Embed Size (px)

Citation preview

© 2014 Research Academy of Social Sciences

http://www.rassweb.com 129

International Journal of Financial Economics

Vol. 2, No. 3, 2014, 129-141

Macroeconomic Variables and Capital Market Performance:

Evidence from Nigeria

Oliver Ike Inyiama1, Michael Chidiebere Ekwe

2

Abstract

The study aims at determining the causalities, correlation, cointegration and the relationship between the

Nigeria Stock Exchange All Share Index(ASI), which is the proxy for capital market performance and

macroeconomic variables proxied by monetary policy rate, inflationary rate, foreign exchange rate and real

gross domestic product from 1985 to 2013. Granger Causality procedure was applied in determining the

causalities, multiple regression model in the form of Ordinary Least Square (OLS) method was applied in

evaluating the relationship between the dependent and independent variables while correlation technique was

applied in ascertaining the strength of the relationship. Johansen cointegration procedure was applied in

testing the sustainability of the relationship in the long run. To test for stationary of the data series, the

Augmented Dickey Fuller (ADF), Phillips-Perron (PP) and the Kwiatkowski-Phillips-Schmidt-Shin (KPSS)

procedures were applied. All the series were non stationary. Except for real gross domestic product which

was differenced at second difference, all the other variables were differenced at first difference. Inflationary

rate, exchange rate and the log of real GDP are negatively but insignificantly related to the log of All Share

Index while interest rate is positively but not significantly related to All Share Index. No causality was

revealed in lag 2 but in lag 1, there is a unidirectional causality running from log of All Share Index to

foreign exchange rate. Johansen cointigration reveals a long run relationship among the variables. The

implication of the findings is that effective regulation of macroeconomic policies, in the direction of the

findings of this study, could impact positively on the performance of the capital market.

1. Introduction

The mobilization, facilitation and accumulation of finance from surplus to deficit sectors of the

economy for investment purposes are the main function of the capital market globally. This effort is however

geared towards the growth and development of emerging economies and sustainability in developed

economies. Osisanwo and Atanda (2012) submits that Capital market is a market for government securities

and corporate bonds and includes all financial institutions established for the purpose of granting of medium

and long-term loans for development. Ita and Duke (2013) explained that mobilization and allocation of

investment funds when done effectively, will enable business and economies maximize human, material and

management resources for optimal output. They emphasized that the stock market is the channel through

which efficiency in capital mobilization, formation and allocation is achieved.

The stock market, as opine by Sohail and Hussain (2009) mobilizes savings from a group of small

savers (including civil servants, small farmers, artisans, small business proprietors, itinerant workers, etc),

activates investment projects, poses as mediator and even a regulator between the small savers and their

borrowers, channels funds into desirable investment, supports reallocation of funds among corporations and

sectors and provides liquidity for domestic expansion and credit growth.

The Nigeria Stock Exchange (NSE), which is an automated exchange, was in 1960 created to provide

listing, trading, clearing, settlement, custodian, delivery, data dissemination and market indices services

1Department of Accountancy, Enugu State University of Science and Technology, Enugu State, Nigeria

2Department of Accountancy, Enugu State University of Science and Technology, Enugu State, Nigeria

O. I. Inyiama & M. C. Ekwe

130

through its associate company, the Central Securities Clearing System (CSCS) Plc. The Securities and

Exchange Commission (SEC) was however established in 1979 to develop and regulate the nation’s capital

market as well as fix stock issue prices after establishing the basis of allotment. The stock exchange was

established to develop the capital market through the promotion of private capital investment for growth and

development (Osisanwo and Atanda, 2012). They emphasized that the capital market offers opportunities to

local and foreign investors to provide long-term funds, far longer than the duration for which they are willing

to commit their funds, in exchange for long-term financial assets.

The success of an increasing privatization of emerging economies like Nigeria will depend crucially on

the presence of an active and efficient stock market. This is the view of Nguyen and Nguyen (2012) citing

Islam and Khaled (2005). They submit that most rational investors are expected to move their investments

into the most profitable projects with an acceptable risk exposure. When a stock market is reasonably large

and developed, it is assumed to serve as an indicator of economic soundness, health and prospects of the

emerging economy and an index of the confidence of domestic and global investors (Ali, 2011).

Prantik

and Vina(2009) explain that it has always been known globally that the stock market esponds to

a large extent to movements in macroeconomic indicators and recently, there has been widespread argument

that the direction of the influence is in the opposite direction. Asaolu and Ogunmuyiwa (2010) submit that

while developed economies like the USA and Canada have taken advantage of the capital market to mobilize

resources for growth and development, the developing countries like Nigeria are yet to fully explore the

benefits of raising capital through the developing capital market. Citing Anyanwu (2005), Ita and Duke

(2013) reveals that in Nigeria, the majority of the studies on stock market growth or development centered on

the relationship between stock market and economic growth while the very few that focused on analyzing the

macroeconomic indicators that determine stock market development restricted themselves to the use of

narrower measures.

