Embed Size (px)

Citation preview

Healthcare & Medical Technologies

Japan Market Study

JANUARY 2018

© Copyright EU Gateway | Business Avenues

The information and views set out in this study are those of the author(s) and do not necessarily reflect the official opinion of the European Union. Neither the European Union institutions and bodies nor any person acting on their behalf may be held responsible for the use which may be made of the information contained therein. The contents of this publication are the sole responsibility of EU Gateway | Business Avenues and can in no way be taken to reflect the views of the European Union. The purpose of this report is to give European companies selected for participation in the EU Gateway | Business Avenues Programme an introductory understanding of the target markets countries and support them in defining their strategy towards those markets. For more information, visit www.eu-gateway.eu.

Healthcare & Medical Technologies – Japan Market Study - Page 3 of 121

EU Gateway to Japan

Central Management Unit

Japan Market Study

JANUARY 2018

Submitted to the European Commission on 10 January 2018

Healthcare & Medical Technologies – Japan Market Study - Page 4 of 121

Table of Contents

TABLE OF FIGURES .................................................................................................................................................. 7

LIST OF ABBREVIATIONS ........................................................................................................................................ 9

1. EXECUTIVE SUMMARY HEALTHCARE & MEDICAL TECHNOLOGIES .......................................................... 11

1.1. JAPANESE MARKET AND THE EU ........................................................................................................... 11

1.2. HEALTHCARE MARKET IN JAPAN ............................................................................................................ 12

1.3. MARKET TRENDS HEALTHCARE & MEDICAL TECHNOLOGIES ................................................................... 13

1.4. ASSISTIVE TECHNOLOGIES ..................................................................................................................... 15

1.5. MEDICAL EQUIPMENT ............................................................................................................................ 15

1.6. ICT FOR HEALTHCARE & MEDICAL TECHNOLOGIES ................................................................................ 16

1.7. TELEMEDICINE AND REMOTE HEALTH MONITORING ................................................................................. 17

1.8. NANOTECHNOLOGY FOR HEALTHCARE & MEDICAL TECHNOLOGIES ........................................................ 17

1.9. BIOTECHNOLOGY FOR HEALTHCARE & MEDICAL TECHNOLOGIES ............................................................ 18

1.10. DENTAL PRODUCTS AND TECHNOLOGIES ............................................................................................. 18

1.11. HEALTHCARE & MEDICAL TECHNOLOGIES REGULATIONS ..................................................................... 19

2. WHAT ARE THE CHARACTERISTICS OF JAPAN? .......................................................................................... 23

2.1. POLITICAL OVERVIEW ............................................................................................................................ 25

2.2. ECONOMIC OVERVIEW ........................................................................................................................... 25

2.3. TRADE OVERVIEW BETWEEN EU AND JAPAN .......................................................................................... 28

3. HEALTHCARE & MEDICAL TECHNOLOGIES MARKET OVERVIEW AND EU ENTRY OPPORTUNITIES .......... 32

3.1. JAPANESE HEALTHCARE & MEDICAL TECHNOLOGIES MARKET ............................................................... 32

3.1.1. Short Historic Healthcare & Medical Technologies Market Overview ........................................... 32

3.1.2. Market Overview Healthcare & Medical Technologies .................................................................. 33

3.1.3. Market Trends Healthcare & Medical Technologies ...................................................................... 40

3.1.4. Import Market of Healthcare & Medical Technologies ................................................................... 42

3.2. ASSISTIVE TECHNOLOGIES ..................................................................................................................... 43

3.2.1. Market Overview Assistive Technologies ...................................................................................... 43

3.2.2. EU Entry Opportunities Assistive Technologies ............................................................................ 47

3.2.3. Japanese Market Players .............................................................................................................. 55

3.3. MEDICAL EQUIPMENT ............................................................................................................................ 58

3.3.1. Market Overview Medical Equipment ............................................................................................ 58

3.3.2. Trends in Medical Device Market .................................................................................................. 62

3.3.3. EU Entry Opportunities Medical Equipment .................................................................................. 63

3.4. ICT FOR HEALTHCARE & MEDICAL TECHNOLOGIES ................................................................................ 66

Healthcare & Medical Technologies – Japan Market Study - Page 5 of 121

3.4.1. Market Overview ICT for Healthcare & Medical Technologies ...................................................... 66

3.4.2. Market Trends ICT for Healthcare & Medical Technologies .......................................................... 67

3.4.3. EU Entry Opportunities for ICT in Healthcare & Medical Technologies ........................................ 69

3.5. TELEMEDICINE AND REMOTE HEALTH MONITORING ................................................................................. 73

3.5.1. Market Overview Telemedicine and Remote Health Monitoring ................................................... 73

3.5.2. Market Trends Telemedicine and Remote Health Monitoring ....................................................... 76

3.5.3. EU Entry Opportunities Telemedicine and Remote Health Monitoring ......................................... 76

3.6. NANOTECHNOLOGY HEALTHCARE .......................................................................................................... 77

3.6.1. Market Overview Nanotechnology Healthcare .............................................................................. 77

3.6.2. Market Trends Nanotechnology Healthcare .................................................................................. 78

3.6.3. EU Entry Opportunities Nanotechnology Healthcare .................................................................... 80

3.7. LIFE SCIENCE / BIOTECHNOLOGY FOR HEALTHCARE ............................................................................... 81

3.7.1. Market Overview Life Science / Biotechnology for Healthcare ...................................................... 81

3.7.2. Market Trends Life Science / Biotechnology for Healthcare ......................................................... 82

3.7.3. EU Entry Opportunities Life Science / Biotechnology for Health ................................................... 83

3.8. DENTAL PRODUCTS AND TECHNOLOGIES ............................................................................................... 85

3.8.1 Market Overview Dental Products .................................................................................................. 85

3.8.2. Market Trends Dental Products ..................................................................................................... 87

3.8.3. EU Entry Opportunities Dental Products ....................................................................................... 88

4. HEALTHCARE & MEDICAL TECHNOLOGIES REGULATIONS ....................................................................... 91

4.1. HEALTHCARE & MEDICAL TECHNOLOGIES REGULATIONS ....................................................................... 91

4.1.1. Pharmaceuticals and Medical Device Act (PMD Act) .................................................................... 91

4.1.2. Application and Approval ............................................................................................................... 92

4.1.3. Long-Term Care Insurance (LCTI) system .................................................................................. 100

4.1.4. Medical Fees and Insurance Reimbursement ............................................................................. 103

4.1.5. Other Regulations ........................................................................................................................ 104

5. ANNEXES............................................................................................................................................................ 106

5.1. HEALTHCARE & MEDICAL TECHNOLOGIES INDUSTRY ASSOCIATIONS ..................................................... 106

5.2. HEALTHCARE & MEDICAL TECHNOLOGIES TRADE FAIRS ....................................................................... 108

5.3. LIST OF HEALTHCARE & MEDICAL TECHNOLOGIES COMPANIES IN JAPAN .............................................. 110

5.3.1. Terumo Corporation ..................................................................................................................... 110

5.3.2. Olympus Corporation ................................................................................................................... 110

5.3.3. Nipro Corporation ........................................................................................................................ 111

5.3.4. Hitachi Healthcare Manufacturing ............................................................................................... 111

5.3.5. Fukuda Denshi ............................................................................................................................. 112

5.3.6. Nihon Kohden .............................................................................................................................. 112

Healthcare & Medical Technologies – Japan Market Study - Page 6 of 121

5.4. EUROPEAN HMT COMPANIES IN JAPAN ................................................................................................ 113

5.4.1. Philips Electronics Japan ............................................................................................................. 113

5.4.2. LivaNova ...................................................................................................................................... 113

5.5. BIBLIOGRAPHY AND REFERENCES ........................................................................................................ 116

Healthcare & Medical Technologies – Japan Market Study - Page 7 of 121

Table of Figures

Figure 1: Various sources, total market value approx. 6.76 trillion JPY in FY2014, Telemedicine is below 1% market share..................................................................... 13

Figure 2: various sources ........................................................................................................... 15

Figure 3: Pharmaceuticals and Medical Devices Agency, https://www.pmda.go.jp/english/review-services/outline/0001.html ............................ 21

Figure 4: Japan Factsheet, several sources .............................................................................. 23

Figure 5: © Abenomics, Cabinet of the Prime Minister website .................................................. 26

Figure 6: EU-Japan Trade Relationship-Facts and Figures, European Commission, 2017 ....... 28

Figure 7: The EU-Japan EPA in 60 seconds, European Commission, Trade, 2017 .................. 29

Figure 8: Eurostat, European Commission, Directorate-General for Trade, May 2017 .............. 29

Figure 9: © Cabinet Public Relations Office, July 2017............................................................... 30

Figure 10: © Five Decades of Universal Health Insurance Coverage in Japan: Lessons and future challenges, Japanese Society of Medical Sciences, Yasuki KOBAYASHI ..... 32

Figure 11: various online resources ........................................................................................... 34

Figure 12: Overview of National Medical Expenditures for 2013, Ministry of Health Labour and Welfare (MLHW) ................................................................................................ 34

Figure 13: United Nations, World Population Prospects, the 2015 Revision .............................. 35

