Embed Size (px)

Citation preview

HMCL Colombia S.A.S.

Individual Financial Statements Accounting Standards and Financial Information -NCIF

March 2019

2

HMCL Colombia S.A.S.

Individual Financial Statements under accounting standards and financial information for the years ending on March 31, 2019 and 2018 and Report of the External Auditor

3

Content

The report is included here (Opinion) of Tax Auditors ....................................................................... 5

Statement of Financial Position .......................................................................................................... 7

Statement of profit or loss .................................................................................................................. 8

Statements of Changes in Equity ........................................................................................................ 9

Notes to the Financial Statements .................................................................................................... 12

1. Reporting Entity ......................................................................................................................... 13

1.1 Summary of the Main Accounting Policies ................................................................................ 14

Basis of Presentation ................................................................................................................. 14

Basis of measurement ............................................................................................................... 14

2. Significant accounting policies .................................................................................................. 15

(a) Foreign Currency Transactions .......................................................................................... 15

(b) Inventories ......................................................................................................................... 16

(c) Financial Instruments ........................................................................................................ 16

(d) Share Capital - Common Shares ........................................................................................ 18

(e) Property, Plant and Equipment ......................................................................................... 18

(f) Leases ................................................................................................................................. 19

(g) Intangibles ......................................................................................................................... 20

(h) Prepaid Expenses ............................................................................................................... 20

(i) Impairment of assets ......................................................................................................... 20

(j) Employees' benefits ........................................................................................................... 21

(k) Provisions and contingencies ............................................................................................. 21

(l) Revenues from regular activities ....................................................................................... 22

(m) Taxes .................................................................................................................................. 22

(n) Contingent Assets and Liabilities ....................................................................................... 23

(o) Contingent Liabilities ......................................................................................................... 23

(p) Contingent Assets .............................................................................................................. 24

(q) Classification of Current and Non-Current Items .............................................................. 24

3. Property, plant and equipment ................................................................................................. 24

4. Intangible assets ........................................................................................................................ 25

5. Trade receivables....................................................................................................................... 25

6. Other financial assets ................................................................................................................ 26

7. Current Tax and Deferred Tax ................................................................................................... 26

7.1. Net Current tax .................................................................................................................. 26

4

7.2. Deferred tax (assets)/ liabilities (net) ................................................................................ 26

8. Other current assets .................................................................................................................. 27

9. Inventories ................................................................................................................................. 27

10. Cash and cash equivalents......................................................................................................... 27

11. Equity share capital ................................................................................................................... 28

12. Non – Current borrowings ......................................................................................................... 29

12.1. Details of long term borrowings of the Company ............................................................. 30

13. Trade Payables........................................................................................................................... 30

14. Other Financial Liabilities .......................................................................................................... 30

15. Provisions .................................................................................................................................. 31

15.1. Details of movement in Other Provisions ......................................................................... 31

16. Other current liabilities ............................................................................................................. 31

17. Current borrowings ................................................................................................................... 32

18. Revenue from operations (gross) .............................................................................................. 33

19. Other income ............................................................................................................................. 33

20. Cost of raw materials consumed ............................................................................................... 34

21. Changes in inventories of finished goods and work-in-progress .............................................. 34

22. Employee benefits expenses ..................................................................................................... 34

23. Finance costs ............................................................................................................................. 35

24. Other expenses .......................................................................................................................... 35

24.1. Payment to auditors .......................................................................................................... 36

25. Depreciation and amortization expenses .................................................................................. 36

26. Production Costs........................................................................................................................ 36

27. Transactions and Balances between Related Part .................................................................... 37

28. Going Concern ........................................................................................................................... 38

6

INDIVIDUAL

FINANCIAL

STATEMENTS

NCIF – MARCH 2019

7

Notes

No.

March 31, 2019

March 31, 2018

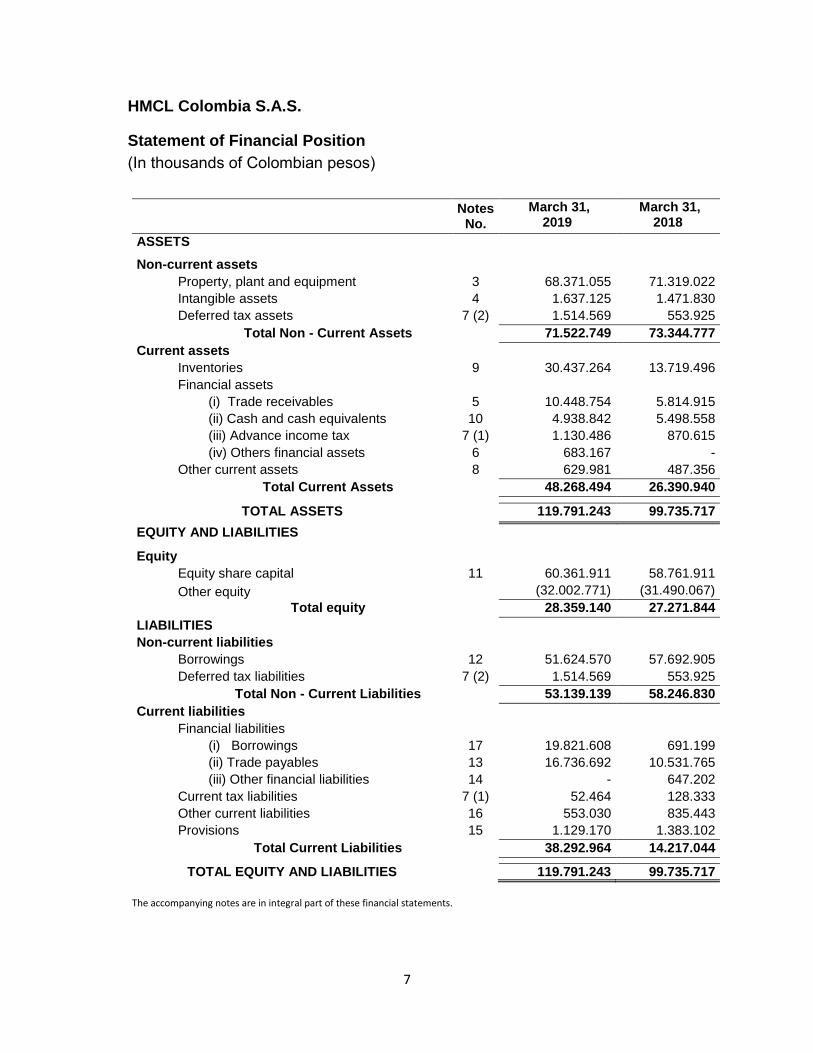

ASSETS

Non-current assets

Property, plant and equipment 3 68.371.055 71.319.022 Intangible assets 4 1.637.125 1.471.830 Deferred tax assets 7 (2) 1.514.569 553.925

Total Non - Current Assets

71.522.749 73.344.777

Current assets

Inventories 9 30.437.264 13.719.496 Financial assets

(i) Trade receivables 5 10.448.754 5.814.915 (ii) Cash and cash equivalents 10 4.938.842 5.498.558 (iii) Advance income tax 7 (1) 1.130.486 870.615 (iv) Others financial assets 6 683.167 -

Other current assets 8 629.981 487.356 Total Current Assets

48.268.494 26.390.940

TOTAL ASSETS 119.791.243 99.735.717

EQUITY AND LIABILITIES

Equity

Equity share capital 11 60.361.911 58.761.911 Other equity

(32.002.771) (31.490.067)

Total equity

28.359.140 27.271.844

LIABILITIES

Non-current liabilities

Borrowings 12 51.624.570 57.692.905 Deferred tax liabilities 7 (2) 1.514.569 553.925

Total Non - Current Liabilities

53.139.139 58.246.830

Current liabilities

Financial liabilities

(i) Borrowings 17 19.821.608 691.199 (ii) Trade payables 13 16.736.692 10.531.765 (iii) Other financial liabilities 14 - 647.202

Current tax liabilities

7 (1) 52.464 128.333 Other current liabilities 16 553.030 835.443 Provisions 15 1.129.170 1.383.102

Total Current Liabilities

38.292.964 14.217.044

TOTAL EQUITY AND LIABILITIES 119.791.243 99.735.717

The accompanying notes are in integral part of these financial statements.

HMCL Colombia S.A.S.

Statement of Financial Position

(In thousands of Colombian pesos)

8

For the year ended 31 March: Notes

No. 2019 2018

Revenue from operations (gross) 18 72.033.565 55.804.296

Other income 19 599.965 259.889

TOTAL INCOME 72.633.530 56.064.185

Cost of raw materials consumed 20 (50.694.403) (38.509.819)

Changes in inventories of finished goods and work-in-progress

21 2.378.124 (5.290.002)

Excise duty on sale of goods

(608.299) (411.203)

Employee benefits expenses 22 (10.025.683) (10.231.099)

Finance costs 23 (6.971.511) (7.697.288)

Depreciation and amortization expenses 25 (3.703.965) (3.990.699)

Other expenses 24 (17.924.724) (18.528.344)

TOTAL EXPENSES (87.550.461) (84.658.454)

LOSS BEFORE TAX (14.916.931) (28.594.269)

Tax expense

Income tax expense 7 (1) (52.464) (128.333)

LOSS FOR THE PERIOD (14.969.395) (28.722.602)

The notes are in integral part of these financial statements.

HMCL Colombia S.A.S.

Statement of profit or loss

(In thousands of Colombian pesos).

9

A. Equity share capital

Number of Shares Amount

Balance as at April 1, 2017 656.399.109 65.639.911

Changes in equity share capital during the year (68.780.000) (6.878.000)

Balance as at March 31, 2018 587.619.109 58.761.911

Changes in equity share capital during the year 16.000.000 1.600.000

Balance as at March 31, 2019 603.619.109 60.361.911

B. Other Equity

Reserves and Surplus

Particulars Securities Premium Reserve

Retained Earnings

Total

Balance as at April 1, 2017 30.340.845 (69.986.200) (39.645.355)

Profit for the year 27.000.001 (18.844.713) 8.155.288

Total Comprehensive Income for the year

27.000.001 (18.844.713) 8.155.288

Balance as at March 31, 2018 57.340.846 (88.830.913) (31.490.067)

Profit for the year 14.400.000 (14.912.704) (512.704)

Total Comprehensive Income for the year

14.400.000 (14.912.704) (512.704)

Balance as at March 31, 2019 71.740.846 (103.743.617) (32.002.771)

HMCL Colombia S.A.S.

