Embed Size (px)

Citation preview

1

[Summary Translation]

HON HAI PRECISION INDUSTRY CO., LTD.

Stock Code: 2317

Annual General Shareholders’ Meeting For Year 2012

Meeting Handbook

June 18, 2012

2

HON HAI PRECISION INDUSTRY CO., LTD.

Annual Shareholders’ Meeting For Year 2012

Meeting Procedure

Time of Meeting: June 18, 2012 (Monday) at 9:00 am Location of Meeting: No.2 Zihyou Street, 5 Floor

Tucheng Industrial Park, Tucheng Dist., New Taipei City, Taiwan

I. To report the total number of shares represented in this AGM meeting II. To announce the commencement of meeting III. Chairman’s addresses IV. Items to be reported V. Matters to be acknowledged and discussed VI. Extraordinary Motions VII. Adjourned Meeting

3

HON HAI PRECISION INDUSTRY CO., LTD.

Regular Shareholders’ Meeting for Year 2012 Agenda

I. Chairman to announce the commencement of meeting.

II. Chairman’s report.

i. To report business of 2011.

ii. Statutory Auditors’ review of 2011 audited financial statements.

iii. Status Report of Company's indirect investment in Mainland China.

iv. Status Report of domestic corporate bond issuance

v. Report on the amendment of meeting norm for the Board of Directors

III. Matters to be acknowledged and discussed:

i. To acknowledge 2011 business operation report and 2011 audited financial

statements.

ii. To acknowledge the proposal for distribution of 2011 profits.

iii. To approve the new shares issuance for capital increase by earnings

re-capitalization.

iv. To approve the global depository receipts (“DR”s) issuance.

v. To amend the Company’s procedures for acquisition or disposal of assets.

vi. To amend the Company’s election policy of Directors and Supervisors.

vii. To amend the Company’s meeting norm of the shareholders' meeting.

viii. To amend the Company’s Articles of Incorporation.

ix. Issuance of new shares for restricted employee stocks

x. Issuance of employee stock options below market price

IV. Extraordinary Motions

V. Adjourned Meeting

4

Matters to be Reported:

Proposal One: Reporting the Company’s Business Operation Reports and Financial Statements for year 2011. Description: 1. Please refer to Appendix 1 for detailed Business Operation Reports. 2. Please refer to Appendix 3 for detailed financial statements.

5

Proposal Two: Please review Statutory Auditors’ review reports and the audited financial statements for the year ended 31 December 2011. Description: 1. Please refer to financial statements.

6

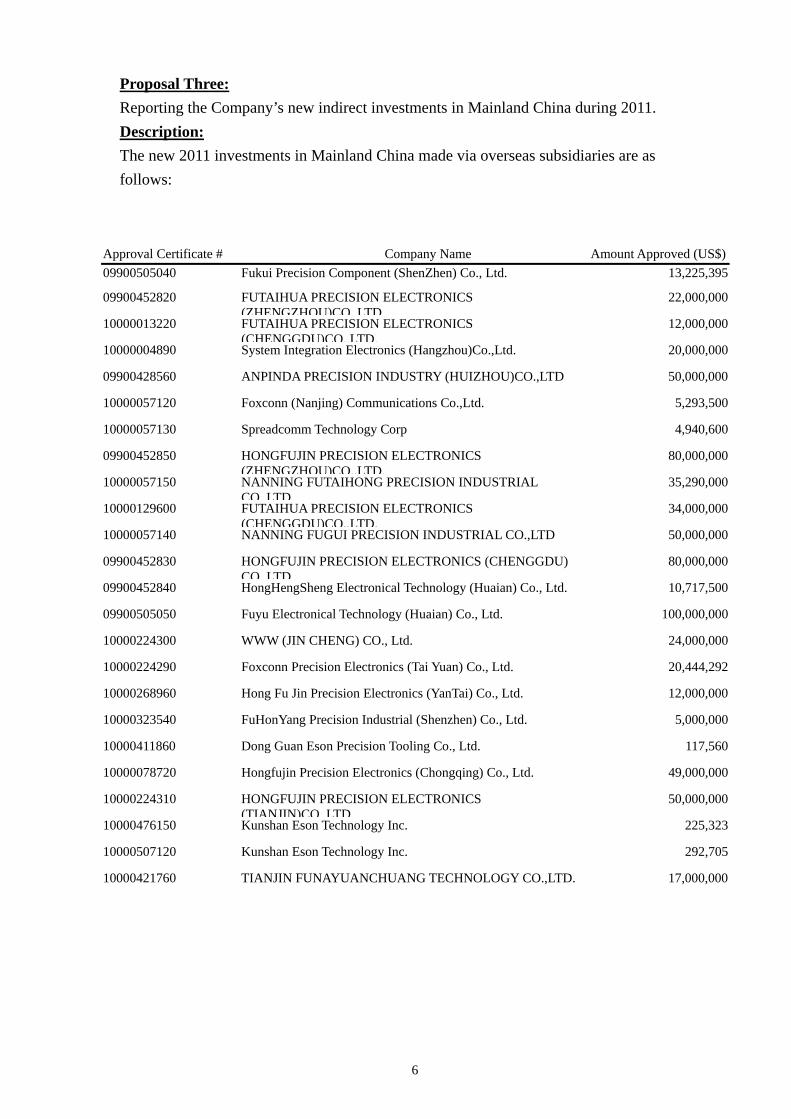

Proposal Three: Reporting the Company’s new indirect investments in Mainland China during 2011. Description: The new 2011 investments in Mainland China made via overseas subsidiaries are as follows:

Approval Certificate # Company Name

Amount Approved (US$)09900505040 Fukui Precision Component (ShenZhen) Co., Ltd. 13,225,395

09900452820 FUTAIHUA PRECISION ELECTRONICS (ZHENGZHOU)CO.,LTD.

22,000,000

10000013220 FUTAIHUA PRECISION ELECTRONICS (CHENGGDU)CO.,LTD.

12,000,000

10000004890 System Integration Electronics (Hangzhou)Co.,Ltd. 20,000,000

09900428560 ANPINDA PRECISION INDUSTRY (HUIZHOU)CO.,LTD 50,000,000

10000057120 Foxconn (Nanjing) Communications Co.,Ltd. 5,293,500

10000057130 Spreadcomm Technology Corp 4,940,600

09900452850 HONGFUJIN PRECISION ELECTRONICS (ZHENGZHOU)CO.,LTD.

80,000,000

10000057150 NANNING FUTAIHONG PRECISION INDUSTRIAL CO.,LTD

35,290,000

10000129600 FUTAIHUA PRECISION ELECTRONICS (CHENGGDU)CO.,LTD.

34,000,000

10000057140 NANNING FUGUI PRECISION INDUSTRIAL CO.,LTD 50,000,000

09900452830 HONGFUJIN PRECISION ELECTRONICS (CHENGGDU) CO.,LTD.

80,000,000

09900452840 HongHengSheng Electronical Technology (Huaian) Co., Ltd. 10,717,500

09900505050 Fuyu Electronical Technology (Huaian) Co., Ltd. 100,000,000

10000224300 WWW (JIN CHENG) CO., Ltd. 24,000,000

10000224290 Foxconn Precision Electronics (Tai Yuan) Co., Ltd. 20,444,292

10000268960 Hong Fu Jin Precision Electronics (YanTai) Co., Ltd. 12,000,000

10000323540 FuHonYang Precision Industrial (Shenzhen) Co., Ltd. 5,000,000

10000411860 Dong Guan Eson Precision Tooling Co., Ltd. 117,560

10000078720 Hongfujin Precision Electronics (Chongqing) Co., Ltd. 49,000,000

10000224310 HONGFUJIN PRECISION ELECTRONICS (TIANJIN)CO.,LTD.

50,000,000

10000476150 Kunshan Eson Technology Inc. 225,323

10000507120 Kunshan Eson Technology Inc. 292,705

10000421760 TIANJIN FUNAYUANCHUANG TECHNOLOGY CO.,LTD. 17,000,000

7

Proposal Four: Status Report of domestic corporate bond issuance. Description: 1. To fulfill the repayment of short-term debt, the Company, after obtaining the approval

from Financial Supervisory Commission of Executive Yuan dated January 7, 2011 with the FSC Approval Certification No. 0990073438 approving of total amount of NT$6.0 billions domestic unsecured corporate bond. (1) Conditions of Issue:

(i) Total Amount of Issue: NT$6 billions (ii) Issue Period: 2011.03.08 ~ 2016.03.08 (iii) Face Value: NT$1,000,000 (iv) Issue Price: NT$100 (At Par) (v) Issue Coupon/Interest Rate: fixed interest rate at 1.47% per anuum (vi) Repayment of Principal: By end of forth and fifth year since the issuing date,

repay 50% of principal. (vii) Distribution of Interest: Since the issuing date, based on the coupon rate

distributing interest once a year with simple interest-bearing. (viii)The Trustee: SinoPac Bank Co., Ltd. (ix) Debt Service Agency: The central downtown branch of the SinoPac Bank.

(2) The Company’s domestic unsecured corporate bonds traded in GreTai Securities Market since the issuing date.

(3) Abovementioned amount of fund raising is fully executed in Q1 2011. 2. To fulfill the repayment of short-term debt,, the Company, after obtaining the approval

from Financial Supervisory Commission of Executive Yuan dated June 1, 2011 with the FSC Approval Certification No. 1000025473 approving of total amount of NT$7.05 billions domestic unsecured corporate bond. (1) Conditions of Issue:

(i) Total Amount of Issue: Coupon A: NT$3 billions, Coupon B: NT$2.65 billions, Coupon C: NT$1.4 billions

(ii) Issue Period: Coupon A: 5-year period, Coupon B: 7-year period, Coupon C: 10-year period

(iii) Face Value: NT$1,000,000 (iv) Issue Price: NT$100 (At Par) (v) Issue Coupon/Interest Rate: fixed interest rate at Coupon A:1.43%, Coupon B:

1.66%, Coupon C: 1.82% per anuum (vi) Repayment of Principal: 100% principal repay upon maturity. (vii) Distribution of Interest: Since the issuing date, based on the coupon rate

distributing interest once a year with simple interest-bearing. (viii) The Trustee: SinoPac Bank Co., Ltd. (ix) Debt Service Agency: The central downtown branch of the SinoPac Bank.

(2) The Company’s domestic unsecured corporate bonds traded in GreTai Securities

8

Market since the issuing date. (3) Abovementioned amount of fund raising is fully executed in Q2 2011.

3. To fulfill the repayment of short-term debt, the Company, after obtaining the approval from Financial Supervisory Commission of Executive Yuan dated July 18, 2011 with the FSC Approval Certification No. 1000031227 approving of total amount of NT$4.95 billions domestic unsecured corporate bond. (1) Conditions of Issue:

(i) Total Amount of Issue: NT$4.95 billions (ii) Issue Period: 2011.07.18 ~ 2016.07.18 (iii) Face Value: NT$1,000,000 (iv) Issue Price: NT$100 (At Par) (v) Issue Coupon/Interest Rate: fixed interest rate at 1.51% per anuum (vi) Repayment of Principal: 100% principal repay upon maturity. (vii) Distribution of Interest: Since the issuing date, based on the coupon rate

distributing interest once a year with simple interest-bearing. (viii) The Trustee: SinoPac Bank Co., Ltd. (ix) Debt Service Agency: The central downtown branch of the SinoPac Bank.

(2) The Company’s domestic unsecured corporate bonds traded in GreTai Securities Market since the issuing date.

(3) Abovementioned amount of fund raising is fully executed in Q1 2012.

9

Proposal Five: Please review the report on the amendment of meeting norm for the Board of Directors. Description: In accordance with the laws and regulations, the Company is proposed to the amendment of meeting norm for the Board of Directors. Please refer to Appendix IV for the comparison table of the amended and the original articles.

10

Motions for Acknowledgement and Discussion (Proposed by the Board of Directors, “BoD”)

Motion 1: The operation performance reports and financial statements of the Company in 2011 have been completed and submitted. Please acknowledge.

