Embed Size (px)

Citation preview

Macquarie Life

Calculating levels of insurance cover

Lauren StylesBusiness Development Manager

This activity has been accredited for continuing professional development points by the Financial Planning Association of Australia but does not constitute FPA’s endorsement of the activity.

Accreditation number 005725 for 1 point.

Disclaimer

Macquarie Life Limited (MLL) ABN 56 003 963 773 AFSL 237 497 and Macquarie Investment Management Limited (MIML) ABN 66 002 867 003 are not authorised deposit-taking institutions for the purposes of the Banking Act 1959 (Cth) and MLL and MIML’s obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542. Macquarie Bank Limited does not guarantee or otherwise provide assurance in respect of the obligations of MLL.

This information is provided as a guide for licensed financial advisers only. Financial advisers are prohibited from passing on this information to any retail client. In no circumstances is it to be used by a potential client for the purposes of making a decision about a financial product or class of products.

This presentation and the case studies are not based on any particular client or their specific needs, any similarities are purely coincidental. Financial Advisers must take into account each individual client’s specific situation, needs and circumstances when recommending levels and types of Insurance.

Agenda

Calculation methods

Disability income / business expenses

Death

TPD

Trauma

Severity based cover

Tailoring your message

3

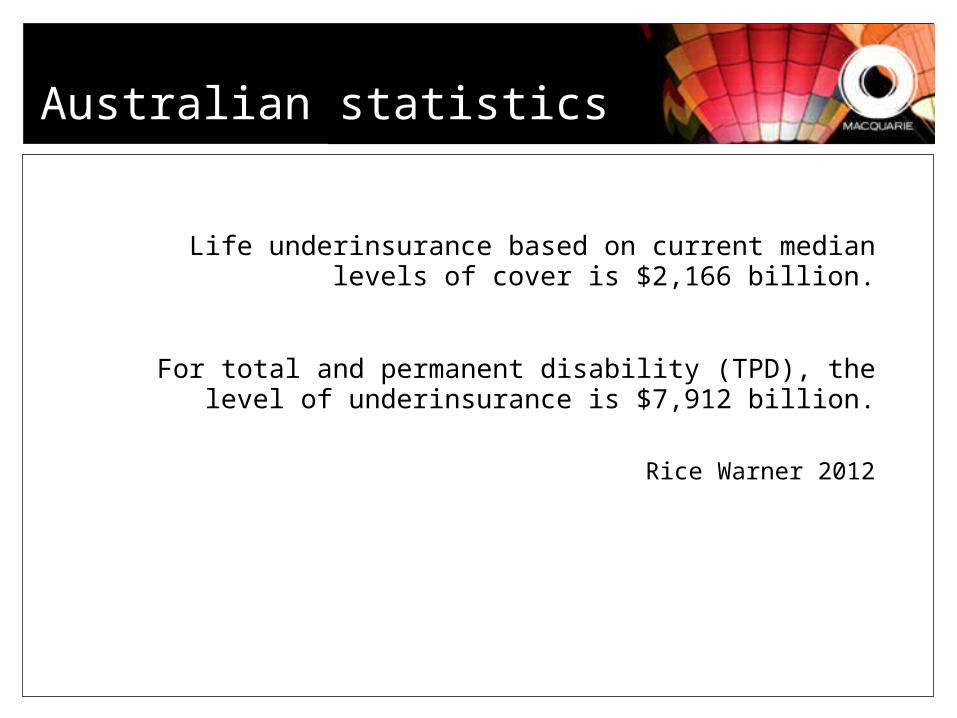

Life underinsurance based on current median levels of cover is $2,166 billion.

For total and permanent disability (TPD), the level of underinsurance is $7,912 billion.

Rice Warner 2012

4

Australian statistics

Australian statistics

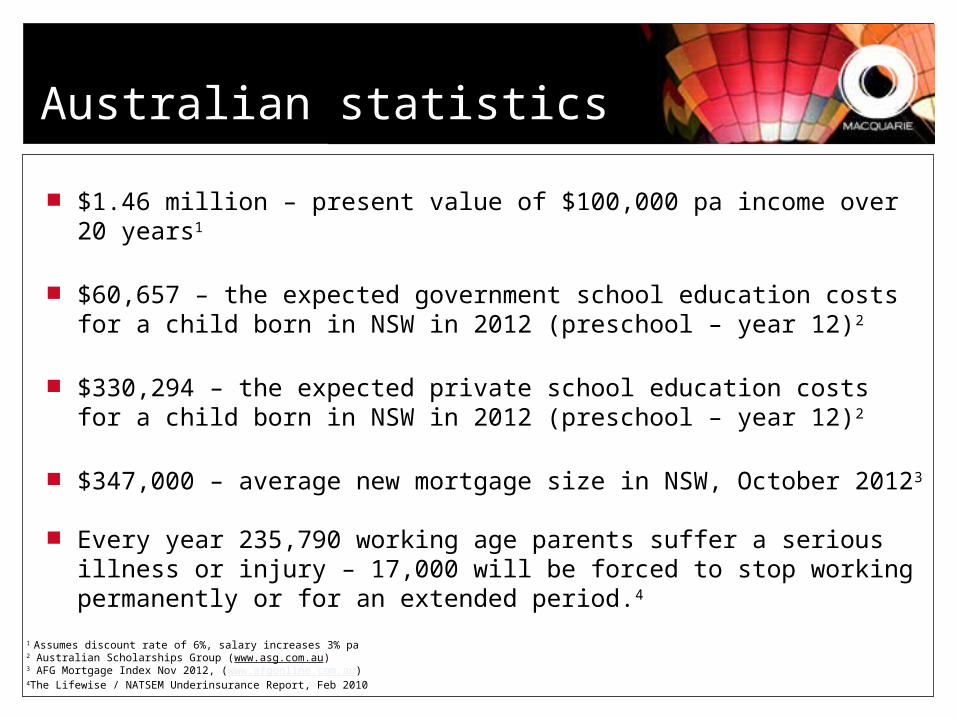

$1.46 million – present value of $100,000 pa income over 20 years1

$60,657 – the expected government school education costs for a child born in NSW in 2012 (preschool – year 12)2

$330,294 – the expected private school education costs for a child born in NSW in 2012 (preschool – year 12)2

$347,000 – average new mortgage size in NSW, October 20123

Every year 235,790 working age parents suffer a serious illness or injury – 17,000 will be forced to stop working permanently or for an extended period.4

1 Assumes discount rate of 6%, salary increases 3% pa 2 Australian Scholarships Group (www.asg.com.au)3 AFG Mortgage Index Nov 2012, (www.afgonline.com.au)4The Lifewise / NATSEM Underinsurance Report, Feb 2010

