Embed Size (px)

Citation preview

Internal Control and Cash

Chapter 7

Copyright ©2014 Pearson Education, Inc. Publishing as Prentice Hall 7-1

Learning Objectives

1. Define internal control and describe the components of internal control and control procedures

2. Apply internal controls to cash receipts

3. Apply internal controls to cash payments

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-2

Learning Objectives

4. Explain and journalize petty cash transactions

5. Demonstrate the use of a bank account as a control device and prepare a bank reconciliation and related journal entries

6. Use the cash ratio to evaluate business performance

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-3

Learning Objective 1

Define internal control and describe the

components of internal control

and control procedures

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-4

What Is Internal Control?

• Safeguard assets• Encourage

employees to follow company policies

• Promote operational efficiency

• Ensure accurate, reliable accounting records

Internal Control is an

organizational plan and the

related measures designed to

accomplish the following:

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-5

Components of Internal ControlCRIME

• Control procedures

• Risk assessment

• Information system

• Monitoring of controls

• Environment

Under the Sarbanes-Oxley Act of 2002,

• Internal control reports are required for publicly

traded companies.• The Public Company Accounting Oversight

Board was created.• Stiff penalties were

established for financial statement fraud.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-6

Internal Control Procedures

• Competent reliable and ethical personnel

• Assignment of responsibilities Separation of Duties

• Audits• Documents• Electronic devices

• E-Commerce– Firewalls, Encryption,

Passwords, and Digital Signatures

• Other Controls– Fireproof vaults– Alarms– Job rotation

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-7

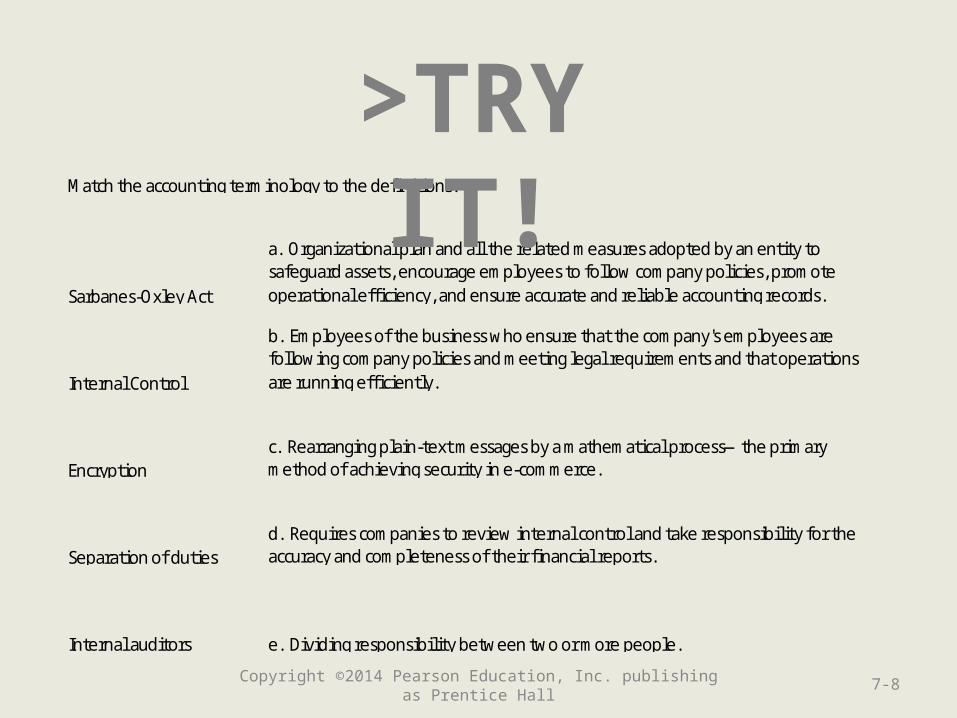

Sarbanes-Oxley Act

a. Organizational plan and all the related measures adopted by an entity to safeguard assets, encourage employees to follow company policies, promote operational effi ciency, and ensure accurate and reliable accounting records.

Internal Control

b. Employees of the business who ensure that the company's employees are following company policies and meeting legal requirements and that operations are running effi ciently.

Encryptionc. Rearranging plain-text messages by a mathematical process—the primary method of achieving security in e-commerce.

Separation of dutiesd. Requires companies to review internal control and take responsibility for the accuracy and completeness of their financial reports.

Internal auditors e. Dividing responsibility between two or more people.

Match the accounting terminology to the definitions.

>TRY IT!

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-8

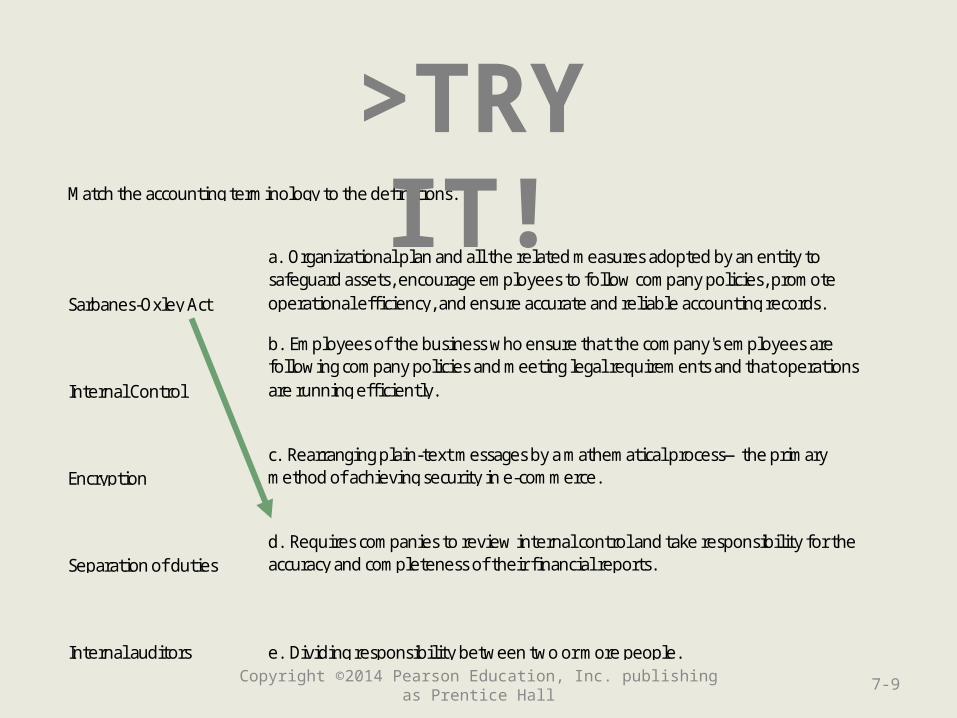

Sarbanes-Oxley Act

a. Organizational plan and all the related measures adopted by an entity to safeguard assets, encourage employees to follow company policies, promote operational effi ciency, and ensure accurate and reliable accounting records.

Internal Control

b. Employees of the business who ensure that the company's employees are following company policies and meeting legal requirements and that operations are running effi ciently.

Encryptionc. Rearranging plain-text messages by a mathematical process—the primary method of achieving security in e-commerce.

Separation of dutiesd. Requires companies to review internal control and take responsibility for the accuracy and completeness of their financial reports.

Internal auditors e. Dividing responsibility between two or more people.

Match the accounting terminology to the definitions.

>TRY IT!

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-9

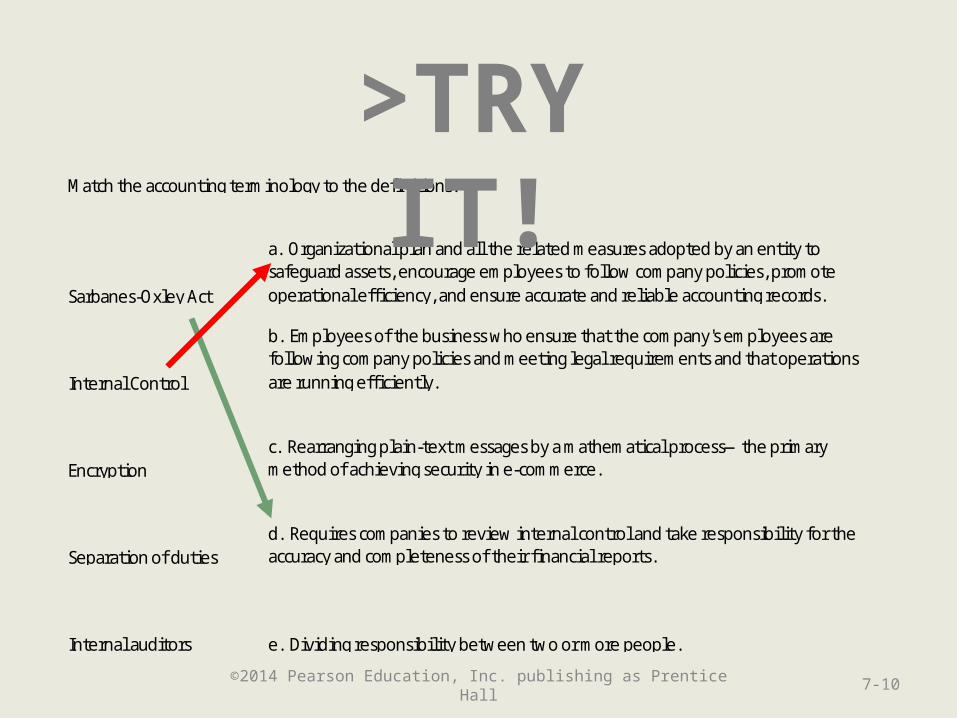

Sarbanes-Oxley Act

a. Organizational plan and all the related measures adopted by an entity to safeguard assets, encourage employees to follow company policies, promote operational effi ciency, and ensure accurate and reliable accounting records.

Internal Control

b. Employees of the business who ensure that the company's employees are following company policies and meeting legal requirements and that operations are running effi ciently.

Encryptionc. Rearranging plain-text messages by a mathematical process—the primary method of achieving security in e-commerce.

Separation of dutiesd. Requires companies to review internal control and take responsibility for the accuracy and completeness of their financial reports.

Internal auditors e. Dividing responsibility between two or more people.

Match the accounting terminology to the definitions.

>TRY IT!

©2014 Pearson Education, Inc. publishing as Prentice Hall 7-10

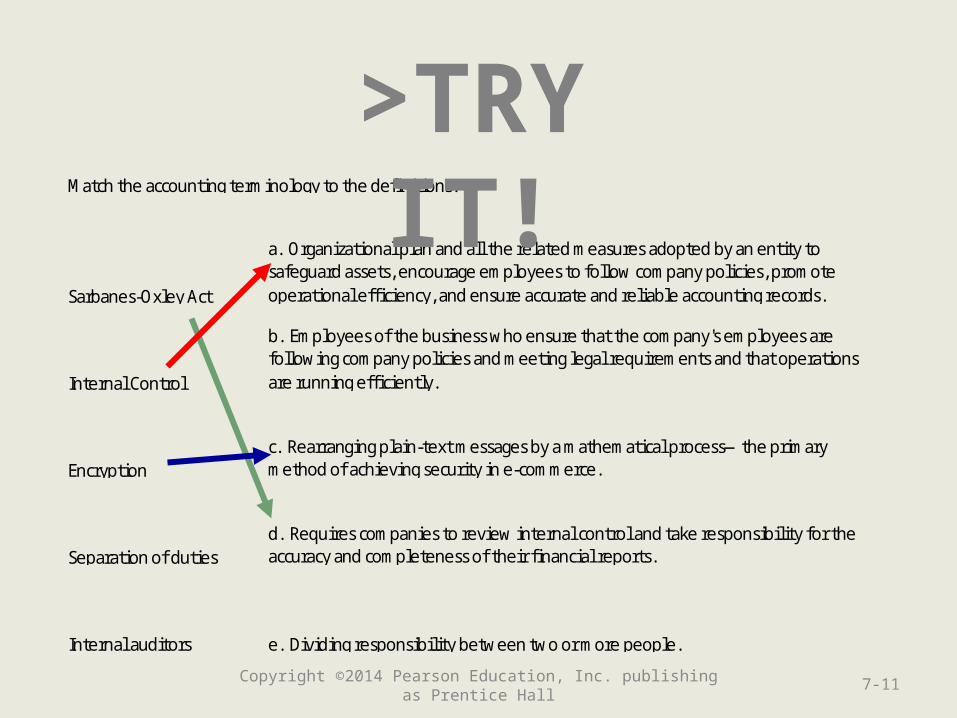

Sarbanes-Oxley Act

a. Organizational plan and all the related measures adopted by an entity to safeguard assets, encourage employees to follow company policies, promote operational effi ciency, and ensure accurate and reliable accounting records.