Descriptions: The operation performance reports and financial statements of the Company in 2011 have been approved by BoD, and have also been reviewed and audited by Supervisors. Please refer to Appendix 1 and Appendix 3 for the Books mentioned as above.

Resolution:

11

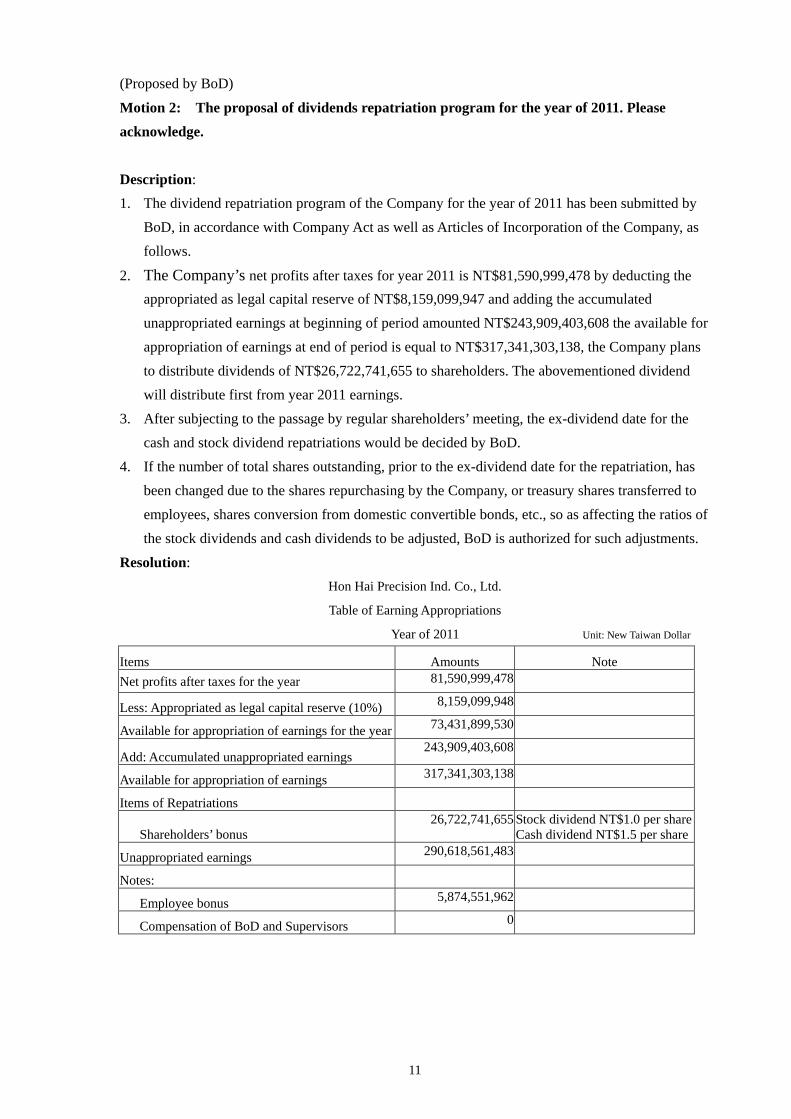

(Proposed by BoD)

Motion 2: The proposal of dividends repatriation program for the year of 2011. Please acknowledge.

Description: 1. The dividend repatriation program of the Company for the year of 2011 has been submitted by

BoD, in accordance with Company Act as well as Articles of Incorporation of the Company, as follows.

2. The Company’s net profits after taxes for year 2011 is NT$81,590,999,478 by deducting the appropriated as legal capital reserve of NT$8,159,099,947 and adding the accumulated unappropriated earnings at beginning of period amounted NT$243,909,403,608 the available for appropriation of earnings at end of period is equal to NT$317,341,303,138, the Company plans to distribute dividends of NT$26,722,741,655 to shareholders. The abovementioned dividend will distribute first from year 2011 earnings.

3. After subjecting to the passage by regular shareholders’ meeting, the ex-dividend date for the cash and stock dividend repatriations would be decided by BoD.

4. If the number of total shares outstanding, prior to the ex-dividend date for the repatriation, has been changed due to the shares repurchasing by the Company, or treasury shares transferred to employees, shares conversion from domestic convertible bonds, etc., so as affecting the ratios of the stock dividends and cash dividends to be adjusted, BoD is authorized for such adjustments.

Resolution: Hon Hai Precision Ind. Co., Ltd.

Table of Earning Appropriations

Year of 2011 Unit: New Taiwan Dollar

Items Amounts Note Net profits after taxes for the year 81,590,999,478

Less: Appropriated as legal capital reserve (10%) 8,159,099,948 Available for appropriation of earnings for the year 73,431,899,530

Add: Accumulated unappropriated earnings 243,909,403,608

Available for appropriation of earnings 317,341,303,138

Items of Repatriations

Shareholders’ bonus 26,722,741,655 Stock dividend NT$1.0 per share

Cash dividend NT$1.5 per share

Unappropriated earnings 290,618,561,483 Notes:

Employee bonus 5,874,551,962 Compensation of BoD and Supervisors 0

12

(Proposed by BoD)

Motion 3: Proposal of capital increase from retained earnings. Please review and discuss. Description: In order to expand the manufacturing capacity, it’s to propose to have capital increase from retained earnings as well as employees’ bonus to issue new shares.

1. Capital increase from retained earnings: The company considers the demand of future business development, it’s to propose to have capital increase from retained earnings as well as employees’ bonus to issue new shares. Appropriated from shareholders’ bonus of NT$10,689,096,660 to issue 1,068,909,666 new shares; while employees’ bonus of NT$5,874,551,962.

2. The conditions of the new share issuance: (1) According to the proposed capital increase plan, 100 common shares will be repatriated

for every 1,000 common shares for free, except for the part of employees’ stock bonus, recorded in the shareholders’ books and calculated as their shares held on the ex-dividend date. The number of shares repatriated to each shareholder for less one share will be purchased by the welfare committee of the Company in par value as calculated to the rounding of New Taiwan Dollar.

(2) The number of shares issued to employees will be the closing price of the previous day of shareholders’ meeting, also need to consider the impact of ex-dividend as the basis for the calculation, it should be distributed in cash to employees for the portion of less than one share after the calculation.

(3) The new shares issuance by the capital increase will carry the same rights and obligations as the current outstanding shares.

(4) The repatriation of employees’ bonus will be in accordance with the employees’ bonus policy of the Company.

(5) The ex-dividend date will be decided by the Board of Directors meeting after the regulators’ approval.

(6) If the number of total shares outstanding, prior to the ex-dividend date for the repatriation, has been changed due to the shares repurchasing by the Company, or treasury shares transferred to employees, shares conversion from the convertible bonds, etc., so as affecting the ratios of the stock dividends to be adjusted, BoD is authorized for such adjustments.

(7) BoD is authorized for any necessary amendments of the capital increase plan due to the needs of actual practices or by the instructions of regulators’ authorities.

Resolution:

13

(Proposed by BoD)

Motion 4: Propose to conduct a capital increase from cash, by means of common shares issuance to participate Global Depositary Receipts (“GDRs”) offerings.

Description: 1. In order to raise funds to support future developments of the Company (include but not

limited to capacity expansion, overseas procurement, long-term investment, debt repayment), as well as to raise capitals by ways of internationalized and diversified, it’s to propose to shareholders’ meeting for the authorization to BoD to increase capitals from cash by means of common shares issuance to participate GDRs offerings.

2. The offerings of GDRs should be in compliance with the following rules, by authorizing BoD to handle the related matters: (1) The newly issued common shares by the capital increase from cash to participate GDRs

offering would not be exceeded 1.1 billion shares. (2) The offering price will be referred to the market price of the common shares at offering;

while the decision of the final offering price will be authorized to Chairman of the Board in discussion with securities underwriters in accordance with market condition at offering. The “market price of the common share at offering” would be referred to and calculated, in accordance with capital market practices and by the agreement between the Company and underwriters, either the close price of the common shares on the pricing date of the GDRs offering, or the average close price of those in certain period prior to the offerings.

(3) Besides the 10% of those reserved for the Company employees’ subscriptions by the Article 267 of the Company Act, the remaining 90% of the newly issued common shares would be proposed to Shareholders’ meeting, by Article 28-1 of the Securities and Exchange Law, for public offering to become the original shares for the GDRs offering. The unsubscribed portion of the reserved shares for employees is authorized Chairman for delegated parties to subscribe or to be participated as the original shares on the GDRs

(4) The offering details for the capital increase from cash, by means of common shares issuance to participate GDRs offering, including the offering price, number of shares (or quota) to be issued, terms and conditions, uses of proceed, amount to be raised, the offering schedule and possible effects, as well as other related offering procedures, are authorized to BoD for the arrangements and modifications according to market conditions. It’s also fully authorized to Chairman for any necessary amendments pursuant to the opinions from regulator authorities or due to the changes from operating valuation or market conditions.

(5) To comply with the capital increase from cash, by means of common shares issuance to

14

participate GDRs offering, it’s to authorize Chairman or other designated persons by Chairman to represent the Company to sign for all of the related documents as well as handling the related matters.

3. The offering price of the issuance should be fair as referred to the market practices and related regulations. In addition, the proposed capital increase from cash by means of new common shares will be issued for up to 1.1 billion, which accounts for 9.4% of the total shares outstanding of the Company. It would not substantially diluted for the shares of the original shareholders, so as not having major impact on the shareholding rights of them.

Resolution:

15

(Proposed by BoD)

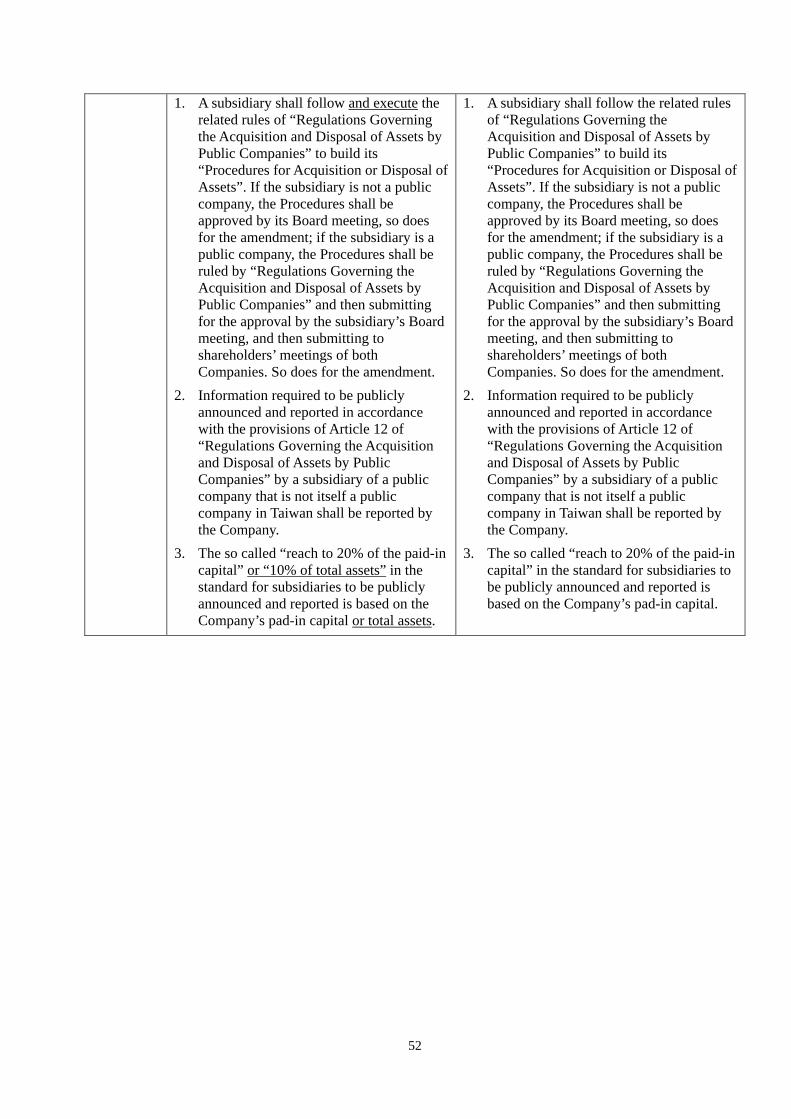

Motion 5: Amend the Procedures for Acquisition or Disposal of Assets of the Company. Please review and discuss.

