Embed Size (px)

Citation preview

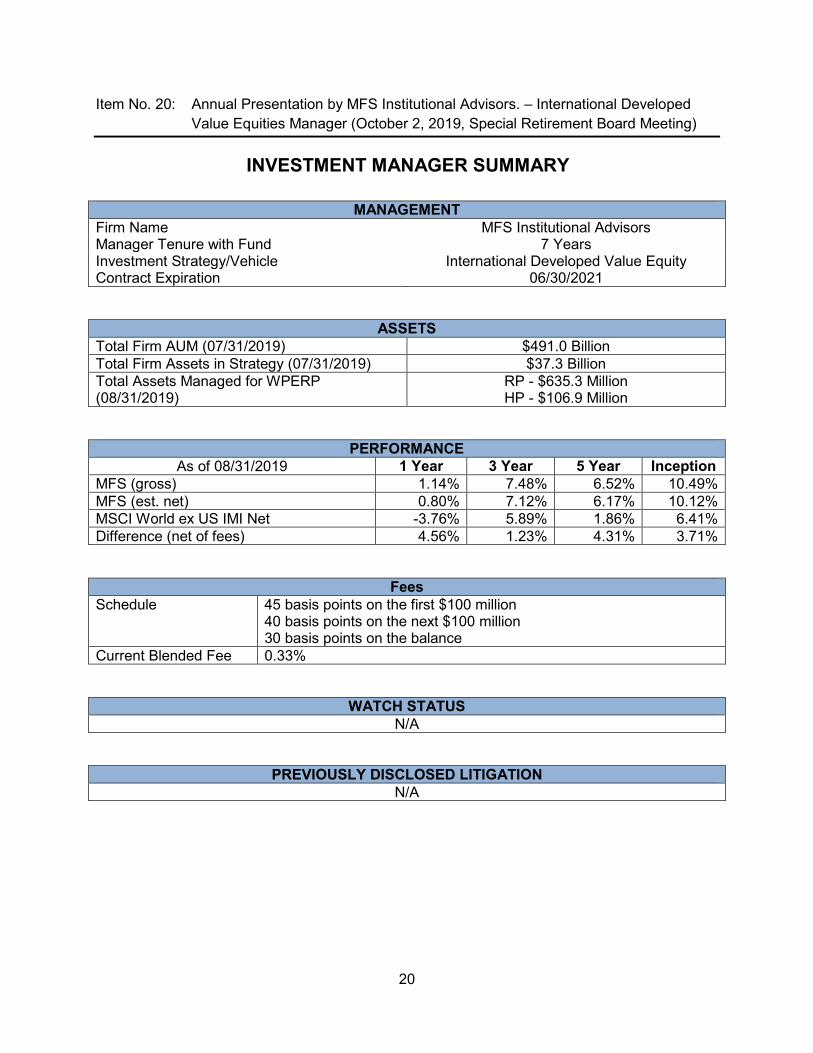

20

Item No. 20: Annual Presentation by MFS Institutional Advisors. – International Developed Value Equities Manager (October 2, 2019, Special Retirement Board Meeting)

INVESTMENT MANAGER SUMMARY

MANAGEMENT Firm Name MFS Institutional Advisors Manager Tenure with Fund 7 Years Investment Strategy/Vehicle International Developed Value Equity Contract Expiration 06/30/2021

ASSETS Total Firm AUM (07/31/2019) $491.0 Billion Total Firm Assets in Strategy (07/31/2019) $37.3 Billion Total Assets Managed for WPERP (08/31/2019)

RP - $635.3 Million HP - $106.9 Million

PERFORMANCE As of 08/31/2019 1 Year 3 Year 5 Year Inception

MFS (gross) 1.14% 7.48% 6.52% 10.49% MFS (est. net) 0.80% 7.12% 6.17% 10.12% MSCI World ex US IMI Net -3.76% 5.89% 1.86% 6.41% Difference (net of fees) 4.56% 1.23% 4.31% 3.71%

Fees Schedule 45 basis points on the first $100 million

40 basis points on the next $100 million 30 basis points on the balance

Current Blended Fee 0.33%

WATCH STATUS N/A

PREVIOUSLY DISCLOSED LITIGATION N/A

The Global Industry Classifi cation Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and S&P Global Market Intelligence Inc. (“S&P Global Market Intelligence”). GICS is a service mark of MSCI and S&P Global Market Intelligence and has been licensed for use by MFS.

MFS® International Intrinsic Value Equity

Presented to

Water and Power Employees' Retirement Plan02 October 2019

19964.12 ex31OCT19FOR ONE-ON-ONE USE ONLY

Effective 1 June 2019, the name of the MFS International Value Equity strategy changed to the MFS International Intrinsic Value Equity strategy. There was no change to the investment strategy or objective.

MFS® International Intrinsic Value Equity ii299-I-CT-IIV-02Oct19.ii

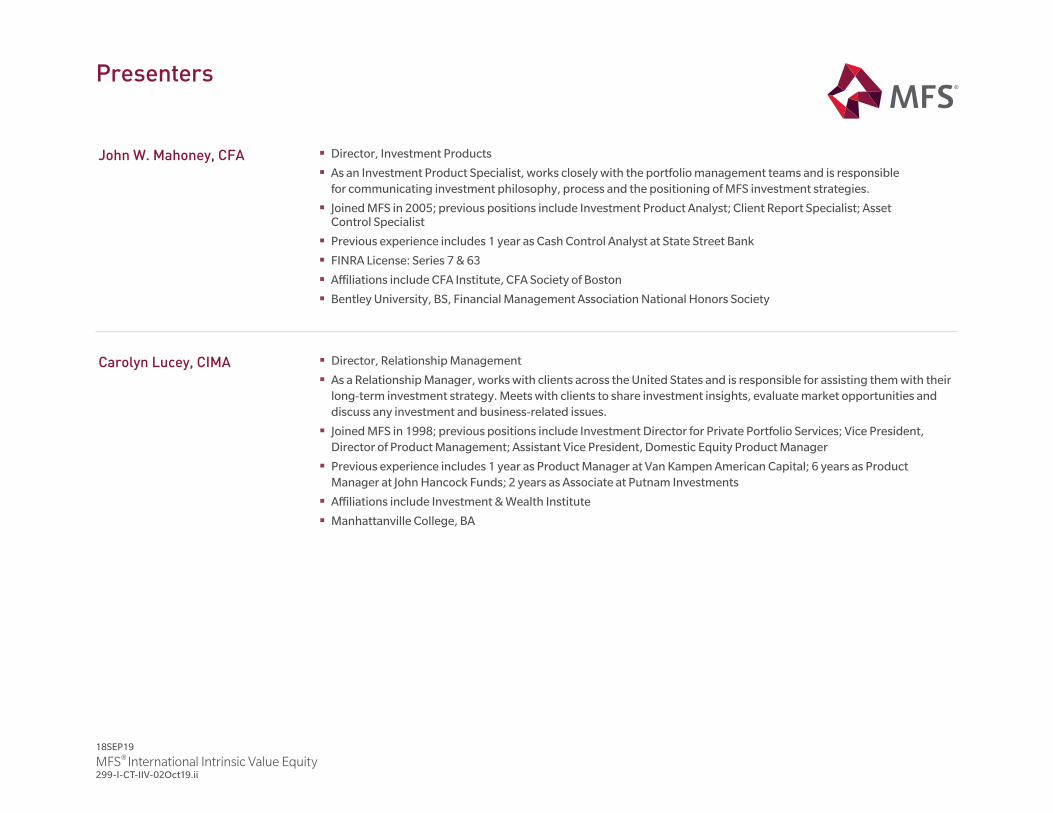

Presenters

John W. Mahoney, CFA Director, Investment Products

As an Investment Product Specialist, works closely with the portfolio management teams and is responsible for communicating investment philosophy, process and the positioning of MFS investment strategies

Joined MFS in 2005; previous positions include Investment Product Analyst; Client Report Specialist; Asset Control Specialist

Previous experience includes 1 year as Cash Control Analyst at State Street Bank

FINRA License: Series 7 & 63

Affiliations include CFA Institute, CFA Society of Boston

Bentley University, BS, Financial Management Association National Honors Society

Carolyn Lucey, CIMA Director, Relationship Management

As a Relationship Manager, works with clients across the United States and is responsible for assisting them with theirlong-term investment strategy. Meets with clients to share investment insights, evaluate market opportunities and discuss any investment and business-related issues.

Joined MFS in 1998; previous positions include Investment Director for Private Portfolio Services; Vice President,Director of Product Management; Assistant Vice President, Domestic Equity Product Manager

Previous experience includes 1 year as Product Manager at Van Kampen American Capital; 6 years as ProductManager at John Hancock Funds; 2 years as Associate at Putnam Investments

Affiliations include Investment & Wealth Institute

Manhattanville College, BA

18SEP19

MFS® International Intrinsic Value Equity iii299-I-CT-IIV-02Oct19.iii

Table of Contents

Contents Tab

Section A: Company Overview 1

Section B: Investment Process and Discipline 2

Section C: Market Overview 3

Section D: Performance Review 4

Section E: Portfolio Review and Characteristics 5

Section F: Fee Schedule 6

Section G: Glossary of Investment Terms 7

Company Overview

MFS® International Intrinsic Value Equity 1299-I-CT-IIV-02Oct19.1

Assets under management (USD) as of 31 July 2019:

Total firm AUM:

491 billion USD

Total MFS International Intrinsic Value Equity strategy AUM:

37.3 billion USD

Personnel Changes

On March 25, 2019, Nola Kopfer, CFA, joined MFS as director of Global Trading. In this role, she has oversight of the firm's global equity and global fixed income trading functions, leading a team of trading professionals across the firm's three trading desks in Boston, London and Toronto.

She joins MFS from UBS Securities, LLC, where she most recently was an executive director and head of Americas Equities Electronic Sales Trading. She previously worked for Goldman, Sachs & Co. for 14 years in multiple roles where she helped champion and lead the implementation of electronic trading, including eight years managing the firm's Boston-based electronic sales trading team. She holds a Bachelor of Arts in Economics from Columbia University and holds the CFA charter as a member of the CFA Institute.

MFS Corporate Update

MFS® International Intrinsic Value Equity 2299-I-CT-IIV-02Oct19.2

We create long-term value by

allocating capital responsibly

for investors

RISK MANAGEMENTLONG-TERM DISCIPLINE

Conviction and longer time horizons

Sustainable investing

Continuity/Succession planning

Engagement

Diversity and collaboration

Integrated research

Risk-aware culture

Understanding material risks

Capacity management

MFS® — Committed to Alignment

COLLECTIVE EXPERTISE

Uncovering market opportunities while striving to protect our clients' reputations

MFS® International Intrinsic Value Equity 3299-I-CT-IIV-02Oct19.3

41718.4

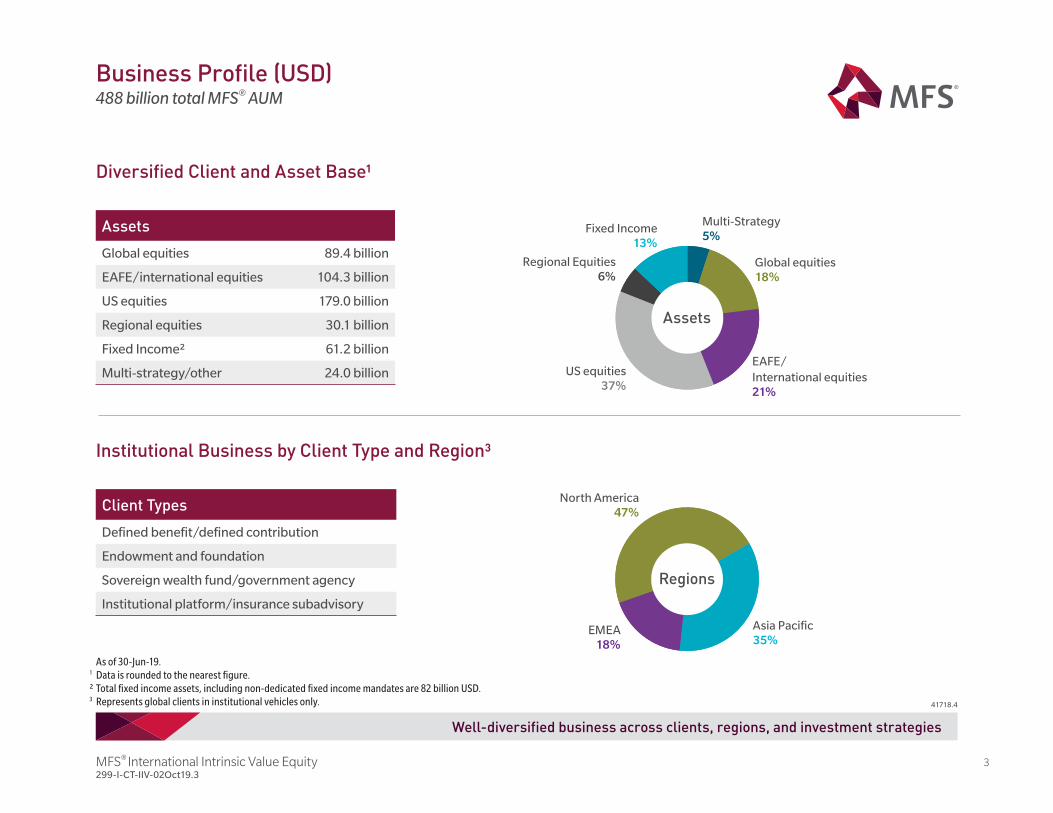

As of 30-Jun-19.1 Data is rounded to the nearest fi gure. ² Total fi xed income assets, including non-dedicated fi xed income mandates are 82 billion USD.3 Represents global clients in institutional vehicles only.

Well-diversified business across clients, regions, and investment strategies

Business Profile (USD) 488 billion total MFS® AUM

Client Types

Defi ned benefi t/defi ned contribution

Endowment and foundation

Sovereign wealth fund/government agency

Institutional platform/insurance subadvisory

Diversified Client and Asset Base¹

Institutional Business by Client Type and Region³

Regions

Assets

Regions

Assets

Fixed Income13%

US equities37%

Regional Equities6%

EMEA18%

North America47%

Global equities18%

EAFE/International equities21%

Asia Pacifi c35%

Multi-Strategy5%

Assets

Global equities 89.4 billion

EAFE/international equities 104.3 billion

US equities 179.0 billion

Regional equities 30.1 billion

Fixed Income² 61.2 billion

Multi-strategy/other 24.0 billion

MFS® International Intrinsic Value Equity 4299-I-CT-IIV-02Oct19.4

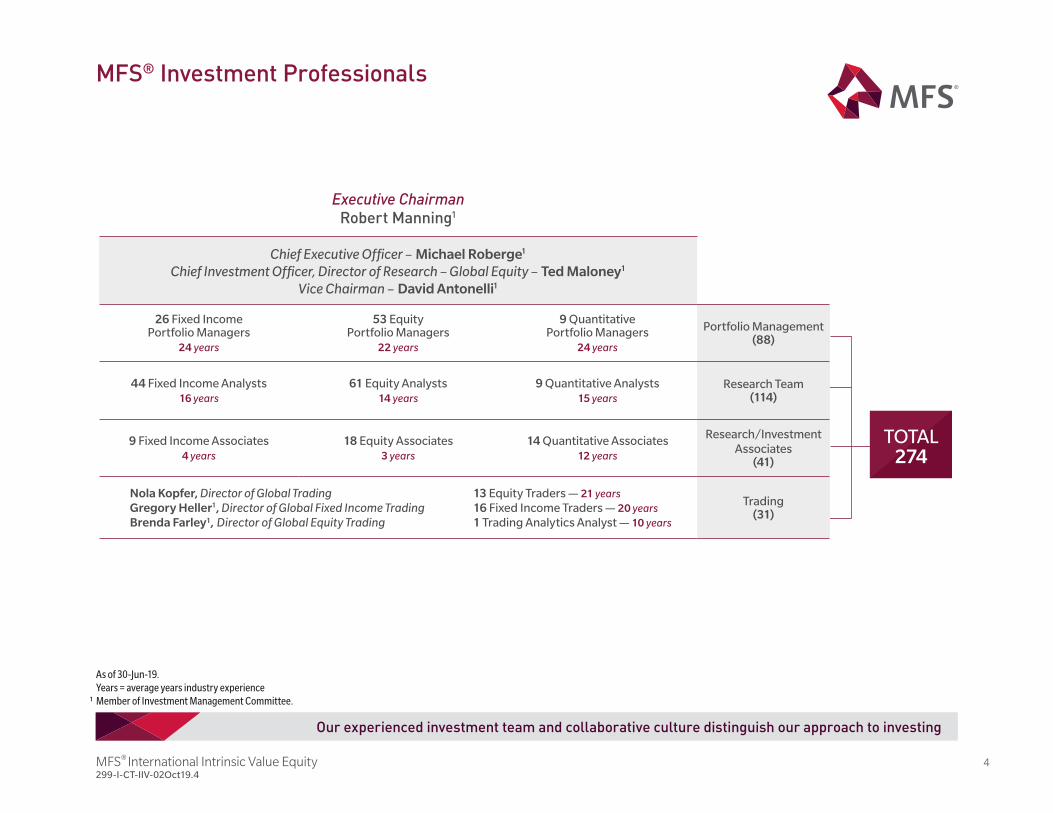

Our experienced investment team and collaborative culture distinguish our approach to investing

MFS® Investment Professionals

As of 30-Jun-19.Years = average years industry experience

¹ Member of Investment Management Committee.

Executive ChairmanRobert Manning1

Chief Executive Offi cer – Michael Roberge1

Chief Investment Offi cer, Director of Research – Global Equity – Ted Maloney1

Vice Chairman – David Antonelli1

26 Fixed IncomePortfolio Managers

24 years

53 EquityPortfolio Managers

22 years

9 QuantitativePortfolio Managers

24 years

Portfolio Management(88)

44 Fixed Income Analysts16 years

61 Equity Analysts14 years

9 Quantitative Analysts15 years

Research Team(114)

9 Fixed Income Associates4 years

18 Equity Associates3 years

14 Quantitative Associates12 years

Research/Investment Associates

(41)

Nola Kopfer, Director of Global Trading 13 Equity Traders — 21 yearsGregory Heller1, Director of Global Fixed Income Trading 16 Fixed Income Traders — 20 yearsBrenda Farley¹, Director of Global Equity Trading 1 Trading Analytics Analyst — 10 years

Trading(31)

TOTAL274

MFS® International Intrinsic Value Equity 5299-I-CT-IIV-02Oct19.5

As of 30-Jun-19.

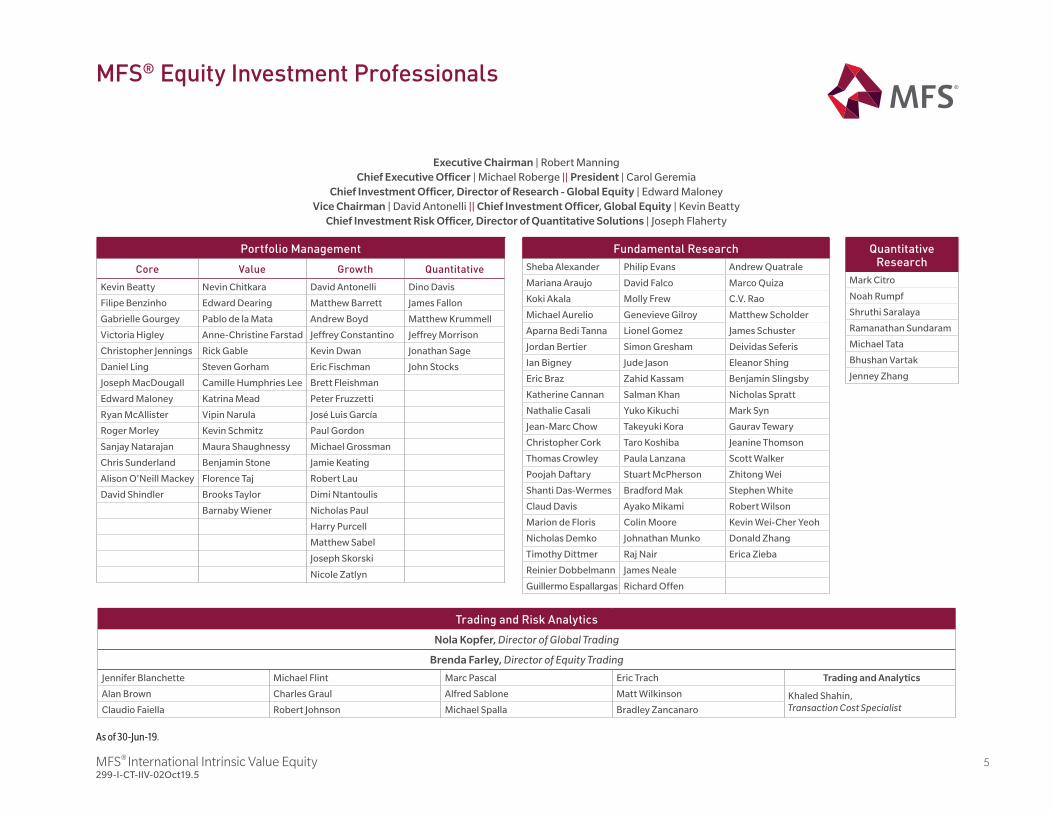

MFS® Equity Investment Professionals

Executive Chairman | Robert ManningChief Executive Offi cer | Michael Roberge || President | Carol Geremia

Chief Investment Offi cer, Director of Research - Global Equity | Edward MaloneyVice Chairman | David Antonelli || Chief Investment Offi cer, Global Equity | Kevin Beatty

Chief Investment Risk Offi cer, Director of Quantitative Solutions | Joseph Flaherty

Portfolio Management

Core Value Growth Quantitative

Kevin Beatty Nevin Chitkara David Antonelli Dino Davis

Filipe Benzinho Edward Dearing Matthew Barrett James Fallon

Gabrielle Gourgey Pablo de la Mata Andrew Boyd Matthew Krummell

Victoria Higley Anne-Christine Farstad Jeffrey Constantino Jeffrey Morrison

Christopher Jennings Rick Gable Kevin Dwan Jonathan Sage

Daniel Ling Steven Gorham Eric Fischman John Stocks

Joseph MacDougall Camille Humphries Lee Brett Fleishman

Edward Maloney Katrina Mead Peter Fruzzetti

Ryan McAllister Vipin Narula José Luis García

Roger Morley Kevin Schmitz Paul Gordon

Sanjay Natarajan Maura Shaughnessy Michael Grossman

Chris Sunderland Benjamin Stone Jamie Keating

Alison O'Neill Mackey Florence Taj Robert Lau

David Shindler Brooks Taylor Dimi Ntantoulis

Barnaby Wiener Nicholas Paul

Harry Purcell

Matthew Sabel

Joseph Skorski

Nicole Zatlyn

Fundamental Research

Sheba Alexander Philip Evans Andrew Quatrale

Mariana Araujo David Falco Marco Quiza

Koki Akala Molly Frew C.V. Rao

Michael Aurelio Genevieve Gilroy Matthew Scholder

Aparna Bedi Tanna Lionel Gomez James Schuster

Jordan Bertier Simon Gresham Deividas Seferis

Ian Bigney Jude Jason Eleanor Shing

Eric Braz Zahid Kassam Benjamin Slingsby

Katherine Cannan Salman Khan Nicholas Spratt

Nathalie Casali Yuko Kikuchi Mark Syn

Jean-Marc Chow Takeyuki Kora Gaurav Tewary

Christopher Cork Taro Koshiba Jeanine Thomson

Thomas Crowley Paula Lanzana Scott Walker

Poojah Daftary Stuart McPherson Zhitong Wei

Shanti Das-Wermes Bradford Mak Stephen White

Claud Davis Ayako Mikami Robert Wilson

Marion de Floris Colin Moore Kevin Wei-Cher Yeoh

Nicholas Demko Johnathan Munko Donald Zhang

Timothy Dittmer Raj Nair Erica Zieba

Reinier Dobbelmann James Neale

Guillermo Espallargas Richard Offen

Quantitative Research

Mark Citro

Noah Rumpf

Shruthi Saralaya

Ramanathan Sundaram

Michael Tata

Bhushan Vartak

Jenney Zhang

Trading and Risk Analytics

Nola Kopfer, Director of Global Trading

Brenda Farley, Director of Equity Trading

Jennifer Blanchette Michael Flint Marc Pascal Eric Trach Trading and Analytics

Alan Brown Charles Graul Alfred Sablone Matt Wilkinson Khaled Shahin, Transaction Cost SpecialistClaudio Faiella Robert Johnson Michael Spalla Bradley Zancanaro