The effects of underinsurance

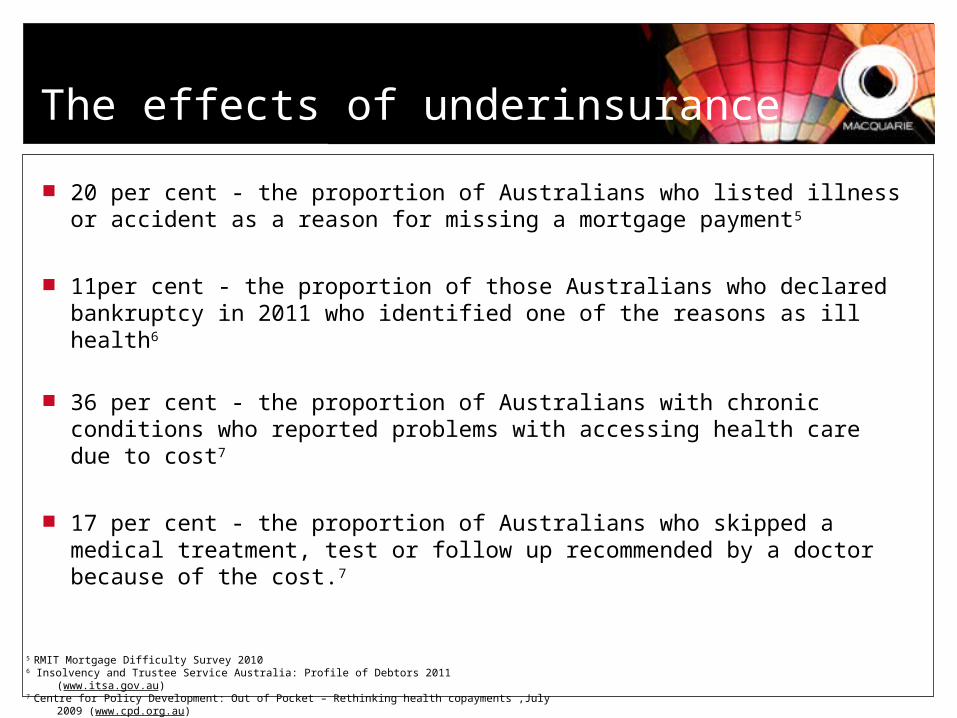

20 per cent - the proportion of Australians who listed illness or accident as a reason for missing a mortgage payment5

11per cent - the proportion of those Australians who declared bankruptcy in 2011 who identified one of the reasons as ill health6

36 per cent - the proportion of Australians with chronic conditions who reported problems with accessing health care due to cost7

17 per cent - the proportion of Australians who skipped a medical treatment, test or follow up recommended by a doctor because of the cost.7

5 RMIT Mortgage Difficulty Survey 20106 Insolvency and Trustee Service Australia: Profile of Debtors 2011 (www.itsa.gov.au)7 Centre for Policy Development: Out of Pocket – Rethinking health copayments ,July 2009 (www.cpd.org.au)

How much is enough?

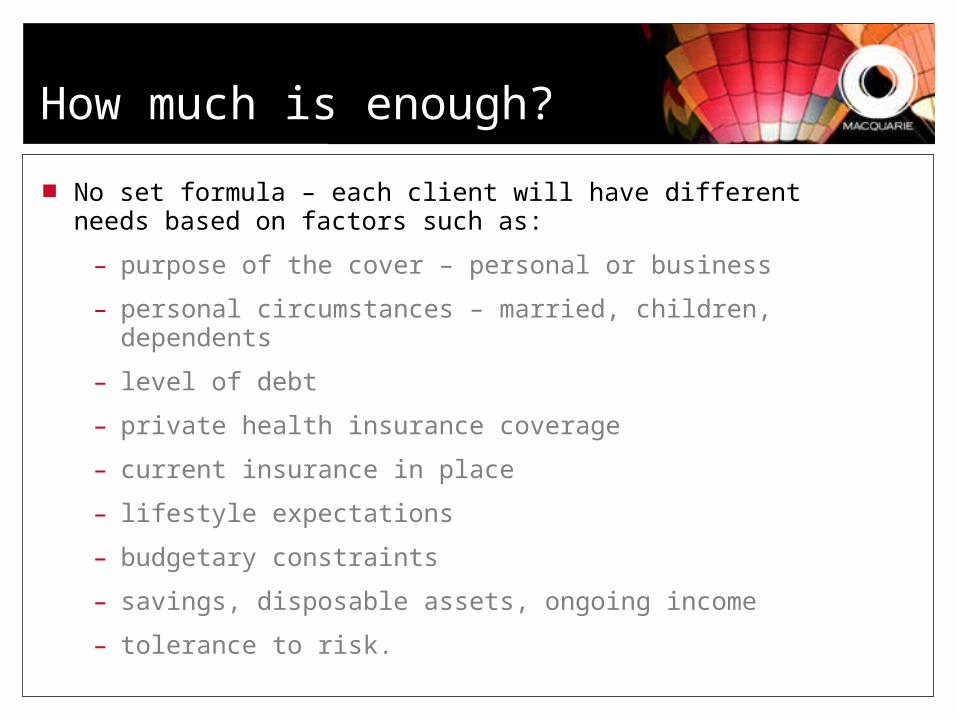

No set formula – each client will have different needs based on factors such as:

– purpose of the cover – personal or business

– personal circumstances – married, children, dependents

– level of debt

– private health insurance coverage

– current insurance in place

– lifestyle expectations

– budgetary constraints

– savings, disposable assets, ongoing income

– tolerance to risk.