Description: In accordance with the laws and regulations, the Company is proposed to the amendment of Procedures for Acquisition or Disposal of Assets. Please refer to Appendix V for the comparison table of the amended and the original articles.

Resolution:

16

(Proposed by BoD)

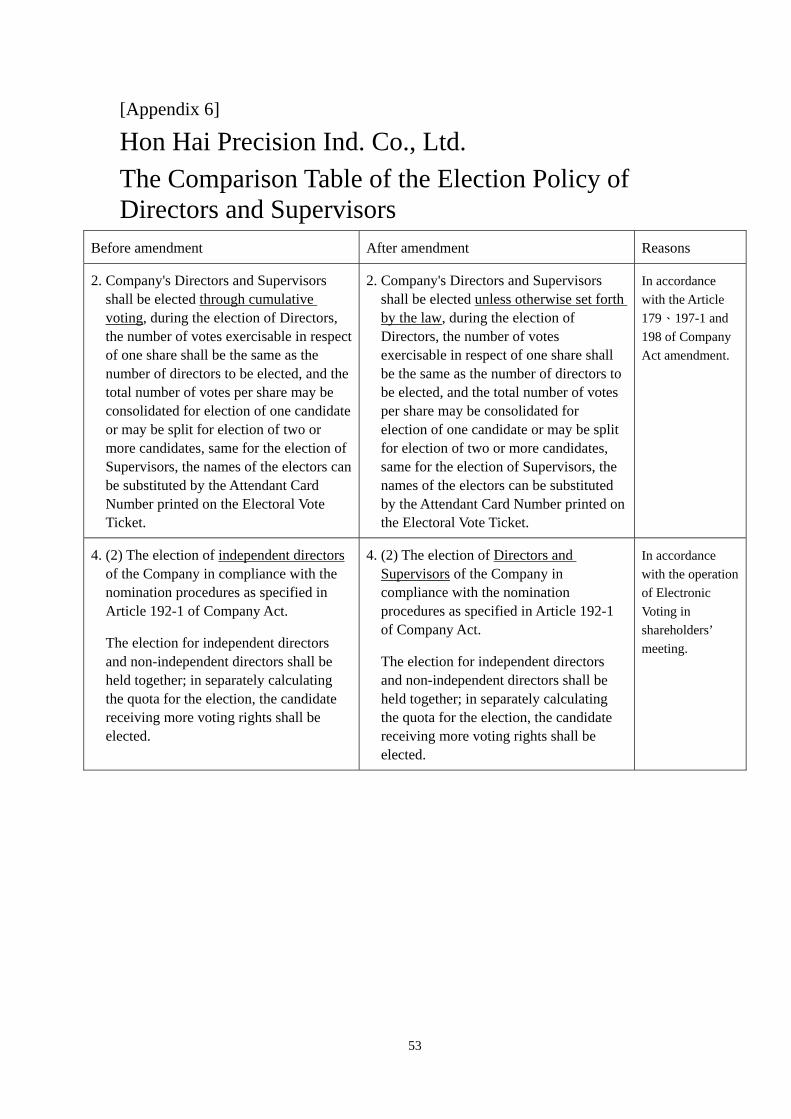

Motion 6: Amend the Election Policy of Directors and Supervisors of the Company. Please review and discuss.

Description: In accordance with the laws and regulations, the Company is proposed to the amendment of Election Policy of Directors and Supervisors. Please refer to Appendix VI for the comparison table of the amended and the original articles.

Resolution:

17

(Proposed by BoD)

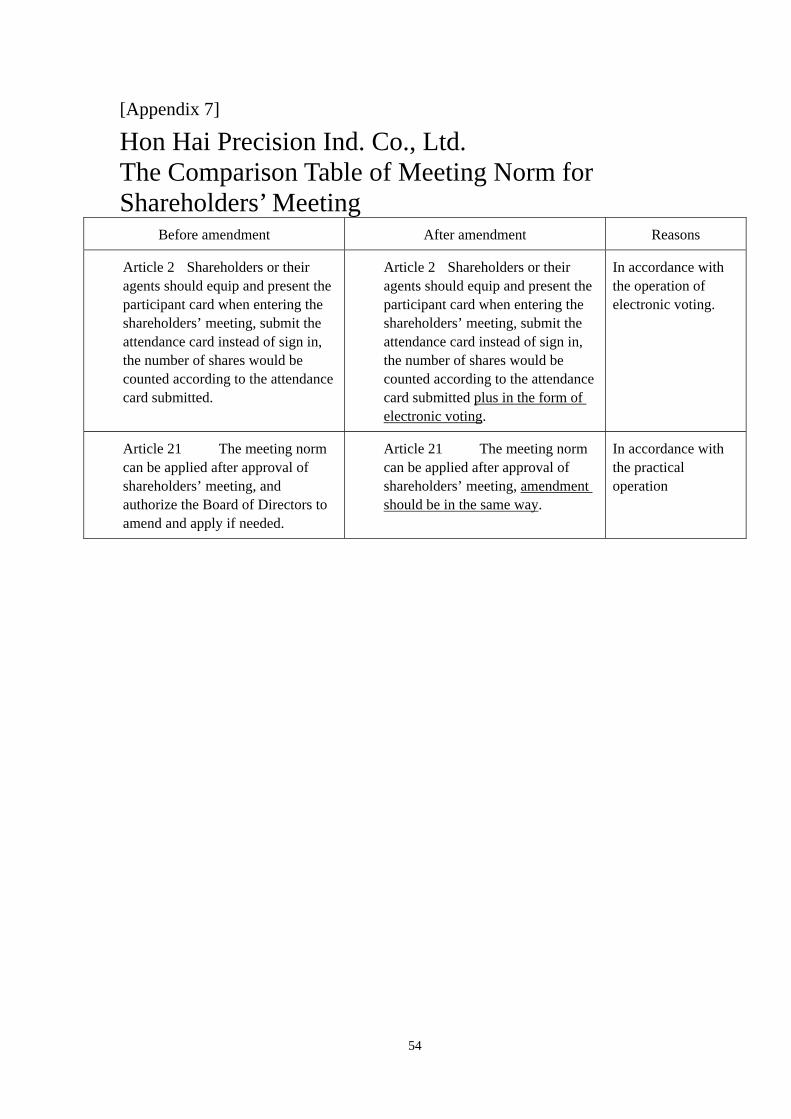

Motion 7: Amend the Meeting Norm of Shareholders’ Meeting of the Company. Please review and discuss.

Description: The Company is proposed to the amendment of Meeting Norm of Shareholders’ Meeting. Please refer to Appendix VII for the comparison table of the amended and the original articles.

Resolution:

18

(Proposed by BoD)

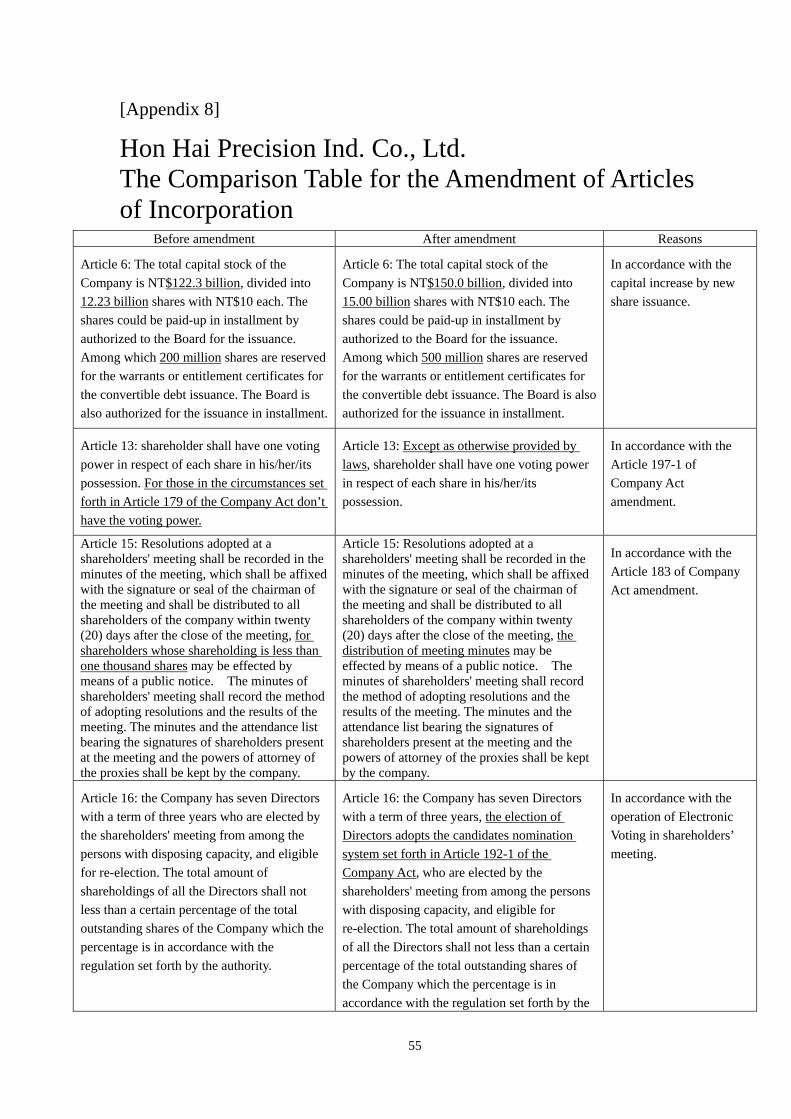

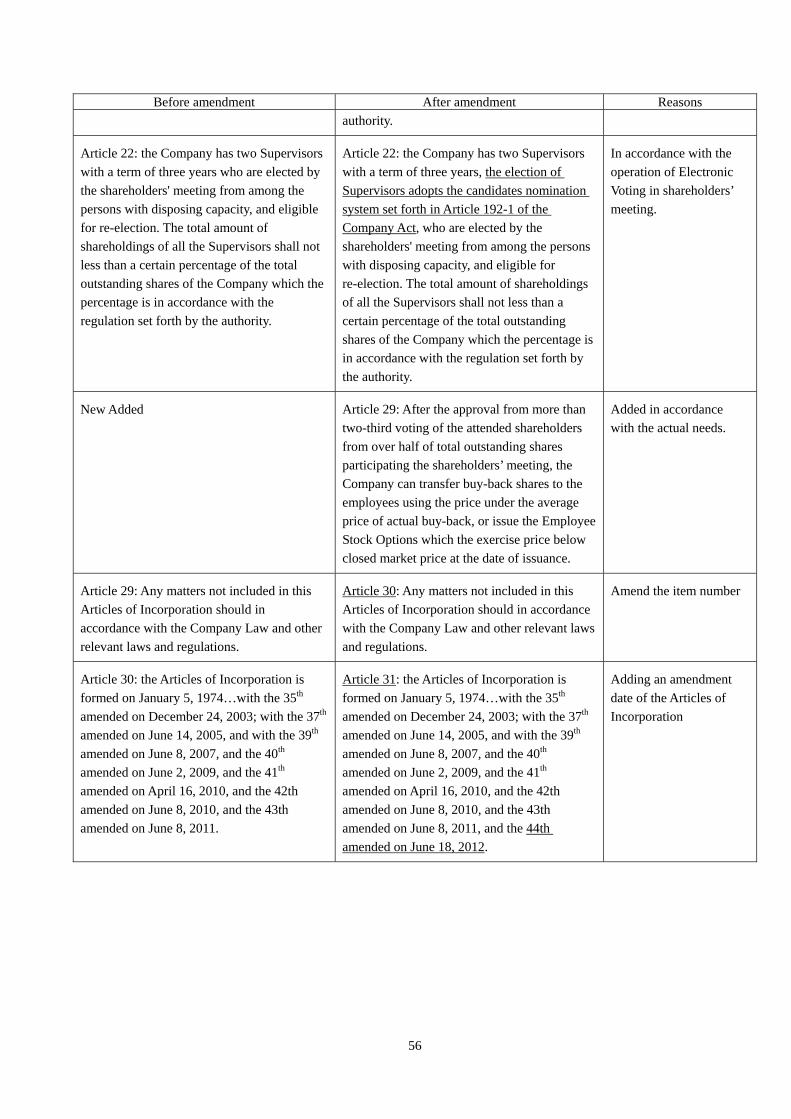

Motion 8: Amend the Articles of Incorporation of the Company. Please review and discuss.

