Embed Size (px)

Citation preview

Stage 2 Feasibility Report

H i g H P l a i n s E x P r E s s i n i t i at i v E

ExEcutivE summary 3

HPx initiativE DEscriPtion 7

Basic information . . . . . . . . . . . . . . . . . . . . . . . 8

Initiative status . . . . . . . . . . . . . . . . . . . . . . . . 8

Estimated process timeframe . . . . . . . . . . . . . . . 8

Conceptual area . . . . . . . . . . . . . . . . . . . . . . . . 8

Initiative participants . . . . . . . . . . . . . . . . . . . 11

BEnEfits of HPx 13

Ratepayer benefits . . . . . . . . . . . . . . . . . . . . . 14

Macroeconomic benefits . . . . . . . . . . . . . . . . . 15

routing/PErmitting finDings 17

Route identification process . . . . . . . . . . . . . . 18

Summary of results . . . . . . . . . . . . . . . . . . . . 19

Permitting plan . . . . . . . . . . . . . . . . . . . . . . . 21

Permitting strategies . . . . . . . . . . . . . . . . . . . 22

Permitting outlook . . . . . . . . . . . . . . . . . . . . . 22

tEcHnical finDings 23

Transmission alternatives . . . . . . . . . . . . . . . . 24

Modeling . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Technical assumptions . . . . . . . . . . . . . . . . . . 26

Transmission line length assumptions . . . . . . . . 26

Transfer capability . . . . . . . . . . . . . . . . . . . . . 27

Cost estimates . . . . . . . . . . . . . . . . . . . . . . . . 28

Integration with other projects . . . . . . . . . . . . . 28

Summary of results . . . . . . . . . . . . . . . . . . . . 30

commErcial finDings 31

Methodology . . . . . . . . . . . . . . . . . . . . . . . . 32

Key assumptions . . . . . . . . . . . . . . . . . . . . . . 33

Resource additions without HPX . . . . . . . . . . . 36

Resource additions with HPX . . . . . . . . . . . . . . 38

Sensitivity cases . . . . . . . . . . . . . . . . . . . . . . . 40

Calculation of revenue requirements for each transmission alternative . . . . . . . . . . . . . . . . . 43

Comparison of net benefits to cost of the line . . . 46

Summary of ratepayer benefit-cost analysis . . . . 54

Other commercial findings . . . . . . . . . . . . . . . 56

conclusion 57

aPPEnDix 60

Glossary of acronyms . . . . . . . . . . . . . . . . . . . 60

Table of Contents

Executive Summarythe High Plains Express (HPx) initiative is a roadmap for transmission development in the Desert

southwest and rocky mountain regions to significantly strengthen the eastern portion of the western

power grid studies indicate that HPx would enhance regional reliability, improve market deliverability

for renewable and other low-cost energy, and potentially provide economic benefits for ratepayers,

utilities and the general public in Wyoming, colorado, new mexico and arizona

5 Executive summaryThe HPX initiative began in 2006 when

a group of interested parties executed a

formal agreement to engage in high-level

studies of the project’s feasibility . Stage 1

of the study effort culminated in a June

2008 Feasibility Study Report . Stage 2

commenced in late 2008 with a more

detailed feasibility assessment conducted

through an Executive Committee and

four standing committees: the Routing/

Permitting Study Committee, Technical

Study Committee, Commercial Study

Committee and Communications

Committee . The following report

summarizes each of the three study

committee’s findings, and marks the

conclusion of Stage 2 .

As outlined in this report, Stage 2 studies

continue to affirm that a high-voltage

transmission system could collect high

quality, low-cost resources and enable

delivery to match demand throughout

Colorado, New Mexico and Arizona .

Stage 2 analyses examined the routing,

technical and economic feasibility of

several transmission line configurations,

with the following general conclusions:

n HPx appears to be feasible from a routing perspective with one or two distinct circuits across the study area

n HPx appears to be technically feasible in any of the proposed line configurations

n HPx economic feasibility is highly dependent on uncertain assumptions

n HPx has the potential to be an economically viable project

The routing/permitting process determined that despite significant siting constraints and areas that present fatal flaws, there are numerous areas where high-voltage transmission could be developed . Project participants accept that there will be challenges associated with developing transmission in or near sensitive areas, and understand that the initiative will be heavily influenced by various regulatory, permitting and land-use activities that may affect the feasibility and risks of a potential project .

Technical analyses evaluated five transmission alternatives: single- and

double-circuit 500kV configurations in a two-corridor approach similar to Stage 1 studies; single- and double-circuit 500kV configurations in a single-corridor approach; and a single-corridor “progressive,” or “telescoping,” configuration that would employ a single 345kV line from Wyoming to Colorado, a double-circuit 345kV line from Colorado to New Mexico, and a single 500kV line from New Mexico to Arizona . Studies found that each of the five alternatives would be technically feasible, with the two-corridor alternatives resulting in both higher transfer capabilities and higher capital investment costs than the single-corridor alternatives .

Despite the seemingly positive outlook on overall project feasibility, the economic findings of Stage 2 present a level of uncertainty that warrants further study before the HPX initiative proceeds as a discrete project into the regulatory, build-out and commissioning stages .

In modeling the economic feasibility of HPX, the Commercial Study Committee and its contractors were required to control the variables surrounding a set of discrete scenarios by making

HPx appears to be feasible in terms of routing and technical considerations

its economic viability is highly dependent on a number of uncertain conditions

6

assumptions about market conditions in the future . Key assumptions are based on load forecasts, renewable demand, cost of generation, price of fuel and electricity, as well as attitude toward power sharing across state lines (as opposed to localized generation) .

Although key assumptions are easily and independently manipulated in the context of the study, there are numerous other factors such as changes to public policy, technological advancements and fluctuating market demands that could have large and unpredictable impacts on the economics of the HPX initiative . Already the results of the study’s limited scenarios demonstrate a wide variation in economic viability—with benefit-cost ratios ranging between .83 and 2 .19 for a single configuration—but in the volatility of the actual market and regulatory environment, these ranges could easily change .

Assumptions used in Stage 2 were based on the best information available to participants at the time of study, but participants recognize that realities

may change at any time to undermine the validity of the economic portion of the report . For example, much of the economic evaluation is based on assumed cost estimates that point to solar options remaining approximately twice the cost of wind—a reality that may or may not be revealed in time . HPX participants also recognize that there are several assumptions used in the study that may or may not align with real markets, or the desires of states or utilities . For example, Stage 2 studies assume no constraints on where renewable energy generation would be located within the four-state study area; however, most or all states have at least some preference for in-state renewables, due to the economic benefits and incentives of such development .

Additional uncertainty exists beyond the assumptions made in the economic evaluation . Even with benefit-cost ratios that exceed 1 .0, no clear mechanisms exist within the HPX footprint for cost allocation and cost recovery, which provides varying benefits to multiple

jurisdictions . Further, a liquid market for

HPX does not currently exist, making

it difficult to monetize the benefits

identified in Stage 2 .

The commercial studies demonstrate

that, under some scenarios, the benefits

provided by HPX would outweigh the

cost of the project . But under other

scenarios, the benefits fall short of the

cost, which could potentially make

the project an imprudent investment

for ratepayers and other entities .

Conversely, if customers or independent

developers are identified who are willing

to financially support the project, there

would be additional incentive for HPX

participants to advance development of

the initiative .

Because of the wide range of outcomes

that are possible at the close of Stage

2, participants have elected to pursue a

Stage 3 evaluation, which will focus on

additional studies and monitor public

policy, market conditions and technical

needs that may impact the viability of the

project .

HPX Initiative DescriptionHPx is intended to be a cost-effective, high-voltage backbone transmission system through

Wyoming, colorado, new mexico and arizona that will enhance reliability and increase access to

renewable and diverse generation resources within regional energy resource zones

9 HPx initiative DescriptionThe initiative was designed to address the region’s:

n anticipated load forecasts, which show a demand for new energy and capacity

n mandated renewable Portfolio standard (rPs) goals

n location-dependent conventional and renewable generation resources, and the cost implications thereof

n Potential risk of renewable curtailment

Basic information

n transmission voltage: 500kv ac

n capacity: 1600 to 8000 mW

n length: approximately 1450 (one-corridor configuration - see figure 2, page 9) to 2250 line-miles (two-corridor configurations - see figure 1, page 10)

n route: originates in southeastern Wyoming and traverses the eastern plains of colorado and new mexico, turning west to a terminus at Palo verde, west of the Phoenix, arizona area

n Preliminary capital cost estimates: $3 4 billion (one-corridor single-circuit line) to $8 3 billion (two-corridor double-circuit lines)

n in-service date: 5 to 8 years after initiation of routing/permitting process

initiativE status

Stage 2, now complete, expanded the feasibility considerations of the transmission alternatives explored in Stage 1, and included more detailed studies to further address issues such as siting, permitting, preliminary design options, and commercial feasibility . The results of Stage 2 confirmed the technical feasibility of various alternatives and refined the transfer capabilities and costs .

