Embed Size (px)

Citation preview

Annexure 2

1

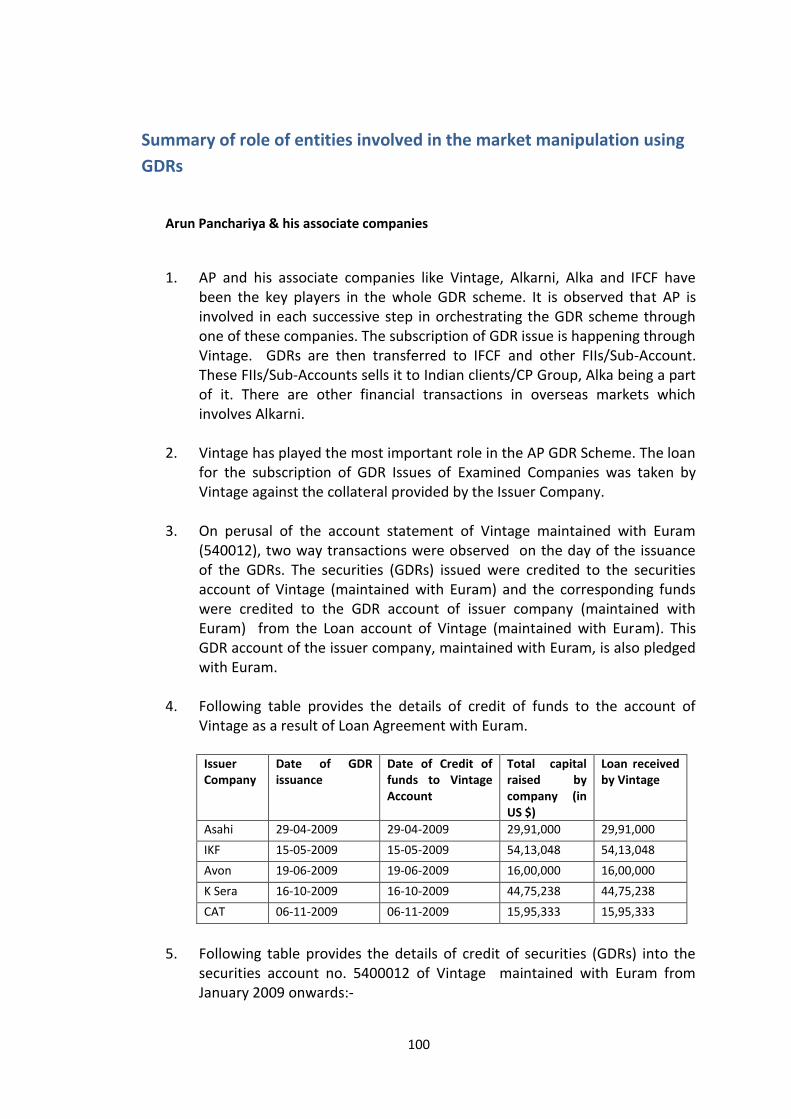

INVESTIGATION REPORT IN THE MATTER OF MARKET

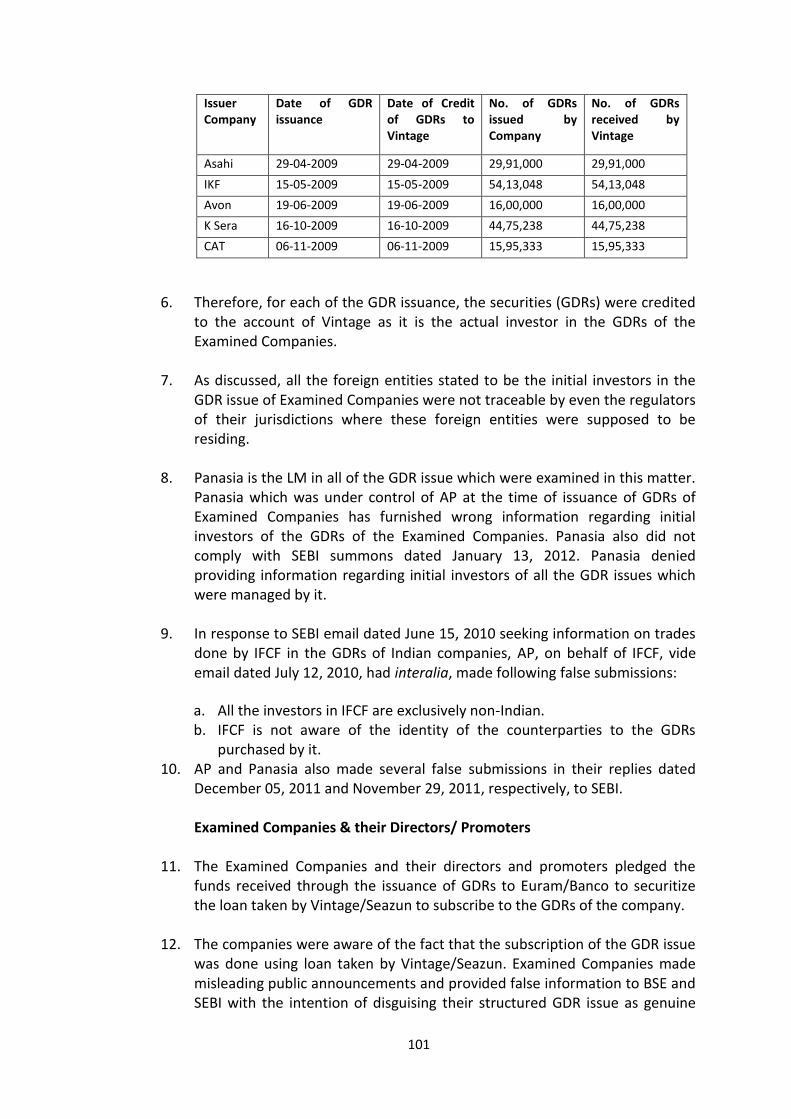

MANIPULATION USING GDR ISSUES.

Contents

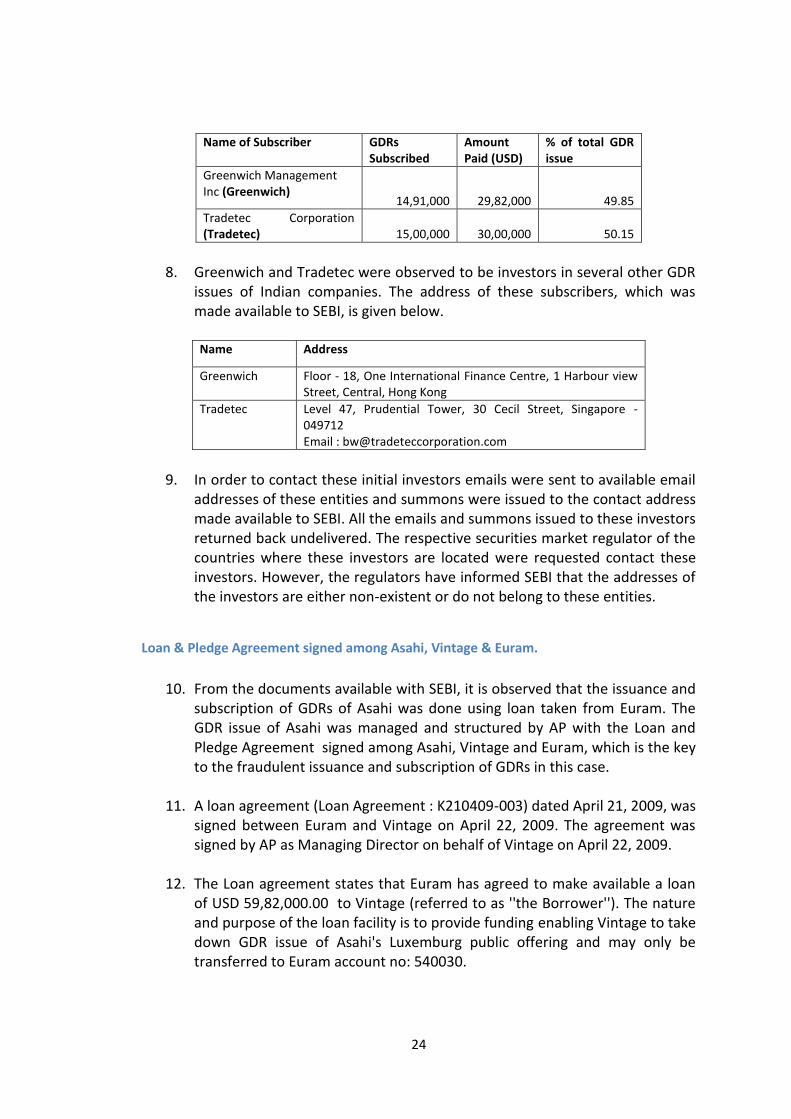

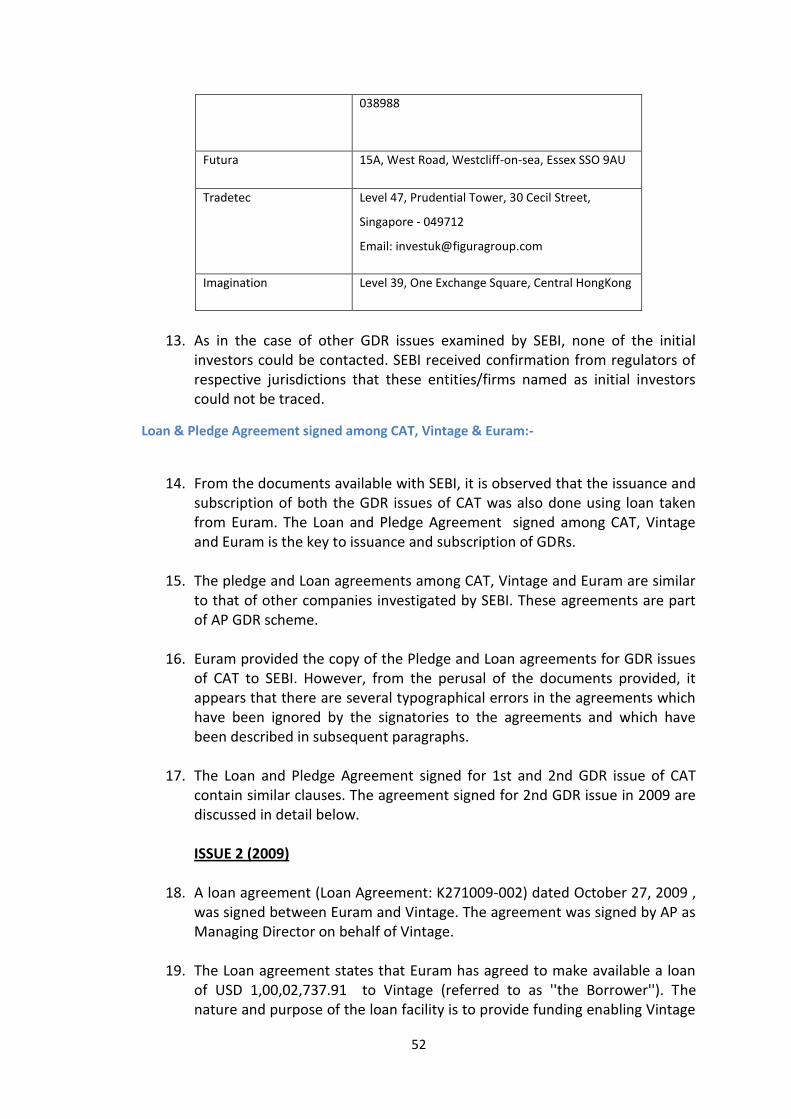

Contents ..................................................................................................................................... 1

Background ................................................................................................................................. 4

PART 1 - SCHEME OF MANIPULATION OF INDIAN MARKETS USING GDRS BY ARUN

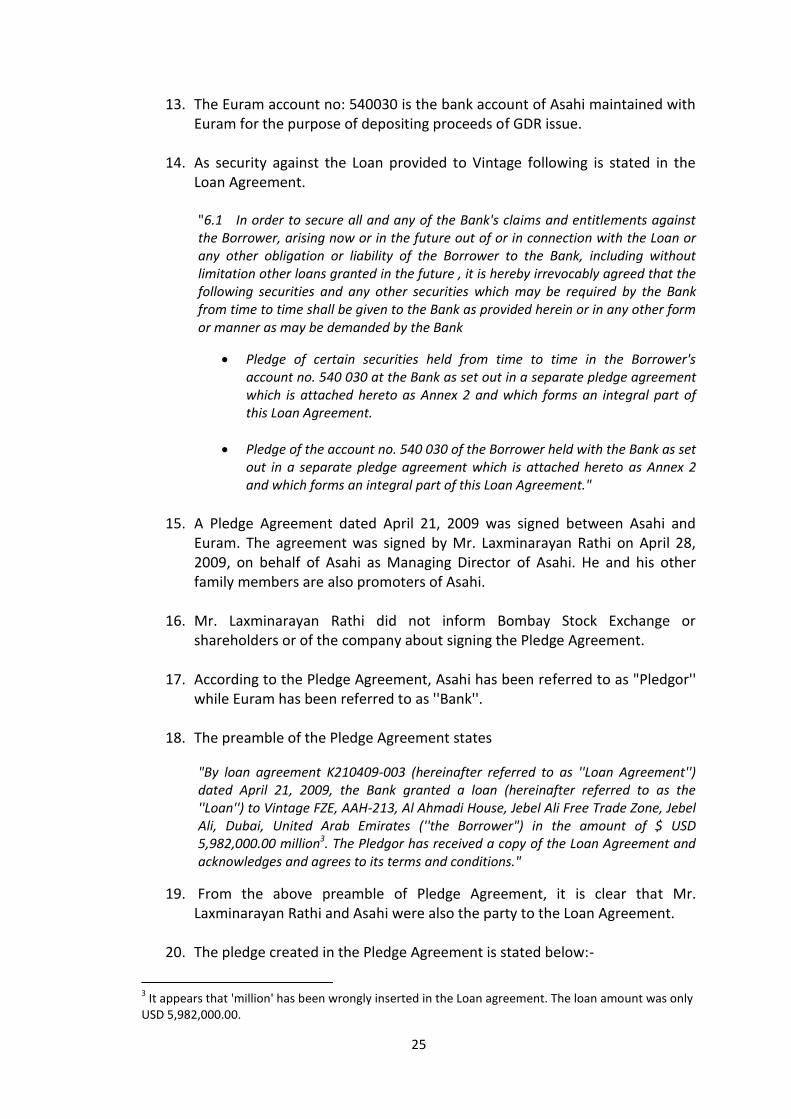

PANCHARIYA ............................................................................................................................... 6

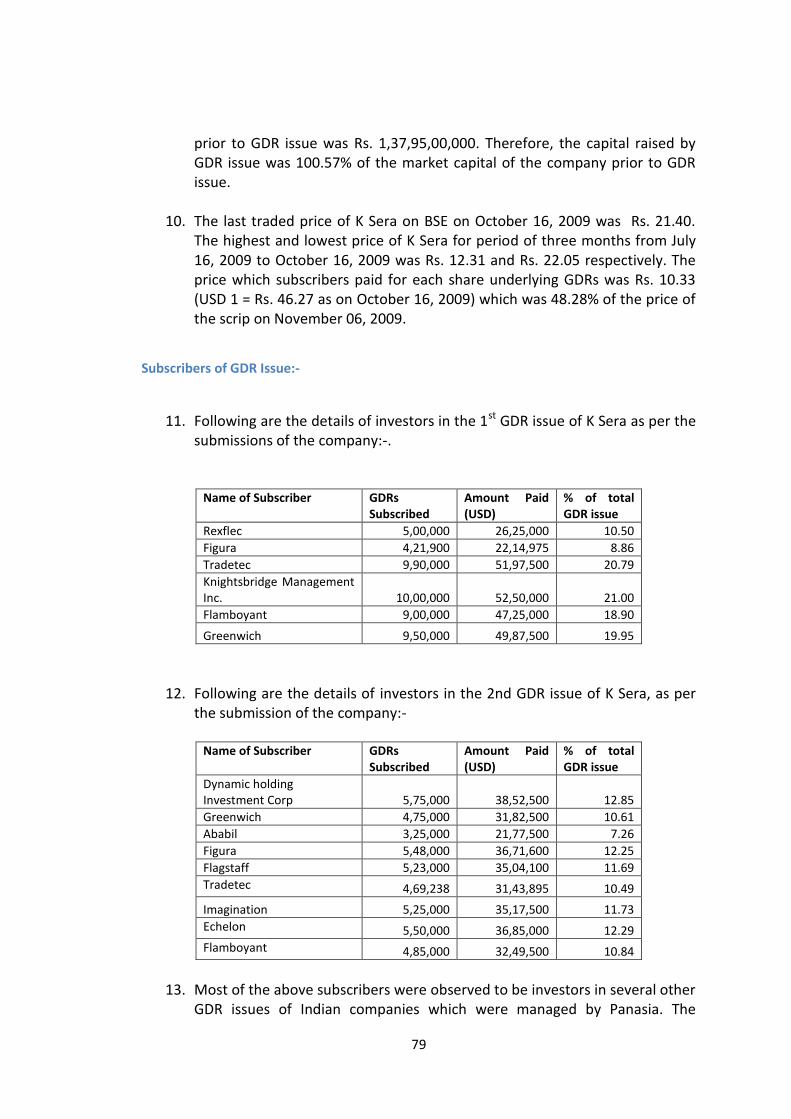

Definitions .................................................................................................................................. 6

Associations of Entities ............................................................................................................. 10

AP GDR Scheme ........................................................................................................................ 14

Step 1:- Issuance of GDRs ..................................................................................................... 15

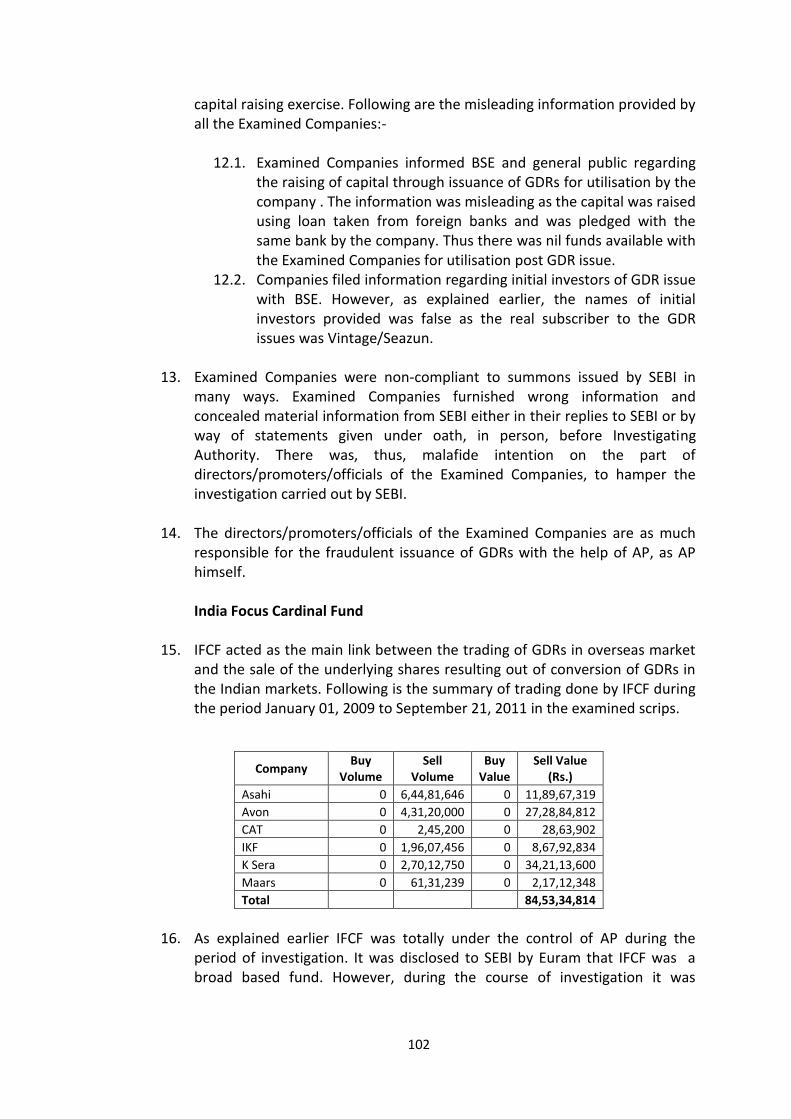

Step 2:- Cancellation of GDRs ............................................................................................... 19

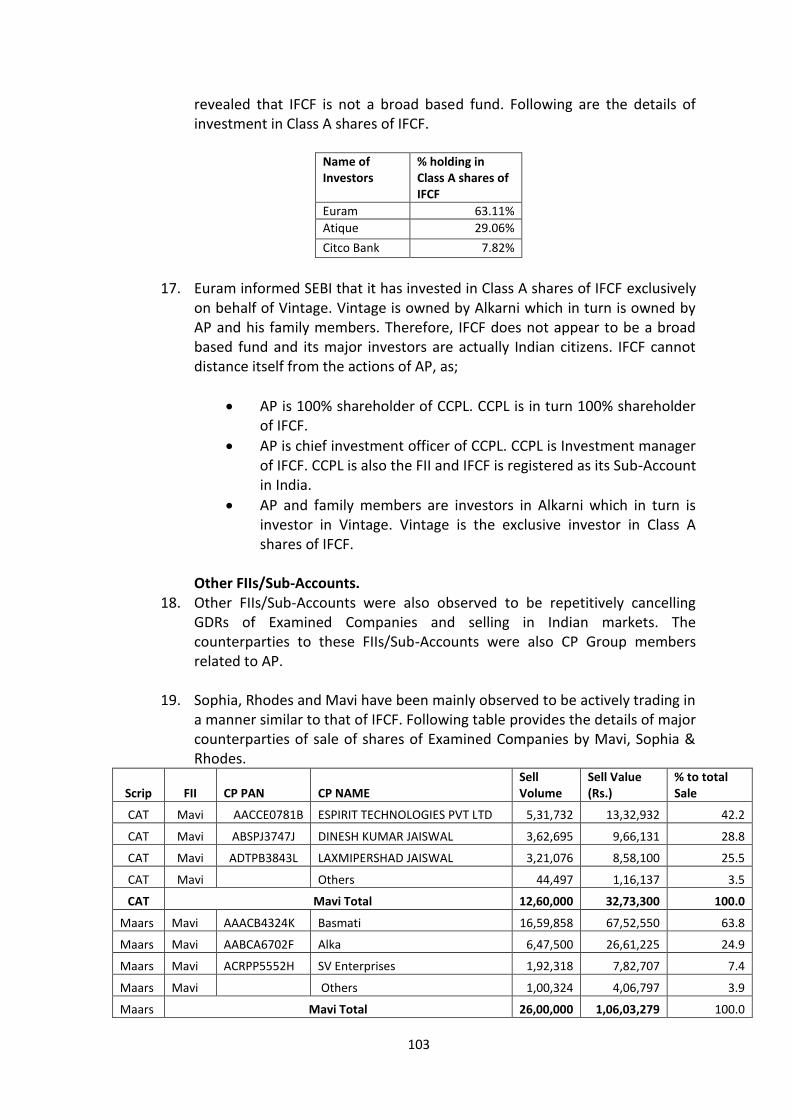

Step 3:-Sale of Shares to group of Indian clients and utilisation of GDR issue proceeds by