Description: To meet the operation needs and in compliance with the Company Law, it’s to propose to amend certain articles of the Articles of Incorporation. Please refer to Appendix VIII for the comparison table of the amended and the original articles.

Resolution:

19

(Proposed by BoD)

Motion 9: Issuance of new shares for restricted employee stocks. Please review and discuss.

Description: 1. It’s to propose to issue new shares for restricted employee stocks in accordance with the

relevant regulations from Article 267 of Company Law and “Regulations Governing the Offering and Issuance of Securities by Securities Issuers” issued by Financial Supervisory Commission of Executive Yuan.

2. Would like to explain in accordance with the provisions of Article 60-2 of “Regulations Governing the Offering and Issuance of Securities by Securities Issuers” as follows: (1) Expected total amounts (shares) of issuance: 213,781,000 shares, NT$10 per share, with

total amounts of NT$2,137,810,000 ( limited to less than 2% of the company's total outstanding common shares).

(2) Determination of the terms and conditions: i. Price to issue: Can issue free allotment to employees, or in the price of less than

50% of market closed price of one day prior to the date of issuance. ii. Conditions to grant: Conform with the seniority and annual performance evaluation

standard set forth on the company's chapters of restricted employee stock issuance. iii. The handling for the employees not achieving to the conditions to grant: The

company will take back or buy back the issued rights and then cancel if employees not achieving to the conditions to grant.

(3) Qualification requirements for employees: i. Should be the full-time employees with certain performance.

ii. The seniority, rank, job performance, overall contribution, special achievements or other consideration shall refer to the company's chapters of issuance of restricted employee stock within the Decree of Act.

iii. Any single employee to be granted shall not exceed 10% of the total shares of restricted employee stock issuance.

(4) Cause of occurrence: Attracting, retaining and increasing the cohesion and sense of belonging of employees to increase the competitiveness of the company and create the common interests for shareholders and the company.

(5) Possible expenses, dilution of EPS and other matters impacting shareholders’ equity: i. Calculation of possible expenses: If based on the market closed price in April 23,

2012 and consider the actuarial assumptions for the estimate, then the annual amortized expenses from 2012 to 2016 will be projected as NT$2,302,080,730, NT$4,604,161,460, NT$4,604,161,460, NT$3,635,980,200 and NT$245,848,150 respectively with the total amounts of NT$15,392,232,000.

ii. Dilution of EPS: If based on the market closed price in April 23, 2012, then the

20

earning dilution from 2012 to 2016 will be projected as NT$0.215, NT$0.431, NT$0.431, NT$0.340 and NT$0.023 respectively.

(6) Other important agreed matters: The new issuance of restricted employee stock can be custody under the form of stock trust.

3. After the issuance of this plan which Board of Directors has been authorized to issue, shall declare to the Authority in accordance with the regulation.

4. If otherwise set forth by the regulations, if this plan has something left over will authorize Board of Directors or who being authorized to amend or execute in accordance with the regulations.

Resolution:

21

(Proposed by BoD)

Motion 10: Issuance of Employee Stock Options below market price. Please review and discuss.

Description: 1. It’s to propose to issue Employee Stock Options below market price in accordance with the

relevant regulations from Article 28-3 of Securities and Exchange Act and “Regulations Governing the Offering and Issuance of Securities by Securities Issuers” issued by Financial Supervisory Commission.

2. Would like to explain in accordance with the provisions of Article 56-1 of “Regulations Governing the Offering and Issuance of Securities by Securities Issuers” as follows: (1) Number of total issued units of the employee stock option certificates, number of shares

each unit represents, total number of new shares to be issued due to exercise of stock option: It’s propose to 213,781 units which the number of shares each unit represents is 1,000 shares. It’s limit to 2% of the total outstanding common shares for the issuance of this Plan of Employee Stock Options, namely should not over 213,781,000 shares.

(2) The principal and reasonableness of the exercise prices: Consideration of the selection, retention and incentive purposes as well as taking into account the shareholders' interests, it is propose to set the exercise price not less than the 50% of closed market price at the date issuing this Employee Stock Options; furthermore, the options can not be exercised within 2 years after the issuing date, and it’s reasonable due to the exercise price is to set not less than 50% of the market closed price.

(3) Conditions of eligibility for subscription rights: i. Eligible to grant the employee stock options only for those who are the full-time

employees of the company or subsidiaries with certain performance required ii. The seniority, rank, job performance, overall contribution, special achievements or

other consideration shall refer to the company's chapters of issuance of employee stock options within the Decree of Act. Any single employee to be granted shall not exceed 10% of the total shares of employee stock options issuance.

(4) Cause of occurrence: Consideration of the selection, retention and incentive purposes for those professionals the Company needed, and raising the cohesion and sense of belonging in order to increase the company’s competence, as well as taking into account the shareholders' interests.

(5) The matters impacting shareholders’ equity: i. Calculation of possible expenses: If based on the market closed price in April 23,

2012 and consider the actuarial assumptions for the estimate, then the annual amortized expenses from 2012 to 2015 will be NT$2,992,934,000, the total amounts will be NT$11,971,736,000.

22

ii. Dilution of EPS: If based on the market closed price in April 23, 2012, then the annual earning dilution from 2012 to 2015 will be NT$0.28 , and total of NT$1.12 in 4 years..

3. After the issuance of this plan which Board of Directors has been authorized to issue, shall declare to the Authority in accordance with the regulation.

4. If otherwise set forth by the regulations, if this plan has something left over will authorize Board of Directors or who being authorized to amend or execute in accordance with the regulations.

Resolution:

23

Other Business or Special Motion

29

[Appendix 1]

2011 Business Report The business of 2011 is reported as follows:

1. The operating results of 2011 are described as below:

The Company has delivered another excellent performance, and for another record year on the revenues and net profits. The consolidated net revenues of 2011 was NT$3.452 trillion, compared with NT$2.997 trillion in 2010, by increase of NT$455.0 billion, a 15.2% YoY growth. The net profit was NT$81.590 billion in 2011, compared with NT$77.154 billion in 2010, for a 5.7% YoY increase.

2. The review of 2011 and the outlook for 2012

Last year was once again a year with unprecedented challenges, through the tremendous efforts of all my colleagues, we are pleased to report to you that we have accomplished many impossible tasks. Not only hereby the Inner China expansion for a large-scale alignment of operational deployment to rapid response the changes in the operating environment and establish cornerstone for the Company’s long-term development, but also our management team was able to score in such great changes of industry dynamic by taking into account the technology development as well as customer and market demand, resulting the consolidated revenue and profit of year 2011 were both record high!

The Governments in the world join forces to save the market after the financial tsunami in 2008, all looking forward the opportunity for slow recovery of the economy, but natural and man-made disasters uninterrupted happened, the world was forced to face reality again. Last year, the 9-magnitude earthquake in Japanese and the worst flooding since last 50 years in Thailand caused huge impact to supply chains of various industries in the world; countries in Europe and the United States have staged the drama of living beyond resulted of the intensified sovereign debt problems in Europe alone with the global stock market crash due to U.S. government bond credit has been de-rated leaving the already fragile global economy continued to add more unpredictable variables.

Regardless of the troubled year, the Company continues to demonstrate the formidable corporate competitiveness, in addition to record high financial results, we also quickly grasp the opportunities from the structural changes of the global economic environment. Based on the model of “Muster and Alliance” by expediting the investment in technology and invitation in talents to be the joint force in the Company’s global platform to meet the new opportunities of the industry changes. Furthermore, the remarkable achievement of the Company is again attract the global attention, the ranking in Fortune Magazine’s "Global 500" moved up to No. 60 in 2011; moreover, the Company granted 1,514 U.S. patents in 2011 and ranked No. 9 in U.S. patent ranking which is the only Chinese company in the list that illustrates how much efforts the Company has dedicated in research and development!

Looking to year 2012, the Company will continue to develop much deeper and trusted strategic partner relationship among those global leading brand customers based on its eCMMS platform and channel service extension, at same time, the Company demonstrates the commitment to corporate social responsibility and build a harmonious society through massive increase of wages alone with lower down the overtime hours for workers. The overall business cycle is still in a highly uncertain, all industries, especially manufacturing industry, must be prepared to face another challenging year, but we believe that under the untiring efforts of all my colleagues, we are confident in break through all difficulties and challenges and bring greater value for you!

Finally I would like to reiterate on behalf of all shareholders, to all the families of staff and staff on the most sincere thanks. And wish the management team continue to work hard to maintain superior operating results. Thanks.

30

[Appendix 2]

The Audited Report by Supervisors

The financial statements and business report have been audited by us as Supervisors of the Company. We deem no inappropriateness on these documents. In accordance with Article 219 of the Company Law, hereto we present for the audited report. Please review.

Submitted to:

2012 Regular Shareholders’ Meeting of the Company

Hon Hai Precision Ind. Co., Ltd.

Supervisor: Qing-Yuan Huang

On the Date of March 29th, 2012

31

The Audited Report by Supervisors

The profit distribution table has been audited by us as Supervisors of the Company. We deem no inappropriateness on these documents. In accordance with Article 219 of the Company Law, hereto we present for the audited report. Please review.

Submitted to:

2012 Regular Shareholders’ Meeting of the Company

Hon Hai Precision Ind. Co., Ltd.

Supervisor: Representative: Qing-Yuan Huang

On the Date of April 29th, 2012

32

The Audited Report by Supervisors

The financial statements and business report have been audited by us as Supervisors of the Company. We deem no inappropriateness on these documents. In accordance with Article 219 of the Company Law, hereto we present for the audited report. Please review.

Submitted to:

2012 Regular Shareholders’ Meeting of the Company

Hon Hai Precision Ind. Co., Ltd.

Supervisor: Fu-Rui International Investment Co., Ltd.

Representative: Wan Jui-Hsia

On the Date of March 29th, 2012

33

The Audited Report by Supervisors

The profit distribution table has been audited by us as Supervisors of the Company. We deem no inappropriateness on these documents. In accordance with Article 219 of the Company Law, hereto we present for the audited report. Please review.

Submitted to:

2012 Regular Shareholders’ Meeting of the Company

Hon Hai Precision Ind. Co., Ltd.

Supervisor: Fu-Rui International Investment Co., Ltd.

