Embed Size (px)

DESCRIPTION

p

Citation preview

i ii

PLANNING ALGORITHMS

Steven M. LaValle

University of Illinois

Copyright 1999-2003

Contents

Preface ix

0.1 What is meant by “Planning Algorithms”? . . . . . . . . . . . . . ix

0.2 Who is the Intended Audience? . . . . . . . . . . . . . . . . . . . x

0.3 Suggested Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . x

0.4 Acknowledgments . . . . . . . . . . . . . . . . . . . . . . . . . . . x

0.5 Help! . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xi

I Introductory Material 1

1 Introduction 3

1.1 Planning to Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2 Illustrative Problems . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.3 Perspective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.4 Mathematical and Algorithmic Preliminaries . . . . . . . . . . . . 8

2 Discrete Planning 9

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.2 Three Representations of Discrete Planning . . . . . . . . . . . . 10

2.2.1 STRIPS-Like Representation . . . . . . . . . . . . . . . . . 10

2.2.2 State Space Representation . . . . . . . . . . . . . . . . . 12

2.2.3 Graph Representation . . . . . . . . . . . . . . . . . . . . 14

2.3 Search Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.3.1 General Forward Search . . . . . . . . . . . . . . . . . . . 15

2.3.2 Particular Forward Search Methods . . . . . . . . . . . . . 17

2.3.3 Other General Search Schemes . . . . . . . . . . . . . . . . 20

2.4 Optimal Planning . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.4.1 State space formulation . . . . . . . . . . . . . . . . . . . . 22

2.4.2 Backwards dynamic programming . . . . . . . . . . . . . . 23

2.4.3 Forward dynamic programming . . . . . . . . . . . . . . . 24

2.4.4 A simple example . . . . . . . . . . . . . . . . . . . . . . . 25

2.5 Other Approaches . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

iii

iv CONTENTS

II Motion Planning 29

3 Geometric Representations and Transformations 333.1 Geometric Modeling . . . . . . . . . . . . . . . . . . . . . . . . . 33

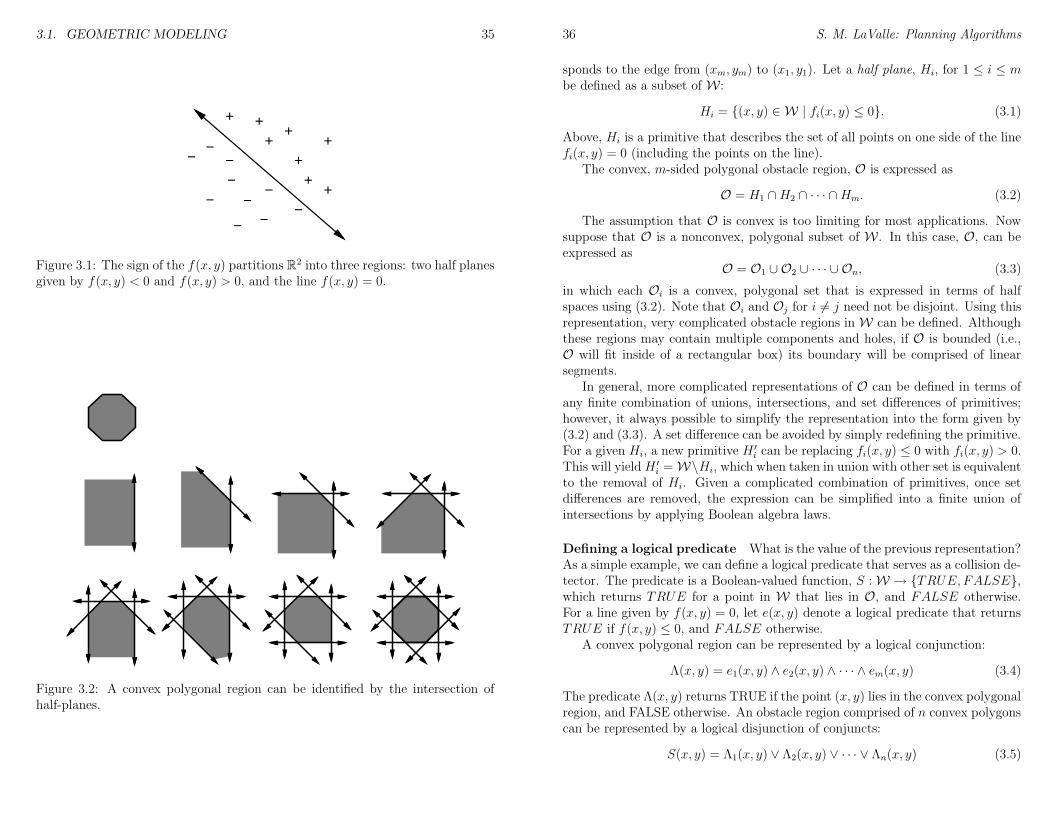

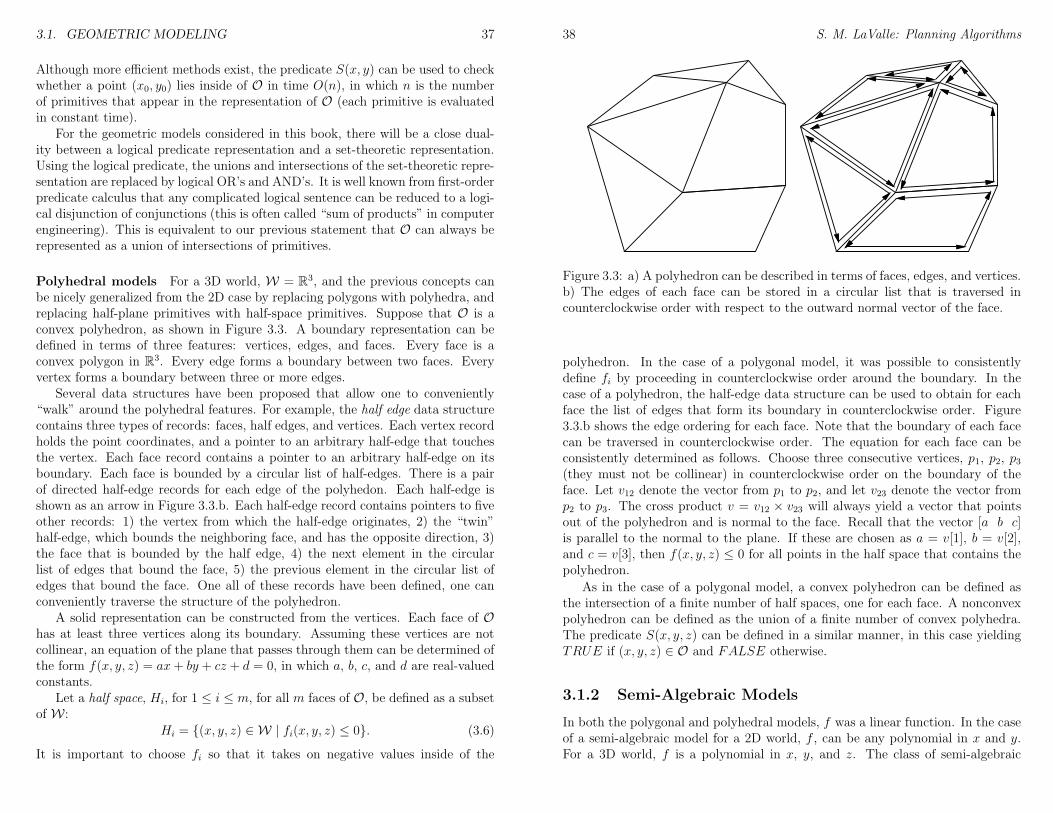

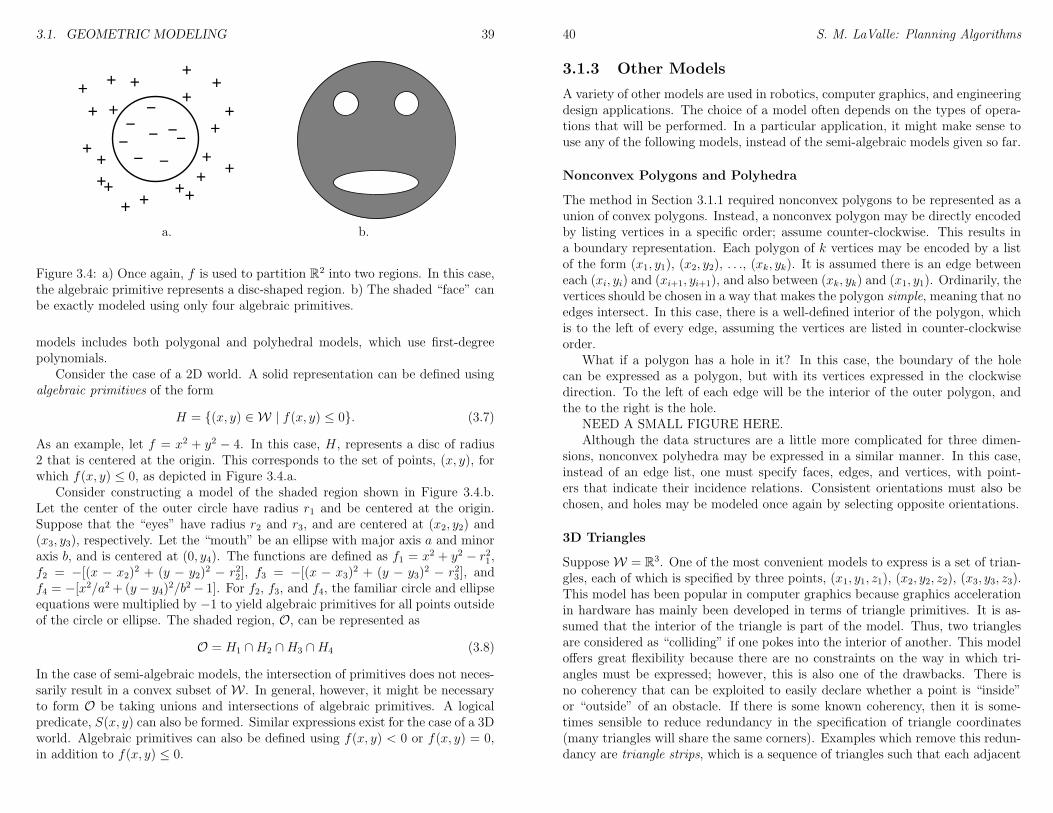

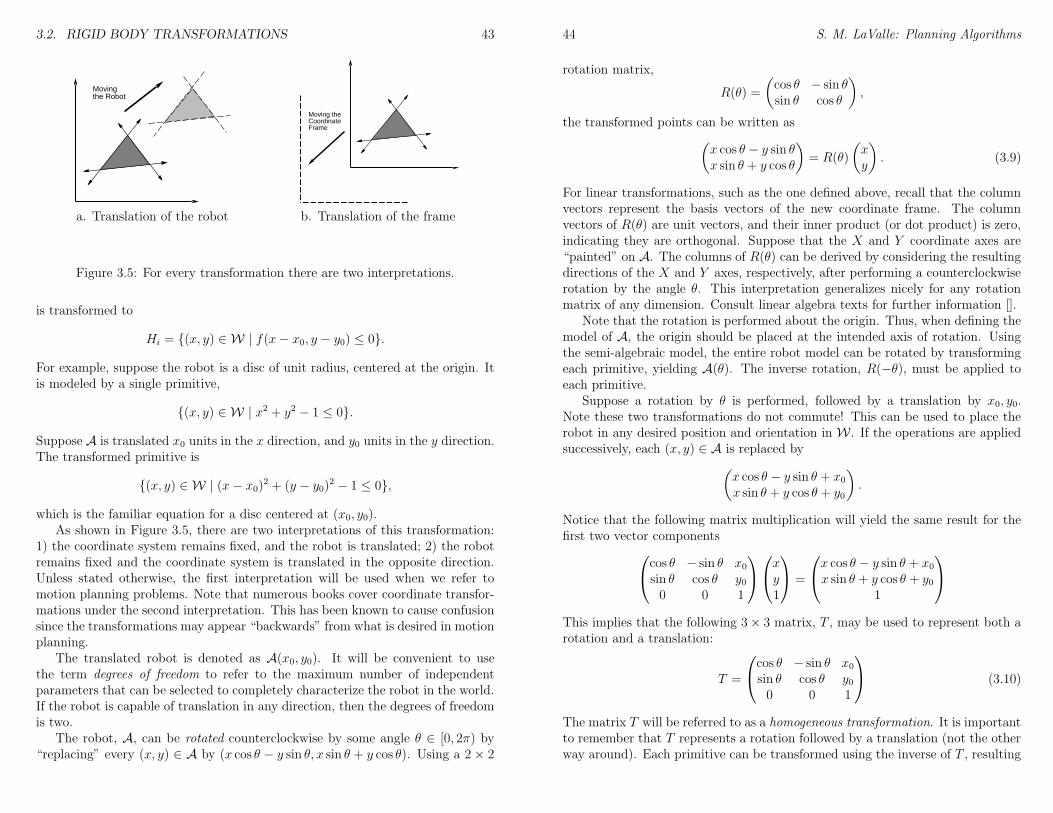

3.1.1 Polygonal and Polyhedral Models . . . . . . . . . . . . . . 343.1.2 Semi-Algebraic Models . . . . . . . . . . . . . . . . . . . . 383.1.3 Other Models . . . . . . . . . . . . . . . . . . . . . . . . . 40

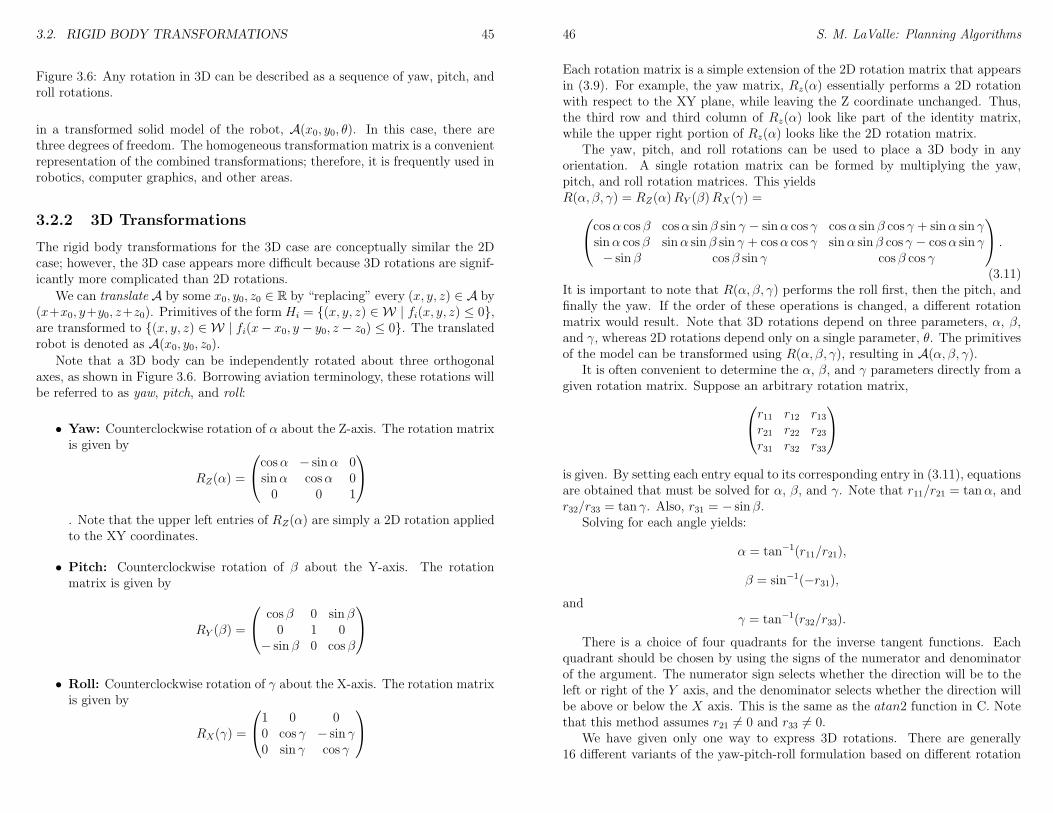

3.2 Rigid Body Transformations . . . . . . . . . . . . . . . . . . . . . 423.2.1 2D Transformations . . . . . . . . . . . . . . . . . . . . . . 423.2.2 3D Transformations . . . . . . . . . . . . . . . . . . . . . . 45

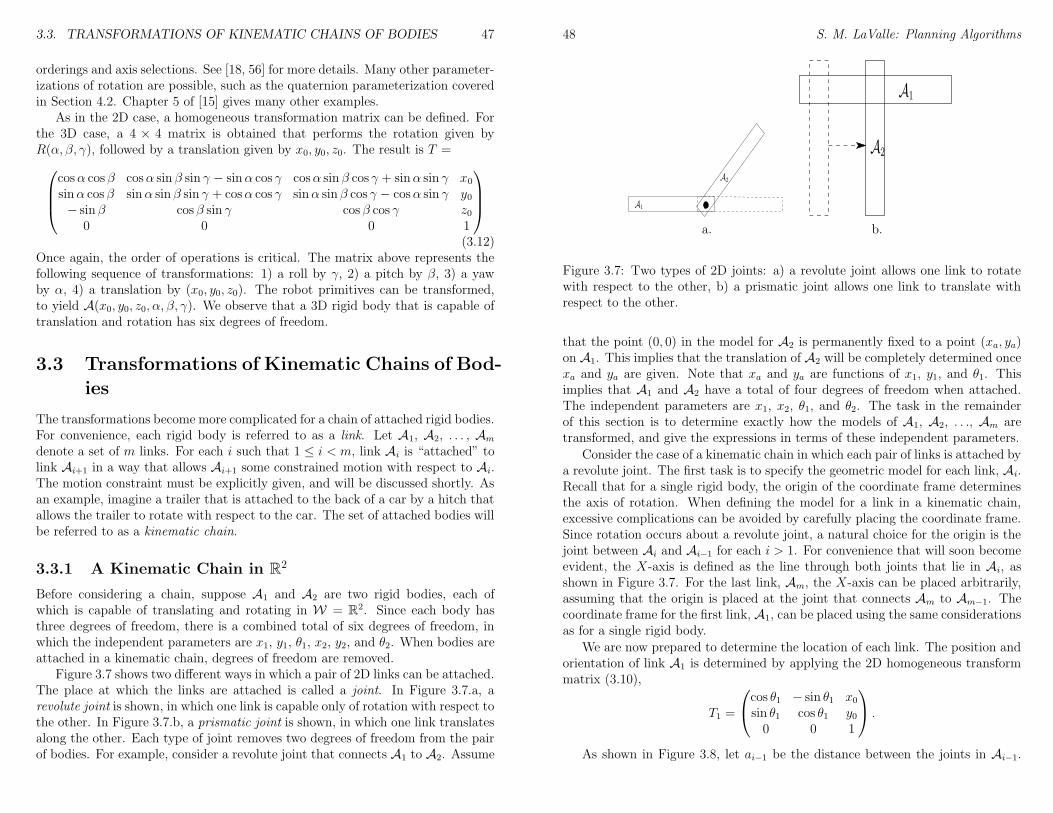

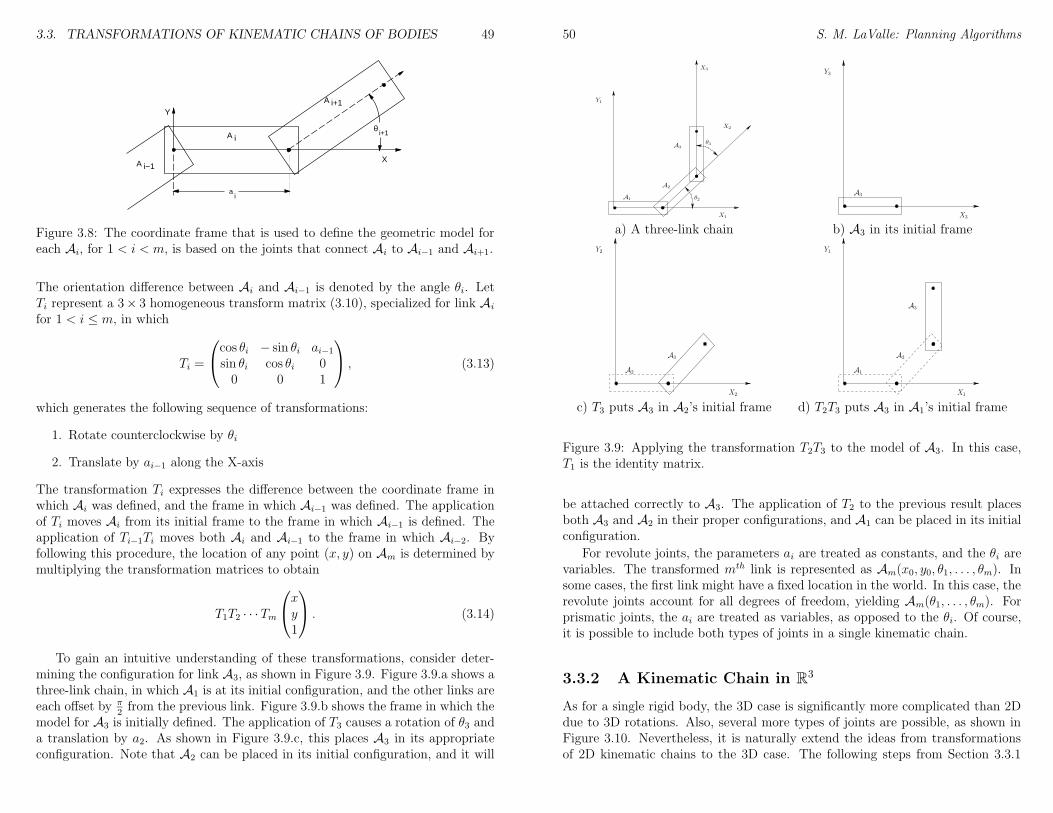

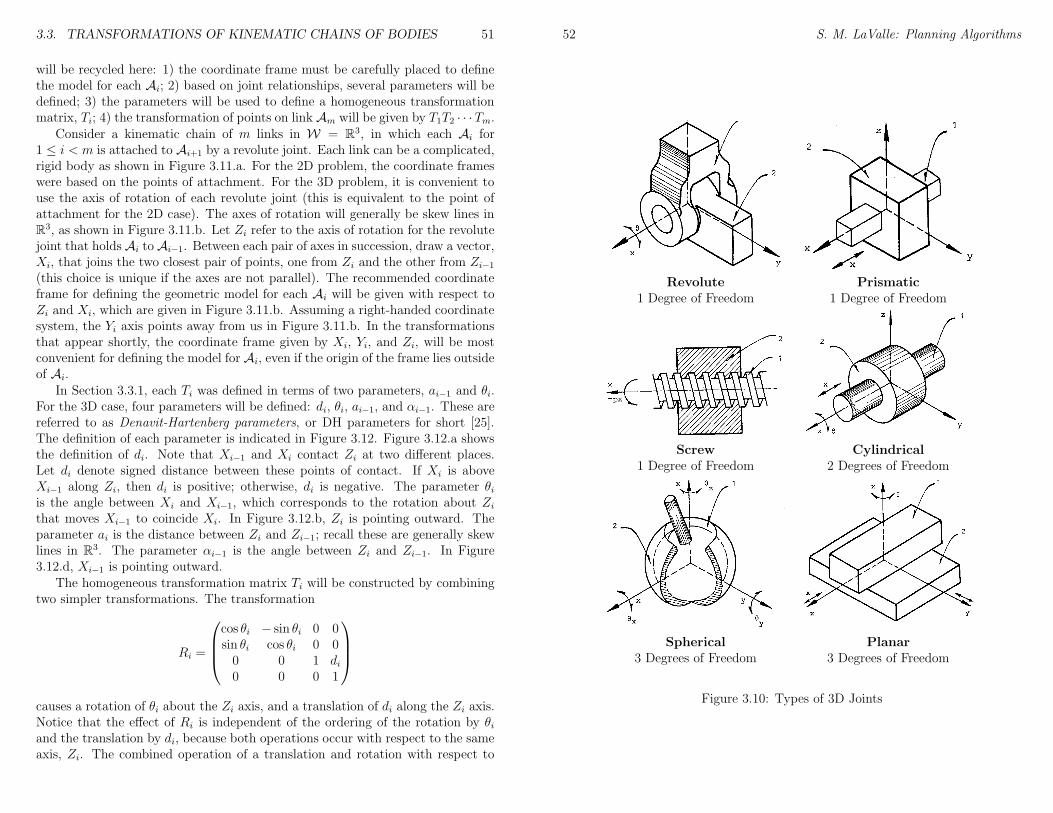

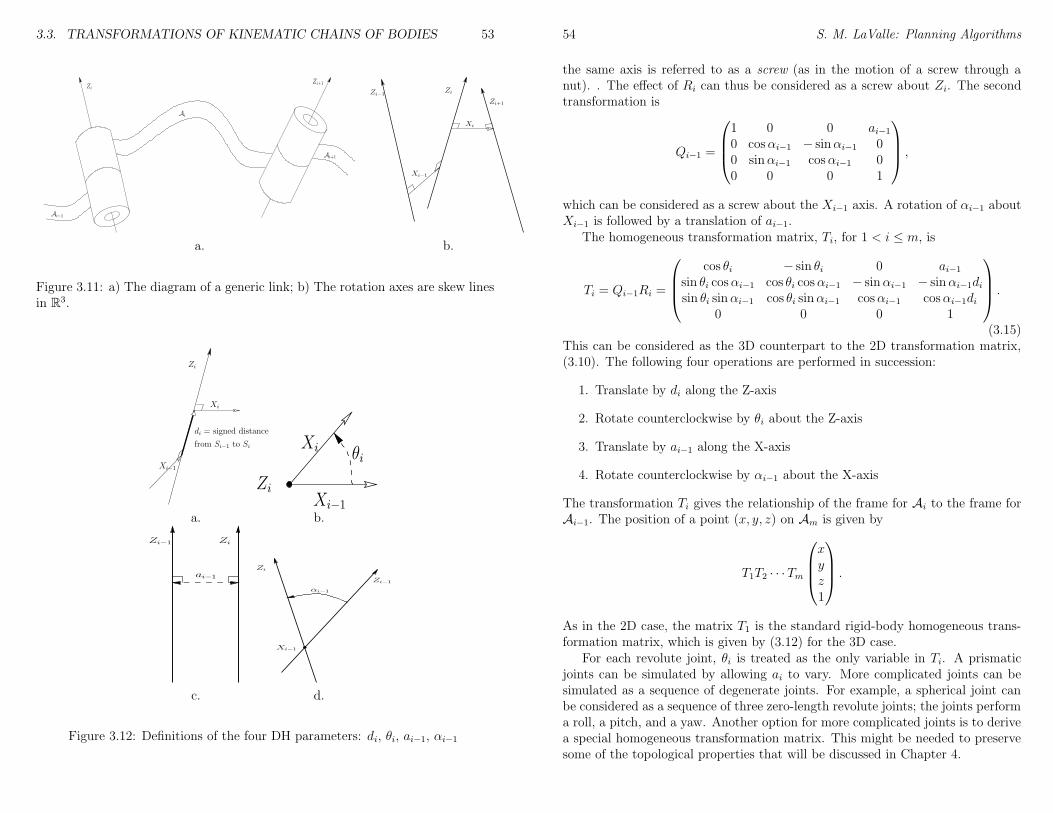

3.3 Transformations of Kinematic Chains of Bodies . . . . . . . . . . 473.3.1 A Kinematic Chain in R2 . . . . . . . . . . . . . . . . . . 473.3.2 A Kinematic Chain in R3 . . . . . . . . . . . . . . . . . . 50

