Embed Size (px)

Citation preview

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 1/80

NEW YEAR 2016

THE GLOBALINVESTMENTOUTLOOKRBC Investment Strategy Committee

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 2/80

The RBC Investment Strategy Committee consists

of senior investment professionals drawn from

across RBC Global Asset Management. The

Committee regularly receives economic and

capital markets related input from internal and

external sources. Important guidance is provided

by the Committee’s regional advisors (North

America, Europe, Far East), from the Global

Fixed Income & Currencies Subcommittee and

and healthcare, consumer discretionary and

consumer staples, industrials and utilities,

energy and materials, telecommunications and

technology). From this it builds a detailed global

investment forecast looking one year forward.

The Committee’s view includes an assessment

as the expected course of interest rates, major

From this global forecast, the RBC Investment

that can be used to manage portfolios.

These include:

instruments, and equities

income and equity portfolios

investments

the suggested sector and geographic make-up

within equity portfolios

the preferred exposure to major currencies

Results of the Committee’s deliberations are

published quarterly in The Global Investment

Outlook.

THE RBC INVESTMENT

STRATEGY COMMITTEE

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 3/80

CONTENTS

EXECUTIVE SUMMARY 2The Global Investment Outlook

Sarah Riopelle, CFA – V.P. & Senior Portfolio Manager,RBC Global Asset Management Inc.

Daniel E. Chornous, CFA RBC Global Asset Management Inc.

ECONOMIC & CAPITAL MARKETS FORECASTS 4RBC Investment Strategy Committee

RECOMMENDED ASSET MIX 5RBC Investment Strategy Committee

CAPITAL MARKETS PERFORMANCE 10 Milos Vukovic, MBA, CFA – Vice President &Head of Investment Policy,RBC Global Asset Management Inc.

GLOBAL INVESTMENT OUTLOOK 13Girding for rate hikes and geopolitical risks

Eric Lascelles – Chief Economist,RBC Global Asset Management Inc.

Eric Savoie, MBA, CFA – Senior Analyst, Investment Strategy,RBC Global Asset Management Inc.

Daniel E. Chornous, CFA RBC Global Asset Management Inc.

GLOBAL FIXED INCOME MARKETS 46Soo Boo Cheah, MBA, CFA – Senior Portfolio Manager,RBC Global Asset Management (UK) Limited

Suzanne Gaynor – V.P. & Senior Portfolio Manager,RBC Global Asset Management Inc.

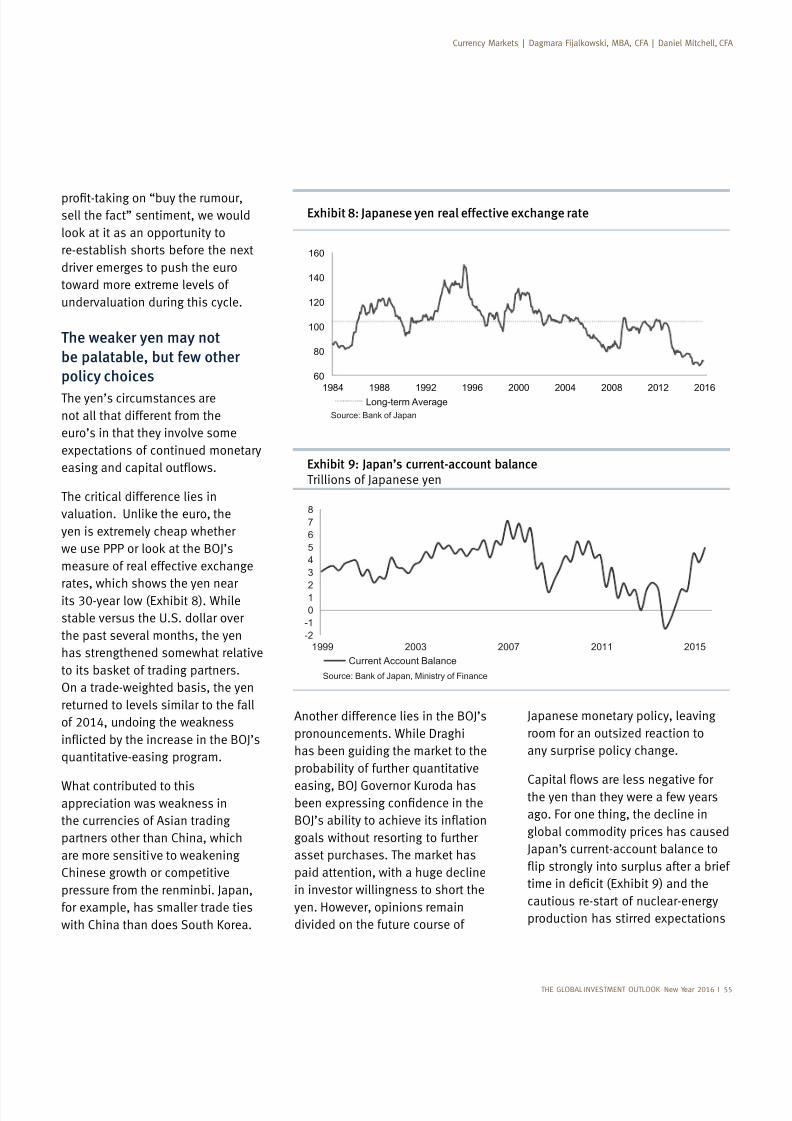

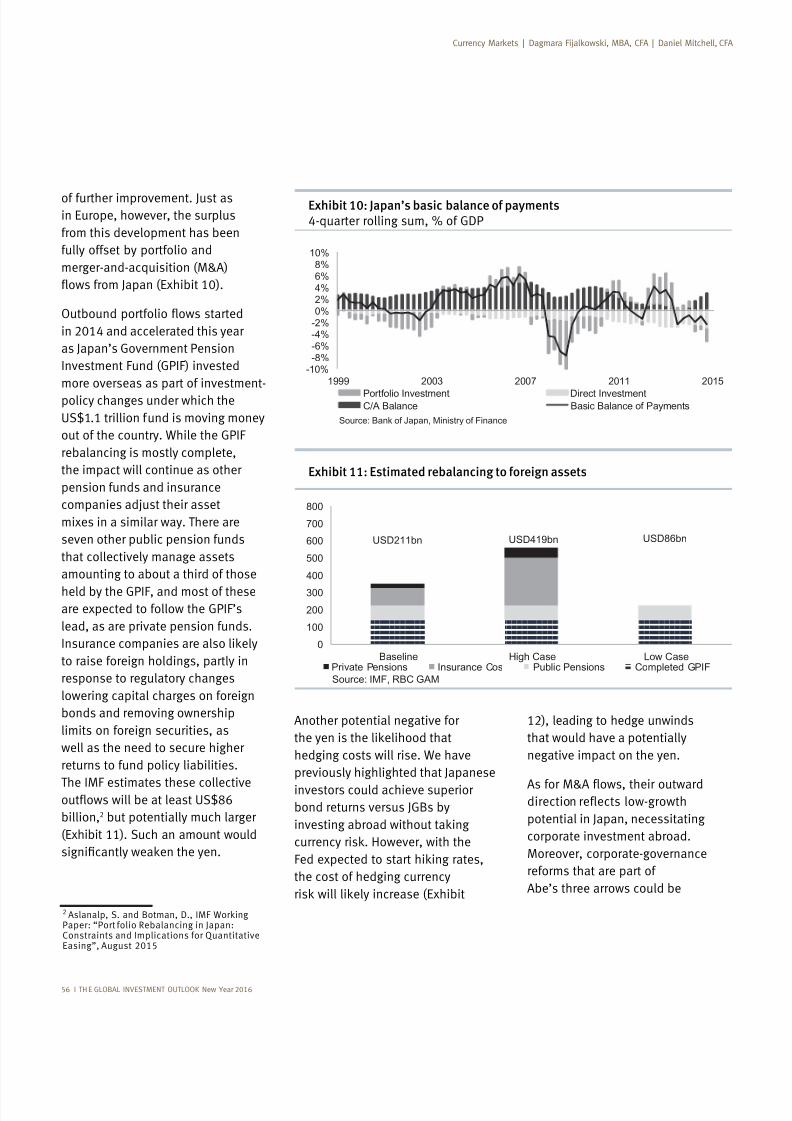

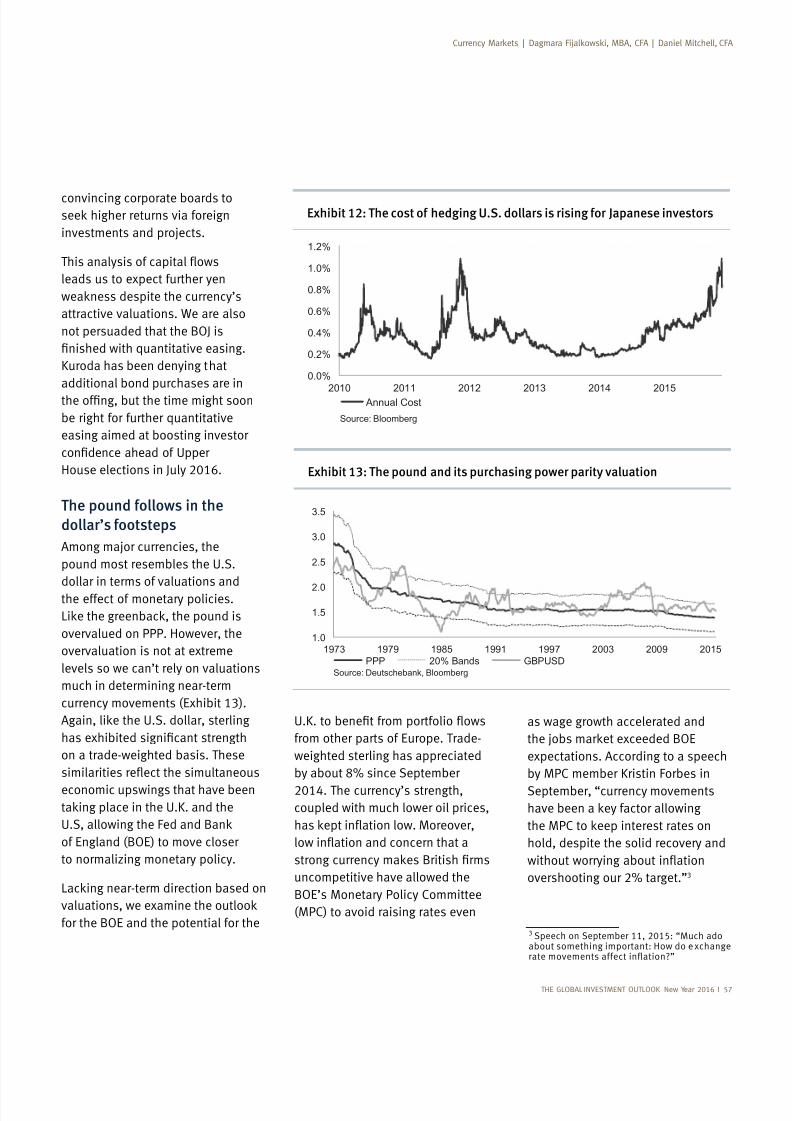

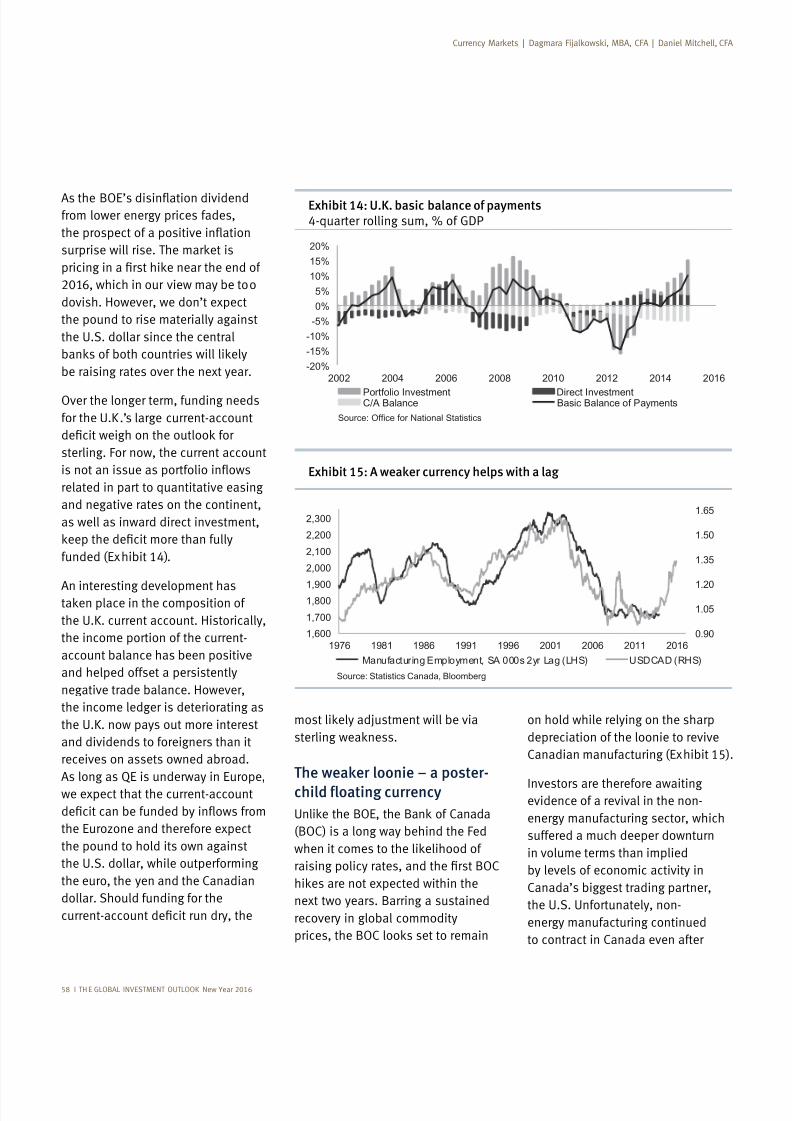

CURRENCY MARKETS 52Dagmara Fijalkowski, MBA, CFA – Head, Global Fixed Incomeand Currencies (Toronto and London),

Daniel Mitchell, CFA – Portfolio Manager,RBC Global Asset Management Inc.

WHY THIS TIME IS DIFFERENT 61Taylor Self, MBA – Analyst,Global Fixed Income and Currencies,RBC Global Asset Management Inc.

REGIONAL EQUITY MARKET OUTLOOK

United States 64Raymond Mawhinney – Senior V.P. & Senior Portfolio Manager,RBC Global Asset Management Inc.

Brad Willock, CFA – V.P. & Senior Portfolio Manager,RBC Global Asset Management Inc.

Canada 66Stuart Kedwell, CFA – Senior V.P. & Senior Portfolio Manager,RBC Global Asset Management Inc.

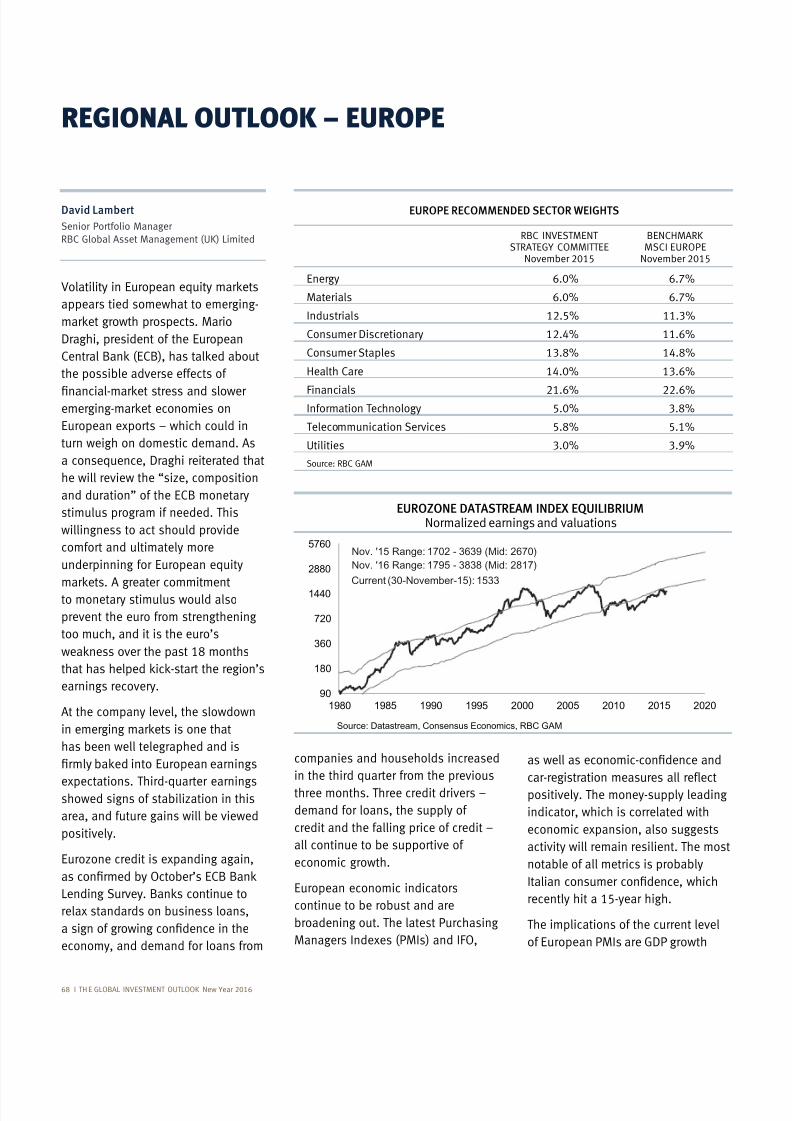

Europe 68David Lambert – Senior Portfolio Manager,RBC Global Asset Management (UK) Limited

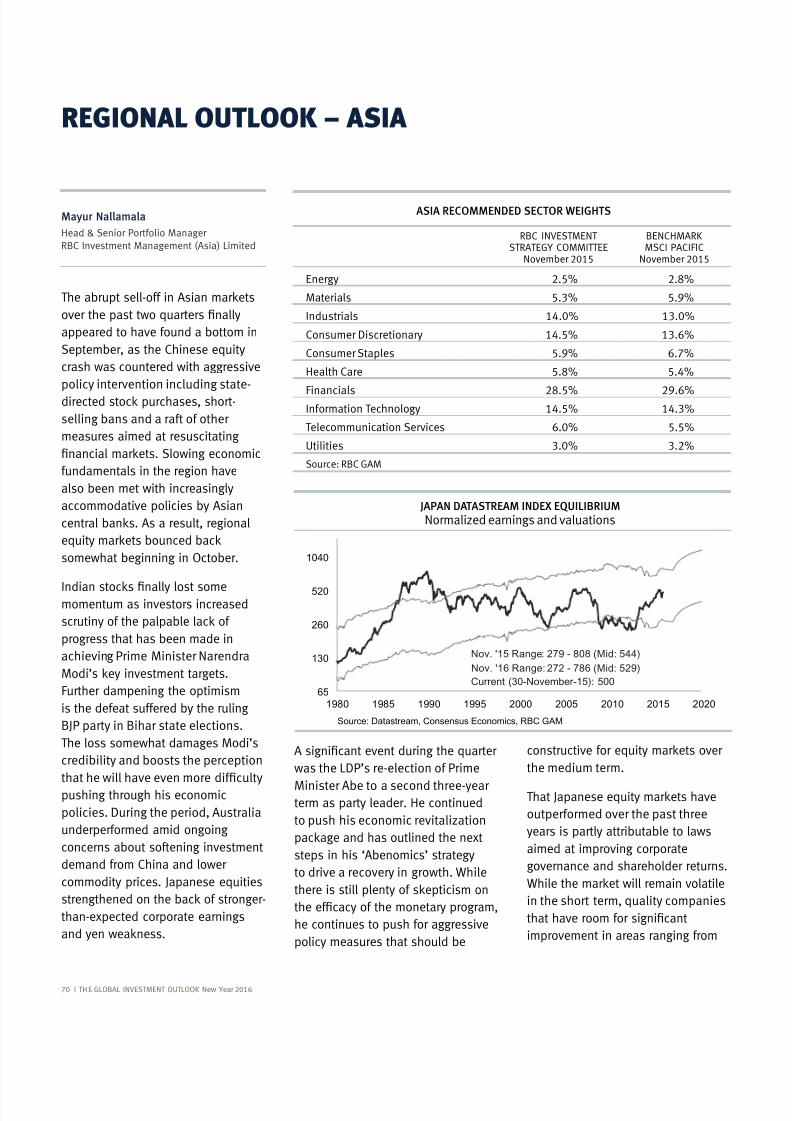

Asia 70Mayur Nallamala – Head & Senior Portfolio Manager,RBC Investment Management (Asia) Limited

Emerging Markets 72 Veronique Erb – Portfolio Manager,RBC Global Asset Management (UK) Limited

RBC INVESTMENT STRATEGY COMMITTEE 74

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 1

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 4/80

creating a challenging environment

for investors. The geopolitical

environment has been fraught

quite some time, and this is only

increasing. The most salient recent

developments relate to ISIS, but there

are also long-term trends brewing

with regard to the polarization of

developed-world politics, Russia’sincreased aggression and China’s

growing global clout. Although

recently stabilized and it continues

to defy hard-landing fears. We would

the prospect of tighter U.S. monetary

policy to the list of headwinds that we

are monitoring closely.

Minor revisions to our

economic forecasts

Global economic growth has

unquestionably slowed over the

past year, with some concerned that

the process is accelerating into a

more severe correction. We fail to

the recent downward trend in the

U.S. ISM Index, the latest batch of

leading indicators has tentatively

pushed higher and global industrial

production remains fairly normal-

higher in the leading indicators

proves prescient, current levels

remain inconsistent with a global

recession. We have made only minor

quarter, nudging them slightly lower

Economic data remains

uninspiring in most regions,

although the threat ofrecession seems modest.

While we continue to expect

moderate economic growth,

we recognize that warning

signs are more and more

evident and that it is prudent

to raise the alert status. The

downward trend for the U.S.