Representative: Wan Jui-Hsia

On the Date of March 29th, 2012

34

[Appendix 3]

Audited Reports by CPA and Financial Statements

35

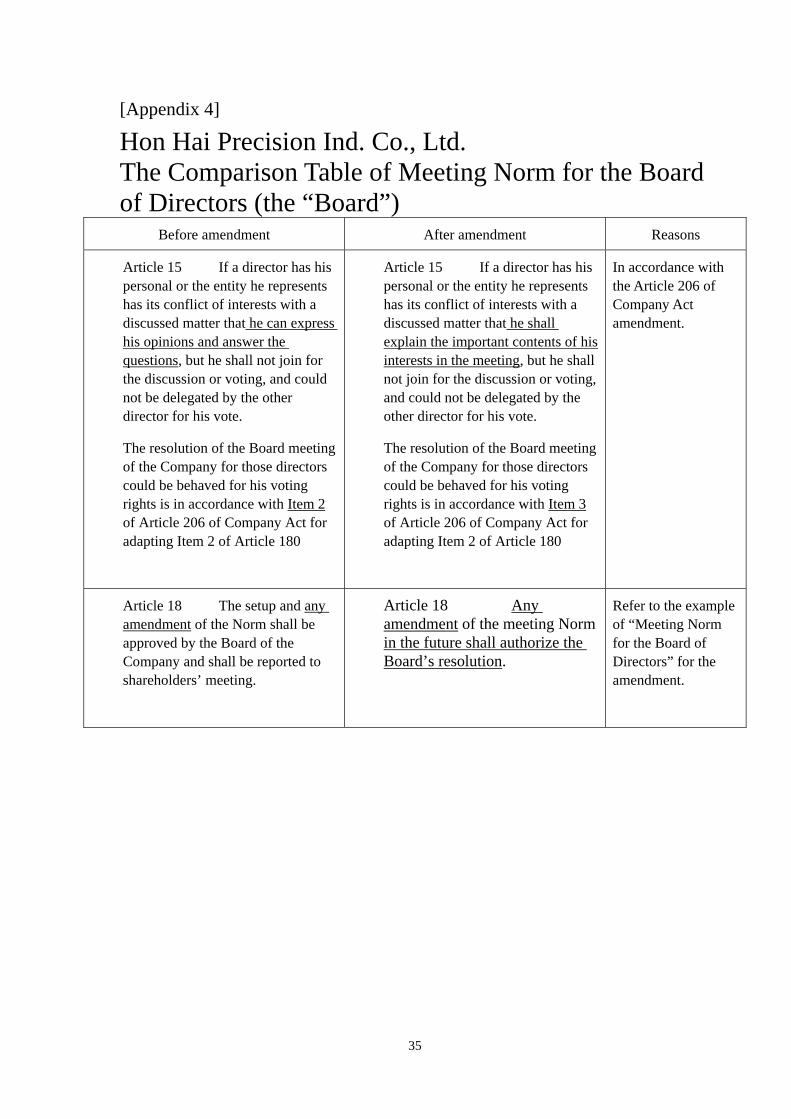

[Appendix 4]

Hon Hai Precision Ind. Co., Ltd. The Comparison Table of Meeting Norm for the Board of Directors (the “Board”)

Before amendment After amendment Reasons

Article 15 If a director has his personal or the entity he represents has its conflict of interests with a discussed matter that he can express his opinions and answer the questions, but he shall not join for the discussion or voting, and could not be delegated by the other director for his vote.

The resolution of the Board meeting of the Company for those directors could be behaved for his voting rights is in accordance with Item 2 of Article 206 of Company Act for adapting Item 2 of Article 180

Article 15 If a director has his personal or the entity he represents has its conflict of interests with a discussed matter that he shall explain the important contents of his interests in the meeting, but he shall not join for the discussion or voting, and could not be delegated by the other director for his vote.

The resolution of the Board meeting of the Company for those directors could be behaved for his voting rights is in accordance with Item 3 of Article 206 of Company Act for adapting Item 2 of Article 180

In accordance with the Article 206 of Company Act amendment.

Article 18 The setup and any amendment of the Norm shall be approved by the Board of the Company and shall be reported to shareholders’ meeting.

Article 18 Any amendment of the meeting Norm in the future shall authorize the Board’s resolution.

Refer to the example of “Meeting Norm for the Board of Directors” for the amendment.

36

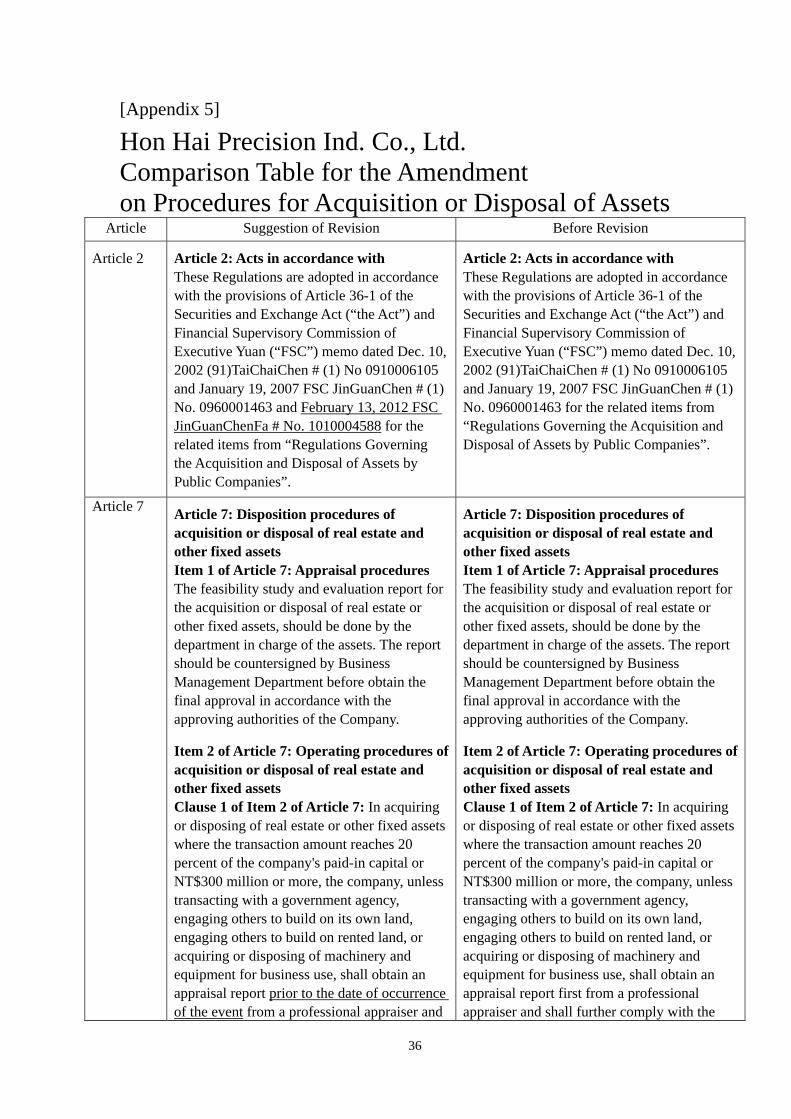

[Appendix 5]

Hon Hai Precision Ind. Co., Ltd. Comparison Table for the Amendment on Procedures for Acquisition or Disposal of Assets

Article Suggestion of Revision Before Revision

Article 2 Article 2: Acts in accordance with These Regulations are adopted in accordance with the provisions of Article 36-1 of the Securities and Exchange Act (“the Act”) and Financial Supervisory Commission of Executive Yuan (“FSC”) memo dated Dec. 10, 2002 (91)TaiChaiChen # (1) No 0910006105 and January 19, 2007 FSC JinGuanChen # (1) No. 0960001463 and February 13, 2012 FSC JinGuanChenFa # No. 1010004588 for the related items from “Regulations Governing the Acquisition and Disposal of Assets by Public Companies”.

Article 2: Acts in accordance with These Regulations are adopted in accordance with the provisions of Article 36-1 of the Securities and Exchange Act (“the Act”) and Financial Supervisory Commission of Executive Yuan (“FSC”) memo dated Dec. 10, 2002 (91)TaiChaiChen # (1) No 0910006105 and January 19, 2007 FSC JinGuanChen # (1) No. 0960001463 for the related items from “Regulations Governing the Acquisition and Disposal of Assets by Public Companies”.

Article 7 Article 7: Disposition procedures of acquisition or disposal of real estate and other fixed assets Item 1 of Article 7: Appraisal procedures The feasibility study and evaluation report for the acquisition or disposal of real estate or other fixed assets, should be done by the department in charge of the assets. The report should be countersigned by Business Management Department before obtain the final approval in accordance with the approving authorities of the Company.

Item 2 of Article 7: Operating procedures of acquisition or disposal of real estate and other fixed assets Clause 1 of Item 2 of Article 7: In acquiring or disposing of real estate or other fixed assets where the transaction amount reaches 20 percent of the company's paid-in capital or NT$300 million or more, the company, unless transacting with a government agency, engaging others to build on its own land, engaging others to build on rented land, or acquiring or disposing of machinery and equipment for business use, shall obtain an appraisal report prior to the date of occurrence of the event from a professional appraiser and

Article 7: Disposition procedures of acquisition or disposal of real estate and other fixed assets Item 1 of Article 7: Appraisal procedures The feasibility study and evaluation report for the acquisition or disposal of real estate or other fixed assets, should be done by the department in charge of the assets. The report should be countersigned by Business Management Department before obtain the final approval in accordance with the approving authorities of the Company.

Item 2 of Article 7: Operating procedures of acquisition or disposal of real estate and other fixed assets Clause 1 of Item 2 of Article 7: In acquiring or disposing of real estate or other fixed assets where the transaction amount reaches 20 percent of the company's paid-in capital or NT$300 million or more, the company, unless transacting with a government agency, engaging others to build on its own land, engaging others to build on rented land, or acquiring or disposing of machinery and equipment for business use, shall obtain an appraisal report first from a professional appraiser and shall further comply with the

37

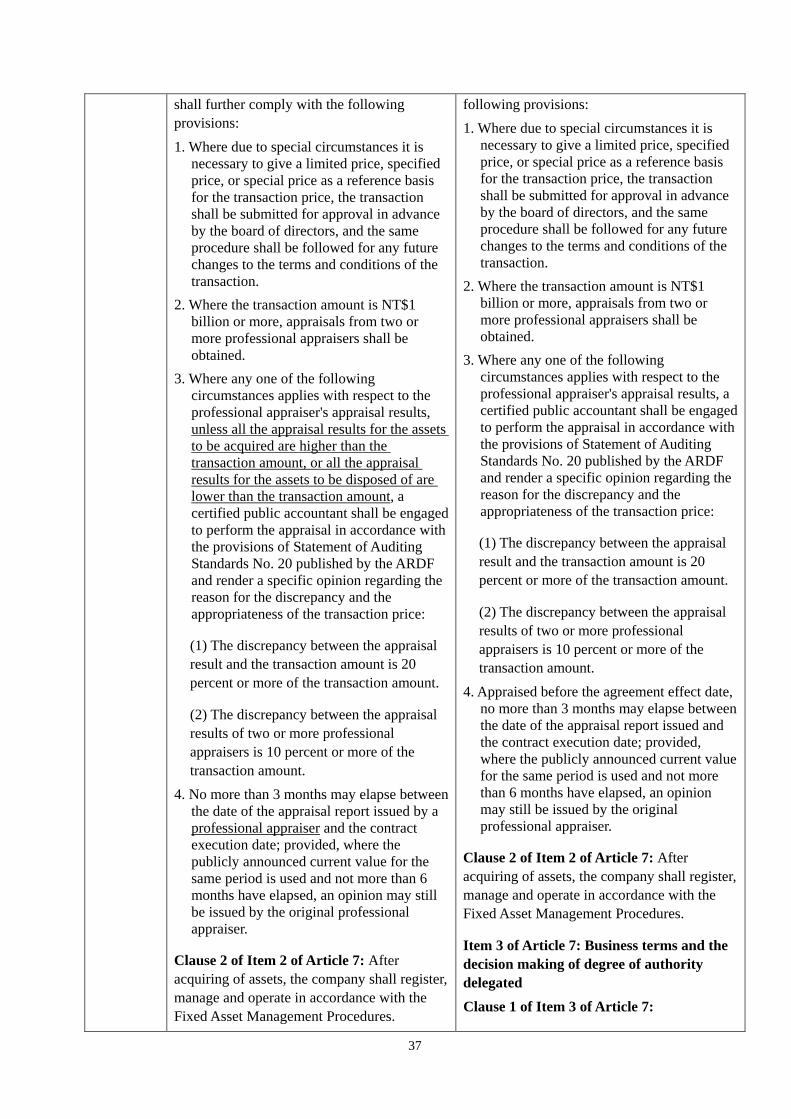

shall further comply with the following provisions: 1. Where due to special circumstances it is

necessary to give a limited price, specified price, or special price as a reference basis for the transaction price, the transaction shall be submitted for approval in advance by the board of directors, and the same procedure shall be followed for any future changes to the terms and conditions of the transaction.

2. Where the transaction amount is NT$1 billion or more, appraisals from two or more professional appraisers shall be obtained.