Statements of Changes in Equity

For the yeard ended 31 March 2019 (In thousands of Colombian pesos).

10

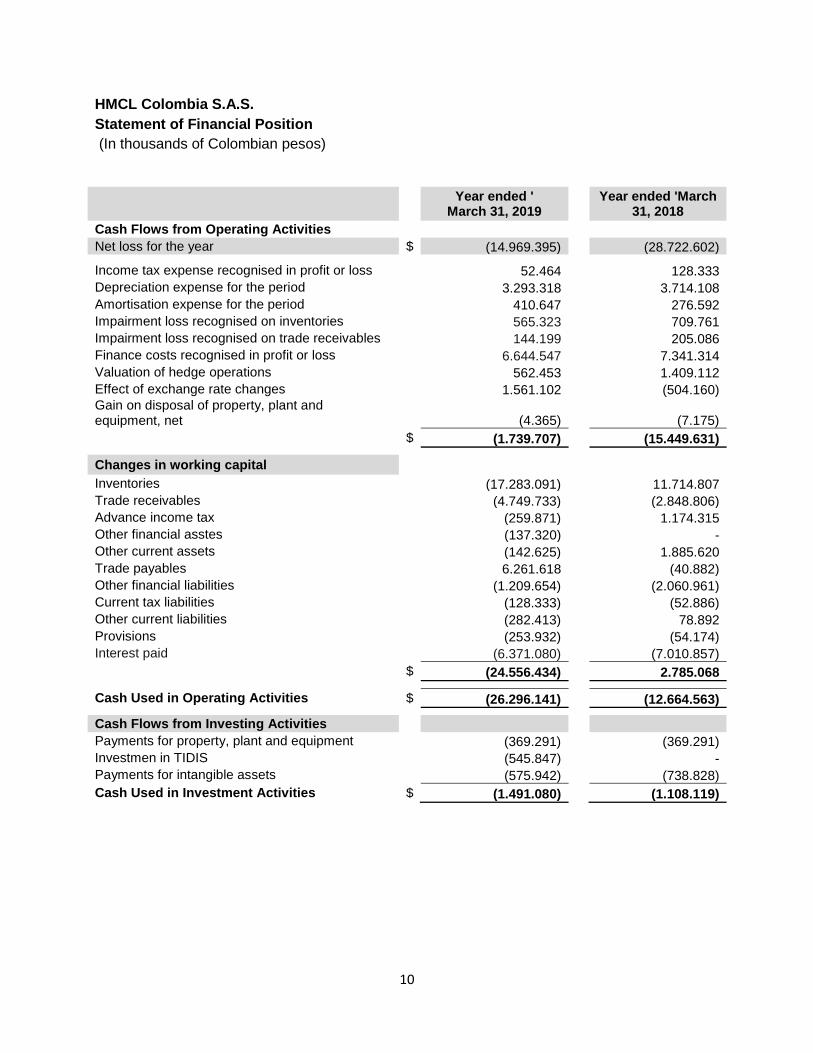

HMCL Colombia S.A.S. Statement of Financial Position (In thousands of Colombian pesos)

Year ended ' March 31, 2019

Year ended 'March 31, 2018

Cash Flows from Operating Activities

Net loss for the year $ (14.969.395) (28.722.602)

Income tax expense recognised in profit or loss 52.464 128.333

Depreciation expense for the period 3.293.318 3.714.108

Amortisation expense for the period 410.647 276.592

Impairment loss recognised on inventories 565.323 709.761

Impairment loss recognised on trade receivables 144.199 205.086

Finance costs recognised in profit or loss 6.644.547 7.341.314

Valuation of hedge operations 562.453 1.409.112

Effect of exchange rate changes 1.561.102 (504.160) Gain on disposal of property, plant and equipment, net

(4.365) (7.175)

$ (1.739.707) (15.449.631)

Changes in working capital

Inventories (17.283.091) 11.714.807

Trade receivables (4.749.733) (2.848.806)

Advance income tax (259.871) 1.174.315

Other financial asstes (137.320) -

Other current assets (142.625) 1.885.620

Trade payables 6.261.618 (40.882)

Other financial liabilities (1.209.654) (2.060.961)

Current tax liabilities (128.333) (52.886)

Other current liabilities (282.413) 78.892

Provisions (253.932) (54.174)

Interest paid (6.371.080) (7.010.857) $ (24.556.434) 2.785.068

Cash Used in Operating Activities $ (26.296.141) (12.664.563)

Cash Flows from Investing Activities

Payments for property, plant and equipment (369.291) (369.291)

Investmen in TIDIS (545.847) -

Payments for intangible assets (575.942) (738.828)

Cash Used in Investment Activities $ (1.491.080) (1.108.119)

11

Cash Flows from Financing Activities

Increase in financial obligations 27.375.258 25.013.510

Payments of financial obligations (16.147.753) (37.554.623) Proceeds from issue of equity instruments of the Company

1.600.000 3.000.000

Proceeds from issue of redeemable preference shares

14.400.000 27.000.000

Cash Increase in Financing Activities 27.227.505 17.458.887

NET INCREASE (USE) OF CASH AND CASH EQUIVALENTS

$ (559.716) 3.686.205

CASH AND CASH EQUIVALENTS

AT THE BEGINNING OF THE YEAR $ 5.498.558 1.812.353

AT THE END OF THE YEAR $ 4.938.842 5.498.558

12

Notes to the Financial

Statements

NCIF 2019 - 2018 In Thousands of Colombian Pesos, except where otherwise indicated

13

1. Reporting Entity

The Company: HMCL Colombiana S.A.S. (hereinafter "The Company"), is a simplified joint stock company with domicile in Colombia, made up of private document No. 0000001 of General Shareholders' Meeting of April 14, 2014 at the 16th Notary´s Office of Bogotá, with indefinite duration. Its main purpose is to act as industrial user of goods and services in one or more free zones and start sales activities on November 22, 2014. As an industrial user of goods, the company may manufacture and assemble motorcycles; market, sell and distribute motorcycles; and carry out all acts, businesses and activities that relate directly or indirectly to the achievement of the objectives above. The company may carry out the construction and adaptation of the facilities, warehouses and production plants, as well as the assembly of machinery and equipment, and other activities detailed in the chamber and commerce certificate of the Company. According to PS qualification act No 001 of June 06, 2014, issued by Zona Franca Permanente Palmaseca, User Operator of Parque Sur Free Zone, the company HMCL COLOMBIA S.A.S. Identified with TIN Not 900.723.988-9 was classified as Industrial User of Goods and Industrial Services for the period between June 6, 2014 and the September 27, 2025, taking into account the date of declaration of Parque Sur Free Zone. Through this special qualification the company acquires the following benefits and commitments: a. Tariff of 15% on income tax for income earned as an industrial user (domestic and external

markets). b. Principle of extraterritoriality outside the customs territory (no customs duties incurred). c. VAT exemption for purchases of raw materials and supplies for production from the national

customs territory or to other industrial free zone users. d. Generation of 50 new direct jobs. e. Investments in productive real fixed assets and land of 15,000 SMMLV (Spanish acronym for

Statutory Monthly Minimum Wages). f. Settle parafiscal and social security contributions on 100% of the value of the payroll and linked

through employee contracts. This benefits and commitments were modified according to the Law 1819 of December 29, 2016. In

the previous law, the rate of income tax for users of the free zone is 20% starting to January 1,

2017.

Its main and business address is Zona Franca Conjunto Industrial Parque Sur LT 6 KM 24, Municipio Villa Rica, Cauca - Colombia.

14

The activities authorized to be developed as an Industrial User of Goods and Industrial Services are the following:

Name of the Activity Social Object Activities

Manufacturing of motorcycles

1. Manufacturing and assembly of two- and three-

wheeled motorcycles. 2. Sale and distribution of two- and three-wheeled

motorcycles manufactured and assembled in the Free Zone.

3. Carry out all the acts, business and activities permitted by the free regime, which relate directly or indirectly to the achievement of the above activities.

4. Painting of metal and/or plastic parts and welding of metal motorcycles parts.

Maintenance and repair of motorcycles

5. Repair and cleaning 6. Technical support, maintenance and repair of motor

vehicles, motorcycles and three-wheelers.

Other activities complementary to transport

7. Integral logistics and distribution, in industrial,

commercial activities and the activities of foreign trade and customs regime, such as the export and import of goods, machinery, equipment, parts, and accessories that are related to the assembly and production of motor vehicles, motorcycles or three-wheelers.

Technical testing and analysis.

8. Evidence of quality or technical support of goods to

both motorcycles, or three-wheelers or equipment and machinery for the assembly of the same.

1.1 Summary of the Main Accounting Policies

Basis of Presentation

Technical Regulatory Framework

The financial statements have been prepared in accordance with the Accounting and Financial

Reporting Standards accepted in Colombia (NCIF by its acronym in Spanish) established in Law 1314

of 2009, for makers of financial information belonging to Group 2, regulated by the Single Regulatory

Decree 2420 of 2015 modified by Decrees 2496 of 2015, 2131 of 2016, 2170 of 2017 and 2483 of

2018. The NCIFs are based on the International Financial Reporting Standard (IFRS) for Small and

Medium Entities (SMEs) in Colombia - IFRS for SMEs, issued by the International Accounting

Standards Board Standards Board - IASB); The basic standard corresponds to the one translated

into Spanish and issued as of December 31, 2015 by the IASB.

Basis of measurement

The individual financial statements have been prepared on the historical cost model.

15

Functional and presentation currency The items included in the Company's separate financial statements are presented in the currency of the primary economic environment where operates the Company (Colombian pesos). These consolidated financial statements are presented in "Colombian pesos", which is the Company’s functional currency. All financial information is presented in thousand pesos and has been rounded to the nearest full figure. Use of judgments and estimates The preparation of the financial statements in accordance with the Accounting and Financial Reporting Standards accepted in Colombia requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the amounts of assets and liabilities at the date of Balance sheet, as well as the income and expenses of the year. Actual results could differ from these estimates. Real results may differ from these estimates. Estimates and underlying assumptions are regularly reviewed. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected. Information about critical judgements in applying accounting policies that have the most significant effect in the financial statements and/or with significant risk is included in the following notes: Note 15 – Provisions

2. Significant accounting policies

The accounting policies set forth below have been applied consistently in the preparation of the financial statements prepared in accordance with the Financial Reporting Standards accepted in Colombia (NCIF).

