Embed Size (px)

Citation preview

JPMorgan Emerging Markets Investment Trust plc

Annual General Meeting

24 November 2017

JPMorgan Emerging Markets Investment Trust plc

Annual General Meeting

24 November 2017

Austin Forey, Portfolio Manager

2

Agenda

The past year

Looking ahead

Staying relevant

And finally…

3

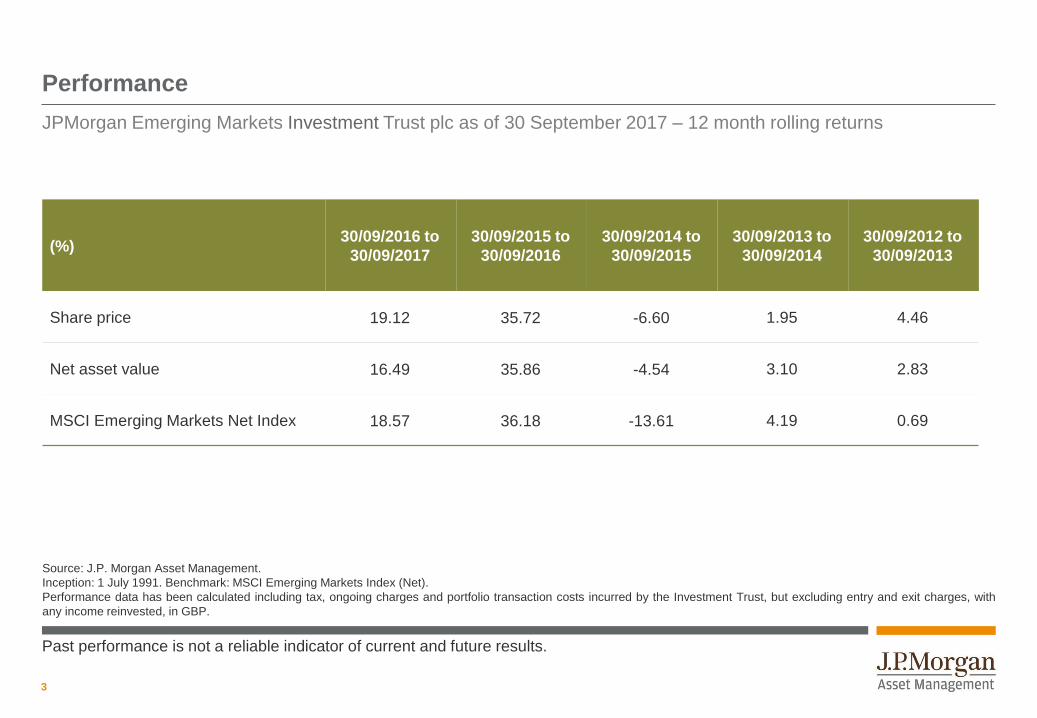

Performance

JPMorgan Emerging Markets Investment Trust plc as of 30 September 2017 – 12 month rolling returns

(%)30/09/2016 to

30/09/2017

30/09/2015 to

30/09/2016

30/09/2014 to

30/09/2015

30/09/2013 to

30/09/2014

30/09/2012 to

30/09/2013

Share price 19.12 35.72 -6.60 1.95 4.46

Net asset value 16.49 35.86 -4.54 3.10 2.83

MSCI Emerging Markets Net Index 18.57 36.18 -13.61 4.19 0.69

Source: J.P. Morgan Asset Management.

Inception: 1 July 1991. Benchmark: MSCI Emerging Markets Index (Net).

Performance data has been calculated including tax, ongoing charges and portfolio transaction costs incurred by the Investment Trust, but excluding entry and exit charges, with

any income reinvested, in GBP.

Past performance is not a reliable indicator of current and future results.

4

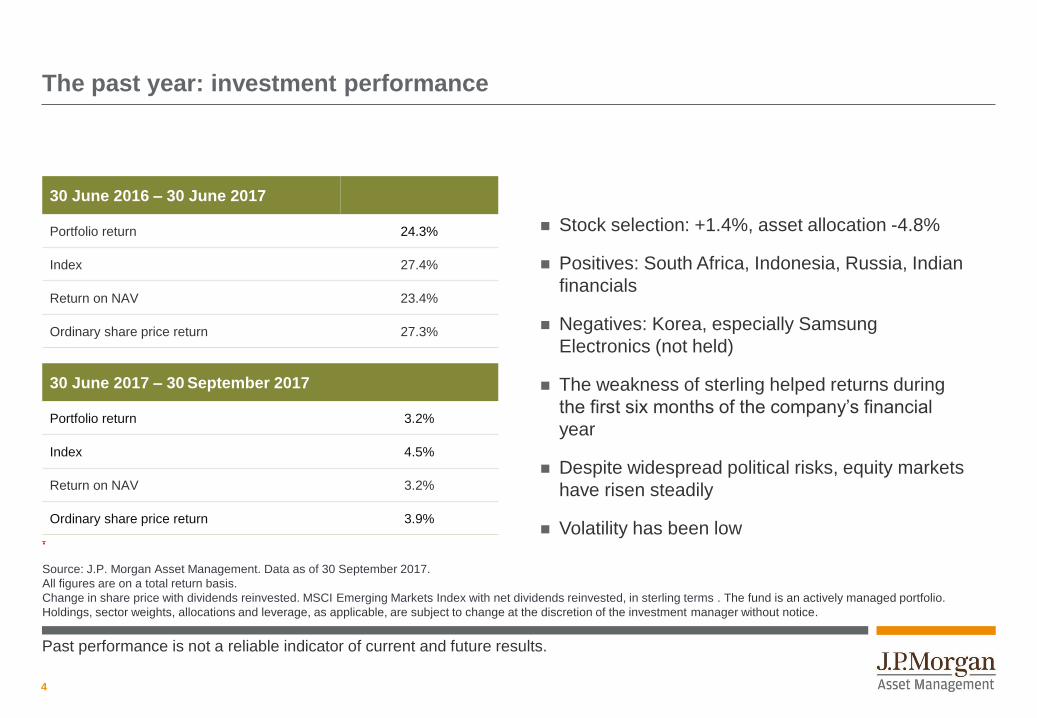

The past year: investment performance

Stock selection: +1.4%, asset allocation -4.8%

Positives: South Africa, Indonesia, Russia, Indian

financials

Negatives: Korea, especially Samsung

Electronics (not held)

The weakness of sterling helped returns during

the first six months of the company’s financial

year

Despite widespread political risks, equity markets

have risen steadily

Volatility has been low.

Source: J.P. Morgan Asset Management. Data as of 30 September 2017.

All figures are on a total return basis.

Change in share price with dividends reinvested. MSCI Emerging Markets Index with net dividends reinvested, in sterling terms . The fund is an actively managed portfolio.

Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager without notice.