This study will however focus on the evaluation of the relationship and causalities between

macroeconomic indicators such as foreign exchange rate, inflationary rate, interest rate and gross domestic

product on capital market performance variable proxied by All Share Index. Nigeria Stock Exchange website

states that the index is an aggregate of the market capitalisation of all of the industrial equities listed in the

market which is computed as the percentage of Current Market Value to Base Market Value of the industrial

equities. The remaining part of the study is divided into four sections. Section 2 focuses on the review of

related literature, Section 3 handles the aspect of methodology for data analysis while section 4 deals with

presentation of empirical findings and discussion of results. Section 5 concludes the study.

2. Review of Related Literature

Theoretical Framework

The study adopts the Arbitrage Pricing Theory (APT) by Ross (1976) as a result of the criticisms

leveled on the popular Efficient Market Hypotheses (EMH). It is believed that most markets have not been

proven to be efficient in getting market information across to the users and/or participants at the same time so

as to influence their investments and returns. Nguyen and Nguyen (2012) submits that the term efficiency is

used to describe a market in which all relevant information is immediately impounded into the price of

financial assets such that investors cannot expect to achieve superior profits from their investment strategies.

Osisanwo and Atanda (2012) opine that early empirical work on APT centered on returns from individual

securities. They argue that it may also be used in an aggregate stock market framework; a situation where a

change in a given macroeconomic variable could reflect a change or cause a movement in an underlying

systemic risk factor, thereby determining future returns. In support of this argument, Rashid (2008) opine

that the Arbitrage Pricing Theory attempts to establish a link between risk associated with particular

macroeconomic variables such as foreign exchange rate, monetary policy rate, gross domestic product, broad

money supply, inflationary rate and expected asset returns as economic forces, especially demand and supply

forces, affect discount rates, ability of firms to generate cash flows and future dividend payments.

International Journal of Financial Economics

131

Empirical Review

Using cointegration and error correction version of Granger causality tests, Nguyen and Nguyen (2012)

investigates the relationship between stock prices and macroeconomic variables in Vietnam stock exchange.

It was revealed that Vietnamese stock market is not informationally efficient in both short- and long-run. The

implication is that the Efficient Market Hypothesis does not hold in this regard as a professional trader can

still make abnormal returns.

In Pakistan, Sohail and Hussain (2009), using VECM analysis, examined the long and short-run

relationships between Lahore Stock Exchange and macroeconomic variable. It was revealed that inflation

rate needs to come down to improve stock returns while exchange rate and money supply associate with

stock returns positively. This implies that a stronger naira to the dollar rate or at least an improvement from

the present exchange rate is desirable to increase stock returns.

An attempt was made by Prantik and Vani (2009) by applying VAR and Artificial Neural Network to

exhume the relationship between the real economic variables and the capital market in India. The study

shows that interest rate, output, money supply, inflation rate and the exchange rates are capable of causing

movements in stock market indices. However, other variables have very negligible impact on the stock

market.

Asaolu and Ogunmuyiwa (2010) in a related study and using Granger Causality test, Co-integration and

Error Correction Method (ECM), investigates the impact of macroeconomic variables on Average Share

Price (ASP) and goes further to determine whether changes in macroeconomic variables explain movements

in stock prices in Nigeria. The analysis reveals a weak relationship between Average Share Price and

macroeconomic variables in the long run.

The relationships between Indian stock market index (BSE Sensex) and five macroeconomic variables

were investigated by Naik and Padhi (2012) using Johansen’s co-integration and vector error correction

model. Long run co integration was revealed as stock prices relate positively to money supply and industrial

production but negatively to inflation. Macroeconomic variable however causes the stock prices in the long-

run as unidirectional causality runs from money supply to stock price, stock price to inflation and interest

rates to stock prices.

Agrawal, Srivastav and Srivastava (2010) analyzes the relationship between Nifty returns and Indian

rupee-US Dollar Exchange Rates and found that Nifty returns and Exchange Rates were non-normally

distributed and correlated negatively. Unidirectional Causality runs from Nifty returns to Exchange Rates.

Simple and multiple regression analysis was applied by AL- Shubiri (2010) to examine the relationship

between micro and macroeconomic factors with the stock prices and found highly positive significant

relationship between market price of stock and net asset value per share; market price of stock dividend

percentage, gross domestic product and negative significant relationship on inflation and lending interest

rate.

Hussainey and Ngoc (2009) investigates the effects of interest rate and the industrial production on

Vietnamese stock prices using cointegration approach and citing Nasseh and Strauss (2000) and Canova and

de Nicolo (1995). The paper found that there are statistically significant associations among the domestic

production sector, money markets, and stock prices in Vietnam and that the US macroeconomic

fundamentals significantly affect Vietnamese stock prices.