As a result of uncertainties that remain at the close of Stage 2, project participants plan to embark on a Stage 3 evaluation effort that will focus on monitoring pertinent regulatory developments, and forming strategies for moving the initiative forward . Stage 3 will include further examination of:

n Energy demand forecasts

n changes in projected costs

n renewable technology developments and improvements

n Public policy developments

n cost recovery mechanisms

n other factors that could impact both the need for and the economic viability of HPx

The length of Stage 3 will depend on how quickly changes occur in the primary factors noted above, but is currently estimated to take between one and three years . It is anticipated that at the conclusion of Stage 3 the participants will

be able to determine whether the project fundamentals justify moving forward with development stages of the project .

EstimatED ProcEss timEframE

n stage 1, preliminary feasibility study (complete) – 2006 to 2008

n stage 2, feasibility study (complete) – 2008 to 2010

n stage 3, evaluation – 2 to 3 years

n corridor development, preliminary engineering and permitting – 3 5-4 5 years (subject to variability on both sides)

n Build-out – 3 to 6 years (subject to variability on both sides)

n commissioning – 2020 to 2025 timeframe

concEPtual arEa

The conceptual area and general transmission routing for the two-corridor and single-corridor alternatives are shown in Figures 1 and 2 . Figure 1, page 9, shows the two-corridor configuration . The eastern/southern corridor originates in Wyoming, follows an easterly route through Colorado and New Mexico, and terminates in central New Mexico at the SunZia Project . The western/northern route also originates in Wyoming, but follows a more western route through Colorado and New Mexico . It also connects to the SunZia Project, but continues into Arizona and terminates at Palo Verde . Figure 2, page 10, shows the

10

figurE 1

HPX Two-Corridor Configuration Conceptual Map

11

figurE 2

HPX One-Corridor Configuration Conceptual Map

12

conceptual routing for the single-corridor alternative . Note that the single-corridor routing overlaps with portions of each of the routes used for the two-corridor alternatives . The transmission would interconnect with numerous substations and coordinate with other proposed transmission projects within the HPX conceptual area .

initiativE ParticiPants

Preliminary meetings to discuss concepts, interest and scope led to the development of an agreement for a transmission feasibility study . Each of the interested parties felt that the best

way to conduct a joint study would be to pool resources and hire independent consultants for the bulk of the transmission studies . These participants entered into a formal agreement that described the scope of the study effort and the participant responsibilities .

Participants include:

n colorado springs utilities

n Public service company of new mexico

n salt river Project

n ls Power

n tri-state g&t

n Western area Power administration

n xcel Energy

n new mexico renewable Energy transmission authority

n Wyoming infrastructure authority

n colorado clean Energy Development authority

n Black Hills corporation

n nextera Energy resources

Participants then divided into five standing committees to distribute study tasks as shown in the following organization chart .

(ls PoWEr) (xcEl EnErgy)

figurE 3

HPX Organization

(xcEl EnErgy & ls PoWEr)

Benefits of HPXas described in the Executive summary (page 3-5), the primary benefits of HPx would be derived from

allowing lower-cost resources to be delivered to markets that they would not otherwise be able to reach

in turn, this would enable these resources to expand utilities’ and states’ options for procuring renewable

energy, and may help them achieve mandated rPs targets furthermore, collaboration among projects

and utilities within the HPx footprint could minimize environmental impacts and control expenses of

future development through the use of shared planned utility corridors

15 Benefits of HPxIn evaluating the viability of the HPX initiative, it is necessary to weigh the quantifiable benefits of HPX—such as potential savings to ratepayers, macroeconomic growth and access to renewable resources—against the total start-up and ongoing costs . This section qualitatively describes the long- and short-term benefits to ratepayers and regional economies . For a quantitative analysis of how these benefits compare to the overall cost of the project, please refer to page 4 (Comparison of net benefits to cost of the line) .

ratEPayEr BEnEfits

Ratepayers benefit when a project reduces a utility’s revenue requirement, lowering the amount the utility needs to collect from its customers . Many factors contribute to offsetting a utility’s revenue requirement, but three primary opportunities for the HPX initiative include: reduction in the cost of resource procurement, operational benefits resulting from increased efficiency of resource dispatch to meet load, and the value of shared capacity resources to meet peaks among balancing authorities .

Stage 2 studies attempt to quantify the

impact that HPX will have on all three

factors .

long-term procurement benefits

Increased transfer capability between

Wyoming, Colorado, New Mexico

and Arizona may benefit ratepayers

by reducing the costs of procuring

energy to meet renewable and load-

service requirements . A transmission

line from Wyoming to Arizona would

allow Colorado, New Mexico and

Arizona utilities to access additional

wind resources to meet their renewable

generation needs . These resources,

developed with the line, may be able to

displace the traditionally higher-cost wind

in Colorado and New Mexico, and the

higher-cost solar resources in New Mexico

and Arizona, thereby reducing the cost of

renewable procurement in each of these

states . While the study presumed that the

highest capacity factor for wind power

would remain in Wyoming, Colorado

and New Mexico may also develop wind

resources for export, depending on the

line’s configuration .

operational benefits

Increasing the transfer capacity among the four states in the study area could initiate more competition among fossil fuel resources in the West, leading to lower costs to ratepayers . The proposed line would allow natural gas generators in Wyoming and Colorado to compete with those in New Mexico and Arizona, displacing power generated with higher-cost Southwestern gas and replacing it with power from plants that have access to the traditionally lower-cost Rockies gas market . Entities in the Southwest may benefit from depressed market prices at the Palo Verde trading hub in Arizona, while those in Colorado and Wyoming that control much of the fossil fleet in that region could benefit due to increased plant operation . Any benefits would be passed on to ratepayers in the region . In addition, the line may provide an outlet to allow surplus solar energy from the Southwest to be transferred back to New Mexico and Colorado .

capacity-sharing benefits

The proposed line would increase the transfer capability among the various utilities in the study area . This increased

HPx would enhance regional reliability, improve market deliverability for

renewable and other low-cost energy, and potentially provide economic benefits

for ratepayers, utilities and the general public

16

transfer capability would allow for increased capacity sharing between utilities as they build generation portfolios to meet planning reserve margins .

Increased transfer capability within the study area would allow for utilities to benefit from the diversity of their peak loads and resource portfolio mix, especially renewable resources . Differences in weather patterns and load characteristics mean that different utilities experience their system peak at different times during the year . The quantity of resources that a given utility needs to build to meet its reserve requirement is determined by that utility’s peak load . Without transfer capability between zones, each utility must build sufficient new capacity to meet the growth of its non-coincident peak . However, HPX would enable additional transfer capability between utilities, increasing their ability to import or export more power during peak load hours to assist neighboring states in meeting load and reserve requirements . This allows utilities to avoid or defer new capacity investments . The benefits from avoided investments in new generation capacity would be shared by ratepayers across the region .

other ratepayer benefits

Increasing the transfer capability between states in the West may also have operational reliability benefits, although

those benefits have not been quantified in this stage . Additional transfer capacity can defer the need for reliability-driven system upgrades and reduce the operating costs associated with maintaining the hour-to-hour reliability of the system .

One particularly interesting operational benefit that has not been quantified in this analysis is the benefit of blending geographically diverse wind resources on time segments of an hour and less . The intermittency of wind generation is one of the major challenges of its integration into the electric power system . However, HPX would facilitate the development of wind generation from multiple remote geographic regions and solar resources in the Southwest, thereby providing a more diverse portfolio of renewable resources . Especially at the high renewable penetrations targeted by some states, this could reduce the cost of operating with respect to the variability and uncertainty of wind and solar resources .

The increased reliability of the system with HPX may ultimately reduce utility costs associated with insurance and risk mitigation measures, however this is not confirmed . System operators would have increased operational flexibility during reliability events because of the increased robustness resulting from the construction of HPX .