Internal Control

b. Employees of the business who ensure that the company's employees are following company policies and meeting legal requirements and that operations are running effi ciently.

Encryptionc. Rearranging plain-text messages by a mathematical process—the primary method of achieving security in e-commerce.

Separation of dutiesd. Requires companies to review internal control and take responsibility for the accuracy and completeness of their financial reports.

Internal auditors e. Dividing responsibility between two or more people.

Match the accounting terminology to the definitions.

>TRY IT!

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-11

Sarbanes-Oxley Act

a. Organizational plan and all the related measures adopted by an entity to safeguard assets, encourage employees to follow company policies, promote operational effi ciency, and ensure accurate and reliable accounting records.

Internal Control

b. Employees of the business who ensure that the company's employees are following company policies and meeting legal requirements and that operations are running effi ciently.

Encryptionc. Rearranging plain-text messages by a mathematical process—the primary method of achieving security in e-commerce.

Separation of dutiesd. Requires companies to review internal control and take responsibility for the accuracy and completeness of their financial reports.

Internal auditors e. Dividing responsibility between two or more people.

Match the accounting terminology to the definitions.

>TRY IT!

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 7-12

Sarbanes-Oxley Act

a. Organizational plan and all the related measures adopted by an entity to safeguard assets, encourage employees to follow company policies, promote operational effi ciency, and ensure accurate and reliable accounting records.

Internal Control

b. Employees of the business who ensure that the company's employees are following company policies and meeting legal requirements and that operations are running effi ciently.

Encryptionc. Rearranging plain-text messages by a mathematical process—the primary method of achieving security in e-commerce.

Separation of dutiesd. Requires companies to review internal control and take responsibility for the accuracy and completeness of their financial reports.

Internal auditors e. Dividing responsibility between two or more people.

Match the accounting terminology to the definitions.

>TRY IT!

7-13Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Learning Objective 2

Apply internal controls to cash

receipts

7-14Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

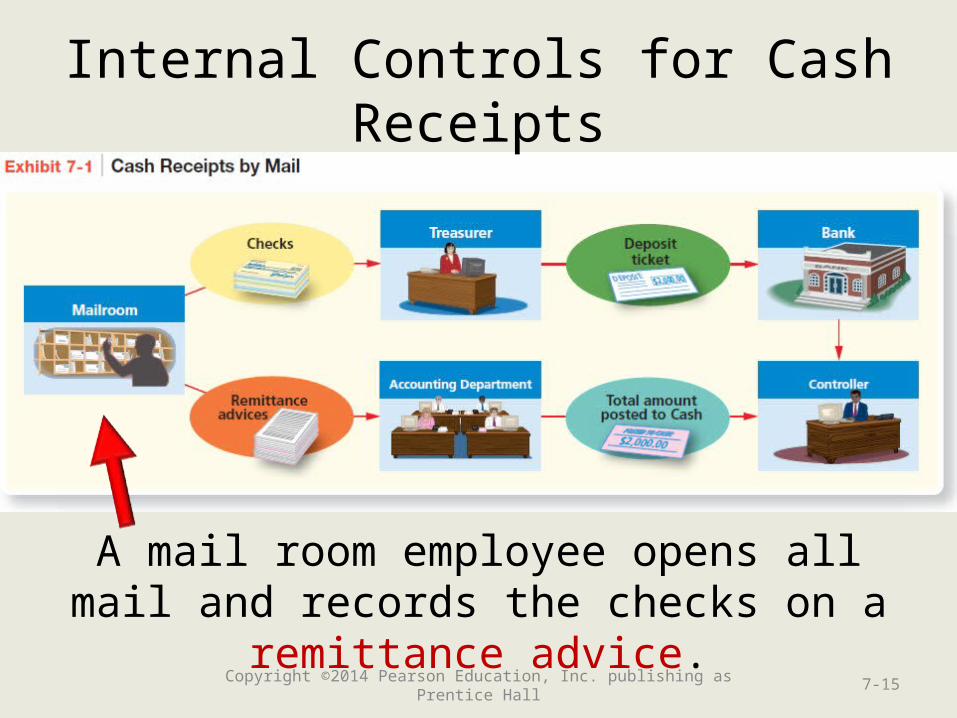

Internal Controls for Cash Receipts

A mail room employee opens all mail and records the checks on a remittance advice.

7-15Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

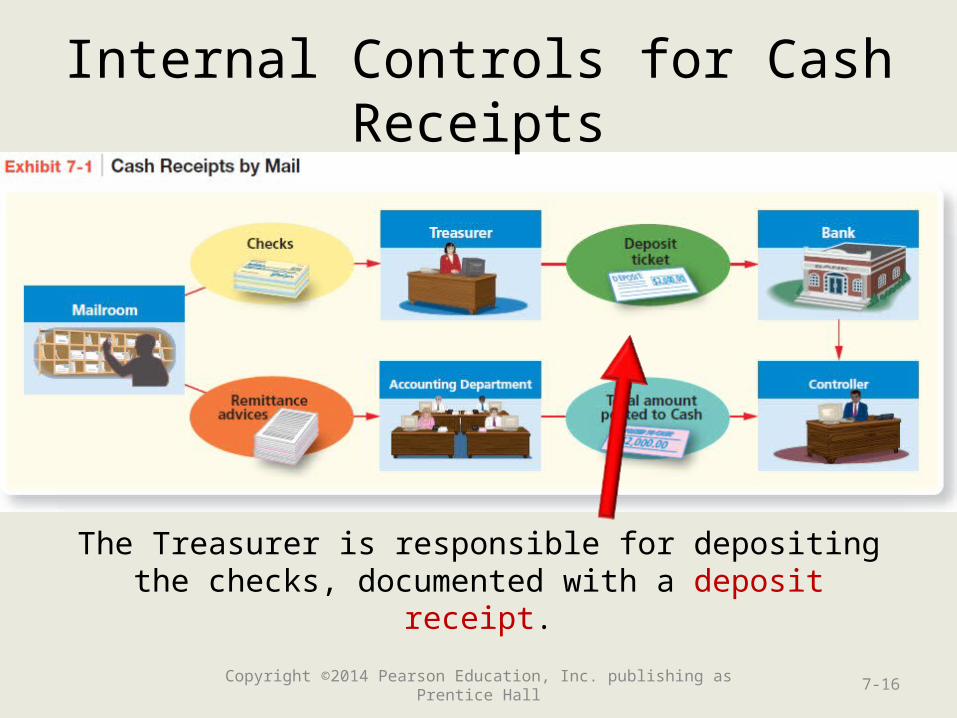

Internal Controls for Cash Receipts

The Treasurer is responsible for depositing the checks, documented with a deposit receipt.

7-16Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

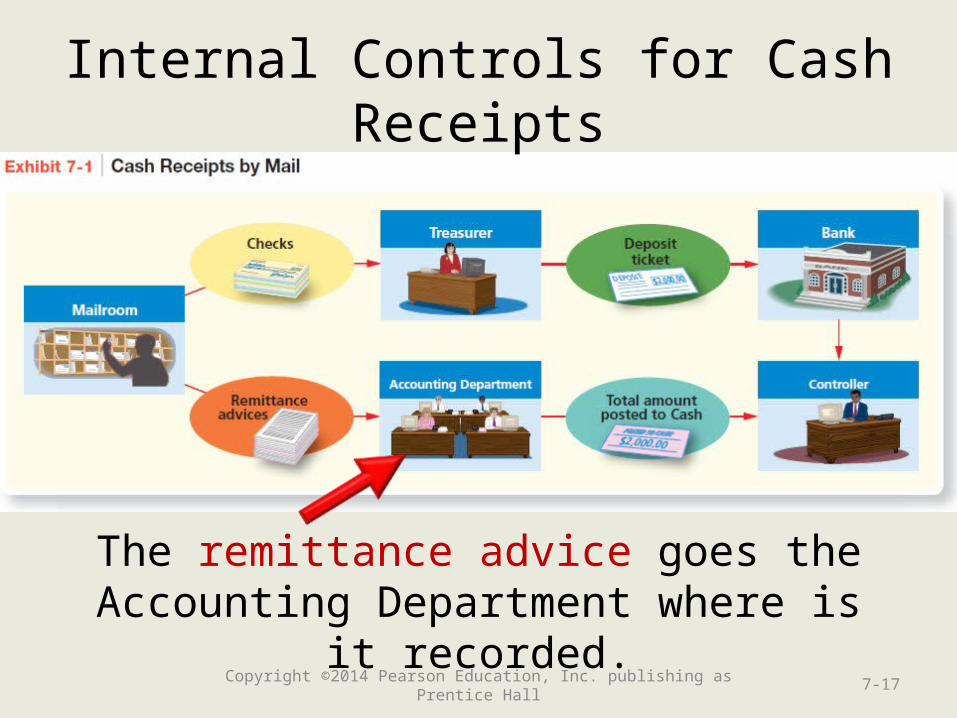

Internal Controls for Cash Receipts

The remittance advice goes the Accounting Department where is it recorded.

7-17Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

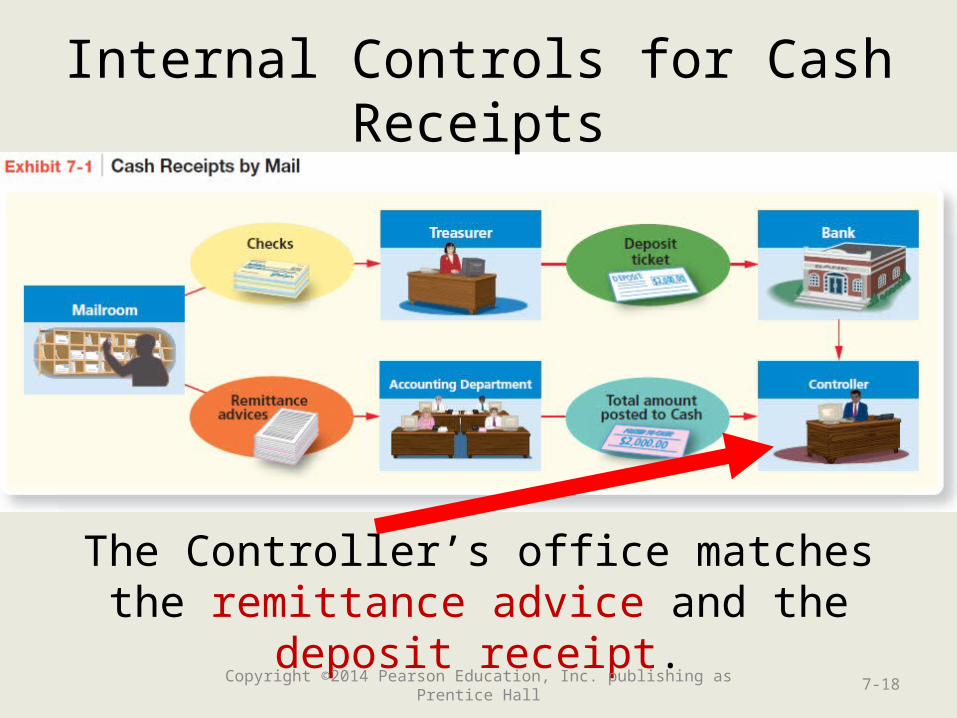

Internal Controls for Cash Receipts

The Controller’s office matches the remittance advice and the deposit receipt.

