Embed Size (px)

DESCRIPTION

Lecture 4 International Finance FN5053/6033. FOREIGN EXCHANGE MARKET OPERATIONS AND MECHANICS. The Foreign Exchange Market. International Trade and Finance of current magnitude would not be possible without the buying and selling of foreign currencies. - PowerPoint PPT Presentation

Citation preview

Lecture 4International Finance

FN5053/6033

FOREIGN EXCHANGE MARKET OPERATIONS AND MECHANICS

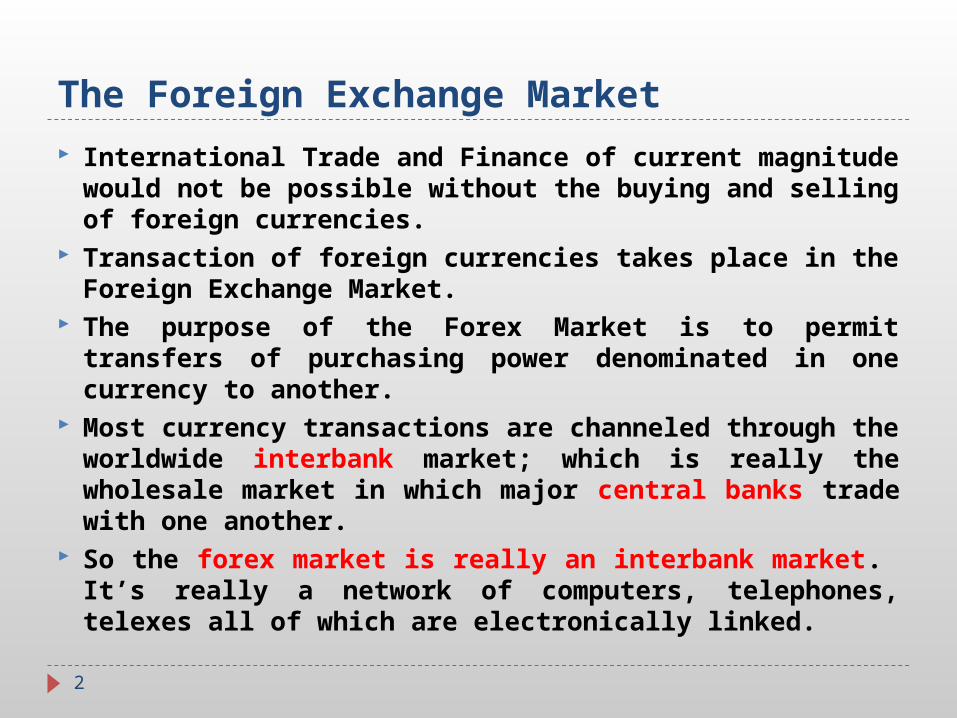

The Foreign Exchange Market International Trade and Finance of current

magnitude would not be possible without the buying and selling of foreign currencies.

Transaction of foreign currencies takes place in the Foreign Exchange Market.

The purpose of the Forex Market is to permit transfers of purchasing power denominated in one currency to another.

Most currency transactions are channeled through the worldwide interbank market; which is really the wholesale market in which major central banks trade with one another.

So the forex market is really an interbank market. It’s really a network of computers, telephones, telexes all of which are electronically linked.

2

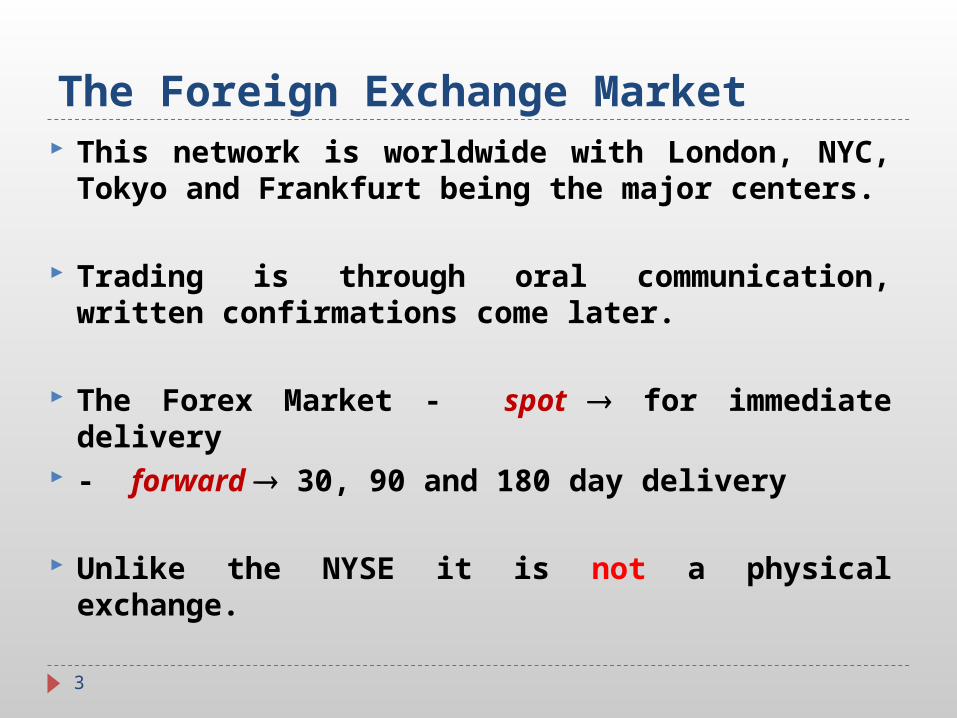

The Foreign Exchange Market This network is worldwide with London, NYC,

Tokyo and Frankfurt being the major centers.

Trading is through oral communication, written confirmations come later.

The Forex Market - spot for immediate delivery

- forward 30, 90 and 180 day delivery

Unlike the NYSE it is not a physical exchange.

