Embed Size (px)

Citation preview

20th

July, 2011

ANS Research Desk (Research Wing of ANS Pvt Ltd)

“ARHAM” Financial Centre

Harihar Chowk, Rajkot (Guj)

Speak to: 0281 – 6699401

Drop a line to: [email protected]

Gujarat Gas Limited (Initiating Coverage)

Nifty 5616

Sensex 18661

Script Details

Equity Capital `̀̀̀ 25.65 Cr

Face Value ` ` ` ` 2

Market Cap `̀̀̀ 5253

52 Weeks High/Low 454/296

6-month avg. volume

(BSE) 9268

(NSE) 3077

Shareholding Pattern As On Sep’10 (%)

Promoters 65.12

Corporate Bodies & 25.48

Institutions

Public 9.40

Research Analyst: Pranav Mehta

Company

Background:

Gujarat Gas Company Limited (GGCL)

largest private sector player in the natural gas transmission and

GGCL has been a pioneer in the natural gas distribution to industrial, commercial and

domestic customers.

since 1997 and currently BG group is the company’s

shareholder.

The company currently

Surat, Ankleshwar and Bharuch.

commercial &

(CNG) users. It has a pipeline network spread over 3700 kms.

Promoter’s background:

The BG group

across 5 continent

chain. It is listed on the London stock exchange and on the US over the counter

market known as OTCQX.

65%

25%10%

PROMOTER CB & INST PUBLIC

Recomm

BSE Code

NSE Code:

Company Overview

Background:

Gujarat Gas Company Limited (GGCL) was incorporated in 19

largest private sector player in the natural gas transmission and

GGCL has been a pioneer in the natural gas distribution to industrial, commercial and

domestic customers. The company has been a part of the British Gas (BG) group

since 1997 and currently BG group is the company’s

shareholder.

The company currently operates in the state of Gujarat in the industrialized regions of

Surat, Ankleshwar and Bharuch. It supplies gas to more than 317000 domestic,

commercial & domestic customers while serving over 144000 compressed natural gas

(CNG) users. It has a pipeline network spread over 3700 kms.

Promoter’s background:

The BG group is located in United Kingdom and it currently

across 5 continents. The company has in-depth experience across the entire gas

chain. It is listed on the London stock exchange and on the US over the counter

market known as OTCQX.

Recommendation: Accumulate Coverage Initiated on:

BSE Code: 523477 Bloomberg Code: GGAS IN CMP

NSE Code: GUJARATGAS Reuters Code: GGAS.BO Buy at

was incorporated in 1980 and is India’s

largest private sector player in the natural gas transmission and distribution business.

GGCL has been a pioneer in the natural gas distribution to industrial, commercial and

The company has been a part of the British Gas (BG) group

since 1997 and currently BG group is the company’s promoter and largest

in the industrialized regions of

supplies gas to more than 317000 domestic,

domestic customers while serving over 144000 compressed natural gas

(CNG) users. It has a pipeline network spread over 3700 kms.

is located in United Kingdom and it currently operates in 27 countries

depth experience across the entire gas

chain. It is listed on the London stock exchange and on the US over the counter

Coverage Initiated on: 20th

July, 2011

GGAS IN CMP `̀̀̀ 410

Buy at `̀̀̀ 385 or less

Promoter’s Presence in India

BG E&P India

Limited

BGIES

GGCL

MGL

Industrial Production in Gujarat

Promoter’s Presence in India :

BG E&P India

Limited

Panna Mukti Tapti(PMT): Jointly operated

Co-venturers: BG (30%), ONGC (40%),

Krishna Godavari Basin -Block KG-OSN

Co-venturers: BG (45%), ONGC (operator 55%)

Mahanadi Basin -MN-DWN-2002/02

Co-venturers: BG (25%), ONGC (operator 75%)

Krishna Godavari Basin -KG-DWN-2009/1

venturers: BG 30% (Operator), ONGC (45%), OIL (15%), APGIC

(10%), BG (25%), ONGC (operator 75%)

BGIES LNG importers, Gas Aggregators ,Bulk Industrial,

operators, Power

GGCL India’s largest private CGD company (by volumes)