Examined Companies. .......................................................................................................... 20

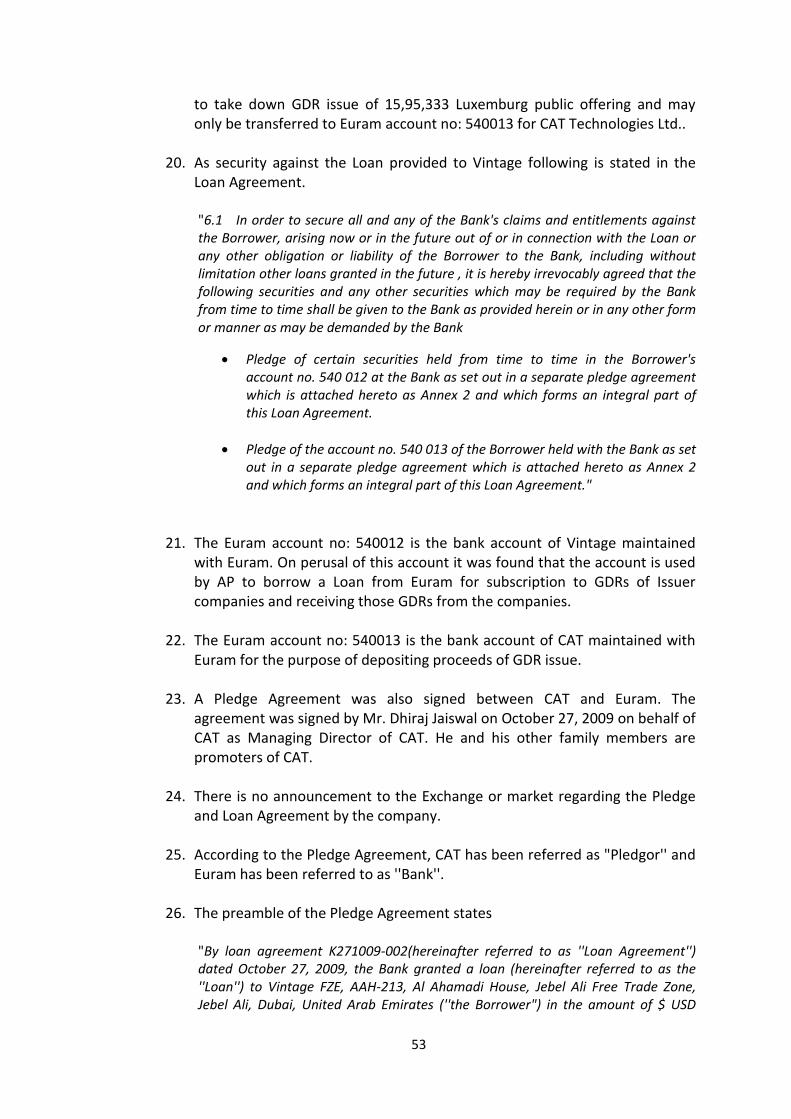

Detailed Investigation of Issuer Companies ............................................................................. 23

(I) ASAHI INFRASTRUCTURE AND POJECTS LTD. ................................................................... 23

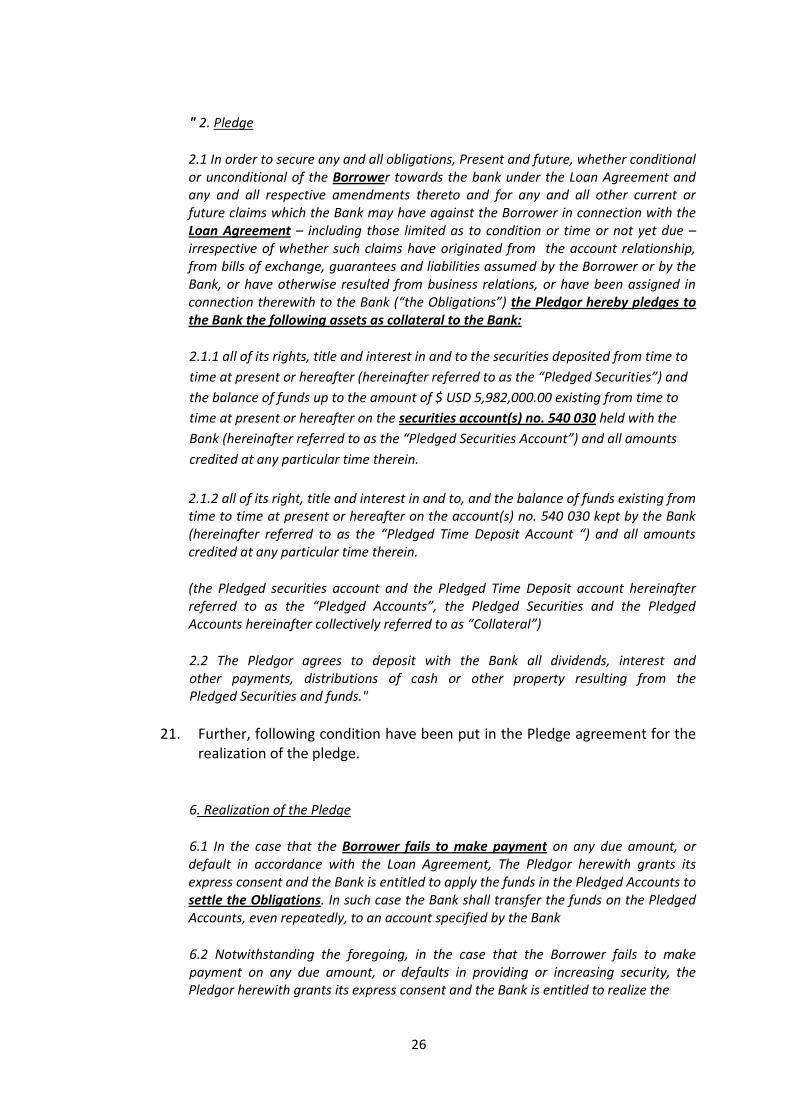

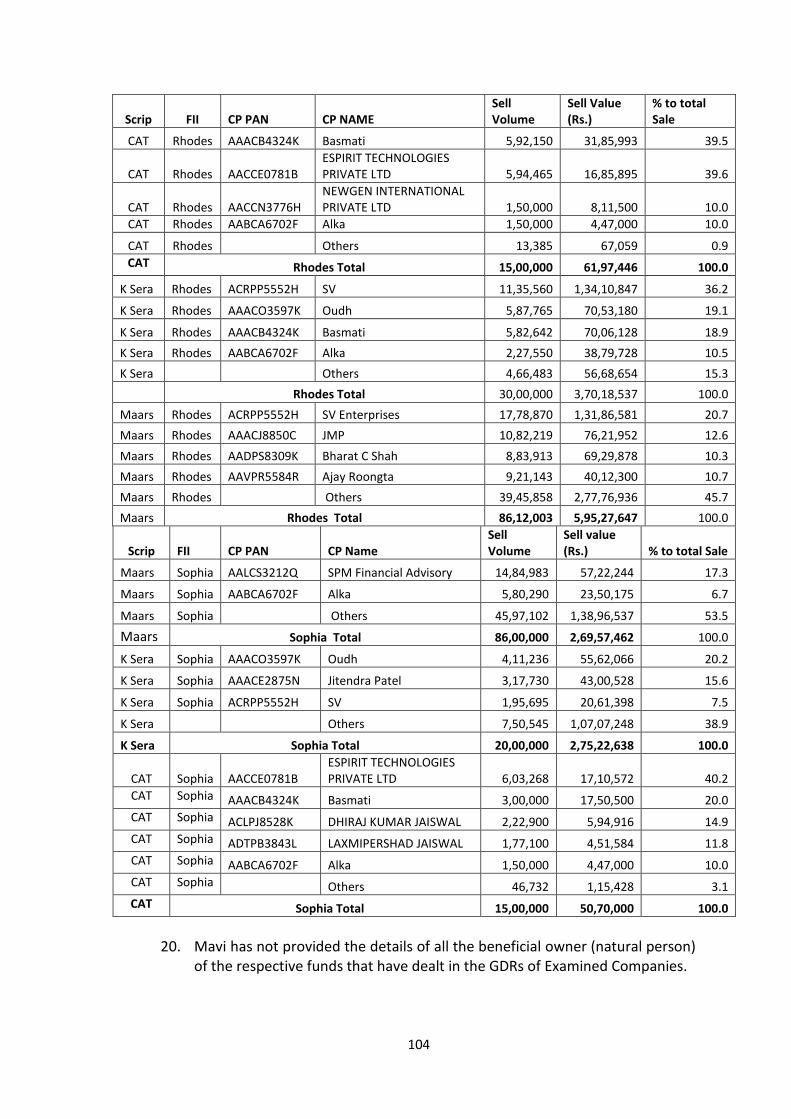

Summary of GDR issue:- ................................................................................................... 23

Subscribers of GDR Issue:- ................................................................................................ 23

Loan & Pledge Agreement signed among Asahi, Vintage & Euram. ................................ 24

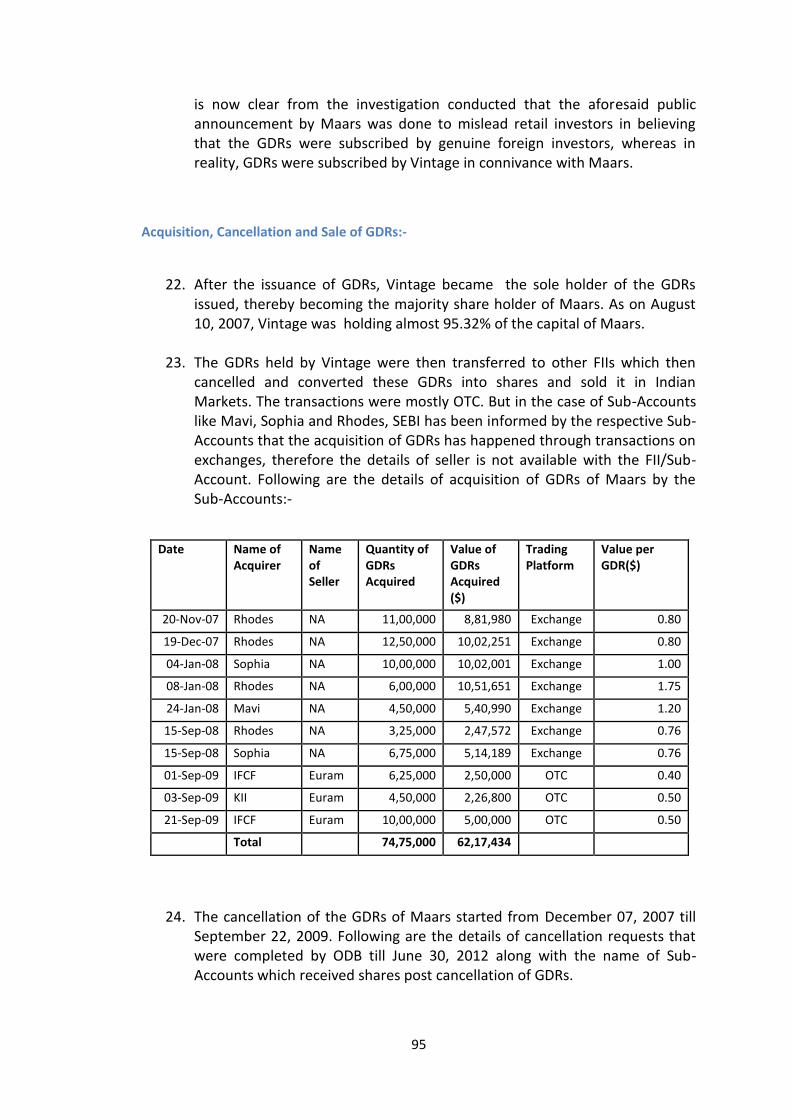

Acquisition Cancellation and Sale of GDRs:-..................................................................... 27

Utilisation of GDR proceeds by Asahi:- ............................................................................. 31

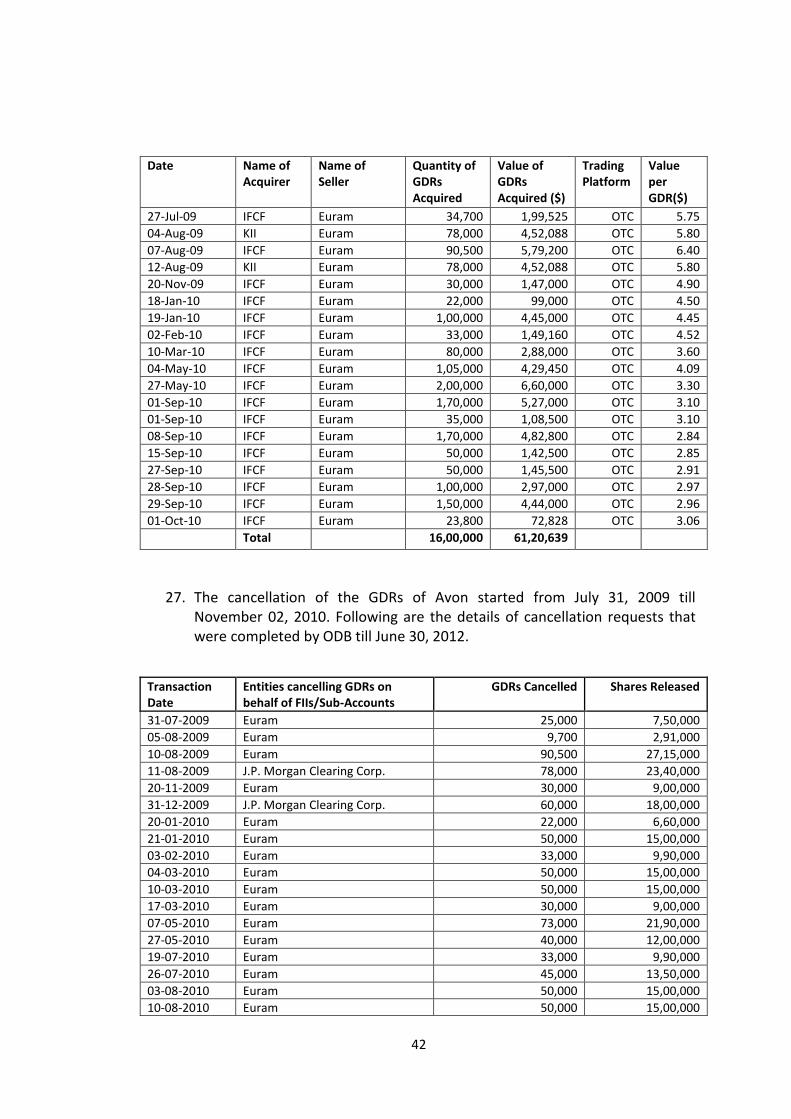

Misleading Submissions by Asahi:- ................................................................................... 35

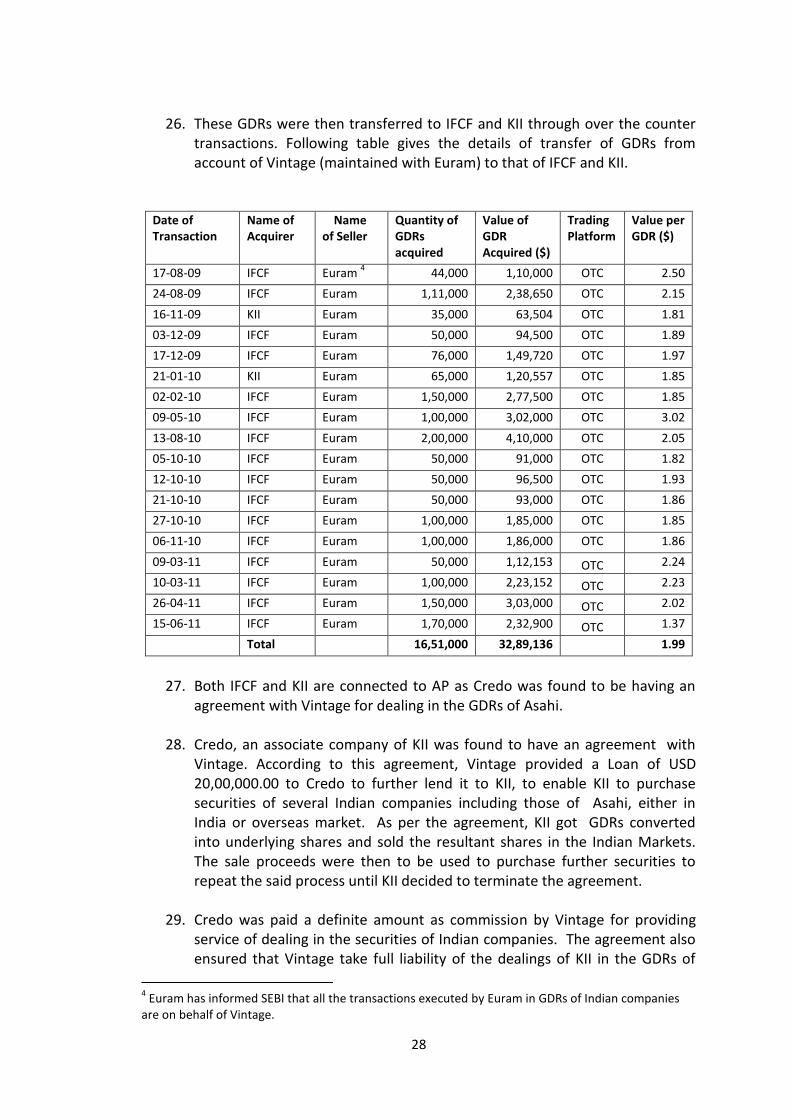

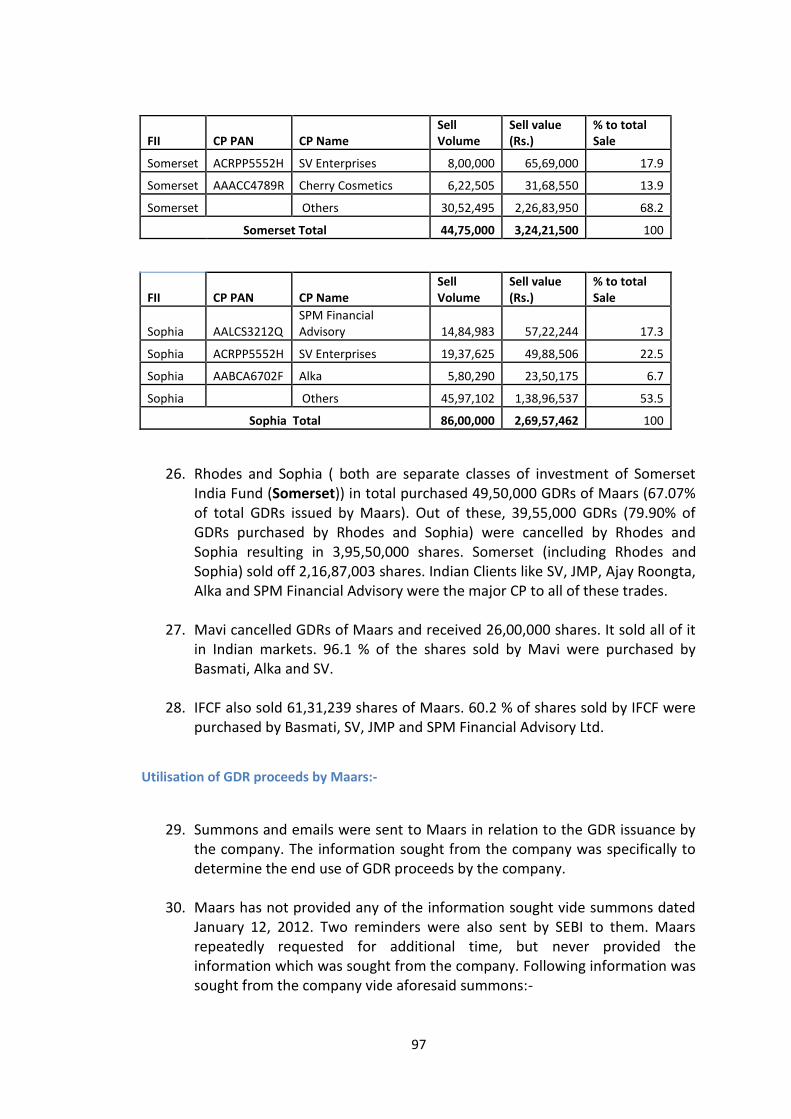

(II) AVON CORPORATION LTD. .............................................................................................. 37

