Embed Size (px)

Citation preview

MANAGEMENT PROCESS

Planning

Organizing

Directing

Controlling

MANAGEMENT PROCESS

PLANNING

planning * Thinking ahead*making future* Projection

* Setup organizational structure, identify groupings, roles, relationships*establish policies and procedure, definite course of action and methods* Prepare budget/ allocate resourcesDevelop and schedule programs, define activities needed & set time frame* Set objectives / determine results desired* Forcecast / estimate future.

PLANNING

Importance of

planning

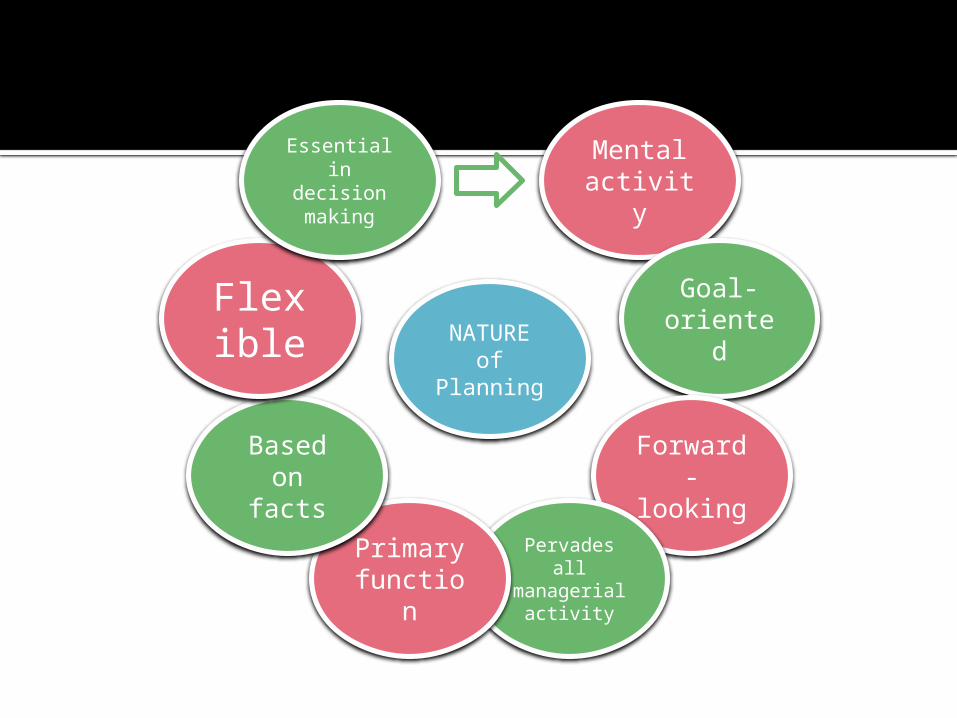

NATURE of

Planning

Mental activity

Goal-oriente

d

Forward-looking

Pervades all

managerial activity

Primary function

Based on facts

Flexible

Essential in decision

making

A well developed plan should:

Limitations

People’s resistanc

e

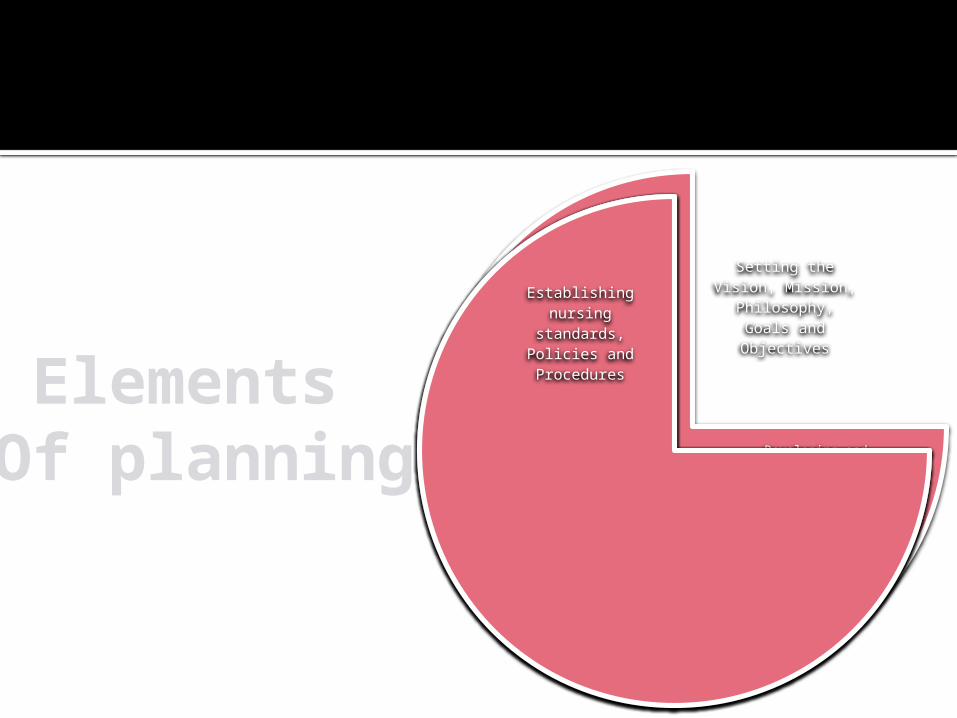

Setting the Vision, Mission,

Philosophy, Goals and Objectives

Developing and Scheduling Programs• The planning

formula• Time

Management

Preparing the Budget

Forecasting

Establishing nursing

standards, Policies and ProceduresElements

Of planning

Organizational purpose

•foundation upon which every successful business is built.•help you know what to include in your business as well as what is not to.•a unifying glue that binds each team member to one another.

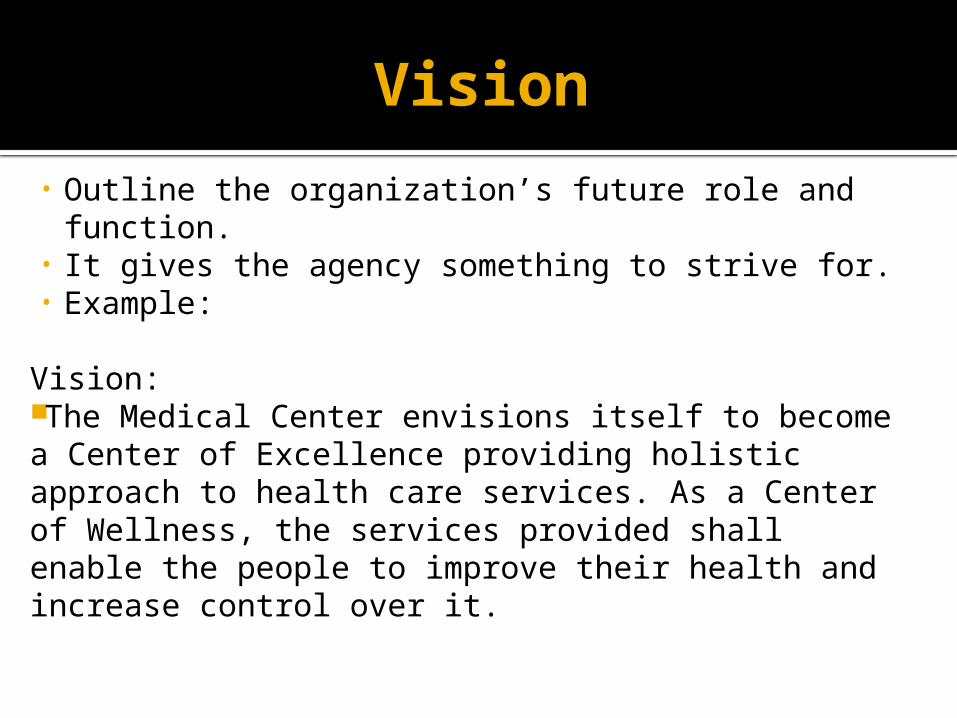

Vision

• Outline the organization’s future role and function.

• It gives the agency something to strive for.• Example:

Vision:The Medical Center envisions itself to become a Center of Excellence providing holistic approach to health care services. As a Center of Wellness, the services provided shall enable the people to improve their health and increase control over it.

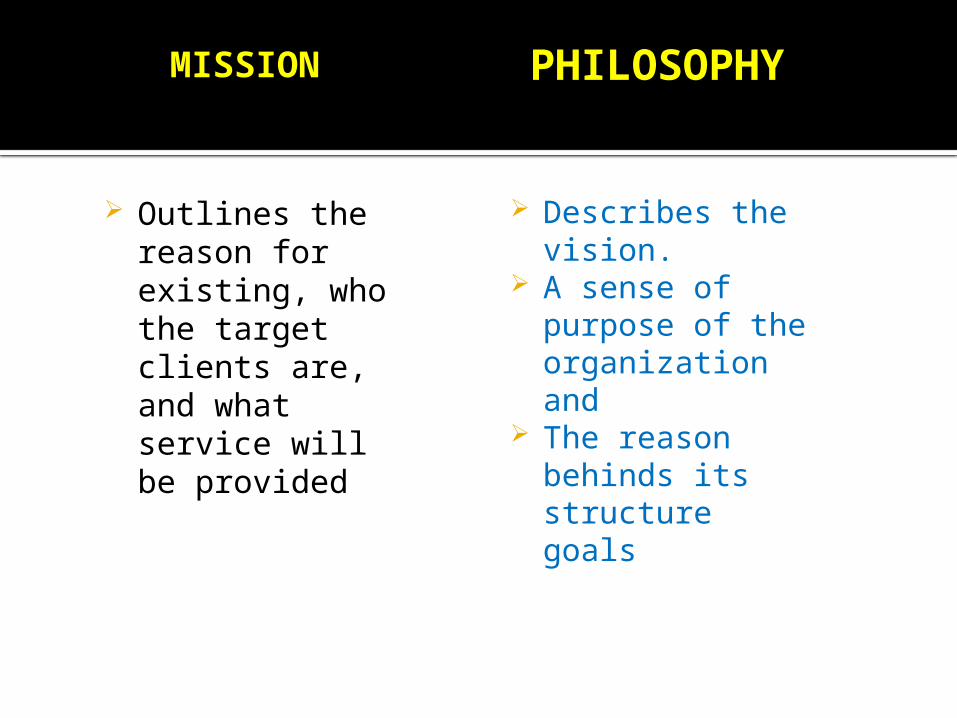

MISSION

Outlines the reason for existing, who the target clients are, and what service will be provided

PHILOSOPHY

Describes the vision.

A sense of purpose of the organization and

The reason behinds its structure goals

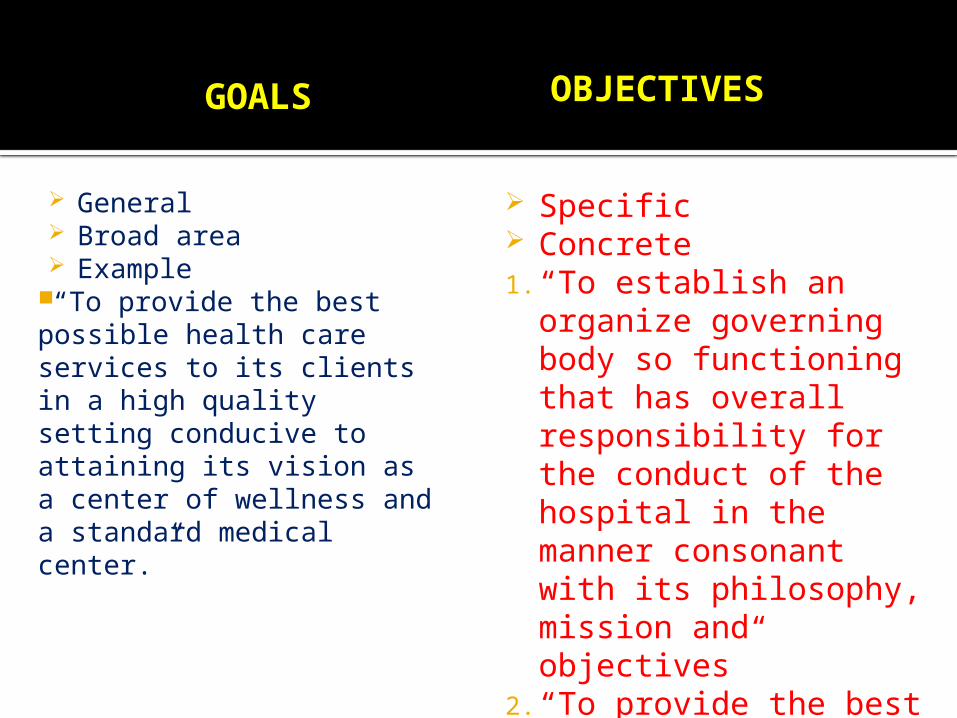

GOALS

General Broad area Example

“To provide the best possible health care services to its clients in a high quality setting conducive to attaining its vision as a center of wellness and a standard medical center.”

OBJECTIVES

Specific Concrete1. “To establish an

organize governing body so functioning that has overall responsibility for the conduct of the hospital in the manner consonant with its philosophy, mission and objectives”

2. “To provide the best quality, accessible and cost-effective health services to all clients.”

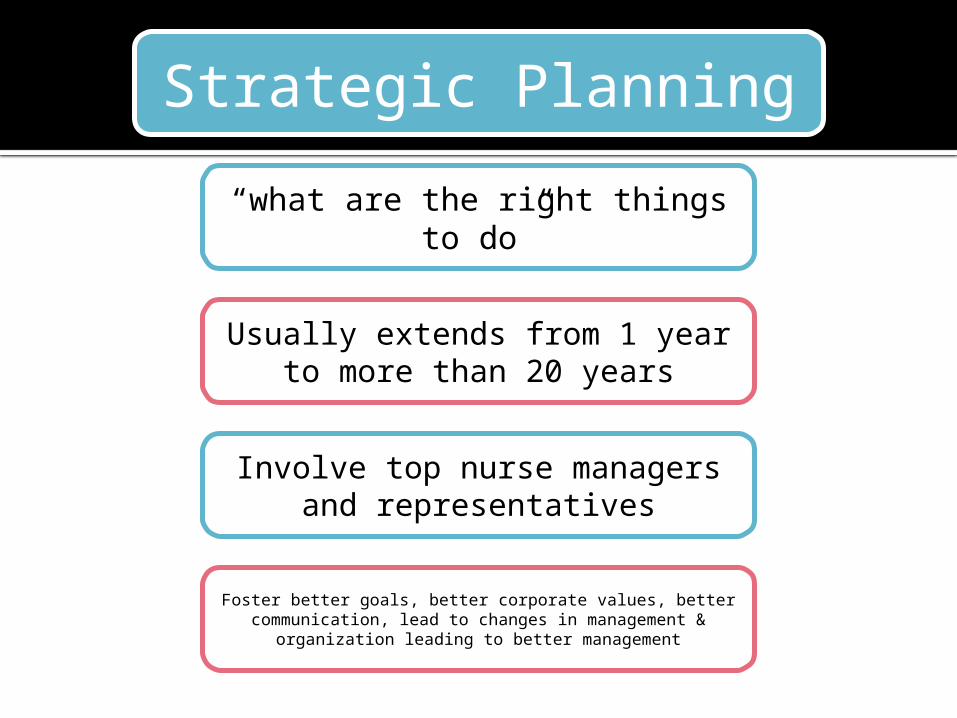

Strategic Planning

“what are the right things to do”

Usually extends from 1 year to more than 20 years

Involve top nurse managers and representatives

Foster better goals, better corporate values, better communication, lead to changes in management &

organization leading to better management

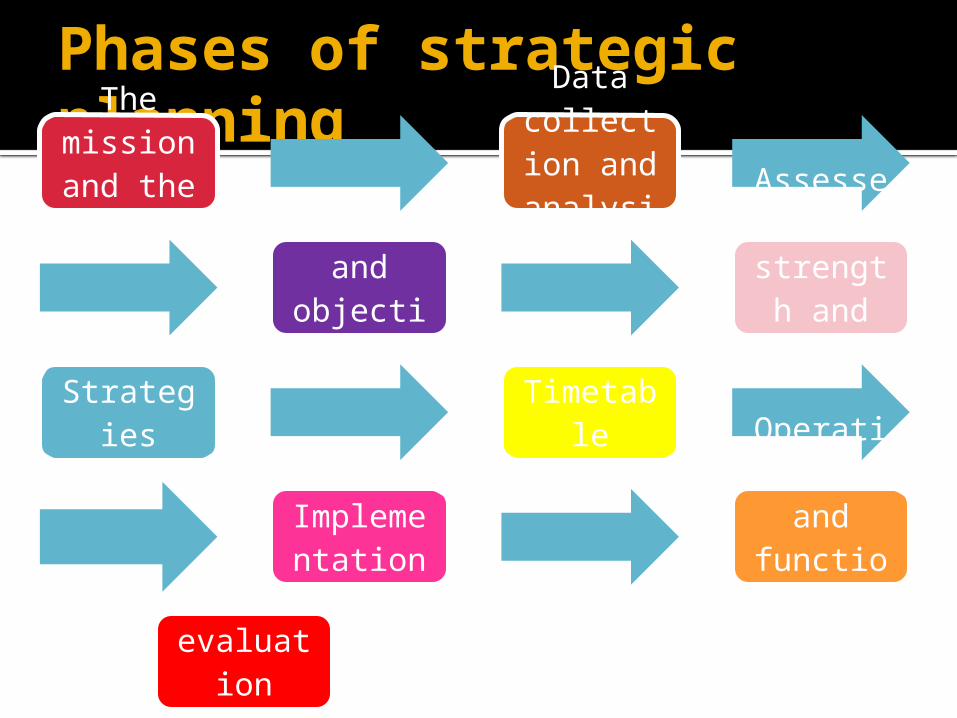

Phases of strategic planningThe mission and the creed

Data collectio

n and analysis Assesses

strength and

weaknesses

Goals and

objectives

Strategies

Timetable

Operational and functional plans

Implementation

evaluation

DECISION MAKING

Choosing among alternatives, systematic process and implementing it.

Models of Decision Making

Normative / Prescriptive Structured problem, predictable Used when info is objective and routine

Descriptive / Behavior Non Routine / Unpredictable option

Decision Tree Visualize alternatives, possible action.

Satisfying solution that minimally meets objectives

Optimizing select the most ideal solution

Intuition

Power to apprehend the possibilities inherent in a situation

Develop through “Brain Storming”

Making a better decision

Educate People Establish Decision Making checking Keep Progress Statistical Analysis Openness to new ideas Consensus building

Prioritization:

Deal in Order Solve easy problem Solve crisis problem

Pitfalls of Decision Making

Pitfalls stem from individual then from computers because individuals are still resistant to change.

Controlling Decision making and omitting from the process those involved

Inadequate fact-finding Time Constraint Poor Communication

Decision Making Process

Establish goals and objectives Identifying and Prioritization of

problems Develop possible solution Select among solution, the most

promising one and implement it Implement the solution Evaluate

PROBLEM SOLVING

Process of identifying course of action, alternatives to alleviate a problem

Critical Thinking

purposeful thinking, outcome directed, aims to make judgment based on scientific evidence.

Steps in Problem Solving:

Assess / Analyze Plan – evaluate effectively, feasibility Choosing best solution Implementation Evaluation

TIME MANAGEMENT

Organize, Prioritize and Schedule

Includes tools techniques for planning and scheduling time

Aim to increase the effectiveness and efficiency of personal and corporate use

8 Basic steps to time management

Decide what you really want in life Set Concrete goals Analyze your current time use Plan your day Follow your everyday cycle Keep a To do list Beware of Big 5

Indecision Guilt Worry Perfectionism Procrastination

Get Organized

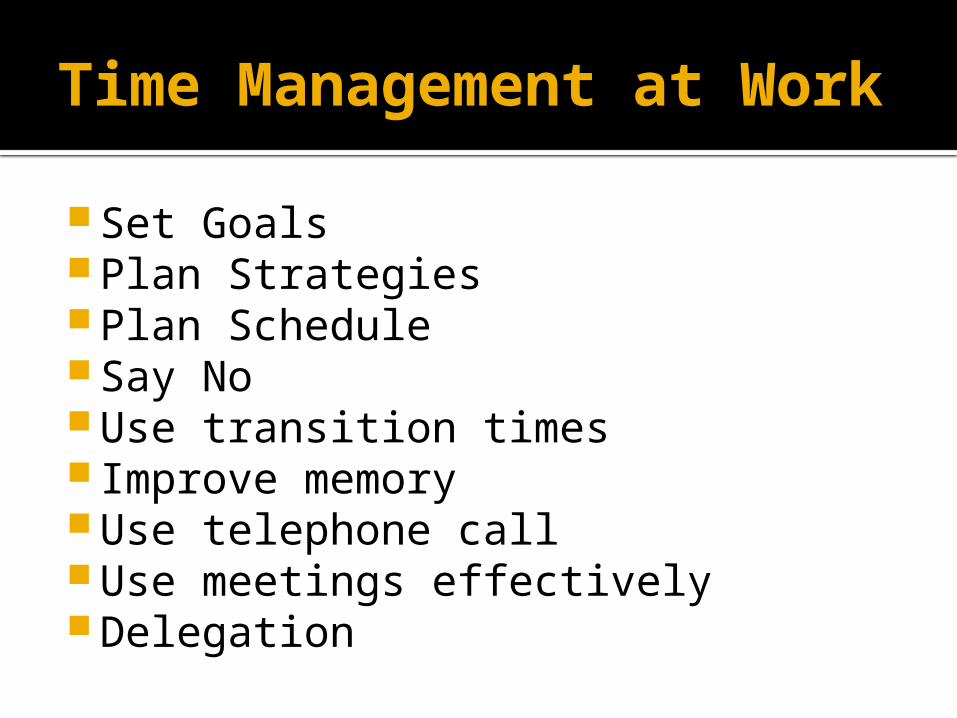

Time Management at Work

Set Goals Plan Strategies Plan Schedule Say No Use transition times Improve memory Use telephone call Use meetings effectively Delegation

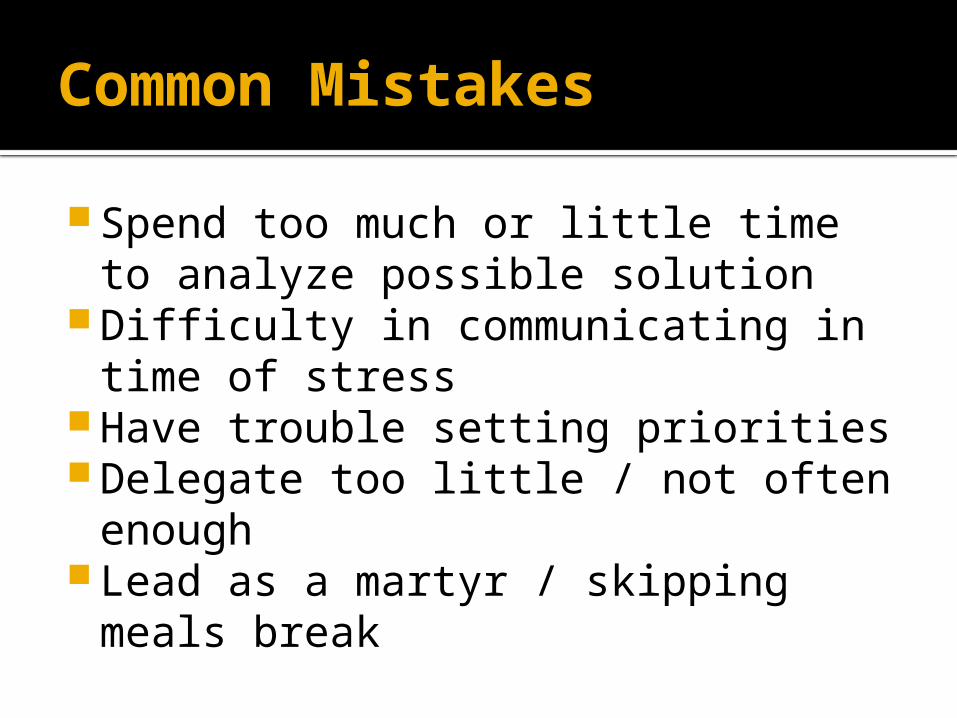

Common Mistakes

Spend too much or little time to analyze possible solution

Difficulty in communicating in time of stress

Have trouble setting priorities Delegate too little / not often enough Lead as a martyr / skipping meals

break

Techniques

Pareto Analysis – 80% Done 20% Time

PERT – Program evaluation and review techniques

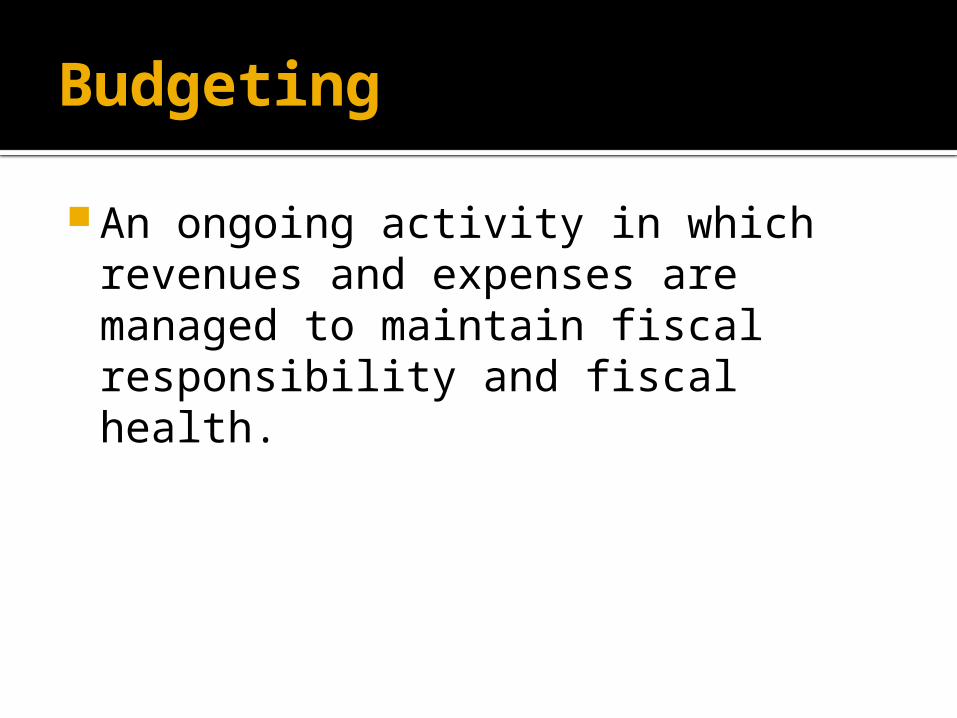

Budgeting

An ongoing activity in which revenues and expenses are managed to maintain fiscal responsibility and fiscal health.

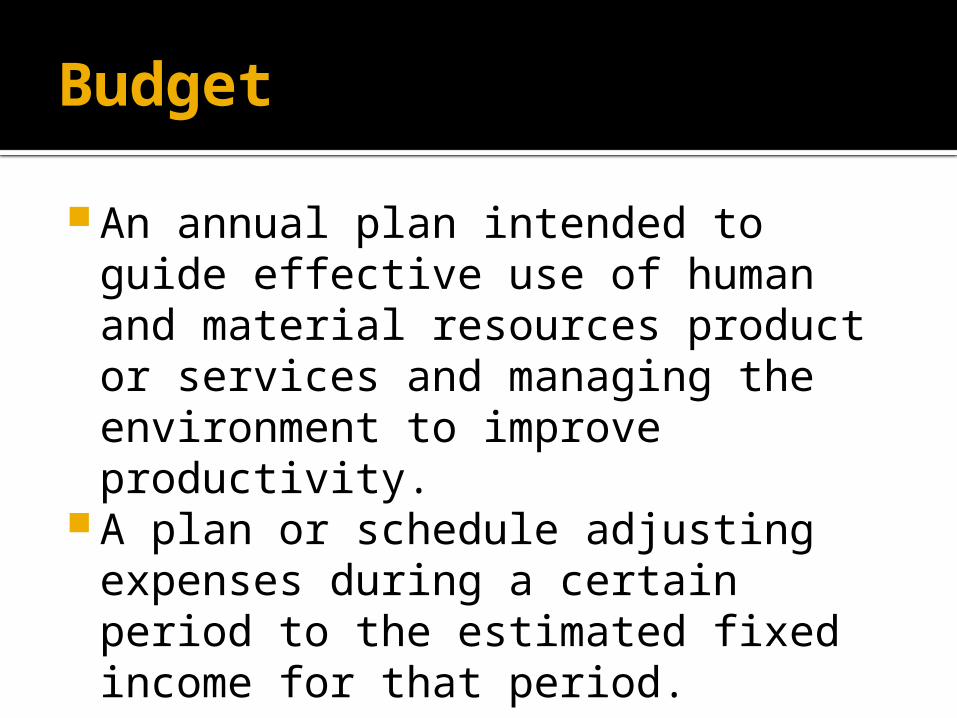

Budget

An annual plan intended to guide effective use of human and material resources product or services and managing the environment to improve productivity.

A plan or schedule adjusting expenses during a certain period to the estimated fixed income for that period.

BUDGET

Budgetary Planning ensures that the best methods are used to achieve financial objectives.

A good budget is based on objectives, is simple, flexible, balanced, has standards and uses available resources first to avoid increasing cost.

Each budget system is designed for the situation at hand, bearing in mind the character of the company, the company’s position and the nature of the plans involved.

Nursing Budget

A systematic plans that is an informed best estimate by nurse administrators of revenues and nursing expenses.

Purpose of Budget

Plan the objectives, programs and activities of nursing services and the fiscal resources needed to accomplish them.

Motivate nursing workers through analysis of actual experiences

Serve as a standard to evaluate the performance of nurse administrators and managers and increase awareness of cost

BUDGET AND PLANNING

The relationship of budget and objectives identifying objective is the chief planning activity and each of the nursing units develop a management plan with a budget for each objective. The source of the nursing budget is the objectives.

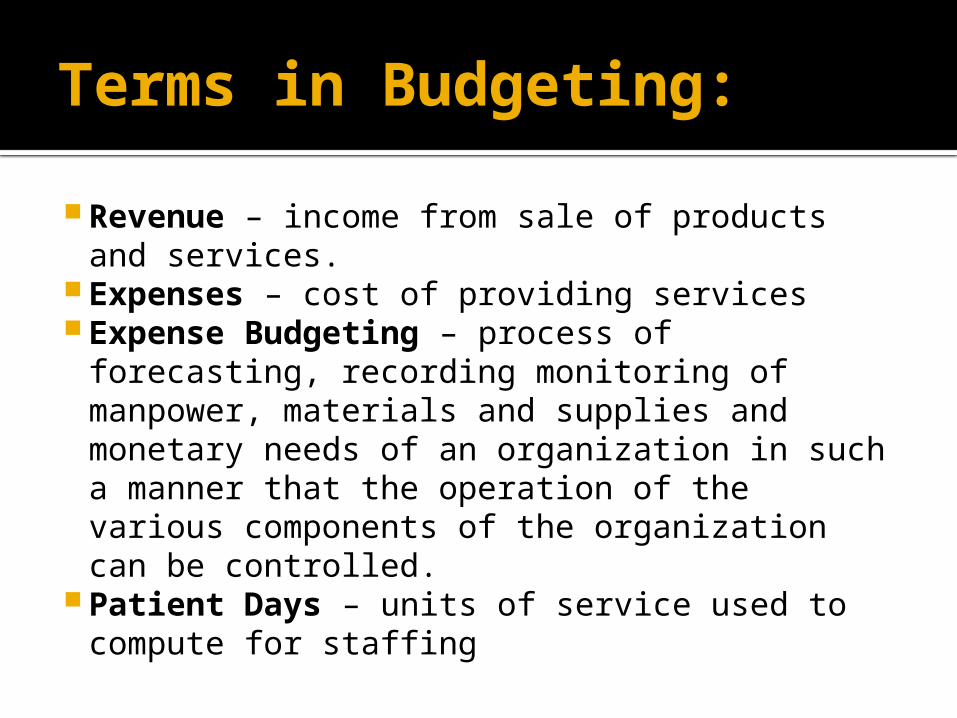

Terms in Budgeting:

Revenue – income from sale of products and services.

Expenses – cost of providing services Expense Budgeting – process of forecasting,

recording monitoring of manpower, materials and supplies and monetary needs of an organization in such a manner that the operation of the various components of the organization can be controlled.

Patient Days – units of service used to compute for staffing

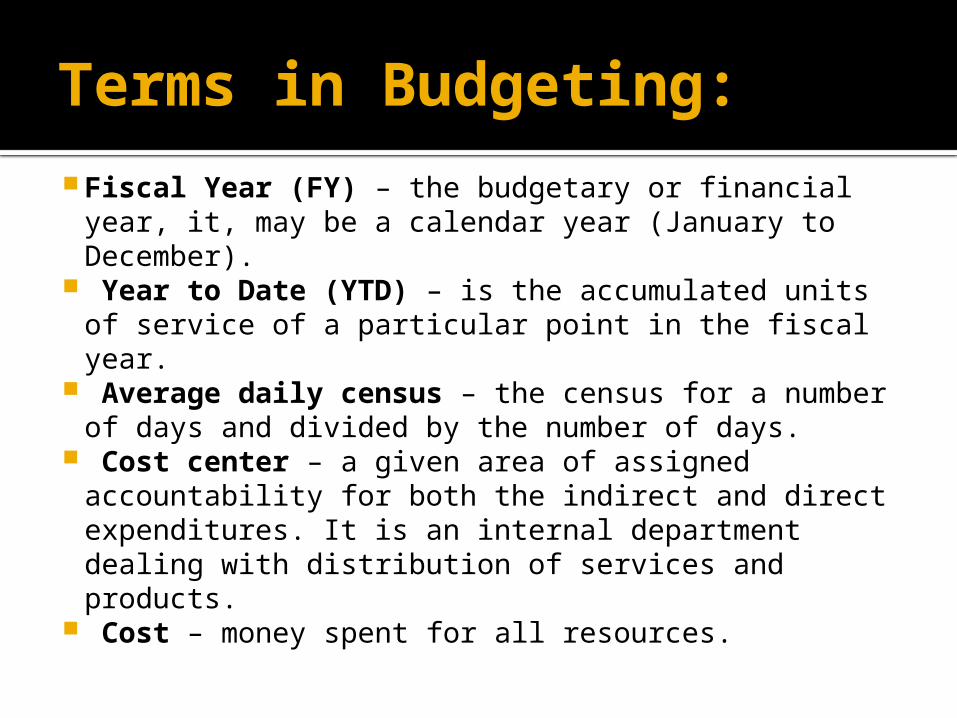

Terms in Budgeting:

Fiscal Year (FY) – the budgetary or financial year, it, may be a calendar year (January to December).

Year to Date (YTD) – is the accumulated units of service of a particular point in the fiscal year.

Average daily census – the census for a number of days and divided by the number of days.

Cost center – a given area of assigned accountability for both the indirect and direct expenditures. It is an internal department dealing with distribution of services and products.

Cost – money spent for all resources.

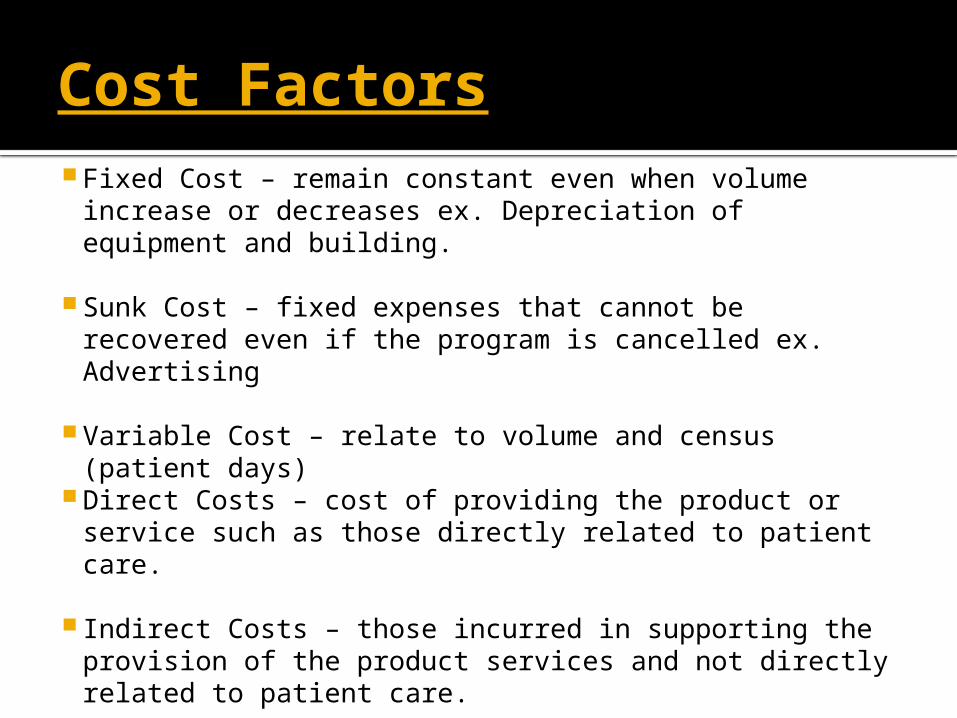

Cost Factors Fixed Cost – remain constant even when volume

increase or decreases ex. Depreciation of equipment and building.

Sunk Cost – fixed expenses that cannot be recovered even if the program is cancelled ex. Advertising

Variable Cost – relate to volume and census (patient days)

Direct Costs – cost of providing the product or service such as those directly related to patient care.

Indirect Costs – those incurred in supporting the provision of the product services and not directly related to patient care.

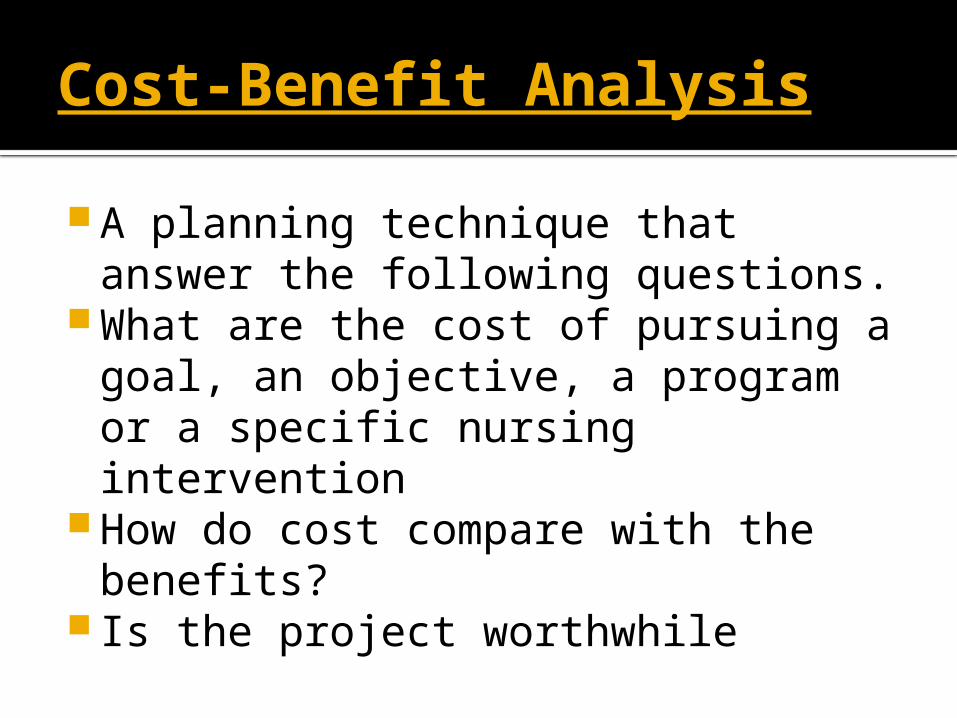

Cost-Benefit Analysis

A planning technique that answer the following questions.

What are the cost of pursuing a goal, an objective, a program or a specific nursing intervention

How do cost compare with the benefits?

Is the project worthwhile

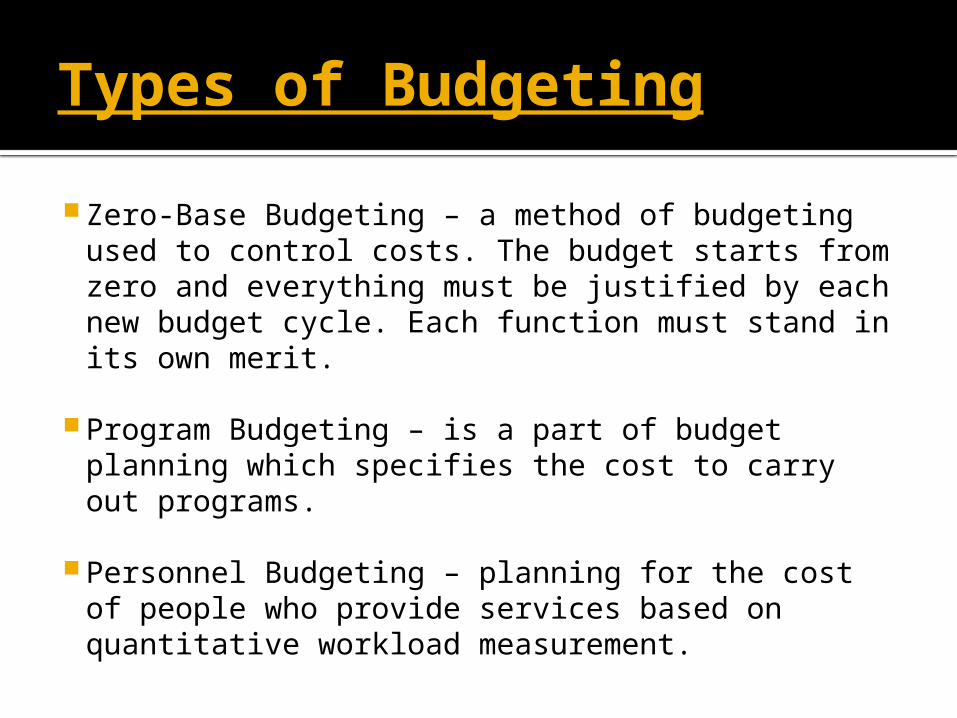

Types of Budgeting

Zero-Base Budgeting – a method of budgeting used to control costs. The budget starts from zero and everything must be justified by each new budget cycle. Each function must stand in its own merit.

Program Budgeting – is a part of budget planning which specifies the cost to carry out programs.

Personnel Budgeting – planning for the cost of people who provide services based on quantitative workload measurement.

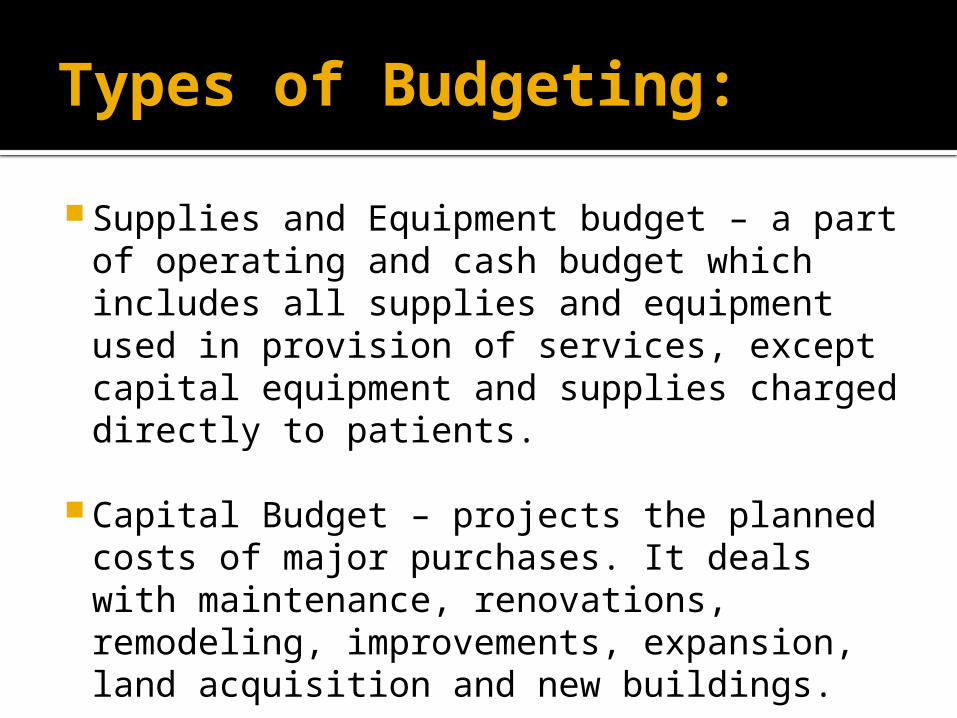

Types of Budgeting:

Supplies and Equipment budget – a part of operating and cash budget which includes all supplies and equipment used in provision of services, except capital equipment and supplies charged directly to patients.

Capital Budget – projects the planned costs of major purchases. It deals with maintenance, renovations, remodeling, improvements, expansion, land acquisition and new buildings.

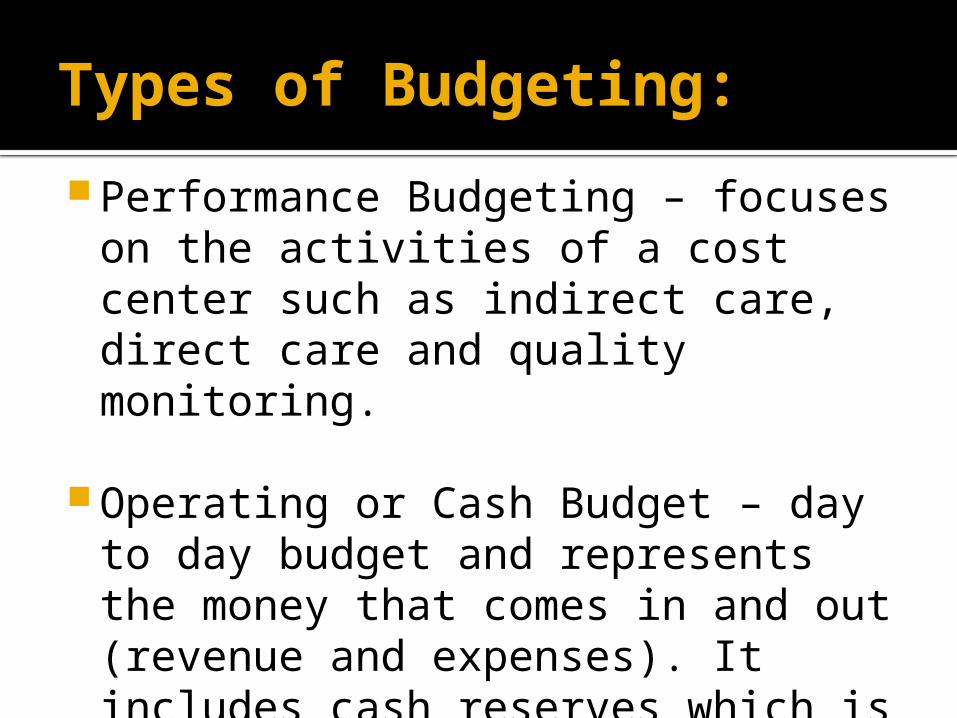

Types of Budgeting:

Performance Budgeting – focuses on the activities of a cost center such as indirect care, direct care and quality monitoring.

Operating or Cash Budget – day to day budget and represents the money that comes in and out (revenue and expenses). It includes cash reserves which is cash budgets paying for bills.

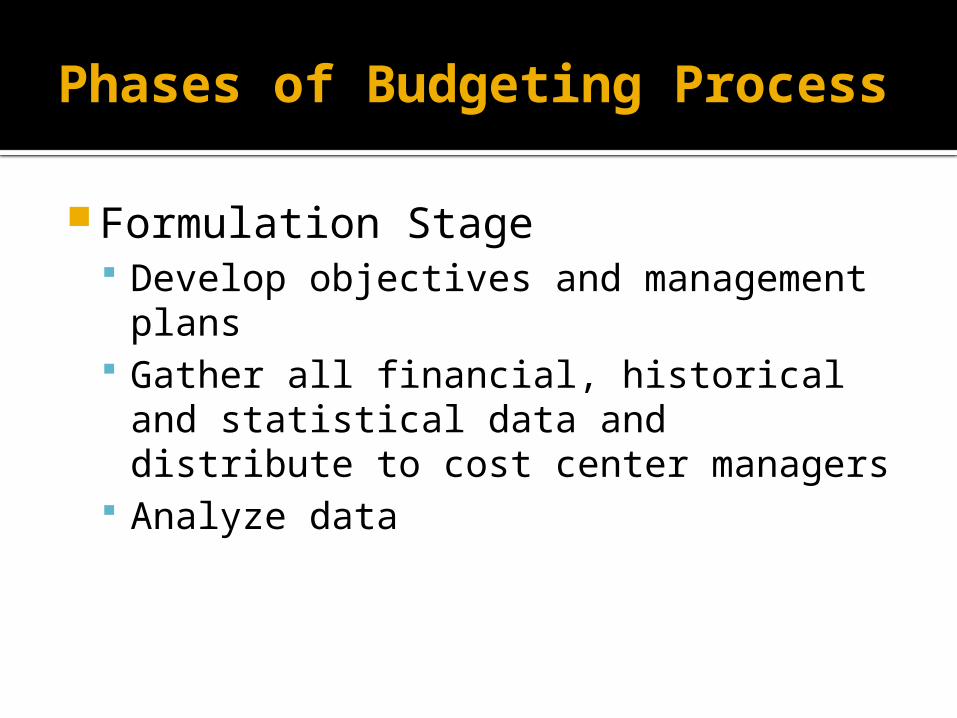

Phases of Budgeting Process

Formulation Stage Develop objectives and management

plans Gather all financial, historical and

statistical data and distribute to cost center managers

Analyze data

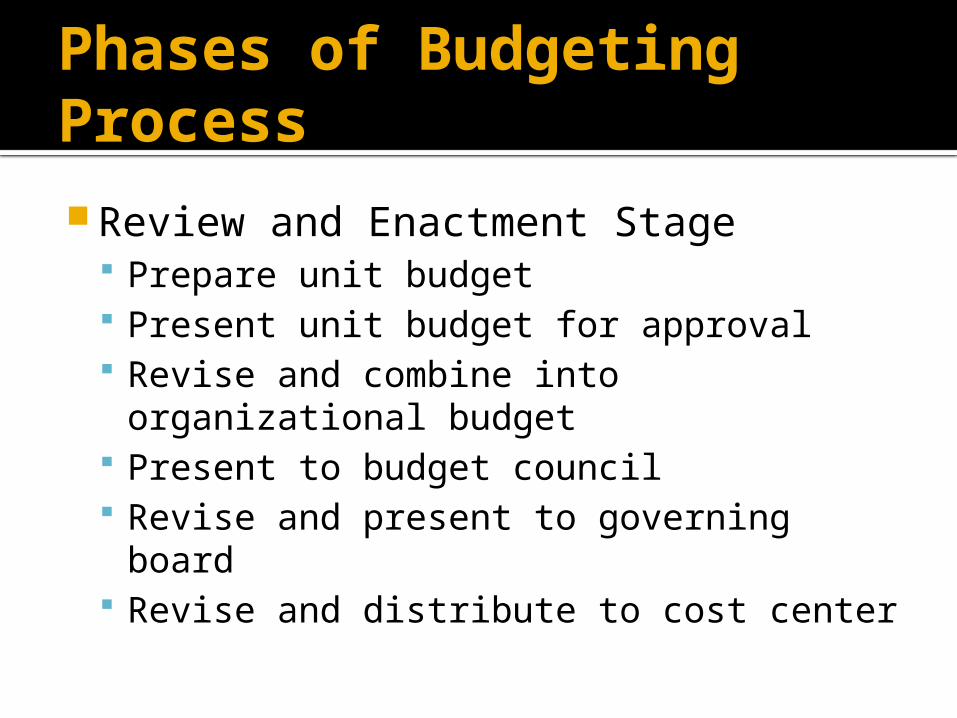

Phases of Budgeting Process

Review and Enactment Stage Prepare unit budget Present unit budget for approval Revise and combine into organizational

budget Present to budget council Revise and present to governing board Revise and distribute to cost center

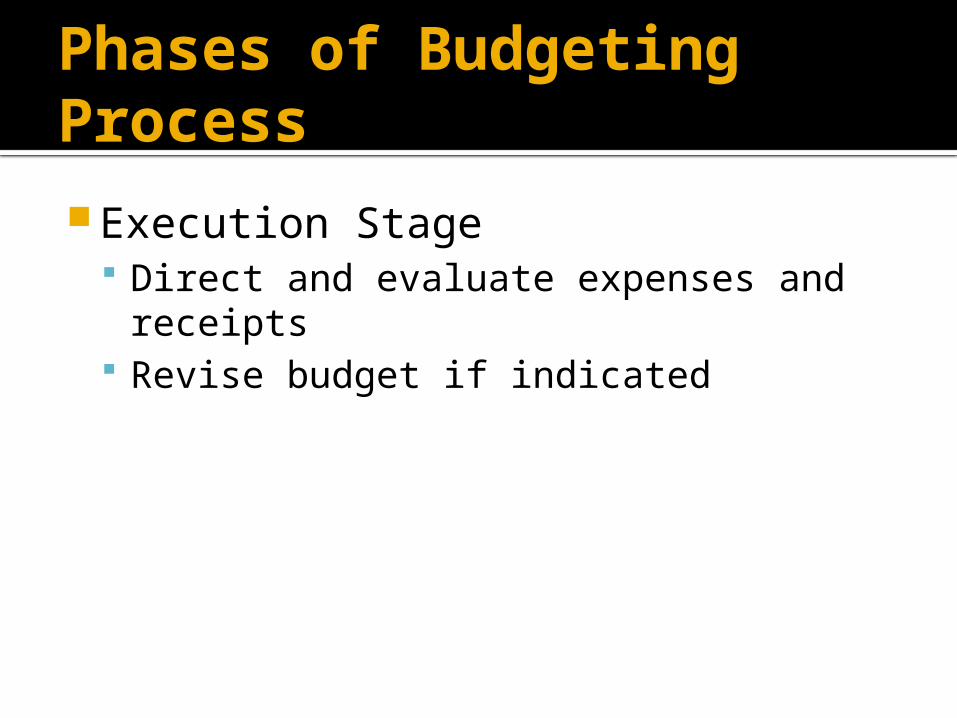

Phases of Budgeting Process

Execution Stage Direct and evaluate expenses and

receipts Revise budget if indicated

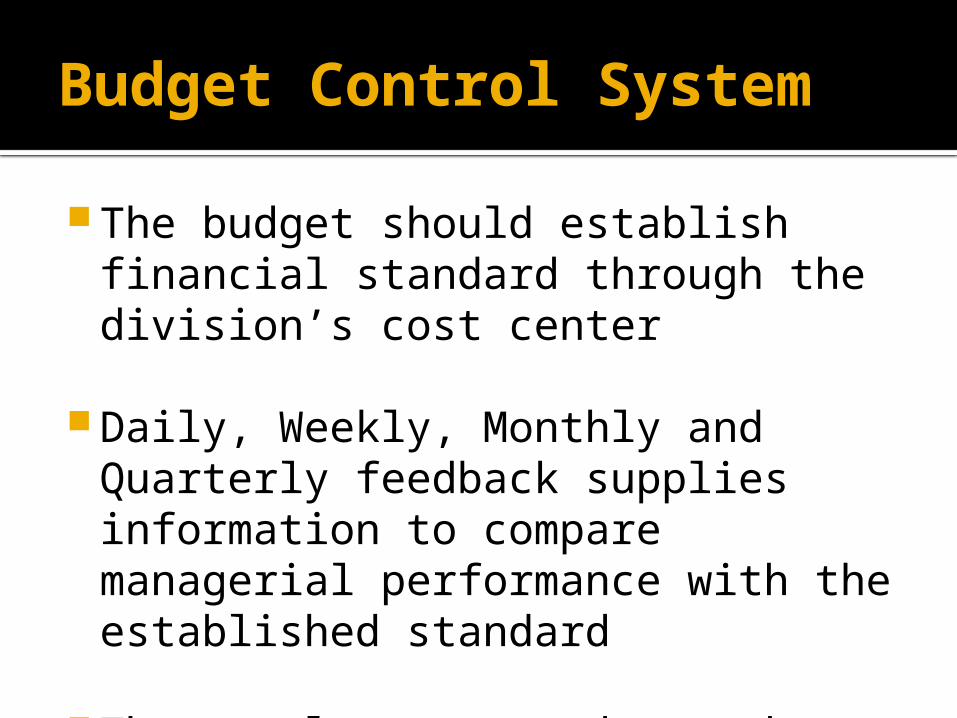

Budget Control System

The budget should establish financial standard through the division’s cost center

Daily, Weekly, Monthly and Quarterly feedback supplies information to compare managerial performance with the established standard

The results are used to make adjustment

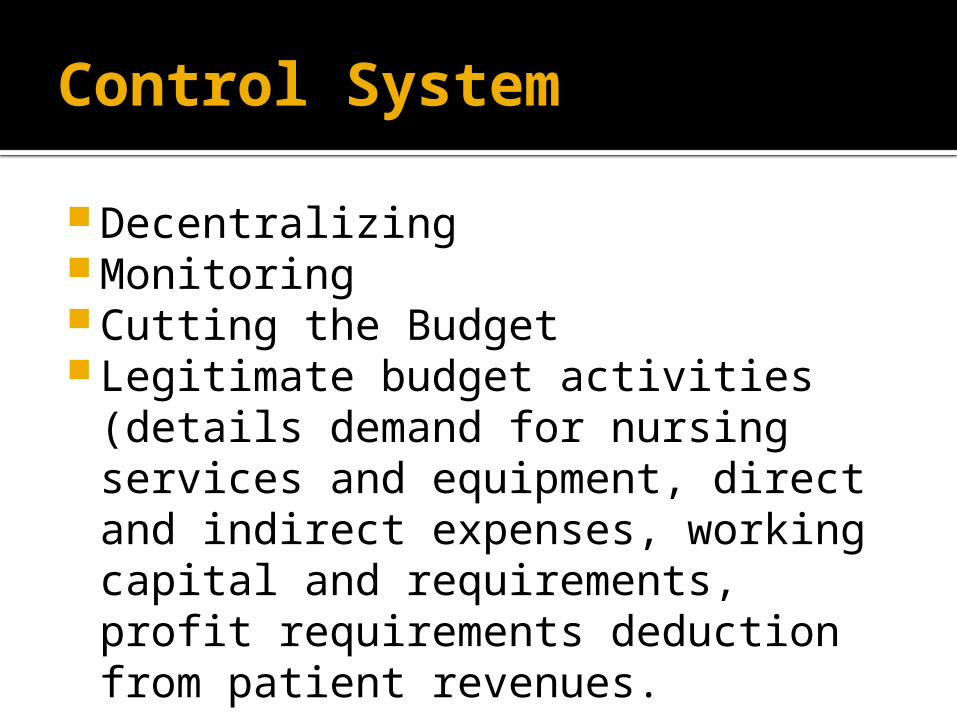

Control System

Decentralizing Monitoring Cutting the Budget Legitimate budget activities (details

demand for nursing services and equipment, direct and indirect expenses, working capital and requirements, profit requirements deduction from patient revenues.

ORGANIZING

ORGANIZATION.

Process of bringing together physical, financial and human resources.

Process involves: Identification of activities Classification of activities Assignment of duties Delegation of authority and

responsibility Coordinating authority and responsibility.

DIRECTING

DIRECTING

It involves leading and the use of motivation and power so as to affect an individual’s behavior towards the attainment of the organizational goal.

Discussing style. Delegating questions.

What’s our goal? What’s the problem? What are our options? What’s our plan?

How should we proceed? When does it need to be done by> Who should do it? Why are we doing this?

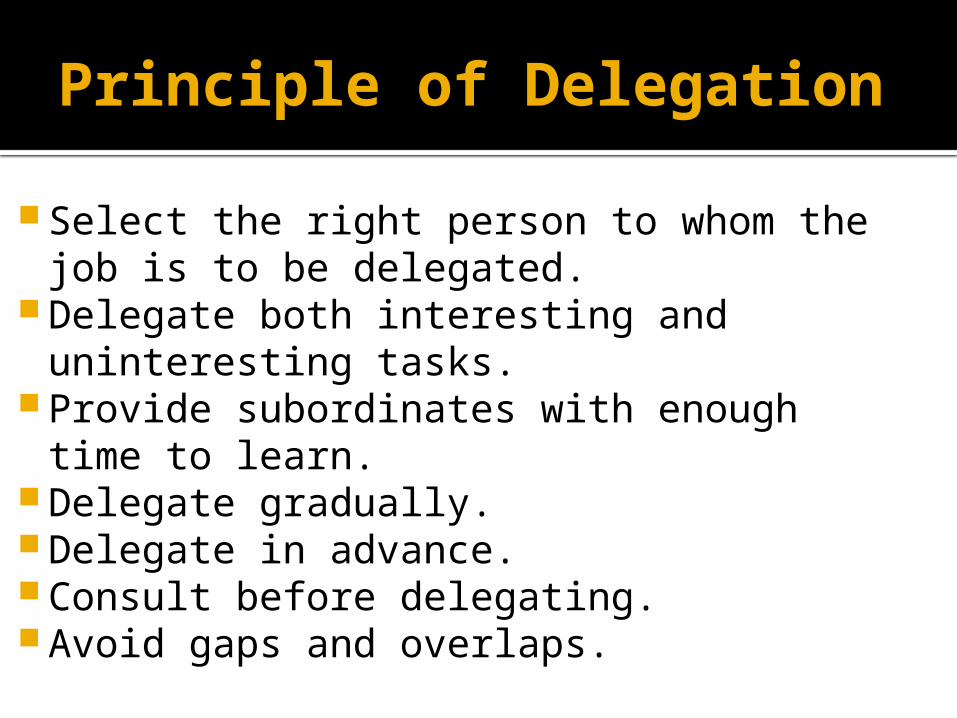

Principle of Delegation

Select the right person to whom the job is to be delegated.

Delegate both interesting and uninteresting tasks.

Provide subordinates with enough time to learn.

Delegate gradually. Delegate in advance. Consult before delegating. Avoid gaps and overlaps.

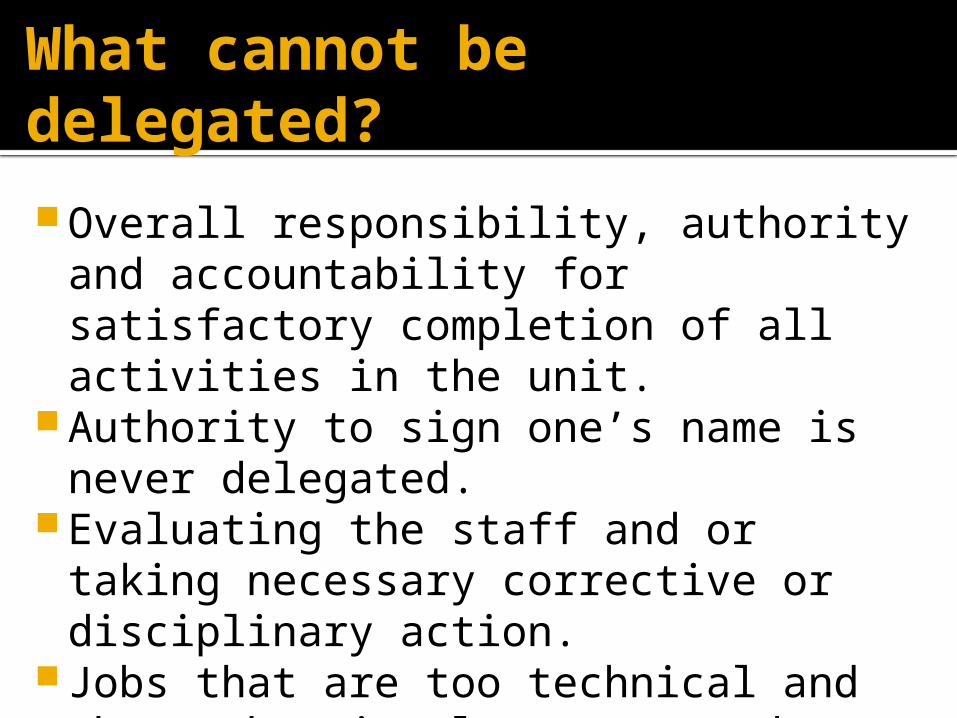

What cannot be delegated?

Overall responsibility, authority and accountability for satisfactory completion of all activities in the unit.

Authority to sign one’s name is never delegated.

Evaluating the staff and or taking necessary corrective or disciplinary action.

Jobs that are too technical and those that involve trust and confidence.

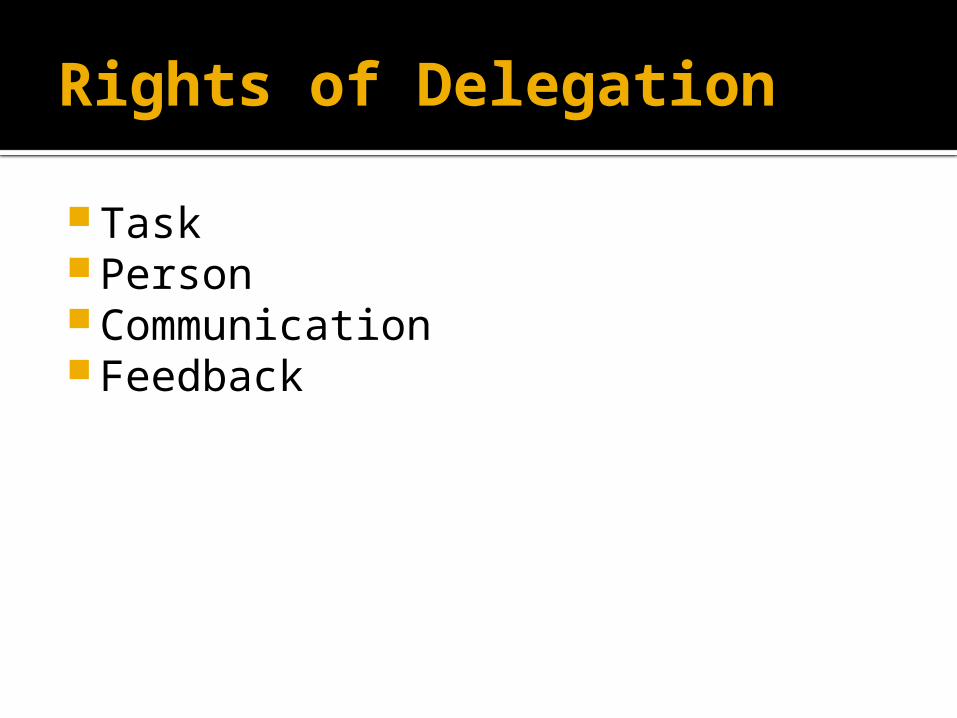

Rights of Delegation

Task Person Communication Feedback

![Transactional Contention Management as a Non-Clairvoyant Scheduling Problem Alessia Milani [Attiya et al. PODC 06] [Attiya and Milani OPODIS 09]](https://img.pdfslide.net/doc/110x75/56649ce25503460f949ada56/transactional-contention-management-as-a-non-clairvoyant-scheduling-problem.jpg)