India’s largest private CGD company (by customers)

JV with GAIL (49.75% each), State Govt. (0.5%)

Source: Company Presentation, BG Group Data book 2 010

Industrial Production in Gujarat

Source: Company presentation Govt. of Gujarat

33%

21%

9%

7%

6%24%

0%

Petro Prod. Chemicals Food Textile Basic Mat

Panna Mukti Tapti(PMT): Jointly operated

venturers: BG (30%), ONGC (40%), RIL (30%)

OSN-2004/1 (Exploration Block)

BG (45%), ONGC (operator 55%)

2002/02(Exploration Block)

BG (25%), ONGC (operator 75%)

2009/1 (Exploration Block) Co-

venturers: BG 30% (Operator), ONGC (45%), OIL (15%), APGIC

(25%), ONGC (operator 75%)

LNG importers, Gas Aggregators ,Bulk Industrial, Fertilizer, CGD

India’s largest private CGD company (by volumes)

India’s largest private CGD company (by customers)

JV with GAIL (49.75% each), State Govt. (0.5%)

Source: Company Presentation, BG Group Data book 2 010

Source: Company presentation Govt. of Gujarat

Others

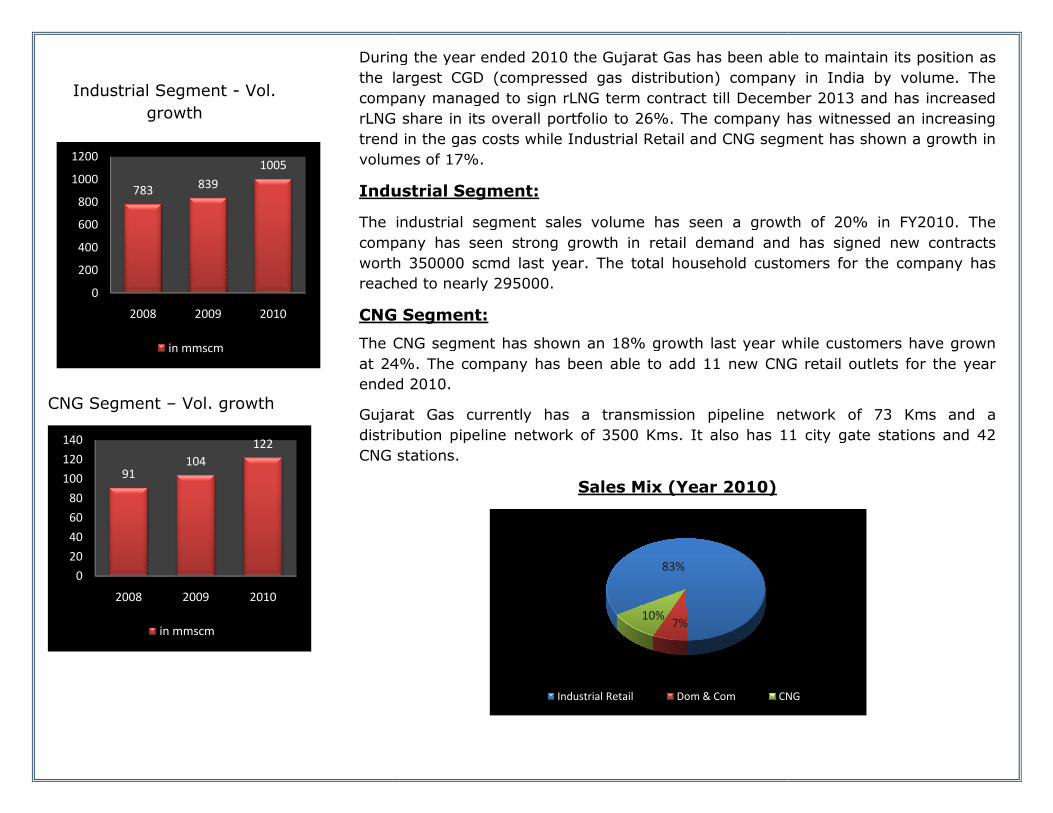

Industrial Segment - Vol.

growth

CNG Segment – Vol. growth

During the year ended 2010 the

the largest CGD (compressed gas distribution) company in India by volume. The

company managed to sign

rLNG share in

trend in the gas costs while Industrial Retail and CNG segment has shown a growth

volumes of

Industrial Segment:

The industrial segment

company has seen strong growth in retail demand

worth 350000 scmd last year. The total household customers for the company has

reached to nearly 295000

CNG

The CNG segment has shown an 18% growth last year while

at 24%. The company has been able to add 11 new CNG retail outlets for the year

ended 2010.