3.4 Transforming Other Models . . . . . . . . . . . . . . . . . . . . . 55

4 The Configuration Space 594.1 Basic Topological Concepts . . . . . . . . . . . . . . . . . . . . . 59

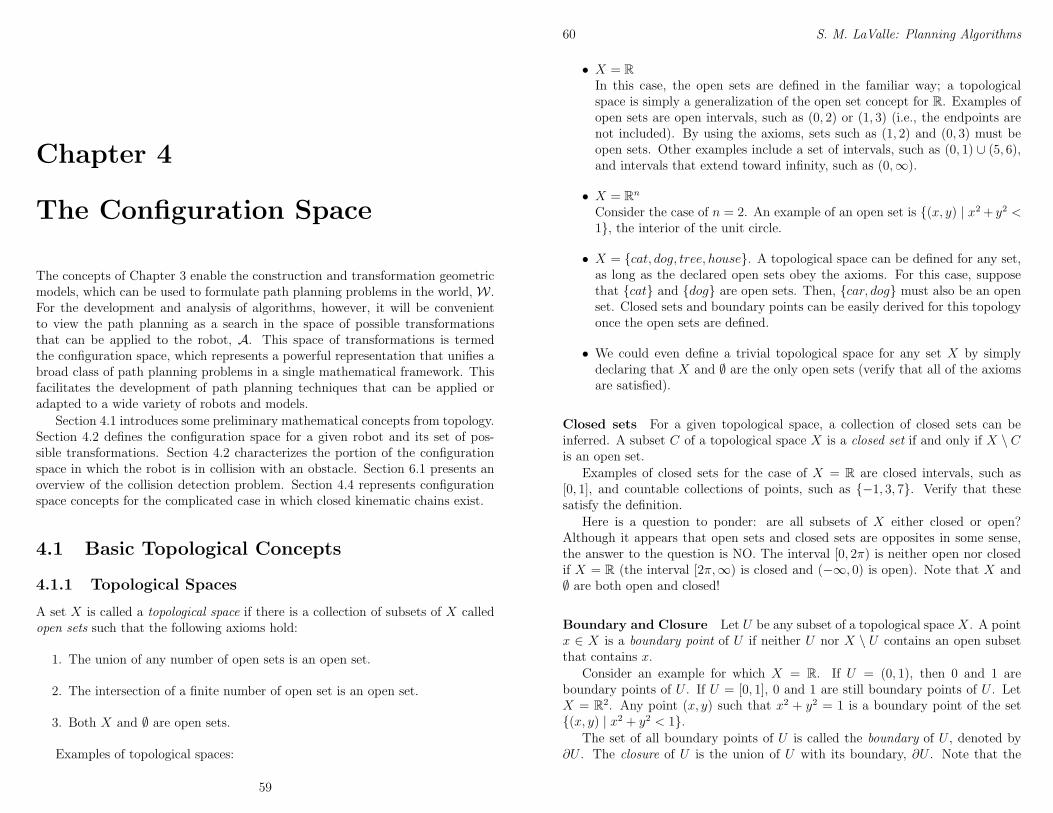

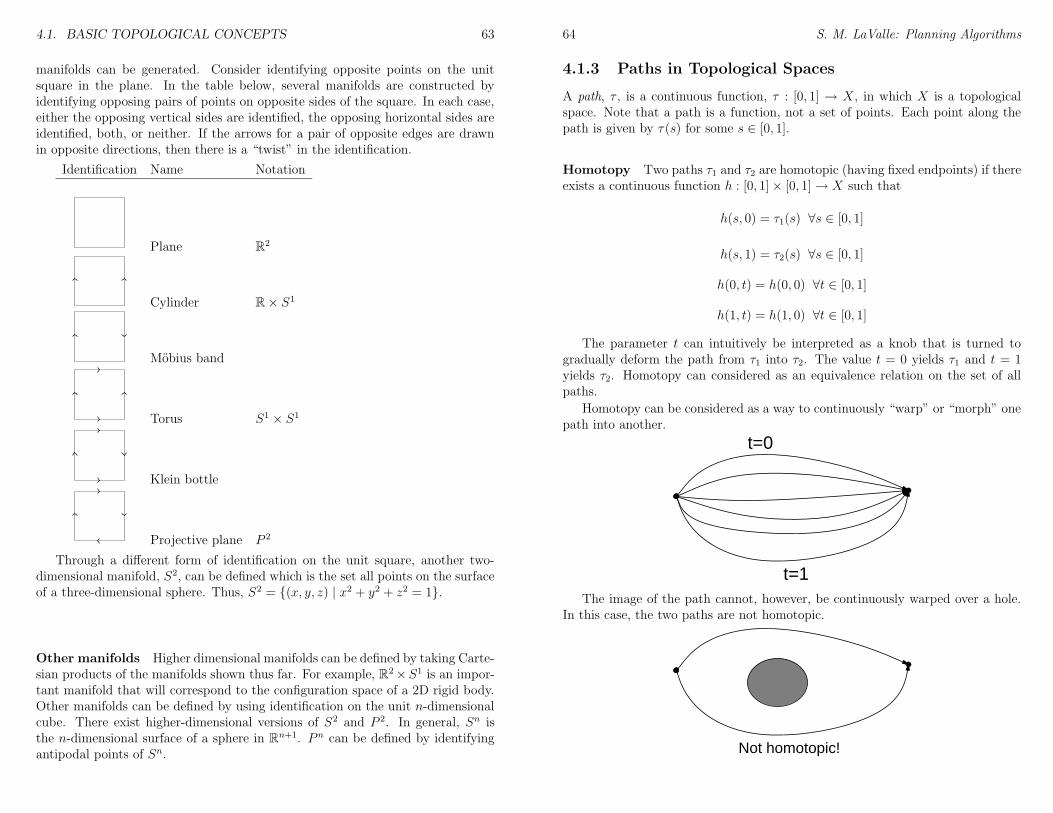

4.1.1 Topological Spaces . . . . . . . . . . . . . . . . . . . . . . 594.1.2 Constructing Manifolds . . . . . . . . . . . . . . . . . . . . 614.1.3 Paths in Topological Spaces . . . . . . . . . . . . . . . . . 64

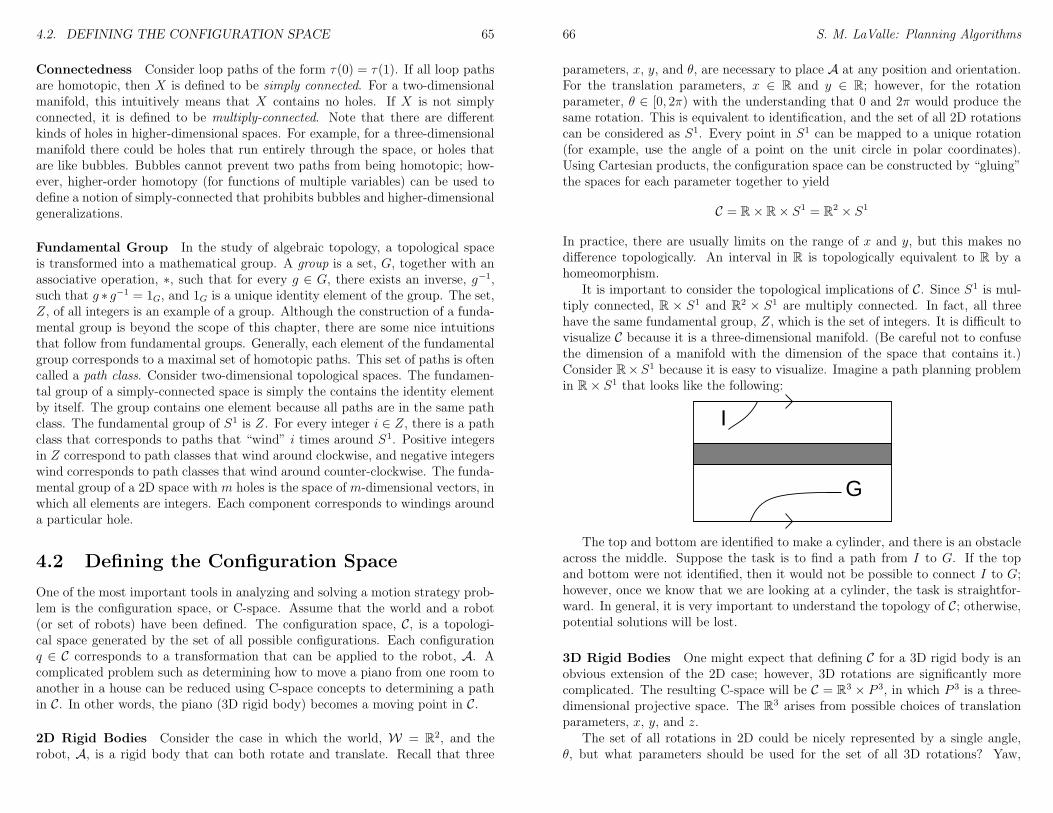

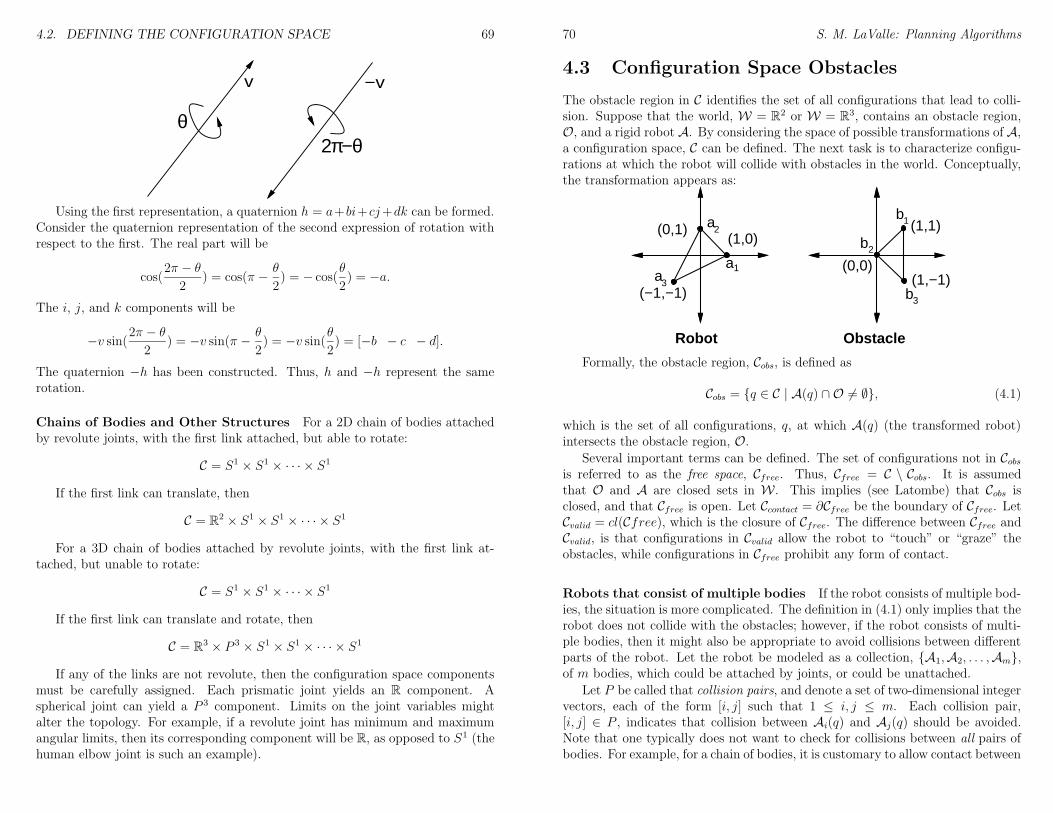

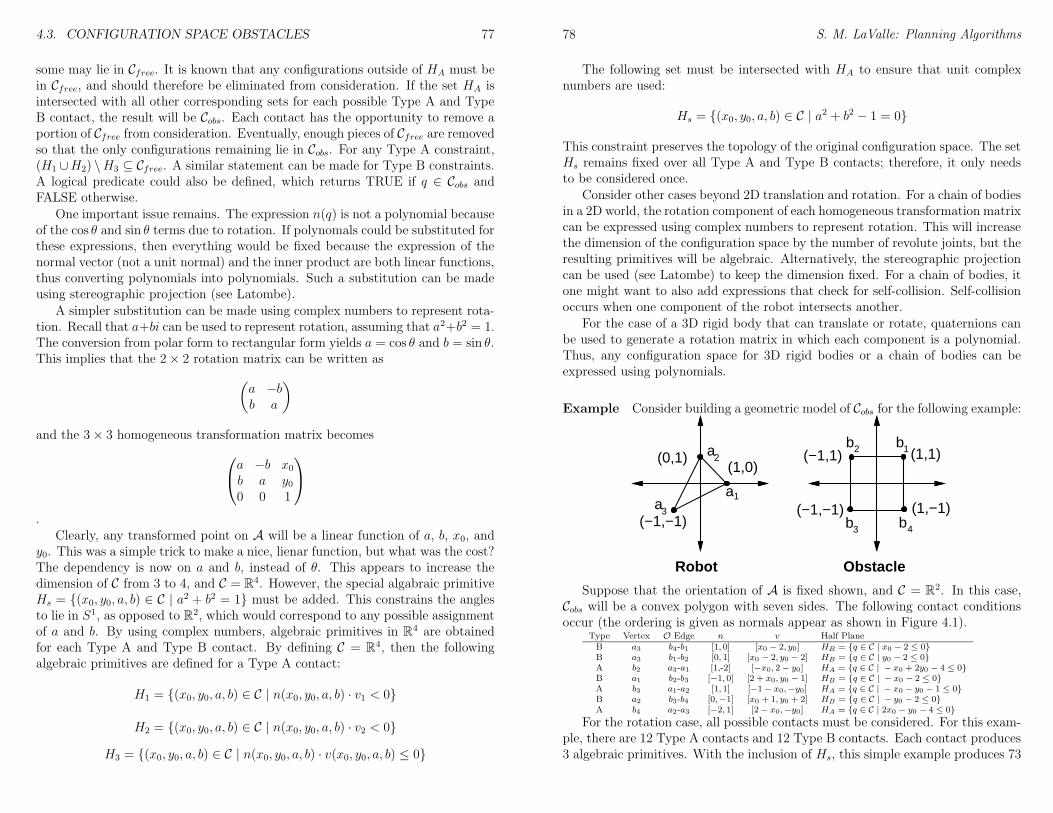

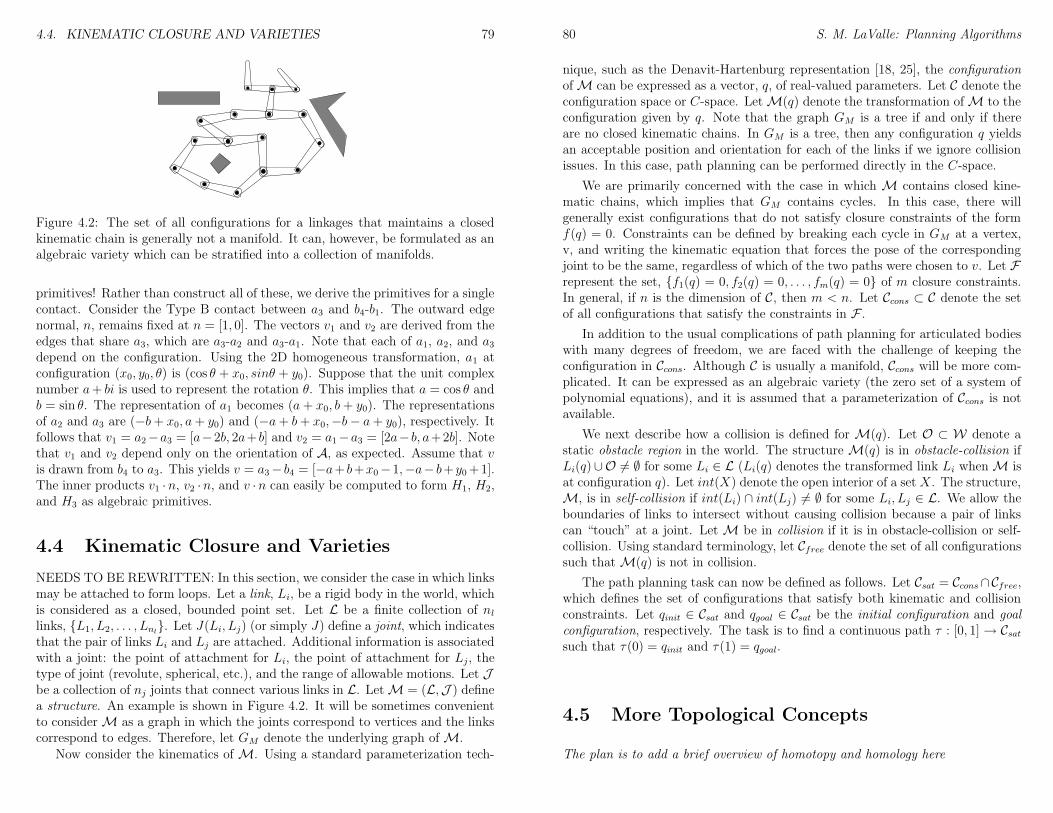

4.2 Defining the Configuration Space . . . . . . . . . . . . . . . . . . 654.3 Configuration Space Obstacles . . . . . . . . . . . . . . . . . . . . 704.4 Kinematic Closure and Varieties . . . . . . . . . . . . . . . . . . . 794.5 More Topological Concepts . . . . . . . . . . . . . . . . . . . . . . 80

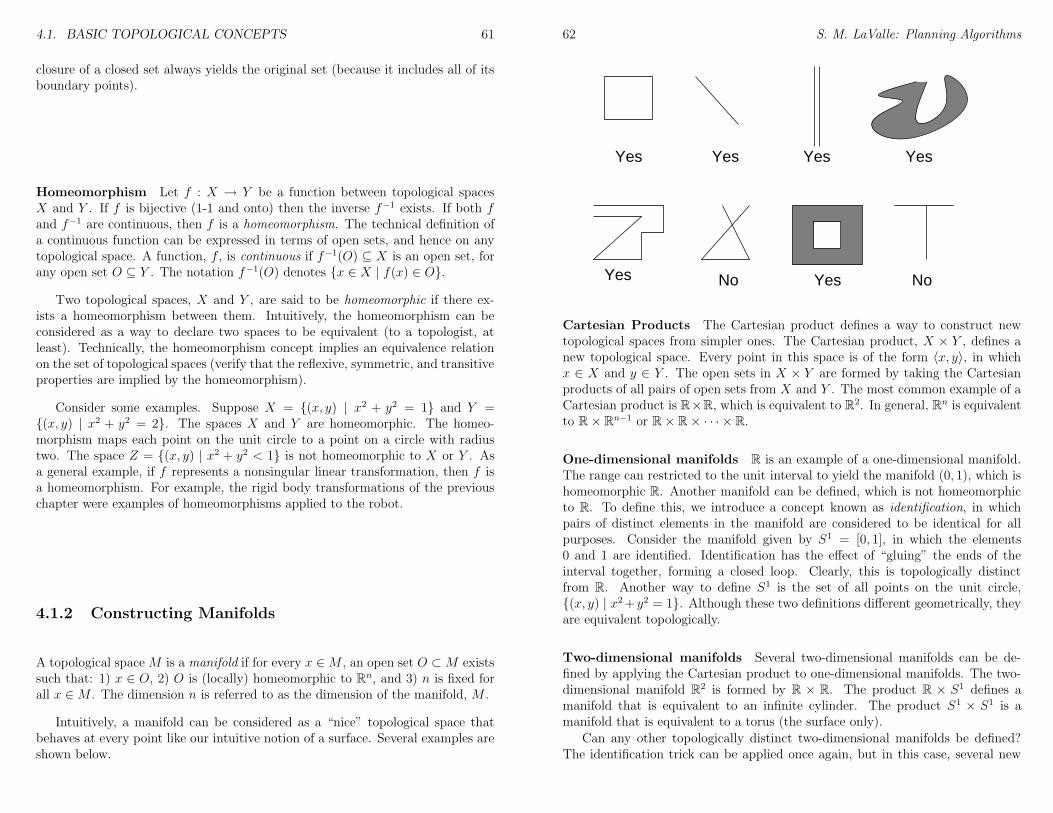

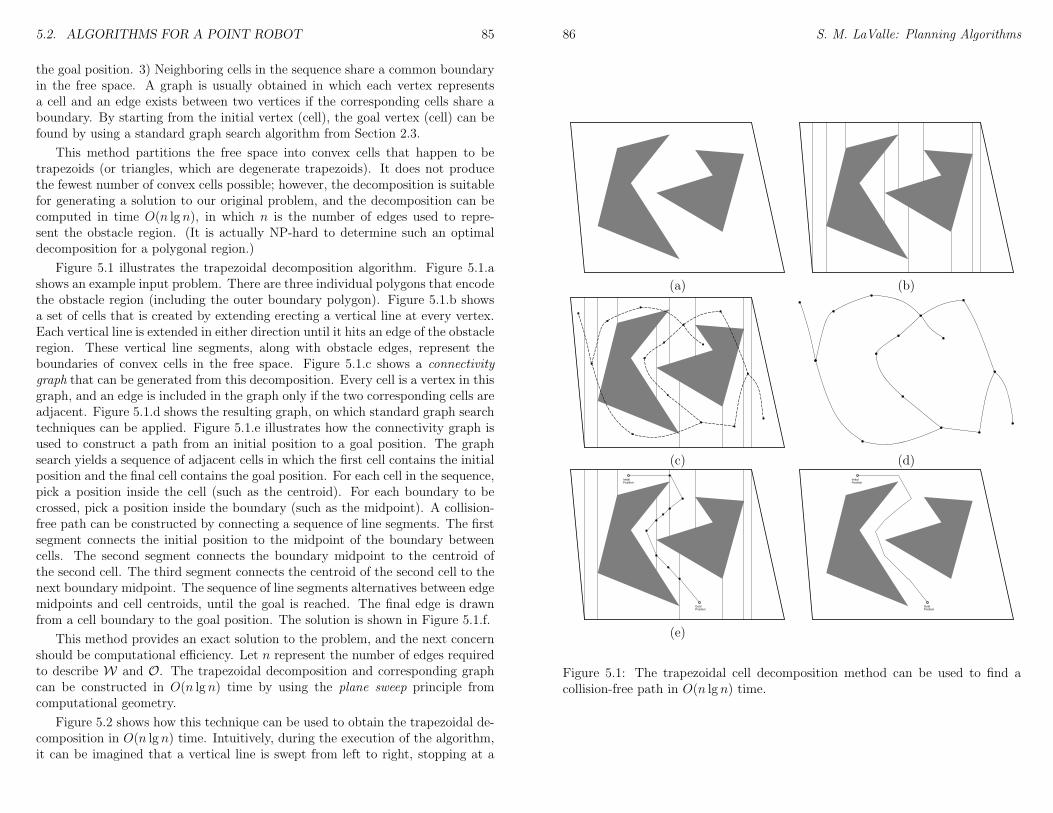

5 Combinatorial Motion Planning 835.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 835.2 Algorithms for a Point Robot . . . . . . . . . . . . . . . . . . . . 84