Using Augmented Dickey Fuller test, Johansen’s co-integration and Granger’s causality test, Ali,

Rehman, Yilmaz, Khan and Afzal (2009) examined the causal relationship between macro-economic

indicators (inflation, exchange rate, balances of trade and index of industrial production) and stock market

prices (represented by the general price Index) in Pakistan Karachi Stock Exchange. Co-integration was

found between industrial production index and stock exchange prices but no causal relationship was found

between macro-economic indicators and stock exchange prices.

O. I. Inyiama & M. C. Ekwe

132

Olugbenga (2011), panel model, investigates the impact of macroeconomic indicators (money supply

(BRDM), interest rate (INTR), exchange rate (ECHR), inflation rate (INF), oil price (OIL) and gross

domestic product (GDP)) on stock prices in Nigeria at the firm’s level. The study found that apart from

inflation rate and money supply, all the other macroeconomic variables have significant impacts on stock

prices in Nigeria.

The above review of related literature indicates that most of the studies on macroeconomic indicators

and capital market performance were done in countries outside Nigeria and at firm levels. Most of the few

studies also did not consider the impact of these indicators on the All Share Index(ASI) which is a broad

based index indicating a total stock market index that paints the overall picture of movements in the prices of

equity shares on a daily basis. However, an attempt in this regard in Nigeria dates back to 2008 using simple

regression and failing to consider Granger causalities among the variables under study. In this study, an

attempt is made to validate the relationship between the macroeconomic variables and All Share Index in a

multiple regression model and to ascertain the causality relationships as well as cointegration among the

variables between 1985 and 2013 in Nigeria.

3. Methodology

Foreign Exchange Rate, Interest Rate, Inflationary Rate and Real Gross Domestic Product data were

obtained from Central Bank Statistical bulletins for several years especially the CBN Statistical Bulletin, 50

years special Anniversary edition. All Share Index time series data was collected from the Nigeria Stock

Exchange for the period covering 1985 to 2013. The choice of 1985 was based on availability of data for the

analysis.

The relationship between the measure of capital market performance (All Share Index) and the

macroeconomic variables (foreign exchange rate, interest rate, inflationary rate and the real gross domestic

product) was estimated using the multiple regression approach. The causalities among the dependent and

independent variables especially at the short run were examined by applying the Granger Causality model

after using the Augmented Dickey Fuller (ADF) and Phillips Perrons’(PP) Test to check for stationary of the

time series data. The Johansen’s cointegration approach is applied to test for long run relationship among and

between the variables under study.

Citing Pasquale (2006), Inyiama(2013) submits that Granger-causality is normally tested in the context

of linear regression models and specified as follows in our bivariate linear autoregressive model of two

variables X1 and X2 based on lagged values as follows:

P p

X1(t) =∑ A11,jX1(t−j) + ∑ A12,jX2(t−j) + E1 (t)

j =1 j =1

P p

X2(t) =∑ A21,jX1(t−j) + ∑ A22,jX2(t−j) + E2 (t)

j =1 j =1

Where;

p is the maximum number of lagged observations included in the equation, the matrix A contains the

coefficients of the equation (i.e., the contributions of each lagged observation to the predicted values of X1(t)

and X2(t) ,

X1 is the share price which is constant while X2 takes the form of various macroeconomic indices identified

above and,

E1 and E2 are residuals (prediction errors) for each time series.

The econometric model applied in data analysis is consistent with the studies done by Hussainey and

Ngoc (2009), Olugbenga (2011), Ali, Rehman, Yilmaz, Khan and Afzal (2009), Agrawal, Srivastav and

Srivastava (2010), Naik and Padhi (2012), Asaolu and Ogunmuyiwa (2010) and Sohail and Hussain (2009).

International Journal of Financial Economics

133

The relationship between foreign exchange rate, interest rate, gross domestic product, inflation rate and

All Share Index (ASI) is specified by the primary model shown below:

ASI = f (Intrate, Infrate, Exchrate, Rgdp)

ASI = α0 +α1 Intrate +α2Infrate + α3Exchrate + α4Rgdp + εt.

Table 1: Description of Variables

INFRATE Inflationary Rate(All items, Year on

Change)

INTRATE Interest Rate

EXCHRATE Exchange Rate

RGDP Real Gross Domestic Product

ASI All Share Index

Multiple regression equation is applied in examining the relationship between All Share Index (ASI)

and Interest Rate, Inflation Rate, Foreign Exchange Rate and Real GDP as adopted in Inyiama(2013). The

equation is estimated in the form:

ASIt = K + β1 INTRATEt+ β2 INFRATEt + β3 EXCHRATEt + β4RGDP

Where;

INFRATEt = Inflation Rate in time t (All items, Year on Change)

INTRATEt = Interest Rate in time t

EXCHRATEt = Exchange Rate in time t.

RGDPt = Real Gross Domestic Product in time, t.

ASI = All Share Index in time, t.