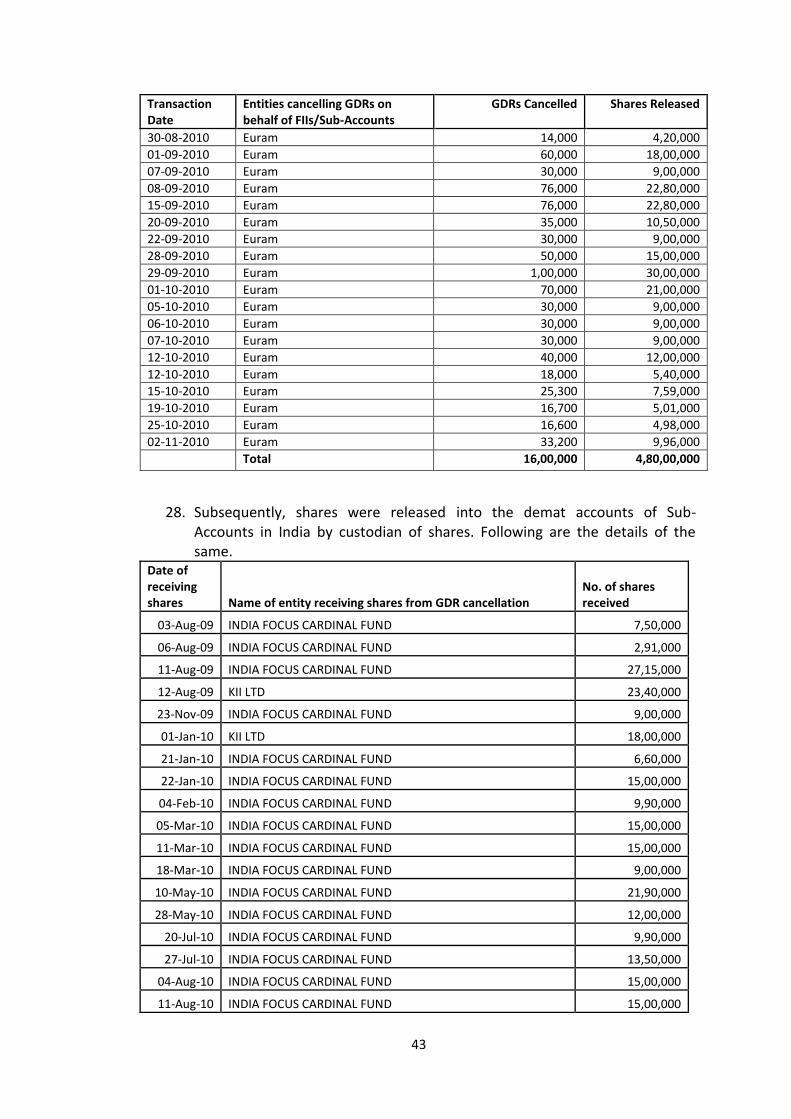

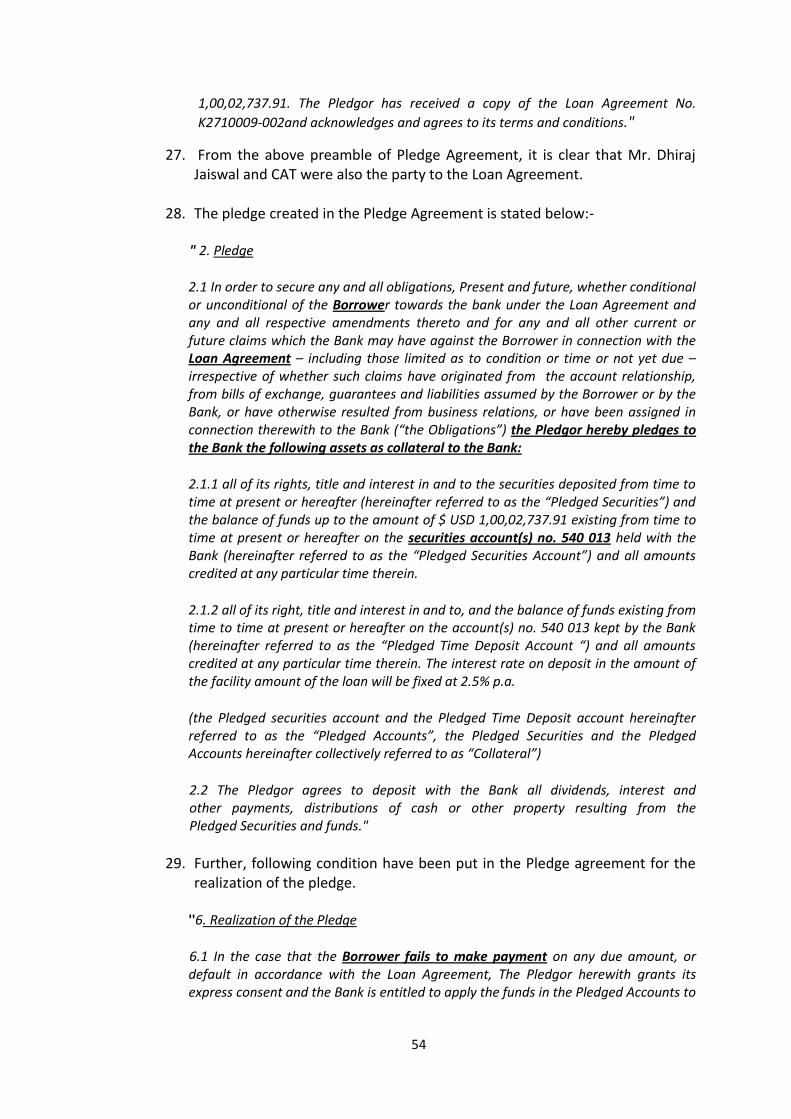

Summary of GDR issue:- ................................................................................................... 37

Subscribers of GDR Issue:- ................................................................................................ 37

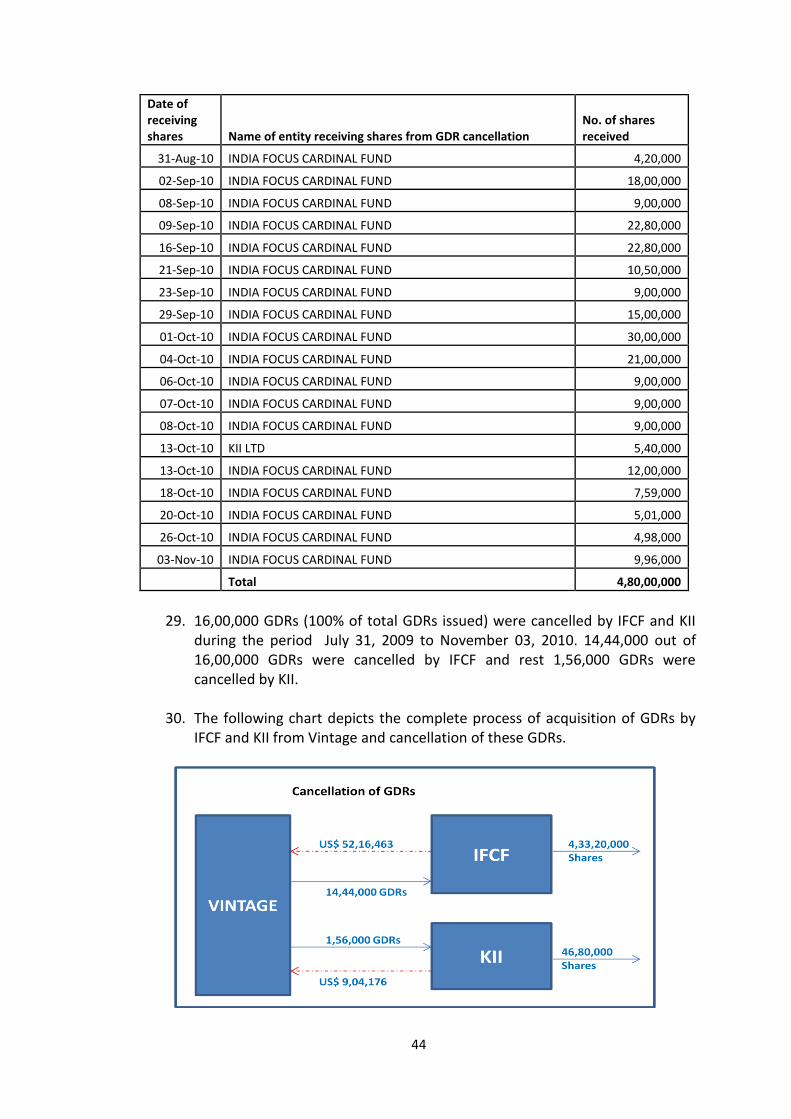

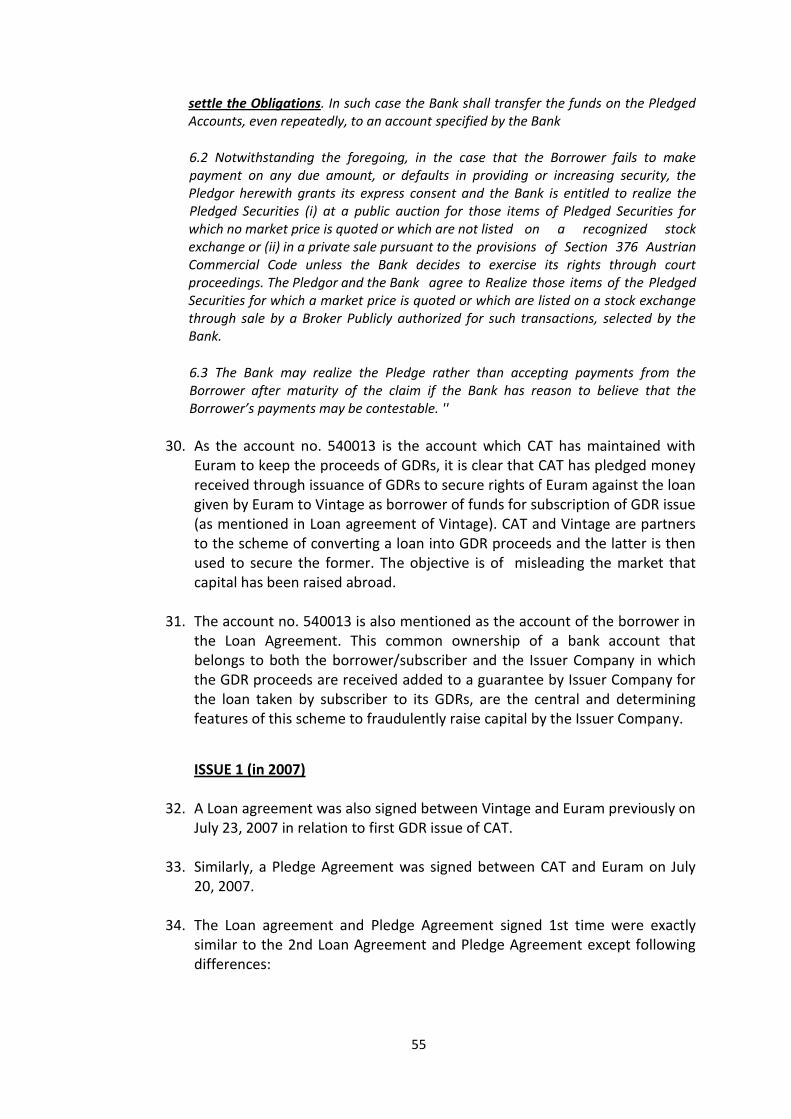

Loan & Pledge Agreement signed among Avon, Vintage & Euram. ................................. 38

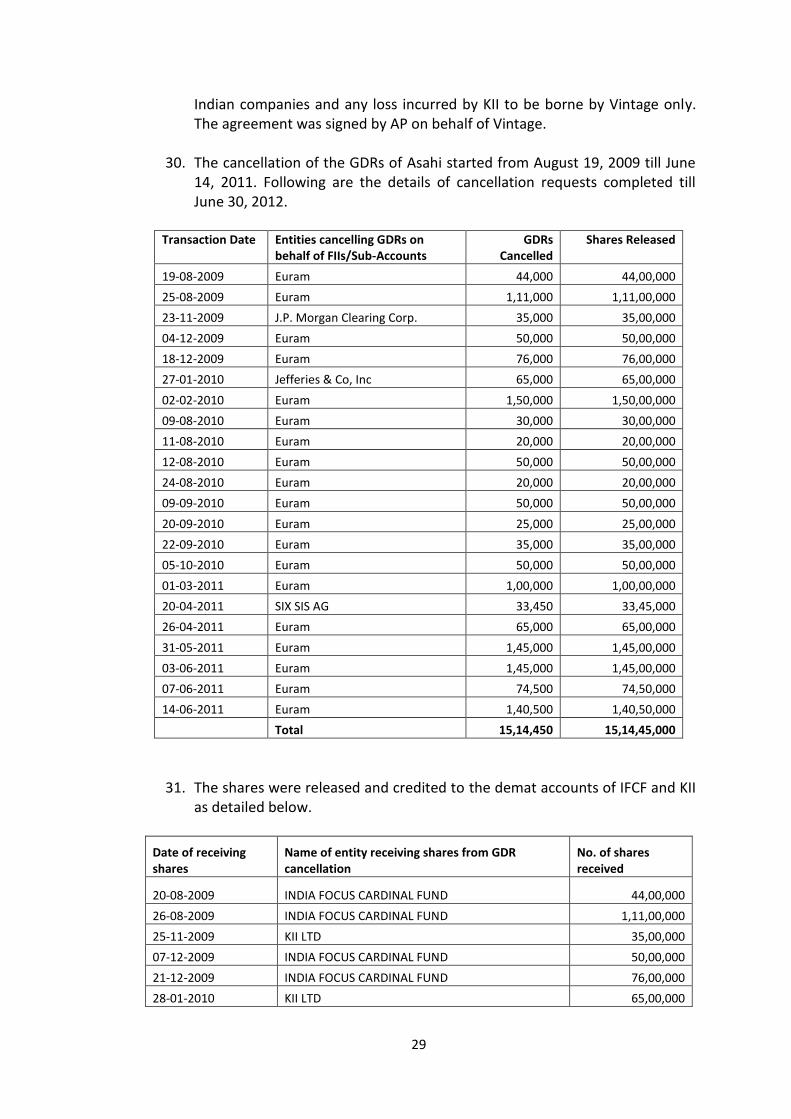

Acquisition Cancellation and Sale of GDRs:-..................................................................... 41

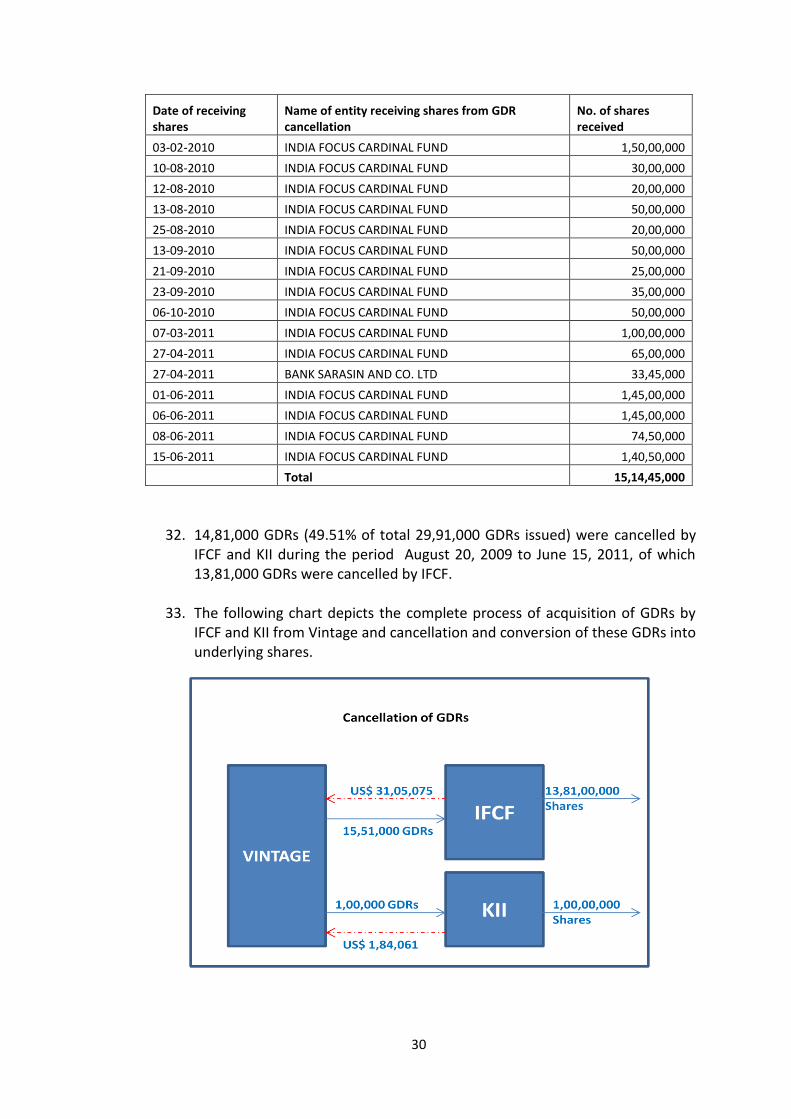

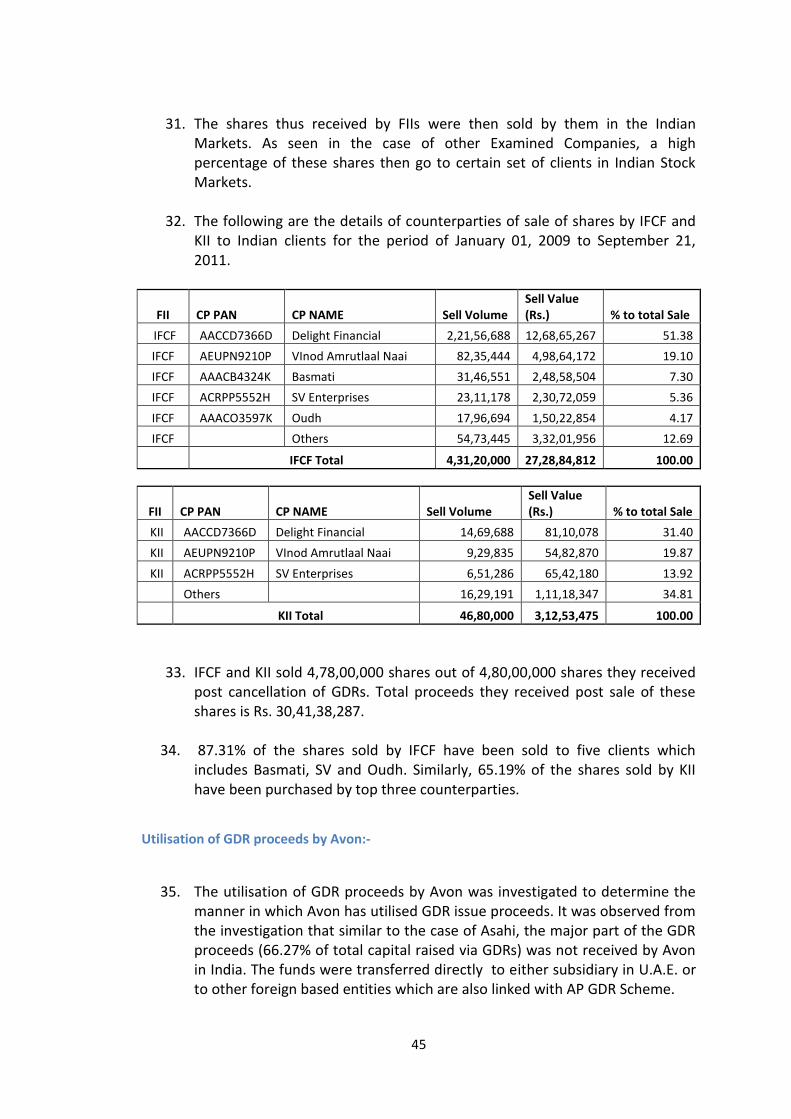

Utilisation of GDR proceeds by Avon:- ............................................................................. 45

Misleading Submissions by Avon:- ................................................................................... 48

(III) CAT TECHNOLOGIES LTD ................................................................................................ 50

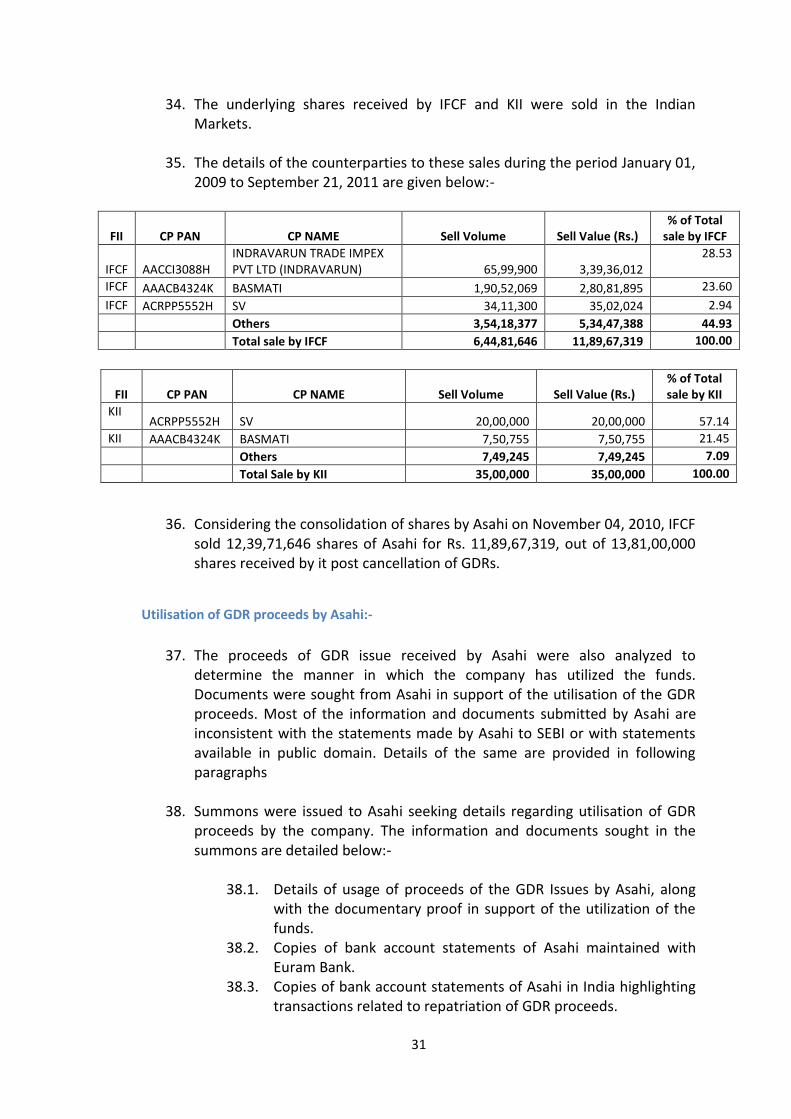

Summary of GDR issue:- ................................................................................................... 50

Subscribers of GDR Issue:- ................................................................................................ 51