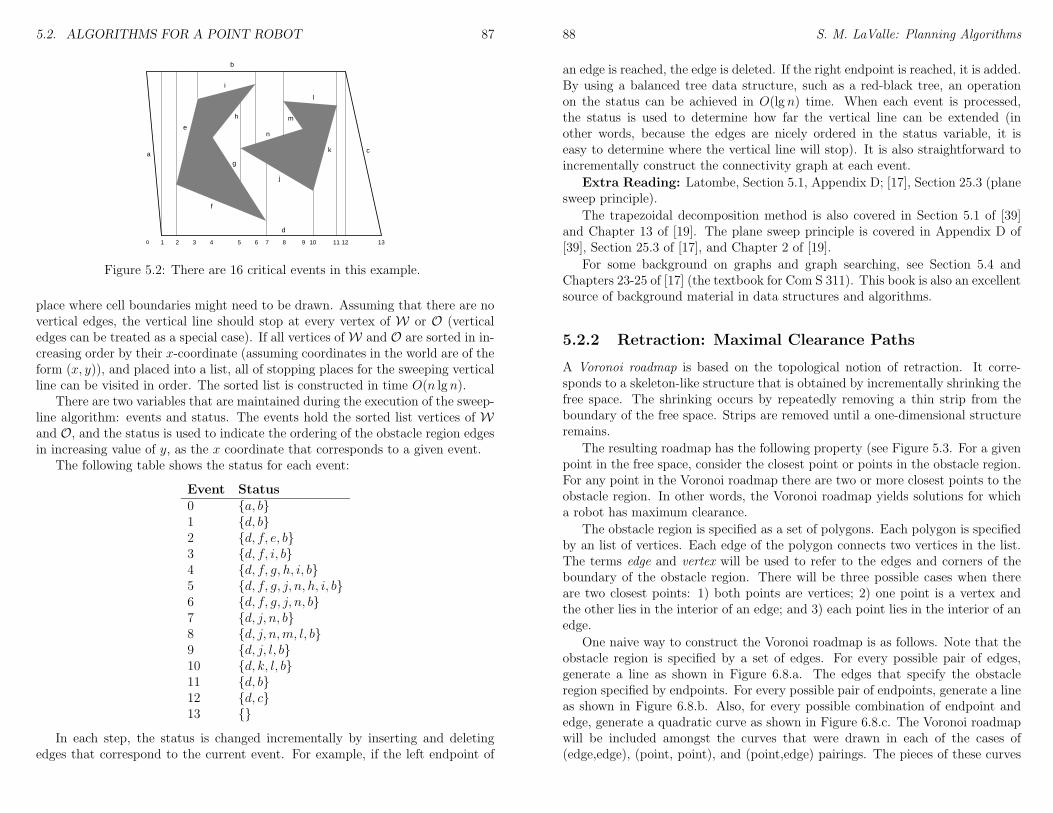

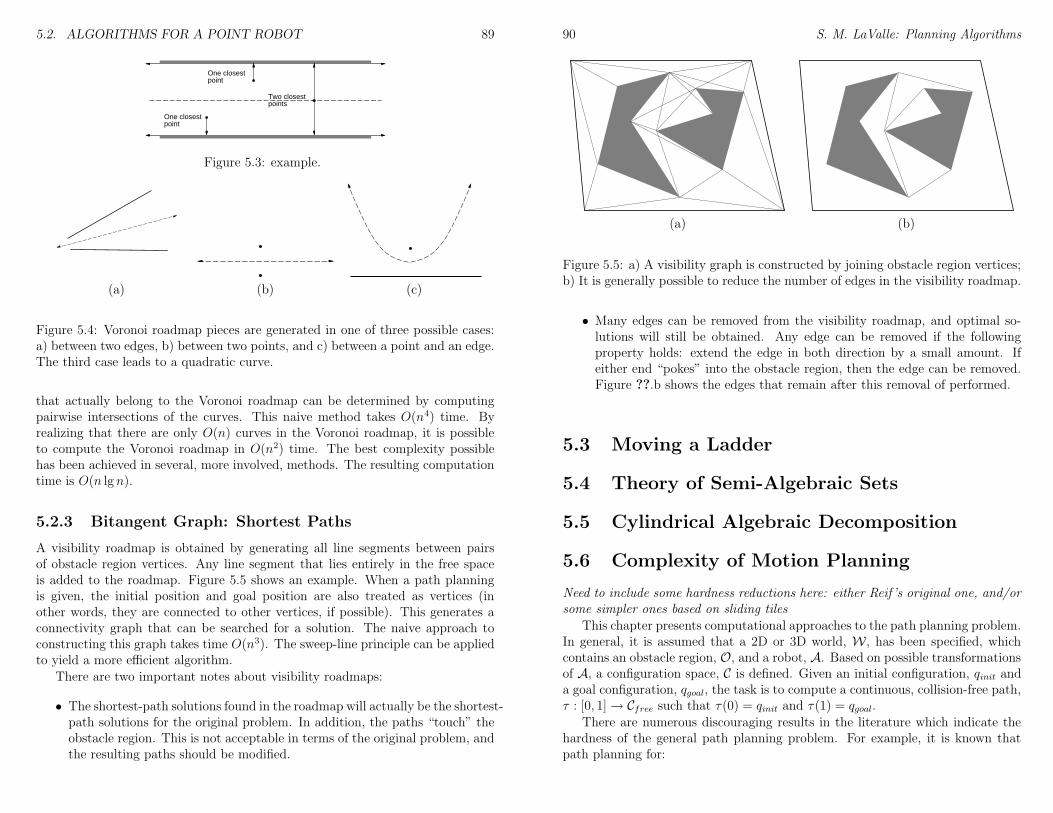

5.2.1 Vertical Cell Decomposition . . . . . . . . . . . . . . . . . 845.2.2 Retraction: Maximal Clearance Paths . . . . . . . . . . . . 885.2.3 Bitangent Graph: Shortest Paths . . . . . . . . . . . . . . 89

5.3 Moving a Ladder . . . . . . . . . . . . . . . . . . . . . . . . . . . 905.4 Theory of Semi-Algebraic Sets . . . . . . . . . . . . . . . . . . . . 905.5 Cylindrical Algebraic Decomposition . . . . . . . . . . . . . . . . 905.6 Complexity of Motion Planning . . . . . . . . . . . . . . . . . . . 905.7 Other Combinatorial Methods . . . . . . . . . . . . . . . . . . . . 92

6 Sampling-Based Motion Planning 936.1 Collision Detection . . . . . . . . . . . . . . . . . . . . . . . . . . 94

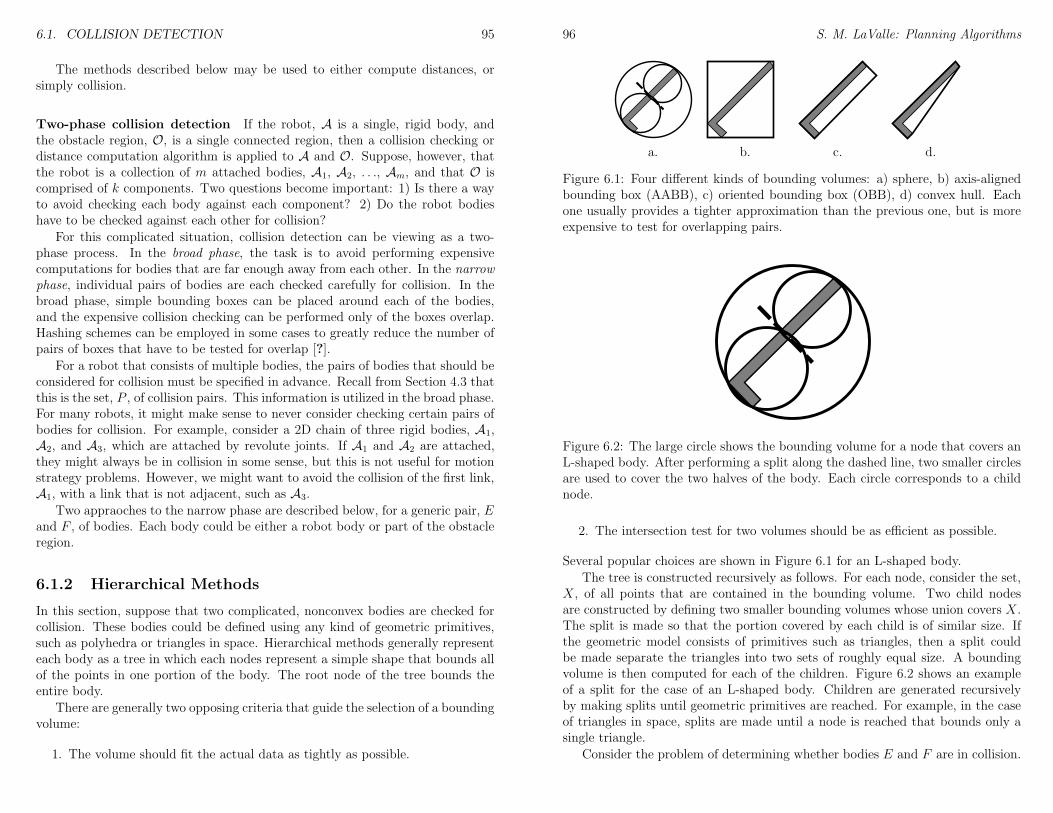

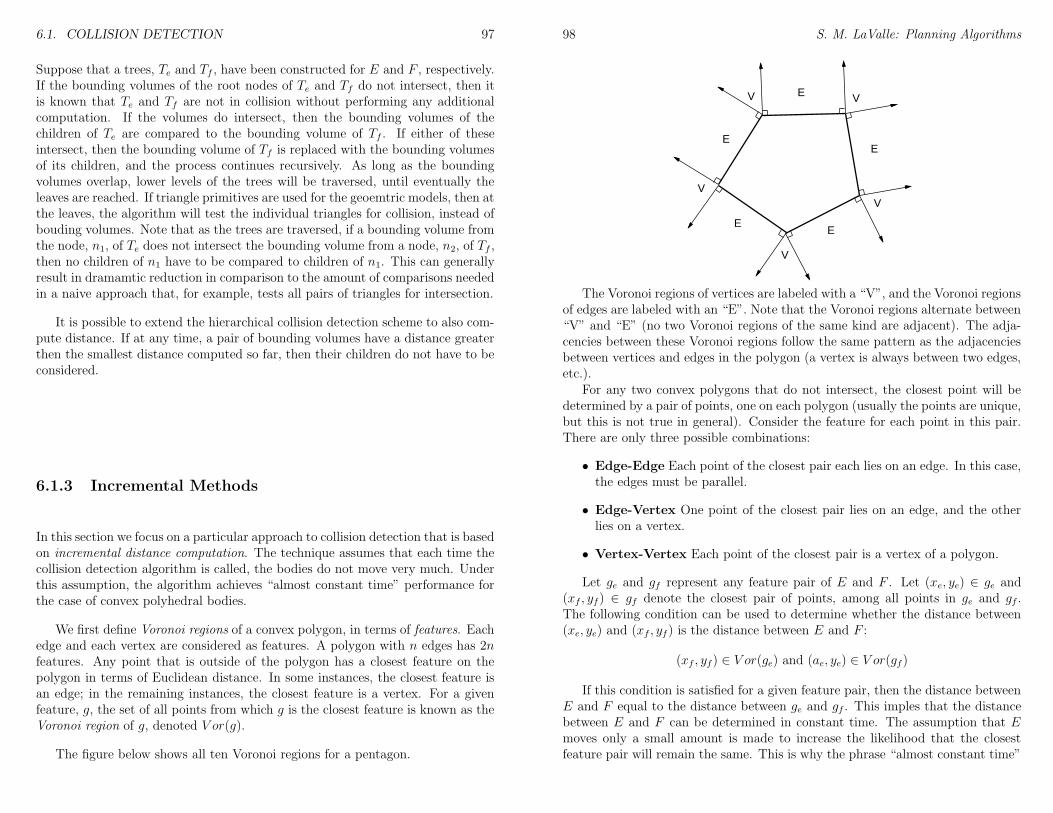

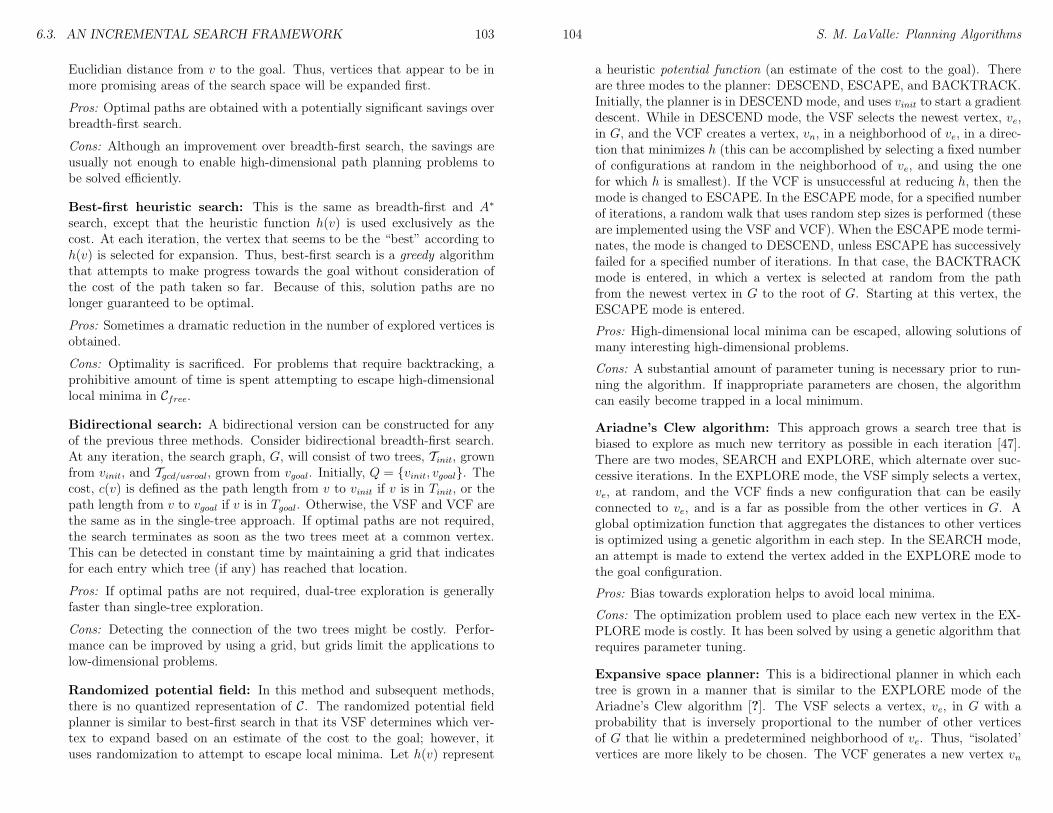

6.1.1 Basic Concepts . . . . . . . . . . . . . . . . . . . . . . . . 946.1.2 Hierarchical Methods . . . . . . . . . . . . . . . . . . . . . 956.1.3 Incremental Methods . . . . . . . . . . . . . . . . . . . . . 97

6.2 Metric Spaces . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 996.3 An Incremental Search Framework . . . . . . . . . . . . . . . . . 101

CONTENTS v

6.4 Classical Grid-Based Search . . . . . . . . . . . . . . . . . . . . . 1056.4.1 Dynamic programming . . . . . . . . . . . . . . . . . . . . 1066.4.2 Other grid-based search algorithms . . . . . . . . . . . . . 107

6.5 Randomized Potential Field . . . . . . . . . . . . . . . . . . . . . 1086.6 Rapidly-Exploring Random Trees . . . . . . . . . . . . . . . . . . 108

6.6.1 Designing Path Planners . . . . . . . . . . . . . . . . . . . 1106.7 Sampling-Based Roadmaps for Multiple Queries . . . . . . . . . . 1146.8 Sampling-Based Roadmap Variants . . . . . . . . . . . . . . . . . 1176.9 Deterministic Sampling Theory . . . . . . . . . . . . . . . . . . . 118

6.9.1 Sampling Criteria . . . . . . . . . . . . . . . . . . . . . . . 1186.9.2 Finite Point Sets and Infinite Sequences . . . . . . . . . . 1196.9.3 Low-Discrepancy Sampling . . . . . . . . . . . . . . . . . . 1206.9.4 Low-Dispersion Sampling . . . . . . . . . . . . . . . . . . . 122

7 Extensions of Basic Motion Planning 1257.1 Time-Varying Problems . . . . . . . . . . . . . . . . . . . . . . . 1257.2 Multiple-Robot Coordination . . . . . . . . . . . . . . . . . . . . 1277.3 Manipulation Planning . . . . . . . . . . . . . . . . . . . . . . . . 1287.4 Assembly Planning . . . . . . . . . . . . . . . . . . . . . . . . . . 129

8 Feedback Motion Strategies 1318.1 Basic Concepts . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1318.2 Potential Functions and Navigation Functions . . . . . . . . . . . 1318.3 Dynamic Programming . . . . . . . . . . . . . . . . . . . . . . . . 1328.4 Harmonic Functions . . . . . . . . . . . . . . . . . . . . . . . . . 1328.5 Sampling-Based Neighborhood Graph . . . . . . . . . . . . . . . . 132

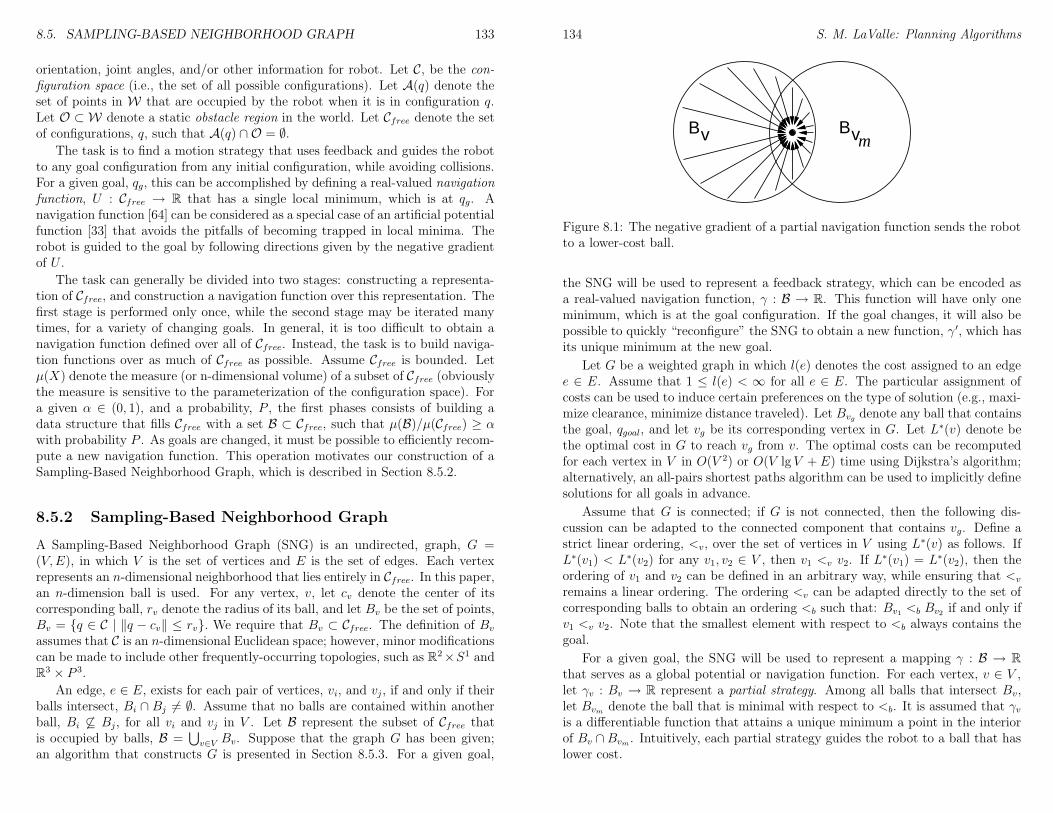

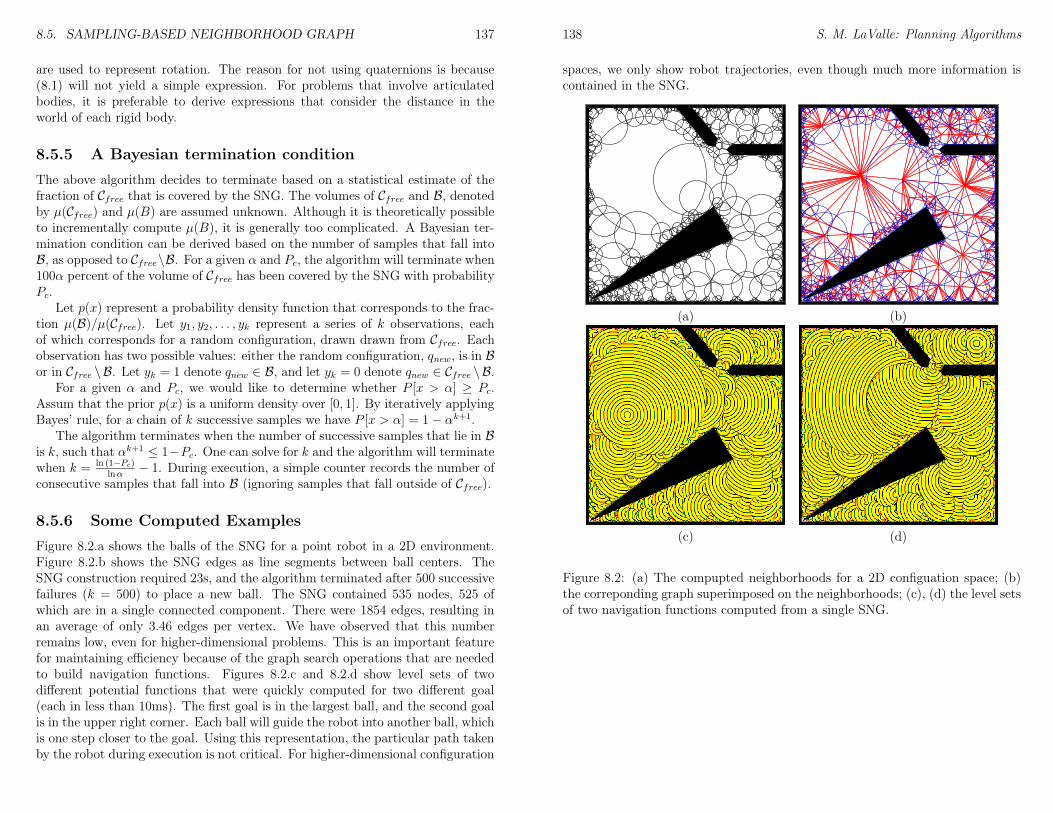

8.5.1 Problem Formulation . . . . . . . . . . . . . . . . . . . . . 1328.5.2 Sampling-Based Neighborhood Graph . . . . . . . . . . . . 1338.5.3 SNG Construction Algorithm . . . . . . . . . . . . . . . . 1358.5.4 Radius selection . . . . . . . . . . . . . . . . . . . . . . . . 1368.5.5 A Bayesian termination condition . . . . . . . . . . . . . . 1378.5.6 Some Computed Examples . . . . . . . . . . . . . . . . . . 137

III Decision-Theoretic Planning 139

9 Basic Decision Theory 1419.1 Basic Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . 1419.2 A Game Against Nature . . . . . . . . . . . . . . . . . . . . . . . 143

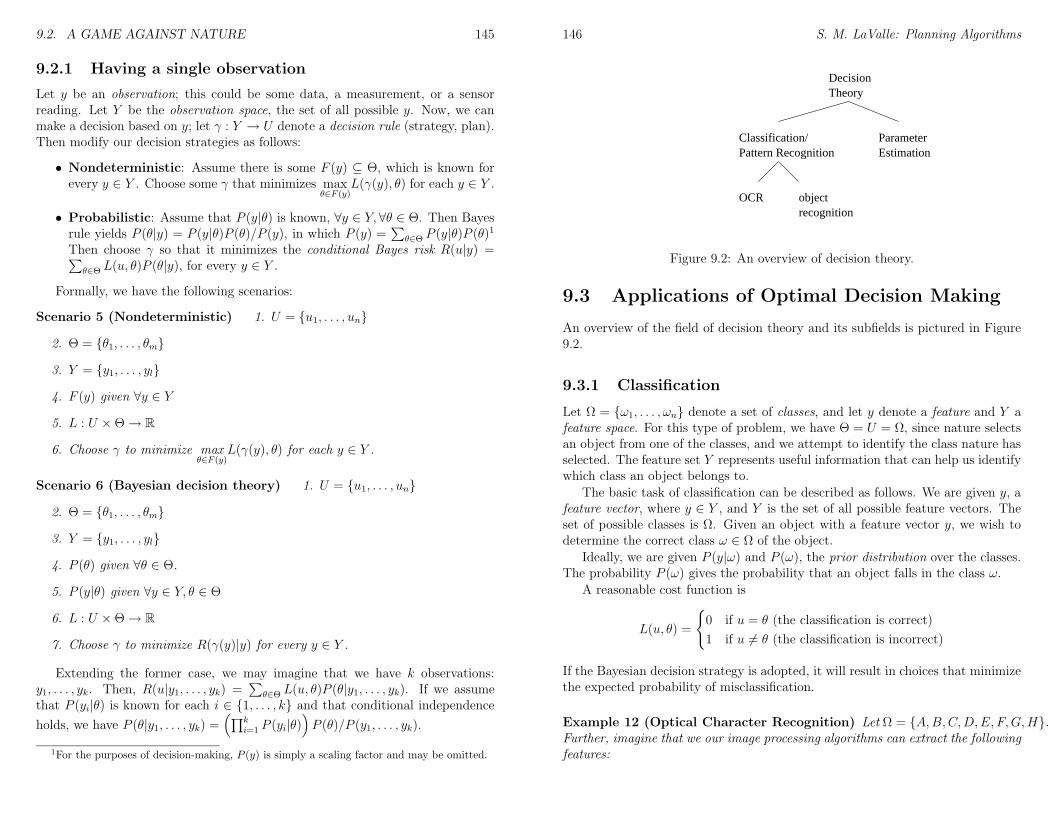

9.2.1 Having a single observation . . . . . . . . . . . . . . . . . 1459.3 Applications of Optimal Decision Making . . . . . . . . . . . . . . 146

9.3.1 Classification . . . . . . . . . . . . . . . . . . . . . . . . . 1469.3.2 Parameter Estimation . . . . . . . . . . . . . . . . . . . . 147