Figure 14: The World Pharmaceutical Markets Fact Book 2014, Espicom ................................ 36

Figure 15: © Basic Review Process for Drug of Medical Device Application, Pharmaceutical and Medical Devices Agency (PMDA) ...................................................................... 37

Figure 16: © Supply Chain of Medical Devices in Japan, Pharmaceutical and Medical Devices Agency (PMDA) .......................................................................................... 37

Figure 17: © Demystifying Device Reimbursement in Japan-Device Talk, EMERGO, 2017 ...... 39

Figure 18: Compiled by JETRO based on the “International Comparison of Regulations for Regenerative Medicine and Cell Therapy 2013” by the National Institute of Health Sciences ................................................................................................................... 40

Figure 19: JETRO, Attractive Sectors: Life Science, 2016 ......................................................... 42

Figure 20: Japan’s Welfare Equipment and Daily Life Support Equipment, Japanese, July 2016 .................................................................................................................. 44

Figure 21: Japan’s Welfare Equipment and Daily Life Support Equipment, Japanese, July 2016 .................................................................................................................. 45

Figure 22: Services available under Long-Term Care Insurance (LTCI) .................................... 46

Figure 23: Assistive Devices available for Rental Services ........................................................ 48

Figure 24: Commercialised Products developed by NRDPMWA ............................................... 50

Figure 25: © Healthcare Support System to Remotely Monitor the Elderly, Fujitsu Journal Online, 2014 .......................................................................................................................... 52

Figure 26: TrendForce, May 2015 .............................................................................................. 54

Figure 27: © AFP/GETTY and © Professor SANKAI, University of Tsukuba/Cyberdyne: Cyberdyne employees wearing a HAL robot-suit walking in Tokyo .......................... 55

Healthcare & Medical Technologies – Japan Market Study - Page 8 of 121

Figure 28: © RIKEN-TRI Collaboration Centre for Human-Interactive Robot Research. RIBA uses two arms to lift a person lying in bed or sitting on a wheelchair, moves and sets the person down ............................................................................. 56

Figure 29: © Robot Seal PARO, Tom Battey .............................................................................. 57

Figure 30: © Annual Report on the Survey of Pharmaceutical Industry Productions 2014, MHLW ....................................................................................................................... 59

Figure 31: © Annual Report on the Survey of Pharmaceutical Industry Productions 2014, MHLW ....................................................................................................................... 60

Figure 32: Gyokai Search, FY2015 Medical Device Industry Sales Ranking, 2016 ................... 61

Figure 33: © Annual Report on the Survey of Pharmaceutical Industry Productions 2014, MHLW ....................................................................................................................... 62

Figure 34: ICT in Healthcare Questionnaire, Ministry of Internal Affairs and Communications, 2016 .......................................................................................................................... 67

Figure 35: © ICT Trends in Japan’s Healthcare Policy, Fujitsu Science Technology, July 2015 .................................................................................................................. 68

Figure 36: © Global Wearable Device Market: Key Research Findings 2016, Yano Research Institute, 2016 ........................................................................................................... 72

Figure 37: © The Japan Times: Prime Minister Shinzo Abe tries out a telemedicine system offered by the city of Minamisoma in Fukushima Prefecture, 2017........................... 74

Figure 38: © Nano Bio First, Kazunori KATAOKA, Funding Program for World-Leading Innovative R&D on Science and Technology (FIRST), 2012 .................................... 79

Figure 39: Nanotechnology Products Database, www.statnano.com ........................................ 80

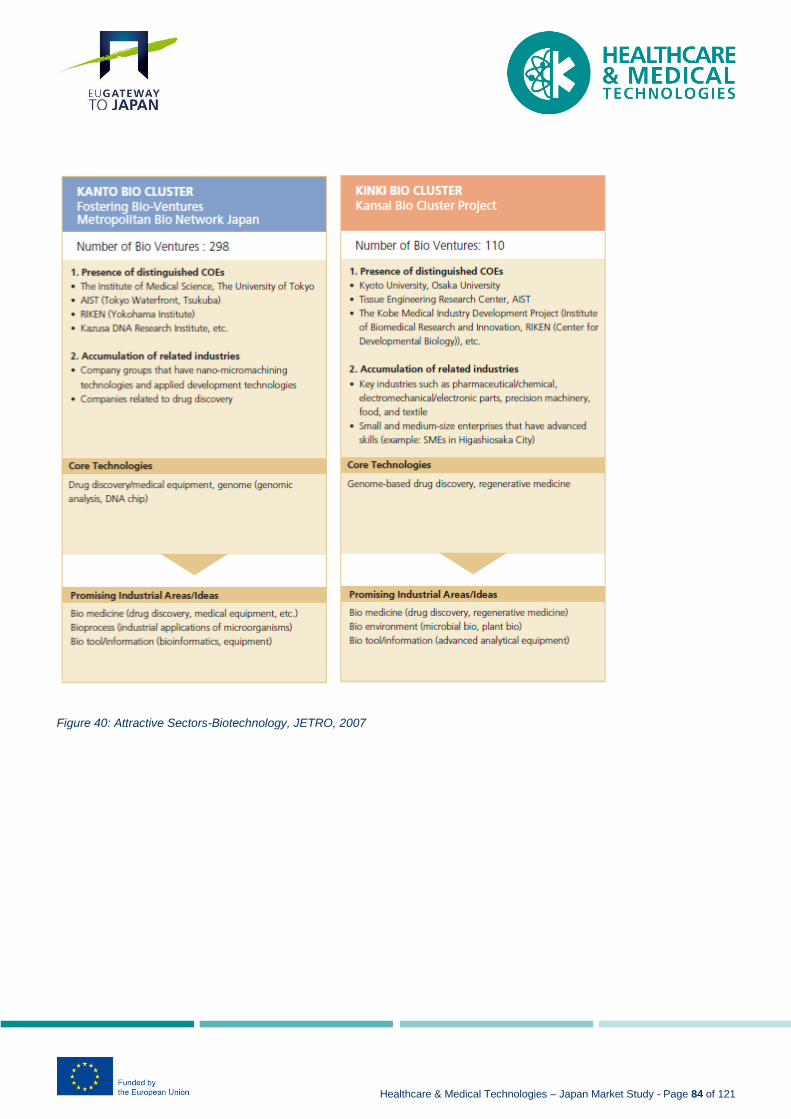

Figure 40: Attractive Sectors-Biotechnology, JETRO, 2007 ....................................................... 84

Figure 41: Figure 36: New Dental Medical Equipment and Dental Medical Technology Industry Vision, Japan Dental Association (JDA), 2017 ............................................ 85

Figure 42: New Dental Medical Equipment and Dental Medical Technology Industry Vision, Japan Dental Association (JDA), 2017 ..................................................................... 87

Figure 43: New Dental Medical Equipment and Dental Medical Technology Industry Vision, Japan Dental Association (JDA), 2017 ..................................................................... 88

Figure 44: Websites MHLW, MIC and others, 2017 ................................................................... 89

Figure 45: © Japan: The Regulatory Process for Medical Devices, Emergo, 2017 .................... 94

Figure 46: © Japan: The Time, Cost and Complexity of Registration, Emergo, 2017 ................. 97

Figure 47: Outline of the Law for Partial Revision of the Pharmaceutical Affairs Law (Act No.84 of 2013) ................................................................................................... 98

Figure 48: Overview LTCI, MHLW 2016 .................................................................................. 100

Figure 49: Overview LTCI, MHLW 2016 .................................................................................. 101

Figure 50: Overview LTCI, MHLW 2016 .................................................................................. 102

Figure 51: Overview LTCI, MHLW 2016 .................................................................................. 103

Figure 52: New Orange Plan, LTCI, MHLW, 2016 ................................................................... 104

Healthcare & Medical Technologies – Japan Market Study - Page 9 of 121

List of Abbreviations

ADEM Agency for Medical Research and Development

AI Artificial Intelligence

AIST National Institute of Advanced Industrial Science and Technology

app(s) Application(s)

ASEAN Association of Southeast Asian Nations

b billion

CAGR Compound Annual Growth Rate

CE Conformité Européene

CT Computed Tomography

DDS Drug Delivery Systems

DPJ Democratic Party of Japan

EHR Electronic Health Record

EPA Economic Partnership Agreement

EU European Union

EUR Euro

FDA Food and Drug Administration

FDI Foreign Direct Investment

FFOPs Follow-On Protein Products

FY Fiscal Year

GDP Gross Domestic Product

HAL Hybrid Assistive Limbo

HHC Home Health Care

HI Health Insurance

IBM International Business Machines

ICT Information and Communication Technology

IoT Internet of Things

iPS Induced Pluripotent Stem

iPSC Induced Pluripotent Stem Cells

IT Information Technology

JASPA Japan Assistive Products Association

JBA Japan Bioindustry Association

JDA Japan Dental Association

JETRO Japan External Trade Organisation

JMDN Japanese Medical Device Nomenclature

JPY Japanese Yen

k thousand

Healthcare & Medical Technologies – Japan Market Study - Page 10 of 121

LDP Liberal Democratic Party

LTCI Long-term Care Insurance

m million

METI Ministry of Economy, Trade and Industry

MEXT Ministry of Education, Culture, Sports, Science and Technology

MHLW Ministry of Health Labour and Welfare

MIC Ministry of Internal Affairs and Communications

MRI Magnetic Resonance Imaging

NHI National Health Insurance

NRDPMWA National Research and Development Program for the Medical and Welfare Apparatus

OECD Organisation for Economic Co-operation and Development

PAL Pharmaceutical Affairs Law

PHR Personal Health Record

PMD Act Pharmaceutical and Medical Device Act

PMDA Pharmaceuticals and Medical Devices Agency

QMS Quality Management Systems

R&D Research and Development

RHS Remote Healthcare Systems

RIBA Robot for Interactive Body Assistance

t trillion

US United States of America

USB Universal Serial Bus

WHO World Health Organisation

Healthcare & Medical Technologies – Japan Market Study - Page 11 of 121

1. Executive Summary Healthcare & Medical Technologies

1.1. Japanese Market and the EU

Japan remains the third largest global economic powerhouse, following the US and China. It aims

to achieve a Gross Domestic Product (GDP) of JPY 600 trillion (EUR 5 trillion) by FY2020, when

the Olympics will be hosted in Tokyo. Prime Minister Shinzo ABE and his cabinet hope to reach

this milestone goal based on his Abenomics strategy containing 3 main “arrows” of boosting the

economy, energising corporate activities and driving innovation and trade.