Annexure 2

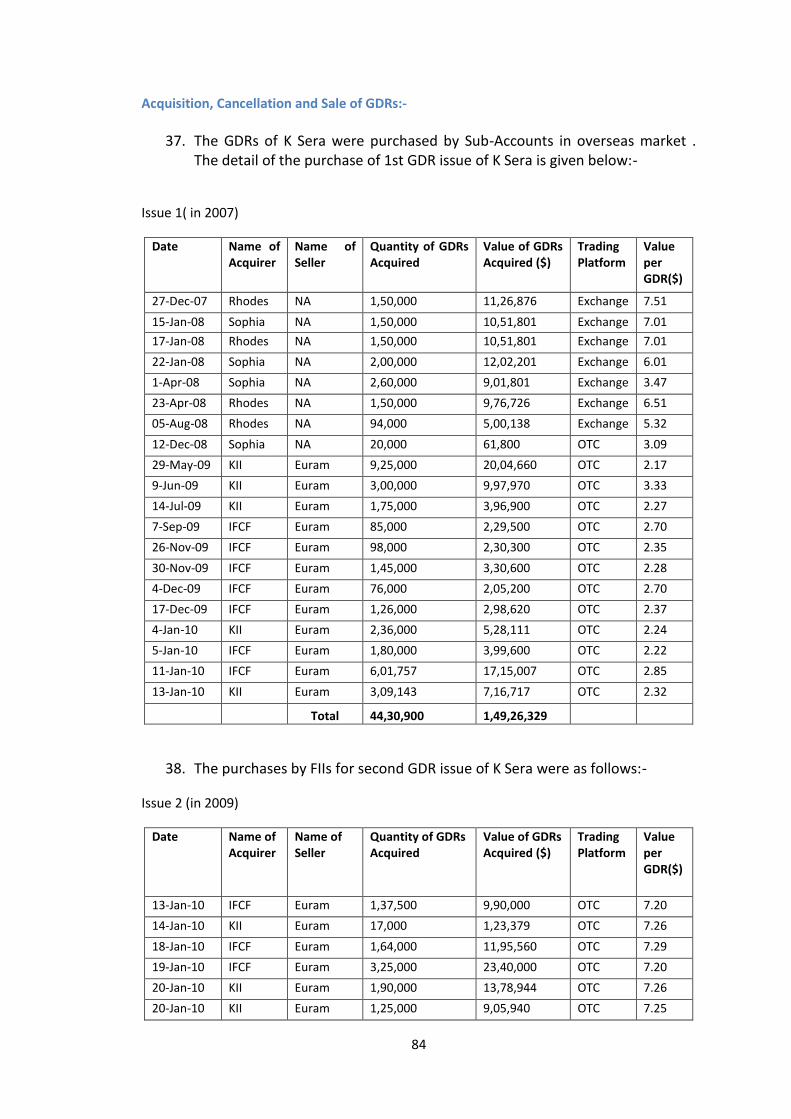

2

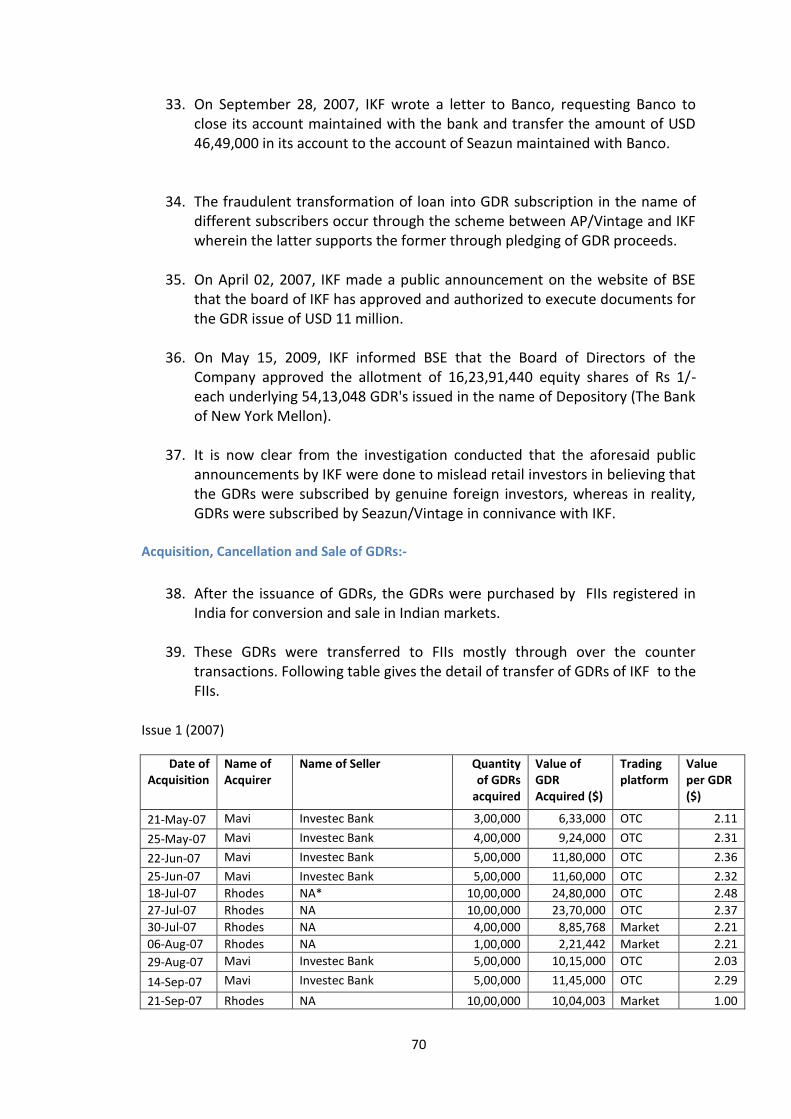

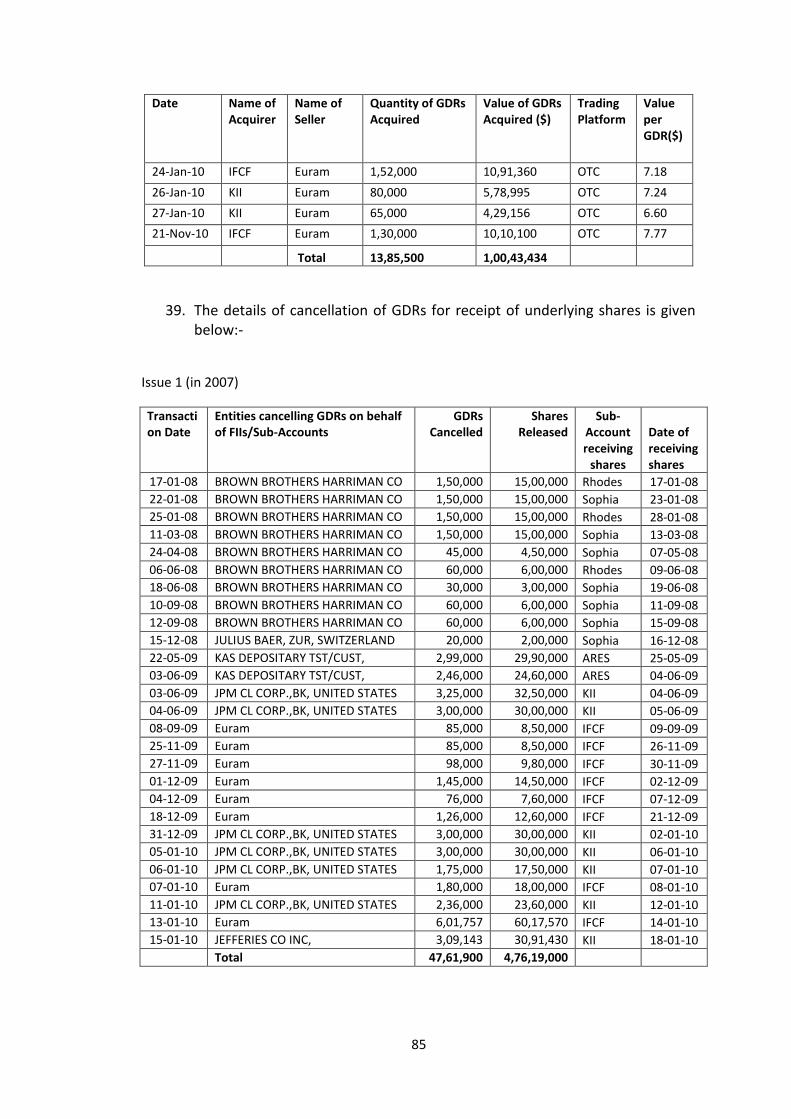

Loan & Pledge Agreement signed among CAT, Vintage & Euram:- ................................. 52

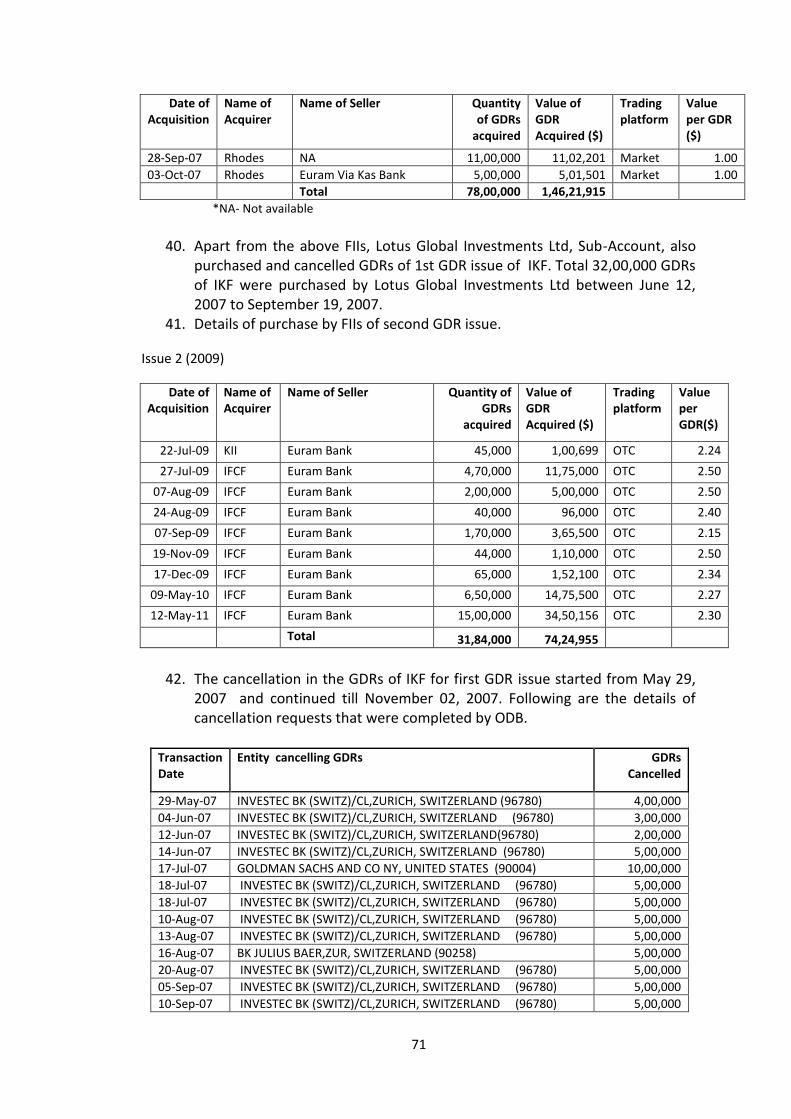

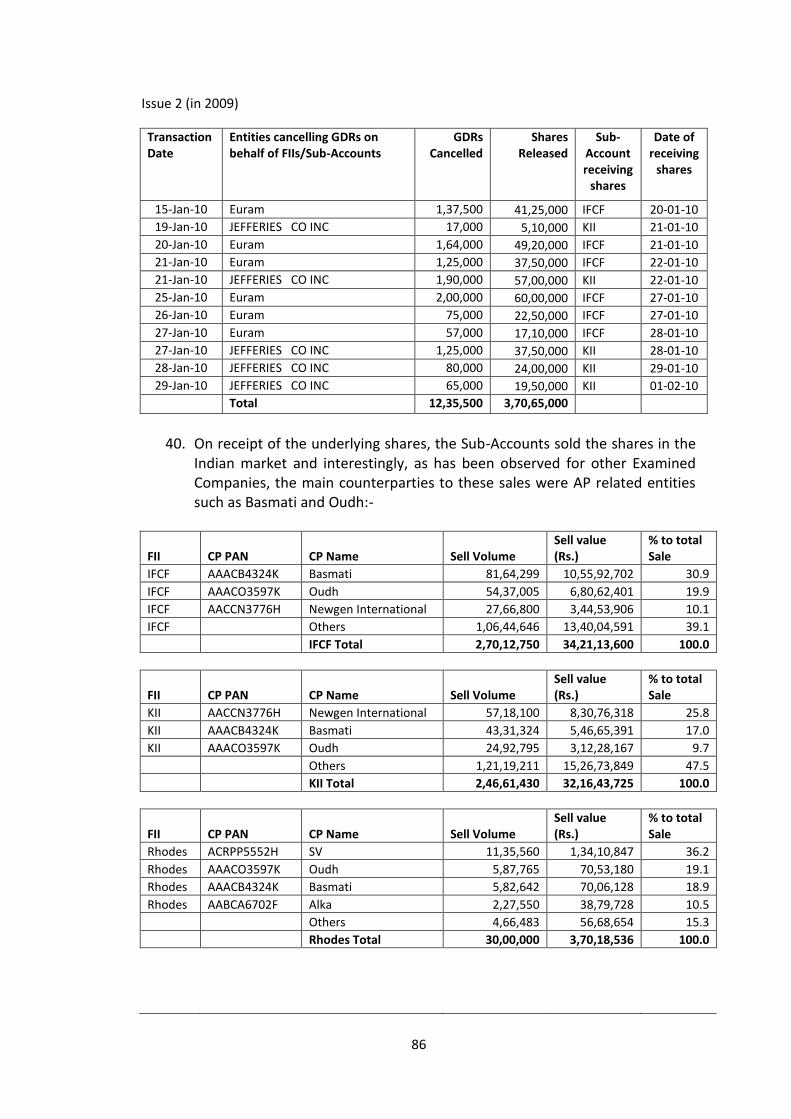

Acquisition Cancellation and Sale of GDRs:-..................................................................... 57

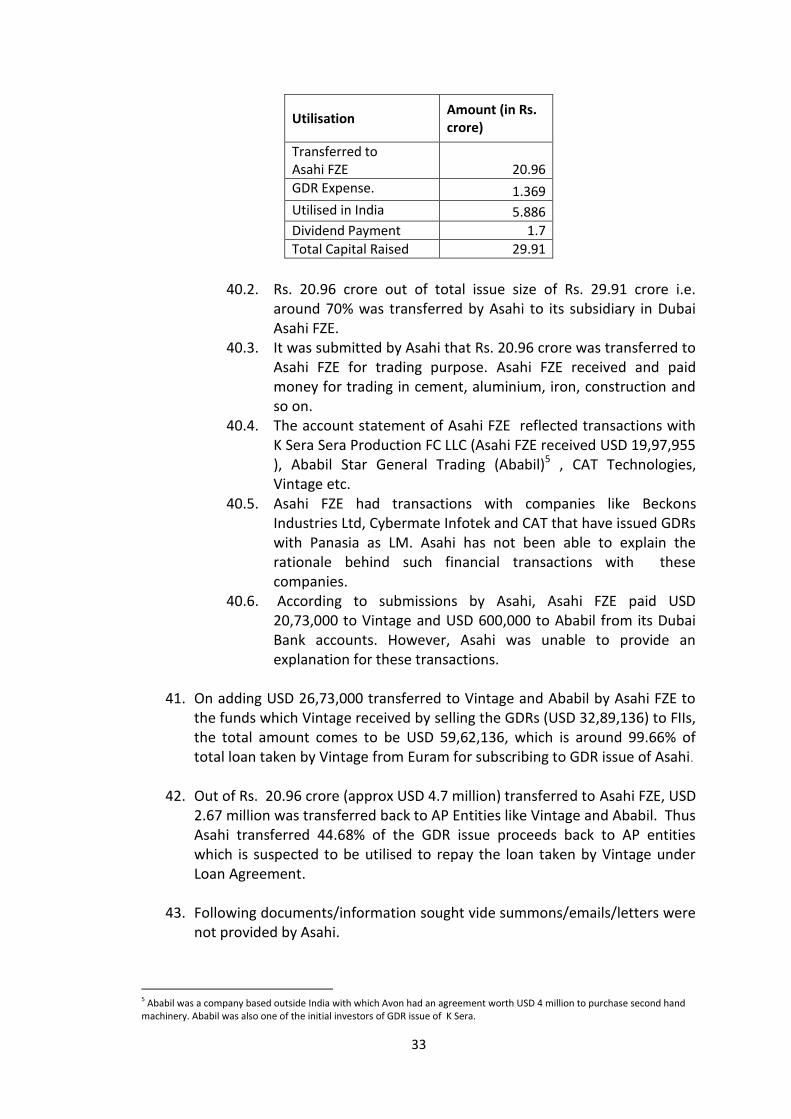

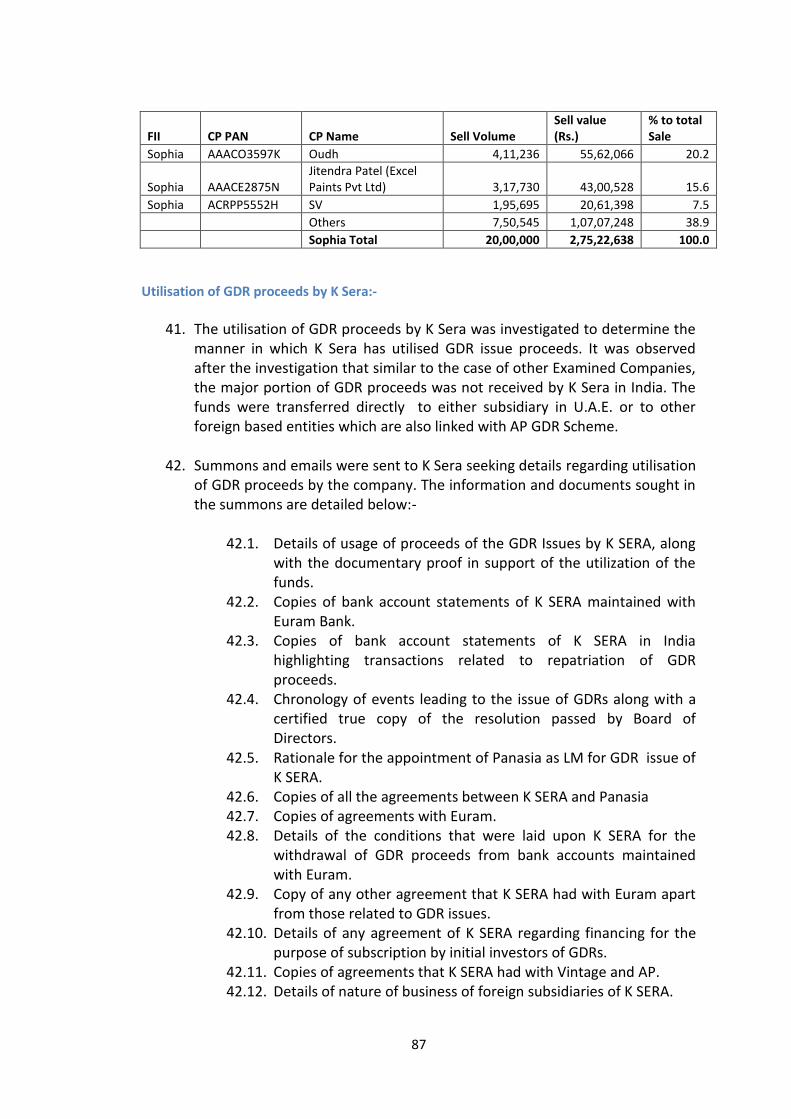

Utilisation of GDR proceeds by CAT:- ............................................................................... 60

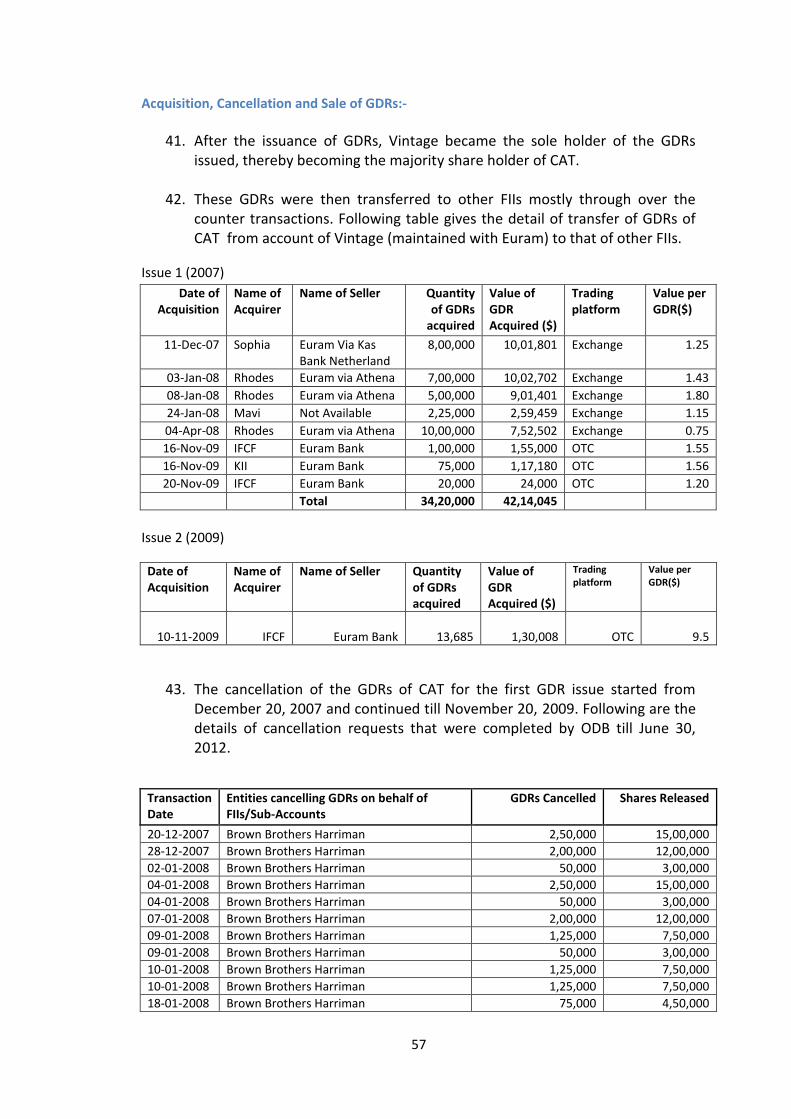

Misleading Submissions by CAT ....................................................................................... 62

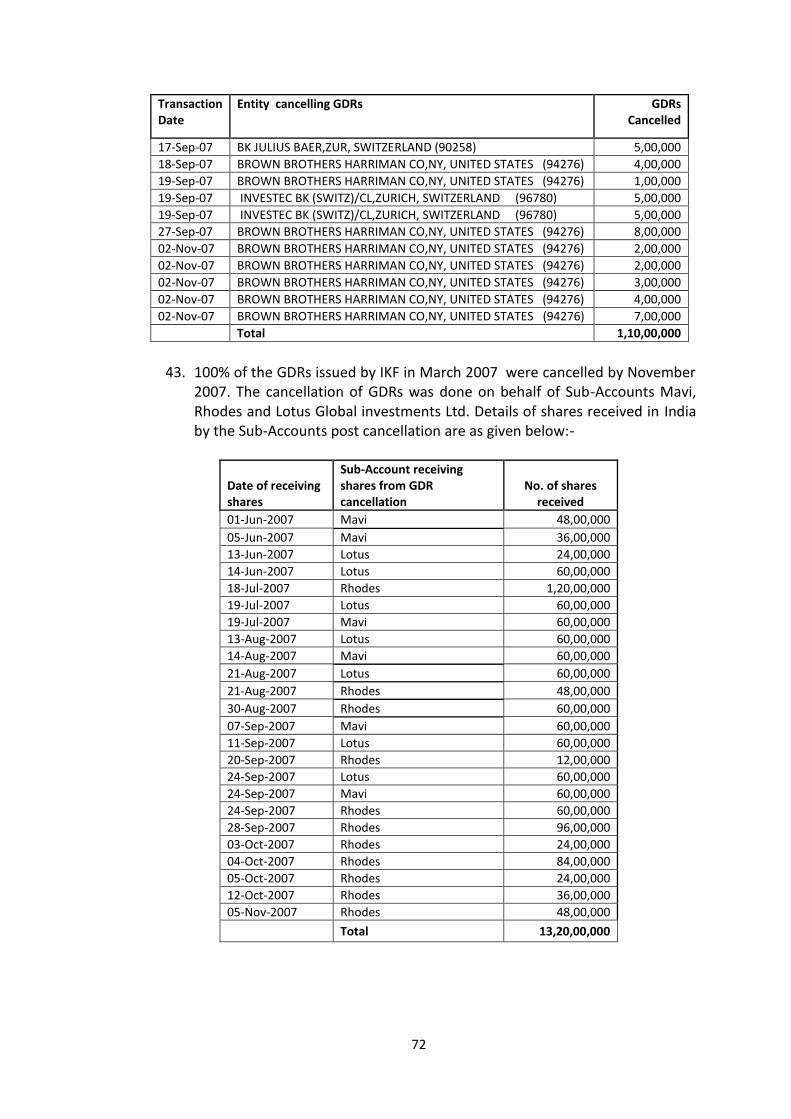

(IV) IKF TECHNOLOGIES LTD ................................................................................................. 64