α0 is a constant term, ‘t’ is the time and ‘ε’ is the random error term.

4. Discussion of Findings

Test of stationary is carried out on all the time series data to check for unit root problems. To achieve

this, three methods of testing for unit root were adopted namely, the Augmented Dickey Fuller (ADF),

Phillips-Perron (PP) and the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) procedure. Data is expected to be

stationary as opine by Naik and Padhi (2012), emphasizing that the mean and variance of such data series

should be constant throughout the period and the value of covariance between two time periods should

depend only on the distance between the two periods and not the time at which the covariance is computed.

This condition is only achievable when the time series data is stationary.

The time series data which includes log of All Share Index, Inflationary Rate, Interest Rate, Foreign

Exchange Rate and log of Real Gross Domestic Product were tested and they could not pass the stationary

test. The graphs below were preliminary evidence of the unit root issues as the line graphs failed to cross the

zero lines repeatedly. However, time series data is integrated of order d when it becomes stationary after

being differenced d times as opine by Hosseini, Ahmad and Lai(2011). This is to avoid spurious results

which may arise as a result of carrying out regressions on time series data with unit root (Asaolu and

Ogunmuyiwa, 2010).

O. I. Inyiama & M. C. Ekwe

134

0

10,000

20,000

30,000

40,000

50,000

60,000

1985 1990 1995 2000 2005 2010

ASINDEX

5

10

15

20

25

30

1985 1990 1995 2000 2005 2010

INFRATE

0

20

40

60

80

1985 1990 1995 2000 2005 2010

INTRATE

0

40

80

120

160

1985 1990 1995 2000 2005 2010

EXCHRATE

0

200

400

600

800

1,000

1985 1990 1995 2000 2005 2010

REALGDP

Figure 1: Graphical Representation of the Variables with Unit Root

Source: Author’s EView 8.0 Output.

Table 2: Augmented Dickey- Fuller (ADF) Test Results

Null Hypothesis: Time Series Data are not Stationary

ALL SHARE

INDEX (LOG)

INFLATION

RATE

INTEREST

RATE

EXCHAN

GE RATE

REAL

GDP

(LOG)

ADF Statistic -4.037542 -7.627110 -4.554271 -5.013504 -7.287220

Critical Value:

1% -3.699871 -3.699871 -3.699871 -3.699871 -3.711457

5% -2.976263 -2.976263 -2.976263 -2.976263 -2.981038

10% -2.627420 -2.627420 -2.627420 -2.627420 -2.629906

Status 1(1) 1(1) 1(1) 1(1) 1(2) Source: Author’s EView 8.0 Computation

Table 3: Phillip-Perron’s (PP) Test Results

Null Hypothesis: Time Series Data are not Stationary

PP Statistic -4.045778 -8.241867 -4.726881 -5.013504 -7.287220

Critical Value:

1%

-3.699871 -3.699871 -3.699871 -3.699871 -3.711457

5% -2.976263 -2.976263 -2.976263 -2.976263 -2.981038

10% -2.627420 -2.627420 -2.627420 -2.627420 -2.629906

Status 1(1) 1(1) 1(1) 1(1) 1(2)

PP Statistic -4.045778 -8.241867 -4.726881 -5.013504 -7.287220 Source: Author’s EView 8.0 Computation

International Journal of Financial Economics

135

Table 4: Kwiatkowski-Phillip’s-Schmidt-Shin(KPSS) Test Results

Null Hypothesis: Time Series Data are not Stationary

KWSS Statistic 0.273198 0.183014 0.165047 0.097043 0.030499

Critical Value:

1%

0.739000 0.739000 0.739000 0.739000 0.739000

5% 0.463000 0.463000 0.463000 0.463000 0.463000

10% 0.347000 0.347000 0.347000 0.347000 0.347000

Status 1(1) 1(1) 1(1) 1(1) 1(2)

KWSS Statistic 0.273198 0.183014 0.165047 0.097043 0.030499 Source: Author’s EView 8.0 Computation

Tables 2, 3 and 4 reveals that when the Augmented Dickey Fuller (ADF), Phillips-Perron (PP) and the

Kwiatkowski-Phillips-Schmidt-Shin (KPSS) procedures were applied respectively in testing for unit root in

the time series data, the log of All Share Index, Inflationary Rate, Interest Rate and Foreign Exchange Rate

achieved stationary at first difference and intercept. Log of Real Gross Domestic Product attained stationary

at second difference and intercept. This means that the time series data except log of real gross domestic

product were integrated of the order one.

Citing Asteriou (2007), Nguyen and Nguyen (2012) submits that most macroeconomic variables are

cointegrated of order one. The result of the unit root test is also supported by other related literature which

established that most macroeconomic variables and stock indexes time series data are non stationary, as they

tend to exhibit either a deterministic or a stochastic trend (Asaolu and Ogunmuyiwa, 2010).The reason for

applying the Phillips-Perron (PP) procedure is because the ADF Test has been accused of its low power

while the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test was for robustness of the model. The graphs

below show clearly the absence of unit root as the line graphs repeatedly crossed the zero lines.