7-18Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

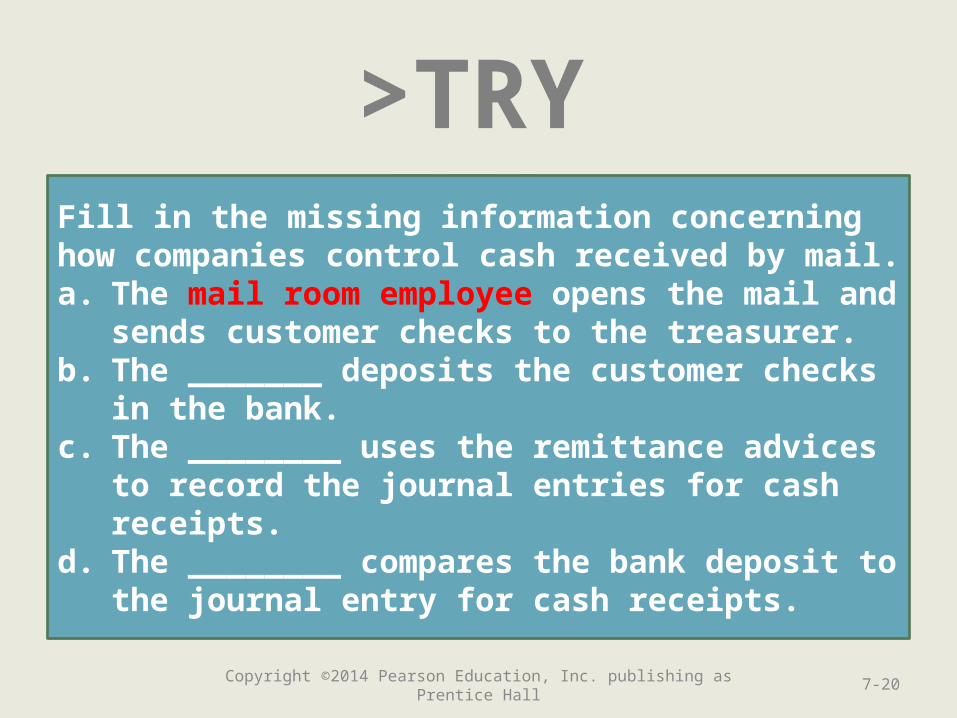

>TRY IT!Fill in the missing information concerning how companies control cash received by mail.a. The ________ opens the mail and sends customer

checks to the treasurer.b. The _______ deposits the customer checks in the

bank.c. The ________ uses the remittance advices to

record the journal entries for cash receipts.d. The ________ compares the bank deposit to the

journal entry for cash receipts.

7-19Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!Fill in the missing information concerning how companies control cash received by mail.a. The mail room employee opens the mail and sends

customer checks to the treasurer.b. The _______ deposits the customer checks in the

bank.c. The ________ uses the remittance advices to

record the journal entries for cash receipts.d. The ________ compares the bank deposit to the

journal entry for cash receipts.

7-20Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

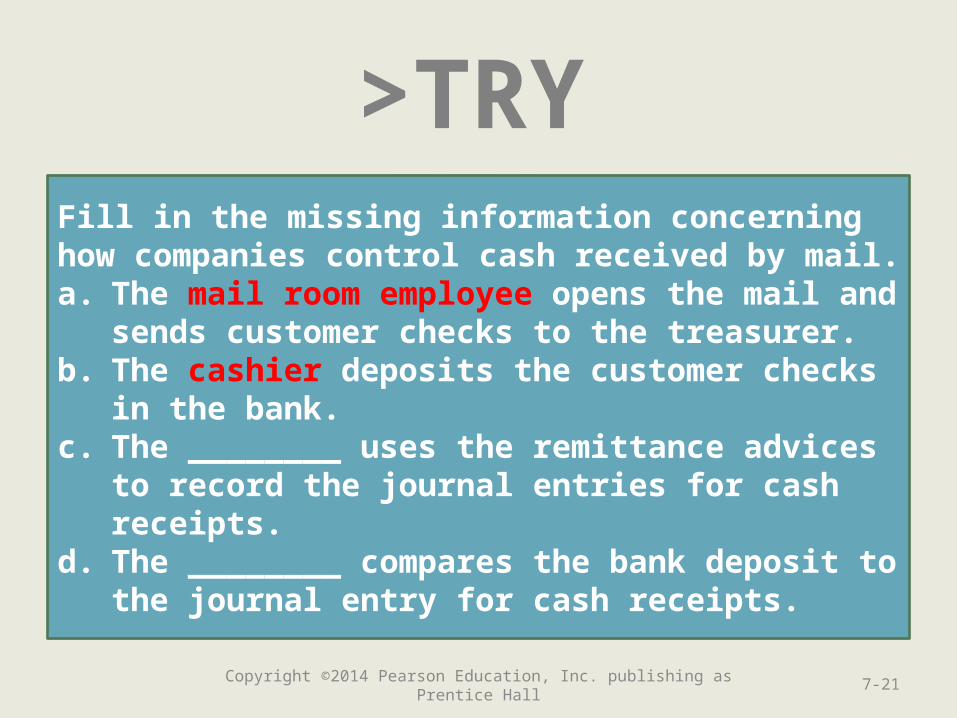

>TRY IT!Fill in the missing information concerning how companies control cash received by mail.a. The mail room employee opens the mail and sends

customer checks to the treasurer.b. The cashier deposits the customer checks in the

bank.c. The ________ uses the remittance advices to

record the journal entries for cash receipts.d. The ________ compares the bank deposit to the

journal entry for cash receipts.

7-21Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

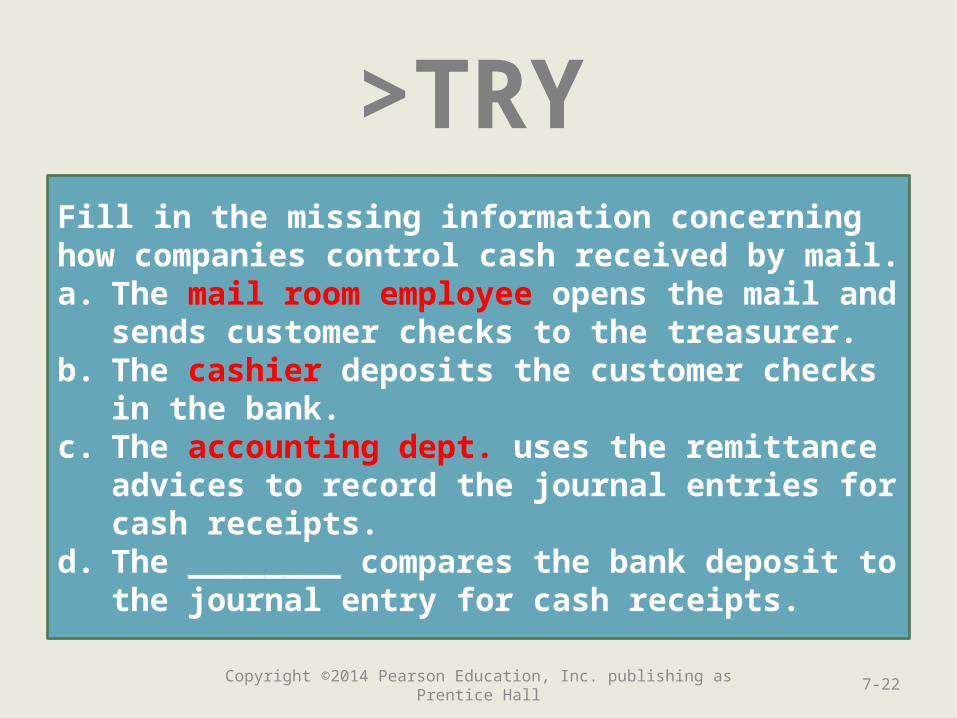

>TRY IT!Fill in the missing information concerning how companies control cash received by mail.a. The mail room employee opens the mail and sends

customer checks to the treasurer.b. The cashier deposits the customer checks in the

bank.c. The accounting dept. uses the remittance advices

to record the journal entries for cash receipts.d. The ________ compares the bank deposit to the

journal entry for cash receipts.

7-22Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

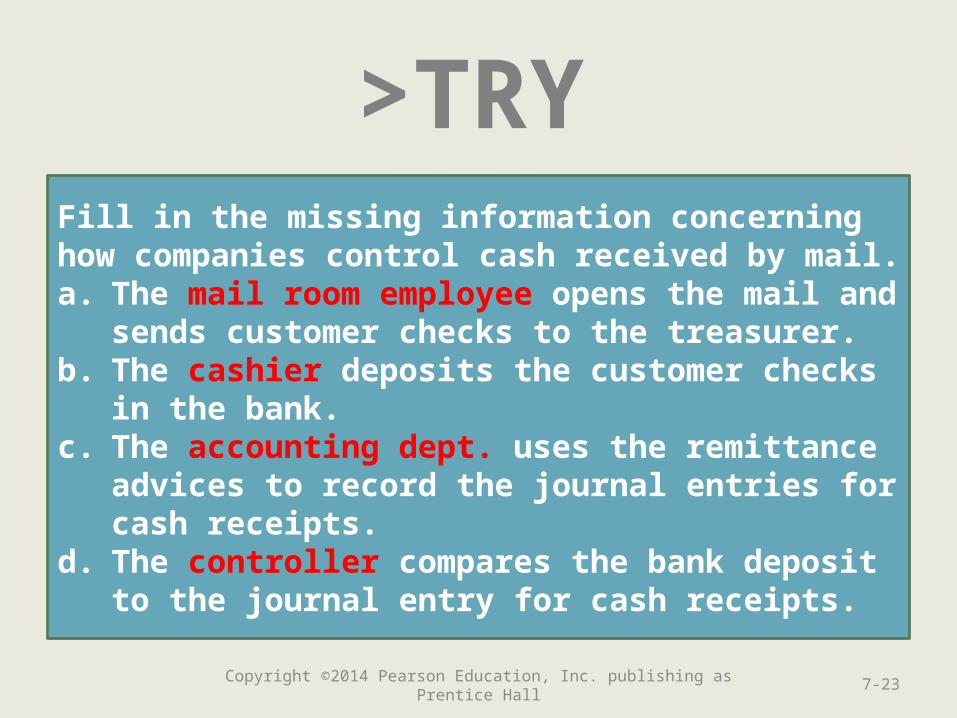

>TRY IT!Fill in the missing information concerning how companies control cash received by mail.a. The mail room employee opens the mail and sends

customer checks to the treasurer.b. The cashier deposits the customer checks in the

bank.c. The accounting dept. uses the remittance advices

to record the journal entries for cash receipts.d. The controller compares the bank deposit to the

journal entry for cash receipts.

7-23Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Learning Objective 3

Apply internal controls to cash

payments

7-24Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

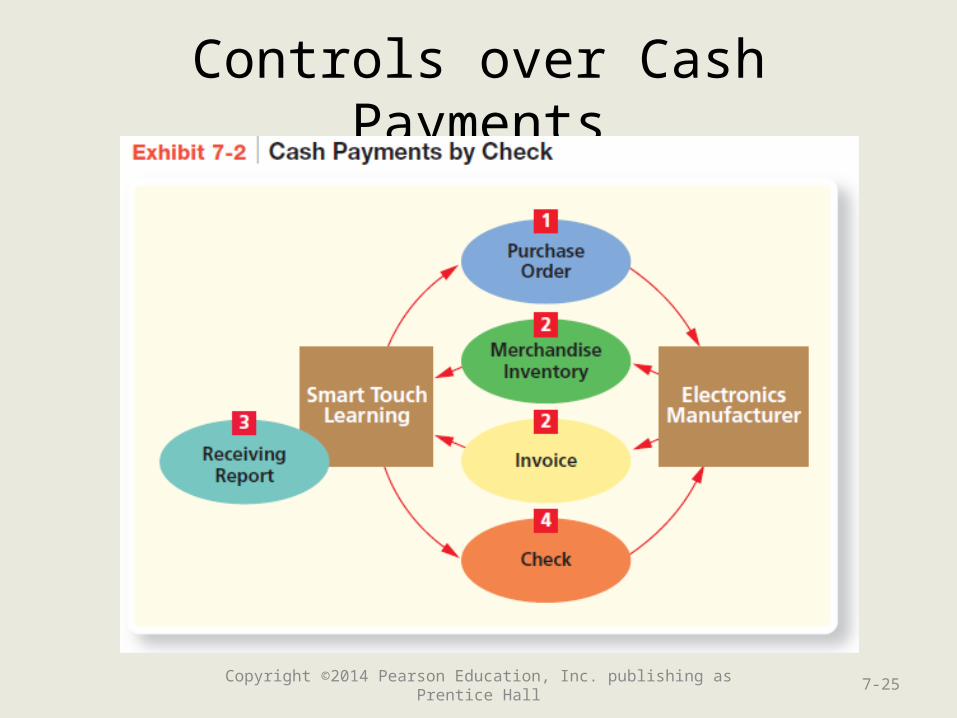

Controls over Cash Payments

7-25Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

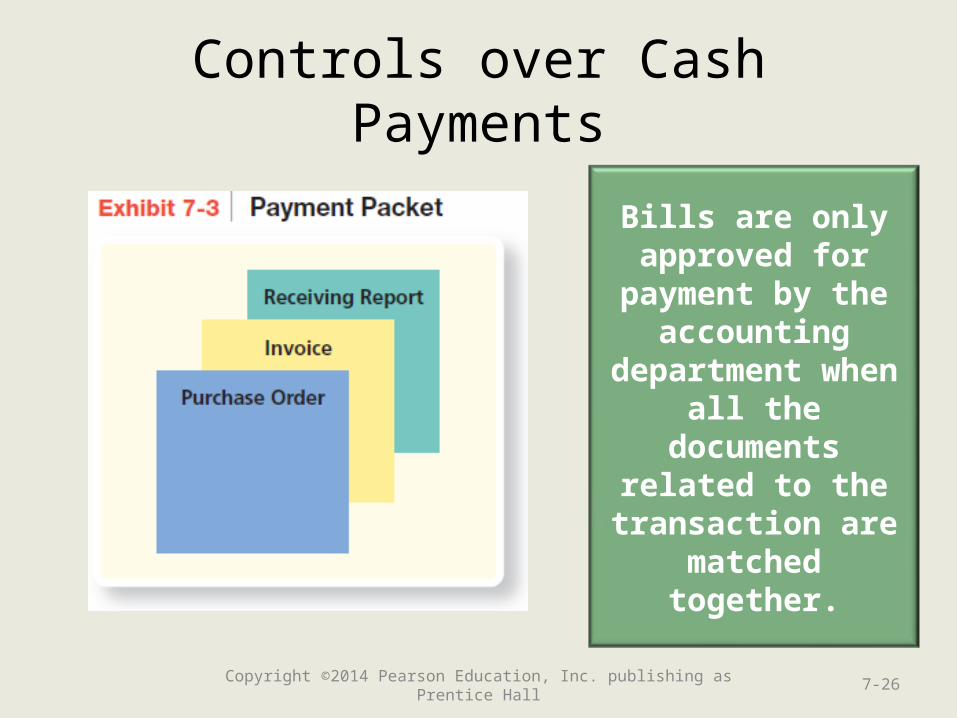

Controls over Cash Payments

Bills are only approved for

payment by the accounting

department when all the documents

related to the transaction are

matched together.