There are several other potential benefits of the line that are not included in the

ratepayer analysis . Non-ratepayer benefits of the line include a possible reduction in WECC-wide greenhouse gas emissions, the potential for lowered regional fuel prices and the availability of other ancillary services .

macroEconomic BEnEfits

In addition to ratepayer benefits, the construction of HPX would bring other benefits to the four affected states . The construction of the line and associated resources would provide macroeconomic benefits to states where the majority of development would occur: the project would provide new jobs and increase the states’ tax bases . Based on the assumptions of the study, Arizona, by contrast, would experience the greatest benefit from ratepayer savings, rather than economic development .

The Stage 2 Economic and Fiscal Impact Analysis performed by Cardno ENTRIX found that there would be three sources of economic impact in Wyoming: the construction and operation of the HPX transmission line, the construction and operation of 3,000 MW of wind power generation, and ratepayer savings . There would be four sources of economic impact in Colorado: the construction and operation of the HPX transmission line, the construction and operation of gas combined turbine (CT) generation, ratepayer savings, and the manufacture of wind turbine blades and towers for

17

HPX-related wind farms located in other states . And there would be two sources of economic impact in New Mexico: the construction and operation of the HPX transmission line and ratepayer savings .

Combined estimated economic impacts, in terms of increased jobs and income, above and beyond what the region would experience without HPX, are as follows:

n construction phase impacts are estimated at $2 7 billion and 21,700 jobs

n construction phase income in each of the three states ranges from $800 million to $1 billion

n total recurring annual operations impacts are estimated at $74 million and 850 annual jobs

n recurring operations phase income ranges from $8 million annually (nm) to $33 million annually (co, Wy)

A portion of the operation and

construction costs of HPX and related

generation facilities would go toward

local and state governments in the form

of taxes . Using income, sales/use and

property tax data collected by Cardno

ENTRIX, it is estimated that total taxes

collected during construction would be

$371 million in Wyoming, $30 million

in Colorado and $51 million in New

Mexico . Ongoing annual tax collection,

almost exclusively due to property

tax, is estimated to total $58 million in

Wyoming, $28 million in Colorado and

$11 million in New Mexico .

Routing/Permitting Findingsstage 2 routing/permitting studies evaluated opportunities and constraints within the

initiative footprint, and developed permitting scenarios at the local, state and federal

levels the study area included 123,000,000 acres, spanning 62 counties in four states, and

representing the gamut of land-ownership classifications as described in figure 4, page 18

19

figurE 4

Land ownership within the HPX study area

routing/Permitting findingsroutE iDEntification ProcEss

An opportunities and constraints analysis is a preliminary activity in the process of identifying routes for a proposed transmission line, though specific corridor and route identification was not a goal of Stage 2 studies . Corridors between interconnection points can be determined by capitalizing on areas of opportunity and attempting to avoid or mitigate the use of areas of constraint within the overall study area . The opportunities and constraints analysis consisted of the following steps:

Data collection

Resource data within the study area were collected from federal, state, and local government agencies as well as non-governmental organizations, HPX participants and private companies . Data obtained were used to prepare resource maps showing the following resource categories: land use, transportation, land cover, utilities, water resources, cultural and historic resources, biological resources, and geology and soils .

identification of opportunities and constraints

Data were classified into one of three categories based on the resource’s compatibility with transmission facilities and restrictions on proximity of those facilities to sensitive resources .

n opportunity areas (14 classes) are considered favorable for transmission line routing and tend to contain existing development or linear features (e g , roads, transmission lines, pipelines) that minimize the need to develop new corridors

n sensitivity areas (50 classes) are areas where environmental effects are likely to occur or be negatively perceived, given the placement of extra-high voltage facilities Examples of sensitive areas include native american reservations, Blm-designated areas of critical Environmental concern, wetlands and big game wintering areas it may be possible to mitigate the effects of facilities in these areas using routing adjustments, careful placement of transmission structures and access roads, and other similar mitigation measures

n Exclusion areas (20+ classes) represent the area of greatest potential environmental, social or economic effects these areas generally are excluded from routing, often as a matter of law or regulation impacts to exclusion areas generally do not have mitigation potential the HPx study area includes more than 6,000,000 acres of exclusions comprised of usfs wilderness, usfs roadless areas, wilderness study areas, national Park services lands, etc

identification of stakeholder issues

There are several transmission projects in various stages of planning and implementation within the HPX study area . Documents containing public input from 17 transmission or generation projects were reviewed to identify potential public concerns and incorporate them into the opportunities and constraints analysis .

20

future considerations

This analysis was designed to consider landscape features and land management at a state/county level . During the data collection effort, 45 additional criteria were identified that would be useful during corridor and route identification in future phases of the initiative . Examples of these criteria include the locations of airports, oil and gas wells, scenic easements, wetlands, floodplains, historic sites, Native American Sacred Sites, occurrences of protected species and separation requirements between high-voltage transmission facilities .

composite mapping

Classification of resources in this manner helps to rapidly assess potential impacts to sensitive areas, and to avoid restricted areas in the corridor identification and routing processes . A composite map was prepared of opportunity, sensitivity, and exclusion areas using GIS analysis (Figure 5) . The opportunities and constraints map for the study area is shown in Figure 6, page 20, in the Results section below .

summary of rEsults

Table 1 summarizes the acreages of opportunity, sensitivity and exclusion areas by state, while Figure 6, page 20, shows an overlay of these areas on a regional map . Locations where opportunity areas overlap are shown in darker green as having the greatest opportunity . Overlapping sensitivities are shown in shades of yellow and orange . Exclusion areas are shown in red .

figurE 5

Opportunities/constraints mapping

taBlE 1

Acreage of opportunities and constraints by state

Category WY

(acres) CO

(acres) NM

(acres) AZ

(acres) Opportunity Areas

11.7 million 17.8 million 24.5 million 13.3 million

Sensitivity Areas

4.3 million 8.0 million 23.5 million 12.6 million

Exclusion Areas

0.4 million 0.4 million 3.5 million 3.0 million

21

figurE 6

Opportunities and constraints within the HPX study area

22

PErmitting Plan

Routing a transmission line and

associated facilities would require

compliance with federal, state and local

laws to varying degrees, dependent

upon the routes, ownership of facilities

and funding mechanisms . The purpose

of a permitting plan is to identify these

requirements for the construction and

operation of HPX . The plan defines

plausible permitting scenarios based

on agency jurisdiction in the study area;

identifies applicable permits, approvals

and process requirements of agencies that may have future guidance for route selection and are necessary to construct and operate HPX; identifies a tentative permitting schedule; and identifies and discusses critical issues that may affect compliance requirements, costs and schedules .

PErmitting scEnarios

Given the broad study area, the proposed length of the HPX transmission project and the number of federal agencies

with jurisdiction pertaining to lands or resources in the study area, it is likely that federal approval and National Environmental Policy Act (NEPA) compliance will be necessary (Figure 7) . Plausible permitting scenarios have been identified based on the type of federal action triggering NEPA, the scope of the NEPA process, and how compliance with state and local regulations would be achieved . The timeframe for permitting a multi-state transmission project can be expected to take approximately 2 .5 to 3 years to complete .

figurE 7

NEPA permitting process

23

PErmitting stratEgiEs

The most land-intensive transmission

alternative for HPX would require

construction of two double-circuit 500kV

AC transmission lines . Given the length of

the proposed line, number of landowners

and agencies involved, and the necessary

coordination between utilities, permitting

will require significant investments in

time and funding .

Other factors that may facilitate

permitting include coordination of

field studies for environmental impacts

that are required by various agencies

and permit applications, as well as

identification of data needed early in the

process . The timing of the NEPA process

and state permit process should also be

considered . The Arizona Corporation

Commission and Power Plant and

Transmission Line Siting Committee,

the Wyoming Industrial Siting Division, and the New Mexico Public Regulation Commission express a strong preference with projects also requiring a NEPA process that at least a draft Environmental Assessment or EIS be completed before public hearings with these state agencies .

PErmitting outlook

While further study is needed to determine the economic viability of proceeding with the development stages of HPX, project participants recognize that the future will likely bring a variety of conditions to the study area that will affect the feasibility of currently proposed routing and permitting strategies, as well as the conceptual schedule . Factors may include:

n Population growth

n oil, gas and wind development

n new wilderness proposals

n Energy corridor designation by state and federal governments

n conservation easement protections

n critical wildlife corridor designations

n more endangered species designations

n increase in permitting and/or mitigation costs

These factors will be critical to track

as the initiative moves forward . An

efficient and productive routing and

permitting process is dependent on

early involvement and comprehensive

participation from stakeholders, including

the public, landowners and permitting

agencies, and will invest the time

necessary to engage diverse stakeholders

from all four states .

