Embed Size (px)

Citation preview

MALAYSIA

Rapid Assessment and Gap Analysis

For Sustainable Energy for All (SE4ALL) Initiative

A Report by the UN Country Team Malaysia

Prepared and Edited by:

Azman Zainal Abidin (Technical Advisor), Prof Dr. Ir. KS Kannan (UNIDO) and Asfaazam Kasbani (UNDP)

Under the guidance of: Economic Planning Unit (EPU) and Ministry of Energy, Green Technology and Water (MEGTW), Malaysia

September 2012

Disclaimer: The findings, interpretation, and conclusions expressed in this report are entirely those of the authors and should not be attributed in any manner to the United Nations Malaysia Country Team, UNDP, UNIDO and to its affiliated organizations or to the countries they represent including its agencies. The authors use information publicly sourced as advised and without prejudice.

1

Sustainable Energy for All (SE4ALL) Brief UN Secretary-General Ban Ki-moon is leading a global initiative on Sustainable Energy for All to mobilize action from all sectors of society: business, governments, investors, community groups and academia. The United Nations is the ideal institution to convene this broad swath of actors and forge common cause in support of three interlinked objectives:

1. Ensure Universal Assess to modern energy services 2. Double the global rate of improvement in energy efficiency (EE) 3. Double the share of renewable energy (RE) in the global energy mix

These objectives are complementary. Progress in achieving one can help with progress toward the

others. All are to be achieved by 2030, and all are necessary to achieve sustainable energy for all. The

Secretary-General’s initiative contributes to the International Year of Sustainable Energy for All in 2012,

as declared by the UN General Assembly, by providing a focus for action by all stakeholders.

OBJECTIVE The purpose of this Rapid Assessment and Gap Analysis is to provide:

A quick brief look of the energy situation in the country (Section 1) within the context of its economic and social development and poverty eradication

A good review of where the country is in terms of the three SE4ALL goals (Section 2), and

A good estimate of the main challenges and opportunities vis-à-vis the three goals of SE4ALL where the major investments, policies and enabling environments will be required (Section 3)

A sound basis and background for an Action Plan that may follow as part of the SE4ALL

activities in the country

2

Abbreviations

AAIBE Akaun Amanah Industri Bekalan Elektrik (AAIBE)

CEB Central Electricity Board

DDC District Development and Review Committee

DID Department of Irrigation and Drainage

EC Energy Commission (English for ST)

EE Energy Efficiency

EIB Energy Information Bureau

EPP Entry Point Projects

EPU Economic Planning Unit

FiT Feed-in-Tariff

GDP Gross Domestic Product

GTP Government Transformation Programme

ICU Implementation Coordination Unit

IPP Independent Power Producer

ktoe Kilo tones of oil equivalent

MDG Millennium Development Goals

MDTCA Ministry of Domestic Trade and Consumer Affairs

MEGTW Ministry of Energy, Green Technology and Water

MESITA Malaysian Electricity Supply Industries Trust

Account (English for AAIBE)

MGTC Malaysia Green Technology Corporation

MHLG Ministry of Housing and Local Government

MITI Ministry of International Trade and Industry

MOA Ministry of Agriculture

MOE Ministry of Education

MOH Ministry of Health

MOSTI Ministry of Science, Technology and Innovation

MP Malaysia Plan

MRRD Ministry of Rural and Regional Development

NDC National Development Council

3

NDPC National Development Planning Council

NEB National Energy Balance

PEMANDU Performance Management and Delivery Unit

PLI Poverty Line Income

PTM Pusat Tenaga Malaysia (Malaysia Energy Center)

RBI Rural Basic Infrastructure

RE Renewable Energy

REPPA Renewable Energy Power Purchase Agreement

REP-PoR Regional Energy Programme for Poverty Reduction

SDC State Development Committee

SEDA Sustainable Energy Development Authority

SEPU State Economic Planning Unit

SESB Sabah Electricity Sdn. Bhd.

SESCO Sarawak Electricity Company

SHS Solar Home System

SME Small and Medium Industries

SREP Small Renewable Energy Projects

ST Suruhanjaya Tenaga (Energy Commission)

TNB Tenaga Nasional Berhad

UNCT United Nations Country Team Malaysia

UNDP United Nations Development Programme

UNIDO United Nations Industrial Development

Organization

4

Table of Contents ABBREVIATIONS ....................................................................................................................... 3 EXECUTIVE SUMMARY ............................................................................................................. 6 SECTION I: INTRODUCTION ..................................................................................................... 8

1.1 COUNTRY OVERVIEW ..........................................................................................................8 Basic socio-economic data for Malaysia .................................................................................. 8

1.2 ENERGY SITUATION .............................................................................................................9 1.2.1 Energy Supply (energy mix, export/import, electricity sector) .......................................... 9 1.2.2 Net Imports and Exports by Fuels Type .........................................................................11 1.2.3 Energy demand .............................................................................................................12 1.2.4 Energy and Economic Development ..............................................................................13 1.2.5 Energy Strategy and Relevant Targets...........................................................................14

SECTION 2: CURRENT SITUATION WITH REGARDS TO SE4ALL GOALS ............................15 2.1 ENERGY ACCESS vis-à-vis GOAL OF SE4ALL ...................................................................15

2.1.1 Overview and assessment .............................................................................................15 2.1.2 Modern energy for thermal applications (cooking, heating) .............................................15 2.1.3 Access to electricity: ......................................................................................................17

2.2 ENERGY EFFICIENCY vis-à-vis GOAL OF SE4ALL ............................................................21 2.2.1 Overview and Assessment .............................................................................................21 2.2.2 Energy intensity of national economy: ............................................................................22

2.3 RENEWABLE ENERGY vis-à-vis GOAL OF SE4ALL ...........................................................24 2.3.1 Overview and Assessment .............................................................................................24 2.3.2 On-grid and off-grid renewable energy ...........................................................................25

2.4 SE4All GOALS .....................................................................................................................26 2.4.1 Energy Access ...............................................................................................................26 2.4.2 Energy Efficiency ...........................................................................................................26 2.4.3 Renewable Energy.........................................................................................................26

SECTION 3: CHALLENGES AND OPPORTUNITIES FOR ACHIEVING SE4ALL GOALS .........27 3.1 INSTITUTIONAL AND POLICY FRAMEWORK ....................................................................27

3.1.1 Energy and development ...............................................................................................27 3.1.2 Thermal energy for households ......................................................................................28 3.1.3 Power sector ..................................................................................................................29 3.1.4 Modern energy for productive sectors ............................................................................29 3.1.5 National monitoring framework for SE4ALL ....................................................................29

3.2 PROGRAMS .........................................................................................................................30 3.2.1 Thermal energy ..............................................................................................................30 3.2.2 Power sector ..................................................................................................................30 3.2.3 Energy efficiency programs ............................................................................................30 3.2.4 Modern energy for productive use ..................................................................................31

3.3 FINANCING ..........................................................................................................................31 3.4 PRIVATE INVESTMENT AND ENABLING BUSINESS ENVIRONMENT .............................33

3.4.1 Thermal energy for households ......................................................................................33 3.4.2 Power sector ..................................................................................................................33 3.4.3 Modern energy for productive sectors ............................................................................34

3.5 GAPS AND BARRIERS ........................................................................................................35 REFERENCES ...........................................................................................................................37 ANNEX 1: OTHER INITIATIVES RELATED TO SE4ALL ............................................................38

5

EXECUTIVE SUMMARY This report is prepared as part of the United Nations Country Team’s effort to support Malaysia in embarking into SE4ALL initiatives. The Rapid Assessment and Gap Analysis report will map out current status of SE4LL which will include sections on Current Situation and Challenges.

Malaysia has been successful in achieving the overall progress of the SE4ALL objectives. Strong and

sustained economic growth has contributed to success in meeting basic energy needs, including rural

electrification and domestic energy for cooking. While there are other factors that contributed to the national

poverty alleviation, rural electrification programme comes closest in linking the energy-poverty nexus. A study

concluded that in general, as electrification progresses, poverty tends to decrease. Starting as a security

programme for lighting villages during the emergency (prior to independence 1957), rural electrification has

graduated into an important component of rural development for uplifting the welfare of the rural population.