(a) Foreign Currency Transactions

Transactions in foreign currencies are translated to the respective functional currencies of the Company at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency at the exchange rate at that date. Non-monetary assets and liabilities that are measured at fair value in a foreign currency are retranslated to the functional currency at the exchange rate at the date that the fair value was determined. The differences in exchange are recognized in profit or loss in the period in which they arise.

• Transactions and Balances

Transactions in foreign currency are initially recognized by the Company at the exchange rate of its functional currency, on the date the transaction meets the criteria for its recognition.

Monetary assets and liabilities denominated in foreign currency are converted to the closing exchange rate of the functional currency in force on the closing date of the reporting period.

Differences arising from the settlement or conversion of monetary items are recognized in the Company's income statement.

The representative market exchange rate at March 31, 2019 in Colombian pesos was $ 3.174,79 (2018 $ 2.780,47).

16

(b) Inventories

Inventories are valued at cost or net realizable value, whichever is lower. The cost of inventories includes disbursements in the acquisition of inventories and other costs incurred in moving them to their current location and conditions. The net realizable value represents the estimated selling price in the normal course of business less the estimated termination costs and costs required for sale. The cost of inventories is determined using the weighted average method. Significant parts and permanent maintenance equipment that the Company identifies and uses for more than one fiscal year are classified as property, plant, and equipment items.

(c) Financial Instruments

Financial assets and liabilities are recognized only when you have the contractual right to receive cash in the future.

(i) FINANCIAL ASSETS AND LIABILITIES

• Recognition, initial measurement and classification

Financial assets and liabilities are measured at the transaction price, including transaction costs, except in the initial measurement of financial assets and liabilities that are then measured at fair value through profit or loss, except if the agreement constitutes a financing transaction for the Company (for a financial liability) or for the counterparty (for a financial asset) of the agreement. An agreement is a financing transaction, if payments are deferred beyond normal commercial terms, or it is financed at an interest rate which is not a market rate, if the agreement constitutes a financing transaction the Company measures the financial asset or the financial liability at present value of the future payments discounted at a market interest rate for a similar debt instrument determined in the initial recognition.

• Subsequent measurement

At the end of each reported period, the basic financial instruments are measured by the Company as follows, without deducting transaction costs that may be incurred on the sale or other type of disposal: a) Debt instruments are measured at amortized cost using the effective interest method. b) The loan commitments are measured at cost less value impairment The amortized cost of a financial asset or a financial liability at each reporting date is the net of the following amounts: a) The amount at which the financial asset or the financial liability is measured at the

initial recognition, b) Less principal repayments, c) Plus or less the accumulated amortization, using the effective interest method of any

difference between the amount at the initial recognition and the amount at maturity, d) Less, in the case of a financial asset, any reduction (recognized directly or using a

corrective account) for impairment or uncollectability.

17

• Impairment of measured financial instruments at amortized cost

At the end of each reported period, the Company assesses whether there is objective evidence of impairment of the financial assets measured at cost or at amortized cost. When there is objective evidence of impairment, the Company immediately recognizes an impairment loss in profit or loss.

• Derecognized assets

A financial asset is derecognized when: a) Expiry the contractual rights on the asset cash flows; b) All the risks and rewards inherent in the ownership of the financial asset are

transferred. c) Risks and rewards inherent in the ownership of the asset are retained substantially,

but control of the same has been transferred. In this case the Company: i) Derecognizes the asset, and ii) Recognizes separately any right and obligation retained or created in the transfer.

• Derecognized liabilities

A financial liability is derecognized when: a) The obligation specified in the contract has been paid, canceled or has expired, and b) Exchange financial instruments with substantially different terms. The Company recognizes in profit or loss, any difference between the carrying amount of the financial liability and the consideration paid, including any transferred asset different from cash and liabilities assumed.

(ii) The most significant basic financial instruments maintained by the Company and

its measurement are:

• Trade receivable

Most of the sales are made under normal credit terms and the amounts of the accounts receivable do not have interests. At the end of each reported period, the carrying amounts of trade debtors and other receivables are reviewed to determine whether there is any objective evidence that they will not be recoverable. If so, any impairment losses are immediately recognized in profit or loss.

• Borrowing, commercial debts

The borrowings are obligations based on the conditions of normal credit and have no interest. The amounts of the borrowings in foreign currency are converted into the functional currency using the exchange rate in effect on the reporting date. Gains and losses for foreign exchange are included in other expenses or in other income

• Cash and Cash equivalents

Cash and cash equivalents comprise cash balances and call deposits with maturities of three months or less from the acquisition date that are subject to an insignificant risk of changes in their fair value and are used by the Company in the management of its short-term commitments.

18

• Derivative Financial Instruments and Hedge Accounting

i) Derivative Financial Instruments

The Company uses forward hedging contracts to manage its exposure to currency risk in foreign currency. Such financial instruments are recognized at fair value on the date the derivative contract is made and are subsequently measured at their fair value at the end of the reporting period. The resulting gain or loss is immediately recognized in gains or losses.

ii) Fair Value Hedges

Changes in the fair value of derivatives that are designated and qualified as fair value hedges are recognized immediately in gains or losses, together with any changes in the fair value of the hedged asset or liability that are attributable to the hedged risk. The change in the fair value of the hedging instrument and the change in the hedged item attributable to the hedged risk are recognized in gains or losses in the item relating to the hedged item. Hedge accounting is discontinued when the Company revokes the hedging relationship, the hedging instrument expires or is sold, terminated, or exercised, or fails to comply with the criteria for hedge accounting. Any fair value adjustments to the carrying amount of the hedged item derived from the hedged risk is amortized in gains or losses as of that date.

(d) Share Capital - Common Shares

The ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares are recognized as a deduction from equity net of any related tax benefit. Income tax related to transaction costs is accounted for in accordance with section 29 - Income Tax.

(e) Property, Plant and Equipment

(i) Recognition and measurement

The item of property, plant and equipment are initially measured at cost less accumulated

depreciation and any accumulated impairment losses. The cost includes expenses that are

directly attributable to the acquisition of the asset, to the process of making the asset fit for

its intended use; the location of the asset in the site and in the necessary conditions and to

dismantle, remove and rehabilitate the site where they are located.

The cost includes expenses that are directly attributable to the acquisition of the asset, to the

process of making the asset fit for its intended use; the location of the asset in the site and

in the necessary conditions and to dismantle, remove and rehabilitate the site where they

are located.

Any gain and loss on derecognition of an item of property, plant and equipment is recognized

in profit or loss.

19

(ii) Depreciation

Depreciation is calculated on the depreciable amount, or another amount that is replaced by the cost, which correspond to the asset cost, less its residual values. Depreciation is recognized in profit or loss based on the straight -line depreciation method.

The estimated shelf lives for the current and comparative periods are as follows:

Class / Category Shelf Life

(Years)

Buildings 30

Planta and Equipment 15

Furniture and fixtures 5

Data processing and Equipment 5

Vehicles 10

Land is not depreciated. The shelf life, depreciation methods, and residual values are reviewed and adjusted at the closing date of the reporting period, if appropriate.

(f) Leases

Assets held by the Company under leases are operative payments made under these leases

are recognized in profit or loss on a straight-line basis over the term.

Determining Whether an Agreement Contains a Lease

When the Company enters into a contract, it determines whether the agreement corresponds to, or contains a lease based on the essence of the agreement at the date of its conclusion, whether compliance with the agreement depends on the use of one or more specific assets, or if the agreement grants the right to use the asset, even if such right is not implicitly specified in the agreement. The Company as a Lessee Leases in which the lessor retains a significant part of the risks and rewards of ownership are classified as operating leases. Operating lease payments (net of any incentive received from the lessor) are recognized as an operating lease expense in the income statement on a straight-line basis over the lease period. The Company takes on lease certain property, plant, and equipment items. Property, plant, and equipment leases in which the Company substantially has all the risks and benefits derived from the property are classified as financial leases. Financial leases are capitalized at the lower of the fair value of the leased asset and the present value of the minimum lease payments at the inception of the lease. Each lease payment is distributed between the liability and the financial burden. The corresponding lease obligations, net of financial charges, are included in accounts payable called loans. The interest portion of the financial burden is recognized as financial costs in the income statement during the period of the lease, in order to obtain a constant periodic interest rate on the debt pending amortization in each period.

20

Property, plant, and equipment acquired through financial leasing are depreciated throughout their shelf lives. However, if there is no reasonable assurance that the Company will obtain the property at the end of the lease term, the asset will depreciate during the shorter period between its estimated shelf life or the lease term.

(g) Intangibles

Intangible assets acquired separately are initially measured at cost, that is, those incurred for their acquisition and to put the program and/or specific license into use. After initial recognition, intangible assets are accounted for at cost less accrued depreciation and any accrued impairment losses, if any.

Subsequent disbursements are capitalized only when the future economic benefits incorporated in the specific asset related to such disbursements increase. The estimated finite shelf lives for the current and comparative periods are as follows:

Class / Category Shelf Life

(Years)

Licenses and Computer Programs

3 - 5

Intangible assets with finite shelf lives are amortized on a straight-line basis over their estimated shelf lives and are reviewed to determine whether they had any impairment in value to the extent that there is any indication that the intangible asset may have suffered such impairment. The amortization period and method for an intangible asset with a finite shelf life are reviewed at least at the close of each reporting period. Changes in the expected shelf life or the expected consumption pattern of the asset are accounted for when the amortization period or method is modified, as appropriate, and are treated prospectively as changes in accounting estimates. The amortization expense of intangible assets with finite shelf lives is recognized in the income statement. Gains or losses arising from derecognition of an intangible asset are measured as the difference between the net ingredient from the sale and the carrying amount of the asset and are recognized in the income statement when the respective asset is derecognized.

(h) Prepaid Expenses

Expenses paid in advance correspond to insurance policies, goods, and services that provide rights and benefits in subsequent periods. These costs are amortized over a period of time during which it is expected to obtain the benefits associated therewith and are recognized as an expense in the income statement.