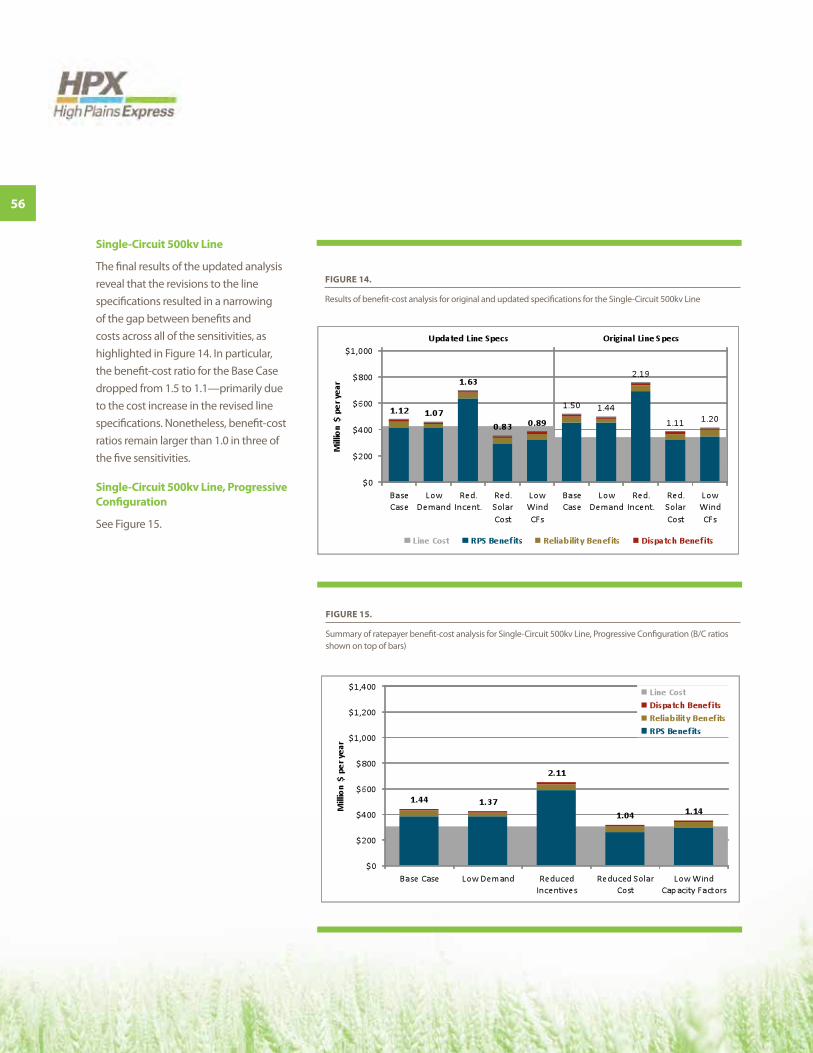

Technical Findingsstage 2 technical studies expanded on the stage 1 effort, and evaluated five transmission

alternatives Each alternative consists of a set of high-voltage transmission system

additions that would originate in Wyoming and terminate in arizona

25 technical findings transmission altErnativEs

Stage 1 studies focused on a line configuration that would occupy two transmission corridors, as shown in Figure 1, page 9 . Stage 2 technical analyses started with that premise, using a slightly modified layout of the corridors . In Wyoming, the transmission was assumed to originate at a proposed Windstar substation, which has been considered as a potential location for wind development . In New Mexico, the eastern corridor was moved farther to the east to interconnect with the existing Blackwater substation . This would allow the project to accommodate resources on the eastern side of New Mexico and would present an opportunity to connect to the proposed Tres Amigas project . In Arizona, the transmission has been extended past the Phoenix area to terminate at the existing Palo Verde station . Finally, since the SunZia project is considered an independent project for the Stage 2 analysis, most studies assumed that SunZia would be in place and the eastern corridor would terminate at the western terminus of SunZia at a substation referred to as “SunZia East” .

In addition to the original two-corridor configuration, Stage 2 studies also examined system alternatives that would utilize a single transmission corridor, shown in Figure 2, page 10 . The single-corridor routing would use portions of the paths used for the two-corridor alternatives . From Wyoming to

Colorado, the western path was used, with transmission running from Windstar through Laramie River, then to Pawnee . From Pawnee, a transmission path would be developed to Wray, where the eastern corridor would be used down to Vilas . From Vilas, the path would connect to Gladstone, where the western/northern corridor would be used into Arizona . The single corridor alternatives still have the potential for coordinating with the Wyoming-Colorado Intertie Project and the Colorado SB100 transmission .

Two of the alternatives evaluated utilized the two-corridor configuration: a single-circuit 500kV transmission, and a double-circuit 500kV transmission in each corridor . Three of the alternatives utilized the new, single-corridor approach: a single-circuit 500kV transmission, a double-circuit 500kV transmission, and a “progressive,” or “telescoping,” alternative . This progressive alternative modeled a single 345kV line from Wyoming to Colorado, a double-circuit 345kV line from Colorado into New Mexico, and a single 500kV line from New Mexico to Arizona . The basic transmission alternatives are summarized in Table 2 . Table 3 lists the interconnection locations that were modeled for the alternatives .

moDEling

Base casesStudies were performed using ten-year planning horizon powerflow and

dynamic models . The WECC-approved 2019 Heavy Summer (19hs1a .sav) was used as the seed case for this analysis . The cases were reviewed and modified by the Technical Study Committee participants to represent the system loads and topology expected for the year 2020 .

resource/interconnection modelingGenerally, the incremental transfer capability as a result of the HPX transmission additions for each alternative was measured by increasing generation at the originating substations in Wyoming, and by decreasing generation in Arizona .

WyomingGeneration was added at the proposed Windstar substation and the existing Laramie River substation in Wyoming . For the most part, generation was added at each location in equal amounts . Generation added in Wyoming was balanced by a generation reduction in Arizona .

coloradoFor Colorado, some generation was added at each interconnection within the state . Many of these have a high potential for renewable energy development . Any increase in generation at the interconnections within Colorado was balanced by (a) an increase in load due to load growth in the 2020 forecast, and (b) reduced generation at Denver-metro fossil-fuel plants . Therefore, there was

26

Alternative Interconnection points – west corridor Interconnection points – east corridor Two-‐corridor, single-‐ or double-‐circuit Windstar

Laramie River Pawnee Big Sandy Boone Gladstone Guadalupe Corona Springerville Abel Palo Verde

Windstar Wray Burlington Lamar Blackwater Corona SunZia East

One-‐corridor, single-‐ or double-‐circuit Windstar Laramie River Pawnee Wray Burlington Lamar Vilas Gladstone Guadalupe Corona Springerville Abel Palo Verde

taBlE 3

HPX interconnection locations

Alternative Description 1 Two single-circuit 500kV lines from Wyoming to Arizona 2 Two double-circuit 500kV lines from Wyoming to Arizona 3 One single-circuit 500kV line from Wyoming to Arizona 4 One double-circuit 500kV line from Wyoming to Arizona 5 “Progressive” 345-kV & 500-kV System (This alternative modeled a single 345kV line from

Wyoming to Colorado; a double-circuit 345kV line from Colorado into New Mexico; and a single 500kV line from New Mexico to Arizona.)

taBlE 2

HPX configuration alternatives

27

no net impact on imports or exports for Colorado as a result of the additional generation within Colorado .

new mexicoFor New Mexico, modeling was conducted with a similar approach as in Colorado . The benchmark base case included 3000 MW of generation associated with the SunZia project, which was scheduled to Arizona . However, the Technical Study Committee agreed to modify the generation to place 1000 MW at three New Mexico locations: SunZia East, Corona, and Blackwater . In addition, some generation was added at Gladstone and Guadalupe . That generation was balanced by (a) an increase in load due to load growth in the 2020 forecast, and (b) reducing generation at New Mexico fossil-fuel plants .

arizonaTo balance the generation added in Wyoming and scheduled on HPX, fossil-fired units in Arizona were decremented on a pro-rata basis . Specifically, the following generation sites were used for balancing the generation increases at Windstar and Laramie River in Wyoming:

n Palo verde Hub area generation (arlington, mesquite, red Hawk, Harquahala)

n Pinal central area generation (Desert Basin)

n Willow generation (Bowie)

n abel s generation (abel)

n springerville sub generation (springerville)

tEcHnical assumPtions

n HPx transmission line characteristics were modeled using 3-conductor bundled 1590 kcmil “lapwing” conductor with a normal rating of 2892 mva and an emergency rating of 3336 mva

n the study assumed 70% series compensation for all HPx line segments stage 1 studies evaluated various levels of series compensation, but this study maintained a level of 70% on all HPx transmission segments the continuous and emergency ratings for the series compensation were assumed to be at least that of the transmission conductors

n impedances for each transmission line segment were calculated based on line length assumptions as described below

transmission linE lEngtH assumPtions

In order to calculate estimated line impedances, the length of each transmission line was estimated . While precise transmission line routing has not been conducted, the Routing/Permitting Study Committee’s findings were used to estimate routing lengths between upload

and download locations . Lengths of each segment are summarized in Table 4 .