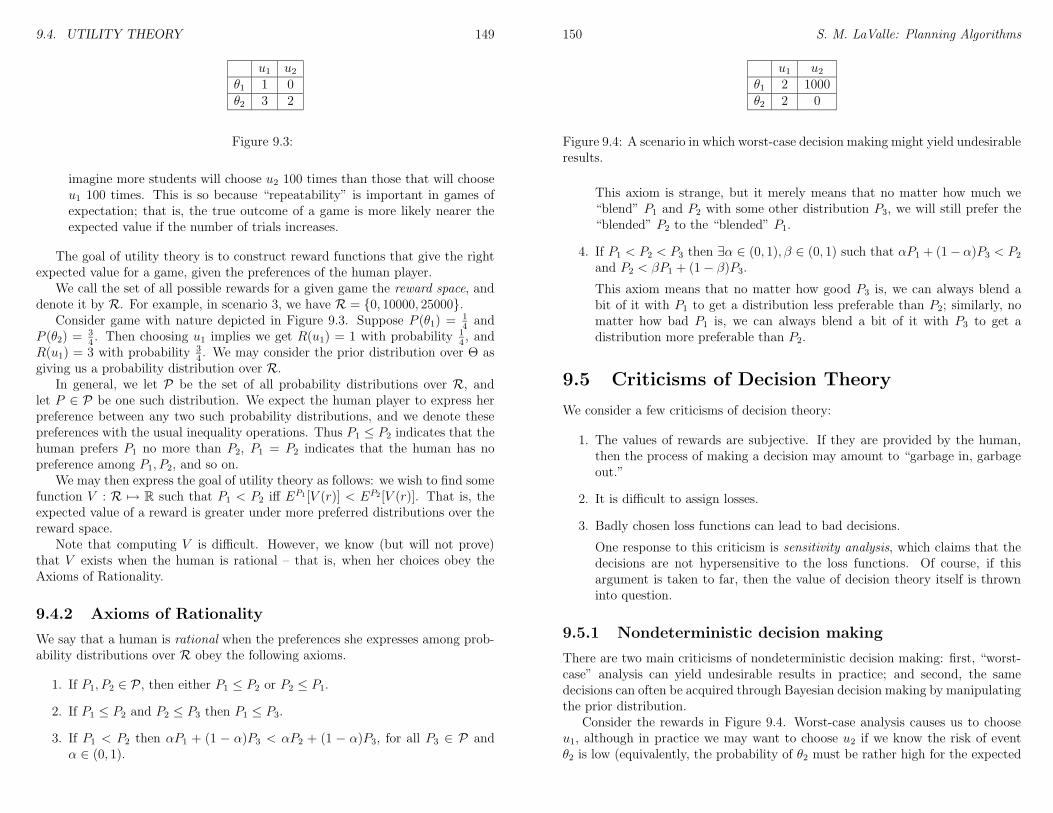

9.4 Utility Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

vi CONTENTS

9.4.1 Choosing a Good Reward . . . . . . . . . . . . . . . . . . 1489.4.2 Axioms of Rationality . . . . . . . . . . . . . . . . . . . . 149

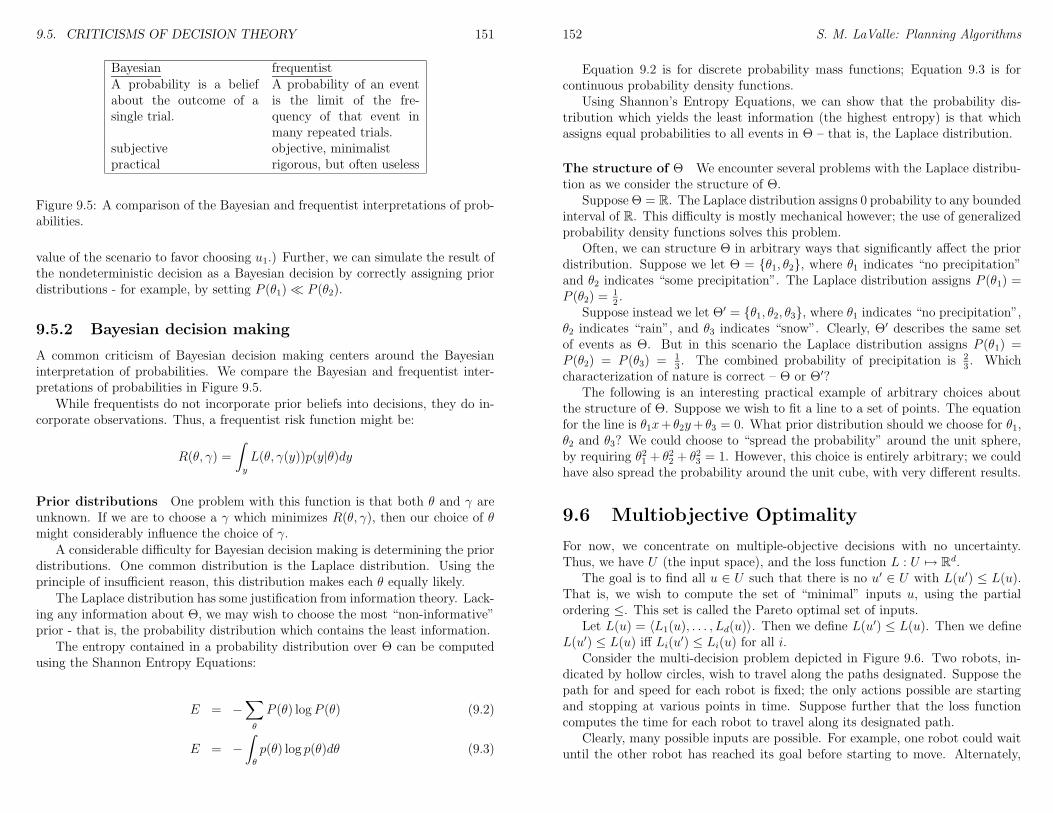

9.5 Criticisms of Decision Theory . . . . . . . . . . . . . . . . . . . . 1509.5.1 Nondeterministic decision making . . . . . . . . . . . . . . 1509.5.2 Bayesian decision making . . . . . . . . . . . . . . . . . . 151

9.6 Multiobjective Optimality . . . . . . . . . . . . . . . . . . . . . . 1529.6.1 Scalarizing L . . . . . . . . . . . . . . . . . . . . . . . . . 153

10 Sequential Decision Theory: Perfect State Information 15510.1 Basic Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

10.1.1 Non-Deterministic Forward Projection . . . . . . . . . . . 15510.1.2 Probabilistic Forward Projection . . . . . . . . . . . . . . 15610.1.3 Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . 156

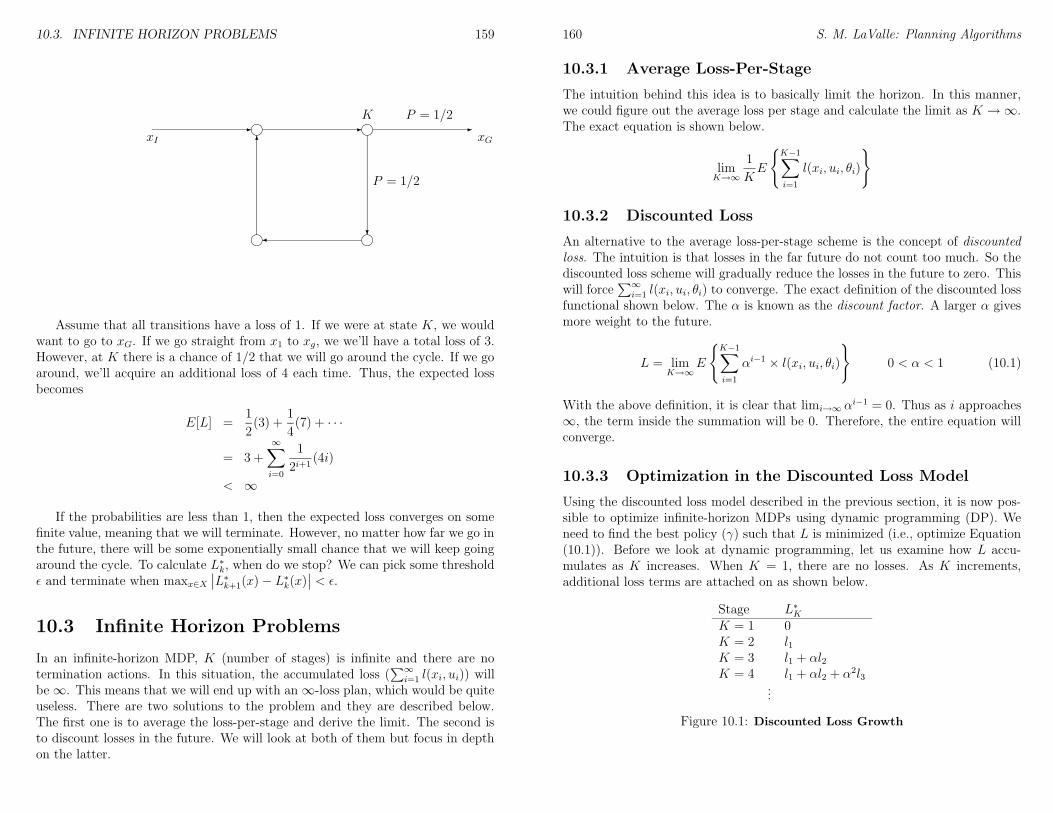

10.2 Dynamic Programming over Discrete Spaces . . . . . . . . . . . . 15710.3 Infinite Horizon Problems . . . . . . . . . . . . . . . . . . . . . . 159

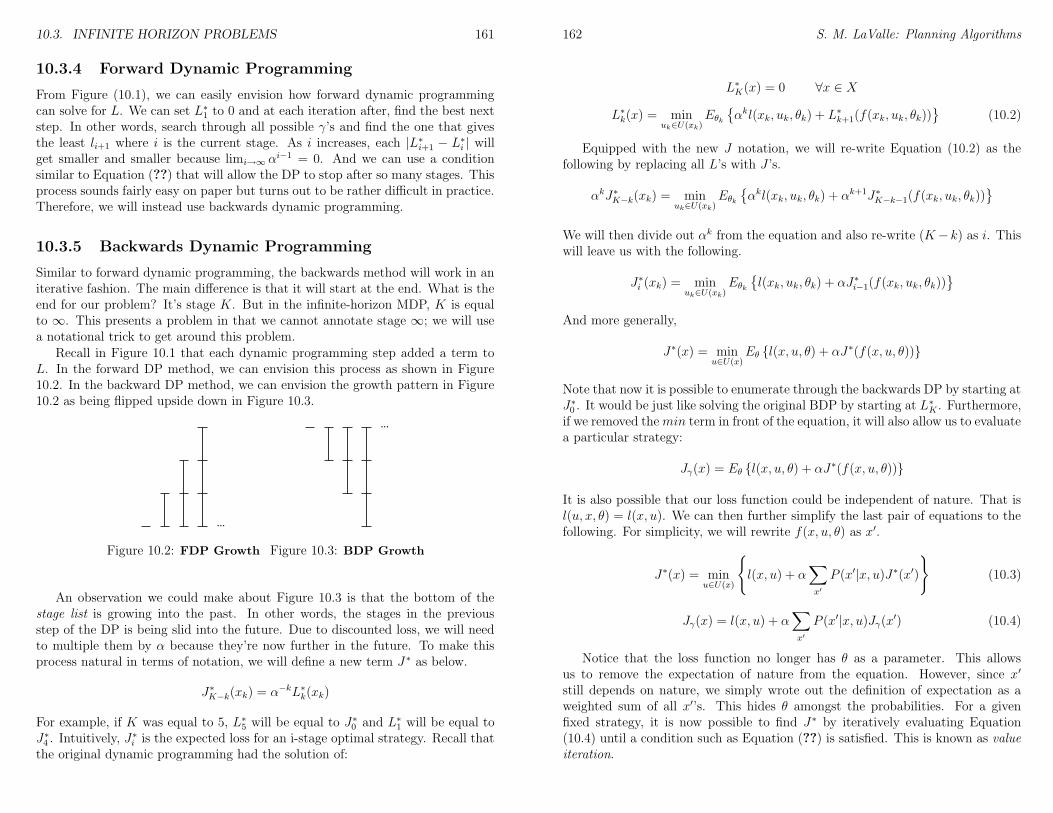

10.3.1 Average Loss-Per-Stage . . . . . . . . . . . . . . . . . . . . 16010.3.2 Discounted Loss . . . . . . . . . . . . . . . . . . . . . . . . 16010.3.3 Optimization in the Discounted Loss Model . . . . . . . . 16010.3.4 Forward Dynamic Programming . . . . . . . . . . . . . . . 16110.3.5 Backwards Dynamic Programming . . . . . . . . . . . . . 16110.3.6 Policy Iteration . . . . . . . . . . . . . . . . . . . . . . . . 163

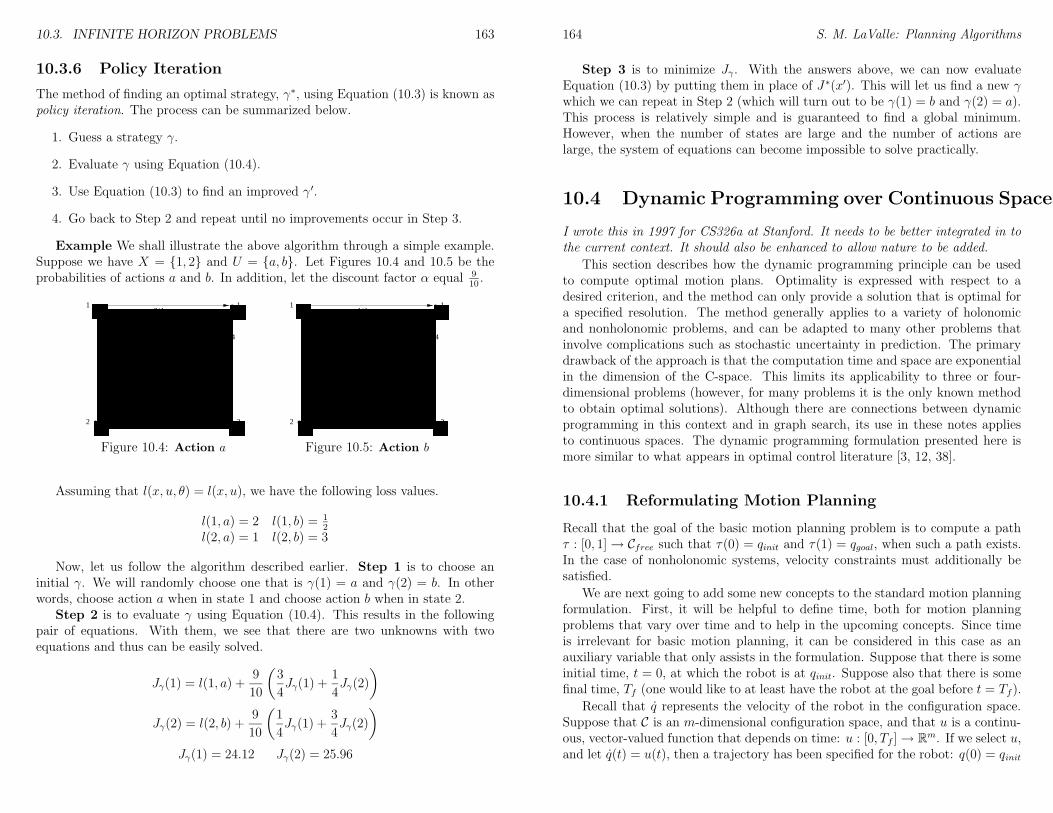

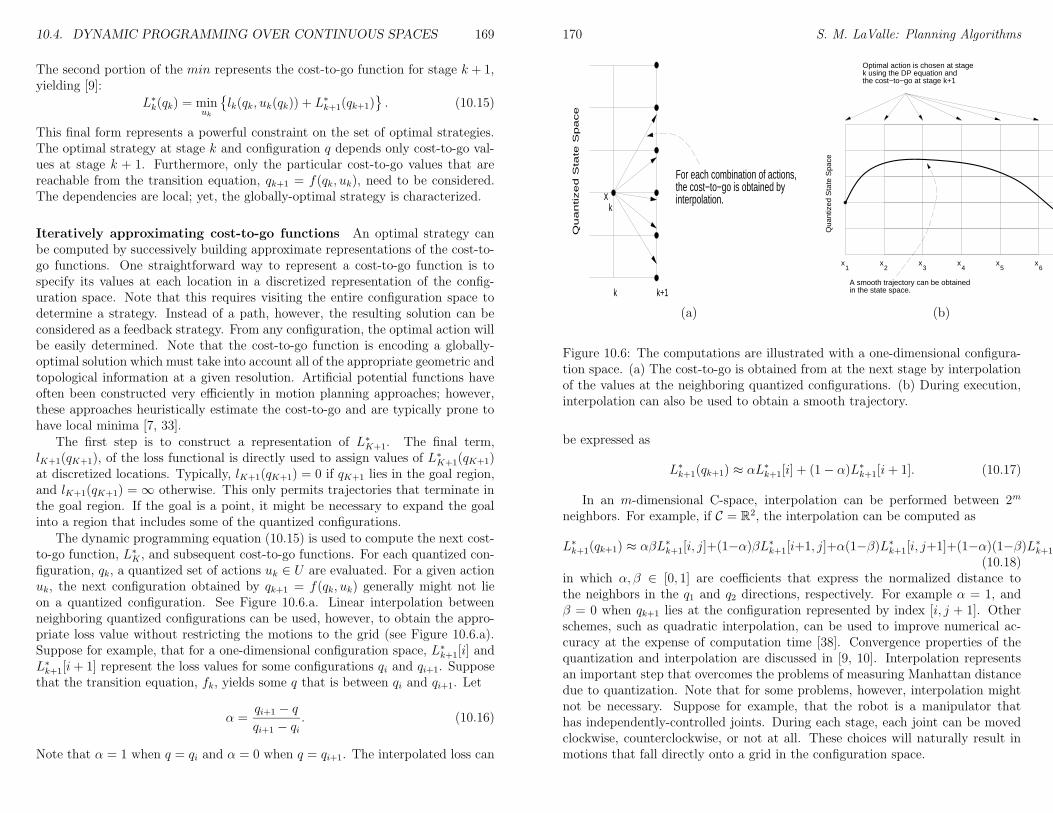

10.4 Dynamic Programming over Continuous Spaces . . . . . . . . . . 16410.4.1 Reformulating Motion Planning . . . . . . . . . . . . . . . 16410.4.2 The Algorithm . . . . . . . . . . . . . . . . . . . . . . . . 167

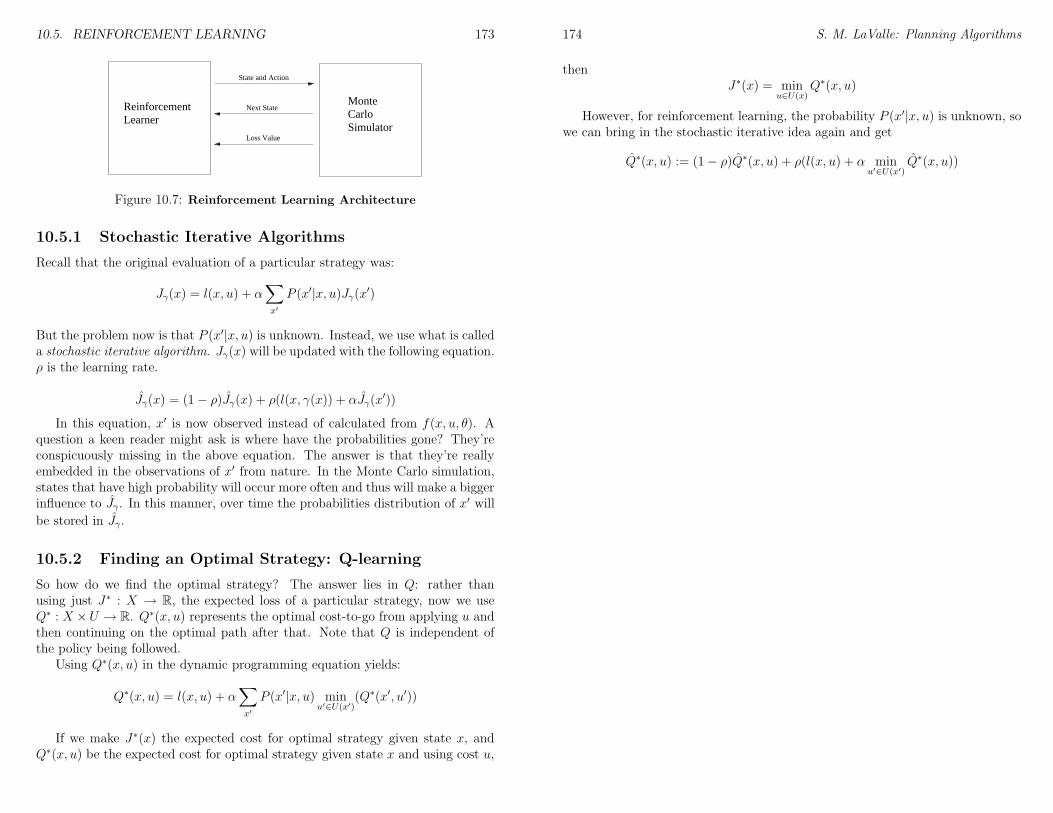

10.5 Reinforcement Learning . . . . . . . . . . . . . . . . . . . . . . . 17210.5.1 Stochastic Iterative Algorithms . . . . . . . . . . . . . . . 17310.5.2 Finding an Optimal Strategy: Q-learning . . . . . . . . . . 173

11 Sequential Decision Theory: Imperfect State Information 17511.1 Information Spaces . . . . . . . . . . . . . . . . . . . . . . . . . . 175

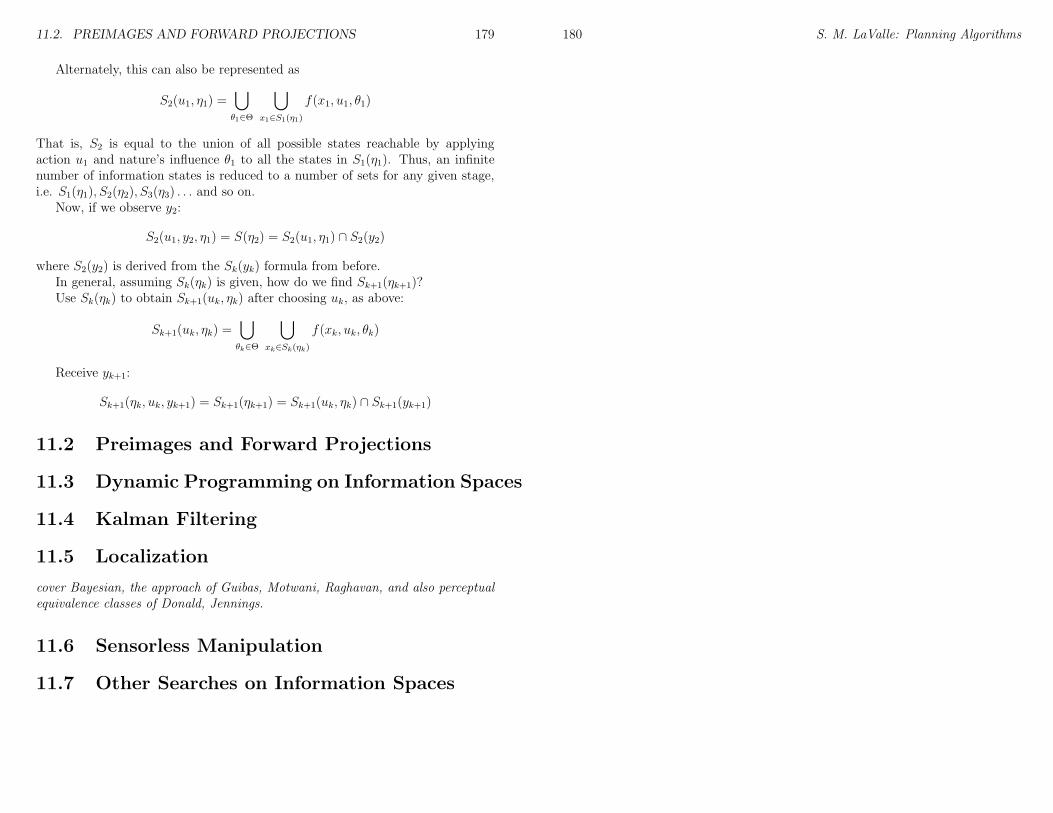

11.1.1 Manipulating the Information Space . . . . . . . . . . . . 17611.2 Preimages and Forward Projections . . . . . . . . . . . . . . . . . 17911.3 Dynamic Programming on Information Spaces . . . . . . . . . . . 17911.4 Kalman Filtering . . . . . . . . . . . . . . . . . . . . . . . . . . . 17911.5 Localization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17911.6 Sensorless Manipulation . . . . . . . . . . . . . . . . . . . . . . . 17911.7 Other Searches on Information Spaces . . . . . . . . . . . . . . . 179