7-26Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

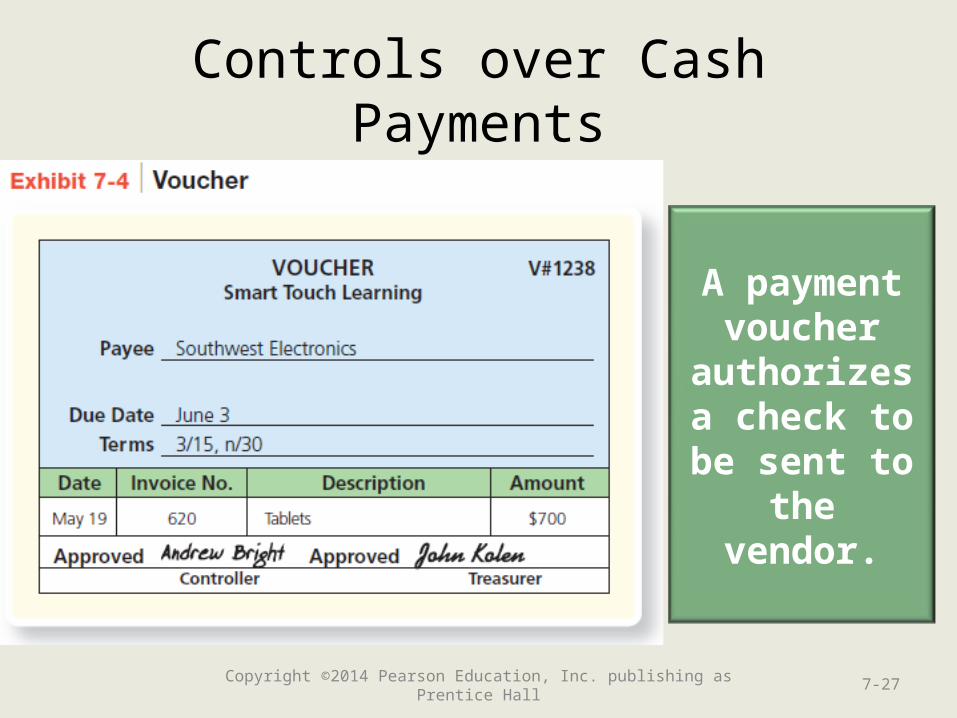

Controls over Cash Payments

A payment voucher

authorizes a check to be sent to the

vendor.

7-27Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

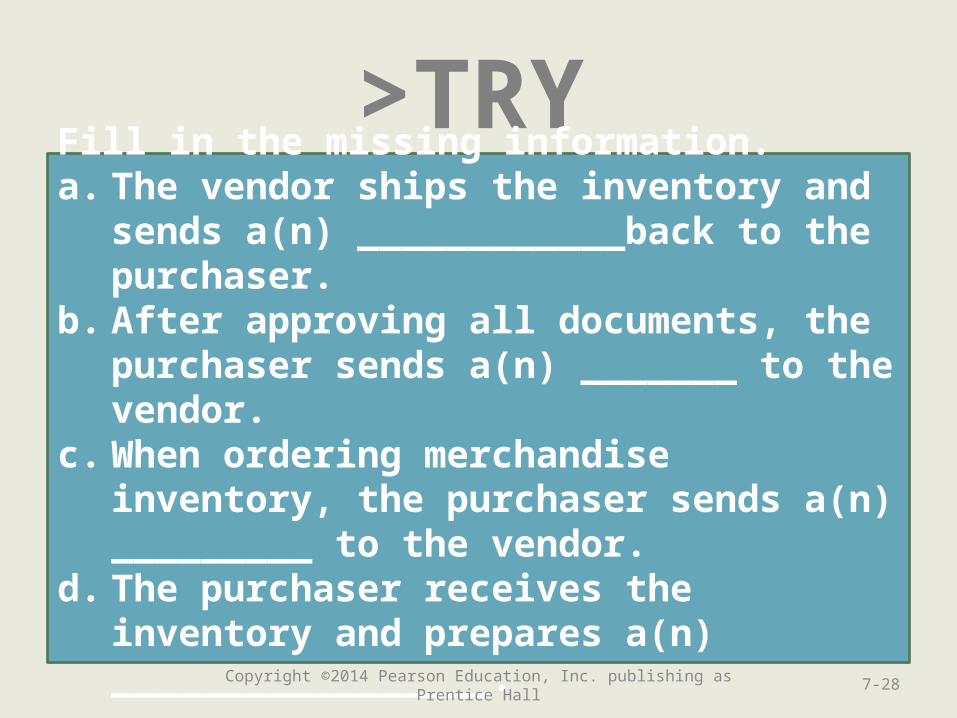

>TRY IT!Fill in the missing information.a. The vendor ships the inventory and sends

a(n) ____________back to the purchaser.b. After approving all documents, the

purchaser sends a(n) _______ to the vendor.c. When ordering merchandise inventory, the

purchaser sends a(n) _________ to the vendor.

d. The purchaser receives the inventory and prepares a(n) _________________.

7-28Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

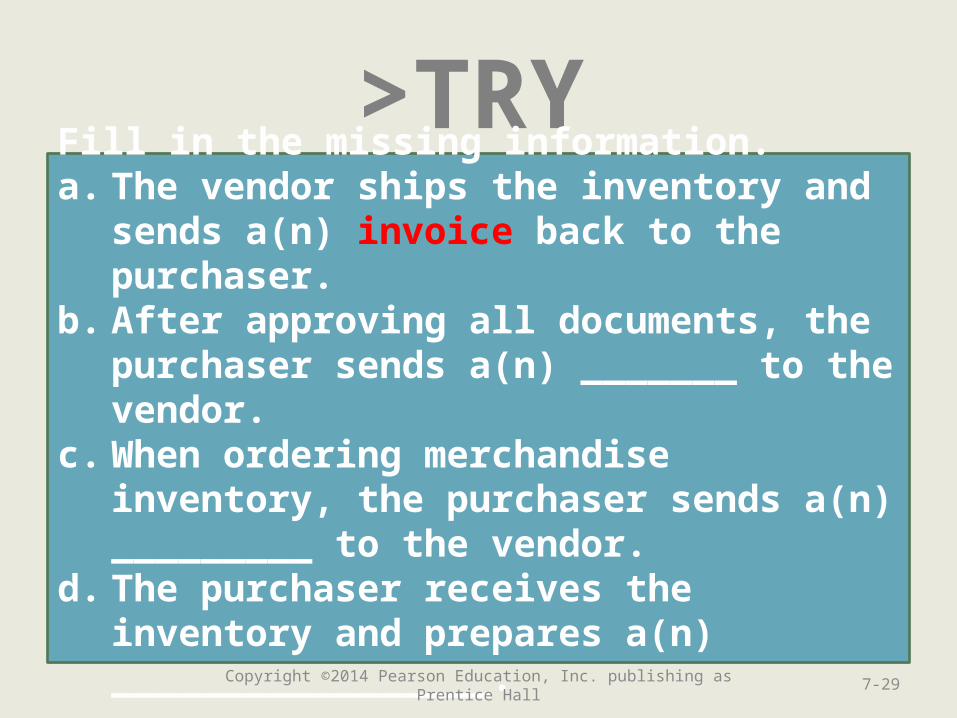

>TRY IT!Fill in the missing information.a. The vendor ships the inventory and sends

a(n) invoice back to the purchaser.b. After approving all documents, the

purchaser sends a(n) _______ to the vendor.c. When ordering merchandise inventory, the

purchaser sends a(n) _________ to the vendor.

d. The purchaser receives the inventory and prepares a(n) _________________.

7-29Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

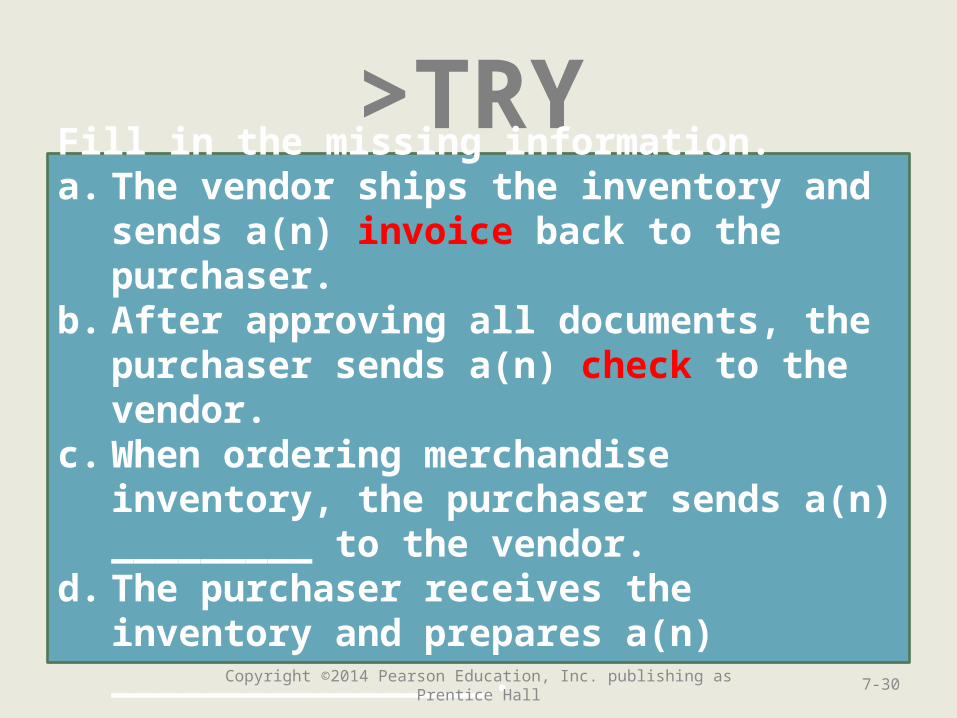

>TRY IT!Fill in the missing information.a. The vendor ships the inventory and sends

a(n) invoice back to the purchaser.b. After approving all documents, the

purchaser sends a(n) check to the vendor.c. When ordering merchandise inventory, the

purchaser sends a(n) _________ to the vendor.

d. The purchaser receives the inventory and prepares a(n) _________________.