One of the main steps to reaching this GDP goal is the principal platform for the Economic

Partnership Agreement (EPA) between the EU and Japan. This EPA was signed in Brussels on

6 July 2017 during the 24th EU-Japan Summit in the presence of Prime Minister Abe, European

Commission President Juncker and European Council President Tusk, after nearly five years of

negotiations. The final approval is expected by mid-2018.

The EU currently exports on an annual basis goods worth EUR 58 billion and services valued at

EUR 28 billion to Japan. The EPA predicts an average 20% growth of EU exports, pushing up the

nominal GDP by 1% and possible creation of 420,000 new jobs.1

In 2015, 8.1% of total EU healthcare and medical device exports were to Japan. For European

companies, the EPA will further reduce costs for export certifications of medical devices, following

Japan’s joining International Standards on Quality Management Systems (QMS) in 2014.

1 Eurostat, European Commission, Directorate-General for Trade, May 2017

Healthcare & Medical Technologies – Japan Market Study - Page 12 of 121

1.2. Healthcare Market in Japan

In 1922, Japan launched its Health Insurance (HI) for industrial workers, followed in 1938 with the

voluntary National Health Insurance (NHI), to additionally include farmers and self-employed

people. From 1961, Japan had implemented a universal health insurance system that covered

nearly all citizens. The last major addition to the system was the Long-Term Care Insurance for

the Elderly, implemented from 2000.2

The public healthcare system is supported by working contributors via a 30% co-payment, but for

older patients this co-payment can vary from 10 to 20% depending upon their income.

Currently and following the 15 September 2017 announcements by the Ministry of Internal Affairs

and Communications (MIC), the Japanese population aged over 65 represents 27.7% of the total

population, equal to 35.14 million inhabitants. Additionally, for the first time, more that 2 million

people are over 90 years old. The average male life expectancy is almost 80 years, while women

average around 86 years. By FY2050, it is estimated that almost 40% of the population will be

over 65, ranking Japan as the highest in the world.

In FY2015, Japan ranked third on the Health Spending Index of the Organisation for Economic

Co-operation and Development (OECD) with 11.2% of its GDP, just behind the US and

Switzerland. Total social security costs, including pensions, healthcare and welfare, stands at

around 23% of the GDP.

This demographic situation creates interesting business opportunities for EU companies in the

Healthcare & Medical Technologies market that wish to increase or begin exports to Japan.

The FY2014 revision of the former Pharmaceuticals Affairs Law (PAL) into the Pharmaceutical

and Medical Device Act (PMD Act) will support future HMT sector growth at an annual rate of 3%.

Japan holds about 10% of the global HMT market share for both drugs and medical devices.

2 Five Decades of Universal Health Insurance Coverage in Japan: Lessons and future challenges, Japanese Society of Medical Sciences,

Yasuki KOBAYASHI

Healthcare & Medical Technologies – Japan Market Study - Page 13 of 121

Market Share Healthcare & Medical Technologies Sub-Sectors in Japan

Figure 1: Various sources, total market value approx. 6.76 trillion JPY in FY2014, Telemedicine is below 1% market share

1.3. Market Trends Healthcare & Medical Technologies

In addition to changing demographic trends in Japan, drastic reformation of the healthcare market

in general is among the key policies of the Abe cabinet. It aims to achieve this through high quality

Research and Development (R&D) and manufacturing of medical devices, together with innovative

healthcare services supported by strong ICT infrastructure. Customised medical care, based upon

Personal Health Records and anonymous cloud-based big data are another key priority. Approval

processes for both new drugs and medical devices will also be shortened substantially.

The total market value for medical devices was JPY 2.68 trillion (EUR 22.3 billion) in FY2013.

This was JPY 1.375 trillion (EUR 11.458 billion) of domestically manufactured medical devices

and JPY 1.30 trillion (EUR 10.84 billion) of imported medical devices, commanding 49% market

Assistive Technologies

21%

Medical Equipment 40%

ICT Healthcare5%

Nanotechnology4%

Biotechnology26%

Dental Equipment4%

Healthcare & Medical Technologies – Japan Market Study - Page 14 of 121

share.3 The revised PMD Act should be a big push due to eased import regulations, which will

drive continued growth of imported medical devices.

Concrete export business opportunities for European companies to Japan, can be found in the

following summary.

Healthcare & Medical Technology Sector Business Opportunities

Assistive Technologies ▪ Continued strong demand for railings, silver cars, walking devices,

walkers and walking assistants following enclosing into long-term rental systems by local governments

▪ Nursing Robot Market to increase to JPY 1.5 trillion (EUR 12.45 billion) by FY2020 (15-fold from FY2015)

▪ Orthopaedic Devices and Surgical Implants demand as Japan’s demand alone is +50% of all Asian-Pacific market

Medical Equipment ▪ Almost 50% of all medical equipment is imported

▪ Future growth potential for endoscopic surgery equipment

▪ Replacement demand of existing MRI equipment

ICT for Healthcare & Medical Technologies

▪ Electronic Medical Record Systems: +23% by FY2020

▪ Community Healthcare Coordination Systems: +66% by FY2020

▪ IoT Technologies: +20% annually between FY2015-2020

Telemedicine and Remote Health Monitoring

▪ Remote monitoring service market to grow to JPY 13.9 billion (EUR 115.83 million) by FY 2025 (almost 50% increase versus FY2016)

▪ Following FY2015 deregulations, telemedicine demand will be brisk for Remote Nursing Care and Remote Healthcare Systems (RHS)

Nanotechnology ▪ Market to triple in value by FY2020 to EUR 94.4 billion

▪ Nanotech applications in Dentistry and Sanitary sectors

▪ Medical equipment with nanotechnology for less invasive surgeries

Life Science / Biotechnology ▪ Market to 10-fold in value by FY2030 to EUR 166 billion

▪ Business potential in participation and collaboration with biotechnology clusters nationwide

Dental Products and Technologies ▪ Dental examination equipment and dental laboratory equipment

(high import ratio)

3 JETRO, Attractive Sectors: Life Science, 2016

Healthcare & Medical Technologies – Japan Market Study - Page 15 of 121

Healthcare & Medical Technology Sector Business Opportunities

▪ CAD/CAM devices for dentistry, dental implant materials, dental impression and reproduction materials, total and partial floor denture materials (+80% import ratio)

Figure 2: various sources

1.4. Assistive Technologies

In Japan, assistive devices and technologies are part of the welfare segment that includes nursing

care, rehabilitation and the home care sector. In FY2014, the Japanese market for the welfare

equipment industry was JPY 1.4 trillion 4 (EUR 11.65 billion) and it is forecasted to reach

JPY 4,5 trillion (EUR 37.5 billion) by FY2025.5

Responding to this trend and driven by the scheduled revision of the Long-Term Nursing Care

Insurance system in FY2018, new business opportunities for European manufacturers in this sub-

sector are emerging.

The market will show especially strong demand for advanced and innovative assistive devices

that meet the needs of Japan’s rapidly ageing population particularly in areas such as mobility

impairment equipment, home care devices and nursing homes, remote monitoring services,

orthopaedic devices and surgical implants.

Further, nursing care robots will play a very significant role, not only in the nursing care sector but

also in the medical sector from general to rehabilitation uses.

1.5. Medical Equipment

The Japanese medical equipment and materials market is the third largest in the world, and it is

expected to grow further as Japan’s ageing population rapidly increases. By FY2050, Japan is

expected to be a “super-aged” society with 40% of its population over 65 years.

