Embed Size (px)

Citation preview

Critical Perspectives on Accounting 19 (2008) 81–96

Mind the gap: Accountants at work and play

David Haynes b,∗,2, Susan P. Briggs a,1, Scott Copeland a

a University of South Australia, School of Commerce, City West Campus,GPO Box 2471, Adelaide 5000, Australia

b University of South Australia, Psychology Department Magill Campus,Lorne Avenue, SA 5072, Australia

Received 14 September 2005; accepted 28 January 2006

Abstract

Unitary scales like the Myers-Briggs type indicator (MBTI) and the NEO-PI-R may be inadequatemeasures of the ability for personality changes across situations. The paper offers an alternativepersonality measure called the typotypical behaviour indicator (TBI) which has been developed bythe authors over a 7-year period to fill the current gap. This paper determines whether students ofaccounting show the same preferences in two important life situations, at work and when socializingusing the MBTI and the TBI.

The results using the MBTI on 356 third year accounting students showed overall preference forthe dimensions of sensing, thinking and judging, of 40% in 2002 and 35% in 2003. Using the TBIthis rose to an alarming 52 and 58% in 2002 and 2003, respectively, at work but plummeted to 13%in both years in social situations, respectively.

These results suggest that many students of accounting adopt quite different personality profilesin different situations. The results also suggest the need for a major reassessment of the assumptionsoften made about stereotypical accountant’s personalities.© 2006 Elsevier Ltd. All rights reserved.

Keywords: Accountants; Personality; Stereotype; Gender; Psychological type; Myers-Briggs type indicator(MBTI); Typotypical behaviour indicator (TBI)

∗ Corresponding author. Tel.: +61 8 8302 0635; fax: +61 8 8302 0992.E-mail addresses: [email protected] (D. Haynes), [email protected] (S.P. Briggs),

[email protected] (S. Copeland).1 Tel.: 61 8 8302 0018; fax: 61 8 8302 0992.2 Tel.: 61 8 8302 4340.

1045-2354/$ – see front matter © 2006 Elsevier Ltd. All rights reserved.doi:10.1016/j.cpa.2006.01.014

82 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

1. Introduction

There have been dramatic changes in the accounting profession in recent decades (Wolkand Nickolai, 1997) and many of the challenges facing the profession today, for example,the increasingly narrow centred goals of turning out procedural accountants (Boyce, 2004),are said to be related to personality (Wheeler, 2001; Wheeler et al., 2004). These include thepersonality characteristics of those entering the profession and the nature of the educationthat they receive (Amernic and Beechy, 1984).

An opportunity exists as Wheeler (2001) pointed out for accounting education researchersto investigate the personality of accounting students and professionals to address the issuesthat are affecting accountants. To be able to understand the personality traits of the indi-viduals who make up the profession and how that affects them at work. However, researchin this area to date, has mostly utilised the Myers-Briggs type indicator (MBTI) or (lessoften) the NEO-PI-R of Costa and McRae (1985). Personality has often been described asrelatively constant across time and situations as though it were a stable entity, leading topredictable and relatively constant behaviours. Much of the research evidence suggests thismay not be true at all. While both give a global assessment of some important personalitytraits, neither show variations across situations. We would like to pose a questions aboutthis. Is personality, in fact, consistent across life situations? Are accountants different atwork than socially? If we have multiple identities, then how do we stitch them together?Does the job/tasks turn individuals into the stereotypical accountant as Max Harris claimedabout the Australian Prime Minister John Howard “who he said was the embodiment ofa Chartered Accountant because he was so coldly reasonable, so piscine, so dead-pan” ascited in Craig (2002) article in the Canberra Times.

This paper addresses Wheeler’ concerns by looking at the personality of third yearaccounting students (most of whom are working) to see if the results of personal-ity preferences are the same as previous researchers findings, like Wolk and Nickolai(1997).

It then looks at the lack of external behavioural validation of the MBTI as ‘true’ typeacross specific situations.