30 June 2016 – 30 June 2017

Portfolio return 24.3%

Index 27.4%

Return on NAV 23.4%

Ordinary share price return 27.3%

30 June 2017 – 30 September 2017

Portfolio return 3.2%

Index 4.5%

Return on NAV 3.2%

Ordinary share price return 3.9%

Past performance is not a reliable indicator of current and future results.

5

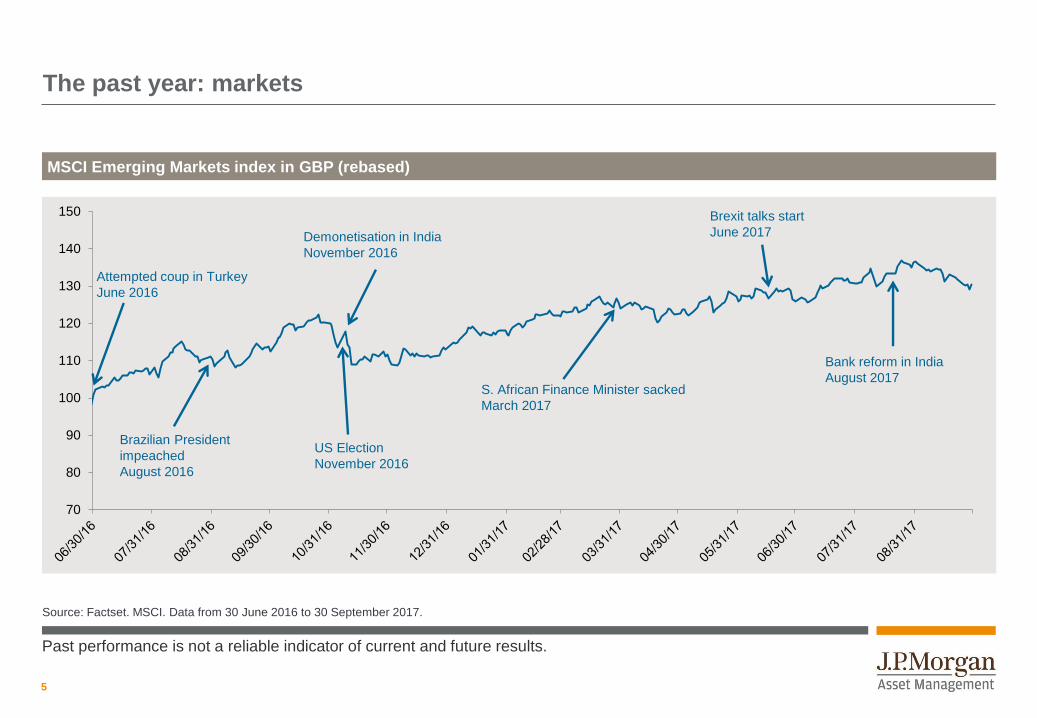

The past year: markets

Source: Factset. MSCI. Data from 30 June 2016 to 30 September 2017.

MSCI Emerging Markets index in GBP (rebased)

70

80

90

100

110

120

130

140

150

Demonetisation in India

November 2016

US Election

November 2016

Bank reform in India

August 2017

Attempted coup in Turkey

June 2016

Brazilian President

impeached

August 2016

S. African Finance Minister sacked

March 2017

Brexit talks start

June 2017

Past performance is not a reliable indicator of current and future results.

6

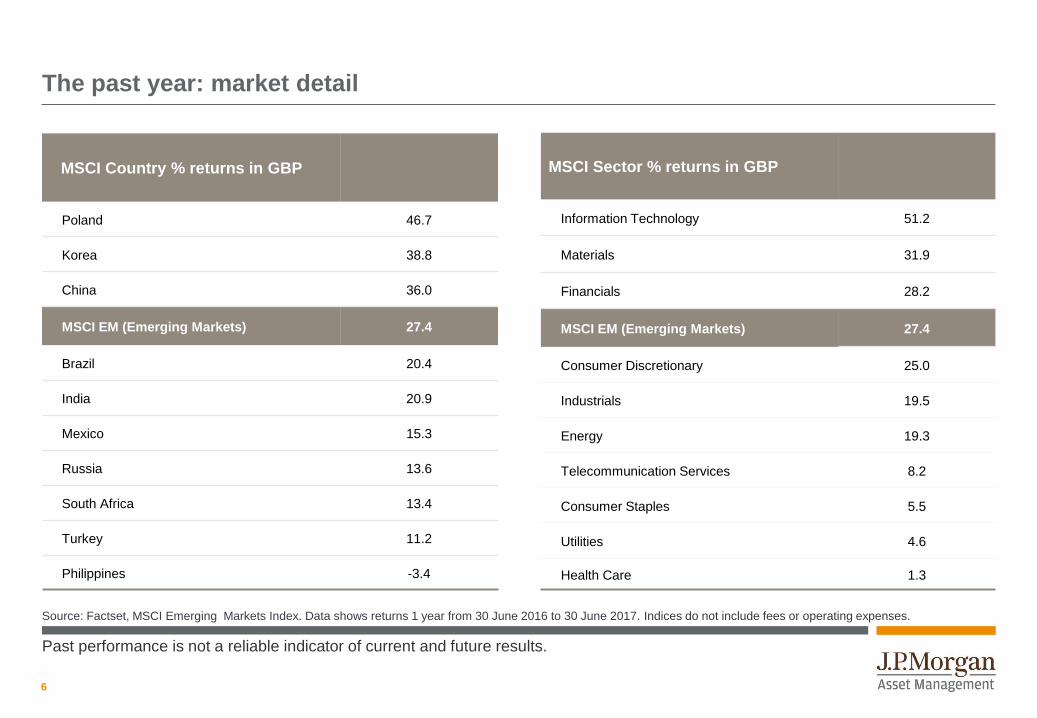

The past year: market detail

Source: Factset, MSCI Emerging Markets Index. Data shows returns 1 year from 30 June 2016 to 30 June 2017. Indices do not include fees or operating expenses.

MSCI Country % returns in GBP

Poland 46.7

Korea 38.8

China 36.0

MSCI EM (Emerging Markets) 27.4

Brazil 20.4

India 20.9

Mexico 15.3

Russia 13.6

South Africa 13.4

Turkey 11.2

Philippines -3.4

MSCI Sector % returns in GBP

Information Technology 51.2

Materials 31.9

Financials 28.2

MSCI EM (Emerging Markets) 27.4

Consumer Discretionary 25.0

Industrials 19.5

Energy 19.3

Telecommunication Services 8.2

Consumer Staples 5.5

Utilities 4.6

Health Care 1.3

Past performance is not a reliable indicator of current and future results.