3

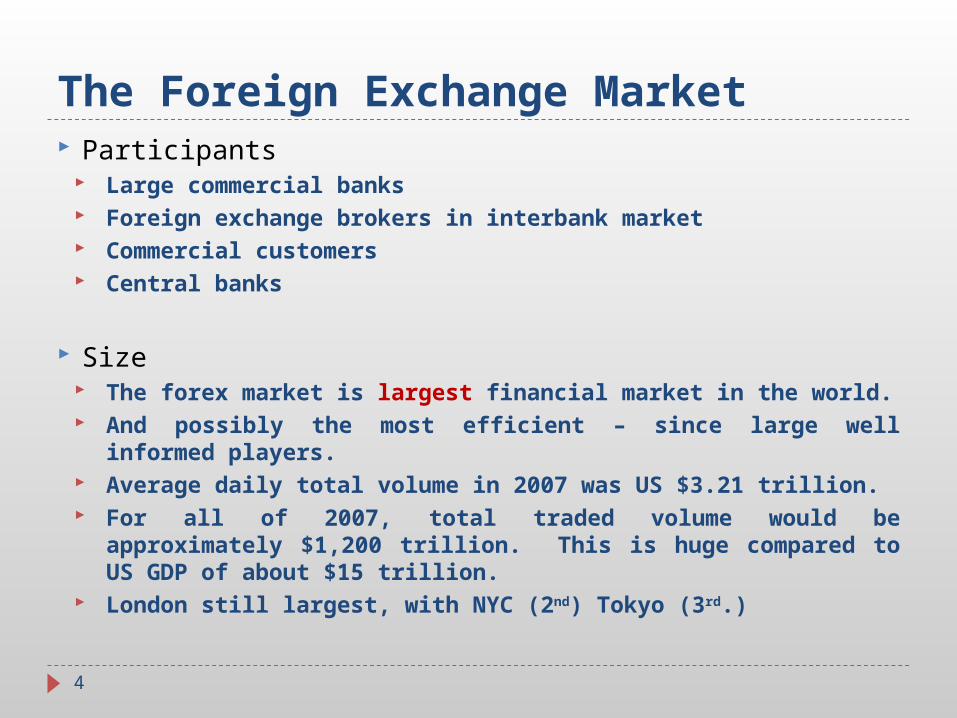

The Foreign Exchange Market Participants

Large commercial banks Foreign exchange brokers in interbank market Commercial customers Central banks

Size The forex market is largest financial market in the world. And possibly the most efficient – since large well informed

players. Average daily total volume in 2007 was US $3.21 trillion. For all of 2007, total traded volume would be

approximately $1,200 trillion. This is huge compared to US GDP of about $15 trillion.

London still largest, with NYC (2nd) Tokyo (3rd.)

4

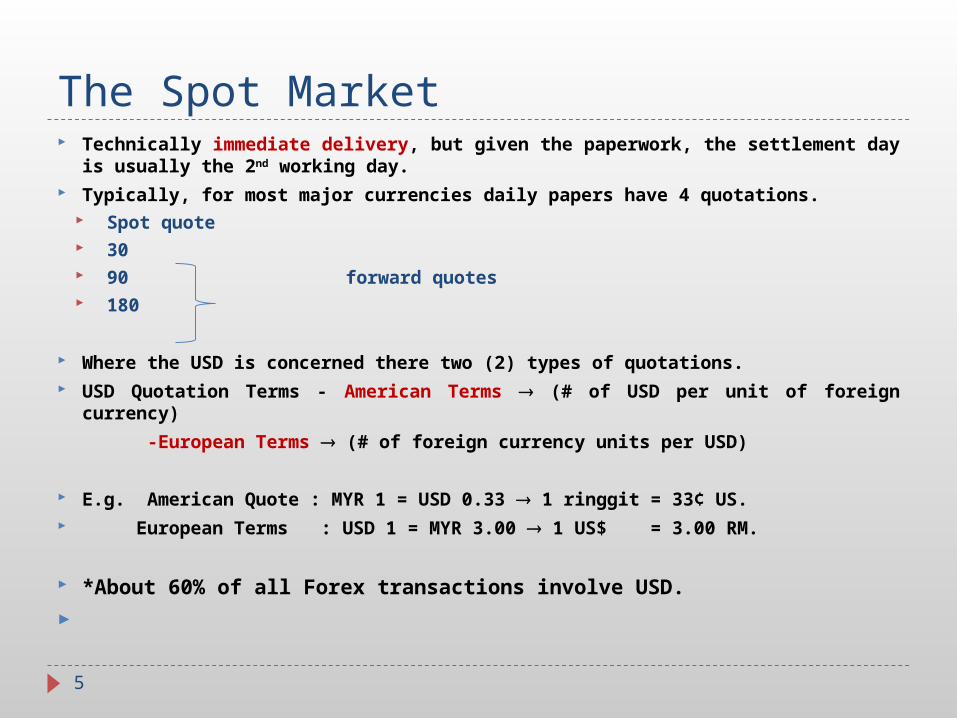

The Spot Market Technically immediate delivery, but given the paperwork, the settlement day

is usually the 2nd working day. Typically, for most major currencies daily papers have 4 quotations.

Spot quote 30 90 forward quotes 180

Where the USD is concerned there two (2) types of quotations. USD Quotation Terms - American Terms (# of USD per unit of foreign

currency)

-European Terms (# of foreign currency units per USD)

E.g. American Quote : MYR 1 = USD 0.33 1 ringgit = 33¢ US. European Terms : USD 1 = MYR 3.00 1 US$ = 3.00 RM.

*About 60% of all Forex transactions involve USD.

5

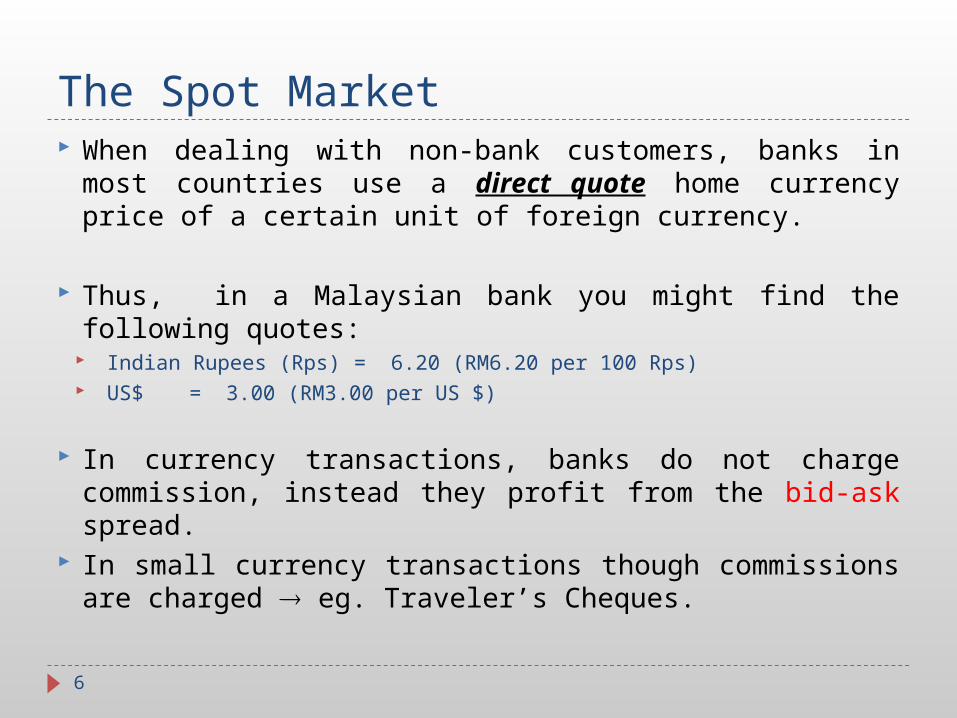

The Spot Market When dealing with non-bank customers, banks in

most countries use a direct quote home currency price of a certain unit of foreign currency.