-.3

-.2

-.1

.0

.1

.2

.3

.4

1985 1990 1995 2000 2005 2010

DLOGASINDEX

-.02

.00

.02

.04

.06

.08

.10

1985 1990 1995 2000 2005 2010

DLOGRGDP

-15

-10

-5

0

5

10

1985 1990 1995 2000 2005 2010

DINFRATE

-60

-40

-20

0

20

40

1985 1990 1995 2000 2005 2010

DINTRATE

-20

0

20

40

60

80

1985 1990 1995 2000 2005 2010

DEXCHRATE

Figure 1: Graphical Representation of the Variables without Unit Root

Source: Author’s EView 8.0 Output.

O. I. Inyiama & M. C. Ekwe

136

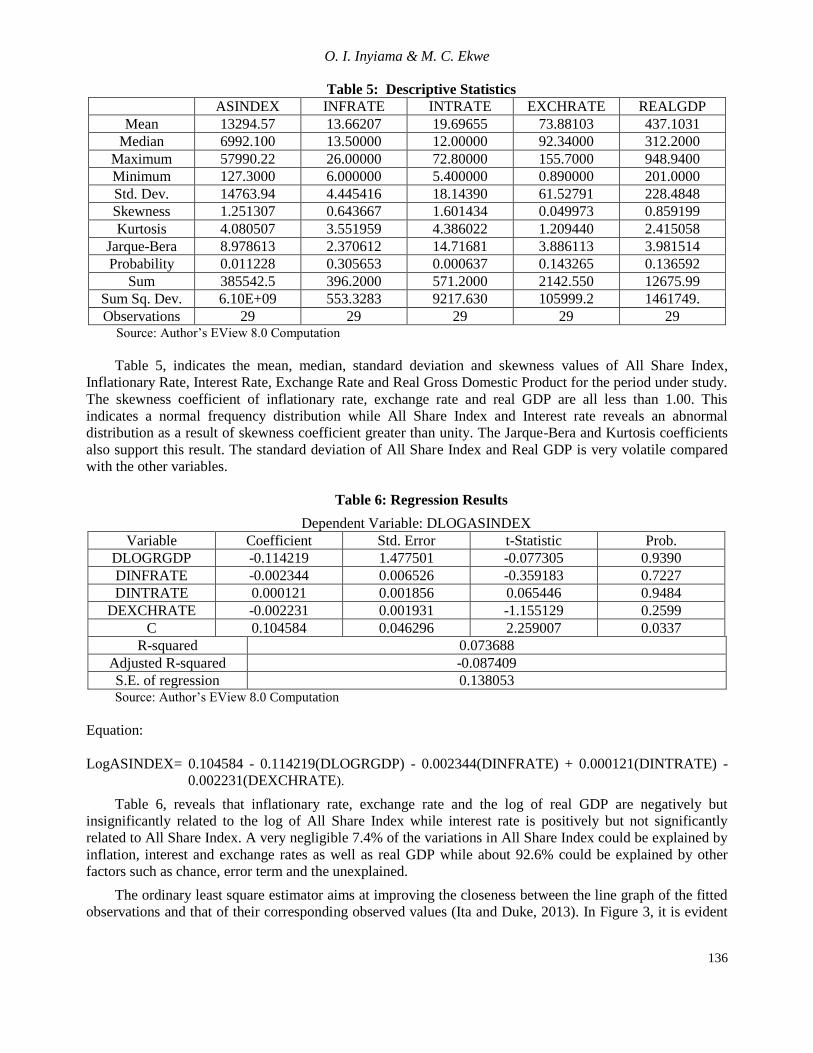

Table 5: Descriptive Statistics

ASINDEX INFRATE INTRATE EXCHRATE REALGDP

Mean 13294.57 13.66207 19.69655 73.88103 437.1031

Median 6992.100 13.50000 12.00000 92.34000 312.2000

Maximum 57990.22 26.00000 72.80000 155.7000 948.9400

Minimum 127.3000 6.000000 5.400000 0.890000 201.0000

Std. Dev. 14763.94 4.445416 18.14390 61.52791 228.4848

Skewness 1.251307 0.643667 1.601434 0.049973 0.859199

Kurtosis 4.080507 3.551959 4.386022 1.209440 2.415058

Jarque-Bera 8.978613 2.370612 14.71681 3.886113 3.981514

Probability 0.011228 0.305653 0.000637 0.143265 0.136592

Sum 385542.5 396.2000 571.2000 2142.550 12675.99

Sum Sq. Dev. 6.10E+09 553.3283 9217.630 105999.2 1461749.

Observations 29 29 29 29 29 Source: Author’s EView 8.0 Computation

Table 5, indicates the mean, median, standard deviation and skewness values of All Share Index,

Inflationary Rate, Interest Rate, Exchange Rate and Real Gross Domestic Product for the period under study.