(i) Impairment of assets

At each closing date of the reporting period, the Company evaluates whether there is any indication that an asset may present impairment loss. If such an indication exists, or when an annual impairment test for an asset is required, the Company estimates the recoverable amount of that asset. The recoverable amount of an asset is the higher of the fair value less sales costs, be it from an asset or from a cash-generating unit, and its value in use; and is determined as an individual asset, unless the asset does not generate cash flows which are substantially independent of those of other assets or groups of assets.

21

When the carrying amount of an asset or a cash-generating unit exceeds its recoverable amount, the asset is considered impaired and its value is reduced to its recoverable amount. When assessing the in use value of an asset, the estimated cash flows are discounted at their present value through a pre-tax discount rate which reflects current market assessments of the time value of money and the specific risks of the asset. For the determination of fair value less sales costs, recent transactions of the main market, if any, are taken into account. If this type of transactions can not be identified, a valuation model that is appropriate, taking into account the most advantageous market, is used. Impairment losses relating to continuing transactions are recognized on the income statement in those categories of expenses that correspond to the impairment of the asset. The possible reversal of impairment losses on nonfinancial assets suffering an impairment loss is reviewed on all dates on which financial information is submitted. The reversal is limited in such a way that the carrying amount of the asset does not exceed its recoverable amount, nor does it exceed the carrying amount that would have been determined, net of depreciation, if an impairment loss had not been recognized for that asset in previous years. Such reversal is recognized in the income statement.

(j) Employees' benefits

Short-term employee benefits Short term benefits to employees, which are employees’ benefits (other than termination benefits) whose payment be totally made in the term of twelve months following the end of the period in which employees have rendered their services. Defined Termination Benefits Termination benefits are recognized as an expense when the Company has committed to a formal detailed plan, either to terminate the employee's contract before the normal retirement age, or to provide termination benefits as a result of an offer made to encourage voluntary resignation. Termination benefits in the case of voluntary resignation are recognized as an expense if the Company has made an offer encouraging the voluntary resignation, and it is likely that the offer is accepted and the number of employees that can be reliably estimated.

(k) Provisions and contingencies

A provision is recognized if is result of a past event, the Company has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected cash flow to the rate before taxes which reflect the current market measurements of the time value of money and the specific risks attached to the obligation. The unwinding of the discount is recognized as finance cost.

Warranties Provisions for warranty-related costs are recognized when the product is sold. The initial recognition is based on the best estimate, by the Administration, of the disbursements required to settle the obligation. The initial estimate of costs relating to guarantees is reviewed annually.

22

(l) Revenues from regular activities

Income from ordinary activities is recognized to the extent that economic benefits are likely to flow to the Company and a reliable measurement thereof can be made, regardless of when the payment is made. Revenue is measured at the fair value of the consideration received or receivable, taking into account contractually defined payment terms and excluding taxes. Revenues are reduced by discounts, rebates, and other similar allowances estimated for customers. Sale of Goods Revenue from ordinary activities from the sale of motorcycles is recognized when the significant risks and the inherent advantages of ownership have been substantially transferred to the buyer, which usually occurs at the time of delivery. Interest For all financial instruments measured at amortized cost, interest earned is recorded using the effective interest rate method, which is the interest rate that accurately establishes the future flow of payments or cash receipts estimated over the expected period of validity of the financial instrument, or a shorter period, as the case may be, with respect to the asset's net carrying amount. Interest earned is included on the financial income line on the income statement.

(m) Taxes

a) Income tax

The income tax includes and represents the sum of current tax and deferred tax.

b) Current tax

It is the tax payable for tax gains for the current period or from prior periods.

A current tax is measured using tax rates and legislation that have been approved, or whose approval process is virtually complete, on the delivery date.

c) Deferred tax

Deferred tax is the tax payable or recoverable in future periods, generally, as a result of the Company recovering or liquidating its assets and liabilities for its current carrying amount. It is generated in the same way by the offsetting of losses or tax credits not used up to the moment from previous periods. Deferred tax is recognized based on the temporary differences that arise between the carrying amounts of the assets and liabilities in the financial statements and their corresponding tax bases. Deferred tax liabilities are recognized for all temporary differences that are expected to increase future taxable income. Deferred tax assets are recognized for all temporary differences that are expected to reduce future taxable income and additionally, any unused tax loss or tax credit. Deferred taxes assets and liabilities are measured using tax rates and tax legislation that have been approved, or whose approval process is virtually complete, on the reporting date. The measurement of deferred tax assets and liabilities will reflect the tax consequences that

23

would arise from the manner in expected by the Company on the date on which it is reported, to recover or settle the carrying amount of related assets and liabilities.

The tax base of an asset is the amount that will be deductible from the economic benefits that, for tax purposes, the Company obtains in the future, when it recovers the carrying amount of said asset. If such economic benefits are not taxed, the tax base of the asset will be equal to its book value. The tax base of a liability is equal to its carrying amount less any amount that is tax deductible with respect to that liability in future periods. Temporary differences are those that exist between the carrying amount of an asset or liability in the statement of financial position and its tax base. A deferred tax asset will be recognized for all deductible temporary differences, to the extent that it is probable that the Company will have future taxable profits against which to use those deductible temporary differences, unless the asset arises from the initial recognition of an asset or passive in a transaction that:

(a) It is not a business combination; and

(b) At the time it was made, it did not affect either the accounting profit or the tax gain

(loss).

An Company will recognize a deferred tax asset for all deductible temporary differences arising from investments in subsidiaries, branches and associates, or interests in joint ventures, only to the extent that it is probable that:

(b) Temporary differences revert in the foreseeable future; and

(d) Taxable profits are available against which these temporary differences may be used. Presentation

Deferred tax liabilities and assets will be recognized as non-current.

Compensation Current tax assets and liabilities or deferred tax assets and liabilities are offset only when there is a legally enforceable right to offset the amounts and can be demonstrated without effort or disproportionate cost that it is intended to liquidate them in net terms or to realize the asset and liquidate the liability simultaneously.

(n) Contingent Assets and Liabilities

In the normal course of transactions, the Company may generate contingent assets and liabilities understood as those rights of a possible nature arising as a result of past events and whose existence shall be confirmed only by the occurrence or non-occurrence of one or more uncertain future events which are not wholly under the control of the Company.

(o) Contingent Liabilities

Contingent liabilities are recognized in the financial statements when it is virtually certain or probable that the Company has an outflow of resources that incorporate economic benefits to settle the obligation, and the amount has been estimated reliably. In case the contingency is possible, the respective disclosure is made in the financial statements.

24

(p) Contingent Assets

The Company does not recognize any type of contingent assets until the same loses its contingent nature.

(q) Classification of Current and Non-Current Items

The Company submits the assets and liabilities in the statement of financial position classified as current and non-current. An asset and a liability are classified as current when the Company expects to realize or settle it in its normal operating cycle, respectively, or twelve months after the reporting period and maintain it for trading purposes.

If the asset is cash or equivalent to unrestricted cash and the liability does not have an unconditional right to defer settlement for a minimum period of twelve months, respectively, they are also classified as current.

All other assets and liabilities are classified as non-current, including deferred tax, in all cases.

3. Property, plant and equipment

Balances in books of property plant and equipment at March 31, is as follows:

Land Buildings Plant and equipment

Furniture and

fixtures Vehicles

Data Processing equipment

Total

At cost At April 1, 2017 9.648.531 47.915.579 19.141.848 1.044.960 1.080.715 772.509 79.604.142

Additions - 49.237 - 217.187 152.075 20.220 438.719 Disposals - - - 87.749 - 87.749 Less: Adjustments - 430.888 (430.888) - - - -

At March 31, 2018 9.648.531 48.395.704 18.710.960 1.262.147 1.145.041 792.729 79.955.112

Additions - - 283.842 - 62.413 23.037 369.291 Disposals - - - - 35.535 - 35.535

At March 31, 2019 9.648.531 48.395.704 18.994.801 1.262.147 1.171.919 815.766 80.288.868

Accumulated depreciation At April 1, 2017 - 2.314.691 1.690.840 339.508 213.439 354.343 4.912.820

Depreciation expense - 1.766.407 1.304.449 278.839 90.987 273.424 3.714.107 Less: Adjustments 34.272 - - (25.109) - 9.163

At March 31, 2018 - 4.115.370 2.995.289 618.347 279.317 627.767 8.636.090

Depreciation expense - 1.527.624 1.230.458 255.587 161.387 118.262 3.293.318 Less: Adjustments - - - (11.595) - (11.595)

At March 31, 2019 - 5.603.713 4.226.181 873.983 421.703 792.233 11.917.813

Carrying amount At April 1, 2017 9.648.531 45.600.888 17.451.008 705.452 867.276 418.166 74.691.322

At March 31, 2018 9.648.531 44.280.334 15.715.671 643.800 865.724 164.962 71.319.022

At March 31, 2019 9.648.531 42.791.991 14.768.620 388.165 750.216 23.532 68.371.055