Westerly route: The western route would start in Wyoming at the proposed Windstar substation near Dave Johnston power plant . The line would interconnect at Laramie River station, then cross into Colorado and interconnect at Pawnee, Big Sandy and Boone . From Boone the line would travel to New Mexico and connect to Gladstone . In New Mexico intermediate interconnection points were modeled at Guadalupe and Corona . Leaving New Mexico, the western corridor would take a more northerly route to Arizona . In Arizona interconnections were modeled at Springerville and Abel, terminating at Palo Verde .

Easterly route: This eastern route would start in Wyoming at the proposed Windstar substation, and follow an easterly route to the eastern Colorado substations at Wray, Burlington, Lamar and Vilas . From Vilas the line would continue through eastern New Mexico and connect to Blackwater . This is a deviation from the Stage 1 studies, where both lines remained in a common corridor from Gladstone to Ft . Craig . For Stage 2, the eastern route continues from Blackwater to Corona, where it would meet with the western corridor . At Corona, a tie would be created to SunZia by a line from Corona to SunZia East substation .

28

transfEr caPaBility

Because HPX would traverse four states and interconnect the existing transmission system at a multitude of locations, it does not make sense to think of the project as having a single MW rating . In fact, the transfer capability will vary along the project length . WECC “paths” are defined by a discrete set of transmission elements that cross a defined boundary . The HPX transmission

configuration crosses many different

existing paths and creates the potential

for numerous path definitions .

To simplify the issue for the Stage 2 study

effort, three new transmission paths were

defined to evaluate potential transfer

capabilities . For simplification, the paths

are now defined by the state boundaries

that the transmission elements crossed .

HPX Path 1 is defined as the Wyoming/

Colorado border, HPX Path 2 is defined

as the Colorado/New Mexico border, and

HPX Path 3 is defined as the New Mexico/

Arizona border .

Stage 2 technical studies established

preliminary transfer capability ratings for

each of these three new paths . It should

be cautioned that the scope of this study

is considered preliminary and is limited,

compared to a complete path rating

Alternative Voltages Line Project Miles 1 2 3 4 5 Windstar – LRS New 75 500X1 500x2 500X1 500x2 345X1 LRS – Pawnee WYCO 180 500X1 500x2 500X1 500x2 345X1 Pawnee – Wray New 85 500X1 500x2 345x1 Wray – Burlington New 60 500X1 500x2 500X1 500x2 345x1 Burlington – Lamar SB100 100 500X1 500x2 500X1 500x2 345x2 Lamar – Vilas SB100 60 500X1 500x2 500X1 500x2 345x2

Vilas – Gladstone New 120 500X1 500x2 345x2 Gladstone–Guadalupe New 104 500X1 500x2 500X1 500x2 345x2 Guadalupe – Corona New 65 500X1 500x2 500X1 500x2 345x2 Corona–SunZia East New 30 500X1 500x1 500X1 500x1 500x1 Corona–Springerville New 262 500X1 500x2 500X1 500x2 500x1 Springerville – Abel New 180 500X1 500x2 500X1 500x2 500x1 Abel – Palo Verde New 127 500X1 500x2 500X1 500x2 500x1 Windstar – Wray New 285 500X1 500x2 -- -- -- Pawnee – Big Sandy New 61 500X1 500x2 -- -- -- Big Sandy – Boone New 79 500X1 500x2 -- -- -- Boone – Gladstone New 140 500X1 500x2 -- -- -- Gladstone – Guadalupe New 104 500X1 500x2 -- -- -- Vilas - Blackwater New 285 500X1 500x2 -- -- -- Blackwater – SunZia East New 150 500X1 500x2 -- -- --

taBlE 4

HPX estimated line lengths and requirements by segment

29

study consistent with the WECC Three Phase Path Rating Process, but more along the lines of a preliminary Phase 1 path rating study .

interaction with sunZia

For comparison purposes, Stage 1 technical studies considered the SunZia Project to be incorporated into the HPX Initiative as a potential segment of HPX and the number of circuits and voltage levels would match other series components . Stage 2 studies, however, model the SunZia project as a separate and independent project from HPX, consisting of two 500kV AC lines for modeling purposes . Between New Mexico and Arizona, the HPX Path 3 transmission consists of either one single-circuit 500kV line or one double-circuit 500kV line stretching from Corona to Palo Verde . To evaluate how HPX and SunZia might complement each other as part of the interconnected system between New Mexico and Arizona, Path 3A has been established to evaluate synergies between HPX and SunZia . Path 3A consists of HPX Path 3 combined with SunZia flows .

cost EstimatEs

The Technical Study Committee also developed planning level cost estimates for each alternative . Transmission cost data was compiled from several sources in the western interconnection including utility data, and information compiled

by the Western Governors’ Association (“WGA”) .1 Costs have been developed for transmission lines (per mile), transformers, substations and reactive devices . From the accumulated cost data, cost estimates have been developed for each of the HPX transmission alternatives . The 500kV transmission alternatives were evaluated as one- and two-corridor configurations (see Figures 1 and 2, pages 9 and 10) . Cost estimates examined both single-circuit and double-circuit designs for each corridor . The single-circuit alternatives also include a cost sensitivity to address the possibility of building single circuit towers in a manner that would facility expansion to double-circuit in the future . Cost estimates are in 2010 dollars .

intEgration WitH otHEr ProjEcts

One of the primary goals of the HPX initiative is to determine how development of the transmission system would be able to coordinate with other high-voltage transmission projects within the region of study . There are several other projects within the HPX project footprint that are under various stages of development including the Wyoming-Colorado Intertie Transmission Project (WCI), the Colorado Senate Bill 07-100 (SB100) transmission projects, the New Mexico Wind Collector System, and the SunZia Southwest Transmission Project (SunZia) . These projects are included in Figure 1, page 9 .

For the Stage 2 technical studies, WCI and the SB100 projects were assumed to be—and modeled as—components of HPX . The New Mexico Wind Collector System does not have any specific projects recommended to date, and therefore neither the collector system nor any components of the system were modeled as components of HPX . The SunZia Project was considered to be independent of HPX, although studies did consider how HPX and SunZia transmissions could complement each other . Most studies modeled the SunZia project as two 500kV AC lines between New Mexico and Arizona . However, some sensitivity work modeled the project as a single 500kV AC line and a single 500kV DC line .

The following sections describe the transmission projects that were considered during the course of studies .

1 Wyoming-colorado intertie

Through a public/private partnership, LS Power and the Wyoming Infrastructure Authority are developing the Wyoming-Colorado Intertie (WCI), an investment in new electric transmission infrastructure between southeast Wyoming and northeast Colorado . The project has been planned as a single 345kV line between Dave Johnston and Laramie River station in Wyoming, and the Pawnee substation in Colorado, northeast of the Denver metro area . Since HPX contemplates having a transmission line from the Dave

1Data published in the Western Renewable Energy Zones (“WREZ”) Transmission Model

30

Johnston/Laramie River to the Pawnee

area, Stage 2 studies considered WCI to

be an integral segment of HPX .

2 colorado sB07-100 projects

In Colorado, Senate Bill 07-100 (“SB 07-

100”) requires regulated utilities in the

state (PSCo and BHP) to designate “Energy

Resource Zones,” plan transmission

projects to alleviate constraints to those

zones, and petition the Colorado Public

Utilities Commission for approval of

such plans . PSCo has developed several

transmission plans as the result of

SB07-100, all of which were modeled in

the Stage 2 studies . One of the planned

projects is the Lamar-Front Range

transmission project . Portions

of that project have the potential to be components of HPX, specifically transmission along the eastern edge of the state .