7-30Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

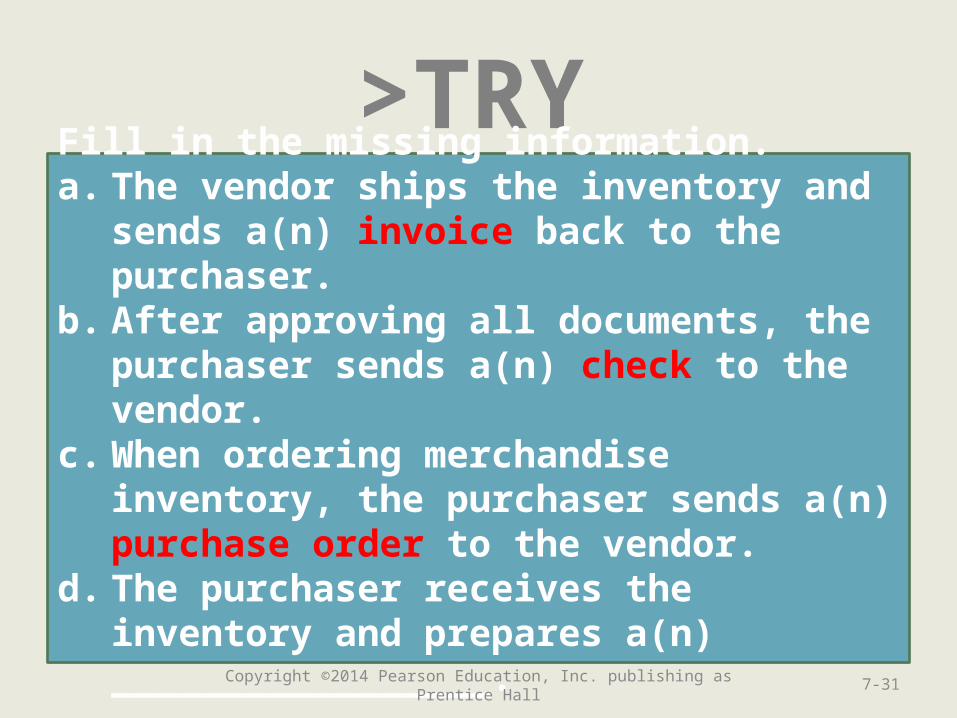

>TRY IT!Fill in the missing information.a. The vendor ships the inventory and sends

a(n) invoice back to the purchaser.b. After approving all documents, the

purchaser sends a(n) check to the vendor.c. When ordering merchandise inventory, the

purchaser sends a(n) purchase order to the vendor.

d. The purchaser receives the inventory and prepares a(n) _________________.

7-31Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

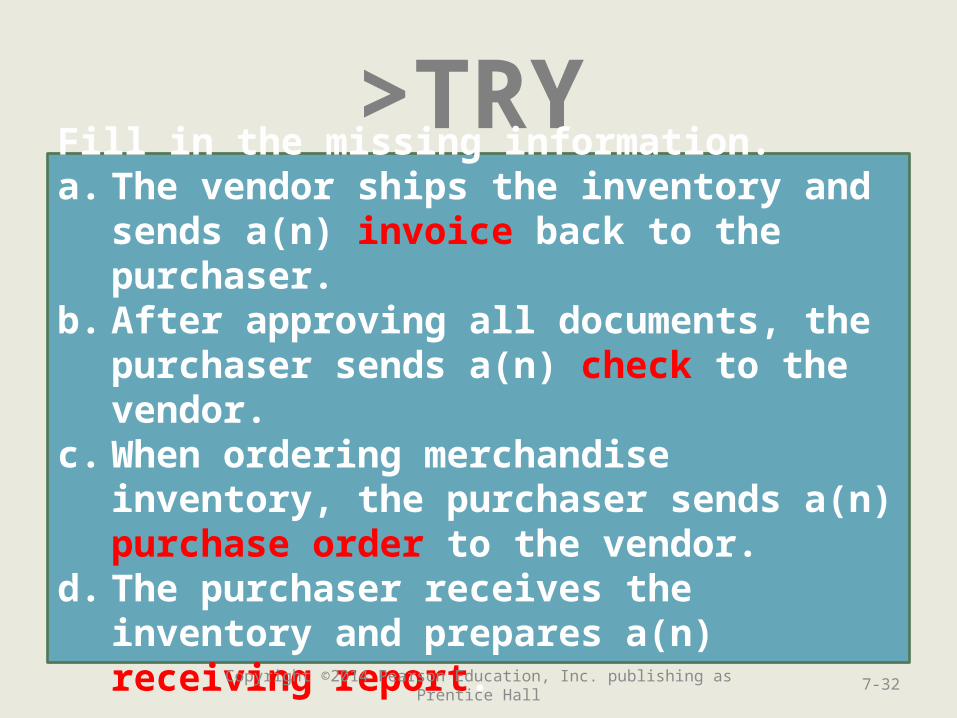

>TRY IT!Fill in the missing information.a. The vendor ships the inventory and sends

a(n) invoice back to the purchaser.b. After approving all documents, the

purchaser sends a(n) check to the vendor.c. When ordering merchandise inventory, the

purchaser sends a(n) purchase order to the vendor.

d. The purchaser receives the inventory and prepares a(n) receiving report.

7-32Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Learning Objective 4

Explain and journalize petty

cash transactions

7-33Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Petty Cash

• Used as an in-office source of cash for small immediate purchases.

• Often the responsibility of a designated employee.

• No cash is removed unless a corresponding receipt is placed in the “box.”

Uses for Petty Cash• Office donuts• Cleaning supplies• Sympathy flowers• Entertaining clients• Public transportation• Tips for service

providers

7-34Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

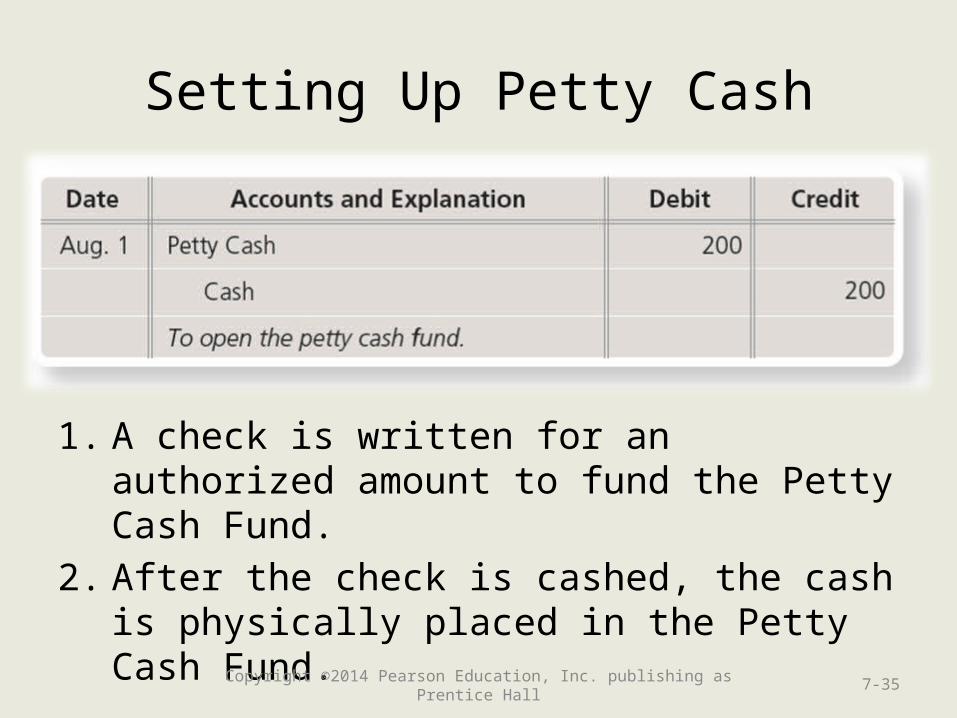

Setting Up Petty Cash

1. A check is written for an authorized amount to fund the Petty Cash Fund.

2. After the check is cashed, the cash is physically placed in the Petty Cash Fund.

7-35Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

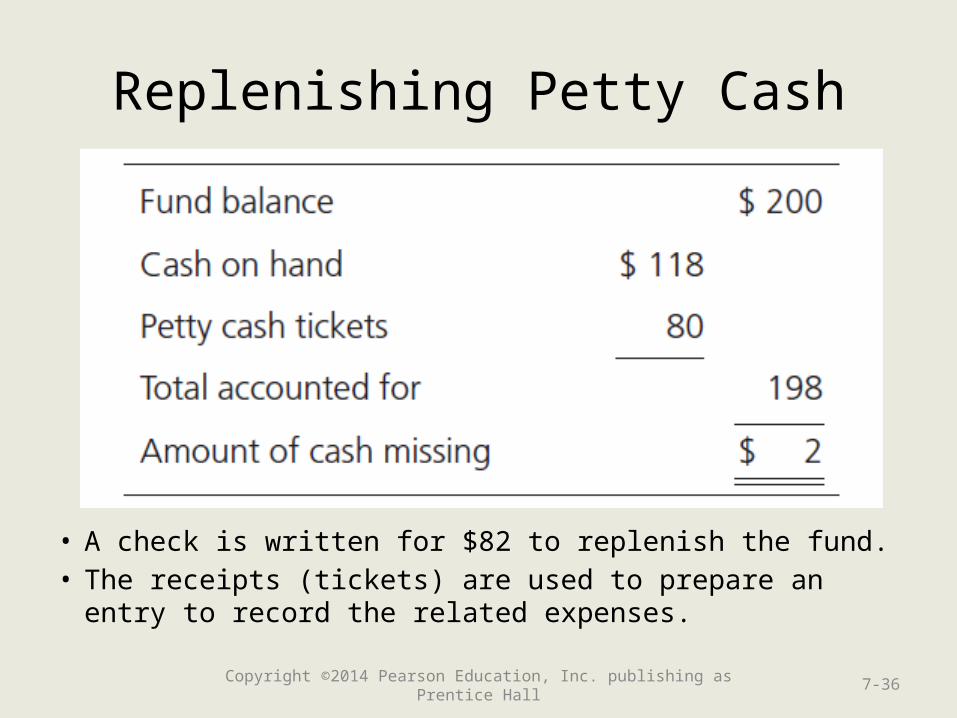

Replenishing Petty Cash

• A check is written for $82 to replenish the fund.• The receipts (tickets) are used to prepare an entry

to record the related expenses.7-36Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

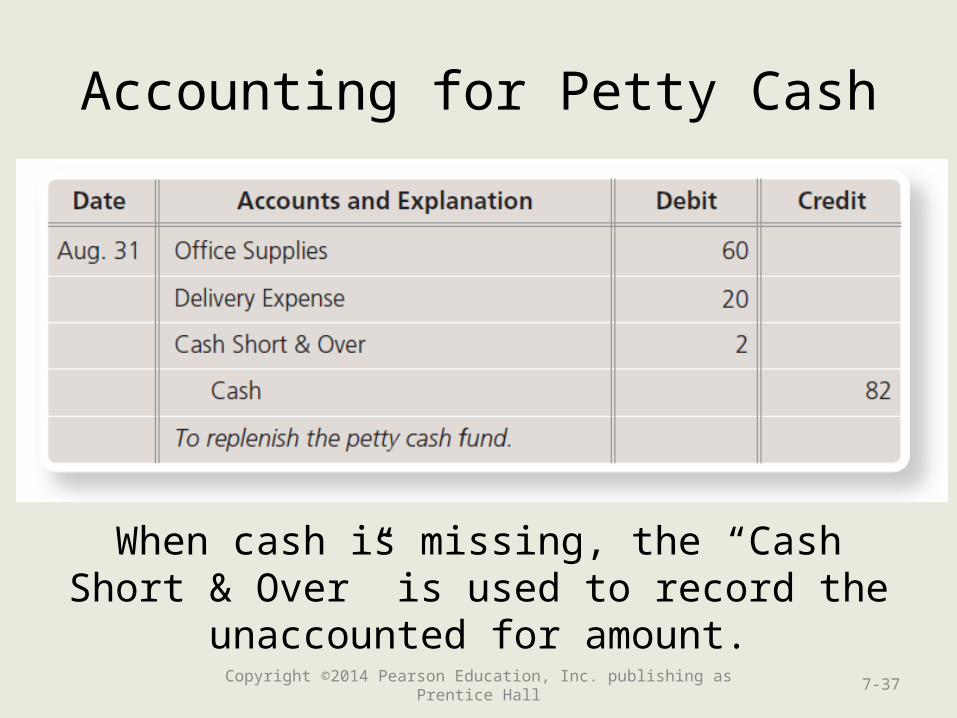

Accounting for Petty Cash

When cash is missing, the “Cash Short & Over” is used to record the unaccounted for