Thus, in a Malaysian bank you might find the following quotes: Indian Rupees (Rps) = 6.20 (RM6.20 per 100 Rps) US$ = 3.00 (RM3.00 per US $)

In currency transactions, banks do not charge commission, instead they profit from the bid-ask spread.

In small currency transactions though commissions are charged eg. Traveler’s Cheques.

6

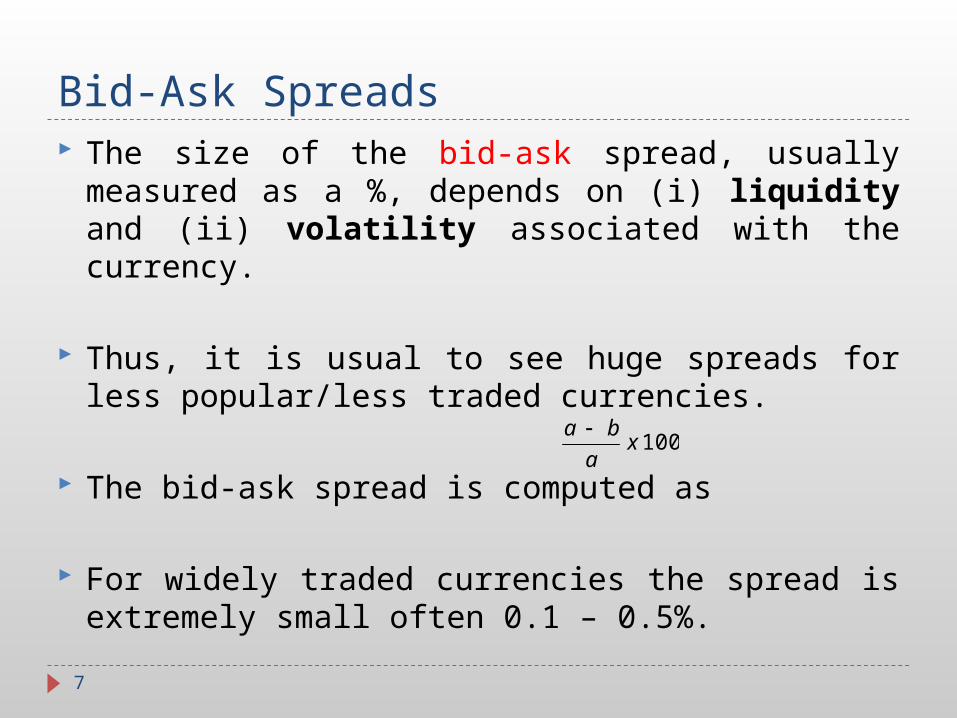

Bid-Ask Spreads The size of the bid-ask spread, usually measured

as a %, depends on (i) liquidity and (ii) volatility associated with the currency.

Thus, it is usual to see huge spreads for less popular/less traded currencies.

The bid-ask spread is computed as

For widely traded currencies the spread is extremely small often 0.1 – 0.5%.

7

100xa

ba

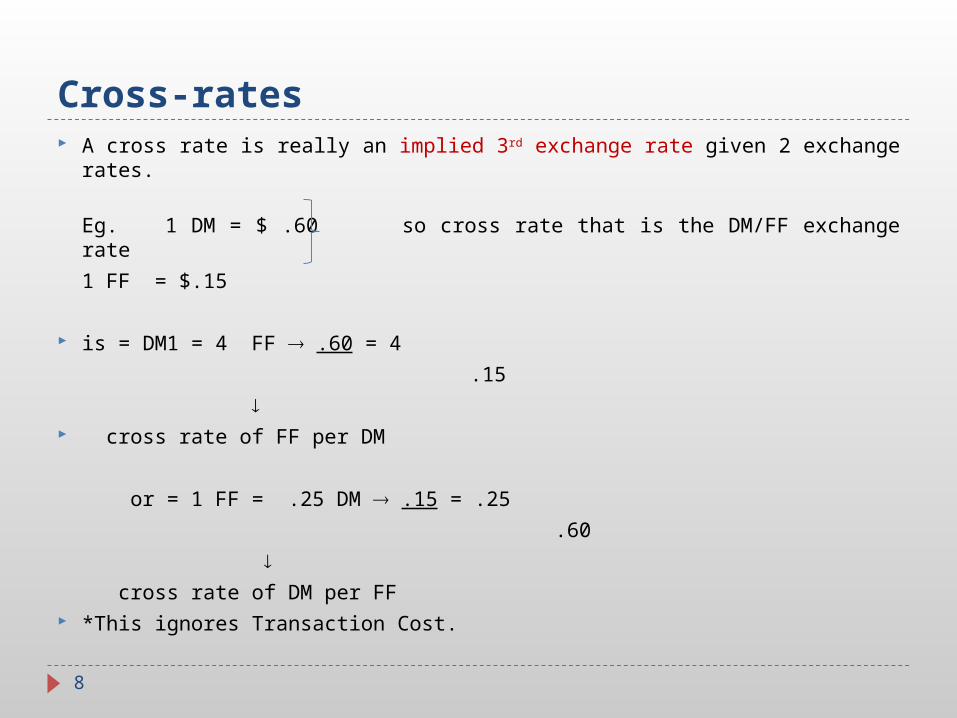

Cross-rates A cross rate is really an implied 3rd exchange rate given 2 exchange

rates.

Eg. 1 DM = $ .60 so cross rate that is the DM/FF exchange rate

1 FF = $.15

is = DM1 = 4 FF .60 = 4

.15

cross rate of FF per DM

or = 1 FF = .25 DM .15 = .25

.60

cross rate of DM per FF *This ignores Transaction Cost.

