Embed Size (px)

Citation preview

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Logistic regression

Quantitative Statistical MethodsDr. Szilágyi Roland

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Independent variable(x)

Qualitative Quantitative

De

pe

nd

en

t(y

)

Qu

alit

ativ

e

crosstabsDiscriminant-analysis,

Logistic regression

Qu

anti

t

ativ

e

ANOVACorrelation-, regression

analysis

Connection Analysis

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Logistic regression• The Logistic regression is a multivariate method

that helps to predict the classification of casesinto groups on the basis of independent variables.So those independent variables (x) are identifiedin the analysis, which cause significant differencein the dependent variables categories .

– binary (the dependent variable has two categories)

– Multinomial

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Logistic regression in practice

• Market research

• Modelling (by or no)

• Segmentation reliability

• Enterprise analysis (default, non default)

• etc.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Stages of Analysis

1• General Purpose

2• Assumptions

3• Estimaton of Function Coefficients

4• Interpretation of Results

5• Validity Tests

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

General purposes• To create logistic regresion function, which is the best

split of the categories of dependent variables as linear combination of independent variables.

• To determine whether there is a significant difference among groups according to independent variables.

• To determine which independent variables explain the most the differences among groups.

• Based on the experience obtained by a known classification, we can predict the group membership of new cases analyzing their independent variables.

• To measure the accuracy of classification

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

The Assumptions for Logistic regression1. Measure of variables

• The dependent variable should be categorized by m (at least 2) text values (e.g.: 1-good student, 2-bad student; or 1-prominent student, 2-average, 3-bad student).

• Independent variables could be measuredon whatever scale.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

The Assumptions for Logistic regression2. Independence

Not only the explanatory variables, but also all

cases must be independent. Therefore,

panel, longitudinal research, or pre-test data

cannot be used for logistic regression

analysis.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

The Assumptions for Logistic regression3. Sample size

It is a general rule, that the larger is the sample size, the more significant is the model. The ratio of number of data to the number of variables is also important. The results can be more generalized if we have at least 60 observations.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

The Assumptions for Logistic regression4. Multivariate normal distribution

In case of normal distribution, the estimation of parameters are easier, because the parameters can be defined according to the density or distribution function. It can be tested by histograms of frequency distributions or hypothesis testing.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

The Assumptions for Logistic regression5. Multicollinearity

Independent variables should be correlated to the dependent variable, however there must be no correlation between the independent variables, because it can bias the results of analysis.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Binary Logistic Regression• The logistic function is useful because it can take any

input linear combination of independent variables (Xi),

whereas the output always takes values between zero

and one and hence is interpretable as a probability. The

logistic function is defined as follows:

• Note that F(x) is interpreted as the probability of the

dependent variable equaling a "success" or "case" ratherthan a failure or non-case.

pp

pp

xx

xx

xe

eF

...

...

)(110

110

1

)1( XYP i

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Binary Logistic Regression

• We can now define the inverse of the logistic

function, the „logit” (log odds):

pp

x

xxx

F

FY ...

1ln 110

)(

)(

ppxx

x eodds

...110

after exponentiating

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Binary Logistic Regression

• „The odds of the dependent variable

equaling a case (given some linearcombination xi of the predictors) is

equivalent to the exponential function of

the linear regression expression

x

x

xP

Podds

1

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Binary Logistic Regression

pp

pp

xx

xx

xe

eP

...

...

110

110

1

x

x

xP

Podds

1

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Maximum Likelihood Method

• The maximum likelihood method finds a set of coefficients (β), called the maximum likelihood estimates, at which the log-likelihood function attains its local maximum:

Forrás: Hajdu Ottó: Többváltozós statisztikai számítások; KSH, Budapest, 2003.

max11

...

...

110

110

n

ixx

xx

pp

pp

e

eL

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Tests of Model Fit

The Binary Logistic Regression procedure reports the Hosmer-Lemeshow goodness-of-fit statistic. Ithelps you to determine whether the model adequately describes the dataHo: model fitsH1: model don’t fitThe Hosmer–Lemeshow test specifically identifies subgroups deciles of fitted risk values. Models for which expected and observed event rates in subgroups are similar (khi square) are called fitted (well calibrated).