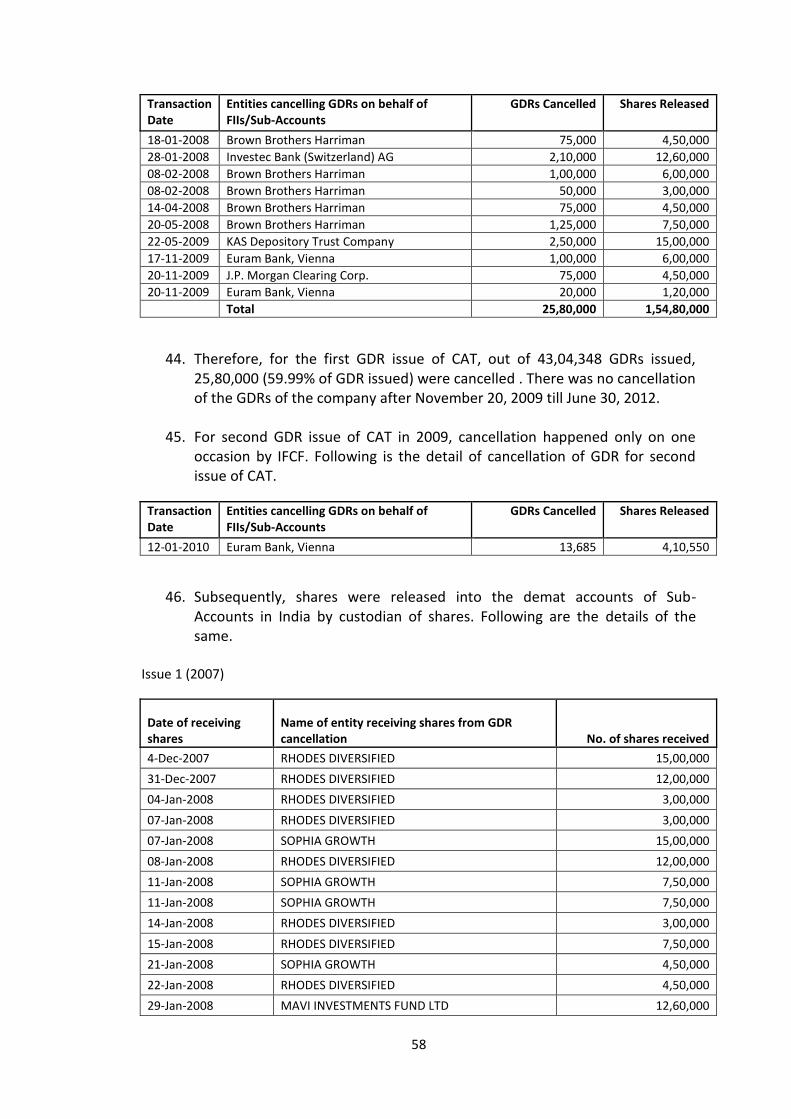

Summary of GDR issue:- ................................................................................................... 64

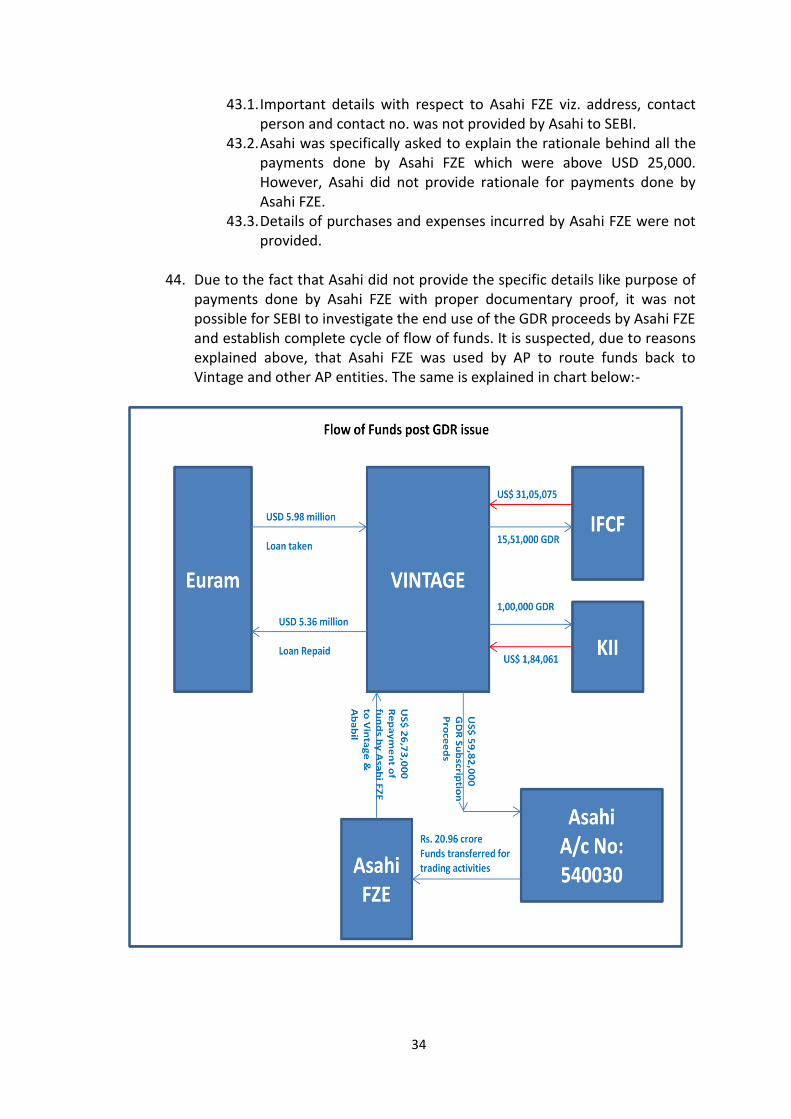

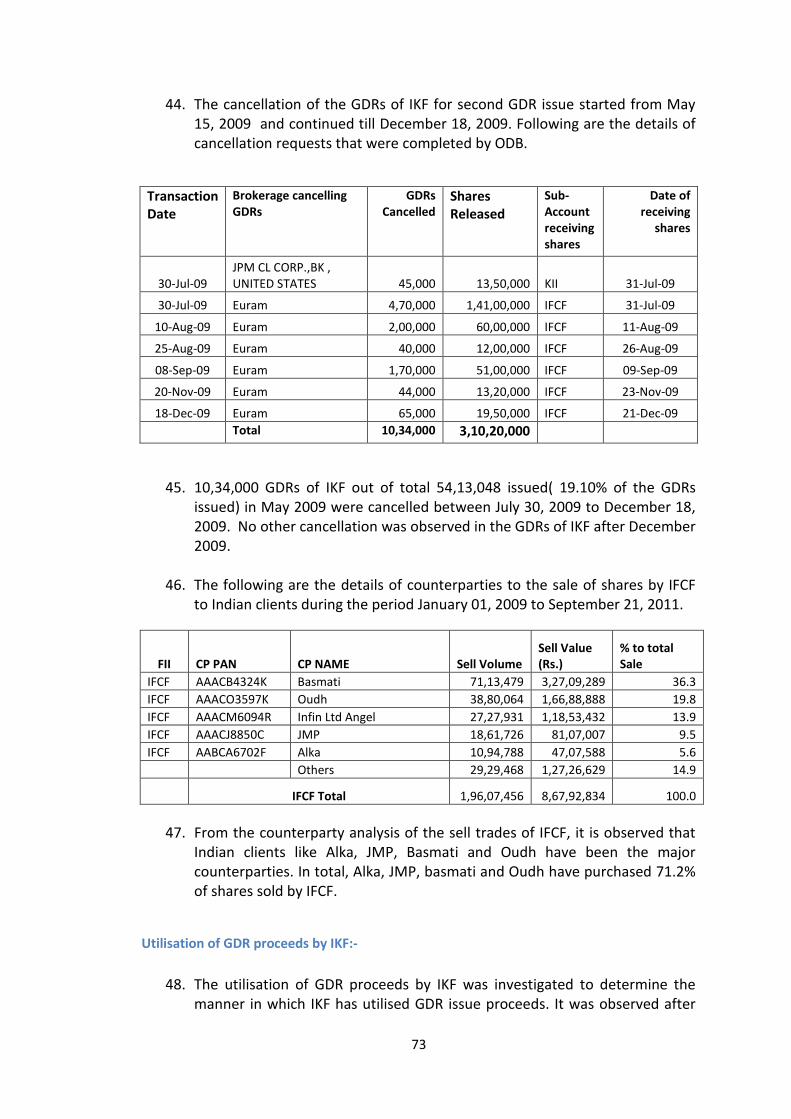

Subscribers of GDR Issue:- ................................................................................................ 65

Loan & Pledge Agreement signed among IKF, Vintage & Euram:- ................................... 65

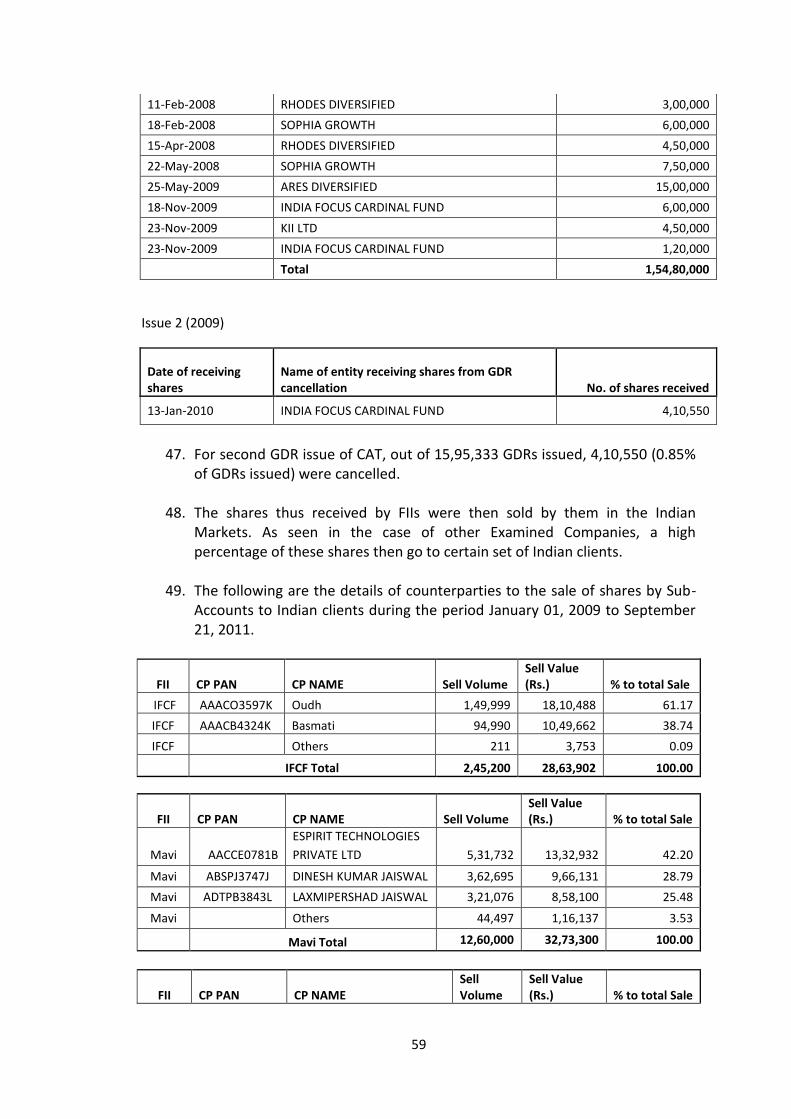

Acquisition Cancellation and Sale of GDRs:-..................................................................... 70

Utilisation of GDR proceeds by IKF:- ................................................................................. 73

Misleading Submissions by IKF ......................................................................................... 76

(V) K SERA SERA LTD ............................................................................................................. 78

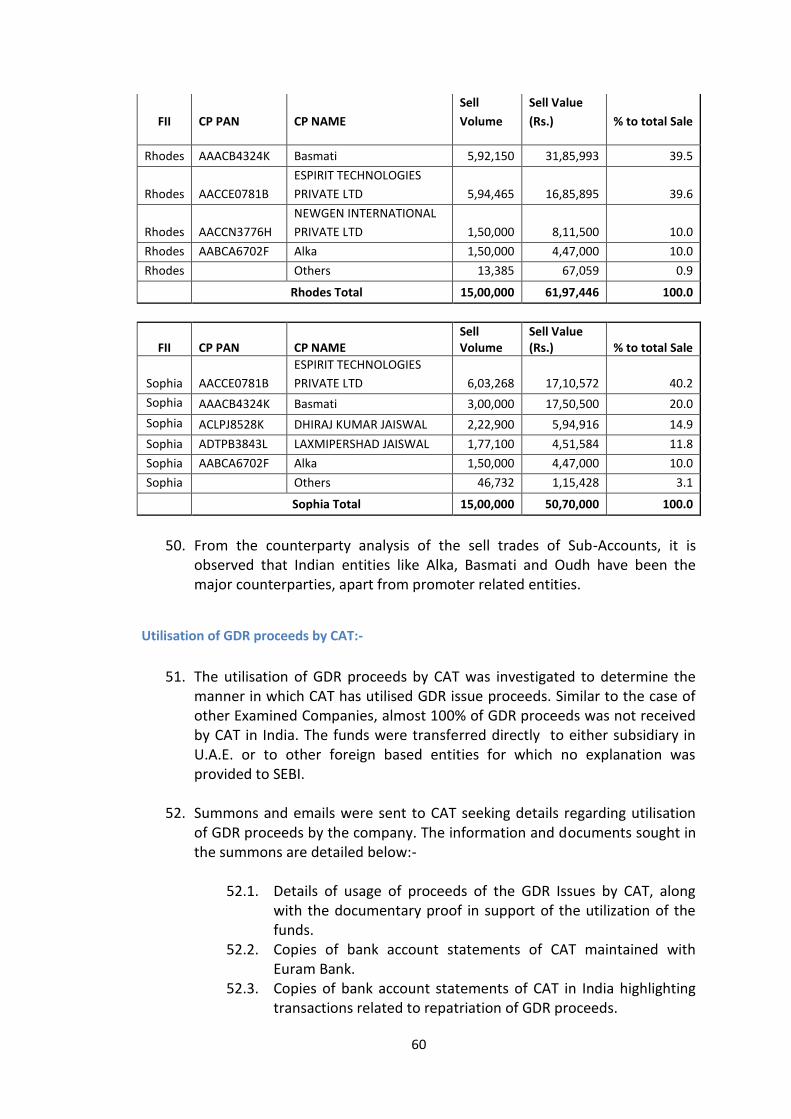

Summary of GDR issue:- ................................................................................................... 78

Subscribers of GDR Issue:- ................................................................................................ 79

Loan & Pledge Agreement signed among K Sera, Vintage & Euram:- .............................. 80

Acquisition Cancellation and Sale of GDRs:-..................................................................... 84

Utilisation of GDR proceeds by K Sera:- ........................................................................... 87

Misleading Submissions by K Sera .................................................................................... 89

(VI) MAARS SOFTWARE INTERNATIONAL LTD ...................................................................... 91

Summary of GDR issue:- ................................................................................................... 91

Subscribers of GDR Issue:- ................................................................................................ 91

Loan & Pledge Agreement signed among Maars, Vintage & Euram:- .............................. 92

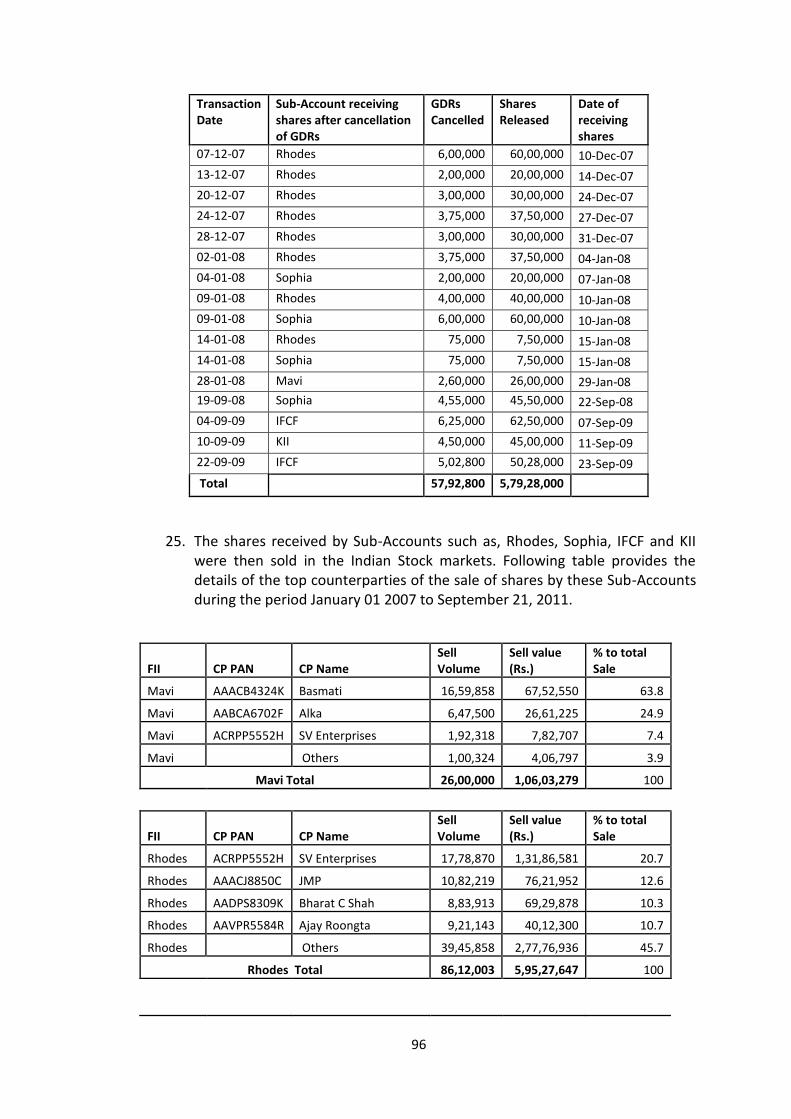

Acquisition Cancellation and Sale of GDRs:-..................................................................... 95

Utilisation of GDR proceeds by Maars:- ........................................................................... 97

Summary of role of entities involved in the market manipulation using GDRs ..................... 100

PART 2 - SCHEME OF MANIPULATION OF INDIAN MARKETS IN CALS REFINERIES ............ Error!

Bookmark not defined.

A. Summary of Cals GDR Issue:- ........................................... Error! Bookmark not defined.

B. Cals Shareholding & Ownership Structure:- .................... Error! Bookmark not defined.

C. Loan Agreement:- ............................................................ Error! Bookmark not defined.

D. Honor Finance Ltd:- ......................................................... Error! Bookmark not defined.

E. Account Charge Agreement:- .......................................... Error! Bookmark not defined.

F. Subscriber to the Cals GDR Issue:-................................... Error! Bookmark not defined.

G. Utilisation of GDR proceeds by Cals:- .............................. Error! Bookmark not defined.

Annexure 2

3

H. Analysis of transaction regarding Asiatexx Enterprises Limited ..... Error! Bookmark not

defined.

I. Misleading submissions made by Cals & Mr. Devanathan Sundararajan, MD of Cals.

Error! Bookmark not defined.

J. Summary of role of entities involved in the market manipulation using GDR issue of

Cals Error! Bookmark not defined.

Annexure 2

4

Background

Based on alerts received by SEBI in its IMSS system regarding a few scrips like IKF Technologies Ltd, Avon Corporation Ltd, Cat Technologies Ltd, Asahi Infrastructure Ltd and K Sera Sera Ltd, preliminary examination of trading in these scrips was conducted. It was revealed in the preliminary examination that certain FIIs/Sub-Accounts were converting the GDRs held by them into shares (known as ‘cancelling’ GDRs) and selling the resultant shares in the Indian markets. Further investigation revealed that the complete process of GDR issuance by these companies was devised and structured by Arun Panchariya (hereinafter referred to as "AP") in connivance with the issuer companies to the detriment of the Indian Investors.

Investigations were initiated in the matter and an Interim Order was passed on September 21, 2011 against AP, 7 listed companies that issued GDRs, 4 Sub-Accounts, 1 FII, 5 Indian companies trading in these scrips, and 1 foreign based Lead Manager. Following are the entities against whom directions were issued in the said Order:-

Lead Manager:- 1. Arun Panchariya (AP) 2. Pan Asia Advisors Ltd (Panasia), Lead Manager

Sub-Accounts/FIIs:-

3. India Focus Cardinal Fund(IFCF), Sub-Account 4. MAVI Investment(Mavi), Sub-Account 5. KII Ltd (KII), Sub-Account 6. Sophia Growth - A share Class of Somerset India Fund (Sophia), Sub-Account 7. European American Investment Bank Ag (Euram), FII

Indian Clients

8. Basmati Securities Pvt. Ltd( Basmati) 9. Oudh Finance & Investment Private Ltd (Oudh) 10. Alka India Ltd (Alka) 11. SV Enterprises (SV) 12. JMP Securities Pvt. Ltd (JMP)

GDR Issuers

13. Asahi Infrastructure & Projects Ltd(Asahi) 14. IKF Technologies Ltd. (IKF) 15. Avon Corporation Ltd (Avon) 16. K Sera Sera Ltd (K Sera) 17. CAT Technologies Ltd (Cat) 18. Maars Software International Ltd (Maars) 19. Cals Refineries Ltd. (Cals)

Annexure 2

5

The investigations conducted into the case have clearly revealed that in the case of Asahi, Avon, IKF, K Sera, CAT and Maars, AP and other entities/companies/FIIs/Sub-Accounts connected to him or to his brother Satish Panchariya (collectively referred to as AP Entities), including Panasia have played key role in structuring of GDR issues of Indian Companies. These GDRs were issued by companies (Issuer Companies) with the help of AP, wherein AP arranged for loans for the subscription of GDRs and thereafter converted the GDRs into underlying shares. The underlying shares were sold to Indian investors with the help of FIIs/Sub-Accounts as well as certain Indian entities connected to AP. The activities of AP along with AP Entities involved in the whole scheme have resulted in Indian retail investors ultimately bearing the cost of these GDRs. The Part 1 of this investigation report deals with this fraudulent scheme perpetrated by AP to defraud Indian retail investors.

Part 2 of the report deals with the fraud perpetrated by promoters and directors of

Cals Refineries Ltd. in Indian Stock Market. Cals announced a huge project of shifting

and relocating a refinery from Germany in West Bengal. However, as investigations

revealed, the GDR issuance was organized to defraud Indian investors and dump the

shares generated out of conversion of GDRs on Indian retail investors.

The detailed investigation of creation of false market by clients connected to AP and

sale of shares by FIIs to such clients and Indian retail investors is dealt in a

supplementary report which will be soon completed. The period of investigation is

from January 01, 2009 to September 21, 2011. In the case of Maars, the examination

period for trading by the FIIs and Counterparty Group is from January 01, 2007 till

September 21, 2011.