ISM Index, sluggish corporate

based indicators, including a

sustained widening of high-

yield-bond spreads, sensitizes

us to the possibility that

the business cycle may be

maturing. Sovereign-bond

yields have traded in a fairly

tight range over the last quarter

still mostly below the levels of

last summer, they have been

of the year. We expect the

heightened level of volatility

to persist over the coming

quarters.

Sarah Riopelle, CFA

Vice President & Senior Portfolio Manager

RBC Global Asset Management Inc.

Daniel E. Chornous, CFA

RBC Global Asset Management Inc.

2 I T HE GLOBAL INVESTMENT OUTLOOK New Year 2016

EXECUTIVE SUMMARY

U.S. dollar bull marketmaturing

Many investors expect continued

dollar strength, and they may be

correct given that previous dollar

incredible dollar strength. The

prospect of policy normalizationby the U.S. Federal Reserve (Fed),

coupled with expansionary monetary

policies elsewhere, means that

run. However, with the U.S. dollar

no longer deeply undervalued and

the prospect of volatility rising, our

four major currencies we expect most

and the Canadian dollar, leaving thepound little changed in our forecasts.

move higher

of the commodity supercycle has

effect over the past few years.

However, we believe the downward

abate as resource prices have largely

completed their swoon and there

is the potential for modest gains

in some commodities in the years

ahead. We continue to believe that

threat remains limited. We can

low today, and those pressures are

inherently temporary. Altogether, we

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 5/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 3

supportive of higher equity prices

going forward. With higher valuation

in 2016 and 2017, but given that

earnings estimates have been coming

down for most of this year, this bears

watching.

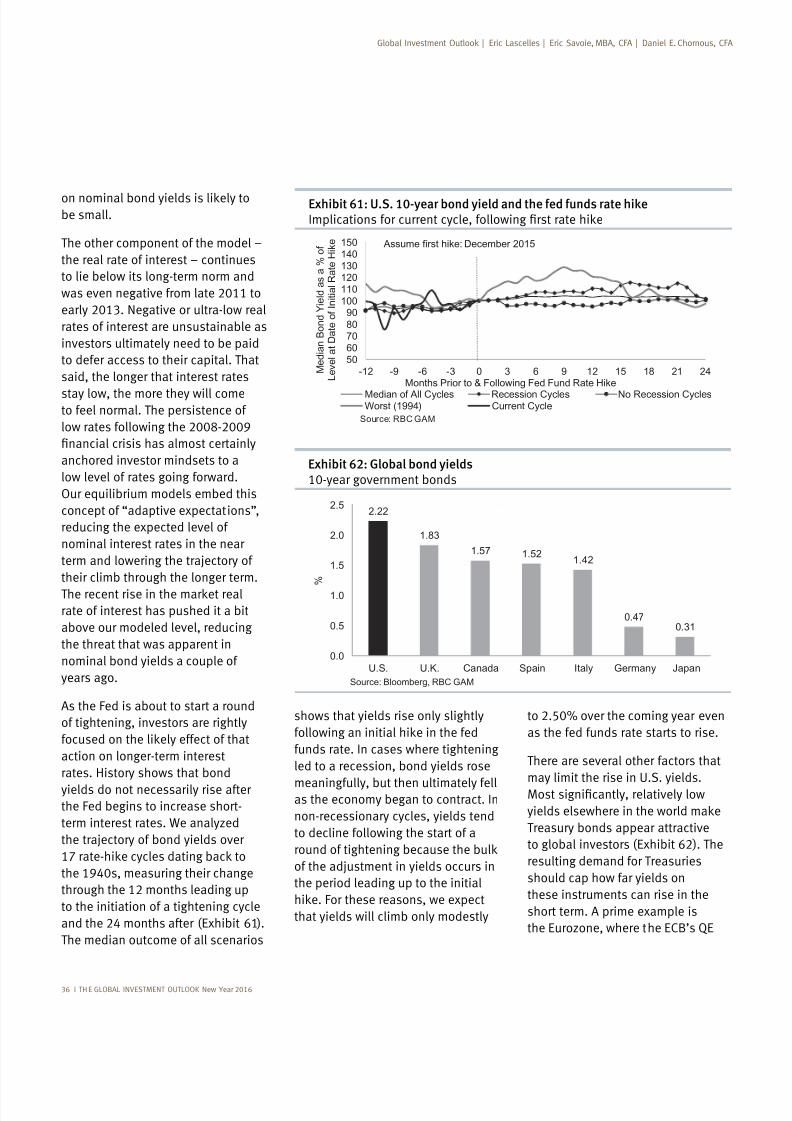

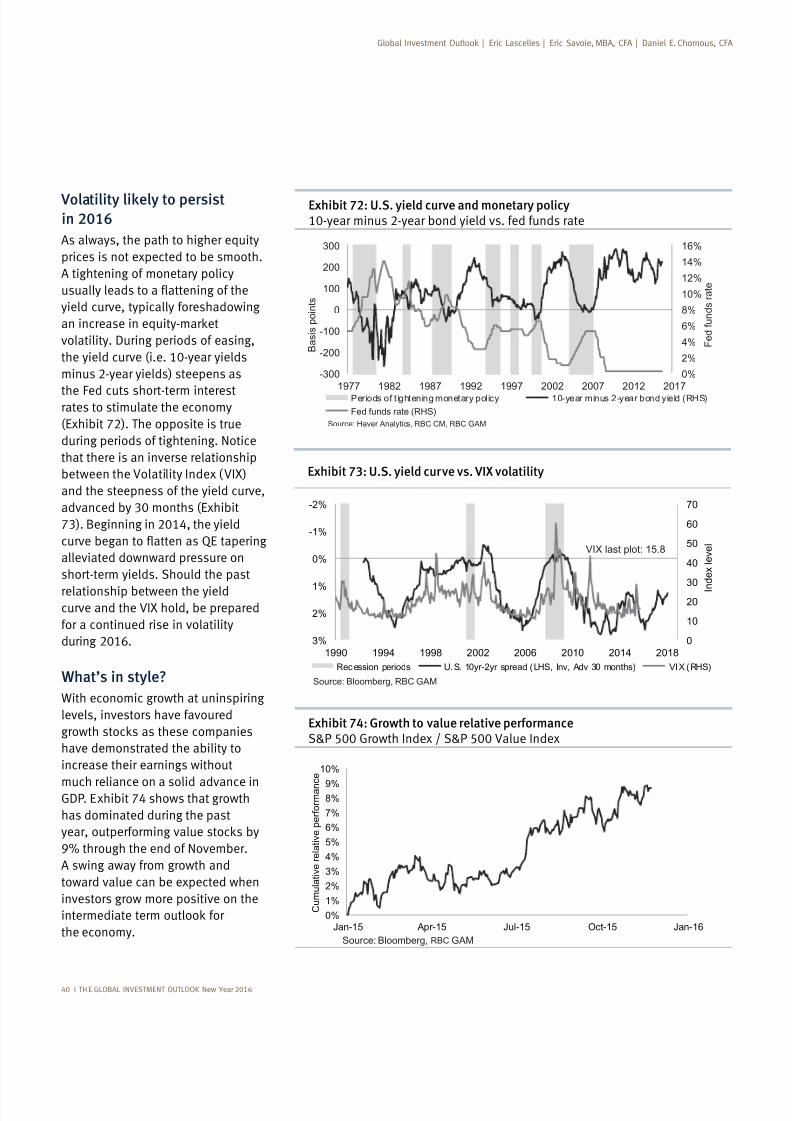

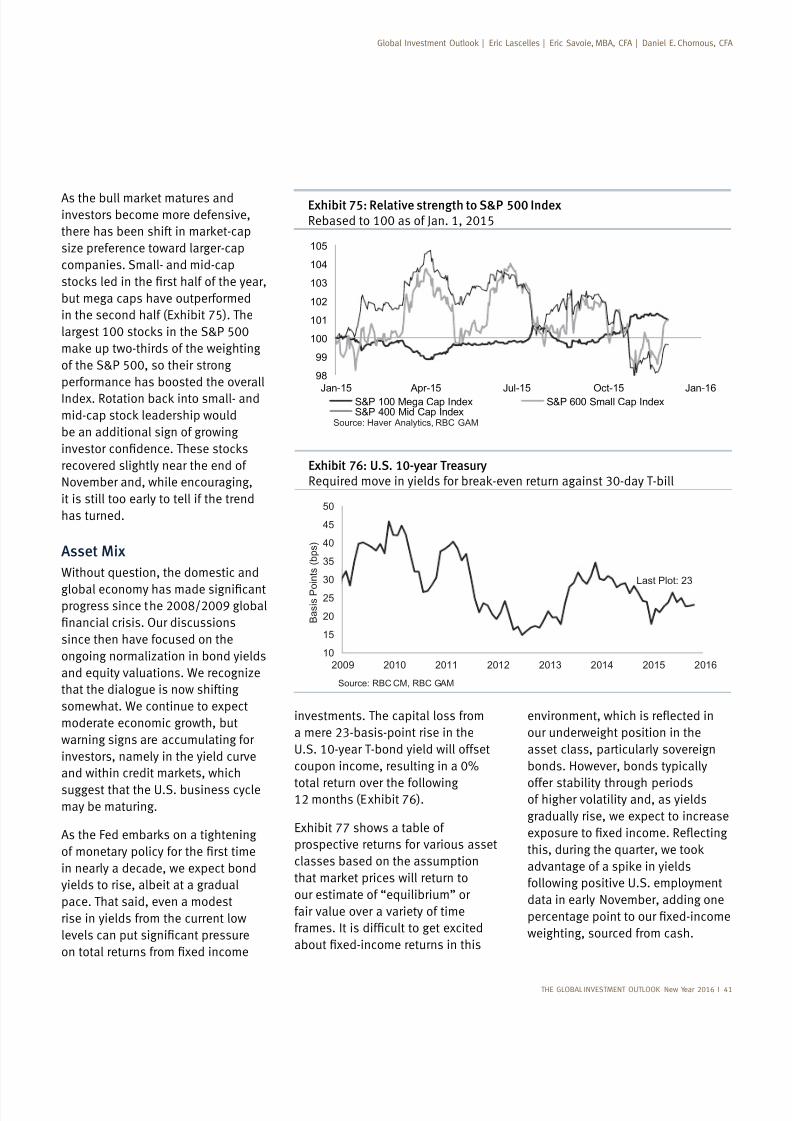

A little less underweight bondsAs the Fed begins a new tightening

cycle, we expect bond yields to rise,

albeit at a gradual pace. That said,

even a modest rise in yields from the

pressure on bond returns. However,

bonds offer stability through periods

of higher volatility and, as yields rise,

we expect to increase our exposure

following positive U.S. employment

data and added one percentage

sourced from cash.

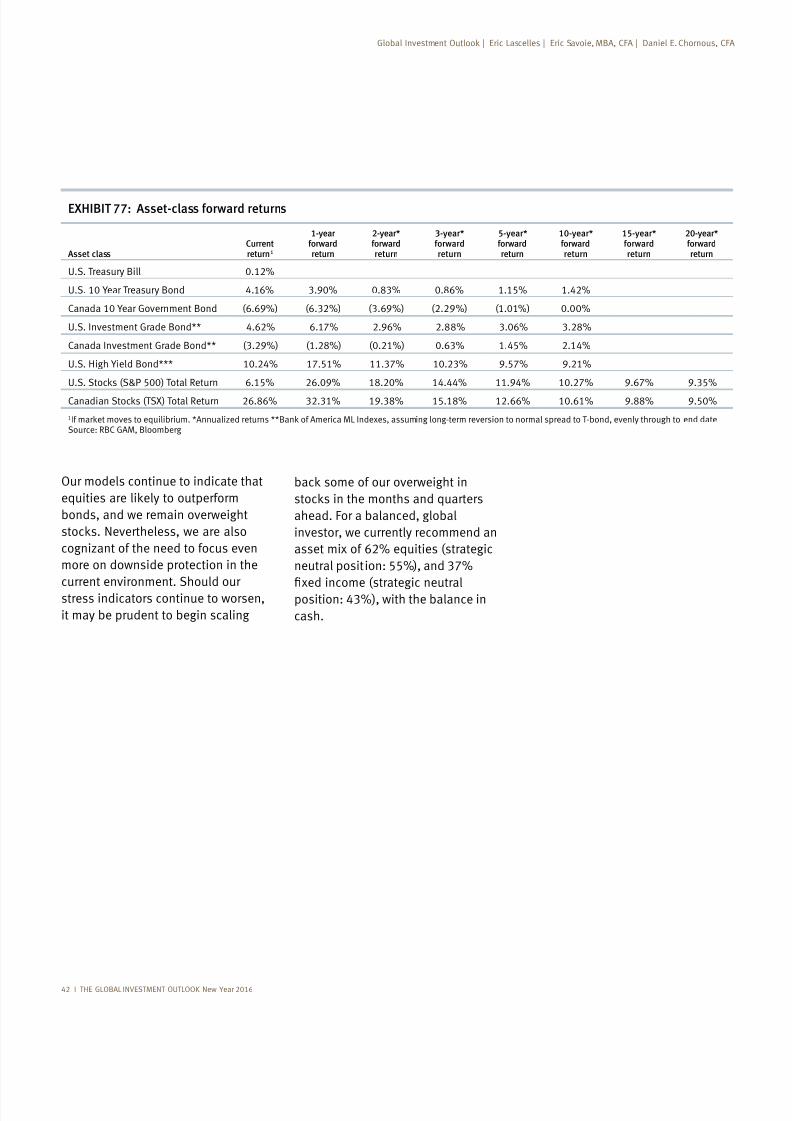

Our models continue to indicate

bonds so we remain overweight

this volatile investing environment.

Should our stress indicators worsen,

it may be prudent to begin scaling

in the months and quarters ahead.

For a balanced, global investor, we

recommend an asset mix of 62%

equities (strategic neutral position:

(strategic neutral position: 43%), with

the balance in cash.

bond yields higher over the comingquarters. However, there are a

number of factors that may discourage

to be patient, subtle and transparent

as it sets itself on the long path

to restoring “normal” monetary

conditions. In addition, relatively low

yields elsewhere in the world have

made U.S. Treasury bonds attractive

to global investors and the demand

for Treasuries should limit how far

yields can rise in the near term.

to outlook

volatility so far in 2015 driven by the

sideways or down through 2015

as valuations have moderated and

earnings estimates have experienced

constant negative revisions since the

end of 2014.

over the last few months has

bolstered the long-term return

fair value in the spring of 2015,

for periods of sustained growth,

Valuations are considerably more

attractive in Europe and other global

However, as expanding valuations

2016, but not all the way to a normallevel, and we suspect that the revival

will be a tad more gradual than the

Divergent monetary policies

The theme of diverging monetary

pronounced in the coming quarters.

entertaining the delivery of more

stimulus, the rationale generally

developed world and decelerating

other monetary policy extreme, the

Fed – is set to begin raising rates. We

the economy on its optimal growth

are priced for this outcome, and the

Fed has emphasized its desire toproceed with extreme caution, this

should not be overly problematic.

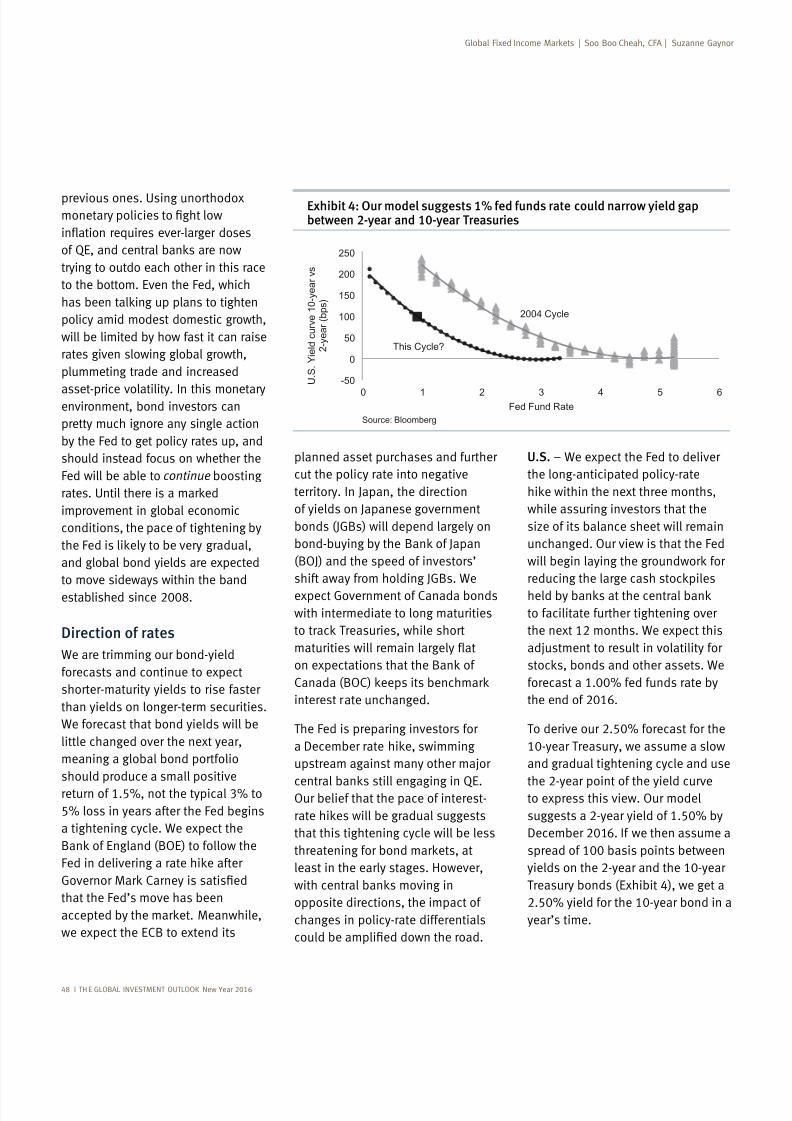

Forecasting a modest increase

in bond yields

Interest rates remain low and have

proven adept at defying widespread

forecasts over the past several years

that they would rise. There is a

especially given the downward

pressure that comes from ultra-

In the U.S., some of these conditions

seem more vulnerable to reversal

than they have been for some time.

new tightening cycle, rising short-

term interest rates should nudge

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 6/80

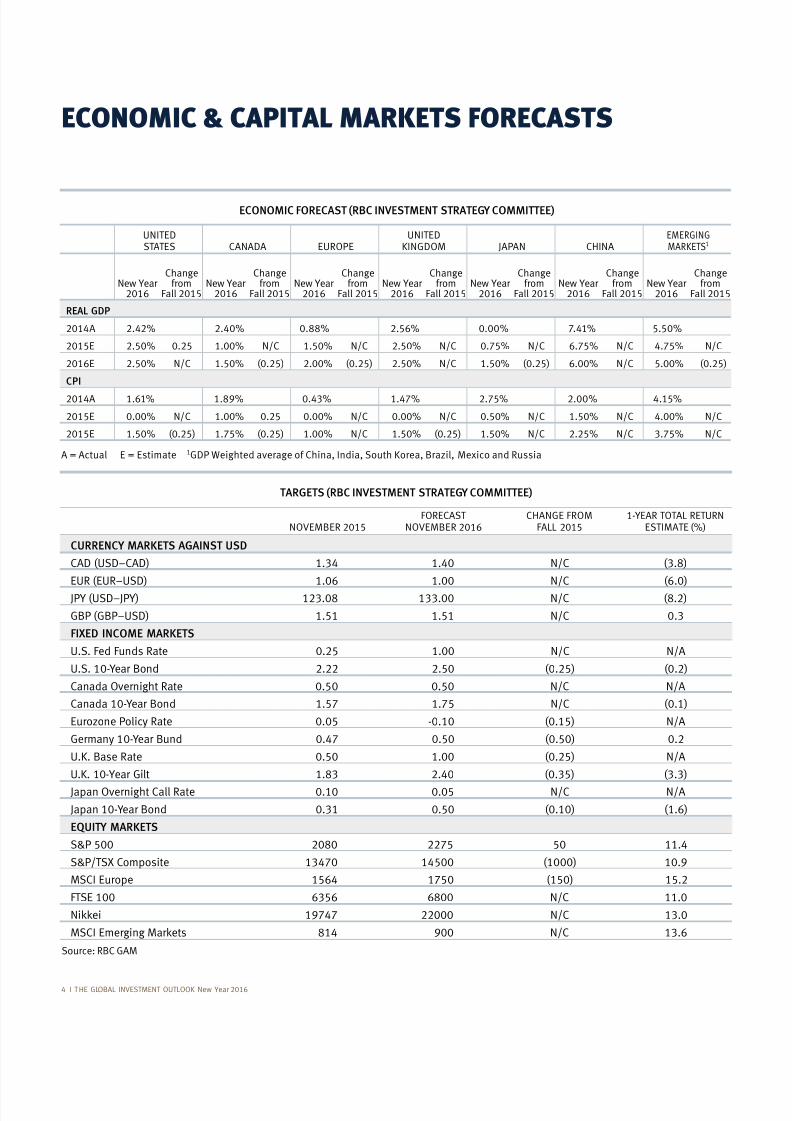

TARGETS (RBC INVESTMENT STRATEGY COMMITTEE)

NOVEMBER 2015FORECAST

NOVEMBER 2016CHANGE FROM

FALL 20151-YEAR TOTAL RETURN

ESTIMATE (%)

CURRENCY MARKETS AGAINST USD

1.34 1.40 N/C

1.06 1.00 N/C (6.0)