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Testinf of parameters (β)

0:

0:

1

0

i

i

H

H

2

i

ii

)s(b

b=Wald

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Choosing the Right Model

• Based on residual sum of squares (linear regression)

• Based on Likelihood ratio (compare the Likelihood of the model with the Likelihood of a baseline (minimal) model)

• Proportion of good predictions.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Pseudo R2

• Cox and Snell's R2 is based on the log likelihood for the model compared to the log likelihood for a baseline model. However, with categorical outcomes, it has a theoretical maximum value of less than 1, even for a "perfect" model.

• Nagelkerke's R2 is an adjusted version of the Cox & Snell R-square that adjusts the scale of the statistic to cover the full range from 0 to 1.

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Example

• If you are a loan officer at a bank, then you want to be able to identify characteristics that are indicative of people who are likely to default on loans, and use those characteristics to identify good and bad credit risks. Variables

Age in years

Level of education

Years with current employer

Years at current address

Household income in thousands

Debt to income ratio (x100)

Credit card debt in thousands

Other debt in thousands

Previously defaulted

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Outputs

Classification Tablea,b

Observed

Predicted

Selected Casesc Unselected Casesd,e

Previously defaulted Percenta

ge Correct

Previously defaulted Percenta

ge CorrectNo Yes No Yes

Step 0Previouslydefaulted

No 375 0 100,0 142 0 100,0

Yes 124 0 ,0 59 0 ,0

Overall Percentage 75,2 70,6

a. Constant is included in the model.

b. The cut value is ,500

Source: Help- IBM SPSS Statistics

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Hosmer and Lemeshow TestStep Chi-square df Sig.1 3,292 8 ,9152 11,866 8 ,1573 9,447 8 ,3064 4,027 8 ,855

Source: Help- IBM SPSS Statistics

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Model Summary

Step-2 Log

likelihoodCox & Snell R

SquareNagelkerke R

Square1 498,012a ,116 ,172

2 447,301b ,201 ,299

3 411,553b ,257 ,381

4 394,721c ,281 ,417

Source : Help- IBM SPSS Statistics

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Classification Tablea

Observed

Predicted

Selected Casesb Unselected Casesc,d

Previously defaultedPercentage

Correct

Previously defaultedPercentage

CorrectNo Yes No Yes

Step 1

Previouslydefaulted

No 361 14 96,3 137 5 96,5Yes 100 24 19,4 45 14 23,7

Overall Percentage 77,2 75,1

Step 2

Previously defaulted

No 351 24 93,6 136 6 95,8Yes 80 44 35,5 36 23 39,0

Overall Percentage 79,2 79,1

Step 3

Previously defaulted

No 348 27 92,8 135 7 95,1Yes 72 52 41,9 28 31 52,5

Overall Percentage 80,2 82,6

Step 4

Previously defaulted

No 352 23 93,9 130 12 91,5Yes 67 57 46,0 27 32 54,2

Overall Percentage 82,0 80,6

a. The cut value is ,500

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Classification table (Confusion matrix)

(predicted)

no (0) yes (1)

(observed)

no (0) true negative (TN)False positive (FP)

Type I

→specificity

TN/(TN+FP)

yes (1)False negative (FN)

Type IITrue positive (TP)

→ sensitivity

TP/(FN+TP)

↓

negative predictive

value

TN/(TN+FN)

↓

positive predictive

value (precision)

TP/(FP+TP)

accuracy

(TP+TN)/

(TN+FP+FN+TP)