Annexure 2

6

PART 1 - SCHEME OF MANIPULATION OF INDIAN

MARKETS USING GDRS BY ARUN PANCHARIYA

Definitions

Alka Alka India Ltd., a company listed on BSE has the following family

members of AP acting as promoters,

1. Ramswaroop Panchariya 2. Ashok Panchariya 3. Gopikishan Panchariya 4. Geetabai M Purohit 5. Satish R Panchariya 6. Arun R Panchariya 7. Ramswaroop B Panchariya 8. Shantidevi Panchariya 9. Saritadevi Panchariya 10. Madhudevi Panchariya 11. Radhadevi Panchariya 12. Shantidevi R Panchariya 13. Radhadevi S Panchariya 14. Arun Ramswaroopji Panchariya 15. Ramswaroopji B Panchariya 16. Satish R Panchariya

Alkarni Alkarni Holdings Ltd, a company registered in British Virgin Island

(BVI) with following shareholders:-

1. Arun Panchariya 2. Ashok Panchariya 3. Radhadevi Satish Panchariya 4. Sarita Arun Panchariya 5. Madhudevi Ashok Panchariya

AP Mr. Arun Panchariya

AP GDR Scheme The scheme devised by AP wherein Structured GDRs are issued by Indian companies with the help of AP and ultimately offloaded in Indian markets to unsuspecting retails investors.

Annexure 2

7

Ashok Mr. Ashok Panchariya, brother of AP & Satish Panchariya

Atique Atique Al Aqadi Trading Company was one of the investor in Class A shares of India Focus Cardinal Fund. It was also one of the shareholders of Panasia.

Banco Banco Efisa SFE, A bank based in Portugal, which financed the first GDR issue of IKF in 2007.

Cancelling GDRs As GDRs are issued, equivalent numbers of shares are issued in India and kept frozen with the Indian custodian. When GDRs are cancelled by any entity, it tenders GDRs to the Overseas Depository Bank (ODB) and equivalent number of shares are issued by the Indian Custodian to that entity.

CCPL Cardinal Capital Partners Ltd, a company owned 100% by AP and it is Investment manager of IFCF. CCPL is also 100% owner of IFCF.

CP Group Counterparty Clients Group, Group of Indian companies/individuals which has acted as major counterparty to selling of shares by FIIs in Indian markets only to gradually sell these shares to genuine retail investors by creating false volumes in Indian markets.

Euram European American Investment Bank AG, Austria , It is a bank based in Vienna Austria which was also registered as an FII with SEBI in INDIA till November 20, 2011.

Euram Accounts

The bank accounts of Issuers and other entities maintained with Euram.

Euram Asia European American Asia Ltd, A joint venture in Dubai between Euram and Panasia. The Joint Venture after its incorporation acts as a Loan agent for Euram and Listing agent for GDR issuing

Examination Period

Period of January 01, 2009 to September 21, 2011 (unless otherwise mentioned)

Examined Companies1

Following 6 companies which were examined for their GDR issues

and trading in Indian markets :-

1. Asahi Infrastructure & Projects Ltd 2. Avon Corporation Ltd 3. CAT Technologies Ltd

1 GDR issues of 7 companies were investigated by SEBI which included CALS Refineries Ltd. A separate report has been prepared for CALS. Therefore, in this report Examined Companies refers to only six companies in which Mr. Arun Panchariya was found to be involved.

Annexure 2

8

4. IKF Technologies Ltd. 5. K Sera Sera Ltd 6. Maars Software International Ltd

GDR Accounts The Bank Account of an Issuer maintained with a foreign bank to deposit the proceeds of GDR issue. In all the GDR issues investigated and discussed in this report (except the first GDR issue of IKF in 2007 which had Banco as the bank maintaining GDR Accounts) the GDR accounts have been maintained with Euram.

GDR Guidelines Scheme for issue of Foreign Currency Convertible Bonds (FCCB) and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993 and guidelines issued by the Central Government there under from time-to-time.

IFCF India Focus Cardinal Fund, a fund based in Mauritius and is registered with SEBI as a Sub-Account. AP is 100% owner of IFCF through its company Cardinal Capital Partners Ltd. AP and its family members are major investors in the fund through their associated companies. AP was director of the IFCF until October 28, 2010.

Interim order SEBI Interim Order dated September 21, 2011 passed against 19 entities due to their role in Structuring of GDRs

Issuers / Issuer Companies

Indian companies which issue GDRs.

KII Ltd KII, A Sub-Account which has similar pattern of trading like IFCF

LM Lead Manager to GDR Issues

Loan Agreement A Loan Agreement signed between the subscriber of GDR issuance and a foreign bank (Euram or Banco) for the purpose of financing of the GDR issues.

Mavi Mavi Investment Fund Ltd., Sub-Account

ODB Overseas Depository Bank; In a GDR issuance the GDRs are issued by the issuer in the name of the overseas depository bank and the overseas depository Bank or ODB subsequently issues the GDRs to non-resident investors, known as GDR holders.

Panasia Pan Asia Advisors Ltd, a lead manager based in UK which was founded by AP. AP is 100% shareholder of Panasia. AP was also

Annexure 2

9

director of the fund until September 29, 2011.

Pledge Agreement

An Agreement signed between foreign bank (Euram or Banco ) with issuer companies wherein the issuer pledges its accounts with bank against the loan provided by bank for subscription of GDR issuance.

Sophia Sophia Growth – A share Class of Somerset Fund, Sub-Account

SP Mr. Satish Panchariya, brother of AP

Structured GDRs GDRs issued by companies with the help of AP wherein AP arranged for loans for the subscription of GDRs (due to insufficient investor appetite, domestic or overseas) and sold to Indian investors with the help of FIIs and Indian clients connected to AP.

Vintage Vintage FZE, a company established in Jebel Ali Free Zone, Dubai on January 02, 2001. AP is founder and director of Vintage and management and control are vested with AP. Alkarni is 100% shareholder of Vintage. Subsequent to Interim order, name of Vintage has now changed to Alta Vista International FZE.

10

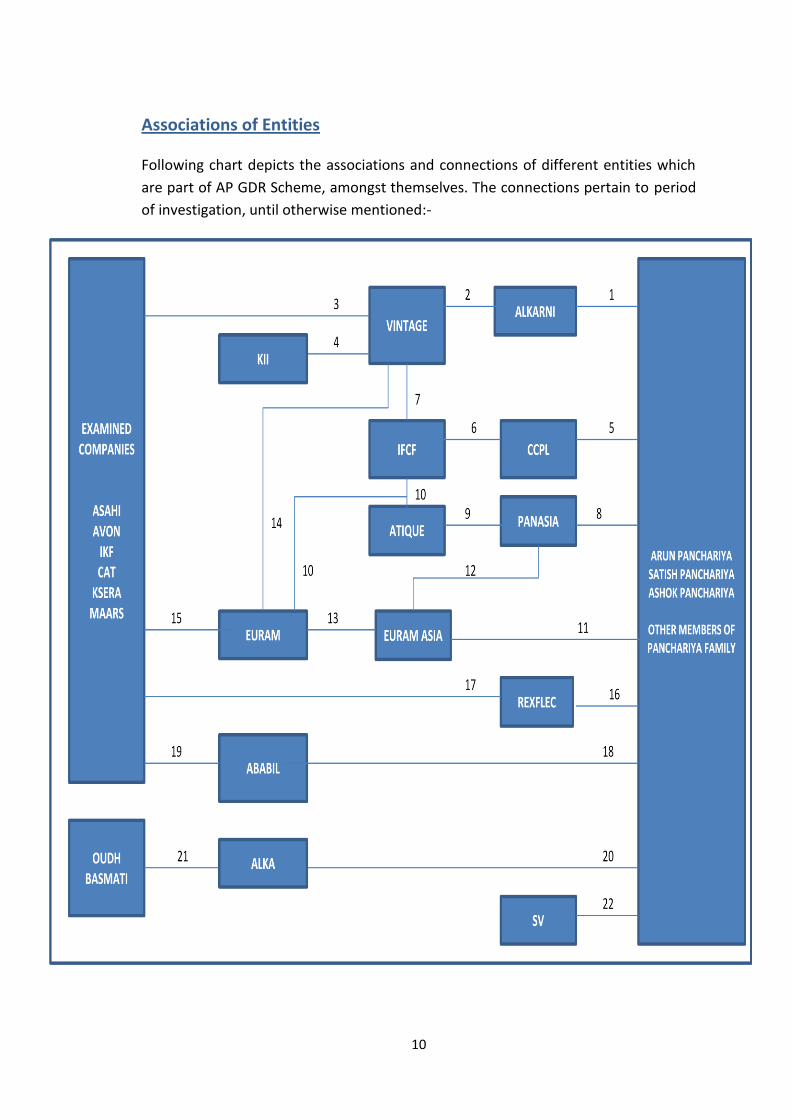

Associations of Entities

Following chart depicts the associations and connections of different entities which

are part of AP GDR Scheme, amongst themselves. The connections pertain to period

of investigation, until otherwise mentioned:-

11

1. Alkarni Holdings Ltd. (Alkarni) is a company registered in British Virgin Island with following family members of Arun Panchariya as shareholders :-

Name of Share Holder

% of shareholding

Arun Panchariya

52.50%

Radhadevi Satish Panchariya

15.00%

Sarita Arun Panchariya

15.00%

Madhudevi Ashok Panchariya

15.00%

Ashok Panchariya

2.50%

2. Vintage FZE, a company established in Jebel Ali Free Zone, Dubai on January

02, 2001. Alkarni is 100% shareholder of Vintage. The founder and director

of Vintage is AP, who also controlled its management. Subsequent to Interim

order, name of Vintage has now changed to Alta Vista International FZE.

3. Vintage is the initial investor of the GDR issues of all the Examined

Companies. By way of its holding of GDRs, Vintage was also the single largest

shareholder of the Examined Companies, after issuance of GDRs. The

association between Vintage and Examined Companies is also evident from

the fact that Examined Companies pledged their funds (GDR proceeds) to

Euram as collateral against the loan taken by Vintage.

4. Credo Investments Holding Ltd (Credo) and KII are group companies of Credo

group. Vintage signed a loan agreement with Credo, wherein it provided loan to Credo to further lend it to KII so that KII can deal in GDRs and shares of Examined Companies.

5. AP was the chief investment officer of CCPL. AP is also 100% shareholder of CCPL.

6. CCPL is 100% shareholder of IFCF. CCPL also acts as Investment manager of

IFCF. CCPL is registered as an FII with SEBI since June 20, 2011 and IFCF is

registered as its Sub-Account in India. Prior to registration of CCPL with SEBI,

Euram was the FII for IFCF.

12

7. Vintage, through Euram, is the largest investor (63.11%) in Class A shares of

IFCF 2.

8. AP is the founder and director of Panasia. He is also 100% shareholder of

Panasia.

9. Atique was also one of the major shareholders of Panasia along with AP prior to AP acquiring Atique's stake in Panasia.

10. IFCF deals in GDRs, exclusively under Class A of its investment. As per information filed by IFCF, following are the investors in Class A shares of IFCF as on September 30, 2011:-

Name of Investors % of investment

Euram Bank 63.11%

Atique Aqadi Trading LLC (Atique)

29.06%

Citco Bank 7.82%

11. Euram Asia is joint venture in Dubai, between Euram and Panasia. AP is

holding 49% in Euram Asia by way of his investment in Panasia.

12. AP and SP were also directors of Euram Asia.

13. Euram holds 51% shareholding in Euram Asia.

14. Vintage signed Loan Agreements with Euram wherein, Euram provided loan

to Vintage for the sole purpose of subscription of GDR issue of Examined Companies.

15. Examined Companies signed Pledge Agreements with Euram. According to

the Pledge Agreements, the proceeds of GDR issuance were deposited and

pledged by the companies with Euram.

16. As per the KYC documents of Rexflec, AP is the director and beneficial owner

of Rexflec.

17. Rexflec is supposedly one of the initial investors in GDR issues of CAT, K Sera

and Maars. Rexflec has the same address as that of one Seychelles based

company called Premier Management Consultancy Ltd. IKF made a payment

to Premier Management Consultancy Ltd as placement fees of GDRs. The

name of Rexflec is now changed to Pan Asia Management Ltd.

2 Class A of IFCF is exclusively investing in the GDRs of Indian companies and subsequently selling in Indian Markets.

13

18. Ababil Star General Trading (Ababil) is shown as one of the initial investors in

GDR issue of K Sera by Panasia. However, from the documents available, it is

found that GDRs were actually issued to Vintage and payments were made to

the issuer from the bank account of Vintage. From this, it is inferred that

Ababil is also connected to AP/AP related entities. Investigations revealed

that Ababil received funds from companies like Avon and Asahi. Asahi and

Avon have transferred funds to Ababil out of GDR issue proceeds.

19. Ababil transferred funds to one of the subsidiary of K Sera in Dubai.

20. Alka India Ltd., a company listed on BSE has the following family members of

AP acting as promoters:-

a) Ramswaroop Panchariya b) Ashok Panchariya c) Gopikishan Panchariya d) Geetabai M Purohit e) Satish R Panchariya f) Arun R Panchariya g) Ramswaroop B Panchariya h) Shantidevi Panchariya i) Saritadevi Panchariya j) Madhudevi Panchariya k) Radhadevi Panchariya l) Shantidevi R Panchariya m) Radhadevi S Panchariya n) Arun Ramswaroopji Panchariya o) Ramswaroopji B Panchariya p) Satish R Panchariya Mr. Satish Panchariya was appointed as the Chairman of company K Sera Sera Ltd in October 2012.

21. Alka India and Oudh were among the shareholders of Basmati. Together, they

held 37.68% of the shares of Basmati. Basmati in turn held 27.8% of the

shares of Oudh. (source: MCA website).

22. SV is the proprietary firm of Sarfaraz Khan Pathan. As per the KYC details provided by the Depository Participants of SV, one of the brothers of AP (Ashok Panchariya) is mentioned as nominee for the demat account of SV. Ashok Panchariya is also mentioned as introducer on the KYC documents for the bank accounts of Sarfaraz Khan.

14

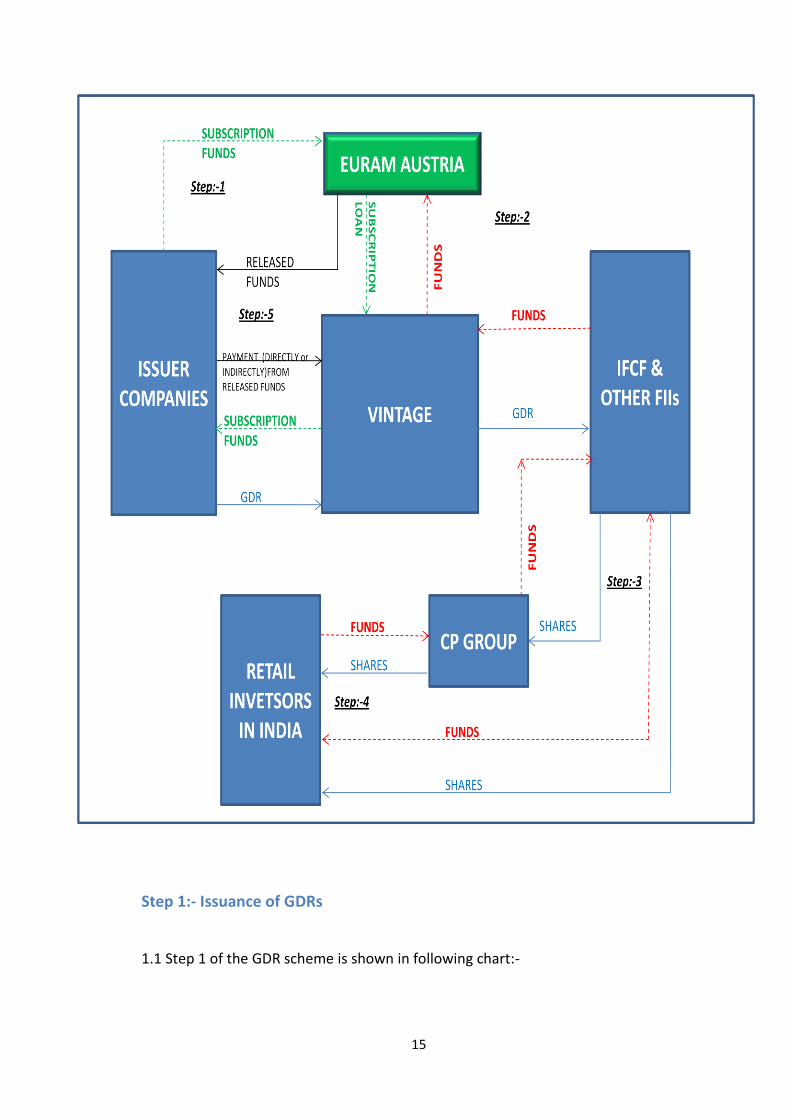

AP GDR Scheme

The following chart depicts the scheme of GDRs wherein AP arranges loans for the subscription to GDRs, subscribes to GDRs, sells the GDRs to FIIs/ Sub accounts (FIIs) who, in turn, sell shares received from conversion of GDRs in Indian securities market. A large portion of shares sold by FIIs are purchased by a set of counterparties (CP Group), who in turn, sell these shares to Indian retail investors. In addition to purchasing shares from FIIs and selling to retail investors, CP Group also creates/maintains liquidity in the scrip by trading among themselves. The GDRs thus issued and sold to Indian investors through steps explained below are hereinafter referred to as Structured GDRs and the complete scheme is referred to as GDR Scheme.

15

Step 1:- Issuance of GDRs

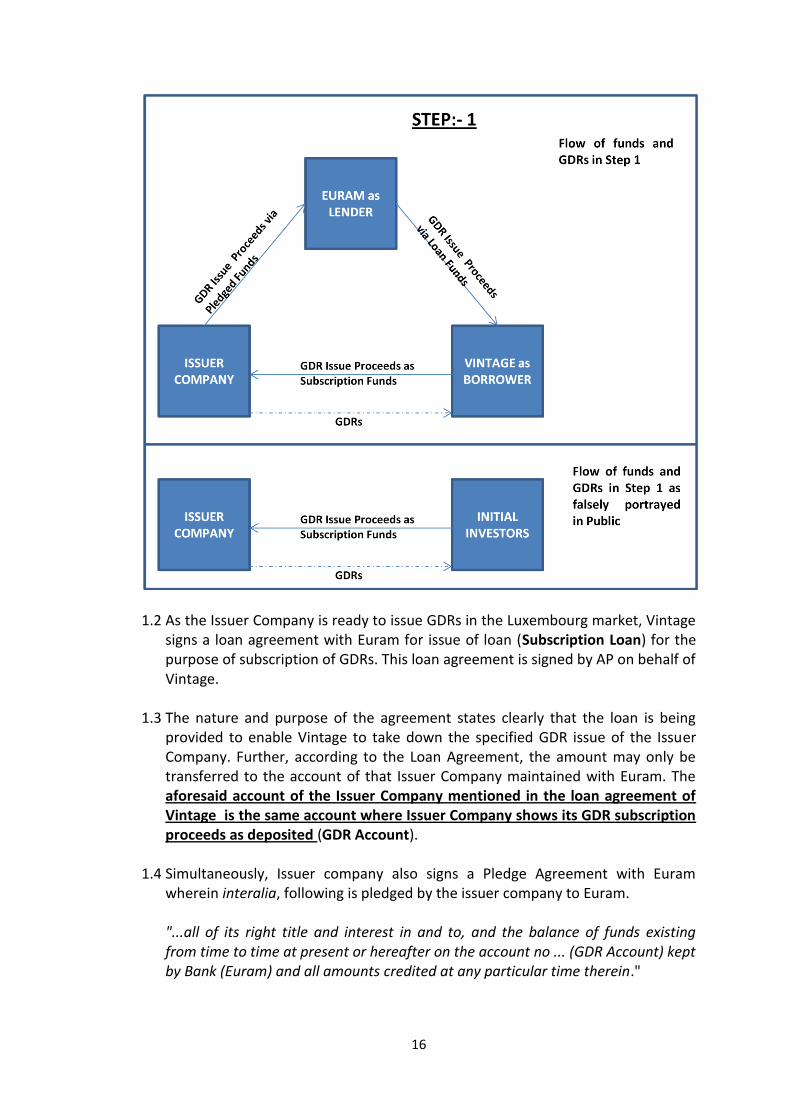

1.1 Step 1 of the GDR scheme is shown in following chart:-

16

1.2 As the Issuer Company is ready to issue GDRs in the Luxembourg market, Vintage

signs a loan agreement with Euram for issue of loan (Subscription Loan) for the purpose of subscription of GDRs. This loan agreement is signed by AP on behalf of Vintage.

1.3 The nature and purpose of the agreement states clearly that the loan is being provided to enable Vintage to take down the specified GDR issue of the Issuer Company. Further, according to the Loan Agreement, the amount may only be transferred to the account of that Issuer Company maintained with Euram. The aforesaid account of the Issuer Company mentioned in the loan agreement of Vintage is the same account where Issuer Company shows its GDR subscription proceeds as deposited (GDR Account).

1.4 Simultaneously, Issuer company also signs a Pledge Agreement with Euram wherein interalia, following is pledged by the issuer company to Euram. "...all of its right title and interest in and to, and the balance of funds existing from time to time at present or hereafter on the account no ... (GDR Account) kept by Bank (Euram) and all amounts credited at any particular time therein."

17

Further, the pledge agreement is also part of the loan agreement and vice versa. The pledge agreement in its preamble states that, "...The Pledgor (Issuer Company) has received a copy of the Loan Agreement and acknowledges and agrees to its terms and conditions."

1.5 The following is also secured as per the Loan agreement:- a. "...In order to secure all and any of the Bank's claims and entitlements against the Borrower (Vintage).......... it is hereby irrevocably agreed that the following securities and any other securities which may be required by the Bank from time to time shall be given to the Bank as provided herein or in any other form or manner as may be demanded by the Bank.....

Pledge of certain securities held from time to time in the Borrower's account no ... at the Bank as set out in a separate pledge agreement which is attached hereto as Annex which forms an integral part of this Loan Agreement.

Pledge of the GDR Account of the Borrower held with the Bank as set out in a separate pledge agreement which is attached hereto as Annex and which forms an integral part of this Loan Agreement.

The GDR account referenced above is the same account wherein the issuer company has deposited the subscription proceeds of the GDR issue. From the above, it is observed that the GDR Account is held in the name of the issuer company while, for all intents and purposes, the actual control of said account ultimately vests with Vintage (effectively AP), as the account is kept as collateral for the loan availed by Vintage.

1.6 As a result of the Loan Agreement and the Pledge Agreement, the Subscription Loan provided to Vintage by Euram is used to acquire the GDRs of Issuer Company by Vintage. This Subscription Loan is thus deposited as Subscription fund in the GDR Account of Issuer Company which is pledged by the Issuer Company with Euram as security against the Loan provided to Vintage.

1.7 The Issuer company then issues GDRs to Initial investors through ODB. In the cases investigated by SEBI, it is observed that the GDRs were transferred not to the account of initial investors but to the security account of Vintage maintained with Euram. The issuer companies and Panasia have provided a list of initial investors to whom GDRs were issued. However, as per documents available with SEBI, it is observed that GDRs have been credited to the securities account of Vintage held with Euram on the day of GDR issuance and a payment for GDRs is made from the Euram Account of Vintage to the GDR Account of Issuer Company. From the foregoing it is clear that the GDRs were directly issued to Vintage. The list of initial investors of GDRs provided to SEBI by the issuer companies, therefore is a list designed to camouflage the name of the actual investor i.e. Vintage and mislead the shareholders of the company and the market.