The skewness coefficient of inflationary rate, exchange rate and real GDP are all less than 1.00. This

indicates a normal frequency distribution while All Share Index and Interest rate reveals an abnormal

distribution as a result of skewness coefficient greater than unity. The Jarque-Bera and Kurtosis coefficients

also support this result. The standard deviation of All Share Index and Real GDP is very volatile compared

with the other variables.

Table 6: Regression Results

Dependent Variable: DLOGASINDEX

Variable Coefficient Std. Error t-Statistic Prob.

DLOGRGDP -0.114219 1.477501 -0.077305 0.9390

DINFRATE -0.002344 0.006526 -0.359183 0.7227

DINTRATE 0.000121 0.001856 0.065446 0.9484

DEXCHRATE -0.002231 0.001931 -1.155129 0.2599

C 0.104584 0.046296 2.259007 0.0337

R-squared 0.073688

Adjusted R-squared -0.087409

S.E. of regression 0.138053 Source: Author’s EView 8.0 Computation

Equation:

LogASINDEX= 0.104584 - 0.114219(DLOGRGDP) - 0.002344(DINFRATE) + 0.000121(DINTRATE) -

0.002231(DEXCHRATE).

Table 6, reveals that inflationary rate, exchange rate and the log of real GDP are negatively but

insignificantly related to the log of All Share Index while interest rate is positively but not significantly

related to All Share Index. A very negligible 7.4% of the variations in All Share Index could be explained by

inflation, interest and exchange rates as well as real GDP while about 92.6% could be explained by other

factors such as chance, error term and the unexplained.

The ordinary least square estimator aims at improving the closeness between the line graph of the fitted

observations and that of their corresponding observed values (Ita and Duke, 2013). In Figure 3, it is evident

International Journal of Financial Economics

137

that the line graph of the fitted observations is as close as possible to the graph of the corresponding observed

values.

-.4

-.2

.0

.2

.4

-.4

-.2

.0

.2

.4

86 88 90 92 94 96 98 00 02 04 06 08 10 12

Residual Actual Fitted Figure 3: Residual graph of the parsimonious model

Source: EViews 8.0 Output

Table 7: Correlation Coefficient

DLOGASINDEX DLOGRGDP DINFRATE DINTRATE DEXCHRATE

DLOGASINDEX 1.000000 0.014188 -0.137865 0.006946 -0.261332

DLOGRGDP 0.014188 1.000000 -0.095899 -0.227625 -0.107480

DINFRATE -0.137865 -0.095899 1.000000 0.162578 0.270619

DINTRATE 0.006946 -0.227625 0.162578 1.000000 -0.008188

DEXCHRATE -0.261332 -0.107480 0.270619 -0.008188 1.000000 Source: Author’s EView 8.0 Computation

Table 7, reveals a positive correlation between interest rate, log of real GDP and log of All Share Index.

A negative correlation is found between exchange rate, inflationary rate and log of All Share Index.

However, amongst all the variables under study, only exchange rate indicates up to 26% magnitude of

correlation as others are found to be very weak in strength.

Table 8: Pairwise Granger Causality Tests

Date: 04/22/14 Time: 20:34

Sample: 1985 2013

Lags: 2

Null Hypothesis: Obs F-Statistic Prob.

DLOGRGDP does not Granger Cause DLOGASINDEX 26 0.62339 0.5458

DLOGASINDEX does not Granger Cause DLOGRGDP 0.29071 0.7507

DINFRATE does not Granger Cause DLOGASINDEX 26 0.50904 0.6083

DLOGASINDEX does not Granger Cause DINFRATE 0.39047 0.6816

DINTRATE does not Granger Cause DLOGASINDEX 26 0.98492 0.3901

DLOGASINDEX does not Granger Cause DINTRATE 0.06209 0.9400

DEXCHRATE does not Granger Cause

DLOGASINDEX 26 0.95854 0.3996

DLOGASINDEX does not Granger Cause DEXCHRATE 2.71243 0.0896

Source: Author’s EView 8.0 Computation

O. I. Inyiama & M. C. Ekwe

138

Table 9: Pairwise Granger Causality Tests

Date: 04/22/14 Time: 20:37

Sample: 1985 2013

Lags: 1

Null Hypothesis: Obs F-Statistic Prob.