Gujarat Gas currently has a transmission pipeline network of 73 Kms and a

distribution pipeline network of 3500 Kms. It also has 11 city gate s

CNG stations.

91104

122

0

20

40

60

80

100

120

140

2008 2009 2010

in mmscm

783839

1005

0

200

400

600

800

1000

1200

2008 2009 2010

in mmscm

During the year ended 2010 the Gujarat Gas has been able to

the largest CGD (compressed gas distribution) company in India by volume. The

company managed to sign rLNG term contract till December 2013 and has increase

rLNG share in its overall portfolio to 26%. The company has witnessed an increasing

trend in the gas costs while Industrial Retail and CNG segment has shown a growth

volumes of 17%.

Industrial Segment:

The industrial segment sales volume has seen a growth of

company has seen strong growth in retail demand and has signed new contracts

worth 350000 scmd last year. The total household customers for the company has

reached to nearly 295000.

CNG Segment:

The CNG segment has shown an 18% growth last year while

at 24%. The company has been able to add 11 new CNG retail outlets for the year

ended 2010.

Gujarat Gas currently has a transmission pipeline network of 73 Kms and a

distribution pipeline network of 3500 Kms. It also has 11 city gate s

CNG stations.

Sales Mix (Year 2010)

83%

7%10%

Industrial Retail Dom & Com CNG

has been able to maintain its position as

the largest CGD (compressed gas distribution) company in India by volume. The

contract till December 2013 and has increased

portfolio to 26%. The company has witnessed an increasing

trend in the gas costs while Industrial Retail and CNG segment has shown a growth in

seen a growth of 20% in FY2010. The

and has signed new contracts

worth 350000 scmd last year. The total household customers for the company has

The CNG segment has shown an 18% growth last year while customers have grown

at 24%. The company has been able to add 11 new CNG retail outlets for the year

Gujarat Gas currently has a transmission pipeline network of 73 Kms and a

distribution pipeline network of 3500 Kms. It also has 11 city gate stations and 42

CNG

Expected Sectoral Gas Utilization

for XI-XII five year plans

Source: Working Group for P&NG

sector for XI plan (2007-12)

Industry Scenario

Presently Natural Gas

and is rapidly gaining popularity in India due to its ease of handling, better energy

efficiency and environmental friendliness. It is expected that by 2020 natural gas will

constitute about 23% o

With the starting of supplies from KG D6 fields there has been a rapid growth in

India’s gas production. The ministry of Petroleum and Natural Gas under the

direction of empowered group of ministers allocates gas from the D6 fiel

Gas Utilization policy. There is

while the demand is expected to

will remain dependent on imported LNG for some years to come.

Currently the main consumers of natural gas are power and fertilizer units. The

demand from City Gas Distribution customers, natural gas vehicles, households and

commercial establishments has also shown good growth over past few years.

GAIL PMT

49%GAIL APM

5%

NIKO

5%

CAIRN

15%rLNG

26%

Gas Sourcing Mix

45%

25%

6%8%13%3%

Power Fertilizer City Gas

Industrial Petrochem Sponge Iron

Industry Scenario

Presently Natural Gas currently forms about 11% of India’s primary energy basket

and is rapidly gaining popularity in India due to its ease of handling, better energy

efficiency and environmental friendliness. It is expected that by 2020 natural gas will

constitute about 23% of India’s energy basket.

With the starting of supplies from KG D6 fields there has been a rapid growth in

India’s gas production. The ministry of Petroleum and Natural Gas under the

direction of empowered group of ministers allocates gas from the D6 fiel

Gas Utilization policy. There is a shortage in availability of gas from indigenous

while the demand is expected to remain on an upward trajectory. As a result

ill remain dependent on imported LNG for some years to come.