25

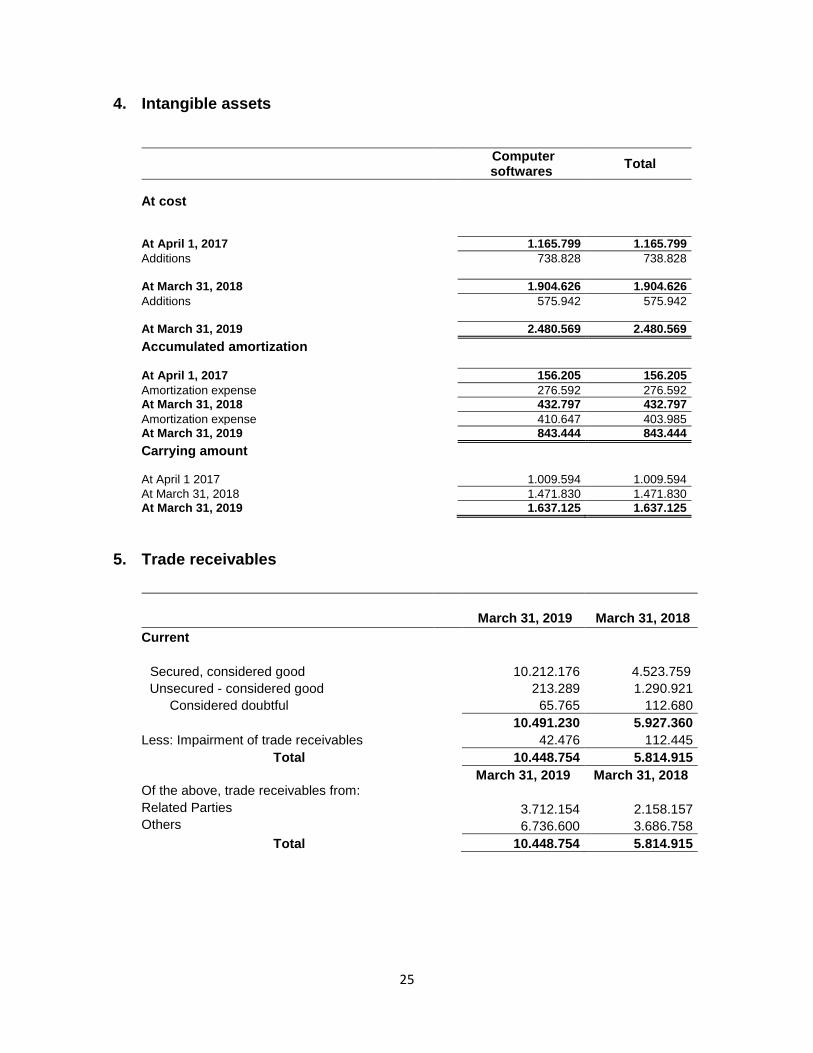

4. Intangible assets

Computer softwares

Total

At cost At April 1, 2017 1.165.799 1.165.799

Additions 738.828 738.828

At March 31, 2018 1.904.626 1.904.626

Additions 575.942 575.942

At March 31, 2019 2.480.569 2.480.569

Accumulated amortization At April 1, 2017 156.205 156.205

Amortization expense 276.592 276.592

At March 31, 2018 432.797 432.797

Amortization expense 410.647 403.985

At March 31, 2019 843.444 843.444

Carrying amount At April 1 2017 1.009.594 1.009.594

At March 31, 2018 1.471.830 1.471.830

At March 31, 2019 1.637.125 1.637.125

5. Trade receivables

March 31, 2019 March 31, 2018

Current

Secured, considered good 10.212.176 4.523.759

Unsecured - considered good 213.289 1.290.921

Considered doubtful 65.765 112.680

10.491.230 5.927.360

Less: Impairment of trade receivables 42.476 112.445

Total 10.448.754 5.814.915

March 31, 2019 March 31, 2018 Of the above, trade receivables from: Related Parties 3.712.154 2.158.157 Others 6.736.600 3.686.758

Total 10.448.754 5.814.915

26

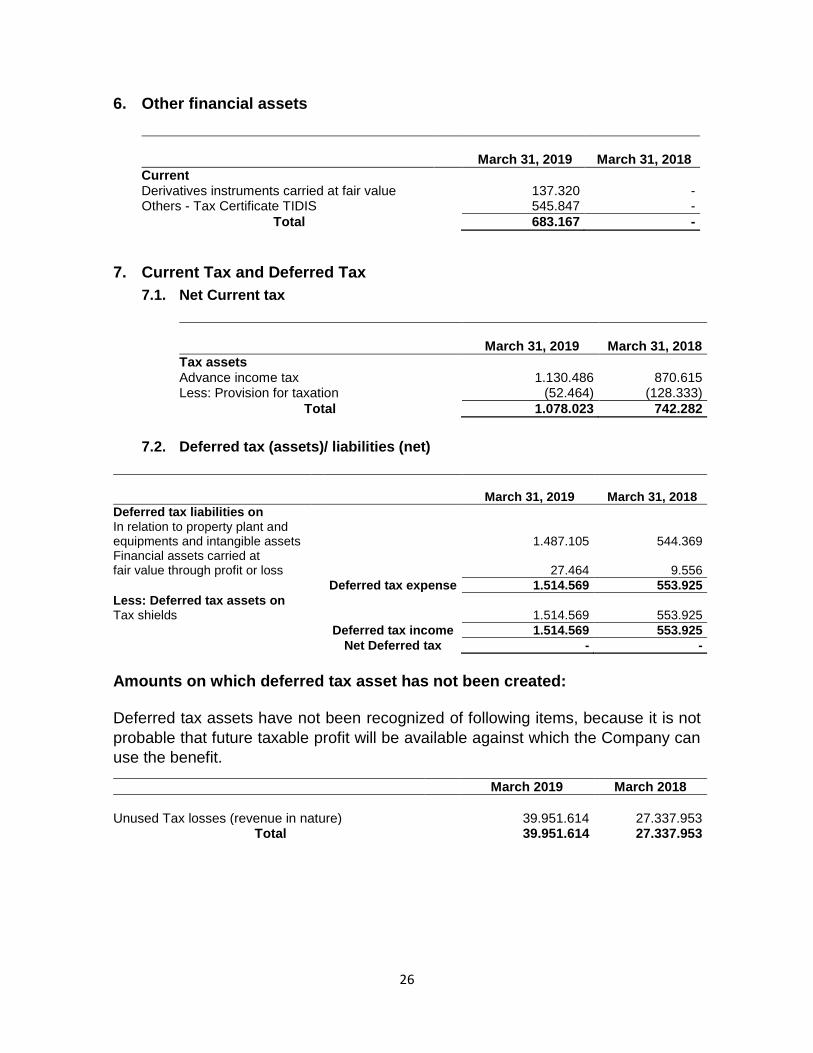

6. Other financial assets

March 31, 2019 March 31, 2018

Current

Derivatives instruments carried at fair value 137.320 - Others - Tax Certificate TIDIS

545.847 -

Total 683.167 -

7. Current Tax and Deferred Tax

7.1. Net Current tax

March 31, 2019 March 31, 2018

Tax assets Advance income tax 1.130.486 870.615 Less: Provision for taxation (52.464) (128.333)

Total 1.078.023 742.282

7.2. Deferred tax (assets)/ liabilities (net)

March 31, 2019 March 31, 2018

Deferred tax liabilities on In relation to property plant and equipments and intangible assets 1.487.105 544.369 Financial assets carried at fair value through profit or loss 27.464

9.556

Deferred tax expense 1.514.569 553.925

Less: Deferred tax assets on Tax shields

1.514.569 553.925

Deferred tax income 1.514.569 553.925

Net Deferred tax - -

Amounts on which deferred tax asset has not been created: Deferred tax assets have not been recognized of following items, because it is not

probable that future taxable profit will be available against which the Company can

use the benefit.

March 2019 March 2018

Unused Tax losses (revenue in nature) 39.951.614 27.337.953

Total 39.951.614 27.337.953

27

8. Other current assets

March 31, 2018 March 31, 2018

Current

Unsecured, considered good Prepaid expenses 125.301 100.317

Other advances 288.959 386.881

Balance with Government authorities

VAT/ sales tax 215.721 158

Total 629.981 487.356

9. Inventories

March 31, 2019 March 31, 2018

Raw materials 15.480.590 3.009.609

Goods in transit of raw materials 8.807.401 8.069.492

Work in progress (Two wheelers) 29.677 230.184

Finished goods Two wheelers 3.563.094 2.215.852

Stores and spares 2.556.502 194.359

Total 30.437.264 13.719.496

The cost of inventories recognized as an expense during the year in respect of continuing operations was COP $47.816.320 (March 31, 2018 COP $43.799.821). The cost of inventories reconised as an expense include is respect of write – down of inventory to net realizable value and has been reduced by is respect of the reversal of such write downs. Previous write - downs have been reversed as a result of increased sales price in certain market. Out of the total inventories, COP $30.437.264 (March 31, 2018 COP $13.719.496), the carrying amount of inventories carried at fair value less costs to sell.

10. Cash and cash equivalents

March 31, 2019 March 31, 2018

Cash on hand 9.937 8.980

Balances with banks

In current accounts

4.928.905 5.489.578

Cash and cash equivalents 4.938.842 5.498.558

28

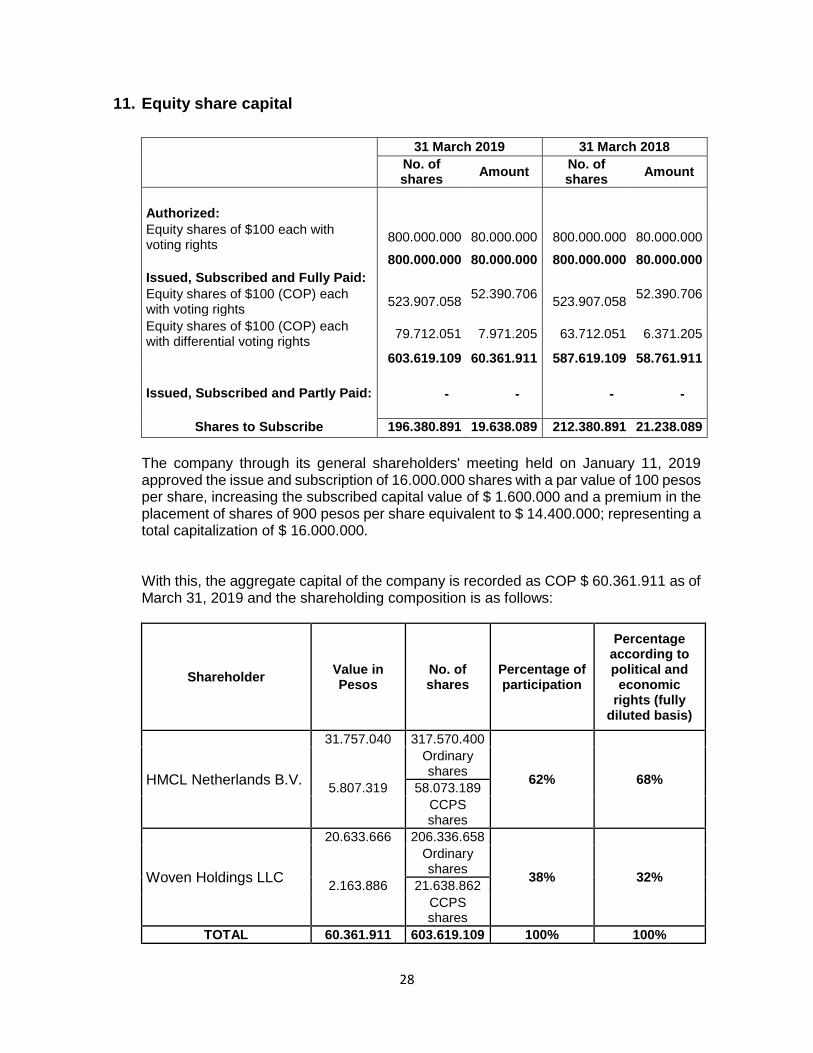

11. Equity share capital

31 March 2019 31 March 2018

No. of shares

Amount No. of shares

Amount

Authorized:

Equity shares of $100 each with voting rights

800.000.000 80.000.000 800.000.000 80.000.000

800.000.000 80.000.000 800.000.000 80.000.000

Issued, Subscribed and Fully Paid:

Equity shares of $100 (COP) each with voting rights

523.907.058 52.390.706

523.907.058 52.390.706

Equity shares of $100 (COP) each with differential voting rights

79.712.051 7.971.205 63.712.051 6.371.205

603.619.109 60.361.911 587.619.109 58.761.911

Issued, Subscribed and Partly Paid: - - - -

Shares to Subscribe 196.380.891 19.638.089 212.380.891 21.238.089

The company through its general shareholders' meeting held on January 11, 2019 approved the issue and subscription of 16.000.000 shares with a par value of 100 pesos per share, increasing the subscribed capital value of $ 1.600.000 and a premium in the placement of shares of 900 pesos per share equivalent to $ 14.400.000; representing a total capitalization of $ 16.000.000. With this, the aggregate capital of the company is recorded as COP $ 60.361.911 as of March 31, 2019 and the shareholding composition is as follows:

Shareholder Value in Pesos

No. of shares

Percentage of participation

Percentage according to political and

economic rights (fully

diluted basis)

HMCL Netherlands B.V.

31.757.040 317.570.400

62% 68%

Ordinary shares

5.807.319 58.073.189

CCPS shares

Woven Holdings LLC

20.633.666 206.336.658

38% 32%

Ordinary shares

2.163.886 21.638.862

CCPS shares

TOTAL 60.361.911 603.619.109 100% 100%

29

The shares with an annual fixed dividend obligatorily convertible into ordinary shares “CCPS” will have a fixed non-cumulative annual dividend of 5%. The CCPS Will be compulsorily convertible into ordinary shares of the Company within ten (10) years from the date of issuance. This period may be modified by the decision of the Board of Directors at it may deem necessary. Each CCPS will be compulsorily converted into ten (10) ordinary shares at the time of conversion. For this conversion, the Board will issue the corresponding rules for the subscription of CCPS and will instruct the legal representative to inform the CCPS holders of the fulfilment of the term and the corresponding conversion of the CCPS into ordinary shares. No further authorization will be required from the CCPS holders for the conversion. Each CCPS will grant ten (10) voting right per share, to the CCPS holders on a fully diluted basis, in the General Assembly of Shareholders. In addition, the CCPS would have the non-cumulative right to participate in the profits of the Company in the same proportion established as voting rights in this article (fully diluted basis). At the time of a liquidation event of the Company, CCPS will be entitled to the liquidation proceeds, at par with the ordinary shares of the Company, on a fully diluted basis.

12. Non – Current borrowings

Rate of Interest

Maturity March 2019 March 2018

Unsecured Borrowings - at amortized Cost

Bonds / Debentures Term Loans (1) From Banks Bancolombia, Preoperative DTF 2022 10.312.500 16.211.341 Long term maturities of Finance Lease Obligations

Banco de Occidente, Cars DTF 2019 - 55.021 Bancolombia, Cars DTF 2021 34.317 75.268 Bancolombia, Machinery DTF 2024 16.500.000 16.508.863 Bancolombia, Building DTF 2028 24.777.753 24.842.412

Total Unsecured Borrowings 51.624.570 57.692.905

Total Borrowings non-current 51.624.570 57.692.905

30

12.1. Details of long term borrowings of the Company

Description of the instrument Currency of Loan

Effective Interest Rate

used for Discounting Cashflows

Coupon Rate

Number of Installments

Date of Redemption

(or) Conversion

Amortised cost as at 31 March

2019

Amortised cost as at 31 March

2018

Term loans from banks:

Bancolombia 44558295 Preoperative COP DTF 5,40% 84 04/05/2022 1.125.000 2.035.382

Bancolombia 44577668 Preoperative COP DTF 5,40% 84 20/05/2022 1.125.000 2.035.066

Bancolombia 44582433 Preoperative COP DTF 5,40% 84 22/05/2022 718.750 1.526.299

Bancolombia 44595743 Preoperative COP DTF 5,40% 84 29/05/2022 1.531.250 2.543.832

Bancolombia 44598005 Preoperative COP DTF 5,40% 84 01/06/2022 1.937.500 3.026.536

Bancolombia 44731107 Preoperative COP DTF 5,40% 84 03/09/2022 3.875.000 5.044.227

Long-term maturities of finance lease obligations:

Boccidente 180-00111097 Vehicle COP DTF 5% 36 29-mar-19 - 36.329

Boccidente 180-00111713 Vehicle COP DTF 5% 36 31-mar-19 - 18.692

Bancolombia 191737 Vehicle COP DTF 6% 60 23-ago-21 34.317 75.268

Bancolombia 179153 Machinery COP DTF 4,70% 96 28-jun-24 16.500.000 16.508.863

Bancolombia 177862 Building COP DTF 5,35% 144 21-oct-28 24.777.753 24.842.412

Total Unsecured 51.624.570 57.692.905

13. Trade Payables

31 March 2019 31 March 2018

Current Non

Current Current

Non Current

Trade payable - Micro ans small enterprises

9.798.348 - 593.997 -

Trade payable - Other than micro ans small enterprises

6.938.344 - 9.937.768 -

Total trade payables 16.736.692 - 10.531.765 -

14. Other Financial Liabilities

March 31, 2019 March 31, 2018

Other Financial Liabilities Measured at Fair value

Derivatives designated and effective as hedging instruments

- 647.202

Total other financial liabilities - 647.202

31

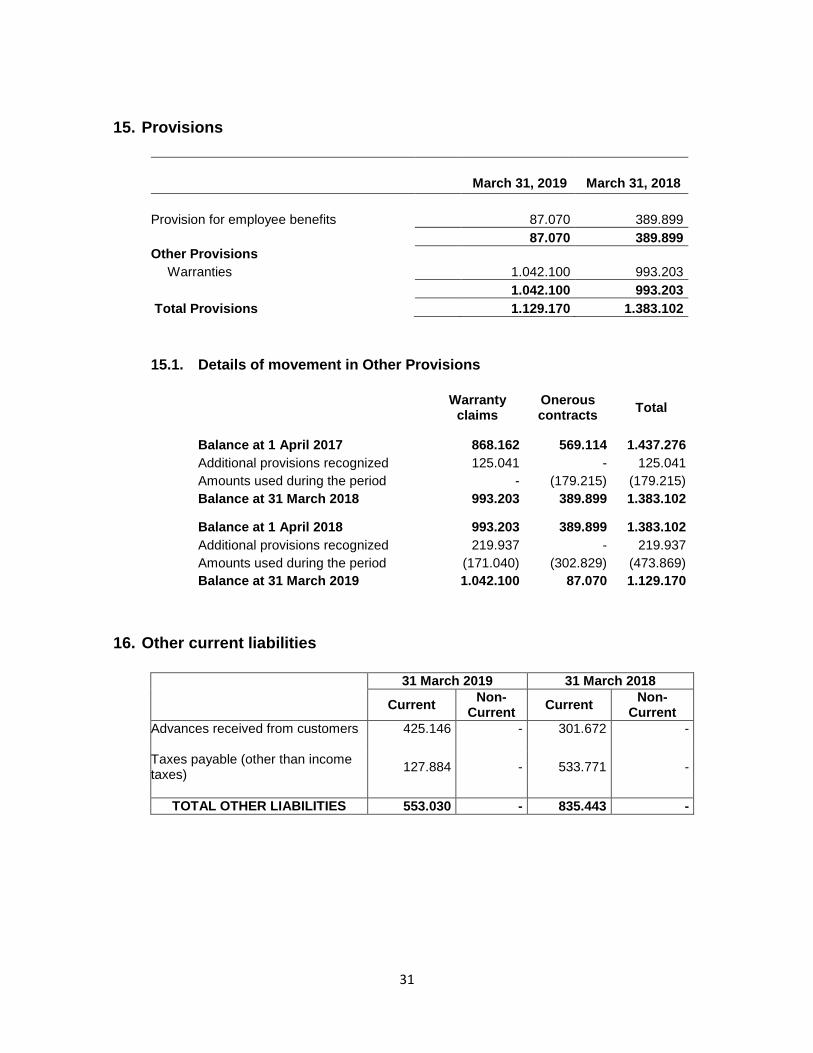

15. Provisions

March 31, 2019 March 31, 2018

Provision for employee benefits 87.070 389.899

87.070 389.899

Other Provisions

Warranties 1.042.100 993.203

1.042.100 993.203

Total Provisions 1.129.170 1.383.102

15.1. Details of movement in Other Provisions

Warranty

claims Onerous contracts

Total

Balance at 1 April 2017 868.162 569.114 1.437.276

Additional provisions recognized 125.041 - 125.041

Amounts used during the period - (179.215) (179.215)

Balance at 31 March 2018 993.203 389.899 1.383.102

Balance at 1 April 2018 993.203 389.899 1.383.102

Additional provisions recognized 219.937 - 219.937

Amounts used during the period (171.040) (302.829) (473.869)

Balance at 31 March 2019 1.042.100 87.070 1.129.170

16. Other current liabilities

31 March 2019 31 March 2018

Current Non-

Current Current

Non- Current

Advances received from customers 425.146 - 301.672 -

Taxes payable (other than income taxes)