DLOGRGDP does not Granger Cause DLOGASINDEX 27 0.37806 0.5444

DLOGASINDEX does not Granger Cause DLOGRGDP 0.67143 0.4206

DINFRATE does not Granger Cause DLOGASINDEX 27 0.10998 0.7430

DLOGASINDEX does not Granger Cause DINFRATE 0.00676 0.9352

DINTRATE does not Granger Cause DLOGASINDEX 27 0.82386 0.3731

DLOGASINDEX does not Granger Cause DINTRATE 0.24188 0.6273

DEXCHRATE does not Granger Cause

DLOGASINDEX 27 1.97934 0.1723

DLOGASINDEX does not Granger Cause DEXCHRATE 5.56307 0.0268

Source: Author’s EView 8.0 Computation

Tables 8 and 9 indicate that no causal relationship exists between All Share Index and all the

independent variables of inflation rate, interest rate and real GDP. However, there is a unidirectional

causality running from log of All Share Index to foreign exchange rate at 5% and 10% levels of significance

and in lag 1. In lag 2, there is no Granger Causality between and among all the variables under study.

Citing Hansen and Juselius (2002), Gunasekarage, Pisedtasalasai and Power(2005) submits that to find

cointegration between nonstationary variables, at least two variables of all variables included in the

cointergration system have to be I(1) They argued that the existence of a cointegration reveals the existence

of a long term relationship between the market index and the macro-economic variables.. In this study, all

share index, interest rate, inflationary rate and exchange rate are integrated in the order 1(1) while only the

real gross domestic product is integrated in the order 1(2). Abraham(2012) opine, while citing Johansen

(1988), Stock and Watson (1988) and Johansen and Juselius (1990) that the two basic test statistics involved

in Johansen and Juselius’s maximum likelihood test are the trace test and the maximal eigenvalue test. These

two tests are conducted below and the result of the trace test indicates two(2) cointegrating equations at the

0.05 level while Maximum Eigenvalue indicates a cointegrating equation at the 0.10 level. The result

indicates that the short run relationship which they presently share can also be sustained in the long-run.

Table 10: Johansen Cointegration Results

a) Unrestricted Cointegration Rank Test (Trace)

Hypothesized

No. of CE(s) Eigenvalue

Trace

Statistic

0.05

Critical Value Prob.**

None * 0.674724 78.56671 69.81889 0.0085

At most 1 * 0.551868 49.36663 47.85613 0.0358

At most 2 0.373105 28.49727 29.79707 0.0700

At most 3 * 0.325491 16.35589 15.49471 0.0370

At most 4 * 0.209669 6.117878 3.841466 0.0134

International Journal of Financial Economics

139

b) Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized

No. of CE(s) Eigenvalue

Max-Eigen

Statistic

0.05

Critical Value Prob.**

None 0.674724 29.20009 33.87687 0.1635

At most 1 0.551868 20.86935 27.58434 0.2842

At most 2 0.373105 12.14138 21.13162 0.5338

At most 3 0.325491 10.23801 14.26460 0.1968

At most 4 * 0.209669 6.117878 3.841466 0.0134 * denotes rejection of the hypothesis at the 0.05 level

Source: EViews 8.0 Output

5. Summary and Conclusion

The study aims at determining the relationship between All Share Index (the proxy for capital market

performance) and real gross domestic product, monetary policy rate, inflationary rate and foreign exchange

rate (the proxy for macroeconomic variables of the study). The regression result reveals that inflationary rate,

exchange rate and the log of real GDP are negatively but insignificantly related to the log of All Share Index

while interest rate is positively but not significantly related to All Share Index. This implies that maintaining

a low inflationary and exchange rates could improve capital market performance while a reasonably high

monetary policy rate could also yield positive results in the performance of capital market. No causal

relationship exists between All Share Index and the independent variables of inflation rate, interest rate and

real GDP except for a unidirectional causality running from log of All Share Index to foreign exchange rate

at 5% and 10% levels of significance and in lag 1 only. Positive correlation is found between interest rate,

log of real GDP and log of All Share Index while negative correlation exist between exchange rate,

inflationary rate and the dependent variable(ASI). The cointegrating equation found is an indication that their

short run relationship could be sustained in the future. Therefore, if macroeconomic variables could be

effectively regulated or controlled by the regulatory agencies such as Nigeria Stock Exchange, Securities and

Exchange Commission and the Central Bank of Nigeria, as suggested by the findings of this study, the

variables are most likely to impact tremendously on the performance of the Nigeria Capital Market.

References

Abraham, T.W(2012). Stock Market Reaction to Selected Macroeconomic Variables in the Nigerian

Economy, CBN Journal of Applied Statistics 2(1), 61-70.

Agrawal, G., Srivastav, A,K. and Srivastava, A.(2010). A Study of Exchange Rates Movement and Stock

Market Volatility, International Journal of Business and Management, 5(12).

Ali, M,B.(2011). Co integrating Relation between Macroeconomic Variables and Stock Return: Evidence

from Dhaka Stock Exchange (DSE), International Journal of Business and Commerce 1(2): 25-38.

Ali I., Rehman K. U., Yilmaz A. K., Khan M. A. and Afzal H. (2010) ‘Causal Relationship between

Macroeconomic Indicators and stock Exchange Prices in Pakistan’ African Journal of Business

Management, 4(3), 312 – 319.