133.00 N/C

1.51 1.51 N/C 0.3

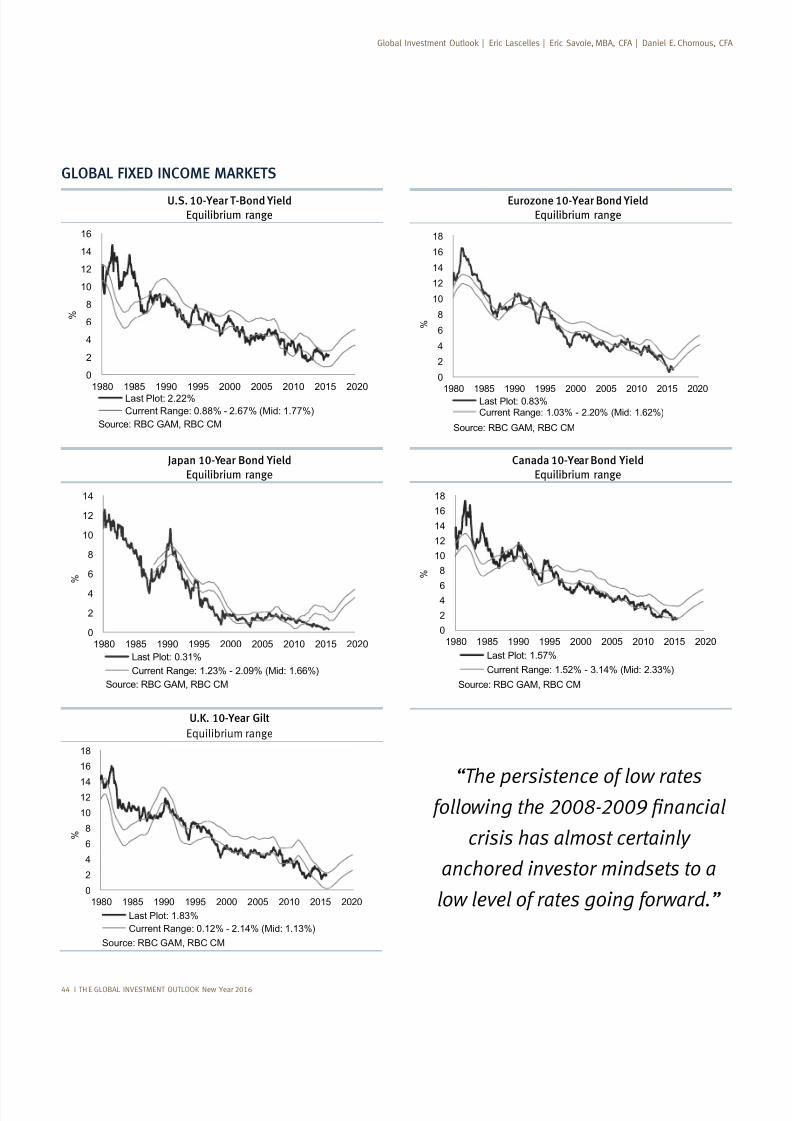

FIXED INCOME MARKETS

U.S. Fed Funds Rate 0.25 1.00 N/C N/A

U.S. 10-Year Bond 2.22 2.50 (0.25) (0.2)

Canada Overnight Rate 0.50 0.50 N/C N/A

Canada 10-Year Bond 1.57 1.75 N/C (0.1)

Eurozone Policy Rate 0.05 -0.10 (0.15) N/A

Germany 10-Year Bund 0.47 0.50 (0.50) 0.2

U.K. Base Rate 0.50 1.00 (0.25) N/A

U.K. 10-Year Gilt 2.40 (0.35) (3.3)

Japan Overnight Call Rate 0.10 0.05 N/C N/A

Japan 10-Year Bond 0.31 0.50 (0.10) (1.6)

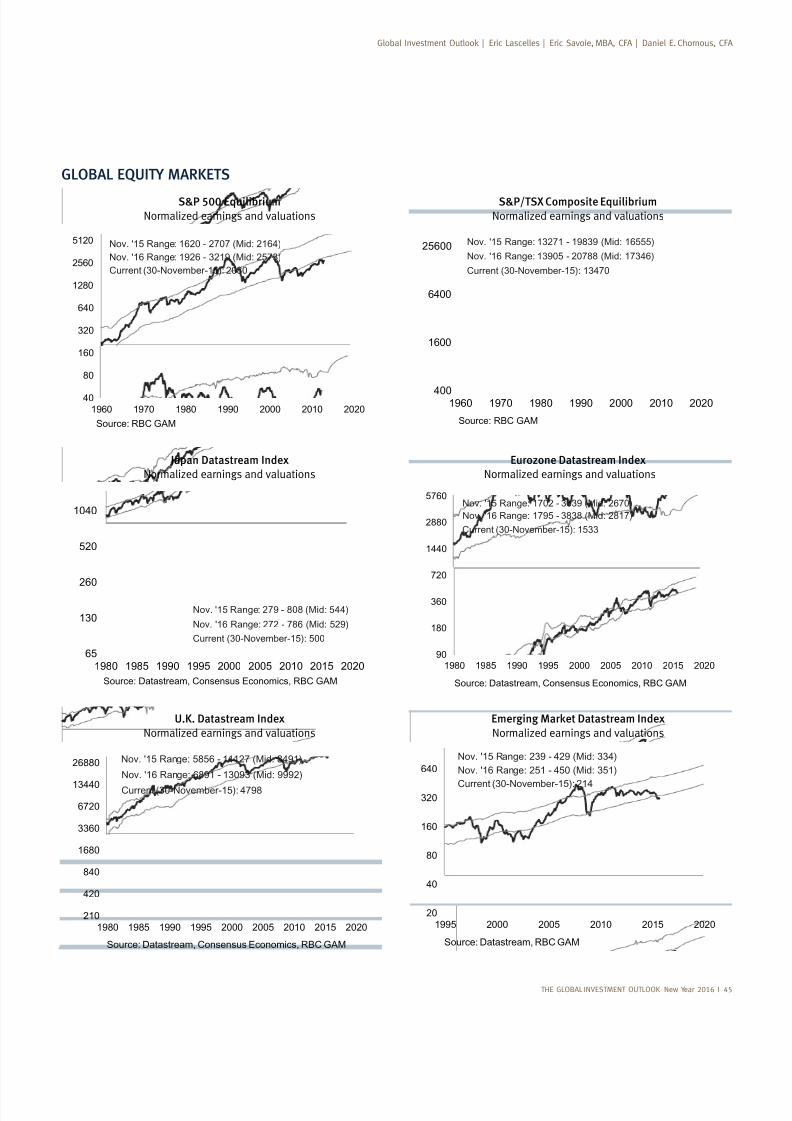

EQUITY MARKETS

S&P 500 2275 50 11.4

S&P/TSX Composite 13470 14500 (1000)

MSCI Europe 1564 1750 (150) 15.2

FTSE 100 6356 N/C 11.0

22000 N/C 13.0

N/C 13.6

Source: RBC GAM

ECONOMIC & CAPITAL MARKETS FORECASTS

ECONOMIC FORECAST (RBC INVESTMENT STRATEGY COMMITTEE)

UNITEDSTATES CANADA EUROPE

UNITEDKINGDOM JAPAN CHINA

EMERGINGMARKETS1

New Year2016

Changefrom

Fall 2015New Year

2016

Changefrom

Fall 2015New Year

2016

Changefrom

Fall 2015New Year

2016

Changefrom

Fall 2015New Year

2016

Changefrom

Fall 2015New Year

2016

Changefrom

Fall 2015New Year

2016

Changefrom

Fall 2015

REAL GDP

2014A 2.42% 2.40% 2.56% 0.00% 7.41% 5.50%

2015E 2.50% 0.25 1.00% N/C 1.50% N/C 2.50% N/C 0.75% N/C 6.75% N/C 4.75% N/C

2016E 2.50% N/C 1.50% (0.25) 2.00% (0.25) 2.50% N/C 1.50% (0.25) 6.00% N/C 5.00% (0.25)

CPI

2014A 1.61% 0.43% 1.47% 2.75% 2.00% 4.15%

2015E 0.00% N/C 1.00% 0.25 0.00% N/C 0.00% N/C 0.50% N/C 1.50% N/C 4.00% N/C

2015E 1.50% (0.25) 1.75% (0.25) 1.00% N/C 1.50% (0.25) 1.50% N/C 2.25% N/C 3.75% N/C

A = Actual E = Estimate 1

4 I T HE GLOBAL INVESTMENT OUTLOOK New Year 2016

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 7/80

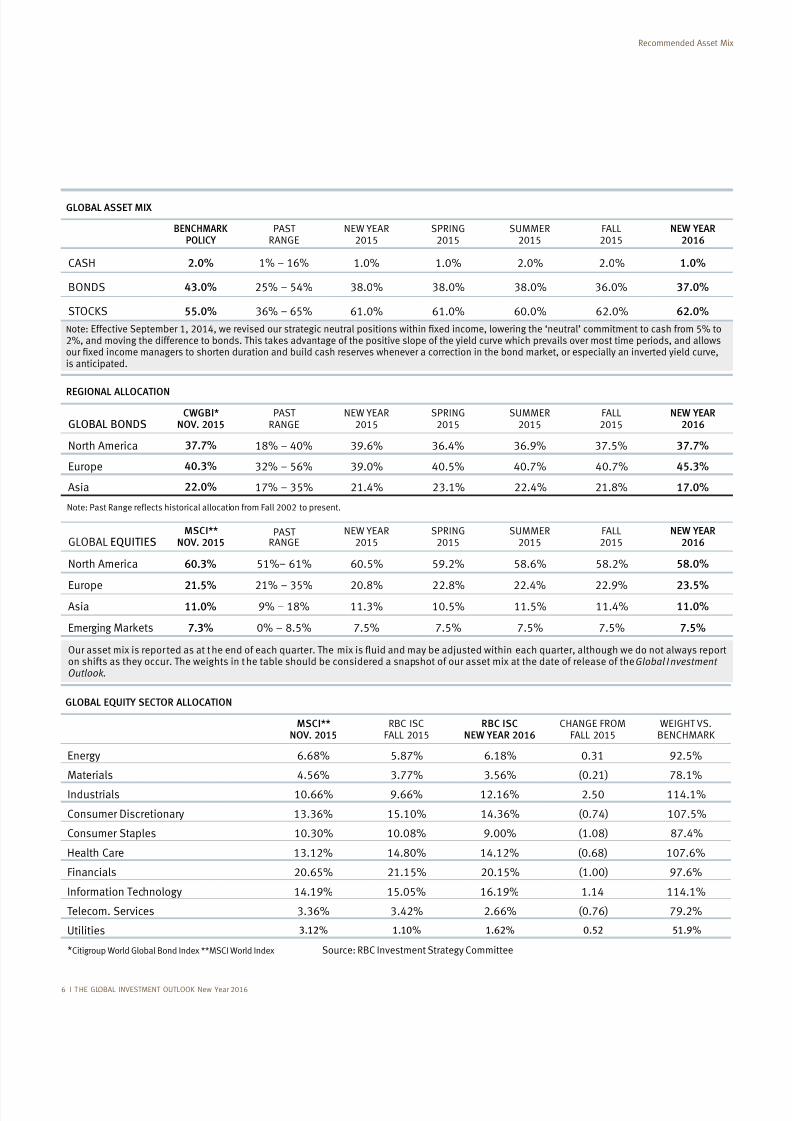

bonds and cash – should include both strategic and

tactical elements. Strategic asset mix addresses the blend

portfolio through many business and investment cycles,

independent of a near-term view of the prospects for the

Every individual has differing return expectations and

strategic asset mix. Based on a 35-year study of historical

returns and the volatility of returns (the range around

the average return within which shorter-term results

aggressive growth. It goes without saying that as investors

accept increasing levels of volatility, and therefore greater

presented below may assist investors in selecting a

strategic asset mix best aligned to their investment goals.

Each quarter, the RBC Investment Strategy Committee

publishes a recommended asset mix based on our current

view of the economy and return expectations for the

major asset classes. These weights are further divided

into recommended exposures to the variety of global

3 2

RECOMMENDED ASSET MIX

asset classes with a goal of tilting portfolios toward

term prospects.

serve as a guide for movement within the ranges allowed

way toward its upper limit of 70% for equities), that would

imply a tactical shift of + 5.02% to 25.02% for the Very

allowed range of +/- 15%).

The value-added of tactical strategies is, of course,

dependent on the degree to which the expected

scenario unfolds.

Regular reviews of portfolio weights are essential to the

ultimate success of an investment plan as they ensure

current exposures are aligned with levels of long-term

investors.

Anchoring portfolios with a suitable strategic asset mix,

tactical positioning, imposes discipline that can limit

damage caused by swings in emotion that inevitably

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 5

1. Average return:

2. Volatility: The standard deviation of returns. Standard deviation is a statistical measure that indicates the range around the averagereturn within which 2/3 of results will fall into, assuming a normal distribution around the long-term average.

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 8/80

*Citigroup World Global Bond Index **MSCI World Index Source: RBC Investment Strategy Committee

GLOBAL ASSET MIX

BENCHMARK

POLICY

PASTRANGE

NEW YEAR2015

SPRING2015

SUMMER2015

FALL2015

NEW YEAR

2016

CASH 2.0% 1% – 16% 1.0% 1.0% 2.0% 2.0% 1.0%

BONDS 43.0% 25% – 54% 36.0% 37.0%

STOCKS 55.0% 36% – 65% 61.0% 61.0% 60.0% 62.0% 62.0%

N is anticipated.

REGIONAL ALLOCATION

GLOBAL BONDSCWGBI*

NOV. 2015

PASTRANGE

NEW YEAR2015

SPRING2015

SUMMER2015

FALL2015

NEW YEAR

2016

North America 37.7% – 40% 36.4% 37.5% 37.7%

Europe 40.3% 32% – 56% 40.5% 40.7% 40.7% 45.3%

Asia 22.0% 17% – 35% 21.4% 23.1% 22.4% 17.0%

Note: Past Range reflects historical allocation from Fall 2002 to present.

GLOBAL EQUITIESMSCI**

NOV. 2015PAST

RANGENEW YEAR

2015SPRING

2015SUMMER

2015FALL2015

NEW YEAR

2016

North America 60.3% 51%– 61% 60.5% 58.0%

Europe 21.5% 21% – 35% 22.4% 23.5%Asia 11.0% – 11.3% 10.5% 11.5% 11.4% 11.0%

Emerging 7.3% 0% – 7.5% 7.5% 7.5% 7.5% 7.5%

on shifts as they occur. The weights in the table should be considered a snapshot of our asset mix at the date of release of the Global InvestmentOutlook.

GLOBAL EQUITY SECTOR ALLOCATION

MSCI**

NOV. 2015

RBC ISCFALL 2015

RBC ISC

NEW YEAR 2016

CHANGE FROMFALL 2015

WEIGHT VS.BENCHMARK

Energy 0.31

Materials 4.56% 3.77% 3.56% (0.21)

Industrials 10.66% 12.16% 2.50 114.1%

13.36% 15.10% 14.36% (0.74) 107.5%

Consumer Staples 10.30%

Health Care 13.12% 14.12% 107.6%

Financials 20.65% 21.15% 20.15% (1.00)

Information Technology 15.05% 1.14 114.1%

Telecom. Services 3.36% 3.42% 2.66% (0.76)

Utilities 3.12% 1.10% 1.62% 0.52 51.9%

6 I T HE GLOBAL INVESTMENT OUTLOOK New Year 2016

Recommended Asset Mix

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 9/80

Recommended Asset Mix

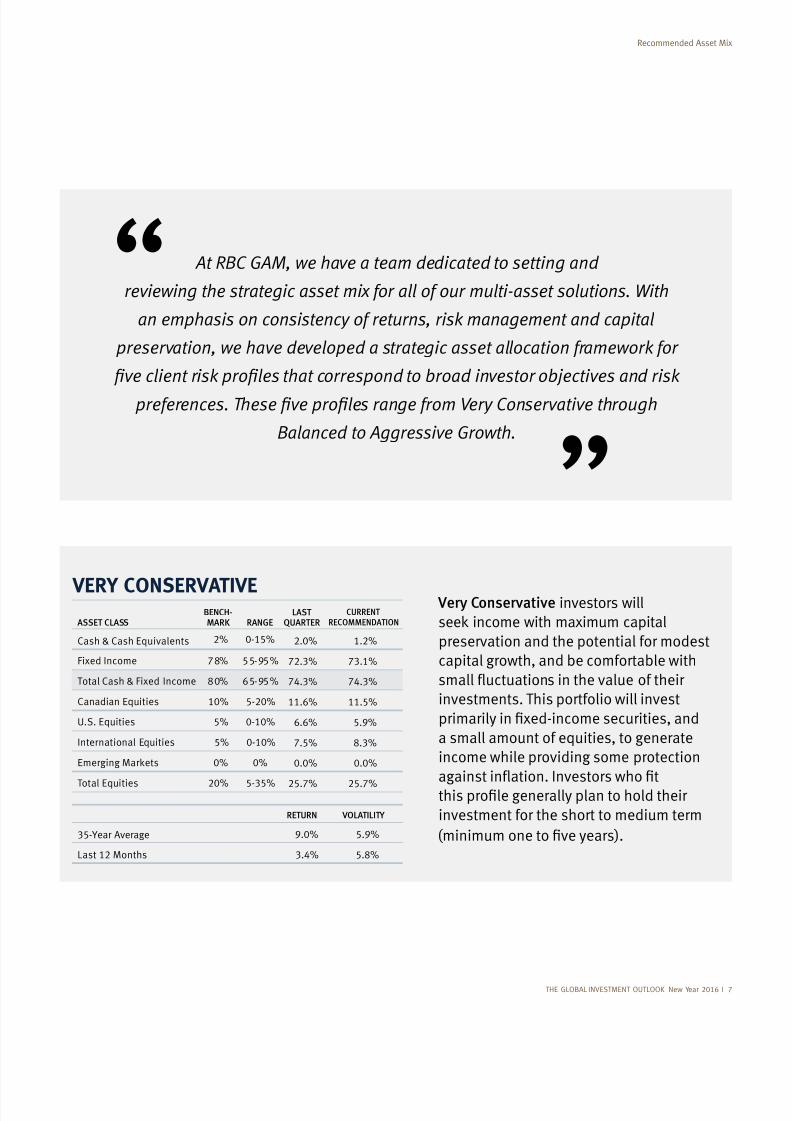

VERY CONSERVATIVE Very Conservative investors will

preservation and the potential for modest

capital growth, and be comfortable with

investments. This portfolio will invest

a small amount of equities, to generate

income while providing some protection

investment for the short to medium term

(minimum

ASSET CLASSBENCH-MARK RANGE

LASTQUARTER

CURRENT

RECOMMENDATION

Cash & Cash Equivalents 2% 0-15% 2.0% 1.2%

Fixed Income 72.3% 73.1%

Total Cash & Fixed Income 74.3% 74.3%

Canadian Equities 10% 5-20% 11.6% 11.5%

U.S. Equities 5% 0-10% 6.6%

International Equities 5% 0-10% 7.5%

0% 0% 0.0% 0.0%

Total Equities 20% 5-35% 25.7% 25.7%

RETURN VOLATILITY

35-Year Average

Last 12 Months 3.4%

At RBC GAM, we have a team dedicated to setting and

reviewing the strategic asset mix for all of our multi-asset solutions. With

an emphasis on consistency of returns, risk management and capital

preservation, we have developed a strategic asset allocation framework for

Balanced to Aggressive Growth.

“

”

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 7

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 10/80

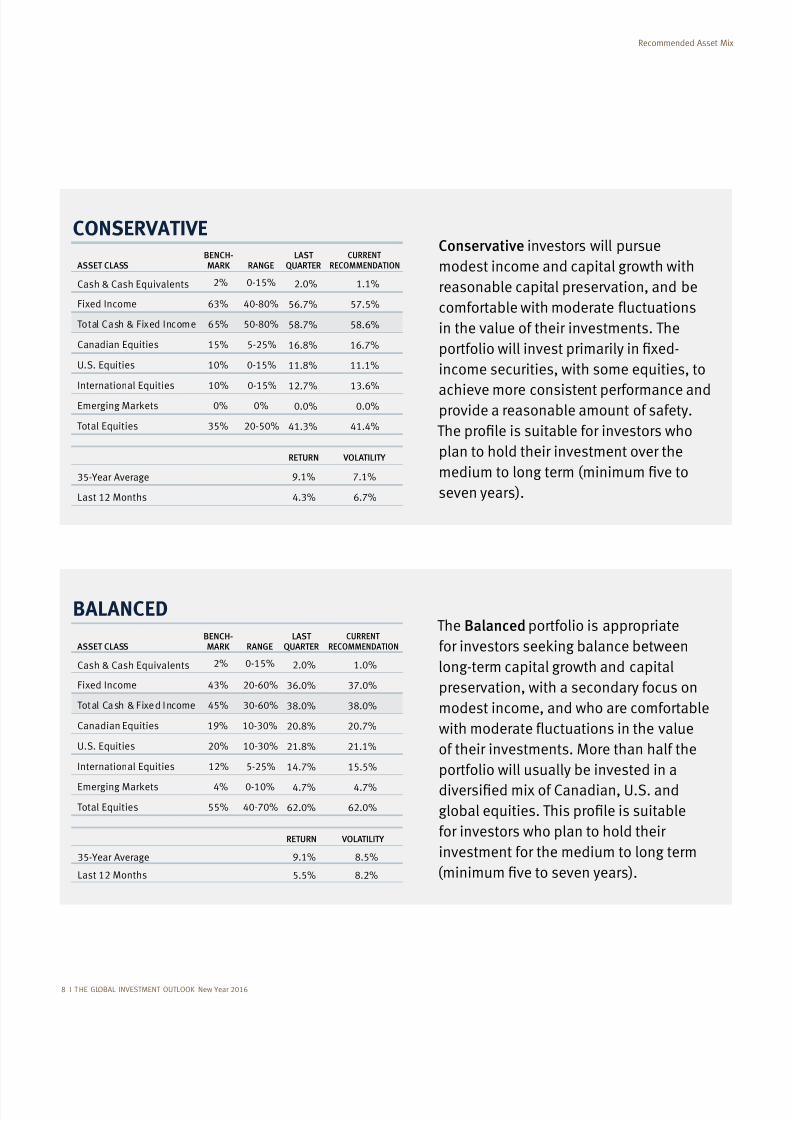

ASSET CLASSBENCH-MARK RANGE

LASTQUARTER

CURRENT

RECOMMENDATION

Cash & Cash Equivalents 2% 0-15% 2.0% 1.0%

Fixed Income 43% 20-60% 36.0% 37.0%

Total Cash & F ixed Income 45% 30-60%

Canadian Equities 10-30% 20.7%

U.S. Equities 20% 10-30% 21.1%

International Equities 12% 5-25% 14.7% 15.5%

4% 0-10% 4.7% 4.7%

Total Equities 55% 40-70% 62.0% 62.0%

BALANCEDThe Balanced portfolio is appropriate

long-term capital growth and capital

preservation, with a secondary focus on

modest income, and who are comfortable

of their investments. More than half the

portfolio will usually be invested in a

for investors who plan to hold their

investment for the medium to long term

RETURN VOLATILITY

35-Year Average

Last 12 Months 5.5%

ASSET CLASSBENCH-MARK RANGE

LASTQUARTER

CURRENT

RECOMMENDATION

Cash & Cash Equivalents 2% 0-15% 2.0% 1.1%

Fixed Income 63% 56.7% 57.5%

Total Cash & Fixed Income 65%

Canadian Equities 15% 5-25% 16.7%

U.S. Equities 10% 0-15% 11.1%

International Equities 10% 0-15% 12.7% 13.6%

0% 0% 0.0% 0.0%

Total Equities 35% 20-50% 41.3% 41.4%

CONSERVATIVEConservative investors will pursue

modest income and capital growth with

reasonable capital preservation, and be

in the value of their investments. The

income securities, with some equities, to

achieve more consistent performance andprovide a reasonable amount of safety.

plan to hold their investment over the

seven years).