4 Japan’s Welfare Equipment and Daily Life Support Equipment, Japanese, July 2016 5 Current Situation and Outlook of the Welfare Market in 2017, Fuji Keizai Group, Japanese, 2017

Healthcare & Medical Technologies – Japan Market Study - Page 16 of 121

Almost 50% or JPY 1.37 trillion (EUR 11.37 billion) of Japan’s medical device and materials

market consists of imported products, particularly sophisticated medical technologies.6

European companies might find it difficult to compete with domestic manufacturers in

e.g. diagnostic imaging, therapeutic and surgical equipment, and biophenomena measuring and

monitoring systems. However, thanks to the amended Pharmaceutical and Medical Device (PMD)

Act, the import market is expected to continue expanding. Business opportunities for European

healthcare manufacturers lie in innovative technologies like cardiology equipment, pacemakers,

orthopaedic implants and medical devices that alleviate pain in general and improve the quality

of life for patients. Furthermore, given Japan's ageing population and the increasing number of

patients with chronic and life-style diseases, the markets for in-home care devices, technologies,

and health ICT related products is expected to grow accordingly.

1.6. ICT for Healthcare & Medical Technologies

At the end of FY2013, the ICT healthcare market was an estimated JPY 374.3 billion

(EUR 3.11 billion), but is predicted to grow to JPY 420.4 billion (EUR 3.5 billion) by FY2020.7

Areas like Electronical Medical Records like Electronic Health Records (EHR) and Personal

Health Records (PHR), Supplier Information Sharing and Remote Safety Check and Confirmation

Systems, Remote Diagnostic Imaging Systems and Internet of Things (IoT) devices are expected

to show double-digit growth on an annual basis8 through FY2020.

Also, wearable devices with healthcare applications, including Smart Watches and Smart Bands,

are estimated to exceed 11 million devices by FY2020 from 3.5 million devices in FY2016.9

Currently, nearly 30% of the Japanese population is aged over 65 years, there will be stronger

demand to alleviate the burden on nursing care workers. This is the opportunity for Robotic

6 Annual Report on Statistics of Production by Pharmaceutical Industry in 2013, Ministry of Health, Labour and Welfare (MHLW) 7 Invest in Tokyo website, 2016 8 ICT in Healthcare Questionnaire, MIC, 2016 9 Global Wearable Device Market: Key Research Findings 2016, Yano Research Institute, 2016

Healthcare & Medical Technologies – Japan Market Study - Page 17 of 121

Devices to emerge. This specific market segment is predicted to grow from JPY 16.7 billion

(EUR 139.15 million) in FY2015 to JPY 404.3 billion (EUR 3.36 billion) by FY2035.10

1.7. Telemedicine and Remote Health Monitoring

Closely linked to the ICT Healthcare market segment, this niche market is still small but is expected

to grow by 30% to JPY 13.2 billion (EUR 110 million) by FY2020. Further growth aims to enhance

nationwide coverage of rural and remote areas mainly occupied by the elderly at present. Sub-

sectors like remote medical/nursing care and remote healthcare systems (RHS) look promising but

attention is currently focused on the telemedicine subsector, given the deregulatory measurements

taken by the Abe government in 2017. New inroads into telemedicine is not limited to customised

telemedicine software as some hospitals and doctors already provide similar services with existing

platforms like Skype, Facebook Messenger and iPhone FaceTime video.

1.8. Nanotechnology for Healthcare & Medical Technologies

Within the nanotechnology field in Japan, healthcare is taking the biggest share at nearly 50%.

The market is predicted to grow to EUR 95 billion by FY2020 and up to EUR 189 billion by

FY2030.11

Currently, R&D and manufacturing is done mainly between universities, research centres and

private companies, with applications focusing on nanomedicines, dentistry, tissue engineering

and medical supplies. Like global trends, Japan is also working rapidly on creating a pinpoint

Nano-Drug Delivery System (DDS) for cancer imaging and target therapy.12

In this phase, cooperation among private Japanese companies like Unicharm and Tokuyama

Dental, or leading academic and research institutes like Kyoto University, Tokyo Institute of

Technology or National Institute for Materials Science, seem to be the most efficient market

10 5-year Plan for Development of Robotic Devices for Nursing Care, METI, 2014 11 Nanotech Cluster and Industry Landscape in Japan, Andrej Zagar, EU-Japan Centre for Industrial Cooperation, 2014 12 Nano Bio First, Kazunori KATAOKA, Funding Program for World-Leading Innovative R&D on Science and Technology (FIRST), 2012

Healthcare & Medical Technologies – Japan Market Study - Page 18 of 121

entrance strategies for EU companies specialising in nanotechnology applications for healthcare

and medical equipment.

1.9. Biotechnology for Healthcare & Medical Technologies

Very closely related to the nanotechnology sector, defined broadly in Japan as life science, this

is one of the Abe cabinet priorities given Japan’s rapidly ageing society and resulting medical

healthcare expenditures.

In FY2015, the Japanese biotech market was JPY 3.11 trillion (EUR 25.91 billion)13 of which 55%

was directly linked to the healthcare and medical industry and valued at JPY 1.74 trillion

(EUR 14.5 billion). The Ministry of Economy, Industry and Trade (METI) also announced its

intention to grow the Japanese biotech market to JPY 20 trillion (EUR 166 billion) by FY2030.14

The Government of Japan also established the Agency for Medical Research and Development

(ADEM) with JPY 126.5 billion (EUR 1.05 billion) budgeted for FY2016 to focus on stem cells,

pharma and medical device cooperation among all market players.

Participation and collaboration in clusters focusing on biotechnology as well as collaboration

projects between private companies and research institutes (eg. NIPRO and Kyoto University on

iCeMS) are likely the best ways to enter the Japanese market for European companies.

1.10. Dental Products and Technologies

Japan’s ageing population has dramatic impact on the nation’s healthcare system in general, and

oral healthcare and dentistry specifically. It has been widely recognised that oral health is

fundamental to general health and the relationship between the medical and dental fields is

starting to further mature and expand.

13 Nikkei Biotechnology and Business, 2015 14 METI Policy announcement to 6-fold bio market to JPY 20 trillion by FY2030, Nikkei, 2015

Healthcare & Medical Technologies – Japan Market Study - Page 19 of 121

Globally, Japan is the second largest dental market with dental examination medical expenditures

of JPY 380 billion (EUR 3.16 billion) in FY2014. Japan imported dental x-ray equipment, dental

equipment and dental materials valued at JPY 60.1 billion (EUR 500 million) in FY2015.15

Japan has a very low percentage of edentulousness because dental professionals practise under

a “treat the original teeth as much as possible” policy. Although often neglected in the past,

patients are now focusing more and more on oral health and aesthetic (cosmetic) dental services.

This has led to increased demand for dental services such as teeth straightening, overbite

correction and bad breath prevention.

Emerging opportunities exist for European manufacturers in advanced dental examination and

diagnostic technologies, preventive technologies, CAD/CAM devices, materials for dental implants,

dental reproduction materials about preventive dental care and modern dental treatment.

1.11. Healthcare & Medical Technologies Regulations

At the end of 2014, the Abe cabinet drastically revised the strict Pharmaceutical Affairs Law (PAL)

and renamed it the Pharmaceutical Medical Device Act (PMD Act) which created eased import

regulations, reduced costs for obtaining certifications and faster review approvals.

Medical devices are now separated from drugs with their own Marketing Authorisation and

Manufacturing License. Also, private third parties can now provide certification services for

Specially Controlled Medical Devices if the established standards and procedures are followed.

The permission system for Manufacturing Licenses of Medical Devices is now simplified to

registration. Lastly, the Standards Compliance Investigation for manufacturing and quality of

medical devices has been rationalised. With the implementation of these deregulations, Japan

aims to create a registration and approval process that is faster than that of the Food and Drug

Administration (FDA) in the US.

