Embed Size (px)

Citation preview

Middle East : Windows of Opportunity

Growth Markets Webcast Seriesby PwC’s Growth Markets Centre

PwC

17 November 20162

Middle East - Windows of Opportunity

Welcome & Introductions

PwC

17 November 2016

Speakers

3Middle East - Windows of Opportunity

Stephen Anderson

Partner

Consulting

Martin Berlin

Partner

Deals

Nadine Bassil

Director

Tax and Regulatory

David Wijeratne

Leader

Growth Markets Centre

Nicolas Boukhalil

Director

Deals

Picture to be

added

PwC

17 November 2016

Agenda

4Middle East - Windows of Opportunity

The Middle Eastern economy in the global context

1

Overview of Middle Eastern markets

2

Opportunities and challenges in key growth sectors

3The tax and regulatory environment in the Middle East

4

PwC in the Middle East

5 6

PwC’s Growth Markets Centre

6

PwC

17 November 2016

The Middle Eastern economy in the global context

5Middle East - Windows of Opportunity

1. The Middle Eastern economy in the global context

PwC

17 November 2016

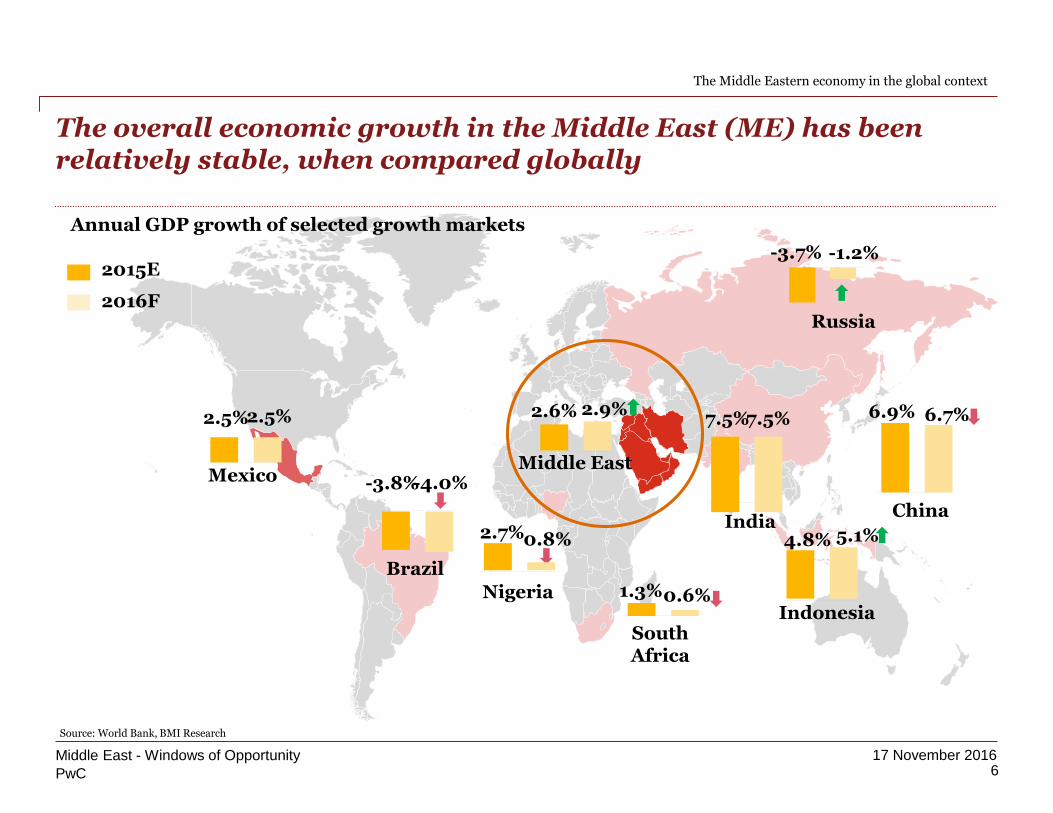

The overall economic growth in the Middle East (ME) has been relatively stable, when compared globally

6Middle East - Windows of Opportunity

2.5%2.5%

Mexico -3.8%-4.0%

Brazil

2.7%0.8%

Nigeria

4.8% 5.1%

Indonesia

6.9% 6.7%

China

Annual GDP growth of selected growth markets

2015E

2016F

7.5%7.5%

India

-3.7% -1.2%

2.6% 2.9%

Middle East

1.3%0.6%

South Africa

Russia

Source: World Bank, BMI Research

The Middle Eastern economy in the global context

PwC

17 November 2016

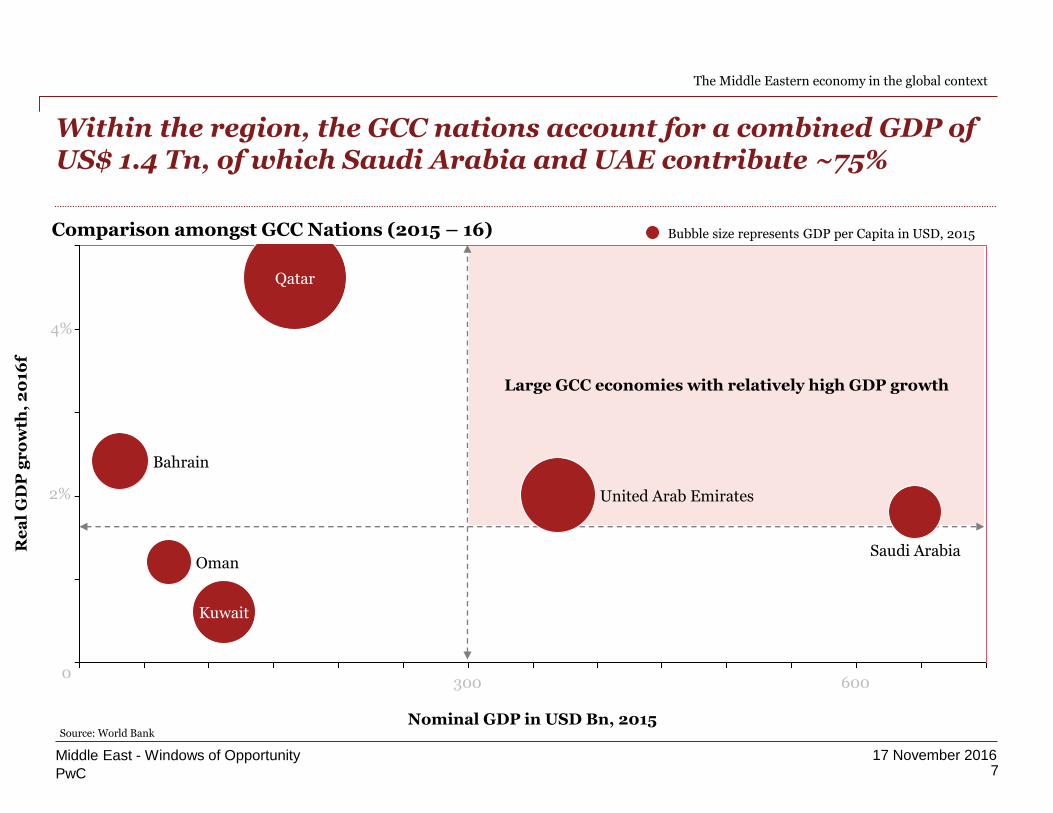

Large GCC economies with relatively high GDP growth

7Middle East - Windows of Opportunity

The Middle Eastern economy in the global context

Within the region, the GCC nations account for a combined GDP of US$ 1.4 Tn, of which Saudi Arabia and UAE contribute ~75%

Comparison amongst GCC Nations (2015 – 16)

Source: World Bank

1.0

1.5

2.0

2.5

3.0

3.5

0 50 100 150 200 250 300 350 400 450 500 550 600 650 700

United Arab Emirates

Saudi Arabia

Qatar

Oman

Kuwait

Bahrain

Re

al

GD

P g

ro

wth

, 2

016

f

Nominal GDP in USD Bn, 2015

Bubble size represents GDP per Capita in USD, 2015

300 6000

2%

4%

PwC

17 November 2016

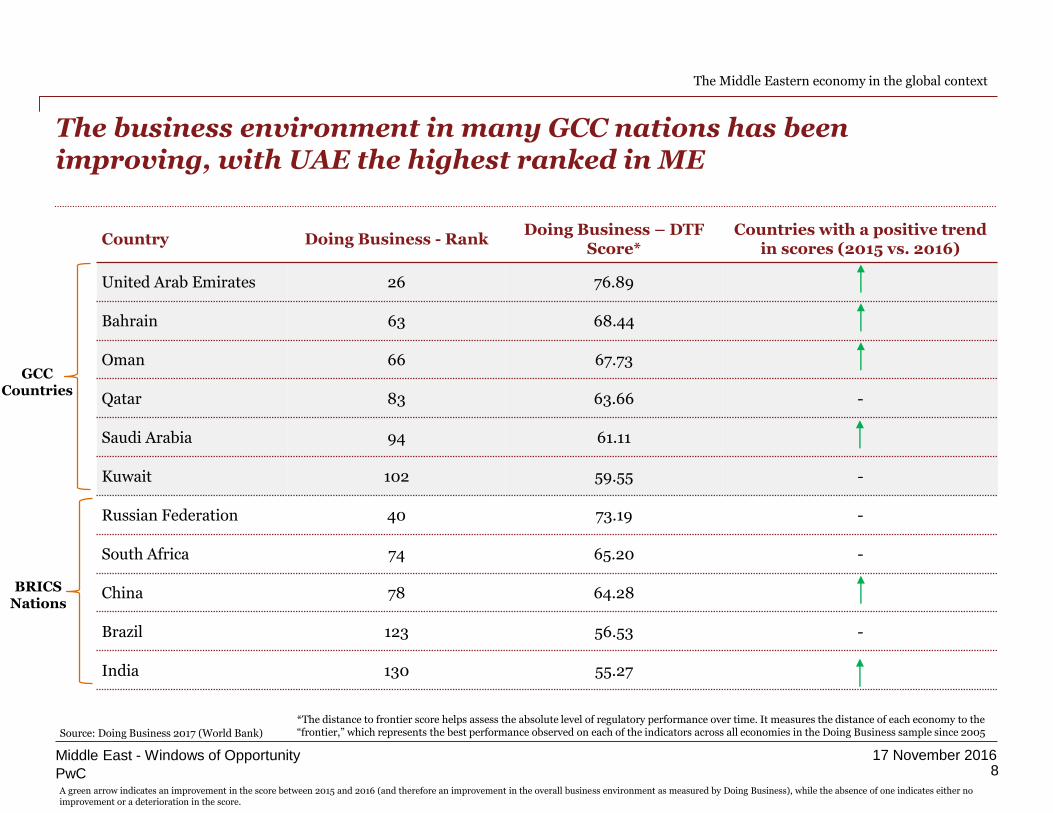

Country Doing Business - RankDoing Business – DTF

Score*Countries with a positive trend

in scores (2015 vs. 2016)

United Arab Emirates 26 76.89

Bahrain 63 68.44

Oman 66 67.73

Qatar 83 63.66 -

Saudi Arabia 94 61.11

Kuwait 102 59.55 -

Russian Federation 40 73.19 -

South Africa 74 65.20 -

China 78 64.28

Brazil 123 56.53 -

India 130 55.27

The business environment in many GCC nations has been improving, with UAE the highest ranked in ME

8Middle East - Windows of Opportunity

Source: Doing Business 2017 (World Bank)

GCC Countries

BRICS Nations

The Middle Eastern economy in the global context

A green arrow indicates an improvement in the score between 2015 and 2016 (and therefore an improvement in the overall business environment as measured by Doing Business), while the absence of one indicates either no improvement or a deterioration in the score.

*The distance to frontier score helps assess the absolute level of regulatory performance over time. It measures the distance of each economy to the “frontier,” which represents the best performance observed on each of the indicators across all economies in the Doing Business sample since 2005

PwC

17 November 2016

2.0%

1.6%

1.9%

3.5%

2.0%

2.4%

1.9%

2.4%2.6%

4.0%

2.3%

3.0%

Bahrain Kuwait Oman Qatar Saudi Arabia United ArabEmirates

GDP Growth Forecast for GCC Countries

2017F 2018F

This is expected to have a positive impact on economic growth, creating opportunities for investment in future

9Middle East - Windows of Opportunity

Source: World Bank Global Economic Prospects, June 2016

The Middle Eastern economy in the global context

2. Overview of Middle Eastern markets

PwC

17 November 2016

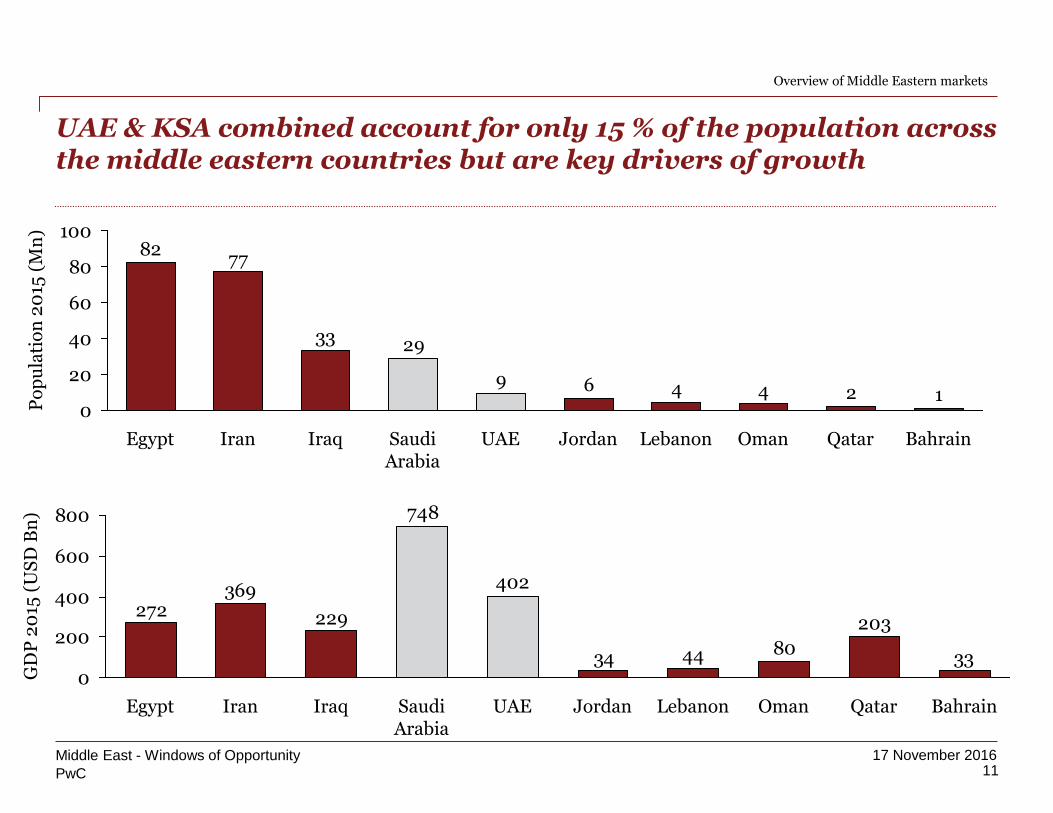

UAE & KSA combined account for only 15 % of the population across the middle eastern countries but are key drivers of growth

124469

2933

7782

0

20

40

60

80

100

Saudi Arabia

UAE Jordan Lebanon Oman Qatar BahrainEgypt IraqIran

Po

pu

lati

on

20

15 (

Mn

)

33

203

804434

402

748

229

369272

0

200

400

600

800

IraqIranEgypt Saudi Arabia

UAE Jordan Lebanon Oman Qatar Bahrain

GD

P 2

015

(U

SD

Bn

)

11Middle East - Windows of Opportunity

Overview of Middle Eastern markets

PwC

17 November 2016

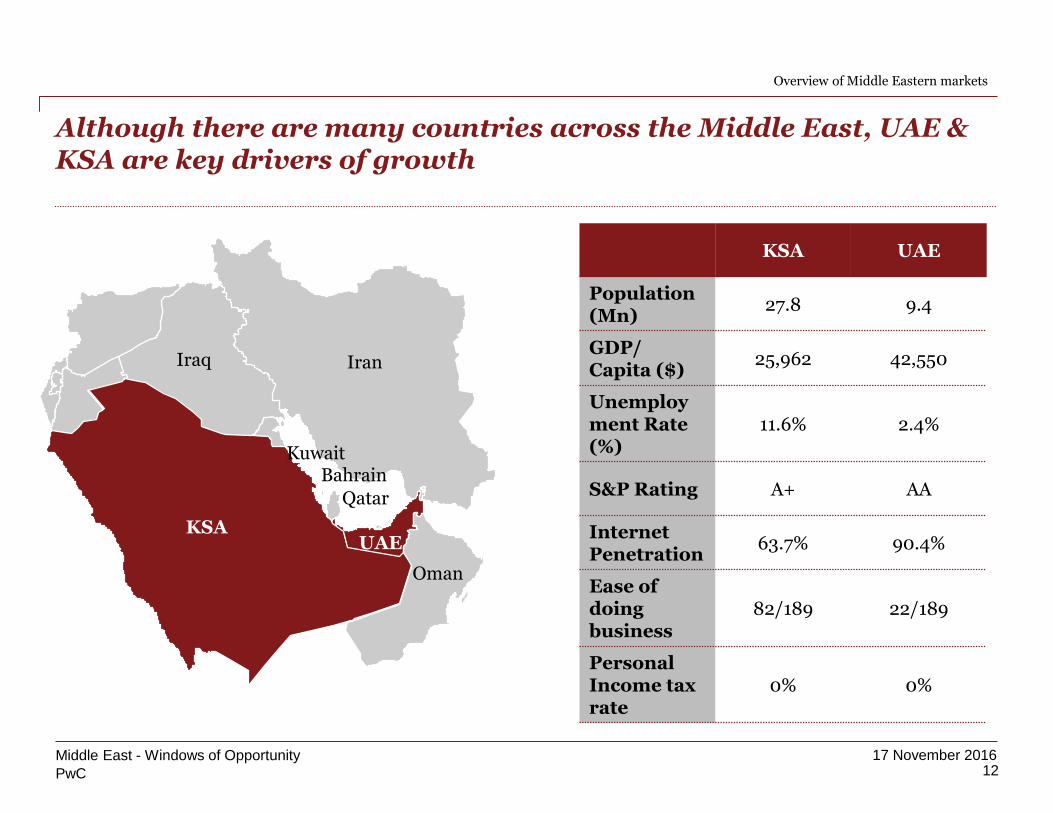

Although there are many countries across the Middle East, UAE & KSA are key drivers of growth

12Middle East - Windows of Opportunity

KSA

Kuwait

Qatar

Bahrain

UAE

Oman

IranIraq

KSA UAE

Population (Mn)

27.8 9.4

GDP/ Capita ($)

25,962 42,550

Unemployment Rate (%)

11.6% 2.4%

S&P Rating A+ AA

InternetPenetration

63.7% 90.4%

Ease of doing business

82/189 22/189

Personal Income tax rate

0% 0%

Overview of Middle Eastern markets

PwC

17 November 2016

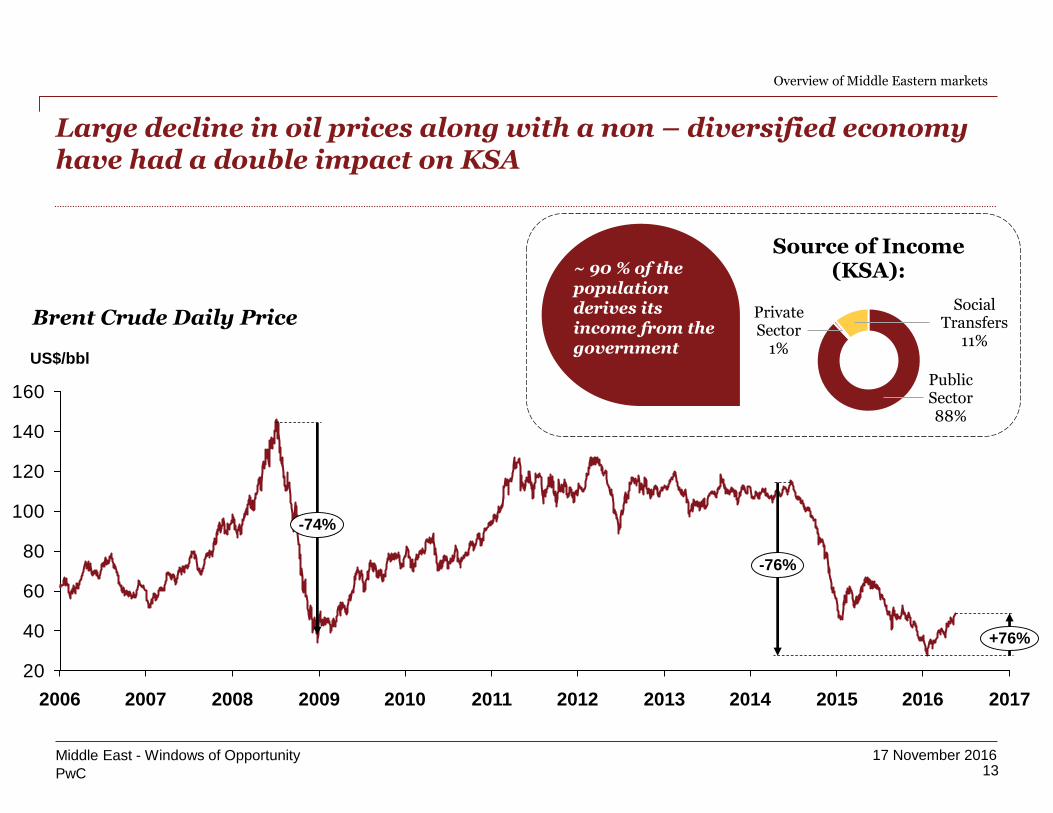

20

40

60

80

100

120

140

160

200820072006 201720162015201420132012201120102009

+76%

-76%

-74%

US$/bbl

Public Sector88%

Private Sector

1%

Social Transfers

11%

Source of Income (KSA):

Large decline in oil prices along with a non – diversified economy have had a double impact on KSA

13Middle East - Windows of Opportunity

Brent Crude Daily Price

~ 90 % of the population derives its income from the government

Overview of Middle Eastern markets

PwC

17 November 2016

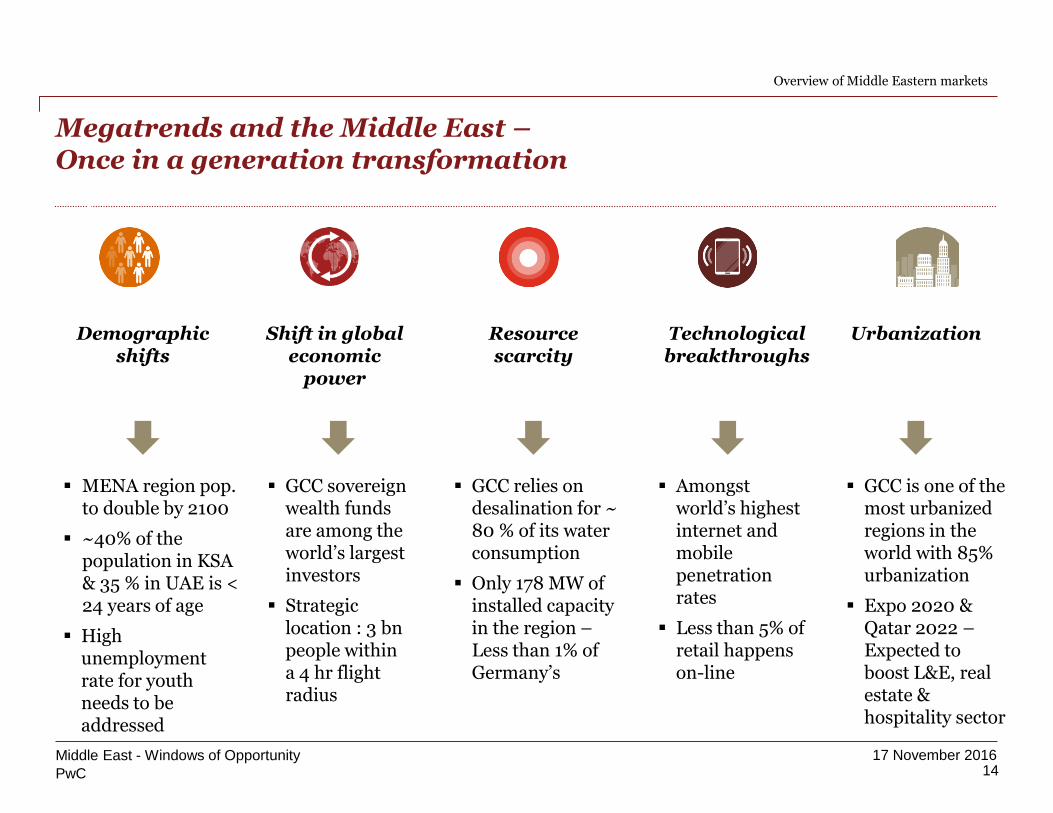

Megatrends and the Middle East –Once in a generation transformation

14Middle East - Windows of Opportunity

Demographicshifts

MENA region pop. to double by 2100

~40% of the population in KSA & 35 % in UAE is < 24 years of age

High unemployment rate for youth needs to be addressed

Resource scarcity

GCC relies on desalination for ~ 80 % of its water consumption

Only 178 MW of installed capacity in the region –Less than 1% of Germany’s

Shift in global economic

power

GCC sovereign wealth funds are among the world’s largest investors

Strategic location : 3 bn people within a 4 hr flight radius

Technologicalbreakthroughs

Amongst world’s highest internet and mobile penetration rates

Less than 5% of retail happens on-line

Urbanization

GCC is one of the most urbanized regions in the world with 85% urbanization

Expo 2020 & Qatar 2022 –Expected to boost L&E, real estate & hospitality sector

Overview of Middle Eastern markets

PwC

17 November 2016

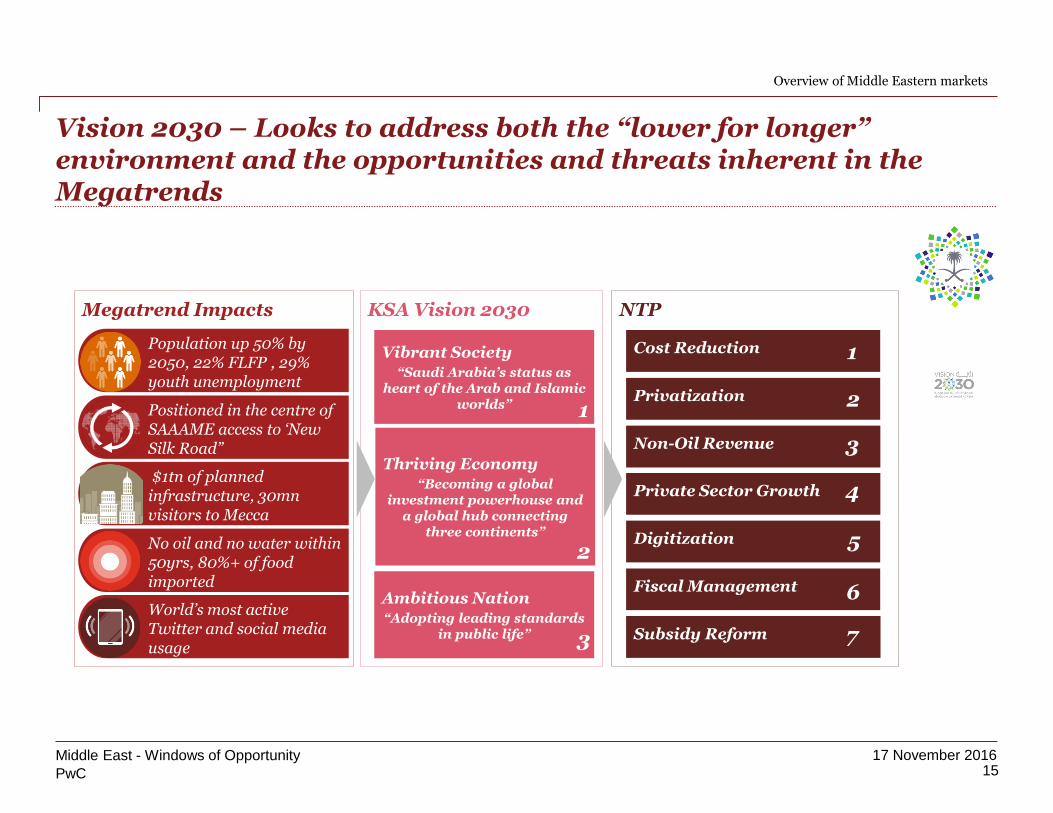

Vision 2030 – Looks to address both the “lower for longer” environment and the opportunities and threats inherent in the Megatrends

15Middle East - Windows of Opportunity

Overview of Middle Eastern markets

KSA Vision 2030 NTP

Vibrant Society“Saudi Arabia’s status as

heart of the Arab and Islamic worlds”

Thriving Economy“Becoming a global

investment powerhouse and a global hub connecting

three continents”

Ambitious Nation“Adopting leading standards

in public life”

1

2

3

Cost Reduction

Privatization

Non-Oil Revenue

Private Sector Growth

Digitization

Fiscal Management

Subsidy Reform

1

2

3

4

5

6

7

Megatrend Impacts

Population up 50% by 2050, 22% FLFP , 29% youth unemployment

Health and education deficienciesPositioned in the centre of SAAAME access to ‘New Silk Road”

$1tn of planned infrastructure, 30mn visitors to Mecca

No oil and no water within 50yrs, 80%+ of food imported

World’s most active Twitter and social media usage

PwC

17 November 2016

Opportunities and challenges in key growth sectors

16Middle East - Windows of Opportunity

3. Opportunities and challenges in key growth sectors

PwC

17 November 2016

Leisure

There are several sectors that are key engines of growth across the Middle East

17Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

Government/ Public Services

Real Estate

Energy, Utilities & Mining

Hospitality

Sovereign Wealth Funds

PwC

17 November 2016

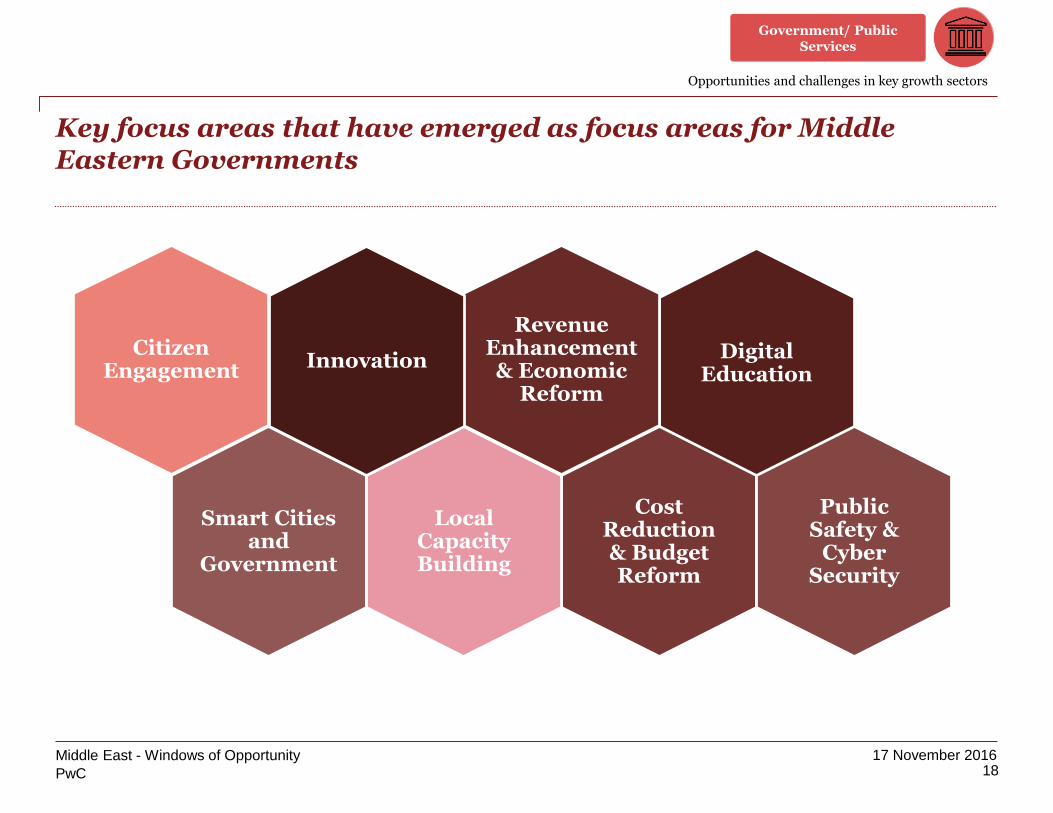

Key focus areas that have emerged as focus areas for Middle Eastern Governments

18Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

Digital Education

Revenue Enhancement & Economic

Reform

Cost Reduction & Budget Reform

Public Safety &

Cyber Security

Smart Cities and

Government

Local Capacity Building

Citizen Engagement Innovation

Government/ Public Services

PwC

17 November 2016

Government Practice Sectors and Themes

19Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

We continue to explore and build capacities in new areas while enhancing our existing sectors/themes taking in consideration current trends and need by ME Governments and public entities

Cities & Local Government

Labor MarketPublic Safety, Security

& JusticeEducation

Strategy Institutional Transformation

MEPSI Economic Development SPMOs

Current Sectors/Themes within G&PS

New Sectors/Themes for FY17

Public FinancePublic Service Delivery Social Affairs

Foreign Affairs National Agendas Defence

Government/ Public Services

PwC

17 November 2016

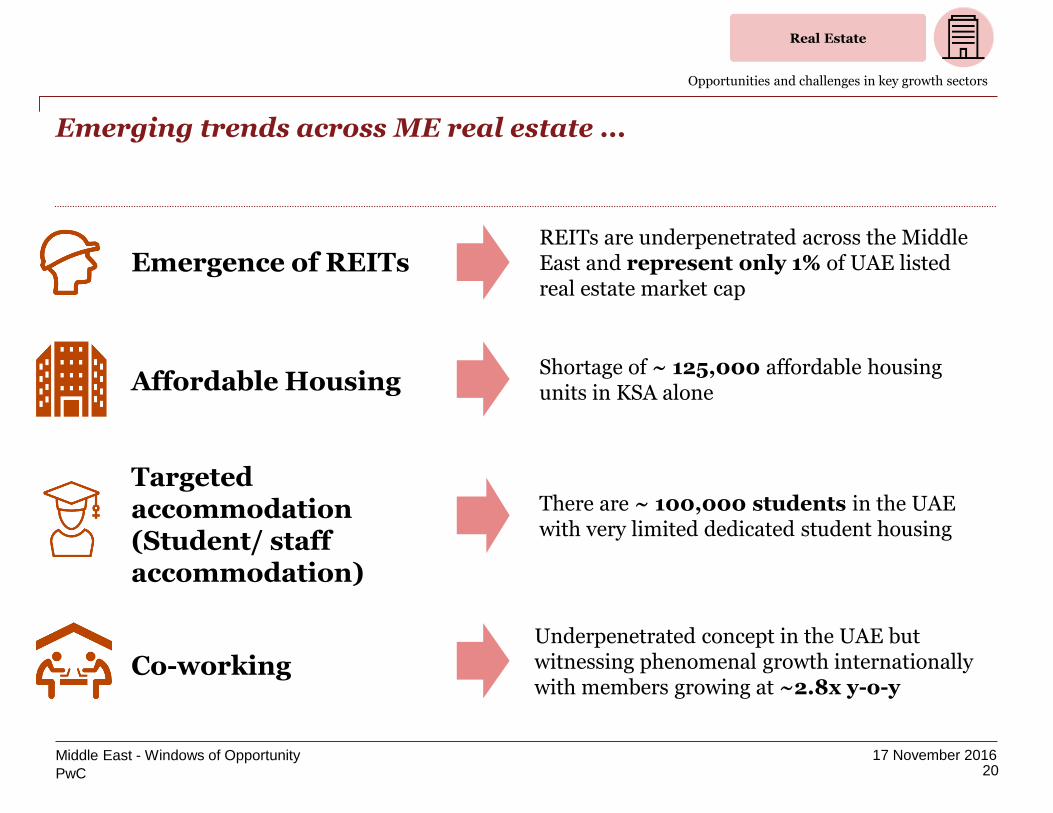

Emerging trends across ME real estate ...

20Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

There are ~ 100,000 students in the UAE with very limited dedicated student housing

REITs are underpenetrated across the Middle East and represent only 1% of UAE listed real estate market cap

Underpenetrated concept in the UAE but witnessing phenomenal growth internationally with members growing at ~2.8x y-o-y

Shortage of ~ 125,000 affordable housing units in KSA alone

Emergence of REITs

Affordable Housing

Co-working

Targeted accommodation (Student/ staff accommodation)

Real Estate

PwC

17 November 2016

REITs are currently underpenetrated in the UAE and represent a significant market opportunity

21Middle East - Windows of Opportunity

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Fin

lan

d

Ma

lay

sia

Irel

an

d

Ca

na

da

Fra

nce

Bel

giu

m

Sp

ain

Ge

rma

ny

Ho

ng

Ko

ng

Ja

pa

n

Sin

ga

po

re

UK

US

Ita

ly

Mex

ico

Net

her

lan

ds

UA

E

Au

stra

lia

So

uth

Afr

ica

Non- REITs

REITs

REIT market cap as a % age of listed real estate market cap

Source: SNL Financial, PwC Analysis

Opportunities and challenges in key growth sectors

1,100300

550

4400

500

1,000

1,500

2,000

2016

US

740

Excluding US

1,650

2010

REIT market cap by market (US $ Bn)

Real Estate

PwC

17 November 2016

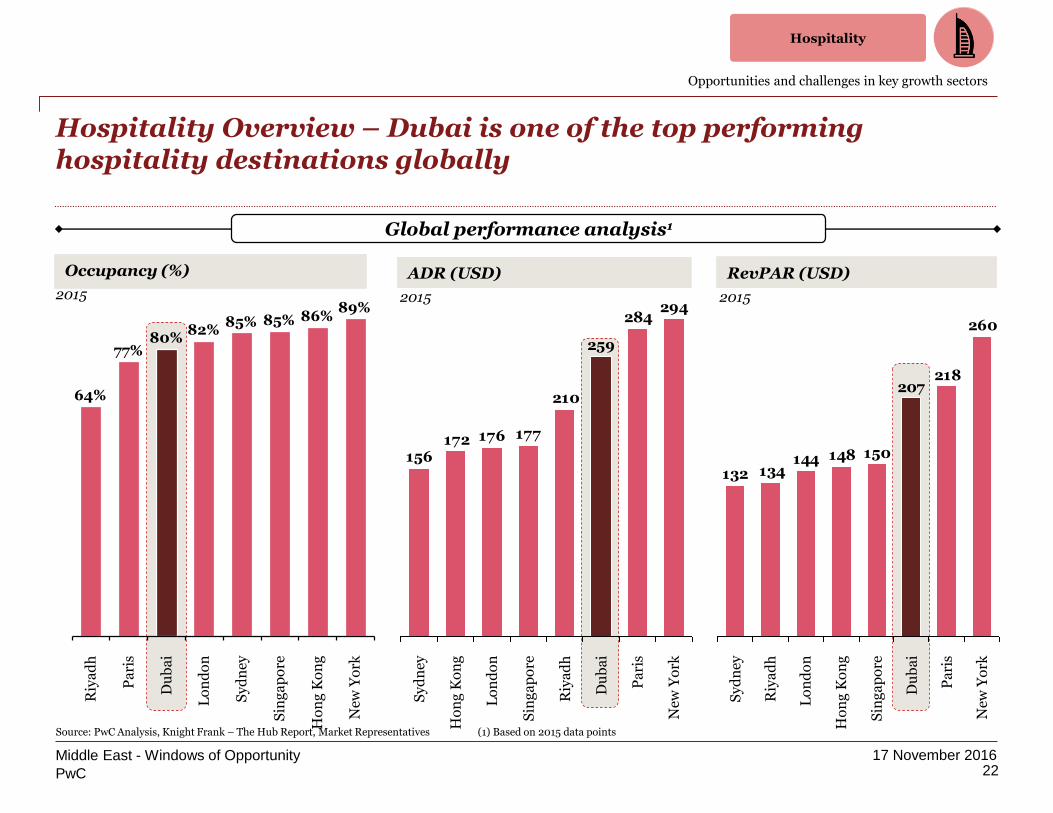

Hospitality Overview – Dubai is one of the top performing hospitality destinations globally

22Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

Ho

ng

Ko

ng

86%

New

Yo

rk

89%

Sin

ga

po

re

85%

Sy

dn

ey

85%

Lo

nd

on

82%

Pa

ris

77%

Du

ba

i

80%

Riy

ad

h

64%

294284

259

210

177176172156

Ho

ng

Ko

ng

New

Yo

rk

Sin

ga

po

re

Sy

dn

ey

Lo

nd

on

Pa

ris

Du

ba

i

Riy

ad

h

2015 2015

Global performance analysis1

Source: PwC Analysis, Knight Frank – The Hub Report, Market Representatives (1) Based on 2015 data points

Occupancy (%) ADR (USD) RevPAR (USD)

260

218207

150148144134132

New

Yo

rk

Ho

ng

Ko

ng

Sin

ga

po

re

Pa

ris

Du

ba

i

Lo

nd

on

Sy

dn

ey

Riy

ad

h

2015

Hospitality

PwC

17 November 2016

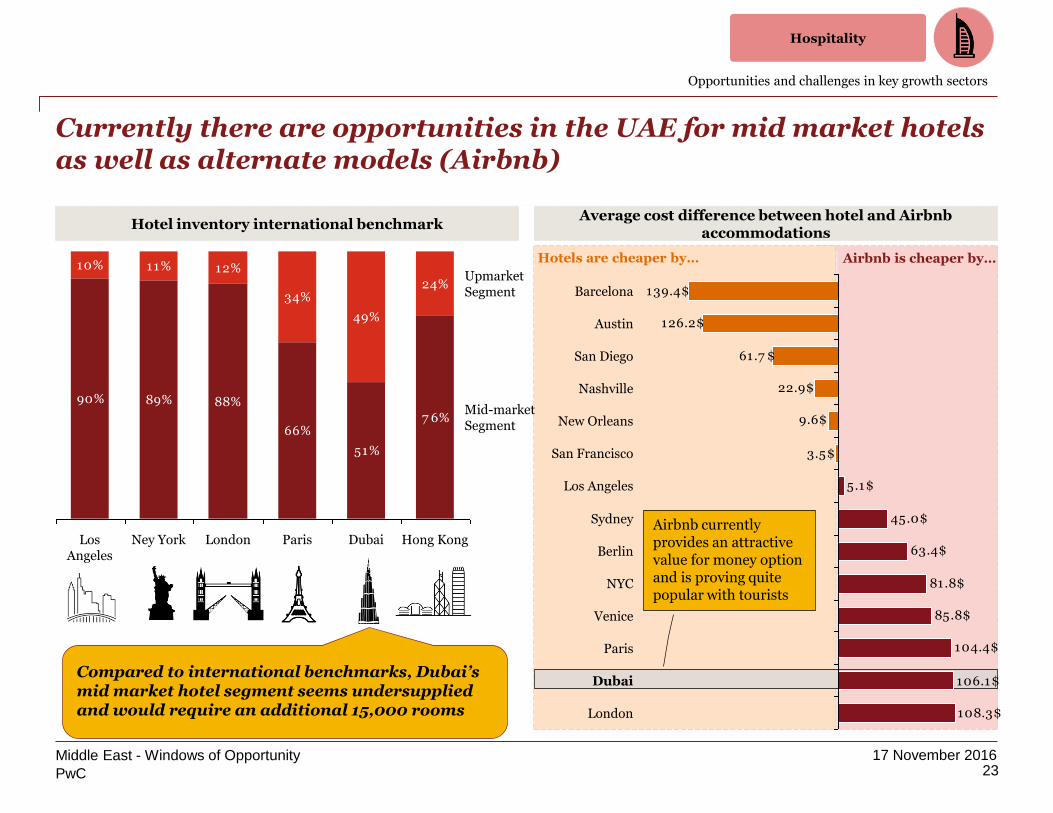

Currently there are opportunities in the UAE for mid market hotels as well as alternate models (Airbnb)

23Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

Hotel inventory international benchmarkAverage cost difference between hotel and Airbnb

accommodations

Hotels are cheaper by… Airbnb is cheaper by…

108.3$

106.1$

104.4$

85.8$

81.8$

63.4$

45.0$

5.1$

3.5$

9.6$

22.9$

61.7 $

126.2$

139.4$

Berlin

Sydney

Nashville

San Diego

Austin

Barcelona

Los Angeles

San Francisco

New Orleans

London

Dubai

Paris

Venice

NYC

90% 89% 88%

66%

51%

7 6%

10% 11% 12%

34%

49%

24%

LondonLos Angeles

UpmarketSegment

Mid-marketSegment

Paris Dubai Hong KongNey York

Compared to international benchmarks, Dubai’s mid market hotel segment seems undersupplied and would require an additional 15,000 rooms

Airbnb currently provides an attractive value for money option and is proving quite popular with tourists

Hospitality

PwC

17 November 2016

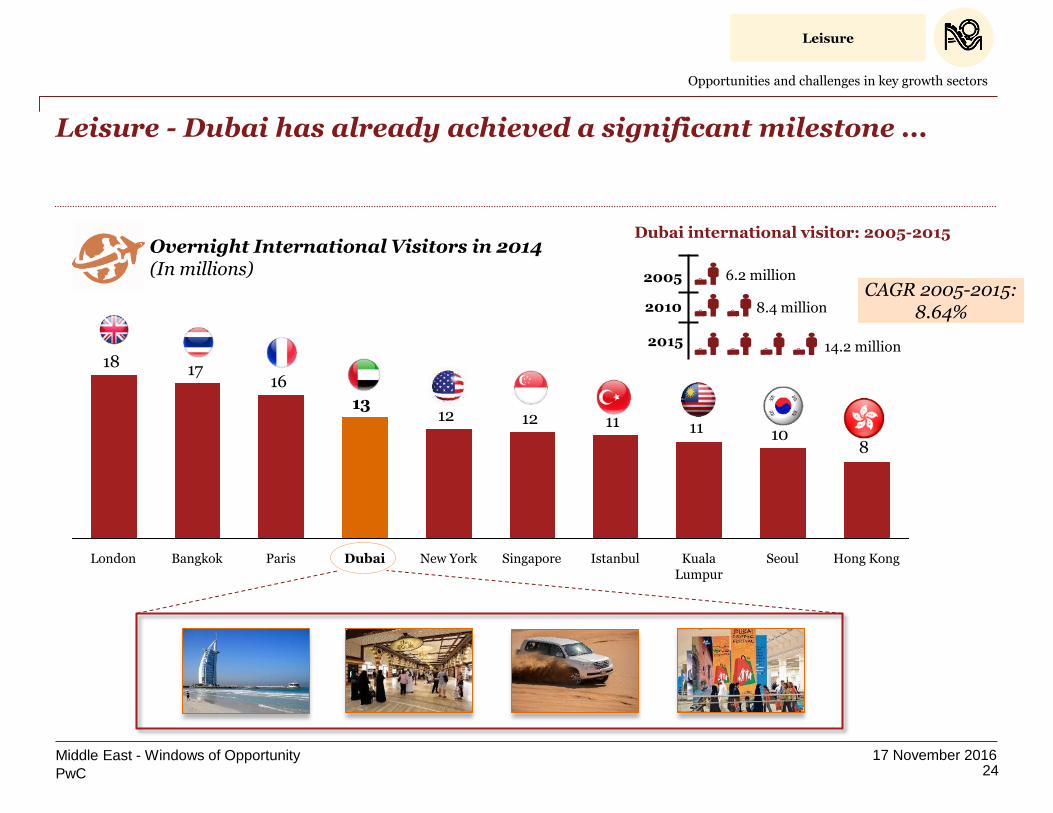

Leisure - Dubai has already achieved a significant milestone ...

24Middle East - Windows of Opportunity

Overnight International Visitors in 2014(In millions)

81011111212

161718

13

SeoulIstanbulDubaiBangkok Kuala Lumpur

Hong KongNew YorkLondon SingaporeParis

Opportunities and challenges in key growth sectors

Dubai international visitor: 2005-2015

2005 6.2 million

2010

2015

8.4 million

14.2 million

CAGR 2005-2015: 8.64%

Leisure

PwC

17 November 201625

Middle East - Windows of Opportunity

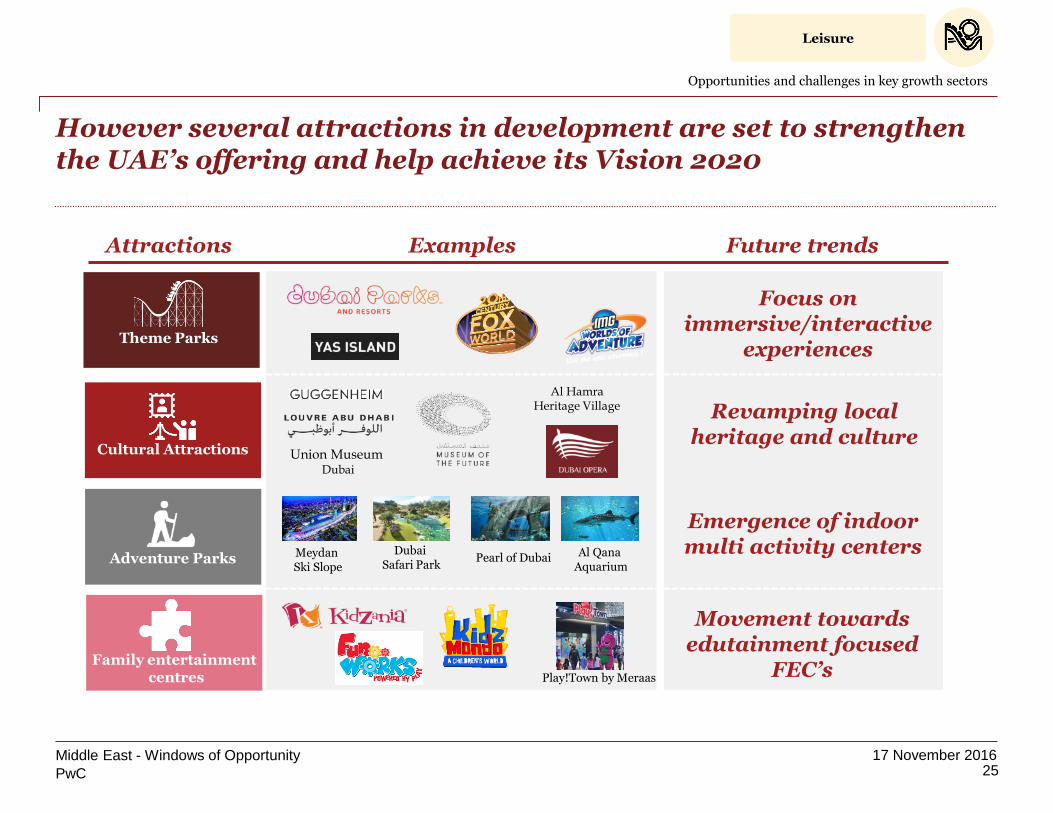

However several attractions in development are set to strengthen the UAE’s offering and help achieve its Vision 2020

Theme Parks

Cultural Attractions

Adventure Parks

Family entertainmentcentres

Al Hamra Heritage Village

Union MuseumDubai

Meydan Ski Slope

Dubai Safari Park

Pearl of Dubai

Attractions Examples

Al Qana Aquarium

Focus on immersive/interactive

experiences

Revamping local heritage and culture

Emergence of indoor multi activity centers

Movement towards edutainment focused

FEC’s

Future trends

Play!Town by Meraas

Opportunities and challenges in key growth sectors

Leisure

PwC

17 November 2016

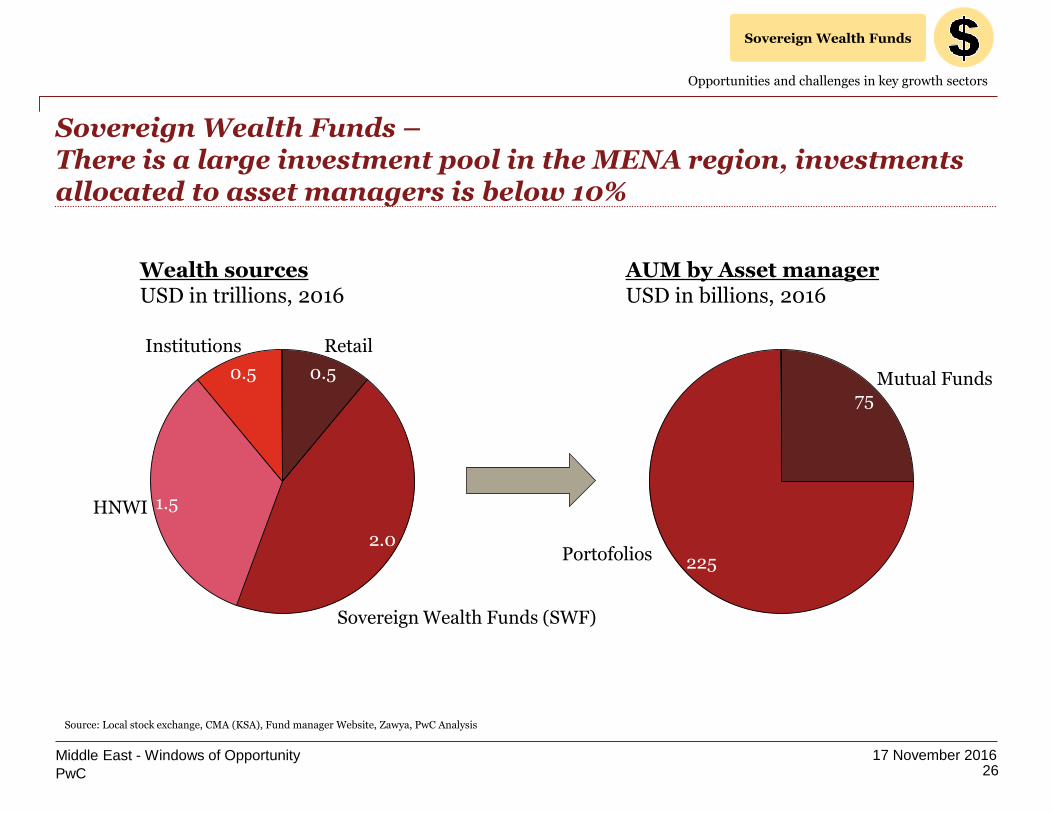

Sovereign Wealth Funds –There is a large investment pool in the MENA region, investments allocated to asset managers is below 10%

26Middle East - Windows of Opportunity

Opportunities and challenges in key growth sectors

Wealth sourcesUSD in trillions, 2016

AUM by Asset manager USD in billions, 2016

0.5

2.0

1.5

Institutions Retail

HNWI

Sovereign Wealth Funds (SWF)

0.5

225

75Mutual Funds

Portofolios

Source: Local stock exchange, CMA (KSA), Fund manager Website, Zawya, PwC Analysis

Sovereign Wealth Funds

PwC

17 November 201627

Middle East - Windows of Opportunity

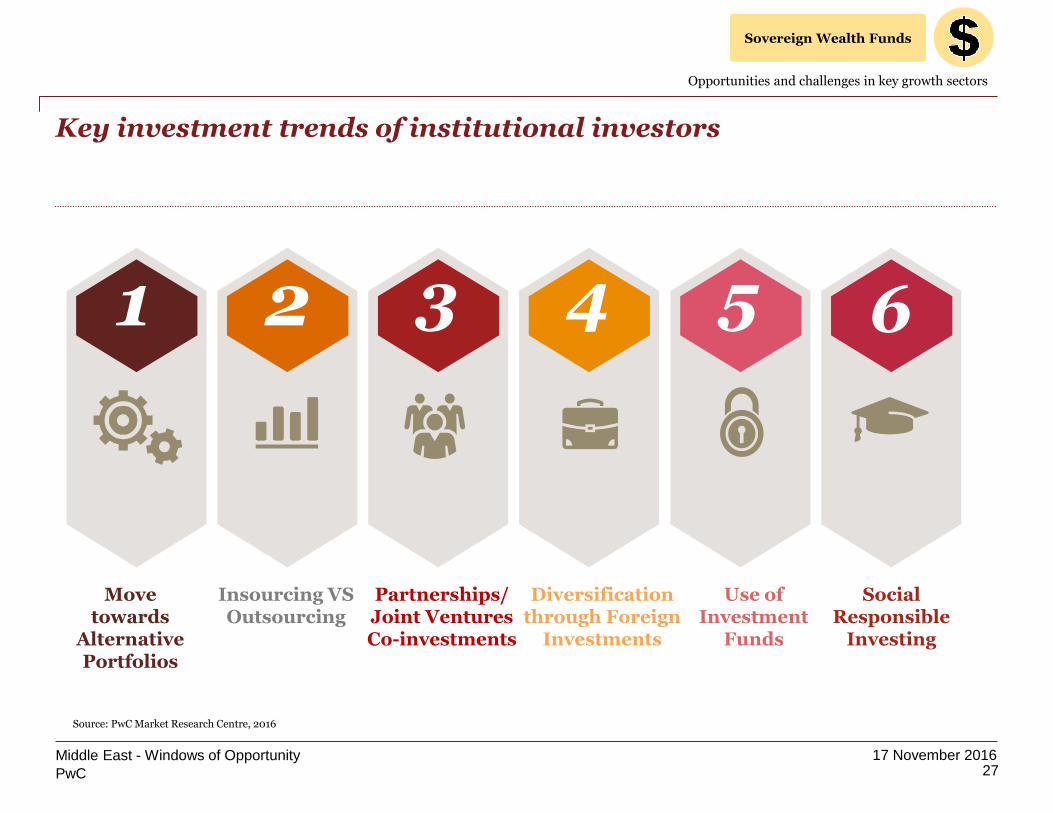

Key investment trends of institutional investors

Source: PwC Market Research Centre, 2016

1 2 3 4 5 6

Move towards

Alternative Portfolios

Insourcing VS Outsourcing

Partnerships/ Joint Ventures Co-investments

Social Responsible

Investing

Use of Investment

Funds

Diversification through Foreign

Investments

Opportunities and challenges in key growth sectors

Sovereign Wealth Funds

PwC

17 November 2016

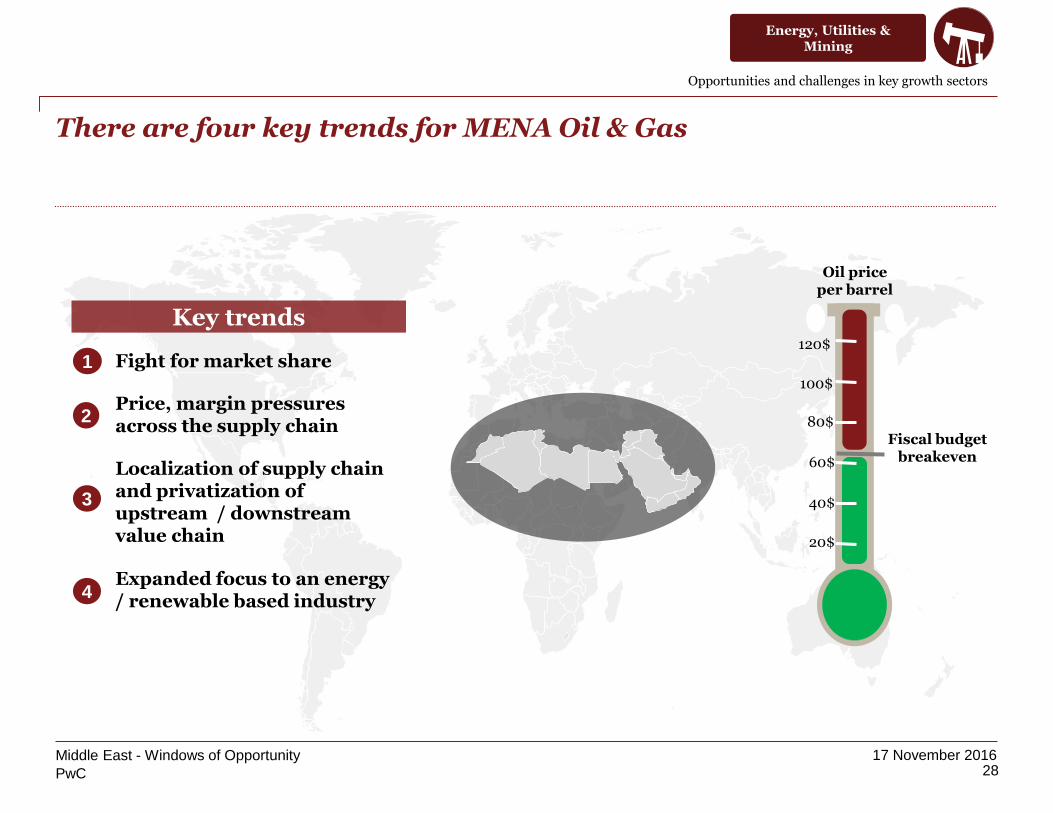

There are four key trends for MENA Oil & Gas

28Middle East - Windows of Opportunity

Key trends

Opportunities and challenges in key growth sectors

Oil price per barrel

20$

40$

60$

80$

100$

120$

Fiscal budget breakeven

1 Fight for market share

2Price, margin pressures across the supply chain

3

Localization of supply chain and privatization of upstream / downstream value chain

4Expanded focus to an energy / renewable based industry

Energy, Utilities & Mining

PwC

17 November 2016

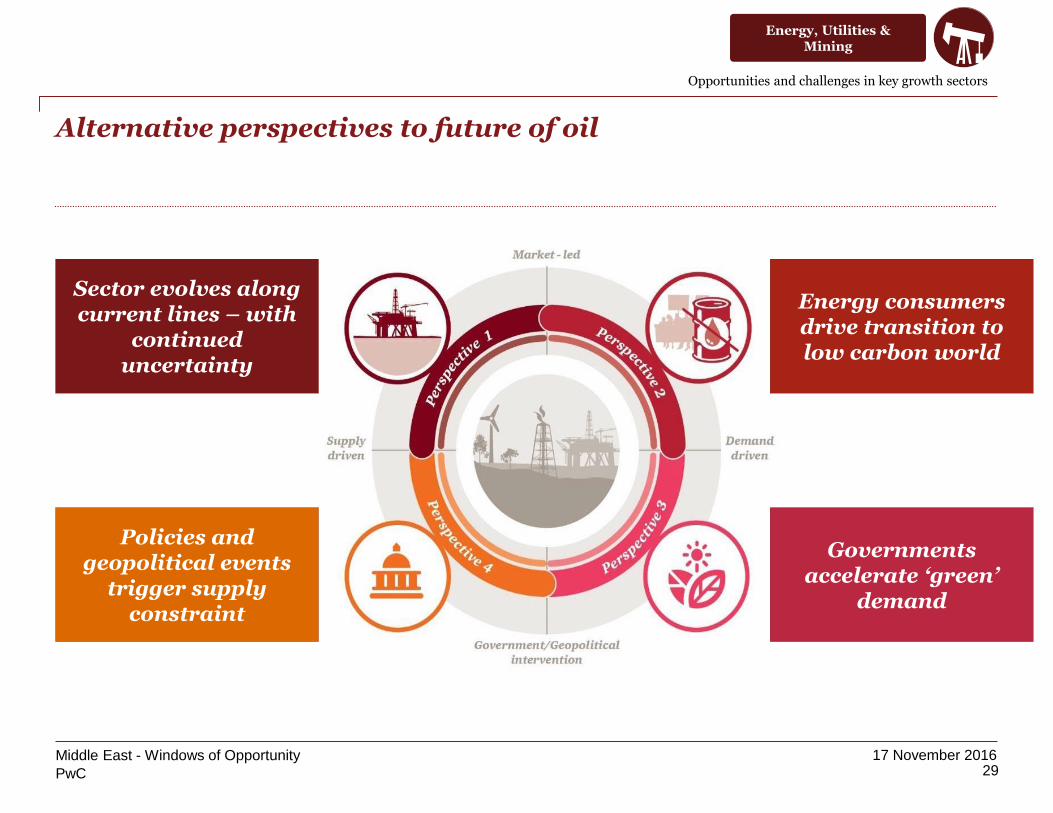

Alternative perspectives to future of oil

29Middle East - Windows of Opportunity

Sector evolves along current lines – with

continued uncertainty

Energy consumers drive transition to low carbon world

Policies and geopolitical events

trigger supply constraint

Governments accelerate ‘green’

demand

Opportunities and challenges in key growth sectors

Energy, Utilities & Mining

PwC

17 November 2016

The tax and regulatory environment in the Middle East

30Middle East - Windows of Opportunity

4. The tax and regulatory environment in the Middle East

PwC

17 November 2016

Perception

• ‘There is no tax in the Middle East, is there?”

Reality

• Number of very different tax systems. Taxation often depends on nationally and residence of ultimate shareholders, type of legal set-up, nature of business activities, and location within the relevant country.

One region, many jurisdictions …

The tax and regulatory environment in the Middle East

31Middle East - Windows of Opportunity

Saudi Arabia

Kuwait

Qatar

Bahrain

Saudi ArabiaU.A.E.

Oman

PwC

17 November 2016

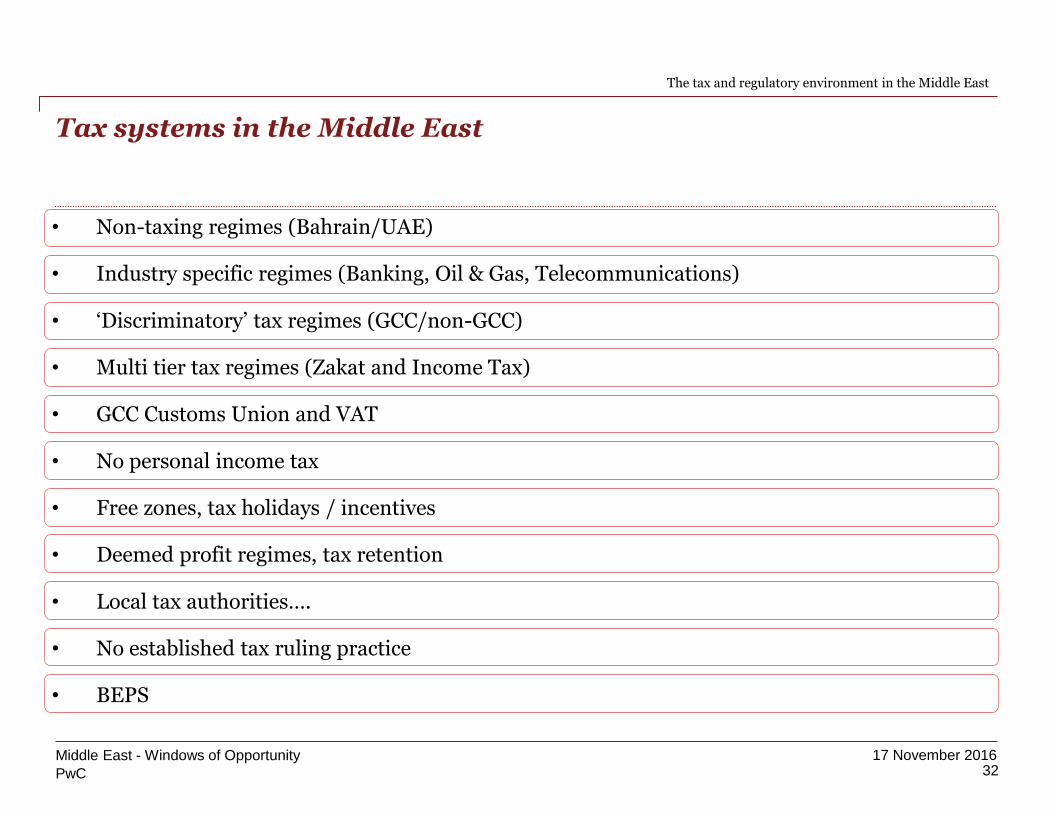

Tax systems in the Middle East

The tax and regulatory environment in the Middle East

32Middle East - Windows of Opportunity

• Non-taxing regimes (Bahrain/UAE)

• Industry specific regimes (Banking, Oil & Gas, Telecommunications)

• ‘Discriminatory’ tax regimes (GCC/non-GCC)

• Multi tier tax regimes (Zakat and Income Tax)

• GCC Customs Union and VAT

• No personal income tax

• Free zones, tax holidays / incentives

• Deemed profit regimes, tax retention

• Local tax authorities….

• No established tax ruling practice

• BEPS

PwC

17 November 2016

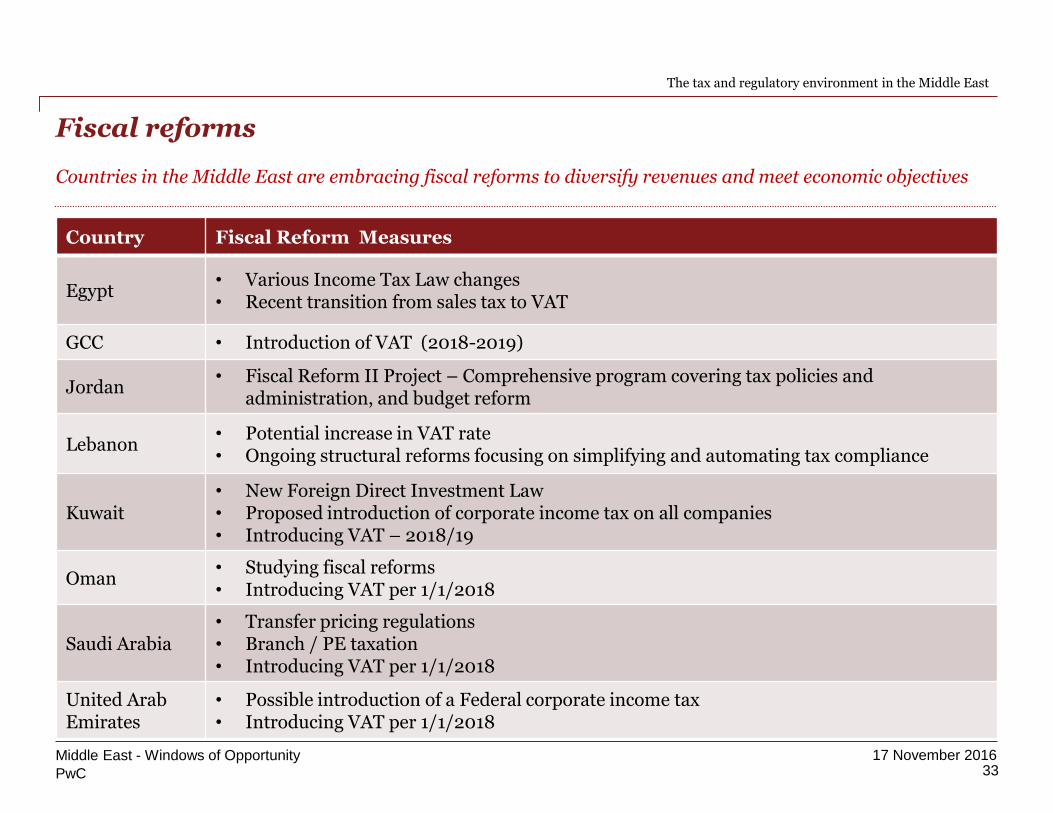

Fiscal reforms

Countries in the Middle East are embracing fiscal reforms to diversify revenues and meet economic objectives

33

The tax and regulatory environment in the Middle East

Middle East - Windows of Opportunity

Country Fiscal Reform Measures

Egypt• Various Income Tax Law changes • Recent transition from sales tax to VAT

GCC • Introduction of VAT (2018-2019)

Jordan• Fiscal Reform II Project – Comprehensive program covering tax policies and

administration, and budget reform

Lebanon• Potential increase in VAT rate• Ongoing structural reforms focusing on simplifying and automating tax compliance

Kuwait• New Foreign Direct Investment Law• Proposed introduction of corporate income tax on all companies • Introducing VAT – 2018/19

Oman• Studying fiscal reforms• Introducing VAT per 1/1/2018

Saudi Arabia• Transfer pricing regulations• Branch / PE taxation • Introducing VAT per 1/1/2018

United Arab Emirates

• Possible introduction of a Federal corporate income tax • Introducing VAT per 1/1/2018

PwC

17 November 2016

Introduction of VAT in the GCC

34Middle East - Windows of Opportunity

The tax and regulatory environment in the Middle East

A Common VAT framework• The GCC Member States are in the process of agreeing a common framework for the

introduction of a VAT system in the GCC• On 16 June 2016 the GCC Finance Ministers approved a Treaty in principle. A formal

announcement of the Treaty is expected in October 2016

Go live • The introduction of VAT across the GCC is expected to take effect from 1 January 2018

VAT Regulations• To bring into effect the VAT legislation, each Member State will also issue implementing

regulations in accordance with their national legislative process• These regulations will provide guidance to tax payers in each GCC Member State on the

interpretation of the VAT legislation in that Member State. We anticipate that the regulations will be issued shortly after the VAT legislation is issued

VAT legislation• Upon ratification of the GCC Treaty, each Member State is expected to issue its own national

VAT legislation based on the agreed common principles• This legislation will set out the applicability of VAT on various goods and services and the

compliance requirements. It is expected that some countries will issue VAT legislation shortly after announcement of the treaty by the GCC

PwC

17 November 2016

Middle East legal and regulatory landscape

The tax and regulatory environment in the Middle East

35Middle East - Windows of Opportunity

Legal

• Most legal systems are mixed legal systems: continental European law applied in civil and commercial matters and administrative law; and Islamic law applied to criminal matters, family law and inheritance/trusts and estates.

• Exceptions: Iran, Saudi Arabia and Oman.

• Lack of precedents & case law

Regulatory

• Foreign ownership restrictions / Free Zones

• Local content rules

• Flexibility of business set-up

• Different regulators for same activities

PwC

17 November 2016

PwC in the Middle East

36Middle East - Windows of Opportunity

5. PwC in the Middle East

PwC

17 November 201637

Middle East - Windows of Opportunity

PwC in the Middle East

One Firm: Transforming our RegionSolving our region’s most important problems and building trust in our society

PwC

17 November 2016

Improving employment in KSA

Developing the new model of Healthcare for KSA

Assuring Emirates Airlines

Transforming e-health and postal service in Qatar

Digitizing the KSA Government

Building the cloud in KSA

Developing the Saudi Arabian Industrial Investment Company (SAIIC)

Transforming finance in UAE

Establishing VAT in the GCC

Developing PPP in Qatar

Housing PPPs in Kuwait

National transformation Oman

Delivering EXPO 2020/Qatar 2022

Ensuring worker welfare in Abu Dhabi

Partnering EUM on strategy and IFRS compliance

Assuring the world’s most valuable company

38Middle East - Windows of Opportunity

PwC in the Middle East

One Firm: Transforming our RegionWe are delivering against our purpose

PwC

17 November 2016

PwC’s Growth Markets Centre

39Middle East - Windows of Opportunity

6. PwC’s Growth Markets Centre

PwC

17 November 201640

Middle East - Windows of Opportunity

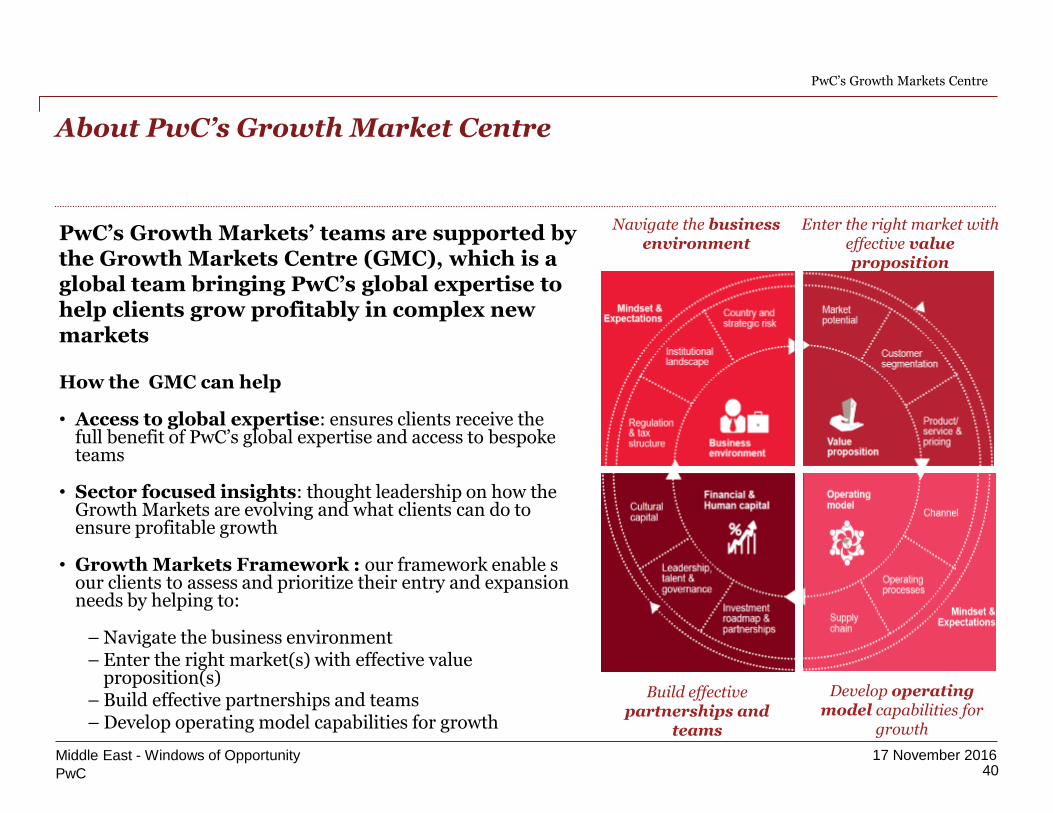

About PwC’s Growth Market Centre

PwC’s Growth Markets’ teams are supported by the Growth Markets Centre (GMC), which is a global team bringing PwC’s global expertise to help clients grow profitably in complex new markets

How the GMC can help

• Access to global expertise: ensures clients receive the full benefit of PwC’s global expertise and access to bespoke teams

• Sector focused insights: thought leadership on how the Growth Markets are evolving and what clients can do to ensure profitable growth

• Growth Markets Framework : our framework enable s our clients to assess and prioritize their entry and expansion needs by helping to:

– Navigate the business environment– Enter the right market(s) with effective value

proposition(s)– Build effective partnerships and teams– Develop operating model capabilities for growth

Navigate the business environment

Enter the right market with effective value proposition

Build effective partnerships and

teams

Develop operating model capabilities for

growth

PwC’s Growth Markets Centre

PwC

17 November 201641

Middle East - Windows of Opportunity

Accessing our growth markets’ point of view

Sector deep-dive analysis:Insights on up and coming sectors across Growth Markets, e.g. “Powering Nigeria for the Future” and “A new delivery: Satisfying Southeast Asia’s appetite through digital”

GMC blogs:Regular updates on growth opportunities and challenges in emerging markets

pwc.com/gmc

www

GMC thought leadership:Addressing key Growth Markets issues whilst highlighting PwC’s expertise in the region

Annual GMC event:Emerging Markets Conference “Growing in the age of volatility”: The GMC has partners with INSEAD to host an annual conference focused on key Growth Markets issues

PwC’s Growth Markets Centre

©2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Q&A

Q&A