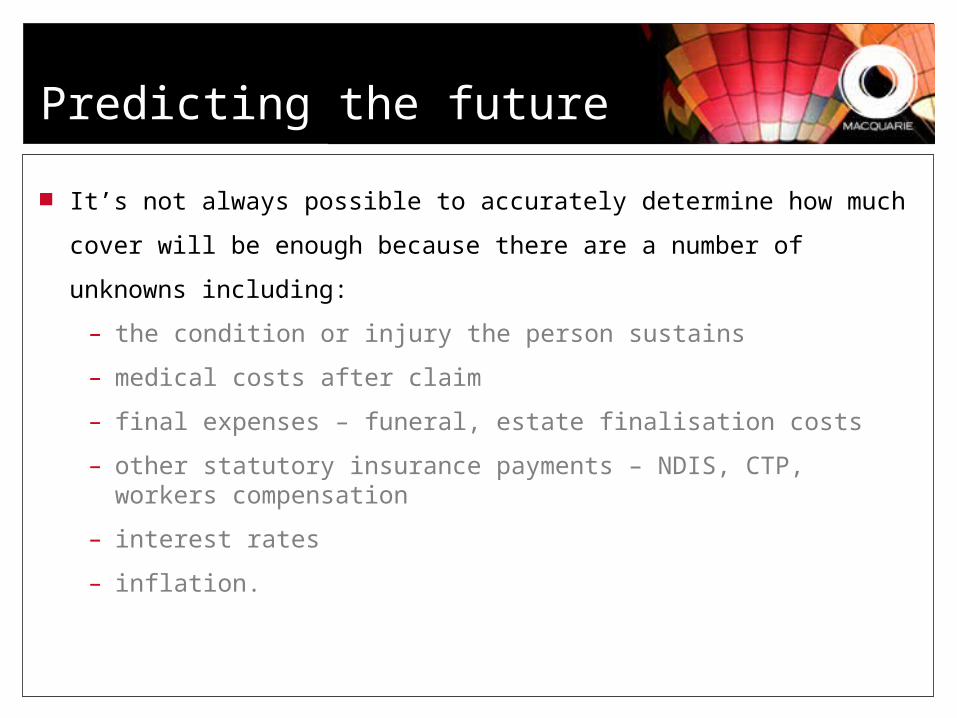

Predicting the future

It’s not always possible to accurately determine how much

cover will be enough because there are a number of unknowns

including:

– the condition or injury the person sustains

– medical costs after claim

– final expenses – funeral, estate finalisation costs

– other statutory insurance payments – NDIS, CTP, workers compensation

– interest rates

– inflation.

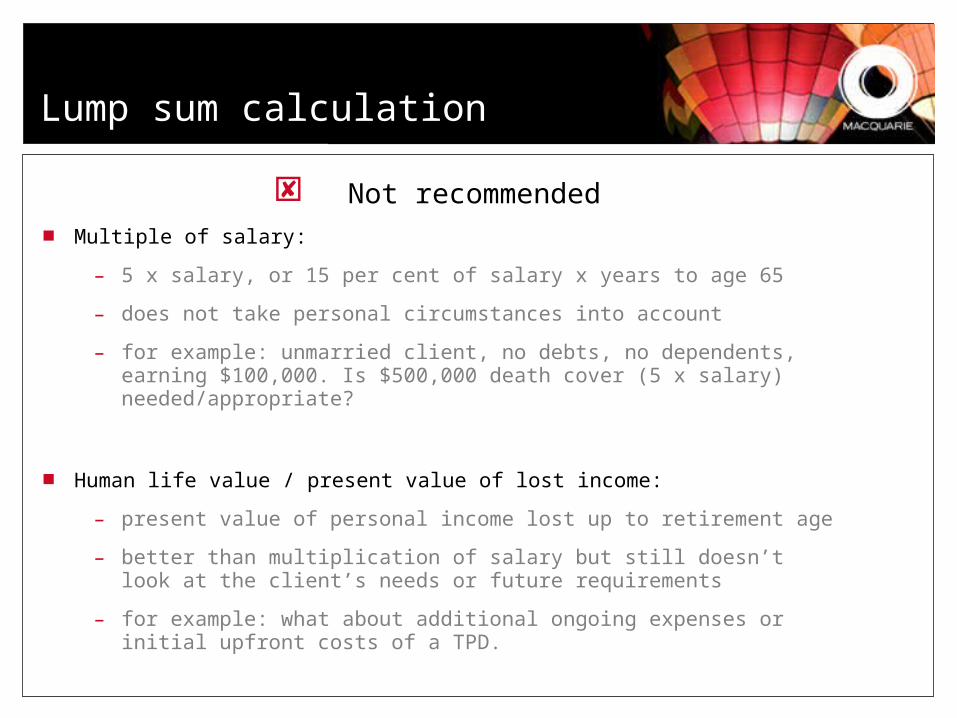

Lump sum calculation

Not recommended Multiple of salary:

– 5 x salary, or 15 per cent of salary x years to age 65

– does not take personal circumstances into account

– for example: unmarried client, no debts, no dependents, earning $100,000. Is $500,000 death cover (5 x salary) needed/appropriate?

Human life value / present value of lost income:

– present value of personal income lost up to retirement age

– better than multiplication of salary but still doesn’t look at the client’s needs or future requirements

– for example: what about additional ongoing expenses or initial upfront costs of a TPD.

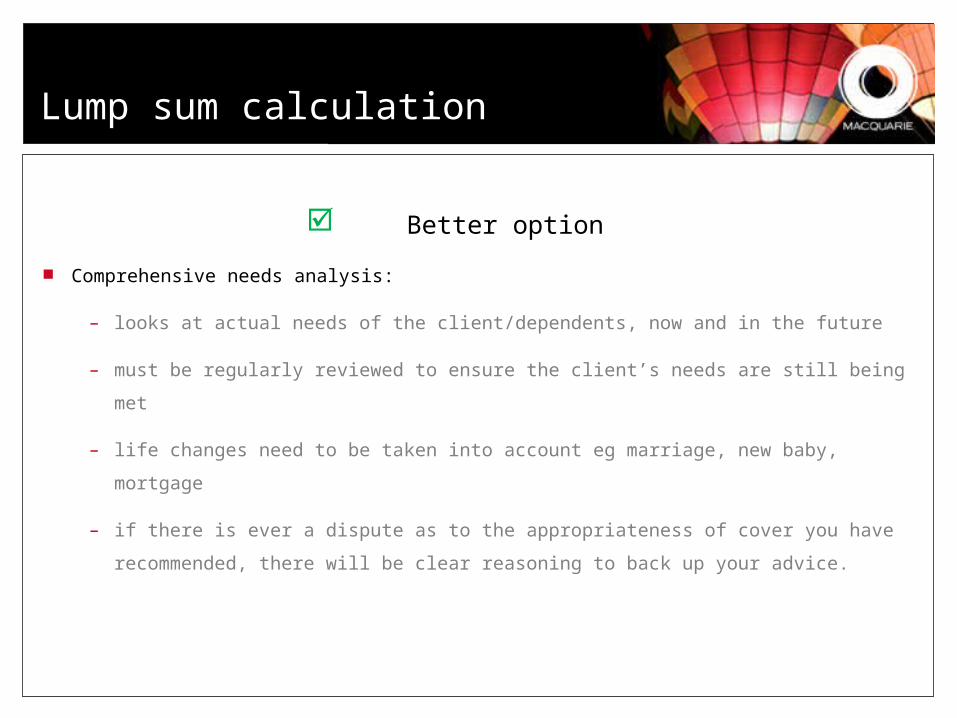

Lump sum calculation

Better option

Comprehensive needs analysis:

– looks at actual needs of the client/dependents, now and in the future

– must be regularly reviewed to ensure the client’s needs are still being met

– life changes need to be taken into account eg marriage, new baby,

mortgage

– if there is ever a dispute as to the appropriateness of cover you have

recommended, there will be clear reasoning to back up your advice.