15 New Dental Medical Equipment and Dental Medical Technology Industry Vision, JDA, 2017

Healthcare & Medical Technologies – Japan Market Study - Page 20 of 121

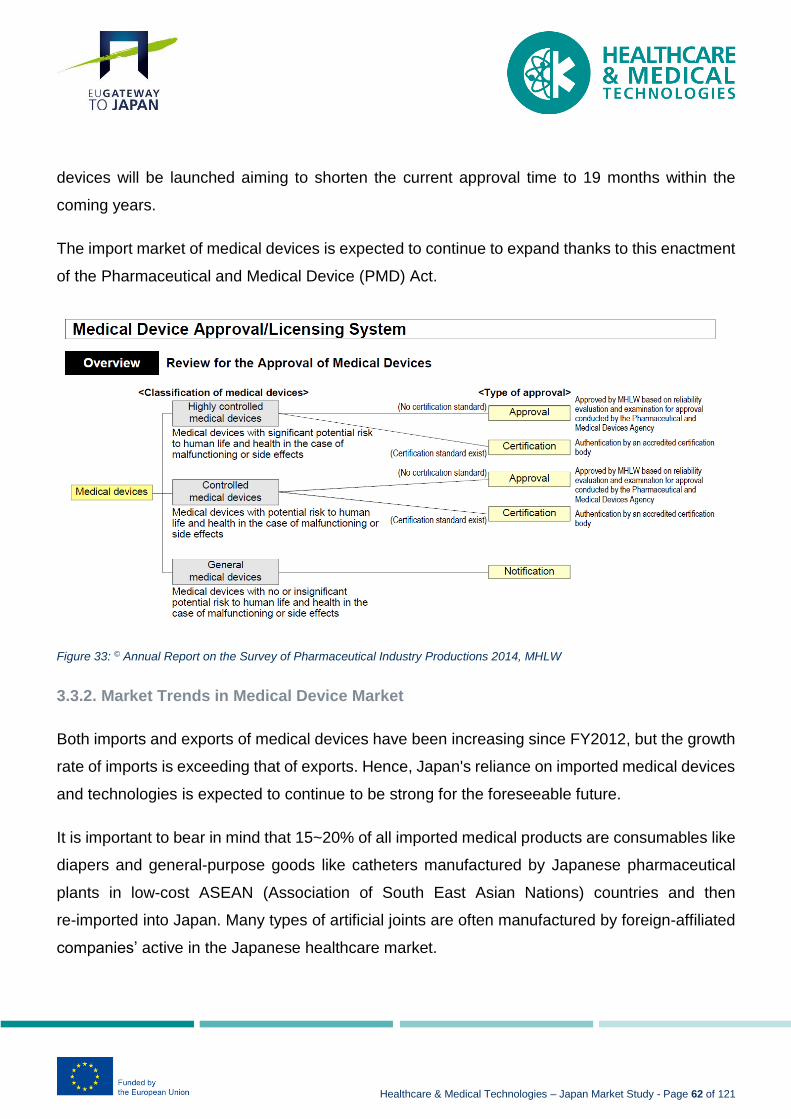

The Pharmaceuticals and Medical Devices Agency (PMDA), an independent entity under

jurisdiction of the Ministry of Health, Labour and Welfare (MHLW), is the responsible body for

evaluations and approvals of both domestic and imported medical devices. Japan does not levy

any custom duties on imported medical devices.

Japan’s medical device classification system is based on four risk level classes as defined by the

Japanese Medical Device Nomenclature (JMDN) codes, which are different from US and

European classifications.

Class I (lowest risk to the human body) is defined as general medical devices (e.g., scalpels,

x-ray film, items for dental techniques…)

Class II (relatively low risk) is defined as controlled medical devices (e.g., MRI equipment,

catheters, dental alloys…)

Class III (relatively high risk) is defined as having a relatively high risk to the human body in

case of failure (e.g., dialyzers, artificial bones, artificial respirators…)

Class IV (highest risk) is defined as specifically controlled devices (e.g., pace makers,

artificial heart valves, stent grafts…)

Healthcare & Medical Technologies – Japan Market Study - Page 21 of 121

Regulatory Review Process Medical Equipment

Figure 3: Pharmaceuticals and Medical Devices Agency, https://www.pmda.go.jp/english/review-services/outline/0001.html

Notably, Japan does not currently accept the CE mark or an FDA certificate, but the principal

agreement on the EPA in 2017 should eliminate this hurdle in the future.

For European companies, to fully understand future business potential of the healthcare and

medical device market in Japan, an important law is the Long-Term Care Insurance (LCTI) for the

Healthcare & Medical Technologies – Japan Market Study - Page 22 of 121

elderly, originally issued in April 2000. This law aims to resolve issues facing its rapidly ageing

society, namely, support in the best way possible independent living and a customer-oriented,

user chosen approach to medical and welfare services, all backed by a robust social insurance

system with clear benefits and burdens. The next major revision of the LCTI is planned for FY2018

will further address these issues and opportunities.

Healthcare & Medical Technologies – Japan Market Study - Page 23 of 121

2. What are the Characteristics of Japan?

Japan Factsheet

Population (last census FY2014) 127,220,000 inhabitants

Land Area 377,962 km2

Capital Tokyo

Currency Japanese Yen (JPY)

Gross Domestic Product (GDP) FY2017 (est.) JPY 554 trillion16 (EUR 4.616 trillion)

Sovereign Debt FY2016 (247% of GDP) JPY 1,371 trillion17 (EUR 11.43 trillion)

Foreign Direct Investment (FDI) FY2016 JPY 27.8 trillion18 (EUR 231 billion)

Country Competitiveness Index FY2016 Global Rank19: 8th

Tax Revenues FY2016 JPY 57.6 trillion20 (EUR 480 billion)

Consumption Tax (Value Added Tax) 8%

Unemployment Rate 2017 2.8%21

Life Expectancy (Men) 80 years

Life Expectancy (Women) 87 years

Figure 4: Japan Factsheet, several sources

It is well known that Japan rapidly strengthened its position in the global economy during the post-

war period. Historically, the primary drivers of Japan’s strong economic growth have been high

rates of investment in production plants and equipment, applications of industrial efficiency, high

education standards, good relations between labour and management, ready access to leading

technologies with significant investments in research and development, increasingly open world

16 www.japan.go.jp/abenomics/index.html 17 www.reuters.com/article/markets-debt-global-idUSL8N1G95BD 18 www.japan.go.jp/abenomics/index.html 19 Top 10 Most Competitive Global Economies, The Global Competitiveness Report 2016-2017 20 www.japan.go.jp/abenomics/index.html 21 www.japan.go.jp/abenomics/index.html

Healthcare & Medical Technologies – Japan Market Study - Page 24 of 121

trade framework and a large domestic market of discerning consumers – all of which have given

Japanese businesses an advantage in scale and operations effectiveness.

At the same time, the rapid ageing of the population has created tremendous structural

implications on the future workforce, the savings rate of the working population, and hence, the

government tax revenue budget.

From a global point of view, in FY2014, Japan was the 2nd biggest Medical Device Market with a

market share of 9.1%, behind the US with 39.3% but ahead of Germany with a share of 7.9%.22

The market share of imported medical devices has historically been hovering just below the 50%

line, but following the enactment of the revised and liberalised PMD Act in FY2014, it is expected

that the import share from overseas medical devices will exceed the 50% threshold from now on.

On average, the device market itself grows at a CAGR of 3% per annum.23

The medical device market is divided between generic domestic manufacturers like Olympus

Medical Systems, Hitachi Medical, Toshiba Medical Systems and foreign capital players like

GE Healthcare Japan, Philips Medical Japan, Siemens Japan and Stryker Japan. Promising

business areas for overseas manufacturers are related to endoscopic surgery, surgical support

robots and image diagnosis equipment like MRI and CT scanners.

In the healthcare service market, Japan expects this segment to grow from JPY 4 trillion

(EUR 33 billion) in FY2013 to JPY 10 trillion (EUR 83 billion) by FY2020. Specifically, promising

sub-segments include nursing care ICT, self-care health equipment and community care systems.

Domestic players include Cyberdyne, Fuji Machine Manufacturing, Panasonic, Omron

Healthcare, Terumo, Fujitsu, NEC and Konica Minolta but showing growth potential for

EU companies that can provide localised Japanese language ICT solutions with maintenance

services after delivery and installation.24

22 Worldwide Medical Market Forecasts to 2019, Espicom, 2014 23 Annual Report on Statistics of Production by the Pharmaceutical Industry, Yano Research Institute, 2014 24 Attractive Sectors: Life Science, JETRO-Invest in Japan, July 2016

Healthcare & Medical Technologies – Japan Market Study - Page 25 of 121

2.1. Political Overview

Japan is a constitutional monarchy, with the Emperor as the symbolic head of state. The system

is a parliamentary democracy with the National Diet as the sole legislative body. The Diet is

composed of an Upper House (House of Councillors) and a Lower House (House of

Representatives), and a Prime Minister, chosen by a Diet ballot, who appoints a cabinet, with a

majority required to be Diet members.

Japan’s voting system is non-obligatory, and the voting age was lowered from 20 to 18 years in

2015, resulting in 104 million eligible voters.

The Liberal Democratic Party (LDP) has governed Japan for most of the last 70 years, and was

only out of power briefly in 1993-1994 and in 2009 when the Democratic Party of Japan (DPJ),

led by Yukio Hatoyama, secured a historical victory that put the DPJ into governing powers.

Since then, following a landslide election victory by the Liberal Democratic Party (LDP), Prime

Minister Shinzo Abe took office as Japan’s 97th re-elected Prime Minister in 2014. Since

August 2016, Abe’s Cabinet has 20 ministers, including the Prime Minister himself. As a result,

Japan’s economic and financial situations have undergone noticeable changes.

2.2. Economic Overview

Today, aiming for a future GDP of JPY 600 trillion (EUR 5 trillion), Japan is still the 3rd largest

global economy, after the US and China. Japan’s main industries are automotive, consumer

electronics, computers, other electronics and pharmaceuticals. Services represent 75% of the

GDP, industrial activities 23.5% and agriculture 1.5%.

Following the financial and real estate bubble bursting in the early 1990’s, and after more than

two decades of economic stagnation, Prime Minister Shinzo Abe and his Cabinet unveiled a

comprehensive economic policy package to revive and sustain the Japanese economy while

maintaining fiscal discipline. This programme became known as Abenomics.

Healthcare & Medical Technologies – Japan Market Study - Page 26 of 121

The centrepiece of Abenomics is the “Three Arrow Policy” targeted at an active monetary policy,

a flexible and stimulant fiscal policy and a sustainable long-term growth strategy - all carried out

through structural reforms to encourage private investments. The economic parameters focus

mainly on boosting productivity, driving innovation and trade, and stimulating corporate activity.