7

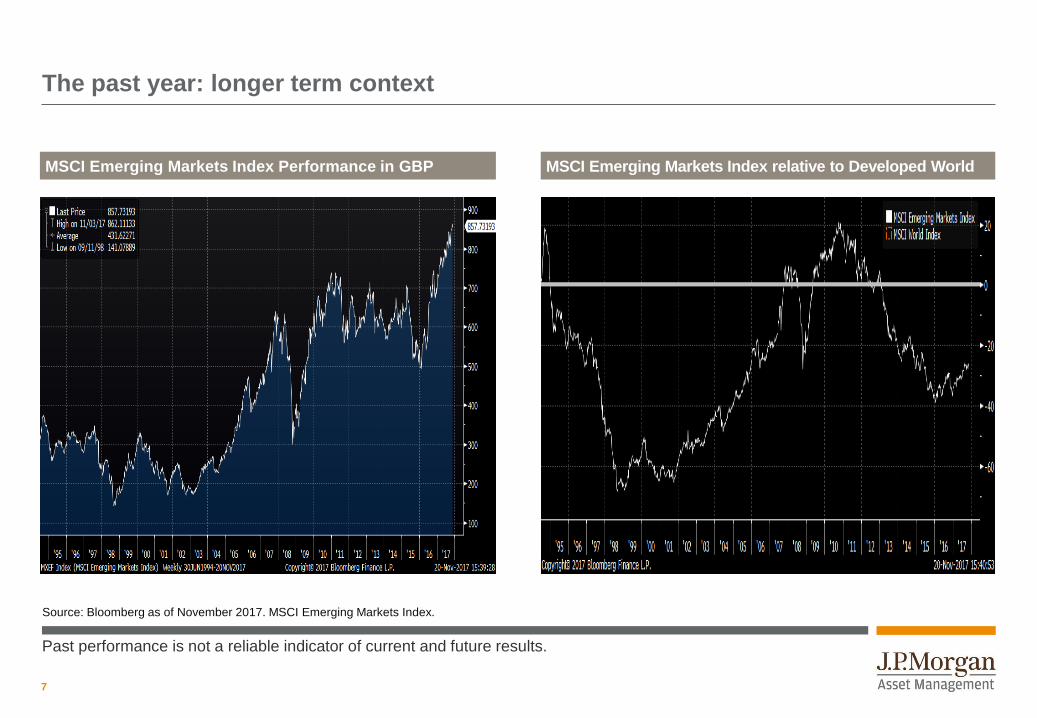

The past year: longer term context

MSCI Emerging Markets Index Performance in GBP MSCI Emerging Markets Index relative to Developed World

Source: Bloomberg as of November 2017. MSCI Emerging Markets Index.

Past performance is not a reliable indicator of current and future results.

8

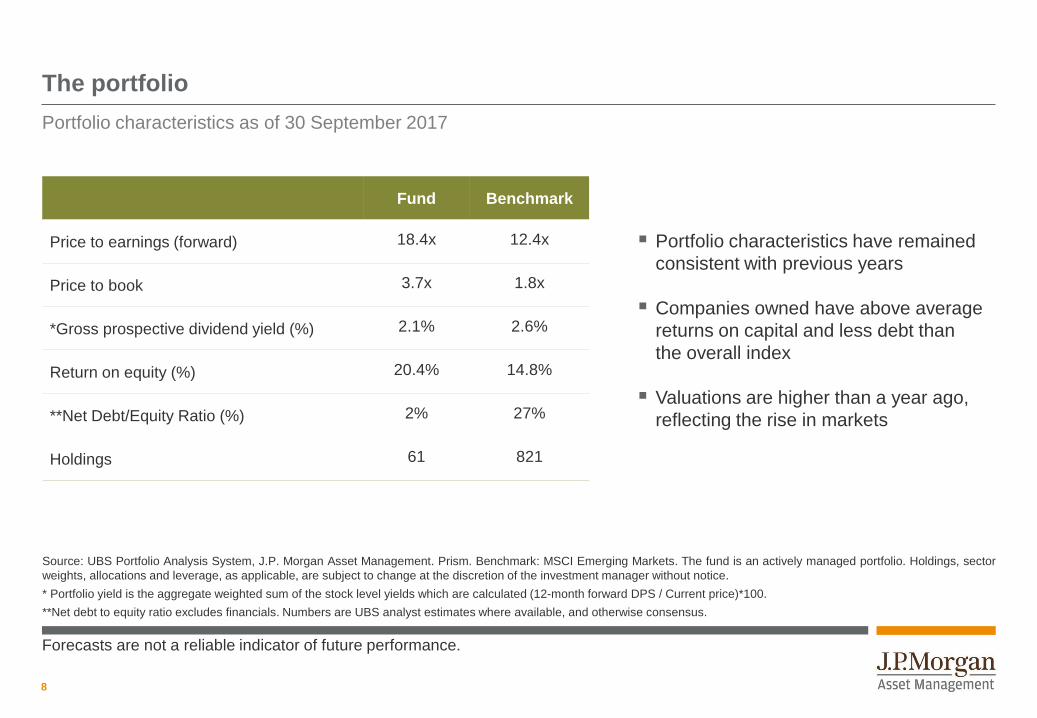

The portfolio

Source: UBS Portfolio Analysis System, J.P. Morgan Asset Management. Prism. Benchmark: MSCI Emerging Markets. The fund is an actively managed portfolio. Holdings, sector

weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager without notice.

* Portfolio yield is the aggregate weighted sum of the stock level yields which are calculated (12-month forward DPS / Current price)*100.

**Net debt to equity ratio excludes financials. Numbers are UBS analyst estimates where available, and otherwise consensus.

Portfolio characteristics as of 30 September 2017

Fund Benchmark

Price to earnings (forward) 18.4x 12.4x

Price to book 3.7x 1.8x

*Gross prospective dividend yield (%) 2.1% 2.6%

Return on equity (%) 20.4% 14.8%

**Net Debt/Equity Ratio (%) 2% 27%

Holdings 61 821

Portfolio characteristics have remained

consistent with previous years

Companies owned have above average

returns on capital and less debt than

the overall index

Valuations are higher than a year ago,

reflecting the rise in markets

Forecasts are not a reliable indicator of future performance.