A new cross-situational behavioural measure that can be related to personality typologyusing the MBTI is introduced and tested with the MBTI on the same third year accountingstudents over the same 2-year period to provide a way of measuring personality across lifesituations.

Hence, this paper is divided into seven parts.First, a brief discussion of the problems associated with the apparent need for change in

the personnel being recruited into the profession. More specifically, the personality makeupof the profession.

Second, a brief look at the MBTI and the NEO-PI-R as two models used to measurepersonality and the parameters generally measured.

Third, a brief summary of the research using the MBTI to date upon accountants’ person-alities. We could find no evidence to date that the NEO-PI-R has been used on accountants.

Fourth, a critical look at the validity of this research. In particular, the assumption thatpersonality is a stable psychological structure, with invariant links to certain preferencesfor behaviour.

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 83

Fifth, a brief discussion of what is known about the stability or changeability of person-ality with time and across situations.

Sixth, and following from the above, an account of our attempt to devise a measureof personality across situations. Or rather, several equivalent measures that can be effec-tively applied to the measurement of self-reported, personality-related behaviours acrosssituations.

Finally, an account of our results over 2 years showing the differences in personality inaccounting students at work and in their social lives. The implications of these results inrelation to the usefulness of conventional measures of personality, the adaptability of (andpossible stresses experienced by) accounting students and future directions for accountingeducation are also discussed.

1.1. The need for change

While there has been only limited research to date on the relationship between personal-ity and problems affecting the accounting profession (Wheeler, 2001; Wheeler et al., 2004)results so far have suggested that there are problems in relation to the desired personal-ity ‘makeup’ of the profession, factors affecting the choice of accounting as a career andthe effects of accounting training on the relative success of students of different personal-ity ‘types’ (Wolk and Nickolai, 1997). The implications for the accounting profession is,irrespective of what attracts people to the profession, be that, class, education and fam-ily background, more varied personality types need to be attracted to and retained by theaccounting profession to address the skills required for the global business environment(Mohammed and Lashire, 2003).

In 1997 the CPA in the United States released a set of vision elements containing thetop five core values, core competencies and core services required by accountants. Thethree categories of competencies were functional, personal and broad business perspective.As an example, one of the competencies mentioned in the vision project is in regards toindividuals preparing to enter the accounting profession, they must be able to use strategiccritical approaches to decision-making. That is, for example, the accountant is required toobjectively consider problems and have the ability to identify alternative solutions. Theyalso are expected to perform risk analysis to identify negative outcomes including fraud(AICPA, 1999, 2000).

The question is do accountants possess the necessary skills to meet this vision andcan they be trained to? Information of this sort should be of interest to accounting firmsand employment organisations who request diverse graduates, to professional bodies whoembrace new sets of skills like critical thinking, to accounting educators to rethink theircourses to enhance the skills required to stamp out the common stereotype of accountants.

1.2. Personality measures

Discussion regarding the best measure of personality has been occurring over the lastdecades. The MBTI and the NEO-PI-R are two favoured models (McRae and Costa, 1989).

In our opinion, the MBTI is of greater interest, as it measures only normal personalitytraits and conceived of these as being composed of opposite, but equally valid, tendencies

84 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

(for example, thinking versus feeling). The NEO-Pi, by contrast, includes measures of‘neurosis’ that can have negative overtones and regards traits as being essentially unipolar:thus it will measure a tendency to feeling (or ‘agreeableness’), but not its opposite. It alsohas no real basis in psychology theory. Wheeler et al. (2004) shared our opinion in theircommentary on using the MBTI. However, both may be inadequate measures of ability forpersonality changes across situations.

2. The Myers-Briggs type indicator (MBTI)

The MBTI is the most popular measure of normal personality preferences in the worldtoday, is taken by several million people annually, and is based on the research of Jung(1875–1961). Jung came to believe that there were certain habitual attitudes or ways ofseeing, or making decisions in the world that people tended to adopt. He thought that sixwere particularly important. First, the two basic attitudes (as he called them) of introver-sion and extraversion. Second, two pairs of functions. Sensing and intuition – two waysof taking in information from the world – termed the perceiving functions. And thinkingand feeling – two ways of making decisions – called the judging functions. The MBTImeasures self-attributed personality preferences on the three Jungian dimensions, extraver-sion versus introversion (EI), sensing versus intuition (SN), thinking versus feeling (TF)and the judging–perceiving axis (JP). It has a forced-choice format for each item, wherebysubjects are asked to choose between two alternative words or statements signifying pref-erences for one side of each preference dimension. Sensing types are those who see theworld as being made up of data, facts, while intuitives prefer ideas and possibilities. Think-ing types use logic or take a rational approach to decision-making whereas, feeling typescreate a world based upon values and human feelings. Judging types like foreclosure andare reluctant to change their mind, whereas perceiving types like to raise possibilities.While Jung conceded that personality varied from time to time and situation to situa-tion, he did believe that most people prefer one of each of the pairs above most of thetime.

The reliability and validity of the measure have been exhaustively described in theliterature (Harvey, 1996; Nunnally and Bernstein, 1994; Wheeler, 2001). Scores on themeasure are utilised for research in two ways. Scores can be used as continuous trait scoresor they may be used as net scores for each preference: this approach yields an individual‘typology’ that can be denoted by the four letters attributed to each preference. Usingthe typological approach often makes findings easier to understand and interpret and thisapproach is supported by a very large literature that purports to show how the different‘types’ behave in a wide variety of situations. For simplicity of explanation, the net scoresapproach will be used in this paper.

2.1. Previous research

While some researchers have tested accounting students like Booth and Winzar (1993)and Laribee (1994) and others have tested accounting professionals like Jacoby (1981),Kriesler (1990), Schloemer and Schloemer (1997) and Shackleton (1980) the results appear

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 85

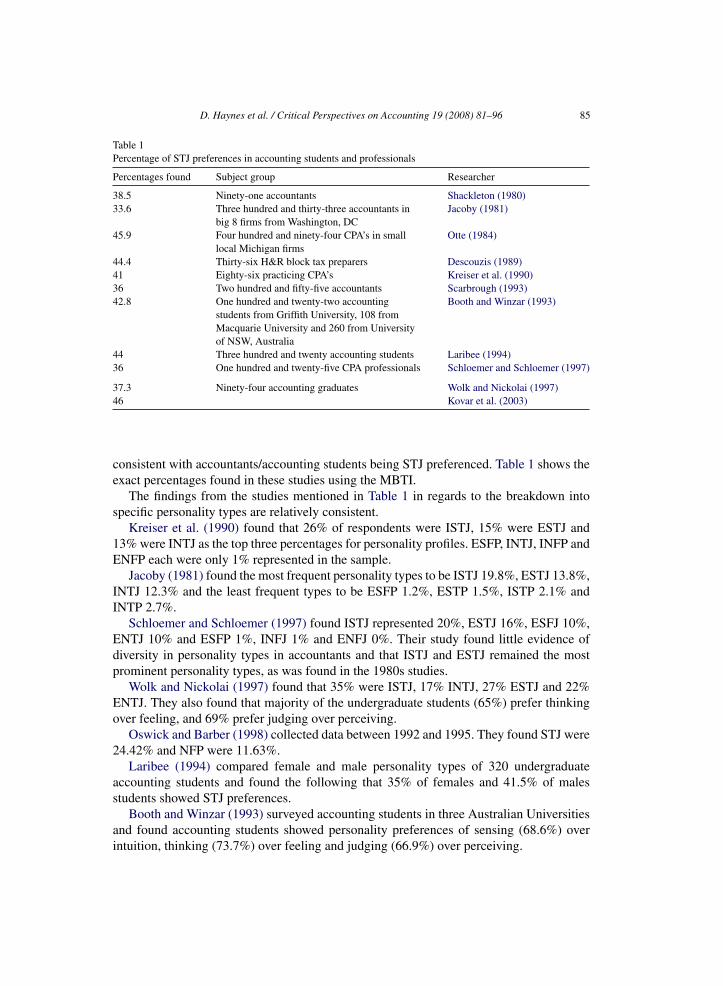

Table 1Percentage of STJ preferences in accounting students and professionals

Percentages found Subject group Researcher

38.5 Ninety-one accountants Shackleton (1980)33.6 Three hundred and thirty-three accountants in

big 8 firms from Washington, DCJacoby (1981)

45.9 Four hundred and ninety-four CPA’s in smalllocal Michigan firms

Otte (1984)

44.4 Thirty-six H&R block tax preparers Descouzis (1989)41 Eighty-six practicing CPA’s Kreiser et al. (1990)36 Two hundred and fifty-five accountants Scarbrough (1993)42.8 One hundred and twenty-two accounting

students from Griffith University, 108 fromMacquarie University and 260 from Universityof NSW, Australia

Booth and Winzar (1993)

44 Three hundred and twenty accounting students Laribee (1994)36 One hundred and twenty-five CPA professionals Schloemer and Schloemer (1997)

37.3 Ninety-four accounting graduates Wolk and Nickolai (1997)46 Kovar et al. (2003)

consistent with accountants/accounting students being STJ preferenced. Table 1 shows theexact percentages found in these studies using the MBTI.

The findings from the studies mentioned in Table 1 in regards to the breakdown intospecific personality types are relatively consistent.

Kreiser et al. (1990) found that 26% of respondents were ISTJ, 15% were ESTJ and13% were INTJ as the top three percentages for personality profiles. ESFP, INTJ, INFP andENFP each were only 1% represented in the sample.

Jacoby (1981) found the most frequent personality types to be ISTJ 19.8%, ESTJ 13.8%,INTJ 12.3% and the least frequent types to be ESFP 1.2%, ESTP 1.5%, ISTP 2.1% andINTP 2.7%.

Schloemer and Schloemer (1997) found ISTJ represented 20%, ESTJ 16%, ESFJ 10%,ENTJ 10% and ESFP 1%, INFJ 1% and ENFJ 0%. Their study found little evidence ofdiversity in personality types in accountants and that ISTJ and ESTJ remained the mostprominent personality types, as was found in the 1980s studies.

Wolk and Nickolai (1997) found that 35% were ISTJ, 17% INTJ, 27% ESTJ and 22%ENTJ. They also found that majority of the undergraduate students (65%) prefer thinkingover feeling, and 69% prefer judging over perceiving.

Oswick and Barber (1998) collected data between 1992 and 1995. They found STJ were24.42% and NFP were 11.63%.

Laribee (1994) compared female and male personality types of 320 undergraduateaccounting students and found the following that 35% of females and 41.5% of malesstudents showed STJ preferences.

Booth and Winzar (1993) surveyed accounting students in three Australian Universitiesand found accounting students showed personality preferences of sensing (68.6%) overintuition, thinking (73.7%) over feeling and judging (66.9%) over perceiving.

86 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

2.2. The validity of research to date

2.2.1. What Jung actually said about type. Consistency of personality and the conceptof true type

The concept of psychological type, as assessed by the Myers-Briggs type indicator, andother measures, is largely based upon the original ideas of Carl Jung. Jung described certaindimensions of personality as mentioned earlier—extraversion and introversion, thinkingand feeling and sensing and intuition, but what did he actually say about the resultantconsistency of type?

That psychological type varies all the time . . . but . . . there were certain constancies forhim. For others, perhaps, just a loose alliance of three pairs of tendency. He clearly stated‘psychological type is nothing constant, it changes always’ (Jung, 1960).

This view is seldom heard in MBTI circles. Rather, it is replaced by the concept of‘true type’. This concept assumes that an individual’s personality type is innate, or at least‘natural’ to that individual and begins to take shape within the first few years of life. Thedevelopment and understanding of one’s ‘true type’ is then considered to be an importantpart of individuation: it is generally assumed that individuals are – or can be – consciouslyaware of their preferences and have a measure of control over their behavioural manifes-tations (see, for example, McCaulley, 1990; Myers, 1993; Myers and McCaulley, 1985).It is also often assumed that an individual’s typology will affect their behaviour in charac-teristic ways in pretty well every situation. That ‘typotypical’ behaviours do exist in everysituation and are well known. Many texts on typology and work, for example, will give ageneral description of the characteristics of a particular personality type and then describe,with apparent precision and certainty, and without any caveats at all, how a person withthis typology will characteristically behave in a variety of work situations. This particularassumption has led to such great interest in the (assumed) relationship between the MBTIand workplace behaviour that currently nearly 40% of MBTI administration is carried outby major corporations for applied purposes such as team building and management devel-opment (Gardner and Martinko, 1996).

All of these statements and assumptions have been criticised, however. Thus, manypsychologists maintain that the MBTI merely measures a few important personality traits(McRae and Costa, 1989; Pittinger, 1993; Wiggins, 1989), perhaps somewhat akin to the‘central traits’ proposed by Allport. This suggestion is the basis for much of the criticismof its psychometric structure. Thus, the forced-choice format of the MBTI (which can yieldonly ipsative and not normative results), the uneven weightings of items and the unequalscale lengths are all the result of the initial attempts to discover items that would maximallydistinguish groups of subjects of different typologies (Myers and McCaulley, 1985).

All of this leads to the crucial issues addressed by this paper. The supposed relative lackof external (behavioural) validation of the MBTI and the inevitable conflict between thenecessity to develop the MBTI as the best available measure of true – or overall – type andthe real need of managers and others to know how individuals are likely to actually behavein specific situations. When the MBTI is used in relation to work behaviour, issues of howtypology and resultant typotypical behaviours might affect competence and of person–jobmatch (the degree to which an individual’s typology can be reconciled to the behaviouraldemands of their job without stress-creation) inevitably arise. This makes it essential to

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 87

know precisely the degree to which an individual’s type relates to (and consistently controls)behaviour across situations.

The basic problem, to summarise is that, while the MBTI may be the best generalmeasure available to measure personality on the four dimensions that it contains, it isprecisely designed to be only a general measure. As it does not measure behaviour inspecific situations, it must lack external validity (Gardner and Martinko, 1996).

2.3. The stability of personality traits

Most theories of personality traditionally assume that personality has a high degree ofconsistency—across time and situations. That is, the behaviours associated with personalityparameters (for example, personality traits like extraversion are relatively constant (Bemand Allen, 1974; Carver and Scheier, 1996; Costa and McRae, 1998; Diener and Larsen,1984). As stated above, items on scales such as the NEO-Pi and the MBTI are based on theassumption that self-reported traits are consistent across time and situations.

However, there has been a long history of controversy as to whether personality canchange, without any consensus within the literature. That is, is personality developed orgiven? In fact Piaget (1932/1965) and other theorists have debated how people learn. Resultsfrom empirical research have been inconsistent and often unconvincing.

While an overview of some of the personality literature seems to suggest that, by earlyadulthood, personality is “set like plaster”(Costa and McRae, 1997) and some studies,including some by Costa and McRae (1988) and McRae and Costa (1990) have providedempirical evidence to support this view, many other studies have not. For example, McRaeet al. (1999) reported differences with age on the NEO-PI-R, in 12,000 subjects from ninecountries. Overall, conscientiousness and agreeableness increased with age, extraversion,openness and neuroticism declined.

As regards consistency across situations, as early as Harshorne and May (1928) found thatdiverse measures of “moral character’ in children showed little consistency across situations.Similarly, Newcomb (1929) found only correlations of about r = 1.4 for extraverted orintroverted behaviours across situations in American boys. Piaget (1932/1965) argued thatmoral development was not simple a process of “stamping in” cultural expectations. Insteadof it being passed from generation to generation, it goes beyond conforming to traditionalrules and is constructed by the individual. Research of this sort led to Mischel (1968) bookPersonality and assessment, in which he concluded that behaviour is determined, more byproperties of situations than by people. He argued that people do not exhibit the cross-situational consistency of behaviour that should be produced by the real existence of traits.He noted that correlations between trait measures and related behaviours seldom exceededr = .3 in the research literature (accounting for only 9% of variance).