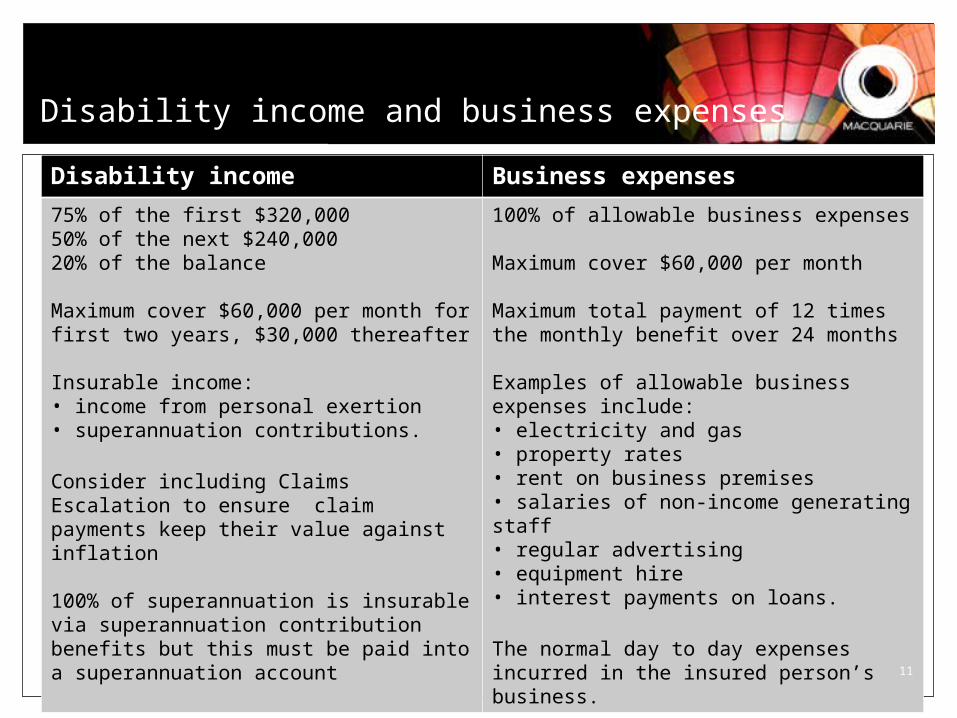

Disability income and business expenses

Disability income Business expenses

75% of the first $320,00050% of the next $240,00020% of the balance

Maximum cover $60,000 per month for first two years, $30,000 thereafter

Insurable income:• income from personal exertion • superannuation contributions.

Consider including Claims Escalation to ensure claim payments keep their value against inflation

100% of superannuation is insurable via superannuation contribution benefits but this must be paid into a superannuation account

100% of allowable business expenses

Maximum cover $60,000 per month

Maximum total payment of 12 times the monthly benefit over 24 months

Examples of allowable business expenses include:• electricity and gas• property rates• rent on business premises• salaries of non-income generating staff• regular advertising• equipment hire• interest payments on loans.

The normal day to day expenses incurred in the insured person’s business.

11

Death cover

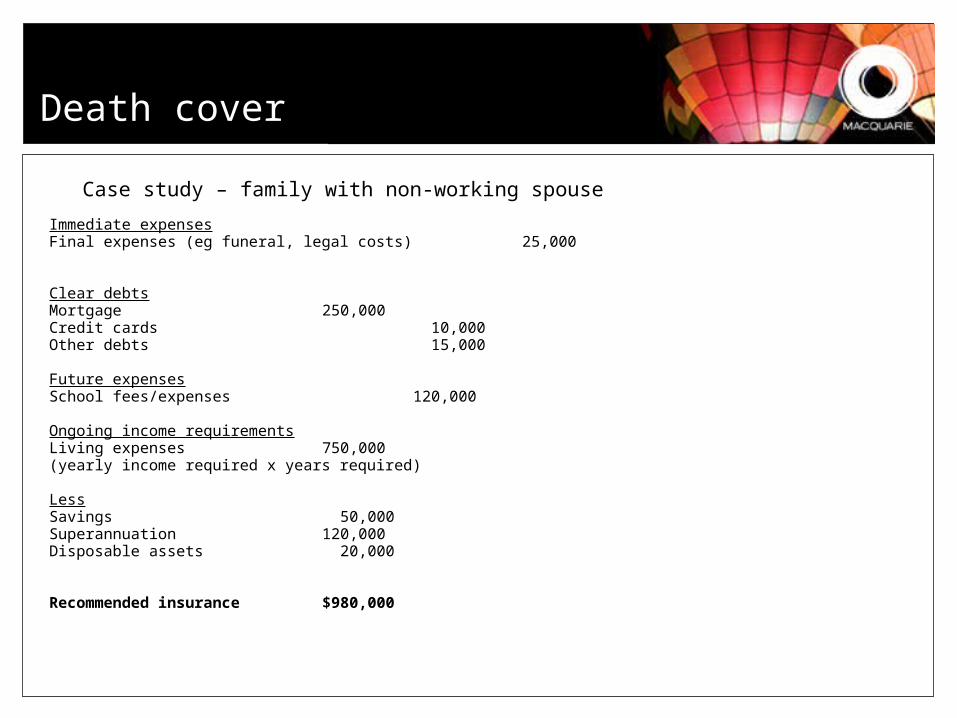

Case study – family with non-working spouse

Immediate expensesFinal expenses (eg funeral, legal costs) 25,000

Clear debtsMortgage 250,000Credit cards 10,000Other debts 15,000

Future expensesSchool fees/expenses 120,000

Ongoing income requirementsLiving expenses 750,000(yearly income required x years required)