The programme has the potential to bring about economic empowerment of the poor via employment and

involvement in agriculture, rural industries, SMEs and energy-based entrepreneurships and also improving

education and health. However, there still remaining pocket of electrified households which will be connected

by end of 2015. At date, rural electrification has successfully penetrated 99% of the country, 100% in

Peninsular, 85% in Sabah and 90% in Sarawak. Further expansion of the rural electrification will have to focus

in Sabah and Sarawak. The lesser penetration rates in Sabah and Sarawak are mainly due to physical and

geographical constraints which entail heavy investments and also the relatively small electricity market due to

the sparsely populated rural areas. The establishment of MESITA in 1997 has successfully catalyzed the rural

electrification. Managed by MEGTW, it is an innovative trust fund where all the major IPPs in the Peninsular

Malaysia and Sabah contribute about 1% of their annual pre-tax profit for rural electrification (including

promotional activities), RE/EE projects and training. It is noted that by the year 2002, a total of USD 100 million

has been disbursed and has successfully benefited more than 250,000 households. Starting in 2010,

PEMANDU with MRRD, has started the Government Transformation Programme Rural Basic Infrastructure

initiative (RBI) which as date, has benefitted more than 50,000 households under the rural electrification

programme. On domestic energy, use of clean energy such as LPG, kerosene (for cooking and heating) is

widely available and sold in the groceries and fuel stations.

Energy efficiency has been in national policy, albeit broadly, since the 7th

Malaysia Plan. The energy

objective of providing efficient utilization of energy serves as the guiding principle of energy efficiency

programme in building, industrial and commercial sectors. The Efficient Management Of Electrical

Energy Regulations 2008, under “Electricity Supply Act 1990” require premises which consume more

than 3,000,000kWh over a period of 6 months, to submit status reports to the Energy Commission,

Malaysia including the establishment of an energy management system. The government is currently

exploring the possibility of establishing a revised National EE Master Plan including an Act to spearhead

EE further. Under the Economic Transformation Programme, PEMANDU together with MEGTW, has

launched the SAVE programme as part of a nation-wide market transformation exercise towards the use

of energy efficient appliance. The government has started its long journey on the subsidy rationalization

programme which eventually will lead to market-based energy pricing in Malaysia.

The passing of the RE Act and the establishment of Sustainable Energy Development Authority (SEDA) has strongly supported Government’s RE agenda. Feed-in-Tariff is currently seen as the most feasible way to promote the use of RE sources in the national generation mix. SEDA’s role is to administer and manage the implementation of the feed-in tariff (FiT) mechanism where the resources focused as now are biomass, biogas, mini-hydropower and solar energy. The response has been encouraging where almost all quotas for solar until 2014 has fully taken up. According to the planned, Malaysia expects to connect 985MW (5.5%) of RE generation capacity by 2015. Institutional set-up for SE4ALL has been matured and it would be natural for central agency like EPU to continue providing direction support on the progress of the targets. MRRD shall be the lead agency for the

6

Universal Access while MEGTW shall be the focal point for EE and RE initiatives. MGTW, the ministry responsible in the development of energy planning and implementation, acts as the guardian for MESITA funds where it works hand-in-hand with MRRD and TNB to continue rural electrification programme by various means. MRRD is responsible for planning and implementation of rural infrastructures development policies, including rural electrification. TNB, as the main utility company is responsible for generation, transmission and distribution of electricity in Peninsular Malaysia. SESCO and SESB are responsible for the same in Sarawak and Sabah respectively.

In conclusion, Malaysia will face no major challenges implementing the three SE4ALL goals if it continues on its

chosen path. In terms of energy access, 99.4% of the country is already electrified and the remote areas shall soon

be connected with the implementation of programs that achieved 310% more electricity connections in 2010-2012

than during the previous period. Regarding EE, the government has launched many projects that will allow Malaysia

to achieve the SE4ALL goal by 2015. Lastly, the 10th

Malaysian Plan aims to increase fivefold the share of

renewable energy sources in the energy mix (to 5.5%) by 2015. Through these efforts to promote a greener, more

efficient and more connected country, Malaysia is to achieve high-income status by 2020. Malaysia has achieved or

is on track to attaining the Millennium development goals (MDGs) at aggregate level by 2015. The primary energy

source for Malaysia comes from natural gas at 43.3% followed by crude oil at 35.5%. Malaysia is a significant net

exporter of natural gas, primarily in the form of liquefied natural gas (LNG). The National Energy policy of 1979

focuses on three different objectives to deal with the energy situation in Malaysia and it encompasses the supply,

utilization and environmental issues surrounding energy.

7

SECTION I: INTRODUCTION

1.1 COUNTRY OVERVIEW

Basic socio-economic data for Malaysia

Population: 28.6 million a

GDP/capita: USD 6,637 a (USD 15,588.66 PPP )

b

Key economic sectors: Industry, Transport, Oil and Gas, Agriculture, Banking and finance.

Poverty rate (current and from 3.8% (2009) to 2.0% c

trend):

Main sources of income: Exports of oil and gas, manufacturing (electrical and electronics), palm oil and rubber FDI: US$ 7 billion

d

Demographic situation: 72.2% urban/27.8% rural, urbanization ranging from 35% to 90% (WB, 2010)

Sources: a: EPU MIEF2011, b: World Bank, c: EPU 10MP, d: UNCTAD Report2011 Malaysia is on track to achieving a developed country status by 2020. Malaysia is projected to be able to attain

the Millennium development goals (MDGs) at aggregate level by 2015. The MDGs consist of 8 different goals

and they are to: eradicate extreme poverty and hunger; achieve universal primary education; promote gender

equality and empower women; reduce child mortality; improve maternal health; combat HIV/AIDS, malaria and

other diseases; Ensure environmental sustainability; and develop a global partnership for development.

Furthermore efforts have been carried out to raise the living standards of low-income households through

greater interagency coordination and improvements in application processes.

Malaysia has experienced three decades of impressive economic and social progress, enabling it to provide

for the health and education of its people, to eradicate poverty in large measure, to build excellent

infrastructure and to become a major global exporter. The changing global landscape, financial and economic

pressures, free movements of human capital, environmental issues and profits affecting Malaysia’s progress

towards Vision 2020. Towards this end, both the New Economic Model and the Tenth Malaysia Plan, which

emphasize inclusive growth, aspire to provide equal opportunities to all Malaysians. Apart from eradicating

poverty, priority will be on increasing the coverage of basic infrastructure such as roads, electricity (universal

assess) and water supplies, and communication networks. Health-care access, coverage and quality will

continue to be improved. In meeting its voluntary commitment of reducing greenhouse gases and to ensure

the sustainability of the environment (including conservation and sustainable use of natural resources),

emphasis will be placed on using renewable energy and on increasing energy efficiency through new

guidelines, standards, laws and incentives, which in directly support the SE4ALL objectives.

8

1.2 ENERGY SITUATION

1.2.1 Energy Supply (energy mix, export/import, electricity sector) Primary Energy Sources

ktoe

Hydropower

Coal and Coke

Crude Oil

Natural Gas*

Petroleum Products &

Others

Source: NEB 2009

The primary energy source for Malaysia comes from natural gas at 41% followed by crude oil at 40.1%

(2009). Its total primary energy supply registered at 74,582 ktoe, a decline of 1.2 percent compared to

72,384 ktoe during the previous year. The decrease was led by lower primary production of natural gas

and crude oil in 2009. This was anticipated also by decreasing imports of total energy due to unattractive

energy demand during the period. Malaysia has one of the most extensive natural gas pipeline networks

in Asia, owing to the multi-phased peninsular Gas Utilization (PGU) project that was completed in 1998.

Natural gas in Malaysia is mainly utilized for electricity generation through natural gas fired power plants,

petrochemical and large industrial uses, and motor vehicles. Upstream industries

The country’s crude oil and condensate reserves amounted to 5.517 billion barrels in 2009. The average

production of domestic crude oil and condensate increased from 681,000 barrels per day (bpd) in 2000

to 658,800 bpd in 2009. Based on this production level, which is in line with the National Depletion

Policy, the reserves are projected to last for 15 years (ADB). Nearly all of Malaysia's oil comes from

offshore fields. The continental shelf is divided into 3 producing basins: the Malay basin offshore

peninsular Malaysia in the west and the Sarawak and Sabah basins in the east. Most of the country’s oil

reserves are located in the Malay basin and tend to be of high quality. Malaysia’s benchmark crude oil,

Tapis Blend, is of the light and sweet variety with an API gravity of 44° and sulfur content of 0.08 percent

by weight. More than half of total Malaysian oil production currently comes from the Tapis field in the

offshore Malay basin. Malaysian oil production has been gradually decreasing since reaching a peak of

862,000 bbl/d in 2004 due to its maturing reservoirs. Malaysia consumes the majority of its oil production

and domestic consumption has been rising as production has been falling. The government is focused

on opening up new investment opportunities by enhancing output from existing fields and developing

new fields in deep water areas offshore Sarawak and Sabah.

9

Gross natural gas production however has been rising steadily, reaching 2.7 Tcf in 2010, while domestic natural gas consumption has also increased steadily, reaching 1.1 Tcf in 2010, 42 percent of production. Downstream Industries Malaysia had about 538,580 barrels per calendar day (b/cd) of refining capacity at seven facilities as of

January 2011. PETRONAS went into refining and distribution in 1983 where it initiated the construction of

refineries at Malacca and at Kerteh in order to reduce its dependence on Royal Dutch/Shell's two refineries at

Port Dickson and Esso's refinery in Sarawak. Malaysia invested heavily in refining activities during the last two

decades and is now able to meet most of its demand for petroleum products domestically, after relying on the

refining industry in Singapore for many years. Petronas operates three refineries (259,000 b/cd total capacity),

while Shell operates two (170,000 b/cd total capacity), ExxonMobil operates one (86,000 b/cd), and Kemanan

Bitumen Co. operates another (23,750 b/cd). Kemanan Bitumen refinery largely produces bitumen from heavy

crudes. The Sabah Oil and Gas Terminal, under construction in Kimanis, Sabah, is expected to be completed

by the end of 2013. It will receive crude from offshore fields, process and distribute the products via a planned

310-mile pipeline linking Sabah with Bintulu, Sarawak. The terminal will have a processing capacity of 300,000

bbl/d of crude and condensate. By 1990, 252 service stations carried the PETRONAS brand, all but twenty

(20) on a franchise basis, and another fifty (50) were planned. Some were set up on grounds of social benefit

rather than of strict commercial calculation.

Electricity sector

Biomass Others

Hydro

Diesel 2%

0% 8%

5%

Oil

1%

Coal Gas

28% 56%

Oil

1%

Hydro

5% Coal

40% Diesel

1%

Other

2% Biomass

Gas 1%

Others

52% 0%

Installed Capacity (2010) Generation Mix (2010)

Source: NEB 2009 As of 2010, installed capacity amounted to 27,179 MW while the generation mix stands at 125,045 GWj where maximum demand was at 15,072 MW.

The Malaysian electricity sector has evolved tremendously for the past 60 years. The national utility (Tenaga

National Berhad) is currently involved in the generation, transmission and distribution of electricity business. In

Peninsular Malaysia, the Company is a major contributor to the total industry capacity through six thermal stations

and three major hydroelectric schemes. It also manages and operates the National Grid which links TNB power

stations and IPPs to the distribution network in the peninsula. The grid is connected to Thailand’s transmission

system in the north and Singapore’s transmission system in the south. In East Malaysia, TNB, through 80%-owned

subsidiary Sabah Electricity Sdn. Bhd. (SESB), manages the Sabah Grid and aims to provide electricity to 95% of

the state’s population by year 2013. TNB’s distribution network is managed through a comprehensive distribution

system, customer service centres and call management centres. Over the years, TNB has diversified from its core

business into the manufacture of transformers, high voltage switchgears and cables; the provision of professional

consultancy services; and architectural, civil, electrical engineering works and services, repair and maintenance. In

2005, TNB embarked on a 20-Year Strategic Plan which entails greater focus on green initiatives such as the

development of renewable sources of fuel, and more effective demand side management via energy efficiency.

These efforts complement the Government’s

10

carbon reduction agenda while also creating a foundation for sustainable energy for the future. Set up as the Central Electricity Board of the Federation of Malaya in 1949, TNB has powered national development efforts for more than 60 years by providing reliable and efficient electricity services.

1.2.2 Net Imports and Exports by Fuels Type

10,000

9,000

8,000 25,000

7,000 20,000

6,000

5,000 15,000

4,000

3,000 10,000

2,000

1,000 5,000

0

0

Coal & Crude Oil Petroleum Natural

LNG

Pet. Products Coal & Coke

Coke Products Gas

Energy Imports in ktoe (2009) Energy Exports in ktoe (2009)

Source: NEB 2009

Coal remains the highest imported fuel mainly for coal-fired power plants. The Liquefied Natural Gas

(LNG) and the crude oil are the largest exported. The majority of Malaysia’s oil exports go to markets in

Japan, Thailand, South Korea and Singapore. The LNG and natural gas products are mostly exported

to Japan, South Korea, and Taiwan. Malaysia is a significant net exporter of natural gas, primarily in

the form of liquefied natural gas (LNG). It was recorded in 2005 that Malaysia exported just over 1 Tcf

(trillion cubic feet) of LNG, mostly to Japan, South Korea, and Taiwan. In 2010, Malaysia exported

234,000 bbl/d of crude oil, down slightly from the 236,000 bbl/d exported in 2009. This was about 35

percent of Malaysia’s crude oil production. The Tapis blend is Malaysia’s major exported crude oil

because its high quality and low sulfur content commands premium prices. In 2010, Malaysia imported

205,000 bbl/d of lower-cost crude oil for processing at its oil refineries.

The production and export of Liquefied Natural Gas (LNG), however, has increased from 23,606 ktoe in 2009 from

22,277 ktoe in 2008 level. Malaysia was the third largest exporter of LNG in the world after Qatar and Indonesia in

2010, exporting over 1 Tcf of LNG, which accounted for 10 percent of total world LNG exports. Japan, South Korea, Taiwan, and China have supply contracts with Malaysia, and are the largest purchasers.

LNG is primarily transported by Malaysia International Shipping Corporation (MISC), which owns and

operates 27 LNG tankers, the single largest LNG tanker fleet in the world by volume of LNG carried. MISC is

62-percent owned by Petronas. The Bintulu LNG complex on Sarawak is the main hub for Malaysia's natural

gas industry. Petronas owns majority interests in Bintulu's three LNG processing plants, which are supplied by

offshore natural gas fields. The Bintulu facility is the largest LNG complex in the world, with 8 production

trains and a total liquefaction capacity of 1.7 Tcf per year following the debottlenecking completed at end-

2010, which raised overall capacity by 0.6 Tcf per year. Japanese financing has been critical to the

development of Malaysia's LNG facilities. Also in Bintulu is Shell’s gas to liquids (GTL) project which has a

production capacity of 14,700 bbl/d. Construction began on Petronas’ Sabah Oil and Gas Terminal (SOGT) in

Kimanis, Sabah in 2011 and is expected to be completed by the end of 2013. It will have a handling capacity

of 1.3 Bcf/d of natural gas per day from the Gumusat-Kakap, Malikai, and Knabalu offshore fields. It will upply

gas for domestic use in Sabah, largely for a new electric power plant slated for completion in 2014. A reported

11

500,000 cubic feet per day will be piped to the Bintulu complex to be exported as LNG. The Sabah-Sarawak Gas Pipeline project is part of this development. 1.2.3 Energy demand

Final Energy Demand in ktoe (1999 vs 2009)

Source: NEB 2009

Energy demands in the transport sector have been increasing swiftly in Malaysia due to improvements in

transportation. The rapid industrialization of the country in recent years has led to high economic growth,

which in turn has led to population growth and an accelerated ownership of motorized vehicles. The total

number of vehicles in the country have increased from about 5 million in 1991 to 19 million in 2009,

thereby registering an average annual growth rate of about 8% during this period. The growth in the

number of vehicles in the country has been faster than the growth in population.

Based on the National Energy Balance, Industrial sector is the main user of electricity in Malaysia with its

share of 44.9 percent from total consumption in 2009. The electricity consumption from the industrial sector

increased by 0.9 percent to register at 3,719 ktoe (43,220 GWh) compared to the previous year. The

consumption of electricity in the commercial sector also increased to reach 2,743 ktoe (31,857 GWh), boosted

by tourism activities following the expansion of new routes by airlines and various tourism promotional

activities organised during the year. The electricity consumption in the residential sector recorded an increase

of 7.4 percent to register at 1,792 ktoe (20,822 GWh). The electricity consumption from the rail transport

sector, however, decreased from 15 ktoe (173 GWh) in 2008 to 12 ktoe (163 GWh) in 2009.

12

1.2.4 Energy and Economic Development Share of energy sector in GDP

Source: ETP 2011

In 2009, the combined oil, gas and energy sectors represented 19 % of GDP equivalent to RM127 billion (USD 41 billion) while in 2015, it is expected that 11.1% of GDP equivalent to RM81.9 billion (USD 26.42 billion). In total, the national oil company, Petronas, provides about 40% of the revenue for federal budget in taxes, dividends and royalties.

Electricity and Economic Growth

120,000 600,000

100,000 500,000

80,000 400,000 Electricity

Consumption

60,000 300,000 (GWh)

GDP (RM mil)

40,000 200,000

20,000 100,000

0 0

Source: NEB 2009

The last 20 years have seen the growth of electricity in tandem with the growth of country’s GDP.

Industrial, commercial and residential sectors are the main users of electricity use and will continue to be

the critical sectors based on the current trend of increasing middle-income families as well the opening

up of new townships and construction of new commercial and residential buildings. The total electricity

consumption recorded a growth of 3.8% compared to the previous year to register at 8,286 ktoe (96,307

GWh). It is clear that the demand for electricity has seen a large increase the past 20 years or so. With

Malaysia’s urban population to reach 78% in 2030 from 63 % 2002, combined with high per capita GDP

growth of 3.4% per annum over the outlook period, it will lead to a change in lifestyle, where energy

consumption will be based mostly on commercial energy sources in the form of electricity (EPU 10MP).

13

1.2.5 Energy Strategy and Relevant Targets

Since independence in 1957, Malaysia has always strive in ensuring universal access to basic infrastructure (roads, electricity, treated water and basic sanitation). During the 10 Malaysia plan period, electricity supply coverage will be expanded through the grid extension and alternative systems such as mini hydro and solar hybrid. Coverage of electricity supply is expected to reach almost 100% in Peninsular Malaysia and 99% in Sabah and Sarawak by 2015.

Malaysia’s concerns on energy security for economic development started during the 1970s oil crisis. The

National Energy policy of 1979 was prepared and focuses on three different objectives: the supply, utilization

and environmental issues surrounding energy. The supply objective aims to ensure adequate, secure and

cost-effective supply of energy; the utilization objective aims to promote efficient utilisation of this energy and

discourage wasteful and non-productive patterns of energy consumption; and finally the environmental

objective aims to ensure factors pertaining to environmental protection are not neglected in production and

utilization of energy. In 1981, the Four-Fuel diversification policy was introduced, which strives to reduce the

over-dependence on a single fuel source; and to focus on four main sources of fuel, i.e. oil, hydropower,

natural gas and coal. To strengthen further, the Fifth-fuel policy was introduced in 2000 which focuses on

incorporating renewable energy as next available fuel for power generation; and expanding fuel sources to

comprise, hydropower, natural gas, coal and renewable energy. Other related policies includes 1974

Petroleum Development Act (establishment of Petronas), 1975 National Petroleum Policy, 1980 National

Depletion Policy, 1990 Electricity Supply Act, 1993 Gas Supply Acts, 1994 Electricity Regulations, 1997 Gas

Supply Regulation and the 2001 Energy Commission Act.

In 2010, the Renewable Energy Action plan was formulated to intensify the development of grid-connected renewable energy, particularly biomass, as the 'fifth fuel' resource under the country’s Fuel Diversification and Fifth-fuel Policies. REAP provides potential targets for RE in Malaysia where more than 6,500 MW can potentially be generated from solar PV: 1,340 MW by 2030 from biomass; 410 MW by 2028 from biogas; 490 MW from mini-hydro by 2020 and about 360 MW by 2022 from Solid waste. Arising from the needs of a dedicated regulation on RE, the RE Act and the Sustainable Energy Development Authority (SEDA) Act were successfully gazetted in 2010 which leads to the official starting of the Feed-in-Tariff mechanism for RE projects in December 2011. It is expected that that renewable energy to reach 985 MW (5.5%) by 2015 and 2,080 MW by 2020.

The New Energy Policy (2011-2015) emphasizes energy security and economic efficiency as well as environmental and social considerations. The Policy will focus on five strategic pillars: initiatives to secure and manage reliable energy supply; measures to encourage energy efficiency (EE); adoption of market-based energy pricing; stronger governance and managing change.

EE initiatives will gain momentum with the finalization of the National Energy Efficiency Master Plan expected to be in 2012, setting of minimum energy performance standards for appliances and development of green technologies. These measures will encourage industries and consumers to use energy productively and minimize waste to be more competitive in the global market.

14

SECTION 2: CURRENT SITUATION WITH REGARDS TO SE4ALL GOALS

2.1 ENERGY ACCESS vis-à-vis GOAL OF SE4ALL

2.1.1 Overview and assessment Rural electrification rate and availability of clean domestic energy (for cooking mainly) will be used in the

context of preparing this Rapid report. As at date, rural electrification has successfully penetrated 99% of

the country, 99.5% in Peninsular Malaysia, 77% in Sabah and 76% in Sarawak. Fossil fuel such as LPG

and kerosene for cooking is available in the market and widely sold in the groceries, supermarkets and

selected gasoline stations. Nevertheless, fuel wood is still being used in some area especially in remote

Peninsular and in highlands of Sabah and Sarawak, where it can be found easily and without cost.

Malaysia has still a large number of small villages and islands, mainly in Sabah and Sarawak that lack 24-hour

electricity, and the probability of connecting them to high voltage gridlines in the near future is poor due to

geographical issues and many other logistical constraints. No exact record on the remaining gaps to cover but

it is estimated nearly 300,000 households are still without 24-hour electricity as per DOS statistic in 2005,

mainly in Sabah and Sarawak. Nevertheless, the government has embarked on several initiatives to find

sustainable ways to cater for the electricity demands of these poor rural villages. Solar home system (SHS) (of

150W less) has been installed in various remote locations since 1990 where a total installed capacity as date

is nearly 2MW in capacity. Solar diesel PV hybrids have been initiated by TNB-Energy Services since the year

2001 in Pekan, Pahang including several islands in Peninsular Malaysia.

Approach to providing 24-hour electricity supply is similar to providing clean and treated water, the

process of adding new power connections across Malaysia involves connecting to grid-based electricity

or implementing solar hybrid systems. The type of new connection hinges upon population density and

the remoteness of a location. The preferred mode of supplying electricity would be to connect to the

electricity grid. However, in rural areas which are very far from any transmission infrastructure, or in

instances where connections to the main grid are very expensive, technologies such as solar hybrid

power generation or micro hydro-electricity are introduced. In the year under review, these alternative

approaches helped ensure the provision of electricity to more villages in rural areas.

Malaysia has matured institutional set-up in the energy industries, covering the oil and gas sector to the

electricity segment. The Economic Planning Unit (EPU) has the overarching responsibility towards energy

policy and planning, both for conventional and non-conventional sources of energy, and poverty reduction in

Malaysia. The Ministry of Rural and Regional Development (MRRD) and the Ministry of Energy, Green

Technology and Water (MEGTW), work in close coordination for the rural electrification programme. In

addition the MEGTW works in tandem with the Energy Commission (EC) and the Sustainable Energy

Development Authority (SEDA) to coordinate national programmes in energy efficiency and renewable energy.

2.1.2 Modern energy for thermal applications (cooking, heating) Availability/quality of supply including status of domestic supply chain: Domestic energy for cooking comes in the form of Liquefied Petroleum Gas (LPG) is sold openly and is

available in many shops in the rural area. Fossil fuel such as gasoline (for transportation) and kerosene

(use for cooking and lighting) is widely sold and can be bought easily even in the un/semi-electrified

places (such as in deep rural in the state of Sabah and Sarawak). On the other hand, traditional fuels

(especially wood) are also popular and still being used considering its abundance in the area.

15

LPG in Malaysia is widely used in households for heating appliances such as ovens and stoves It is also used

in industries such as iron and steel industry, aerosol propellant industry, glass and ceramic manufacture,

copper tubing and cable manufacture. For cooking, it comes in three cylinder sizes which are the 12, 14 and

50 kg cylinders. The 12, 14 and 50 kg cylinders are painted according to the manufacturers’ specification

(yellow for Shell, Green for Petronas and Blue for Esso). In 2009, LPG accounted for 2.9% of the total

production of oil refinery, 10.4% of the total demand and 6% of the final consumption for petroleum products. Affordability Gasoline and LPG are under government’s controlled items and sold with subsidized price. In 2012, the price is as below

RM 1.90 (USD 0.61)/L for RON 95; RM 2.10 (USD 0.677/L for RON 97; RM 1.80 (USD 0.58) /L for Diesel; RM 1.90 (USD 0.61) /kg for LPG

Use of subsidy allows energy prices to be managed within the affordability level of the majority Malaysians. Average monthly household expenditure of, as below, shows that the cost of total energy is below 5% of the average monthly income.

Average Monthly and Share of Household Expenditure for Urban and Rural, 2004/05

Expenditure group Total (RM)

Urban Rural (RM)

Urban share of Rural share of

(RM) expenditure (%) expenditure (%)

Housing, Water, 429.57 522.3 247.4 22.86 19.01

Electricity

Electricity 59.33 71.38 35.62 3.12 2.74

Gas 9.27 8.84 10.13 0.39 0.78

Liquid Fuels 0.19 0.08 0.4 0.004 0.03

Other Fuels 0.44 0.15 1.01 0.01 0.08

(Source: DOS)

Pattern of Household Expenditure on Fuels in 2005

Share of households without access to modern cooking/heating is estimated to be 0.5% mainly using forest products. Population without electricity is estimated to be 200,000 as of 2011.

16

Subsidies: Continuing from the above Affordability section, below is the detail subsidy structure:

Fuel type Consumer price/L Price without subsidy/L Share of subsidy in (RM) (RM) retail price

RON95 1.90 2.93 35% Diesel 1.80 2.66 32%

LPG (for 14kg unit) 26.60 48.02 45%

Domestic energy has generally enjoys 30 to 40% subsidy from the government in ensuring the sold price

are within the reach of the mass. These energy subsidies may be direct cash transfers to producers,

consumers, or related bodies, as well as indirect support mechanisms, such as tax exemptions and

rebates, price controls, trade restrictions, and limits on market access. The subsidies makes the fuel

more affordable as it ensures adequate domestic supply by supporting indigenous fuel production in

order to reduce import dependency, or supporting overseas activities of national energy companies.

2.1.3 Access to electricity: Physical access:

Grid connection: 99.7 % of population in Malaysia Urban/rural areas: 99.5% in Peninsular Malaysia, 77% in Sabah and 76% in Sarawak in 2009 Target group: The remote areas in Peninsular Malaysia, islands and the states of Sabah and Sarawak.

Generally, major populated areas are connected to efficient grid systems as below.

Source: Energy Commission Rural Electrification Programme Since the 1950s, rural electrification has been promoted as part of rural development programme to bring

about security and physical development to the rural areas in the then Malaya. Rural electrification of

villages, implemented through the then Central Electricity Board was initially supplied using diesel

generators, mainly for security reasons in the fight against communist insurgencies. Rural electrification

has since been incorporated as part of rural development programme and received allocation under its

Five Year Development Plans, beginning from the First Malaya Plan (1960-1965) and later in the First

Malaysia Plan (1966-1970) up to the present Tenth Malaysia Plan (2010 - 2015).

The rural electrification programme is aimed at providing electricity supply to homes and villages, which are beyond

the operational areas of the local authorities, including the ‘orang asli’ in Peninsular and the indigenous groups of

Sabah and Sarawak by means of extending the grid lines, provision of generator sets and use of alternative energy

such as SHSs and solar-hybrid system. Rural electrification forms part of efforts to

17

provide social amenities to enhance the quality of life and living standards among the rural communities. Priorities for rural electrification programme will be to provided transmission lines best to 33kV lines, low voltage line to the villages and to upgrade infrastructure of 12 hours to 24 hours electricity supply.

Since 1970s, rural electrification has been incorporated in the New Economic Policy (NEP) framework for

eradicating poverty and increasing the quality of life in the rural areas, especially of the rural poor.

Increasing use of electricity is expected to increase productivity and incomes in the agriculture, industry

and commercial sectors and also affect the modernization and attitudinal change in the rural sector.

Qualifying Criteria for different types of Electrification Programme

Extension of Grid

Generator Set SHS Solar-Hybrid system

Lines

Priority will be Easy assess to the No proper road Nearest 11kV

given to villages site via roads or leading to the area overhead line is

which have high rivers Will not be more than 10 km

population and Nearest grid lines receiving any grid No plan for grid

available public are more than line extension in connection in the

amenities such as 10km away the next 5 years next 3 years

schools, clinics and Will not be Public amenities Depending on

religious centres. receiving any grid will be given locations where

Average cost for line extension in priority project cost is

the project is the next 5 years No potential for cheaper than grid

estimated around Average cost for mini/micro hydro extension

RM25,000 (USD the project is system Clustered housing

8,065) per house estimated to be For housing unit, units with at least

around RM15,000 maximum output is 20 homes will be

(USD 4,839) per 100-150W capacity given priority.

house Maximum output

shall be 50kW

capacity

Source: MRRD / MESITA

Current Approach to Rural Electrification Programme under PEMANDU NKRA Rural Basic Initiatives: Rural development continues to be a fundamental component of the national agenda. Since Independence,

the government, via the many Malaya and Malaysia Plans, as above, has rolled out development initiatives for

roads, water, electricity and housing to ensure that the fruits of modernisation benefit all. In 2010, the Rural

Basic Infrastructure (RBI) NKRA was conceived to accelerate these efforts by delivering unprecedented big

and quick wins to rural communities. In 2011, the MRRD and the various implementing agencies were once

again tasked with spearheading RBI efforts. They continued to build upon the good momentum achieved in

the previous year and the rural landscape was further transformed for the better. Their efforts centred on

ensuring improved accessibility via new and upgraded roads, providing a clean, constant water supply and an

uninterrupted electricity supply, as well as building and refurbishing homes for rural communities. In 2010 and

2011 alone, a total of 54,222 houses have been benefitted under this programme. In 2012, it is targeted to

achieve 39,442 houses with allocated budget of RM 1 billion (USD 323 million).

18

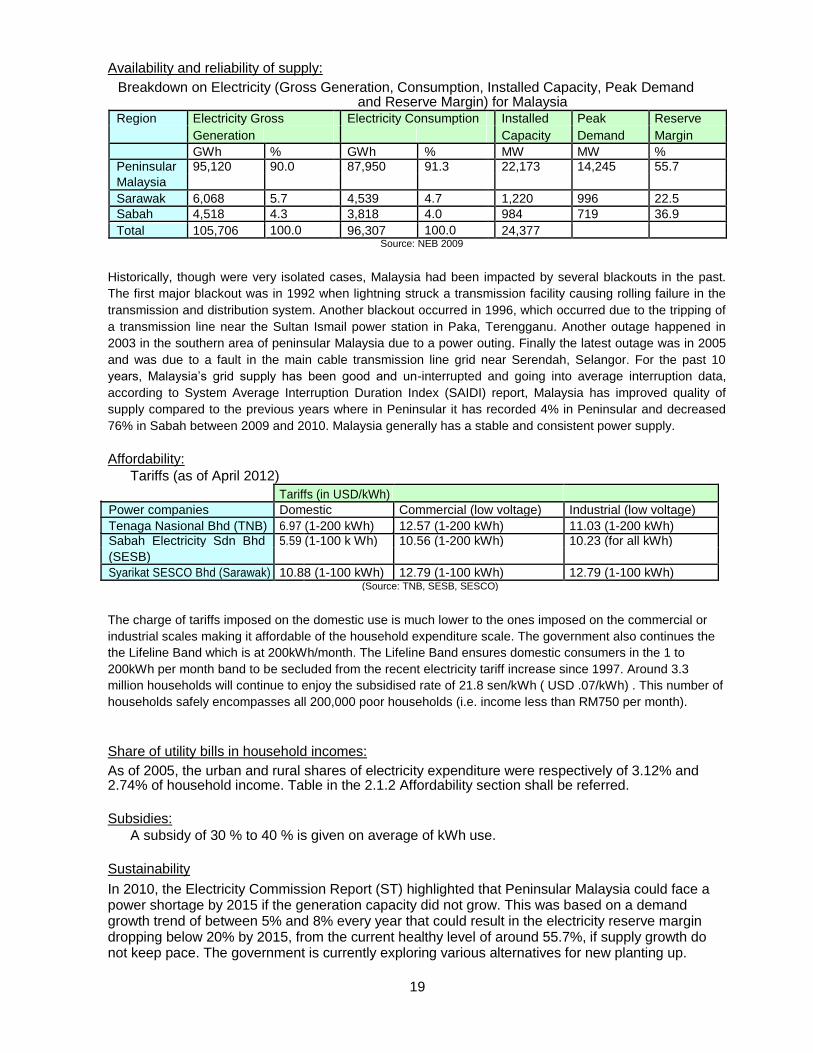

Availability and reliability of supply: Breakdown on Electricity (Gross Generation, Consumption, Installed Capacity, Peak Demand

and Reserve Margin) for Malaysia Region Electricity Gross Electricity Consumption Installed Peak Reserve

Generation Capacity Demand Margin

GWh % GWh % MW MW %

Peninsular 95,120 90.0 87,950 91.3 22,173 14,245 55.7

Malaysia

Sarawak 6,068 5.7 4,539 4.7 1,220 996 22.5

Sabah 4,518 4.3 3,818 4.0 984 719 36.9

100.0

100.0

Total 105,706 96,307 24,377

Source: NEB 2009

Historically, though were very isolated cases, Malaysia had been impacted by several blackouts in the past.

The first major blackout was in 1992 when lightning struck a transmission facility causing rolling failure in the

transmission and distribution system. Another blackout occurred in 1996, which occurred due to the tripping of

a transmission line near the Sultan Ismail power station in Paka, Terengganu. Another outage happened in

2003 in the southern area of peninsular Malaysia due to a power outing. Finally the latest outage was in 2005

and was due to a fault in the main cable transmission line grid near Serendah, Selangor. For the past 10

years, Malaysia’s grid supply has been good and un-interrupted and going into average interruption data,

according to System Average Interruption Duration Index (SAIDI) report, Malaysia has improved quality of

supply compared to the previous years where in Peninsular it has recorded 4% in Peninsular and decreased

76% in Sabah between 2009 and 2010. Malaysia generally has a stable and consistent power supply. Affordability:

Tariffs (as of April 2012) Tariffs (in USD/kWh)

Power companies Domestic Commercial (low voltage) Industrial (low voltage) Tenaga Nasional Bhd (TNB) 6.97 (1-200 kWh) 12.57 (1-200 kWh) 11.03 (1-200 kWh) Sabah Electricity Sdn Bhd 5.59 (1-100 k Wh) 10.56 (1-200 kWh) 10.23 (for all kWh) (SESB)

Syarikat SESCO Bhd (Sarawak) 10.88 (1-100 kWh) 12.79 (1-100 kWh) 12.79 (1-100 kWh) (Source: TNB, SESB, SESCO)

The charge of tariffs imposed on the domestic use is much lower to the ones imposed on the commercial or

industrial scales making it affordable of the household expenditure scale. The government also continues the

the Lifeline Band which is at 200kWh/month. The Lifeline Band ensures domestic consumers in the 1 to

200kWh per month band to be secluded from the recent electricity tariff increase since 1997. Around 3.3

million households will continue to enjoy the subsidised rate of 21.8 sen/kWh ( USD .07/kWh) . This number of

households safely encompasses all 200,000 poor households (i.e. income less than RM750 per month). Share of utility bills in household incomes: As of 2005, the urban and rural shares of electricity expenditure were respectively of 3.12% and 2.74% of household income. Table in the 2.1.2 Affordability section shall be referred.

Subsidies:

A subsidy of 30 % to 40 % is given on average of kWh use. Sustainability In 2010, the Electricity Commission Report (ST) highlighted that Peninsular Malaysia could face a power shortage by 2015 if the generation capacity did not grow. This was based on a demand growth trend of between 5% and 8% every year that could result in the electricity reserve margin dropping below 20% by 2015, from the current healthy level of around 55.7%, if supply growth do not keep pace. The government is currently exploring various alternatives for new planting up.

19

Share of renewable energy sources (RES) in power mix: Share of sustainable biomass and other RES:

Type of RE Capacity of generated energy connected to the grid (MW)

Biomass 30 Solid waste 5.5

Biogas 2 Mini hydro 2

Solar PV 1 Others (wind) 23.5

64

As for 2010, RES accounted for less than 1% of total generated electricity.

20

2.2 ENERGY EFFICIENCY vis-à-vis GOAL OF SE4ALL

2.2.1 Overview and Assessment

Energy efficiency (EE) measures (including demand side management) have been ongoing since the 7th

Malaysia Plan period (1996-2000) and in 10 Malaysia Plan, it has been intensified to harness energy

savings potential and reduce Malaysia’s carbon emissions and dependence on fossil fuels. Intrinsic

barriers to energy efficiency that pose challenges in capturing this opportunity are being addressed. EE

covers the efficiency of power generation, transmission and distribution of electricity as well as various

end uses of energy such as in the industrial, commercial and residential. In other words it can be divided

into supply and demand side perspectives. In the recent 10th Malaysia Plan (2011-2015), the key

emphasis is on the short-term goals vested in National Green Technology Policy (2009), these include

promotion of EE for power producer, establishment of EE targets and standards.

The Efficient Management Of Electrical Energy Regulations which was launched in 2008, under “Electricity Supply Act 1990” require premises which consume more than 3,000,000kWh over a period of 6 months, to submit status reports to the “Energy Commission”, Malaysia including the establishment of an energy management system. The government is currently exploring the possibility of establishing a revised National EE Master Plan including an Act to spearhead EE further. PEMANDU together with MEGTW, has launched the SAVE programme as part of a nation-wide market transformation exercise towards the use of energy efficient appliance.

There are a number of completed and ongoing projects which will support national EE programme such

as the DANIDA Capacity building in integrated resources planning at government and related agencies,

DANIDA’s Center on Training on EE & RE (CETREE) Capacity building project, MEGTW Low Energy

Office (LEO) at Putrajaya; TNB’s Demand Side Management, Green township, JICA’s Low Carbon

Society (LCS) in Iskandar Development Region, UNDP /GEF Malaysia Industrial Energy Efficiency

Improvement Project and the UNDP/GEF Building Sector Energy Efficiency Project (BSEEP).

SAVE or Sustainability Achieved via Energy Efficiency, is a program spearheaded by the Ministry of

Energy, Green Technology and Water to improve energy efficiency in Malaysia. It is launched in 2011 as

a quick start programme to encourage residential users to change into energy efficient appliances when

making new purchases. It is to create a culture of efficient energy usage among general public and

business entities. This initiative targets the final end user through the retailers of electronic appliances

and it is targeted to provide national savings up to 7,300 GWh of energy saved by the year 2020. It is

also to accelerate the transformation of the consumer appliances market to increase the share of Energy

Efficient (EE) models and to phase out inefficient models from the local market so as to reduce the price

premium for EE products. 100,000 rebate vouchers for 5-Star rated refrigerators and 65,000 vouchers for

5-Star rated air conditioners have been allocated to states across Malaysia. Rebates will be awarded on

a first-come, first-served basis to qualified domestic consumers who purchase 5-Star rated refrigerators,

air conditioners or chillers during the rebate offer period through participating retailers. As date, over

more than 4,000 retail outlets nationwide are registered with KeTTHA under the SAVE Rebate Program,

with 12 different brands to choose from. The rebate program starts on July 7, 2011 and will last until all

rebates are taken at the end of 2012. To date, about 12.4 per cent and 7.1 per cent of market share of

five-star rated energy efficient refrigerators and air conditioners respectively have been recorded through

the initiatives being implemented, with total energy saving accumulation of 66.3 GWh.

Under the PEMANDU Energy, Oil and Gas cluster, EPP9, Malaysia will focus on five relevant levers to improve EE which are,

1. to lead by example on energy-efficiency practices and philosophy, 2. to stimulate sales of energy-efficient appliances, 3. the Government will work with TNB to make co-generation economically viable,

21

4. to regulate better insulated buildings and 5. to stimulate the sale of energy-efficient vehicles.

In March 2011, it was announced that Faber Group Berhad will spearhead the pilot project for the Energy Performance Management System (EPMS) for government entities. Faber has commenced and completed energy audits at five hospitals in the northern states of Peninsular Malaysia. To stimulate the use of fuel efficient cars, the import duty on all hybrid cars has been exempted, bringing the cost of hybrid models such as the Toyota Prius and Honda Insight to more competitive levels. Sales of hybrid cars are expected to achieve record highs in 2011. This exemption was extended to the end of 2013 in the recent Budget 2012 announcement. The implementation of Energy Performance Contracting (EPC) in 120 top energy- using government buildings will be further explored for implementation in all government buildings and private properties.

2.2.2 Energy intensity of national economy:

(Source: 2010 MDG report)

2.2.3 Industrial Energy Intensity Industrial Energy Intensity stands at 78 toe/RM million in 2009 (NEB 2009)

Under the Malaysian Industrial Energy Efficiency Improvement Project (MIEEIP) from 2000-2007 which was

funded by United Nations Development Program (UNDP), Global Environmental Facility (GEF), private sector

and Government of Malaysia, eight industrial sectors, cement, ceramic, food, glass, iron & steel, pulp & paper,

rubber and wood has been identified to have the potential to promote and improve energy efficiency. Electrical Energy- use Equipment has been produced to give a the guidelines to encourage industries to

adopt energy efficiency practices and improving their energy utilization for a commonly used equipment

such as fans, motors, pumps, chillers, transformers and air-compressors. A standard general energy

audit guideline, the Industrial Energy Audit Guidelines shall be used as a reference material by energy

consulting firms in their audit services to industries. There are 54 energy audits in the eight industrial sub

sectors under MIEEIP. The project has highlighted a number of important issues and some significant

lessons have been learnt. The experiences and the outcomes in the form of industry involvement and the

demonstration models will provide exemplars for further steps in energy efficiency throughout Malaysia.

2.2.4 Residential Energy Consumption Residential Energy Consumption is at 3042 ktoe in 2012 (NEB 2009).

EE appliances which participated in the voluntary rating programme are Refrigerators, Domestic Electric Fans, Ballast for Fluorescent Lamps, Electric Lamps, Air Conditioners (Split Unit), Televisions, High Efficiency Motors and Insulation Materials. Out of these eight appliances only four (4) appliances have participated in the voluntary ‘star labelling’ programme (as below) which are televisions, refrigerators, Domestic Electric Fans and Air Conditioners (Split Unit).

22

Sample of a Malaysian voluntary labelling programme

2.2.5 Potential cumulative energy savings by 2015 The 10 Malaysia Plan estimated that there would be a potential cumulative energy saving of 4,000 ktoe by 2015.

As explained, the national energy efficiency master plan will be drawn up and measures such as phasing out incandescent light bulbs and requiring more devices to have EE labelling will be introduced. In addition, there will be a ratings system for green townships, led by Putrajaya and Cyberjaya, along with minimum energy performance standards for equipment and machinery.

23

2.3 RENEWABLE ENERGY vis-à-vis GOAL OF SE4ALL

2.3.1 Overview and Assessment Policy on renewable energy (RE) has been mainstreamed and recognised as early in the year 2000. The advent of

the Fifth fuel policy has further reinforced Malaysia’s position in developing the RE industries. It was initially targeted

to contribute 5% of the country’s electricity demand by year 2005 and the Small Renewable Energy Program (SREP)

was launched in May 2001 under the initiative of the Special Committee on Renewable Energy (SCORE) aimed to

support the government’s strategy in intensifying the development utilization of RE, where by 2005, equal to between

500 and 600 megawatt (MW) of installed capacity to be made available. The policy has been reinforced by fiscal

incentives, such as investment tax allowances and accelerated capital allowance which encourages the connection

of small renewable power generation plants to the national grid.

The buy-back tariff started with a fixed price from RM 0.17/kWh (USD 0.055 /kWh), RM 0.19/kWh (USD 0.062 /kWh) and finally RM 0.21/kWh (USD 0.067 /kWh). However, despite the efforts, RE pricing was seen still unattractive to compete with the level playing field with the fossil-fuel tariff and a need to restructure the RE industries was needed.

On 2nd April 2010, the Cabinet approved the National Renewable Energy Policy and Action Plan that

would be the cornerstone for a more aggressive deployment of RE in the country. The policy and

objectives of the National Renewable Energy Policy and Action Plan are to enhance the utilisation of

indigenous RE resources to contribute towards national electricity supply security and sustainable

socioeconomic development. Finally, in 2011, Malaysia’s Parliment gazzeted the Renewable Energy Act

(RE Act) and the Sustainable Energy Development Authority (SEDA) to spearhead the RE in Malaysia.

Its key role is to administer and manage the implementation of the feed-in tariff (FiT) mechanism where

the resources focused as of now are biomass, biogas, mini-hydropower and solar energy. Applications

for the FiT opened on 1 December 2011, with quota for solar photovoltaic cells of 150MW, biomass

(including solid waste) of 240MW, biogas (including landfill) of 90MW and small hydro of 150MW offered

to any interested party through an open online application system. The quota allocation for solar

photovoltaic up until 2014 was almost fully applied for within 24 hours of its launch, whilst applications for

quota allocation for biomass, biogas and small hydro have been similarly encouraging.

Installed Capacity (MW) of Plants in Progress

Year

Sm

all

Hyd

ro

Bio

mas

s (S

olid

Was

te

)

Ind

ivid

ua

l

Non

-indi

vidu

al (≤

500k

W)

Non

-indi

vidu

al (>

500k

W)

Hou

sing

Dev

elop

er

Bio

ga

s (

Land

fill /

Sew

age)

Bio

gas

Bio

ma

ss

Total

2012 8.36 5.38 9.2 8.9 33 6.53 2.37 61.02 0 134.75

2013 4 2.8 28.3 0 48.5 2.86 3.28 58.5 0 148.25

2014 0 0 42.05 0 6 0 0.79 30.53 0 79.37

Cumulative 12.36 8.18 79.55 8.9 87.5 9.39 6.45 150.05 0 362.37

Source: SEDA’s Website September 2012 Currently, electricity generation from RE sources is very costly and not competitive with large scale plants

using conventional fossil fuel sources. The higher cost per unit has made investment in RE not attractive to

investors and electricity utility. The objective of FiT is to spur RE growth in Malaysia. FiT will be used to

subsidise the difference between the premium tariff rate and the current selling price of a unit of electricity from

RE developers to TNB under the SREP programme (i.e. at a maximum price of 21 sen/kWh).

24

2.3.2 On-grid and off-grid renewable energy

Category Mini-hydro Biomass & biogas Solar PV Wind Total Grid-

connected 23.8 32 1 - 56.8

(MW)

Off-grid (MW) - 447 6.1 0.2 453.3 Total 23.8 479 0.2 7.1 510.1

On-grid and off-grid RE in MW, Source: Energy Commission 2010

RE Operational Capacity (source: SEDA’s website August 2012)

As RE Act has recently started in December 2011, progress on RE projects with FiT is relatively new and many still in planning and commissioning stage. As date, 43.90 MW capacity has been in operation. Use of renewable energy sources (RES) for thermal applications (cooking/heating) As date, there is no official record on Malaysia’s rural using RE for cooking and heating. Use of RES for productive activities As date, there is no official record on Malaysia’s industries using RE for cooking and heating. However, there

were research projects undertaken by the National University of Malaysia (UKM) and Malaysia Research and

Development on Agriculture Industries (MARDI) on the use of solar drying for agriculture products.

25

2.4 SE4All GOALS

2.4.1 Energy Access Malaysia is committed to ensuring universal access to modern energy services and providing 100% electricity to the rural area. Under the Government Transformation Programme, universal access is targeted to be achieved 2015. Targets for additional houses to be supplied with electricity are about 6,000 houses in Peninsular Malaysia, 59,000 houses in Sabah and 76,000 houses in Sarawak. 2.4.2 Energy Efficiency The National Energy Efficiency Master Plan, 2010 is a holistic implementation roadmap to drive efficiency measures across sectors with a target to achieve cumulative energy savings of 4,000 kilo ton of oil equivalent (ktoe) by 2015 according to the 10 Malaysia Plan.

2.4.3 Renewable Energy

The share of renewable energy sources in the electricity sector will be increased from less than one percent

today to 5.5% in 2015 (985 MW). The doubling of rate on the use of RE at the national context (based on

business-as-usual scenario and upon the successful introduction of FiT) may happen middle of 2013.

RE Generation Capacity Targets under FiT (MW)

Solid Solar Year Biogas Biomass Waste Hydro PV TOTAL 2011 20 110 20 60 9 219 2012 35 150 50 110 20 365 2013 50 200 90 170 33 543 2014 75 260 140 230 48 753 2015 100 330 200 290 65 985 2016 125 410 240 350 84 1,209 2017 155 500 280 400 105 1,440 2018 185 600 310 440 129 1,664 2019 215 700 340 470 157 1,882 2020 240 800 360 490 190 2,080 2025 350 1,190 380 490 455 2,865 2030 410 1,340 390 490 1,370 4,000

26

SECTION 3: CHALLENGES AND OPPORTUNITIES FOR ACHIEVING SE4ALL

GOALS

3.1 INSTITUTIONAL AND POLICY FRAMEWORK

3.1.1 Energy and development Energy in national development and poverty reduction strategies and plans Energy is an important factor to Malaysia’s economic growth, constituting about 20 per cent of the nation’s Gross Domestic Product (GDP). The Government plans to increase diversification of the energy industry, step up exploration for new oil and gas resources, enhance production from known reserves, and encourage the use of alternative energy sources such as solar, hydro-electric and even nuclear. The energy sector’s contributions to our GNI are expected to rise from RM110 billion in 2009 to RM241 billion in 2020. Hence, the energy sector needs to be more efficient and resilient to be able to deliver adequate and reliable energy supply to support our country’s rapid growth against a backdrop of depleting energy resources as well as escalating and volatile energy prices.

Trend: GDP vs Electricity Consumption

GD

P (

RM

Mill

ion)

600,000

500,000

400,000

300,000

200,000

100,000

0

1

1

8

6

4

2

There is a strong correlationship between the rate of electrification and the reduction of poverty level in

Malaysia, although it will only due to rural electrification factor alone. Strong poverty alleviation programme

especially in the beginning of 1970s together with extensive completion of rural basic infrastructure (roads,

water, sanitation, schools and clinics) including rural education have contributed to the success of the poverty

eradication programme. The rise of electricity consumption is in tandem with the growth of GDP. Energy governance:

Energy policy in Malaysia is set and overseen by the Economic Planning Unit (EPU), with close coordination

with the line ministries (MEGTW, on electricity matters) and agencies (i.e. Energy Commission and SEDA).

MEGTW regulates the non-oil and electricity sector (and gas energy and security sectors) while EC regulates

the energy supply activities and enforces energy supply laws. SEDA, is a newly set up statutory body formed

under the Sustainable Energy Development Authority Act 2011 whose role is to administer and manage the

implementation of the feed-in tariff mechanism mandated under the Renewable Energy Act 2011. Malaysia

Green Technology Corporation (MGTC) from time to time provides promotion, policy research and awareness

support to MEGTW related to green technology including RE and EE initiatives.

27

E P U PEMANDU / ICU /

- formulates overall policy on rural development State EPUs

- incorporates impacts of infrastructure Oversee

development to social and economic growth implementation

MEGTW

- guardian of the MESITA fund

- energy policy

EC:

MOE

MOH Regulates electricity MRRD

industry receives information on rural

- rural school

- rural clinic

SEDA: development programme

electrification

electrification

Administrator of RE Act

including rural electrification

MGTC: (basic infrastructure)

Energy R&D on EE /RE

PWD / TNB PWD / TNB PWD / TNB - project - project - project

SubContractors SubContractors SubContractors

- installations / - installations / - installations /

Linkages of Electricity Institutions related to Rural Electrification Projects

With respect to oil and gas industries, Petroliam National Berhad (PETRONAS), holds exclusive

ownership rights to all oil and gas exploration and production projects in Malaysia, for all licensing

procedures, and is subject to only the Prime Minister, who also controls appointments to the company

board. The company holds stakes in the majority of oil and gas blocks in Malaysia. It is the single largest

contributor of Malaysian government revenues, (over 40 percent in 2010), by way of taxes and dividends.

Malaysia's oil and gas policy has historically focused on maintaining the reserve base to ensure long

term supply security while providing affordable fuel to its population. In July 2010, the government

introduced subsidy reductions for gasoline, diesel, and liquid petroleum gas (LPG) with the aim of

gradually decreasing fuel subsidies to reduce expenditures. Further cuts in fuel subsidies are planned.

Generally, Malaysia plans for adoption of market-based energy pricing, in line with overall strategy to

rationalize subsidies where energy subsidies will be reduced, with the goal of achieving market pricing by

2015. Gas prices for the power and non-power sectors will be reviewed every six months to gradually

reflect market prices. A decoupling approach for energy pricing will be undertaken to explicitly itemize

subsidy value in consumer energy bills and eventually delink subsidy from energy use. For low-income

households and other groups for which the social safety net is required, different forms of assistance will

be provided. Malaysia also belives in the stronger governance of the energy sector where the goal to

raise productivity and efficiency. In this regard, the gas supply industry will be further liberalized to

facilitate the entry of new suppliers and third-party access arrangements. The electricity supply industry

will also be restructured to instil greater market discipline. 3.1.2 Thermal energy for households LPG industry in Malaysia is currently dominated by state owned Petronas followed by Shell and Esso among others while piped gas supply is regulated by the EC.

28

3.1.3 Power sector MEGTW is the responsible ministry and the utility are provided by the utility companies (TNB in Peninsular Malaysia, SESB in Sabah and SESCO in Sarawak. 3.1.4 Modern energy for productive sectors RE is poised to be connected with up to 5.5% of total generation mix by 2015. MEGTW is responsible on the execution of the RE Act policy while SEDA is to administer the FiT mechanism under the RE Act. 3.1.5 National monitoring framework for SE4ALL Proposed indicators to measure and monitor achievement of national SE4ALL goals Energy access indicators:

- Country rural electrification rate - Share of households with access to electricity/energy for cooking & heating

- Impacts of electricity to rural

people EE indicators:

- Average electricity consumption of households - Primary and final energy intensity by sector - Efficiency of total electricity generation - GDP / unit of Energy Used - Energy Used per capita

RE indicators:

- Share of renewables in gross electricity consumption - Share of renewables in electricity generating capacity - Share of households using modern energy for heating/cooking

Data requirements, gaps and associated capacity development needs Related to 3.5

29

3.2 PROGRAMS

3.2.1 Thermal energy Programme LPG for cooking has been widely used. As date, there is no program on the use of thermal energy from RE for domestic cooking and heating. Use of charcoal from biomass briquette is negligible.

For industrial usage, efforts are already on going on the use of RE sources from industrial by-products (i.e. wood chips, MDF waste, saw dust, empty fruit bunch) mainly for producing steam (low pressure/ high pressure) for manufacturing processes. Sustainability Research and development and pilot projects on briquette / pellet production especially from biomass palm oil waste (EFB/blended) and rice husk has already in existence. Commercial production has yet to be fully taken off. The processing cost is estimated at RM 150 per tonne and the selling price for export market at RM 600 to RM 700 per tonne. 3.2.2 Power sector Physical access (electrification) As at date, rural electrification has successfully penetrated 99% of the country, 99.5% in Peninsular Malaysia, 77% in Sabah and 76% in Sarawak (10 Malaysia Plan) Reliability (grid maintenance/upgrade) The utility companies (TNB, SESB, SESCO) has ongoing programme on ensuring continuous supply of power.

Sustainability (investment in renewable energy, on-grid and off grid, and energy efficiency) The advent of RE Act has allowed the use of RE sources for power generation. Refer 2.3 for details.

3.2.3 Energy efficiency programs

Sector Initiatives

Residential Phasing out of incandescent light bulbs by 2014 to reduce carbon dioxide emissions by an estimated 732,000 tons and reducing energy usage by 1,074 GW a year. Increasing energy performance labeling from four (air conditioner, refrigerator, television and fan) to ten electrical appliances (six additional appliances - rice cooker, electric kettle, washing machine, microwave, clothes dryer and dishwasher). Labeling appliances enables consumers to make informed decisions as they purchase energy efficient products. Robust tariff structures (“the more you use, the more you pay principle”) to encourage energy saving and avoid wastages. Encourages use of passive designs at home

Township Introduction of guidelines for green townships and rating scales based on carbon footprint baseline and promoting such townships starting with Putrajaya and Cyberjaya.

30

Implementation of the newly formulated Low Carbon City Framework (LCCF) to encourage less GHG emissions especially from energy usage Promotes energy efficient / multi modal public transport system

Industrial Increasing the use of energy efficient machineries and equipment such as high efficiency motors, pumps and variable speed drive controls. Encourages energy benchmarking among subsectors of industries Encourages the setting up of Energy Management Team to look into energy consumption and measures and Energy Manager Encourages the use of ISO 5000 energy Management System Mandatory reporting of the energy usage and its management plan for electricity users of 500,000kWh / year

Buildings Introduction of Minimum Energy Performance Standards for selected appliances to restrict the manufacture, import and sale of inefficient appliances to consumers. Promotes the use of rating tools such as the Green Building Index (GBI), LEEDS and CIDB Pass Promotes the Life-Cycle analysis (“cradle-to-cradle”) for building construction industries under Carbon Common Metric (CCM)

Transport Effective public transportation system

Use of Bus Rapid Transit in Iskandar Development Region (pilot phase) Source: EPU 10MP

3.2.4 Modern energy for productive use

Sector Initiatives, currently ongoing

Community Use of micro-hydro system for electricity generation Livelihood Use of solar hybrid for electricity generation

Solar home system (per household) for rural area Use of grid-connected solar PV system

Agriculture Use of solar drying in processing agriculture products (pilot stage) Use of micro-hydro system for pumps ( irrigation) Energy Supply On-grid: Introduction of feed-in-Tariff for wide spread electricity generation from

RE sources (biomass, biogas, PV, mini-hydro) Off-grid: promotes the use of hybrid-diesel, micro-hydro and wind

Industries Use of biomass/biogas for in-house electricity generation use Use of biomass/biogas for use in the manufacturing processes (heating)

Education Use of solar PV for rural schools for ICT and communication