Figure 5: © Abenomics, Cabinet of the Prime Minister website

Internationally, the Brexit (UK) in July 201625 and the inauguration of US President Donald Trump

in early 2017 had strong but temporary impact on the exchange rates between the JPY and the

Euro. Since the middle of 2017, the rate is back to usual trade levels and has been hovering

around JPY 130 for EUR 1.

Given the long-term low and negative interest rates by the Central Bank of Japan, it is believed

that the Japanese Yen will remain relatively strong for the near future against other global

currencies, including the Euro, thus creating export business opportunities for overseas

manufacturers and suppliers.

25 http://www.reuters.com/article/us-global-forex/yen-advances-on-brexit-impact-fears-pound-plunges-to-31-year-low-idUSKCN0ZM00T

Healthcare & Medical Technologies – Japan Market Study - Page 27 of 121

In recent years, multinationals like Apple (US), Nokia (Finland), Continental (Germany) and BASF

(Germany), have created major Research and Development (R&D) centres in Japan. Internet

companies like Facebook, Google and Amazon (all US) have also had presence in the country

for some time now. Recently, however, newer internet companies like TripAdvisor, Airbnb, Uber,

Netflix, Hulu and Spotify also have established representative offices in Japan. For FY2020,

Japan is targeting JPY 35 trillion (EUR 291 billion) of inbound Foreign Direct Investment (FDI).

Tokyo is and continues to be the favourite city to establish a presence (35%) in Japan, while Osaka

represents 16% of total FDI value. Nagoya remains a popular destination for automotive

manufacturing and related businesses, given Toyota Motors has its global headquarters there.

Yokohama is especially popular for larger scaled R&D centres. Both cities have an FDI share of 11%

each. These four major cities combined represent almost 75% of total FDI value in Japan. Across all

foreign direct investments in Japan, Asia represents 40%, Europe 31% and the USA 29%.26

Since Prime Minister Abe took office in 2012, annual corporate profits have increased to

JPY 68.2 trillion (EUR 568 billion) in May 2017. As an indicator, the Nikkei Index has remained in

the JPY 19,000 range since the beginning of 2017. These results were mainly obtained through

large-scale monetary easing policies, consecutive tax reforms (corporate tax ratio was 37% in

2013 and Abe’s cabinet is aiming for 29.74% by 2018).

26 JETRO, Invest Japan Report 2016

Healthcare & Medical Technologies – Japan Market Study - Page 28 of 121

2.3. Trade Overview between EU and Japan

2.3.1 Japan and EU business in Figures

EPA Facts and Figures Infographic

Figure 6: EU-Japan Trade Relationship-Facts and Figures, European Commission, 2017

Healthcare & Medical Technologies – Japan Market Study - Page 29 of 121

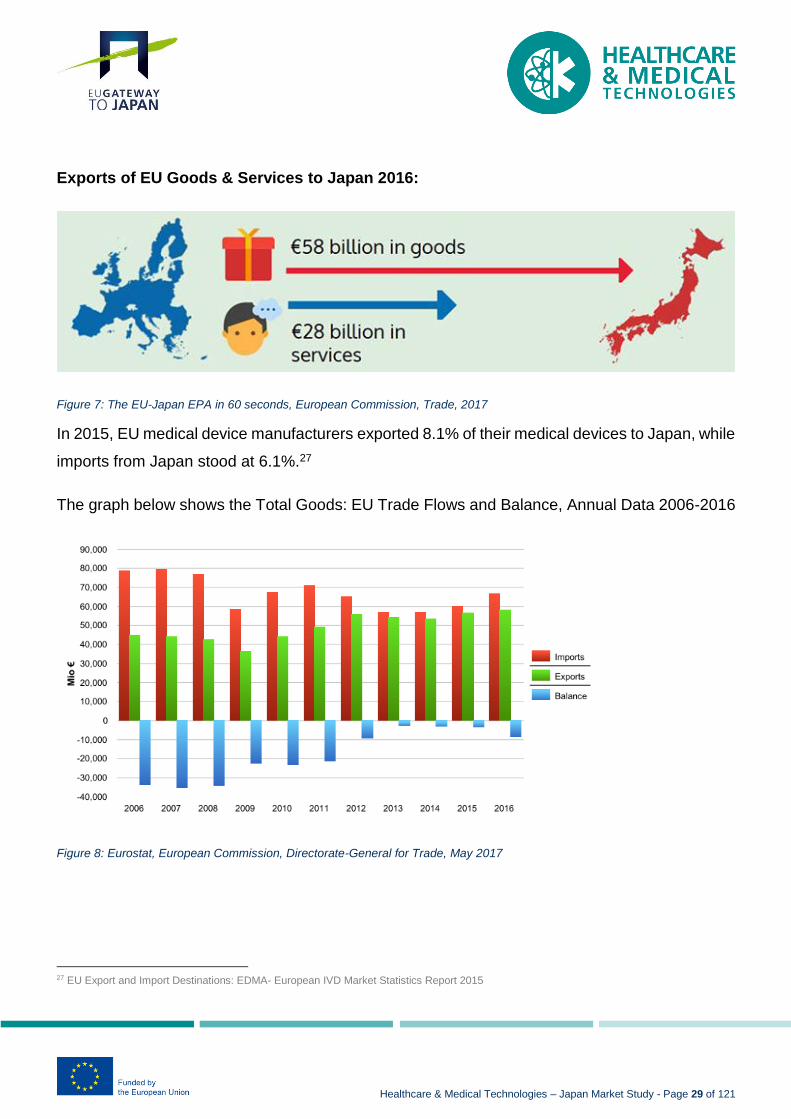

Exports of EU Goods & Services to Japan 2016:

Figure 7: The EU-Japan EPA in 60 seconds, European Commission, Trade, 2017

In 2015, EU medical device manufacturers exported 8.1% of their medical devices to Japan, while

imports from Japan stood at 6.1%.27

The graph below shows the Total Goods: EU Trade Flows and Balance, Annual Data 2006-2016

Figure 8: Eurostat, European Commission, Directorate-General for Trade, May 2017

27 EU Export and Import Destinations: EDMA- European IVD Market Statistics Report 2015

Healthcare & Medical Technologies – Japan Market Study - Page 30 of 121

2.3.2 EU-Japan Economic Partnership Agreement (EPA)

The EU and Japan together account for 33% of the world’s GDP and have a combined population

of 632 million people. On 6 July 2017, during the 24th EU-Japan Summit held in Brussels, the

President of the European Commission Jean-Claude Juncker, the President of the European

Council Donald Tusk and the Prime Minister of Japan Shinzo Abe announced the principle

agreement of the Economic Partnership Agreement between the EU and Japan.

Figure 9: © Cabinet Public Relations Office, July 2017

Negotiations between both parties started back in 2013 and took in total 18 rounds on technical

and political levels to conclude the most important bilateral trade deal ever. Upon ratification of

the agreement, predictions are that EU exports to Japan could increase by 33% while Japan’s

exports to the EU are expected to grow 24%. The EPA is said to boost trade in goods and

services, with an estimated GDP growth up to 0.8% for the EU and up to 1% for Japan, while

creating investment opportunities for both economic blocks that might result in 420,000 new jobs.

It also includes the protection of EU standards and will further eliminate trade barriers and ease

regulatory standards over the next decade. In addition, the EU will gain improved access to

Japan’s public procurement systems at both government and private enterprise levels. In return,

Japan will gain eased market entrance for automotive, pharmaceutical and home electronics

industries.

Healthcare & Medical Technologies – Japan Market Study - Page 31 of 121

Final agreement and approval of the EPA is expected by mid-2018 with full implementation

targeted for early 2019.

Concretely, for European Healthcare & Medical Technologies companies, this EPA will mean

profoundly reduced costs for certifications of exported medical devices following the adaptation

of the International Standards on Quality Management Systems (QMS) by Japan in 2014.

Healthcare & Medical Technologies – Japan Market Study - Page 32 of 121

3. Healthcare & Medical Technologies Market Overview and EU Entry Opportunities

3.1. Japanese Healthcare & Medical Technologies Market

3.1.1. Short Historic Healthcare & Medical Technologies Market Overview

As early as 1922, the Japanese government launched the Health Insurance (HI) (Kenko Hoken

in Japanese) covering industrial workers in its first phase. Just before World War II in 1938,

the government added the voluntary National Health Insurance (NHI) (Kokumin Kenko Hoken in

Japanese) to the health insurance system, aiming to also cover farmers and self-employed people

with this new nationwide system.

From 1958 on, following a major revision of the National Health Insurance Law, the NHI became

mandatory. Three years later, in 1961, Japan established a universal health insurance system

covering all Japanese citizens.

Brief history of Japan’s Health Insurance System

1922 Introduction of Health Insurance (HI)

1927 Nationwide Enforcement of HI

1938 Introduction of National Health Insurance (NHI)

1950s Encouragement of the Merger of Towns and Villages

1958 Revision of NHI

1961 Establishment of Universal Coverage

1983 Introduction of Health Services Law for the Aged

2000 Introduction of Long-term Care Insurance for the Elderly

2008 Introduction of Health Care Program for the Elderly aged 75 and over

Figure 10: ©Five Decades of Universal Health Insurance Coverage in Japan: Lessons and future challenges, Japanese Society of Medical Sciences, Yasuki KOBAYASHI

Healthcare & Medical Technologies – Japan Market Study - Page 33 of 121

In 1961, the timing for the introduction of a universal health insurance system was perfect given

the costs of health care at that moment were low, Japan’s economy was growing quickly and

there was a strong feeling of solidarity amongst its people.