9

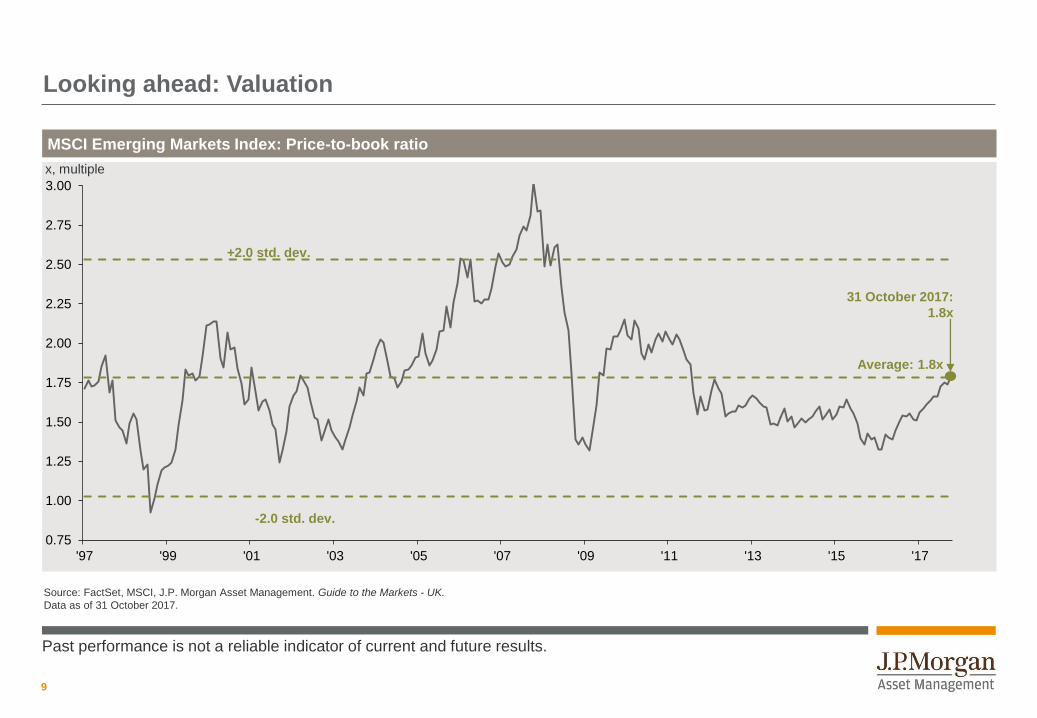

GTM – UK |Looking ahead: Valuation

MSCI Emerging Markets Index: Price-to-book ratio

Source: FactSet, MSCI, J.P. Morgan Asset Management. Guide to the Markets - UK.

Data as of 31 October 2017.

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

'97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17

x, multiple

-2.0 std. dev.

+2.0 std. dev.

Average: 1.8x

31 October 2017:

1.8x

Past performance is not a reliable indicator of current and future results.

10

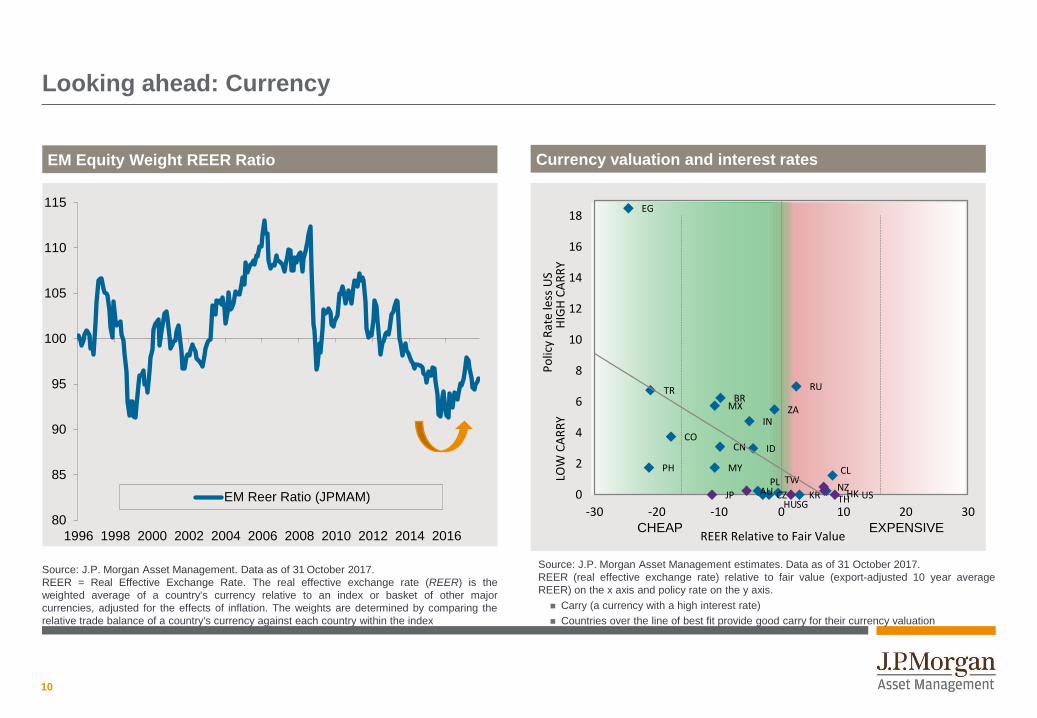

Looking ahead: Currency

EM Equity Weight REER Ratio

Source: J.P. Morgan Asset Management estimates. Data as of 31 October 2017.

REER (real effective exchange rate) relative to fair value (export-adjusted 10 year average

REER) on the x axis and policy rate on the y axis.

Carry (a currency with a high interest rate)

Countries over the line of best fit provide good carry for their currency valuation

Source: J.P. Morgan Asset Management. Data as of 31 October 2017.

REER = Real Effective Exchange Rate. The real effective exchange rate (REER) is the

weighted average of a country's currency relative to an index or basket of other major

currencies, adjusted for the effects of inflation. The weights are determined by comparing the

relative trade balance of a country's currency against each country within the index

Currency valuation and interest rates

80

85

90

95

100

105

110

115

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

EM Reer Ratio (JPMAM)