MFS® International Intrinsic Value Equity 6299-I-CT-IIV-02Oct19.6

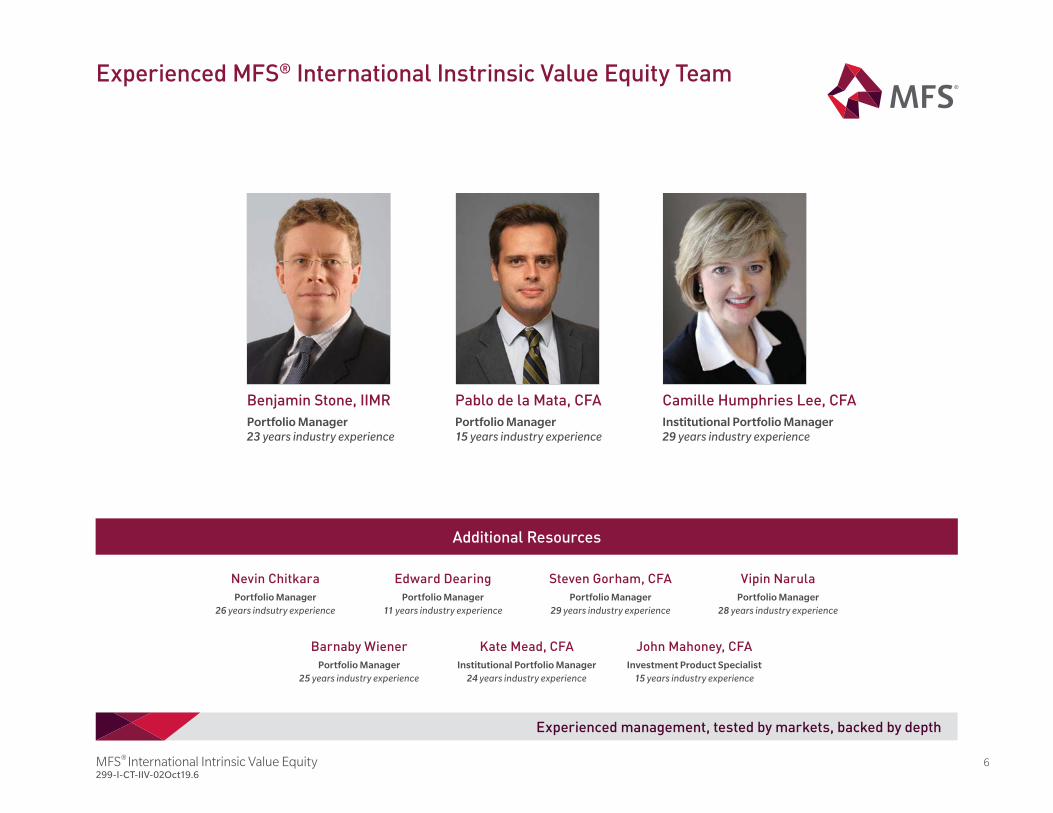

Experienced MFS® International Instrinsic Value Equity Team

Experienced management, tested by markets, backed by depth

Additional Resources

Barnaby Wiener

Portfolio Manager

25 years industry experience

Kate Mead, CFA

Institutional Portfolio Manager

24 years industry experience

John Mahoney, CFA

Investment Product Specialist

15 years industry experience

Nevin Chitkara

Portfolio Manager

26 years indsutry experience

Edward Dearing

Portfolio Manager

11 years industry experience

Steven Gorham, CFA

Portfolio Manager

29 years industry experience

Vipin Narula

Portfolio Manager

28 years industry experience

Benjamin Stone, IIMR

Portfolio Manager

23 years industry experience

Pablo de la Mata, CFA

Portfolio Manager

15 years industry experience

Camille Humphries Lee, CFA

Institutional Portfolio Manager

29 years industry experience

MFS® International Intrinsic Value Equity 7299-I-CT-IIV-02Oct19.7

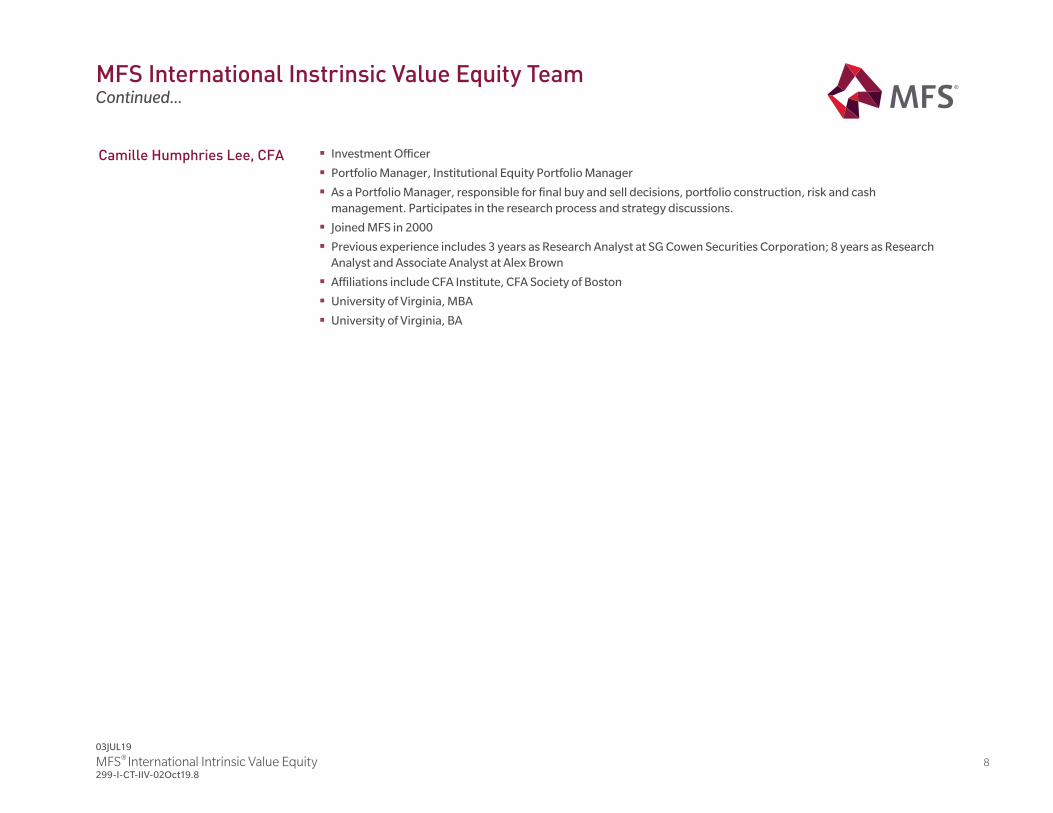

MFS International Instrinsic Value Equity Team

Benjamin Stone, IIMR Investment Officer

Equity Portfolio Manager

As an Equity Portfolio Manager, responsible for buy and sell decisions, portfolio construction, risk control and cash management. Participates in the research process and strategy discussions.

Joined MFS in 2005; previous positions include Equity Research Analyst

Previous experience includes 9 years as Research Analyst at Schroders Investment Management

Affiliations include Institute of Investment Management and Research

Durham University, BA, 2:1

Pablo de la Mata, CFA Investment Officer

Equity Portfolio Manager

As a Non-U.S. Equity Portfolio Manager, responsible for final buy and sell decisions, portfolio construction, risk and cash management. Participates in the research process and strategy discussions.

Joined MFS in 2008; previous positions include Global Equity Research Analyst

Previous experience includes 1 year as Equity Research Analyst at Magnetar Capital; 3 years as Equity Research Analyst at Blackrock/Merrill Lynch Investment Managers; 1 year as Wholesale Support at Merrill Lynch Investment Managers

Affiliations include CFA Institute

Colegio Universitario de Estudios Financieros (CUNEF), BS

03JUL19

MFS® International Intrinsic Value Equity 8299-I-CT-IIV-02Oct19.8

MFS International Instrinsic Value Equity Team

Camille Humphries Lee, CFA Investment Officer

Portfolio Manager, Institutional Equity Portfolio Manager

As a Portfolio Manager, responsible for final buy and sell decisions, portfolio construction, risk and cash management. Participates in the research process and strategy discussions.

Joined MFS in 2000

Previous experience includes 3 years as Research Analyst at SG Cowen Securities Corporation; 8 years as Research Analyst and Associate Analyst at Alex Brown

Affiliations include CFA Institute, CFA Society of Boston

University of Virginia, MBA

University of Virginia, BA

Continued...

03JUL19

MFS® International Intrinsic Value Equity 9299-I-CT-IIV-02Oct19.9

Commitment to world class client service results in enduring relationships

Non-profit & other

Archdiocese of New York

Children’s Hospital of Pittsburgh

Furman University

National Gallery of Art

Northwell Health System, Inc.

Oregon and Southwest Washington Painters

REST Industry Super, Australia

Saskatchewan Healthcare Employees' Pension

Plan, Canada

Texas A&M Foundation

Trinity University

UFCW Tri-State Pension

University of British Columbia, Canada

University of Western Ontario, Canada

Corporate funds

American Airlines

Bristol-Myers Squibb

CenturyLink

Manulife Financial, Canada

PepsiCo Inc.

Robert Bosch GmbH

Soka-Bau-Zusatzversorgungskassedes Baugewerbes AG

Telstra Super, Australia

Toyota Motor Corporation, Japan

Sub-advised accounts

ANZ New Zealand Investments

Financière des professionnels, Canada

GuideStone Capital Management, USA

NTUC Income Insurance, Singapore

1 As of 30-Jun-19. This does not represent a complete list of MFS’ institutional clients. The selection of clients represents a sampling of those who have agreed to the use of their names.It is not known whether the listed clients approve or disapprove of MFS Institutional Advisors Inc. or the advisory service provided. The criteria used to include the above listed clients are a mix of investment style, type of client, and other considerations.

Representative MFS Institutional Client List1

Serving over 800 institutional clients globally

Commitment to world class client service results in enduring relationships

Public funds

Andra AP-Fonden

Bureau of Labor Funds, Taiwan

Canada Post Corporation, Canada

County of Los Angeles

Federation of National Public Service Workers

Personnel Mutual Aid Associations, Japan

Government Pension Investment Fund of Japan

Government Pension Fund, Thailand

Kapitalforeningen Lærernes Pension Invest, Denmark

Kapitalforeningen LD

LSR, The Pension Fund for State Employees in Iceland

Nebraska Investment Council

Parliamentary Contributory Pension Fund

30848.10

MFS® International Intrinsic Value Equity 10299-I-CT-IIV-02Oct19.10

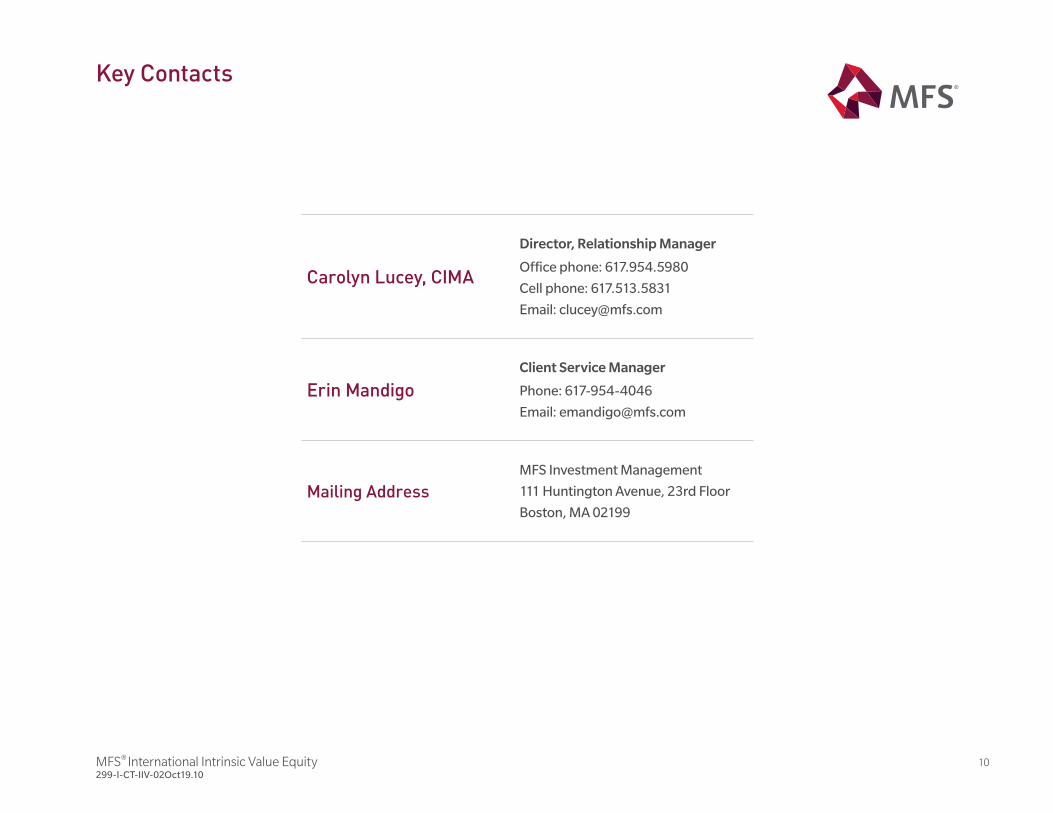

Key Contacts

Carolyn Lucey, CIMA

Director, Relationship Manager

Office phone: 617.954.5980

Cell phone: 617.513.5831

Email: [email protected]

Erin Mandigo

Client Service Manager

Phone: 617-954-4046

Email: [email protected]

Mailing Address

MFS Investment Management

111 Huntington Avenue, 23rd Floor

Boston, MA 02199

Investment Process and Discipline

MFS® International Intrinsic Value Equity 12299-I-CT-IIV-02Oct19.12

Investment Approach

Leverage long-term analysis to exploit market inefficiencies

Investment Objective

Seeks capital appreciation.

GoalOutperform the MSCI World ex US IMI Index (net div) over a full market cycle. The MSCI World alue ex US IMI Index (net div) is a secondary benchmark.

Investment Philosophy

We believe that, a relentless focus on intrinsic value, can help manage a client's capital and generate stronger, risk-adjusted returns, over the long-run.

Intrinsic value is about understanding the full context of how a company's cash flows are generated and using that understanding to develop a durable, reliable and stable notion of a company's value.

Strategy

Invest rather than speculate

Most market participants speculate on near-term information and over-react to short term news flow. We, on the other hand, assess investment opportunities in the context of a 10-year time horizon.

Intrinsic cashflows not earnings

Most investors define value from accounting earnings. We seek to gain a better notion of value through understanding the full context of how companies generate cashflows.

Downside not upside

Most market participants overemphasize the upside potential versus downside risk. We aim to avoid stocks with substantial downside risk, and only invest where we believe valuations more than compensate for the inherent risks.

MFS® International Intrinsic Value Equity 13299-I-CT-IIV-02Oct19.13

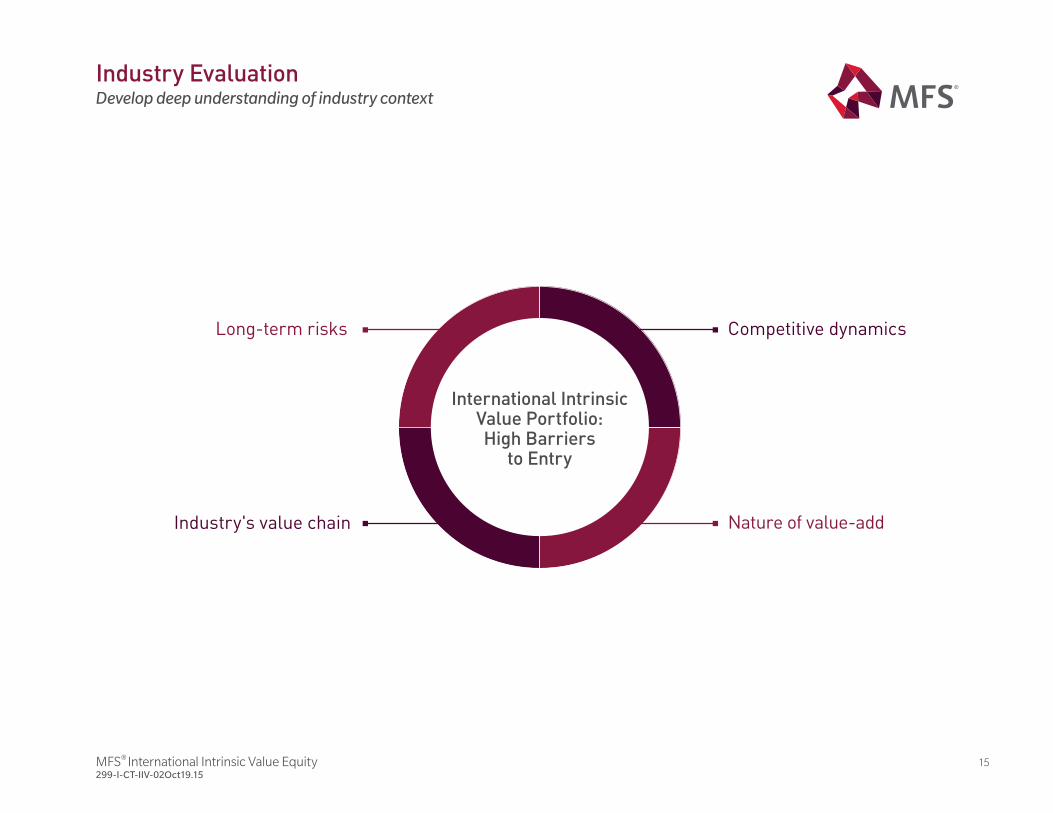

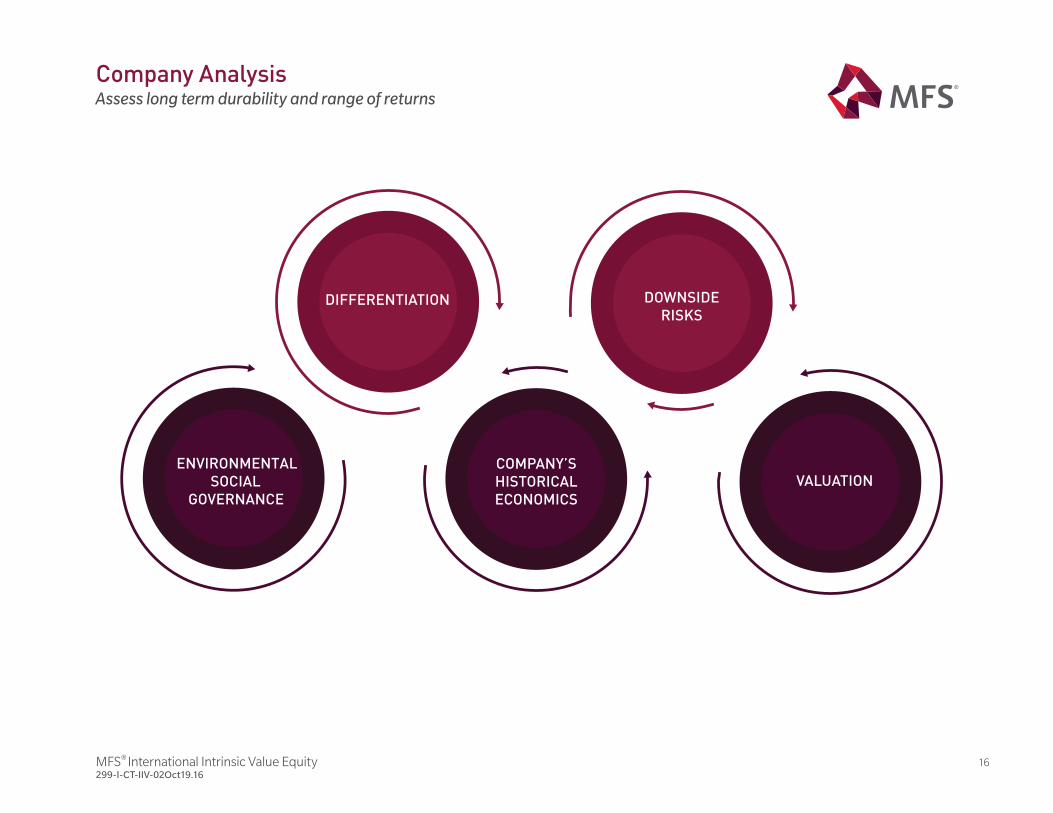

Investment Process Overview

Idea generationFundamental analysis

Portfolio construction

Industry evaluation and company analysis

Comprehensive analysis of industry context

Assess long term durability and range of returns

Focus on aimingto minimize downside risk

Broad diversifi cation

Position sizing a function of downside risk

Constant search for new ideas

Proprietary Research

Company Managements

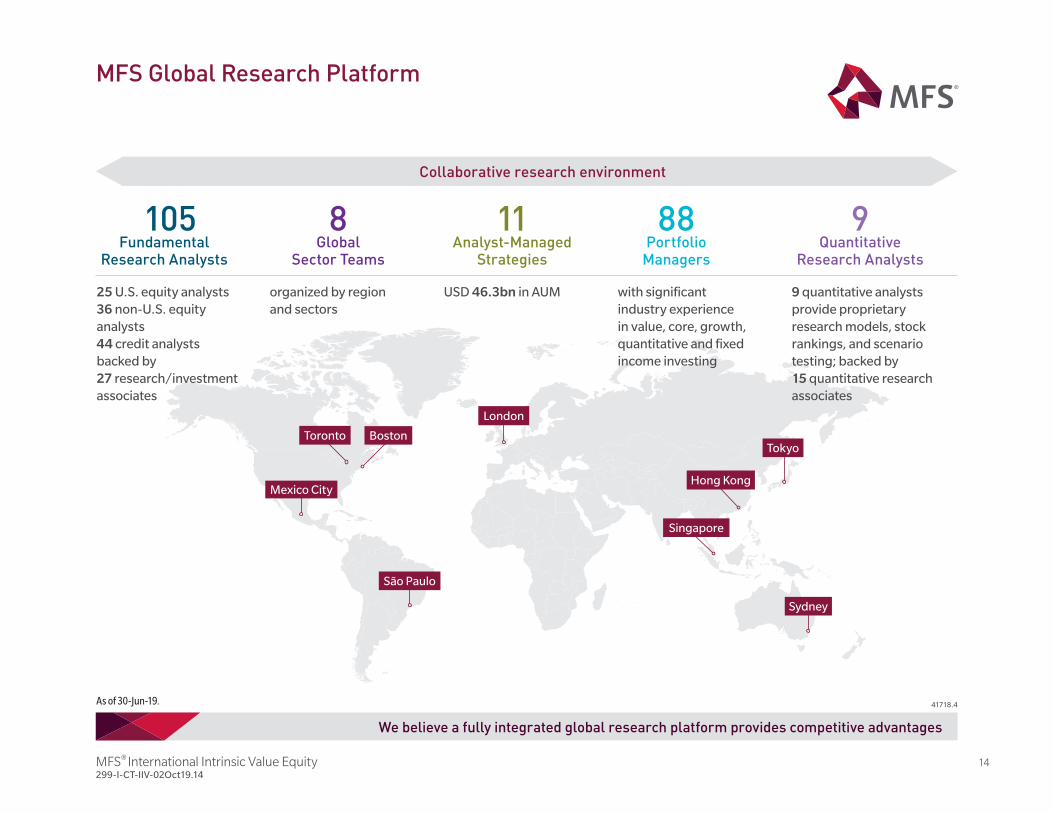

Global Research Platform

Best high-quality ideas

Generally, has held 80-110 holdings

The information listed above is current as of the date of the material, and any additions, modifi cations, or deletions that have occurred since that date are not refl ected.