3. Where any one of the following circumstances applies with respect to the professional appraiser's appraisal results, unless all the appraisal results for the assets to be acquired are higher than the transaction amount, or all the appraisal results for the assets to be disposed of are lower than the transaction amount, a certified public accountant shall be engaged to perform the appraisal in accordance with the provisions of Statement of Auditing Standards No. 20 published by the ARDF and render a specific opinion regarding the reason for the discrepancy and the appropriateness of the transaction price:

(1) The discrepancy between the appraisal result and the transaction amount is 20 percent or more of the transaction amount.

(2) The discrepancy between the appraisal results of two or more professional appraisers is 10 percent or more of the transaction amount.

4. No more than 3 months may elapse between the date of the appraisal report issued by a professional appraiser and the contract execution date; provided, where the publicly announced current value for the same period is used and not more than 6 months have elapsed, an opinion may still be issued by the original professional appraiser.

Clause 2 of Item 2 of Article 7: After acquiring of assets, the company shall register, manage and operate in accordance with the Fixed Asset Management Procedures.

following provisions: 1. Where due to special circumstances it is

necessary to give a limited price, specified price, or special price as a reference basis for the transaction price, the transaction shall be submitted for approval in advance by the board of directors, and the same procedure shall be followed for any future changes to the terms and conditions of the transaction.

2. Where the transaction amount is NT$1 billion or more, appraisals from two or more professional appraisers shall be obtained.

3. Where any one of the following circumstances applies with respect to the professional appraiser's appraisal results, a certified public accountant shall be engaged to perform the appraisal in accordance with the provisions of Statement of Auditing Standards No. 20 published by the ARDF and render a specific opinion regarding the reason for the discrepancy and the appropriateness of the transaction price:

(1) The discrepancy between the appraisal result and the transaction amount is 20 percent or more of the transaction amount.

(2) The discrepancy between the appraisal results of two or more professional appraisers is 10 percent or more of the transaction amount.

4. Appraised before the agreement effect date, no more than 3 months may elapse between the date of the appraisal report issued and the contract execution date; provided, where the publicly announced current value for the same period is used and not more than 6 months have elapsed, an opinion may still be issued by the original professional appraiser.

Clause 2 of Item 2 of Article 7: After acquiring of assets, the company shall register, manage and operate in accordance with the Fixed Asset Management Procedures.

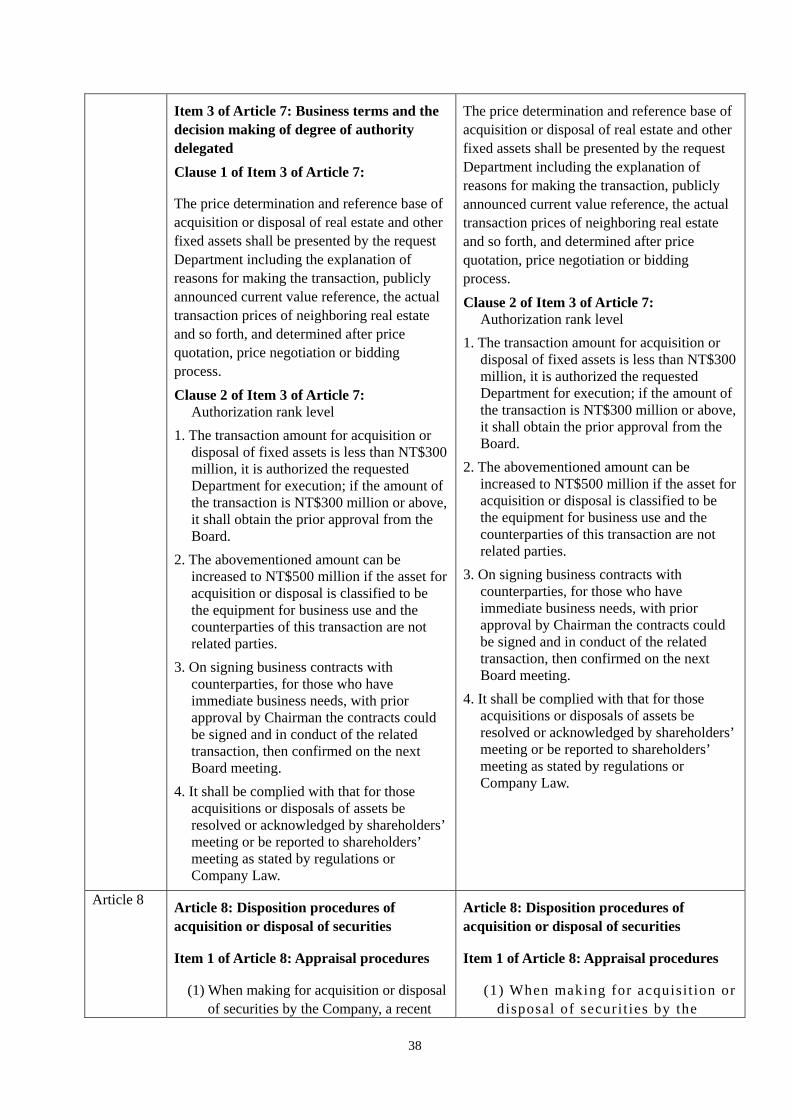

Item 3 of Article 7: Business terms and the decision making of degree of authority delegated Clause 1 of Item 3 of Article 7:

38

Item 3 of Article 7: Business terms and the decision making of degree of authority delegated Clause 1 of Item 3 of Article 7:

The price determination and reference base of acquisition or disposal of real estate and other fixed assets shall be presented by the request Department including the explanation of reasons for making the transaction, publicly announced current value reference, the actual transaction prices of neighboring real estate and so forth, and determined after price quotation, price negotiation or bidding process. Clause 2 of Item 3 of Article 7:

Authorization rank level 1. The transaction amount for acquisition or

disposal of fixed assets is less than NT$300 million, it is authorized the requested Department for execution; if the amount of the transaction is NT$300 million or above, it shall obtain the prior approval from the Board.

2. The abovementioned amount can be increased to NT$500 million if the asset for acquisition or disposal is classified to be the equipment for business use and the counterparties of this transaction are not related parties.

3. On signing business contracts with counterparties, for those who have immediate business needs, with prior approval by Chairman the contracts could be signed and in conduct of the related transaction, then confirmed on the next Board meeting.

4. It shall be complied with that for those acquisitions or disposals of assets be resolved or acknowledged by shareholders’ meeting or be reported to shareholders’ meeting as stated by regulations or Company Law.

The price determination and reference base of acquisition or disposal of real estate and other fixed assets shall be presented by the request Department including the explanation of reasons for making the transaction, publicly announced current value reference, the actual transaction prices of neighboring real estate and so forth, and determined after price quotation, price negotiation or bidding process. Clause 2 of Item 3 of Article 7:

Authorization rank level 1. The transaction amount for acquisition or

disposal of fixed assets is less than NT$300 million, it is authorized the requested Department for execution; if the amount of the transaction is NT$300 million or above, it shall obtain the prior approval from the Board.

2. The abovementioned amount can be increased to NT$500 million if the asset for acquisition or disposal is classified to be the equipment for business use and the counterparties of this transaction are not related parties.

3. On signing business contracts with counterparties, for those who have immediate business needs, with prior approval by Chairman the contracts could be signed and in conduct of the related transaction, then confirmed on the next Board meeting.

4. It shall be complied with that for those acquisitions or disposals of assets be resolved or acknowledged by shareholders’ meeting or be reported to shareholders’ meeting as stated by regulations or Company Law.

Article 8 Article 8: Disposition procedures of acquisition or disposal of securities

Item 1 of Article 8: Appraisal procedures

(1) When making for acquisition or disposal of securities by the Company, a recent

Article 8: Disposition procedures of acquisition or disposal of securities

Item 1 of Article 8: Appraisal procedures

(1) When making for acquisit ion or disposal of securi t ies by the

39

audited or reviewed financial statement by certified public accountant of the target securities company shall be obtained prior to the date of occurrence of the event, for reference to the transaction price.

(2) When the transaction amount achieving 20% of paid-in capital of the Company, or over NT$300 mill ion, i t shall be conducted with cert if ied public accountants prior to the date of occurrence of the event for the fairness opinion on the transaction, if cert ified public accountants require to use of expert’s report , then shall process in accordance with the provisions of Statement of Auditing Standards No. 20 published by the ARDF; but i t is not l imited for those securit ies with active market trading prices or those specifically regulated by FSC.

Item 2 of Article 8: Operation procedures

(1) Evaluation, trade, settlement, book-keeping: handled by each requested Department

(2) Custody: all of the securities acquired by the Company are in collected custody by Finance Department or kept in the safe-deposit box.

(3) Evaluation: Financial Department to collect relevant information in accordance with the provisions of the relevant accounting bulletin and send to Accounting Department for follow-up periodic evaluation.

Item 3 of Article 8: The decision procedures for the transaction terms and authorized quota limit

(1) For the government bonds, corporate bonds, bank indentures, fund securities, and asset back securities as specified in Item 1 of Article 3 of the Procedures, if

Company, a recent audited or reviewed financial statement by cert ified public accountant of the target securi t ies company shall be prior obtained for reference to the transaction price.

(2) When the transaction amount achieving 20% of paid-in capital of the Company, or over NT$300 mill ion, i t shall be conducted with cert if ied public accountants for the fairness opinion on the transaction; but i t is not l imited for those securit ies with active market trading prices or those specifically regulated by FSC.

Item 2 of Article 8: Operation procedures

(1) Evaluation, trade, settlement, book-keeping: handled by each requested Department

(2) Custody: all of the securities acquired by the Company are in collected custody by Finance Department or kept in the safe-deposit box.

(3) Evaluation: Financial Department to collect relevant information in accordance with the provisions of the relevant accounting bulletin and send to Accounting Department for follow-up periodic evaluation.

Item 3 of Article 8: The decision procedures for the transaction terms and authorized quota limit

(1) For the government bonds, corporate bonds, bank indentures, fund securities, and asset back securities as specified in Item 1 of Article 3 of the Procedures, if the transaction amount is less than 20% of the paid-in capital of the Company, CFO is authorized for the execution; if it’s achieved 20% or more of that, it shall be approved by the Board before the execution.

(2) For the equity, depositary receipts, call

40

the transaction amount is less than 20% of the paid-in capital of the Company, CFO is authorized for the execution; if it’s achieved 20% or more of that, it shall be approved by the Board before the execution.

(2) For the equity, depositary receipts, call (put) warrants and entitlement of certificates as specified in Item 1 of Article 3 of the Procedures, if the transaction amount is less than or equal to 5% of paid-in capital of the Company, the request Department is authorized for the execution; if it exceed 5% of that, it shall be approved by the Board meeting before the execution.

(put) warrants and entitlement of certificates as specified in Item 1 of Article 3 of the Procedures, if the transaction amount is less than or equal to 5% of paid-in capital of the Company, the request Department is authorized for the execution; if it exceed 5% of that, it shall be approved by the Board meeting before the execution.

Article 9 Article 9: Disposition procedures of acquisition or disposal of intangible assets

Item 1 of Article 9: Appraisal procedures

The acquisition or disposal of intangible assets of the Company shall be evaluated on the feasibility by the request Department, and also reporting to Intellectual Properties Department

Item 2 of Article 9: Operation procedures

An appraisal report shall be acquired from professional appraisal institution in advance for the acquisition or disposal of intangible assets of the Company; if the transaction amount would be or above 20% of the paid-in capital of the Company or over NT$ 300 million, it shall additionally request for fairness opinion prior to the date of occurrence of the event on the transaction price from certified public accountant.

Item 3 of Article 9: The decision procedures for the transaction terms and authorized quota limit

(1) Price decision method and reference source: reported by the requested Department for reference transaction prices on similar intangible asset transaction in the markets; if there is no

Article 9: Disposition procedures of acquisition or disposal of intangible assets

Item 1 of Article 9: Appraisal procedures

The acquisition or disposal of intangible assets of the Company shall be evaluated on the feasibility by the request Department, and also reporting to Intellectual Properties Department

Item 2 of Article 9: Operation procedures

An appraisal report shall be acquired from professional appraisal institution in advance for the acquisition or disposal of intangible assets of the Company; if the transaction amount would be or above 20% of the paid-in capital of the Company or over NT$ 300 million, it shall additionally request for fairness opinion on the transaction price from certified public accountant.