RETURN VOLATILITY

35-Year Average 7.1%

Last 12 Months 4.3% 6.7%

New Year 2016

Recommended Asset Mix

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 11/80

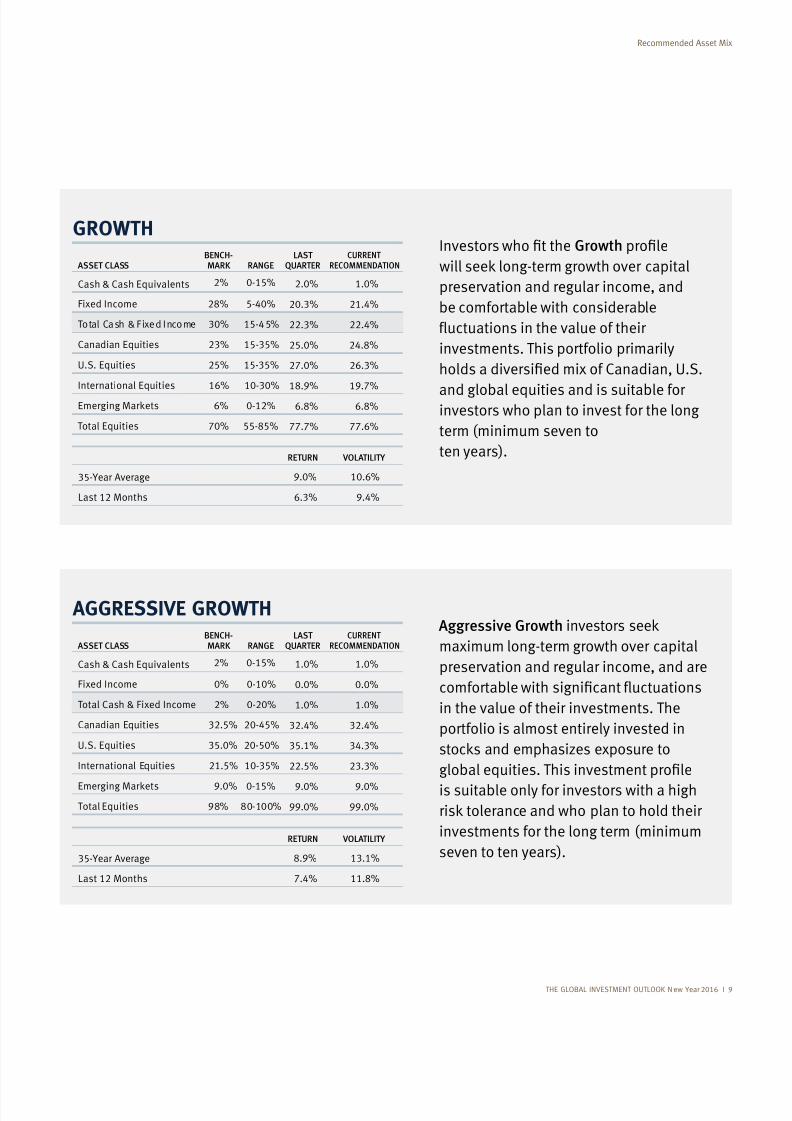

ASSET CLASSBENCH-MARK RANGE

LASTQUARTER

CURRENT

RECOMMENDATION

Cash & Cash Equivalents 2% 0-15% 2.0% 1.0%

Fixed Income 5-40% 20.3% 21.4%

Total Cash & F ixed Income 30% 15-45% 22.3% 22.4%

Canadian Equities 23% 15-35% 25.0%

U.S. Equities 25% 15-35% 27.0% 26.3%

International Equities 16% 10-30%

6% 0-12%

Total Equities 70% 77.7% 77.6%

GROWTHInvestors Growth

preservation and regular income, and

be comfortable with considerable

investments. This portfolio primarily

and global equities and is suitable forinvestors who plan to invest for the long

term (minimum seven to

ten years).RETURN VOLATILITY

35-Year Average 10.6%

Last 12 Months 6.3%

ASSET CLASSBENCH-MARK RANGE

LASTQUARTER

CURRENT

RECOMMENDATION

Cash & Cash Equivalents 2% 0-15% 1.0% 1.0%

Fixed Income 0% 0-10% 0.0% 0.0%

Total Cash & Fixed Income 2% 0-20% 1.0% 1.0%

Canadian Equities 32.5% 20-45% 32.4% 32.4%

U.S. Equities 35.0% 20-50% 35.1% 34.3%

International Equities 21.5% 10-35% 22.5% 23.3%

0-15%

Total Equities

AGGRESSIVE GROWTH

RETURN VOLATILITY

35-Year Average 13.1%

Last 12 Months 7.4%

Aggressive Growth

maximum long-term growth over capital

preservation and regular income, and are

in the value of their investments. The

portfolio is almost entirely invested in

is suitable only for investors with a high

investments for the long term (minimum

seven to ten years).

THE GLOBAL INVESTMENT OUTLOOK N ew Year 2016

Recommended Asset Mix

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 12/80

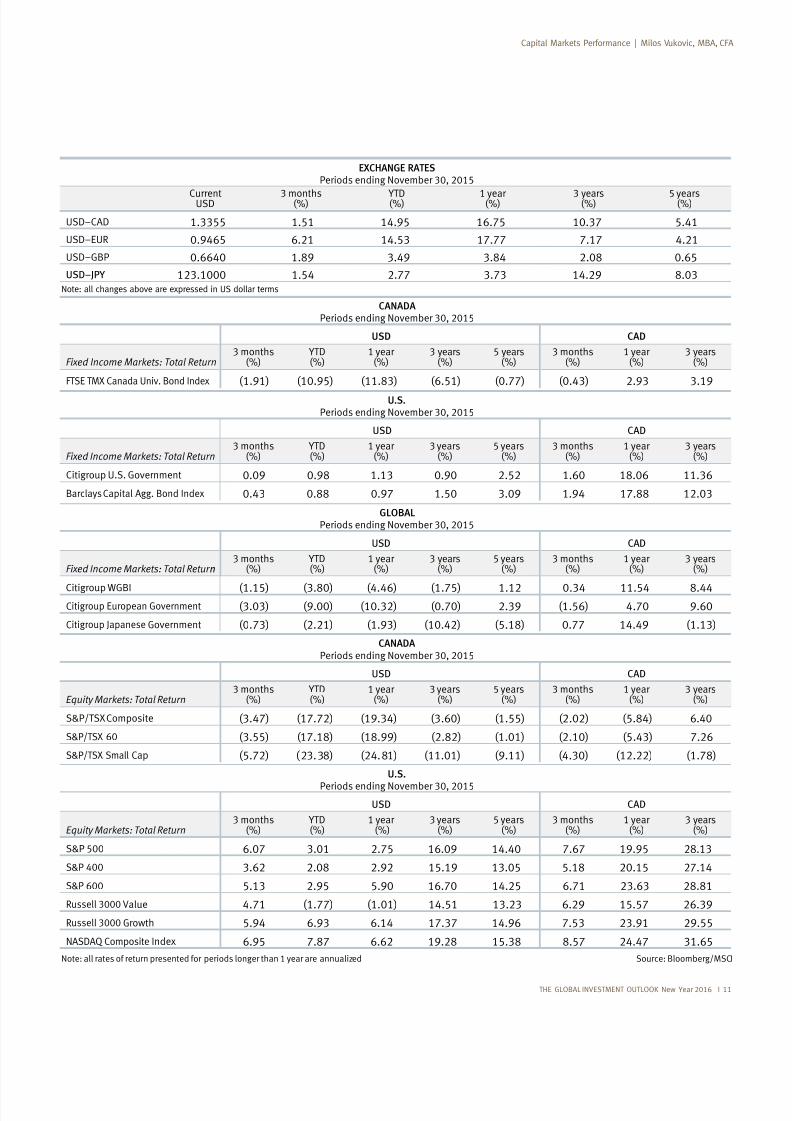

The U.S. dollar rose against all major

currencies between September

1, 2015, and November 30, 2015.

pound, and 1.5% against both

the yen and the Canadian dollar.Over the 12-month period ended

November 30, 2015, the U.S. dollar

sterling and 3.7% versus the yen.

modestly in the U.S. during the

three-month period, but currency

depreciation contributed to bond

losses elsewhere. The Barclays

Capital Aggregate Bond Index,

income performance, climbed 0.4%.

European bonds fell 3.0% in U.S.

dollar terms as measured by the

Citigroup WGBI – Europe Index.

The FTSE TMX Canada Universe

Milos Vukovic, MBA, CFA

Vice President & Head of Investment Policy

RBC Global Asset Management Inc.

10 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

CAPITAL MARKETS PERFORMANCE

Japanese bonds, as measured bythe Citigroup Japanese Government

Bond Index, decreased 0.7%.

during the latest three-month period,

amid further drops in commodity

prices. The S&P 500 climbed 6.1%,

followed by a 1.6% rise for the MSCI

Japan and a 0.3% gain for the MSCI

Europe. Within Europe, the MSCI

gained 0.2%. Over the 12-month

and the MSCI Japan gained 7.7%.

However, the MSCI U.K. lost 6.4%,

followed by a 3.7% drop in the MSCI

France. The S&P/TSX Composite

Index lost 3.5% in U.S. dollar terms

during the three months, versus the

3.6% drop for the large-cap S&P/TSX60 Index and a 5.7% decline in the

S&P/TSX Small Cap Index. The MSCI

during the three-month period and

dropped 17.0% over the 12-month

period.

The S&P 400 Index, a measure of

in the latest three months and rose

the S&P 600 Index, a gauge of small-

cap performance, gained 5.1% in the

the 12 months. The Russell 3000

quarter versus a 4.7% increase for

the Russell 3000 Value Index. Over

the 12 months, the Russell 3000

Growth Index rose 6.1%, while the

Russell 3000 Value Index lost 1.0%.

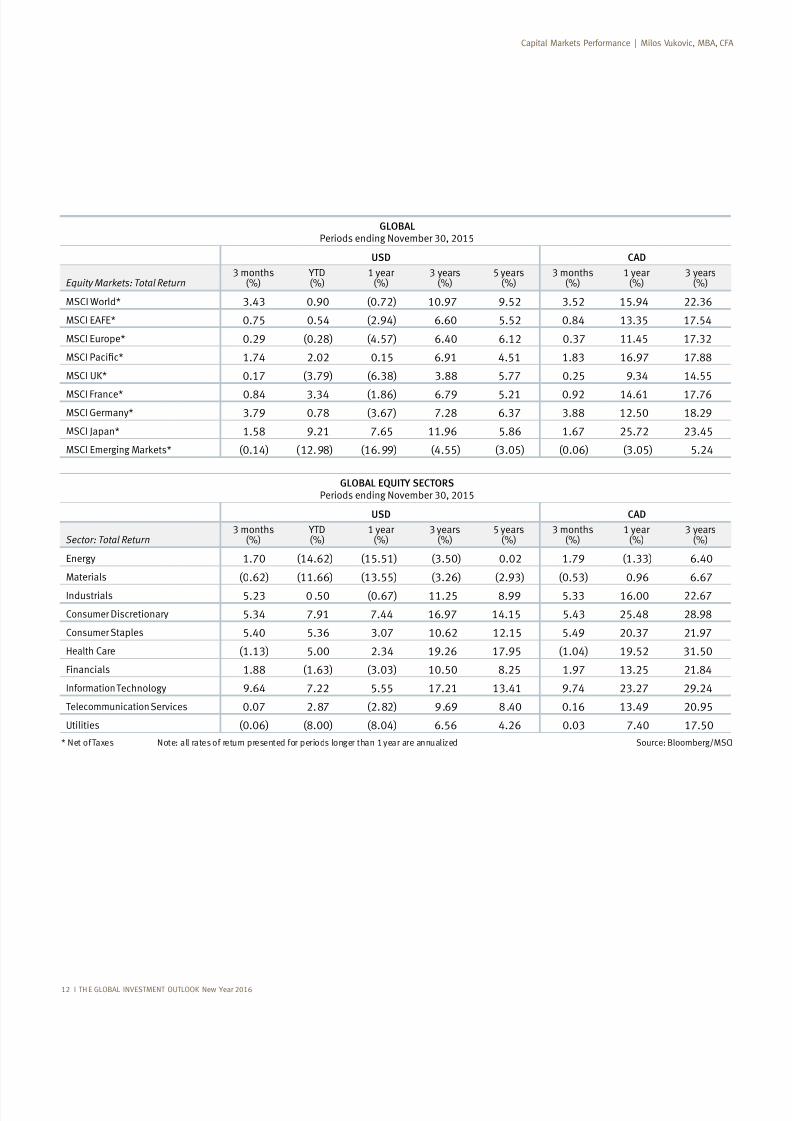

Seven of the 10 global equity sectors

climbed during the quarter ended

November 30, 2015. The best-

performing sector was Information

followed by Consumer Staples

with a rise of 5.4%, and Consumer

The worst-performing sectors over

the past three months were Health

Care, which lost 1.1%; Materials,

which lost 0.6%; and Utilities, with

period, the best-performing sectors

Information Technology and

Consumer Staples, and the worst-

performing were Energy, Materials

and Utilities.

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 13/80

CANADA

Periods ending November 30, 2015

USD CAD

Equity Markets: Total Return3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

S&P/TSX Composite (3.47) (17.72) (3.60) (1.55) (2.02) 6.40

S&P/TSX 60 (3.55) (1.01) (2.10) (5.43) 7.26

S&P/TSX Small Cap (5.72) (11.01) (4.30) (12.22)

U.S.

Periods ending November 30, 2015

USD CAD

Equity Markets: Total Return3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

S&P 500 6.07 3.01 2.75 14.40 7.67

S&P 400 3.62 13.05 20.15 27.14

S&P 600 5.13 16.70 14.25 6.71 23.63

Russell 3000 Value 4.71 (1.77) (1.01) 14.51 13.23 15.57

Russell 3000 Growth 6.14 17.37 7.53

N Index 6.62 24.47 31.65

EXCHANGE RATES

Periods ending November 30, 2015

Current 3 months(%) (%) 1 year(%) 3 years(%) 5 years(%)

1.3355 1.51 16.75 10.37 5.41

6.21 14.53 17.77 7.17 4.21

0.6640 0.65

USD–JPY 123.1000 1.54 2.77 3.73

Source: Bloomberg/MSCI

CANADA

Periods ending November 30, 2015

USD CAD

Fixed Income Markets: Total Return3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

FTSE TMX Canada Univ. Bond Index (6.51) (0.77) (0.43)

U.S.

Periods ending November 30, 2015

USD CAD

Fixed Income Markets: Total Return3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

Citigroup U.S. Government 1.13 2.52 1.60 11.36

Barclays Capital Agg. Bond Index 0.43 1.50 12.03

GLOBAL

Periods ending November 30, 2015

USD CAD

Fixed Income Markets: Total Retur n3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

Citigroup WGBI (1.15) (4.46) (1.75) 1.12 0.34 11.54 Citigroup European Government (3.03) (10.32) (0.70) (1.56) 4.70

Citigroup Japanese Government (0.73) (2.21) (10.42) 0.77 (1.13)

Note: all changes above are expressed in US dollar terms

Note: all rates of return presented for periods longer than 1 year are annualized

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 11

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 14/80

GLOBAL

Periods ending November 30, 2015

USD CAD

Equity Markets: Total Return3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

MSCI World* 3.43 (0.72) 3.52 22.36

MSCI EAFE* 0.75 0.54 6.60 5.52 13.35 17.54

MSCI Europe* (4.57) 6.40 6.12 0.37 11.45 17.32

MSCI 1.74 2.02 0.15 4.51

MSCI UK* 0.17 5.77 0.25 14.55

MSCI France* 3.34 5.21 14.61 17.76

MSCI Germany* (3.67) 6.37 12.50

MSCI Japan* 7.65 1.67 25.72 23.45

MSCI Emerging M (0.14) (4.55) (3.05) (0.06) (3.05) 5.24

Source: Bloomberg/MSCI

GLOBAL EQUITY SECTORS Periods ending November 30, 2015

USD CAD

Sector: Total Return3 months

(%) (%)

1 year(%)

3 years(%)

5 years(%)

3 months(%)

1 year(%)

3 years(%)

Energy 1.70 (14.62) (15.51) (3.50) 0.02 (1.33) 6.40

Materials (0.62) (11.66) (13.55) (3.26) (0.53) 6.67

Industrials 5.23 0 .50 (0.67) 11.25 5.33 16.00 22.67

Consumer 5.34 7.44 14.15 5.43

Consumer Staples 5.40 5.36 3.07 10.62 12.15 20.37

Health Care (1.13) 5.00 2.34 (1.04) 31.50

F inancials (1.63) (3.03) 10.50 13.25

Information Technology 7.22 5.55 17.21 13.41 23.27

T elecommunication Services 0.07 0.16

Utilities (0.06) 6.56 4.26 0.03 7.40 17.50

* Net of Taxes Note: all rates of return presented for periods longer than 1 year are annualized

12 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 15/80

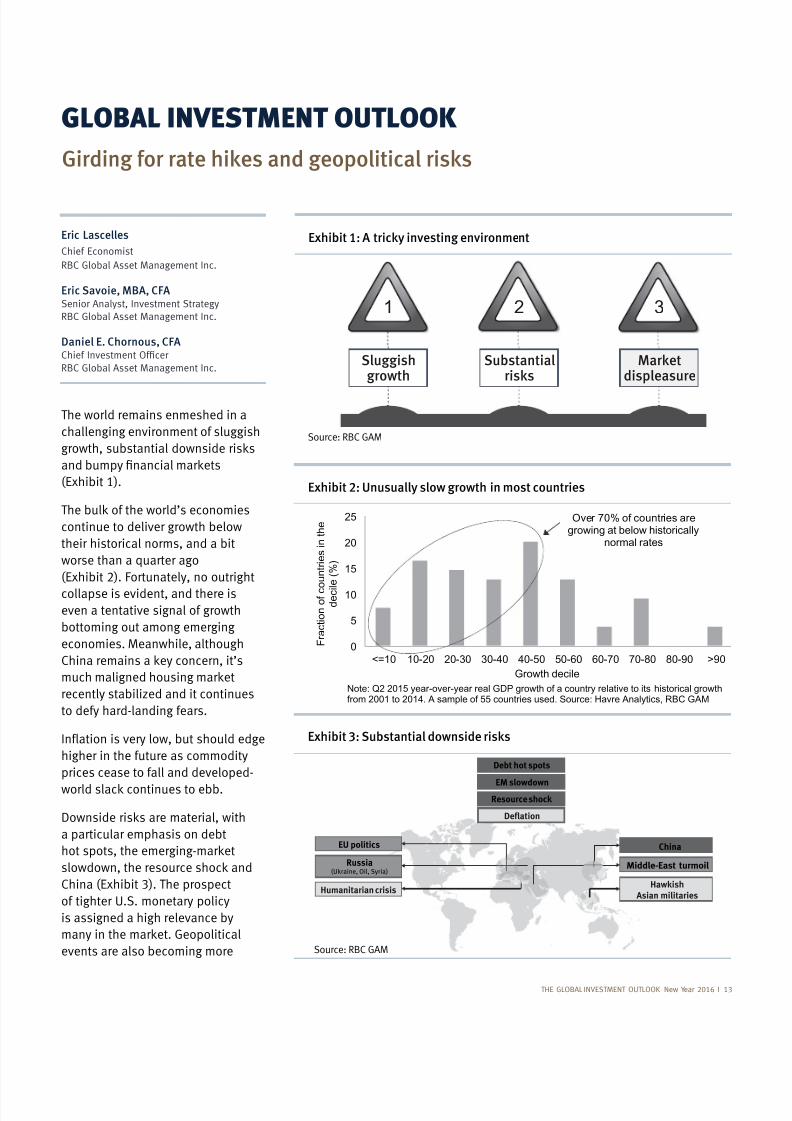

Girding for rate hikes and geopolitical risks

The world remains enmeshed in a

challenging environment of sluggish

(Exhibit 1).

continue to deliver growth below

their historical norms, and a bit

worse than a quarter ago

(Exhibit 2). Fortunately, no outright

collapse is evident, and there iseven a tentative signal of growth

bottoming out among emerging

economies. Meanwhile, although

recently stabilized and it continues

to defy hard-landing fears.

higher in the future as commodity

prices cease to fall and developed-

a particular emphasis on debt

China (Exhibit 3). The prospect

of tighter U.S. monetary policy

is assigned a high relevance by

events are also becoming more

GLOBAL INVESTMENT OUTLOOK

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 13

Exhibit 1: A tricky investing environment

1 2 3

Sluggishgrowth

Substantialrisks

Marketdispleasure

Exhibit 2: Unusually slow growth in most countries

0

5

10

15

20

25

<=10 10-20 20-30 30-40 40-50 50-60 60-70 70-80 80-90 >90

F r a c t i o n o f c o u n t r i e s i n t h e

d e c i l e ( % )

Growth decile

Note: Q2 2015 year-over-year real GDP growth of a country relative to its historical growthfrom 2001 to 2014. A sample of 55 countries used. Source: Havre Analytics, RBC GAM

Over 70% of countries aregrowing at below historically

normal rates

Eric Lascelles

Chief Economist

RBC Global Asset Management Inc.