MY

CN

TW

RU

ID

THKR

MXBR

CZ

IN

CO

TR

PL

HU

ZA

EG

CLPH

USAU NZHK

SGJP0

2

4

6

8

10

12

14

16

18

-30 -20 -10 0 10 20 30

Po

licy

Rat

e le

ss U

SREER Relative to Fair Value

CHEAP EXPENSIVE

LOW

CA

RR

YH

IGH

CA

RR

Y

11

0

2

4

6

8

10

12

14

16

18

20

0

20

40

60

80

100

120

140

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

e

20

18

e

20

19

N

20

20

e

20

21

e

20

22

eEPS ROE

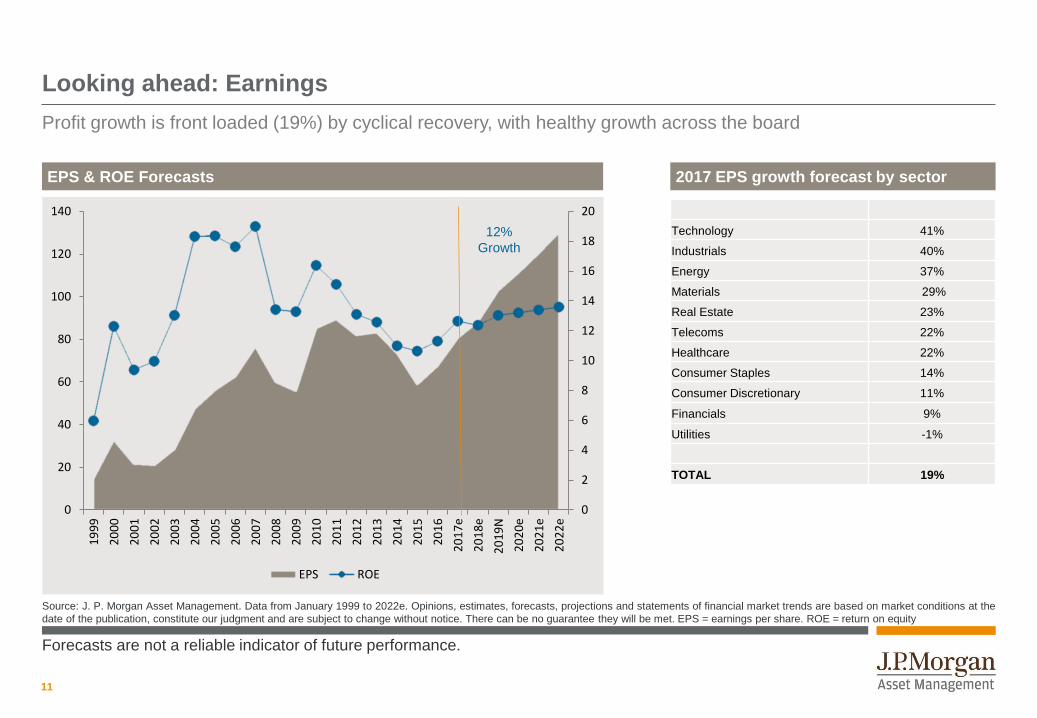

Looking ahead: Earnings

Profit growth is front loaded (19%) by cyclical recovery, with healthy growth across the board

Source: J. P. Morgan Asset Management. Data from January 1999 to 2022e. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the

date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met. EPS = earnings per share. ROE = return on equity

12%

Growth

EPS & ROE Forecasts 2017 EPS growth forecast by sector

Technology 41%

Industrials 40%

Energy 37%

Materials 29%

Real Estate 23%

Telecoms 22%

Healthcare 22%

Consumer Staples 14%

Consumer Discretionary 11%

Financials 9%

Utilities -1%

TOTAL 19%

Forecasts are not a reliable indicator of future performance.

12

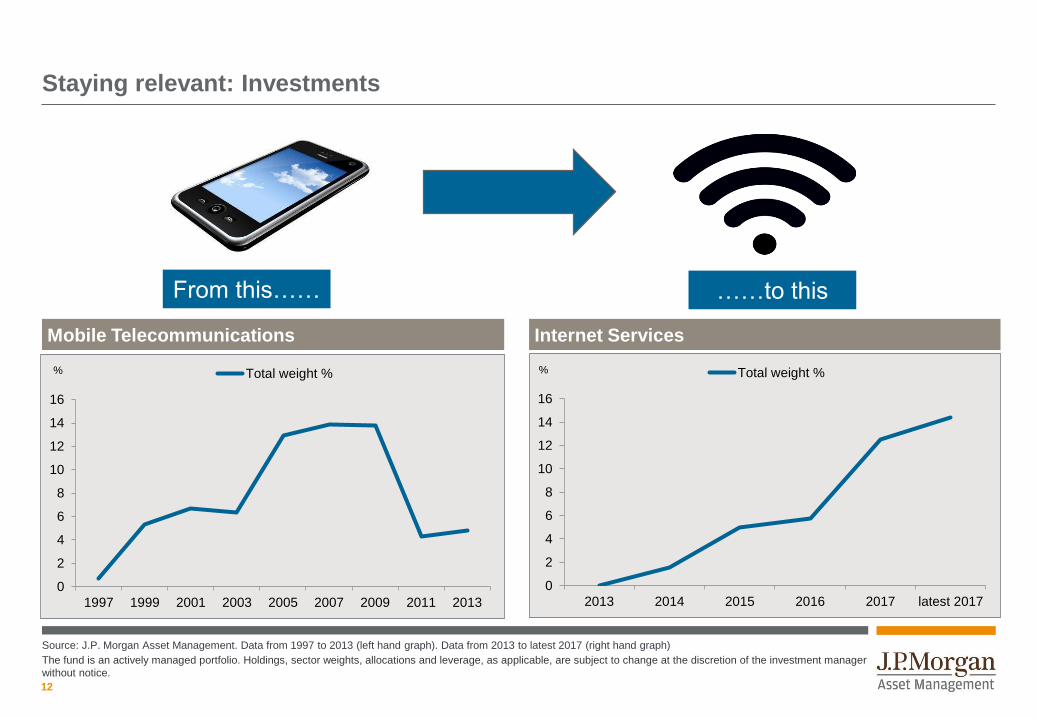

Staying relevant: Investments

Source: J.P. Morgan Asset Management. Data from 1997 to 2013 (left hand graph). Data from 2013 to latest 2017 (right hand graph)

The fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager

without notice.

From this…… ……to this

Mobile Telecommunications Internet Services

0

2

4

6

8

10

12

14

16

2013 2014 2015 2016 2017 latest 2017

Total weight %%

0

2

4

6

8

10

12

14

16

1997 1999 2001 2003 2005 2007 2009 2011 2013

Total weight %%

13

First

investedTop 10 Holdings Country Sector

Fund

weight (%)

2015 Tencent China Information Technology 6.0

1998 HDFC India Financials 5.6

1996 TSMC Taiwan Information Technology 5.5

2017 Alibaba China Information Technology 4.7

2014 Indusind Bank India Financials 4.5

2010 AIA Group China Financials 3.5

2017 Ping An Insurance China Financials 2.8

2015 EPAM Systems Belarus Information Technology 2.5

2013 Tata Consultancy Services India Information Technology 2.4

2011 Clicks Group South Africa Consumer Staples 2.2

Source: J.P. Morgan Asset Management. Data as of 30 September 2017. The Fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to

change at the discretion of the Investment Manager without notice.