Item 3 of Article 9: The decision procedures for the transaction terms and authorized quota limit

(1) Price decision method and reference source: reported by the requested Department for reference transaction prices on similar intangible asset transaction in the markets; if there is no transaction price available in the market,

41

transaction price available in the market, the report from professional appraisal institutions shall be referred.

(2) The levels to which authority is delegated:

1. If the transaction amount is less than or equal to NT$ 300 million, the request Department is authorized for the execution; if it exceed NT$ 300 million of that, it shall be approved by the Board meeting before the execution; for those who have immediate business needs, the decision can be executed by Chairman first, and then confirmed on the next board meeting.

2. It shall be complied with that for those acquisitions or disposals of intangible assets be resolved or acknowledged by shareholders’ meeting or be reported to shareholders’ meeting as stated by regulations or Company Law.

the report from professional appraisal institutions shall be referred.

(2) The levels to which authority is delegated:

1. If the transaction amount is less than or equal to NT$ 300 million, the request Department is authorized for the execution; if it exceed NT$ 300 million of that, it shall be approved by the Board meeting before the execution.

2. It shall be complied with that for those acquisitions or disposals of intangible assets be resolved or acknowledged by shareholders’ meeting or be reported to shareholders’ meeting as stated by regulations or Company Law.

Article 9-1 ( newly

added)

Article 9-1: Calculation of the transaction amounts The calculation of the transaction amounts

referred to in Article 7. 8 and 9 shall be done in accordance with clause 5 of Item 2 of Article 13 herein, and "within the preceding year" as used herein refers to the year preceding the date of occurrence of the current transaction. Items for which an appraisal report from a professional appraiser or a CPA's opinion has been obtained need not be counted toward the transaction amount.

Newly added

Article 10 Article 10: Disposition procedures of related party transactions

Item 1 of Article 10: Appraisal and operation procedures

(1) In addition to follow Article 7, 8 or 9 respectively for the appraisal and operation procedures of acquisition or disposal of assets from or to a related party depending on the types of assets, if the transaction amount reaches 10% of the Company’s total assets, the Company shall also obtain an appraisal report from a professional appraiser or a CPA's opinion in compliance with the provisions of the

Article 10: Disposition procedures of acquisition of real estate from related partyItem 1 of Article 10: In addition to follow Article 7 for disposition procedures of acquisition of real estate from related party, if the Company acquires or exchanges of real estate from related party shall execute the related decision making procedures and evaluate the reasonableness of the preliminary transaction terms in accordance with the regulations. When judging whether a trading counterparty is a related party, in addition to legal formalities, the substance of the relationship shall also be

42

Article 7, 8 or 9. (2) When the Company intends to acquire or

dispose of real property from or to a related party, or when it intends to acquire or dispose of assets other than real property from or to a related party and the transaction amount reaches 20 percent or more of paid-in capital, 10 percent or more of the company's total assets, or NT$300 million or more, the Company shall evaluate and prepare various information required by Item 1 of this Article and obtain the approval from the board of Directors and recognition from the Supervisors.

(3) The calculation of the transaction amounts referred to in the preceding 2 clauses shall be made in accordance with Clause 5 of Item 2 of Article 13, and "within the preceding year" as used herein refers to the year preceding the date of occurrence of the current transaction. Items that have been obtained appraisal report from a professional appraiser or a CPA's opinion or approved by the board of directors and recognized by the supervisors need not be counted toward the transaction amount.

(4) When judging whether a trading counterparty is a related party, in addition to legal formalities, the substance of the relationship shall also be considered.

Item 2 of Article 10: The decision making procedure of degree of authority delegated (1) To acquire or dispose of real property

from or to a related party, or to acquire or dispose of assets other than real property from or to a related party and the transaction amount reaches 20 percent or more of paid-in capital, 10 percent or more of the Company's total assets, or NT$300 million or more, the Company may not proceed to enter into a transaction contract or make a payment until the following matters have been approved by the board of directors and recognized by the supervisors, but if acquisition or disposal of machinery or equipment among the Company and subsidiaries, and the transaction amount is less than 10% of the Company’s paid-in capital, Chairman can make decision first and then confirmed on the next Board meeting:

1. The purpose, necessity and

considered. Item 2 of Article 10: Appraisal and

operation procedures To acquire real estate from related party, the Company shall not proceed until the following matters have been approved by the board of directors and recognized by the supervisors: (1) The purpose, necessity and anticipated

benefit of the acquisition or disposal of assets.

(2) The reason for choosing the related party as a trading counterparty.

(3) The information regarding appraisal of the reasonableness of the preliminary transaction terms in accordance with the Clause 1 and 4 of Item 3 of this Article.

(4) The date and price at which the related party originally acquired the real property, the original trading counterparty, and that trading counterparty's relationship to the company and the related party.

(5) Monthly cash flow forecasts for the year commencing from the anticipated month of signing of the contract, and evaluation of the necessity of the transaction, and reasonableness of the funds utilization.

(6) Restrictive covenants and other important stipulations associated with the transaction.

Item 3 of Article 10: Evaluation of the reasonableness of the transaction costs (1) The Company acquires real property from

a related party shall evaluate the reasonableness of the transaction costs by the following means:

1. Based upon the related party's transaction price plus necessary interest on funding and the costs to be duly borne by the buyer. "Necessary interest on funding" is imputed as the weighted average interest rate on borrowing in the year the company purchases the property; provided, it may not be higher than the maximum non-financial industry lending rate announced by the Ministry of Finance.

2. Total loan value appraisal from a

43

anticipated benefit of the acquisition or disposal of assets.

2. The reason for choosing the related party as a trading counterparty.

3. With respect to the acquisition of real property from a related party, information regarding appraisal of the reasonableness of the preliminary transaction terms in accordance with the Clause 1, 2, 3, 4 and 6 of Item 3 of this Article.

4. The date and price at which the related party originally acquired the real property, the original trading counterparty, and that trading counterparty's relationship to the company and the related party.

5. Monthly cash flow forecasts for the year commencing from the anticipated month of signing of the contract, and evaluation of the necessity of the transaction, and reasonableness of the funds utilization.

6. An appraisal report from a professional appraiser or a CPA's opinion obtained in compliance with the Item 1 of this Article.

7. Restrictive covenants and other important stipulations associated with the transaction.

(2) The calculation of the transaction amounts referred to in the preceding Item shall be made in accordance with Clause 5 of Item 2 of Article 13, and "within the preceding year" as used herein refers to the year preceding the date of occurrence of the current transaction. Items that have been approved by the board of directors and recognized by the supervisors need not be counted toward the transaction amount.

(3) Acquiring or disposing the assets other than stated in Clause 1 shall follow in accordance with the preceding 3 Articles.

Item 3 of Article 10: Evaluation of the reasonableness of the transaction costs

financial institution where the related party has previously created a mortgage on the property as security for a loan; provided, the actual cumulative amount loaned by the financial institution shall have been 70 percent or more of the financial institution's appraised loan value of the property and the period of the loan shall have been 1 year or more. However, this shall not apply where the financial institution is a related party of one of the trading counterparties.

(2) Where land and structures thereupon are combined as a single property purchased in one transaction, the transaction costs for the land and the structures may be separately appraised in accordance with either of the means listed in the preceding paragraph.

(3) The Company that acquires real property from a related party and appraises the cost of the real property in accordance with Clause 1 and 2 of Item 3 of this Article shall also engage a CPA to check the appraisal and render a specific opinion.

(4) Acquiring real estate from related party, the Company's appraisal conducted in accordance with Clause 1 and 2 of Item 3 of this Article are uniformly lower than the transaction price, the matter shall be handled in compliance with Clause 5 of Item 5 of this Article. However, where the following circumstances exist, objective evidence has been submitted and specific opinions on reasonableness have been obtained from a professional real property appraiser and a CPA have been obtained, this restriction shall not apply:

1. Where the related party acquired undeveloped land or leased land for development, it may submit proof of compliance with one of the following conditions:

1) Where undeveloped land is appraised in accordance with the means in the preceding Article, and structures according to the related party's construction cost plus reasonable construction profit are

44

(1) The Company acquires real property from a related party shall evaluate the reasonableness of the transaction costs by the following means:

1. Based upon the related party's transaction price plus necessary interest on funding and the costs to be duly borne by the buyer. "Necessary interest on funding" is imputed as the weighted average interest rate on borrowing in the year the company purchases the property; provided, it may not be higher than the maximum non-financial industry lending rate announced by the Ministry of Finance.

2. Total loan value appraisal from a financial institution where the related party has previously created a mortgage on the property as security for a loan; provided, the actual cumulative amount loaned by the financial institution shall have been 70 percent or more of the financial institution's appraised loan value of the property and the period of the loan shall have been 1 year or more. However, this shall not apply where the financial institution is a related party of one of the trading counterparties.

(2) Where land and structures thereupon are combined as a single property purchased in one transaction, the transaction costs for the land and the structures may be separately appraised in accordance with either of the means listed in the preceding paragraph.

(3) The Company that acquires real property from a related party and appraises the cost of the real property in accordance with Clause 1 and 2 of Item 3 of this Article shall also engage a CPA to check the appraisal and render a specific opinion.

(4) Acquiring real estate from related party, the Company's appraisal conducted in accordance with Clause 1 and 2 of Item 3 of this Article are uniformly lower than the transaction price, the matter shall be handled in compliance with Clause 5 of

valued in excess of the actual transaction price. The "Reasonable construction profit" shall be deemed the average gross operating profit margin of the related party's construction division over the most recent 3 years or the gross profit margin for the construction industry for the most recent period as announced by the Ministry of Finance, whichever is lower. 2) Completed transactions by unrelated parties within the preceding year involving other floors of the same property or neighboring or closely valued parcels of land, where the land area and transaction terms are similar after calculation of reasonable price discrepancies in floor or area land prices in accordance with standard property market practices. 3) Completed leasing transactions by unrelated parties for other floors of the same property from within the preceding year, where the transaction terms are similar after calculation of reasonable price discrepancies among floors in accordance with standard property leasing market practices.

2. Where the Company acquiring real property from a related party provides evidence that the terms of the transaction are similar to the terms of transactions completed for the acquisition of neighboring or closely valued parcels of land of a similar size by unrelated parties within the preceding year. Completed transactions for neighboring or closely valued parcels of land in the preceding paragraph in principle refers to parcels on the same or an adjacent block and within a distance of no more than 500 meters or parcels close in publicly announced current value; transaction for similarly sized parcels in principle refers to transactions completed by unrelated parties for parcels with a land area of no less than 50 percent of the property in the planned transaction; within the preceding year refers to the year

45

Item 5 of this Article. However, where the following circumstances exist, objective evidence has been submitted and specific opinions on reasonableness have been obtained from a professional real property appraiser and a CPA have been obtained, this restriction shall not apply:

1. Where the related party acquired undeveloped land or leased land for development, it may submit proof of compliance with one of the following conditions:

1) Where undeveloped land is appraised in accordance with the means in the preceding Article, and structures according to the related party's construction cost plus reasonable construction profit are valued in excess of the actual transaction price. The "Reasonable construction profit" shall be deemed the average gross operating profit margin of the related party's construction division over the most recent 3 years or the gross profit margin for the construction industry for the most recent period as announced by the Ministry of Finance, whichever is lower. 2) Completed transactions by unrelated parties within the preceding year involving other floors of the same property or neighboring or closely valued parcels of land, where the land area and transaction terms are similar after calculation of reasonable price discrepancies in floor or area land prices in accordance with standard property market practices. 3) Completed leasing transactions by unrelated parties for other floors of the same property from within the preceding year, where the transaction terms are similar after calculation of reasonable price discrepancies among floors in accordance with standard property leasing market practices.

2. Where the Company acquiring real property from a related party provides evidence that the terms of

preceding the date of occurrence of the acquisition of the real property.

(5) Where the Company acquires real property from a related party and the results of appraisals conducted in accordance with Clause 1 and 2 of Item 3 of this Article are uniformly lower than the transaction price, the following steps shall be taken. Furthermore, the Company that has set aside a special reserve under the preceding paragraph may not utilize the special reserve until it has recognized a loss on decline in market value of the assets it purchased at a premium, or they have been disposed of, or adequate compensation has been made, or the status quo ante has been restored, or there is other evidence confirming that there was nothing unreasonable about the transaction, and the Securities and Futures Commission has given its consent.