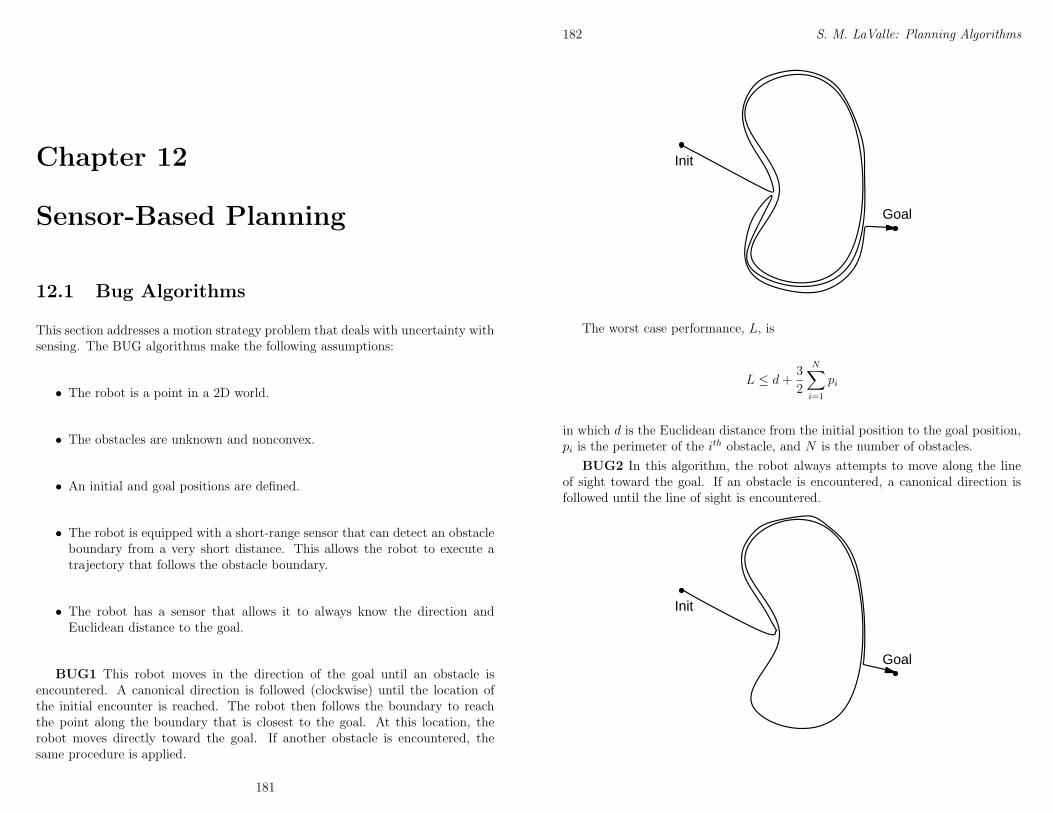

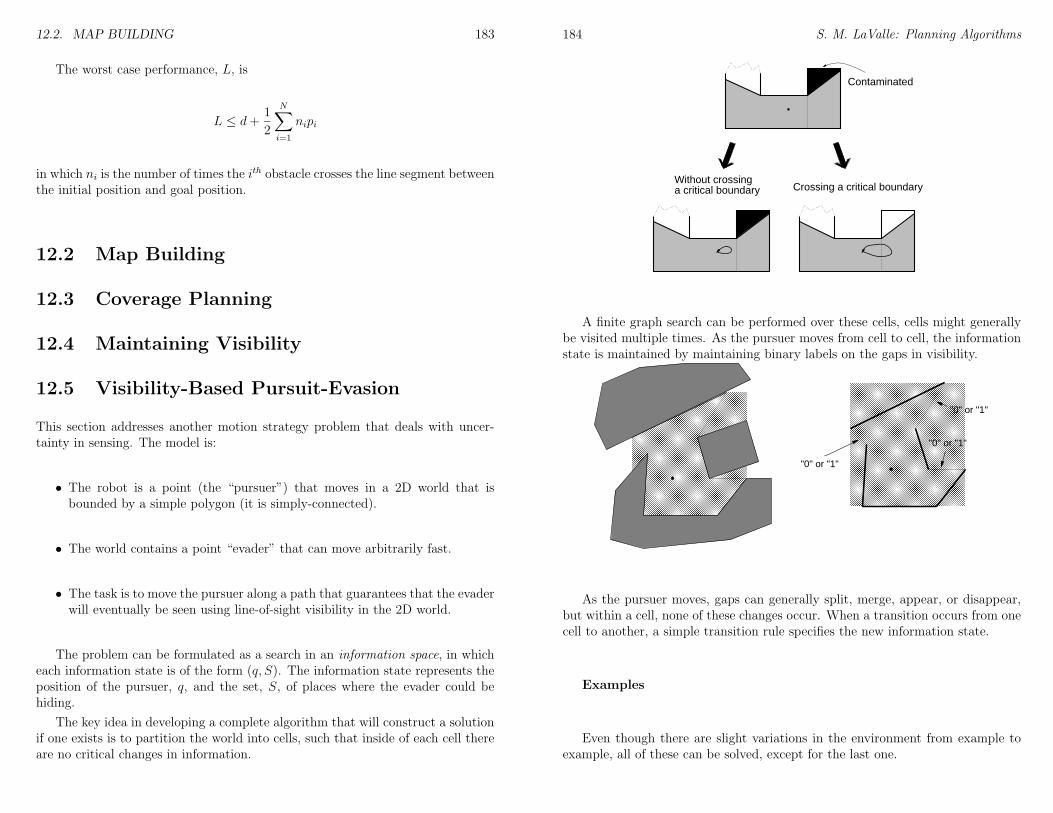

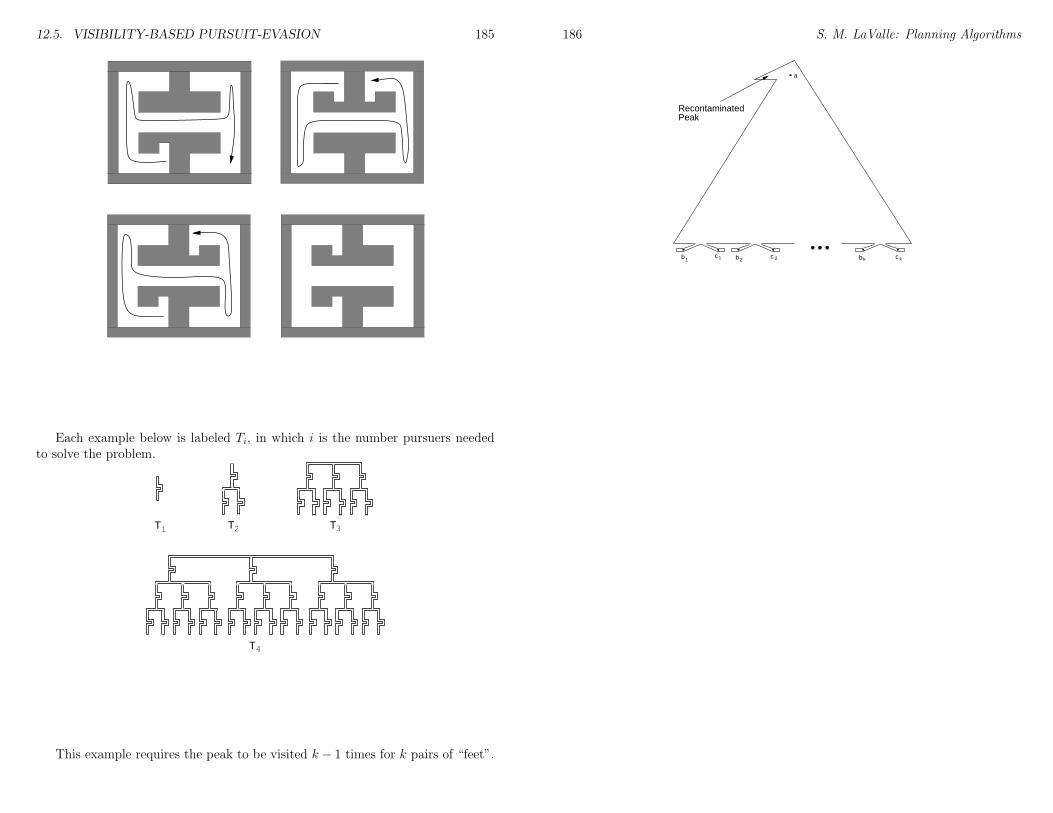

12 Sensor-Based Planning 18112.1 Bug Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18112.2 Map Building . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18312.3 Coverage Planning . . . . . . . . . . . . . . . . . . . . . . . . . . 18312.4 Maintaining Visibility . . . . . . . . . . . . . . . . . . . . . . . . . 18312.5 Visibility-Based Pursuit-Evasion . . . . . . . . . . . . . . . . . . . 183

CONTENTS vii

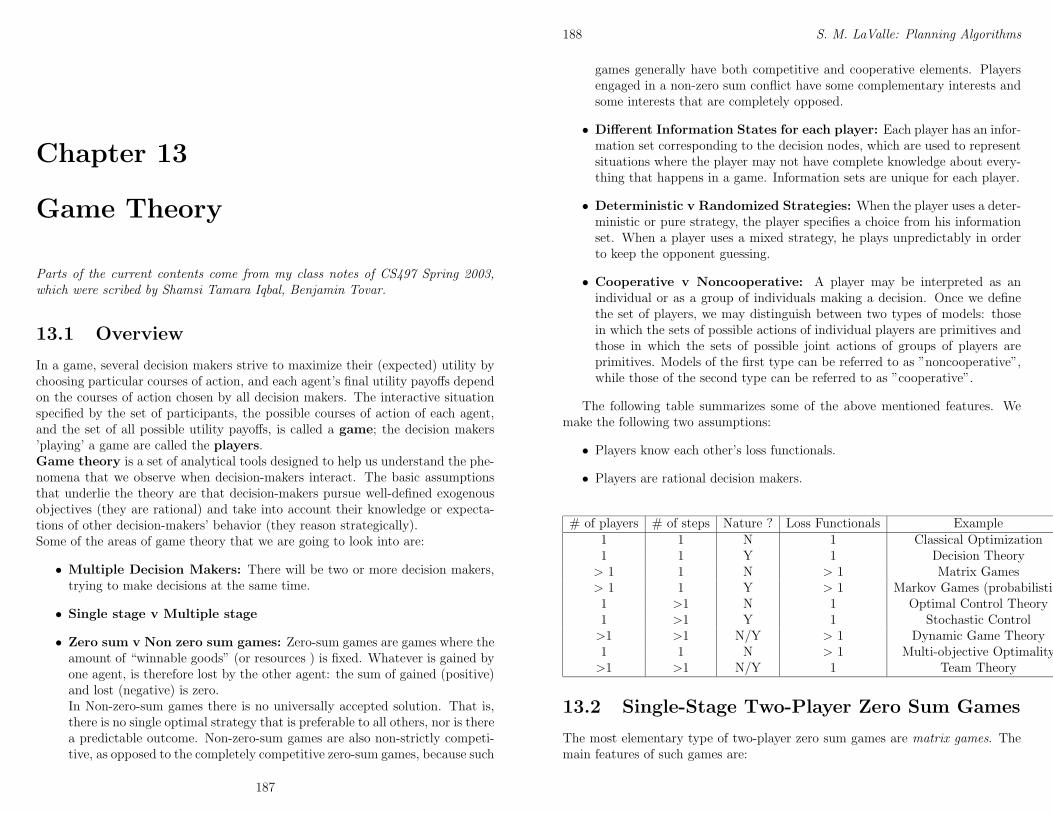

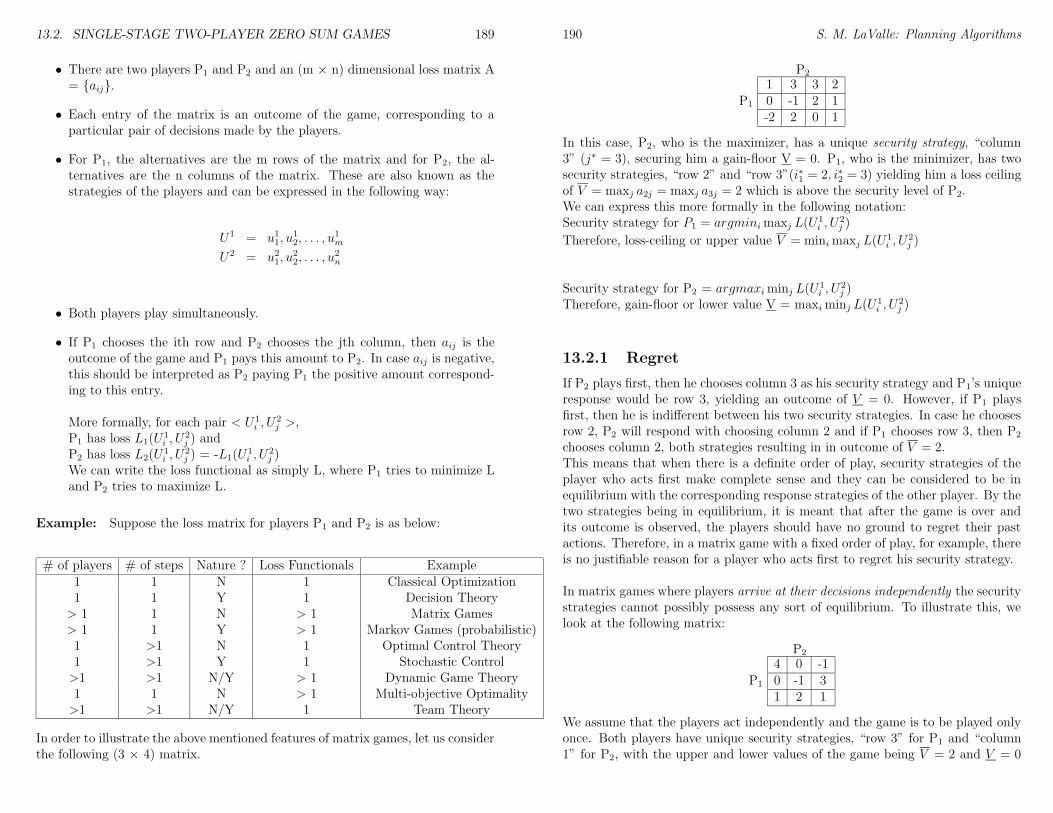

13 Game Theory 18713.1 Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18713.2 Single-Stage Two-Player Zero Sum Games . . . . . . . . . . . . . 188

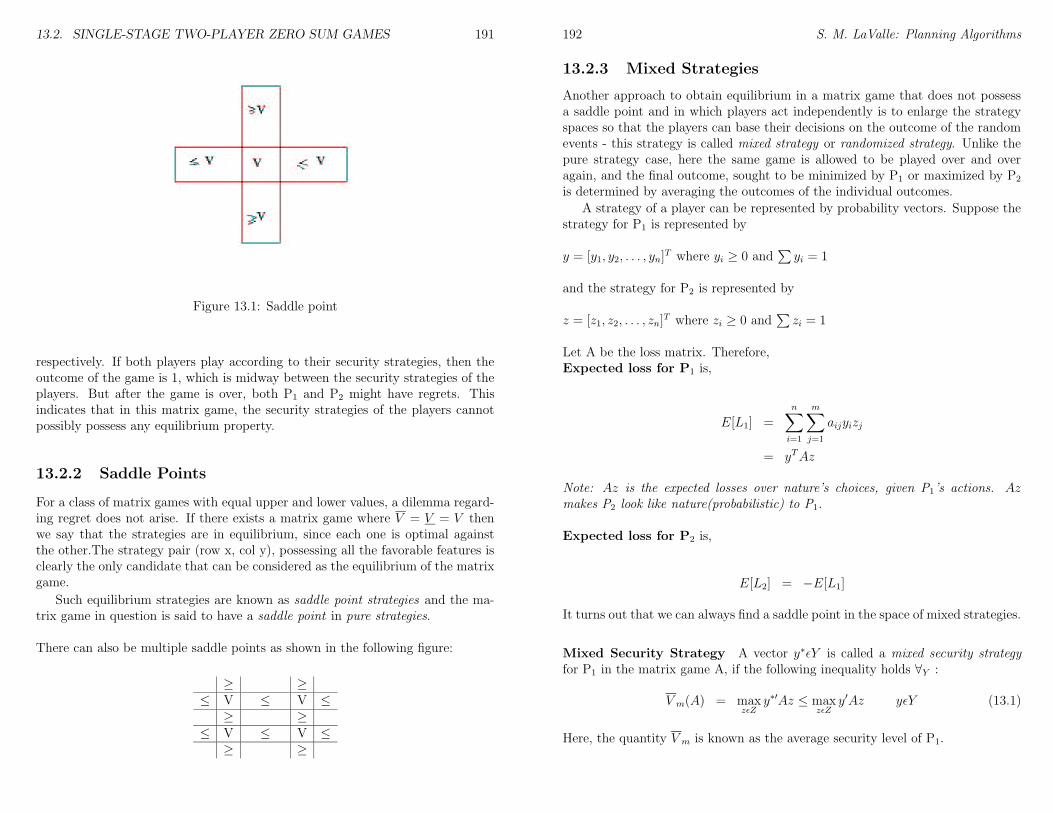

13.2.1 Regret . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19013.2.2 Saddle Points . . . . . . . . . . . . . . . . . . . . . . . . . 19113.2.3 Mixed Strategies . . . . . . . . . . . . . . . . . . . . . . . 19213.2.4 Computation of Equilibria . . . . . . . . . . . . . . . . . . 193

13.3 Nonzero Sum Games . . . . . . . . . . . . . . . . . . . . . . . . . 19513.3.1 Nash Equilibria . . . . . . . . . . . . . . . . . . . . . . . . 19613.3.2 Admissibility . . . . . . . . . . . . . . . . . . . . . . . . . 19713.3.3 The Prisoner’s Dilemma . . . . . . . . . . . . . . . . . . . 19813.3.4 Nash Equilibrium for mixed strategies . . . . . . . . . . . 198

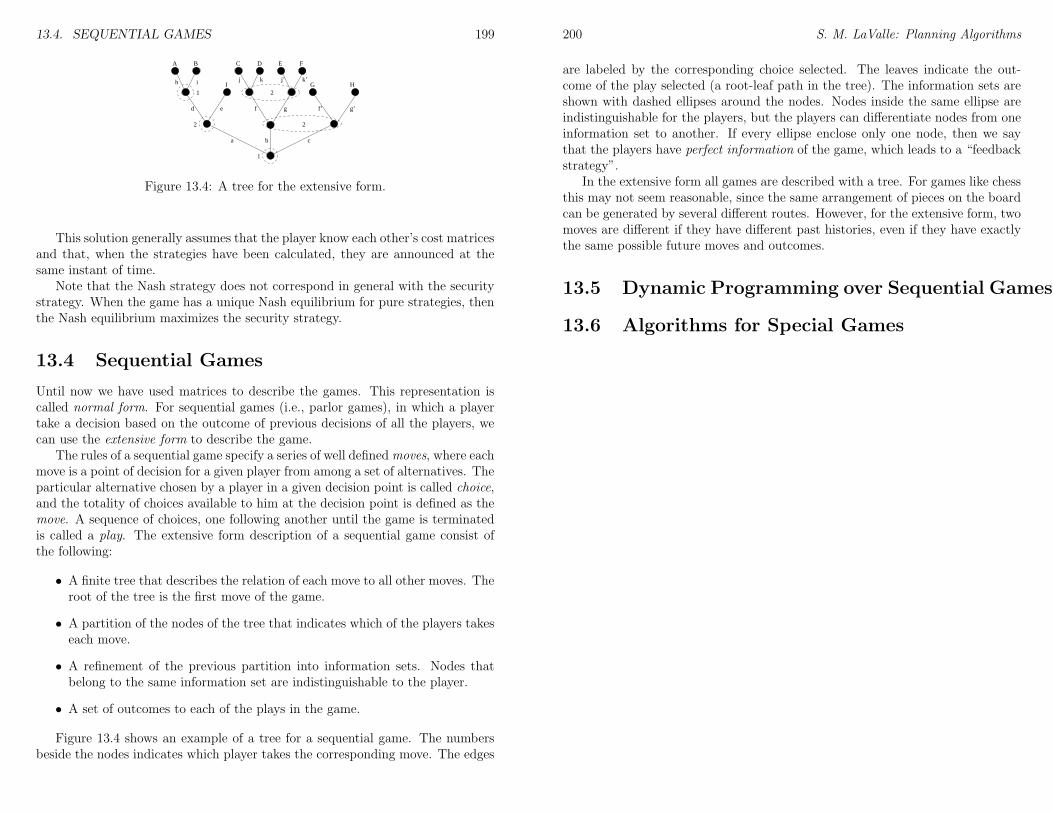

13.4 Sequential Games . . . . . . . . . . . . . . . . . . . . . . . . . . . 19913.5 Dynamic Programming over Sequential Games . . . . . . . . . . . 20013.6 Algorithms for Special Games . . . . . . . . . . . . . . . . . . . . 200

IV Continuous-Time Planning 201

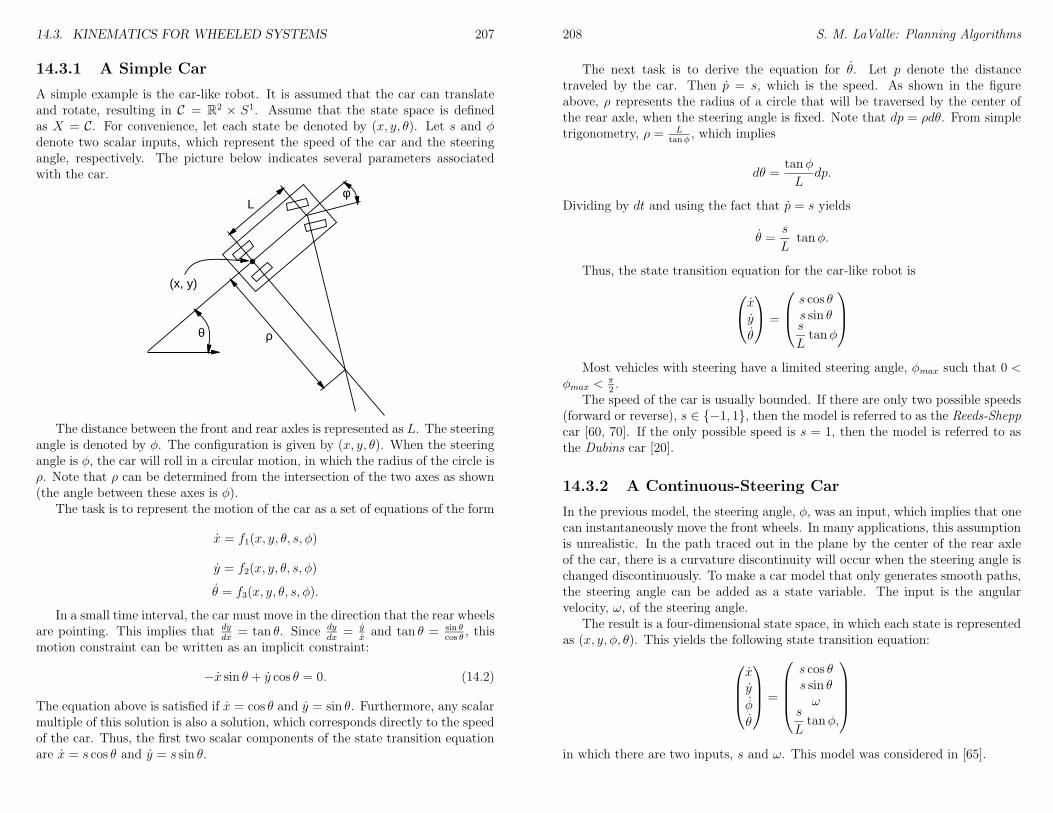

14 Differential Models 20314.1 Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20314.2 Representing Differential Constraints . . . . . . . . . . . . . . . . 20314.3 Kinematics for Wheeled Systems . . . . . . . . . . . . . . . . . . 206

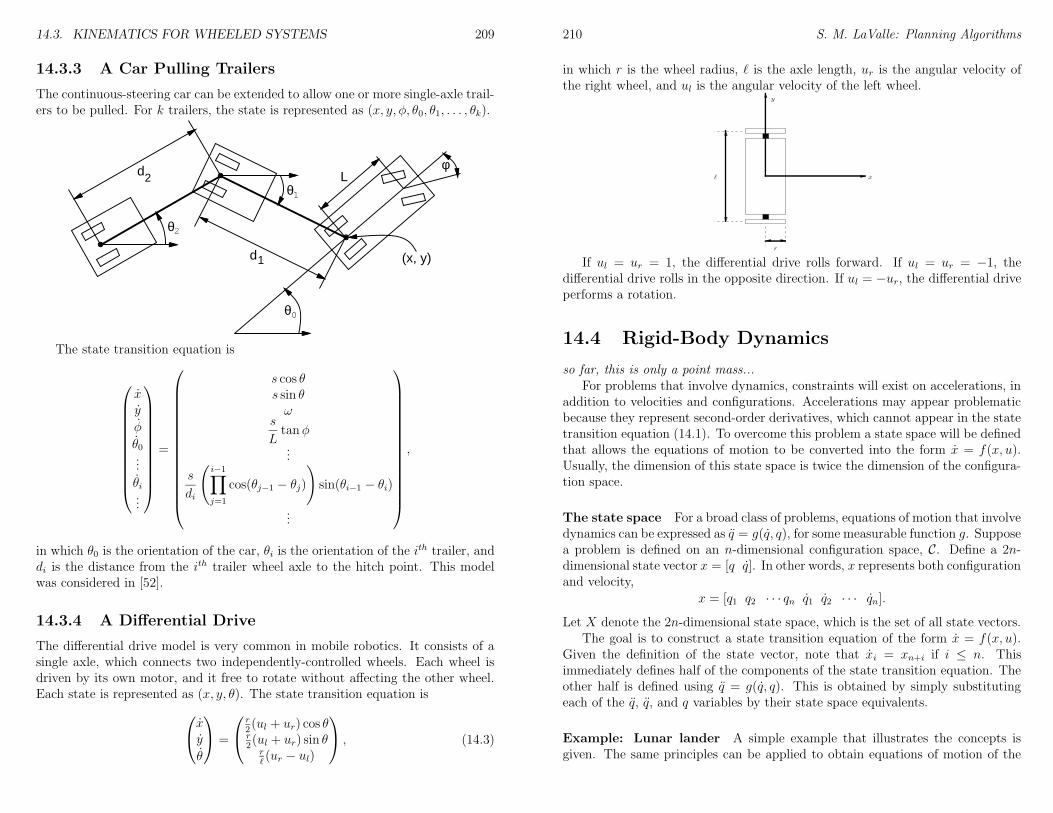

14.3.1 A Simple Car . . . . . . . . . . . . . . . . . . . . . . . . . 20714.3.2 A Continuous-Steering Car . . . . . . . . . . . . . . . . . . 20814.3.3 A Car Pulling Trailers . . . . . . . . . . . . . . . . . . . . 20914.3.4 A Differential Drive . . . . . . . . . . . . . . . . . . . . . . 209

14.4 Rigid-Body Dynamics . . . . . . . . . . . . . . . . . . . . . . . . 21014.5 Multiple-Body Dynamics . . . . . . . . . . . . . . . . . . . . . . . 21214.6 More Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212

15 Nonholonomic System Theory 21315.1 Vector Fields and Distributions . . . . . . . . . . . . . . . . . . . 21315.2 The Lie Bracket . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21515.3 Integrability and Controllability . . . . . . . . . . . . . . . . . . . 21615.4 More Differential Geometry . . . . . . . . . . . . . . . . . . . . . 220

16 Planning Under Differential Constraints 22116.1 Functional-Based Dynamic Programming . . . . . . . . . . . . . . 22116.2 Tree-Based Dynamic Programming . . . . . . . . . . . . . . . . . 22116.3 Geodesic Curve Families . . . . . . . . . . . . . . . . . . . . . . . 22216.4 Steering Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . 22316.5 RRT-Based Methods . . . . . . . . . . . . . . . . . . . . . . . . . 22316.6 Other Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . 224

viii CONTENTS

Preface

0.1 What is meant by “Planning Algorithms”?

Due to many exciting developments in the fields of robotics, artificial intelligence,and control theory, three topics that were once quite distinct are presently on acollision course. In robotics, motion planning was originally concerned with prob-lems such as how to move a piano from one room to another in a house withouthitting anything. The field has grown, however, to include complications such asuncertainties, multiple bodies, and dynamics. In artificial intelligence, planningoriginally meant a search for a sequence of logical operators or actions that trans-form an initial world state into a desired goal state. Presently, planning extendsbeyond this to include many decision-theoretic ideas such as Markov decisionprocesses, imperfect state information, and game-theoretic equilibria. Althoughcontrol theory has traditionally been concerned with issues such as stability, feed-back, and optimality, there has been a growing interest in designing algorithmsthat find feasible open-loop trajectories for nonlinear systems. In some of thiswork, the term motion planning has been applied, with a different interpretationof its use in robotics. Thus, even though each originally considered different prob-lems, the fields of robotics, artificial intelligence, and control theory have expandedtheir scope to share an interesting common ground.