3 new mexico Wind collector

Public Service Company of New Mexico (PNM) has been evaluating transmission alternatives for wind collector systems that could deliver power from potential wind resource development zones to load centers in the state . No specific projects have been recommended to date, so there were no high-voltage collector systems modeled for Stage 2 studies .

4 sunZia

The SunZia Southwest transmission project (“SunZia”) is contemplated

as an approximately 500-mile, 500kV

transmission system that would run

between central New Mexico and

southern Arizona . SunZia is currently

evaluating two primary permitting

alternatives . The first consists of two

500kV AC lines with a transmission

capacity of approximately 3000 MW .

The second is a hybrid configuration

consisting of one 500kV AC line and

a bi-pole 500kV DC line . The hybrid

configuration would have a transmission

capacity of approximately 4500 MW .

Stage 2 studies modeled the SunZia

project as a separate and independent

project from HPX, consisting of two 500kV

AC lines for modeling purposes .

Alternative HPX Path Transfer Capability (MW) Cost ($Billions)

#. Description Path 1 (WY-CO)

Path 2 (CO-NM)

Path 3 (NM-AZ)

Path 3A (Path 3+SunZia)

1 Two corridors; Single-circuit 500Kv

3500 3700 2200 6000 $5.5-$7.22

2 Two corridors; Double-circuit 500kV

6700 6800 4000 7900 $8.3

3 One Corridor Single-circuit 500

1600 1800 1600 1600 $3.4-$4.52

4 One Corridor Double-circuit 500

3900 3700 4300 8000 $5.5

5 Progressive

1000 2000 2000 5800 $4.8

taBlE 5

Summary of alternative flows and costs

2The single-circuit transmission alternatives show a range of costs. The lower cost reflects a scenario in which the project is constructed with single-circuit towers. The higher cost reflects the increase in cost if the towers are constructed so that a second circuit could be added in the future (“double-circuit capable”).

31

summary of rEsults

Table 5 shows the approximate transfer capabilities of each of the HPX paths, and the estimated costs for each of the transmission alternatives . The ratings are “non-simultaneous,” meaning that they do not consider interaction with any other existing or accepted WECC path ratings . Further detailed studies will be

required in subsequent stages of the HPX

Initiative to verify that the paths chosen

are appropriate, and determine any

impacts or interaction with other WECC

paths and regional projects . The costs

shown in the table represent the costs of

each transmission alternative alone, and

do not include any costs to potentially

adjust other transmission system

elements that experience a change in load with the addition of HPX .

To achieve some of the transfer capability values listed in Table 5, mitigation measures will be required for certain contingency conditions . The mitigation generally is expected to consist of generator tripping for double-circuit outages of HPX lines .

Commercial Findingsstage 2 commercial studies evaluated potential economic benefits of the construction of

HPx in relation to overall project costs the HPx commercial study committee contracted

Energy+Environmental Economics (E3), a san francisco-based firm that specializes in large-

scale predictive modeling and analysis for the electricity industry, to perform the economic

analysis for stage 2 this report contains an abridged version of E3’s findings

33

# Technical Study Commercial Study (original) Commercial Study (updated)

1 Two-‐corridor, single-‐circuit 500kV Parallel single-‐circuit 500kV lines 2 Two-‐corridor, double-‐circuit

500kV

3 One-‐corridor, single-‐circuit 500kV Single-‐circuit 500kV line Single-‐circuit 500kV line (updated specs)

4 One-‐corridor, double-‐circuit 500kV Double-‐circuit 500kV line 5 Progressive (single 345kV/double

345kV/single 500kV)

6 Single-‐circuit 500kV Line in the progressive configuration

7 Parallel single-‐circuit 500kV lines in the progressive configuration

Please note that, due to time constraints

in Stage 2, the Commercial Study

Committee and the Technical Study

Committee performed their evaluations

simultaneously . The Commercial Study

Committee used the best information

available at the time to identify probable

scenarios and key assumptions, and

to estimate project costs and transfer

capability . However, over the course

of the study it became clear that the

findings of the Technical Study diverged

from the assumptions used in the

Commercial Study . Rather than delay the

completion of Stage 2, the Commercial

Study Committee used initial cost

estimates from the Technical Study to

update the analysis for the single-circuit

500kV transmission alternative, which

was believed at the time to offer the

best balance of benefit-cost and overall

cost considerations . The new results for

this alternative are labeled as “updated specs,” while the results of the other four configurations considered by the Commercial Study Committee remain unchanged from their original estimates prior to the Technical Study’s conclusions . All results will be updated or addressed as appropriate in Stage 3 .

It should also be noted that the Commercial and Technical Study Committees had identified slightly different configuration specs for their respective studies: three configurations are the same in both studies, while two are different . This discrepancy does not affect the outcome of the study, but for purposes of clarity is outlined in Table 6 .

mEtHoDology

E3 calculated the benefits of the HPX project—assuming that there is free

capacity on HPX unhindered by any single transmission tariff—and compared these benefits to the cost of the transmission project . This method is intended to allow an overall evaluation of the project’s cost-effectiveness, independent of any cost-allocation decisions . In order to project realistic outcomes for the HPX initiative, E3 developed a series of the most likely scenarios in which certain market variables were held constant and others were manipulated . The assumptions used to create these scenarios are described on page 33 .

A benefit-to-cost ratio for each scenario was then derived using state-by-state resource plans that comply with any and all regulations within that state . This includes consideration of how the different state requirements treat different classes of utilities (public, cooperative, IOUs, etc .), but does not

taBlE 6

Comparison of alternatives between the Technical and Commercial Studies

34

differentiate between utilities within

a state when building up portfolios .

Instead, E3’s model aggregates all utilities

within a state into a single “state-utility,”

which bases its renewable requirements

on the requirements for each individual

utility within the state, and selects

resources to meet the aggregated need .

This methodology allows E3 to evaluate

the relative magnitude of the line’s impact

on ratepayers in each state without

modeling individual utilities; it also

enables E3 to integrate the results of the

production simulation into the analysis .

Again, this simplification may affect the

distribution of costs and benefits, but will

not affect the overall cost-effectiveness of

the line .

The resource portfolios developed in the

model are designed to ensure that all

RPS, energy and capacity requirements

are met . For RPS requirements, the

model takes into account provisions

of the specific laws that constrain the

resource mix—for instance, Arizona’s 30%

distributed generation requirement .3

Once the renewable portfolios are

developed, the model adds combined-

cycle gas turbines (CCGTs) and simple

cycle gas turbines (CTs) to ensure that

energy and peak capacity and reserve

requirement needs are adequately met .

The economic analysis did not investigate

the addition of conventional coal-fired

generation .

The analysis done by E3 is a “snapshot”

analysis, looking at the effect of the line

in 2025 . This year was chosen because

this is the first year in which the full

RPS requirements are in effect in every

state . Full production cost modeling

of all hours of the year was conducted .

A snapshot analysis is appropriate

because the primary benefit is due to

long-term procurement of renewable

resources, however it should be noted

that a snapshot analysis does not

capture expected long-term changes in

operational benefits .

The resource plans developed for each

state-utility are used to estimate each

state-utility’s electric sector revenue

requirement, both with and without

HPX . Each state’s revenue requirement

utilized in this study was considered to

be all-inclusive, taking into account the

costs associated with transmission and

distribution assets, as well as fixed and

variable costs of generation, though

individual studies of those factors were

not conducted . Thus, the difference

between the revenue requirements

with and without the line (neither of

which include the cost of the HPX line)

represents the gross potential benefits

that the HPX project could deliver to

the region . These benefits can then be

compared to the estimated revenue

requirement of the HPX project to

determine the relative benefit-cost ratio .

kEy assumPtions

load forecast

Power demand in the four states affected by HPX is projected to rise steadily as population increases . The largest demand is projected to be in Arizona, while the greatest opportunities for energy development—and cost-effective energy resources—exist in Wyoming . Using the Transmission Expansion Planning Policy Committee’s (TEPPC) 2020 production simulation cases, load growth estimates within each state were developed . Peak demand in each state was assumed to grow at the same rate as load .

renewable demand

Renewable Portfolio Standard (RPS) is a legal requirement that exists in many states to promote renewable energy investment by mandating that a percentage of energy must come from renewable sources . RPS targets create a marketplace for renewable energy and change the mix of conventional and alternative resources used for power generation . HPX would provide an opportunity for states to pool renewable resources to meet portfolio standard goals, if desired .

