Embed Size (px)

Citation preview

Meaning for

Mining

AUGUST 20 | AURA DAY

AUGUST 2020 | AURA DAY

Corporate Strategy

Rodrigo Barbosa – CEO

7

"To find, mine and deliver the planet's most important and essential minerals

that enable the world and humankind to create, innovate, and prosper"

Purpose Driven

INNOVATE PROSPERCREATE

8

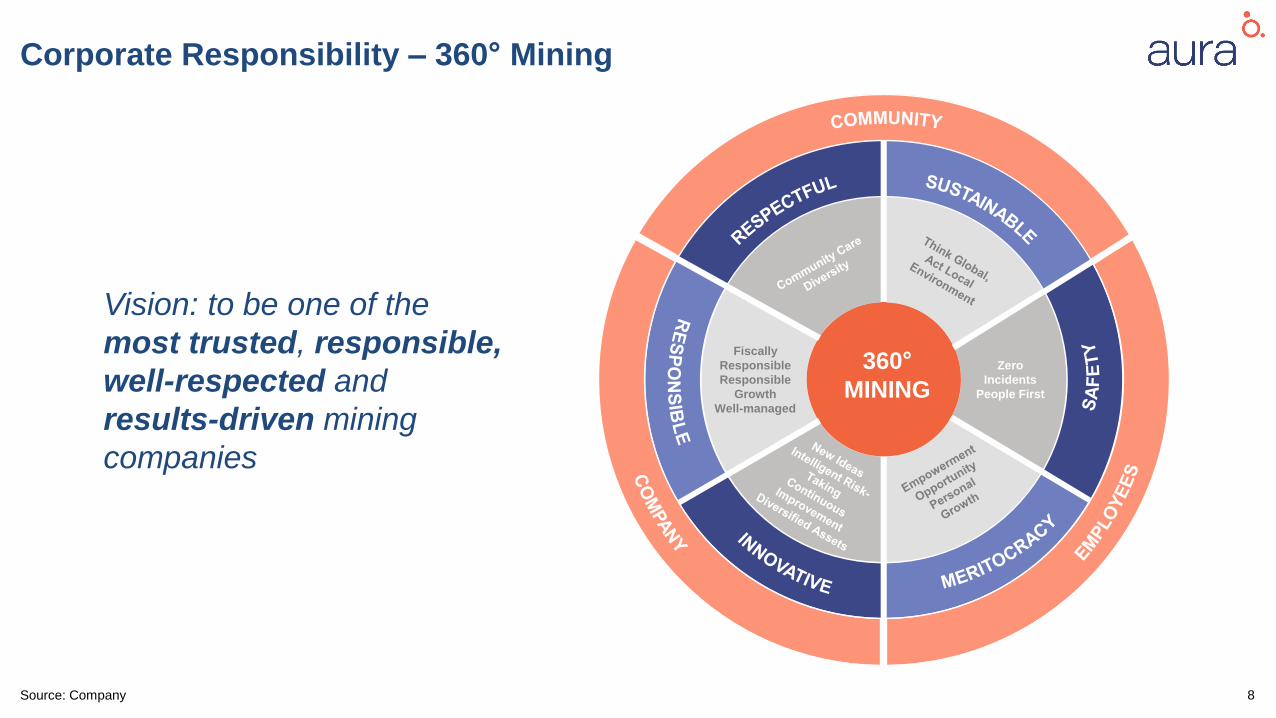

Corporate Responsibility – 360° Mining

Source: Company

360°

MINING

Fiscally

Responsible

Responsible

Growth

Well-managed

Zero

Incidents

People First

Vision: to be one of the

most trusted, responsible,

well-respected and

results-driven mining

companies

9

We Have Built a Solid Base – Ready to Grow

1. As disclosed in the Company's second quarter 2020 MD&A

Source: Company

1

2

3

8

65

7

4

▪ Profitable gold and copper mining company with attractive economics

and growth perspective

▪ Aura has a superior combination of cash flow and internal growth

projects with exploration upside

▪ Diversified production base with operating assets in mining friendly

jurisdictions

▪ 360º mining: focus on company, community and employees

▪ Listed on the Toronto Stock Exchange (TSX-ORA) and B3 (AURA32.SA)

in Brazil

Overview Operations and Projects

2nd Semester 106

72

2019

118-138

78

2020

1st Semester

178

196-216

Production guidance1

000 GEO

1

2

3

4

5

6

7

8

Aranzazu (prod1. 62-68 kGEO)

San Andrés (prod1. 63-69 kOz Au)

EPP (prod1. 62-68 kOz Au)

Gold Road (prod1. 8-10 kOz Au)

Almas

Matupá

São Francisco

Tolda Fria

Annualized:

222-264k Oz

10

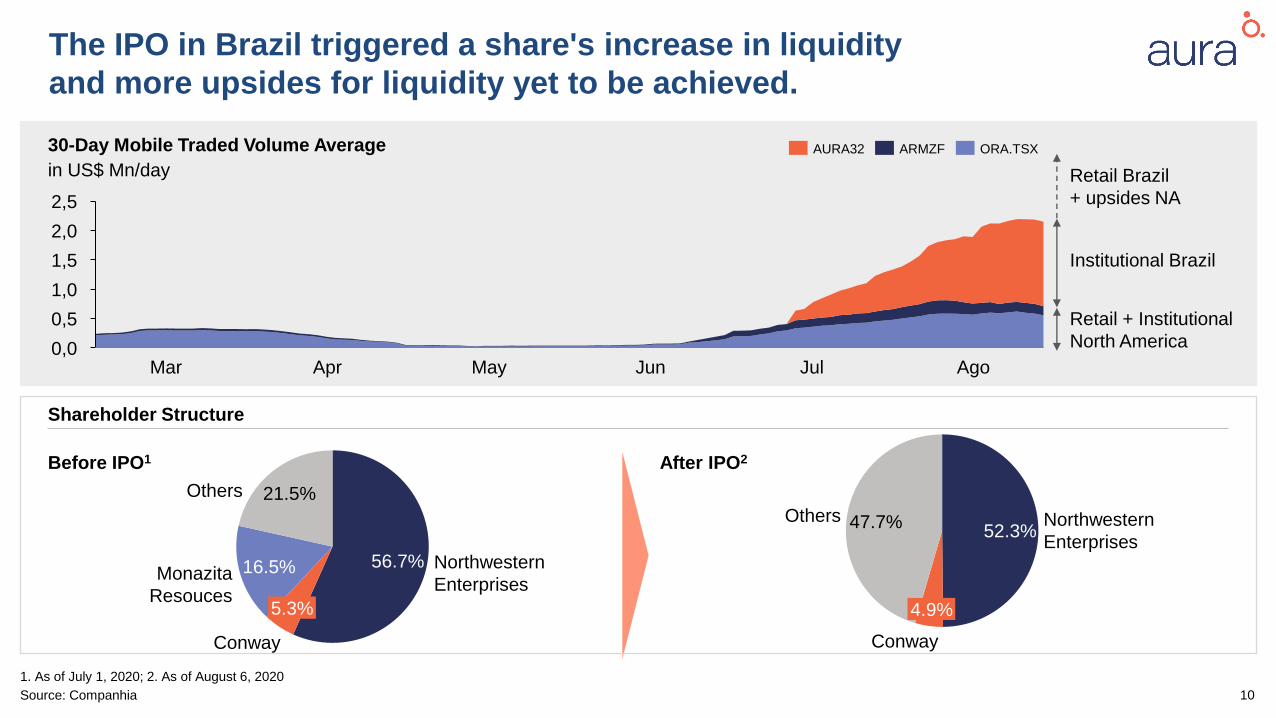

52.3%Northwestern

Enterprises47.7%

4.9%

Conway

Others

The IPO in Brazil triggered a share's increase in liquidity

and more upsides for liquidity yet to be achieved.