amount.7-37Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

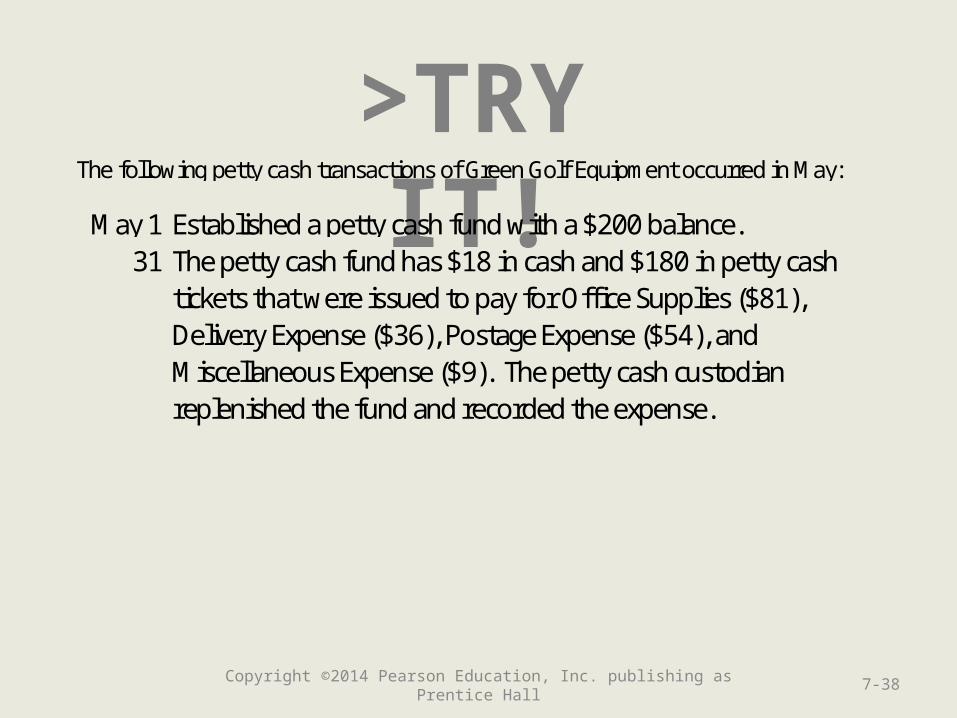

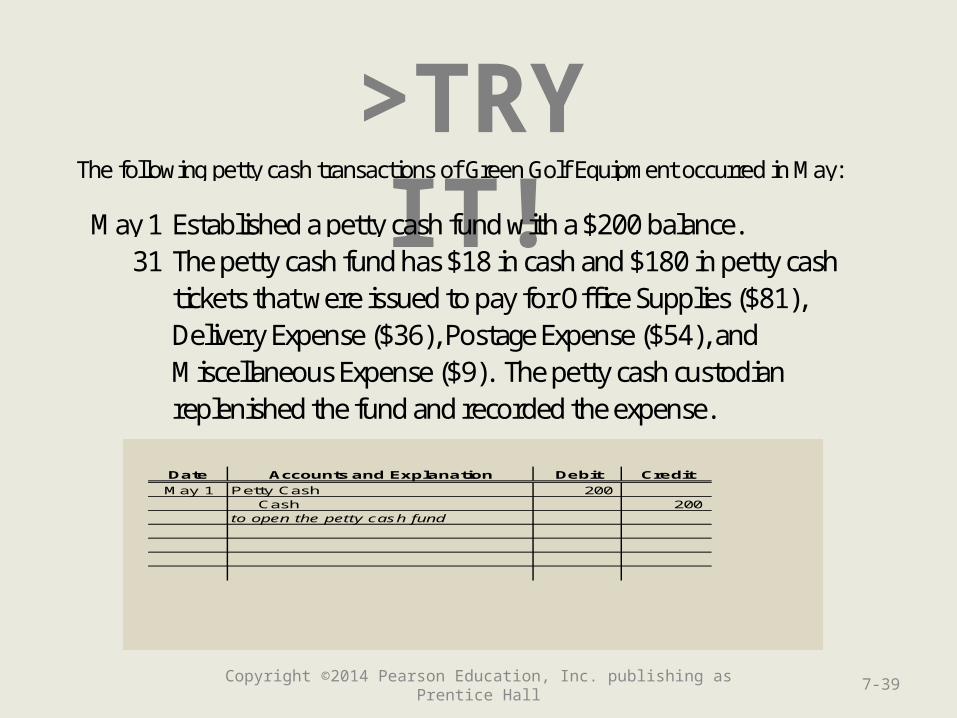

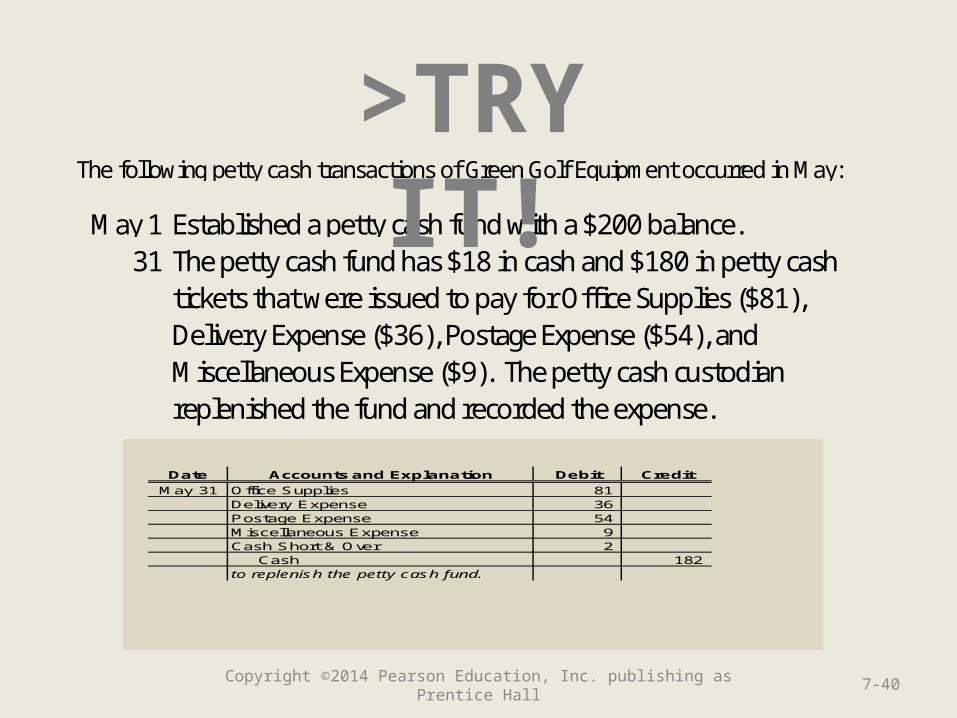

>TRY IT! May 1 Established a petty cash fund with a $200 balance.

31 The petty cash fund has $18 in cash and $180 in petty cash tickets that were issued to pay for Office Supplies ($81), Delivery Expense ($36), Postage Expense ($54), and Miscellaneous Expense ($9). The petty cash custodian replenished the fund and recorded the expense.

The following petty cash transactions of Green Golf Equipment occurred in May:

7-38Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!

Date Accounts and Explanation Debit Credit

May 1 Petty Cash 200 Cash 200 to open the petty cash fund

May 1 Established a petty cash fund with a $200 balance.31 The petty cash fund has $18 in cash and $180 in petty cash

tickets that were issued to pay for Office Supplies ($81), Delivery Expense ($36), Postage Expense ($54), and Miscellaneous Expense ($9). The petty cash custodian replenished the fund and recorded the expense.

The following petty cash transactions of Green Golf Equipment occurred in May:

7-39Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

May 1 Established a petty cash fund with a $200 balance.31 The petty cash fund has $18 in cash and $180 in petty cash

tickets that were issued to pay for Office Supplies ($81), Delivery Expense ($36), Postage Expense ($54), and Miscellaneous Expense ($9). The petty cash custodian replenished the fund and recorded the expense.

The following petty cash transactions of Green Golf Equipment occurred in May:

>TRY IT!

Date Accounts and Explanation Debit Credit

May 31 Office Supplies 81 Delivery Expense 36 Postage Expense 54 Miscellaneous Expense 9 Cash Short & Over 2 Cash 182 to replenish the petty cash fund.

7-40Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Learning Objective 5

Demonstrate the use of a bank account as a

control device and prepare a bank

reconciliation and related journal entries

7-41Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Bank Account as a Control Device

• Signature Card• Deposit Ticket• Check• Bank Statement• Electronic Funds

Transfers• Bank Reconciliation

During the 1960’s, Frank Abagnale

passed $2.8 million of forged checks in over 26 different countries by exploiting weak controls over bank

accounts.

7-42Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

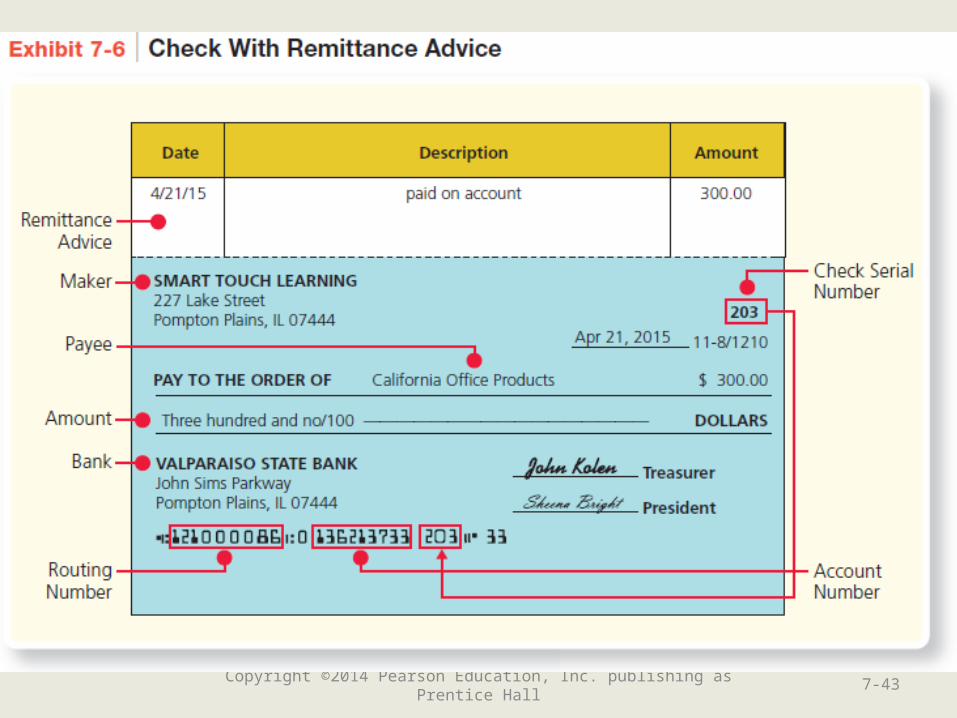

7-43Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Bank Reconciliation

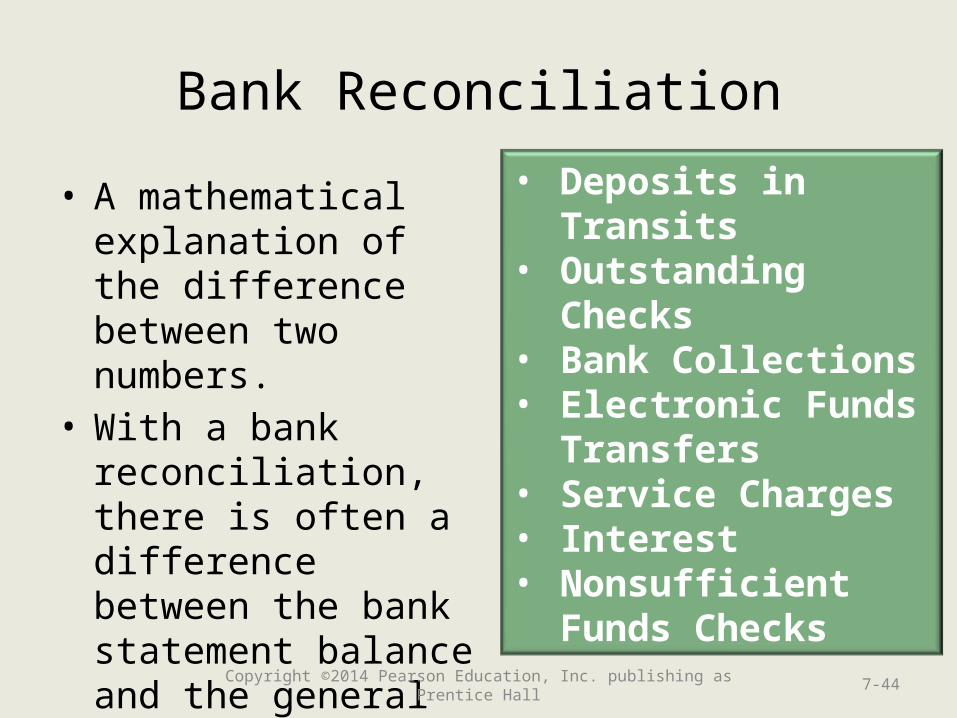

• A mathematical explanation of the difference between two numbers.