8

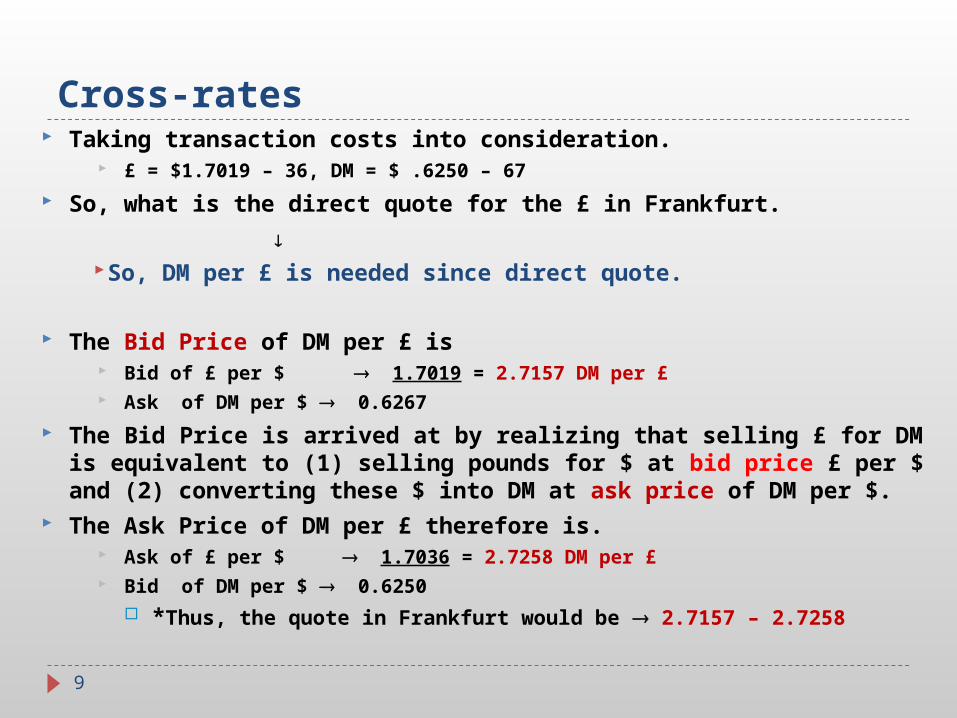

Cross-rates Taking transaction costs into consideration.

£ = $1.7019 – 36, DM = $ .6250 – 67

So, what is the direct quote for the £ in Frankfurt.

So, DM per £ is needed since direct quote.

The Bid Price of DM per £ is Bid of £ per $ 1.7019 = 2.7157 DM per £ Ask of DM per $ 0.6267

The Bid Price is arrived at by realizing that selling £ for DM is equivalent to (1) selling pounds for $ at bid price £ per $ and (2) converting these $ into DM at ask price of DM per $.

The Ask Price of DM per £ therefore is. Ask of £ per $ 1.7036 = 2.7258 DM per £ Bid of DM per $ 0.6250

*Thus, the quote in Frankfurt would be 2.7157 – 2.7258

9

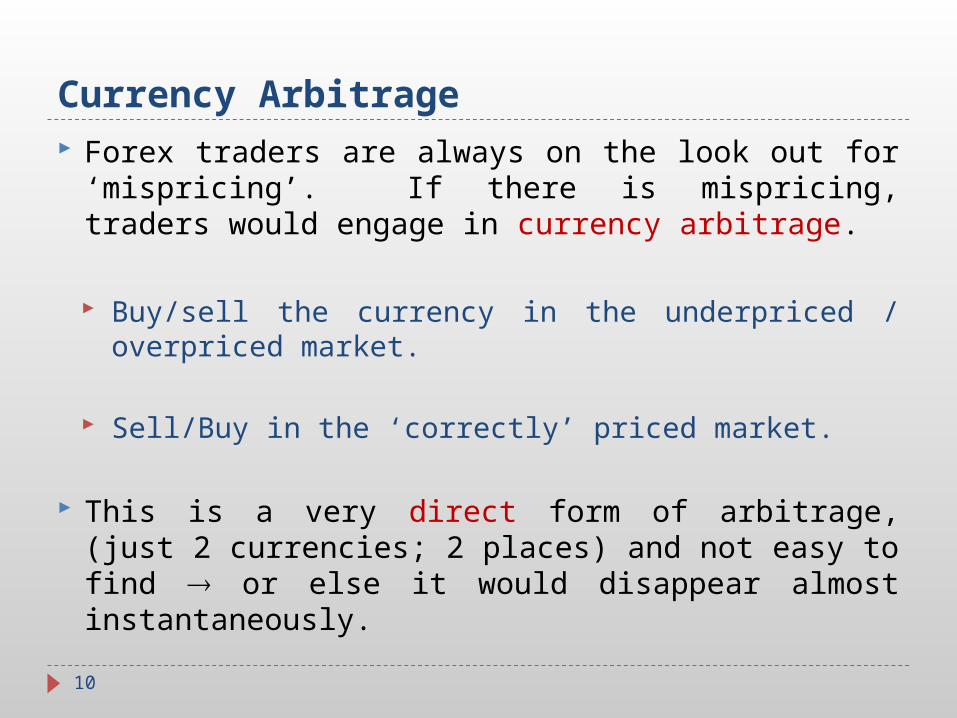

Currency Arbitrage Forex traders are always on the look out for

‘mispricing’. If there is mispricing, traders would engage in currency arbitrage.

Buy/sell the currency in the underpriced / overpriced market.

Sell/Buy in the ‘correctly’ priced market.

This is a very direct form of arbitrage, (just 2 currencies; 2 places) and not easy to find or else it would disappear almost instantaneously.

10

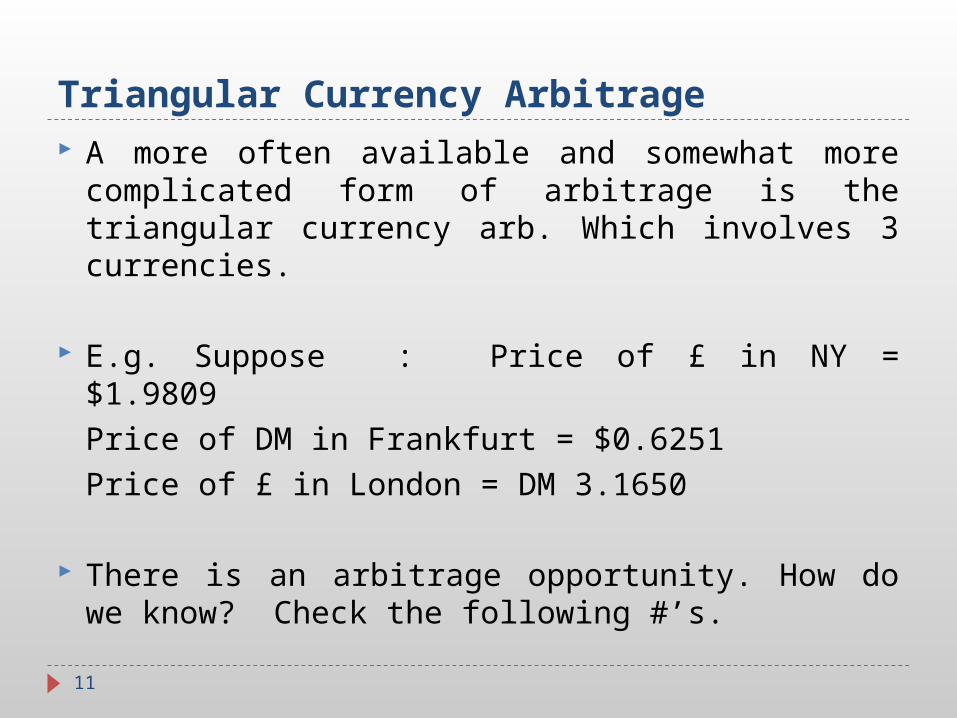

Triangular Currency Arbitrage A more often available and somewhat more

complicated form of arbitrage is the triangular currency arb. Which involves 3 currencies.

