturn in the

exports of readymade garments and avoid further job losses in the textile sector.´

© Infrastructure²The government has been proclaiming that infrastructure is the engine of

growth. To boost the infrastructure, the India Infrastructure Finance Company Ltd. (IIFCL)

has been authorised to raise Rs 14,000 crores through tax-free bonds. These funds will be

used to finance infrastructure, more especially highways and ports. It may be mentioned that

µrefinance¶ refers to the replacement of an existing debt obligation with a debt obligation

bearing better terms, meaning thereby at lower rates or a changed repayment schedule. The

IIFCL will be permitted to raise further resources by the issue of such bonds so that a public-

private partnership ( PPP ) programme of Rs 1,00,000 crores in the highway sector is

promoted.

(d) Exports²Exports which accounted for 22 per cent of the GD P are expected to fall by 12

per cent. The government¶s fiscal package provides an interest rate subsidy of two per cent on

exports for the labour±intensive sectors such as textiles, handicrafts, leather, gems and

jewellery, but the Federation of Indian Export Organization (FIE O) felt the measures are not

8/7/2019 Global Financial Crisis complete

http://slidepdf.com/reader/full/global-financial-crisis-complete 63/106

6 3

enough as they will not make the exports price-competitive and, therefore, will not boost

exports. G.K. Pillai, the Commerce Secretary, has estimated a loss of 1.5 million jobs in the

export sector alone during 2008-09 on account of the $15 billion decline in the expected

exports.

(e) Small and Medium Enterprises (SMEs)²The government has announced a guarantee

cover of 50 per cent for loans between Rs 50 lakhs to Rs 1 crore for SMEs. The lockin period

for loans covered under the existing schemes will be reduced from 24 months to 18 months to

encourage banks to cover more loans under the scheme. Besides, the government will instruct

state-owned companies to ensure prompt payment of bills of SMEs so that they do not suffer