AL- Shubiri, F(2010). Analysis the Determinants of Market Stock Price Movements: An Empirical Study of

Jordanian Commercial Banks, International Journal of Business & Management:

5(10):137.Available athttp://connection.ebscohost.com/c/articles/56104197/analysis-determinants-

market-stock- pricemovements- empirical-study-jordanian-commercial-banks

Anyanwu, J. C. (2005). Stock Market Development and Nigeria’s Economic Growth, The Nigerian Financial

Review, 13(3): 6-13

O. I. Inyiama & M. C. Ekwe

140

Asaolu, T.O., and Ogunmuyiwa, M.S. (2011). An Econometric Analysis of the Impact of Macroeconomic

Variables on Stock Market Movement in Nigeria. Asian Journal of Business Management, 3(1), 72-

78.

Asteriou, D. and Hall, S.G., 2007, Applied Econometrics: A Modern Approach Using Eviews and

Microfit, Revised Edition. Palgrave Macmillan

Central Bank of Nigeria (CBN), Annual Reports and Statement of Accounts - Various Years.

Dickey, D. A. and Fuller, W. A., 1979, Distributions of the estimators for autoregressive time series with a

unit root. Journal of the American Statistical Association, 74. 423–431.

Gunasekarage, A., Pisedtasalasai, A., and Power, D.M (2005). Macro-economic Influences on the Stock

Market: Evidence from an Emerging Market in South Asia.

Granger, C. W. J.(1986), Developments in the Study of Cointegrated Economic Variables, Oxford Bulletin

of Economics and Statistics 48, 213-27.

Hansen, H. and K. Juselius (2002), CATS in RATS Cointegration Analysis of Time Series, Estima.

Hosseini, S. M., Ahmad, Z., and Lai, Y. W.(2011). The Role of Macroeconomic variables on stock market

index in China and India, International Journal of Economics a nd Finance, 3 (6), 233-243.

Hussainey and Ngoc (2009), ‘Impact of Macroeconomic Variables on Vietnamese Stock Exchange’ Journal

of Risk Finance, 4, 18-46.

Inyiama, O.(2013), Does Inflation Weaken Economic Growth? Evidence from Nigeria, European Journal of

Accounting Auditing and Finance Research, 1(4), 139-150.

Ita, J,J and Duke, J.(2013). Macroeconomic Factors That Influence Stock Market Development In

Nigeria, International Journal of Business and Management Review, 1(2), 43-56.

Islam, A. and Khaled, M. (2005). Tests of Weak Form Efficiency of the Dhaka Stock Exchange. Journal of

Business Finance and Accounting, 32, 1613-1624.

Johansen, S. (1988) ‘Statistical Analysis of Cointegration Vectors’, Journal of Economic Dynamics and

Control, 12, 231-254.

Johansen, S., and K. Juselius, (1990) ‘Maximum Likelihood Estimation and Inference on Cointegration –

With Applications to the demand for money’, Oxford Bulletin of Economics and Statistics,52,169-

210

Kwiatkowski, D., P. C. B. Phillips, P. Schmidt and Y. Shin (1992), Testing the null hypothesis of trend

stationarity. Journal of Econometrics, 54, 159-178.

Naik and Padhi, (2012), The Impact of Macroeconomic Fundamentals on Stock Prices Revisited: Evidence

from Indian Data, Eurasian Journal of Business and Economics, 5 (10), 25-44.

Nguyen, T, H. and Nguyen, T, B.(2012). Stock Prices and Macroeconomic Variables in Vietnam:An

Empirical Analysis

Osisanwo, B, G., and Atanda, A.(2012). Determinants of Stock Market Returns in Nigeria: A Time Series

Analysis, African Journal of Scientific Research 9(1).

Olugbenga, A, A.(2011). The Impact of Macroeconomic Indicators on Stock Prices in Nigeria, Developing

Country Studies www.iiste.org 1(2).

Prantik, R

and Vani, V (2009). What Moves Indian Stock Market: A Study on the Linkage with Real

Economy in the Post-Reform Era.

Phillips, P. C. B., and P. Perron, (1988), Testing for a Unit Root in Time Series Regression, Biometrika 75,

335-46.

International Journal of Financial Economics

141

Pasquale, F. (2006). "Testing for Granger causality between stock prices and economic growth," MPRA

Paper 2962, University Library of Munich, Germany, revised 2007.

Rashid, A.(2008): Macroeconomic Variables and Stock Market Performance: Testing for Dynamic Linkages

with a Known Structural Break. Published in: Saving and Development, 1:77-102.

Ross, S.A., (1976), “The Arbitrage Theory of Capital Asset Pricing”, Journal of Economic Theory,13, 341-

360.

Sohail, N and Hussain, K.(2009). Long-Run And Short-Run Relationship Between Macroeconomic

Variables And Stock Prices In Pakistan :The Case Of Lahore Stock Exchange, Pakistan Economic

and Social Review 47, (2), 183-198.