18

1.8 Effectively, there is no real movement of funds involved from Step 1.1 to 1.7. By

way of entries in the books of Euram, funds are released from loan account of Vintage to GDR account of issuer company and are kept as collateral with Euram. Thus, without any actual inflow of funds into the company, the issuer Company is successful in issuing large amount of GDRs which gives a respectable appearance to the financial statement of the company, which is misleading. In reality, few book entries result in large surge in the capital of the company. Thus, these GDRs are created without any purchase transactions or for any cost (apart from interest and commission earned by Euram).

1.9 The initial investors to the GDRs appear to be just fictitious/front entities created by AP and Panasia. Efforts to contact these original investors were futile. Emails sent have bounced back. Letters sent to these investors have also returned undelivered. SEBI also sought help of regulators of respective jurisdiction where these investors have been stated to be based. Foreign regulators have been unable to locate these investors.

1.10 Following are the details of the GDRs issued by the companies examined by SEBI.

Sr. No Issuer

Date of GDR Issue

Pre GDR equity (‘000)

Shares issued under GDR

(‘000)

% GDR to Pre GDR

equity

Market Cap prior to GDR

issue( Rs Crore)

Capital raised by

GDR Issue(Rs.

Crore)

% Capital raised to pre GDR Market

Cap

1 IKF 31-03-07 1,06,690 1,32,000 123 79.60 47.96 60.25

2 CAT 27-07-07 5,750 25,286 440 3.00 26.13 871.20

3 Maars 10-08-07 66,160 73,800 112 29.71 72.93 265.02

4 K Sera 26-10-07 19,513 47,619 244 71.02 98.42 138.58

6 Asahi 29-04-09 37,196 2,99,100 804 2.64 32.99 1137.94

7 IKF 15-05-09 2,68,190 1,62,391 61 79.66 54.44 68.35

8 Avon 19-06-09 16,580 48,000 289 14.71 48.13 327.19

9 K Sera 16-10-09 67,131 1,34,257 200 137.95 138.73 100.57

10 CAT 06-11-09 31,576 47,860 152 50.81 46.83 92.17

1.11 From the above table, it is clear that the amount of capital raised via issuing GDRs

is significantly large when compared to existing capital of the companies.

1.12 For the purpose of subscription of the GDRs of the aforementioned Examined Companies, loan agreements were signed by various entities with the banks. This loan was then utilised for subscribing to the GDRs of the Examined Companies, as detailed in Para 1.1 to 1.7 and summarised in Para 1.8.

1.13 Following are the details of loan agreements signed for the purpose of

subscription of GDRs of Examined Companies.

19

Sr. No.

Issuer

Date of GDR Issue

GDR Issue Size

($ '000)

Borrower Loan Amount ($ '000)

Date of Loan

Agreement

Lender Date of Pledge

Agreement

1 IKF 31-03-07 11,000 Seazun 14,000 27-03-07 Banco 27-03-07

2 CAT 27-07-07 6,457 Vintage 6,457 23-07-07 Euram 20-07-07

3 Maars 10-08-07 17,933 Vintage 17,933 27-07-07 Euram 27-07-07

4 K Sera 26-10-07 25,000 Vintage 25,000 30-10-07 Euram 30-10-07

6 Asahi 29-04-09 5,982 Vintage 5,982 21-04-09 Euram 21-04-09

7 IKF 15-05-09 10,988 Vintage 10,988 28-04-09 Euram 28-04-09

8 Avon 19-06-09 10,000 Vintage 10,000 10-06-09 Euram 10-06-09

9 K Sera 16-10-09 29,984 Vintage 29,984 06-10-09 Euram 06-10-09

10 CAT 06-11-09 10,003 Vintage 10,003 27-10-09 Euram 27-10-09

Step 2:- Cancellation of GDRs

2.1 The GDRs created at the end of Step 1 were transferred to the account of Vintage held with Euram. Subsequently, Vintage through over the counter transactions, sold the GDRs to FIIs such as IFCF, KII etc or other FIIs which had an agreement with AP for the purpose of purchasing GDRs. The GDRs were then converted into underlying shares and these shares were sold in the Indian market.

2.2 Euram Bank informed SEBI vide letter dated March 27, 2012 that their investment in IFCF is on behalf of Vintage. Similarly, Atique is also connected with AP. Thus 92.17% of Class A shares of IFCF was held by entities with established connection with AP and all the dealings of IFCF in the GDRs of Examined Companies were under control of AP.

2.3 Arrangements between Credo, KII and Vintage for dealing in GDRs of Examined Companies have been observed. Vintage signed a loan agreement with Credo, wherein it provided loan to Credo to further lend it to KII so that KII can purchase GDRs of Examined Companies and convert into shares to sell in Indian Markets. The market risk of these transactions was borne by Vintage. Thus, the dealings of KII in the GDRs of Examined Companies were also under control of AP.

2.4 It is observed that IFCF and KII started dealing in the GDRs of Examined Companies from June 2009 and after that no other FII/Sub-Account has cancelled GDRs of Examined Companies except KII and IFCF. Following table provides details of cancellation of GDRs of Examined Companies done by KII and IFCF as on June 30, 2012.

20

GDR Issue Date

Total GDRs Issued

Total GDRs Cancelled till June 30, 2012

GDRs cancelled between June 01, 2009 to June 30, 2012

GDRs cancelled by IFCF

GDRs cancelled by KII

% of GDRs cancelled by IFCF & KII to total GDRs cancelled

% of GDRs cancelled by IFCF & KII to total GDRs cancelled between June 01, 2009 to June 30, 2012

Asahi 29-04-09 29,91,000 15,14,450 15,14,450 13,81,000 1,00,000 97.8 97.8

Avon 19-06-09 16,00,000 16,00,000 16,00,000 14,44,000 1,56,000 100.0 100.0

CAT 27-07-07 43,04,348 25,80,000 1,95,000 1,20,000 75,000 7.6 100.0

CAT 06-11-09 15,95,333 13,685 13,685 13,685 0 100.0 100.0

IKF 31-03-07 1,10,00,000 1,10,00,000 0 0 0 0.0 0.0

IKF 15-05-09 54,13,048 10,34,000 10,34,000 9,89,000 45,000 100.0 100.0

K Sera 26-10-07 47,61,900 47,61,900 33,41,900 13,96,757 19,45,143 70.2 100.0

K Sera 16-10-09 44,75,238 12,35,500 12,35,500 7,58,500 4,77,000 100.0 100.0

Maars 10-08-07 73,80,000 57,92,800 15,77,800 11,27,800 4,50,000 27.2 100.0

From the above table, it is clear that from June 01, 2009, the activity of cancelling

GDRs and converting to shares was done entirely under direct control of AP.

2.5 To summarise, the funds for the purchase of GDRs are provided by AP to FIIs, either by direct investment in the fund like IFCF or by entering into contractual agreement and providing loan to FIIs/Sub-Accounts (e.g. KII , etc). In reality, funds have only moved from one AP controlled company (IFCF) to another AP controlled company (Vintage) and vice versa.

Step 3:-Sale of Shares to group of Indian clients and utilisation of GDR issue

proceeds by Examined Companies.

3.1 The step 3 of the GDR scheme involves selling of shares (received post conversion

of GDRs of Examined Companies) on Indian stock exchanges by FIIs. It has been observed that the shares sold by FIIs are purchased in large quantities by certain set of Indian clients (CP Group) . These Indian clients then sell these shares purchased from FIIs to other retail investors. It has also been observed that the members of the CP Group traded in large quantities among themselves which increased the liquidity of the scrip of Examined Companies. SEBI in its interim Order dated September 21, 2011 identified one such group of clients which had connections with AP and made following observations in Para 5 on Page 3 of the aforesaid order:-

The average daily volume has increased significantly on the days when the entities, Sub-Accounts

and Group, have been observed to be trading in the scrip. In the case of Asahi it is nearly 26 times

the days when these entities have not trade , indicating the major role these entities have played

in creating liquidity in the scrip.

21

On days when Sub-Accounts have sold the shares their concentration is ranging from 18% to 53%

of day’s net volume. On such days, the volume has increased from 7 times (Cat) to 74 times

(Maars) than compared to when Sub-Accounts are not trading. Thus the selling of the Sub-Account

is expected to have a huge downward pressure on the price of the scrip.

During the days the Group has traded its total trading is nearly 1/3rd

of the total trading in the

scrip on a gross basis.

3.2 Following chart explains the manner in which the shares received from

cancellation of GDRs are ultimately sold to Indian retail investors:-

3.3 The next step in the GDR scheme involves the CP Group selling shares to the Indian retail investors with a view to generate profit. Uptil now, each transaction has been controlled by AP or SP. In this last step, since the shares are being sold to the retail investors, the price paid by such investors goes to the sellers (CP Group or FIIs) and thereby to AP, as the CP Group, FIIs and AP are related/connected with each other. Thus, it is the Indian Investors, and not the foreign investors, who have ultimately paid for the GDRs.

3.4 As the investigations conducted by SEBI revealed that the GDR issue of Examined Companies were not a capital raising exercise as it was portrayed by these companies and Lead Manager, SEBI investigated the utilisation of GDR issue proceeds by the Examined Companies.

3.5 Investigations have revealed that all the Examined Companies have utilised majority of the GDR issue proceeds through their foreign subsidiaries in other countries. Majority of these foreign subsidiaries have following common aspects:-

3.5.1. Most of these are based in free zones of U.A.E. 3.5.2. In almost all the case, the major portion of the GDR issue (100% in one of

the case viz, CAT) is directly transferred to foreign subsidiary and is not repatriated to India.

3.5.3. Mostly, these have been incorporated during or after the period of GDR issue.

3.5.4. These are mostly trading companies generally dealing in commodities/ products unrelated to the business of parent company.

22

3.5.5. They have financial transactions with Vintage, Initial investors of GDR issues of other companies and foreign subsidiaries of other companies which have issued GDRs managed by AP and Panasia.

3.6 None of the Examined Companies have provided SEBI with adequate explanation

of the transfer of funds to their foreign subsidiaries. Due to the non cooperation by companies, many aspects like bank accounts, financial transactions, nature of business and dealings with AP connected entities of foreign subsidiaries of Issuer companies could not be investigated in detail by SEBI. However, from the limited documents and material available with SEBI, it is revealed that foreign subsidiaries are being used to make payments to AP/AP related entities. The rationale for such transaction has not been explained to SEBI. However, in light of the findings of the investigation indicating that AP/AP related entities have colluded with the companies to issue GDRs fraudulently, it is probable that the financial transaction between the foreign subsidiary and AP/AP related entities could possibly be a route for the issuer company to compensate AP for services rendered by him.

23

Detailed Investigation of Issuer Companies

(I) ASAHI INFRASTRUCTURE AND POJECTS LTD.

Summary of GDR issue:-

1. The GDR Issue of Asahi for US $ 5.98 Million closed on April 29, 2009 and was

fully subscribed. The allotment of 29,91,000 GDRs representing 299,100,000 equity shares of Rs 1/- each at USD 2.00 by the company was done on April 29, 2009.

2. Panasia was appointed as the LM to the GDR issue by the company.

3. Asahi consolidated equity shares on November 04, 2010 from 10 equity

shares of Rs. 1 each to 1 equity shares of Rs. 10 each. For ease of understanding, each share of Asahi transacted post consolidation of shares has been treated as 10 shares of face value Rs. 1.00 in our calculation in this report.

4. Prior to GDR issue, Asahi had 37,196,000 fully paid equity shares. Therefore, the equity shares represented by the GDRs were approximately 804.03% of Asahi's outstanding share capital at the time of GDR issue.

5. The total capital raised by Asahi vide GDRs was USD 5,982,000 which is equal to Rs. 30,04,16,040 considering conversion price of USD 1 = Rs. 50.22 as on April 29, 2009. The market cap of Asahi prior to GDR issue was Rs. 2,64,00,000. Therefore, the capital raised by GDR issue was 1137.94% of the market capital of the company prior to GDR issue.

6. The last traded price of Asahi on BSE on April 29, 2009 was Rs. 0.74. The highest and lowest price of Asahi for period of three months from January 29, 2009 to April 29, 2009 was Rs. 0.89 and Rs. 0.53 respectively. The price which subscribers paid for each share underlying GDRs was Rs. 1.04 (USD 1 = Rs. 50.22 as on April 29, 2009) which was 140.54% of the price of the scrip on same day.

Subscribers of GDR Issue:-

7. Following are the details of investors in the GDR issue of Asahi, as per the

submissions of the company:-

24

Name of Subscriber GDRs Subscribed

Amount Paid (USD)

% of total GDR issue

Greenwich Management Inc (Greenwich)

14,91,000 29,82,000 49.85

Tradetec Corporation (Tradetec) 15,00,000 30,00,000 50.15

8. Greenwich and Tradetec were observed to be investors in several other GDR

issues of Indian companies. The address of these subscribers, which was made available to SEBI, is given below.

Name Address

Greenwich Floor - 18, One International Finance Centre, 1 Harbour view Street, Central, Hong Kong

Tradetec Level 47, Prudential Tower, 30 Cecil Street, Singapore - 049712 Email : [email protected]

9. In order to contact these initial investors emails were sent to available email

addresses of these entities and summons were issued to the contact address made available to SEBI. All the emails and summons issued to these investors returned back undelivered. The respective securities market regulator of the countries where these investors are located were requested contact these investors. However, the regulators have informed SEBI that the addresses of the investors are either non-existent or do not belong to these entities.

Loan & Pledge Agreement signed among Asahi, Vintage & Euram.

10. From the documents available with SEBI, it is observed that the issuance and

subscription of GDRs of Asahi was done using loan taken from Euram. The GDR issue of Asahi was managed and structured by AP with the Loan and Pledge Agreement signed among Asahi, Vintage and Euram, which is the key to the fraudulent issuance and subscription of GDRs in this case.

11. A loan agreement (Loan Agreement : K210409-003) dated April 21, 2009, was signed between Euram and Vintage on April 22, 2009. The agreement was signed by AP as Managing Director on behalf of Vintage on April 22, 2009.

12. The Loan agreement states that Euram has agreed to make available a loan of USD 59,82,000.00 to Vintage (referred to as ''the Borrower''). The nature and purpose of the loan facility is to provide funding enabling Vintage to take down GDR issue of Asahi's Luxemburg public offering and may only be transferred to Euram account no: 540030.

25

13. The Euram account no: 540030 is the bank account of Asahi maintained with Euram for the purpose of depositing proceeds of GDR issue.

14. As security against the Loan provided to Vintage following is stated in the Loan Agreement. "6.1 In order to secure all and any of the Bank's claims and entitlements against the Borrower, arising now or in the future out of or in connection with the Loan or any other obligation or liability of the Borrower to the Bank, including without limitation other loans granted in the future , it is hereby irrevocably agreed that the following securities and any other securities which may be required by the Bank from time to time shall be given to the Bank as provided herein or in any other form or manner as may be demanded by the Bank

Pledge of certain securities held from time to time in the Borrower's account no. 540 030 at the Bank as set out in a separate pledge agreement which is attached hereto as Annex 2 and which forms an integral part of this Loan Agreement.

Pledge of the account no. 540 030 of the Borrower held with the Bank as set out in a separate pledge agreement which is attached hereto as Annex 2 and which forms an integral part of this Loan Agreement."

15. A Pledge Agreement dated April 21, 2009 was signed between Asahi and

Euram. The agreement was signed by Mr. Laxminarayan Rathi on April 28, 2009, on behalf of Asahi as Managing Director of Asahi. He and his other family members are also promoters of Asahi.

16. Mr. Laxminarayan Rathi did not inform Bombay Stock Exchange or shareholders or of the company about signing the Pledge Agreement.

17. According to the Pledge Agreement, Asahi has been referred to as "Pledgor'' while Euram has been referred to as ''Bank''.

18. The preamble of the Pledge Agreement states

"By loan agreement K210409-003 (hereinafter referred to as ''Loan Agreement'') dated April 21, 2009, the Bank granted a loan (hereinafter referred to as the ''Loan'') to Vintage FZE, AAH-213, Al Ahmadi House, Jebel Ali Free Trade Zone, Jebel Ali, Dubai, United Arab Emirates (''the Borrower") in the amount of $ USD 5,982,000.00 million3. The Pledgor has received a copy of the Loan Agreement and acknowledges and agrees to its terms and conditions."

19. From the above preamble of Pledge Agreement, it is clear that Mr. Laxminarayan Rathi and Asahi were also the party to the Loan Agreement.

20. The pledge created in the Pledge Agreement is stated below:-

3 It appears that 'million' has been wrongly inserted in the Loan agreement. The loan amount was only

USD 5,982,000.00.

26

" 2. Pledge

2.1 In order to secure any and all obligations, Present and future, whether conditional or unconditional of the Borrower towards the bank under the Loan Agreement and any and all respective amendments thereto and for any and all other current or future claims which the Bank may have against the Borrower in connection with the Loan Agreement – including those limited as to condition or time or not yet due – irrespective of whether such claims have originated from the account relationship, from bills of exchange, guarantees and liabilities assumed by the Borrower or by the Bank, or have otherwise resulted from business relations, or have been assigned in connection therewith to the Bank (“the Obligations”) the Pledgor hereby pledges to the Bank the following assets as collateral to the Bank:

2.1.1 all of its rights, title and interest in and to the securities deposited from time to

time at present or hereafter (hereinafter referred to as the “Pledged Securities”) and

the balance of funds up to the amount of $ USD 5,982,000.00 existing from time to

time at present or hereafter on the securities account(s) no. 540 030 held with the

Bank (hereinafter referred to as the “Pledged Securities Account”) and all amounts

credited at any particular time therein.

2.1.2 all of its right, title and interest in and to, and the balance of funds existing from time to time at present or hereafter on the account(s) no. 540 030 kept by the Bank (hereinafter referred to as the “Pledged Time Deposit Account “) and all amounts credited at any particular time therein.

(the Pledged securities account and the Pledged Time Deposit account hereinafter referred to as the “Pledged Accounts”, the Pledged Securities and the Pledged Accounts hereinafter collectively referred to as “Collateral”)

2.2 The Pledgor agrees to deposit with the Bank all dividends, interest and other payments, distributions of cash or other property resulting from the Pledged Securities and funds."

21. Further, following condition have been put in the Pledge agreement for the realization of the pledge.

6. Realization of the Pledge

6.1 In the case that the Borrower fails to make payment on any due amount, or default in accordance with the Loan Agreement, The Pledgor herewith grants its express consent and the Bank is entitled to apply the funds in the Pledged Accounts to settle the Obligations. In such case the Bank shall transfer the funds on the Pledged Accounts, even repeatedly, to an account specified by the Bank

6.2 Notwithstanding the foregoing, in the case that the Borrower fails to make payment on any due amount, or defaults in providing or increasing security, the Pledgor herewith grants its express consent and the Bank is entitled to realize the

27

Pledged Securities (i) at a public auction for those items of Pledged Securities for which no market price is quoted or which are not listed on a recognized stock exchange or (ii) in a private sale pursuant to the provisions of Section 376 Austrian Commercial Code unless the Bank decides to exercise its rights through court proceedings. The Pledgor and the Bank agree to Realize those items of the Pledged Securities for which a market price is quoted or which are listed on a stock exchange through sale by a Broker Publicly authorized for such transactions, selected by the Bank.

6.3 The Bank may realize the Pledge rather than accepting payments from the Borrower after maturity of the claim if the Bank has reason to believe that the Borrower’s payments may be contestable.

22. As the account no. 540030 is the account which Asahi has maintained with Euram to keep the proceeds of GDRs, it is clear that Asahi has pledged money received through issuance of GDRs to secure rights of Euram against the loan given by Euram to Vintage for subscription of GDR issue (as mentioned in Loan agreement of Vintage). This account (540030) is also referred to as borrowers (Vintage) account in the Loan Agreement. This common ownership of a bank account that belongs to both the borrower/subscriber and the Issuer Company in which the GDR proceeds are received added to a guarantee by Issuer Company for the loan taken by subscriber to its GDRs, are the central and determining features of this scheme to fraudulently raise capital by the Issuer Company

23. The fraudulent transformation of loan into GDR subscription in the name of different subscribers occur through the scheme between AP/Vintage and Asahi wherein the latter supports the former through pledging of GDR proceeds.

24. On June 01, 2009, Asahi informed BSE that the Company had allotted 29,91,00,000 equity shares of Rs 1/- each underlying 29,91,000 GDRs available for conversion, to the foreign entities namely, Greenwich and Tradetec. Subsequently, this information was made public to retail investors on BSE website. It is now clear from the investigation conducted that the said public announcement by Asahi was done to mislead retail investors in believing that the GDRs were subscribed by genuine foreign investors, whereas in reality, GDRs were subscribed by Vintage in connivance with Asahi and the proceeds simultaneously pledged with the Euram.

Acquisition, Cancellation and Sale of GDRs:-

25. After the issuance of GDRs, Vintage became the sole holder of the GDRs

issued, thereby becoming the majority share holder of Asahi. As on April 29, 2009, Vintage held 29,91,000 GDRs of Asahi, which made Vintage 88.94% shareholder of the company.

28

26. These GDRs were then transferred to IFCF and KII through over the counter

transactions. Following table gives the details of transfer of GDRs from account of Vintage (maintained with Euram) to that of IFCF and KII.

Date of Transaction

Name of Acquirer

Name of Seller

Quantity of GDRs acquired

Value of GDR Acquired ($)

Trading Platform

Value per GDR ($)

17-08-09 IFCF Euram 4 44,000 1,10,000 OTC 2.50

24-08-09 IFCF Euram 1,11,000 2,38,650 OTC 2.15

16-11-09 KII Euram 35,000 63,504 OTC 1.81

03-12-09 IFCF Euram 50,000 94,500 OTC 1.89

17-12-09 IFCF Euram 76,000 1,49,720 OTC 1.97

21-01-10 KII Euram 65,000 1,20,557 OTC 1.85

02-02-10 IFCF Euram 1,50,000 2,77,500 OTC 1.85

09-05-10 IFCF Euram 1,00,000 3,02,000 OTC 3.02

13-08-10 IFCF Euram 2,00,000 4,10,000 OTC 2.05

05-10-10 IFCF Euram 50,000 91,000 OTC 1.82

12-10-10 IFCF Euram 50,000 96,500 OTC 1.93

21-10-10 IFCF Euram 50,000 93,000 OTC 1.86

27-10-10 IFCF Euram 1,00,000 1,85,000 OTC 1.85

06-11-10 IFCF Euram 1,00,000 1,86,000 OTC 1.86

09-03-11 IFCF Euram 50,000 1,12,153 OTC 2.24

10-03-11 IFCF Euram 1,00,000 2,23,152 OTC 2.23

26-04-11 IFCF Euram 1,50,000 3,03,000 OTC 2.02

15-06-11 IFCF Euram 1,70,000 2,32,900 OTC 1.37

Total 16,51,000 32,89,136 1.99

27. Both IFCF and KII are connected to AP as Credo was found to be having an

agreement with Vintage for dealing in the GDRs of Asahi.