At the end of FY2014, Japan had a total of almost 177,500 medical care institutions of which

roughly 8,500 are hospitals, 100,500 are medical clinics and 68,500 are dental clinics, which are

operated by 104,000 dentists. About 2,150 hospitals have 50 to 99 beds, giving them the biggest

share at 25%. The specialty of Internal Medicine practice is offered by 6,838 hospitals and almost

64,000 medical clinics. Other specialties include cardiovascular, gastroenterological and

respiratory medicine.28

In the same period, the total number of beds was 1,681,000, while general beds have been

decreasing over the past 2 decades, the beds for long-term care have been increasing, keeping

the total number almost stable.

At present, Japan has 13.4 hospital beds per 1,000 people, making it rank 1st among OECD

countries and its ratio of nurse to physicians is ranked 2nd.29

3.1.2. Market Overview Healthcare & Medical Technologies

Key Market Indicators for the Healthcare & Medical Technology Sector

Average Life Expectancy Male: 79.55 years

Female: 86.30 years

+65 years old 27.7% (35.14 million persons) of total population; 49% of medical costs

+90 years old 2.06 million persons

+65 years old by 2050 38.8%, highest in the world

Causes of Death for +65 years 1. Osteo Arthritis & Rheumatoid Arthritis: 24% 2. Dementia: 24%

3. Cancer: 23%

Low Birth rate Low birth rate of 1.37 births/couple for FY2009

28 Survey of Medical Institutions, MHLW, 2015 29 OECD Factbook, OECD, 2016

Healthcare & Medical Technologies – Japan Market Study - Page 34 of 121

Key Market Indicators for the Healthcare & Medical Technology Sector

Infant Mortality 1/1,000 new born

Market Growth 2.2% annual growth expected till at least FY2018

Public Healthcare System Privately supported via co-payment by patient at 30%

Co-payments by elder patients vary from 10-20%

Healthcare Costs 11.2% of Japan’s GDP in FY2015

Total Social Security Costs (Pensions, Healthcare, Welfare ...)

Approximately 23% of GDP

Figure 11: various online resources

According to the Organisation for Economic Co-operation and Development (OECD) Health

Statistics released in June 2016, Japan’s total health spending accounted for 11.2% of its Gross

Domestic Product (GDP) in FY2015. Japan is ranked third out of 35 OECD member states, trailing

only the US (16.9%) and Switzerland (11.5%).

Figure 12: Overview of National Medical Expenditures for 2013, Ministry of Health Labour and Welfare (MLHW)

Healthcare & Medical Technologies – Japan Market Study - Page 35 of 121

Percentage of Population over Age 65 by 2050

Figure 13: United Nations, World Population Prospects, the 2015 Revision

As for the domestic market size of medical devices, it was JPY 2.675 trillion (EUR 22.2 billion) for

FY2013, representing a growth rate of +3% in FY2012. The market is expected to continue

expanding at a similar rate for the immediate future, following the enactment of the

Pharmaceutical and Medical Device (PMD) Act in FY2014 and the continuous, rapidly ageing

population. At present, Japan is and remains the second-largest global market after the US and

it holds an approximate 10% global market share.

Healthcare & Medical Technologies – Japan Market Study - Page 36 of 121

Global Medical Device Market: Share by Country 2014

Figure 14: The World Pharmaceutical Markets Fact Book 2014, Espicom

Contrary to most business segments in Japan, the medical devices and technologies sector is one

of the few market segments where Japan imports more than it exports – this clearly shows both the

present market size and the future growth potential for European companies in this segment.

Presently, the Pharmaceuticals and Medical Devices Agency (PMDA) is in charge of reviewing

applications for domestically manufactured and imported medical devices, through using

transparent methods bearing in mind quality, safety and efficacy through experts, while promoting

international harmonisation between existing quality and approval standards.

USA39%

Japan9%

Germany8%

China6%

France4%

UK3%

Italy3%

Canada2%

Russia2%

Others24%

Global Medical Device Market

USA Japan Germany China France UK Italy Canada Russia Others

Healthcare & Medical Technologies – Japan Market Study - Page 37 of 121

Basic Review Process of Medical Device Application in Japan30

Figure 15: © Basic Review Process for Drug of Medical Device Application, Pharmaceutical and Medical Devices Agency (PMDA)

Standard Supply Chain Flow of Medical Devices in Japan31

Figure 16: © Supply Chain of Medical Devices in Japan, Pharmaceutical and Medical Devices Agency (PMDA)

30 http://www.pmda.go.jp/english/review-services/reviews/0001.html 31 QMS for Medical Device in Japan, PMDA, 2016

Healthcare & Medical Technologies – Japan Market Study - Page 38 of 121

Marketing approval in Japan is required for any new medical devices, prior to domestic distribution

and sales, and can be obtained by the following bodies:

Marketing Authorisation Holder (MAH): Japanese organisation who obtains the marketing

approval. MAH needs to comply with Japanese Quality Manufacturing Standards (QMS) and

released medical devices need to meet Japan’s approved specifications

Foreign Restrictive Authorisation Holder (FRAH): Foreign organisation who obtains the

marketing approval but will need to designate a MAH in Japan

Designated MAH: Japanese organisation designated by FRAH to conduct manufacturing

and quality control duties in Japan. Needs to take necessary measures to prevent public

health hazards

The basic document flow for marketing approval of medical devices is straightforward, especially

since the PMD Act revision in FY2014, but specific device and equipment related questions and

extra document requests can be expected.

Pre-Market Submission (Todokede in Japanese): This is a pre-market notification request for

General Medical Devices (Class I) to the PDMA but no actual reviews or assessments will

be conducted by the PMDA for Class I devices

Pre-Market Certification (Ninsho in Japanese): Class II (and a limited number of Class III)

medical devices, with an associated certification standard like Japan Industrial Standards

(JIS), often based upon existing ISO/IEC standards, are subject to pre-market certification.

MAH will file the application with a Registered Certification Body (RCB), comparable with

European CE Marking process where reviews are also handled by external third parties

Pre-Market Approval (Shonin in Japanese): Class II and III devices without a specific

certification standard are subject to the pre-market approval process, and it is the same for

Healthcare & Medical Technologies – Japan Market Study - Page 39 of 121

all Class IV medical devices. MAH needs to file a pre-market approval application with the

PMDA and ultimately obtain approval from the MHLW.32

Reimbursement Categories of Medical Devices in Japan

Figure 17: © Demystifying Device Reimbursement in Japan-Device Talk, EMERGO, 2017

For pricing of medical devices, usually Japanese companies have their standard price list but the

actual sales prices are not really known, as this depends on typical commercial talks between

manufacturer and final customer. The final sales price varies in relation to ordered quantities,

required delivery terms, agreed payment terms, past business volume and price quotes of

competitors, too name only a few.

The market shows a trend of more direct business transactions between manufacturer and

customer, especially in the segment of large and expensive medical devices. For consumables

32 PMDA Medical Device Registration Approval Process, Emergo, 2017

Healthcare & Medical Technologies – Japan Market Study - Page 40 of 121

and high-volume equipment, the final customer tends to procure through major wholesalers

specialised in medical equipment and devices.

3.1.3. Market Trends Healthcare & Medical Technologies

Continuous improvements and adaptations to the national healthcare system are an important

cornerstone within the Abenomics Revival Strategy. The focus is to create a flexible regulatory

framework with both a fast R&D process and license approval system for regenerative medicines.

This should allow Japan to become a central hub for regenerative medicines, with an estimated

market value of JPY 26 trillion (EUR 216 billion) by FY2020.