In this text, I use the term planning in a broad sense that encompasses thiscommon ground. This does not, however, imply that the term is meant covereverything important in the fields of robotics, artificial intelligence, and controltheory. The presentation is focused primarily on algorithm issues relating to plan-ning. Within robotics, the focus is on designing algorithms that generate usefulmotions by processing complicated geometric models. Within artificial intelli-gence, the focus is on designing systems that use decision-theoretic models com-pute appropriate actions. Within control theory, the focus of the presentationis on algorithms that numerically compute feasible trajectories or even optimalfeedback control laws. This means that analytical techniques, which account forthe majority of control theory literature, are not addressed here.

The phrase “planning and control” is often used to identify complementary is-sues in developing a system. Planning is often considered as a higher-level processthan control. In this text, we make no such distinctions. Ignoring old connotationsthat come with the terms, “planning” or “control” could be used interchangeably.

ix

x PREFACE

Both can refer to some kind of decision making in this text, with no associatednotion of “high” or “low” level. A hierarchical planning (or control!) strategycould be developed in any case.

0.2 Who is the Intended Audience?

The text is written primarily for computer science and engineering students atthe advanced undergraduate or beginning graduate level. It is also intended asan introduction to recent techniques for researchers and developers in roboticsand artificial intelligence. It is expected that the presentation here would beof interest to those working in other areas such as computational biology (drugdesign, protein folding), virtual prototyping, and computer graphics.

I have attempted to make the book as self-contained and readable as possible.Advanced mathematical concepts (beyond concepts typically learned by under-graduates in computer science and engineering) are introduced and explained.For readers with deeper mathematical interests, directions for further study aregiven at the end of some chapters.

0.3 Suggested Use

The ideas should flow naturally from chapter to chapter, but at the same time,the text has been designed to make it easy to skip chapters.

If you are only interested in robot motion planning, it is only necessary toread Chapters 3-8, possibly with the inclusion of search algorithm material fromChapter 2. Chapters 3 and 4 provide the foundations needed to understand basicrobot motion planning. Chapters 5 and 6 present algorithmic techniques to solvethis problem. Chapters 7 and 8 consider extensions of the basic problem. Chapter12 is covers sensor-based extension of motion planning, for those interested.

If you are additionally interested in nonholonomic planning and other problemsthat involve differential constraints, then it is safe to jump ahead to Chapters 14-16, after completing Chapters 3-6.

If you are mainly interested in decision-theoretic planning, then you can readChapter 2, and jump straight to Chapters 9-11. The extension to multiple decisionmakers is covered in Chapter 13. The material in these later chapters does notdepend much on Chapters 3 and 4, which lay the foundations of robot motionplanning. Thus, if you are not interested in this case, it may be easily skipped.

0.4 Acknowledgments

I am very grateful to many students and colleagues who have given me extensivefeedback and advice in developing this text. I am also thankful for the support-ive environments provided both by Iowa State University and the University of

0.5. HELP! xi

Illinois. In both universities, I have been able to develop courses for which thematerial presented here has been developed and refined.

0.5 Help!

Since the text appears on the web, it is easy for me to incoprorate feedbackfrom readers. This will be very helpful as I complete this project. If you findmistakes, have requests for coverage of topics, find some explanations difficultto follow, have suggested exercises, etc., please let me know by sending mail [email protected]. Note that this book is current a work in progress. Please bepatient as I update parts over the coming year or two.

xii PREFACE

Part I

Introductory Material

1

Chapter 1

Introduction

1.1 Planning to Plan

Planning is a term that means different things to different groups of people. Afundamental need in robotics is to have algorithms that can automatically tellrobots how to move when they are given high-level commands. The terms motionplanning and trajectory planning are often used for these kinds of problems. Aclassical version of motion planning is sometimes referred to as the Piano Mover’sProblem. Imagine giving a precise 3D CAD model of a house and a piano as inputto an algorithm. The algorithm must determine how to move the piano from oneroom to another in the house without hitting anything. Most of us have encoun-tered similar problems when moving a sofa or mattress up a set of stairs. Robotmotion planning usually ignores dynamics and other differential constraints, andfocuses primarily on the translations and rotations required to move the piano.Recent work, however, does consider other aspects, such as uncertainties, differ-ential constraints, modeling uncertainties, and optimality. Trajectory planningusually refers to the problem of taking the solution from a robot motion planningalgorithm and determining how to move along the solution in a way that respectsthe mechanical limitations of the robot.

Control theory has historically been concerned with designing inputs to sys-tems described by differential equations. These could include mechanical systemssuch as cars or aircraft, electrical systems such as noise filters, or even systemsarising in areas as diverse as chemistry, economics, and sociology. Classically,control theory has developed feedback policies, which enable an adaptive responseduring execution, and has focused on stability, which ensures that the dynamicsdo not cause the system to become wildly out of control. A large emphasis is alsoplaced on optimizing criteria to minimize resource consumption, such as energyor time. In recent control theory literature, motion planning sometimes refers tothe construction of inputs to a nonlinear dynamical system that drives it from aninitial state to a specified goal state. For example, imagine trying to operate aremote-controlled hovercraft that glides over the surface of a frozen pond. Sup-

3

4 S. M. LaValle: Planning Algorithms

pose we would like the hovercraft to leave its current resting location and come torest at another specified location. Can an algorithm be designed that computesthe desired inputs, even in an ideal simulator that neglects uncertainties that arisefrom model inaccuracies? It is possible to add other considerations, such as uncer-tainties, feedback, and optimality, but the problem is already challenging enoughwithout these.

In artificial intelligence, the term AI planning takes on a more discrete flavor.Instead of moving a piano through a continuous space, as in the robot motionplanning problem, the task might be to solve a puzzle, such as the Rubik’s cube ora sliding tile puzzle. Although such problems could be modeled with continuousspaces, it seems natural to define a finite set of actions that can be applied toa discrete set of states, and to construct a solution by giving the appropriatesequence of actions. Historically, planning has been considered different fromproblem solving; however, the distinction seems to have faded away in recentyears. In this book, we do not attempt to make a distinction between the two.Also, substantial effort has been devoted to representation language issues inplanning. Although some of this will be covered, it is mainly outside of ourfocus. Many decision-theoretic ideas have recently been incorporated into the AIplanning problem, to model uncertainties, adversarial scenarios, and optimization.These issues are important, and are considered here in detail.

Given the broad range of problems to which the term planning has been ap-plied in the artificial intelligence, control theory, and robotics communities, onemight wonder whether it has a specific meaning. Otherwise, just about anythingcould be considered as an instance of planning. Some common elements for plan-ning problems will be discussed shortly, but first we consider planning as a branchof algorithms. Hence, this book is entitled Planning Algorithms. The primaryfocus is on algorithmic and computational issues of planning problems that havearisen in several disciplines. On the other hand, this does not mean that planningalgorithms refers to an existing community of researchers within the general algo-rithms community. This book will not be limited to combinatorics and asymptoticcomplexity analysis, which is the main focus in pure algorithms. The focus hereincludes numerous modeling considerations and concepts that are not necessarilyalgorithmic, but aid in solving or analyzing planning problems.

The obvious goal of virtually any planning algorithm is to produce a plan.Natural questions are: What is a plan? How is a plan represented? What is itsupposed to achieve? How will its quality be evaluated? Who or what is going touse it? Regarding the user of the plan, it obviously depends on the application.In most applications, an algorithm will execute the plan; however, sometimes theuser may be a human. Imagine, for example, that the planning algorithm providesyou with an investment strategy. A generic term that will used frequently hereto refer to the user is decision maker. In robotics, the decision maker is simplyreferred to as a robot. In artificial intelligence and related areas, it has becomepopular in recent years to use the term agent, possibly with adjectives to make

1.2. ILLUSTRATIVE PROBLEMS 5

intelligent agent or software agent. Control theory usually refers to the decisionmaker as a system or plant. The plan in this context is sometimes referred to asa policy or control law. In a game-theoretic context, it might make sense to referto decision makers as players. Regardless of the terminology used in a particulardiscipline, this book is concerned with planning algorithms that find a strategy forone or more decision makers. Therefore, it is important to remember that termslike “robot”, “agent”, and “system” are interchangeable.

Section 1.2 presents several motivating planning problems, and Section ??gives an overview of planning concepts that will appear throughout the book.

1.2 Illustrative Problems

This is only written for motion planning–need other examples from discrete plan-ning, game theory, etc.

Suppose that we have a tiny mobile robot that can move along the floor in abuilding. The task is to determine a path that it should follow from a startinglocation to a goal location, while avoiding collisions. A reasonable model can beformulated by assuming that the robot is a moving point in a two-dimensionalenvironment that contains obstacles.

Let W = R2 denote a two-dimensional world which contains a point robot,denoted by A. A subset, O, of the world is called the obstacle region. Let theremaining portion of the world, W \ O be referred to as the free space. Thetask is to design an algorithm that accepts an obstacle region defined by a set ofpolygons, an initial position, and a goal position. The algorithm must return apath that will bring the robot from the initial position to the goal position, whileonly traversing the free space.

1.3 Perspective

The following elements are common to basic planning problems:

1. State: Planning problems will involve a state space that captures all possiblesituations that could exist. The state could, for example, represent theconfiguration of a robot, the locations of tiles in a puzzle, or the positionand velocity of a helicopter. Both discrete (finite, or countably infinite) andcontinuous (uncountably infinite) state spaces will be allowed.

2. Time: All planning problems involve a sequence of decisions that must beapplied over time. Time might be explicitly modeled, as in a problem such asdriving a car as quickly as possible through an obstacle course. Alternatively,time may be implicit, by simply reflecting the fact that actions must followin succession, as in the case of solving the Rubik’s cube. The particulartime is unimportant, but the proper sequence must be maintained. Another

6 S. M. LaValle: Planning Algorithms

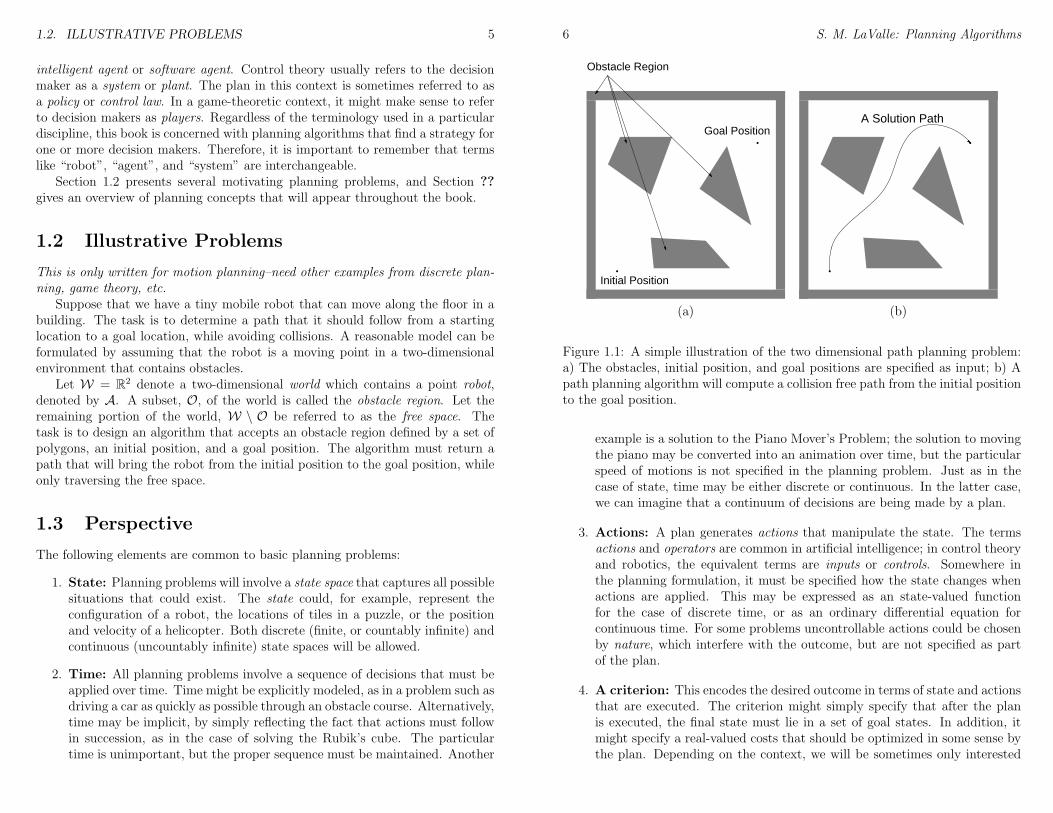

Goal Position

Obstacle Region

Initial Position

A Solution Path

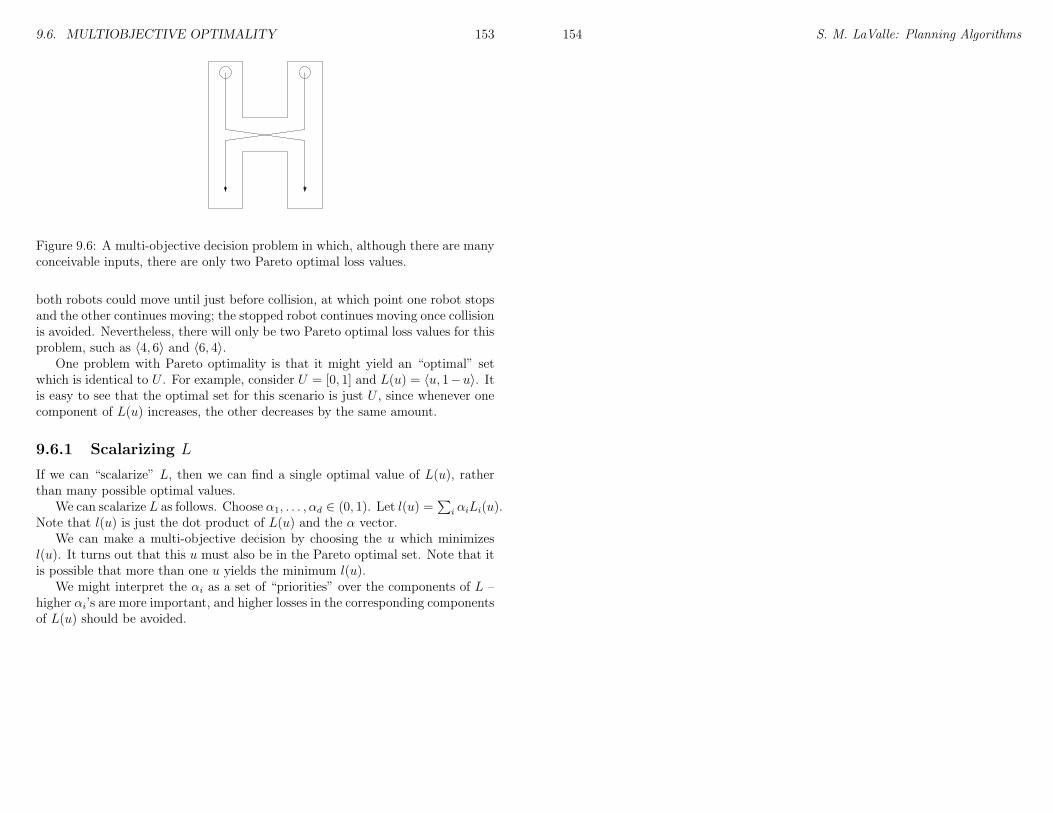

(a) (b)

Figure 1.1: A simple illustration of the two dimensional path planning problem:a) The obstacles, initial position, and goal positions are specified as input; b) Apath planning algorithm will compute a collision free path from the initial positionto the goal position.

example is a solution to the Piano Mover’s Problem; the solution to movingthe piano may be converted into an animation over time, but the particularspeed of motions is not specified in the planning problem. Just as in thecase of state, time may be either discrete or continuous. In the latter case,we can imagine that a continuum of decisions are being made by a plan.

3. Actions: A plan generates actions that manipulate the state. The termsactions and operators are common in artificial intelligence; in control theoryand robotics, the equivalent terms are inputs or controls. Somewhere inthe planning formulation, it must be specified how the state changes whenactions are applied. This may be expressed as an state-valued functionfor the case of discrete time, or as an ordinary differential equation forcontinuous time. For some problems uncontrollable actions could be chosenby nature, which interfere with the outcome, but are not specified as partof the plan.

4. A criterion: This encodes the desired outcome in terms of state and actionsthat are executed. The criterion might simply specify that after the planis executed, the final state must lie in a set of goal states. In addition, itmight specify a real-valued costs that should be optimized in some sense bythe plan. Depending on the context, we will be sometimes only interested

1.3. PERSPECTIVE 7

3 54

2

1

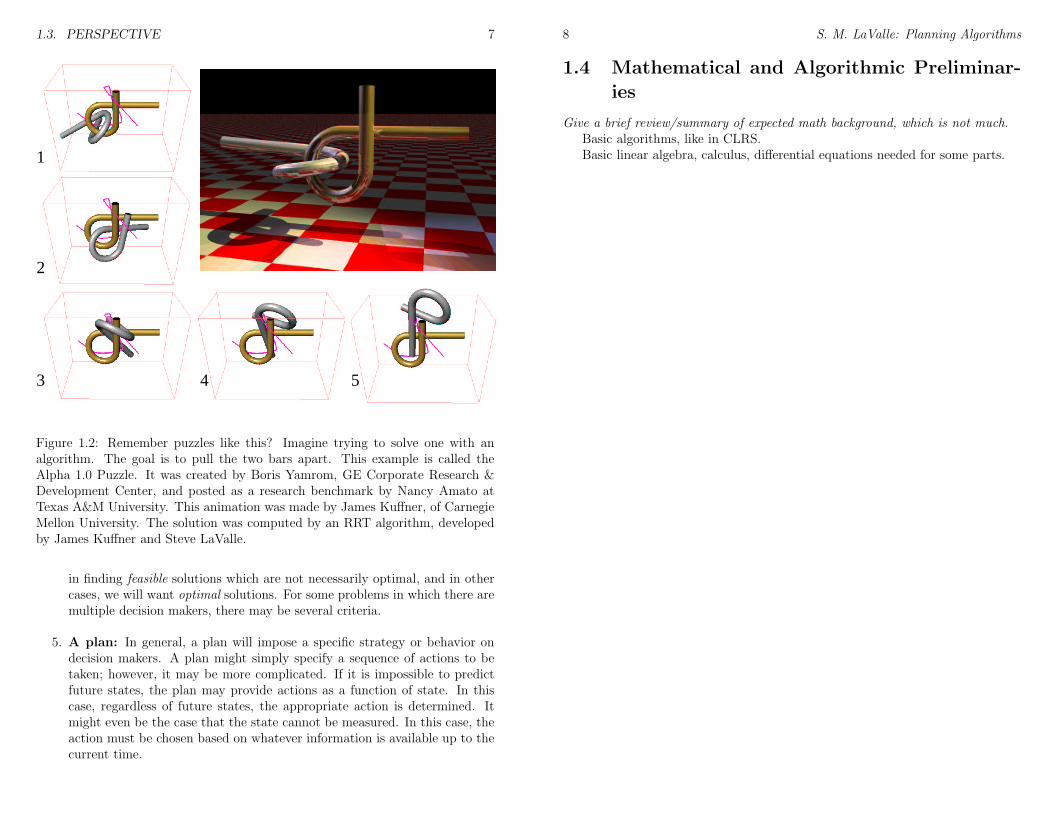

Figure 1.2: Remember puzzles like this? Imagine trying to solve one with analgorithm. The goal is to pull the two bars apart. This example is called theAlpha 1.0 Puzzle. It was created by Boris Yamrom, GE Corporate Research &Development Center, and posted as a research benchmark by Nancy Amato atTexas A&M University. This animation was made by James Kuffner, of CarnegieMellon University. The solution was computed by an RRT algorithm, developedby James Kuffner and Steve LaValle.

in finding feasible solutions which are not necessarily optimal, and in othercases, we will want optimal solutions. For some problems in which there aremultiple decision makers, there may be several criteria.

5. A plan: In general, a plan will impose a specific strategy or behavior ondecision makers. A plan might simply specify a sequence of actions to betaken; however, it may be more complicated. If it is impossible to predictfuture states, the plan may provide actions as a function of state. In thiscase, regardless of future states, the appropriate action is determined. Itmight even be the case that the state cannot be measured. In this case, theaction must be chosen based on whatever information is available up to thecurrent time.

8 S. M. LaValle: Planning Algorithms

1.4 Mathematical and Algorithmic Preliminar-

ies

Give a brief review/summary of expected math background, which is not much.Basic algorithms, like in CLRS.Basic linear algebra, calculus, differential equations needed for some parts.

Chapter 2

Discrete Planning

This covers discrete, classical AI planning, which models no uncertaintiesSome parts of the current contents come from my class notes of CS497 Spring

2003, which were originally scribed by Rishi Talreja.

2.1 Introduction

The chapter provides introductory concepts that serve as an entry point intoother parts of the book. The planning problems considered here are the simplestto describe because the state space will be finite in most cases. When it is notfinite, it will at least be countably infinite (i.e., every state can be enumeratedwith a distinct integer). Therefore, no geometric models or differential equationswill be needed to characterize the discrete planning problems.

The most important parts of this chapter are the representations of planningproblems (Section ), and the basic search algorithms, which will be useful through-out the book as more complicated forms of planning are considered (Section 2.3).Section 2.4 takes a close look at optimal discrete planning, and various forms ofdynamic programming that can be applied. It is useful to understand these alter-native forms in the context of discrete planning because in more-general settings,only one particular form may apply. In the present setting, all of the variants canbe explained, to help you understand how they are related. Section 2.5 presentsseveral planning algorithms that were developed particularly for discrete planning.

Although this chapter addresses a form of planning, it may also be consideredproblem solving. Throughout the history of artificial intelligence research, thedistinction between problem solving and planning has been rather elusive. For ex-ample, in a current leading textbook [1], two of the eight major parts are termed“Problem-solving” and “Planning”. The problem solving part begins by stating,“Problem solving agents decide what to do by finding sequences of actions thatlead to desirable states.” ([1], p. 59). The planning part begins with, “The task ofcoming up with a sequence of actions that will achieve a goal is called planning.”([1], p. 375). The STRIPS system is considered one of the first planning algo-

9

10 S. M. LaValle: Planning Algorithms

rithms and representations [?], and its name means STanford Research InstituteProblem Solver. Perhaps the term “planning” carries connotations of future time,where as “problem solving” sounds somewhat more general. A problem solvingtask might be to take evidence from a crime scene and piece together the actionstaken by suspects. It might seem odd to call this a “plan” because it occurred inthe past.

Given that there are no clear distinctions between problem solving and plan-ning, we will simply refer to both as planning. This also helps to keep with thetheme of the book. Note, however, that some of the concepts apply to a broaderset of problems that what is often meant by planning.

2.2 Three Representations of Discrete Planning

In this section, we formulate discrete planning three different ways. Althoughthis might seem tedious, there are good reasons to give redundant formulations.Section 2.2.1 introduces STRIPS-like representations, which have been used inthe earliest formulations of planning, and for certain kinds of problems, they offercompact representations. One problem with these representations is that they aredifficult to generalize to problems that involve concerns such as uncertainty orcontinuous variables. This motivates the introduction of the state space represen-tation in Section 2.2.2. It will be easy to extend and adapt this representation tothe problems covered throughout this book. Since many forms of planning reduceto a kind of search, it will be sometimes convenient to refer to a graph representa-tion of planning, which is the subject of Section 2.2.3. In this way, some forms ofplanning may be understood as running a search algorithm on a large, unexploredgraph.