Currently the main consumers of natural gas are power and fertilizer units. The

demand from City Gas Distribution customers, natural gas vehicles, households and

commercial establishments has also shown good growth over past few years.

Source: Working Group for P&NG sector for XI plan (2007

Source: Company Annual Report

0

50

100

150

200

250

300

350

2010 2011 2012 2013

Demand

currently forms about 11% of India’s primary energy basket

and is rapidly gaining popularity in India due to its ease of handling, better energy

efficiency and environmental friendliness. It is expected that by 2020 natural gas will

With the starting of supplies from KG D6 fields there has been a rapid growth in

India’s gas production. The ministry of Petroleum and Natural Gas under the

direction of empowered group of ministers allocates gas from the D6 fields as per

availability of gas from indigenous fields

remain on an upward trajectory. As a result India

ill remain dependent on imported LNG for some years to come.

Currently the main consumers of natural gas are power and fertilizer units. The

demand from City Gas Distribution customers, natural gas vehicles, households and

commercial establishments has also shown good growth over past few years.

Group for P&NG sector for XI plan (2007-12)

Source: Company Annual Report, Company Presentation

2014

LATEST QUARTER’S FINANCIAL HIGHLIGHTS

Source: ACE Equity, ANS Research

PROFIT & LOSS (6 months ended 2010) (CONSOLIDATED RESULTS)

(In Crores)

Particulars Mar-2011 Mar-2010 % VAR

Net Sales 520.30 401.40 29.62

Other Income 10.13 3.96 156

Total Exp. 420.36 307.49 36.71

Op. Profit 118.90 106.50 11.64

Interest 0.04 0.03 9.38

Depreciation 14.51 12.84 13.02

PBT 104.36 93.63 11.45

Tax 32.06 31.64 1.33

PAT 72.30 62.0 16.61

Adjusted EPS (Annualized) 22.48 19.24 16.86

PBIDTM % 22.11 25.58 13.55

PATM% 13.45 14.89 9.69

PROFIT & LOSS (CONSOLIDATED

Particulars Dec 13 (E) Dec 12 (E) Dec 11 (E) Dec

Net Sales 2885.74 2531.35 2182.20 1849.33

Total Exp. 2258.08 1980.77 1707.56 1435.15

Other Income 40.40 35.44 30.55 23.83

EBIDTA 627.66 550.58 474.63 438.01

Depreciation 78.40 71.64 62.60 54.21

Interest 0.65 0.57 0.49 0.46

EBT 548.60 478.36 411.54 383.34

Tax 177.91 155.13 133.46 124.32

PAT/ Net Profit 369.42 321.96 276.80 257.75

Adjusted EPS 28.84 25.15 21.64 20.20

Div (%) 225 200 200 600

BALANCE SHEET (CONSOLIDATED

Particulars Dec 13 (E) Dec 12 (E) Dec 11 (E) Dec

Share Capital 40.05 40.05 40.05 40.05

Total Funds 1636.21 1335.49 1074.74 859.14

Total Debts 242.41 212.64 183.31 155.35

Net Block 1050.92 906.11 775.05 661.46

Net Current Assets -284.17 -243.52 -208.69 -174.78

Total Assets 1851.48 1586.66 1359.72 1165.24

Cont. Liabilities 41.84 41.84 41.84 41.84

Book Value/Share 127.31 103.91 83.62 66.99

0

300

600

900

1200

1500

1800

2100

2400

2700

3000

3300

3600

Net Sales Total Exp.

2009 2010 2011 (E)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Funds Debt

2009 2010 2011 (E) 2012 (E)

CONSOLIDATED RESULTS)

(IN CRORES)

Dec 10 Dec 09

1849.33 1419.67

1435.15 1140.17

23.83 26.65

438.01 306.15

54.21 47.38

0.46 0.14

383.34 258.63

124.32 83.61

257.75 174.16

20.20 13.65

600 400

CONSOLIDATED RESULTS)

(IN CRORES)

Dec 10 Dec 09

40.05 40.05

859.14 779.70

155.35 127.37

661.46 606.43

174.78 -144.05

1165.24 1021.71

41.84 35.0

66.99 60.80

EBIDTA PAT

2012 (E) 2013 (E)