• With a bank reconciliation, there is often a difference between the bank statement balance and the general ledger cash balance.

• Deposits in Transits• Outstanding Checks• Bank Collections• Electronic Funds

Transfers• Service Charges• Interest• Nonsufficient Funds

Checks

7-44Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

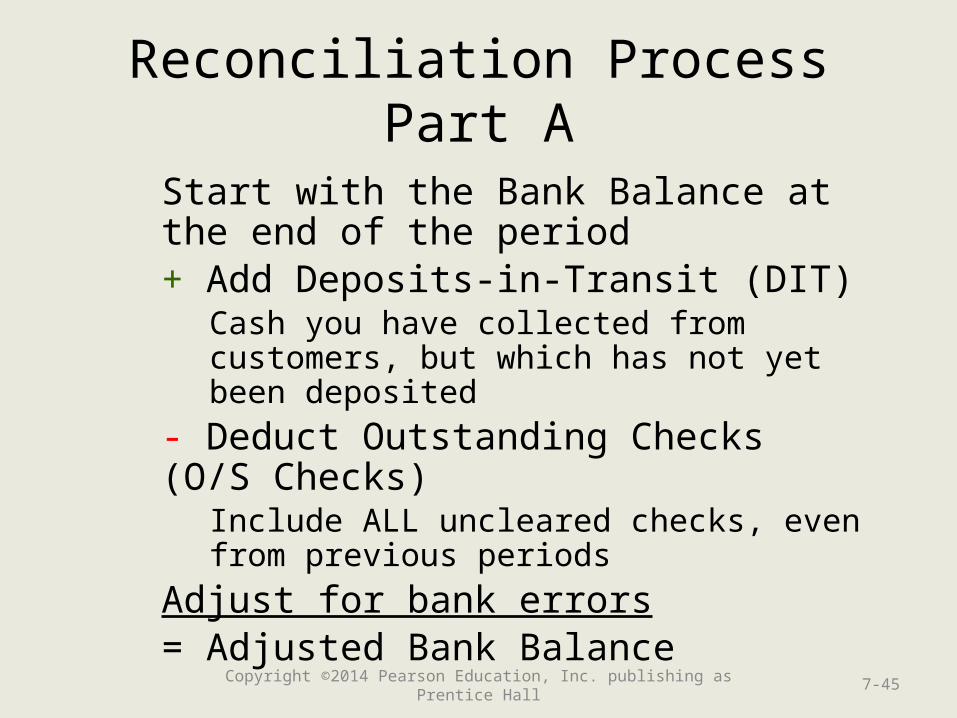

Reconciliation ProcessPart A

Start with the Bank Balance at the end of the period+ Add Deposits-in-Transit (DIT)

Cash you have collected from customers, but which has not yet been deposited

- Deduct Outstanding Checks (O/S Checks)

Include ALL uncleared checks, even from previous periods

Adjust for bank errors= Adjusted Bank Balance

7-45Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

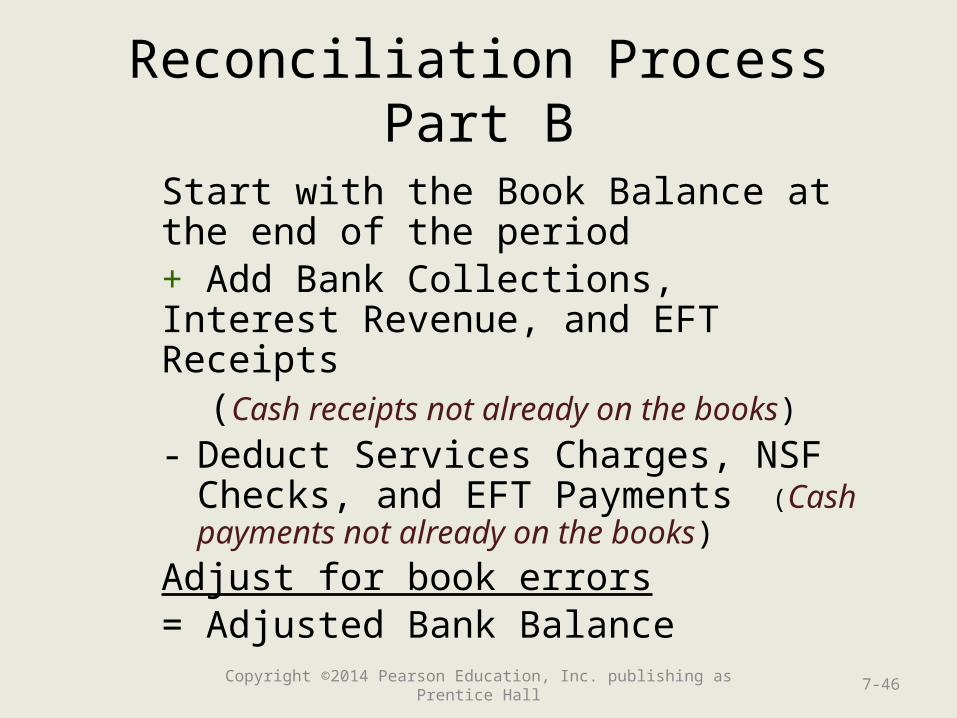

Reconciliation ProcessPart B

Start with the Book Balance at the end of the period+ Add Bank Collections, Interest Revenue, and EFT Receipts

(Cash receipts not already on the books)

- Deduct Services Charges, NSF Checks, and EFT Payments (Cash payments not already on the books)

Adjust for book errors= Adjusted Bank Balance

7-46Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

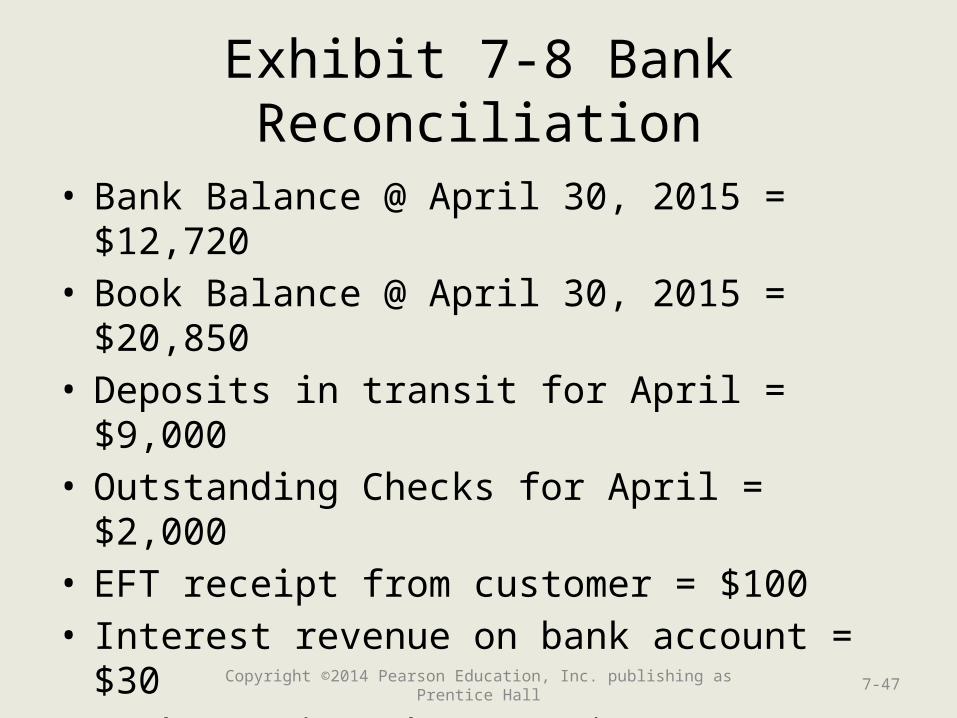

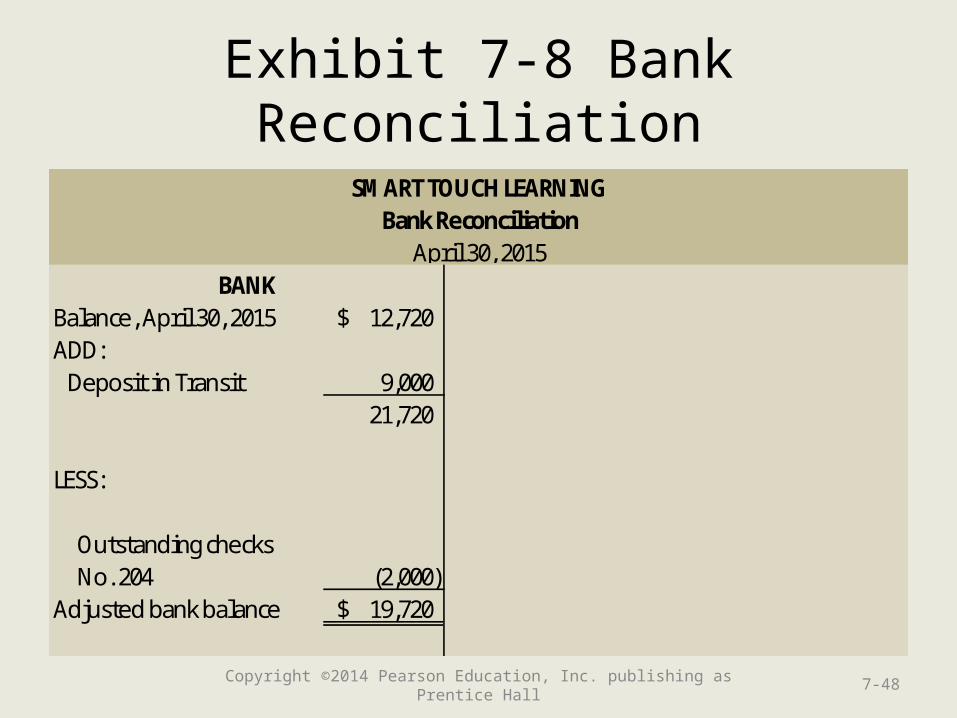

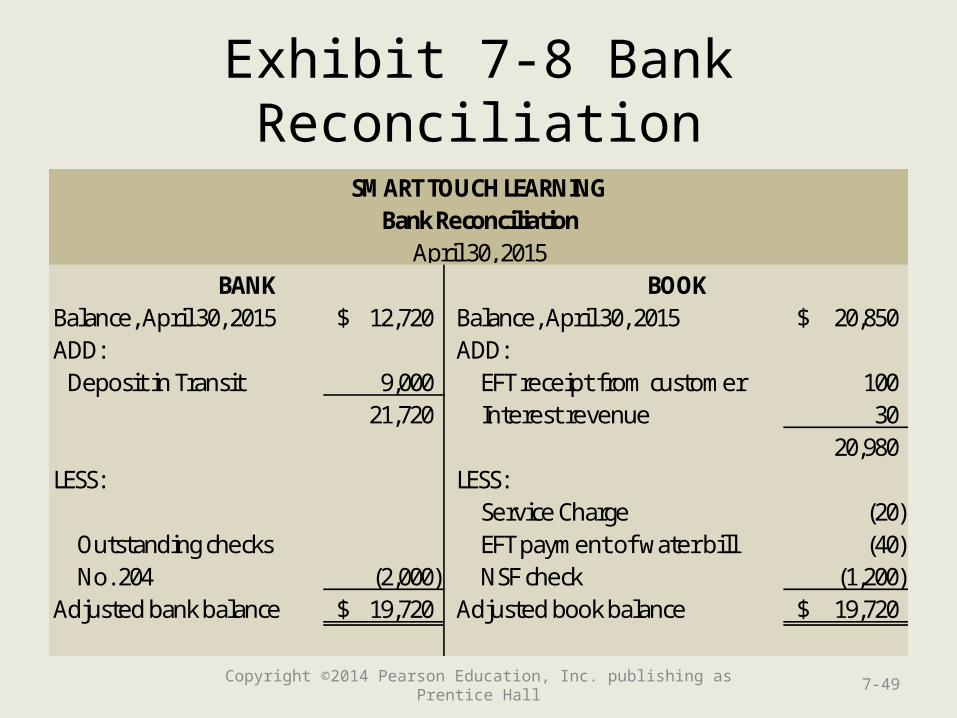

Exhibit 7-8 Bank Reconciliation

• Bank Balance @ April 30, 2015 = $12,720• Book Balance @ April 30, 2015 = $20,850• Deposits in transit for April = $9,000• Outstanding Checks for April = $2,000• EFT receipt from customer = $100• Interest revenue on bank account = $30• Bank service charge = $20• EFT payment of water bill = $40• NSF Check = $1,200