LessSavings 50,000Superannuation 120,000Disposable assets 20,000

Recommended insurance $980,000

TPD insurance

13

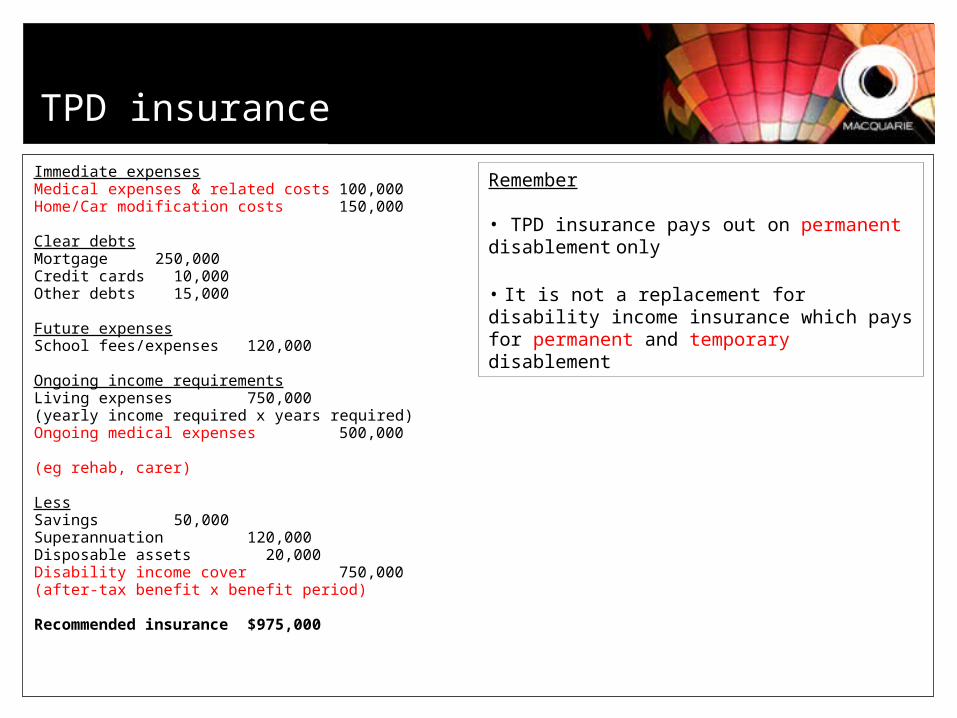

Immediate expensesMedical expenses & related costs 100,000Home/Car modification costs 150,000

Clear debtsMortgage 250,000Credit cards 10,000Other debts 15,000

Future expensesSchool fees/expenses 120,000

Ongoing income requirementsLiving expenses 750,000(yearly income required x years required)Ongoing medical expenses 500,000 (eg rehab, carer)

LessSavings 50,000Superannuation 120,000Disposable assets 20,000Disability income cover 750,000(after-tax benefit x benefit period)

Recommended insurance$975,000

Remember

• TPD insurance pays out on permanent disablement only

• It is not a replacement for disability income insurance which pays for permanent and temporary disablement

Trauma insurance

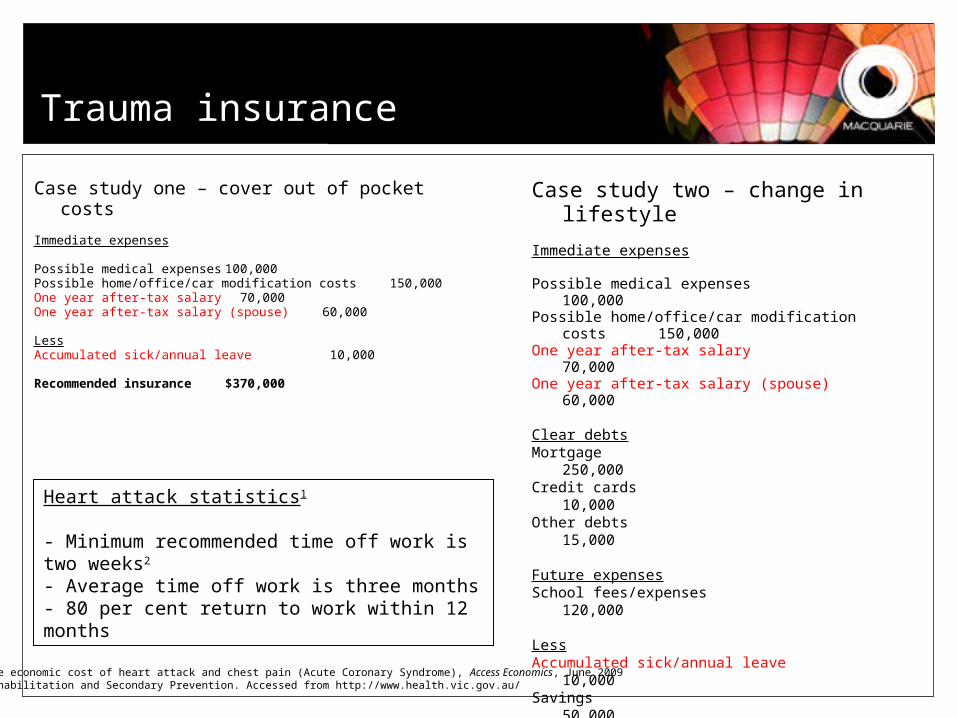

Case study one – cover out of pocket costs

Immediate expenses

Possible medical expenses 100,000Possible home/office/car modification costs150,000One year after-tax salary 70,000One year after-tax salary (spouse) 60,000

LessAccumulated sick/annual leave 10,000

Recommended insurance $370,000

Case study two – change in lifestyle

Immediate expenses

Possible medical expenses100,000

Possible home/office/car modification costs150,000

One year after-tax salary 70,000

One year after-tax salary (spouse) 60,000

Clear debtsMortgage

250,000Credit cards

10,000Other debts

15,000

Future expensesSchool fees/expenses

120,000

LessAccumulated sick/annual leave

10,000Savings

50,000Disposable assets

20,000

Recommended insurance$695,000

Heart attack statistics1

- Minimum recommended time off work is two weeks2

- Average time off work is three months- 80 per cent return to work within 12 months

1The economic cost of heart attack and chest pain (Acute Coronary Syndrome), Access Economics, June 20092Rehabilitation and Secondary Prevention. Accessed from http://www.health.vic.gov.au/