Total Assets B.V./Share

2012 (E) 2013 (E)

CASH FLOW (CONSOLIDATED RESULTS)

(IN CRORES)

Particulars Dec 13 (E) Dec 12 (E) Dec 11 (E) Dec 10 Dec 09

EBIT 548.60 478.36 411.54 383.34 258.63

Depreciation 78.40 71.64 62.60 54.21 47.38

Working Capital Changes -40.64 -34.83 -33.91 -14.0 -36.42

Taxes -177.91 -155.13 -133.46 -123.62 -77.84

Cash From Operations 409.01 360.52 307.17 287.36 178.16

Capital Expenditure 148.12 126.93 108.78 115.15 155.31

Free Cash Flow 260.89 233.59 198.39 172.21 22.85

Cash From Investments -199.37 -162.46 -154.79 -216.41 -196.60

Cash From Financing -39.58 -32.45 -33.74 -69.5 3.89

Net Cash Inflow/Outflow 170.06 165.61 118.64 1.45 -14.55

Opening Cash & Cash Equity 293.62 128 9.36 7.91 22.47

Closing Cash & Cash Equiv. 463.67 293.62 128 9.36 7.91

Z-Score Sheet

Particulars 06 07 08 09 10

Working Capital/Total Assets -0.12 -0.09 -0.08 -0.15 -0.16

Retained Earn/Total Assets 0.13 0.19 0.16 0.06 0.07

EBIT/Total Assets 0.24 0.33 0.27 0.28 0.36

MCAP/Total Liabilities 0.31 1.77 1.07 3.43 4.88

Net Worth/Total Liabilities 5.16 5.28 5.72 5.05 4.17

Z-Score 6.64 7.75 7.88 6.34 5.96

Safe Safe Safe Safe Safe

IMPORTANT RATIOS (CONSOLIDATED RESULTS)

Particulars Dec 13 (E) Dec 12 (E) Dec 11 (E) Dec 10 Dec 09

EBIDTA Margin (%) 21.45 21.45 21.45 23.38 21.17

Net Profit Margin (%) 12.62 12.54 12.51 13.76 12.04

D/E 0.15 0.16 0.17 0.18 0.16

Financial Leverage (X) 1.16 1.22 1.31 1.33 1.30

Current Ratio 3.53 3.53 3.53 4.10 3.42

Cash Ratio 1.30 1.0 0.57 0.24 0.20

ROANW (%) 24.86 26.72 28.63 31.46 23.15

ROAIC (%) 37.84 38.50 38.65 40.35 32.09

EV/Sales 1.74 2.04 2.43 2.91 2.20

EV/EBIDTA 8.0 9.38 11.16 13 11.16

Profit Plough back (%) 84.40 84.10 81.51 40.58 41.38

Total Asset Turnover (X) 1.68 1.72 1.73 1.69 1.45

DCF Valuation (Per share):

Source: ANS Research

FY 11 FY 12 FY 13 FY 14 FY 15 Terminal

EBIDTA 474.63 550.58 627.66 702.98 787.33

Tax Payable 133.46 155.13 177.91 198.24 220.84

Changes in W.C. 33.91 34.83 40.64 47.43 55.34

Capex 108.78 126.93 148.12 172.84 201.69

Free Cash Flow 265.81 302.77 341.62 378.59 419.34 241.29

Intermediate growth rate 8%

Terminal growth rate 3%

WACC 7.56%

Enterprise Value 6414

Debt 155.35

Per Share value 487

Investment Positives

Changing perception about Natural Gas will result in good growth potential for the

company

Natural gas consumption is slowly gaining acceptance among both the industrial and

retail users. With the green initiative being launched across the world to counter global

warming, natural gas has been accepted as one of the preferred sources of energy due

to its greener and cleaner image. This change in perception will definitely play a very

important role in helping Gujarat gas grow its business.