Staying relevant: Investments

14

Staying relevant: Investments

0

100

200

300

400

500

600

700

800

900

1000

1 4 7

10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

55

58

61

64

67

70

73

76

79

82

85

88

91

94

97

100

103

106

109

112

115

118

121

To

tal R

etu

rn

Months since purchase

HDFC TSMC Alibaba Tencent AIA

Tata Consultancy EPAM PingAn Clicks Group Indusind Bank

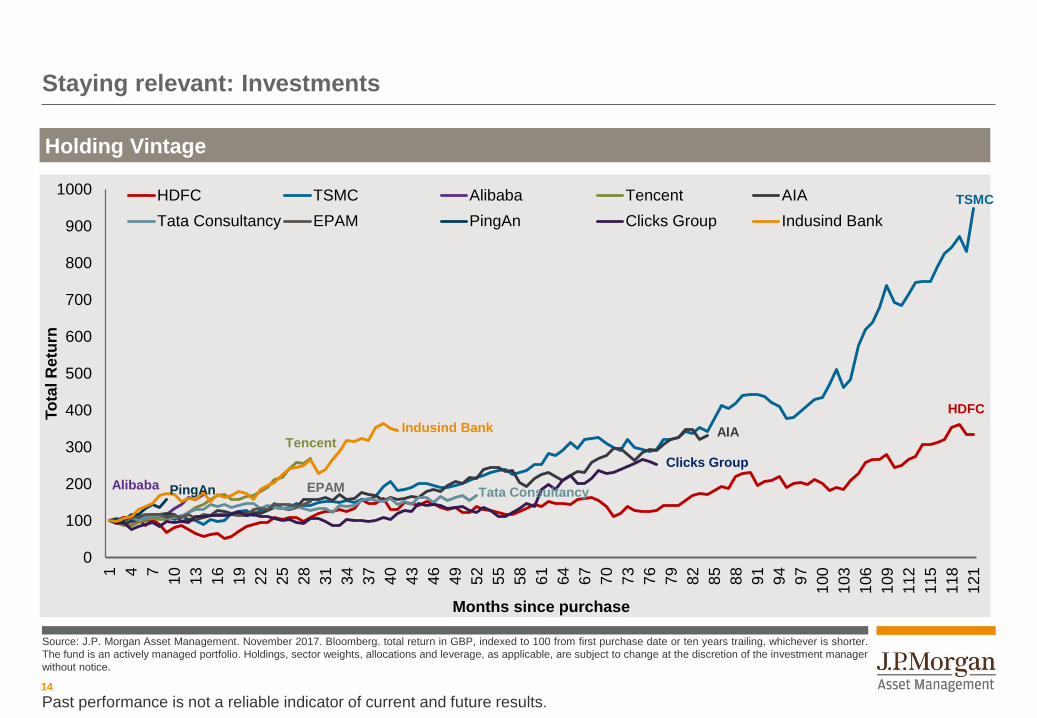

Holding Vintage

Source: J.P. Morgan Asset Management. November 2017. Bloomberg. total return in GBP, indexed to 100 from first purchase date or ten years trailing, whichever is shorter.

The fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager

without notice.

TSMC

HDFC

Alibaba

TencentAIA

Tata ConsultancyPingAn

Clicks Group

Indusind Bank

EPAM

Past performance is not a reliable indicator of current and future results.

15

40

60

80

100

2001 2003 2005 2007 2009 2011 2013 2015

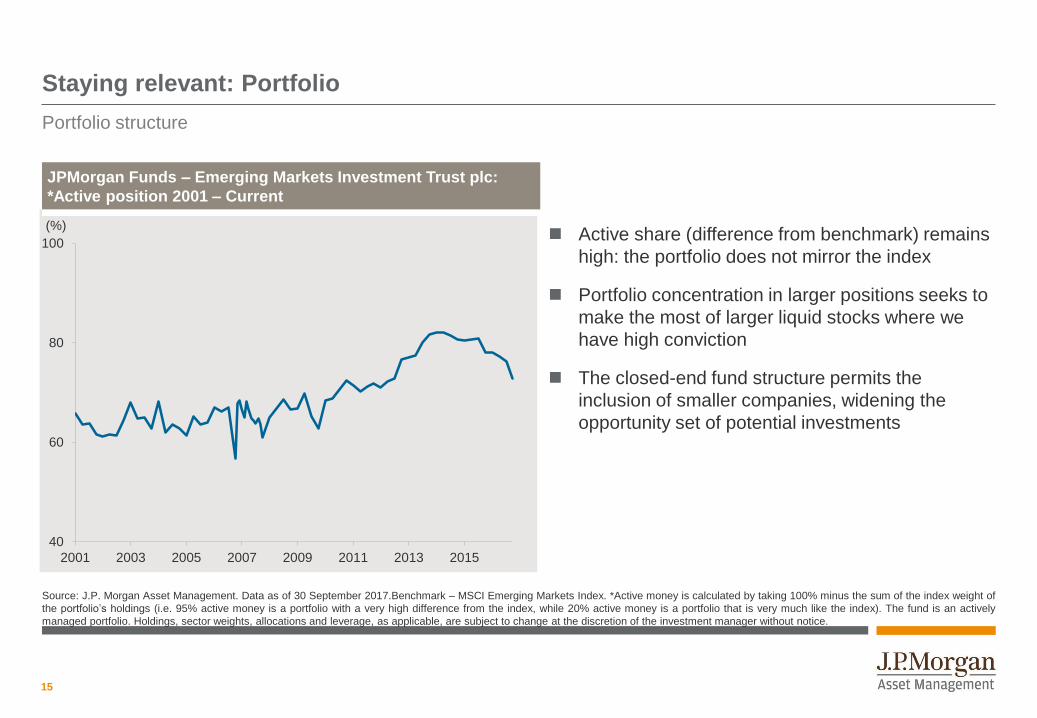

Staying relevant: Portfolio

Portfolio structure

Active share (difference from benchmark) remains

high: the portfolio does not mirror the index

Portfolio concentration in larger positions seeks to

make the most of larger liquid stocks where we

have high conviction

The closed-end fund structure permits the

inclusion of smaller companies, widening the

opportunity set of potential investments

Source: J.P. Morgan Asset Management. Data as of 30 September 2017.Benchmark – MSCI Emerging Markets Index. *Active money is calculated by taking 100% minus the sum of the index weight of

the portfolio’s holdings (i.e. 95% active money is a portfolio with a very high difference from the index, while 20% active money is a portfolio that is very much like the index). The fund is an actively

managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager without notice.

JPMorgan Funds – Emerging Markets Investment Trust plc:

*Active position 2001 – Current

(%)

16

15

53

43

34

10

0

10

20

30

40

50

60

Average EMCompany

Infosys SamsungElectronics

HDFC Gazprom

1 03

0 1

0

10

20

30

40

50

60

Average EMCompany

Infosys SamsungElectronics

HDFC Gazprom

Staying relevant: Portfolio

Source: Bloomberg, Factset J.P. Morgan Asset Management, as of March 2017. MSCI India Index and MSCI Emerging Markets Index. Returns are in USD. The companies/securities above are shown

for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell. J.P. Morgan Asset Management may or may not hold positions on behalf of its clients in any or

all of the aforementioned securities. EM = Emerging Markets.

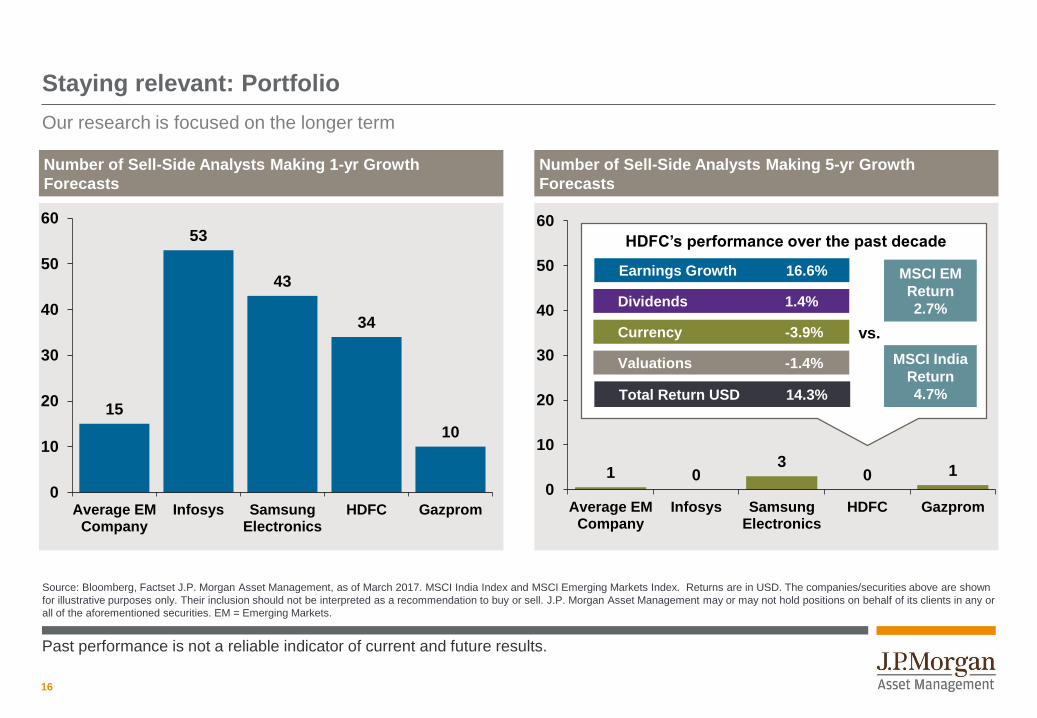

Number of Sell-Side Analysts Making 1-yr Growth

Forecasts

Number of Sell-Side Analysts Making 5-yr Growth

Forecasts

Dividends 1.4%

Earnings Growth 16.6%

Currency -3.9%

Valuations -1.4%

Total Return USD 14.3%

vs.

MSCI EM

Return

2.7%

MSCI India

Return

4.7%

HDFC’s performance over the past decade

Our research is focused on the longer term

Past performance is not a reliable indicator of current and future results.

17

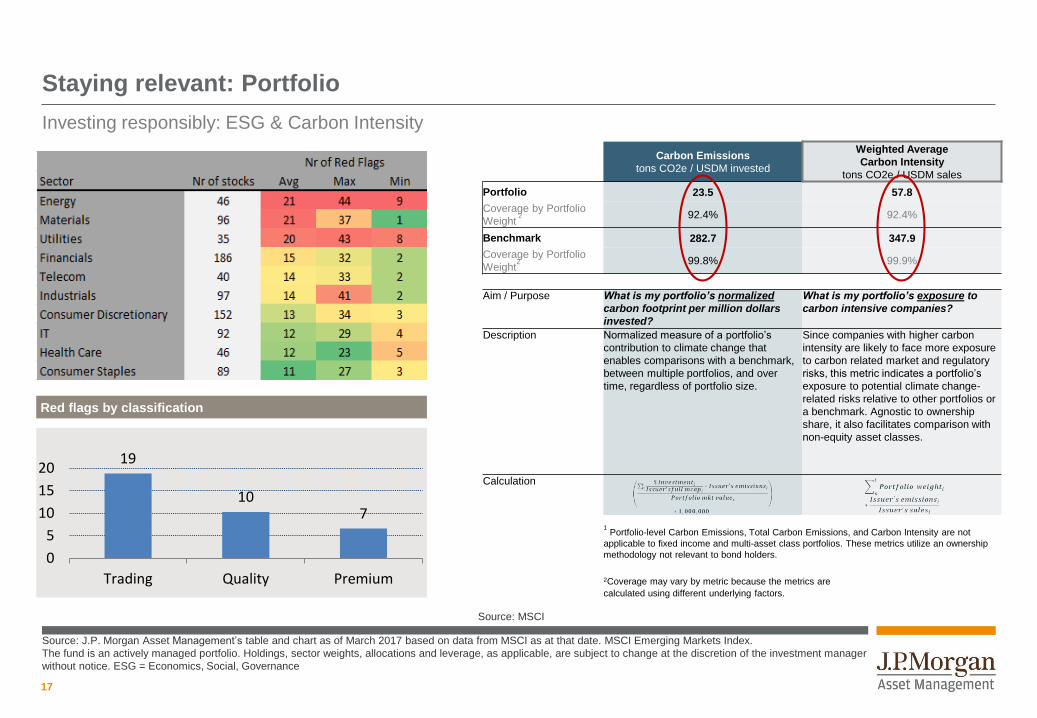

19

107

0

5

10

15

20

Trading Quality Premium

Red flags by classification

Source: J.P. Morgan Asset Management’s table and chart as of March 2017 based on data from MSCI as at that date. MSCI Emerging Markets Index.

The fund is an actively managed portfolio. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager

without notice. ESG = Economics, Social, Governance

Staying relevant: Portfolio

Investing responsibly: ESG & Carbon Intensity

Carbon Emissions

tons CO2e / USDM invested

Weighted Average

Carbon Intensity

tons CO2e / USDM sales

Portfolio 23.5 57.8

Coverage by Portfolio

Weight2 92.4% 92.4%

Benchmark 282.7 347.9

Coverage by Portfolio

Weight2 99.8% 99.9%

Aim / Purpose What is my portfolio’s normalized

carbon footprint per million dollars

invested?

What is my portfolio’s exposure to

carbon intensive companies?

Description Normalized measure of a portfolio’s

contribution to climate change that

enables comparisons with a benchmark,

between multiple portfolios, and over

time, regardless of portfolio size.

Since companies with higher carbon

intensity are likely to face more exposure

to carbon related market and regulatory

risks, this metric indicates a portfolio’s

exposure to potential climate change-

related risks relative to other portfolios or

a benchmark. Agnostic to ownership

share, it also facilitates comparison with

non-equity asset classes.

Calculation

1Portfolio-level Carbon Emissions, Total Carbon Emissions, and Carbon Intensity are not

applicable to fixed income and multi-asset class portfolios. These metrics utilize an ownership

methodology not relevant to bond holders.

2Coverage may vary by metric because the metrics are

calculated using different underlying factors.

Source: MSCI

18

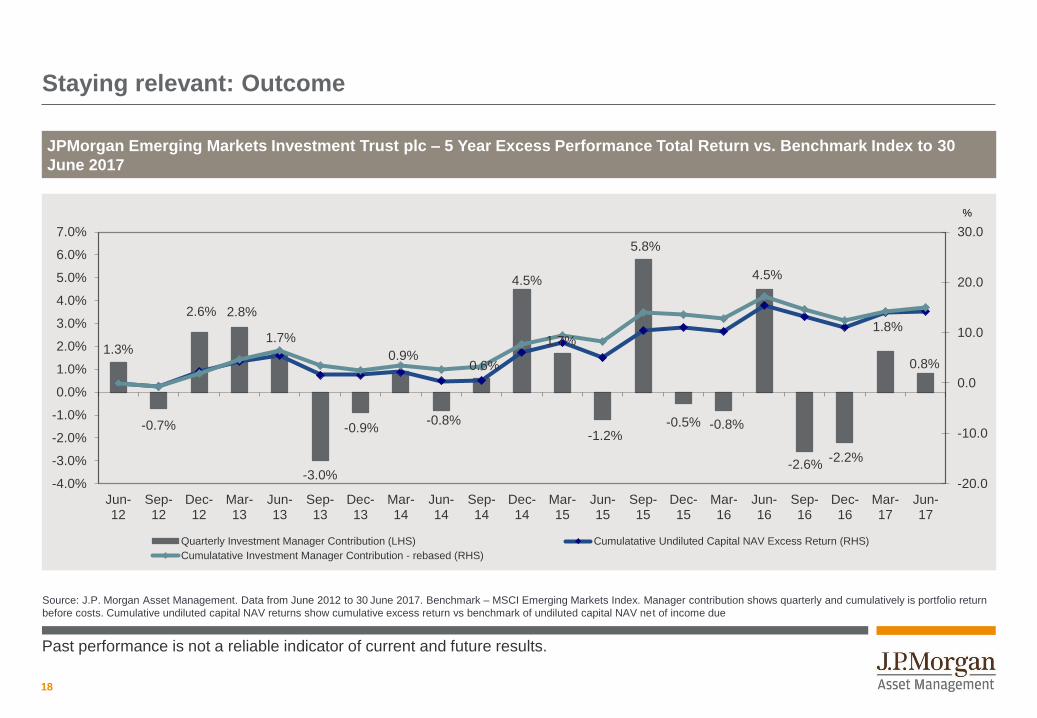

Staying relevant: Outcome

Source: J.P. Morgan Asset Management. Data from June 2012 to 30 June 2017. Benchmark – MSCI Emerging Markets Index. Manager contribution shows quarterly and cumulatively is portfolio return

before costs. Cumulative undiluted capital NAV returns show cumulative excess return vs benchmark of undiluted capital NAV net of income due

JPMorgan Emerging Markets Investment Trust plc – 5 Year Excess Performance Total Return vs. Benchmark Index to 30

June 2017

1.3%

-0.7%

2.6% 2.8%

1.7%

-3.0%

-0.9%

0.9%

-0.8%

0.6%

4.5%

1.7%

-1.2%

5.8%

-0.5% -0.8%

4.5%

-2.6%-2.2%

1.8%

0.8%

-20.0

-10.0

0.0

10.0

20.0

30.0

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

Mar-16

Jun-16

Sep-16

Dec-16

Mar-17

Jun-17

Quarterly Investment Manager Contribution (LHS) Cumulatative Undiluted Capital NAV Excess Return (RHS)

Cumulatative Investment Manager Contribution - rebased (RHS)

Past performance is not a reliable indicator of current and future results.

%

19

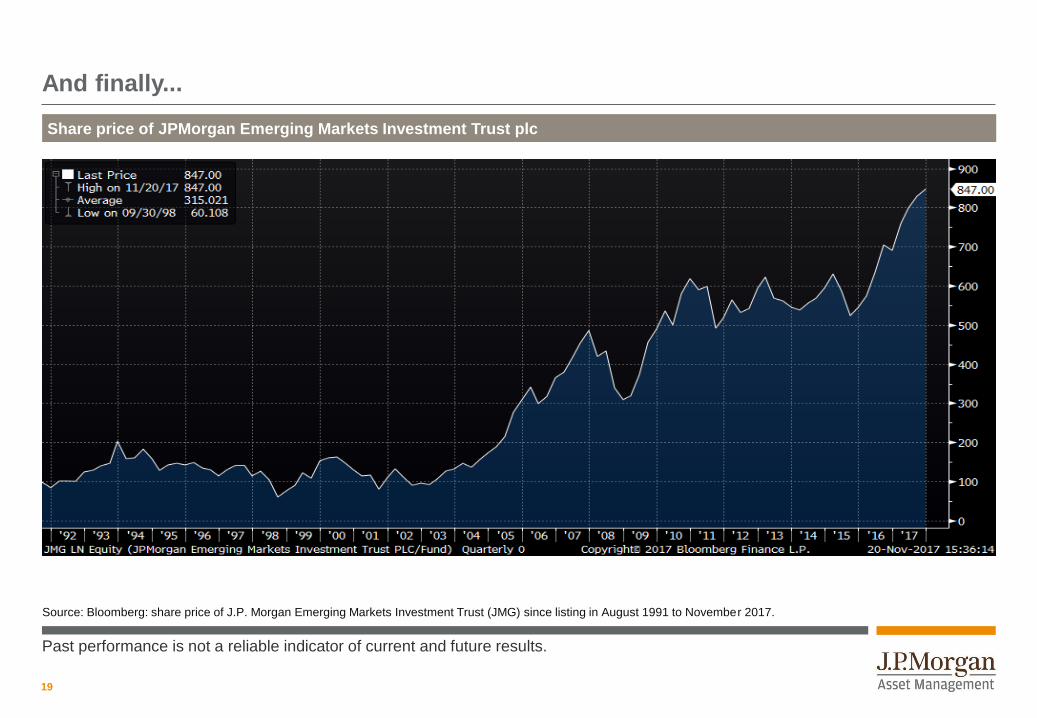

And finally...

Source: Bloomberg: share price of J.P. Morgan Emerging Markets Investment Trust (JMG) since listing in August 1991 to November 2017.

Share price of JPMorgan Emerging Markets Investment Trust plc

Past performance is not a reliable indicator of current and future results.

20

Thank you

21

Investment objectives and risk profile

Investment objectiveCapital growth from emerging markets worldwide. Invests in a diversified portfolio with no more than 50% of the Company’s assets

invested in any one region.

Risk Profile

Investing in emerging markets may involve a higher element of risk due to political and economic instability and underdeveloped markets and systems, and

may be illiquid.

Exchange rate changes may cause the value of underlying overseas investments to be volatile.

Some investment trusts may have warrants or subscription shares in issue, which if exercised may have an effect on the net asset value.

Investments in smaller companies may involve a higher degree of risk as these are usually more sensitive to price movements.

Please refer to the Investment Trust’s Investor Disclosure Document and the Company’s annual report, a copy of which is available from its website.

JPMorgan Emerging Markets Investment Trust plc (the Company) as of 30 September 2017

22

Important Information

This is a marketing communication and as such the views contained herein are not to be taken as an advice or recommendation to buy or sell any investment or

interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have

been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do

not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment

techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be

reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or

notification to you.

It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and

investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or

underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made

will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those

objectives will be met.

J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent

permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal

policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy

www.jpmorgan.com/jpmpdf/1320694304816.pdf.

Investment is subject to documentation (Investment Disclosure Document, [Key Features and Terms and Conditions]), copies of which can be obtained free of

charge from JPMorgan Asset Management (UK) Limited. This communication is issued by JPMorgan Asset Management (UK), Limited which is authorised and

regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14

5JP.

0903c02a81fd8258

6cde0880-ce9c-11e7-b5e0-005056960c63

JPMorgan Emerging Markets Investment Trust plc

Annual General Meeting

24 November 2017