E.g. Suppose : Price of £ in NY = $1.9809Price of DM in Frankfurt =

$0.6251Price of £ in London = DM

3.1650

There is an arbitrage opportunity. How do we know? Check the following #’s.

11

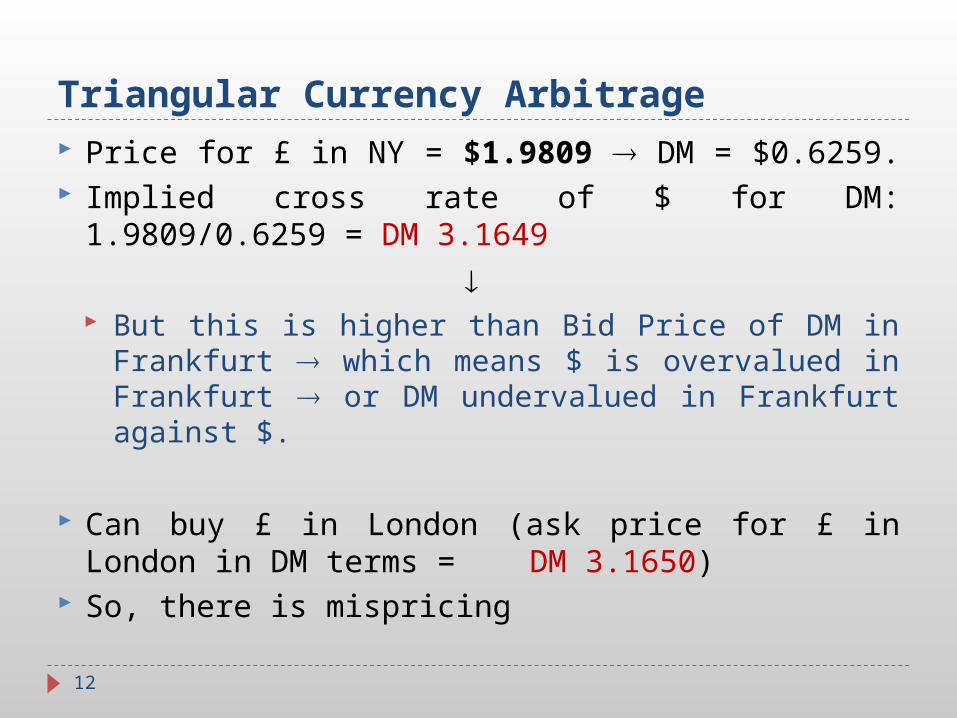

Triangular Currency Arbitrage Price for £ in NY = $1.9809 DM = $0.6259. Implied cross rate of $ for DM: 1.9809/0.6259 =

DM 3.1649

But this is higher than Bid Price of DM in Frankfurt

which means $ is overvalued in Frankfurt or DM undervalued in Frankfurt against $.

Can buy £ in London (ask price for £ in London in DM terms = DM 3.1650)

So, there is mispricing

12

Triangular Currency Arbitrage

13

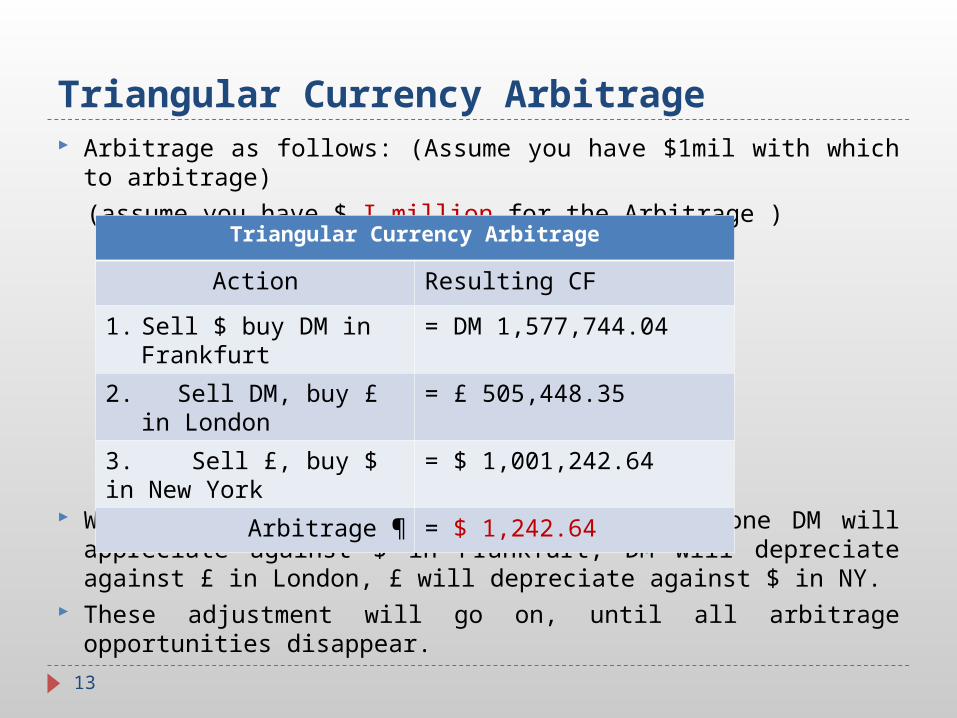

Arbitrage as follows: (Assume you have $1mil with which to arbitrage)

(assume you have $ I million for the Arbitrage )

When more and more of this arbitrage is done DM will appreciate against $ in Frankfurt, DM will depreciate against £ in London, £ will depreciate against $ in NY.

These adjustment will go on, until all arbitrage opportunities disappear.