127.884 - 533.771 -

TOTAL OTHER LIABILITIES 553.030 - 835.443 -

32

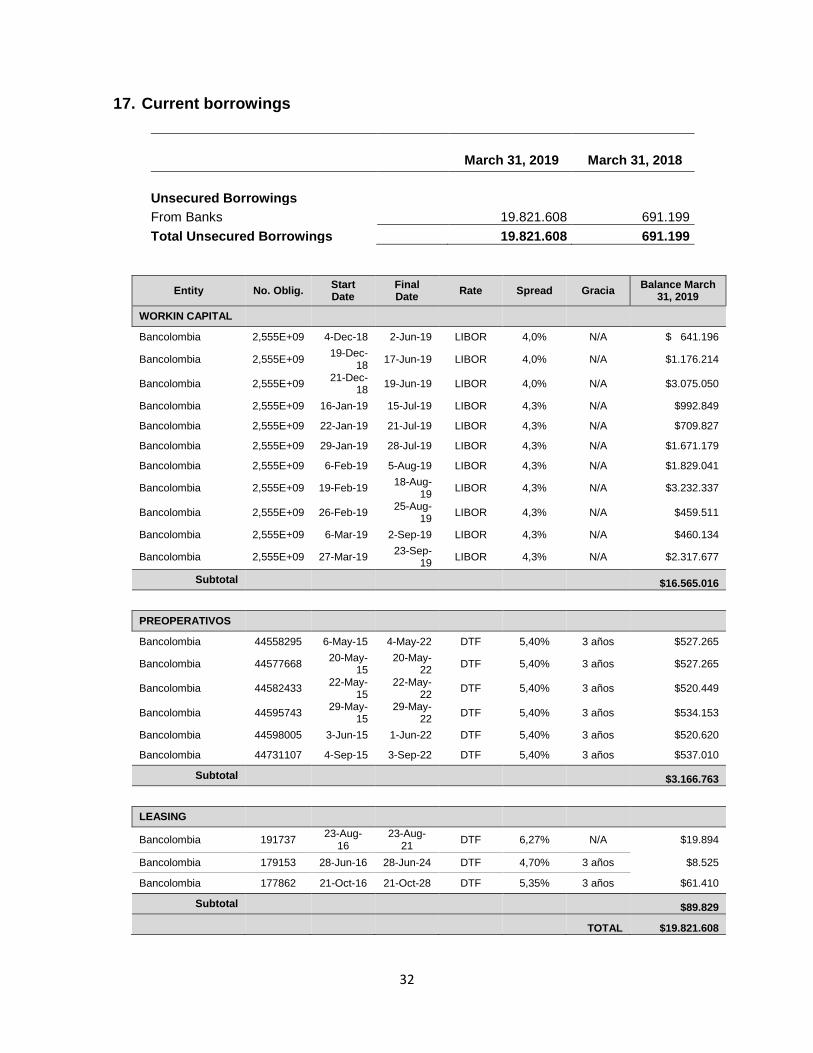

17. Current borrowings

March 31, 2019 March 31, 2018

Unsecured Borrowings

From Banks 19.821.608 691.199

Total Unsecured Borrowings 19.821.608 691.199

Entity No. Oblig. Start Date

Final Date

Rate Spread Gracia Balance March

31, 2019

WORKIN CAPITAL

Bancolombia 2,555E+09 4-Dec-18 2-Jun-19 LIBOR 4,0% N/A $ 641.196

Bancolombia 2,555E+09 19-Dec-

18 17-Jun-19 LIBOR 4,0% N/A $1.176.214

Bancolombia 2,555E+09 21-Dec-

18 19-Jun-19 LIBOR 4,0% N/A $3.075.050

Bancolombia 2,555E+09 16-Jan-19 15-Jul-19 LIBOR 4,3% N/A $992.849

Bancolombia 2,555E+09 22-Jan-19 21-Jul-19 LIBOR 4,3% N/A $709.827

Bancolombia 2,555E+09 29-Jan-19 28-Jul-19 LIBOR 4,3% N/A $1.671.179

Bancolombia 2,555E+09 6-Feb-19 5-Aug-19 LIBOR 4,3% N/A $1.829.041

Bancolombia 2,555E+09 19-Feb-19 18-Aug-

19 LIBOR 4,3% N/A $3.232.337

Bancolombia 2,555E+09 26-Feb-19 25-Aug-

19 LIBOR 4,3% N/A $459.511

Bancolombia 2,555E+09 6-Mar-19 2-Sep-19 LIBOR 4,3% N/A $460.134

Bancolombia 2,555E+09 27-Mar-19 23-Sep-

19 LIBOR 4,3% N/A $2.317.677

Subtotal $16.565.016

PREOPERATIVOS

Bancolombia 44558295 6-May-15 4-May-22 DTF 5,40% 3 años $527.265

Bancolombia 44577668 20-May-

15 20-May-

22 DTF 5,40% 3 años $527.265

Bancolombia 44582433 22-May-

15 22-May-

22 DTF 5,40% 3 años $520.449

Bancolombia 44595743 29-May-

15 29-May-

22 DTF 5,40% 3 años $534.153

Bancolombia 44598005 3-Jun-15 1-Jun-22 DTF 5,40% 3 años $520.620

Bancolombia 44731107 4-Sep-15 3-Sep-22 DTF 5,40% 3 años $537.010

Subtotal $3.166.763

LEASING

Bancolombia 191737 23-Aug-

16 23-Aug-

21 DTF 6,27% N/A $19.894

Bancolombia 179153 28-Jun-16 28-Jun-24 DTF 4,70% 3 años $8.525

Bancolombia 177862 21-Oct-16 21-Oct-28 DTF 5,35% 3 años $61.410

Subtotal $89.829

TOTAL $19.821.608

33

18. Revenue from operations (gross)

For the year ended

March 31, 2019 For the year

ended March 31, 2018

Sale of products Two wheelers 62.892.435 50.693.095

Spare parts 2.719.369 -

65.611.804 50.693.095

Income from services Services - others 2.382 3.219

2.382 3.219

Other operating revenue Miscellaneous income (1) 6.419.379 5.107.982

6.419.379 5.107.982

Total 72.033.565 55.804.296

(1) The Miscellaneus income comprise at March 31, 2019 and 2018 as follow:

For the year ended March

31, 2019

For the year ended March

31, 2018

Recovery from advertising $ 4.800.647 4.092.266

Recovery of provisions 1.066.710 602.057

Others 552.022 413.658

Total $ 6.419.379 5.107.982

19. Other income

For the year ended

March 31, 2019 For the year ended

March 31, 2018

Interest income on financial assets carried at amortized cost

592.537 249.981 Profit on sale of property, plant and equipments

7.428 9.908

Total 599.965 259.889

34

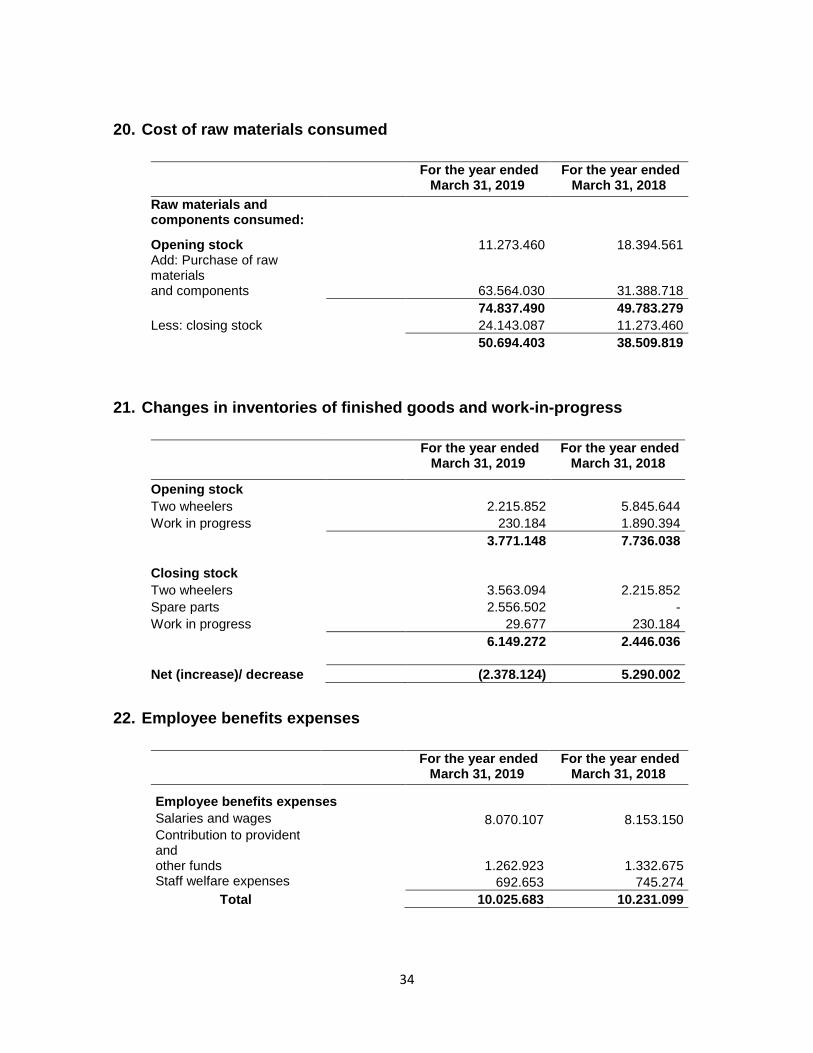

20. Cost of raw materials consumed

For the year ended

March 31, 2019 For the year ended

March 31, 2018

Raw materials and components consumed: Opening stock 11.273.460 18.394.561 Add: Purchase of raw materials and components 63.564.030 31.388.718