2.2.1 STRIPS-Like Representation

STRIPS and its variants are the most common representations of planning prob-lems in artificial intelligence. The STRIPS language is a very simple logic basedonly on (ground) literals and predicates. Let I denote a finite set of instances(often referred to as propositional literals), which serve as the basic objects in theworld. For example, I, might include the names of automobile parts in a planningproblem that involves assembling a car. For example,

I = Radiator, RadiatorHose, Alternator, SparkP lug.

Let P denote a finite set of predicates, which are binary valued functions ofone or more instances. In other words, each p ∈ P , may be considered as p :I×I×· · ·×I → False, True. An example might be a predicate called Attached,which indicates which automobile parts are attached. Example values could beAttached(RadiatorHose,Radiator) = true andAttached(SparkP lug,Radiator) =

2.2. THREE REPRESENTATIONS OF DISCRETE PLANNING 11

false). In some applications, it might make sense to restrict the domain of eachp to “relevant” instances; however, this will not be considered here.

As far as planning is concerned, the state of the world is completely determinedonce the predicates are fully specified. Every possible question regarding theinstances will have an answer of true or false. If each predicate was a functionof exactly k instances, then there would be |P | |I|k possible questions. Typically,the number of arguments will vary over the predicates. Each question is referredto as a (first-order) literal. If the literal is true, it is called positive; otherwise, itis called negative.

The state of the world can be specified by giving the complete set of positiveliterals. All other literals are assumed to be negative. The initial state is specifiedin this way. The goal is expressed as a set of positive and negative literals. Thetask of a planning is to transform the world into any state that satisfies all of thegoal literals. Any literals not mentioned the goal are permitted to be either trueor false.

To solve a planning problem, we need to transform the world from one stateto another. This is achieved by a set, O, of operators. In addition to its name,each operator has two components:

1. The precondition, which lists positive and negative literals that must besatisfied for the operator to be applicable. To avoid tedious specifications ofpreconditions for every instance, variables are allowed to appear in predicatearguments. For example, Attached(x,Radiator) indicates that anythingmay be attached to the radiator for the operator to apply. Without usingthe variable x, we would be required to define an operator for every instance.

2. The effect, which specifies precisely how the world is changed. Some literalsmay be made positive, and others may be made negative. This is specifiedas a list of positive and negative literals. Any literals not mentioned in theoperator effect are unaffected by the operator. Variables may also be usedhere.

Consider the following example, based on contemporary politics. Suppose thatGeorge W. Bush’s team of experts is using STRIPS planning to determine someway to avoid hostile threats. Suppose that the instances are country names,

I = Canada, France, Iraq, Thailand, China, Zaire, ....

The predicates are

P = HasWMD,Friendly, Angry,

each of which is assumed to be a function from I to false, true.The world must be manipulated through operators. Suppose there are only

two:O = Attack,Befriend.

12 S. M. LaValle: Planning Algorithms

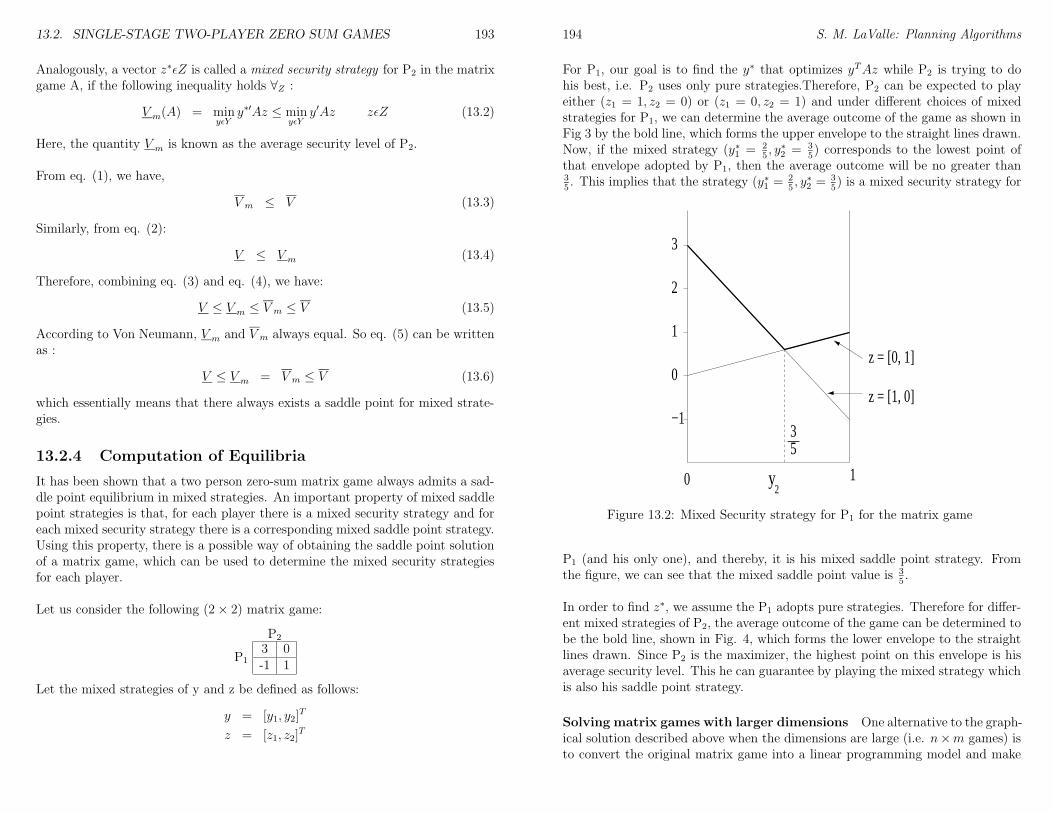

The Attack operator could be defined as

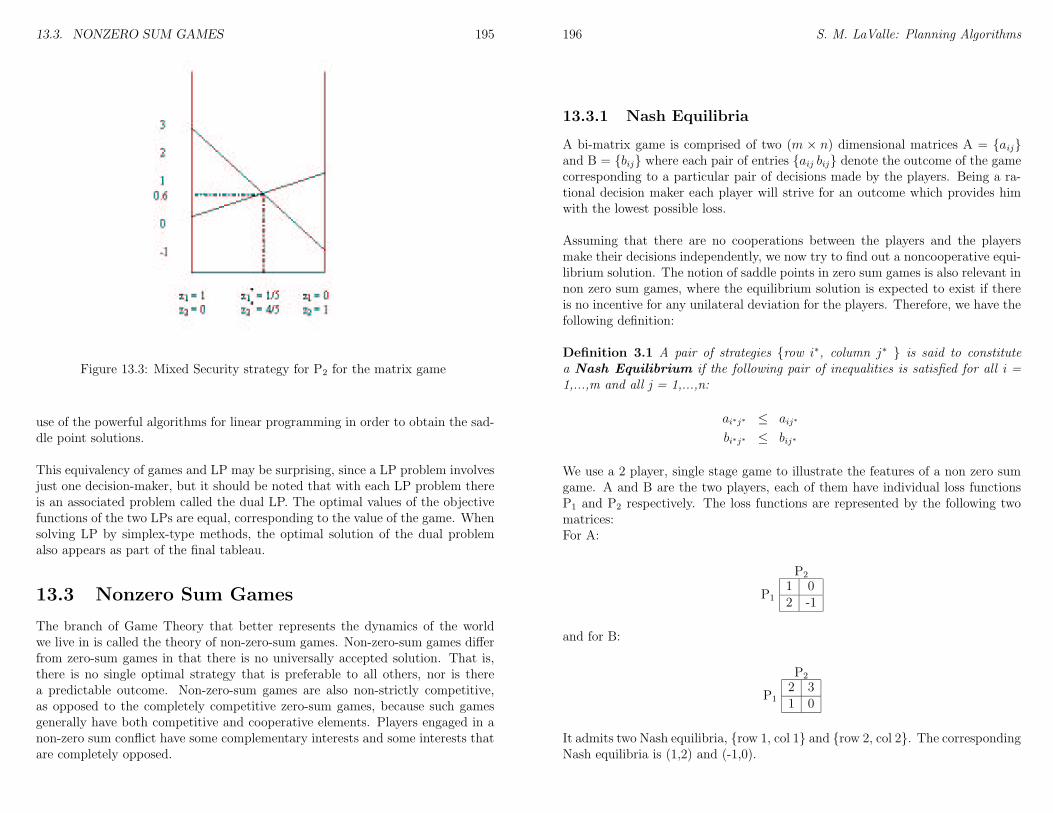

Op(NAME : Attack(i),

PRECONDITION : HasWMD(i) ∧ ¬Friendly(i),

EFFECT : ¬HasWMD(i) ∧ Angry(i))

Above, logic notation has been used: ∧means logical conjunction (AND); ¬meanslogical negation (NOT). The precondition states that the operator can be appliedwhen a country has weapons of mass destruction and is not friendly. Under thesame condition, another operator that could be applied is

Op(NAME : Befriend(i),

PRECONDITION : HasWMD(i) ∧ ¬Friendly(i),

EFFECT : Friendly(i))

Initially, the values for all predicates are fully specified. The goal could requirespecific countries to be without weapons of mass destruction, and others to befriendly. One kind of goal that seems reasonable is to have every country, i, tobe either Friendly(i) or ¬HasWMD(i). Unfortunately, such disjunctive goalsare not allowed in the original STRIPS representation. It is possible, however, toextend the representation to allow this.

Once all of the components have been specified, the planning task can bestated. Find a sequence of operators that can be applied in succession from theinitial state, and that cause the world to be transformed into a goal state.

The STRIPS representation is very nice for representing planning problems ina descriptive way that corresponds closely to the application. Also, the operatordefinitions enable problems that have enormous complexity to be expressed com-pactly in many cases. One problem with these representations, however, is thatthey are difficult to extend to more general settings.

2.2.2 State Space Representation

Consider representing the discrete planning problem in terms of states and statetransitions. We first give a list of formal definitions, and then describe how toconvert a planning problem represented with STRIPS operators in to a state spacerepresentation.

1. Let X be a nonempty, finite set which is called the state space. Let x ∈ Xdenote a specific state.

2. Let xI denote the initial state.

2.2. THREE REPRESENTATIONS OF DISCRETE PLANNING 13

3. Let XG ⊂ X denote a set of goal states.

4. For each x ∈ X, let U(x) denote a nonempty, finite set of actions. LetU = ∪x∈XU(x) denote the set of all possible actions.

5. Define a partial function, f : X × U → X, called the state transition equa-tion. This is used to produce new states, x′ = f(x, u), given some statex ∈ X and action u ∈ U(x). The reason f is a partial function is becausesome actions are not applicable in some states.

Now consider converting a planning problem represented with STRIPS into thestate space representation. The set of questions from Section ?? may be encodedas a sequence of bits, referred to as a binary string, by imposing an linear orderingto the instances, I, and the predicates, P . The state of the world is then specifiedin order,. Using the example from Section 2.2.1, this might appear like:

(HasWMD(Russia),¬HasWMC(Jamaica), . . . , F riendly(Canada), . . .).

Using the binary string, each element can be “0” to denote false, or “1” to denotetrue. The resulting state would be x = 110 · · · 1 · · · .

The initial state xI is given by specifying a string, and XG is the set of allstrings that are consistent with the goal positive and negative goal literals. Youcan alternatively imagine a string that has a “0” for each negative literal, a “1”for each positive literal, and a “δ” for all others, in which the δ means “don’tcare.”

The next step is to convert the operators. For each state, x ∈ X, the set U(x)will represent the set of operators who preconditions are satisfied by the statex. The effect of the operator is encoded by the state transition equation. If thestate is given, it is straightforward to determine which bits to flip in the string,resulting in x′.

There are both advantages and disadvantages to the the state space represen-tation. First, consider disadvantages. One obvious drawback with the state spacerepresentation described here is the useful descriptive information that appearedin the STRIPS model has been dropped. Also, note that using the STRIPS modelit might be possible to succinctly describe a planning problem that would be ex-tremely tedious to specify using the state space representation. Many problemsto which the STRIPS model is applied have huge state spaces, which are muchtoo large to fit into any electronic storage. Therefore, it is not feasible to performthe entire conversion as described above.

Next, consider advantages. First of all, the representation does not need tobe explicitly constructed by an algorithm. It is more useful as a precise way toformulate and analyze planning problems. In algorithms, any one of a number ofrepresentations may be preferable depending on the context. However, regardlessof the representation chosen in implementation, an underlying state space can be

14 S. M. LaValle: Planning Algorithms

defined. It is implicitly determined once the planning problem is defined, eventhough there is not an explicit representation of it.

The most significant advantage of the state space representation is that is gen-eralizes nicely to many other planning problems. It is very difficult to incorporateelements such as probabilistic uncertainty, continuous instance spaces, and game-theoretic notions into the STRIPS model. On the other hand, it is very naturalto incorporate these notions using the state space representation. In fact, mostof the literature on these more complicated problems, which have been studied inartificial intelligence, robotics, and control theory, all involve state space repre-sentations. Therefore, the state space representation will be prevalent throughoutthis book. However, one should remember that in a particular implementation,an alternative representation, such as STRIPS, might be preferable (if it can bedirectly used).

2.2.3 Graph Representation

Once the state space representation has been given, it is not difficult to see anunderlying graph structure in which the states are vertices, and the actions aredirected edges that connect states. Let G = (V,E) be a directed graph. Define thevertex set to be the set of all possible states, V = X. The edge set is somewhattricky to define. From every vertex, a set of outgoing edges is defined in whichthere is one edge for each u ∈ U(x). The set, E, of all edges, represents the unionof all of these edges. Note that E is generally larger than the set U because thesame action may apply at many states, and each time it generates a new edge inE.

The graph representation will seem most natural at the algorithm level, espe-cially for planning problems that reduce to a kind of search. Just as in the caseof the state space representation, the graph representation does not have to beexplicitly constructed in advance. In viewing planning as a kind of search, we canimagine that an enormous graph is implicitly defined once the STRIPS model isgiven for a particular problem. The planning problem reduces to exploring thisgraph in the hopes of finding a goal state. This is the topic of Section 2.3.

2.3 Search Algorithms

We already know that the discrete planning problem may be interpreted as asearch in a graph. In most applications, the graph is enormous, but not explicitlyencoded at the outset. Instead, the graph is gradually revealed, step by step,through the use of a search algorithm. Graph searching is a basic part of algo-rithms [17]. The presentation in this section can be considered as graph searchalgorithms tailored to planning problems.

2.3. SEARCH ALGORITHMS 15

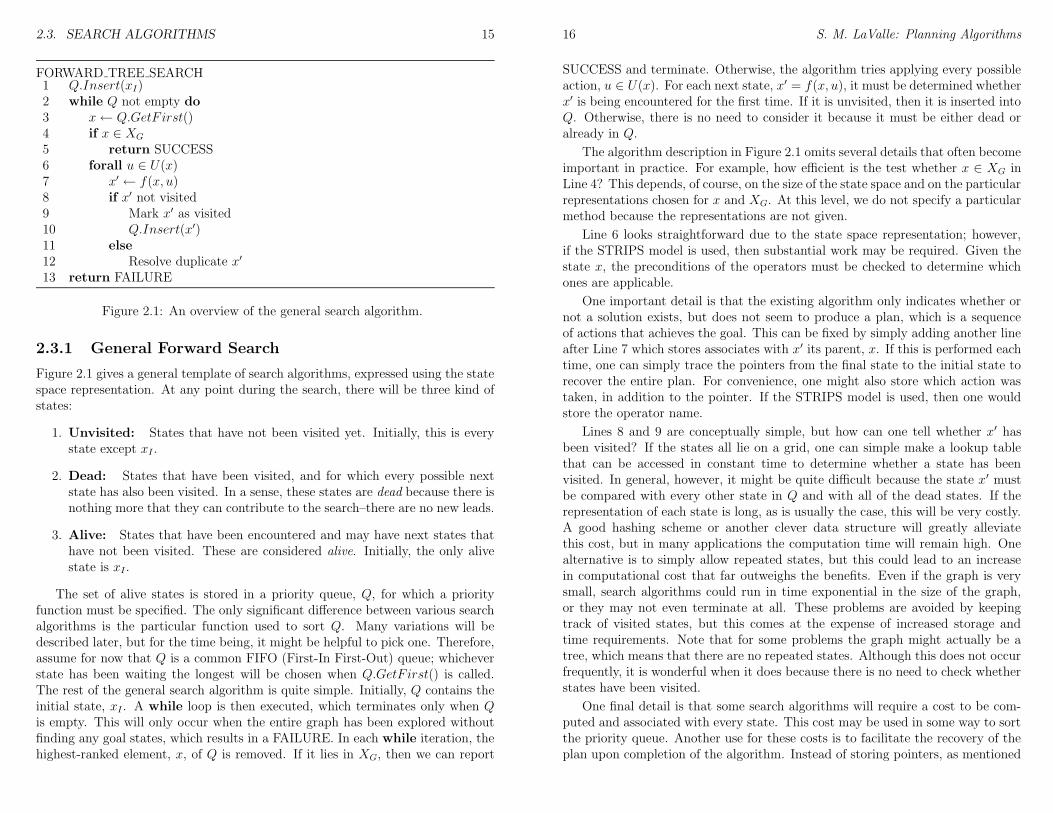

FORWARD TREE SEARCH1 Q.Insert(xI)2 while Q not empty do3 x← Q.GetF irst()4 if x ∈ XG

5 return SUCCESS6 forall u ∈ U(x)7 x′ ← f(x, u)8 if x′ not visited9 Mark x′ as visited10 Q.Insert(x′)11 else12 Resolve duplicate x′

13 return FAILURE

Figure 2.1: An overview of the general search algorithm.

2.3.1 General Forward Search

Figure 2.1 gives a general template of search algorithms, expressed using the statespace representation. At any point during the search, there will be three kind ofstates:

1. Unvisited: States that have not been visited yet. Initially, this is everystate except xI .

2. Dead: States that have been visited, and for which every possible nextstate has also been visited. In a sense, these states are dead because there isnothing more that they can contribute to the search–there are no new leads.

3. Alive: States that have been encountered and may have next states thathave not been visited. These are considered alive. Initially, the only alivestate is xI .

The set of alive states is stored in a priority queue, Q, for which a priorityfunction must be specified. The only significant difference between various searchalgorithms is the particular function used to sort Q. Many variations will bedescribed later, but for the time being, it might be helpful to pick one. Therefore,assume for now that Q is a common FIFO (First-In First-Out) queue; whicheverstate has been waiting the longest will be chosen when Q.GetF irst() is called.The rest of the general search algorithm is quite simple. Initially, Q contains theinitial state, xI . A while loop is then executed, which terminates only when Qis empty. This will only occur when the entire graph has been explored withoutfinding any goal states, which results in a FAILURE. In each while iteration, thehighest-ranked element, x, of Q is removed. If it lies in XG, then we can report

16 S. M. LaValle: Planning Algorithms

SUCCESS and terminate. Otherwise, the algorithm tries applying every possibleaction, u ∈ U(x). For each next state, x′ = f(x, u), it must be determined whetherx′ is being encountered for the first time. If it is unvisited, then it is inserted intoQ. Otherwise, there is no need to consider it because it must be either dead oralready in Q.

The algorithm description in Figure 2.1 omits several details that often becomeimportant in practice. For example, how efficient is the test whether x ∈ XG inLine 4? This depends, of course, on the size of the state space and on the particularrepresentations chosen for x and XG. At this level, we do not specify a particularmethod because the representations are not given.

Line 6 looks straightforward due to the state space representation; however,if the STRIPS model is used, then substantial work may be required. Given thestate x, the preconditions of the operators must be checked to determine whichones are applicable.

One important detail is that the existing algorithm only indicates whether ornot a solution exists, but does not seem to produce a plan, which is a sequenceof actions that achieves the goal. This can be fixed by simply adding another lineafter Line 7 which stores associates with x′ its parent, x. If this is performed eachtime, one can simply trace the pointers from the final state to the initial state torecover the entire plan. For convenience, one might also store which action wastaken, in addition to the pointer. If the STRIPS model is used, then one wouldstore the operator name.

Lines 8 and 9 are conceptually simple, but how can one tell whether x′ hasbeen visited? If the states all lie on a grid, one can simple make a lookup tablethat can be accessed in constant time to determine whether a state has beenvisited. In general, however, it might be quite difficult because the state x′ mustbe compared with every other state in Q and with all of the dead states. If therepresentation of each state is long, as is usually the case, this will be very costly.A good hashing scheme or another clever data structure will greatly alleviatethis cost, but in many applications the computation time will remain high. Onealternative is to simply allow repeated states, but this could lead to an increasein computational cost that far outweighs the benefits. Even if the graph is verysmall, search algorithms could run in time exponential in the size of the graph,or they may not even terminate at all. These problems are avoided by keepingtrack of visited states, but this comes at the expense of increased storage andtime requirements. Note that for some problems the graph might actually be atree, which means that there are no repeated states. Although this does not occurfrequently, it is wonderful when it does because there is no need to check whetherstates have been visited.

One final detail is that some search algorithms will require a cost to be com-puted and associated with every state. This cost may be used in some way to sortthe priority queue. Another use for these costs is to facilitate the recovery of theplan upon completion of the algorithm. Instead of storing pointers, as mentioned

2.3. SEARCH ALGORITHMS 17

previously, the optimal cost to to return to the initial state could be stored witheach state. This cost alone is sufficient to determine the action sequence thatleads to any state visited state. Solution paths can be constructed in the sameway by using the computed costs after running Dijkstra’s algorithm.

2.3.2 Particular Forward Search Methods

We now discuss several single-tree search algorithms, each of which is a special caseof the algorithm in Figure 2.1, obtained by defining a different sorting functionfor Q. Most of these are just classical graph search algorithms; see [17]. Sincethe graph is finite, all of the methods below are complete: if a solution exists, thealgorithm will find it; otherwise, it will terminate in finite time and report failure.The completeness is based on the assumption that the algorithm keeps track ofvisited states. Without this information some of the algorithms below may runforever by cycling through the same states.

Breadth First

The method given in Section 2.3.1 specifiesQ as a FIFO queue, which selects statesusing the first-come, first-serve principle. This causes the search frontier to growuniformly, and is therefore referred to as breadth-first search. All plans that havek steps are exhausted before plans with k + 1 steps are investigated. Therefore,breadth first guarantees that the first solution found will use the smallest numberof steps. Upon detection that a state has been revisited, there is no work to do inLine 12. Given its systematic exploration, breadth first search is complete withoutkeeping track of visited states (although the running time increases dramatically).

The running time breadth first search is O(|V | + |E|), in which |V | and |E|are the numbers of vertices and edges, respectively, in the graph representationof the planning problem. This assumes that all operations, such as determiningwhether a state has been visited, are performed in constant time. In practice,these operations will typically require more time, and must be counting as partof the algorithm complexity. The running time be expressed in terms of the otherrepresentations. Recall that |V | = |X| is the number of states. If the sameactions, U , are available from every state, then |E| = |U ||X|. If action sets U(x1)and U(x2) are pairwise disjoint for any x1, x2 ∈ X, then |E| = |U |. In terms ofSTRIPS, the case of the same actions available from any state would mean thatall operators can be applied from any state, resulting in |E| = |O||X|. In the caseof pairwise disjoint actions, each operator applies only in a single state, resultingin |E| = |O||X|. Recall that |X| can be expressed in terms of the number ofinstances and predicates, if all predicates have the same number, k, of arguments.The result is |X| = |I||P |k.

18 S. M. LaValle: Planning Algorithms

Depth First

By making Q a stack (Last-In, First-Out), aggressive exploration is the graphoccurs, as opposed to the uniform expansion of breadth first search. The resultingvariant is called depth first search because the search dives quickly into the graph.The preference is toward investigating longer plans very early. Although thisaggressive behavior might seem desirable, note that the particular choice of longerplans is arbitrary. Actions are applied in the forall loop in whatever order theyhappen to be defined. Once again, if a state is revisited, there is no work to do inLine 12. The running time of this algorithm is also O(|V |+ |E|).

Dynamic Programming (Dijkstra)

Up to this point, there has been no reason to prefer any action or operator overany other in the search. Section 2.4 will formalize optimal discrete planning, andwill present several algorithms that find optimal plans. Before going into that,we present an optimal planning here as a variant of forward search. The resultis the well-known Dijkstra’s algorithm for finding single-source shortest paths ina graph []. Suppose that every edge, e ∈ E, in the graph representation of adiscrete planning problem, has an associated positive cost l(e), which is the costto apply the action or operator. The cost l(e) could be written using the statespace representation as l(x, u), indicating that it costs l(x, u) to apply action ufrom state x. The total cost of a plan is just the sum of the edge costs over thepath from the initial state to a goal state.

The priority queue, Q, will be sorted according to a function, L∗ : X → [0,∞],called the optimal cost-to-come or just cost-to-come if it is clearly optimal fromthe context. For each state, x, the value L∗(x) will represent the optimal cost toreach x from the initial state, xI . This optimal cost is obtained by summing edgecosts, l(e), over all possible paths from xI to x, and using the path produces theleast cumulative cost.

The cost-to-come is computed incrementally during the execution of the searchalgorithm in Figure 2.1. Initially, L∗(xI) = 0. Each time the state x′ is generated,a cost is computed as: L(x′) = L∗(x) + l(e), in which e is the edge from x to x′

(equivalently, we may write L(x′) = L∗(x) + l(x, u)). Here, L(x′) represents bestcost-to-come that is known so far, but we do not write L∗ because it is not yetknown whether x′ was reached optimally. Because of this, some work is requiredin Line 12. If x′ already exists in Q, then it is possible that the newly-discoveredpath to x′ is more efficient. If so, then the cost-to-come value L(x′) must beupdated for x′, and Q must be updated accordingly.