Triangular Currency Arbitrage

Action Resulting CF

1. Sell $ buy DM in Frankfurt

= DM 1,577,744.04

2. Sell DM, buy £ in London

= £ 505,448.35

3. Sell £, buy $ in New York

= $ 1,001,242.64

Arbitrage ¶ = $ 1,242.64

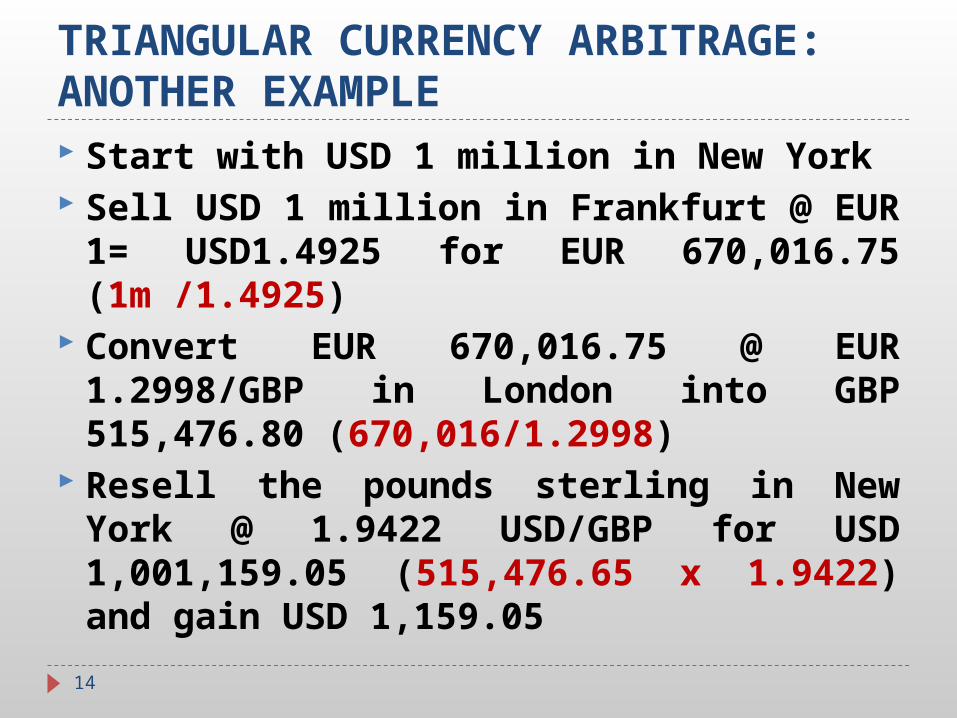

TRIANGULAR CURRENCY ARBITRAGE: ANOTHER EXAMPLE Start with USD 1 million in New York Sell USD 1 million in Frankfurt @ EUR

1= USD1.4925 for EUR 670,016.75 (1m /1.4925)

Convert EUR 670,016.75 @ EUR 1.2998/GBP in London into GBP 515,476.80 (670,016/1.2998)

Resell the pounds sterling in New York @ 1.9422 USD/GBP for USD 1,001,159.05 (515,476.65 x 1.9422) and gain USD 1,159.05

14

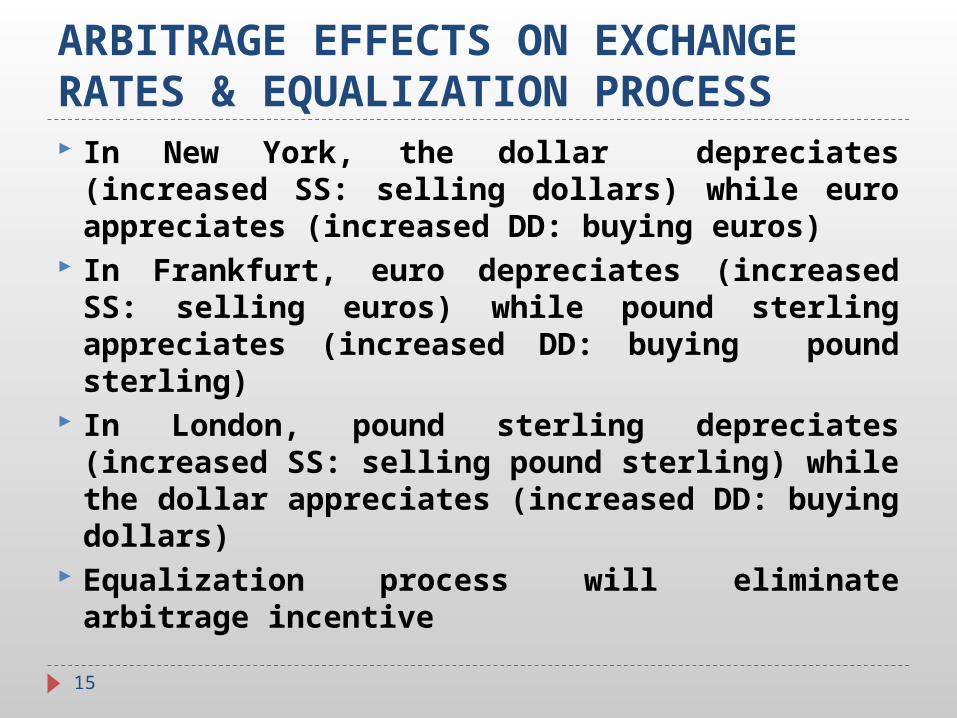

ARBITRAGE EFFECTS ON EXCHANGE RATES & EQUALIZATION PROCESS In New York, the dollar depreciates

(increased SS: selling dollars) while euro appreciates (increased DD: buying euros)

In Frankfurt, euro depreciates (increased SS: selling euros) while pound sterling appreciates (increased DD: buying pound sterling)

In London, pound sterling depreciates (increased SS: selling pound sterling) while the dollar appreciates (increased DD: buying dollars)