Rigorous analysis of business, risk and valuation

MFS® International Intrinsic Value Equity

MFS® International Intrinsic Value Equity 14299-I-CT-IIV-02Oct19.14

organized by regionand sectors

41718.4

USD 46.3bn in AUM

We believe a fully integrated global research platform provides competitive advantages

Toronto Boston

Mexico City

São Paulo

London

Tokyo

Hong Kong

Singapore

Sydney

105Fundamental

Research Analysts

8Global

Sector Teams

88Portfolio

Managers

with signifi cant industry experience in value, core, growth, quantitative and fi xed income investing

9 quantitative analysts provide proprietary research models, stock rankings, and scenario testing; backed by15 quantitative researchassociates

Collaborative research environment

MFS Global Research Platform

Analyst-Managed Strategies

11Quantitative

Research Analysts

9

25 U.S. equity analysts 36 non-U.S. equity analysts44 credit analysts backed by27 research/investment associates

As of 30-Jun-19.

MFS® International Intrinsic Value Equity 15299-I-CT-IIV-02Oct19.15

Industry EvaluationDevelop deep understanding of industry context

Long-term risks

Nature of value-add

Competitive dynamics

International IntrinsicValue Portfolio: High Barriers

to Entry

Industry's value chain

MFS® International Intrinsic Value Equity 16299-I-CT-IIV-02Oct19.16

DOWNSIDE

RISKS

COMPANY’S

HISTORICAL

ECONOMICS

VALUATION

DIFFERENTIATION

Company AnalysisAssess long term durability and range of returns

MFS® International Intrinsic Value Equity 17299-I-CT-IIV-02Oct19.17

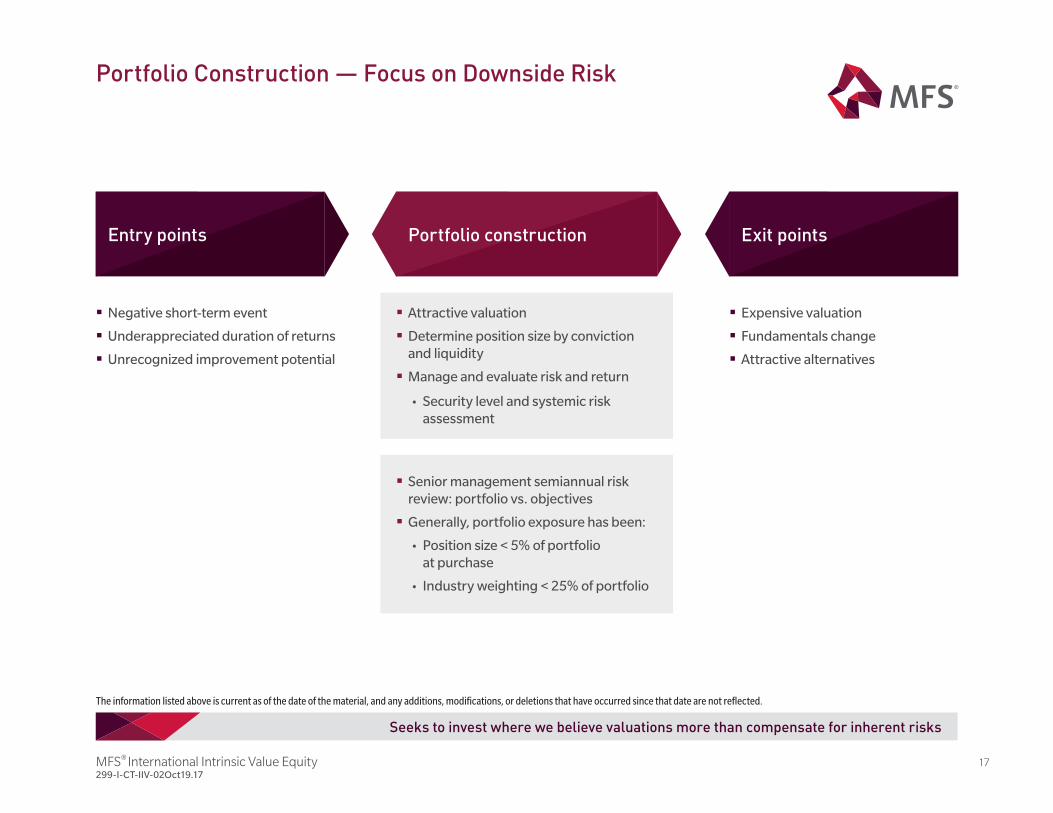

Entry points Portfolio construction Exit points

Negative short-term event

Underappreciated duration of returns

Unrecognized improvement potential

Attractive valuation

Determine position size by conviction and liquidity

Manage and evaluate risk and return

• Security level and systemic risk assessment

Senior management semiannual risk review: portfolio vs. objectives

Generally, portfolio exposure has been:

• Position size < 5% of portfolio at purchase

• Industry weighting < 25% of portfolio

Expensive valuation

Fundamentals change

Attractive alternatives

Portfolio Construction — Focus on Downside Risk

Seeks to invest where we believe valuations more than compensate for inherent risks

The information listed above is current as of the date of the material, and any additions, modifications, or deletions that have occurred since that date are not reflected.

MFS® International Intrinsic Value Equity 18299-I-CT-IIV-02Oct19.18

Note: This section is only intended to serve as a summary of the client’s investment guidelines.Please consult the current investment management agreement for complete investment guidelines.

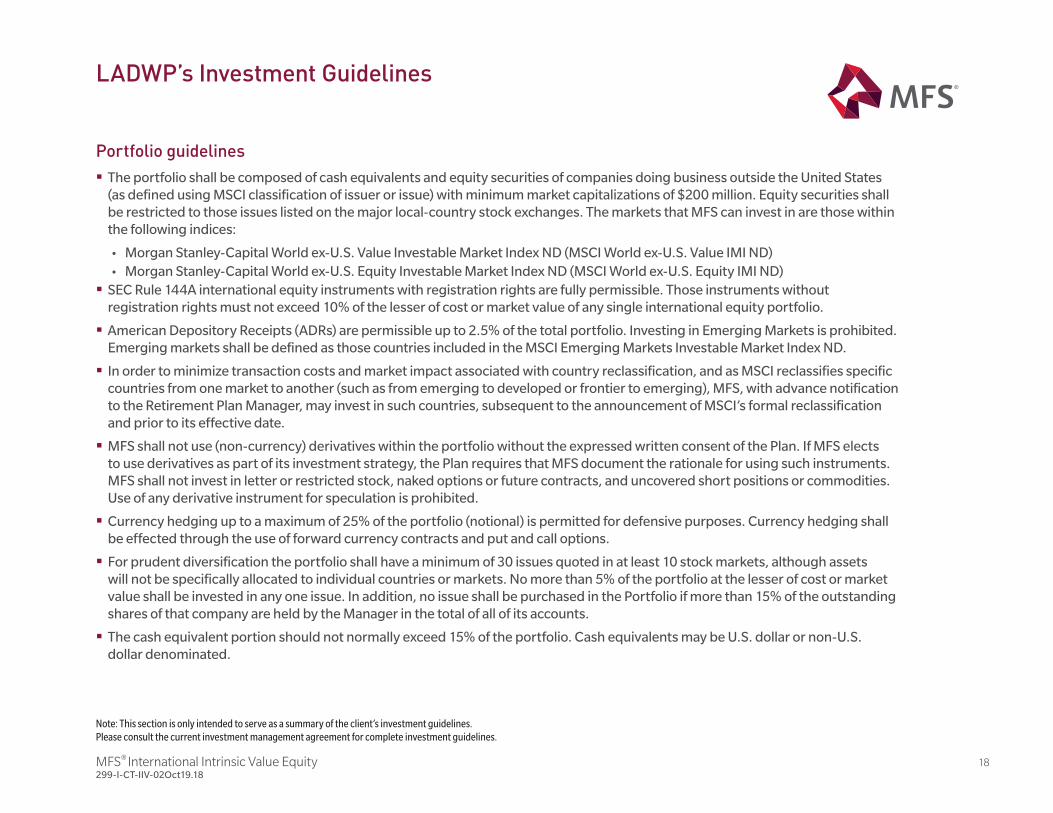

Portfolio guidelines

The portfolio shall be composed of cash equivalents and equity securities of companies doing business outside the United States (as defined using MSCI classification of issuer or issue) with minimum market capitalizations of $200 million. Equity securities shall be restricted to those issues listed on the major local-country stock exchanges. The markets that MFS can invest in are those within the following indices:

• Morgan Stanley-Capital World ex-U.S. Value Investable Market Index ND (MSCI World ex-U.S. Value IMI ND) • Morgan Stanley-Capital World ex-U.S. Equity Investable Market Index ND (MSCI World ex-U.S. Equity IMI ND)

SEC Rule 144A international equity instruments with registration rights are fully permissible. Those instruments without registration rights must not exceed 10% of the lesser of cost or market value of any single international equity portfolio.

American Depository Receipts (ADRs) are permissible up to 2.5% of the total portfolio. Investing in Emerging Markets is prohibited. Emerging markets shall be defined as those countries included in the MSCI Emerging Markets Investable Market Index ND.

In order to minimize transaction costs and market impact associated with country reclassification, and as MSCI reclassifies specific countries from one market to another (such as from emerging to developed or frontier to emerging), MFS, with advance notification to the Retirement Plan Manager, may invest in such countries, subsequent to the announcement of MSCI’s formal reclassification and prior to its effective date.

MFS shall not use (non-currency) derivatives within the portfolio without the expressed written consent of the Plan. If MFS elects to use derivatives as part of its investment strategy, the Plan requires that MFS document the rationale for using such instruments. MFS shall not invest in letter or restricted stock, naked options or future contracts, and uncovered short positions or commodities. Use of any derivative instrument for speculation is prohibited.

Currency hedging up to a maximum of 25% of the portfolio (notional) is permitted for defensive purposes. Currency hedging shall be effected through the use of forward currency contracts and put and call options.

For prudent diversification the portfolio shall have a minimum of 30 issues quoted in at least 10 stock markets, although assets will not be specifically allocated to individual countries or markets. No more than 5% of the portfolio at the lesser of cost or market value shall be invested in any one issue. In addition, no issue shall be purchased in the Portfolio if more than 15% of the outstanding shares of that company are held by the Manager in the total of all of its accounts.

The cash equivalent portion should not normally exceed 15% of the portfolio. Cash equivalents may be U.S. dollar or non-U.S. dollar denominated.

LADWP’s Investment Guidelines

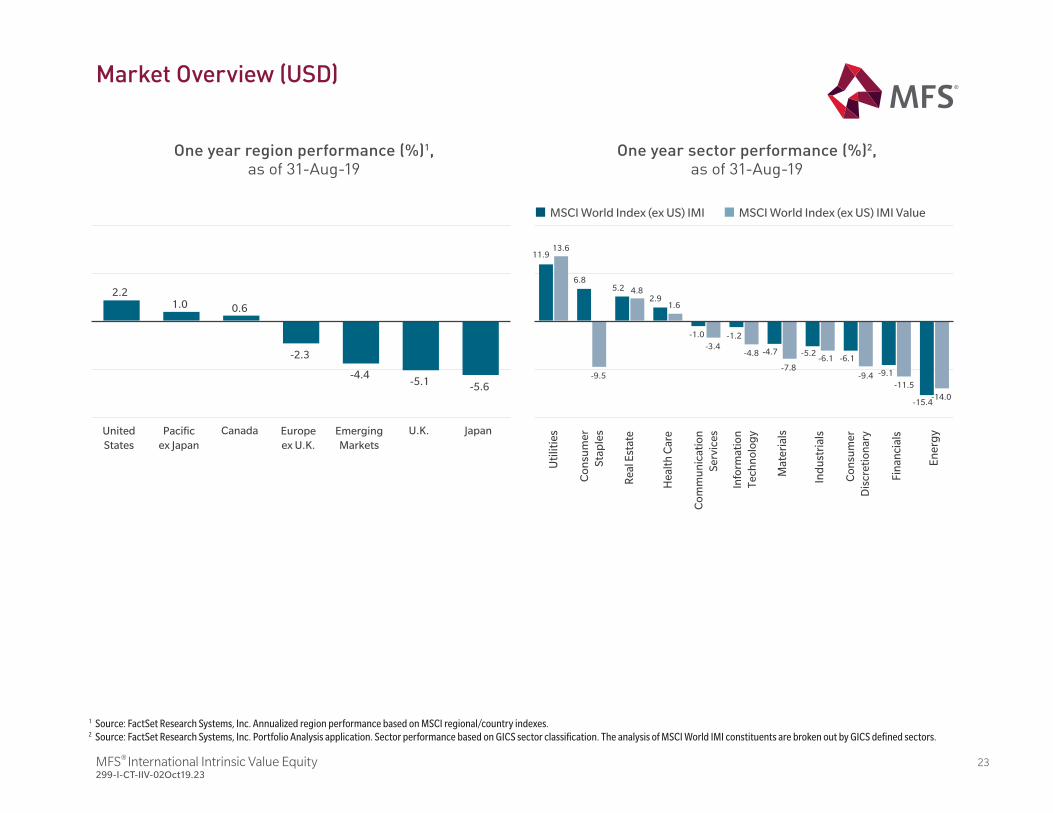

Market Overview

MFS® International Intrinsic Value Equity 20299-I-CT-IIV-02Oct19.20

The views expressed in this presentation are subject to change at any time. These views should not be relied upon as investment advice, as securities recommendation, or as an indication of trading intent on behalf of any other MFS investment product.

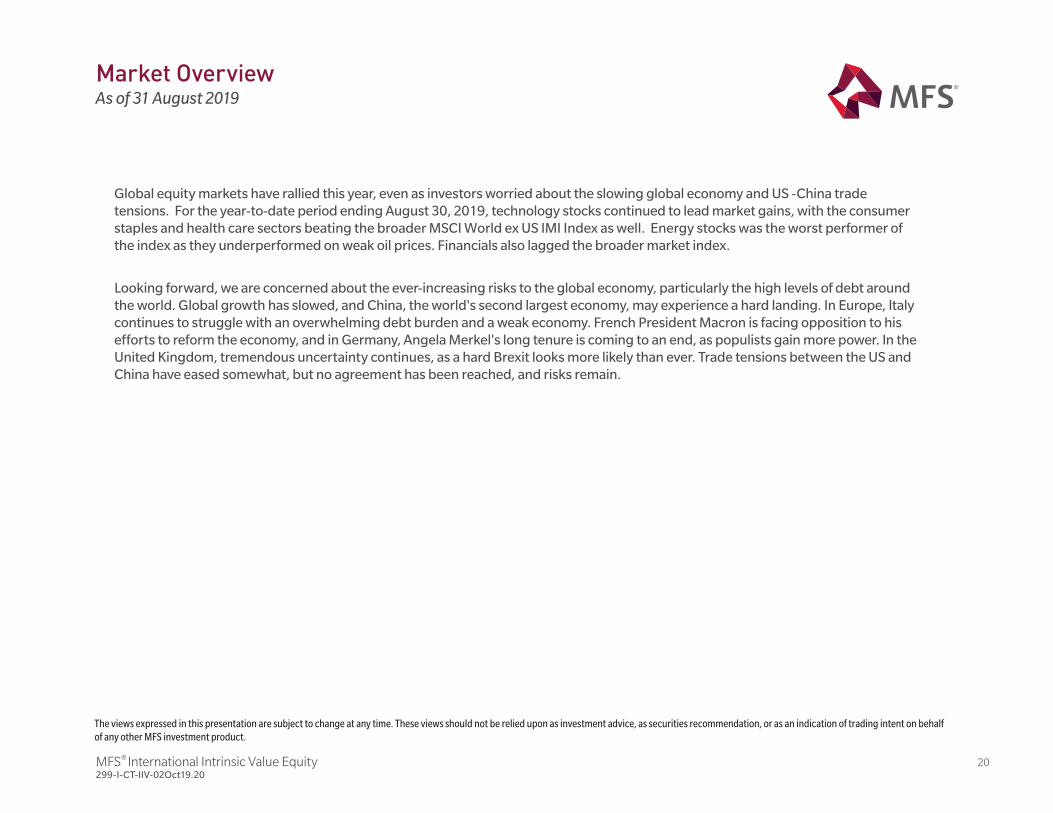

Global equity markets have rallied this year, even as investors worried about the slowing global economy and US -China trade tensions. For the year-to-date period ending August 30, 2019, technology stocks continued to lead market gains, with the consumer staples and health care sectors beating the broader MSCI World ex US IMI Index as well. Energy stocks was the worst performer of the index as they underperformed on weak oil prices. Financials also lagged the broader market index.

Looking forward, we are concerned about the ever-increasing risks to the global economy, particularly the high levels of debt around the world. Global growth has slowed, and China, the world's second largest economy, may experience a hard landing. In Europe, Italy continues to struggle with an overwhelming debt burden and a weak economy. French President Macron is facing opposition to his efforts to reform the economy, and in Germany, Angela Merkel's long tenure is coming to an end, as populists gain more power. In the United Kingdom, tremendous uncertainty continues, as a hard Brexit looks more likely than ever. Trade tensions between the US and China have eased somewhat, but no agreement has been reached, and risks remain.

Market OverviewAs of 31 August 2019

Performance Review

MFS® International Intrinsic Value Equity 22299-I-CT-IIV-02Oct19.22

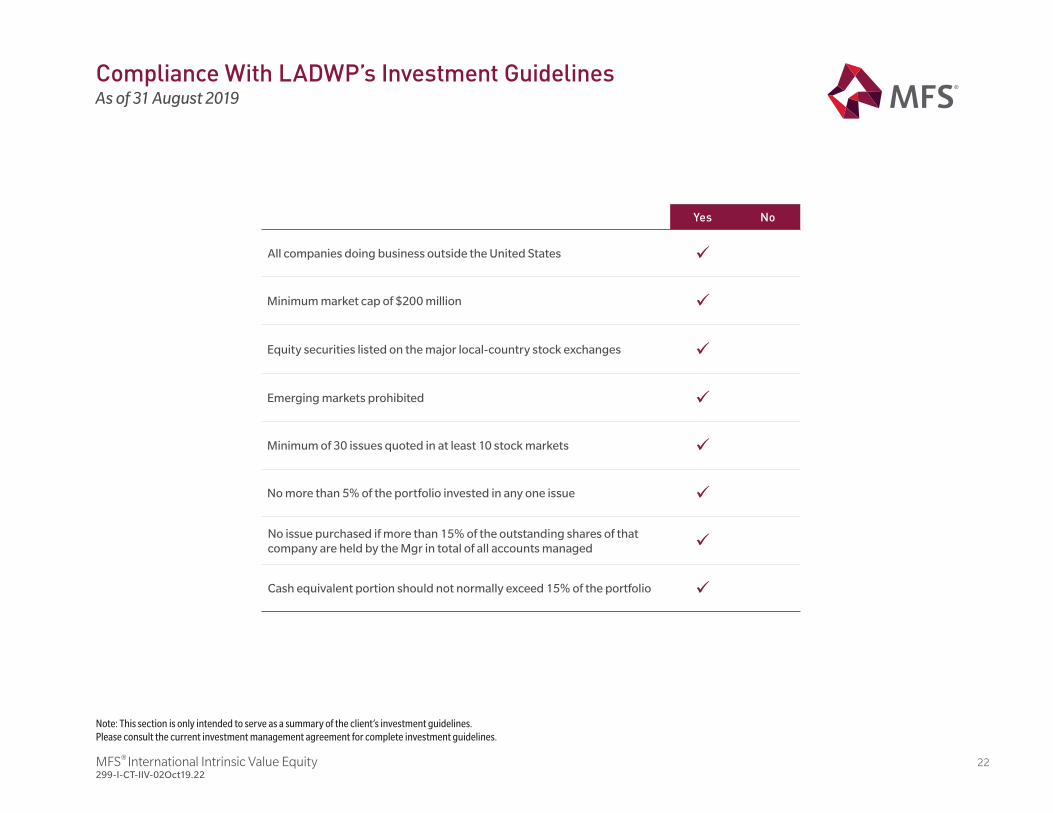

Compliance With LADWP’s Investment GuidelinesAs of 31 August 2019

Yes No

All companies doing business outside the United States

Minimum market cap of $200 million

Equity securities listed on the major local-country stock exchanges

Emerging markets prohibited

Minimum of 30 issues quoted in at least 10 stock markets

No more than 5% of the portfolio invested in any one issue

No issue purchased if more than 15% of the outstanding shares of that company are held by the Mgr in total of all accounts managed

Cash equivalent portion should not normally exceed 15% of the portfolio

Note: This section is only intended to serve as a summary of the client’s investment guidelines.Please consult the current investment management agreement for complete investment guidelines.

MFS® International Intrinsic Value Equity 23299-I-CT-IIV-02Oct19.23

One year region performance (%)1, as of 31-Aug-19

One year sector performance (%)2, as of 31-Aug-19

UnitedStates

Pacificex Japan

Canada Europeex U.K.