Shareholder Structure

30-Day Mobile Traded Volume Average

in US$ Mn/day

2,0

0,5

0,0

1,5

1,0

2,5

AURA32 ARMZF ORA.TSX

Mar Apr May Jun Jul Ago

Retail + Institutional

North America

Institutional Brazil

Retail Brazil

+ upsides NA

Before IPO1 After IPO2

56.7%Monazita

Resouces

Northwestern

Enterprises

21.5%

5.3%

Conway

Others

16.5%

1. As of July 1, 2020; 2. As of August 6, 2020

Source: Companhia

11Source: Company

With the pillars of our strategy… … we transformed Aura Over

the Past 3 Years

Strong Balance

Sheet

Business-Building

Culture

High Quality

Assets and Projects

Generate value with

high-quality assets

and further

development of

advanced-stage

projects

Low leverage, wide

bank relationship, and

increasing free cash

flow to support

sustainable growth

Build a team and

culture to support an

evolving business

committed to

excellence

New

controlling shareholder

We Redeveloped a

mine

Restart of Aranzazu

We Enhanced

corporate governance,

created a strong culture

and attracted top talents

Listing IPO

on B3, becoming the

first gold producer to be

listed in Brazil

We made strategic

deals

Serrote's sale for US$

40 mn and Merger with

Rio Novo

We Strengthened

Our balance sheet,

reduced costs and

developed local bank

relationship

We Acquired

Gold Road which

should be in production

already in 2S20

2017

2020

12

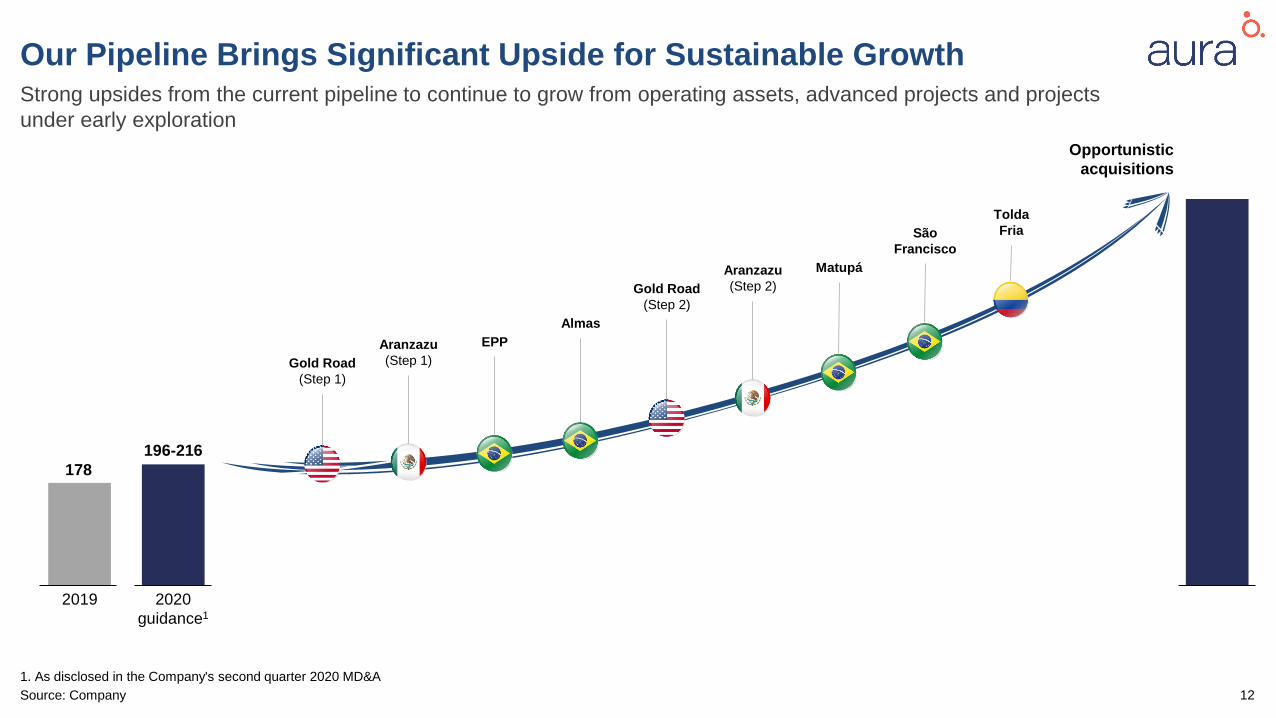

Our Pipeline Brings Significant Upside for Sustainable GrowthStrong upsides from the current pipeline to continue to grow from operating assets, advanced projects and projects

under early exploration

Opportunistic

acquisitions

Almas

Matupá

São

Francisco

Tolda

Fria

EPPAranzazu

(Step 1)

Aranzazu

(Step 2)

Gold Road

(Step 1)

Gold Road

(Step 2)

196-216

2020

guidance1

1. As disclosed in the Company's second quarter 2020 MD&A

Source: Company

2019

178

AUGUST 2020 | AURA DAY

Operations

Glauber Luvizotto – COO

14

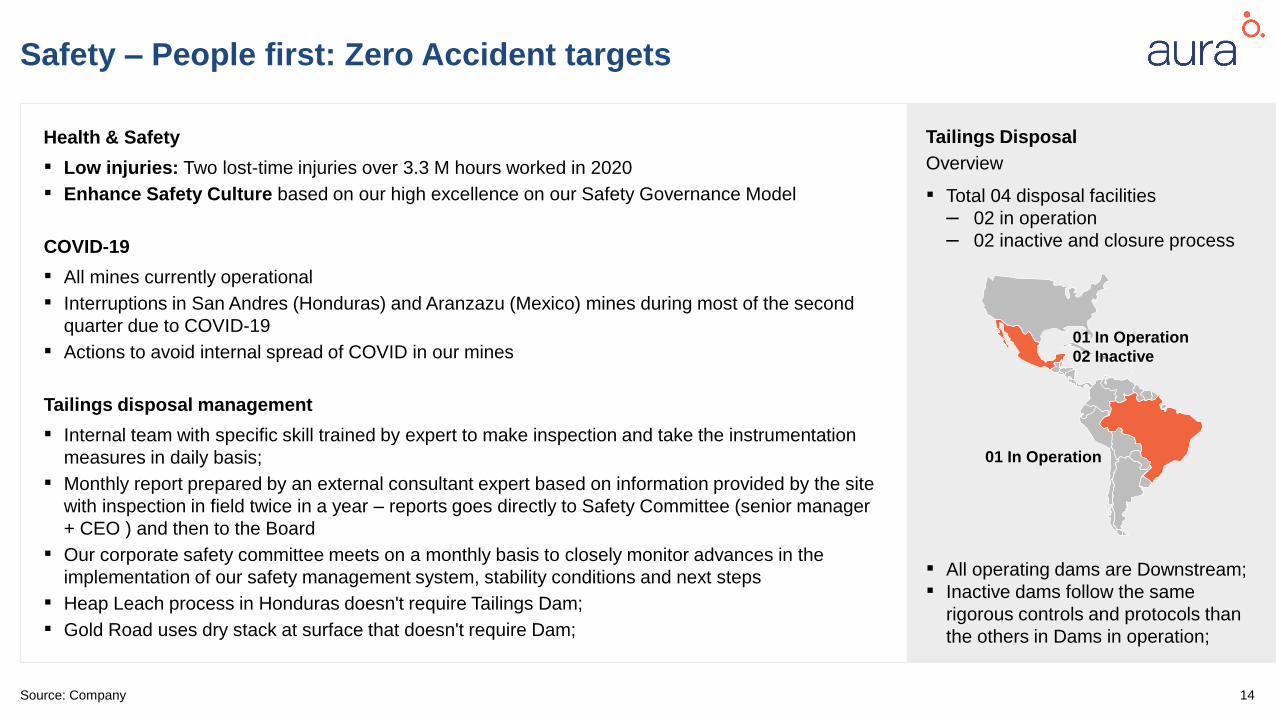

Safety – People first: Zero Accident targets

Health & Safety

▪ Low injuries: Two lost-time injuries over 3.3 M hours worked in 2020

▪ Enhance Safety Culture based on our high excellence on our Safety Governance Model

COVID-19

▪ All mines currently operational

▪ Interruptions in San Andres (Honduras) and Aranzazu (Mexico) mines during most of the second

quarter due to COVID-19

▪ Actions to avoid internal spread of COVID in our mines

Tailings disposal management

▪ Internal team with specific skill trained by expert to make inspection and take the instrumentation

measures in daily basis;

▪ Monthly report prepared by an external consultant expert based on information provided by the site

with inspection in field twice in a year – reports goes directly to Safety Committee (senior manager

+ CEO ) and then to the Board

▪ Our corporate safety committee meets on a monthly basis to closely monitor advances in the

implementation of our safety management system, stability conditions and next steps

▪ Heap Leach process in Honduras doesn't require Tailings Dam;

▪ Gold Road uses dry stack at surface that doesn't require Dam;

Tailings Disposal

Overview

▪ Total 04 disposal facilities

– 02 in operation

– 02 inactive and closure process

▪ All operating dams are Downstream;

▪ Inactive dams follow the same

rigorous controls and protocols than

the others in Dams in operation;

01 In Operation

01 In Operation

02 Inactive

Source: Company

15

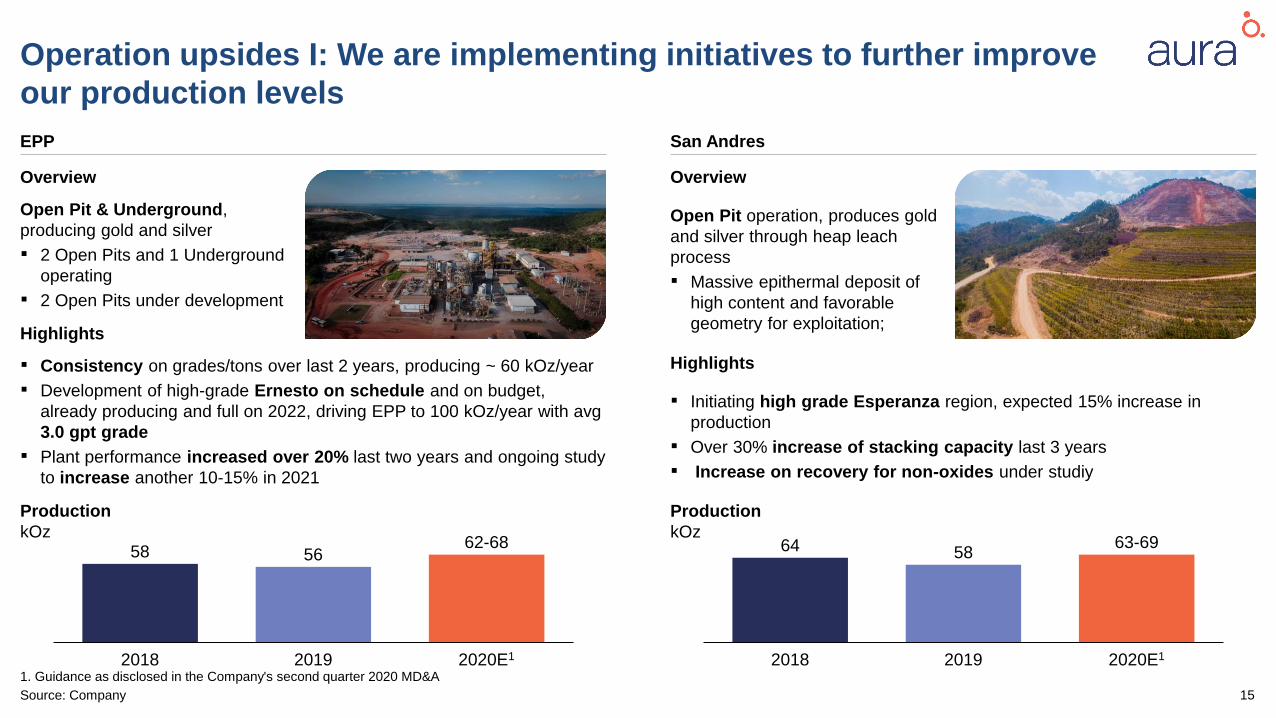

Operation upsides I: We are implementing initiatives to further improve

our production levels

2020E12018

58

2019

5662-68

Overview

EPP San Andres

Open Pit & Underground,

producing gold and silver

▪ 2 Open Pits and 1 Underground

operating

▪ 2 Open Pits under development

Highlights

▪ Consistency on grades/tons over last 2 years, producing ~ 60 kOz/year

▪ Development of high-grade Ernesto on schedule and on budget,

already producing and full on 2022, driving EPP to 100 kOz/year with avg

3.0 gpt grade

▪ Plant performance increased over 20% last two years and ongoing study

to increase another 10-15% in 2021

Production

kOz

2018 2020E12019

64 5863-69

Overview

Open Pit operation, produces gold

and silver through heap leach

process

▪ Massive epithermal deposit of

high content and favorable

geometry for exploitation;

Highlights

▪ Initiating high grade Esperanza region, expected 15% increase in

production

▪ Over 30% increase of stacking capacity last 3 years

▪ Increase on recovery for non-oxides under studiy

Production

kOz

1. Guidance as disclosed in the Company's second quarter 2020 MD&A

Source: Company

16

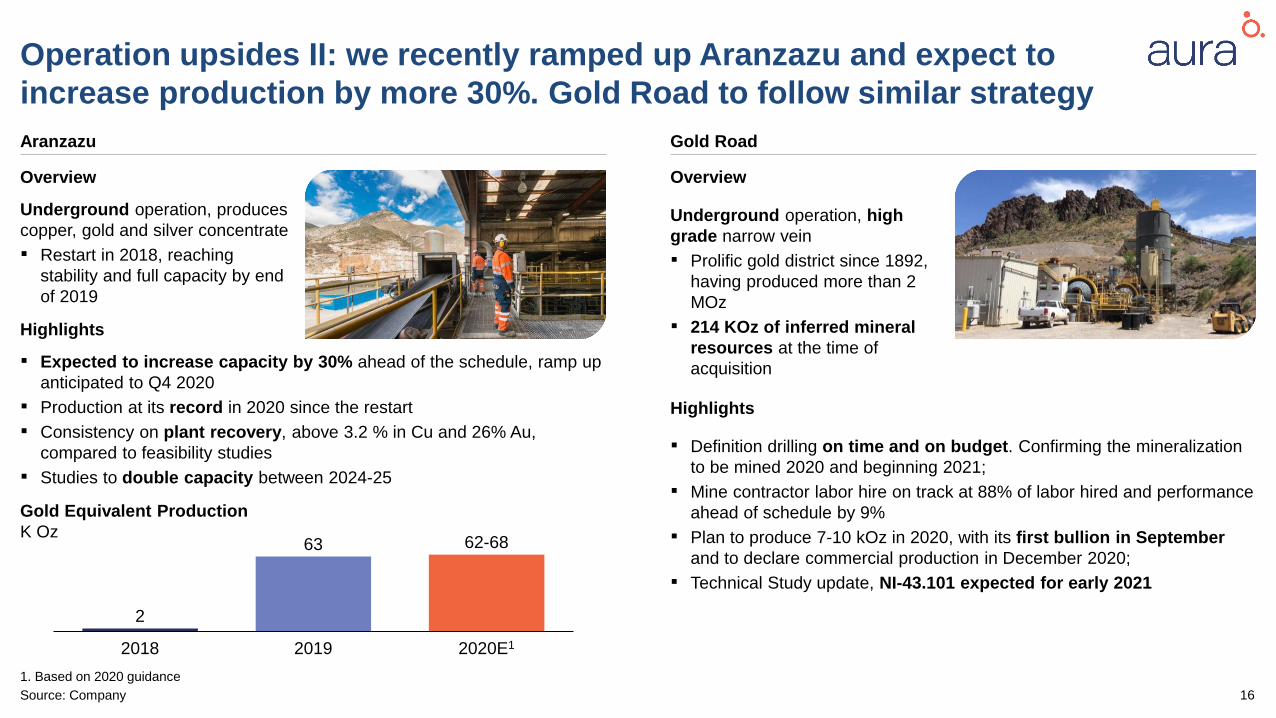

Operation upsides II: we recently ramped up Aranzazu and expect to

increase production by more 30%. Gold Road to follow similar strategy

2018

62-68

2019 2020E1

2

63

Overview

Aranzazu Gold Road

Underground operation, produces

copper, gold and silver concentrate

▪ Restart in 2018, reaching

stability and full capacity by end

of 2019

Highlights

▪ Expected to increase capacity by 30% ahead of the schedule, ramp up

anticipated to Q4 2020

▪ Production at its record in 2020 since the restart

▪ Consistency on plant recovery, above 3.2 % in Cu and 26% Au,

compared to feasibility studies

▪ Studies to double capacity between 2024-25

Gold Equivalent Production

K Oz

Overview

Underground operation, high

grade narrow vein

▪ Prolific gold district since 1892,

having produced more than 2

MOz

▪ 214 KOz of inferred mineral

resources at the time of

acquisition

Highlights

▪ Definition drilling on time and on budget. Confirming the mineralization

to be mined 2020 and beginning 2021;

▪ Mine contractor labor hire on track at 88% of labor hired and performance

ahead of schedule by 9%

▪ Plan to produce 7-10 kOz in 2020, with its first bullion in September

and to declare commercial production in December 2020;

▪ Technical Study update, NI-43.101 expected for early 2021

1. Based on 2020 guidance

Source: Company

17

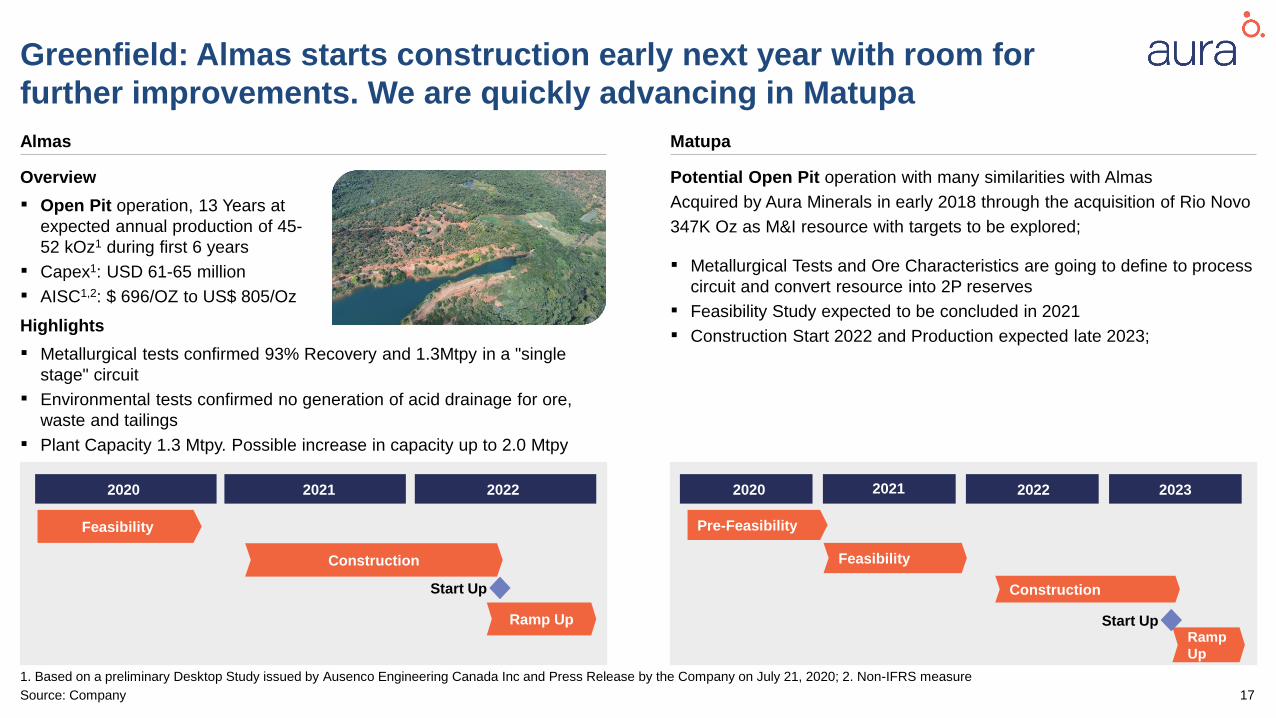

Greenfield: Almas starts construction early next year with room for

further improvements. We are quickly advancing in Matupa

Overview

Almas Matupa

▪ Open Pit operation, 13 Years at

expected annual production of 45-

52 kOz1 during first 6 years

▪ Capex1: USD 61-65 million

▪ AISC1,2: $ 696/OZ to US$ 805/Oz

Highlights

▪ Metallurgical tests confirmed 93% Recovery and 1.3Mtpy in a "single

stage" circuit

▪ Environmental tests confirmed no generation of acid drainage for ore,

waste and tailings

▪ Plant Capacity 1.3 Mtpy. Possible increase in capacity up to 2.0 Mtpy

Potential Open Pit operation with many similarities with Almas

Acquired by Aura Minerals in early 2018 through the acquisition of Rio Novo

347K Oz as M&I resource with targets to be explored;

▪ Metallurgical Tests and Ore Characteristics are going to define to process

circuit and convert resource into 2P reserves

▪ Feasibility Study expected to be concluded in 2021

▪ Construction Start 2022 and Production expected late 2023;

Feasibility

Construction

Ramp Up

2020

Pre-Feasibility

Feasibility

Start UpRamp

Up

Construction

1. Based on a preliminary Desktop Study issued by Ausenco Engineering Canada Inc and Press Release by the Company on July 21, 2020; 2. Non-IFRS measure

Source: Company

Start Up

2021 2022 2020 2022 20232021

AUGUST 2020 | AURA DAY

Transformation Office

Sergio Castanho – CTO

19

Transformation Office

1. People and Performance

Management

2. Exploration Geology 3. Business Development

and Innovation

The Transformation Office addresses the

strategic areas to transform the Company

growth and performance

20

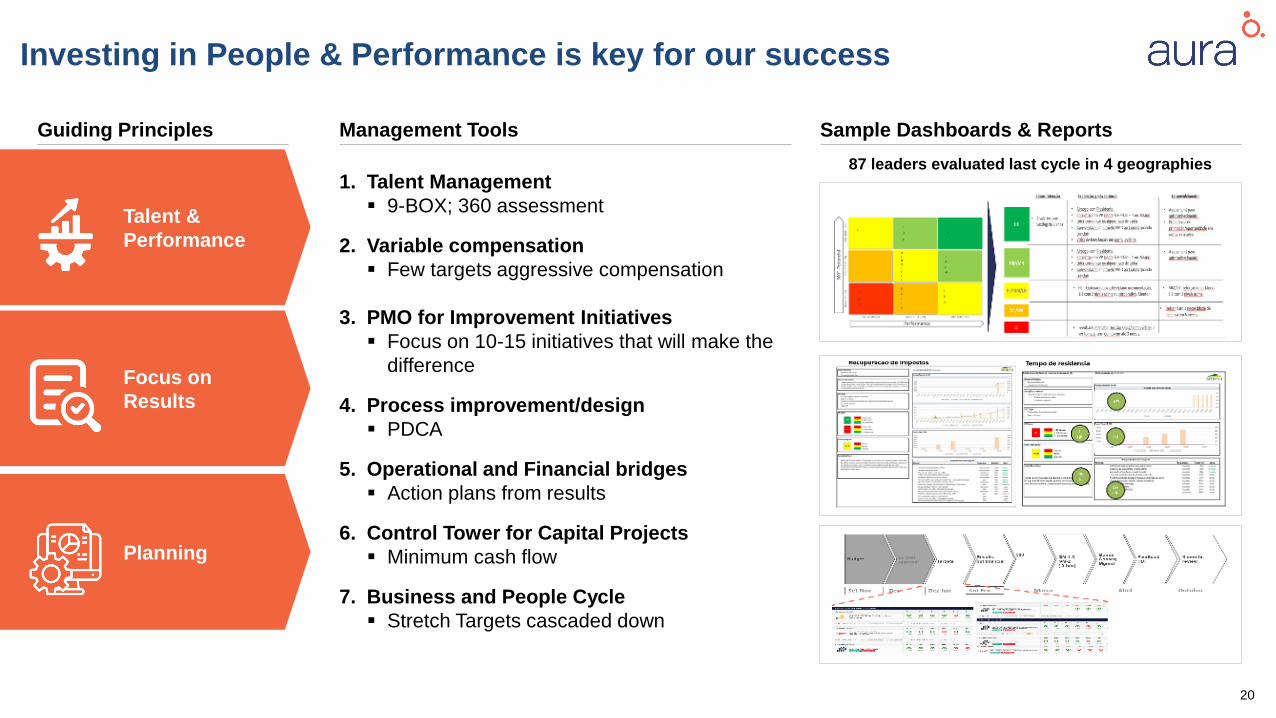

Investing in People & Performance is key for our success

87 leaders evaluated last cycle in 4 geographies

Sample Dashboards & ReportsGuiding Principles

Talent &

Performance

Planning

Management Tools

1. Talent Management

▪ 9-BOX; 360 assessment

2. Variable compensation

▪ Few targets aggressive compensation

3. PMO for Improvement Initiatives

▪ Focus on 10-15 initiatives that will make the

difference

4. Process improvement/design

▪ PDCA

5. Operational and Financial bridges

▪ Action plans from results

6. Control Tower for Capital Projects

▪ Minimum cash flow

7. Business and People Cycle

▪ Stretch Targets cascaded down

Focus on

Results

21

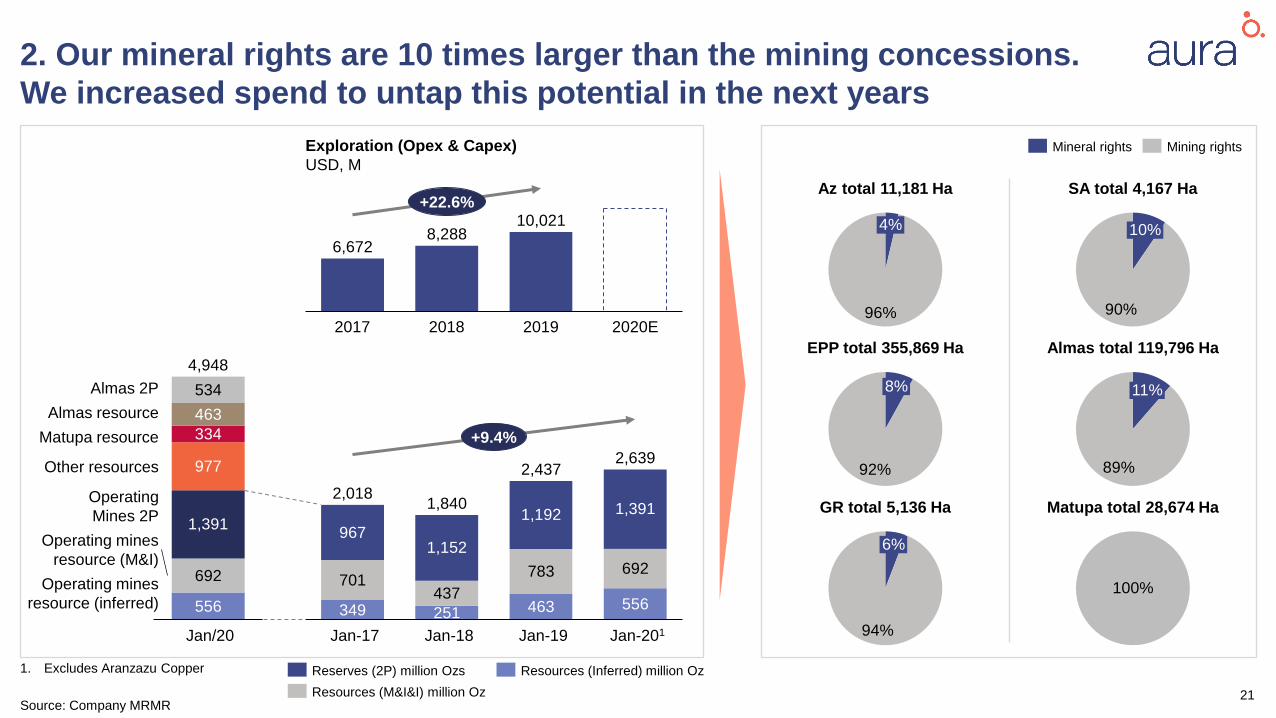

2. Our mineral rights are 10 times larger than the mining concessions.

We increased spend to untap this potential in the next years

1. Excludes Aranzazu Copper

Source: Company MRMR

96%

4%

90%

10%

92%

8%

89%

11%

94%

6%

100%

Mineral rights Mining rights

2017 2018 2020E2019

6,6728,288

10,021+22.6%

556

692

977

334

463

534

Jan/20

1,391

Almas 2P

Almas resource

Matupa resource

Other resources

Operating

Mines 2P

Operating mines

resource (M&I)

Operating mines

resource (inferred)

4,948

349 251 463 556

701437

783 692

967

Jan-201Jan-17

1,192

1,152

2,639

Jan-18

1,391

Jan-19

2,0181,840

2,437

+9.4%

Reserves (2P) million Ozs Resources (Inferred) million Oz

Resources (M&I&I) million Oz

Exploration (Opex & Capex)

USD, M

Az total 11,181 Ha SA total 4,167 Ha

EPP total 355,869 Ha Almas total 119,796 Ha

GR total 5,136 Ha Matupa total 28,674 Ha

22

As a result of recent investment, we already have interesting results

coming from the exploration work

Source: Company

AranzazuA

Down dip positive

hole at more than 200

meters deeper from

the known inferred

resources1

Conversion inferred

to M&I at better

grades than expected1

▪ GH down dip

completed & positive,

infill underway

▪ Well balanced

pipeline – El Cobre

ready for drilling and

other targets

identified

Upcoming:

▪ El Cobre start by EOY

Bananal South can add

significant LOM

Extensions of current

pits replacing reserves2

EPPB

▪ Completed initial

exploration drilling in

Bananal N

▪ Started infill in

Bananal S

▪ Kicked-off regional

program

Upcoming:

▪ Bananal infill results in

Q3

New exploration targets

by the end of the year

San AndresC

▪ Started Zona Bufa

▪ Started regional

mapping

Upcoming:

▪ Zona Bufa results in

Q4

The results of the first 4

drill holes confirmed

projected grade from

the inferred mineral

resources in the current

mine plan3

New targets identified

by the end of the year

Gold RoadD

▪ Initial results of

Phase I drilling

program

▪ Sharpe stope drilling

from surface started

Upcoming:

▪ Drilling results in Q4

Matupa working on

resources (Serrinha)

and Reserves (X1)

ProjectsE

▪ Increase resource

basis and confirm

porphyry in Matupá

Upcoming:

▪ Drilling start in Q3,

complete by Q4,

results in Q1 ‘21

See press release dated August 19, 2020 for further information; 2. See press release dated February 12, 2020 for further information; 3. See press release dated July14th, 2020 for further information

23

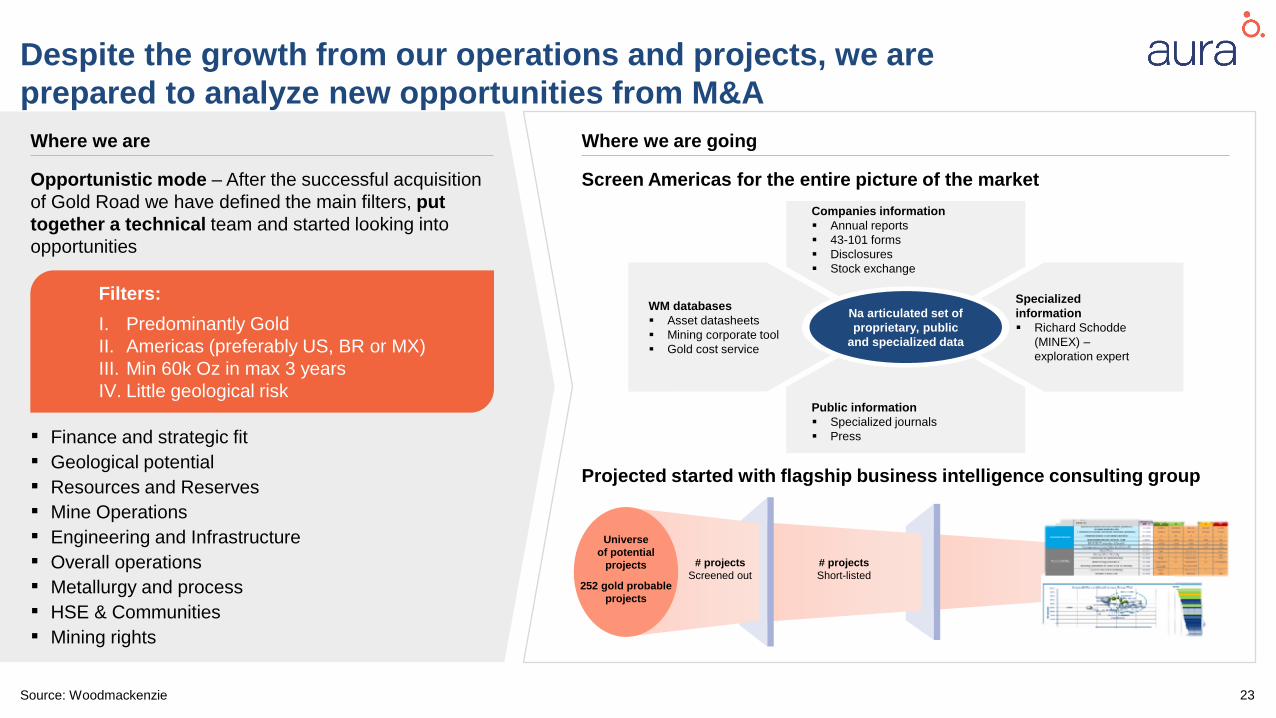

Despite the growth from our operations and projects, we are

prepared to analyze new opportunities from M&A

Source: Woodmackenzie

Where we are

Opportunistic mode – After the successful acquisition

of Gold Road we have defined the main filters, put

together a technical team and started looking into

opportunities

▪ Finance and strategic fit

▪ Geological potential

▪ Resources and Reserves

▪ Mine Operations

▪ Engineering and Infrastructure

▪ Overall operations

▪ Metallurgy and process

▪ HSE & Communities

▪ Mining rights

Filters:

I. Predominantly Gold

II. Americas (preferably US, BR or MX)

III. Min 60k Oz in max 3 years

IV. Little geological risk

Where we are going

Screen Americas for the entire picture of the market

Na articulated set of

proprietary, public

and specialized data

WM databases

▪ Asset datasheets

▪ Mining corporate tool

▪ Gold cost service

Specialized

information

▪ Richard Schodde

(MINEX) –

exploration expert

Companies information

▪ Annual reports

▪ 43-101 forms

▪ Disclosures

▪ Stock exchange

Public information

▪ Specialized journals

▪ Press

Universe

of potential

projects

252 gold probable

projects

# projects

Screened out

# projects

Short-listed

Projected started with flagship business intelligence consulting group

AUGUST 2020 | AURA DAY

Finance

Kleber Cardoso – CFO

25

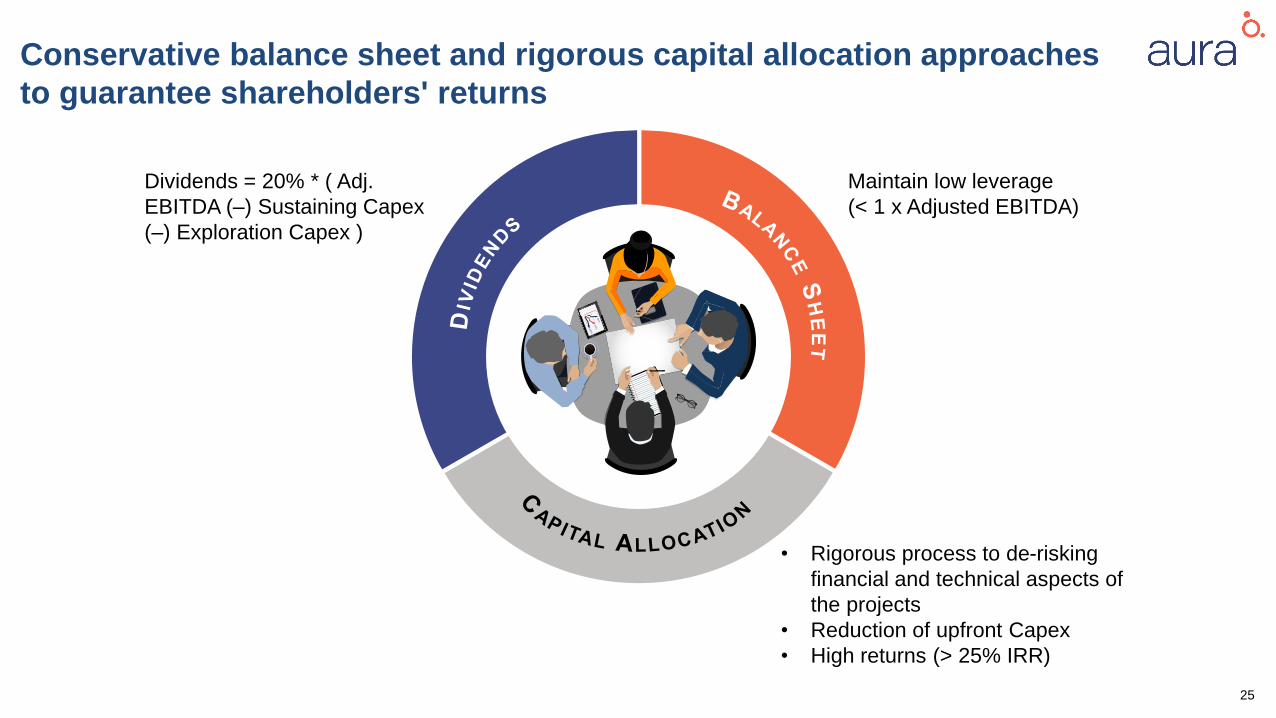

Conservative balance sheet and rigorous capital allocation approaches

to guarantee shareholders' returns

Dividends = 20% * ( Adj.

EBITDA (–) Sustaining Capex

(–) Exploration Capex )

Maintain low leverage

(< 1 x Adjusted EBITDA)

• Rigorous process to de-risking

financial and technical aspects of

the projects

• Reduction of upfront Capex

• High returns (> 25% IRR)

26

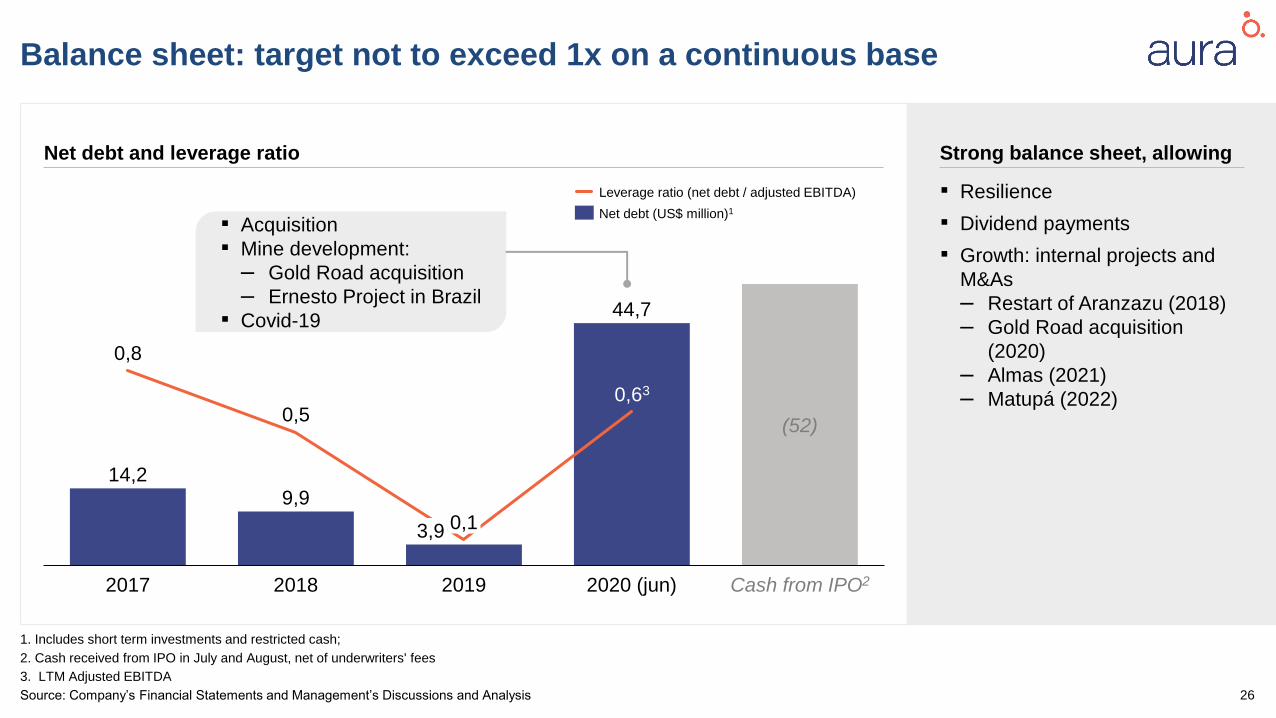

Balance sheet: target not to exceed 1x on a continuous base

1. Includes short term investments and restricted cash;

2. Cash received from IPO in July and August, net of underwriters' fees

3. LTM Adjusted EBITDA

Net debt and leverage ratio

0,8

0,5

9,9

0,1

20192017

14,2

2018

3,9

(52)

2020 (jun) Cash from IPO2

44,7

0,63

Leverage ratio (net debt / adjusted EBITDA)

Net debt (US$ million)1

▪ Acquisition

▪ Mine development:

– Gold Road acquisition

– Ernesto Project in Brazil

▪ Covid-19

▪ Resilience

▪ Dividend payments

▪ Growth: internal projects and

M&As

– Restart of Aranzazu (2018)

– Gold Road acquisition

(2020)

– Almas (2021)

– Matupá (2022)

Strong balance sheet, allowing

Source: Company’s Financial Statements and Management’s Discussions and Analysis

27

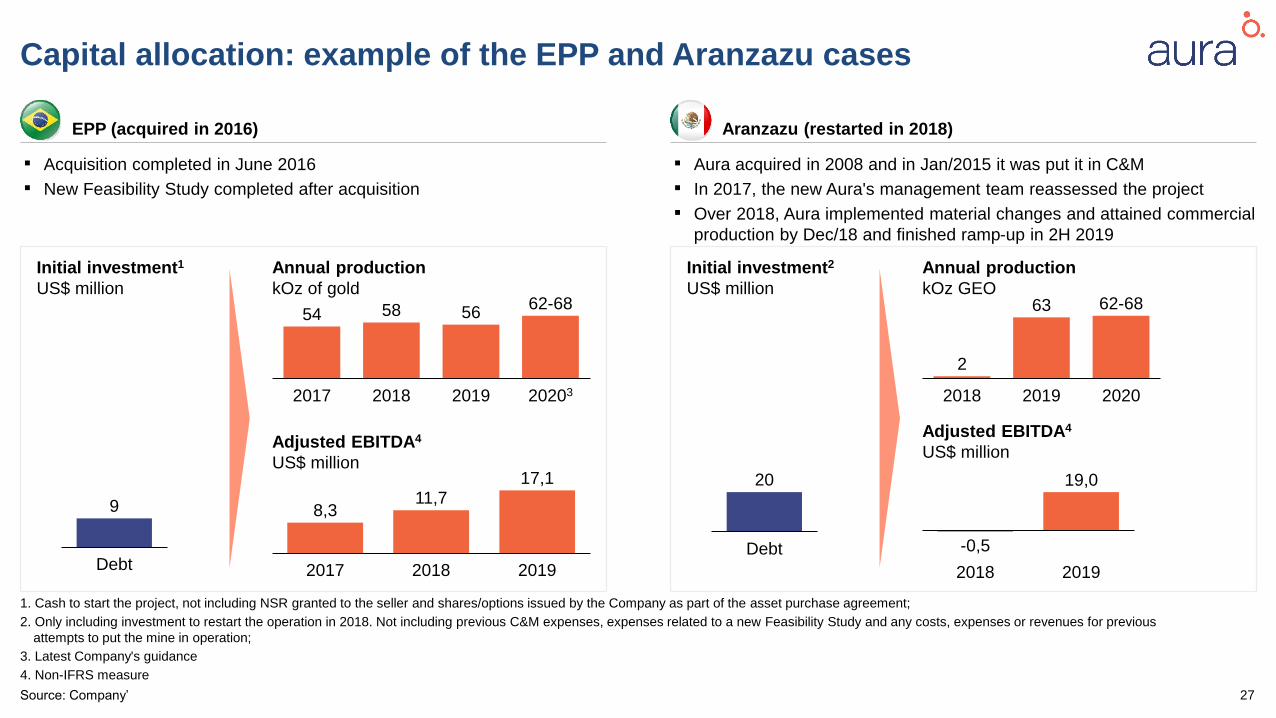

Capital allocation: example of the EPP and Aranzazu cases

1. Cash to start the project, not including NSR granted to the seller and shares/options issued by the Company as part of the asset purchase agreement;

2. Only including investment to restart the operation in 2018. Not including previous C&M expenses, expenses related to a new Feasibility Study and any costs, expenses or revenues for previous

attempts to put the mine in operation;

3. Latest Company's guidance

4. Non-IFRS measure

▪ Acquisition completed in June 2016

▪ New Feasibility Study completed after acquisition

EPP (acquired in 2016) Aranzazu (restarted in 2018)

▪ Aura acquired in 2008 and in Jan/2015 it was put it in C&M

▪ In 2017, the new Aura's management team reassessed the project

▪ Over 2018, Aura implemented material changes and attained commercial

production by Dec/18 and finished ramp-up in 2H 2019

Initial investment1

US$ million

Annual production

kOz of gold

Initial investment2

US$ million

Annual production

kOz GEO

Adjusted EBITDA4

US$ million

Adjusted EBITDA4

US$ million

9

Debt

17,1

2017 2018 2019

11,78,3

62-68

2017

5654

2018 202032019

58

20

Debt

2018 2019

-0,5

19,0

63

20192018 2020

2

62-68

Source: Company’

28

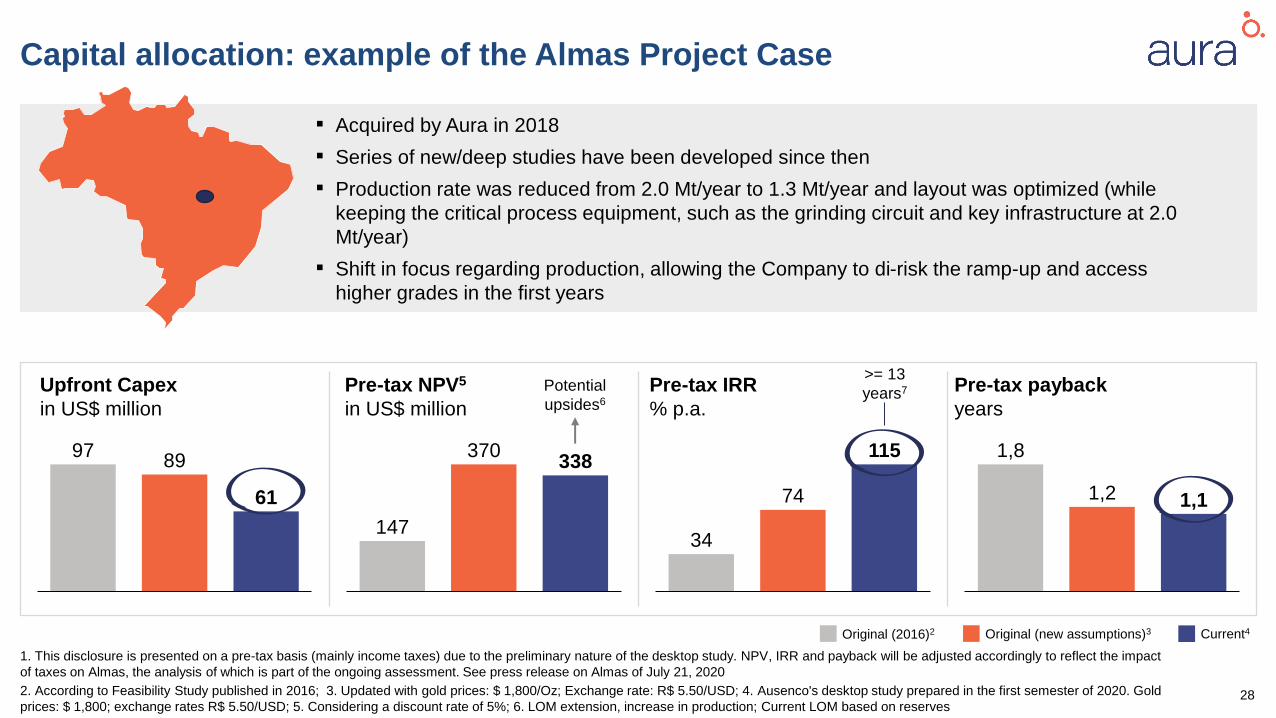

Capital allocation: example of the Almas Project Case

1. This disclosure is presented on a pre-tax basis (mainly income taxes) due to the preliminary nature of the desktop study. NPV, IRR and payback will be adjusted accordingly to reflect the impact

of taxes on Almas, the analysis of which is part of the ongoing assessment. See press release on Almas of July 21, 2020

2. According to Feasibility Study published in 2016; 3. Updated with gold prices: $ 1,800/Oz; Exchange rate: R$ 5.50/USD; 4. Ausenco's desktop study prepared in the first semester of 2020. Gold

prices: $ 1,800; exchange rates R$ 5.50/USD; 5. Considering a discount rate of 5%; 6. LOM extension, increase in production; Current LOM based on reserves

▪ Acquired by Aura in 2018

▪ Series of new/deep studies have been developed since then

▪ Production rate was reduced from 2.0 Mt/year to 1.3 Mt/year and layout was optimized (while

keeping the critical process equipment, such as the grinding circuit and key infrastructure at 2.0

Mt/year)

▪ Shift in focus regarding production, allowing the Company to di-risk the ramp-up and access

higher grades in the first years

Upfront Capex

in US$ million

Pre-tax NPV5

in US$ million

Pre-tax IRR

% p.a.

Pre-tax payback

years

9789

61

147

370338

34

74

115 1,8

1,2 1,1

Original (2016)2 Original (new assumptions)3 Current4

Potential

upsides6

>= 13

years7

AUGUST 2020 | AURA DAY

Final Comments

Rodrigo Barbosa – CEO

30

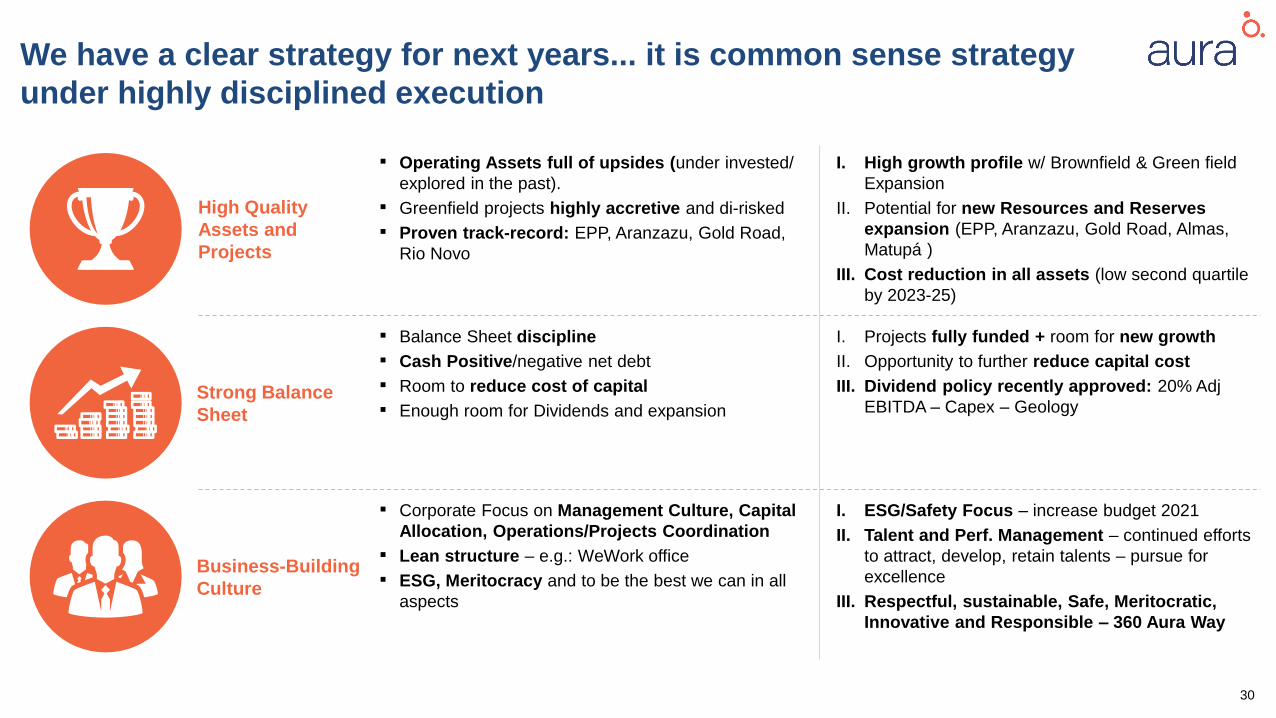

We have a clear strategy for next years... it is common sense strategy

under highly disciplined execution

High Quality

Assets and

Projects

▪ Operating Assets full of upsides (under invested/

explored in the past).

▪ Greenfield projects highly accretive and di-risked

▪ Proven track-record: EPP, Aranzazu, Gold Road,

Rio Novo

I. High growth profile w/ Brownfield & Green field

Expansion

II. Potential for new Resources and Reserves

expansion (EPP, Aranzazu, Gold Road, Almas,

Matupá )

III. Cost reduction in all assets (low second quartile

by 2023-25)

Strong Balance

Sheet

▪ Balance Sheet discipline

▪ Cash Positive/negative net debt

▪ Room to reduce cost of capital

▪ Enough room for Dividends and expansion

I. Projects fully funded + room for new growth

II. Opportunity to further reduce capital cost

III. Dividend policy recently approved: 20% Adj

EBITDA – Capex – Geology

Business-Building

Culture

▪ Corporate Focus on Management Culture, Capital

Allocation, Operations/Projects Coordination

▪ Lean structure – e.g.: WeWork office

▪ ESG, Meritocracy and to be the best we can in all

aspects

I. ESG/Safety Focus – increase budget 2021

II. Talent and Perf. Management – continued efforts

to attract, develop, retain talents – pursue for

excellence

III. Respectful, sustainable, Safe, Meritocratic,

Innovative and Responsible – 360 Aura Way

August 20, 2020

"To find, mine and deliver the planet's most

important and essential minerals that enable the

world and humankind to create, innovate, and

prosper"

THANK YOU!