Eric Savoie, MBA, CFASenior Analyst, Investment StrategyRBC Global Asset Management Inc.

Daniel E. Chornous, CFA

RBC Global Asset Management Inc.

Exhibit 3: Substantial downside risks

Debt hot spots

EM slowdownResource shock

Deflation

China

Middle-East turmoil

Hawkish Asian militaries

EU politics

Russia (Ukraine, Oil, Syria)

Humanitarian crisis

Source: RBC GAM

Source: RBC GAM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 16/80

14 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

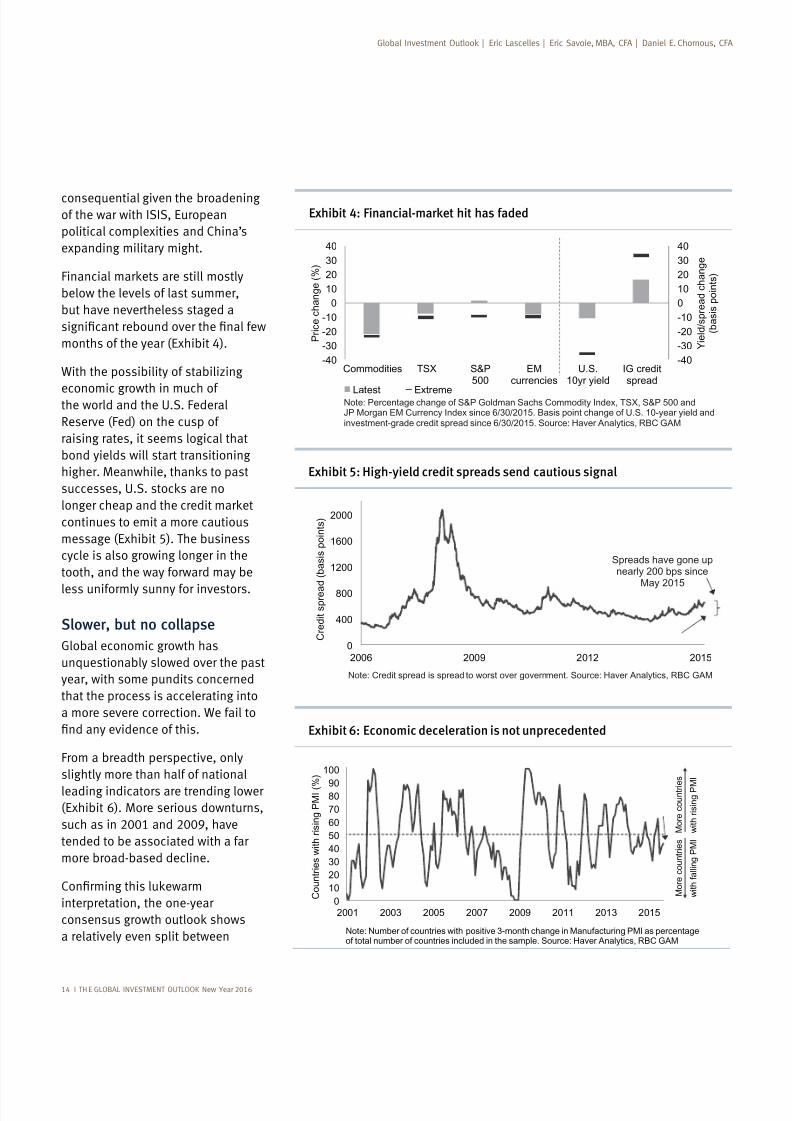

Exhibit 4: Financial-market hit has faded

-40

-30

-20

-10

0

10

20

30

40

-40

-30

-20

-10

0

10

20

30

40

Commodities TSX S&P500

EMcurrencies

U.S.10yr yield

IG creditspread

Y i e l d / s p r e a d c h a n g e

( b a s i s p o i n t s )

P r i c e c h a n g e ( % )

Latest ExtremeNote: Percentage change of S&P Goldman Sachs Commodity Index, TSX, S&P 500 andJP Morgan EM Currency Index since 6/30/2015. Basis point change of U.S. 10-year yield andinvestment-grade credit spread since 6/30/2015. Source: Haver Analytics, RBC GAM

Exhibit 5: High-yield credit spreads send cautious signal

0

400

800

1200

1600

2000

2006 2009 2012 2015

C r e d i t s p r e a

d ( b a s i s p o i n t s )

Note: Credit spread is spread to worst over government. Source: Haver Analytics, RBC GAM

Spreads have gone upnearly 200 bps since

May 2015

consequential given the broadeningof the war with ISIS, European

political complexities and China’s

expanding military might.

below the levels of last summer,

but have nevertheless staged a

months of the year (Exhibit 4).

With the possibility of stabilizing

economic growth in much ofthe world and the U.S. Federal

Reserve (Fed) on the cusp of

raising rates, it seems logical that

bond yields will start transitioning

continues to emit a more cautious

message (Exhibit 5). The business

cycle is also growing longer in the

tooth, and the way forward may be

less uniformly sunny for investors.

Slower, but no collapse

Global economic growth has

unquestionably slowed over the past

year, with some pundits concerned

that the process is accelerating into

a more severe correction. We fail to

From a breadth perspective, only

slightly more than half of national

leading indicators are trending lower(Exhibit 6). More serious downturns,

tended to be associated with a far

more broad-based decline.

interpretation, the one-year

a relatively even split between

Exhibit 6: Economic deceleration is not unprecedented

0

10

20

30

40

50

60

70

8090

100

2001 2003 2005 2007 2009 2011 2013 2015

C o u n t r i e s w i t h r i s i n g P M I ( %

)

Note: Number of countries with positive 3-month change in Manufacturing PMI as percentageof total number of countries included in the sample. Source: Haver Analytics, RBC GAM

M o r e c o u n t r i e s

w i t h f a l l i n g P M I

M o r e c o u n t r i e s

w i t h r i s i n g P M

I

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 17/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 15

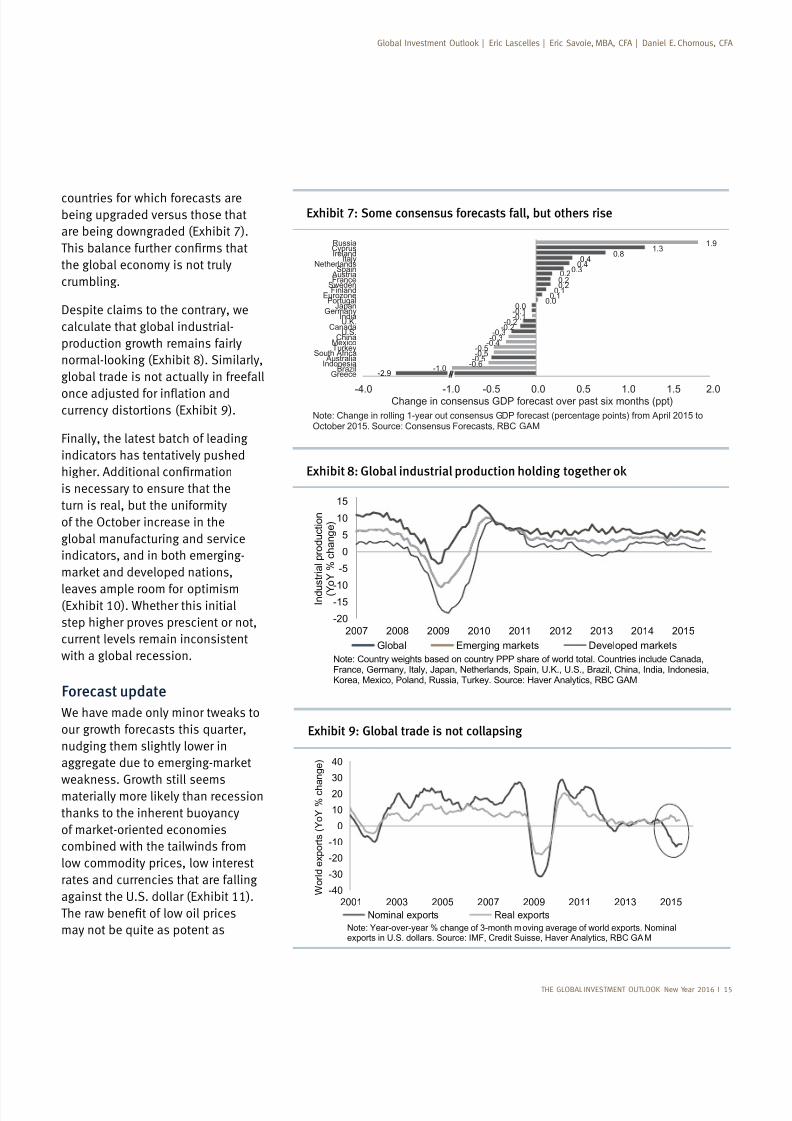

Exhibit 7: Some consensus forecasts fall, but others rise

-2.9-1.0

-0.6-0.5-0.5-0.5

-0.4-0.3-0.3

-0.2-0.2

-0.1-0.10.0

0.00.1

0.10.20.20.2

0.30.40.4

0.81.3

1.9

-4.0 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

GreeceBrazil

Indonesia Australia

South AfricaTurkeyMexico

ChinaU.S.

CanadaU.K.India

GermanyJapan

PortugalEurozone

FinlandSwedenFrance Austria

SpainNetherlands

ItalyIrelandCyprusRussia

Change in consensus GDP forecast over past six months (ppt)

Note: Change in rolling 1-year out consensus GDP forecast (percentage points) from April 2015 toOctober 2015. Source: Consensus Forecasts, RBC GAM

Exhibit 8: Global industrial production holding together ok

-20

-15-10

-5

0

5

10

15

2007 2008 2009 2010 2011 2012 2013 2014 2015

I n d u

s t r i a l p r o d u c t i o n

( Y

o Y % c

h a n g e )

Global Emerging markets Developed markets

Note: Country weights based on country PPP share of world total. Countries include Canada,France, Germany, Italy, Japan, Netherlands, Spain, U.K., U.S., Brazil, China, India, Indonesia,Korea, Mexico, Poland, Russia, Turkey. Source: Haver Analytics, RBC GAM

countries for which forecasts arebeing upgraded versus those that

are being downgraded (Exhibit 7).

the global economy is not truly

crumbling.

calculate that global industrial-

production growth remains fairly

global trade is not actually in freefall

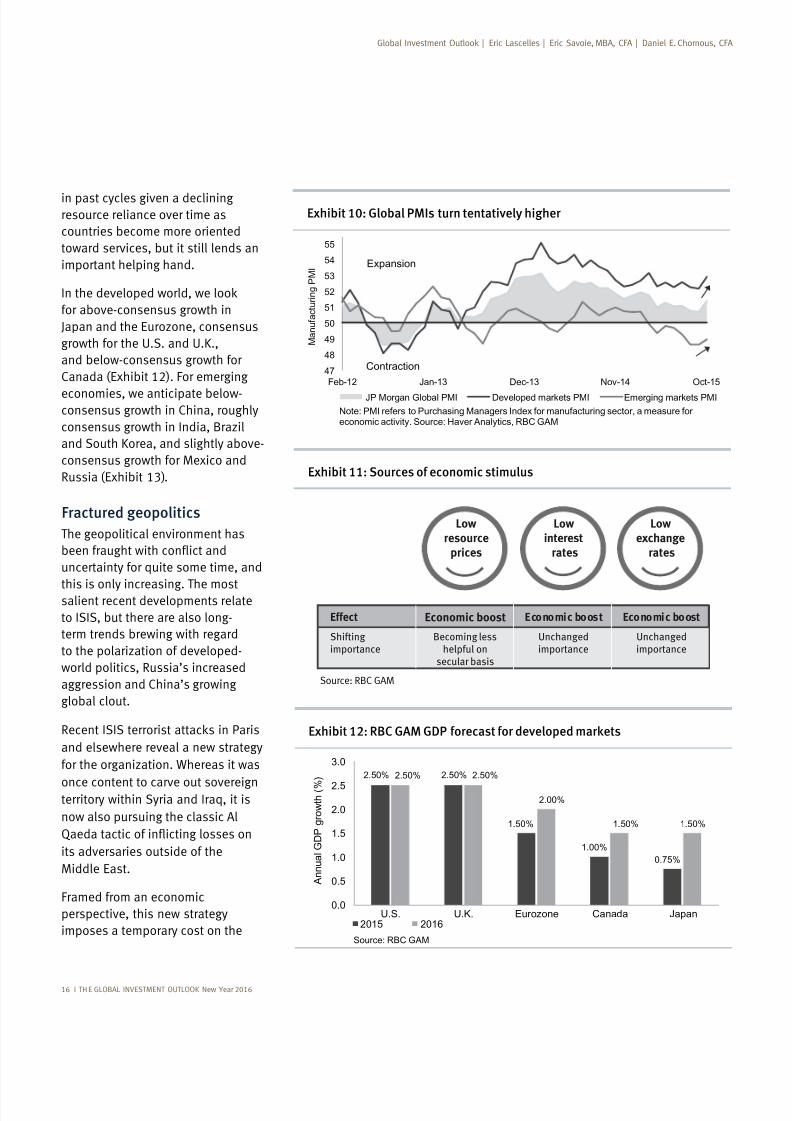

Finally, the latest batch of leading

indicators has tentatively pushed

is necessary to ensure that the

turn is real, but the uniformity

of the October increase in the

global manufacturing and service

indicators, and in both emerging-

leaves ample room for optimism(Exhibit 10). Whether this initial

step higher proves prescient or not,

current levels remain inconsistent

with a global recession.

Forecast update

our growth forecasts this quarter,

nudging them slightly lower in

combined with the tailwinds from

low commodity prices, low interest

rates and currencies that are falling

against the U.S. dollar (Exhibit 11).

may not be quite as potent as

Exhibit 9: Global trade is not collapsing

-40

-30

-20

-10

0

10

20

30

40

2001 2003 2005 2007 2009 2011 2013 2015 W o r l d e x p o r t s ( Y o Y % c h a n g e )

Nominal exports Real exports

Note: Year-over-year % change of 3-month moving average of world exports. Nominalexports in U.S. dollars. Source: IMF, Credit Suisse, Haver Analytics, RBC GAM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 18/80

16 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

Exhibit 10: Global PMIs turn tentatively higher

47

48

49

50

51

52

53

54

55

Feb-12 Jan-13 Dec-13 Nov-14 Oct-15

M a n u f a c t u r i n g P M I

JP Morgan Global PMI Developed markets PMI Emerging markets PMI

Note: PMI refers to Purchasing Managers Index for manufacturing sector, a measure foreconomic activity. Source: Haver Analytics, RBC GAM

Contraction

Expansion

Exhibit 11: Sources of economic stimulus

Lowresource

prices

Lowinterest rates

Lowexchange

rates

Effect Economic boost Economic boost Economic boost

Shiftingimportance

Becoming lesshelpful on

secular basis

Unchangedimportance

Unchangedimportance

in past cycles given a decliningresource reliance over time as

countries become more oriented

toward services, but it still lends an

important helping hand.

for above-consensus growth in

Japan and the Eurozone, consensus

growth for the U.S. and U.K.,

and below-consensus growth for

Canada (Exhibit 12). For emerging

economies, we anticipate below-consensus growth in China, roughly

consensus growth in India, Brazil

and South Korea, and slightly above-

consensus growth for Mexico and

Russia (Exhibit 13).

Fractured geopolitics

The geopolitical environment has

uncertainty for quite some time, and

this is only increasing. The mostsalient recent developments relate

to ISIS, but there are also long-

term trends brewing with regard

to the polarization of developed-

world politics, Russia’s increased

aggression and China’s growing

global clout.

and elsewhere reveal a new strategy

for the organization. Whereas it was

once content to carve out sovereignterritory within Syria and Iraq, it is

now also pursuing the classic Al

its adversaries outside of the

Middle East.

Framed from an economic

perspective, this new strategy

imposes a temporary cost on the

Exhibit 12: RBC GAM GDP forecast for developed markets

2.50% 2.50%

1.50%

1.00%

0.75%

2.50% 2.50%

2.00%

1.50% 1.50%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

U.S. U.K. Eurozone Canada Japan

A n n u a l G D P g r o w t h ( %

)

2015 2016

Source: RBC GAM

Source: RBC GAM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 19/80

HE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 17

targeted countries via lost tourism,

aversion. But the consequences are

usually not lasting. By far, the greater

challenge is political as voters and

by tilting even further toward far-

left and far-right political agendas

that result in a sub-optimal policy

mix of diminished immigration,

less free trade and fewer individual

liberties. Particularly in Europe,

provide another catalyst, voters are

increasingly inclined in this direction.

remains complicated. The multi-

faceted battle between ISIS, the

Syrian government, the Iraqi

government, non-ISIS Syrian

rebels, Kurdish forces, Russia and

the U.S. and its allies remains the

most troubling situation. Given the

reluctance of Western nations toengage in another ground war in

support of local forces and logistical

efforts to undermine ISIS’s oil sales,

combatants.

There also remain serious

disagreements along Sunni-Shia

lines even between established

regional powers, as demonstratedby the ongoing proxy war in Yemen

between Saudi Arabia and Iran.

countries managing any sort of

material progress toward democracy

or greater stability.

Russia continues to merit close

examination given its recent military

aggressions: the earlier annexation

its new involvement in Syria. One

can hope that the latest round of

cooperation between Russia and the

other Western powers in Syria, asthis maximizes the odds of reducing

the world.

Whereas Russia remains globally

relevant from a military perspective,

it has ceased to be a global

economic power. China is the mirror

image of this: an ascending global

economic power with only regional

an increasingly aggressive stancein both the East China and South

China seas, but has never in its long

to expand its military reach beyond

From an economic perspective,

however, China is indisputably

relevant. Historically, global trade

and global growth appear to thrive

during hegemonic eras – when

one country effectively rules the

world – a position helmed by the

U.S. for the better part of the last

intuitive sense as the world is not

divided into competing factions.

However, with China’s ascensionit would appear we are now

transitioning toward a more multi-

polar world. This could act as one

of several factors constraining the

further progress of globalization.

There are already tentative signs

of consequences, such as the new

(TPP) trade deal that excludes China,

contrasted against China’s recent

efforts to develop its own regional

trade bloc.

There are a few common

conclusions that emerge from

these observations. Geopolitical

uncertainty promises to be unusually

high in the future due to the

East, the increased possibility of

Exhibit 13: RBC GAM GDP forecast for emerging markets

7.25%6.75%

2.50% 2.25%

-2.75% -2.75%

7.75%

6.00%

3.00% 3.00%

-0.75%

0.25%

-4

-2

0

2

4

6

8

India China South Korea Mexico Brazil Russia

A n n u a l G D P g r o w t h ( % )

2015 2016

Source: RBC GAM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 20/80

New Year 2016

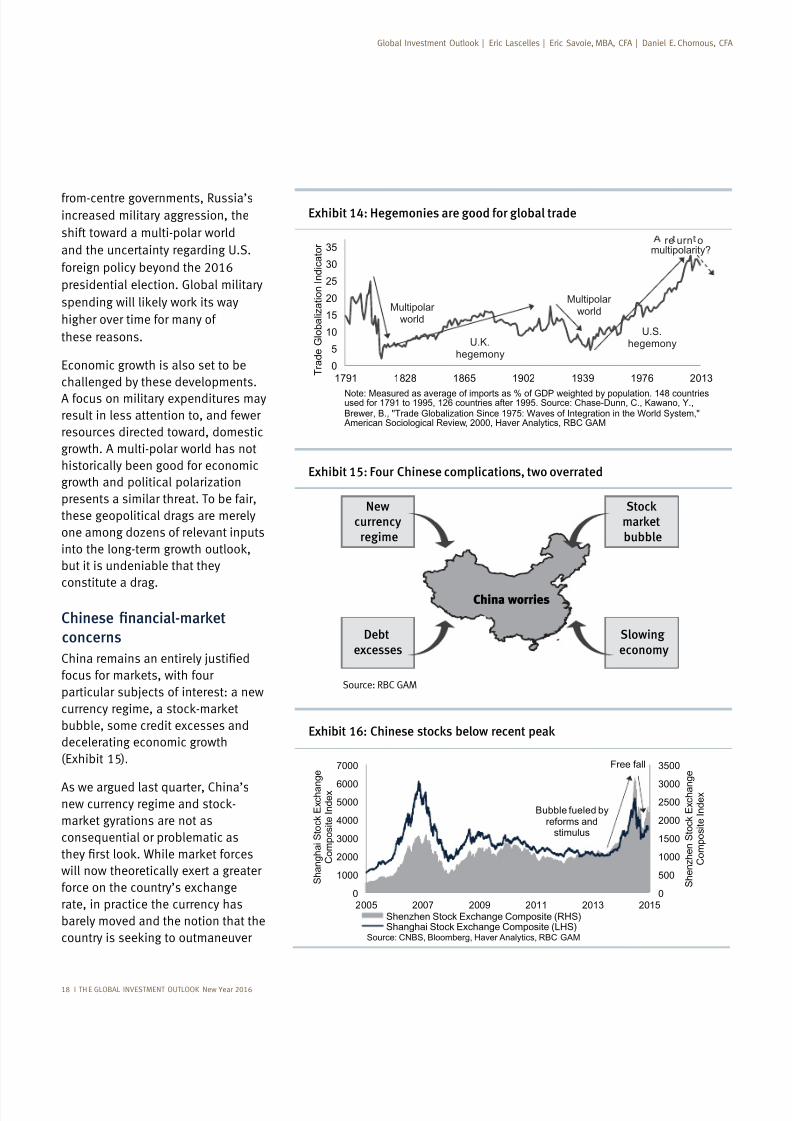

Exhibit 14: Hegemonies are good for global trade

0

5

10

15

20

25

30

35

1791 1828 1865 1902 1939 1976 2013 T r a d e G l o b a l i z a t i o n I n d i c a t o r

Note: Measured as average of imports as % of GDP weighted by population. 148 countriesused for 1791 to 1995, 126 countries after 1995. Source: Chase-Dunn, C., Kawano, Y.,Brewer, B., "Trade Globalization Since 1975: Waves of Integration in the World System," American Sociological Review, 2000, Haver Analytics, RBC GAM

U.K.hegemony

U.S.hegemony

Multipolar world

re urn omultipolarity?