The constraint of meeting RPS policies in each state will guide resource development over the next decade by encouraging substantial investments in new renewable energy . Because the major benefits of the HPX project

3The one exception is that E3 did not include Colorado’s 25% bonus for in-state renewable development.

35

stem from the opportunity to alter the conditions for renewable development in the West, the RPS policy assumptions are critical inputs to the ratepayer model . Each state’s RPS policy is uniquely codified in the Database of State Incentives for Renewables & Efficiency (DSIRE), and includes different requirements for different provider types . The total demand for renewables within each state is calculated by combining data on these RPS policies with the forecasts of statewide retail sales; each state’s demand, as calculated by a third party (E3 in this case), is shown in Table 8 .

cost of generation resources

Within the four states affected by HPX,

the cost to produce new power sources is unequal, and depends on resources available, as well as capital costs and regulations involved in startup and commissioning . At the time of the study, Busbar costs indicated that Wyoming wind is the least expensive of the renewable opportunities considered, while solar photovoltaics in the Desert Southwest were estimated to be approximately 2 .5 times as costly . This inequity is the key to realizing benefits via providing high-demand areas with access to less costly resources .

Table 9 shows the average cost of renewable technologies utilized for this evaluation . For most technologies,

these costs are based on the average cost of the corresponding cost in the Western Renewable Energy Zones (WREZ) Transmission Model . Adjustments to the WREZ average cost were made for two technologies where WREZ data was deemed insufficient . Distributed solar PV is assumed to be 20% higher than the capital cost of large-scale solar PV with a fixed axis . E3 developed a proxy for large-scale solar by blending solar thermal and large-scale solar PV . This cost is assumed to be 15% less than the average cost of solar thermal with wet cooling .

Table 10 lists the assumptions used for the cost of conventional generating technologies . It is assumed that all new

Arizona Colorado New

Mexico Wyoming

Net Energy to Load (GWh) 2008 84,155 62,293 23,280 11,880 2020 109,483 72,399 24,785 18,540 Growth Rate 2.2% 1.3% 0.5% 3.8%

Retail Sales (GWh)

2008 79,106 58,555 21,884 11,167 2020 102,914 68,055 23,297 17,428 2025 114,839 72,455 23,913 20,979 Growth Rate 2.2% 1.3% 0.5% 3.8%

Peak Demand (MW) 2008 19,428 11,603 4,075 1,753 2020 25,276 13,486 4,338 2,736 Growth Rate 2.2% 1.3% 0.5% 3.8%

taBlE 7

Load forecast assumptions within the HPX study area

36

Arizona Colorado New

Mexico Wyoming

IOU 9,451 12,684 3,237 672 Publics 6,478 1,254 -‐ -‐ Cooperative 646 1,717 483 333 Federal -‐ -‐ -‐ -‐ Facility -‐ -‐ -‐ -‐ Total RPS Requirement 16,575 15,655 3,720 1,005

Existing Resources 996 3,824 525 3,633 Total RPS Net Short 15,579 11,831 3,195 -‐

taBlE 10

Characterization of new conventional generating technologies in each state

taBlE 8

Renewable demand and RPS net short calculation in 2025 (GWh) .

taBlE 9

Average costs of new renewable technologies used in E3’s ratepayer model of HPX4

Capital Cost

($/kW)

Fixed O&M

($/kW-‐yr)

Variable O&M

($/MWh)

Heat Rate (Btu/kWh)

Biomass $4,354 $-‐ $33.69 15,000 Geothermal 6,321 -‐ 36.56 -‐ Distributed Solar PV 5,512 50.00 -‐ -‐ Large Scale Solar 4,414 66.00 -‐ -‐ Wind 2,453 60.00 -‐ -‐

Generator State Capital Cost ($/kW)

Fixed O&M

($/kW-‐yr)

Variable O&M

($/MWh) Heat Rate

Capacity Factor (%)

Gas CCGT Arizona $1,130 $10.57 $4.81 6,924 71.5% Gas CCGT Colorado 1,145 10.80 4.88 6,924 71.7% Gas CCGT New Mexico 1,124 10.49 4.79 6,924 66.5% Gas CCGT Wyoming 1,109 10.25 4.72 6,924 59.6% Gas CT Arizona 799 14.46 4.74 9,600 12.8% Gas CT Colorado 825 14.78 4.90 9,600 14.1% Gas CT New Mexico 790 14.35 4.69 9,600 10.8% Gas CT Wyoming 764 14.03 4.53 9,600 8.0%

4Participants understand that costs for these technologies have changed drastically in recent time, and will likely continue to be volatile in the future. Stage 3 efforts will closely monitor the relative costs of renewable technologies and the impacts those costs will have both on the benefit-cost and overall cost requirements of the HPX initiative.

37

conventional plants will be gas-fired combined cycle gas turbines (CCGTs) or simple cycle gas turbines (CTs) . The cost and performance assumptions vary by state and are summarized below .

E3 utilized a pro-forma financing model to calculate the levelized cost of each resource . It is assumed that the each resource cost is based on power purchase agreement (PPA) between an independent power producer and a utility . Key inputs to the financing model are summarized in Table 11 .

The pro-forma model calculates the levelized costs over the lifetime of the technology based on cost and performance of each technology . The generic all-in levelized costs for new technologies is summarized in Figure 8, page 37 .

fuel and electricity price assumptions

The forecast gas prices used in the ratepayer model to evaluate the potential benefits of HPX is based on a combination of NYMEX Henry Hub futures and a characterization of the western natural gas markets developed by the Northwest Power and Conservation Council (NWPCC) . The NWPCC models expected basis differentials from Henry Hub at major natural gas hubs throughout the WECC, which E3 uses to calculate the monthly cost of natural gas at various locations in 2020 . The burnertip cost of gas within each of the load bubbles is

calculated based on the monthly gas cost at the local trading hub, a local delivery charge (LDC) obtained from TEPPC, and any relevant excise taxes on gas within the state .

E3’s ratepayer model also includes a basic characterization of wholesale energy markets at various critical points in the WECC used to evaluate the cost of balancing load and resources . While Wyoming, Colorado, and New Mexico do not have a major liquid trading hub like Palo Verde in Arizona, E3 has developed estimates of the value of energy in each of the 24 time periods used in the model, which serves as a proxy for such a market . The market characterization relies upon historical data on spot market prices and gas prices at Palo Verde between 2006 and 2008; this data is used to estimate the average market heat rate at this hub during each of the 24 time periods .5 The product of these market heat rates and the forecasted monthly gas prices yields a reasonable estimate of average wholesale market prices at Palo Verde in 2020 .

rEsourcE aDDitions WitHout HPx

rPs resources

Without HPX, each state-utility will fill its RPS gap with locally available renewable resources . Each state’s renewable resource mix is based directly on projected resource builds developed by the TEPPC, which were based largely on published

utility resource plans for each region .

The plans reflect the availability and

relative quality of different renewable

technologies in the region, as well as the

nuances of each state’s RPS policy . For

instance, Arizona relies predominantly

on large-scale solar resources to meet

its goals, but its projected portfolio

includes a 30% set-aside for distributed

generation and a limited amount of local

wind and geothermal . At the other end

of the spectrum, Colorado’s portfolio

is dominated by the development of

high-quality wind . New Mexico’s portfolio

is the most balanced; its goals are met

by a combination of local solar and wind

resources . Table 12 summarizes the base

case assumptions for local resource

additions to meet each state’s RPS goals

without the large-scale interstate power-

sharing capabilities of HPX . The energy

and dependable capacity associated

with these renewable resources are

also assumed to contribute to each

state-utility’s required additions to meet

growth .

It should be noted that state-by-state

policies toward Renewable Energy Credits

(RECs) can significantly impact how the RPS

requirements are achieved in each state .

Stage 2 studies considered annual demand,

but aspects such as banking, in-state

development incentives, bundled delivery

and anything other than specific carve-

outs were not factored in at this stage .

5Electricity and gas spot market prices used to characterize the Palo Verde trading hub were obtained from the Intercontinental Exchange (ICE) Report Center: https://www.theice.com/marketdata/reports/ReportCenter.shtml.