Rapid Growth expected in company’s region of operations

The southern belt of Gujarat consisting of Ankleshwar, Bharuch and Surat has been

seeing rapid development for past few years and these regions are slowly being

heavily industrialized due to the efforts of Gujarat Government. Surat is one of India’s

fastest growing cities and many MOUs have been signed by the Gujarat government

during the Vibrant Gujarat Global Investors’ summit in 2011 for investments in and

around Surat and Bharuch districts. These factors would help Gujarat Gas in achieving

good growth going forward as more and more industries set up their operations in the

region and switch to cleaner fuels like natural gas for their energy needs.

Parent’s strong global positioning and focus on increasing rLNG in supply mix

BG’s global rLNG portfolio will help Gujarat gas ride out these tough times wherein the

input costs have been increasing due to higher LNG prices. Due to its proximity to BG

the company will be able to source rLNG at competitive prices. Moreover Gujarat Gas

is also expected to increasingly target industrial segments which might provide greater

headroom for price hikes thereby helping it maintain its margins.

Investment Risks

Sourcing of Gas will remain a key challenge

Gujarat gas may face supply problems from indigenous sources of natural gas due to

shortfall in the overall supply. To protect itself from the domestic shortfall of natural

gas the company has entered into a contract with its parent BG group for receiving

rLNG supply for the medium term.

Increasing prices of Natural Gas

Due to strained supplies and higher demand, the prices of natural gas have

been increasing resulting in margin pressures building up on the company.

Other Risks

Regulatory Challenges

Competitive Challenges

Peer Comparison Particulars (Mar 2011) GSPL Petronet LNG Indraprastha Gas

(In Crores) Standalone Standalone Standalone

Net Sales 1046 13197.29 1966.92

Total Expenditure 77.16 11980.98 1263.49

EBIDTA 990.99 1284.26 505.48

PAT 506.38 619.62 259.77

EPS 8.97 8.26 18.55

Equity Capital 562.58 750 140

Total Reserves 1442.42 1930.16 1003

Total Debt 1483.50 3216.14 463.30

Latest Enterprise Value 6354.26 14184 5934.69

D/E 0.74 1.20 0.46

PBIDTM (%) 92.63 9.73 25.70

PATM (%) 48.39 4.70 13.21

ROCE (%) 28.29 20.69 34.30

ROE (%) 28.38 25.21 28.40

Dividend (%) 10 20 50

Sources: ANS Research

1 Year performance of Gujarat Gas vs.

Nifty

Valuation & Recommendations

Gujarat Gas is solely focused on natural gas which has a bright future in India. The

company is being backed by one of big International gas player and it has been

successfully able to leverage this relationship in its domestic operations. Going

forward management is confident that company will be able to deliver good growth

and would be able to maintain its margins provided that the input costs of natural

gas do not rise considerably.

We have assumed that revenues are likely to grow by a CAGR of 15% over FY11 (E)-

13(E) period and have kept the EBIDTA margins in the range of 21% as per historical

performance.

At the current market price of ` 410 GGCL trades at a trailing PE of 20.14. We expect

FY 11 (E) forward EPS to be ` 21.64 and FY 12 (E) forward EPS to be ` 25.15. So at

CMP GGCL is trading at a one year forward PE of 18.94 and a two year forward PE

of 16.30 respectively.

We think that the stock has potential to go to higher levels and our target price

comes to nearly ` 487. Investors can accumulate this stock near ` 385 or below

levels. The stock has outperformed the general markets in last 2 years giving a

return of 272% since March 2009 and so investors should remain cautious on the

near term return performance of the stock. However, the stock is a good long term

play on the natural gas with a good management and very low cost debt and so

investors can hope to get good returns with a 3-4 years perspective.

Disclaimer: The information being provided to you is compiled from sources we believe to be reliable. ANS Pvt. Ltd cannot and does not take any

guarantees about the accuracy, reliability, validity or timeliness of the information and/or data provided/made available to you in this document.

The views are purely indicative. Neither ANSPL nor any of its associates, subsidiaries, affiliates, directors, and/or officials become liable or have any

kind of responsibility for any loss or damage that you may incur from any decisions taken by you based on our recommendations. None of the

information contained herein constitutes a solicitation from ANSPL to Buy and/or Sell securities and/or any Future, Options or Other Financial

Contracts. Clients may exercise their own caution and double check or verify the information contained in our recommendations.