Multipolar world

Exhibit 15: Four Chinese complications, two overrated

China worries

Newcurrency

regime

Stockmarket

bubble

Slowing

economy

Debt

excesses

from-centre governments, Russia’sincreased military aggression, the

shift toward a multi-polar world

and the uncertainty regarding U.S.

foreign policy beyond the 2016

presidential election. Global military

higher over time for many of

these reasons.

Economic growth is also set to be

challenged by these developments.

A focus on military expenditures may

result in less attention to, and fewer

resources directed toward, domestic

growth. A multi-polar world has not

historically been good for economic

growth and political polarization

presents a similar threat. To be fair,

these geopolitical drags are merely

one among dozens of relevant inputs

but it is undeniable that they

constitute a drag.

concerns

particular subjects of interest: a new

bubble, some credit excesses and

decelerating economic growth

(Exhibit 15).

As we argued last quarter, China’s

consequential or problematic as

will now theoretically exert a greater

force on the country’s exchange

rate, in practice the currency has

barely moved and the notion that the

Source: RBC GAM

Exhibit 16: Chinese stocks below recent peak

0

500

1000

1500

2000

25003000

3500

0

1000

2000

3000

4000

50006000

7000

2005 2007 2009 2011 2013 2015Shenzhen Stock Exchange Composite (RHS)Shanghai Stock Exchange Composite (LHS)

Source: CNBS, Bloomberg, Haver Analytics, RBC GAM

Bubble fueled byreforms and

stimulus

S h a n g h a i S t o c k E x c h a n

g e

C o m p o s i t e I n d e x

S h e n z h e n S t o c k E x c h a n

g e

C o m p o s i t e I n d e x

Free fall

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 21/80

THE GLOBAL INVESTMENT OUTLOOK New Year

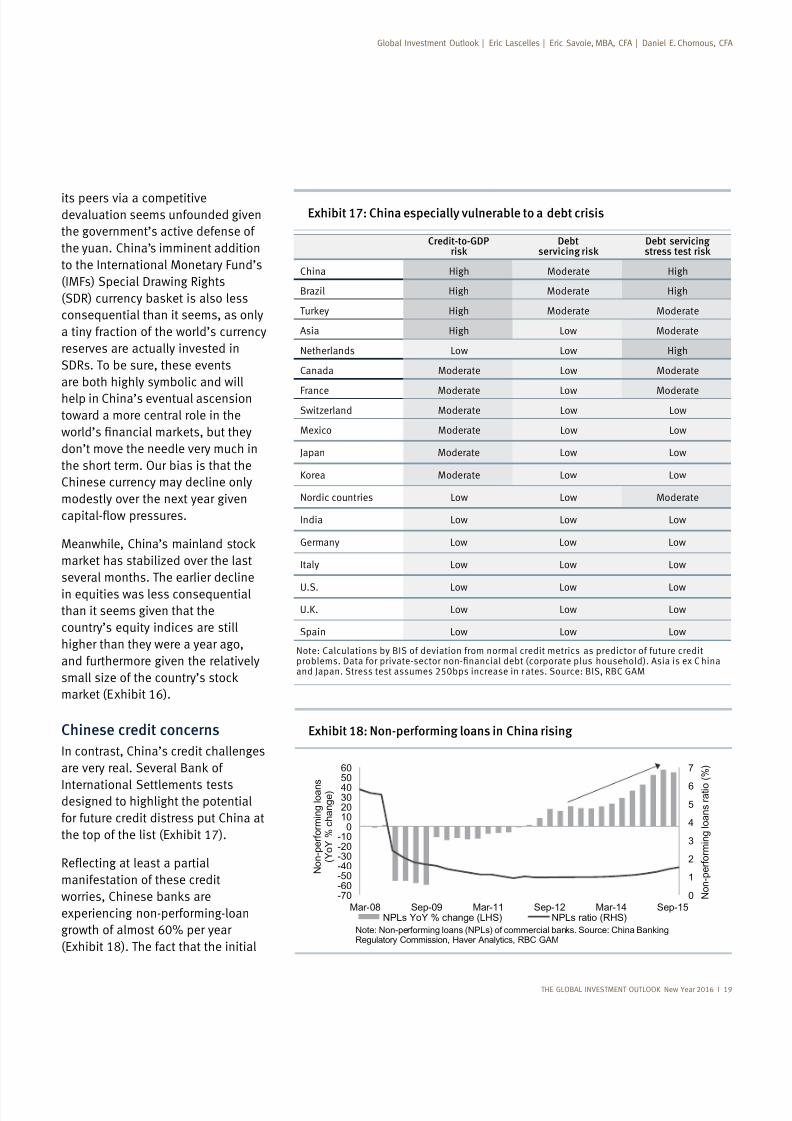

Exhibit 17: China especially vulnerable to a debt crisis

Exhibit 18: Non-performing loans in China rising

0

1

2

3

4

5

6

7

-70-60-50-40-30-20-10

010203040

5060

Mar-08 Sep-09 Mar-11 Sep-12 Mar-14 Sep-15 N o n - p e r f o r m i n g l o a n s r a t i o

( % )

N o n - p e r f o r m i n g l o a n s

( Y o Y % c

h a n g e )

NPLs YoY % change (LHS) NPLs ratio (RHS)

Note: Non-performing loans (NPLs) of commercial banks. Source: China BankingRegulatory Commission, Haver Analytics, RBC GAM

its peers via a competitivedevaluation seems unfounded given

the government’s active defense of

the yuan. China’s imminent addition

to the International Monetary Fund’s

consequential than it seems, as only

a tiny fraction of the world’s currency

reserves are actually invested in

are both highly symbolic and will

help in China’s eventual ascension

toward a more central role in the

don’t move the needle very much in

the short term. Our bias is that the

Chinese currency may decline only

modestly over the next year given

several months. The earlier decline

in equities was less consequentialthan it seems given that the

country’s equity indices are still

higher than they were a year ago,

and furthermore given the relatively

Chinese credit concerns

In contrast, China’s credit challenges

International Settlements testsdesigned to highlight the potential

for future credit distress put China at

the top of the list (Exhibit 17).

manifestation of these credit

experiencing non-performing-loan

growth of almost 60% per year

Credit-to-GDPrisk

Debtservicing risk

Debt servicingstress test risk

China High Moderate High

Brazil High Moderate High

High Moderate Moderate

Asia High Low Moderate

Netherlands Low Low High

Canada Moderate Low Moderate

France Moderate Low Moderate

Switzerland Moderate Low Low

Mexico Moderate Low Low

Japan Moderate Low Low

Korea Moderate Low Low

Nordic countries Low Low Moderate

India Low Low Low

Germany Low Low Low

Italy Low Low Low

U.S. Low Low Low

U.K. Low Low Low

Spain Low Low Low

Note: Calculations by BIS of deviation from normal credit metrics as predictor of future credit and Japan. Stress test assumes 250bps increase in r ates. Source: BIS, RBC GAM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 22/80

20 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

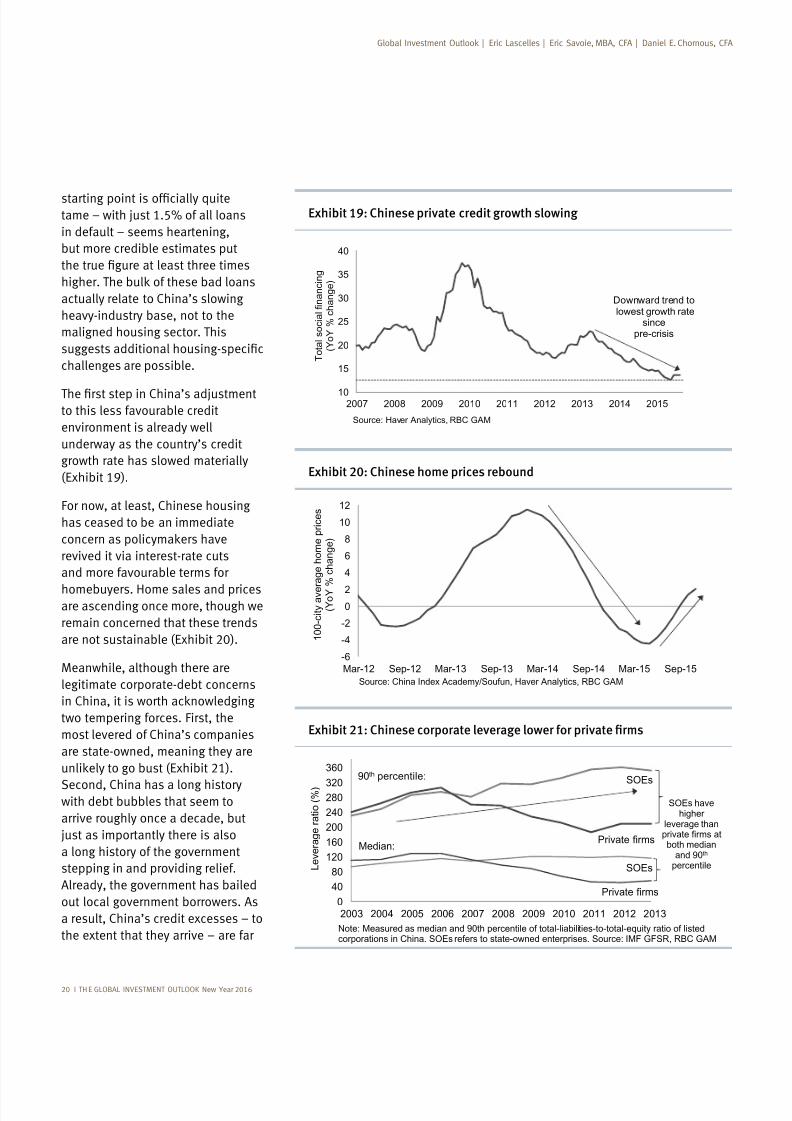

Exhibit 19: Chinese private credit growth slowing

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014 2015

T o t a l s o c i a l f i n a n c i n g

( Y o Y % c h a n g e )

Source: Haver Analytics, RBC GAM

Downward trend tolowest growth rate

sincepre-crisis

Exhibit 20: Chinese home prices rebound

-6

-4

-2

0

2

4

6

8

10

12

Mar-12 Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15

1 0 0 - c i t y a v e

r a g e h o m e p r i c e s

( Y o Y

% c h a n g e )

Source: China Index Academy/Soufun, Haver Analytics, RBC GAM

tame – with just 1.5% of all loans

in default – seems heartening,

but more credible estimates put

actually relate to China’s slowing

heavy-industry base, not to the

maligned housing sector. This

challenges are possible.

to this less favourable credit

environment is already well

underway as the country’s credit

growth rate has slowed materially

For now, at least, Chinese housing

has ceased to be an immediate

revived it via interest-rate cuts

and more favourable terms for

homebuyers. Home sales and pricesare ascending once more, though we

remain concerned that these trends

are not sustainable (Exhibit 20).

Meanwhile, although there are

legitimate corporate-debt concerns

two tempering forces. First, the

most levered of China’s companies

are state-owned, meaning they are

Second, China has a long historywith debt bubbles that seem to

arrive roughly once a decade, but

just as importantly there is also

a long history of the government

stepping in and providing relief.

Already, the government has bailed

out local government borrowers. As

a result, China’s credit excesses – to

the extent that they arrive – are far

0

40

80

120

160

200

240

280320

360

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

L e v e r a g e r a t i o ( % )

Note: Measured as median and 90th percentile of total-liabilities-to-total-equity ratio of listedcorporations in China. SOEs refers to state-owned enterprises. Source: IMF GFSR, RBC GAM

SOEs

Private firms

SOEs

Private firms

SOEs havehigher

leverage thanprivate firms atboth median

and 90th

percentile

90th percentile:

Median:

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 23/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 21

Exhibit 22: China rebalancing to slower growth

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

1995 1999 2003 2007 2011 2015

E c o n o m i c A c t i v i t y I n d e x

( s t a n d a r d d e v i a t i o n s f r o m

h i s t o r i c a l n o r m )

C h i n a G D P g r o w t h

( Y o Y % c h a n g e )

GDP Growth (LHS) Economic Activity Index (RHS)Note: Index constructed using sixteen proxies for real economic activity in China.Source: Bloomberg, Haver Analytics, RBC GAM

-100

-50

0

50

2008 2009 2010 2011 2012 2013 2014 2015 C h a n g e i n c e n t r a l b a n k p o l i c y r a t e s

( % r a i s i n g

/ c u t t i n g i n m o n t h )

% of central banks tightening % of central banks easing

Net % of banks easingNote: Based on policy rate for 30 countries. Source: Haver Analytics, RBC GAM

Widespread easingin reaction tofinancial crisis

Emergingmarket ledtightening

Persistentlyaccomodative policy

Tightening

Easing

economic growth than to manifest

the world.

Decelerating Chinese growth

The Chinese economy has

decelerated for a number of years,

and is now expanding at just

under a 7% annual pace. Given the

diminished competitiveness, growth

growth target of 6.5% per annum,

down from the prior 7.0% goal. We

suspect actual growth may come

in even a little below the newly

diminished target.

the Chinese economy is actually

metric broadly agrees with the

pessimistic interpretations tend to

focus on heavy-industry metrics

such as electricity consumption and

rail shipments. Heavy industry is

indeed struggling, but consumer-

oriented and service sectors are

underweighted in such measures,

China has slowed but not collapsed.

Divergent monetary policy

set to become even more apparent

in the near future. Whereas the Fed

wishes to tighten rates imminently,

the vast majority of the world’s major

in monetary-easing mode (Exhibit

23). China and India both recently

cut their policy rates again, the

Japan (BOJ) contemplates additional

stimulus as well.

entertaining the delivery of more

stimulus, the rationale generally

developed world and decelerating

extent that this additional monetary

stimulus helps to spur growth in

an otherwise sluggish economic

environment, it is welcome. Since the

a country’s currency.

At the other monetary policy

extreme, the world’s bellwether

begin raising rates (Exhibit 24). Most

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 24/80

22 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

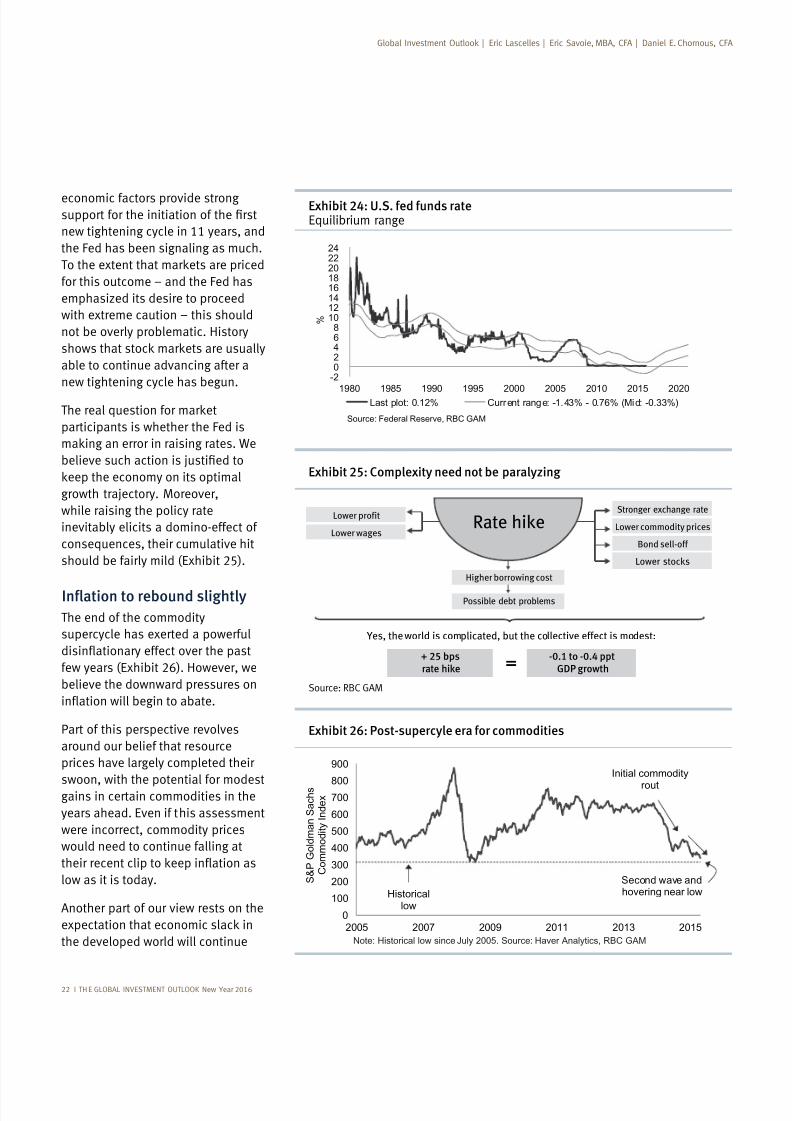

Exhibit 25: Complexity need not be paralyzing

Stronger exchange rate

Lower commodity prices

Bond sell-off

Lower stocks

Higher borrowing cost

Possible debt problems

Lower profit

Lower wagesRate hike

+ 25 bpsrate hike

-0.1 to -0.4 ppt

GDP growth

Yes, the world is complicated, but the collective effect is modest:

=

Exhibit 26: Post-supercyle era for commodities

0

100

200

300

400

500

600

700800

900

2005 2007 2009 2011 2013 2015

S & P G o l d m a n S a c h s

C o m m o d i t y I n d e x

Note: Historical low since July 2005. Source: Haver Analytics, RBC GAM

Initial commodity

rout

Second wave andhovering near lowHistorical

low

economic factors provide strong

new tightening cycle in 11 years, and

the Fed has been signaling as much.

for this outcome – and the Fed has

emphasized its desire to proceed

with extreme caution – this should

not be overly problematic. History

able to continue advancing after a

new tightening cycle has begun.

participants is whether the Fed is

growth trajectory. Moreover,

while raising the policy rate

inevitably elicits a domino-effect of

consequences, their cumulative hit

should be fairly mild (Exhibit 25).

The end of the commodity

supercycle has exerted a powerful

few years (Exhibit 26). However, we

believe the downward pressures on

Part of this perspective revolves

around our belief that resource

prices have largely completed their

swoon, with the potential for modestgains in certain commodities in the

years ahead. Even if this assessment

were incorrect, commodity prices

would need to continue falling at

low as it is today.

Another part of our view rests on the

the developed world will continue

Source: RBC GAM

Exhibit 24: U.S. fed funds rateEquilibrium range

-202468

1012141618202224

1980 1985 1990 1995 2000 2005 2010 2015 2020

%

Last plot: 0.12% Current range: -1.43% - 0.76% (Mid: -0.33%)

Source: Federal Reserve, RBC GAM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 25/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 23

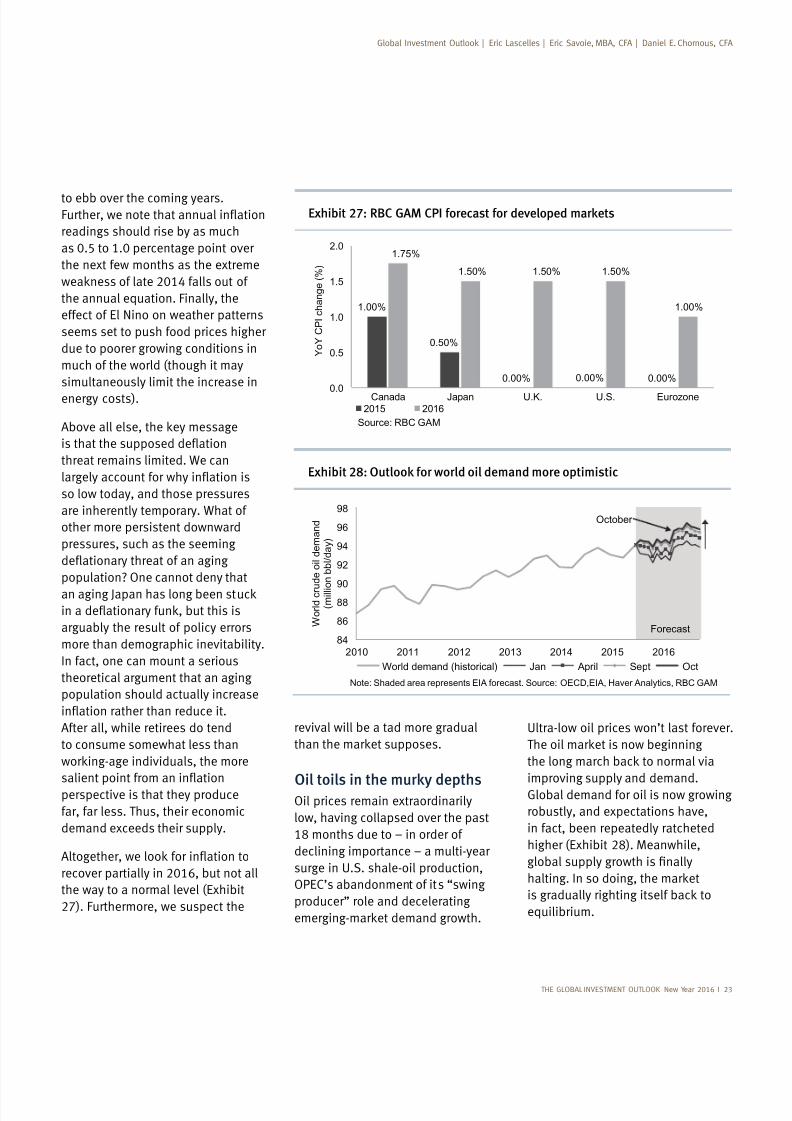

Exhibit 27: RBC GAM CPI forecast for developed markets

1.00%

0.50%

0.00% 0.00% 0.00%

1.75%

1.50% 1.50% 1.50%

1.00%

0.0

0.5

1.0

1.5

2.0

Canada Japan U.K. U.S. Eurozone

Y o Y C P I c h a n g e ( % )

2015 2016

Source: RBC GAM

Exhibit 28: Outlook for world oil demand more optimistic

84

86

8890

92

94

96

98

2010 2011 2012 2013 2014 2015 2016

W o r l d c r u d e o i l d e m a n d

( m i l l i o n b b l / d a y )

World demand (historical) Jan April Sept Oct

October

Forecast

Note: Shaded area represents EIA forecast. Source: OECD,EIA, Haver Analytics, RBC GAM

to ebb over the coming years.

readings should rise by as much

as 0.5 to 1.0 percentage point over

the next few months as the extreme

the annual equation. Finally, the

effect of El Nino on weather patterns

seems set to push food prices higher

due to poorer growing conditions in

much of the world (though it may

simultaneously limit the increase in

energy costs).

threat remains limited. We can

so low today, and those pressures

are inherently temporary. What of

other more persistent downward

pressures, such as the seeming

population? One cannot deny that

arguably the result of policy errors

more than demographic inevitability.