EmergingMarkets

U.K. Japan

2.21.0 0.6

-2.3

-4.4-5.1 -5.6

Uti

litie

s

Co

nsu

mer

Stap

les

Rea

l Est

ate

Hea

lth

Car

e

Com

mu

nic

atio

nSe

rvic

es

Info

rmat

ion

Tech

nol

ogy

Mat

eria

ls

Ind

ustr

ials

Con

sum

erD

iscr

etio

nar

y

Fina

ncia

ls

Ener

gy

11.913.6

6.8

-9.5

5.2 4.82.9

1.6

-1.0

-3.4-1.2

-4.8 -4.7

-7.8

-5.2-6.1 -6.1

-9.4 -9.1

-11.5

-15.4-14.0

MSCI World Index (ex US) IMI MSCI World Index (ex US) IMI Value

Market Overview (USD)

1 Source: FactSet Research Systems, Inc. Annualized region performance based on MSCI regional/country indexes.2 Source: FactSet Research Systems, Inc. Portfolio Analysis application. Sector performance based on GICS sector classification. The analysis of MSCI World IMI constituents are broken out by GICS defined sectors.

MFS® International Intrinsic Value Equity 24299-I-CT-IIV-02Oct19.24

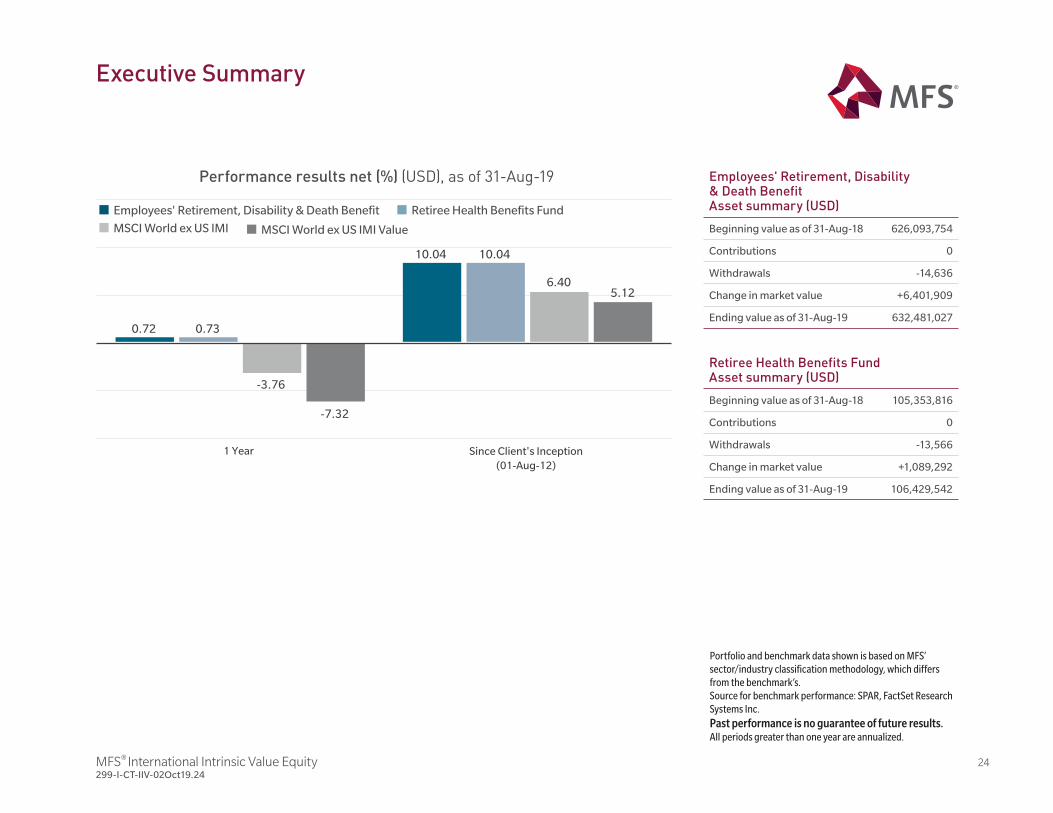

Executive Summary

Employees' Retirement, Disability & Death Benefit Asset summary (USD)

Beginning value as of 31-Aug-18 626,093,754

Contributions 0

Withdrawals -14,636

Change in market value +6,401,909

Ending value as of 31-Aug-19 632,481,027

Portfolio and benchmark data shown is based on MFS’ sector/industry classification methodology, which differs from the benchmark’s.Source for benchmark performance: SPAR, FactSet Research Systems Inc.Past performance is no guarantee of future results. All periods greater than one year are annualized.

Performance results net (%) (USD), as of 31-Aug-19

1 Year Since Client's Inception(01-Aug-12)

0.72 0.73

-3.76

-7.32

10.04 10.04

6.405.12

Employees' Retirement, Disability & Death Benefit

MSCI World ex US IMI

Retiree Health Benefits Fund Asset summary (USD)

Beginning value as of 31-Aug-18 105,353,816

Contributions 0

Withdrawals -13,566

Change in market value +1,089,292

Ending value as of 31-Aug-19 106,429,542

Retiree Health Benefits Fund

MSCI World ex US IMI Value

MFS® International Intrinsic Value Equity 25299-I-CT-IIV-02Oct19.25

Please note the composite shown is unrestricted and allows for investment in Emerging Markets and US securities.

Historical Relative Performance in Diverse MarketsGross of fees (USD)

MFS International Intrinsic Value Equity Unrestricted Composite vs MSCI World (ex-US) Investable Market Index (net div)January 1998-June 2019

Market return less than -5%

Market return -5% to +5%

Market return greater than +5%

Total

Average quarterly relative performance (%) +4.03 +0.96 -0.79 +0.99

Nu

mb

er o

f qu

arte

rs a

bov

e /b

elow

ben

chm

ark

Source: Benchmark performance from SPAR, FactSet Research Systems Inc. The exhibit above reflects the performance of a fully discretionary composite; individual portfolio results will vary. This performance information is supplemental to the composite's compliant presentation. Please see appendix for composite report, and other information. It is not possible to invest directly in an index.Past performance is not a reliable indicator for future results. All financial investments involve an element of risk. The value of investments may rise and fall so you may get back less than originally invested. Investors should consider the risks, including lower returns, related to currency movements between their investing currency and the portfolio's base currency, if different.

Number of outperforming quarters Number of underperforming quarters

0

10

20

30

40

50

60

MFS® International Intrinsic Value Equity 26299-I-CT-IIV-02Oct19.26

13.3310.37

4.21

0.72

-3.76

-7.32

7.13 5.894.11

6.11

1.86

-0.50

9.75

6.06 4.70

10.04

6.40 5.12

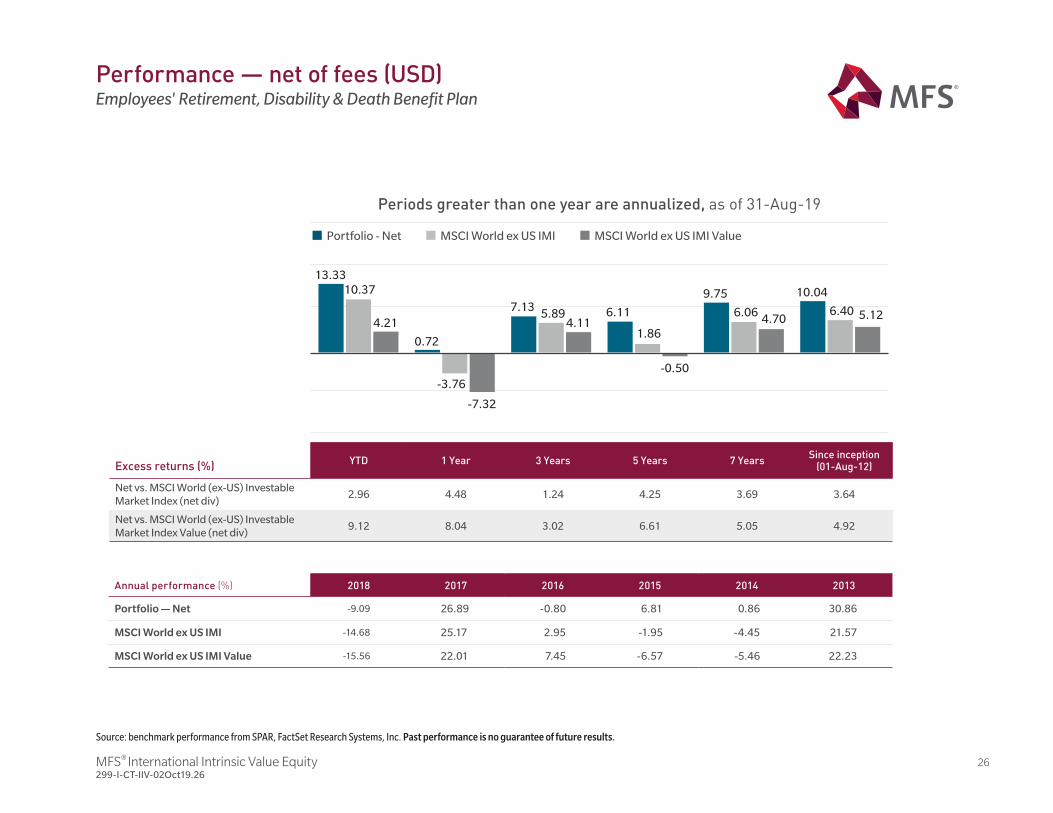

Periods greater than one year are annualized, as of 31-Aug-19

Annual performance (%) 2018 2017 2016 2015 2014 2013

Portfolio — Net -9.09 26.89 -0.80 6.81 0.86 30.86

MSCI World ex US IMI -14.68 25.17 2.95 -1.95 -4.45 21.57

MSCI World ex US IMI Value -15.56 22.01 7.45 -6.57 -5.46 22.23

Source: benchmark performance from SPAR, FactSet Research Systems, Inc. Past performance is no guarantee of future results.

Excess returns (%)YTD 1 Year 3 Years 5 Years 7 Years

Since inception (01-Aug-12)

Net vs. MSCI World (ex-US) Investable Market Index (net div)

2.96 4.48 1.24 4.25 3.69 3.64

Net vs. MSCI World (ex-US) Investable Market Index Value (net div)

9.12 8.04 3.02 6.61 5.05 4.92

Portfolio - Net MSCI World ex US IMI Value MSCI World ex US IMI

Performance — net of fees (USD)Employees' Retirement, Disability & Death Benefit Plan

MFS® International Intrinsic Value Equity 27299-I-CT-IIV-02Oct19.27

Source: benchmark performance from SPAR, FactSet Research Systems, Inc. Past performance is no guarantee of future results.

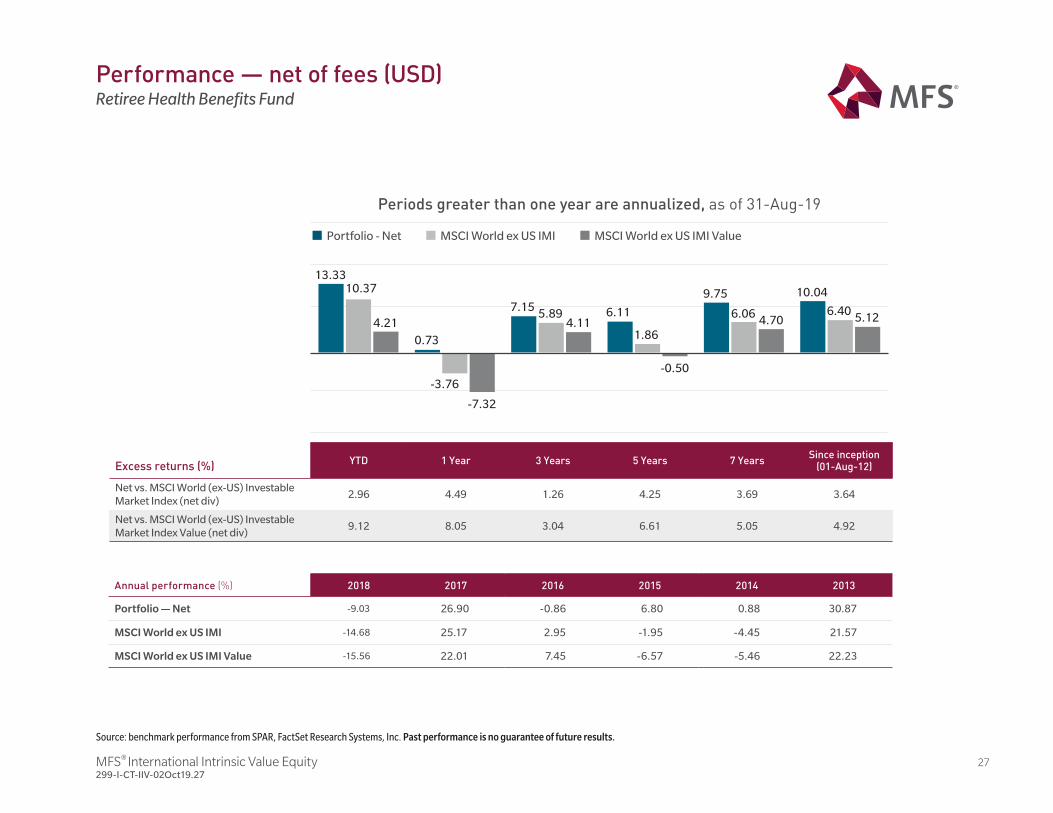

Performance — net of fees (USD)Retiree Health Benefits Fund

13.3310.37

4.21

0.73

-3.76

-7.32

7.15 5.894.11

6.11

1.86

-0.50

9.75

6.06 4.70

10.04

6.40 5.12

Periods greater than one year are annualized, as of 31-Aug-19

Annual performance (%) 2018 2017 2016 2015 2014 2013

Portfolio — Net -9.03 26.90 -0.86 6.80 0.88 30.87

MSCI World ex US IMI -14.68 25.17 2.95 -1.95 -4.45 21.57

MSCI World ex US IMI Value -15.56 22.01 7.45 -6.57 -5.46 22.23

Excess returns (%)YTD 1 Year 3 Years 5 Years 7 Years

Since inception (01-Aug-12)

Net vs. MSCI World (ex-US) Investable Market Index (net div)

2.96 4.49 1.26 4.25 3.69 3.64

Net vs. MSCI World (ex-US) Investable Market Index Value (net div)

9.12 8.05 3.04 6.61 5.05 4.92

Portfolio - Net MSCI World ex US IMI Value MSCI World ex US IMI

MFS® International Intrinsic Value Equity 28299-I-CT-IIV-02Oct19.28

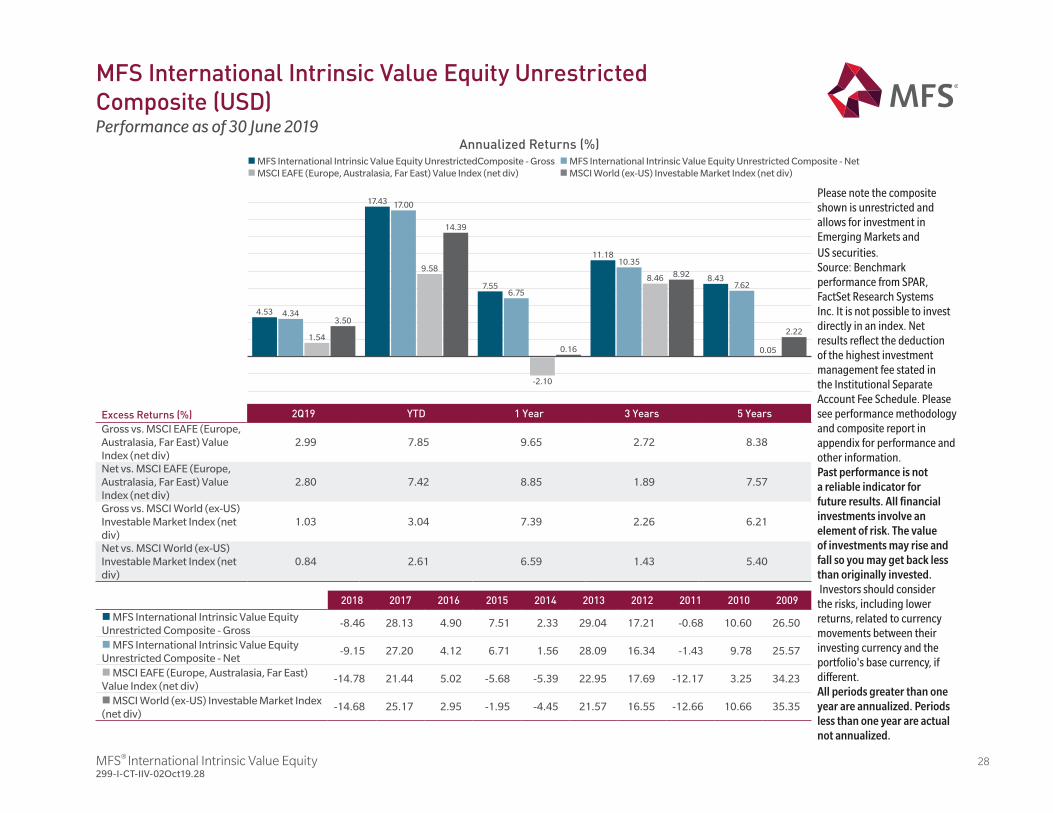

Annualized Returns (%)

Excess Returns (%) 2Q19 YTD 1 Year 3 Years 5 YearsGross vs. MSCI EAFE (Europe, Australasia, Far East) Value Index (net div)

2.99 7.85 9.65 2.72 8.38

Net vs. MSCI EAFE (Europe, Australasia, Far East) Value Index (net div)

2.80 7.42 8.85 1.89 7.57

Gross vs. MSCI World (ex-US) Investable Market Index (net div)

1.03 3.04 7.39 2.26 6.21

Net vs. MSCI World (ex-US) Investable Market Index (net div)

0.84 2.61 6.59 1.43 5.40

2018 2017 2016 2015 2014 2013 2012 2011 2010 2009

n MFS International Intrinsic Value Equity Unrestricted Composite - Gross

-8.46 28.13 4.90 7.51 2.33 29.04 17.21 -0.68 10.60 26.50

n MFS International Intrinsic Value Equity Unrestricted Composite - Net

-9.15 27.20 4.12 6.71 1.56 28.09 16.34 -1.43 9.78 25.57

n MSCI EAFE (Europe, Australasia, Far East) Value Index (net div)

-14.78 21.44 5.02 -5.68 -5.39 22.95 17.69 -12.17 3.25 34.23

n MSCI World (ex-US) Investable Market Index (net div)

-14.68 25.17 2.95 -1.95 -4.45 21.57 16.55 -12.66 10.66 35.35

n MFS International Intrinsic Value Equity UnrestrictedComposite - Grossn MSCI EAFE (Europe, Australasia, Far East) Value Index (net div)

n MFS International Intrinsic Value Equity Unrestricted Composite - Netn MSCI World (ex-US) Investable Market Index (net div)

Please note the composite shown is unrestricted and allows for investment in Emerging Markets and US securities. Source: Benchmark performance from SPAR, FactSet Research Systems Inc. It is not possible to invest directly in an index. Net results reflect the deduction of the highest investment management fee stated in the Institutional Separate Account Fee Schedule. Please see performance methodology and composite report in appendix for performance and other information.Past performance is not a reliable indicator for future results. All financial investments involve an element of risk. The value of investments may rise and fall so you may get back less than originally invested. Investors should consider the risks, including lower returns, related to currency movements between their investing currency and the portfolio's base currency, if different.All periods greater than one year are annualized. Periods less than one year are actual not annualized.

MFS International Intrinsic Value Equity Unrestricted Composite (USD)Performance as of 30 June 2019

4.53 4.34

1.54

3.50

17.43 17.00

9.58

14.39

7.556.75

-2.10

0.16

11.1810.35

8.46 8.92 8.437.62

0.05

2.22

MFS® International Intrinsic Value Equity 29299-I-CT-IIV-02Oct19.29

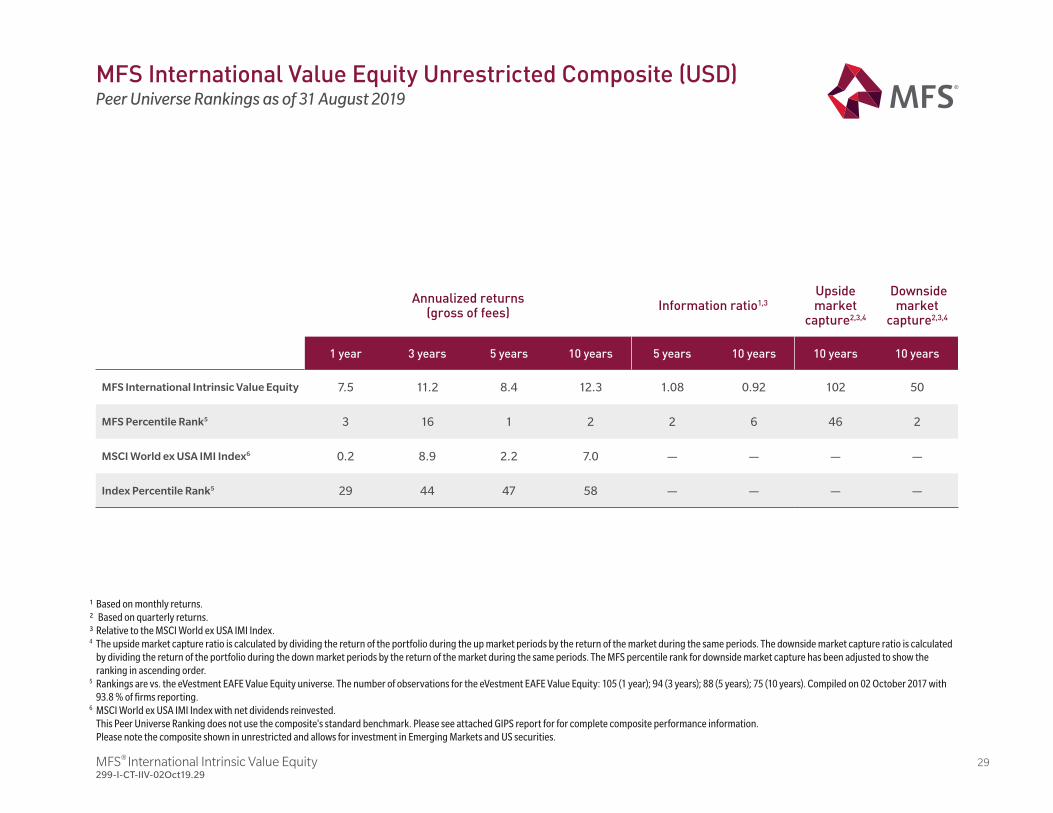

¹ Based on monthly returns.² Based on quarterly returns.³ Relative to the MSCI World ex USA IMI Index.4 The upside market capture ratio is calculated by dividing the return of the portfolio during the up market periods by the return of the market during the same periods. The downside market capture ratio is calculated

by dividing the return of the portfolio during the down market periods by the return of the market during the same periods. The MFS percentile rank for downside market capture has been adjusted to show the ranking in ascending order.

5 Rankings are vs. the eVestment EAFE Value Equity universe. The number of observations for the eVestment EAFE Value Equity: 105 (1 year); 94 (3 years); 88 (5 years); 75 (10 years). Compiled on 02 October 2017 with 93.8 % of firms reporting.

6 MSCI World ex USA IMI Index with net dividends reinvested. This Peer Universe Ranking does not use the composite's standard benchmark. Please see attached GIPS report for for complete composite performance information. Please note the composite shown in unrestricted and allows for investment in Emerging Markets and US securities.