7-47Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Exhibit 7-8 Bank Reconciliation

Balance, April 30, 2015 12,720$ ADD: Deposit in Transit 9,000

21,720

LESS:

Outstanding checks No. 204 (2,000) Adjusted bank balance 19,720$

BANK

SMART TOUCH LEARNINGBank Reconciliation

April 30, 2015

7-48Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Exhibit 7-8 Bank Reconciliation

Balance, April 30, 2015 12,720$ Balance, April 30, 2015 20,850$ ADD: ADD: Deposit in Transit 9,000 EFT receipt from customer 100

21,720 Interest revenue 30 20,980

LESS: LESS: Service Charge (20)

Outstanding checks EFT payment of water bill (40) No. 204 (2,000) NSF check (1,200) Adjusted bank balance 19,720$ Adjusted book balance 19,720$

BANK BOOK

SMART TOUCH LEARNINGBank Reconciliation

April 30, 2015

7-49Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Exhibit 7-8 Bank Reconciliation

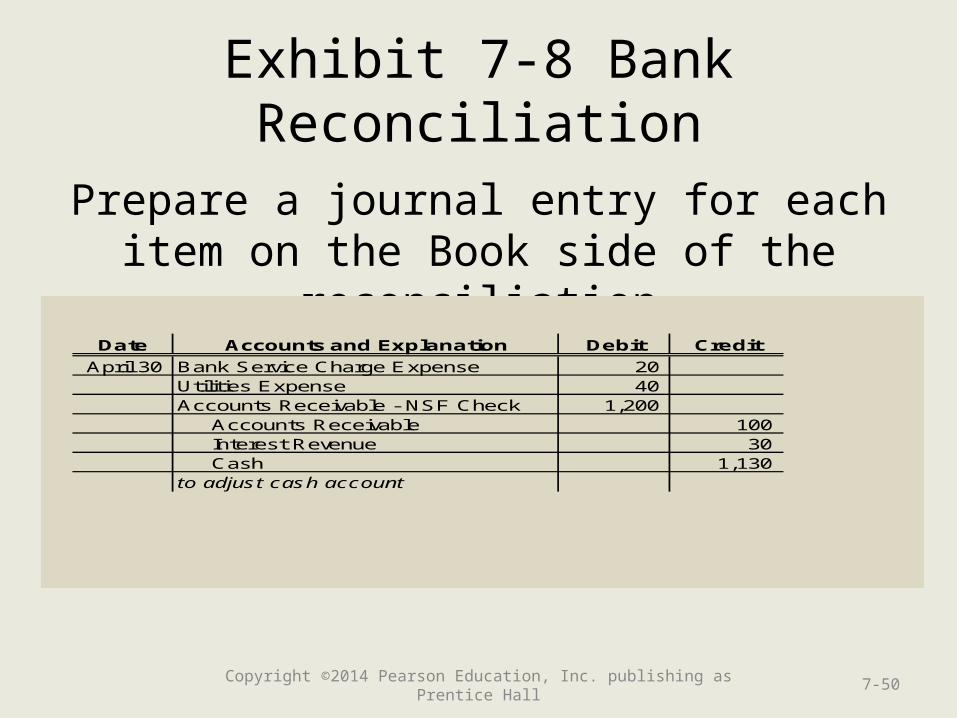

Prepare a journal entry for each item on the Book side of the reconciliation

Date Accounts and Explanation Debit Credit

April 30 Bank Service Charge Expense 20 Utilities Expense 40 Accounts Receivable - NSF Check 1,200 Accounts Receivable 100 Interest Revenue 30 Cash 1,130 to adjust cash account

7-50Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

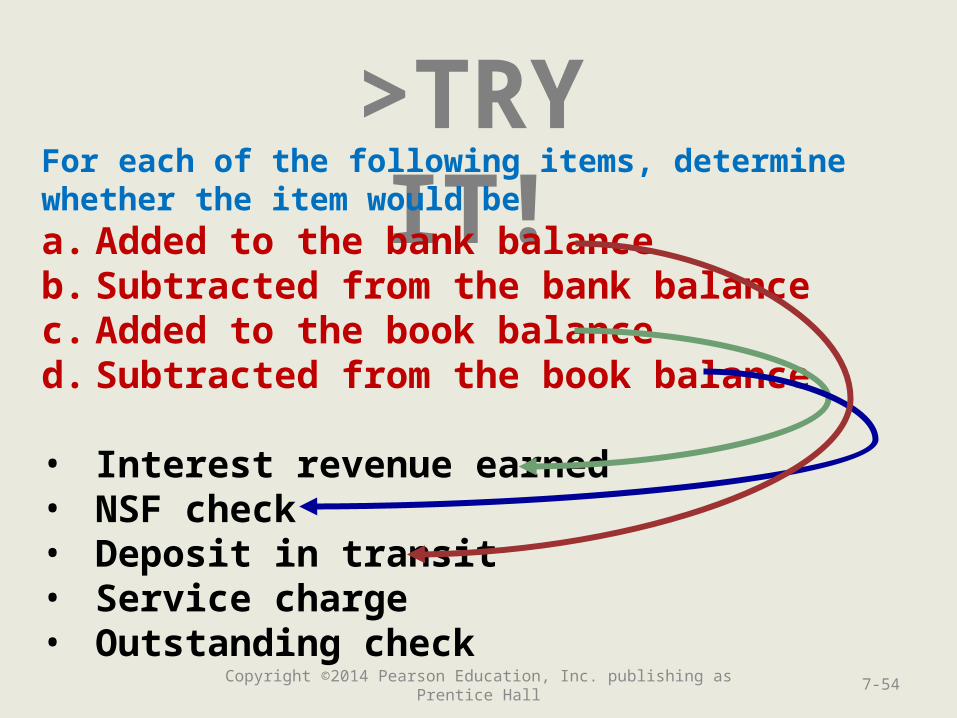

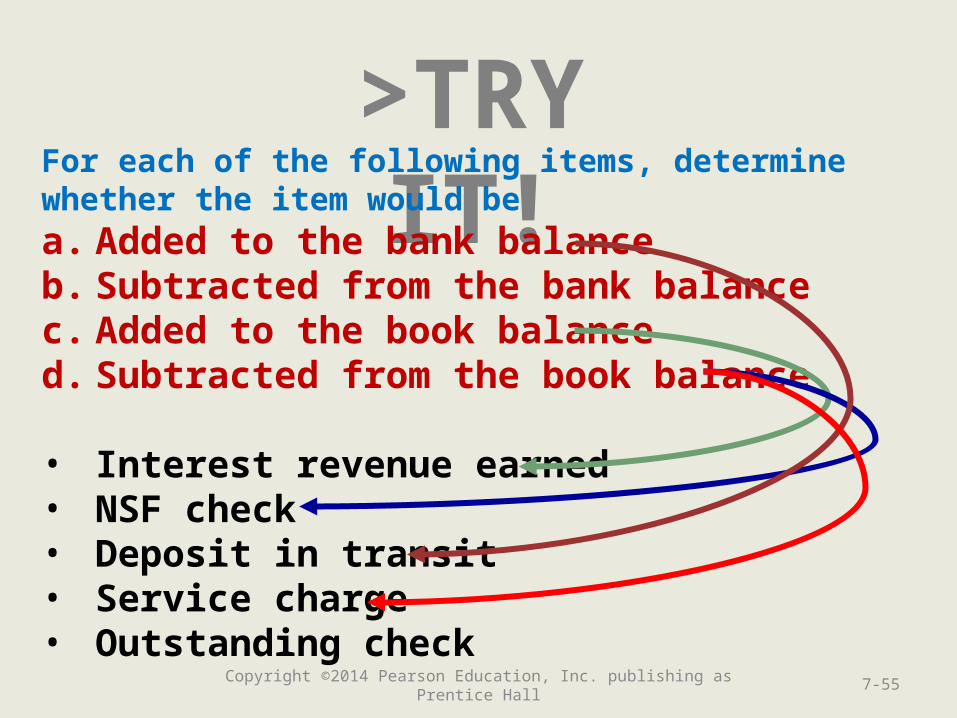

>TRY IT!For each of the following items, determine whether the item would bea. Added to the bank balanceb. Subtracted from the bank balancec. Added to the book balanced. Subtracted from the book balance

• Interest revenue earned• NSF check• Deposit in transit• Service charge• Outstanding check

7-51Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!For each of the following items, determine whether the item would bea. Added to the bank balanceb. Subtracted from the bank balancec. Added to the book balanced. Subtracted from the book balance

• Interest revenue earned• NSF check• Deposit in transit• Service charge• Outstanding check

7-52Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!For each of the following items, determine whether the item would bea. Added to the bank balanceb. Subtracted from the bank balancec. Added to the book balanced. Subtracted from the book balance

• Interest revenue earned• NSF check• Deposit in transit• Service charge• Outstanding check

7-53Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!For each of the following items, determine whether the item would bea. Added to the bank balanceb. Subtracted from the bank balancec. Added to the book balanced. Subtracted from the book balance

• Interest revenue earned• NSF check• Deposit in transit• Service charge• Outstanding check

7-54Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!For each of the following items, determine whether the item would bea. Added to the bank balanceb. Subtracted from the bank balancec. Added to the book balanced. Subtracted from the book balance

• Interest revenue earned• NSF check• Deposit in transit• Service charge• Outstanding check

7-55Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

>TRY IT!For each of the following items, determine whether the item would bea. Added to the bank balanceb. Subtracted from the bank balancec. Added to the book balanced. Subtracted from the book balance

• Interest revenue earned• NSF check• Deposit in transit• Service charge• Outstanding check

7-56Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Learning Objective 6

Use the cash ratio to evaluate business

performance

7-57Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

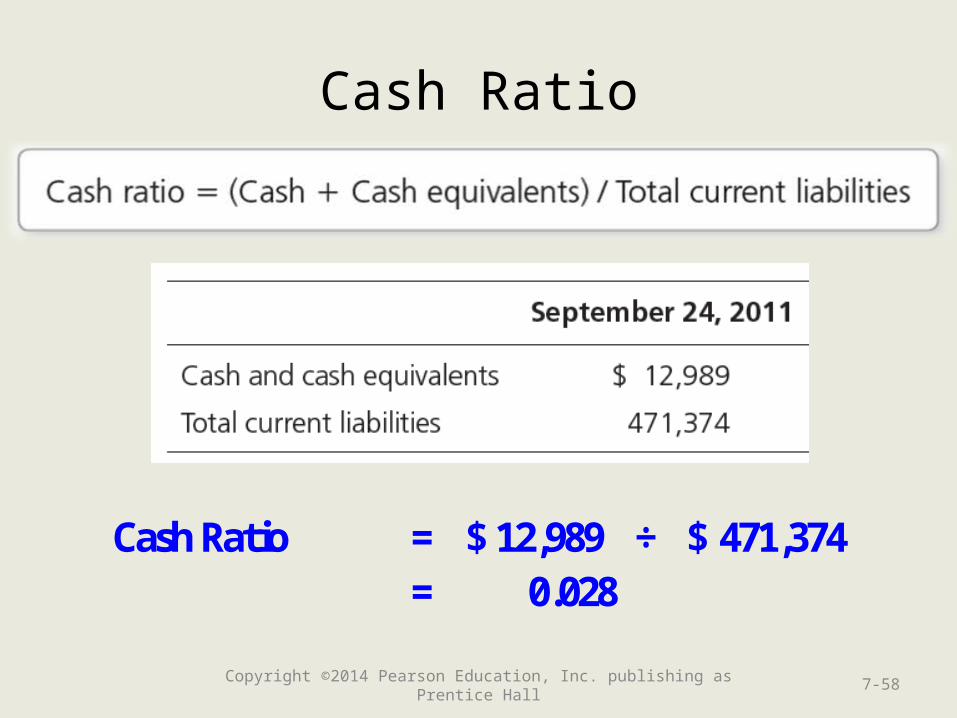

Cash Ratio

7-58

Cash Ratio = 12,989$ ÷ 471,374$ = 0.028

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

End of Chapter 7

7-59Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall