Embed Size (px)

DESCRIPTION

Mengenai penilaian perusahaan

Citation preview

Business Valuation(Penilaian Perusahaan)

A philosophical basis for Valuation• Many investors believe that the pursuit of 'true value'

based upon financial fundamentals is a fruitless (kurang bermakna) one in markets where prices often seem to have little to do with value.

• There have always been investors in financial markets who have argued that market prices are determined by the perceptions (and misperceptions) of buyers and sellers, and not by anything as prosaic as (sebagaimana biasanya) cashflows or earnings.

• Perceptions matter, but they cannot be all the matter.• Asset prices cannot be justified by merely using the

“bigger fool/trick” theory.

Valuation

• Pengertian:

proses penilaian/konversi atas suatu peramalan atau forecasting ke dalam suatu perkiraan nilai perusahaan atau nilai atas beberapa komponen dalam perusahaan tersebut, seperti hutang, dan ekuitas

• Pengertian lain dari valuasi ini adalah penentuan harga yang wajar atas suatu perusahaan (Vf = Dm + Em)

Valuation

• Untuk melakukan valuasi terhadap perusahaan perlu dilakukan analisis terhadap perkiraan perolehan cash flow perusahaan untuk masa datang dan selanjutnya dilakukan perhitungan komponen hutang dan ekuitas atau harga saham berdasarkan proyeksi bisnis dan keuangan

• Dalam proyeksi ini faktor yang perlu dipertimbangkan adalah faktor pertumbuhan, baik pertumbuhan dari dalam (internal growth) maupun pertumbuhan dari luar (external growth) akibat dilakukan merger atau atu akuisisi

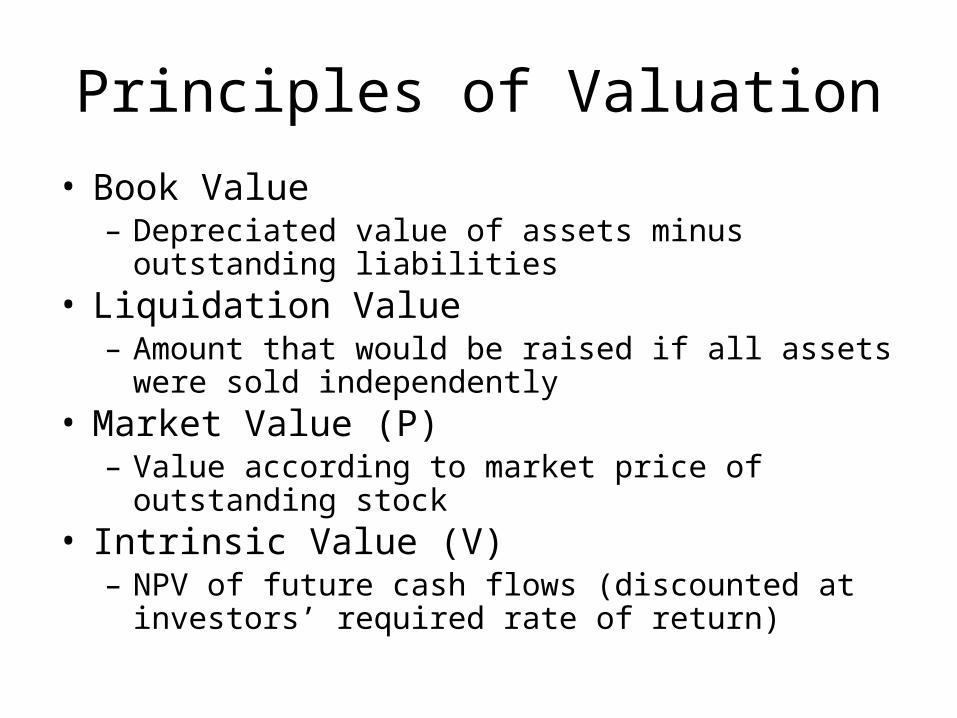

Principles of Valuation

• Book Value– Depreciated value of assets minus outstanding

liabilities• Liquidation Value

– Amount that would be raised if all assets were sold independently

• Market Value (P)– Value according to market price of outstanding stock

• Intrinsic Value (V)– NPV of future cash flows (discounted at investors’

required rate of return)

Tahap2 ValuationTahap2 analisis yang dilakukan pada valuasi ini meliputi:1. Analisis atas laporan keuangan untuk menilai kinerja

historis perusahaan serta melakukan normalisasi atas laporan keuangan tersebut, biasanya selama 5 tahun terakhir. Comparability Adjustments dengan perusahaan sejenis; Non-operating Adjustments (untuk asset non operasional), etc

2. Melakukan analisis atas strategi perusahaan dan analisis lingkungan industrinya, serta menetapkan berbagai skenario

3. Berdasarkan analisis strategi dan analisis lingkungan industri di atas di buat perkiraan atas laba-rugi (pendapatan dan biaya operasional) serta rencana investasi dan rencana penambahan modal kerja

4. Melakukan penilaian terhadap harga perusahaan atau harga saham dengan menggunakan beberapa model

Metode Valuasi

Beberapa metode yang dapat digunakan dalam melakukan penilaian perusahaan atau harga sahamnya adalah

1. Discounted Cash Flow Method 2. Book Value of Equity Method (Assets Based

Approach)3. Dividend Method 4. Price Earning Ratio Method5. Economic Value Added (EVA)and Market Value

Added (MVA) Method

Metode Valuasi

• Dalam valuasi ini metode yang banyak digunakan adalah metode Discounted Cash Flow (DCF) karena sesuai dengan prinsip dalam Time Value of Money dimana uang yang diterima sekarang lebih tinggi nilainya dari pada diterima pada masa datang

• Untuk mengetahui nilai perusahaan yang layak pada pendekatan atau model DCF diperlukan estimasi terhadap (1) increamental cash flow, (2) cost of capital (WACC)

Metode Valuasi

• Metode yang umum digunakan untuk memprediksi annual cash flow adalah dengan melakukan estimasi periode per periode sampai manajemen tidak terlalu yakin untuk melakukan estimasi lebih jauh.

• Hal ini sangat tergantung kepada (1) keadaan industri, apakah stabil atau bergejolak, (2) Kebijakan manajemen atau kemampuan manajemen dalam memproyeksikan masa datang

• Biasanya masa untuk periode per periode ini berkisar antara 5 sampai denga 10 tahun

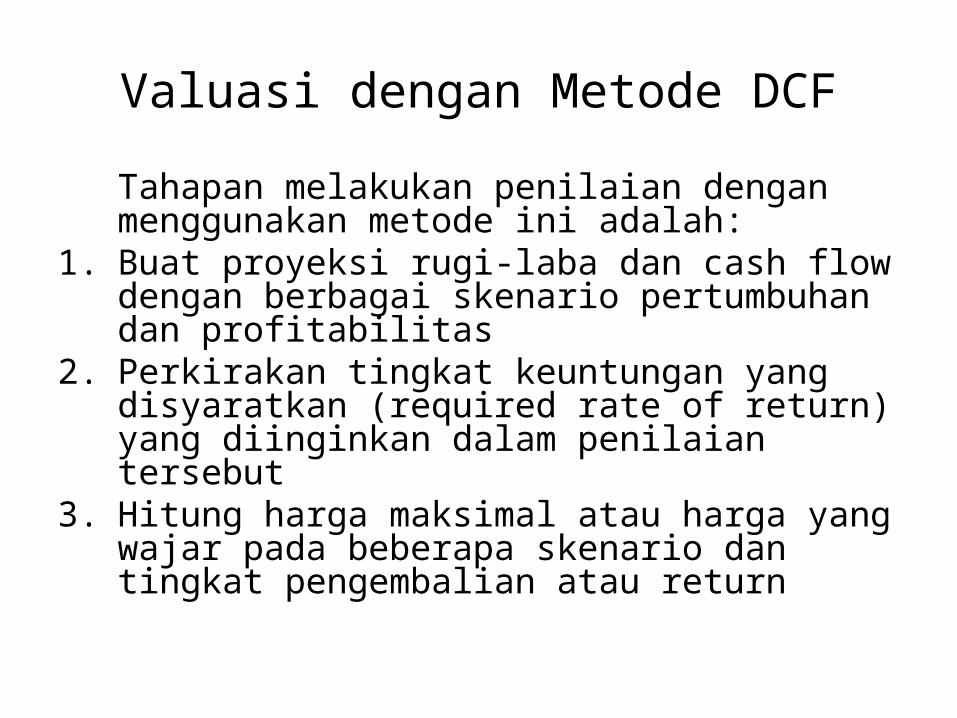

Valuasi dengan Metode DCF

Tahapan melakukan penilaian dengan menggunakan metode ini adalah:

1. Buat proyeksi rugi-laba dan cash flow dengan berbagai skenario pertumbuhan dan profitabilitas

2. Perkirakan tingkat keuntungan yang disyaratkan (required rate of return) yang diinginkan dalam penilaian tersebut

3. Hitung harga maksimal atau harga yang wajar pada beberapa skenario dan tingkat pengembalian atau return

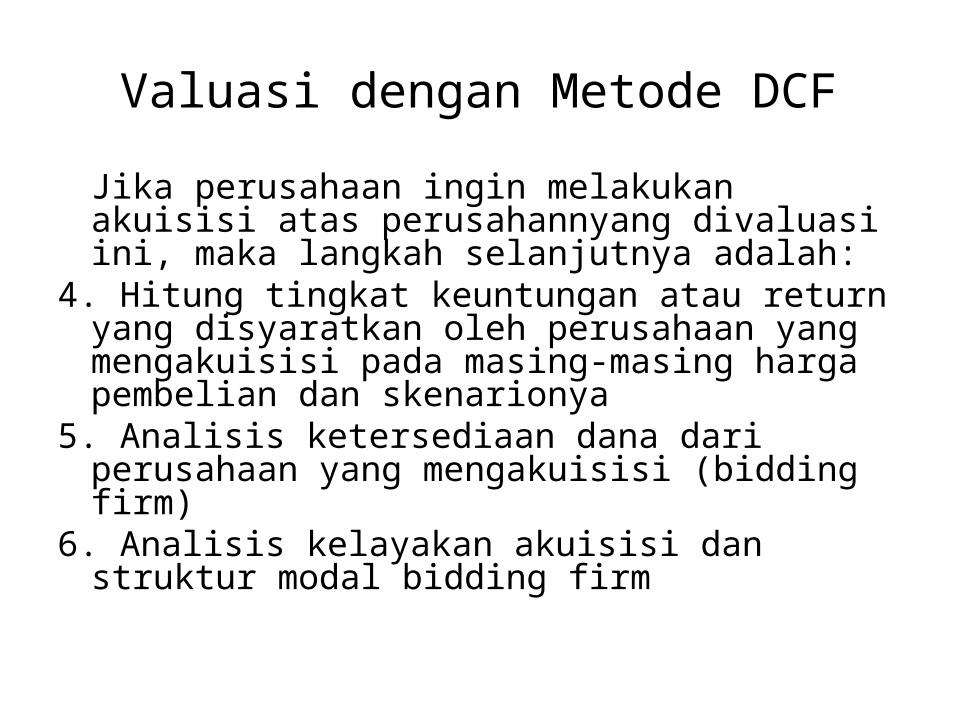

Valuasi dengan Metode DCF

Jika perusahaan ingin melakukan akuisisi atas perusahannyang divaluasi ini, maka langkah selanjutnya adalah:

4. Hitung tingkat keuntungan atau return yang disyaratkan oleh perusahaan yang mengakuisisi pada masing-masing harga pembelian dan skenarionya

5. Analisis ketersediaan dana dari perusahaan yang mengakuisisi (bidding firm)

6. Analisis kelayakan akuisisi dan struktur modal bidding firm

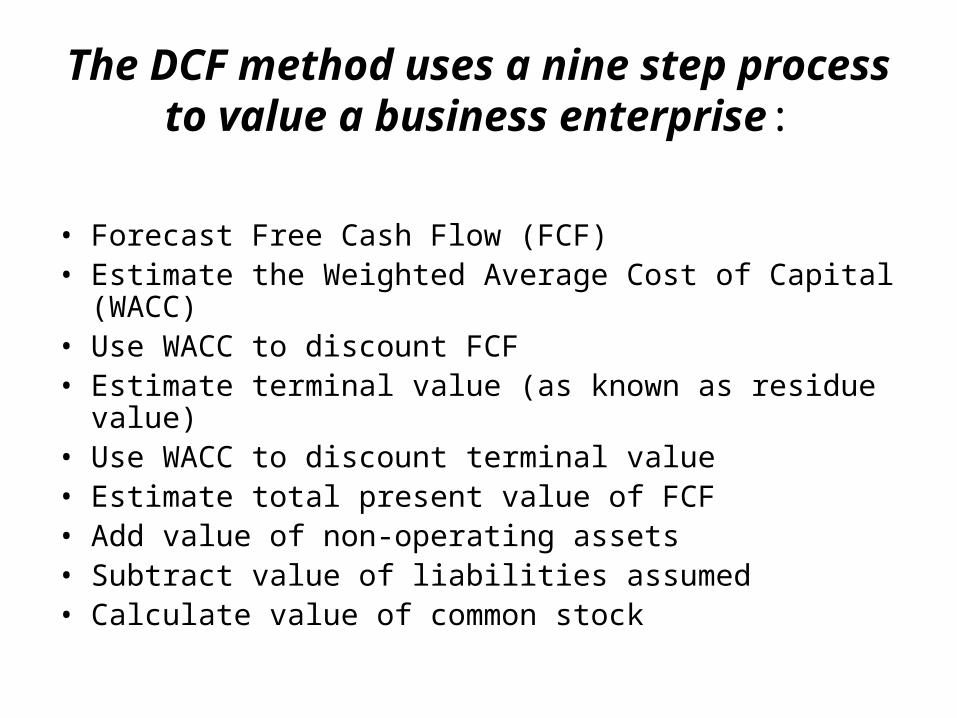

The DCF method uses a nine step process to value a business enterprise:

• Forecast Free Cash Flow (FCF) • Estimate the Weighted Average Cost of Capital (WACC) • Use WACC to discount FCF • Estimate terminal value (as known as residue value) • Use WACC to discount terminal value • Estimate total present value of FCF • Add value of non-operating assets • Subtract value of liabilities assumed • Calculate value of common stock

Valuasi dengan Metode DCF

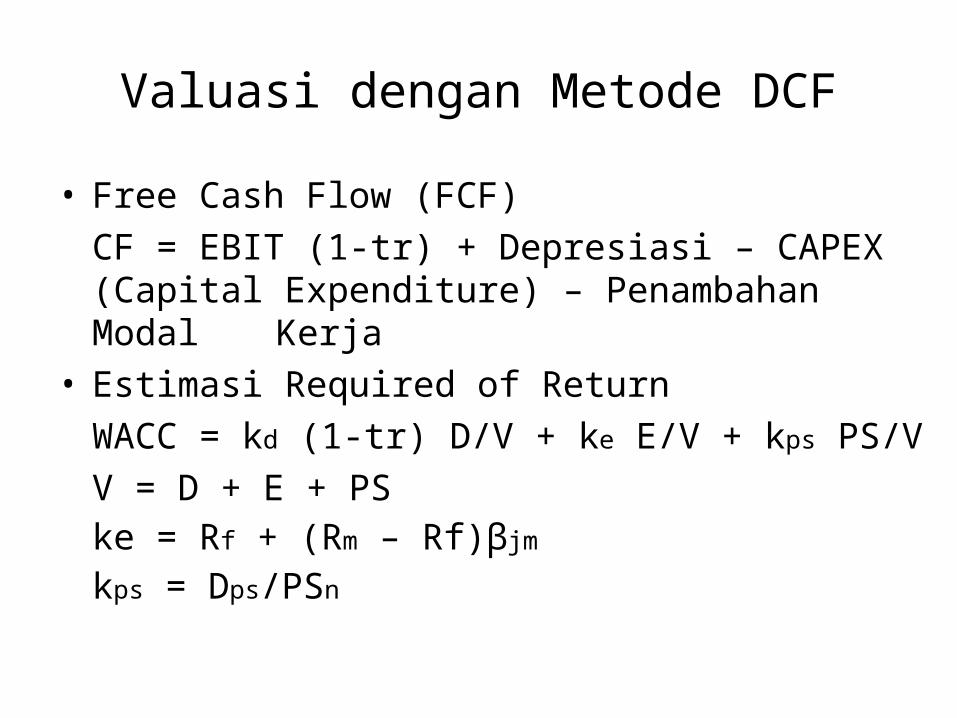

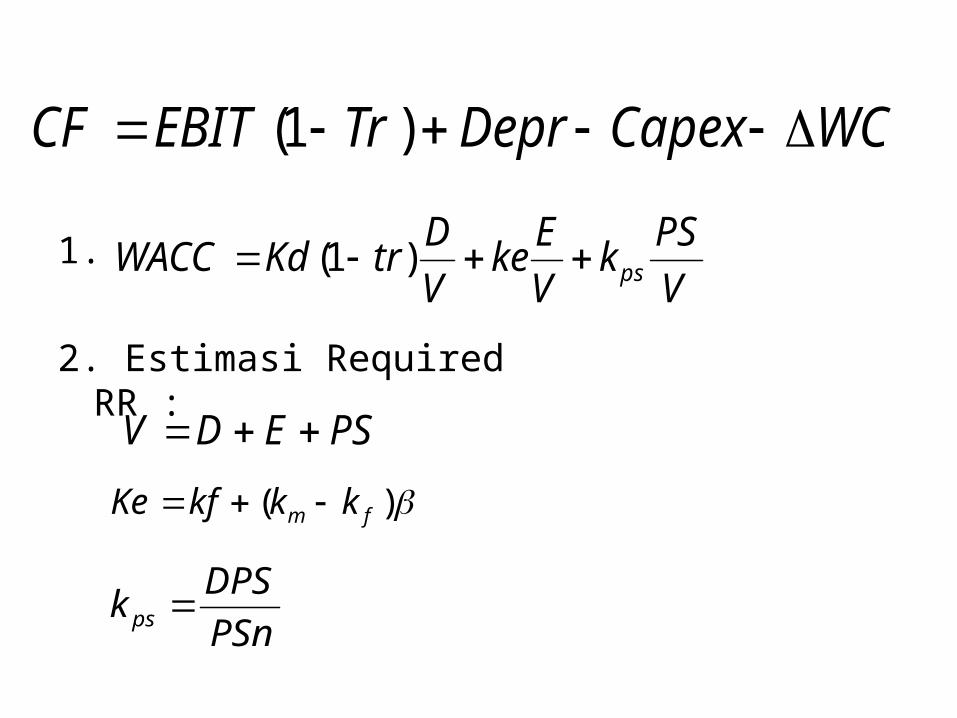

• Free Cash Flow (FCF)

CF = EBIT (1-tr) + Depresiasi – CAPEX (Capital Expenditure) – Penambahan Modal Kerja

• Estimasi Required of Return

WACC = kd (1-tr) D/V + ke E/V + kps PS/V

V = D + E + PSke = Rf + (Rm – Rf)βjm

kps = Dps/PSn

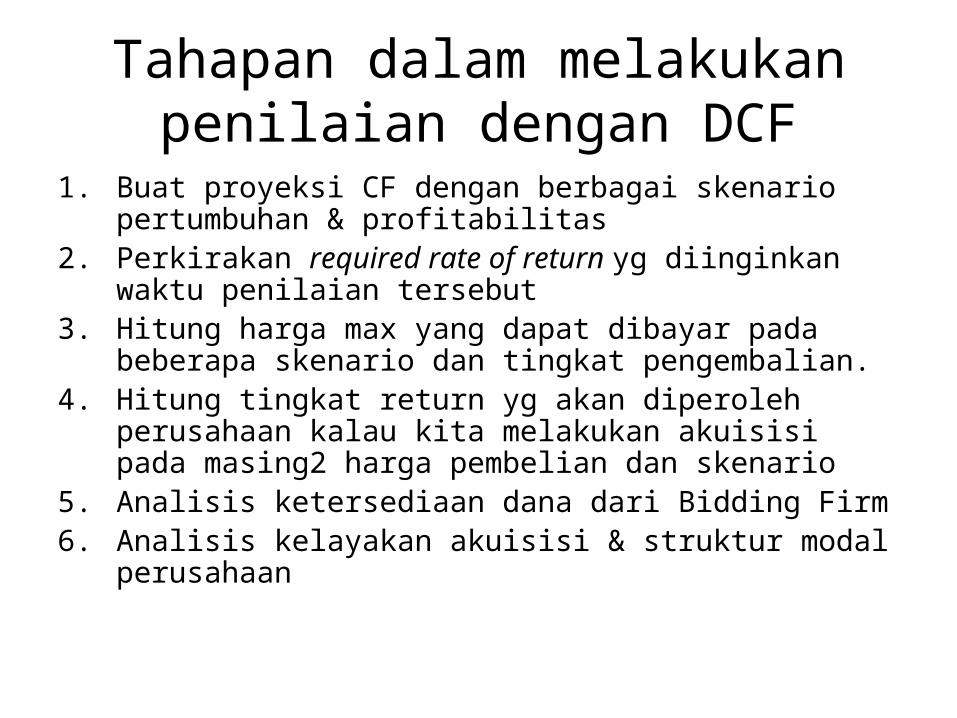

Tahapan dalam melakukan penilaian dengan DCF

1. Buat proyeksi CF dengan berbagai skenario pertumbuhan & profitabilitas

2. Perkirakan required rate of return yg diinginkan waktu penilaian tersebut

3. Hitung harga max yang dapat dibayar pada beberapa skenario dan tingkat pengembalian.

4. Hitung tingkat return yg akan diperoleh perusahaan kalau kita melakukan akuisisi pada masing2 harga pembelian dan skenario

5. Analisis ketersediaan dana dari Bidding Firm6. Analisis kelayakan akuisisi & struktur modal

perusahaan

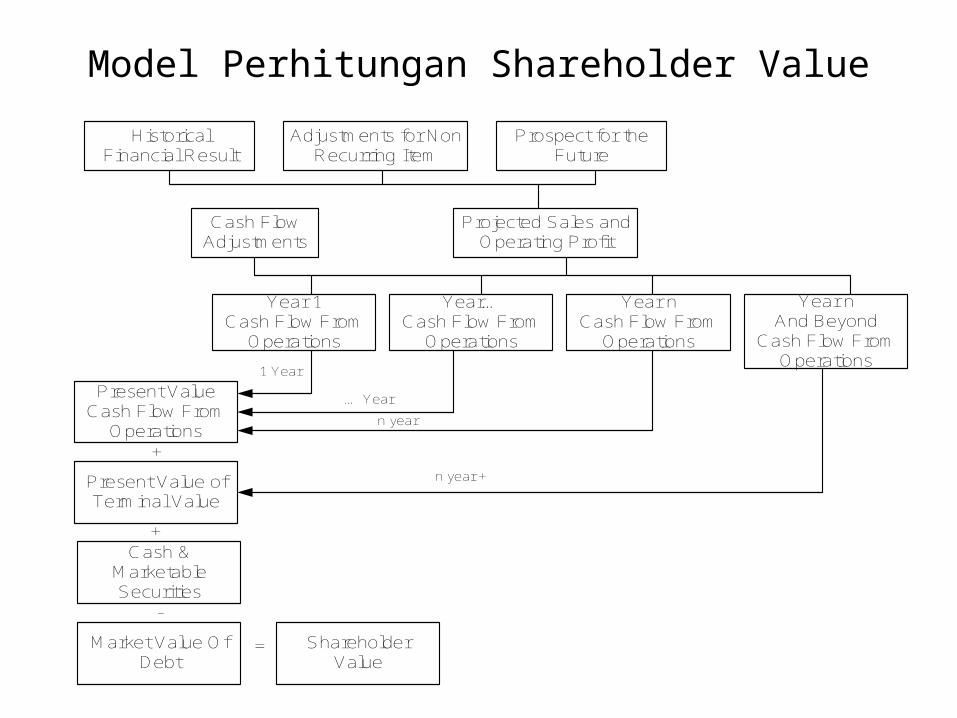

Model Perhitungan Shareholder Value

Historical Financial Result

Adjustments for Non Recurring Item

Prospect for the Future

Cash Flow Adjustments

Projected Sales and Operating Profit

Year 1Cash Flow From

Operations

Year…Cash Flow From

Operations

Year nCash Flow From

Operations

Year nAnd Beyond

Cash Flow From Operations

Present Value Cash Flow From

Operations

Present Value of Terminal Value

+

Cash & Marketable Securities

+

Market Value Of Debt

-

Shareholder Value

=

1 Year

… Year

n year

n year +

1.

2. Estimasi Required RR :

WCCapexDeprTrEBITCF )1(

PSEDV

)( fm kkkfKe

PSn

DPSk ps

V

PSk

V

Eke

V

DtrKdWACC ps )1(

Short Cut Method:

2/)/()

( PnPn

PnPBKd

Accurate Method

k

tnkd

bPn1 )1(

1

k

tnt

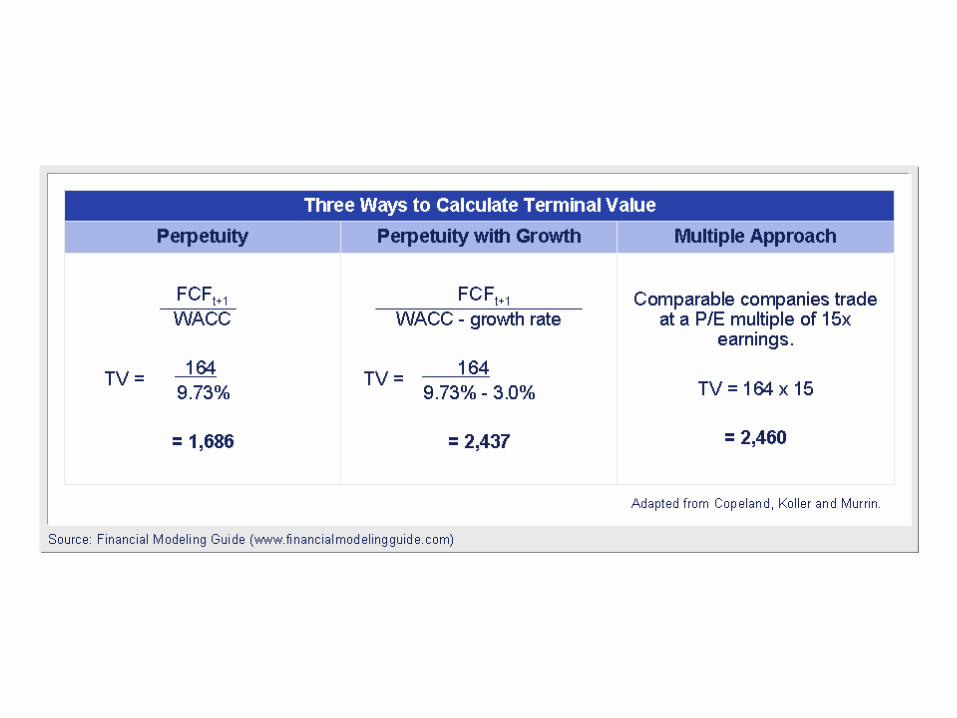

tDCF WACC

TV

WAACC

CFPV

1 )1()1(

TV = Terminal Value, CF, g = Pertumbuhan CF Secara Konstan

V

PSk

V

Eke

V

DtrKdWACC ps )1(

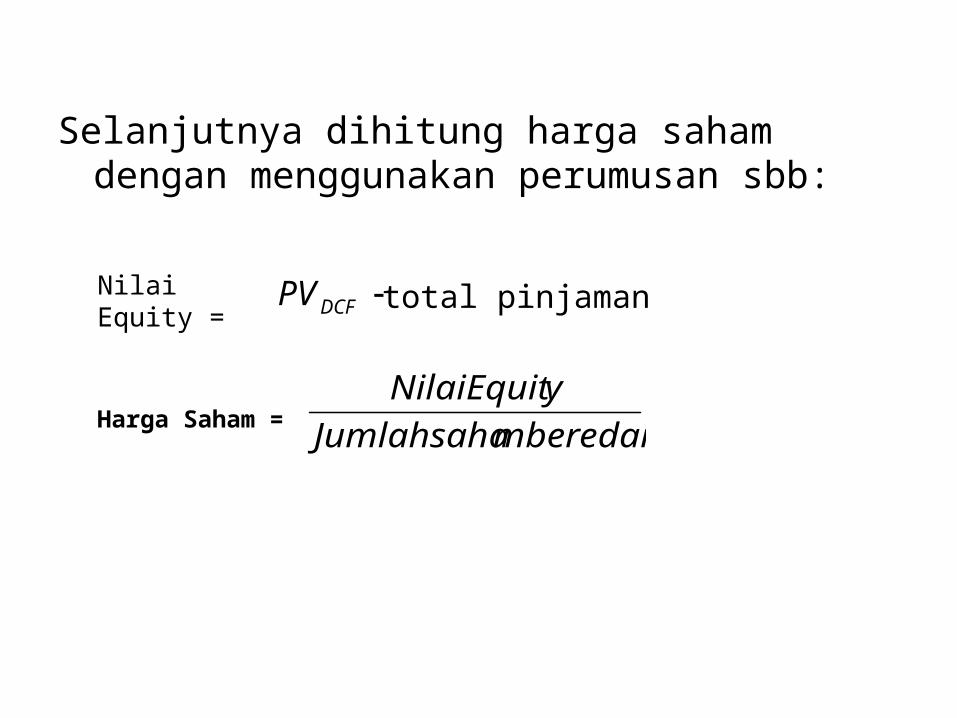

Selanjutnya dihitung harga saham dengan menggunakan perumusan sbb:

Nilai Equity = DCFPV total pinjaman

Harga Saham = mberedarJumlahsaha

yNilaiEquit

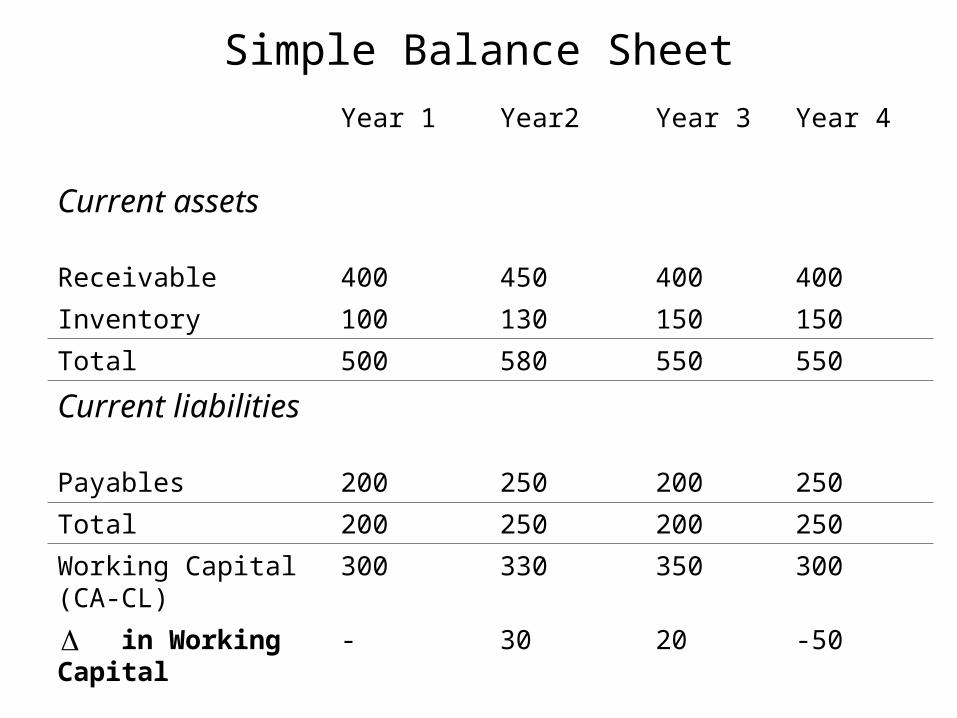

Simple Balance Sheet

Year 1 Year2 Year 3 Year 4

Current assets

Receivable 400 450 400 400

Inventory 100 130 150 150

Total 500 580 550 550

Current liabilities

Payables 200 250 200 250

Total 200 250 200 250

Working Capital(CA-CL)

300 330 350 300

in Working Capital - 30 20 -50

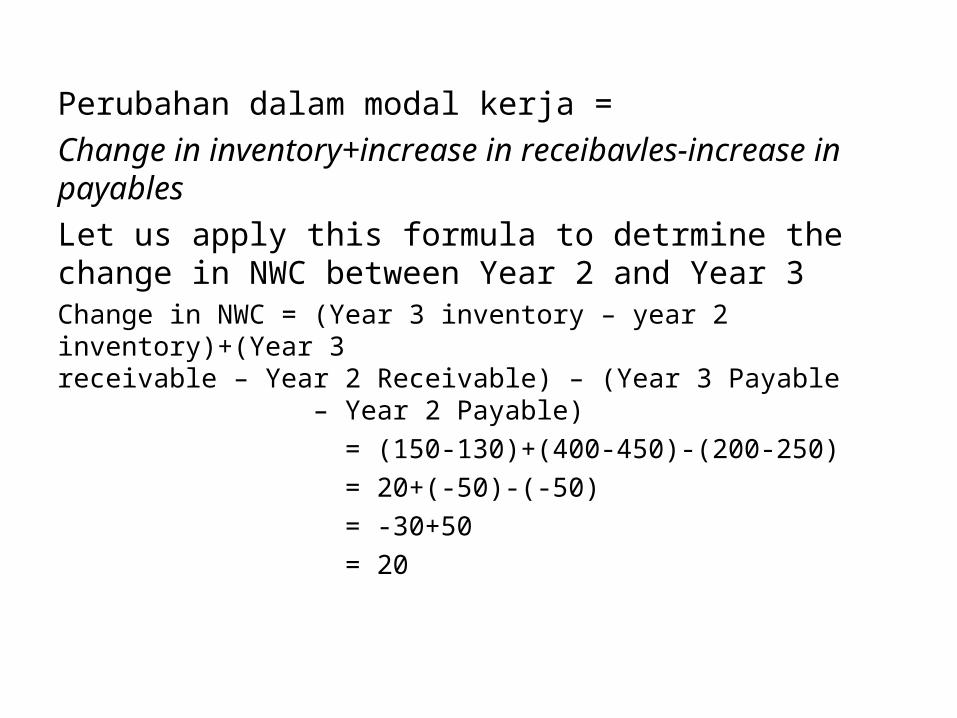

Perubahan dalam modal kerja =

Change in inventory+increase in receibavles-increase in payables

Let us apply this formula to detrmine the change in NWC between Year 2 and Year 3Change in NWC = (Year 3 inventory – year 2 inventory)+(Year 3

receivable – Year 2 Receivable) – (Year 3 Payable – Year 2 Payable)

= (150-130)+(400-450)-(200-250)

= 20+(-50)-(-50)

= -30+50

= 20

Income Statement

Year 1 Year 2 Year 3

Revenue 3.000 3.500 4.000

Less: COGS (1.950) (2.275) (2.600)

Gross profit 1.050 1.225 1.400

Less: Administrative expense (150) (175) (200)

Less: Sales expence (180) (210) (240)

EBITDA 720 840 960

Less : Depreciation&Amort (165) (170) (175)

EBIT 555 670 785

Less: Interest expence (net) (110) (120) (125)

EBT (pre-tax profit) 445 550 660

Less:Tax (125) (154) (185)

Net profit 320 396 475

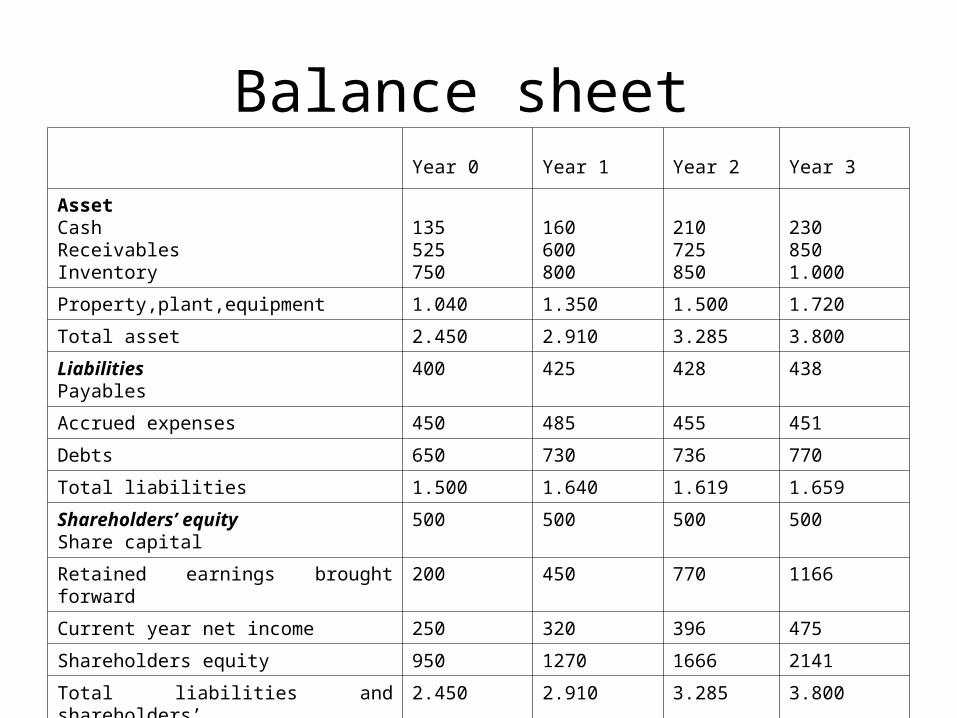

Balance sheet Year 0 Year 1 Year 2 Year 3

AssetCashReceivablesInventory

135525750

160600800

210725850

2308501.000

Property,plant,equipment 1.040 1.350 1.500 1.720

Total asset 2.450 2.910 3.285 3.800

Liabilities Payables

400 425 428 438

Accrued expenses 450 485 455 451

Debts 650 730 736 770

Total liabilities 1.500 1.640 1.619 1.659

Shareholders’ equityShare capital

500 500 500 500

Retained earnings brought forward 200 450 770 1166

Current year net income 250 320 396 475

Shareholders equity 950 1270 1666 2141

Total liabilities and shareholders’ 2.450 2.910 3.285 3.800

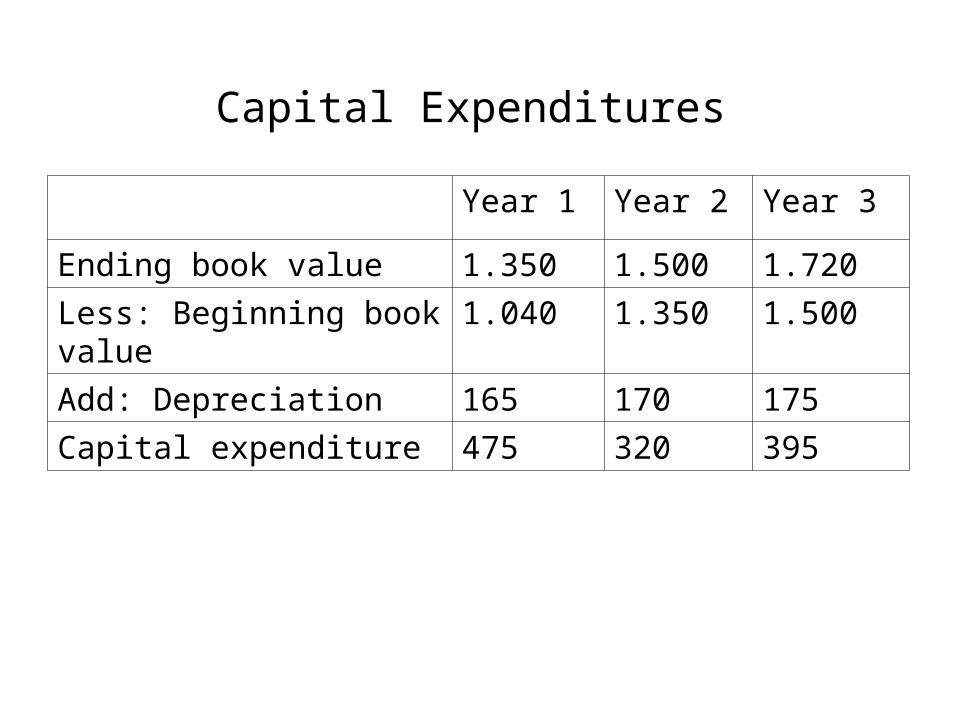

Capital Expenditures

Year 1 Year 2 Year 3

Ending book value 1.350 1.500 1.720

Less: Beginning book value 1.040 1.350 1.500

Add: Depreciation 165 170 175

Capital expenditure 475 320 395

Perhitungan perubahan NWC

Year 0 Year 1 Year 2 Year 3

Non-cash current assets Receivables 525 600 725 850

Inventory 750 800 850 1.000

Total current assets 1.275 1.400 1.575 1.850

Current Liabilities (Account Payables)

400 425 428 438

Accrued Expenses 450 485 455 451

Total Current Liabilities 850 910 883 889

Net working capital 425 490 692 961

Change in working capital 65 202 269

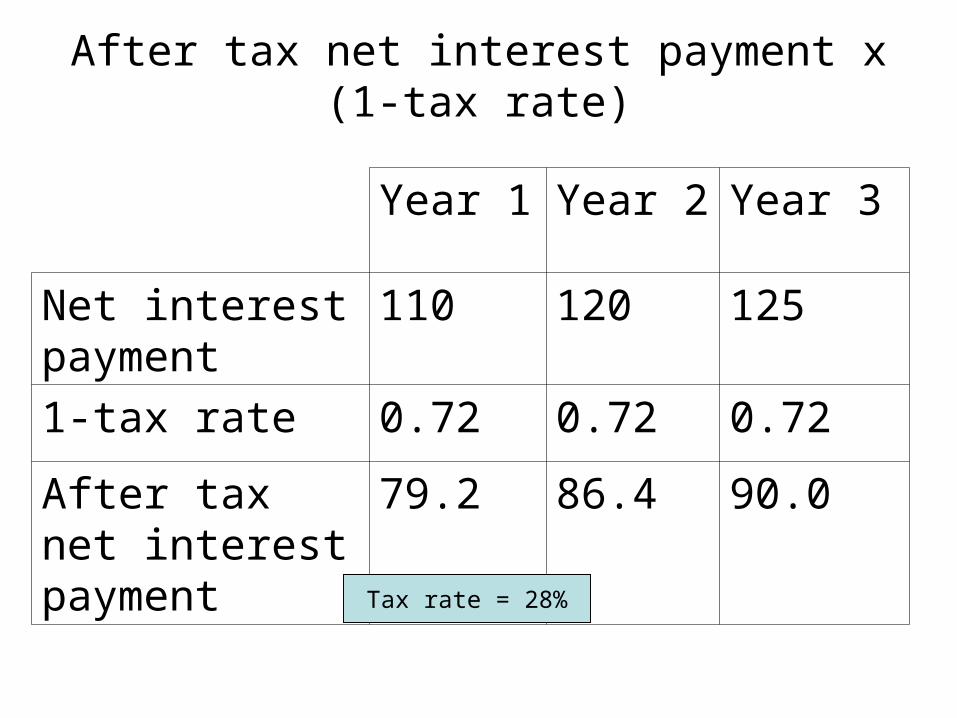

After tax net interest payment x (1-tax rate)

Year 1 Year 2 Year 3

Net interest payment

110 120 125

1-tax rate 0.72 0.72 0.72

After tax net interest payment

79.2 86.4 90.0

Tax rate = 28%

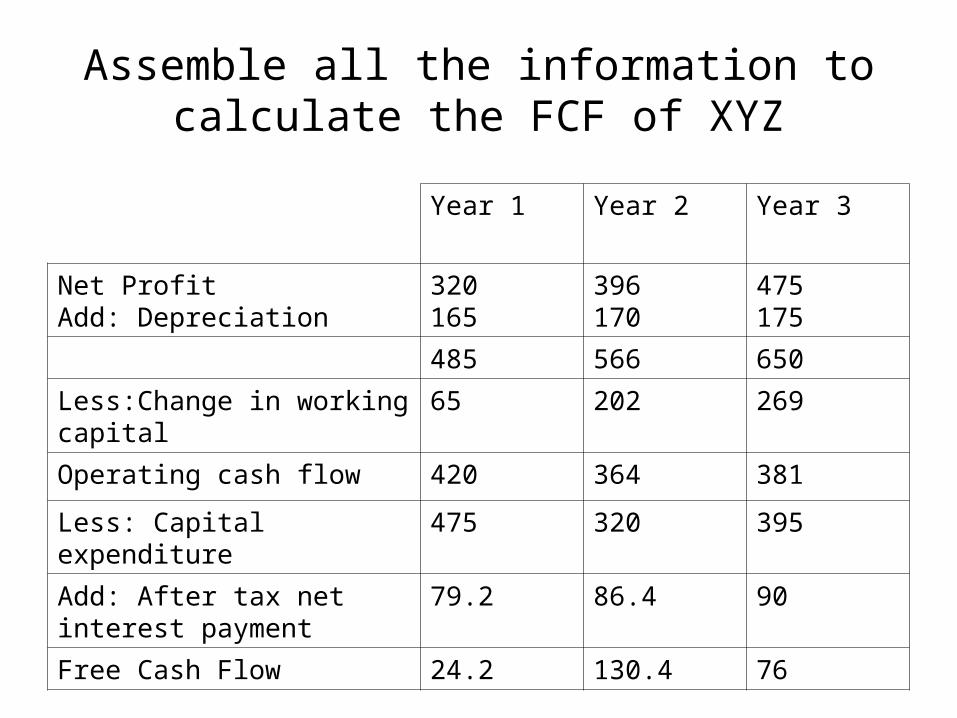

Assemble all the information to calculate the FCF of XYZ

Year 1 Year 2 Year 3

Net ProfitAdd: Depreciation

320165

396170

475175

485 566 650

Less:Change in working capital 65 202 269

Operating cash flow 420 364 381

Less: Capital expenditure 475 320 395

Add: After tax net interest payment

79.2 86.4 90

Free Cash Flow 24.2 130.4 76

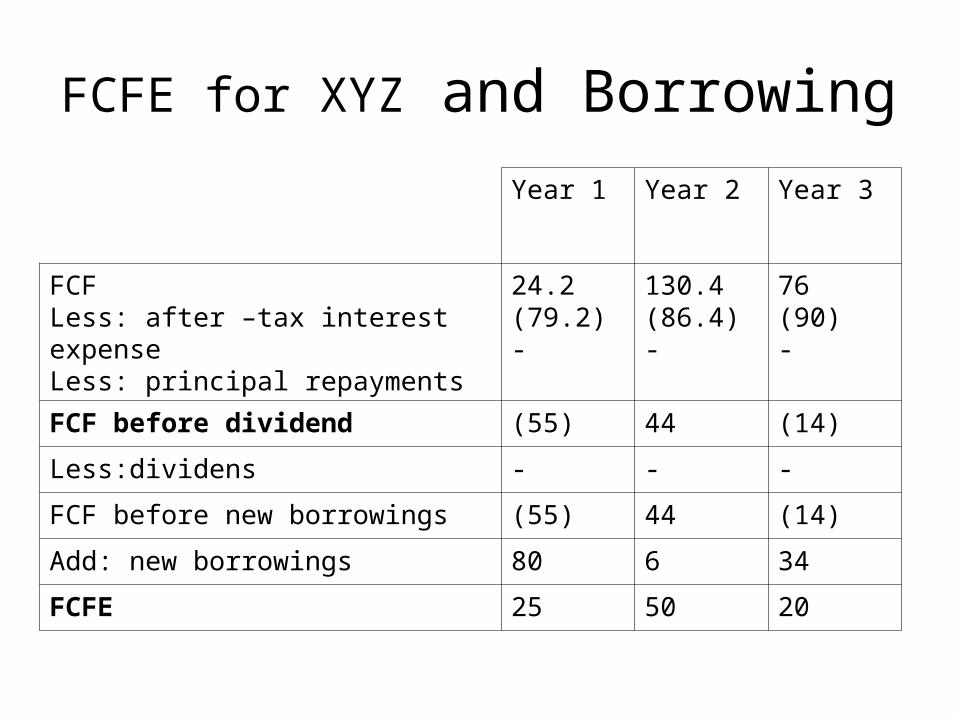

FCFE for XYZ and Borrowing

Year 1 Year 2 Year 3

FCFLess: after –tax interest expenseLess: principal repayments

24.2(79.2)-

130.4(86.4)-

76(90)-

FCF before dividend (55) 44 (14)

Less:dividens - - -

FCF before new borrowings (55) 44 (14)

Add: new borrowings 80 6 34

FCFE 25 50 20

How to Get the Best Price When Selling a Business

Selling a business is the most popular exit strategy for business owners. In some cases, there are no successors who want to continue the business; in others, it was always the business owner's plan to convert the business into liquid assets at a certain point. Whatever the reason you want to sell yours, following these tips for selling a business will help ensure that you get the best price and that your business sells.

How to Get the Best Price When Selling a Business

1) Sell at the right time for the right reasons.The most common reason for selling a business is that a business owner falls ill or gets too old to continue to run it - the worst time to be selling a business. For one thing, it's going to be extremely difficult for you to deal with the additional stress of selling a business in those circumstances; for another, the buyer will use your circumstances as leverage against you.So don't wait until then. The right time is when you're still hale and hearty and have a successful business to sell.And what are the right reasons? Selling a business is very like selling a house in some respects. When you're selling a house, you don't say that you want to sell because the house is too small. You say that you want to move to be closer to work, for instance. When selling a business, you want to sell because you want to pursue a different opportunity or because you're seeking a different lifestyle (such as retirement).

How to Get the Best Price (cont’d)

2) Be clear about what you're selling.Before selling a business, you need to consider what all the assets of a business are and decide what you are selling. Determine what physical assets you are selling and what other assets you have to sell. Selling a business often includes assets such as good will, trademarks or client lists as well as physical assets. The value of these will depend on their quality.If your business is incorporated, you also need to decide if you are going to sell your business as an asset sale (where you sell everything in the corporation but not the incorporated company itself) or a share sale (where you sell everything including your incorporated company).

How to Get the Best Price (cont’d)3) Determine what your business is actually

worth.Facetiously but truthfully, your business is worth as much as it will fetch in the marketplace. But determining just what that price is the trick. There are several different business valuation methods ranging from asset-based to future earnings approaches. Of course, no one approach can be used in isolation; the current market, economic trends and what other similar businesses have sold for also need to be taken into account.If I was only going to give one piece of advice about selling a business, it would be to have a professional business valuation done. While legally anyone can do a business valuation, a business valuation done by a professional will be regarded more favorably by potential buyers and may save you legal hassles later on."...a number of court cases have recognized the distinction between evidence provided by a qualified business valuator and that provided by someone without the same degree of competence and education" ("How Much Is Your Business Worth?", Grant Thornton LLP).

How to Get the Best Price (cont’d)

4) Make sure your house is in order.When you're selling your business, you need to be especially careful not to let things slide. In fact, this is the time that making the extra effort to keep things in tip-top shape can really pay off. Think again of selling a house; like a house that's up for sale, you want your business to show well.So whether you have any interest left in running the business, you need to make sure that you are keeping the business's records up to date, the inventory up and the premises maintained. People want to buy thriving businesses, not neglected ones.

How to Get the Best Price (cont’d)

5) Get professional help when selling a business.Selling a business is an even more complex transaction than selling a house - and arguably, one that has even more emotional impact. Besides providing necessary expertise to guide you through the selling process, hiring professional help can help you maintain the emotional distance and objectivity you need to successfully sell your business.Which professionals should you hire?As already mentioned, a professional valuator can determine what your business is worth. His or her valuation will be much more credible to a potential buyer than yours. A commercial realtor or business broker can be a real boon in terms of finding and dealing with prospective buyers of your business and helping you navigate the sales process.A lawyer can draw up and/or review the documents necessary to sell your business, such as the document that summarizes your business for prospective buyers and the purchase and sales agreement.