Annualized returns (gross of fees)

Information ratio1,3

Upside market

capture2,3,4

Downside market

capture2,3,4

1 year 3 years 5 years 10 years 5 years 10 years 10 years 10 years

MFS International Intrinsic Value Equity 7.5 11.2 8.4 12.3 1.08 0.92 102 50

MFS Percentile Rank5 3 16 1 2 2 6 46 2

MSCI World ex USA IMI Index6 0.2 8.9 2.2 7.0 — — — —

Index Percentile Rank5 29 44 47 58 — — — —

MFS International Value Equity Unrestricted Composite (USD)Peer Universe Rankings as of 31 August 2019

MFS® International Intrinsic Value Equity 30299-I-CT-IIV-02Oct19.30

Please note the composite shown is unrestricted and allows for investment in Emerging Markets and US securities.

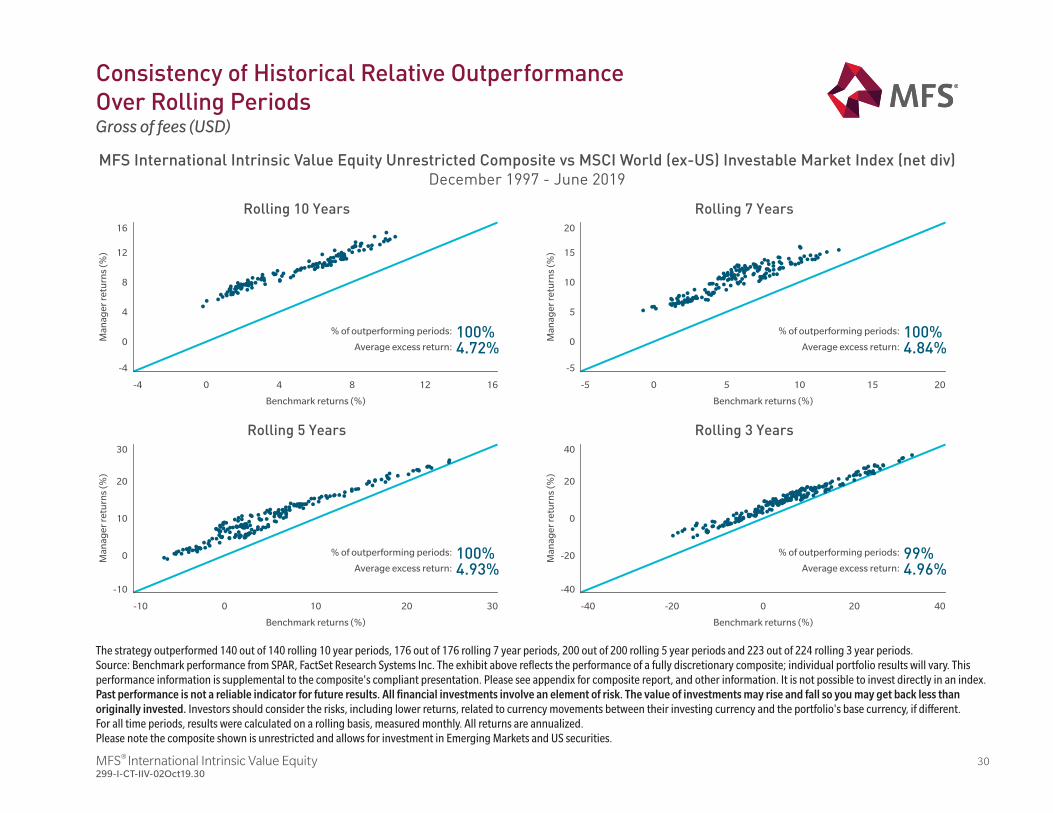

MFS International Intrinsic Value Equity Unrestricted Composite vs MSCI World (ex-US) Investable Market Index (net div)December 1997 - June 2019

Benchmark returns (%)Benchmark returns (%)

Benchmark returns (%)Benchmark returns (%)

Rolling 10 Years

-4 0 4 8 12 16

-4

0

4

8

12

16

Man

ager

ret

urn

s (%

)

Rolling 7 Years

-5 0 5 10 15 20

-5

0

5

10

15

20

Man

ager

ret

urn

s (%

)

Rolling 5 Years

-10 0 10 20 30

-10

0

10

20

30

Man

ager

ret

urn

s (%

)

Rolling 3 Years

-40 -20 0 20 40

-40

-20

0

20

40

Man

ager

ret

urn

s (%

)

% of outperforming periods:

Average excess return:100%4.72%

% of outperforming periods:

Average excess return:100%4.84%

% of outperforming periods:

Average excess return:100%4.93%

% of outperforming periods:

Average excess return:99%4.96%

MFS International Intrinsic Value Equity Composite vs. MSCI World (ex-US) Investable Market Index (net div)December 1997 - June 2019

The strategy outperformed 140 out of 140 rolling 10 year periods, 176 out of 176 rolling 7 year periods, 200 out of 200 rolling 5 year periods and 223 out of 224 rolling 3 year periods.Source: Benchmark performance from SPAR, FactSet Research Systems Inc. The exhibit above reflects the performance of a fully discretionary composite; individual portfolio results will vary. This performance information is supplemental to the composite's compliant presentation. Please see appendix for composite report, and other information. It is not possible to invest directly in an index.Past performance is not a reliable indicator for future results. All financial investments involve an element of risk. The value of investments may rise and fall so you may get back less than originally invested. Investors should consider the risks, including lower returns, related to currency movements between their investing currency and the portfolio's base currency, if different.For all time periods, results were calculated on a rolling basis, measured monthly. All returns are annualized.

Consistency of Historical Relative OutperformanceOver Rolling PeriodsGross of fees (USD)

MFS® International Intrinsic Value Equity 31299-I-CT-IIV-02Oct19.31

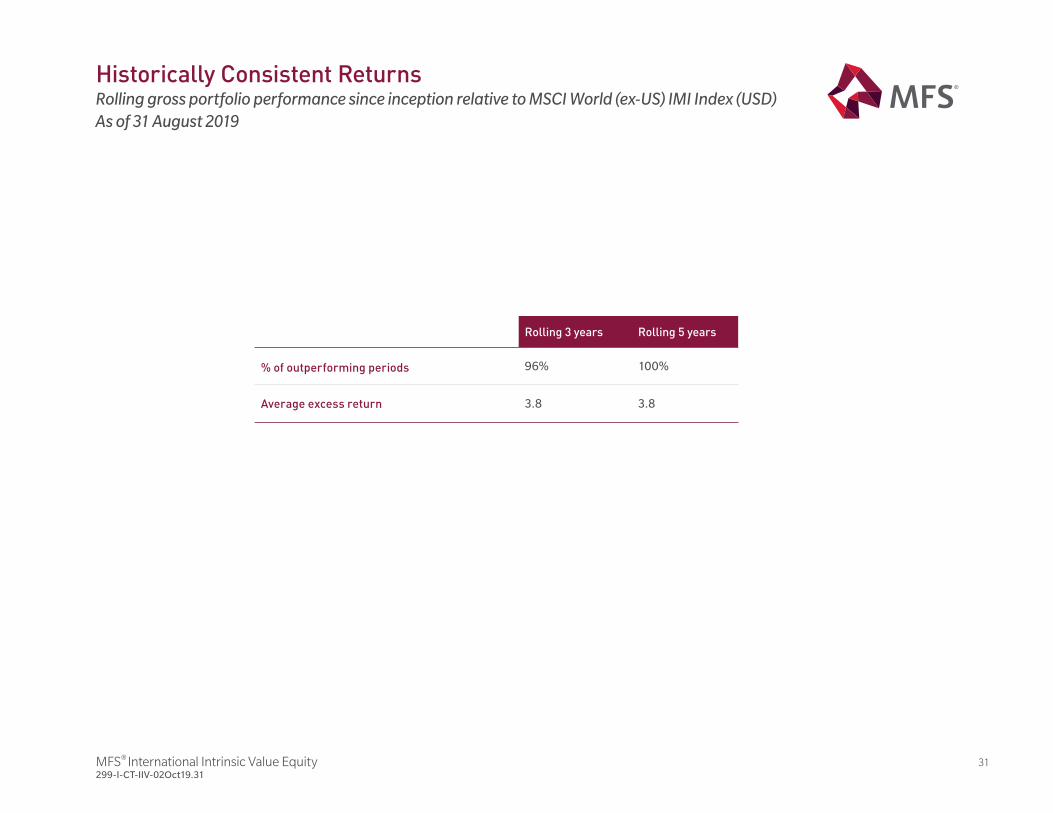

Rolling 3 years Rolling 5 years

% of outperforming periods 96% 100%

Average excess return 3.8 3.8

Historically Consistent ReturnsRolling gross portfolio performance since inception relative to MSCI World (ex-US) IMI Index (USD)As of 31 August 2019

MFS® International Intrinsic Value Equity 32299-I-CT-IIV-02Oct19.32

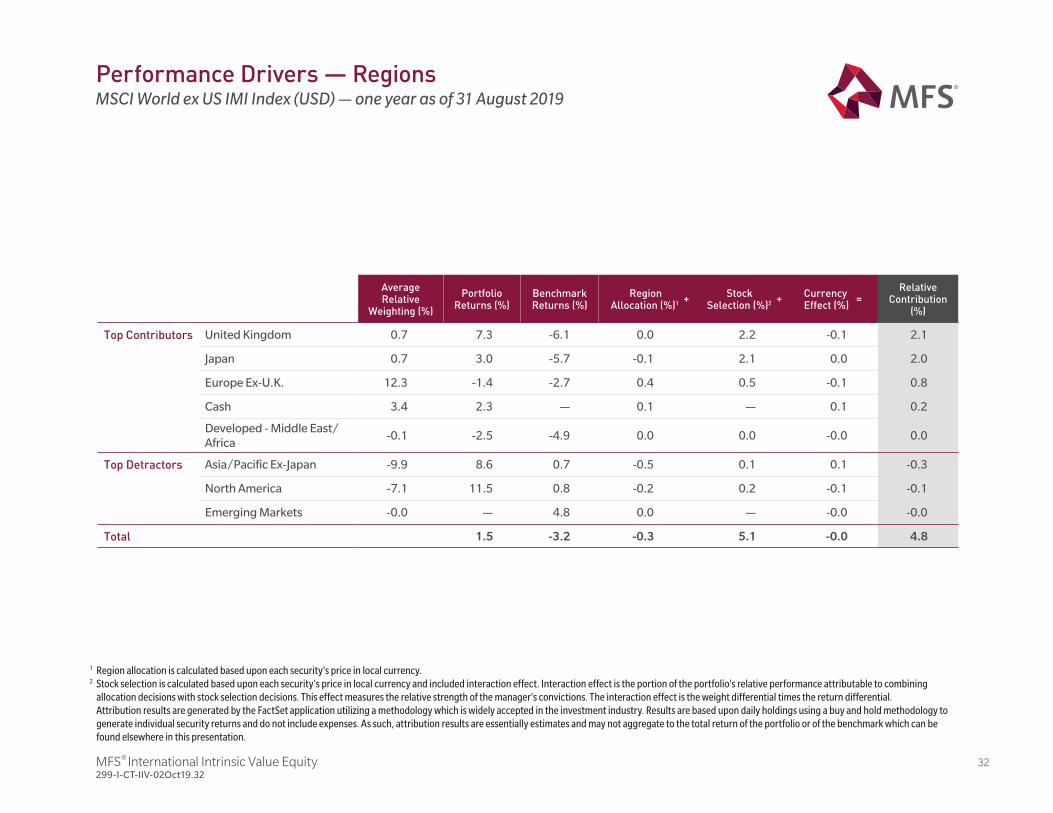

Performance Drivers — RegionsMSCI World ex US IMI Index (USD) — one year as of 31 August 2019

1 Region allocation is calculated based upon each security's price in local currency.2 Stock selection is calculated based upon each security's price in local currency and included interaction effect. Interaction effect is the portion of the portfolio's relative performance attributable to combining

allocation decisions with stock selection decisions. This effect measures the relative strength of the manager's convictions. The interaction effect is the weight differential times the return differential.Attribution results are generated by the FactSet application utilizing a methodology which is widely accepted in the investment industry. Results are based upon daily holdings using a buy and hold methodology to generate individual security returns and do not include expenses. As such, attribution results are essentially estimates and may not aggregate to the total return of the portfolio or of the benchmark which can be found elsewhere in this presentation.

Average Relative

Weighting (%)

Portfolio Returns (%)

Benchmark Returns (%)

Region Allocation (%)1

+ Stock Selection (%)2

+Currency Effect (%)

=Relative

Contribution (%)

Top Contributors United Kingdom 0.7 7.3 -6.1 0.0 2.2 -0.1 2.1

Japan 0.7 3.0 -5.7 -0.1 2.1 0.0 2.0

Europe Ex-U.K. 12.3 -1.4 -2.7 0.4 0.5 -0.1 0.8

Cash 3.4 2.3 — 0.1 — 0.1 0.2

Developed - Middle East/Africa

-0.1 -2.5 -4.9 0.0 0.0 -0.0 0.0

Top Detractors Asia/Pacific Ex-Japan -9.9 8.6 0.7 -0.5 0.1 0.1 -0.3

North America -7.1 11.5 0.8 -0.2 0.2 -0.1 -0.1

Emerging Markets -0.0 — 4.8 0.0 — -0.0 -0.0

Total 1.5 -3.2 -0.3 5.1 -0.0 4.8

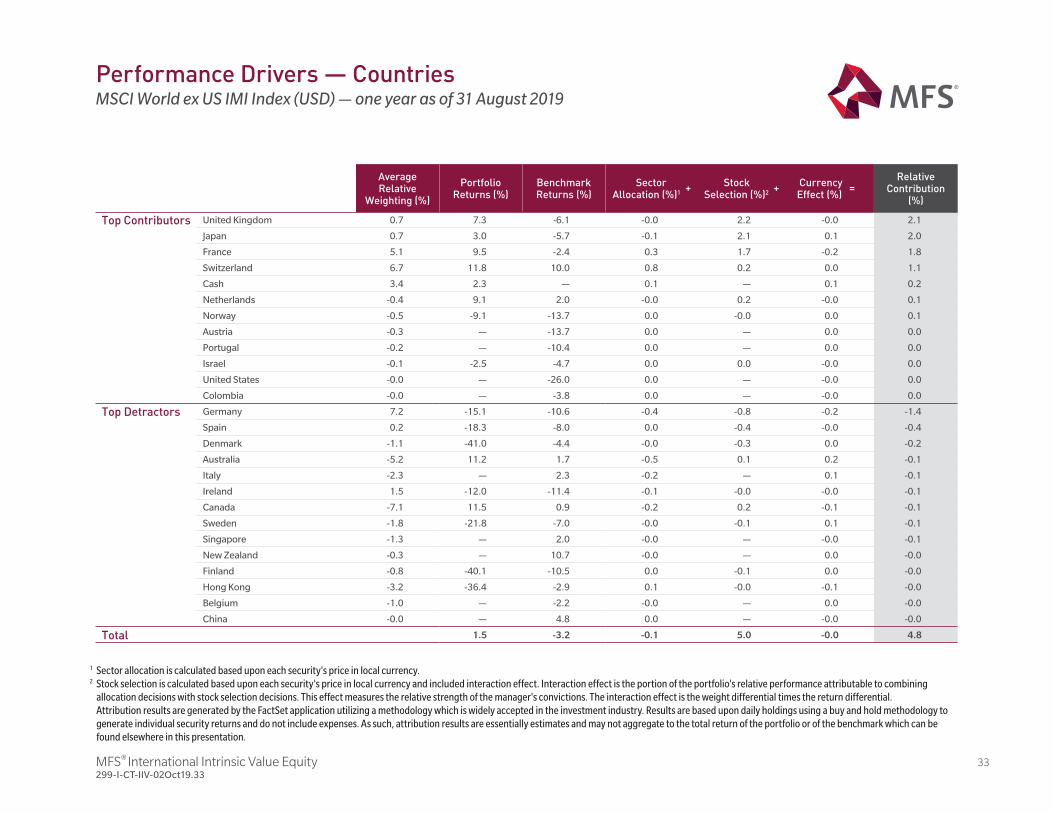

MFS® International Intrinsic Value Equity 33299-I-CT-IIV-02Oct19.33

Average Relative

Weighting (%)

Portfolio Returns (%)

Benchmark Returns (%)

Sector Allocation (%)1

+ Stock Selection (%)2

+ Currency Effect (%)

=Relative

Contribution (%)

Top Contributors United Kingdom 0.7 7.3 -6.1 -0.0 2.2 -0.0 2.1

Japan 0.7 3.0 -5.7 -0.1 2.1 0.1 2.0

France 5.1 9.5 -2.4 0.3 1.7 -0.2 1.8

Switzerland 6.7 11.8 10.0 0.8 0.2 0.0 1.1

Cash 3.4 2.3 — 0.1 — 0.1 0.2

Netherlands -0.4 9.1 2.0 -0.0 0.2 -0.0 0.1

Norway -0.5 -9.1 -13.7 0.0 -0.0 0.0 0.1

Austria -0.3 — -13.7 0.0 — 0.0 0.0

Portugal -0.2 — -10.4 0.0 — 0.0 0.0

Israel -0.1 -2.5 -4.7 0.0 0.0 -0.0 0.0

United States -0.0 — -26.0 0.0 — -0.0 0.0

Colombia -0.0 — -3.8 0.0 — -0.0 0.0

Top Detractors Germany 7.2 -15.1 -10.6 -0.4 -0.8 -0.2 -1.4

Spain 0.2 -18.3 -8.0 0.0 -0.4 -0.0 -0.4

Denmark -1.1 -41.0 -4.4 -0.0 -0.3 0.0 -0.2

Australia -5.2 11.2 1.7 -0.5 0.1 0.2 -0.1

Italy -2.3 — 2.3 -0.2 — 0.1 -0.1

Ireland 1.5 -12.0 -11.4 -0.1 -0.0 -0.0 -0.1

Canada -7.1 11.5 0.9 -0.2 0.2 -0.1 -0.1

Sweden -1.8 -21.8 -7.0 -0.0 -0.1 0.1 -0.1

Singapore -1.3 — 2.0 -0.0 — -0.0 -0.1

New Zealand -0.3 — 10.7 -0.0 — 0.0 -0.0

Finland -0.8 -40.1 -10.5 0.0 -0.1 0.0 -0.0

Hong Kong -3.2 -36.4 -2.9 0.1 -0.0 -0.1 -0.0

Belgium -1.0 — -2.2 -0.0 — 0.0 -0.0

China -0.0 — 4.8 0.0 — -0.0 -0.0

Total 1.5 -3.2 -0.1 5.0 -0.0 4.8

Performance Drivers — CountriesMSCI World ex US IMI Index (USD) — one year as of 31 August 2019

1 Sector allocation is calculated based upon each security's price in local currency.2 Stock selection is calculated based upon each security's price in local currency and included interaction effect. Interaction effect is the portion of the portfolio's relative performance attributable to combining

allocation decisions with stock selection decisions. This effect measures the relative strength of the manager's convictions. The interaction effect is the weight differential times the return differential.Attribution results are generated by the FactSet application utilizing a methodology which is widely accepted in the investment industry. Results are based upon daily holdings using a buy and hold methodology to generate individual security returns and do not include expenses. As such, attribution results are essentially estimates and may not aggregate to the total return of the portfolio or of the benchmark which can be found elsewhere in this presentation.

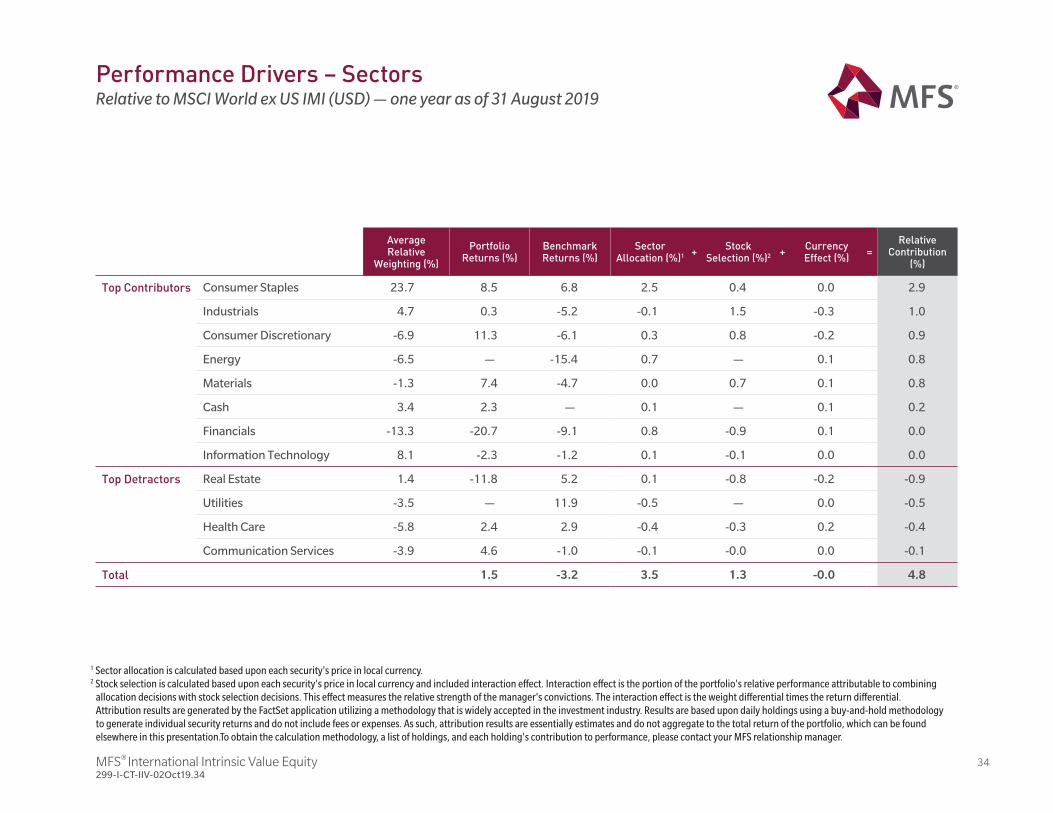

MFS® International Intrinsic Value Equity 34299-I-CT-IIV-02Oct19.34

Average Relative

Weighting (%)

Portfolio Returns (%)

Benchmark Returns (%)

Sector Allocation (%)1 +

Stock Selection (%)2 +

Currency Effect (%)

=Relative

Contribution (%)

Top Contributors Consumer Staples 23.7 8.5 6.8 2.5 0.4 0.0 2.9

Industrials 4.7 0.3 -5.2 -0.1 1.5 -0.3 1.0

Consumer Discretionary -6.9 11.3 -6.1 0.3 0.8 -0.2 0.9

Energy -6.5 — -15.4 0.7 — 0.1 0.8

Materials -1.3 7.4 -4.7 0.0 0.7 0.1 0.8

Cash 3.4 2.3 — 0.1 — 0.1 0.2

Financials -13.3 -20.7 -9.1 0.8 -0.9 0.1 0.0

Information Technology 8.1 -2.3 -1.2 0.1 -0.1 0.0 0.0

Top Detractors Real Estate 1.4 -11.8 5.2 0.1 -0.8 -0.2 -0.9

Utilities -3.5 — 11.9 -0.5 — 0.0 -0.5

Health Care -5.8 2.4 2.9 -0.4 -0.3 0.2 -0.4

Communication Services -3.9 4.6 -1.0 -0.1 -0.0 0.0 -0.1

Total 1.5 -3.2 3.5 1.3 -0.0 4.8

1 Sector allocation is calculated based upon each security's price in local currency.2 Stock selection is calculated based upon each security's price in local currency and included interaction effect. Interaction effect is the portion of the portfolio's relative performance attributable to combining

allocation decisions with stock selection decisions. This effect measures the relative strength of the manager's convictions. The interaction effect is the weight differential times the return differential.Attribution results are generated by the FactSet application utilizing a methodology that is widely accepted in the investment industry. Results are based upon daily holdings using a buy-and-hold methodology to generate individual security returns and do not include fees or expenses. As such, attribution results are essentially estimates and do not aggregate to the total return of the portfolio, which can be found elsewhere in this presentation.To obtain the calculation methodology, a list of holdings, and each holding's contribution to performance, please contact your MFS relationship manager.