Seamless connection from R&D to commercialisation for the manufacturing of world's

top-class medical services

Promotion and development of innovative health care services for medical treatment,

nursing care, health promotion, disease prevention and daily life support

Realising efficient and high-quality medical services by ICT

Figure 18: Compiled by JETRO based on the “International Comparison of Regulations for Regenerative Medicine and Cell Therapy 2013” by the National Institute of Health Sciences

Healthcare & Medical Technologies – Japan Market Study - Page 41 of 121

Separate from the aforesaid main policies, Japan is also optimising and liberalising the following

healthcare regulations that will determine the future trends in the domestic market for healthcare

and medical devices:

Further amendments of the Pharmaceutical Affairs Law (PAL)

Enforcement of the New Act for Regenerative Medicines

Creation of a faster R&D process in regenerative medicine

Promotion of R&D of orphan drugs fulfilling unmet medical needs

Establishment of laws for medical treatment of patients with intractable diseases

Establishment of government policies for drug prices

Lower premium drug prices with generic drugs

Establishment of policies for promoting usage of generic drugs

Promotion of market entries from overseas healthcare and medical device companies

Enhancement of nursing care by optimal ICT implementation

Promotion of self-care health equipment and related service markets

Enhancement of remote and preventive medical care services and face-to-face medical

examinations (effects to be evaluated based on a FY2018 revision of medical service fees)

Integration and storage of personal medical information using big data to provide customised

medical care by FY2020

Analysis of aggregated anonymous medical records to advance medical research

Creation of National Strategic Special Zones as hubs for cardiac, neurologic and ophthalmic

treatment

Acceleration of development of Advanced Heart Failure treatment, such as myoblast

cell-sheet and cardiomyocyte sheet transplantation therapy

Healthcare & Medical Technologies – Japan Market Study - Page 42 of 121

Enhancement of world-class R&D on iPS like the world’s first successful iPS origin retinal

cell transplant operation for age-related macular degeneration

3.1.4. Import Market of Healthcare & Medical Technologies

The total market value for medical devices is JPY 2.676 trillion (EUR 22.3 billion), representing a

combined value of JPY 1.375 trillion (EUR 11.458 billion) of domestic production and

JPY1.301 trillion (EUR 10.84 billion), equal to almost 49% market share, of imported medical

devices and equipment in FY2013.33

Figure 19: JETRO, Attractive Sectors: Life Science, 2016

33 JETRO, Attractive Sectors: Life Science, 2016

Healthcare & Medical Technologies – Japan Market Study - Page 43 of 121

3.2. Assistive Technologies

3.2.1. Market Overview Assistive Technologies

According to World Health Organisation (WHO), assistive devices and technologies are those

whose primary purpose is to maintain or improve an individual’s functioning and independence to

facilitate participation and to enhance overall well-being. They can also help prevent impairments

and secondary health conditions. Examples of assistive devices and technologies include

wheelchairs, prostheses, hearing aids, visual aids, and specialised computer software and

hardware that increases, respectively, mobility, hearing, vision, or communication capacities.

In Japan, slightly different from Europe, assistive devices and technologies are part of the welfare

segment that also includes nursing care, rehabilitation and the home-care sector. The Japan

Assistive Products Association (JASPA) has assistive/welfare devices defined as follows.34

Assistive devices that support autonomy and nursing care for elderly and disabled persons

in daily life, regardless of home or facility, and assistive devices that improve the living

environment

Assistive devices (including computer systems and assistive technologies) that are used in

care facilities to improve services for elderly and/or disabled people, and contribute to

labour-saving within the facilities. Devices and technologies that support independence of

residents, nursing care support, and improvement of the environment, different from the

above-mentioned definition

Welfare equipment, devices and social infrastructures that support the actions of elderly

and/or disabled people in public places like elevators in public buildings (train stations being

most common), braille blocks, and audio signals for the visually impaired, amongst others

34 Ageing Population, National Health Insurance, Japanese, March 2017

Healthcare & Medical Technologies – Japan Market Study - Page 44 of 121

Categories and Examples of Assistive Devices and Technologies in Japan

Products covered by care insurance Electric bed for medical care or nursing care, manual wheelchair, electric wheelchair, bedsore prevention mat, handrail, silver car (walker for an aged or disabled person), wandering sensing equipment for people with dementia and elderly people, walking aid cane, slope, automatic excretion treatment device, transfer devices (patient lifts for vertical transfer), bathing assistant, toilet seat, simple bathtub

Nursing care and disposable products Adult disposable diapers, urine leakage pants, elderly underwear, shoes for the elderly, waterproof sheets, wet tissues for nursing care, oral wet tissues for nursing care, mouth sponge brush for nursing care, mouth moisturizing agent, cleanser, nursing gloves

Nursing devices and instruments Special bathing equipment, rehabilitation equipment for exercise therapy, evaluation measuring equipment for rehabilitation, radio paging equipment for home, care robot, communication robot

Systems and services Senior citizen home delivery service, housekeeping substitution for the elderly, emergency response system, sensor type home safety confirmation, infrastructure monitoring, dialogue confirmation, support for nursing care and welfare facilities, school lunch for nursing care and welfare facilities, linen for hospitals/nursing care/welfare facilities, security for nursing care and welfare facilities, prevention of long-term care and rehabilitation, dispensing pharmacies for nursing care and welfare facilities, collaboration support for long-term care

Figure 20: Japan’s Welfare Equipment and Daily Life Support Equipment, Japanese, July 2016

The global assistive technology market is estimated at EUR 17 billion in 2015, with a Compound

Annual Growth Rate (CAGR) of 6% during the period from 2015 to 2020.

The market size of the Japanese welfare equipment industry in FY2014 totalled JPY 1.399 trillion

(EUR 11.65 billion), up 3.8% from the previous year. The overall market size has shown steady

growth since FY2009. Looking at specific products per category, we see that general products

such as wigs, dentures, hot water washing toilet seats, seat shifts for cars, home elevators,

glasses and hearing aids were up 3.9% compared to the previous year FY2013.35 Materials and

devices subject to the nursing-care insurance are showing a recovering trend up 7.4% in FY2014.

35 Market Size of Welfare Equipment, Japan Assistive Products Association (JASPA), 2014

Healthcare & Medical Technologies – Japan Market Study - Page 45 of 121

Market Size in Japan of Assistive Devices and Technologies

FY2010 (JPY/EUR) FY2014 (JPY/EUR)

Total Assistive Devices & Technologies 1,165b/9.7b 1,399b/11.65b

Assistive Devices & Technologies (Total Type A) 1,123b/9.35b 1,340b/11.16b

Home Treatment Equipment (Type A) 73.9b/615m 70.3b/585m

Prostheses and Braces (Type A) 171.3b/1.42b 222.4b/1.85b

Personal Care related products (Type A) 334.6b/2.78b 427.5b/3.56b

Moving Equipment and related products (Type A) 97.5b/812m 128.8b/1.07b

Furniture & Fixtures (Type A) 78.8b/656m 102.3b/852m

Communication Equipment (Type A) 325.5b/2.71b 346b/2.88b

Home Nursing Equipment and related products (Type A) 40.3b/335m 40.9b/340m

Miscellaneous (Type A) 2b/16.6m 2b/16.6m

Nursing Home Equipment and Systems (Type B) 4b/33.3m 6.7b/55.8m

Support and Assistive Devices for return to Society (Type C) 37.3b/310m 44.6b/371m

Assistive Devices covered by Long-term care insurance 218.7b/1.82b 286.2b/2.38b

Figure 21: Japan’s Welfare Equipment and Daily Life Support Equipment, Japanese, July 2016

According to the above table, the market size of welfare equipment in FY2014 is about

JPY 1.4 trillion (EUR 11.65 billion), and home treatment equipment, prostheses and braces, and

personal care-related products have the biggest share in the market.

The main driver is the scheduled revision by Abe’s Cabinet of the current long-term nursing care

insurance system in FY2018. The study also foresees a strong need for convenient purchasing

of lower-priced assistive devices and technology products. Additionally, Japan will need to

formulate an adequate response to the needs of almost 80% of the elderly population who do not

Healthcare & Medical Technologies – Japan Market Study - Page 46 of 121

require special nursing care but do want to enjoy an active retirement, often referred to in Japan

as “Silver Life.”

Figure 22: Services available under Long-Term Care Insurance (LTCI)

Purchase Conditions for above Assistive Devices under LTCI:

Purchasing Limit: Maximum JPY 100,000 (EUR 833) total per fiscal year

Users pay 10% or 20% of the total cost

Same products can only be purchased once per year to receive eligible support

Conditions for Home Renovation under LTCI:

Purchasing Limit: Maximum JPY 200,000 (EUR 1,666) total per fiscal year

Users pay 10% or 20% of the total cost

Total amount of JPY 200,000 can be spread out over several renovations

Products: Handrail installations; step elimination; resurfacing floors to prevent slipping; replacing

hinged doors with sliding doors; replacing Japanese-style toilets with Western-style toilets

Healthcare & Medical Technologies – Japan Market Study - Page 47 of 121

The recent study "Current Situation and Outlook of the Welfare Market in 2017," published by the

Fuji Keizai Group, states that many new assistive products and services will find their way into

the Japanese welfare market.

The same research paper predicts the total market value of assistive devices and technologies

to reach almost JPY 4.5 trillion (EUR 37.5 billion) by FY2025 with a breakdown of almost 40% of

all care products covered by health insurance, approximately 50% for care products and

disposables not covered by the aforementioned insurance, and the remaining 10% for nursing

devices and equipment.36

3.2.2. EU Entry Opportunities Assistive Technologies

For FY2017, the market is expected to expand following new market development by wholesalers

and rental companies of assistive devices now that the personal liability of people with mild

cognitive impairment has been abandoned.

The market will show particularly strong demand for railings, silver cars, walking devices, walkers

and walking assistants as these are also a necessity for elderly people who prefer to maintain

independent living and care prevention. Furthermore, local government services are expected to

purchase these products of durable quality for long-term use for their rental systems, thereby

creating promising business opportunities for European manufacturers.

36 Current Situation and Outlook of the Welfare Market in 2017, Fuji Keizai Group, Japanese, June 2016

Healthcare & Medical Technologies – Japan Market Study - Page 48 of 121

Figure 23: Assistive Devices available for Rental Services

Healthcare & Medical Technologies – Japan Market Study - Page 49 of 121