Embed Size (px)

Citation preview

R E P O R T

MILLENNIUM PORT AUTHORITYBaton Rouge, Louisiana

JUNE 30,2005

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date

MILLENNIUM PORT AUTHORITYBaton Rouge, Louisiana

INDEX TO REPORT

JUNE 30, 2005

PAGE

INDEPENDENT AUDITOR'S REPORT 1 - 2

MANAGEMENT'S DISCUSSION AND ANALYSIS 3-6

FINANCIAL STATEMENTS:

Government-wide Financial Statements:

Statement of Net Assets 7

Statement of Activities 8

Fund Financial Statements

Balance Sheet 9

Reconciliation of the Balance Sheet to the Statement of Net Assets 10

Statement of Revenue, Expenditures and Changes in Fund Balance 11

Reconciliation of the Statement of Revenue, Expenditures andChanges in Fund Balance to the Statement of Activities 12

Notes to Financial Statements 13 -16

REPORT ON INTERNAL CONTROL OVER FINANCIALREPORTING AND ON COMPLIANCE AND OTHERMATTERS BASED ON A FINANCIAL STATEMENTAUDIT PERFORMED IN ACCORDANCE WITHGOVERNMENT AUDITING STANDARDS 17 -18

REQUIRED SUPPLEMENTARY INFORMATION:

Budget Comparison Schedule 19

SUPPLEMENTARY INFORMATION:

Schedule of Transportation Expenditures 20

htt

mDUPLANTIER, HRAPMANN,

HOGAN & MAHER, L.L.P

MICHAEL j. o-ROURKE, c.P.A. • • • • • • CERTIFIED PUBLIC ACCOUNTANTS A; DUPLANTIER( JR-/ CEA.WILLIAM G. STAMM, C.P.A. • • • • • • (1919-1985)CLIFFORD J. GIFFIN, JR., C.P.A. FELLX J. HRAPMANN, JR., C.P.A.DAVID A. BURGARD, C.P.A. (1919-1990)LINDSAY j. CALUB, C.P.A., L.L.c. 134Q Poydras St., Suite 2000 • New Orleans, LA 70112 WILLIAM R. HOGAN, JR., C.P.A.GUY L. DUPLANTIER, CP.A. (1920-1996)MICHELLE H. CUNNINGHAM, C.P.A. (D\J<±) JOO-OOOO JAMES MAKER, JR., C.P.A.

DENNIS W.DILLON, C.P.A, FAX (5()4) 525_5888 <1921-1999>

ANN M. HARGES, C.P.A. [email protected] A. STROHMEYER, C.P.A. r r MEMBERS

AMERICAN INSTITUTE OFKENNETH J. BROOKS, C.P.A., ASSOCIATE CERTIFIED PUBLIC ACCOUNTANTS

SOCIETY OF LA. C.P.A.s

INDEPENDENT AUDITOR'S REPORT

July 26, 2005Millennium Port AuthorityBaton Rouge, Louisiana

We have audited the accompanying financial statements of the Millennium Port Authority, acomponent unit of the State of Louisiana, as of and for the year ended June 30, 2005, as listed in theindex to report. These financial statements are the responsibility of the Millennium Port Authority'smanagement. Our responsibility is to express an opinion on these financial statements based on ouraudit.

We conducted our audit in accordance with auditing standards generally accepted in the UnitedStates of America and Government Auditing Standards, issued by the Comptroller General of the UnitedStates. Those standards require that we plan and perform the audit to obtain reasonable assurance aboutwhether the financial statements are free of material misstatement. An audit includes examining, on a testbasis, evidence supporting the amounts and disclosures in the financial statements. An audit alsoincludes assessing the accounting principles used and significant estimates made by management, as wellas evaluating the overall financial statement presentation. We believe that our audit provides areasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, thefinancial position of the Millennium Port Authority, as of June 30, 2005 and the results of its operationsfor the year then ended in conformity with accounting principles generally accepted in the United Statesof America

The accompanying financial statements have been prepared assuming that the Millennium PortAuthority will continue as a going concern. As discussed in Note 7 to the financial statements, theMillennium Port Authority has not received state appropriations for the 2004 or 2005 legislative sessions.The Millennium Port Authority has also not received any additional grants or other sources of fundingduring the 2005 fiscal year ended. These conditions raise substantial doubt about its ability to continueas a going-concern. The financial statements do not include any adjustments that might result from theoutcome of this uncertainty.

PAGE 2

Management's Discussion and Analysis and the Budget Comparison Schedule on pages 3 through6 and page 19, respectively, are not required parts of the basic financial statements but are supplementaryinformation required by the Governmental Accounting Standards Board. We have applied certainlimited procedures, which consisted primarily of inquiries of management regarding the methods ofmeasurement and presentation of the supplementary information. However, we did not audit theinformation and express no opinion on it.

Our audit was conducted for the purpose of forming an opinion on the financial statements takenas a whole. The accompanying supplementary information on page 20 is presented for purposes ofadditional analysis and is not a required part of the financial statements of the Millennium Port Authority.The supplementary information on page 20 for the year ended June 30, 2005, has been subjected to theauditing procedures applied in the audit of the general purpose financial statements and, in our opinion, isfairly presented in all material respects in relation to the financial statements taken as a whole.

In accordance with Government Auditing Standards, we have also issued a report dated July 26,2005 on our consideration of Millennium Port Authority's internal control over financial reporting andon compliance and other matters. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards and should be read in conjunction with this report in considering theresults of our audit.

PAGE 3

MILLENNIUM PORT AUTHORITYMANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30. 2005

The Management's Discussion and Analysis of the Millennium Port Authority's financial performancepresents a narrative overview and analysis of Millennium Port Authority's financial activities for theyear ended June 30, 2005. This document focuses on the current year's activities, resulting changes,and currently known facts in comparison with the prior year's information. Please read this documentin conjunction with the additional information contained in the Millennium Port Authority's financialstatements, which begin on page 7.

FINANCIAL HIGHLIGHTS

* The Millennium Port Authority's assets exceeded its liabilities at the close of fiscal year 2005by $236,632.

* The Millennium Port Authority's revenue was $63,289 and the net results from activities was$(304,860).

OVERVIEW OF THE FINANCIAL STATEMENTS

The following graphic illustrates the minimum requirements established by Governmental AccountingStandards Board Statement 34, Basic Financial Statements—and Management's Discussion andAnalysis—for State and Local Governments.

Management's Discussion arid Analysis

. • ' < • : . • £ • ' . - < - ; - % * . ' , ' ^ : - < . - - . . - • .1 ;-;y Basic Financial Statements -a'^•>••; -Ov */ ;:

"-'':;,-•• :•.•,."**•.;••„* -^^.:y.^.^-V^^,:^-;;\^-r/ :

Required supplementary information •(other than MD& A) '

These financial statements consist of three sections - Management's Discussion and Analysis (thissection), the basic financial statements (including the notes to the financial statements), and requiredsupplementary information.

PAGE 4

MILLENNIUM PORT AUTHORITYMANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30. 2005

Basic Financial Statements

The basic financial statements present information for the Millennium Port Authority as a whole, in aformat designed to make the statements easier for the reader to understand. The statements in thissection include the government-wide financial statements and fund financial statements.

Government-wide Financial Statements: The government-wide financial statements are designed toprovide readers with a broad overview of the Millenium Port Authority's finances, in a manner similarto private-sector business. The government-wide financial statements include:

Statement of Net Assets - this statement presents the current and long term portions of assetsand liabilities separately. The difference between total assets and total liabilities is net assets andmay provide a useful indicator of whether the financial position of the Millennium PortAuthority is improving or deteriorating.

Statement of Activities - this statement presents information showing how Millennium PortAuthority's assets changed as a result of current year operations. Regardless of when cash isaffected, all changes in net assets are reported when the underlying transactions occur. As aresult, there are transactions included that will not affect cash until future fiscal periods.

Fund Financial Statements: A fund is a grouping of related accounts that is used to maintain controlover resources that have been segregated for specific activities or objectives. The Millenium PortAuthority, like other state and local governments, uses fund accounting to ensure and demonstratecompliance with finance-related legal requirements. All of the funds of the Millenium Port Authorityare considered governmental funds.

FINANCIAL ANALYSIS OF THE ENTITY

Statement of Net Assets

2005June 30,

Current assetsCashAccounts receivable

Total current assetsNon-current assets

Capital assets - equipment, net of depreciationTotal assets

Liabilities:Accounts payable

Total liabilitiesFund balances/net assets

Invested in capital assets, net of related depreciationUnreserved/Unrestricted

Total fund balances/net assetsTotal liabilities and fund balances/net assets

$ 258,42616.667

275,093

13.373288.466

51.83451,834

13,373223.259236.632

S 288.466

2004

542,624

542,624

16.785559.410

17,91817.918

16,785524.707541.492559.410

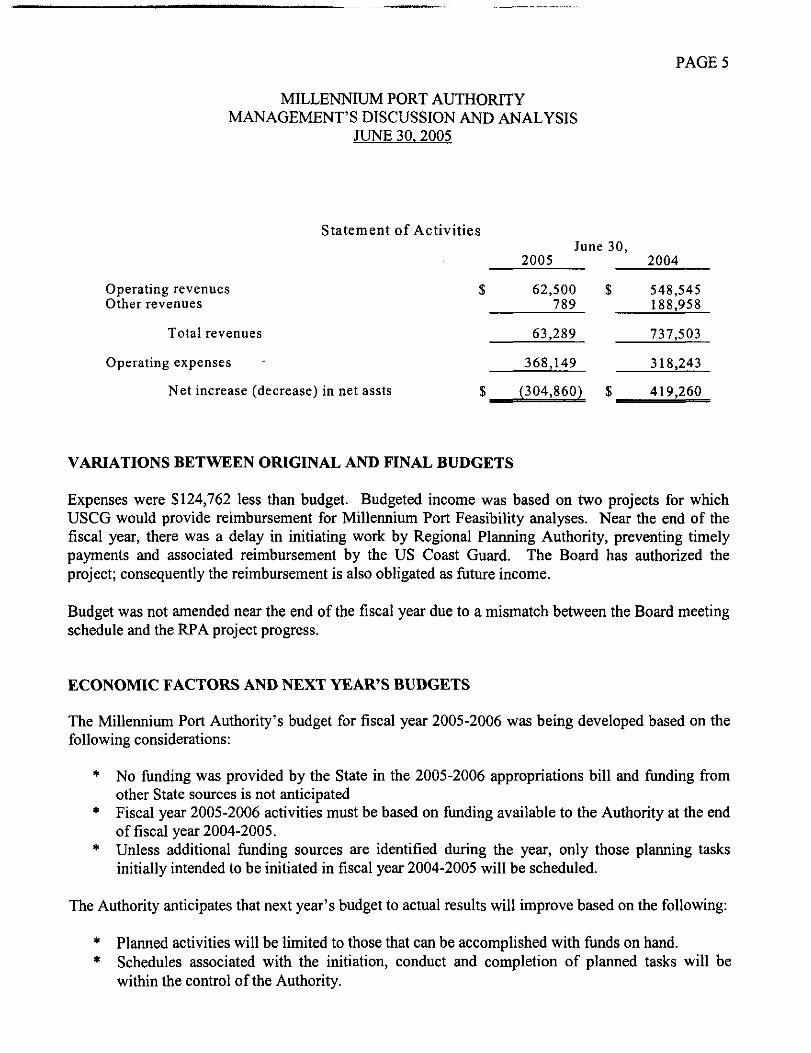

PAGES

MILLENNIUM PORT AUTHORITYMANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30. 2005

Statement of ActivitiesJune 30,

2005 2004

Operating revenues $ 62,500 $ 548,545Other revenues 789 188,958

Total revenues 63,289 737,503

Operating expenses - 368,149 318,243

Net increase (decrease) in net assts $ (304,860) $ 419,260

VARIATIONS BETWEEN ORIGINAL AND FINAL BUDGETS

Expenses were $124,762 less than budget. Budgeted income was based on two projects for whichUSCG would provide reimbursement for Millennium Port Feasibility analyses. Near the end of thefiscal year, there was a delay in initiating work by Regional Planning Authority, preventing timelypayments and associated reimbursement by the US Coast Guard. The Board has authorized theproject; consequently the reimbursement is also obligated as future income.

Budget was not amended near the end of the fiscal year due to a mismatch between the Board meetingschedule and the RPA project progress.

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS

The Millennium Port Authority's budget for fiscal year 2005-2006 was being developed based on thefollowing considerations:

* No funding was provided by the State in the 2005-2006 appropriations bill and funding fromother State sources is not anticipated

* Fiscal year 2005-2006 activities must be based on funding available to the Authority at the endof fiscal year 2004-2005.

* Unless additional funding sources are identified during the year, only those planning tasksinitially intended to be initiated in fiscal year 2004-2005 will be scheduled.

The Authority anticipates that next year's budget to actual results will improve based on the following:

* Planned activities will be limited to those that can be accomplished with funds on hand.* Schedules associated with the initiation, conduct and completion of planned tasks will be

within the control of the Authority.

PAGE 6

MILLENNIUM PORT AUTHORITYMANAGEMENT'S DISCUSSION AND ANALYSIS

JUNE 30.2005

CONTACTING THE MILLENNIUM PORT AUTHORITY'S MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, and investors andcreditors with a general overview of the Millennium Port Authority's finances and to show theMillennium Port Authority's accountability for the money it receives. If you have questions about thisreport or need additional financial information, contact Ned Peak (504) 528-3366.

PAGE?

MILLENNIUM PORT AUTHORITYSTATEMENT OF NET ASSETS

JUNE 30. 2005

ASSETS:

Current assetsCash $ 258,426

Accounts receivable 16,667Total current assets 275,093

Non-current assetsCapital assets - equipment, net of depreciation 13,373

Total assets 288,466

LIABILITIES:

Liabilities.Accounts payable 51,834

NET ASSETS:

Invested in capital assets, net of related depreciation 13,373Unrestricted 223,259

Total net assets $ 236.632

See accompanying notes.

MILLENNIUM PORT AUTHORITYSTATEMENT OF ACTIVITIES

JUNE 30 2005

PAGES

Function/Programs

Transportation

Expenses

$ 368,149 $

Charges forServices

OperatingGrants and

Contributions

CapitalGrants and

Contributions

Net (Expense)Revenue and

Change inNet Assets

62,500 $ $ (305,649)

General revenues:State appropriationsUnrestricted interest income

Total general revenuesChange in net assetsNet assets - beginning of yearNet assets - end of year

789789

(304,860)

541,492

236,632

See accompanying notes.

MILLENNIUM PORT AUTHORITYGOVERNMENTAL FUNDS BALANCE SHEET

JUNE 30. 2005

PAGE 9

ASSETS:

CashAccounts receivable

Total assets

LIABILITIES:

Accounts payable

Total liabilities

FUND BALANCE:

Unreserved

Total fund balance

Total liabilities and fund balance

GeneralFund

258,42616.667

275.093

$ 51,834

51,834

223,259

223,259

$ 275.093

See accompanying notes.

PAGE 10

MILLENNIUM PORT AUTHORITYRECONCILIATION OF THE GOVERNMENTAL FUND

BALANCE SHEET TO THE STATEMENT OF NET ASSETSJUNE 30. 2005

Amounts reported for governmental fund in the statementof net assets are different because:

Total Fund Balance at June 30, 2005 $ 223,259

Capital assets net of accumulated depreciation at June 30, 2005 13,373

TOTAL NET ASSETS AS OF JUNE 30, 2005 $ 236.632

See accompanying notes.

PAGE 11

MILLENNIUM PORT AUTHORITYGOVERNMENTAL FUNDS

STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCEFOR THE YEAR ENDED JUNE 30, 2005

REVENUES;Federal grants $ 62,500Interest income 789

Total revenues 63,289

EXPENDITURES:Transportation 364,737

Total expenditures 364,737

Net change in fund balance

Fund balance - beginning

FUND BALANCE - ENDING

See accompanying notes.

PAGE 12

MILLENNIUM PORT AUTHORITYRECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES

AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDSTO THE STATEMENT OF ACTIVITIESFOR THE YEAR ENDED JUNE 30. 2005

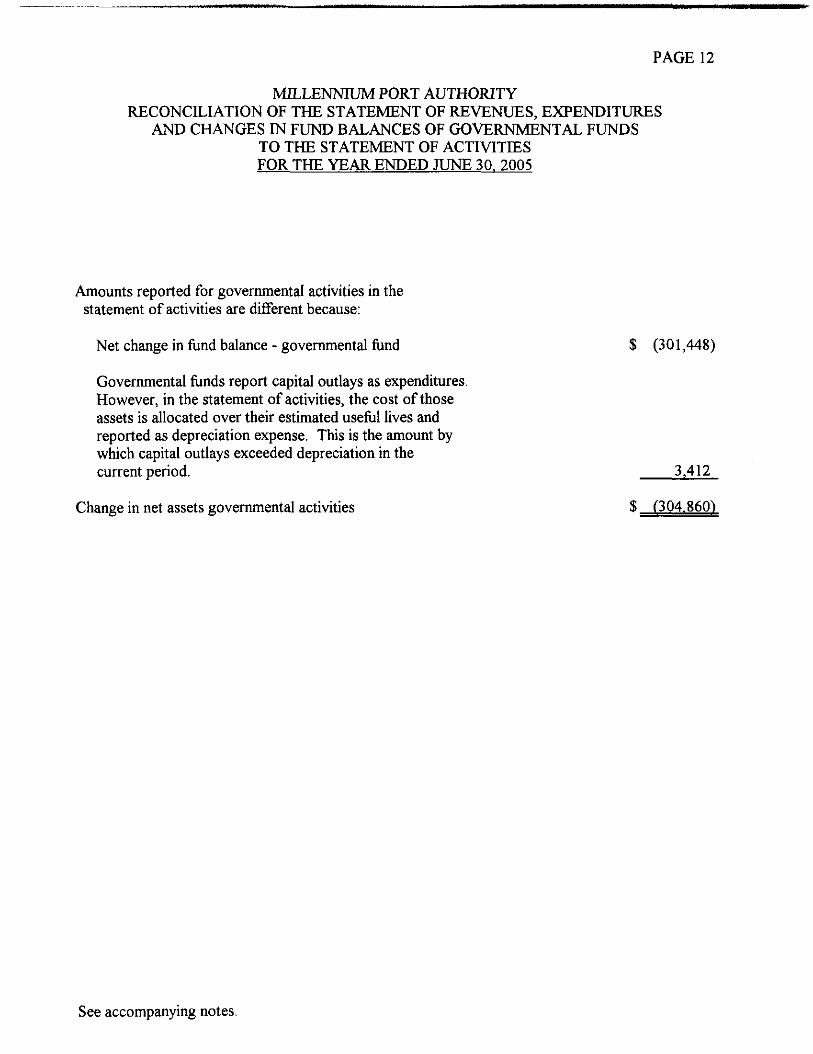

Amounts reported for governmental activities in thestatement of activities are different because:

Net change in fund balance - governmental fund $ (301,448)

Governmental funds report capital outlays as expenditures.However, in the statement of activities, the cost of thoseassets is allocated over their estimated useful lives andreported as depreciation expense. This is the amount bywhich capital outlays exceeded depreciation in thecurrent period. 3,412

Change in net assets governmental activities

See accompanying notes.

PAGE 13

MILLENNIUM PORT AUTHORITYNOTES TO FINANCIAL STATEMENTS

JUNE 30, 2005

The Millennium Port Authority (Authority) was established and provided for by R.S. 34:3471 of theLouisiana Revised Statutes (LRS). It was created as a political subdivision of the state to plan, constructand operate a deep draft intermodal terminal facility. The Authority is governed by a Board of elevenCommissioners who are appointed by the governor. Commissioners serve without compensation for a termof two years. Members of the Board of Commissioners shall be selected based on the criteria set forth inR.S. 34:3474.

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

The financial statements of the Millennium Port Authority are prepared in accordance with thestandards established by the Governmental Accounting Standards Board (GASB) as the successor ofthe National Council on Governmental Accounting (NCGA).

Financial Reporting Entity:

In June 1991, the Governmental Accounting Standards Board (GASB) issued Statement No. 14,The Financial Reporting Entity, The definition of the reporting entity is based primarily on the notionof financial accountability.

In determining financial accountability for legally separate organizations, the Authorityconsidered whether its officials appoint a voting majority of an organization's governing body andwhether they are able to impose their will on that organization or there is a potential for theorganization to provide specific financial burdens to, or to impose specific financial burdens on, theAuthority. The State also considered whether there are organizations that are fiscally dependent on it.There are no component units of the Millennium Port Authority.

The Millennium Port Authority is a component unit of the State of Louisiana and its financialstatements are included in the financial statements of the State of Louisiana.

Basis of Presentation:

The accompanying financial statements of the Millennium Port Authority have been prepared inconformity with generally accepted accounting principles (GAAP) as applied to governmental units.The Governmental Accounting Standards Board (GASB) is the accepted standard setting body forestablishing governmental accounting and financial reporting principles. In addition, these financialstatements include the provisions of GASB Statement Number 34, Basic Financial Statements - andManagement's Discussion and Analysis-far State and Local Governments and related standards. Thisstandard provides for significant changes in terminology, recognition of contributions in the Statementof Revenues, Expenses and Changes in Net Assets, inclusion of a management discussion and analysisas supplementary information and other changes.

PAGE 14MILLENNIUM PORT AUTHORITY

NOTES TO FINANCIAL STATEMENTSJUNE 30. 2005

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (Continued)

Basis of Presentation: (Continued)

The accompanying financial statements of the Millennium Port Authority present informationonly as to the transactions of the programs of the Millennium Port Authority as authorized by Louisianastatutes and administrative regulations.

Government-wide and Fund Financial Statements:

In accordance with Statement No. 34 of the Governmental Accounting Standards Board(GASB), Basic Financial Statements - and Management's Discussion and Analysis -for State andLocal Governments, included in the Port's Comprehensive Annual Financial Report for the year endedJune 30, 2005 are the Management Discussion and Analysis (MD&A), government-wide financialstatements which include the Statement of Net Assets and the Statement of Activities, and fundfinancial statements which include the Balance Sheet, Reconciliation of the Balance Sheet to theStatement of Net Assets, Statement of Revenues, Expenditures and Change in Fund Balance andReconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balance to theStatement of Activities.

Measurement Focus. Basis of Accounting and Financial Statement Presentation:

The government-wide financial statements are reported using the economic resourcesmeasurement focus and the accrual basis of accounting. Revenues are recorded when earned andexpenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Grantsand similar items are recognized as revenue as soon as all eligibility requirements imposed by theprovider have been met. Amounts reported as program revenues include operating grants. Likewise,general revenues include state appropriations and interest.

Governmental fund financial statements are reported using the current financial resourcesmeasurement focus and the modified accrual basis of accounting. With this measurement focus, onlycurrent assets and current liabilities generally are included on the balance sheet. Operating statementsof these funds present increases (i.e., revenues and other financing sources) and decreases (i.e.,expenditures and other financing uses) in net current assets.

The modified accrual basis of accounting is used by all governmental fund types. Under thismethod, revenues are recognized when susceptible to accrual (i.e., when they become both measurableand available). "Measurable" means the amount of the transaction can be determined and "available"means collectible within the current period or soon enough thereafter to be used to pay liabilities of thecurrent period. Expenditures are recorded when the related fund liability is incurred.

Fund Accounting:

The accounts of the Millennium Port Authority are organized on the basis of a fund. Theoperations of the fund are accounted for with a separate set of self-balancing accounts that comprises itsassets, liabilities, fund equity, revenues, and expenditures. Revenues are accounted for in thisindividual fund based upon the purpose for which they are to be spent and the means by whichspending activities are controlled. The fund presented in the financial statements is described asfollows:

PAGE 15

MILLENNIUM PORT AUTHORITYNOTES TO FINANCIAL STATEMENTS

JUNE 30.2005

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (Continued)

Fund Accounting: (Continued)

Governmental Fund:

General Fund:

The General Fund is the principal fund of the Millennium Port Authority and is used to accountfor the operations of the Millennium Port Authority.

Budget Practices

Budgets are prepared and adopted annually by the Millennium Port Authority. TheMillennium Port Authority budgets its expenses based on state appropriations and grants it expectsto receive each year. The budget was prepared using the modified accrual basis of accounting. Allbudgetary appropriations lapse at the end of each fiscal year.

Property and Equipment:

Property and equipment are reported in the government-wide financial statements. The costof property, plant and equipment is depreciated over the estimated useful lives of the related assets.Depreciation is computed on the straight-line method for financial reporting purposes.

2. CASH:

At June 30, 2005, the carrying amount of cash was $258,426 and the bank balance was$258,426. The bank balance of $258,426 was covered by Federal Depository Insurance and pledgedcollateral which is held by a "third-party safekeeper" in joint custody with the Millenium PortAuthority.

3. COMPENSATION TO BOARD MEMBERS:

The board members do not receive compensation for being on the board.

4. USE OF ESTIMATES:

The process of preparing financial statements in conformity with accounting principlesgenerally accepted in the United States of America requires the use of estimates and assumptionsregarding certain types of assets, liabilities, revenues and expenses. Such estimates primarily relate tounsettled transactions and events as of the date of the financial statements. Accordingly, uponsettlement, actual results may differ from estimated amounts.

PAGE 16

MILLENNIUM PORT AUTHORITYNOTES TO FINANCIAL STATEMENTS

JUNE 30.2005

5. CAPITAL ASSETS:

The following is a summary of capital assets - at cost, less accumulated depreciation:

Beginning balance $ 20,283AdditionsLess: accumulated depreciation (6.910)

Total

6. SUBSEQUENT EVENTS:

Since inception, the Port received a substantial portion of its funding from State appropriations.For the 2004 - 2005 and 2005 - 2006 fiscal years, the State eliminated the appropriation funding for theMillennium Port.

7. GOING CONCERN:

The accompanying financial statements have been prepared in conformity with generallyaccepted accounting principles, which contemplates continuation of the company as a going concern.However, the Millennium Port Authority has sustained a substantial operating loss during the year,which required the Millennium Port Authority to use substantial amounts of working capital in itsoperations. Further, the Millennium Port Authority has not received State appropriations for the 2004or 2005 legislative sessions; nor have they received or expect to receive any additional funding duringthe 2005 fiscal year ended.

MICHAEL J. O'ROURKE, C.P.A.WILLIAM G. STAMM, C.P.A.CLIFFORD J. GIFFIN, JR., C.P.A.DAVID A. BURGARD, C.P.A.LINDSAY J. CALUB, C.P.A., L.L.C.GUY L. DUPLANTIER, C.P.A.MICHELLE H. CUNNINGHAM, C.P.A.DENNIS W. DILLON, C.P.A.

ahim

DUPLANTIER, HRAPMANN,HQGAN & MAHER, L.L.P.

CERTIFIED PUBLIC ACCOUNTANTS

ANN M. BARGES, C.P.A.ROBIN A. STROHMEYER, C.P.A.

1340 Poydras St., Suite 2000 • New Orleans, LA 70112(504) 586-8866

FAX (504) 525-5888cpa@dhhmcpa. com

KENNETH J. BROOKS, C.P.A., ASSOCIATE

A.J. DUPLANTIER, JR., C.P.A.(1919-1985)

FELIX J. HRAPMANN, JR., C.P.A.(1919-1990)

WILLIAM R. HOGAN, JR., C.P.A.(1920-1996)

JAMES MAKER, JR., C.P.A.(1921-1999)

MEMBERSAMERICAN INSTITUTE OF

CERTIFIED PUBLIC ACCOUNTANTSSOCIETY OF LA. C.P.A.s

REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING AND ON COMPLIANCE AND

OTHER MATTERS BASED ON A FINANCIAL STATEMENT AUDITPERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Board of Commissioners of theMillennium Port AuthorityBaton Rouge, Louisiana

July 26,2005

We have audited the financial statements of the Millennium Port Authority, as of and for the yearended June 30, 2005, and have issued our report thereon dated July 26, 2005. We conducted our audit inaccordance with auditing standards generally accepted in the United States of America and the standardsapplicable to financial audits contained in Government Auditing Standards, issued by the ComptrollerGeneral of the United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the Millennium Port Authority's internalcontrol over financial reporting in order to determine our auditing procedures for the purpose ofexpressing our opinion on the financial statements and not to provide assurance on the internal controlover financial reporting. Our consideration of internal control over financial reporting would notnecessarily disclose all matters in the internal control that might be material weaknesses.

A material weakness is a reportable condition in which the design or operation of one or more ofthe internal control components does not reduce to a relatively low level the risk that misstatements inamounts that would be material in relation to the financial statements being audited may occur and not bedetected within a timely period by employees in the normal course of performing their assignedfunctions. We noted no matters involving the internal control over financial reporting and its operationthat we consider to be material weaknesses.

PAGE 18

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Millennium Port Authority's financialstatements are free of material misstatement, we performed tests of its compliance with certainprovisions of laws, regulations and contracts, noncompliance with which could have a direct and materialeffect on the determination of financial statement amounts. However, providing an opinion oncompliance with those provisions was not an objective of our audit and, accordingly, we do not expresssuch an opinion. The results of our tests disclosed material instances of noncompliance that are requiredto be reported under Government Auditing Standards which are described as follows:

Several meal reimbursements tested were not in compliance with the Louisiana Travel Guide.Items were noted such as, meals were provided for contractors and commissioners for local monthlymeetings, several meals did not contain proper documentation.

It is our understanding that the Authority is required to follow the Louisiana Travel Guide. Werecommend that the Authority follow the guidelines set forth in the Louisiana Travel Guide. If theAuthority feels as though it does not fall under the jurisdiction of the Louisiana Travel Guide, werecommend that they seek an Attorney General's opinion regarding meal reimbursement.

The operating budget was not amended when revenues fell below 5% or more of the projectedbudget. It was also noted that the Authority did not publish a notice in the newspaper which states thatthe proposed budget is available for public inspection. Not following the preceding procedures is aviolation of the Louisiana Budget Act (L.R.S. 39:1305-1308). We recommend that the Millennium PortAuthority amend the budget when revenues fall below 5% of projected amounts and publish a notice inthe local newspaper that the proposed budget is available for public inspection.

This report is intended for the information of the Board of Commissioners and management ofMillennium Port Authority and the office of the Legislative Auditor of the State of Louisiana and is notintended to be and should not be used by anyone other than these specified parties. Under LouisianaRevised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

0

PAGE 19

MILLENNIUM PORT AUTHORITYREQUIRED SUPPLEMENTARY INFORMATION

BUDGET COMPARISON SCHEDULEFOR THE YEAR ENDED JUNE 30. 2005

Revenues:Other

TOTAL REVENUES

Expenditures/expenses:Transportation

PersonnelOperating expensesProfessional servicesTravel and meetings

$$

$

Originaland FinalBudgetAmount

125,000

125.000

100,00010,000

354,50025,000

ActualAmounts

$ 63,290

$ 63.290

$ 100,0004,882

250,1499,706

StatementVariancePositive

(Negative')

$ (61,710)

$ (61.7101

(5,118)(104,351)

(15,294)

TOTAL EXPENSES

PAGE 20

MILLENNIUM PORT AUTHORITYSUPPLEMENTARY INFORMATION

GOVERNMENTAL FUNDSSCHEDULE OF TRANSPORTATION EXPENDITURES

FOR THE YEAR ENDED JUNE 30. 2005

Transportation expenditures;

Bank charges $ 319Consulting fees 245,880Dues and subscriptions 1,574Office supplies 2,360Personnel 100,000Printing and reproduction 455Postage and delivery 174Professional fees 4,269Travel and meetings 9,706

TOTAL TRANSPORTATION EXPENDITURES $ 364.737

OFFICE OF STATEWIDE REPORTING PACKAGE

Millennium Port AuthoritySTATE OF LOUISIANA

Annual Financial StatementsJune 30, 2004

C O N T E N T S

Statements

MD&A (See audit report pages 3-6)

Balance Sheet A

Statement of Revenues, Expenses, and Changes in Fund Net Assets B

Statement of Activities C

Statement of Cash Flows D

Notes to the Financial Statements 1 - 6A. Summary of Significant Accounting PoliciesB. Budgetary AccountingC. Deposits with Financial Institutions and InvestmentsD. Capital AssetsE. InventoriesF. Restricted AssetsG. LeaveH. Retirement SystemI. Post Retirement Health Care and Life Insurance BenefitsJ. LeasesK. Long-Term LiabilitiesL. LitigationM. Related Party TransactionsN. Accounting ChangesO. In-Kind ContributionsP. Defeased IssuesQ. Cooperative EndeavorsR. Government-Mandated Nonexchange Transactions (Grants)S. Violations of Finance-Related Legal or Contractual ProvisionsT. Short-Term DebtU. Disaggregation of Receivable BalancesV. Disaggregation of Payable BalancesW. Subsequent EventsX. Segment InformationY. Due to/Due from and TransfersZ. Liabilities Payable from Restricted Assets

AA. Prior-Year Restatement of Net AssetsAB. Going Concern

Schedules1 Schedule of Per Diem Paid Board Members2 Schedule of State Funding3 Schedules of Long-Term Debt4 Schedules of Long-Term Debt Amortization15 Schedule of Comparison Figures and Instructions

STATE OF LOUISIANAMillennium Port AuthorityBALANCE SHEETAS OF June 30, 2005

ASSETSCURRENT ASSETS:

Cash and cash equivalents (Note C1)Investments (Note C2)Receivables (net of allowance for doubtful accounts){Note U)Due from other funds (Note Y)Due from federal governmentInventoriesPrepaymentsNotes receivableOther current assets

Total current assetsNONCURRENT ASSETS:

Restricted assets (Note F):CashInvestmentsReceivables

Notes receivableInvestmentsCapital assets (net of depreciation)(Note D)

LandBuildings and improvementsMachinery and equipmentInfrastructureConstruction in progress

Other noncurrent assetsTotal noncurrent assets

Total assetsLIABILITIESCURRENT LIABILITIES:

Accounts payable and accruals (Note V)Due to other funds (Note Y)Due to federal governmentDeferred revenuesAmounts held in custody for othersOther current liabilitiesCurrent portion of long-term liabilities:

Contracts payableReimbursement contracts payableCompensated absences payable (Note K)Capital lease obligations - (Note J)Notes payableLiabilities payable from restricted assets (Note Z)Bonds payableOther long-term liabilities

Total current liabilitiesNON-CURRENT LIABILITIES:

Contracts payableReimbursement contracts payableCompensated absences payable (Note K)Capital lease obligations (Note J)Notes payableLiabilities payable from restricted assets (Note Z)Bonds payableOther long-term liabilities

Total long-term liabilitiesTotal liabilities

NET ASSETSInvested in capital assets, net of related debtRestricted for:

Capital projectsDebt serviceUnemployment compensationOther specific purposes

UnrestrictedTotal net assets

Total liabilities and net assets

258.426

16.667

275.093

13.373

13.373

51.834

51.834

51.834

13.373

223.259236.632

The accompanying notes are an integral part of this financial statement.Statement A

STATE OF LOUISIANAMillennium Port AuthoritySTATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET ASSETSFOR THE YEAR ENDED June 30,2005

OPERATING REVENUESSales of commodities and servicesAssessmentsUse of money and propertyLicenses, permits, and feesOtherTotal operating revenues

OPERATING EXPENSESCost of sales and servicesAdministrativeDepreciationAmortizationTotal operating expenses

Operating income(loss)

NON-OPERATING REVENUES(EXPENSES)State appropriationsIntergovernmental revenues (expenses)TaxesUse of money and propertyGain (loss) on disposal of fixed assetsFederal grantsInterest expenseOtherTotal non-operating revenues(expenses)

lncome(loss) before contributions and transfers

Capital contributionsTransfers inTransfers out

Change in net assets

Total net assets - beginning as restated

Total net assets - ending

62,500

62,500

14,588350,149

3,412

368,149

(305,649)

789

789

(304,860)

(304,860)

541,492

236.632

The accompanying notes are an integral part of this financial statement.Statement B

STATE OF LOUISIANAMillennium Port AuthoritySTATEMENT OF ACTIVITIESFOR THE YEAR ENDED June 30,2005

Program Revenues

Millennium

Port Authority

Expenses

$ 368,149 $

Charges for

Services

Operating

Grants and

Contributions

Capital

Grants and

Contributions

62,500 $

Net (Expense)

Revenue and

Changes in

Net Assets

(305,649)

General revenues:

Taxes

State appropriations

Grants and contributions not restricted to specific programs

Interest

Miscellaneous

Special items

Transfers

Total general revenues, special items, and transfers

Change in net assets

Net assets - beginning

Net assets - ending

789

789(304,860)

541.492

236,632

The accompanying notes are an integral part of this financial statement.

Statement C

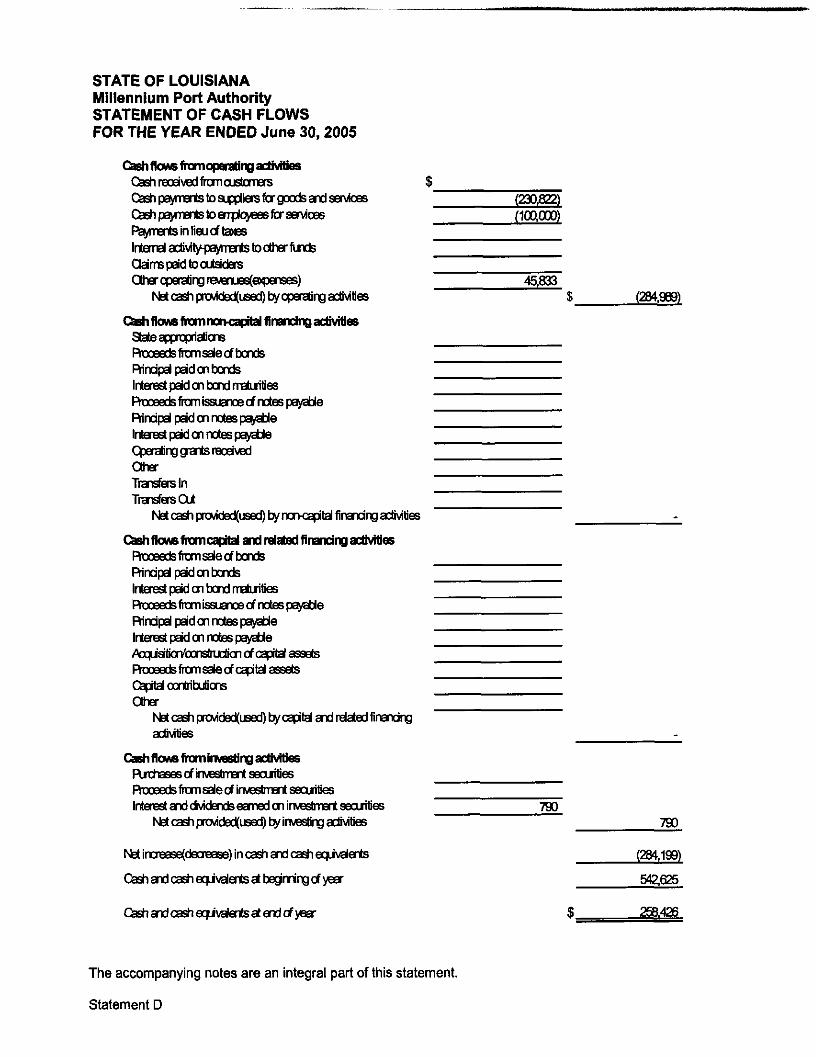

STATE OF LOUISIANAMillennium Port AuthoritySTATEMENT OF CASH FLOWSFOR THE YEAR ENDED June 30, 2005

Cashflows from operating activitiesCash received from customersCSshpaymerts to suppliers fcr gocdsand services _ (230,622)Cfeehpe^n^rtstoarplQyeesfcrservices _ (100,000)Foments in lieu of tawes

Claims paid to outsiders _Other operating revenues(e>$)enses) _ 45,833

Net cash provided(used) by operating actMfles $ _ (284.969)

Cash fkMS from ricrKaprtalfiriandng activitiesState appropriations _Rraeedsfrornsale of bonds _Rindpal paid on bonds _Interest paid on bond maturities _Ftaceedsfrom issuance of notes payable _Rincipal paid on notes payable _Interest paid on notes payable _Operating oja^ received _Other _Transfers In _Transfers Out _

Net cash provided(usecl) by rmopital financing activities _ -_

Cash flows fmmcatJU and related financing activitiesFtosedsfrornsaleofbonds _Rindpal paid on bonds _Interest paid en bend maturities _Rroeedsfiari issuance of notes payable _Rindpal paid on notes payable _Interest paid on notes payable _AcquisitiorVconstiTJcticncif capital assets _^^^^^__^^^^_Roceedsfrom sate of capital assets _Capital contributions _Other _

Net cash provided(used) by capital and related financingactivities _ -_

Cash flows from investing activitiesRntiasescfirivestment securities _FtoeeoslramsaJecifirweslrrentsecuities _Interest anddvidends earned on investrnentseoiities 790

Net cash provided(used) by investing activities 790

I increaEe(decrease)incashandca^equvaIerits (284,199)

Cash and cash equvaJentsatbegnring of ysar 542,625

Cash and cash equvatents at end of year £ 25a426

The accompanying notes are an integral part of this statement.

Statement D

STATE OF LOUISIANAMillennium Port AuthoritySTATEMENT OF CASH FLOWSFOR THE YEAR ENDED June 30,2005

Reconciliation of operating income(loss) to net cash provided(used) by operating activities:

Operating income(loss) $ (305.649)Adjustments to reconcile operating income(loss) to net cash

Depreciation/amortization 3,412Provision for uncollectible accountsChanges in assets and liabilities: _____

(Increase)decrease in accounts receivable, net (16,667)(Increase^decrease in due from other funds(Increase)decrease in prepayments(lncrease)decrease in inventories(Increase)decrease in other assetsIncrease(decrease) in accounts payable and accruals 33,915"Increase(decrease) in accrued payroll and related benefitsIncrease(decrease) in compensated absences payableIncrease(decrease) in due to other fundsIncrease(decrease) in deferred revenuesIncrease(decrease) in other liabilities

Net cash provided (used) by operating activities $ (284.9891

Schedule of noncash investing, capital, and financing activities:

Borrowing under capital lease

Contributions of fixed assets

Purchases of equipment on account

Asset trade-ins

Other (specify)

Total noncash investing, capital, andfinancing activities:

(Concluded)

The accompanying notes are an integral part of this statement.

Statement D

STATE OF LOUISIANAMillennium Port AuthorityNotes to the Financial StatementAs of and for the year ended June 30,2005

INTRODUCTION

The Millennium Port Authority was created by the Louisiana State Legislature under the provisions of LouisianaRevised Statute 34:3471. The following is a brief description of the operations of Millennium Port Authority whichincludes the parish/parishes in which the Millennium Port Authority is located:

A. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

1. BASIS OF ACCOUNTING

In April of 1984, the Financial Accounting Foundation established the Governmental Accounting StandardsBoard (GASB) to promulgate generally accepted accounting principles and reporting standards withrespect to activities and transactions of state and local governmental entities. The GASB has issued aCodification of Governmental Accounting and Financial Reporting Standards (GASB Codification). Thiscodification and subsequent GASB pronouncements are recognized as generally accepted accountingprinciples for state and local governments. The accompanying financial statements have been prepared inaccordance with such principles.

The accompanying financial statements of the Millennium Port Authority presents information only as tothe transactions of the programs of the Millennium Port Authority as authorized by Louisiana statutes andadministrative regulations.

Basis of accounting refers to when revenues and expenses are recognized and reported in the financialstatements. Basis of accounting relates to the timing of the measurements made, regardless of themeasurement focus applied.

The accounts of the Millennium Port Authority are maintained in accordance with applicable statutoryprovisions and the regulations of the Division of Administration - Office of Statewide Reporting andAccounting Policy as follows:

Revenue Recognition

Revenues are recognized using the full accrual basis of accounting; therefore, revenues are recognizedin the accounting period in which they are earned and become measurable.

Expense Recognition

Expenses are recognized on the accrual basis; therefore, expenses, including salaries, are recognizedin the period incurred, if measurable.

B. BUDGETARY ACCOUNTING

Budgets are adopted by the Millennium Port Authority annually. The Millennium Port Authority budgets itsexpenses based on the state appropriations and grants it expects to receive each year. The budget wasprepared using the modified accrual basis of accounting. All budgetary appropriations lapse at the end ofeach fiscal year.

C. DEPOSITS WITH FINANCIAL INSTITUTIONS AND INVESTMENTS

1. DEPOSITS WITH FINANCIAL INSTITUTIONS

For reporting purposes, deposits with financial institutions include savings, demand deposits, timedeposits, and certificates of deposit. Under state law the Millennium Port Authority may deposit fundswithin a fiscal agent bank selected and designated by the Interim Emergency Board. Further, the (BTA)may invest in time certificates of deposit in any bank domiciled or having a branch office in the state ofLouisiana; in savings accounts or shares of savings and loan associations and savings banks and in shareaccounts and share certificate accounts of federally or state chartered credit unions.

1

STATE OF LOUISIANAMillennium Port AuthorityNotes to the Financial StatementAs of and for the year ended June 30, 2005

For the purpose of the Statement of Cash Flows, all highly liquid investments (including restricted assetswith a maturity of three months or less when purchased) are considered to be cash equivalents.

Deposits in bank accounts are stated at cost, which approximates market. Under state law these depositsmust be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent bank.The market value of the pledged securities plus the federal deposit insurance must at all times equal theamount on deposit with the fiscal agent. These pledged securities are held in the name of the pledgingfiscal agent bank in a holding or custodial bank in the form of safekeeping receipts held by the StateTreasurer.

GASB Statement 40 amended GASB Statement 3 to eliminate the requirement to disclose alldeposits by the 3 categories of risk. GASB Statement 40 requires only the disclosure of depositsthat are considered to be exposed to custodial credit risk. An entity's deposits are exposed tocustodial credit risk if the deposit balances are either 1) uninsured and uncollateralized, 2)uninsured and col lateral ized with securities held by the pledging financial institution, or 3)uninsured and col lateral ized with securities held by the pledging financial institution's trustdepartment or agent, but not in the entity's name.

The deposits at June 30, 2005 consisted of the following:

Galfficctes QherCash ofCaxsit fCesoribe) Totd

DEpcats in EErkAmrteFerBaaToeSreet $ 253426 $ $ $ 293,426

Efcrk BElarces of Cfepcats Bpoeed to QjEtoda1 Ctedt Rska UinsuBdanduxdlateia'izd $b LhnaredandodlaterElizBdwthseaiities

h^bythepleclgngirBtiUicric LhnajHJaidcdiaerdi dwthsaGLiitJeshdd

by tre piecing instiUicrfstnjstdepalrrHt oracBtbutnotHithemtity'snErre

Tola1 B=rkBalances-Al Deposits $ 293.426 $ $ $ 256,426

NOTE: The "Total Bank Balances - All Deposits" will not necessarily equal the "Deposits in Bank Accountper Balance Sheet" due to outstanding items.

STATE OF LOUISIANAMillennium Port AuthorityNotes to the Financial StatementAs of and for the year ended June 30,2005

The following is a breakdown by banking institution, program, account number, and amount of the balancesshown above:

Banking institution Program

1. Bank One2.3.4.

Amount

258.426

Cash in State Treasury and petty cash are not required to be reported in the note disclosure. However,to aid in reconciling amounts reported on the balance sheet to amounts reported in this note, list belowany cash in treasury and petty cash that are included on the balance sheet.

Cash in State Treasury $Petty cash $

2. INVESTMENTS

The Millennium Port Authority does not maintain investment accounts.

D. CAPITAL ASSETS - INCLUDING CAPITAL LEASE ASSETS

The fixed assets used in the Special Purpose Government Engaged only in Business-Type Activities areincluded on the balance sheet of the entity and are capitalized at cost. Depreciation of all exhaustiblefixed assets used by the entity is charged as an expense against operations. Accumulated depreciation isreported on the balance sheet. Depreciation for financial reporting purposes is computed by the straight-tine method over the useful lives of the assets.

STATE OF LOUISIANAMillennium Port AuthorityNotes to the Financial StatementAs of and for the year ended June 30,2005

Year ended June 30,2005Prior Adjusted

Balance Period Balance6/30/2004 Adjustment 7/1/2004 Additions Transfers* Retirements

Balance6/30/2005

Capital assets not being depredatedLandNon-depreciable land improvementsCapitalized collectionsConstruction in progress

Total capital assets not beingdepreciated

Other capital assetsFurniture, fixtures, and equipmentLess accumulated depreciationTotal furniture, fixtures, and equipment

Buildings and ImprovementsLess accumulated depreciationTotal buildings and improvements

Depreciable land improvementsLess accumulated depreciationTotal depreciable land improvements

InfrastructureLess accumulated depreciationTotal infrastructure

Total other capital assets

Capital Asset Summary:Capital assets not being depreciatedOther capital assets, at cost

Total cost of capital assetsLess accumulated depreciation

Capital assets, net

- $

20,283 $(3.498)

_ $

(3.412)20,283(6,910)

16,785 (3.412) 13,373

13,373

$

20,28320,283(3,498)

16,785 $ - $

_

(3.412)

- $ (3,412)$

20,28320,283(6,910)

- $ - $ 13,373

* Should be used only for those completed projects coming out of construction-in-progress to fixed assets; not associatedwith transfers reported elsewhere in this packet

E. INVENTORIES N/AF. RESTRICTED ASSETS N/AG. LEAVE N/AH. RETIREMENT SYSTEM N/AI. POST RETIREMENT HEALTH CARE AND LIFE INSURANCE BENEFITS N/A

J. LEASES N/AK. LONG-TERM LIABILITIES N/AM. RELATED PARTY TRANSACTIONS N/AN. ACCOUNTING CHANGES N/AO. IN-KIND CONTRIBUTIONS N/AP. DEFEASED ISSUES N/A

STATE OF LOUISIANAMillennium Port AuthorityNotes to the Financial StatementAs of and for the year ended June 30, 2005

Q. COOPERATIVE ENDEAVORS N/AR. GOVERNMENT-MANDATED NONEXCHANGE TRANSACTIONS (GRANTS) N/AS. VIOLATIONS OF FINANCE-RELATED LEGAL OR CONTRACTUAL PROVISIONS N/AT. SHORT-TERM DEBT N/AU. DISAGGREGATION OF RECEIVABLE BALANCES

Receivables at June 30, 2005, were as follows:

ActivityTransportation

CustomerReceivables Taxes

$ $

Receivablesfrom other

Governments$

OtherReceivables

3 16,667

TotalReceivables

$ 16.667-

Gross receivablesLess allowance for

uncollectible accountsReceivables, net $

Amounts not scheduledfor collection during the

subsequent year $ $

16,667 $

16.667 $

16,667

16,667

V. DISAGGREGATION OF PAYABLE BALANCES

Payables at June 30, 2005, were as follows:

Activity

Transportation $Transportation

Total payables $

Salaries

and AccruedVendors Benefits Interest

$ 18,500 $ $

- $ 18.500 3 - $

Other

Payables

33,334

33,334

$

$

Total

Payables18,50033,334

51,834

W. SUBSEQUENT EVENTS

Since inception, the Port received a substantial portion of its funding from State appropriations. For the2004 - 2005 and 2005 - 2006 fiscal years, the State eliminated the appropriation funding for the MillenniumPort.

X. SEGMENT INFORMATION N/A

Y. DUE TO/DUE FROM AND TRANSFERS N/A

Z. LIABILITIES PAYABLE FROM RESTRICTED ASSETS N/A

AA. PRIOR-YEAR RESTATEMENT OF NET ASSETS N/A

STATE OF LOUISIANAMillennium Port AuthorityNotes to the Financial StatementAs of and for the year ended June 30,2005

AB. GOING CONCERN

The accompanying financial statements have been prepared in conformity with generally acceptedaccounting principles, which contemplates continuation of the company as a going concern. However, theMillennium Port Authority has sustained a substantial operating loss during the year, which required theMillennium Port Authority to use substantial amounts of working capital in its operations. Further, theMillennium Port Authority has not received State appropriations for the 2004 or 2005 legislative sessions; norhave they received or expect to receive any additional funding during the 2005 fiscal year ended.

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF PER DIEM PAID TO BOARD MEMBERSFor the Year Ended June 30,2005

N/A- No commission members paid a per diem

Amount

SCHEDULE 1

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITYSCHEDULE OF STATE FUNDINGFor the Year Ended June 30, 2005

Description of Funding Amount

1. N/A - No state funding $

2.

3.

4.

5.

6.

7.

8.

9.

10.

Total

SCHEDULE 2

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF REIMBURSEMENT CONTRACTS PAYABLEJune 30,2005

N/A

Issue

Principal Principal InterestDate of Original Outstanding Redeemed Outstanding Interest OutstandingIssue Issue 6/30/PY (Issued) 6/30/CY Rates 6/30/CY

$ $. $ $_ $

Total

*Send copies of new amortization schedules

SCHEDULE 3-A

N/A

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITYSCHEDULE OF NOTES PAYABLE

June 30,2005

Issue

Principal Principal InterestDate of Original Outstanding Redeemed Outstanding Interest OutstandingIssue Issue 6/30/PY (Issued) 6/30/CY Rates 6/30/CY

$ $ $_ $_

Total $=

*Send copies of new amortization schedules

SCHEDULE 3-B

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF BONDS PAYABLEJune 30,2005

N/A

Issue

Principal Principal InterestDate of Original Outstanding Redeemed Outstanding Interest OutstandingIssue Issue 6/30/PY (issued) 6/30/CY Rates 6/30/CY

$ $_ $ $ $

Total $_

*Send copies of new amortization schedules

SCHEDULE 3-C

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF REIMBURSEMENT CONTRACTS PAYABLE AMORTIZATIONFor The Year Ended June 30,2005

N/A

Fiscal YearEnding: Principal Interest

2006 $ $20072008

200920102011201220132014

20152016

2017

2018

2019202020212022

2023

20242025

2026

2027

2028

20292030

Total

SCHEDULE 4-A

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF CAPITAL LEASE AMORTIZATIONFor The Year Ended June 30,2005

N/A

Fiscal YearEnding: Payment Interest Principal Balance

2006

2007

2008

2009

2020

2011-2015

2016-2020

2021-2025

2026-2030

Total

SCHEDULE 4-B

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF NOTES PAYABLE AMORTIZATION

N/A

Fiscal YearEnding: Principal

2006

2007

2008

2009

2010

2011-2015

2016-2020

2021-2025

2026-2030

Total

SCHEDULE 4-C

STATE OF LOUISIANAMILLENNIUM PORT AUTHORITY

SCHEDULE OF BONDS PAYABLE AMORTIZATIONFor The Year Ended June 30,2005

N/A

Fiscal YearEnding: Principal Interest

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

20212022

2023

2024

20252026

2027

2028

2029

2030

Total

SCHEDULE 4-D

STATE OF LOUISIANA

MILLENNIUM PORT AUTHORITY

COMPARISON FIGURES

To assist OSRAP in determining the reason for the change in financial position for the State, please completethe schedule below. If the change is greater than $1 million, explain the reason for the change.

1) Revenues

Expenses

2) Capital assets

Long-term debt

Net Assets

2005

63,289 $ 737,503 $

318,243368,149

13,373

236.632 $

16.785

541,492 $

Difference

(674.214)

49.906

(3.412)

(304.860)

PercentageChanae

(1,065)%

14%

(25)%

(129)%

Explanation for change:

SCHEDULE 15

ahim

DUPLANTIER, HRAPMANN,HOGAN & MAHER, L.L.E

MICHAELJ.O<ROURKE,C.P.A. |^| • fll CERTIFIED PUBLIC ACCOUNTANTS A.j.DUPLANTIER, JR.,C.P.A.WILLIAM G. STAMM, C.P.A. • • • • • • (1919-1985)CLIFFORD J. GIFFIN, JR., C.P.A. FELIX J. HRAPMANN, JR., C.P.A.DAVID A. BURGARD, C.P.A. (1919-1990)LINDSAYJ.CALUB,C.P.A.,L.L.C. 1340 Poydras St., Suite 2000 • New Orleans, LA 70112 WILLIAM R. HOGAN, JR., C.P.A.GUY L. DUPLANTIER, C.P.A. J /cn-1\ CQ£ QQ,I£ (1920-1996)MICHELLE H. CUNNINGHAM, C.P.A. (5U4) b«6-»»66 JAMES MAKER, JR., C.P.A.

DENNIS W. DILLON, C.F.A. FAX (5Q4) 525-5888 (1921-1999)

ANN M. BARGES, C.P.A. [email protected] A. STROHMEYER, C.P.A. MEMBERS

AMERICAN INSTITUTE OF

KENNETH J. BROOKS, C.P.A., ASSOCIATE CERTI™D.?H5LJS *S?:?™TANTS

Legislative AuditorEngagement ProcessingPost Office Box 94397Baton Rouge, LA 70804

SCHEDULES AND DATA COLLECTION FORM

SECTION 1: SUMMARY OF AUDITOR'S REPORT

A. FINANCIAL STATEMENT AUDIT OPINION:

We have audited the financial statements of the Millenium Port Authority as of and for the year endedJune 30, 2005 and have issued our report thereon dated July 26, 2005. We conducted our audit inaccordance with auditing standards generally accepted in the United States of America and thestandards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States. Our audit of the financial statements as of June 30, 2005resulted in an unqualified opinion.

The financial statements have been prepared in conformity with accounting principles generallyaccepted in the United States of America, which contemplates continuation of the company as a goingconcern. However, the Millennium Port Authority has sustained a substantial operating loss during theyear, which required the Millennium Port Authority to use substantial amounts of working capital in itsoperations. Further, the Millennium Port Authority has not received State appropriations for the 2004or 2005 legislative sessions; nor have they received any additional funding during the 2005 fiscal yearended.

B. REPORT ON COMPLIANCE AND ON INTERNAL CONTROL OVERFINANCIAL REPORTING:

Internal Control:

Material weaknesses - None notedReportable conditions - None noted

Compliance:

Noncompliance - See attached 05-01 through 05-02

-2-

SECTION 2: FINANCIAL STATEMENT FINDINGS

A. CURRENT YEAR FINDINGS:

05-01

Several meal reimbursements tested were not in compliance with the Louisiana Travel Guide. Itemswere noted such as, meals were provided for contractors and commissioners for local monthly meetingsand several meals did not contain proper documentation. It is our understanding that the Authority isrequired to follow the Louisiana Travel Guide. We recommend that the Authority follow theguidelines set forth in the Louisiana Travel Guide. If the Authority feels as though it does not fallunder the jurisdiction of the Louisiana Travel Guide, we recommend that they seek an AttorneyGeneral's opinion regarding meal reimbursement.

05-02

During the testing of the Louisiana Budget Act, it was discovered that the Millennium Port Authority didnot amend the budget when revenues fell below 5% or more of the projected budget. It was also notedthat the Authority did not publish a notice in a newspaper which states that the proposed budget isavailable for public inspection. Not following the preceding procedures is a violation of the LouisianaBudget Act (L.R.S. 39:1305-1308). We recommend that the Millennium Port Authority amend thebudget when revenues fall below 5% of projected amounts, and publish a notice in the local newspaperthat the proposed budget is available for public inspection.

-3-

SECTION 3: PRIOR YEAR FINANCIAL STATEMENT FINDINGS

B. PRIOR YEAR FINDINGS:

04-01

During the prior year audit it was noted that several travel and meal reimbursements tested were not incompliance with the Louisiana Travel Guide. The Authority paid in excess of the meal allowance andpaid meals for those not traveling. Paying in excess of the state travel policy for meals and paying mealsfor those not traveling is in violation of state travel policy. We recommend that the Authority seek anAttorney General's opinion regarding meal reimbursement. This comment regarding mileage has beenresolved during 2005; the comment regarding meal reimbursement is repeated hi 2005.

04-02

The Millennium Port Authority did not submit the accounting financial reporting package by August 30,2004 as required by The Division of Administration, Office of Statewide Reporting and AccountingPolicy (OSRAP). This has been resolved in 2005.

04-03

In the prior year it was noted the controls over federal and state funds were inadequate. The Authority didnot have an adequate review procedure for grant agreements nor did they have a system in place to ensureall federal and states funds were spent properly. Without proper procedures in place, the Authority couldobtain federal funds improperly. This issue has been resolved in 2005.

MIUEMNIUM PORT 135° Port of New Orleans Placek UTHORITY New Orleans, Louisiana 70130

d^g jjjjjjjjj&g ! Telephone: 504-528-3366 / 3282

August 26,2005

Legislative AuditorState of LouisianaPost Office Box 94397Baton Rouge, Louisiana

Dear Legislative Auditor,

During the conduct of the current year audit, the outside auditor identified two instanceswhere the Authority was considered to be not in compliance with all laws and regulations. Oneinvolved meal reimbursement expenses and the other included some budget handling issues. Thefollowing responses to these instances of noncompliance are provided for your consideration.

The Authority has provided several meals in conjunction with meetings in keeping withthe attached written policy. The "Policy on Meals and Entertainment" is similar to that followedby several ports and has been submitted to the Attorney General for an opinion as shown in theattachment. An opinion has not yet been rendered.

The Millennium Port Authority budget was approved at the 31st meeting of the Authorityon August 17,2004. At that time, revenue was expected by reimbursement from the federalgovernment for Millennium Port Feasibility Study expenditures; revenue is based on 50%reimbursement of study expenditures upon submission of paid invoices. Near the end of thefiscal year, we expected to receive some reimbursement for expenditures for a "TransportationInfrastructure Study". Due to scheduling delays on the study, invoices were not available forsubmission and reimbursement was not received. Near the end of the Fiscal Year, receipt ofthese invoices was anticipated and it was considered not cost effective to call a special Boardmeeting to adjust proposed budget documents while the possibility existed of having to changethe budget again upon actual arrival of the invoices. An invoice has now been received and isbeing processed for federal reimbursement. The Authority will advertise the availability of thecurrent and future budgets as required.

Sincere!

Edward PeakExecutive Director

AttachmentMPA letter to Attorney General dated June 8, 2005