Performance Drivers – SectorsRelative to MSCI World ex US IMI (USD) — one year as of 31 August 2019

MFS® International Intrinsic Value Equity 35299-I-CT-IIV-02Oct19.35

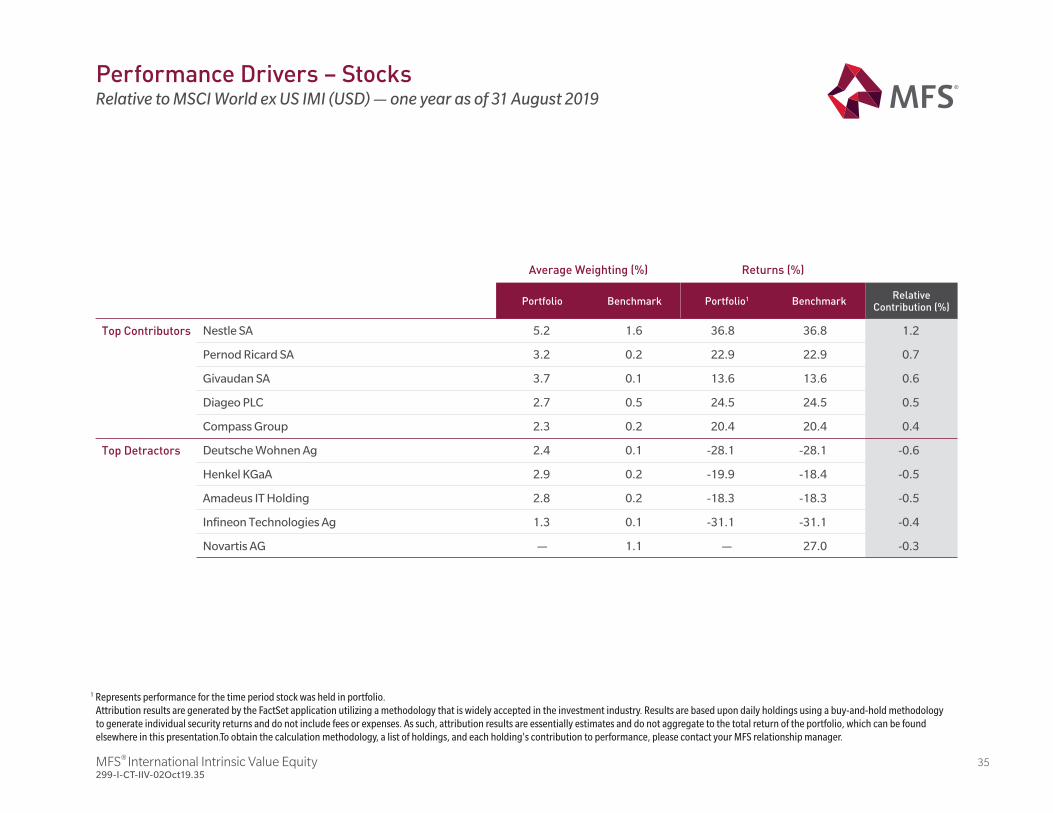

Average Weighting (%) Returns (%)

Portfolio Benchmark Portfolio1 BenchmarkRelative

Contribution (%)

Top Contributors Nestle SA 5.2 1.6 36.8 36.8 1.2

Pernod Ricard SA 3.2 0.2 22.9 22.9 0.7

Givaudan SA 3.7 0.1 13.6 13.6 0.6

Diageo PLC 2.7 0.5 24.5 24.5 0.5

Compass Group 2.3 0.2 20.4 20.4 0.4

Top Detractors Deutsche Wohnen Ag 2.4 0.1 -28.1 -28.1 -0.6

Henkel KGaA 2.9 0.2 -19.9 -18.4 -0.5

Amadeus IT Holding 2.8 0.2 -18.3 -18.3 -0.5

Infineon Technologies Ag 1.3 0.1 -31.1 -31.1 -0.4

Novartis AG — 1.1 — 27.0 -0.3

1 Represents performance for the time period stock was held in portfolio.Attribution results are generated by the FactSet application utilizing a methodology that is widely accepted in the investment industry. Results are based upon daily holdings using a buy-and-hold methodology to generate individual security returns and do not include fees or expenses. As such, attribution results are essentially estimates and do not aggregate to the total return of the portfolio, which can be found elsewhere in this presentation.To obtain the calculation methodology, a list of holdings, and each holding's contribution to performance, please contact your MFS relationship manager.

Performance Drivers – StocksRelative to MSCI World ex US IMI (USD) — one year as of 31 August 2019

Portfolio Review and Characteristics

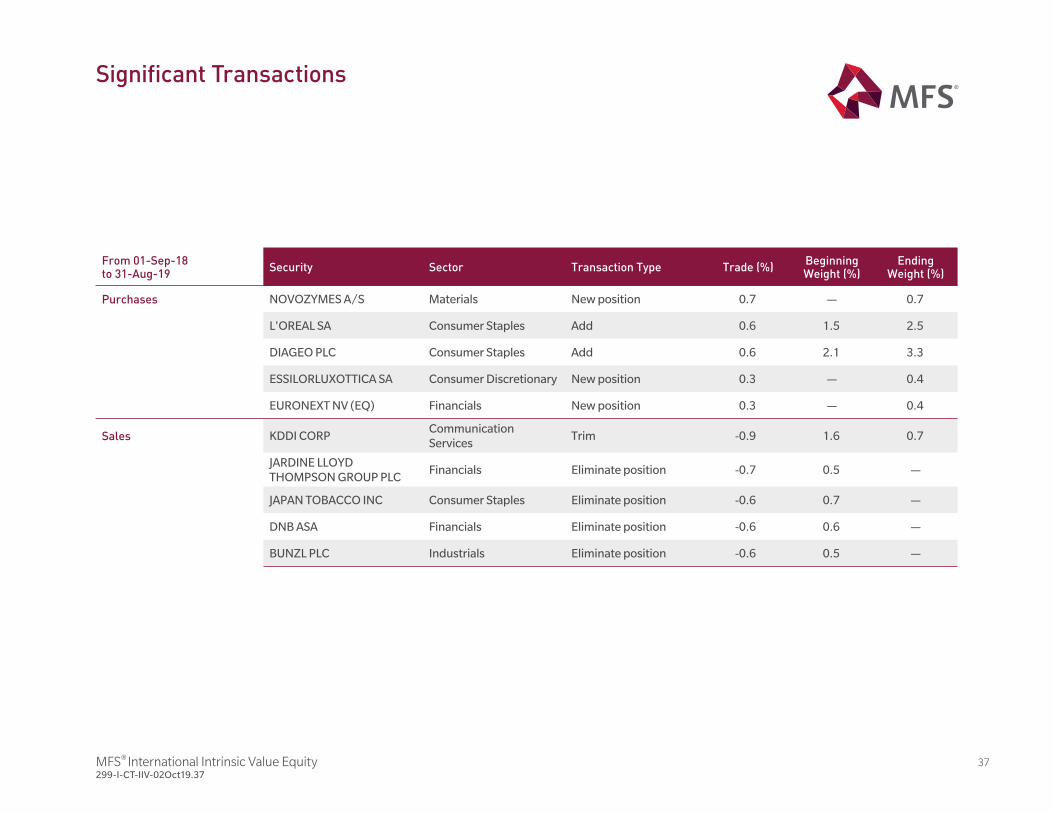

MFS® International Intrinsic Value Equity 37299-I-CT-IIV-02Oct19.37

From 01-Sep-18to 31-Aug-19

Security Sector Transaction Type Trade (%)Beginning Weight (%)

Ending Weight (%)

Purchases NOVOZYMES A/S Materials New position 0.7 — 0.7

L'OREAL SA Consumer Staples Add 0.6 1.5 2.5

DIAGEO PLC Consumer Staples Add 0.6 2.1 3.3

ESSILORLUXOTTICA SA Consumer Discretionary New position 0.3 — 0.4

EURONEXT NV (EQ) Financials New position 0.3 — 0.4

Sales KDDI CORPCommunication Services

Trim -0.9 1.6 0.7

JARDINE LLOYD THOMPSON GROUP PLC

Financials Eliminate position -0.7 0.5 —

JAPAN TOBACCO INC Consumer Staples Eliminate position -0.6 0.7 —

DNB ASA Financials Eliminate position -0.6 0.6 —

BUNZL PLC Industrials Eliminate position -0.6 0.5 —

Significant Transactions

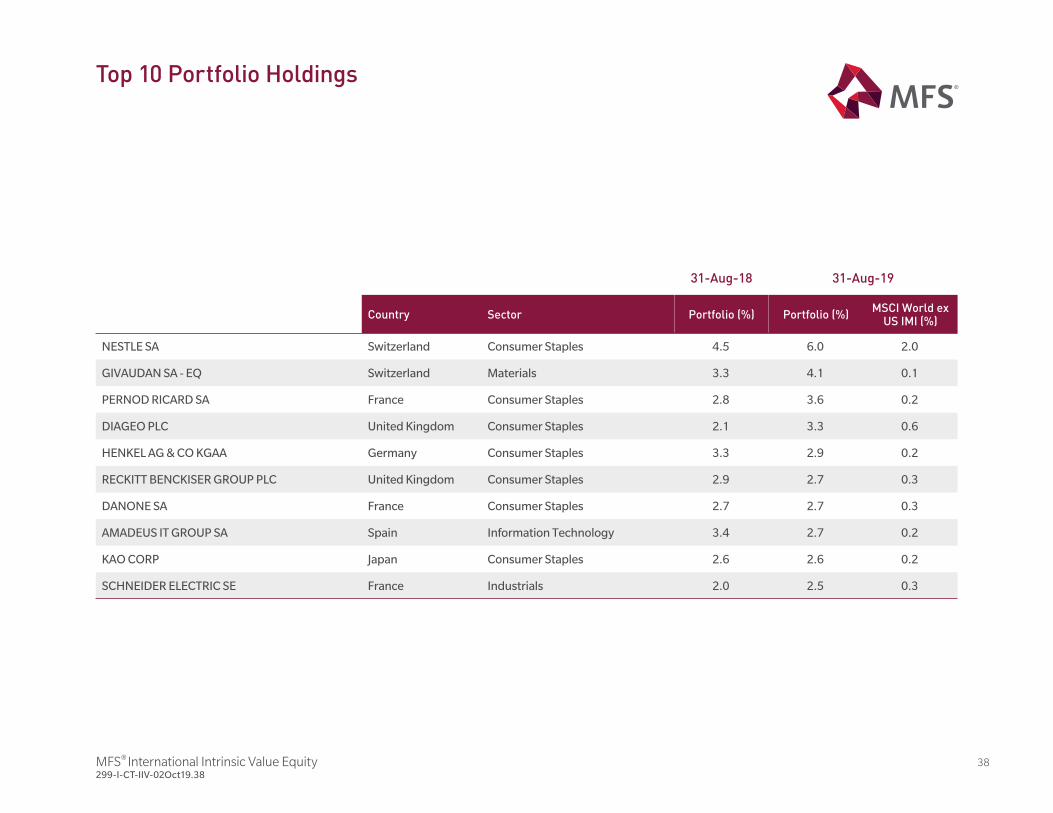

MFS® International Intrinsic Value Equity 38299-I-CT-IIV-02Oct19.38

31-Aug-18 31-Aug-19

Country Sector Portfolio (%) Portfolio (%)MSCI World ex

US IMI (%)

NESTLE SA Switzerland Consumer Staples 4.5 6.0 2.0

GIVAUDAN SA - EQ Switzerland Materials 3.3 4.1 0.1

PERNOD RICARD SA France Consumer Staples 2.8 3.6 0.2

DIAGEO PLC United Kingdom Consumer Staples 2.1 3.3 0.6

HENKEL AG & CO KGAA Germany Consumer Staples 3.3 2.9 0.2

RECKITT BENCKISER GROUP PLC United Kingdom Consumer Staples 2.9 2.7 0.3

DANONE SA France Consumer Staples 2.7 2.7 0.3

AMADEUS IT GROUP SA Spain Information Technology 3.4 2.7 0.2

KAO CORP Japan Consumer Staples 2.6 2.6 0.2

SCHNEIDER ELECTRIC SE France Industrials 2.0 2.5 0.3

Top 10 Portfolio Holdings

MFS® International Intrinsic Value Equity 39299-I-CT-IIV-02Oct19.39

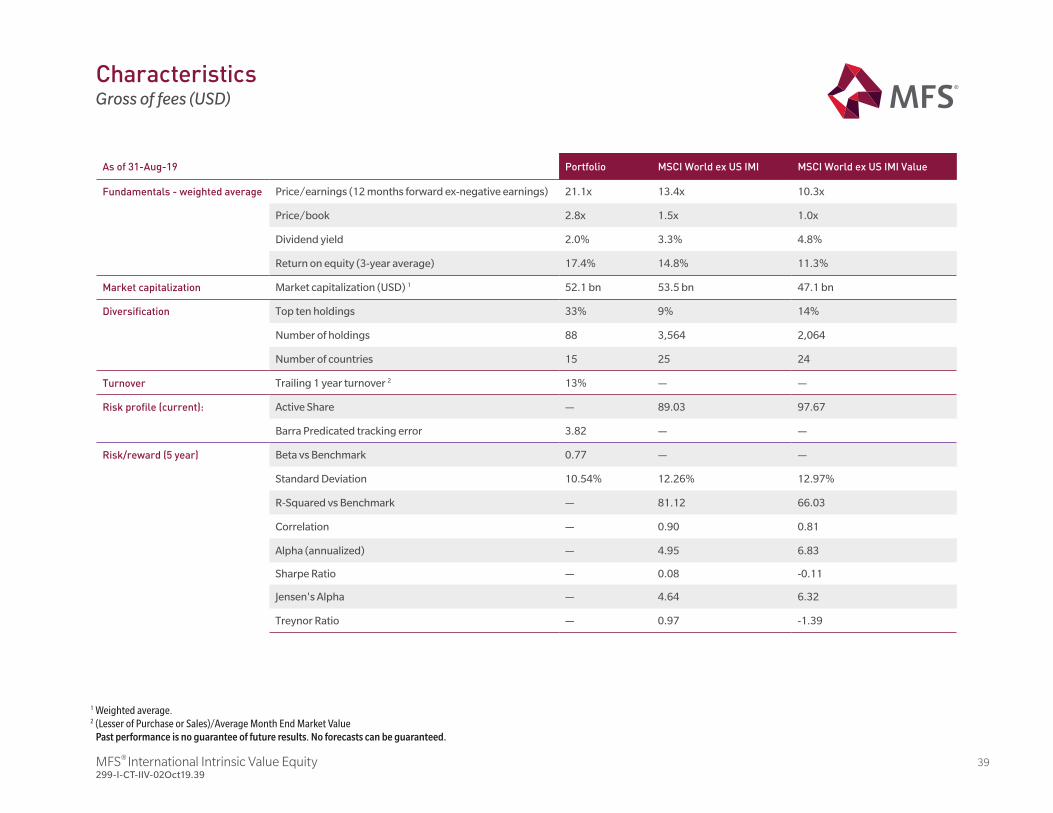

CharacteristicsGross of fees (USD)

1 Weighted average.2 (Lesser of Purchase or Sales)/Average Month End Market Value

Past performance is no guarantee of future results. No forecasts can be guaranteed.

As of 31-Aug-19 Portfolio MSCI World ex US IMI MSCI World ex US IMI Value

Fundamentals - weighted average Price/earnings (12 months forward ex-negative earnings) 21.1x 13.4x 10.3x

Price/book 2.8x 1.5x 1.0x

Dividend yield 2.0% 3.3% 4.8%

Return on equity (3-year average) 17.4% 14.8% 11.3%

Market capitalization Market capitalization (USD) 1 52.1 bn 53.5 bn 47.1 bn

Diversification Top ten holdings 33% 9% 14%

Number of holdings 88 3,564 2,064

Number of countries 15 25 24

Turnover Trailing 1 year turnover 2 13% — —

Risk profile (current): Active Share — 89.03 97.67

Barra Predicated tracking error 3.82 — —

Risk/reward (5 year) Beta vs Benchmark 0.77 — —

Standard Deviation 10.54% 12.26% 12.97%

R-Squared vs Benchmark — 81.12 66.03

Correlation — 0.90 0.81

Alpha (annualized) — 4.95 6.83

Sharpe Ratio — 0.08 -0.11

Jensen's Alpha — 4.64 6.32

Treynor Ratio — 0.97 -1.39

MFS® International Intrinsic Value Equity 40299-I-CT-IIV-02Oct19.40

NorthAmerica

Europeex-U.K.

UnitedKingdom

Developed –Middle East/

Africa

Japan Asia PacificEx-Japan

EmergingMarkets

OtherCountries

Perc

ent (

%)

-7.2

-1.7

12.4

1.3 1.0

-0.7

0.0

-0.2

0.5

3.7

-10.2

-7.6

0.0

4.9

0.00.5

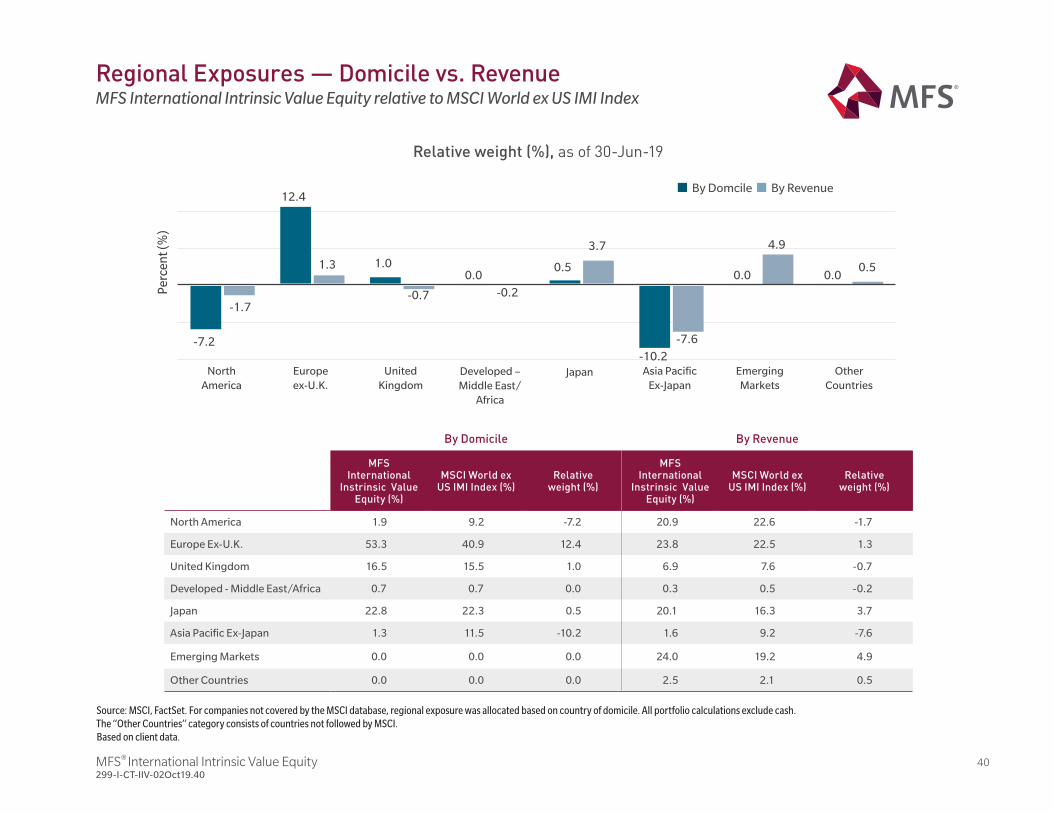

Regional Exposures — Domicile vs. RevenueMFS International Intrinsic Value Equity relative to MSCI World ex US IMI Index

Source: MSCI, FactSet. For companies not covered by the MSCI database, regional exposure was allocated based on country of domicile. All portfolio calculations exclude cash.The “Other Countries” category consists of countries not followed by MSCI.Based on client data.