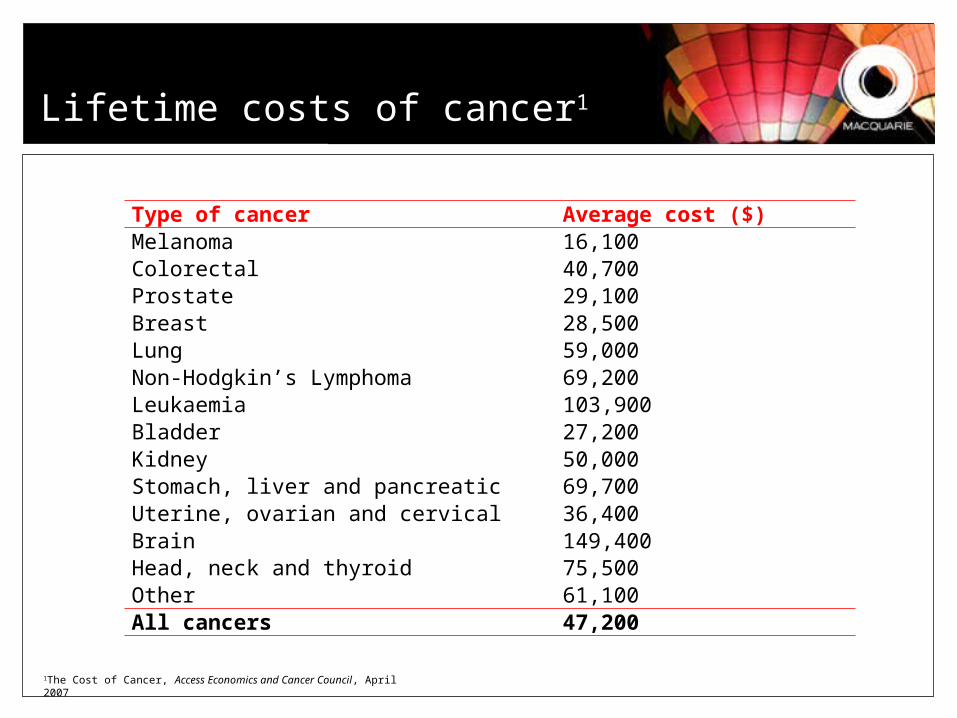

Lifetime costs of cancer1

15

Type of cancer Average cost ($)Melanoma 16,100Colorectal 40,700Prostate 29,100Breast 28,500Lung 59,000Non-Hodgkin’s Lymphoma 69,200Leukaemia 103,900Bladder 27,200Kidney 50,000Stomach, liver and pancreatic 69,700Uterine, ovarian and cervical 36,400Brain 149,400Head, neck and thyroid 75,500Other 61,100All cancers 47,200

1The Cost of Cancer, Access Economics and Cancer Council, April 2007

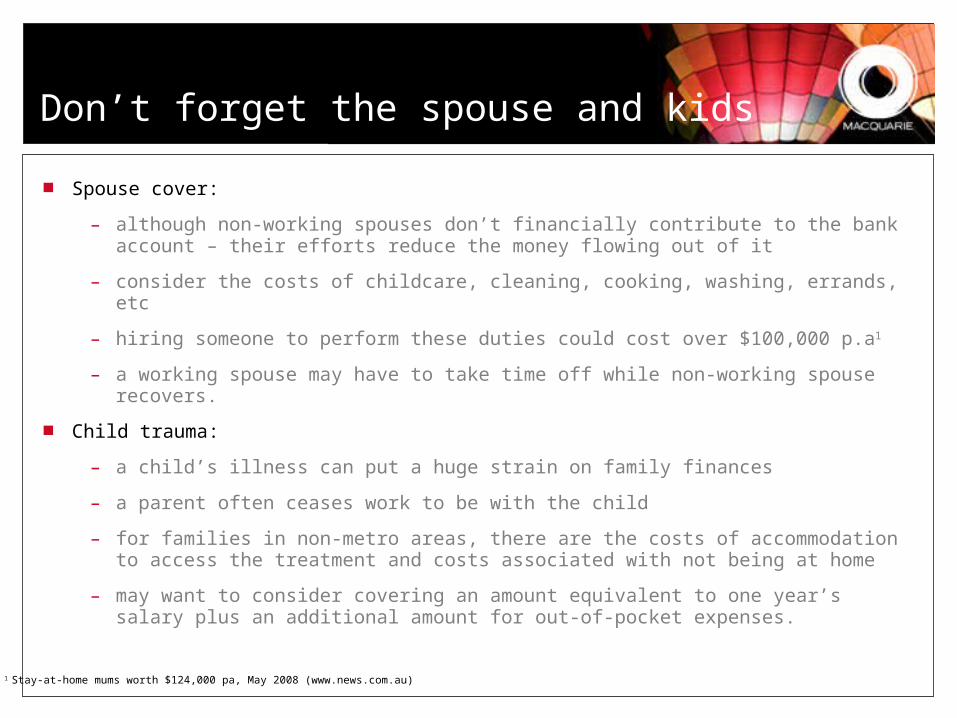

Don’t forget the spouse and kids

Spouse cover:

– although non-working spouses don’t financially contribute to the bank account – their efforts reduce the money flowing out of it

– consider the costs of childcare, cleaning, cooking, washing, errands, etc

– hiring someone to perform these duties could cost over $100,000 p.a1

– a working spouse may have to take time off while non-working spouse recovers.

Child trauma:

– a child’s illness can put a huge strain on family finances

– a parent often ceases work to be with the child

– for families in non-metro areas, there are the costs of accommodation to access the treatment and costs associated with not being at home

– may want to consider covering an amount equivalent to one year’s salary plus an additional amount for out-of-pocket expenses.

1 Stay-at-home mums worth $124,000 pa, May 2008 (www.news.com.au)

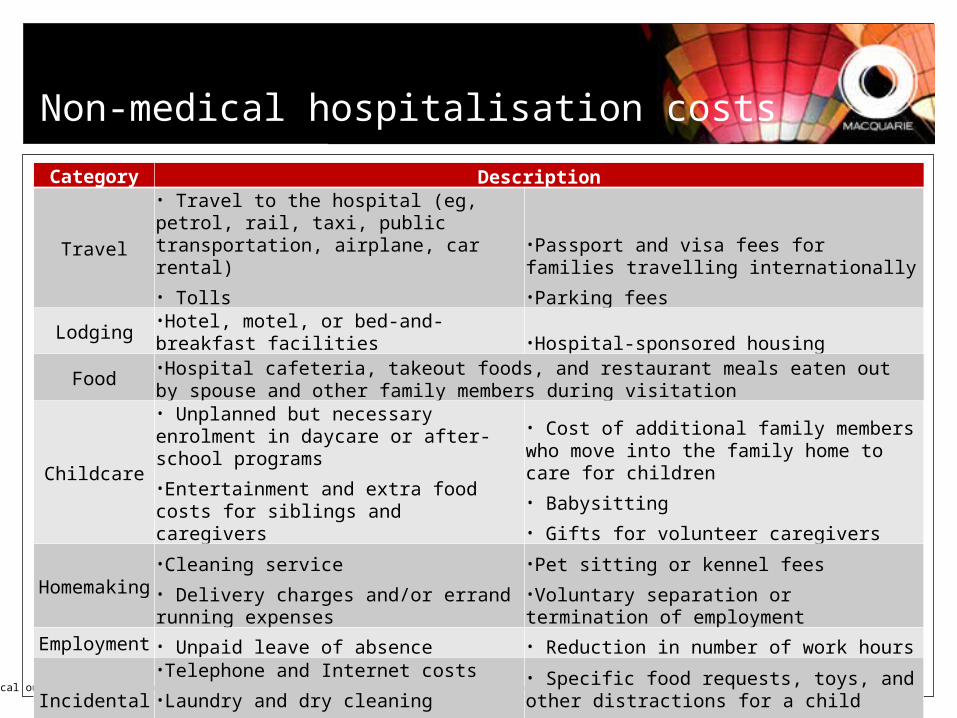

Non-medical hospitalisation costs

Nonmedical out-of-pocket expenses: A hidden cost of hospitalization, Journal of paediatric nursing 2011

Category Description

Travel

• Travel to the hospital (eg, petrol, rail, taxi, public transportation, airplane, car rental)

• Tolls

•Passport and visa fees for families travelling internationally

•Parking fees

Lodging•Hotel, motel, or bed-and-breakfast facilities •Hospital-sponsored housing

Food•Hospital cafeteria, takeout foods, and restaurant meals eaten out by spouse and other family members during visitation

Childcare• Unplanned but necessary enrolment in daycare or after-school programs

•Entertainment and extra food costs for siblings and caregivers

• Cost of additional family members who move into the family home to care for children

• Babysitting

• Gifts for volunteer caregivers

Homemaking

•Cleaning service

• Delivery charges and/or errand running expenses

•Pet sitting or kennel fees

•Voluntary separation or termination of employment

Employment • Unpaid leave of absence • Reduction in number of work hours

Incidental expenses

•Telephone and Internet costs

•Laundry and dry cleaning

•Toiletries, over-the-counter medications

• Specific food requests, toys, and other distractions for a child

• Clothing needed to be purchased because of unexpected admission

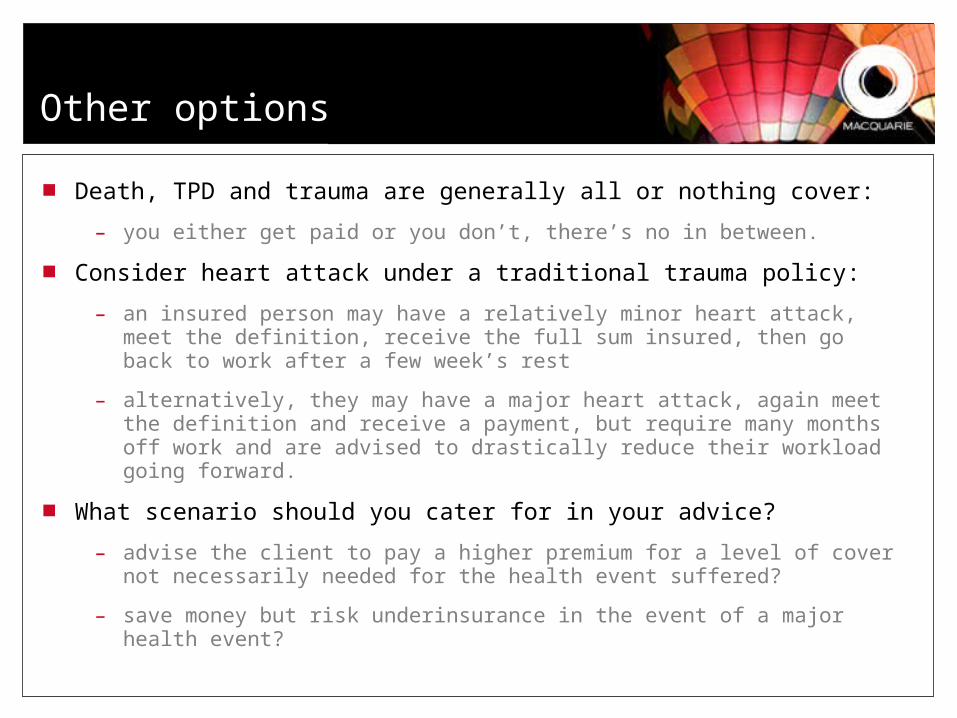

Other options

Death, TPD and trauma are generally all or nothing cover:

– you either get paid or you don’t, there’s no in between.

Consider heart attack under a traditional trauma policy:

– an insured person may have a relatively minor heart attack, meet the definition, receive the full sum insured, then go back to work after a few week’s rest

– alternatively, they may have a major heart attack, again meet the definition and receive a payment, but require many months off work and are advised to drastically reduce their workload going forward.

What scenario should you cater for in your advice?

– advise the client to pay a higher premium for a level of cover not necessarily needed for the health event suffered?

– save money but risk underinsurance in the event of a major health event?

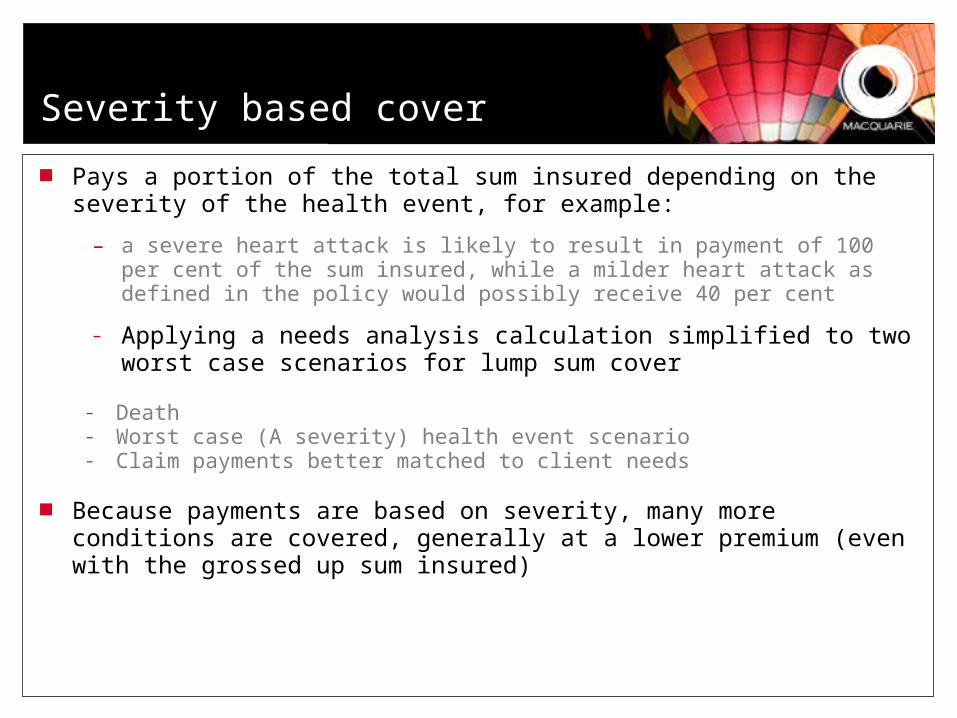

Severity based cover

Pays a portion of the total sum insured depending on the severity of the health event, for example:

– a severe heart attack is likely to result in payment of 100 per cent of the sum insured, while a milder heart attack as defined in the policy would possibly receive 40 per cent

– Applying a needs analysis calculation simplified to two worst case scenarios for lump sum cover

– Death– Worst case (A severity) health event scenario– Claim payments better matched to client needs

Because payments are based on severity, many more conditions are covered, generally at a lower premium (even with the grossed up sum insured)

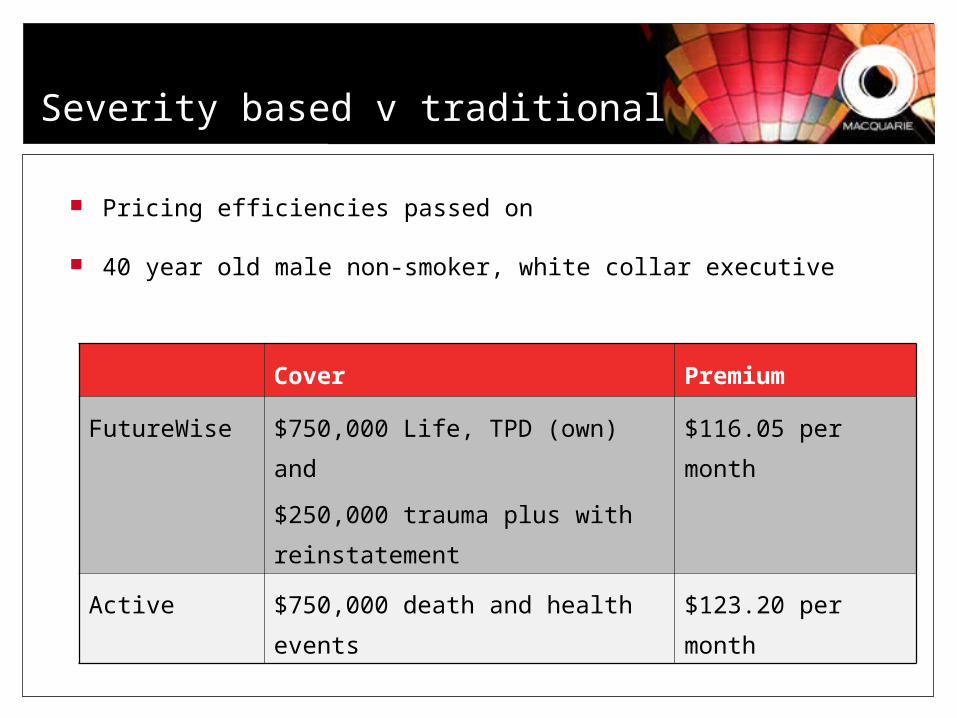

Severity based v traditional

20

Cover Premium

FutureWise $750,000 Life, TPD (own) and

$250,000 trauma plus with

reinstatement

$116.05 per month

Active $750,000 death and health events $123.20 per month

Pricing efficiencies passed on

40 year old male non-smoker, white collar executive

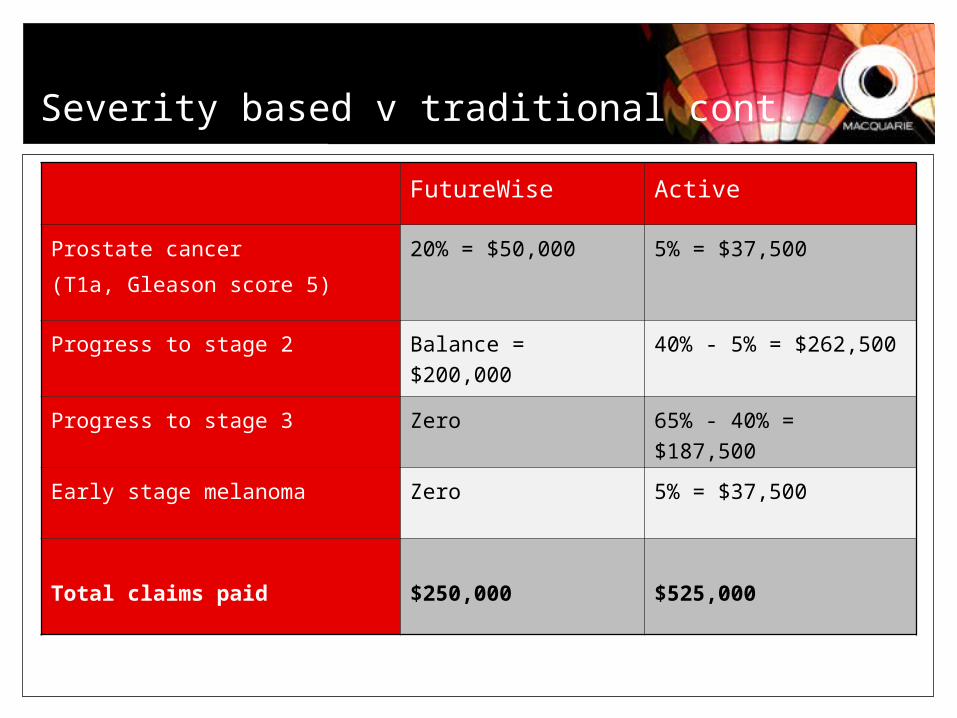

Severity based v traditional cont.

21

FutureWise Active

Prostate cancer

(T1a, Gleason score 5)

20% = $50,000 5% = $37,500

Progress to stage 2 Balance = $200,000 40% - 5% = $262,500

Progress to stage 3 Zero 65% - 40% = $187,500

Early stage melanoma Zero 5% = $37,500

Total claims paid $250,000 $525,000

Remember: tailor your messages

22

Men need a wake up call1:

– language and content that shakes them out of their complacency

– content that questions their assumptions of invulnerability

– believable, concrete facts to overcome cynicism. Women need a connection1:

– language that reassures and content that tells a story they can relate to

– analogies that makes sense to them

– ammunition in the form of facts and anecdotes to promote and fuel the insurance debate at home.

1IFSA/TNS - A Nation Exposed: Closing the Protection Gap 2005

IFSA/TNS Research suggests -