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Variables in the Equation

B S.E. Wald df Sig. Exp(B)95% C.I.for EXP(B)Lower Upper

Step 1a Debt to income ratio (x100) ,121 ,017 52,676 1 ,000 1,129 1,092 1,166

Constant -2,476 ,230 116,315

1 ,000 ,084

Step 2b Years with current employer -,140 ,023 38,158 1 ,000 ,869 ,831 ,909

Debt to income ratio (x100) ,134 ,018 54,659 1 ,000 1,143 1,103 1,185

Constant -1,621 ,259 39,038 1 ,000 ,198

Step 3c Years with current employer -,244 ,033 54,676 1 ,000 ,783 ,734 ,836

Debt to income ratio (x100) ,069 ,022 9,809 1 ,002 1,072 1,026 1,119

Credit card debt in thousands ,506 ,101 25,127 1 ,000 1,658 1,361 2,021

Constant -1,058 ,280 14,249 1 ,000 ,347

Step 4d Years with current employer -,247 ,034 51,826 1 ,000 ,781 ,731 ,836

Years at current address -,089 ,023 15,109 1 ,000 ,915 ,875 ,957

Debt to income ratio (x100) ,072 ,023 10,040 1 ,002 1,074 1,028 1,123

Credit card debt in thousands ,602 ,111 29,606 1 ,000 1,826 1,470 2,269

Constant -,605 ,301 4,034 1 ,045 ,546

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Meaning of coefficients

• The meaning of a logistic regression coefficient is not as straightforward as that of a linear regression coefficient. While B is convenient for testing the usefulness of predictors, Exp(B) is easier to interpret. Exp(B) represents the ratio-change in the odds of the event of interest for a one-unit change in the predictor (Xi ) CeterisParibus (all other things being equal).

Source : Help- IBM SPSS Statistics

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

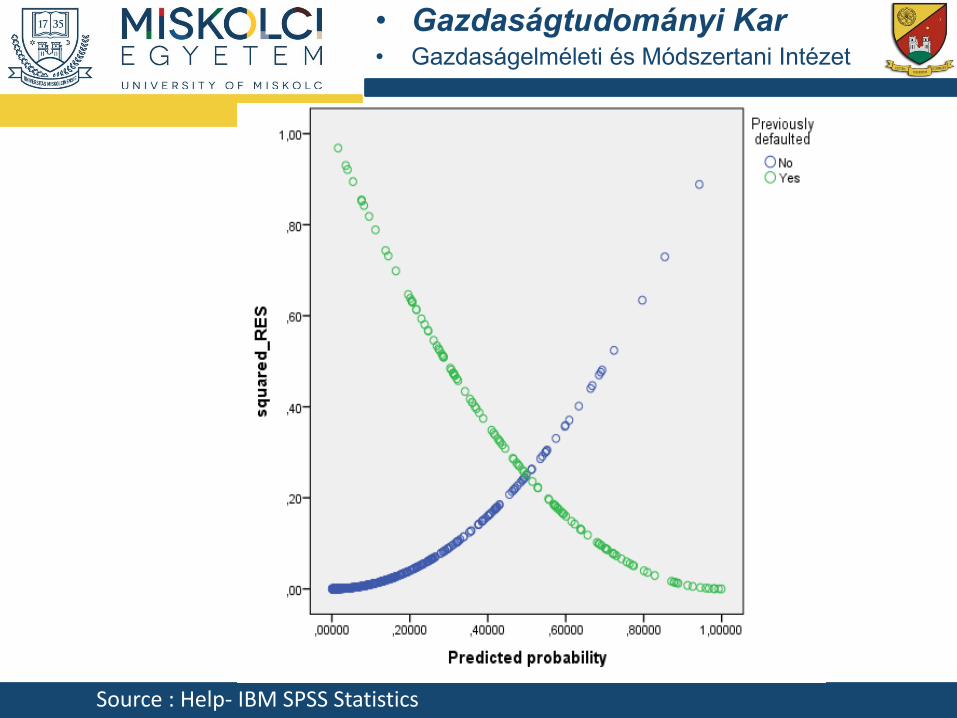

Source : Help- IBM SPSS Statistics

• Gazdaságtudományi Kar• Gazdaságelméleti és Módszertani Intézet

Thank you for your attention!

email: [email protected]

![The Logistic Function - mygeodesy.id.au Logistic Function.pdf · courbe logistique [the logistic curve]. The properties of the logistic curve are derived and a general equation developed](https://img.pdfslide.net/doc/110x75/5b95cda609d3f2c2678cb9ab/the-logistic-function-logistic-functionpdf-courbe-logistique-the-logistic.jpg)