Equalization process will eliminate arbitrage incentive

15

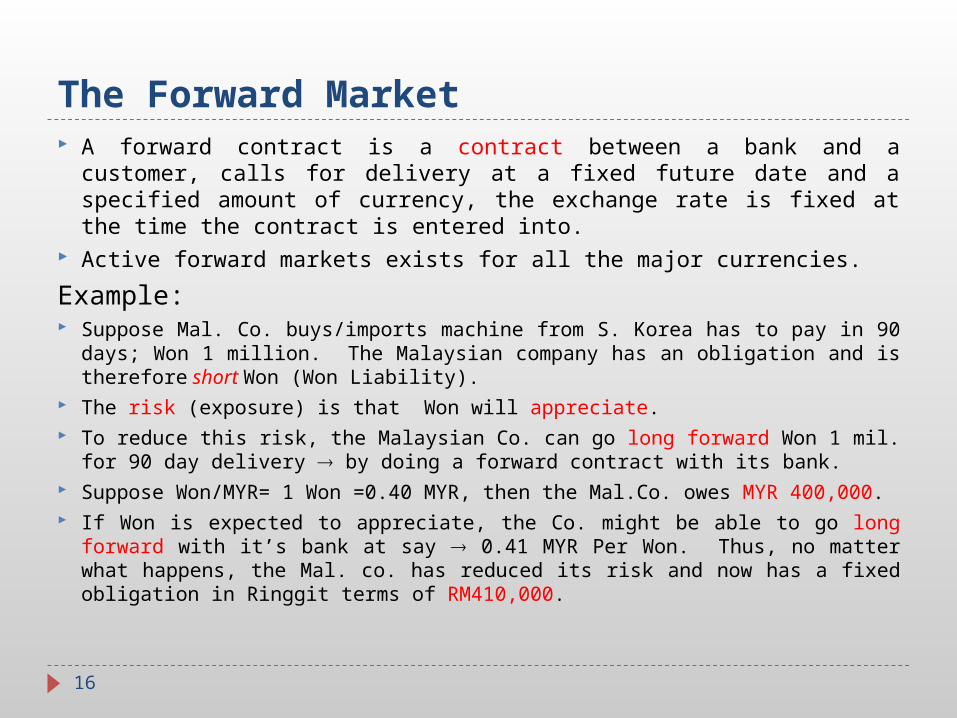

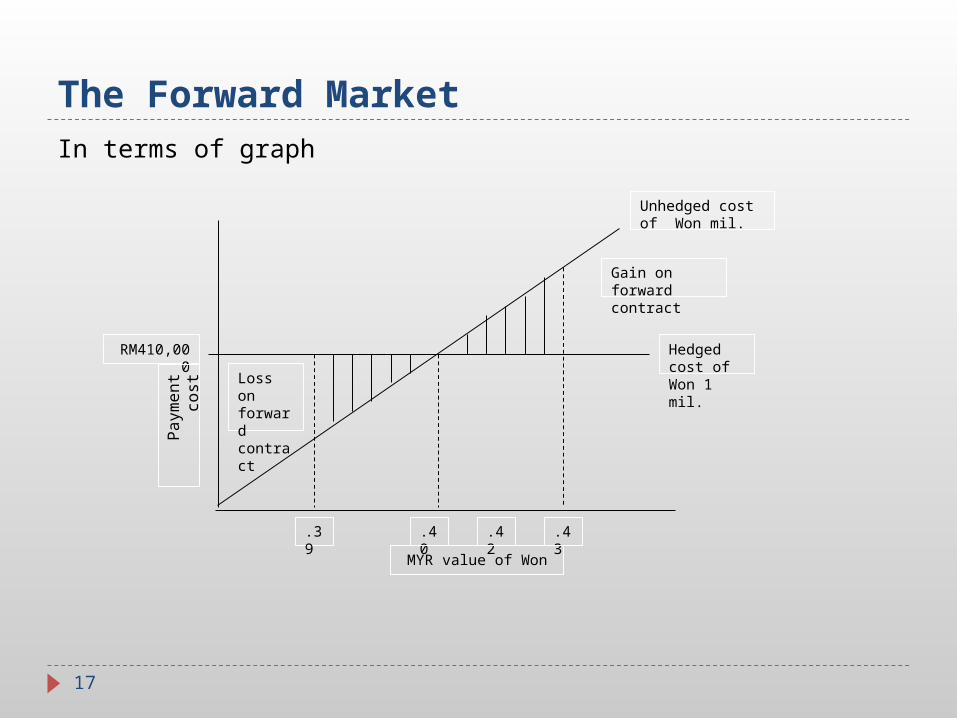

The Forward Market A forward contract is a contract between a bank and a customer,

calls for delivery at a fixed future date and a specified amount of currency, the exchange rate is fixed at the time the contract is entered into.

Active forward markets exists for all the major currencies.

Example: Suppose Mal. Co. buys/imports machine from S. Korea has to pay in 90

days; Won 1 million. The Malaysian company has an obligation and is therefore short Won (Won Liability).

The risk (exposure) is that Won will appreciate. To reduce this risk, the Malaysian Co. can go long forward Won 1 mil. for

90 day delivery by doing a forward contract with its bank. Suppose Won/MYR= 1 Won =0.40 MYR, then the Mal.Co. owes MYR

400,000. If Won is expected to appreciate, the Co. might be able to go long forward

with it’s bank at say 0.41 MYR Per Won. Thus, no matter what happens, the Mal. co. has reduced its risk and now has a fixed obligation in Ringgit terms of RM410,000.

16

The Forward MarketIn terms of graph

17

RM410,000

Pay

men

t cos

t Loss on forward contract

Unhedged cost of Won mil.

Gain on forward contract

Hedged cost of Won 1 mil.

.39 .40 .43.42

MYR value of Won

Forward Market Participants Arbitrageurs seek to earn risk-free by taking

advantage differences in interest rates among countries (HOT MONEY) they use forward contracts to hedge their exposure.

Traders : to cover exposures due to their import or export transactions.

Hedgers : Mostly MNCs hedge to protect the home currency value of various foreign currency-denominated assets and liabilities on their balance sheets

Speculators : unlike hedgers they have no underlying position, but simply go long or short forward to from the forward gains that could accrue.

18

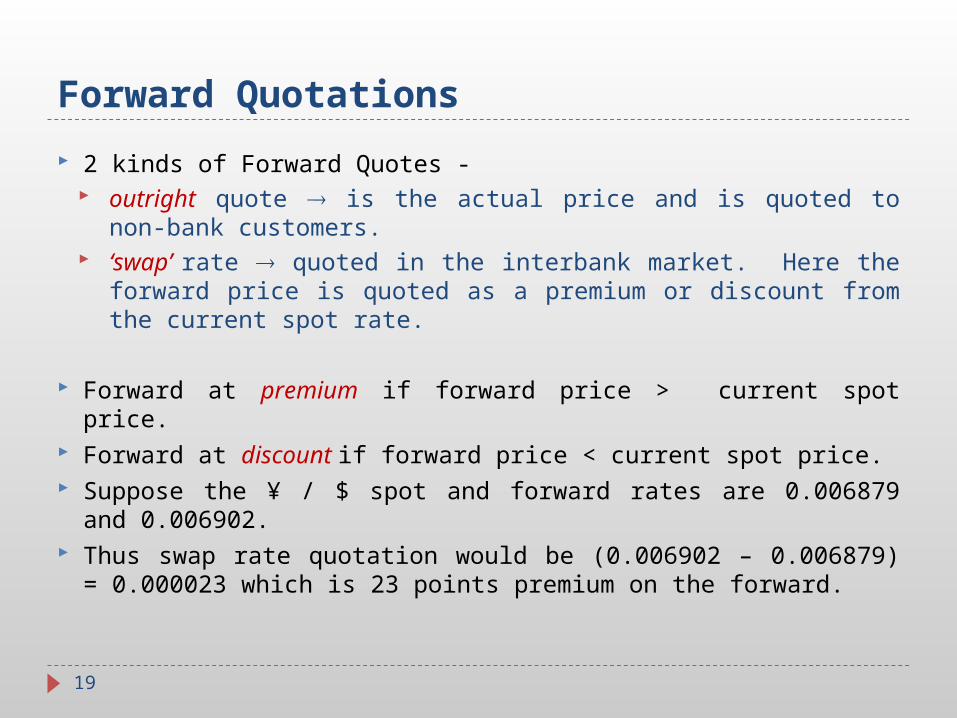

Forward Quotations

2 kinds of Forward Quotes - outright quote is the actual price and is quoted to non-

bank customers. ‘swap’ rate quoted in the interbank market. Here the

forward price is quoted as a premium or discount from the current spot rate.

Forward at premium if forward price > current spot price. Forward at discount if forward price < current spot price. Suppose the ¥ / $ spot and forward rates are 0.006879 and

0.006902. Thus swap rate quotation would be (0.006902 – 0.006879) =

0.000023 which is 23 points premium on the forward.