38

Generic IPP Solar IPP

Financing Lifetime (yrs) 20 20 Debt Cost (%) 7.27% 7.27% Equity Cost (%) 15.29% 13.25% Equity Share (%) 40.00% 55.00% Federal Tax (%) 35.00% 35.00% State Tax (%) 8.84% 8.84% After-‐Tax Nominal WACC (%) 8.70% 9.23%

taBlE 11

Financing assumptions used to calculate the levelized costs of renewable and conventional generating technologies

figurE 8

Summary of all-in levelized costs of generic new resources in the HPX ratepayer model

taBlE 12

Base case resources added to meet RPS goals without HPX (GWh)

Generation (GWh) Installed Capacity (MW)

Arizona

Colorado New Mexico

Wyoming

Arizona

Colorado

New Mexico

Wyoming

WITHOUT HPX Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐ Distributed Solar PV 3,029 1,252 97 -‐ 1,533 637 48 -‐ Large Scale Solar 10,652 421 1,173 -‐ 4,466 207 499 -‐ Wind 1,711 9,559 2,022 -‐ 595 2,959 621 -‐ Gas CCGT 6,761 -‐ -‐ 6,762 1,080 -‐ -‐ 1,296

Gas CT 2,988 1,685 17 -‐ 2,664 1,369 18 -‐

39

Delivery Point

Arizona Colorado

New Mexico

Wyoming

Colorado 82% 0% 18% 0% New Mexico 100% 0% 0% 0%

Expo

rt

Zone

Wyoming 46% 44% 10% 0%

conventional resources

In addition to meeting RPS targets, each state must add new resources to keep pace with load growth: each state’s total new resources must provide enough energy to meet growth in demand and sufficient capacity to meet peak period demand plus each state’s planning reserve margin .6 Thus, any growth that is not met by new renewable resources must be met with a combination of combined-cycle (CCGT) and simple cycle (CT) gas turbines . CCGTs, which operate with a high capacity factor, are used to meet energy requirements, while CTs are built to meet any remaining capacity or reserve requirements . However, E3 models an interaction between the two: CCGTs provide reliable capacity as well as energy, while CTs will produce a small amount of energy to offset the requirement of CCGTs . This planning framework for the fossil build-out minimizes the fixed costs of new fossil resources required to maintain reliability .

rEsourcE aDDitions WitH HPx

rPs resources

The ratepayer analysis assumes that the construction of HPX would greatly expand the options for renewable development in the four states, enabling access to remote, high-quality renewable resources that could not be delivered over existing transmission . The set of additional resources considered for development is based on resource zones identified in the WREZ model . Individual ranking costs are calculated for each of the resources included in the non-HPX resource plans and the WREZ model; the least costly resources in the WREZ model are assumed to displace the highest cost resources in the non-HPX build, subject to the transmission capacity available along each segment of the HPX line . HPX would thus expand the supply curve of renewables from which portfolios in each state are constructed .

One key modeling assumption that affects the distribution of benefits among the four state-utilities is the allocation of renewable resources developed along HPX for RPS compliance accounting purposes . Should HPX development proceed, utilities along the line would contract with renewable developers to deliver energy and the associated renewable energy credits, allowing them to count those resources towards their individual RPS goals . For this analysis, E3 assumes that resources developed along the line would be divided among downstream states in direct proportion to each state’s renewable demand . For instance, claims to all resources in Wyoming are divided among Arizona (46%), Colorado (44%), and New Mexico (10%), while claims to resources in New Mexico are assigned exclusively to Arizona (shown in Table 13) . The capacity freed up by the delivery of high-quality renewables to various points on the line is used to export lower

taBlE 13

Allocation of renewable resources developed with HPX among the state-utilities

6The planning reserve margin is a reliability criterion that requires utilities to maintain excess capacity above its forecasted peak demand to account for potential grid contingencies and uncertainty in load forecasting. For the ratepayer analysis, E3 assumes each state-utility maintains a planning reserve margin of 17%.

40

taBlE 14

Base Case resources added to meet RPS goals with HPX

Generation (GWh) Installed Capacity (MW)

Arizona

Colorado New Mexico

Wyoming

Arizona

Colorado

New Mexico

Wyoming

PARALLEL SINGLE-‐CIRCUIT 500kv LINES Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐ Distributed Solar PV 3,029 1,252 97 -‐ 1,533 637 48 -‐ Large Scale Solar 1,193 421 1,173 -‐ 500 207 499 -‐ Wind -‐ 7,931 2,022 12,985 -‐ 2,455 621 3,500 Gas CCGT 5,228 -‐ -‐ 6,762 835 -‐ -‐ 1,296

Gas CT 5,237 1,715 23 -‐ 4,668 1,393 25 -‐

PARALLEL SINGLE-‐CIRCUIT 500kv LINES (PROGRESSIVE CONFIGURATION) Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐ Distributed Solar PV 3,029 1,252 97 -‐ 1,533 637 48 -‐ Large Scale Solar 1,193 421 1,173 -‐ 500 207 499 -‐

Wind -‐ 9,310 10,846 2,782 -‐ 2,882 3,371 750

Gas CCGT 5,029 -‐ -‐ 6,762 803 -‐ -‐ 1,296

Gas CT 5,244 1,696 19 -‐ 4,674 1,377 20 -‐

SINGLE-‐CIRCUIT 500kv LINE

Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐ Distributed Solar PV 3,029 1,252 97 -‐ 1,533 637 48 -‐ Large Scale Solar 4,160 421 1,173 -‐ 1,744 207 499 -‐ Wind 1,711 9,559 2,022 6,492 595 2,959 621 1,750 Gas CCGT 5,642 -‐ -‐ 6,762 901 -‐ -‐ 1,296

Gas CT 4,517 1,700 20 -‐ 4,026 1,381 21 -‐

SINGLE-‐CIRCUIT 500kv LINE (PROGRESSIVE CONFIGURATION) Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐ Distributed Solar PV 3,029 1,252 97 -‐ 1,533 637 48 -‐ Large Scale Solar 4,661 421 1,173 -‐ 1,954 207 499 -‐ Wind 1,711 9,559 5,231 2,782 595 2,959 1,621 750 Gas CCGT 5,717 -‐ -‐ 6,762 913 -‐ -‐ 1,296

Gas CT 4,393 1,696 19 -‐ 3,916 1,377 20 -‐

DOUBLE-‐CIRCUIT

41

quality local resources downstream

(e .g . Colorado off-takes Wyoming wind

and uploads Colorado wind for delivery

to Arizona) . This framework allows for

cascading benefits along the length of

the line without hindering renewable

development in Colorado and New

Mexico .

conventional resources

Once the renewable builds for each state

with the construction of HPX are set, the

model determines the appropriate build-

out of fossil resources . The methodology

for determining the required capacity

from new CTs and CCGTs is identical to

that described in the scenario without

HPX; however, because the renewable

mix in each state will have changed due

to the construction of HPX, the residual

gaps in energy and peak demand growth

will be different, and will require a

different fossil build-out than in the non-

HPX case .

sEnsitivity casEs

The value to ratepayers of constructing HPX is highly sensitive to a number of key modeling inputs, including but not limited to assumptions regarding specific resource cost and performance, demand for renewables, and federal policy regarding clean energy in the future . Many of these parameters are highly uncertain, and it is difficult to confidently predict the landscape for renewable development in the WECC by 2020 . E3

taBlE 14

Base Case resources added to meet RPS goals with HPX

SINGLE-‐CIRCUIT 500kv LINE (PROGRESSIVE CONFIGURATION) Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐

Distributed Solar PV 3,029 1,252 97 -‐

1,533 637 48 -‐

Large Scale Solar 4,661 421 1,173 -‐

1,954 207 499 -‐

Wind 1,711 9,559 5,231 2,782 595 2,959 1,621 750 Gas CCGT 5,717 -‐ -‐ 6,762 913 -‐ -‐ 1,296

Gas CT 4,393 1,696 19 -‐

3,916 1,377 20 -‐

DOUBLE-‐CIRCUIT 500kv LINE Biomass -‐ 30 324 -‐ -‐ 4 43 -‐ Geothermal -‐ 149 -‐ -‐ -‐ 19 -‐ -‐

Distributed Solar PV 3,029 1,252 97 -‐

1,533 637 48 -‐

Large Scale Solar 1,193 421 1,173 -‐ 500 207 499 -‐ Wind -‐ 7,931 2,022 12,985 -‐ 2,455 621 3,500 Gas CCGT 5,228 -‐ -‐ 6,762 835 -‐ -‐ 1,296

Gas CT 5,237 1,715 23 -‐

4,668 1,393 25 -‐

42

developed five sensitivity cases that show the effects of manipulating several assumptions to which the line’s value is most sensitive . This scenario analysis reveals the wide range of potential net benefits, both positive and negative, associated with the line .

case 1: Base case