By Domicile By Revenue

MFS International

Instrinsic Value Equity (%)

MSCI World ex US IMI Index (%)

Relative weight (%)

MFS International

Instrinsic Value Equity (%)

MSCI World ex US IMI Index (%)

Relative weight (%)

North America 1.9 9.2 -7.2 20.9 22.6 -1.7

Europe Ex-U.K. 53.3 40.9 12.4 23.8 22.5 1.3

United Kingdom 16.5 15.5 1.0 6.9 7.6 -0.7

Developed - Middle East/Africa 0.7 0.7 0.0 0.3 0.5 -0.2

Japan 22.8 22.3 0.5 20.1 16.3 3.7

Asia Pacific Ex-Japan 1.3 11.5 -10.2 1.6 9.2 -7.6

Emerging Markets 0.0 0.0 0.0 24.0 19.2 4.9

Other Countries 0.0 0.0 0.0 2.5 2.1 0.5

Relative weight (%), as of 30-Jun-19

By RevenueBy Domcile

MFS® International Intrinsic Value Equity 41299-I-CT-IIV-02Oct19.41

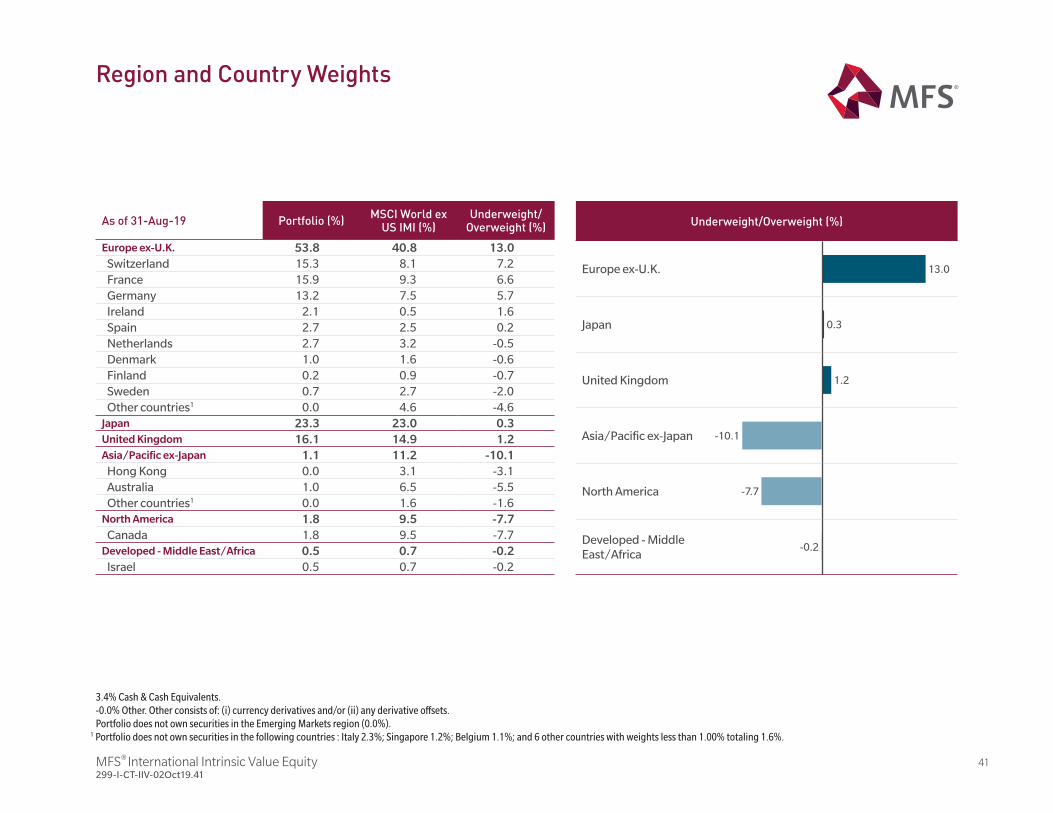

As of 31-Aug-19 Portfolio (%)MSCI World ex

US IMI (%)Underweight/

Overweight (%)

Europe ex-U.K. 53.8 40.8 13.0

Switzerland 15.3 8.1 7.2France 15.9 9.3 6.6Germany 13.2 7.5 5.7Ireland 2.1 0.5 1.6Spain 2.7 2.5 0.2Netherlands 2.7 3.2 -0.5Denmark 1.0 1.6 -0.6Finland 0.2 0.9 -0.7Sweden 0.7 2.7 -2.0Other countries1 0.0 4.6 -4.6

Japan 23.3 23.0 0.3

United Kingdom 16.1 14.9 1.2

Asia/Pacific ex-Japan 1.1 11.2 -10.1

Hong Kong 0.0 3.1 -3.1Australia 1.0 6.5 -5.5Other countries1 0.0 1.6 -1.6

North America 1.8 9.5 -7.7

Canada 1.8 9.5 -7.7Developed - Middle East/Africa 0.5 0.7 -0.2

Israel 0.5 0.7 -0.2

Underweight/Overweight (%)

Europe ex-U.K. 13.0

Japan 0.3

United Kingdom 1.2

Asia/Pacific ex-Japan -10.1

North America -7.7

Developed - Middle East/Africa

-0.2

3.4% Cash & Cash Equivalents.-0.0% Other. Other consists of: (i) currency derivatives and/or (ii) any derivative offsets.Portfolio does not own securities in the Emerging Markets region (0.0%).

1 Portfolio does not own securities in the following countries : Italy 2.3%; Singapore 1.2%; Belgium 1.1%; and 6 other countries with weights less than 1.00% totaling 1.6%.

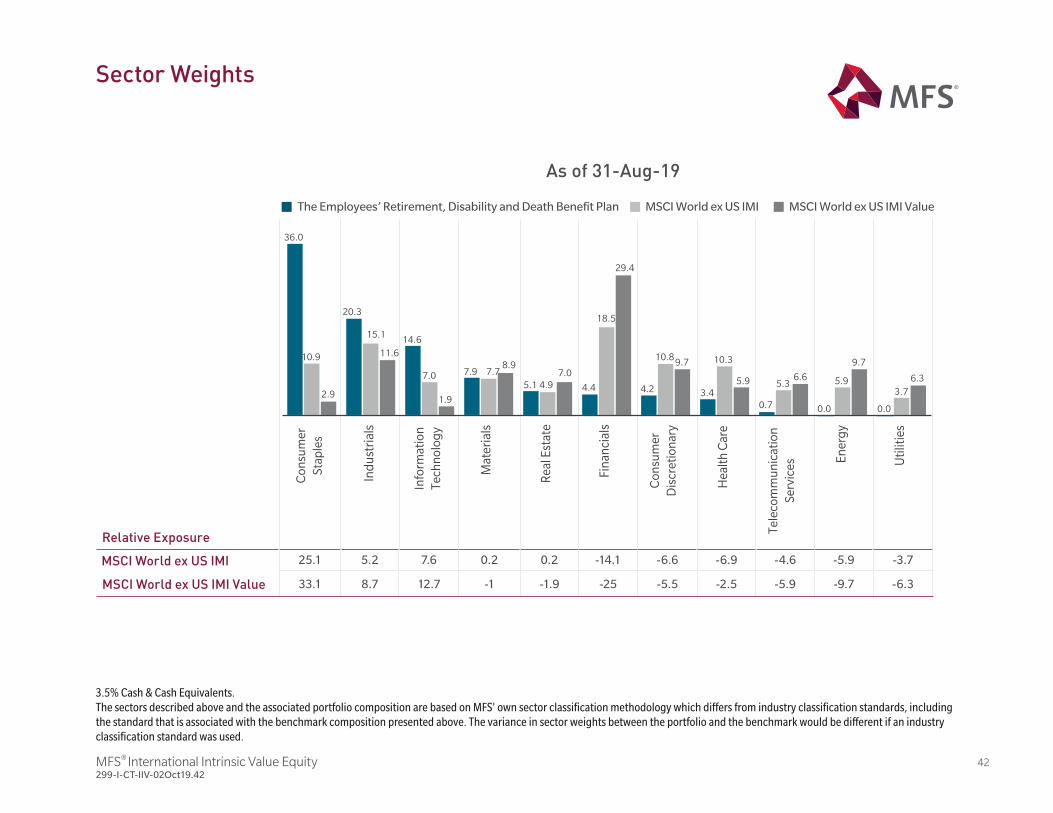

Region and Country Weights

42

Relative Exposure

MSCI World ex US IMI 25.1 5.2 7.6 0.2 0.2 -14.1 -6.6 -6.9 -4.6 -5.9 -3.7

MSCI World ex US IMI Value 33.1 8.7 12.7 -1 -1.9 -25 -5.5 -2.5 -5.9 -9.7 -6.3

Co

nsu

me

r

Sta

ple

s

Ind

ust

ria

ls

Info

rma

tio

n

Te

ch

no

log

y

Ma

teri

als

Re

al E

sta

te

Fin

an

cia

ls

Co

nsu

me

r

Dis

cre

tio

na

ry

He

alt

h C

are

Te

lec

om

mu

nic

ati

on

Se

rvic

es E

ne

rgy

Uti

litie

s

36.0

10.9

2.9

20.3

15.1

11.6

14.6

7.0

1.9

7.9 7.78.9

5.1 4.9

7.0

4.4

18.5

29.4

4.2

10.89.7

3.4

10.3

5.9

0.7

5.36.6

0.0

5.9

9.7

0.0

3.7

6.3

Sector Weights

3.5% Cash & Cash Equivalents.The sectors described above and the associated portfolio composition are based on MFS own sector classification methodology which differs from industry classification standards, including the standard that is associated with the benchmark composition presented above. The variance in sector weights between the portfolio and the benchmark would be different if an industry classification standard was used.

MFS® International Intrinsic Value Equity 299-I-CT-IIV-02Oct19.42

As of 31-Aug-19

The Employees’ Retirement, Disability and Death Benefit Plan MSCI World ex US IMI MSCI World ex US IMI Value

MFS® International Intrinsic Value Equity 43299-I-CT-IIV-02Oct19.43

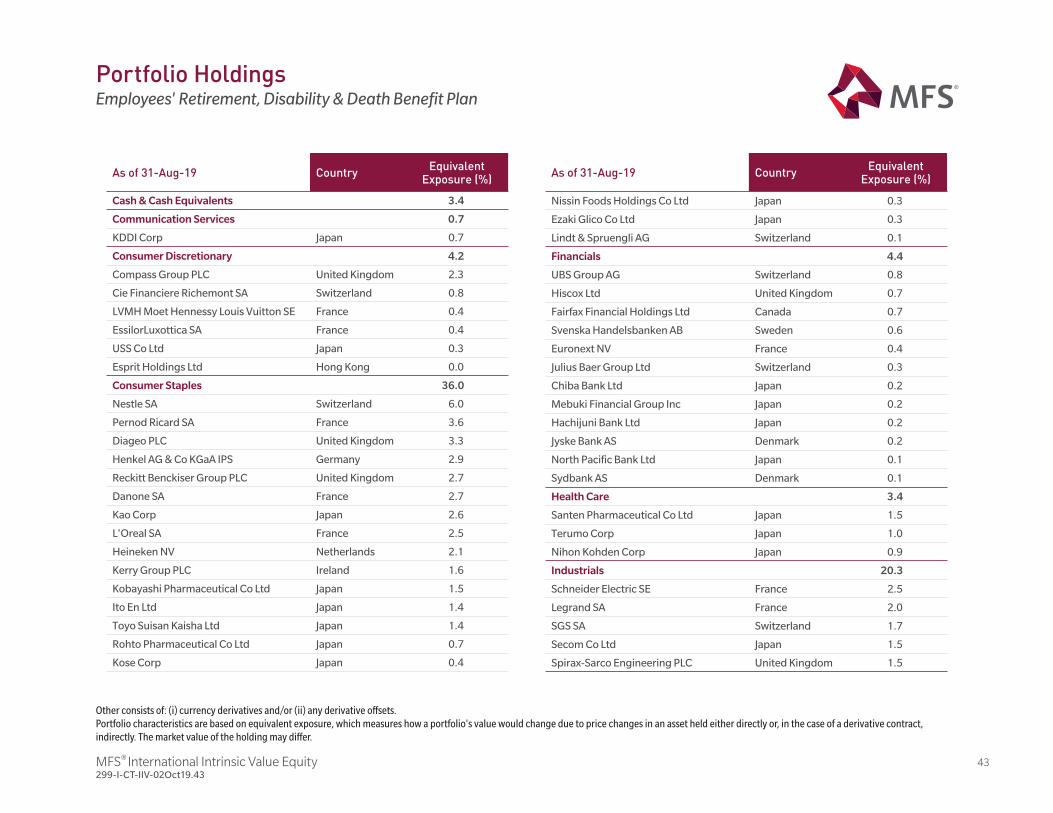

Portfolio Holdings Employees' Retirement, Disability & Death Benefit Plan

As of 31-Aug-19 CountryEquivalent

Exposure (%)

Cash & Cash Equivalents 3.4

Communication Services 0.7

KDDI Corp Japan 0.7

Consumer Discretionary 4.2

Compass Group PLC United Kingdom 2.3

Cie Financiere Richemont SA Switzerland 0.8

LVMH Moet Hennessy Louis Vuitton SE France 0.4

EssilorLuxottica SA France 0.4

USS Co Ltd Japan 0.3

Esprit Holdings Ltd Hong Kong 0.0

Consumer Staples 36.0

Nestle SA Switzerland 6.0

Pernod Ricard SA France 3.6

Diageo PLC United Kingdom 3.3

Henkel AG & Co KGaA IPS Germany 2.9

Reckitt Benckiser Group PLC United Kingdom 2.7

Danone SA France 2.7

Kao Corp Japan 2.6

L'Oreal SA France 2.5

Heineken NV Netherlands 2.1

Kerry Group PLC Ireland 1.6

Kobayashi Pharmaceutical Co Ltd Japan 1.5

Ito En Ltd Japan 1.4

Toyo Suisan Kaisha Ltd Japan 1.4

Rohto Pharmaceutical Co Ltd Japan 0.7

Kose Corp Japan 0.4

As of 31-Aug-19 CountryEquivalent

Exposure (%)

Nissin Foods Holdings Co Ltd Japan 0.3

Ezaki Glico Co Ltd Japan 0.3

Lindt & Spruengli AG Switzerland 0.1

Financials 4.4

UBS Group AG Switzerland 0.8

Hiscox Ltd United Kingdom 0.7

Fairfax Financial Holdings Ltd Canada 0.7

Svenska Handelsbanken AB Sweden 0.6

Euronext NV France 0.4

Julius Baer Group Ltd Switzerland 0.3

Chiba Bank Ltd Japan 0.2

Mebuki Financial Group Inc Japan 0.2

Hachijuni Bank Ltd Japan 0.2

Jyske Bank AS Denmark 0.2

North Pacific Bank Ltd Japan 0.1

Sydbank AS Denmark 0.1

Health Care 3.4

Santen Pharmaceutical Co Ltd Japan 1.5

Terumo Corp Japan 1.0

Nihon Kohden Corp Japan 0.9

Industrials 20.3

Schneider Electric SE France 2.5

Legrand SA France 2.0

SGS SA Switzerland 1.7

Secom Co Ltd Japan 1.5

Spirax-Sarco Engineering PLC United Kingdom 1.5

Other consists of: (i) currency derivatives and/or (ii) any derivative offsets.Portfolio characteristics are based on equivalent exposure, which measures how a portfolio's value would change due to price changes in an asset held either directly or, in the case of a derivative contract, indirectly. The market value of the holding may differ.

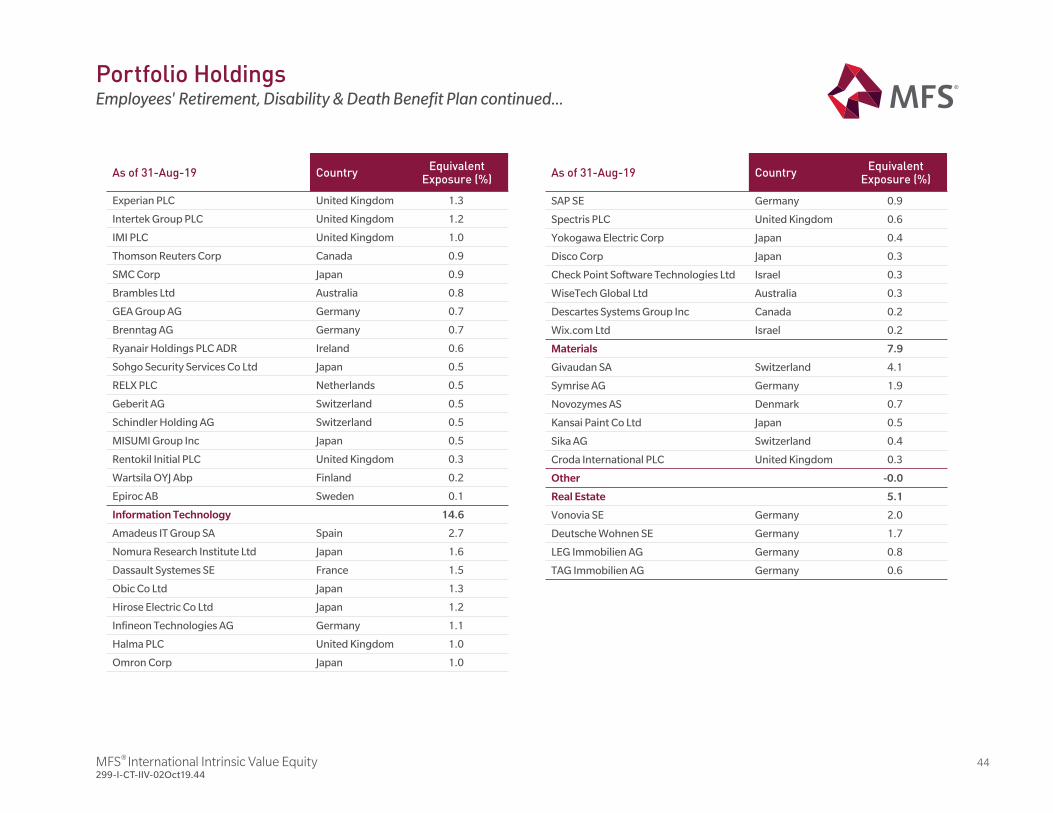

MFS® International Intrinsic Value Equity 44299-I-CT-IIV-02Oct19.44

As of 31-Aug-19 CountryEquivalent

Exposure (%)

Experian PLC United Kingdom 1.3

Intertek Group PLC United Kingdom 1.2

IMI PLC United Kingdom 1.0

Thomson Reuters Corp Canada 0.9

SMC Corp Japan 0.9

Brambles Ltd Australia 0.8

GEA Group AG Germany 0.7

Brenntag AG Germany 0.7

Ryanair Holdings PLC ADR Ireland 0.6

Sohgo Security Services Co Ltd Japan 0.5

RELX PLC Netherlands 0.5

Geberit AG Switzerland 0.5

Schindler Holding AG Switzerland 0.5

MISUMI Group Inc Japan 0.5

Rentokil Initial PLC United Kingdom 0.3

Wartsila OYJ Abp Finland 0.2

Epiroc AB Sweden 0.1

Information Technology 14.6

Amadeus IT Group SA Spain 2.7

Nomura Research Institute Ltd Japan 1.6

Dassault Systemes SE France 1.5

Obic Co Ltd Japan 1.3

Hirose Electric Co Ltd Japan 1.2

Infineon Technologies AG Germany 1.1

Halma PLC United Kingdom 1.0

Omron Corp Japan 1.0

As of 31-Aug-19 CountryEquivalent

Exposure (%)

SAP SE Germany 0.9

Spectris PLC United Kingdom 0.6

Yokogawa Electric Corp Japan 0.4

Disco Corp Japan 0.3

Check Point Software Technologies Ltd Israel 0.3

WiseTech Global Ltd Australia 0.3

Descartes Systems Group Inc Canada 0.2

Wix.com Ltd Israel 0.2

Materials 7.9

Givaudan SA Switzerland 4.1

Symrise AG Germany 1.9

Novozymes AS Denmark 0.7

Kansai Paint Co Ltd Japan 0.5

Sika AG Switzerland 0.4

Croda International PLC United Kingdom 0.3

Other -0.0

Real Estate 5.1

Vonovia SE Germany 2.0

Deutsche Wohnen SE Germany 1.7

LEG Immobilien AG Germany 0.8

TAG Immobilien AG Germany 0.6

Portfolio Holdings Employees' Retirement, Disability & Death Benefit Plan continued...

MFS® International Intrinsic Value Equity 45299-I-CT-IIV-02Oct19.45

Other consists of: (i) currency derivatives and/or (ii) any derivative offsets.Portfolio characteristics are based on equivalent exposure, which measures how a portfolio's value would change due to price changes in an asset held either directly or, in the case of a derivative contract, indirectly. The market value of the holding may differ.

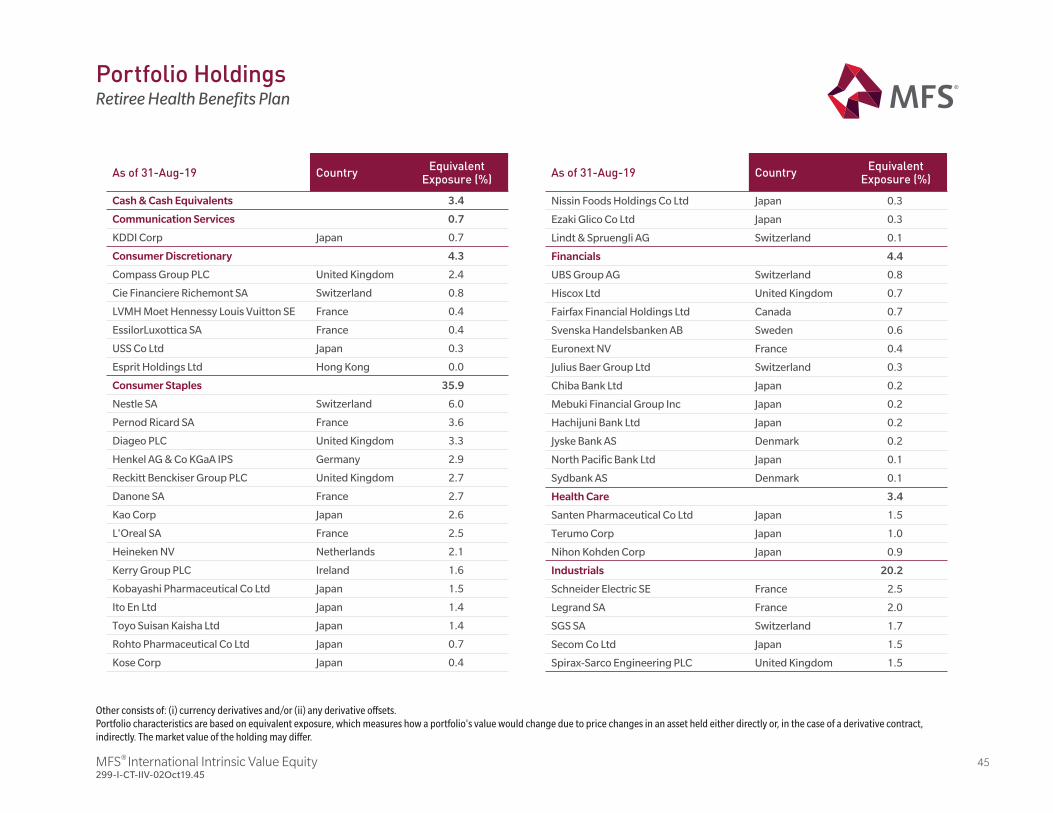

Portfolio HoldingsRetiree Health Benefits Plan

As of 31-Aug-19 CountryEquivalent

Exposure (%)

Cash & Cash Equivalents 3.4

Communication Services 0.7

KDDI Corp Japan 0.7

Consumer Discretionary 4.3

Compass Group PLC United Kingdom 2.4

Cie Financiere Richemont SA Switzerland 0.8

LVMH Moet Hennessy Louis Vuitton SE France 0.4

EssilorLuxottica SA France 0.4

USS Co Ltd Japan 0.3

Esprit Holdings Ltd Hong Kong 0.0

Consumer Staples 35.9

Nestle SA Switzerland 6.0

Pernod Ricard SA France 3.6

Diageo PLC United Kingdom 3.3

Henkel AG & Co KGaA IPS Germany 2.9

Reckitt Benckiser Group PLC United Kingdom 2.7

Danone SA France 2.7

Kao Corp Japan 2.6

L'Oreal SA France 2.5

Heineken NV Netherlands 2.1

Kerry Group PLC Ireland 1.6

Kobayashi Pharmaceutical Co Ltd Japan 1.5

Ito En Ltd Japan 1.4

Toyo Suisan Kaisha Ltd Japan 1.4

Rohto Pharmaceutical Co Ltd Japan 0.7

Kose Corp Japan 0.4

As of 31-Aug-19 CountryEquivalent

Exposure (%)