19

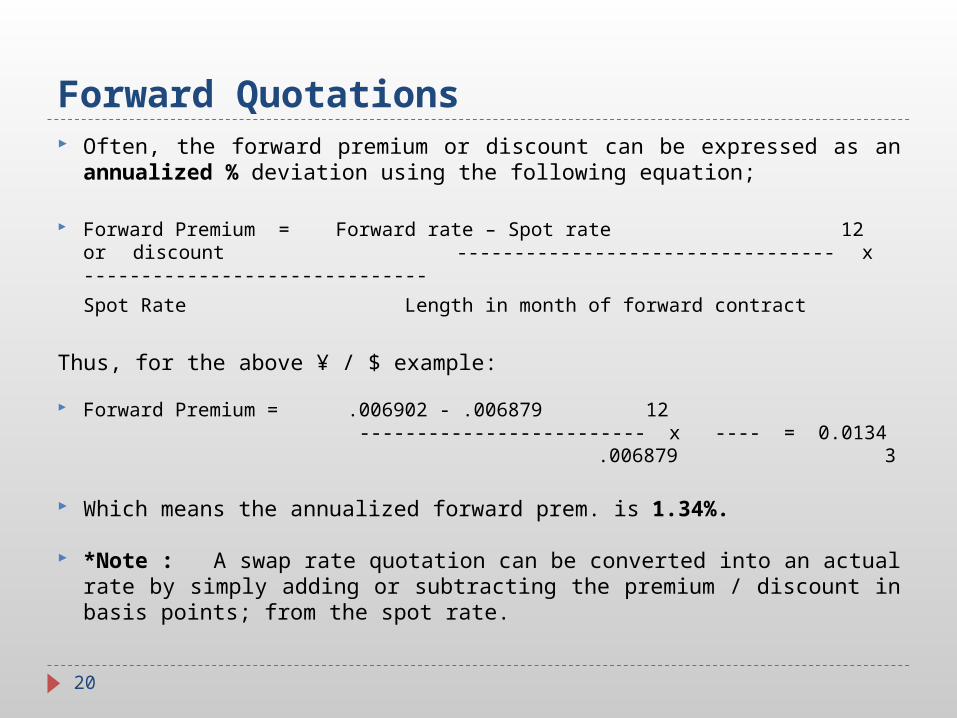

Forward Quotations Often, the forward premium or discount can be expressed as an

annualized % deviation using the following equation;

Forward Premium = Forward rate – Spot rate 12or discount --------------------------------- x ------------------------------

Spot Rate Length in month of forward contract

Thus, for the above ¥ / $ example:

Forward Premium = .006902 - .006879 12 ------------------------- x ---- = 0.0134

.006879 3 Which means the annualized forward prem. is 1.34%.

*Note : A swap rate quotation can be converted into an actual rate by simply adding or subtracting the premium / discount in basis points; from the spot rate.

20

Forward Quotations

Also note : The bid – ask spread increases for longer maturity forward. This is logical since, further time to there’s more

uncertainty.

Maturity Market for longer term forward would be much

thinner, therefore more risk for dealer.

21

Forward Contract Maturities

Normally available for 1, 2, 3, 6 & 12 month delivery. But 1, 3 and 6 months most popular.

Generally, there is no margin for forward transactions, however, if a bank is

(a) worried about the credit – worthiness of the counter party and;

(b) if the bank suspects that currency speculation may be involved, then banks might require the posting of margin % could depend on the situation.

22

Takeaway Messages Interbank market: wholesale mkt for major

banks Spot market represents 33% of the forex mkt Forward market constitutes 12% Swap transactions (package of spot &

forward contracts) form 55% ‘Ask’ price > ‘bid’ price: % spread = (a-b/a) x

100 Currency arbitrage takes advantage of

‘mispricing’ of currencies in different markets, resulting in price equalization

Forward contract protects against ER risk

23

Takeaway Messages Traders cover exposures arising from

export and import transactions Investors hedge to protect their foreign

assets/liabilities from forex risk Forward discount = Xt-Xo/Xo, where Xt <

Xo Forward premium = Xt-Xo/Xo, where Xt >

Xo Forward contracts, unlike options, are

legally binding commitments for both sellers & buyers

24

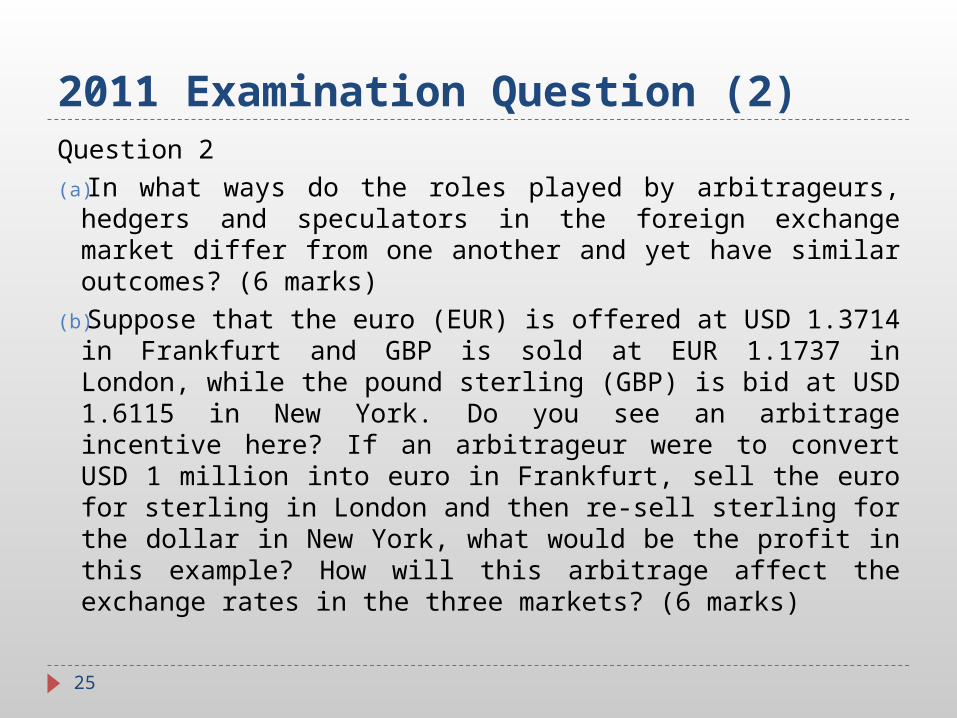

2011 Examination Question (2)Question 2(a)In what ways do the roles played by arbitrageurs,

hedgers and speculators in the foreign exchange market differ from one another and yet have similar outcomes? (6 marks)

(b)Suppose that the euro (EUR) is offered at USD 1.3714 in Frankfurt and GBP is sold at EUR 1.1737 in London, while the pound sterling (GBP) is bid at USD 1.6115 in New York. Do you see an arbitrage incentive here? If an arbitrageur were to convert USD 1 million into euro in Frankfurt, sell the euro for sterling in London and then re-sell sterling for the dollar in New York, what would be the profit in this example? How will this arbitrage affect the exchange rates in the three markets? (6 marks)

25

STAY BLESSED!

26

END OF LECTURE 4