28. Credo, an associate company of KII was found to have an agreement with Vintage. According to this agreement, Vintage provided a Loan of USD 20,00,000.00 to Credo to further lend it to KII, to enable KII to purchase securities of several Indian companies including those of Asahi, either in India or overseas market. As per the agreement, KII got GDRs converted into underlying shares and sold the resultant shares in the Indian Markets. The sale proceeds were then to be used to purchase further securities to repeat the said process until KII decided to terminate the agreement.

29. Credo was paid a definite amount as commission by Vintage for providing service of dealing in the securities of Indian companies. The agreement also ensured that Vintage take full liability of the dealings of KII in the GDRs of

4 Euram has informed SEBI that all the transactions executed by Euram in GDRs of Indian companies

are on behalf of Vintage.

29

Indian companies and any loss incurred by KII to be borne by Vintage only. The agreement was signed by AP on behalf of Vintage.

30. The cancellation of the GDRs of Asahi started from August 19, 2009 till June 14, 2011. Following are the details of cancellation requests completed till June 30, 2012.

Transaction Date Entities cancelling GDRs on

behalf of FIIs/Sub-Accounts GDRs

Cancelled Shares Released

19-08-2009 Euram 44,000 44,00,000

25-08-2009 Euram 1,11,000 1,11,00,000

23-11-2009 J.P. Morgan Clearing Corp. 35,000 35,00,000

04-12-2009 Euram 50,000 50,00,000

18-12-2009 Euram 76,000 76,00,000

27-01-2010 Jefferies & Co, Inc 65,000 65,00,000

02-02-2010 Euram 1,50,000 1,50,00,000

09-08-2010 Euram 30,000 30,00,000

11-08-2010 Euram 20,000 20,00,000

12-08-2010 Euram 50,000 50,00,000

24-08-2010 Euram 20,000 20,00,000

09-09-2010 Euram 50,000 50,00,000

20-09-2010 Euram 25,000 25,00,000

22-09-2010 Euram 35,000 35,00,000

05-10-2010 Euram 50,000 50,00,000

01-03-2011 Euram 1,00,000 1,00,00,000

20-04-2011 SIX SIS AG 33,450 33,45,000

26-04-2011 Euram 65,000 65,00,000

31-05-2011 Euram 1,45,000 1,45,00,000

03-06-2011 Euram 1,45,000 1,45,00,000

07-06-2011 Euram 74,500 74,50,000

14-06-2011 Euram 1,40,500 1,40,50,000

Total 15,14,450 15,14,45,000

31. The shares were released and credited to the demat accounts of IFCF and KII as detailed below.

Date of receiving shares

Name of entity receiving shares from GDR cancellation

No. of shares received

20-08-2009 INDIA FOCUS CARDINAL FUND 44,00,000

26-08-2009 INDIA FOCUS CARDINAL FUND 1,11,00,000

25-11-2009 KII LTD 35,00,000

07-12-2009 INDIA FOCUS CARDINAL FUND 50,00,000

21-12-2009 INDIA FOCUS CARDINAL FUND 76,00,000

28-01-2010 KII LTD 65,00,000

30

Date of receiving shares

Name of entity receiving shares from GDR cancellation

No. of shares received

03-02-2010 INDIA FOCUS CARDINAL FUND 1,50,00,000

10-08-2010 INDIA FOCUS CARDINAL FUND 30,00,000

12-08-2010 INDIA FOCUS CARDINAL FUND 20,00,000

13-08-2010 INDIA FOCUS CARDINAL FUND 50,00,000

25-08-2010 INDIA FOCUS CARDINAL FUND 20,00,000

13-09-2010 INDIA FOCUS CARDINAL FUND 50,00,000

21-09-2010 INDIA FOCUS CARDINAL FUND 25,00,000

23-09-2010 INDIA FOCUS CARDINAL FUND 35,00,000

06-10-2010 INDIA FOCUS CARDINAL FUND 50,00,000

07-03-2011 INDIA FOCUS CARDINAL FUND 1,00,00,000

27-04-2011 INDIA FOCUS CARDINAL FUND 65,00,000

27-04-2011 BANK SARASIN AND CO. LTD 33,45,000

01-06-2011 INDIA FOCUS CARDINAL FUND 1,45,00,000

06-06-2011 INDIA FOCUS CARDINAL FUND 1,45,00,000

08-06-2011 INDIA FOCUS CARDINAL FUND 74,50,000

15-06-2011 INDIA FOCUS CARDINAL FUND 1,40,50,000

Total 15,14,45,000

32. 14,81,000 GDRs (49.51% of total 29,91,000 GDRs issued) were cancelled by IFCF and KII during the period August 20, 2009 to June 15, 2011, of which 13,81,000 GDRs were cancelled by IFCF.

33. The following chart depicts the complete process of acquisition of GDRs by IFCF and KII from Vintage and cancellation and conversion of these GDRs into underlying shares.

31

34. The underlying shares received by IFCF and KII were sold in the Indian Markets.

35. The details of the counterparties to these sales during the period January 01, 2009 to September 21, 2011 are given below:-

FII CP PAN CP NAME Sell Volume Sell Value (Rs.) % of Total

sale by IFCF

IFCF AACCI3088H INDRAVARUN TRADE IMPEX PVT LTD (INDRAVARUN) 65,99,900 3,39,36,012

28.53

IFCF AAACB4324K BASMATI 1,90,52,069 2,80,81,895 23.60

IFCF ACRPP5552H SV 34,11,300 35,02,024 2.94

Others 3,54,18,377 5,34,47,388 44.93

Total sale by IFCF 6,44,81,646 11,89,67,319 100.00

FII CP PAN CP NAME Sell Volume Sell Value (Rs.) % of Total sale by KII

KII ACRPP5552H SV 20,00,000 20,00,000 57.14

KII AAACB4324K BASMATI 7,50,755 7,50,755 21.45

Others 7,49,245 7,49,245 7.09

Total Sale by KII 35,00,000 35,00,000 100.00

36. Considering the consolidation of shares by Asahi on November 04, 2010, IFCF sold 12,39,71,646 shares of Asahi for Rs. 11,89,67,319, out of 13,81,00,000 shares received by it post cancellation of GDRs.

Utilisation of GDR proceeds by Asahi:-

37. The proceeds of GDR issue received by Asahi were also analyzed to

determine the manner in which the company has utilized the funds. Documents were sought from Asahi in support of the utilisation of the GDR proceeds. Most of the information and documents submitted by Asahi are inconsistent with the statements made by Asahi to SEBI or with statements available in public domain. Details of the same are provided in following paragraphs

38. Summons were issued to Asahi seeking details regarding utilisation of GDR proceeds by the company. The information and documents sought in the summons are detailed below:-

38.1. Details of usage of proceeds of the GDR Issues by Asahi, along with the documentary proof in support of the utilization of the funds.

38.2. Copies of bank account statements of Asahi maintained with Euram Bank.

38.3. Copies of bank account statements of Asahi in India highlighting transactions related to repatriation of GDR proceeds.

32

38.4. Chronology of events leading to the issue of GDRs along with a certified true copy of the resolution passed by Board of Directors.

38.5. Rationale for the appointment of Panasia as LM for GDR issue of Asahi.

38.6. Copies of all the agreements between Asahi and Panasia 38.7. Copies of agreements with Euram. 38.8. Details of the conditions that were laid upon Asahi for the

withdrawal of GDR proceeds from bank accounts maintained with Euram.

38.9. Copy of any other agreement that Asahi had with Euram apart from those related to GDR issues.

38.10. Details of any agreement of Asahi regarding financing for the purpose of subscription by initial investors of GDRs.

38.11. Copies of agreements that Asahi had with Vintage and AP. 38.12. Details of nature of business of the subsidiary of Asahi in U.A.E

viz, Asahi Infrastructure & Projects Ltd FZE (Asahi FZE). 38.13. Copies of Bank Account Statements of Asahi FZE. 38.14. Details of payments made to Panasia or companies associated

with Panasia. 38.15. Name of the directors and promoters of Asahi at the time of

issue of GDRs. 38.16. Details of money paid by Asahi FZE, be it on account of

purchases or expenses or loan, to other entities for more than USD 25,000 from incorporation. Asahi was specifically asked to provide details like name of entities to which payments were done, purpose of payments and amount paid by Asahi FZE.

38.17. Audit Report of Asahi FZE along with financial statements for the year ending March 2010 and March 2011.

38.18. Detail of remittance of USD 60,798 done to Pan Asia Management by Asahi on July 15, 2010.

38.19. Contact details, Nature of business and Bank Account statements of Asahi FZE

39. Summons dated March 28, 2012 was issued to Managing Director of Asahi to appear in person on April 16, 2012 before Investigating Authority at SEBI head office. On April 16, 2012, Mr. Ravi Ramaiya, Practicing Chartered Accountant appeared on behalf of Asahi with authorisation letter signed by Mr. Laxminarayan Rathi, MD of Asahi and the representative's statement was recorded before Investigating Authority.

40. From the perusal of the documents submitted in response to the summons and statement given by the representative of Asahi, following are observed:-

40.1. Asahi submitted the details of utilisation of GDR proceeds. Summary of the same is given below:-

33

Utilisation Amount (in Rs. crore)

Transferred to Asahi FZE 20.96

GDR Expense. 1.369

Utilised in India 5.886

Dividend Payment 1.7

Total Capital Raised 29.91

40.2. Rs. 20.96 crore out of total issue size of Rs. 29.91 crore i.e. around 70% was transferred by Asahi to its subsidiary in Dubai Asahi FZE.

40.3. It was submitted by Asahi that Rs. 20.96 crore was transferred to Asahi FZE for trading purpose. Asahi FZE received and paid money for trading in cement, aluminium, iron, construction and so on.

40.4. The account statement of Asahi FZE reflected transactions with K Sera Sera Production FC LLC (Asahi FZE received USD 19,97,955 ), Ababil Star General Trading (Ababil)5 , CAT Technologies, Vintage etc.

40.5. Asahi FZE had transactions with companies like Beckons Industries Ltd, Cybermate Infotek and CAT that have issued GDRs with Panasia as LM. Asahi has not been able to explain the rationale behind such financial transactions with these companies.

40.6. According to submissions by Asahi, Asahi FZE paid USD 20,73,000 to Vintage and USD 600,000 to Ababil from its Dubai Bank accounts. However, Asahi was unable to provide an explanation for these transactions.

41. On adding USD 26,73,000 transferred to Vintage and Ababil by Asahi FZE to

the funds which Vintage received by selling the GDRs (USD 32,89,136) to FIIs, the total amount comes to be USD 59,62,136, which is around 99.66% of total loan taken by Vintage from Euram for subscribing to GDR issue of Asahi.

42. Out of Rs. 20.96 crore (approx USD 4.7 million) transferred to Asahi FZE, USD 2.67 million was transferred back to AP Entities like Vintage and Ababil. Thus Asahi transferred 44.68% of the GDR issue proceeds back to AP entities which is suspected to be utilised to repay the loan taken by Vintage under Loan Agreement.

43. Following documents/information sought vide summons/emails/letters were not provided by Asahi.

5 Ababil was a company based outside India with which Avon had an agreement worth USD 4 million to purchase second hand machinery. Ababil was also one of the initial investors of GDR issue of K Sera.

34

43.1. Important details with respect to Asahi FZE viz. address, contact person and contact no. was not provided by Asahi to SEBI.

43.2. Asahi was specifically asked to explain the rationale behind all the payments done by Asahi FZE which were above USD 25,000. However, Asahi did not provide rationale for payments done by Asahi FZE.

43.3. Details of purchases and expenses incurred by Asahi FZE were not provided.

44. Due to the fact that Asahi did not provide the specific details like purpose of payments done by Asahi FZE with proper documentary proof, it was not possible for SEBI to investigate the end use of the GDR proceeds by Asahi FZE and establish complete cycle of flow of funds. It is suspected, due to reasons explained above, that Asahi FZE was used by AP to route funds back to Vintage and other AP entities. The same is explained in chart below:-

35

Misleading Submissions by Asahi:-

45. Apart from not providing aforementioned critical information to SEBI, wrong

information was also provided by Asahi. The wrong submissions of Asahi were particularly related to Pledge and Loan Agreements to which Asahi was one of the party.

46. It was confirmed by Asahi in its submissions that there were no conditions prescribed under any Agreement with Euram with regard to withdrawal of funds from GDR Account.

47. Asahi denied having any other agreement with Euram other than Escrow Account agreement.

48. Asahi also denied having any agreement with Vintage or AP.

49. Asahi denied having any agreement with any entity regarding financing of subscription of GDR Issues.

50. The submission by Asahi that it did not have any other agreement with Euram, Panasia, Vintage or AP is false as Pledge was signed by the Managing Director of the company with Euram. Further, this Pledge Agreement is part of the Loan Agreement between Vintage and Euram. Similarly it is mentioned in the Pledge Agreement that the Pledgor has received the Loan Agreement and agrees to its conditions.

51. Asahi also made a false submission of no restriction/condition on its GDR Account for withdrawal of funds. From the perusal of Pledge Agreement it is observed that the GDR Account is a collateral against the Loan taken by Vintage and therefore funds can only be withdrawn when the loan is repaid by Vintage

52. Asahi did not disclose details of outstanding GDRs in its quarterly disclosure of share holding pattern to exchanges. As per BSE website, the equity held with custodians is shown as nil for Asahi even after issuance of GDR issue.

53. The above explained falsification of information regarding Pledge and Loan Agreements and concealment of information regarding utilisation of funds by foreign subsidiary supports the suspicion of SEBI that part of the proceeds of GDR issue were routed back to AP entities.

54. In conclusion, it may be said that Asahi having executed the fraudulent

transaction of claiming subscription of GDRs by two foreign investors while it was only purchased by the LM/AP related entity and finding the proceeds being encumbered due to the underlying loan taken by AP, finally received, in India, not more than 30% of the money raised. The remaining funds were paid out to various parties without any clear purpose of such transfers

36

mentioned in the books of the company. These highly material events are not explained clearly in the financial statements of the company nor were ever disclosed to the market. The shareholders of Asahi were adversely and without warning impacted due to the slide in prices on account of the large sale of shares upon cancellation of GDRs.

37

(II) AVON CORPORATION LTD.

Summary of GDR issue:-

1. The GDR Issue of Avon for US $ 10 Million closed on June 19, 2009 and was

fully subscribed. The allotment of 16,00,000 Global Depository Receipts representing 4,80,00,000 equity shares of Rs 10/- each at $6.25 by the company was done on June 19, 2009.

2. Panasia was appointed as the LM to the GDR issue by the company.

3. Prior to GDR issue, Avon had 1,65,80,317 fully paid equity shares. Therefore, the equity shares represented by the GDRs were approximately 289.50% of Avon's outstanding share capital at the time of GDR issue.

4. The total capital raised by Avon vide GDRs was USD 1,00,00,000 which is equal to Rs. 48,13,00,000 considering conversion price of USD 1 = Rs. 48.13 as on June 19, 2009. The market cap of Avon prior to GDR issue was Rs. 14,71,00,000. Therefore, the capital raised by GDR issue was 327.19% of the market capital of the company prior to GDR issue.

5. The last traded price of Avon on BSE on June 19, 2009 was Rs. 8.87. The highest and lowest price of Avon for a period of three months from March 19, 2009 to June 19, 2009 was Rs. 10.30 and Rs. 3.95 respectively. The price which subscribers paid for each share underlying GDRs was Rs. 10.02 (USD 1 = Rs. 48.13 as on June 19, 2009) which was 112.05% of the price of the scrip on same day.

Subscribers of GDR Issue:-

6. Following are the details of investors in the GDR issue of Avon, as submitted

by the company.

Name of Subscriber GDRs Subscribed

Amount Paid (USD)

% of total GDR issue

Flamboyant International Ltd (Flamboyant) 2,40,000 15,00,000 15.00

Trendsetter Enterprises Cops.(Trendsetter) 3,20,000 20,00,000 20.00

Green Management Inc (Greenwich) 2,88,000 18,00,000 18.00

Flagstaff Investments LTD (Flagstaff) 2,24,000 14,00,000 14.00

Imagination Network Inc.(Imagination) 2,40,000 15,00,000 15.00

Figura Group LTD (Figura) 2,88,000 18,00,000 18.00

38

7. All the above subscribers were observed to be investors in several other GDR issues of Indian companies which were managed by Panasia. The addresses of these subscribers which were made available to SEBI are as following.

Name of Subscriber Address

Flamboyant 21st

Floor, ICBC Tower, Citibank Plaza No: 3, Garden Road, Hong Kong

Trendsetter Level 42, Suntec 4, 8 Temasek BLVD, Singapore - 038988

Greenwich Floor - 18, One International Finance Centre, 1 Harbour view Street, Central, Hong Kong Email : [email protected]

Flagstaff 10th Floor, Al Odaid Office Tower, Airport Road, P.O. Box 128161, Abu Dhabi, UAE

Imagination Level 39, One Exchange Square, Central HongKong

Figura 15 A, West Road, West Cliff Onsea, Essex SS09AU

8. All the attempts to contact these subscribers were unsuccessful, just like in

all the other cases where LM to the GDR issue is Panasia. None of the letters, emails or summons got delivered to these subscribers due to wrong email addresses and other contact addresses. Even the financial market regulators regulating the region where these subscribers were located could not trace these subscribers. In most of the cases SEBI got a reply from the respective regulators that no such address exist that have been provided by SEBI.

Loan & Pledge Agreement signed among Avon, Vintage & Euram.

9. From the documents available with SEBI, it is observed that the issuance and

subscription of GDRs of Avon was done using loan taken from Euram. The GDR issue of Avon is issued using AP GDR Scheme and Loan and Pledge Agreement signed among Avon, Vintage and Euram is the key to issuance and subscription of GDRs in this case.

10. The Pledge and Loan agreements among Avon, Vintage and Euram are similar to that of Asahi and other companies examined by SEBI. These agreements are part of AP GDR scheme.

11. A loan agreement (Loan Agreement : 100609-002) dated June 10, 2009, was signed between Euram and Vintage on June 12, 2009. The agreement was signed by AP as Managing Director on behalf of Vintage on June 12, 2009.

12. The Loan agreement states that Euram has agreed to make available a loan of USD 1,00,00,000.00 to Vintage (referred to as ''the Borrower''). The nature and purpose of the loan facility is to provide funding enabling Vintage to take down GDR issue of Avon's Luxemburg public offering and may only be transferred to Euram account no: 540084.

39

13. The Euram account no: 540084 is the bank account of Avon maintained with Euram for the purpose of depositing proceeds of GDR issue.

14. As security against the Loan provided to Vintage following is stated in the Loan Agreement. "6.1 In order to secure all and any of the Bank's claims and entitlements against the Borrower, arising now or in the future out of or in connection with the Loan or any other obligation or liability of the Borrower to the Bank, including without limitation other loans granted in the future , it is hereby irrevocably agreed that the following securities and any other securities which may be required by the Bank from time to time shall be given to the Bank as provided herein or in any other form or manner as may be demanded by the Bank

Pledge of certain securities held from time to time in the Borrower's account no. 540 084 at the Bank as set out in a separate pledge agreement which is attached hereto as Annex 2 and which forms an integral part of this Loan Agreement.

Pledge of the account no. 540 084 of the Borrower held with the Bank as set out in a separate pledge agreement which is attached hereto as Annex 2 and which forms an integral part of this Loan Agreement."

15. A Pledge Agreement dated June 10, 2009 was signed between Avon and Euram. The agreement was signed by Mr. Pankaj Saraiya on June 12, 2009 on behalf of Avon, as CEO of Avon. He and his other family members are promoters of Avon.

16. According to the Pledge Agreement, Avon has been referred as "Pledgor'' and Euram has been referred to as ''Bank''.

17. The preamble of the Pledge Agreement states

"By loan agreement K210409-003 (hereinafter referred to as ''Loan Agreement'') dated June 10, 2009, the Bank granted a loan (hereinafter referred to as the ''Loan'') to Vintage FZE, AAH-213, Al Ahmadi House, Jebel Ali Free Trade Zone, Jebel Ali, Dubai, United Arab Emirates (''the Borrower") in the amount of $ USD 10,000,000.00. The Pledgor has received a copy of the Loan Agreement and acknowledges and agrees to its terms and conditions."

18. From the above preamble of Pledge Agreement, it is clear that Mr. Pankaj Saraiya and Avon were also the party to the Loan Agreement between Vintage and Euram.

19. The pledge created in the Pledge Agreement is stated below:-

40

" 2. Pledge

2.1 In order to secure any and all obligations, Present and future, whether conditional or unconditional of the Borrower towards the bank under the Loan Agreement and any and all respective amendments thereto and for any and all other current or future claims which the Bank may have against the Borrower in connection with the Loan Agreement – including those limited as to condition or time or not yet due – irrespective of whether such claims have originated from the account relationship, from bills of exchange, guarantees and liabilities assumed by the Borrower or by the Bank, or have otherwise resulted from business relations, or have been assigned in connection therewith to the Bank (“the Obligations”) the Pledgor hereby pledges to the Bank the following assets as collateral to the Bank:

2.1.1 all of its rights, title and interest in and to the securities deposited from time to time at present or hereafter (hereinafter referred to as the “Pledged Securities”) and the balance of funds up to the amount of $ USD 10,000,000.00 existing from time to time at present or hereafter on the securities account(s) no. 540 084 held with the Bank (hereinafter referred to as the “Pledged Securities Account”) and all amounts credited at any particular time therein.

2.1.2 all of its right, title and interest in and to, and the balance of funds existing from time to time at present or hereafter on the account(s) no. 540 084 kept by the Bank (hereinafter referred to as the “Pledged Time Deposit Account “) and all amounts credited at any particular time therein.

(the Pledged securities account and the Pledged Time Deposit account hereinafter referred to as the “Pledged Accounts”, the Pledged Securities and the Pledged Accounts hereinafter collectively referred to as “Collateral”)

2.2 The Pledgor agrees to deposit with the Bank all dividends, interest and other payments, distributions of cash or other property resulting from the Pledged Securities and funds."

20. Further, following condition have been put in the Pledge agreement for the realization of the pledge.

"6. Realization of the Pledge

6.1 In the case that the Borrower fails to make payment on any due amount, or default in accordance with the Loan Agreement, The Pledgor herewith grants its express consent and the Bank is entitled to apply the funds in the Pledged Accounts to settle the Obligations. In such case the Bank shall transfer the funds on the Pledged Accounts, even repeatedly, to an account specified by the Bank

6.2 Notwithstanding the foregoing, in the case that the Borrower fails to make payment on any due amount, or defaults in providing or increasing security, the Pledgor herewith grants its express consent and the Bank is entitled to realize the Pledged Securities (i) at a public auction for those items of Pledged Securities for which no market price is quoted or which are not listed on a recognized stock exchange or (ii) in a private sale pursuant to the provisions of Section 376 Austrian Commercial Code unless the Bank decides to exercise its rights through court

41

proceedings. The Pledgor and the Bank agree to Realize those items of the Pledged Securities for which a market price is quoted or which are listed on a stock exchange through sale by a Broker Publicly authorized for such transactions, selected by the Bank.

6.3 The Bank may realize the Pledge rather than accepting payments from the Borrower after maturity of the claim if the Bank has reason to believe that the Borrower’s payments may be contestable. "