Nissin Foods Holdings Co Ltd Japan 0.3

Ezaki Glico Co Ltd Japan 0.3

Lindt & Spruengli AG Switzerland 0.1

Financials 4.4

UBS Group AG Switzerland 0.8

Hiscox Ltd United Kingdom 0.7

Fairfax Financial Holdings Ltd Canada 0.7

Svenska Handelsbanken AB Sweden 0.6

Euronext NV France 0.4

Julius Baer Group Ltd Switzerland 0.3

Chiba Bank Ltd Japan 0.2

Mebuki Financial Group Inc Japan 0.2

Hachijuni Bank Ltd Japan 0.2

Jyske Bank AS Denmark 0.2

North Pacific Bank Ltd Japan 0.1

Sydbank AS Denmark 0.1

Health Care 3.4

Santen Pharmaceutical Co Ltd Japan 1.5

Terumo Corp Japan 1.0

Nihon Kohden Corp Japan 0.9

Industrials 20.2

Schneider Electric SE France 2.5

Legrand SA France 2.0

SGS SA Switzerland 1.7

Secom Co Ltd Japan 1.5

Spirax-Sarco Engineering PLC United Kingdom 1.5

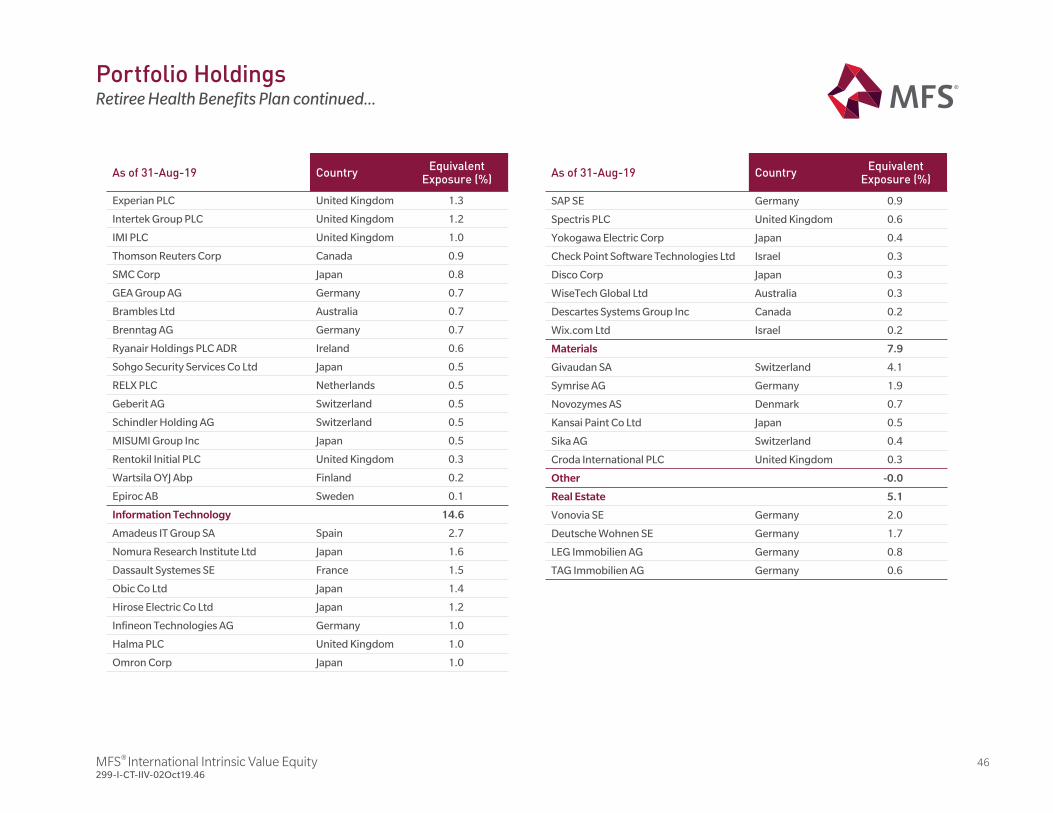

MFS® International Intrinsic Value Equity 46299-I-CT-IIV-02Oct19.46

As of 31-Aug-19 CountryEquivalent

Exposure (%)

Experian PLC United Kingdom 1.3

Intertek Group PLC United Kingdom 1.2

IMI PLC United Kingdom 1.0

Thomson Reuters Corp Canada 0.9

SMC Corp Japan 0.8

GEA Group AG Germany 0.7

Brambles Ltd Australia 0.7

Brenntag AG Germany 0.7

Ryanair Holdings PLC ADR Ireland 0.6

Sohgo Security Services Co Ltd Japan 0.5

RELX PLC Netherlands 0.5

Geberit AG Switzerland 0.5

Schindler Holding AG Switzerland 0.5

MISUMI Group Inc Japan 0.5

Rentokil Initial PLC United Kingdom 0.3

Wartsila OYJ Abp Finland 0.2

Epiroc AB Sweden 0.1

Information Technology 14.6

Amadeus IT Group SA Spain 2.7

Nomura Research Institute Ltd Japan 1.6

Dassault Systemes SE France 1.5

Obic Co Ltd Japan 1.4

Hirose Electric Co Ltd Japan 1.2

Infineon Technologies AG Germany 1.0

Halma PLC United Kingdom 1.0

Omron Corp Japan 1.0

As of 31-Aug-19 CountryEquivalent

Exposure (%)

SAP SE Germany 0.9

Spectris PLC United Kingdom 0.6

Yokogawa Electric Corp Japan 0.4

Check Point Software Technologies Ltd Israel 0.3

Disco Corp Japan 0.3

WiseTech Global Ltd Australia 0.3

Descartes Systems Group Inc Canada 0.2

Wix.com Ltd Israel 0.2

Materials 7.9

Givaudan SA Switzerland 4.1

Symrise AG Germany 1.9

Novozymes AS Denmark 0.7

Kansai Paint Co Ltd Japan 0.5

Sika AG Switzerland 0.4

Croda International PLC United Kingdom 0.3

Other -0.0

Real Estate 5.1

Vonovia SE Germany 2.0

Deutsche Wohnen SE Germany 1.7

LEG Immobilien AG Germany 0.8

TAG Immobilien AG Germany 0.6

Portfolio HoldingsRetiree Health Benefits Plan continued...

Fee Schedule

MFS® International Intrinsic Value Equity 48299-I-CT-IIV-02Oct19.48

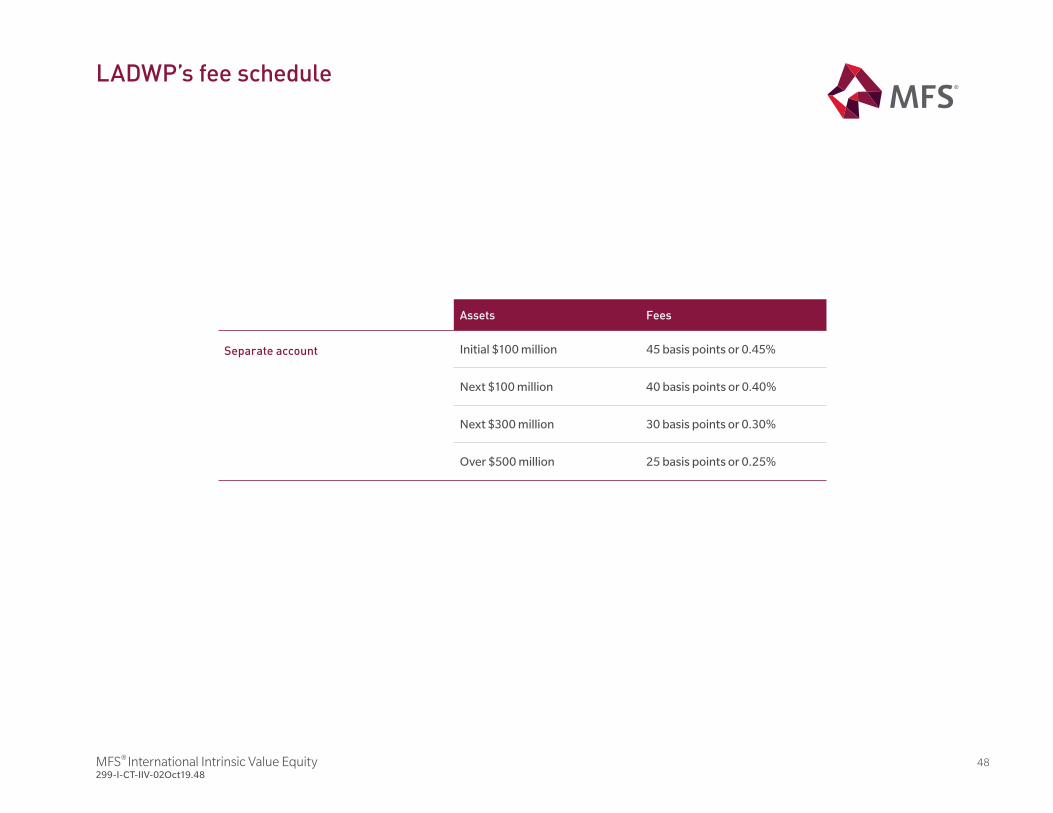

LADWP’s fee schedule

Assets Fees

Separate account Initial $100 million 45 basis points or 0.45%

Next $100 million 40 basis points or 0.40%

Next $300 million 30 basis points or 0.30%

Over $500 million 25 basis points or 0.25%

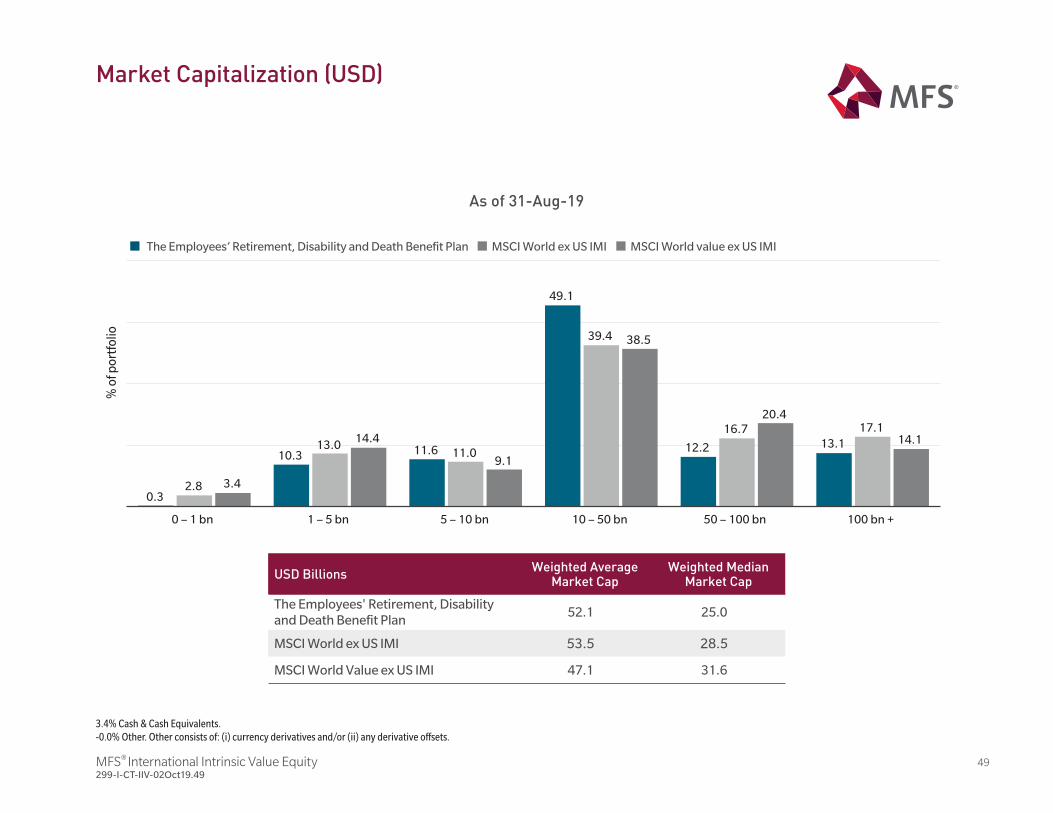

49

0 – 1 bn 1 – 5 bn 5 – 10 bn 10 – 50 bn 50 – 100 bn 100 bn +

% o

f por

tfol

io

0.32.8 3.4

10.313.0 14.4

11.6 11.09.1

49.1

39.4 38.5

12.2

16.720.4

13.117.1

14.1

As of 31-Aug-19

BillionsWeighted Average

Market CapWeighted Median

Market Cap

The Employees' Retirement, Disability and Death Benefit Plan

52.1 25.0

MSCI World ex US IMI 53.5 28.5

MSCI World Value ex US IMI 47.1 31.6

MFS® International Intrinsic Value Equity 299-I-CT-IIV-02Oct19.49

Market Capitalization (USD)

The Employees’ Retirement, Disability and Death Benefit Plan MSCI World ex US IMI MSCI World value ex US IMI

3.4% Cash & Cash Equivalents.-0.0% Other. Other consists of: (i) currency derivatives and/or (ii) any derivative offsets.

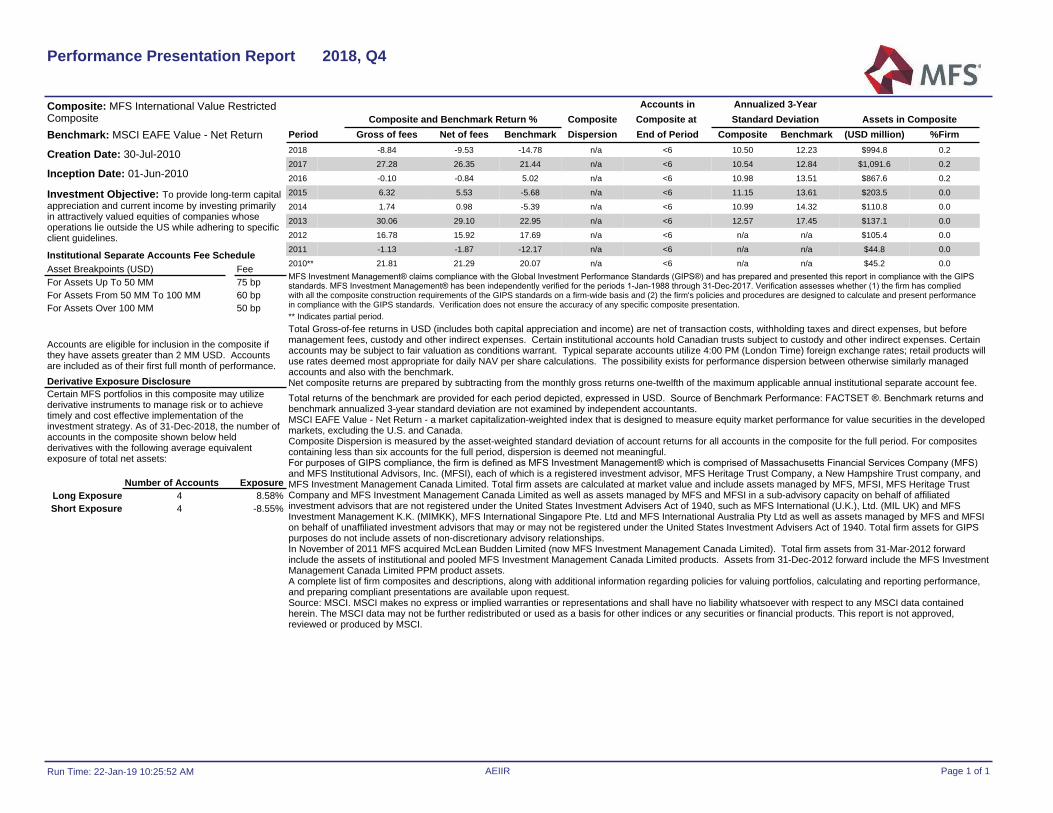

Composite: MFS International Value Equity CompositeBenchmark: MSCI EAFE Value - Net Return

Creation Date: 19-Oct-2005

Inception Date: 01-Dec-1997

Investment Objective: To provide long-term capital appreciation and current income by investing principally in attractively valued equities of companies whose operations lie outside of the U.S. Stock selection is based solely on MFS proprietary research process and therefore excludes assets managed by external parties or non-MFS sub-advisors.

Institutional Separate Accounts Fee ScheduleAsset Breakpoints (USD) FeeFor Assets Up To 50 MM 75 bpFor Assets From 50 MM To 100 MM 60 bpFor Assets Over 100 MM 50 bp

Derivative Exposure DisclosureCertain MFS portfolios in this composite may utilize derivative instruments to manage risk or to achieve timely and cost effective implementation of the investment strategy. As of 31-Dec-2018, the number of accounts in the composite shown below held derivatives with the following average equivalent exposure of total net assets:

Number of Accounts ExposureLong Exposure 11 6.12%Short Exposure 11 -6.09%

Accounts are eligible for inclusion in the composite if they have assets greater than 2 MM USD. Accounts are included as of their first full month of performance.

Accounts in Annualized 3-YearComposite and Benchmark Return % Composite Composite at Standard Deviation Assets in Composite

Period Gross of fees Net of fees Benchmark Dispersion End of Period Composite Benchmark (USD million) %Firm2018 -8.46 -9.15 -14.78 0.27 14 10.20 12.23 $32,892.8 7.7

2017 28.13 27.20 21.44 0.13 14 9.66 12.84 $38,627.0 7.9

2016 4.90 4.12 5.02 0.24 15 10.29 13.51 $31,474.5 7.4

2015 7.51 6.71 -5.68 0.29 18 10.85 13.61 $32,903.4 8.0

2014 2.33 1.56 -5.39 0.23 19 10.87 14.32 $27,757.3 6.5

2013 29.04 28.09 22.95 0.58 20 12.32 17.45 $22,037.3 5.3

2012 17.21 16.34 17.69 0.23 19 14.59 20.56 $12,317.2 3.8

2011 -0.68 -1.43 -12.17 0.10 12 19.87 24.86 $6,494.2 2.9

2010 10.60 9.78 3.25 n/a 9 n/a n/a $5,104.7 2.3

2009 26.50 25.57 34.23 n/a <6 n/a n/a $3,009.2 1.6MFS Investment Management® claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. MFS Investment Management® has been independently verified for the periods 1-Jan-1988 through 31-Dec-2017. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm's policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. MFS International Value Equity Composite has been examined for the periods 01-Dec-1997 through 31-Dec-2017. The verification and performance examination reports are available upon request.

Total Gross-of-fee returns in USD (includes both capital appreciation and income) are net of transaction costs, withholding taxes and direct expenses, but before management fees, custody and other indirect expenses. Certain institutional accounts hold Canadian trusts subject to custody and other indirect expenses. Certain accounts may be subject to fair valuation as conditions warrant. Typical separate accounts utilize 4:00 PM (London Time) foreign exchange rates; retail products will use rates deemed most appropriate for daily NAV per share calculations. The possibility exists for performance dispersion between otherwise similarly managed accounts and also with the benchmark. Net composite returns are prepared by subtracting from the monthly gross returns one-twelfth of the maximum applicable annual institutional separate account fee. Returns based on actual management fees, including non-separate account fees and performance based fees, would be lower for the following periods - 2009: 25.44.Total returns of the benchmark are provided for each period depicted, expressed in USD. Source of Benchmark Performance: FACTSET ®. Benchmark returns and benchmark annualized 3-year standard deviation are not examined by independent accountants. MSCI EAFE Value - Net Return - a market capitalization-weighted index that is designed to measure equity market performance for value securities in the developed markets, excluding the U.S. and Canada. Composite Dispersion is measured by the asset-weighted standard deviation of account returns for all accounts in the composite for the full period. For composites containing less than six accounts for the full period, dispersion is deemed not meaningful. Prior to 31-Mar-2009 accounts have been eligible for inclusion in the composite if they had assets greater than 5.0 MM USD. Certain accounts in this composite may make tactical allocation to U.S. and Canadian based securities, where each investment is deemed to be consistent with the composite's overall investment objective. For purposes of GIPS compliance, the firm is defined as MFS Investment Management® which is comprised of Massachusetts Financial Services Company (MFS) and MFS Institutional Advisors, Inc. (MFSI), each of which is a registered investment advisor, MFS Heritage Trust Company, a New Hampshire Trust company, and MFS Investment Management Canada Limited. Total firm assets are calculated at market value and include assets managed by MFS, MFSI, MFS Heritage Trust Company and MFS Investment Management Canada Limited as well as assets managed by MFS and MFSI in a sub-advisory capacity on behalf of affiliated investment advisors that are not registered under the United States Investment Advisers Act of 1940, such as MFS International (U.K.), Ltd. (MIL UK) and MFS Investment Management K.K. (MIMKK), MFS International Singapore Pte. Ltd and MFS International Australia Pty Ltd as well as assets managed by MFS and MFSI on behalf of unaffiliated investment advisors that may or may not be registered under the United States Investment Advisers Act of 1940. Total firm assets for GIPS purposes do not include assets of non-discretionary advisory relationships.In November of 2011 MFS acquired McLean Budden Limited (now MFS Investment Management Canada Limited). Total firm assets from 31-Mar-2012 forward include the assets of institutional and pooled MFS Investment Management Canada Limited products. Assets from 31-Dec-2012 forward include the MFS Investment Management Canada Limited PPM product assets. A complete list of firm composites and descriptions, along with additional information regarding policies for valuing portfolios, calculating and reporting performance, and preparing compliant presentations are available upon request. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Run Time: 22-Jan-19 10:23:52 AM AEDIV Page 1 of 1

Performance Presentation Report 2018, Q4

Composite: MFS International Value Restricted CompositeBenchmark: MSCI EAFE Value - Net Return

Creation Date: 30-Jul-2010

Inception Date: 01-Jun-2010

Investment Objective: To provide long-term capital appreciation and current income by investing primarily in attractively valued equities of companies whose operations lie outside the US while adhering to specific client guidelines.

Institutional Separate Accounts Fee ScheduleAsset Breakpoints (USD) FeeFor Assets Up To 50 MM 75 bpFor Assets From 50 MM To 100 MM 60 bpFor Assets Over 100 MM 50 bp

Derivative Exposure DisclosureCertain MFS portfolios in this composite may utilize derivative instruments to manage risk or to achieve timely and cost effective implementation of the investment strategy. As of 31-Dec-2018, the number of accounts in the composite shown below held derivatives with the following average equivalent exposure of total net assets:

Number of Accounts ExposureLong Exposure 4 8.58%Short Exposure 4 -8.55%

Accounts are eligible for inclusion in the composite if they have assets greater than 2 MM USD. Accounts are included as of their first full month of performance.

Accounts in Annualized 3-YearComposite and Benchmark Return % Composite Composite at Standard Deviation Assets in Composite

Period Gross of fees Net of fees Benchmark Dispersion End of Period Composite Benchmark (USD million) %Firm2018 -8.84 -9.53 -14.78 n/a <6 10.50 12.23 $994.8 0.2

2017 27.28 26.35 21.44 n/a <6 10.54 12.84 $1,091.6 0.2

2016 -0.10 -0.84 5.02 n/a <6 10.98 13.51 $867.6 0.2

2015 6.32 5.53 -5.68 n/a <6 11.15 13.61 $203.5 0.0

2014 1.74 0.98 -5.39 n/a <6 10.99 14.32 $110.8 0.0

2013 30.06 29.10 22.95 n/a <6 12.57 17.45 $137.1 0.0

2012 16.78 15.92 17.69 n/a <6 n/a n/a $105.4 0.0

2011 -1.13 -1.87 -12.17 n/a <6 n/a n/a $44.8 0.0