74.837.490 49.783.279

Less: closing stock 24.143.087 11.273.460

50.694.403 38.509.819

21. Changes in inventories of finished goods and work-in-progress

For the year ended

March 31, 2019 For the year ended

March 31, 2018

Opening stock Two wheelers 2.215.852 5.845.644

Work in progress 230.184 1.890.394

3.771.148 7.736.038

Closing stock Two wheelers 3.563.094 2.215.852

Spare parts 2.556.502 -

Work in progress 29.677 230.184

6.149.272 2.446.036

Net (increase)/ decrease (2.378.124) 5.290.002

22. Employee benefits expenses

For the year ended

March 31, 2019 For the year ended

March 31, 2018

Employee benefits expenses

Salaries and wages

8.070.107 8.153.150 Contribution to provident and other funds

1.262.923 1.332.675 Staff welfare expenses

692.653 745.274

Total 10.025.683 10.231.099

35

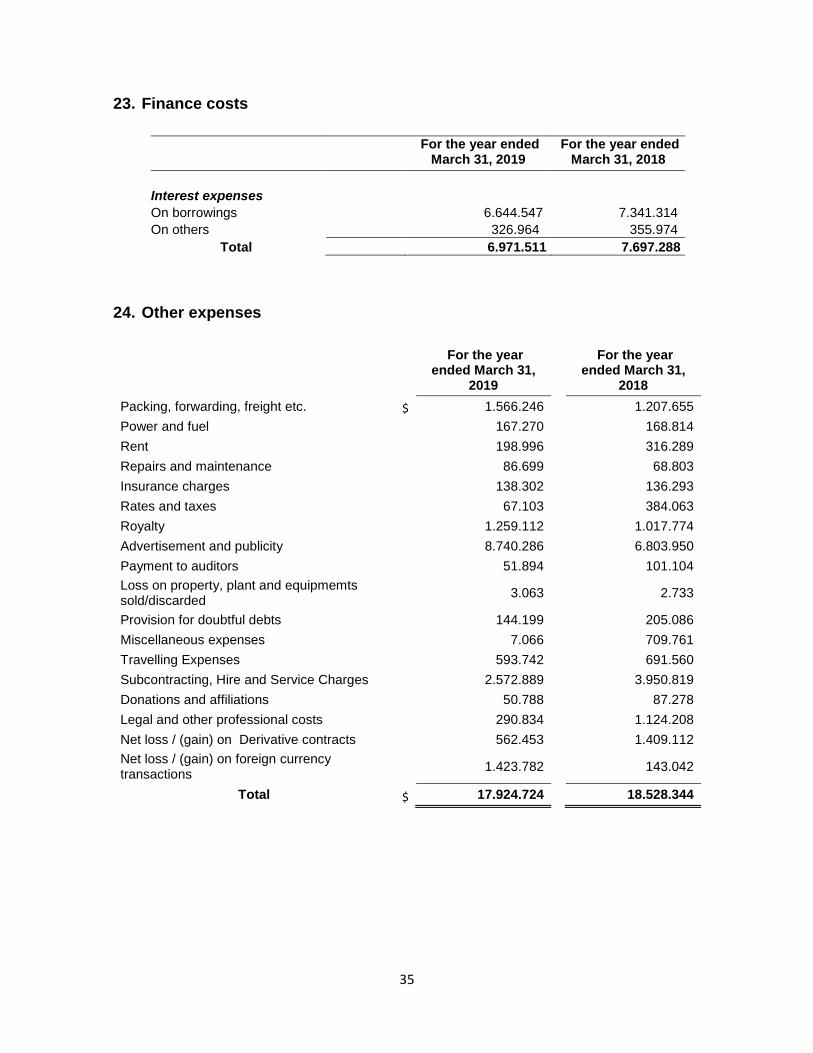

23. Finance costs

For the year ended

March 31, 2019 For the year ended

March 31, 2018

Interest expenses On borrowings 6.644.547 7.341.314

On others 326.964 355.974

Total 6.971.511 7.697.288

24. Other expenses

For the year

ended March 31, 2019

For the year

ended March 31, 2018

Packing, forwarding, freight etc. $ 1.566.246 1.207.655

Power and fuel 167.270 168.814

Rent 198.996 316.289

Repairs and maintenance 86.699 68.803

Insurance charges 138.302 136.293

Rates and taxes 67.103 384.063

Royalty 1.259.112 1.017.774

Advertisement and publicity 8.740.286 6.803.950

Payment to auditors 51.894 101.104

Loss on property, plant and equipmemts sold/discarded

3.063 2.733

Provision for doubtful debts 144.199 205.086

Miscellaneous expenses 7.066 709.761

Travelling Expenses 593.742 691.560

Subcontracting, Hire and Service Charges 2.572.889 3.950.819

Donations and affiliations 50.788 87.278

Legal and other professional costs 290.834 1.124.208

Net loss / (gain) on Derivative contracts 562.453 1.409.112

Net loss / (gain) on foreign currency transactions

1.423.782 143.042

Total $ 17.924.724 18.528.344

36

24.1. Payment to auditors

For the year ended

March 31, 2019 For the year ended

March 31, 2018

a)As Statutory Audit

-Audit fee 51.894 101.104

Total 51.894 101.104

25. Depreciation and amortization expenses

For the year ended March 31, 2019

For the year ended March 31, 2018

Depreciation expenses

Administration expenses 1.241.015 1.311.098

Selling expenses 337.874 175.546

Production Costs 1.714.429 2.227.463

Total 3.293.318 3.714.108

Amortization expenses

Administration expenses 406.886 269.550

Selling expenses 0 244

Production Costs 3.761 6.798

Total 410.647 276.592

Depreciation and amortization expenses

3.703.965 3.990.699

26. Production Costs

For the year ended March 31, 2019

For the year ended March 31, 2018

Personal expenses 4.158.342 4.431.845

Packing, forwarding, freight etc. 42.260 5.235

Power and fuel 609.446 553.187

Rent 18.470 16.736

Repairs and maintenance 404.154 276.945

Insurance charges 127.612 135.580

Rates and taxes 15.435 6.298

Travelling Expenses 34.701 47.791

Subcontracting, Hire and Service Charges

2.132.357 1.769.769

Donations and affiliations 202.504 291.710

Legal and other professional costs

5.588 16.654

Depreciation expenses 1.714.429 2.227.463

amortization expenses 3.761 6.798

Total 9.469.059 5.354.166

37

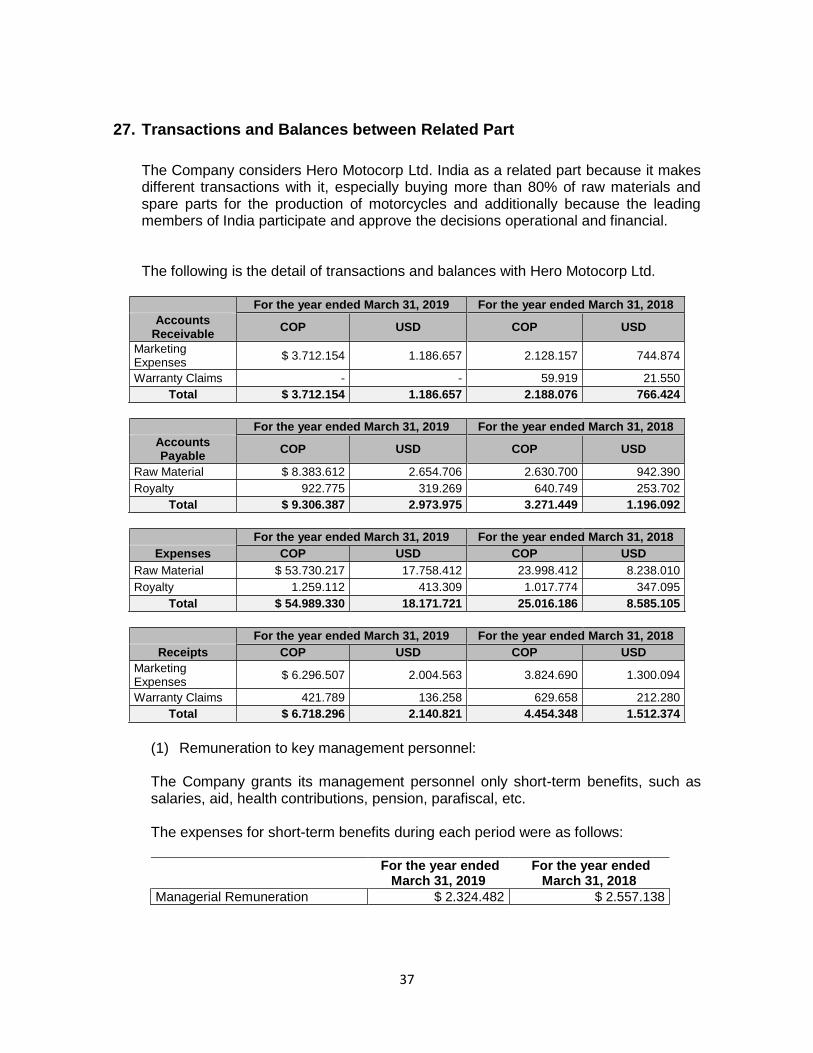

27. Transactions and Balances between Related Part

The Company considers Hero Motocorp Ltd. India as a related part because it makes different transactions with it, especially buying more than 80% of raw materials and spare parts for the production of motorcycles and additionally because the leading members of India participate and approve the decisions operational and financial.

The following is the detail of transactions and balances with Hero Motocorp Ltd.

For the year ended March 31, 2019 For the year ended March 31, 2018

Accounts Receivable

COP USD COP USD

Marketing Expenses

$ 3.712.154 1.186.657 2.128.157 744.874

Warranty Claims - - 59.919 21.550

Total $ 3.712.154 1.186.657 2.188.076 766.424

For the year ended March 31, 2019 For the year ended March 31, 2018

Accounts Payable

COP USD COP USD

Raw Material $ 8.383.612 2.654.706 2.630.700 942.390

Royalty 922.775 319.269 640.749 253.702

Total $ 9.306.387 2.973.975 3.271.449 1.196.092

For the year ended March 31, 2019 For the year ended March 31, 2018

Expenses COP USD COP USD

Raw Material $ 53.730.217 17.758.412 23.998.412 8.238.010

Royalty 1.259.112 413.309 1.017.774 347.095

Total $ 54.989.330 18.171.721 25.016.186 8.585.105

For the year ended March 31, 2019 For the year ended March 31, 2018

Receipts COP USD COP USD

Marketing Expenses

$ 6.296.507 2.004.563 3.824.690 1.300.094

Warranty Claims 421.789 136.258 629.658 212.280

Total $ 6.718.296 2.140.821 4.454.348 1.512.374

(1) Remuneration to key management personnel:

The Company grants its management personnel only short-term benefits, such as salaries, aid, health contributions, pension, parafiscal, etc.

The expenses for short-term benefits during each period were as follows:

For the year ended

March 31, 2019 For the year ended

March 31, 2018

Managerial Remuneration $ 2.324.482 $ 2.557.138

38

28. Going Concern

The company is in the growth phase, seeking to position the brand in the national and international market and in this way to get closer to the fulfillment of the installed capacity. For this reason, the company are making investments in the brand, improvement the market share, allowing our consumers to know more about of our motorcycles. It should be noted that the company is aligned with the projections of established losses.

According with the note 11 (Equity share capital), the company received a capitalization of the COP 16.000.000 to support the cash flow.