When does L(x) finally become L∗(x) for some state x? Once x is removedfrom Q using Q.GetF irst(), the state becomes dead, and it is known that there isno better way to reach it. This can be argued by induction. For the initial state,L∗(xI) is known, and this serves as the base case. Now assume that all deadstates have their optimal cost-to-come correctly determined. This means that

2.3. SEARCH ALGORITHMS 19

their cost-to-come values can no longer change. For the first element, x, of Q, thevalue must be optimal because any path that has lower total cost would have totravel through another state in Q, but these states already have higher cost. Allpaths that pass only through dead states were already considered in producingL(x). Once all edges leaving x are explored, then x can be declared as dead, andthe induction continues. This is not enough detail to constitute a proof; muchmore detailed arguments appear in [17]. The running time is O(|V | lg |V |+|E|), inwhich |V | and |E| are the numbers of edges and vertices, respectively, in the graphrepresentation of the discrete planning problem. This assumes that the priorityqueue is implemented with a Fibonacci heap, and that all other operations, suchas determining whether a state has been visited, are performed in constant time.If other data structures are used to implement the priority queue, then differentrunning times will be obtained.

A∗

The A∗ search algorithm is a variant of dynamic programming that tries to reducethe total number of states explored by incorporating a heuristic estimate of thecost to get the goal from a given state. Let LI(x) denote the cost-to-come from xIto x, and let LG(x) denote the cost-to-go from x to some state in XG. AlthoughL∗I(x) can be computed incrementally by dynamic programming, there is no wayto know the true optimal cost-to-go. However, in many applications it is possibleto construct a reasonable underestimate of this cost. For example, if you aretrying to get from one point to another in a labyrinth, the line-of-sight distanceserves as a reasonable underestimate of the distance you must travel through thecorridors of the labyrinth. Of course, zero could also serve as an underestimate,but that will not provide any helpful information to the algorithm. The aim is tocompute an estimate that is as close as possible to the optimal cost-to-go, and isalso guaranteed to be no greater. Let LG(x) denote such an estimate.

The A∗ search algorithm works in exactly the same way as the previous dy-namic programming algorithm. The only difference is the function used to sort Q.In the A∗ algorithm, the sum LI(x

′) + LG(x′) is used, implying that the priority

queue is sorted by estimates of the optimal cost from xI to XG. If LG(x) is anunderestimate of the true optimal cost-to-go for all x ∈ X, the A∗ algorithm isguaranteed to find optimal plans [?, ?]. As LG becomes closer to LG, fewer nodestend to be explored in comparison with dynamic programming. This would al-ways seem advantageous, but in some problems it is not possible to find a goodheuristic. Note that when LG(x) = 0 for all x ∈ X, then A∗ degenerates to theprevious dynamic programming algorithm.

Best First

For best first search, the priority queue is sorted according to LG, which is anestimate of the optimal cost-to-go. The solutions obtained in this way are not

20 S. M. LaValle: Planning Algorithms

necessarily optimal; therefore, it does not matter whether or not the estimateexceeds the true optimal cost-to-go. Although optimal solutions are not found,in many cases, far fewer nodes are explored, which results in much faster runningtimes. There is no guarantee, however, that this will happen. The worst-case per-formance of best first search is worst than that of A∗ and dynamic programming.One must be careful when applying it in practice. In a sense, the approach is themost greedy of the algorithms so far because it prefers states that “look good”very early in the search. If these are truly the best states, then great performancebenefits are obtained. If they are not, then the price must be paid for beinggreedy!

Need to make a 2D local minimum example for this algorithm, and maybe acouple of others. The spiral death trap is good for this one.

Iterative Deepening

Depth limited and IDA∗ can fit here.

2.3.3 Other General Search Schemes

This section covers two other general templates for search algorithms. The firstone is simply a “backwards” version of the tree search algorithm in Figure 2.1.The second one is a bidirectional approach that grows two search trees, one fromthe initial state, and one from a goal state.

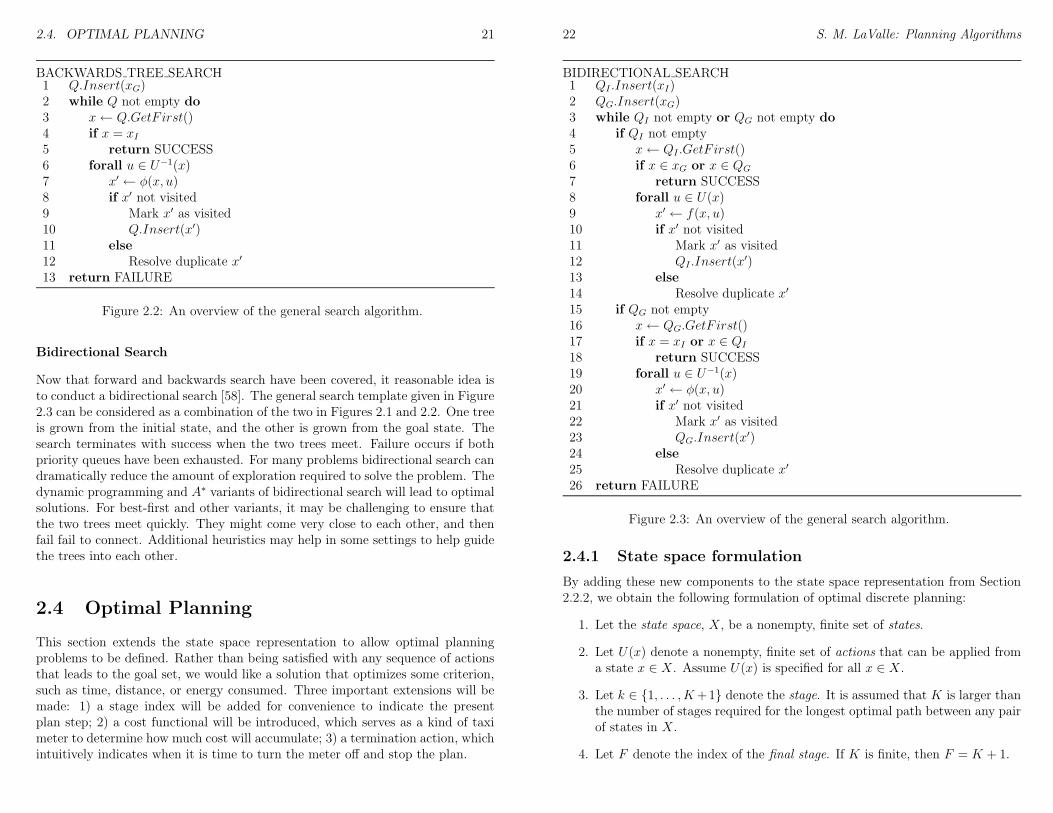

Backwards Tree Search

Suppose that there is a single goal state, xG. For many planning problems, it mightbe the case that the branching factor is large when starting from xI . It this cases,it might be more efficient to start the search at a goal state and work backwardsuntil the initial state is encountered. A general template for this approach is givenin Figure 2.2. To apply this idea, the particular planning problem must allow usto define an inverse of the state transition equation. In the forward search case,an action u ∈ U is applied at a state x ∈ X, to obtain a new state, x′ = f(x, u).To enable backwards search, we must be able to determine a set of state/actionpairs that bring the world into some state x in one step. For a given state x, letU−1(x) denote the set of actions that could be applied from other states to arriveat x. In other words, if u ∈ U−1(x), then there exists some x′ ∈ X and u ∈ U(x′)such that x = f(x′, u). The state x′ is given by the expression φ(x, u) in Line 7,which is determined by inverting f , the state transition equation. If it possible toperform such an inversion, then there is a perfect symmetry with respect to theforward search of Section 2.3.1. Any of the search algorithm variants from Section2.3.2 could be adapted to the template in Figure 2.2.

2.4. OPTIMAL PLANNING 21

BACKWARDS TREE SEARCH1 Q.Insert(xG)2 while Q not empty do3 x← Q.GetF irst()4 if x = xI5 return SUCCESS6 forall u ∈ U−1(x)7 x′ ← φ(x, u)8 if x′ not visited9 Mark x′ as visited10 Q.Insert(x′)11 else12 Resolve duplicate x′

13 return FAILURE

Figure 2.2: An overview of the general search algorithm.

Bidirectional Search

Now that forward and backwards search have been covered, it reasonable idea isto conduct a bidirectional search [58]. The general search template given in Figure2.3 can be considered as a combination of the two in Figures 2.1 and 2.2. One treeis grown from the initial state, and the other is grown from the goal state. Thesearch terminates with success when the two trees meet. Failure occurs if bothpriority queues have been exhausted. For many problems bidirectional search candramatically reduce the amount of exploration required to solve the problem. Thedynamic programming and A∗ variants of bidirectional search will lead to optimalsolutions. For best-first and other variants, it may be challenging to ensure thatthe two trees meet quickly. They might come very close to each other, and thenfail fail to connect. Additional heuristics may help in some settings to help guidethe trees into each other.

2.4 Optimal Planning

This section extends the state space representation to allow optimal planningproblems to be defined. Rather than being satisfied with any sequence of actionsthat leads to the goal set, we would like a solution that optimizes some criterion,such as time, distance, or energy consumed. Three important extensions will bemade: 1) a stage index will be added for convenience to indicate the presentplan step; 2) a cost functional will be introduced, which serves as a kind of taximeter to determine how much cost will accumulate; 3) a termination action, whichintuitively indicates when it is time to turn the meter off and stop the plan.

22 S. M. LaValle: Planning Algorithms

BIDIRECTIONAL SEARCH1 QI .Insert(xI)2 QG.Insert(xG)3 while QI not empty or QG not empty do4 if QI not empty5 x← QI .GetF irst()6 if x ∈ xG or x ∈ QG

7 return SUCCESS8 forall u ∈ U(x)9 x′ ← f(x, u)10 if x′ not visited11 Mark x′ as visited12 QI .Insert(x

′)13 else14 Resolve duplicate x′

15 if QG not empty16 x← QG.GetF irst()17 if x = xI or x ∈ QI

18 return SUCCESS19 forall u ∈ U−1(x)20 x′ ← φ(x, u)21 if x′ not visited22 Mark x′ as visited23 QG.Insert(x

′)24 else25 Resolve duplicate x′

26 return FAILURE

Figure 2.3: An overview of the general search algorithm.

2.4.1 State space formulation

By adding these new components to the state space representation from Section2.2.2, we obtain the following formulation of optimal discrete planning:

1. Let the state space, X, be a nonempty, finite set of states.

2. Let U(x) denote a nonempty, finite set of actions that can be applied froma state x ∈ X. Assume U(x) is specified for all x ∈ X.

3. Let k ∈ 1, . . . , K+1 denote the stage. It is assumed that K is larger thanthe number of stages required for the longest optimal path between any pairof states in X.

4. Let F denote the index of the final stage. If K is finite, then F = K + 1.

2.4. OPTIMAL PLANNING 23

5. Let f denote a state transition equation, which yields xk+1 = f(xk, uk) forany xk ∈ X and uk ∈ U(xk).

6. Let xI denote the initial state, and let xG denote the goal state. Alterna-tively, we may consider a set of goal states, XG, or there may be no explicitgoal.

7. Let L denote an additive loss functional, which is applied to the sequence,u1, . . . , uK , of applied actions, and achieved states, x1, . . . , xF :

L =K∑

k=1

l(xk, uk) + lF (xF ). (2.1)

The final term, lF (xF ) is usually defined as lF (xF ) = 0 if xF ∈ XG, andlF (xF ) =∞ otherwise.

8. Each U(x) contains a special termination action, uT . If uT is applied to xk,then the action is repeatedly applied until stage K, and the state remainsin xk until the final stage. Furthermore, no loss accumulates: l(xk, uT ) = 0for any k and xk.

9. The task is to find a sequence of actions, u1, . . . , uK that minimizes L.

To correspond to STRIPS planning, the following cost functions can be used:l(x, u) = 0, lF (xF ) = 0 if xF ∈ XG and lF (xF ) = 1, otherwise. To obtain optimal-step planning, let l(x, u) = 1, lF (xF ) = 0 if xF ∈ XG and lF (xF ) =∞, otherwise.

2.4.2 Backwards dynamic programming

Since it involves less notation, we first consider the case of backwards dynamic pro-gramming. In this case, dynamic programming becomes a recursive formulationof the optimal cost-to-go to the goal.

Suppose that the final-stage loss is defined as lF (xF ) = 0 if xF = xG, andlF (xF ) =∞ otherwise. The final-stage optimal cost-to-go is:

L∗F,F (xF ) = lF (xF ). (2.2)

This makes intuitive sense: since there are no stages in which an action can beapplied, we immediately receive the penalty for not being in the goal.

For an intermediate stage, k ∈ 2, . . . , K the following represents the optimalcost-to-go:

L∗k,F (xk) = minuk,...,uK

K∑

i=k

l(xi, ui) + lF (xF )

(2.3)

In the minimization above, it is assumed that ui ∈ U(xi) for every i ∈ k, . . . ,K.Equation (2.3) expresses the lowest possible loss that can be received by starting

24 S. M. LaValle: Planning Algorithms

from xk and applying actions over K − k + 1 stages. The termination action canbe applied at any stage, but a loss, lF (xF ) must be paid at the final stage. Thus,if you are not already in the goal, you are forced to move; otherwise, infinite losswill be obtained.

The final step in backwards dynamic programming is the arrival at the initialstage. The cost-to-go in this case is

L∗1,F (x1) = minu1,...,uK

lI(x1) +K∑

i=1

l(xi, ui) + lF (xF )

, (2.4)

in which lI(x1) denotes an initial loss. For most applications of backwards dynamicprogramming, we can safely make lI(x1) = 0 for all x1 ∈ X. In forward dynamicprogramming, lI becomes more important, and lF becomes unimportant.

The dynamic programming equation expresses L∗k,F in terms of L∗k+1,F :

L∗k,F (xk) = minuk∈U(xk)

L∗k+1,F (xk+1) + l(xk, uk)

. (2.5)

Note that xk+1 is given by the state transition equation: xk+1 = f(xk, uk).

2.4.3 Forward dynamic programming

Dynamic programming in this case involves the recursive formulation of the cost-to-come from an initial state. Notice that the concepts here are the symmetricequivalent of backwards dynamic programming concepts.

Suppose that the initial loss is defined as lI(x1) = 0 if x1 = xI , and lI(x1) =∞otherwise. This will ensure that only paths that start at xI are considered (in thebackwards case, lF ensures that only paths which end at xG are considered).

The initial optimal cost-to-come is:

L∗1,1(x1) = lI(x1). (2.6)

For an intermediate stage, k ∈ 2, . . . , K the following represents the optimalcost-to-come:

L∗1,k(xk) = minu1,...,uk−1

lI(x1) +k−1∑

i=1

l(xi, ui)

. (2.7)

Note that the sum refers to a sequence of states, x1, . . . , xk, which are the result ofapplying the action sequence u1, . . . , uk−1. As in (2.3) it is assumed that ui ∈ U(xi)for every i ∈ 1, . . . , k − 1. The resulting xk, obtained after applying uk−1 mustbe the same xk that is named in the argument on the right side of (2.7). It mightappear odd that x1 appears inside the min above; however, this is not a problem.The state x1 can be completely determined once u1, . . . , uk−1 and xk are given.

The final step in forward dynamic programming is the arrival at the final stage.The cost-to-come in this case is

L∗1,F (xF ) = minu1,...,uK

lI(x1) +K∑

i=1

l(xi, ui) + lF (xF )

. (2.8)

2.4. OPTIMAL PLANNING 25

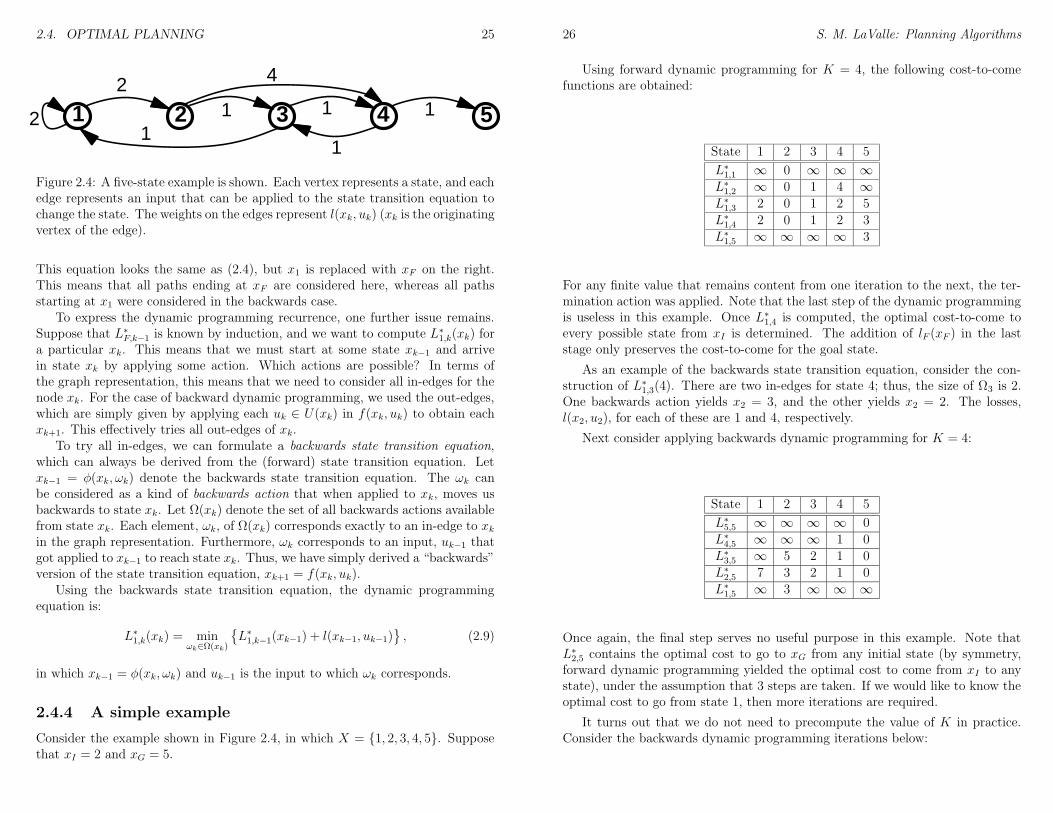

1 2 3 4 52

11

111

42

Figure 2.4: A five-state example is shown. Each vertex represents a state, and eachedge represents an input that can be applied to the state transition equation tochange the state. The weights on the edges represent l(xk, uk) (xk is the originatingvertex of the edge).

This equation looks the same as (2.4), but x1 is replaced with xF on the right.This means that all paths ending at xF are considered here, whereas all pathsstarting at x1 were considered in the backwards case.

To express the dynamic programming recurrence, one further issue remains.Suppose that L∗F,k−1 is known by induction, and we want to compute L∗1,k(xk) fora particular xk. This means that we must start at some state xk−1 and arrivein state xk by applying some action. Which actions are possible? In terms ofthe graph representation, this means that we need to consider all in-edges for thenode xk. For the case of backward dynamic programming, we used the out-edges,which are simply given by applying each uk ∈ U(xk) in f(xk, uk) to obtain eachxk+1. This effectively tries all out-edges of xk.

To try all in-edges, we can formulate a backwards state transition equation,which can always be derived from the (forward) state transition equation. Letxk−1 = φ(xk, ωk) denote the backwards state transition equation. The ωk canbe considered as a kind of backwards action that when applied to xk, moves usbackwards to state xk. Let Ω(xk) denote the set of all backwards actions availablefrom state xk. Each element, ωk, of Ω(xk) corresponds exactly to an in-edge to xkin the graph representation. Furthermore, ωk corresponds to an input, uk−1 thatgot applied to xk−1 to reach state xk. Thus, we have simply derived a “backwards”version of the state transition equation, xk+1 = f(xk, uk).

Using the backwards state transition equation, the dynamic programmingequation is:

L∗1,k(xk) = minωk∈Ω(xk)

L∗1,k−1(xk−1) + l(xk−1, uk−1)

, (2.9)

in which xk−1 = φ(xk, ωk) and uk−1 is the input to which ωk corresponds.

2.4.4 A simple example

Consider the example shown in Figure 2.4, in which X = 1, 2, 3, 4, 5. Supposethat xI = 2 and xG = 5.

26 S. M. LaValle: Planning Algorithms

Using forward dynamic programming for K = 4, the following cost-to-comefunctions are obtained:

State 1 2 3 4 5

L∗1,1 ∞ 0 ∞ ∞ ∞L∗1,2 ∞ 0 1 4 ∞L∗1,3 2 0 1 2 5

L∗1,4 2 0 1 2 3

L∗1,5 ∞ ∞ ∞ ∞ 3

For any finite value that remains content from one iteration to the next, the ter-mination action was applied. Note that the last step of the dynamic programmingis useless in this example. Once L∗1,4 is computed, the optimal cost-to-come toevery possible state from xI is determined. The addition of lF (xF ) in the laststage only preserves the cost-to-come for the goal state.

As an example of the backwards state transition equation, consider the con-struction of L∗1,3(4). There are two in-edges for state 4; thus, the size of Ω3 is 2.One backwards action yields x2 = 3, and the other yields x2 = 2. The losses,l(x2, u2), for each of these are 1 and 4, respectively.

Next consider applying backwards dynamic programming for K = 4:

State 1 2 3 4 5

L∗5,5 ∞ ∞ ∞ ∞ 0

L∗4,5 ∞ ∞ ∞ 1 0

L∗3,5 ∞ 5 2 1 0

L∗2,5 7 3 2 1 0

L∗1,5 ∞ 3 ∞ ∞ ∞

Once again, the final step serves no useful purpose in this example. Note thatL∗2,5 contains the optimal cost to go to xG from any initial state (by symmetry,forward dynamic programming yielded the optimal cost to come from xI to anystate), under the assumption that 3 steps are taken. If we would like to know theoptimal cost to go from state 1, then more iterations are required.

It turns out that we do not need to precompute the value of K in practice.Consider the backwards dynamic programming iterations below:

2.5. OTHER APPROACHES 27

State 1 2 3 4 5

L∗9,9 ∞ ∞ ∞ ∞ 0

L∗8,9 ∞ ∞ ∞ 1 0

L∗7,9 ∞ 5 2 1 0

L∗6,9 7 3 2 1 0

L∗5,9 5 3 2 1 0

L∗4,9 5 3 2 1 0

L∗3,9 5 3 2 1 0

L∗2,9 5 3 2 1 0

L∗1,9 ∞ 3 ∞ ∞ ∞

After some number of iterations, the cost-to-go values stabilize. After this point,the termination action is being applied from all reachable states and no furtherloss accumulates. Once the values remain constant, the iterations can be stopped.If some vertices are not reachable, their values will also remain constant, at ∞.

How is an optimal action sequence returned? Assume that backwards dynamicprogramming is used. One method that always works is to store the action, uk,that minimized (10.15) at vertex xk. Alternatively, if the final step is skipped,then the optimal action sequence can be obtained using any starting state byrepeatedly selecting uk to minimize

L∗(xk+1) + l(xk, uk), (2.10)

in which L∗ denotes the stabilized cost-to-go that is computed by the backwardsdynamic programming computations (skipping the final step, which converts mostvalues to ∞).

COMPARE TO DIJKSTRA’S ALGORITHM FROM SECTION 2.3.

2.5 Other Approaches

Maybe cover partial order planning, hierarchical planning, ... this could easilyexpand into 2 or 3 sections. If there gets to be too much material for this chapter,then another chapter can be started.

Literature

Fikes, R.E. and Nilsson, N.J. (1971) ”STRIPS: a New Approach to the Applicationof Theorem Proving”, Artificial Intelligence,2, 189-208.

Korf, R.E. (1988) Search: A Survey of Recent Results. In H.E. Shrobe (ed.)Exploring Artificial Intelligence: Survey Talks from the National ConferencesonArtificial Intelligence,San Mateo: Morgan Kaufmann.

Pearl, J. (1984) Heuristics: Intelligent Search Strategies for Computer ProblemSolving,Reading, MA: Addison-Wesley.

28 S. M. LaValle: Planning Algorithms

Exercies

1. Reformulate the general search algorithm of Section 2.3 so that it is ex-pressed in terms of STRIPS-like operators.

Part II

Motion Planning

29

31

Overview of Part II: Motion Planning

Chapters 3-8 cover planning problems and algorithms that are inrpired by roboticsapplications. The topic will generally be referred to as motion planning, and thedecision maker will generally be referred to as a robot (even though it may notbe a robot in many applications). These problems involve geometric reasoningin continuous spaces; therefore, Chapter 3 covers geometric modeling and trans-formations of geometric models. This provides sufficient backgound to express amotion planning problem, which can be considered as a kind of search through acontinuous space of transformations. Chapter 4 presents the mathematical con-cepts needed to accurately characterize the spaces of transformations that typi-cally arise in motion planning. These are referred to as configuration spaces.

Following Chapters 3 and 4, you should have all of the background needed tounderstand and develop motion planning algorithms. These algorithms are gener-ally organized into two categories: combinatorial (Chapter 5) and sampling-based(Chapter 6). Combinatorial motion algorithms typically convert the continuousplanning motion planning problem into one that is discrete, without even los-ing any information. They provide what are sometimes called exact or completesolutions to the motion planning problem. Sampling-based algorithms usuallyinvolve the use of a collision-detection algorithm to iteratively probe the config-uration space while searching for a solution. In contrast to combinatorial algo-rithms, sampling-based algorithms are not exact; however, they are typically muchmore efficient at finding solutions to challenging problems that arise in practice.The combinatorial algorithms can theoretically solve the most difficult of motionplanning problems, but implementation difficulty and long running times haveinhibited widespread application. For many special motion planning problems,however, they lead to elegant solutions that are much more efficient than thoseobtained by sampling-based methods. Therefore, it is important to study bothkind of methods before determining which style is appropriate for your problemof interest.