In fact, one can mount a serious

theoretical argument that an aging

population should actually increase

After all, while retirees do tend

to consume somewhat less than

perspective is that they produce

far, far less. Thus, their economic

demand exceeds their supply.

recover partially in 2016, but not all

the way to a normal level (Exhibit

27). Furthermore, we suspect the

revival will be a tad more gradual

Oil toils in the murky depthsOil prices remain extraordinarily

low, having collapsed over the past

declining importance – a multi-year

surge in U.S. shale-oil production,

OPEC’s abandonment of its “swing

producer” role and decelerating

Ultra-low oil prices won’t last forever.

improving supply and demand.

Global demand for oil is now growing

robustly, and expectations have,

in fact, been repeatedly ratcheted

equilibrium.

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 26/80

24 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

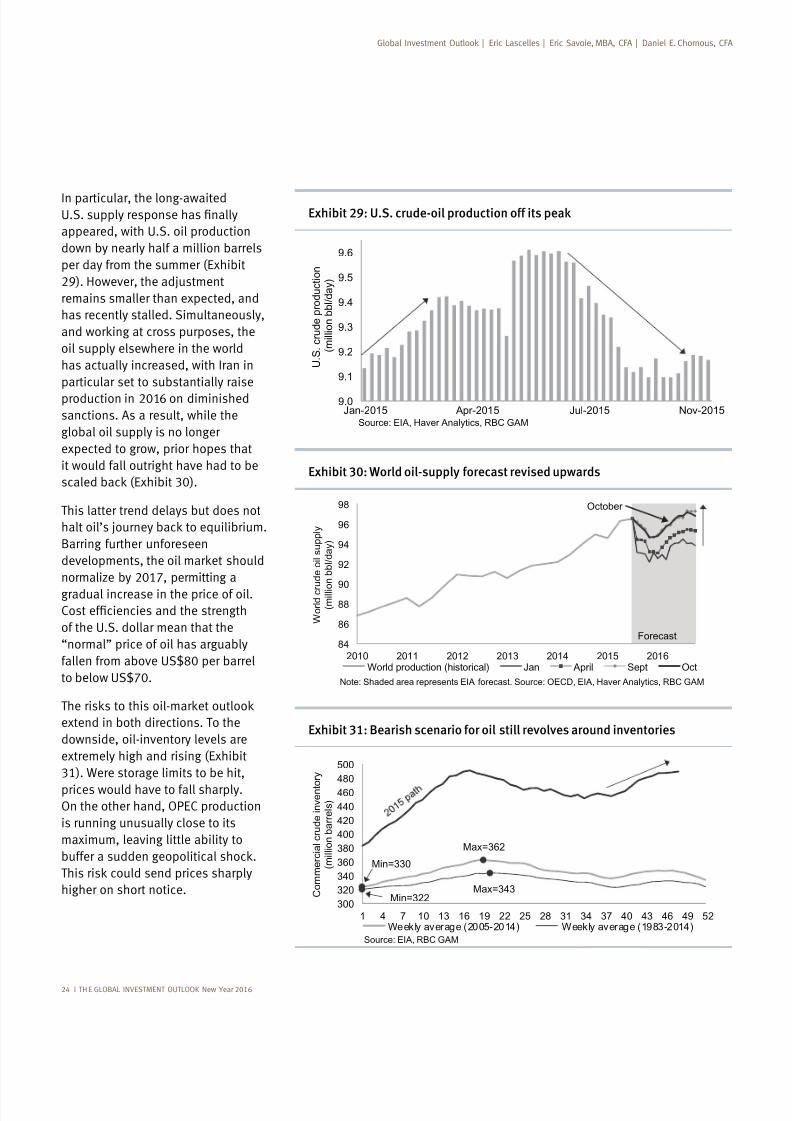

Exhibit 29: U.S. crude-oil production off its peak

9.0

9.1

9.2

9.3

9.4

9.5

9.6

Jan-2015 Apr-2015 Jul-2015 Nov-2015

U . S . c r u d e p r o d u c t i o n

( m i l l i o n b b l / d a y )

Source: EIA, Haver Analytics, RBC GAM

Exhibit 30: World oil-supply forecast revised upwards

84

86

8890

92

94

96

98

2010 2011 2012 2013 2014 2015 2016

W o r l d c r

u d e o i l s u p p l y

( m i l l i o n b b l / d a y )

World production (historical) Jan April Sept Oct

October

Forecast

Note: Shaded area represents EIA forecast. Source: OECD, EIA, Haver Analytics, RBC GAM

Exhibit 31: Bearish scenario for oil still revolves around inventories

Max=343Min=322

Max=362

Min=330

300

320

340

360

380

400

420

440

460

480

500

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

C o m m e r c i a l c r u d e i n v e n t o

r y

( m i l l i o n b a r r e l s )

Weekly average (2005-2014) Weekly average (1983-2014)Source: EIA, RBC GAM

In particular, the long-awaited

appeared, with U.S. oil production

down by nearly half a million barrels

per day from the summer (Exhibit

remains smaller than expected, and

has recently stalled. Simultaneously,

oil supply elsewhere in the world

has actually increased, with Iran in

particular set to substantially raise

production in 2016 on diminished

sanctions. As a result, while the

global oil supply is no longer

expected to grow, prior hopes that

it would fall outright have had to be

This latter trend delays but does not

Barring further unforeseen

normalize by 2017, permitting a

gradual increase in the price of oil.

of the U.S. dollar mean that the

“normal” price of oil has arguably

to below US$70.

extend in both directions. To the

downside, oil-inventory levels are

extremely high and rising (Exhibit

31). Were storage limits to be hit,

prices would have to fall sharply.On the other hand, OPEC production

is running unusually close to its

maximum, leaving little ability to

higher on short notice.

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 27/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 25

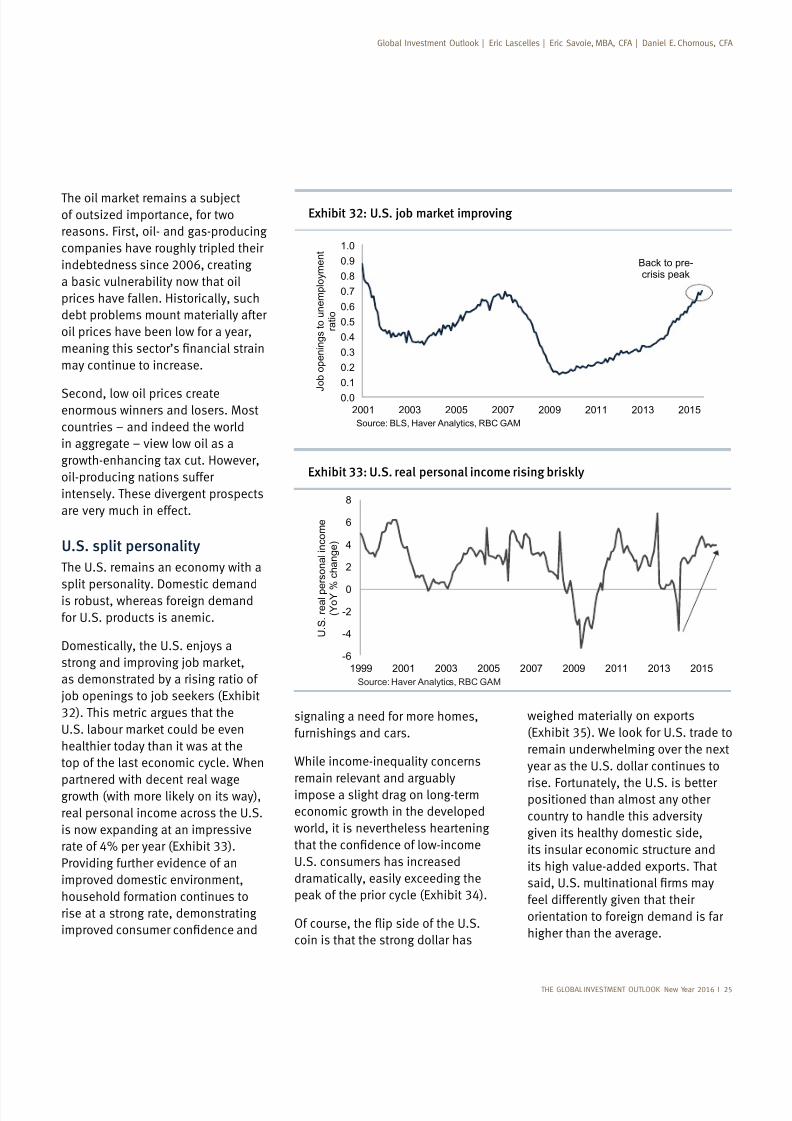

Exhibit 32: U.S. job market improving

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

2001 2003 2005 2007 2009 2011 2013 2015

J o b o p e n i n g s t o u n e m p l o y m e n t

r a t i o

Source: BLS, Haver Analytics, RBC GAM

Back to pre-crisis peak

Exhibit 33: U.S. real personal income rising briskly

-6

-4

-2

0

2

4

6

8

1999 2001 2003 2005 2007 2009 2011 2013 2015

U . S . r e a l p e r s o n a l i n c o m e

( Y o Y %

c h a n g e )

Source: Haver Analytics, RBC GAM

of outsized importance, for two

reasons. First, oil- and gas-producing

companies have roughly tripled their

indebtedness since 2006, creating

a basic vulnerability now that oil

prices have fallen. Historically, such

debt problems mount materially after

oil prices have been low for a year,

may continue to increase.

Second, low oil prices createenormous winners and losers. Most

countries – and indeed the world

in aggregate – view low oil as a

growth-enhancing tax cut. However,

oil-producing nations suffer

intensely. These divergent prospects

are very much in effect.

U.S. split personality

The U.S. remains an economy with a

is robust, whereas foreign demand

for U.S. products is anemic.

as demonstrated by a rising ratio of

32). This metric argues that the

healthier today than it was at the

top of the last economic cycle. When

partnered with decent real wage

real personal income across the U.S.

is now expanding at an impressive

rate of 4% per year (Exhibit 33).

Providing further evidence of an

improved domestic environment,

household formation continues to

rise at a strong rate, demonstrating

signaling a need for more homes,

furnishings and cars.

While income-inequality concerns

remain relevant and arguably

impose a slight drag on long-term

economic growth in the developed

world, it is nevertheless heartening

U.S. consumers has increased

dramatically, easily exceeding the

coin is that the strong dollar has

weighed materially on exports

remain underwhelming over the next

year as the U.S. dollar continues to

rise. Fortunately, the U.S. is betterpositioned than almost any other

country to handle this adversity

given its healthy domestic side,

its insular economic structure and

its high value-added exports. That

feel differently given that their

orientation to foreign demand is far

higher than the average.

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 28/80

26 I THE GLOBAL INVESTMENT OUTLOOK New Year 2016

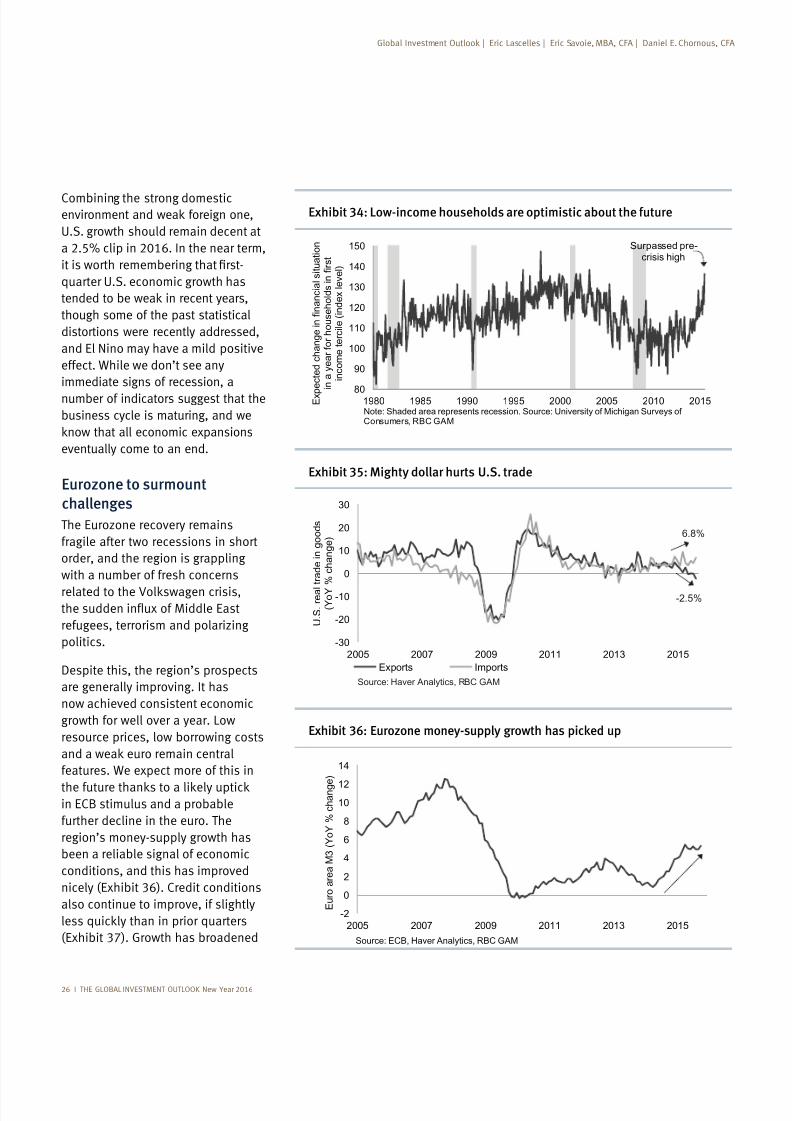

Exhibit 35: Mighty dollar hurts U.S. trade

-30

-20

-10

0

10

20

30

2005 2007 2009 2011 2013 2015

U . S . r e a l t r a d e i n g o o d s

( Y o Y

% c

h a n g e )

Exports Imports

Source: Haver Analytics, RBC GAM

6.8%

-2.5%

Exhibit 36: Eurozone money-supply growth has picked up

-2

0

2

4

6

8

10

12

14

2005 2007 2009 2011 2013 2015

E u r o a r e a M 3 ( Y o Y %

c h a n g e )

Source: ECB, Haver Analytics, RBC GAM

Combining the strong domesticenvironment and weak foreign one,

U.S. growth should remain decent at

a 2.5% clip in 2016. In the near term,

it is worth remembering that first-

quarter U.S. economic growth has

tended to be weak in recent years,

though some of the past statistical

distortions were recently addressed,

and El Nino may have a mild positive

effect. While we don’t see any

immediate signs of recession, a

number of indicators suggest that the

business cycle is maturing, and we

know that all economic expansions

eventually come to an end.

Eurozone to surmount

challenges

The Eurozone recovery remains

fragile after two recessions in short

order, and the region is grappling

with a number of fresh concerns

related to the Volkswagen crisis,the sudden influx of Middle East

refugees, terrorism and polarizing

politics.

Despite this, the region’s prospects

are generally improving. It has

now achieved consistent economic

growth for well over a year. Low

resource prices, low borrowing costs

and a weak euro remain central

features. We expect more of this in

the future thanks to a likely uptickin ECB stimulus and a probable

further decline in the euro. The

region’s money-supply growth has

been a reliable signal of economic

conditions, and this has improved

nicely (Exhibit 36). Credit conditions

also continue to improve, if slightly

less quickly than in prior quarters

(Exhibit 37). Growth has broadened

Global Investment Outlook | Eric Lascelles | Eric Savoie, MBA, CFA | Daniel E. Chornous, CFA

Exhibit 34: Low-income households are optimistic about the future

80

90

100

110

120

130

140

150

1980 1985 1990 1995 2000 2005 2010 2015Note: Shaded area represents recession. Source: University of Michigan Surveys ofConsumers, RBC GAM

Surpassed pre-crisis high

E x p

e c

t e d c

h a n g e

i n f i n a n c

i a l s

i t u a

t i o n

i n a y e a r

f o r

h o u s e

h o

l d s

i n f i r s t

i n c o m e

t e r c

i l e ( i n d e x

l e v e

l )

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 29/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016 I 27

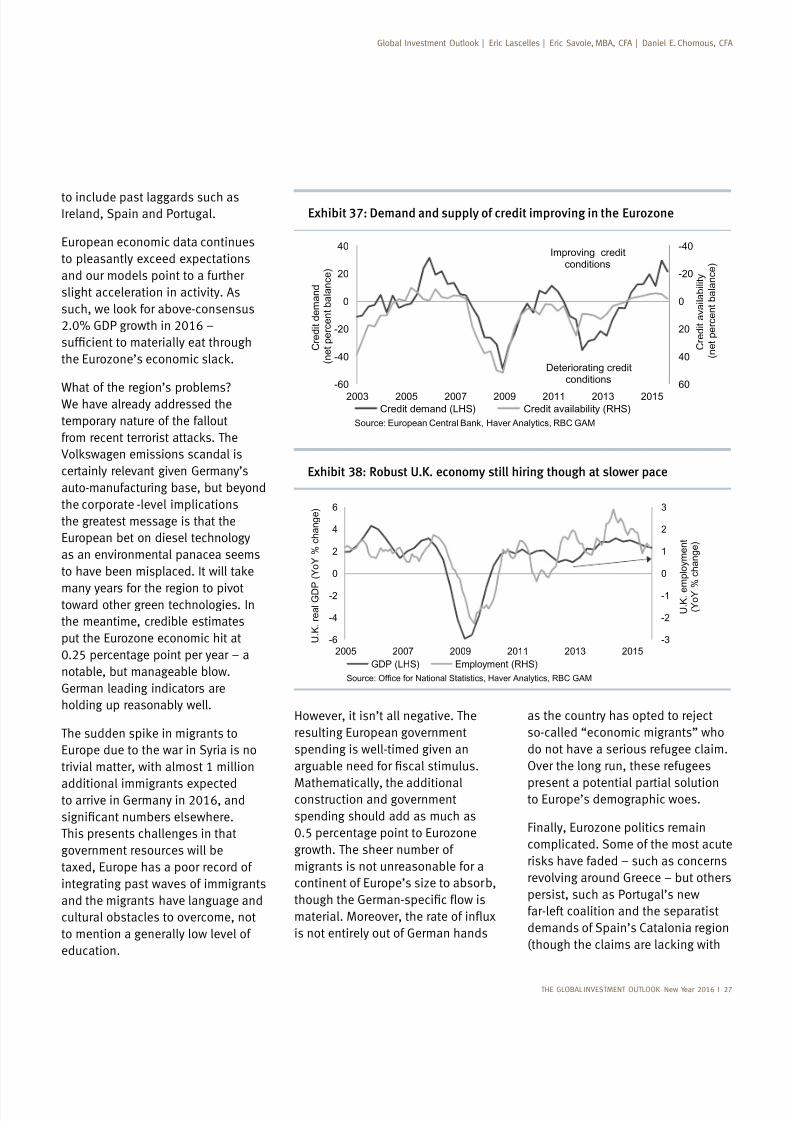

to include past laggards such asIreland, Spain and Portugal.

European economic data continues

to pleasantly exceed expectations

and our models point to a further

slight acceleration in activity. As

What of the region’s problems?We have already addressed the

temporary nature of the fallout

certainly relevant given Germany’s

auto-manufacturing base, but beyond

the corporate -level implications

the greatest message is that the

European bet on diesel technology

as an environmental panacea seems

many years for the region to pivottoward other green technologies. In

the meantime, credible estimates

put the Eurozone economic hit at

0.25 percentage point per year – a

notable, but manageable blow.

German leading indicators are

holding up reasonably well.

Europe due to the war in Syria is no

trivial matter, with almost 1 million

additional immigrants expectedto arrive in Germany in 2016, and

This presents challenges in that

government resources will be

taxed, Europe has a poor record of

integrating past waves of immigrants

and the migrants have language and

cultural obstacles to overcome, not

to mention a generally low level of

education.

Exhibit 37: Demand and supply of credit improving in the Eurozone

-40

-20

0

20

40

60-60

-40

-20

0

20

40

2003 2005 2007 2009 2011 2013 2015

C r e d i t a v a i l a b i l i t y

( n e t p e r c e n t b a l a n c e )

C r e d i t d e m a n d

( n e t p e r c e n t b a l a n c e )

Credit demand (LHS) Credit availability (RHS)

Source: European Central Bank, Haver Analytics, RBC GAM

Improving creditconditions

Deteriorating creditconditions

Exhibit 38: Robust U.K. economy still hiring though at slower pace

-3

-2

-1

0

1

2

3

-6

-4

-2

0

2

4

6

2005 2007 2009 2011 2013 2015

U . K . e m p l o y m e n t

( Y o Y % c h a n g e )

U . K . r e a l G D P ( Y o Y % c h a n g e )

GDP (LHS) Employment (RHS)

Source: Office for National Statistics, Haver Analytics, RBC GAM

However, it isn’t all negative. The

resulting European government

spending is well-timed given an

Mathematically, the additionalconstruction and government

spending should add as much as

0.5 percentage point to Eurozone

growth. The sheer number of

migrants is not unreasonable for a

continent of Europe’s size to absorb,

is not entirely out of German hands

as the country has opted to reject

so-called “economic migrants” who

do not have a serious refugee claim.

Over the long run, these refugees

present a potential partial solutionto Europe’s demographic woes.

Finally, Eurozone politics remain

complicated. Some of the most acute

revolving around Greece – but others

persist, such as Portugal’s new

far-left coalition and the separatist

demands of Spain’s Catalonia region

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 30/80

New Year 2016

regard to legitimacy and legality).

European politics will continue to

drift further from centre as hot-

button issues such as bailouts,

continue to push voters in a more

populist direction.

U.K. steady

The British economy continues to

trundle along at a reasonable rate ofgrowth, providing one of the more

stable economic environments in

the world. Economic growth and job

creation are both adequate, if a bit

less zippy than in the recent past

Anecdotes from the ground

remain fairly good, though leading

indicators have softened a touch.

austerity, achieved greater political

Conservative government and is not

yet staring at a promised referendum

on EU membership in the face.

British economy no longer has much

success, but also brings the reality

of higher wages and the prospect of

seriously contemplating tightening

monetary policy (Exhibit 40). We

the Fed.

continued steady and roughly

consensus economic growth of

around 2.5%. A reviving Eurozone

economy is helpful, as is the recent

Japanese silver linings

It is easy to be sour on Japan.

demographics and high public debt

Prime Minister Abe’s three-year-old

“Abenomics,” has been a failure.

However, in our opinion, this grim

perspective misses some important

victories.

As an opening observation,

the country’s recent economic

performance is not quite as poor as

it seems. Much of the latest quarterly

decline in output related to inventory

has also continued to shift higher,

Exhibit 39: U.K. wage growth accelerates

-3

-2

-1

0

1

2

3

4

5

6

2005 2007 2009 2011 2013 2015

T o t a l p r i v a t e s e c t o r p a y

( Y o Y % c h a n g e )

Note: 6-month moving average of year-over-year % change of private sector pay.Source: Office for National Statistics, Haver Analytics, RBC GAM

Exhibit 40: U.K. base rate equilibrium range

-2

0

2

4

6

8

10

12

14

16

18

1980 1985 1990 1995 2000 2005 2010 2015 2020

%

Last plot: 0.50% Current range: -1.87% - 0.71% (Mid: -0.58%)

Source: RBC GAM, RBC CM

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 31/80

THE GLOBAL INVESTMENT OUTLOOK New Year 2016

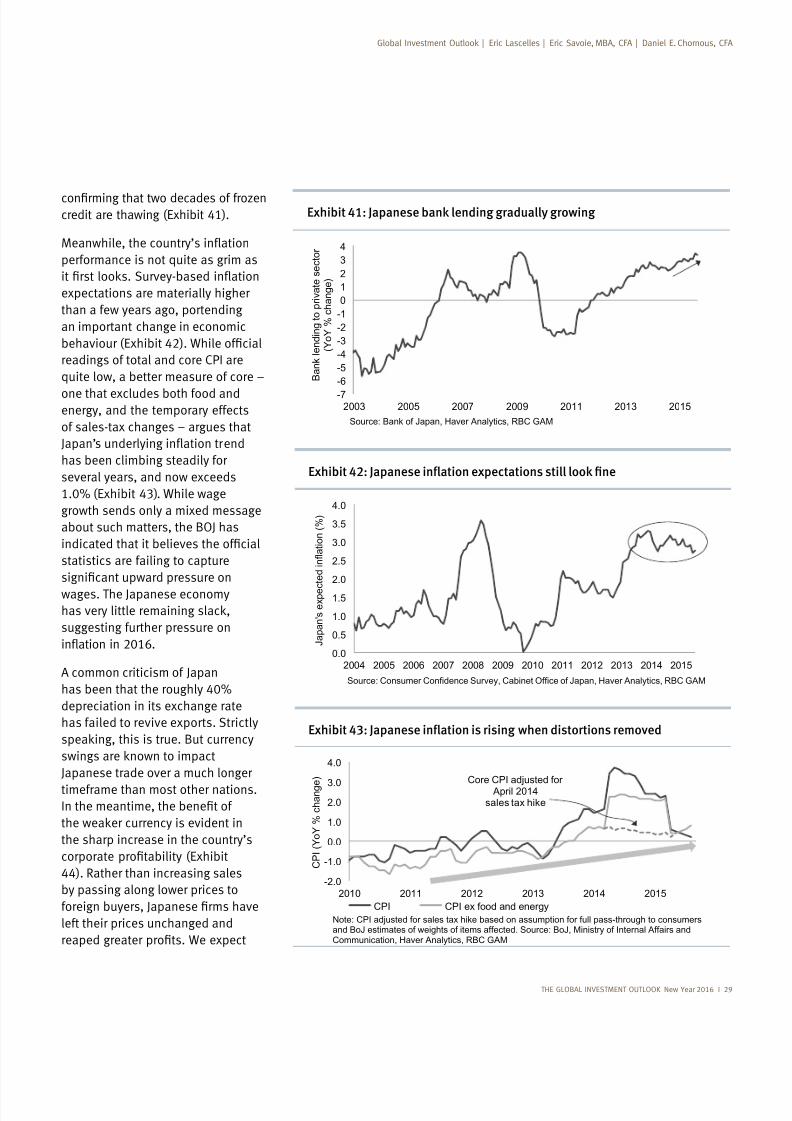

credit are thawing (Exhibit 41).

performance is not quite as grim as

expectations are materially higher

than a few years ago, portending

an important change in economic

readings of total and core CPI are

quite low, a better measure of core –

one that excludes both food andenergy, and the temporary effects

of sales-tax changes – argues that

has been climbing steadily for

several years, and now exceeds

1.0% (Exhibit 43). While wage

growth sends only a mixed message

about such matters, the BOJ has

statistics are failing to capture

wages. The Japanese economy

suggesting further pressure on

A common criticism of Japan

has been that the roughly 40%

depreciation in its exchange rate

has failed to revive exports. Strictly

Japanese trade over a much longer

timeframe than most other nations.

the sharp increase in the country’s

44). Rather than increasing sales

by passing along lower prices to

left their prices unchanged and

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

2003 2005 2007 2009 2011 2013 2015

B a n k l e n d i n g t o p r i v a t e s e c t o r

( Y o Y % c h a n g e )

Source: Bank of Japan, Haver Analytics, RBC GAM

Exhibit 41: Japanese bank lending gradually growing

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

J a p a n ' s e x p e c t e d i n f l a t i o n ( % )

Source: Consumer Confidence Survey, Cabinet Office of Japan, Haver Analytics, RBC GAM

-2.0

-1.0

0.0

1.0

2.03.0

4.0

2010 2011 2012 2013 2014 2015

C P I ( Y o Y % c h a n g e )

CPI CPI ex food and energy

Note: CPI adjusted for sales tax hike based on assumption for full pass-through to consumersand BoJ estimates of weights of items affected. Source: BoJ, Ministry of Internal Affairs andCommunication, Haver Analytics, RBC GAM

Core CPI adjusted for April 2014

sales tax hike

7/25/2019 Global Investment Outlook

http://slidepdf.com/reader/full/global-investment-outlook 32/80

30 I TH E GLOBAL INVESTMENT OUTLOOK New Year 2016

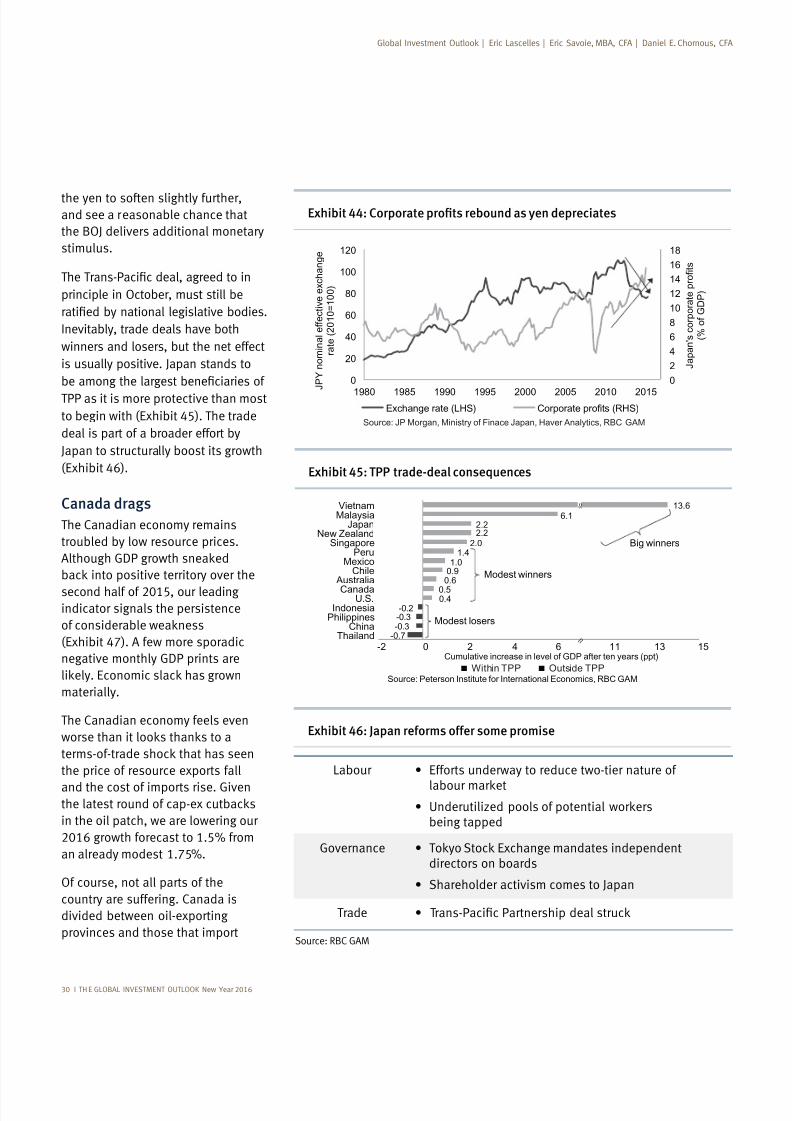

the yen to soften slightly further,and see a reasonable chance that

the BOJ delivers additional monetary

stimulus.

principle in October, must still be

Inevitably, trade deals have both

winners and losers, but the net effect

is usually positive. Japan stands to

TPP as it is more protective than most

to begin with (Exhibit 45). The trade

deal is part of a broader effort by

Japan to structurally boost its growth

(Exhibit 46).

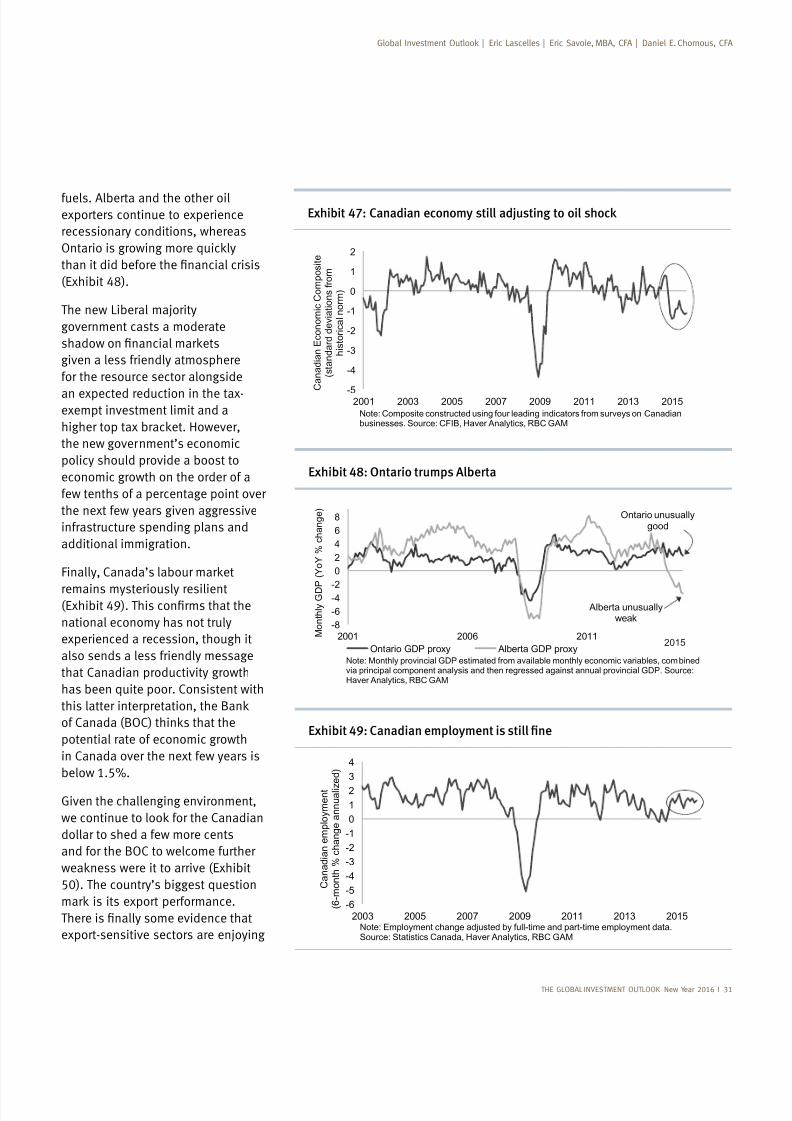

Canada drags

The Canadian economy remains

troubled by low resource prices.

second half of 2015, our leadingindicator signals the persistence

(Exhibit 47). A few more sporadic

materially.

The Canadian economy feels even

the price of resource exports fall

and the cost of imports rise. Given

in the oil patch, we are lowering our

2016 growth forecast to 1.5% from

an already modest 1.75%.

Of course, not all parts of the

country are suffering. Canada is

divided between oil-exporting

provinces and those that import

0

2

4

6

8

10

12

14

16

18

0

20

40

60

80

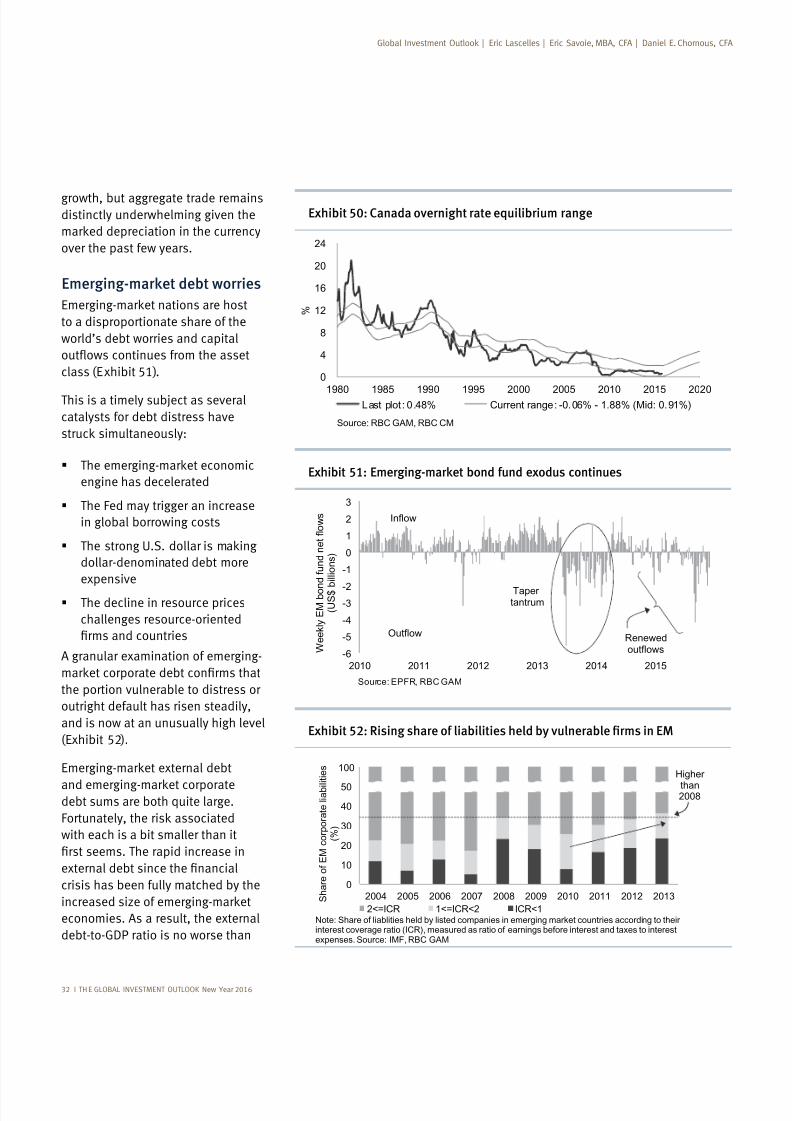

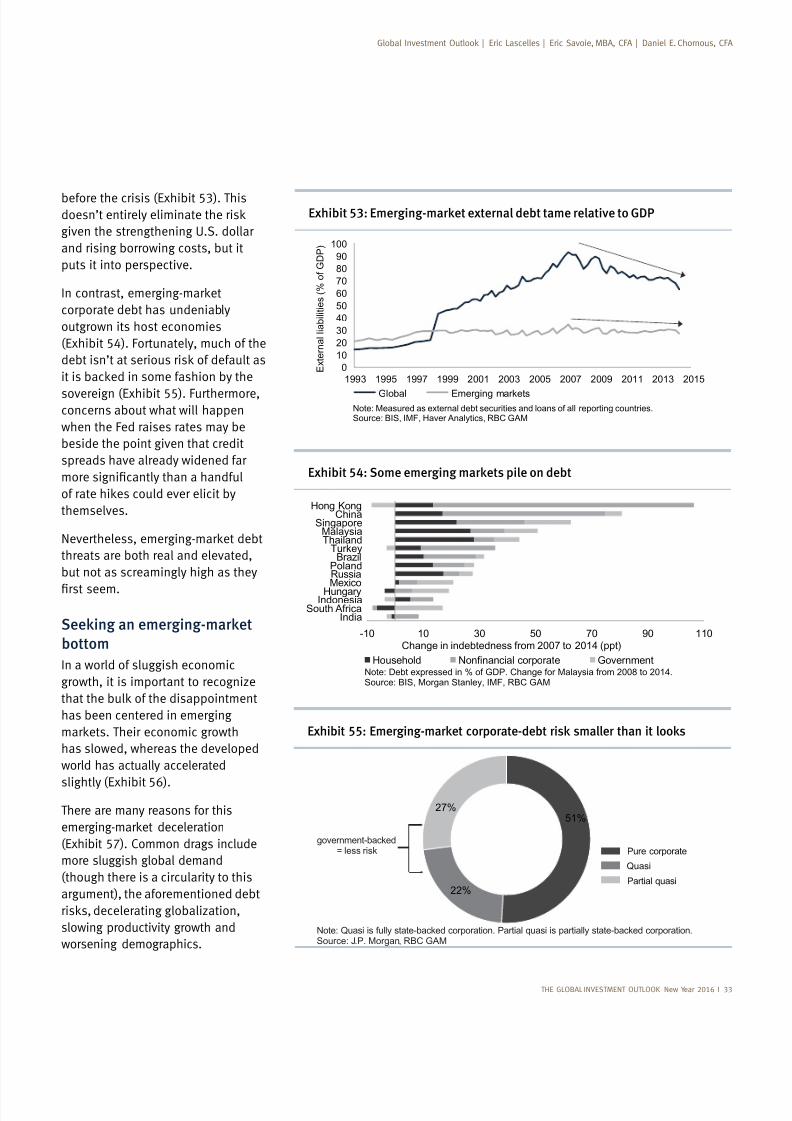

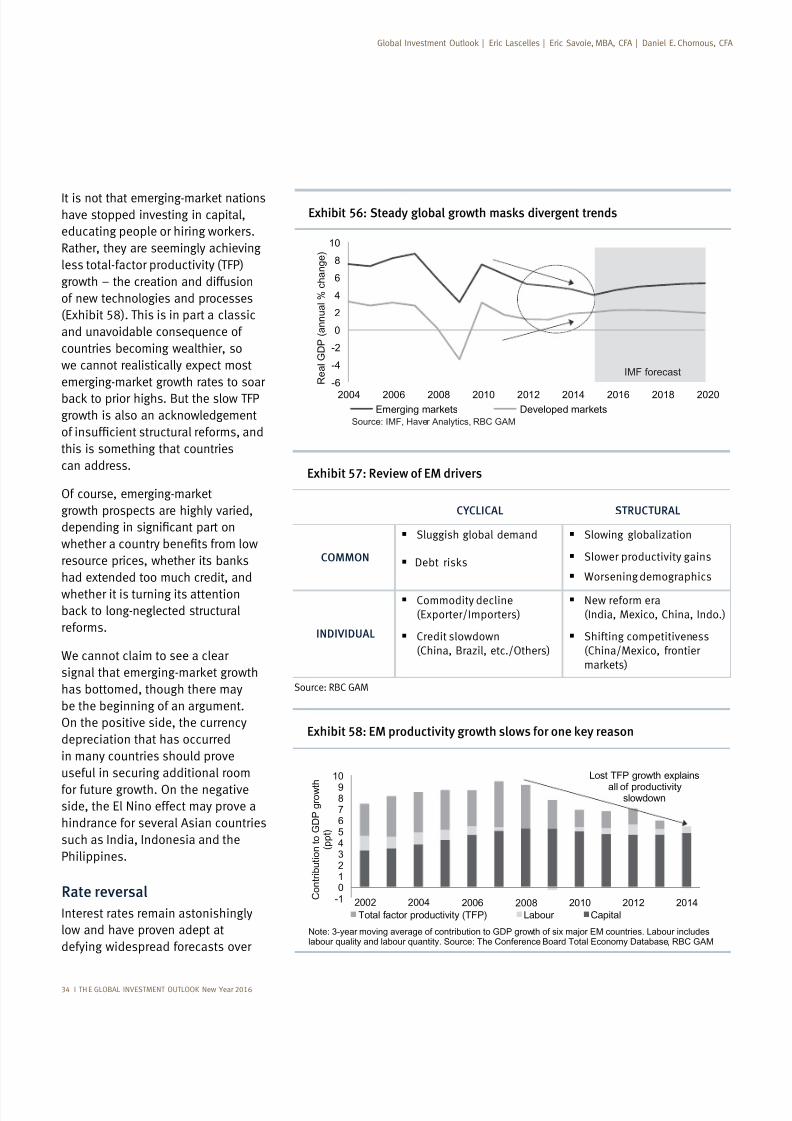

100