1. A special reserve shall be set aside in accordance with Article 41, paragraph 1 of the Act against the difference between the real property transaction price and the appraised cost, and may not be distributed or used for capital increase or issuance of bonus shares. Where a public company uses the equity method to account for its investment in another company, then the special reserve called for under Article 41, paragraph of the Act shall be set aside pro rata in a proportion consistent with the share of public company's equity stake in the other company.

2. Supervisors shall comply with Article 218 of the Company Act.

3. Actions taken pursuant to subparagraph 1 and subparagraph 2 shall be reported to a shareholders meeting, and the details of the transaction shall be disclosed in the annual report and any investment prospectus

(6) The Company that acquires real property from a related party and appraises the cost

46

the transaction are similar to the terms of transactions completed for the acquisition of neighboring or closely valued parcels of land of a similar size by unrelated parties within the preceding year. Completed transactions for neighboring or closely valued parcels of land in the preceding paragraph in principle refers to parcels on the same or an adjacent block and within a distance of no more than 500 meters or parcels close in publicly announced current value; transaction for similarly sized parcels in principle refers to transactions completed by unrelated parties for parcels with a land area of no less than 50 percent of the property in the planned transaction; within the preceding year refers to the year preceding the date of occurrence of the acquisition of the real property.

(5) Where the Company acquires real property from a related party and the results of appraisals conducted in accordance with Clause 1 and 2 of Item 3 of this Article are uniformly lower than the transaction price, the following steps shall be taken. Furthermore, the Company that has set aside a special reserve under the preceding paragraph may not utilize the special reserve until it has recognized a loss on decline in market value of the assets it purchased at a premium, or they have been disposed of, or adequate compensation has been made, or the status quo ante has been restored, or there is other evidence confirming that there was nothing unreasonable about the transaction, and the Financial Supervisory Commission has given its consent.

1. A special reserve shall be set aside in accordance with Article 41, paragraph 1 of the Act against the difference between the real property transaction price and the appraised cost, and may not be distributed or used for capital increase or issuance of bonus shares. Where a public

of the real property in accordance with Clause 1, 2 and 3 of Item 3 of this Article shall also engage a CPA to check the appraisal and render a specific opinion. Where the Company acquires real property from a related party and one of the following circumstances exists, the acquisition shall be conducted in accordance with Item 1 and 2 of this Article and the preceding three paragraphs do not apply:

1. The related party acquired the real property through inheritance or as a gift.

2. More than 5 years will have elapsed from the time the related party signed the contract to obtain the real property to the signing date for the current transaction.

3. The real property is acquired through signing of a joint development contract with the related party.

(7) When the Company obtains real property from a related party, it shall also comply with the Clause 5 of Item 3 of this Article if there is other evidence indicating that the acquisition was not an arms length transaction.

47

company uses the equity method to account for its investment in another company, then the special reserve called for under Article 41, paragraph of the Act shall be set aside pro rata in a proportion consistent with the share of public company's equity stake in the other company.

2. Supervisors shall comply with Article 218 of the Company Act.

3. Actions taken pursuant to subparagraph 1 and subparagraph 2 shall be reported to a shareholders meeting, and the details of the transaction shall be disclosed in the annual report and any investment prospectus

(6) The Company that acquires real property from a related party and appraises the cost of the real property in accordance with Clause 1, 2 and 3 of Item 3 of this Article shall also engage a CPA to check the appraisal and render a specific opinion. Where the Company acquires real property from a related party and one of the following circumstances exists, the acquisition shall be conducted in accordance with Item 2 of this Article and the preceding three paragraphs do not apply:

1. The related party acquired the real property through inheritance or as a gift.

2. More than 5 years will have elapsed from the time the related party signed the contract to obtain the real property to the signing date for the current transaction.

3. The real property is acquired through signing of a joint development contract with the related party.

(7) When the Company obtains real property from a related party, it shall also comply with the Clause 5 of Item 3 of this Article if there is other evidence indicating that the acquisition was not an arms length

48

transaction.

Article 12 (amended

Clause 8 of Item 2)

Article 12: Disposition procedures of Mergers and Consolidations, Splits, Acquisitions, and Assignment of Shares

Item 1 of Article 12: Appraisal and operation procedures

…………………

Item 2 of Article 12: Other notice items

…………………

Clause 8 of Item 2 of Article 12:

When participating in a merger, spin off, acquisition, or transfer of another company's shares, a company that is listed on an exchange or has its shares traded on an OTC market shall, within the same day starting two days of passage of a resolution by the Board, report (in the prescribed format and via the Internet-based information system) the information set out in subparagraphs 1 and 2 of the preceding paragraph to the FSC for recordation.

Article 12: Disposition procedures of Mergers and Consolidations, Splits, Acquisitions, and Assignment of Shares

Item 1 of Article 12: Appraisal and operation procedures

…………………………………………

Item 2 of Article 12: Other notice items

…………………………………………

Clause 8 of Item 2 of Article 12:

When participating in a merger, spin off, acquisition, or transfer of another company's shares, a company that is listed on an exchange or has its shares traded on an OTC market shall, within two days of passage of a resolution by the Board, report (in the prescribed format and via the Internet-based information system) the information set out in subparagraphs 1 and 2 of the preceding paragraph to the FSC for recordation.

Article 13 Article 13: Procedures for information public disclosure

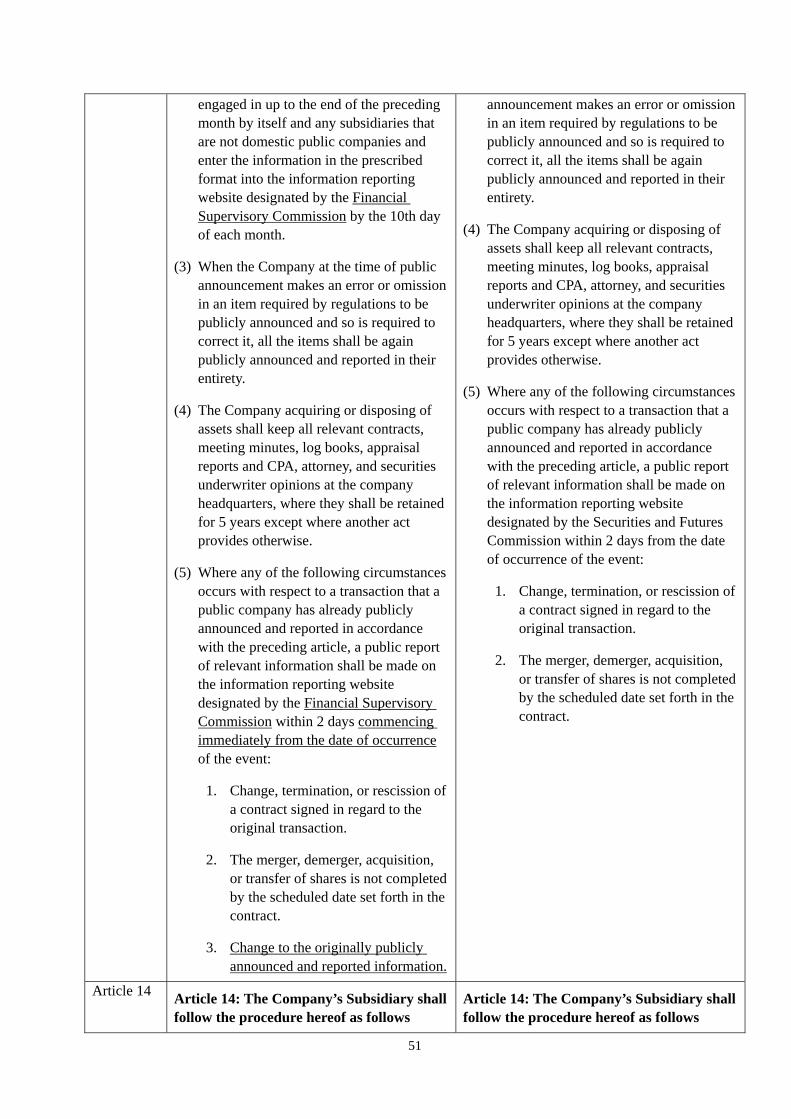

Item 1 of Article 13: Timing of the public announcement and regulatory filing procedures

If within the public announcement items and the transaction amount reach to the standard for publicly announced and reported when acquiring or disposing assets, the Company shall publicly announce and report the relevant information on the FSC's designated website in the appropriate format as prescribed by regulations within 2 days commencing immediately from the date of occurrence of the event.

Item 2 of Article 13: Public announcement items and standard for publicly announced and reported

(4) Acquisition or disposal of real property from a related party, or the transaction

Article 13: Procedures for information public disclosure

Item 1 of Article 13: Timing of the public announcement and regulatory filing procedures

If within the public announcement items and the transaction amount reach to the standard for publicly announced and reported when acquiring or disposing assets, the Company shall publicly announce and report the relevant information on the FSC's designated website in the appropriate format as prescribed by regulations within 2 days commencing immediately from the date of occurrence of the event.

Item 2 of Article 13: Public announcement items and standard for publicly announced and reported

(1) Acquisition of real property from a related party

49

amount from the acquisition or disposal of other assets than the real property from a related party reaches to 20% of the Company’s paid-in capital, 10% of the Company’s total assets or above NT$ 300 million. But this shall not apply to trading of government bonds or bonds under repurchase and resale agreements.

(5) Mergers and Consolidations, Splits, Acquisitions, and Assignment of Shares

(6) Losses from derivatives trading reaching the limits on aggregate losses or losses on individual contracts set out in the procedures adopted by the company

(7) In addition to the asset transaction, financial institutions to dispose of claims or investment in the mainland China area other than the preceding three items, the transaction amount reach to 20% of the Company’s paid-in capital or above NT$ 300 million. However, this shall not apply to the following circumstances:

1. Trading of government bonds.

2. Securities trading by investment professionals on foreign or domestic securities exchanges or over-the-counter markets.

3. Trading of bonds under repurchase/resale agreements.

4. Where the type of asset acquired or disposed is equipment/machinery for business use, the trading counterparty is not a related party, and the transaction amount is less than NT$500 million.

5. Acquisition or disposal by a public company in the construction business of real property for construction use, where the trading counterparty is not a related party, and the transaction amount is less than NT$500 million.

6. Where land is acquired under an arrangement on engaging others to

(2) Investment in the mainland China area

(3) Mergers and Consolidations, Splits, Acquisitions, and Assignment of Shares

(4) Losses from derivatives trading reaching the limits on aggregate losses or losses on individual contracts set out in the procedures adopted by the company

(5) In addition to the asset transaction or financial institutions to dispose of claims other than the preceding four items, the transaction amount reach to 20% of the Company’s paid-in capital or above NT$ 300 million. However, this shall not apply to the following circumstances:

1. Trading of government bonds.

2. Securities trading by investment professionals on foreign or domestic securities exchanges or over-the-counter markets.

3. Trading of bonds under repurchase/resale agreements.

4. Where the type of asset acquired or disposed is equipment/machinery for business use, the trading counterparty is not a related party, and the transaction amount is less than NT$500 million.

5. Acquisition or disposal by a public company in the construction business of real property for construction use, where the trading counterparty is not a related party, and the transaction amount is less than NT$500 million.

6. Where land is acquired under an arrangement on engaging others to build on the company's own land, joint construction and allocation of housing units, joint construction and allocation of ownership percentages, or joint construction and separate sale, and the amount the company expects to invest in the transaction is

50

build on the company's own land, engaging others to build on rented land, joint construction and allocation of housing units, joint construction and allocation of ownership percentages, or joint construction and separate sale, and the amount the company expects to invest in the transaction is less than NT$500 million.

(8) "Within the preceding year" as used in the preceding paragraph Clause 5 refers to the year preceding the date of occurrence of the current transaction. Items duly announced in accordance with these Regulations need not be counted toward the transaction amount.

1. The amount of any individual transaction.