While there have been many responses to Mischel’s critique over the last three to fourdecades, it has never been convincingly refuted. Mischel and Peake (1982), for example,found only a cross-situational correlation for .03 for conscientiousness across (academic)conscientiousness, as compared to Funder and Colvin (1991) who found correlations of.37–.68 in cross-situational withdrawal, domineeringness, serious intelligence and hetero-sexuality. So, it clearly has not been proved that personality traits are stable personalitybuilding blocks.

88 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

Moreover, much research has suggested that situational constraints and situational rele-vance are important determinants of behaviour. Thus, Price and Bouffard (1974) found thatcertain settings were associated with a large range of behaviours: far more in parks thanin churches, for example. Powerful situations were assumed to elicit behaviour specificto the situation (churches), while in weak situations individual differences may becomemore apparent (parks). Monson et al. (1982) found that introvert–extravert differences werereduced in strong situations and Tett and Gutterman (2000) have suggested that, in fact, per-sonality traits require trait-relevant situations for their expression. The situation is neededto ‘activate’ the trait.

In summary, although there is some consensus that self-reported traits may be useful inpredicting behaviour when situational constraints are weak, but not when they are strong,research evidence is not yet conclusive.

The present research therefore – at the very least – has attempted to fill a pretty widegap in the literature, by attempting to measure the variations in (self-reported) trait-relatedbehaviours (and important traits) in two important and (for accountants) universal situations:work and social life. Before it could begin, however, it was necessary to devise an appropriateinstrument.

2.4. The development of the typotypical behaviour indicator (TBI)

While the Myers-Briggs type indicator (MBTI) is the most used and most successfulmeasure available today of the four important parameters of normal personality, it has alsoattracted criticism (especially from psychologists) in relation to its conceptual foundations,its psychometric properties, its intended objects of measurement and – and especially forour purposes today – its supposed relative lack of external (criterion) validity (Gardner andMartinko, 1996). This latter criticism, as we have seen, is particularly relevant to argumentsabout the degree to which the MBTI can, or should be used as a measure of actual andsituation-specific behaviours.

What, then, do the items of the MBTI actually measure? An examination of the items ofthe MBTI (Form K) reveals that the great majority of scored items (81/94) are not relatedto behaviours in specific environmental contexts (such items will be termed ‘situation-neutral’ in orientation below). Rather, they are designed to measure general self-perception:while the majority of non-word choice items do relate to behaviour, they are carefully de-contextualised. There are some exceptions, however. Thus, 10 items (numbers 9, 18, 19, 21,23, 27, 78, 90 and 105 and 108) are clearly related to social behaviour and 3 (numbers 7, 22and 102) to behaviour in the work environment. These contaminate the situation-neutralityof the measure and its overall orientation should be regarded as generally situation-neutral,but with something of a bias towards measuring social behaviour. It cannot be said to directlymeasure behaviour in work, home, university or other environments.

This finding has been noted by many organisational users of the MBTI. In a reviewof a psychological type and management research, Gardner and Martinko (1996), whileacknowledging the extensive evidence of criterion validity for the MBTI obtained fromtype distribution tables, and a few behavioural findings in relation to type, maintain that the‘lack’ of stronger behavioural validation, together with the fact that the items of the MBTIdo not directly relate to the managerial characteristics and workplace behaviours that are of

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 89

greatest research interest has had an unfortunate effect upon the reputation and usage of theMBTI. This, in turn, has led to the development of a wide range of ‘MBTI-clone’ measuresthat are specifically designed to measure (usually managerial) personality and self-reportedbehaviour in the workplace. Unfortunately, however, none of these measures contain itemsthat are provenly equivalent to those of the MBTI. And results from the Singer–LoomisInventory, the Gray Wheelwright Test and many other measures have consistently shown thatdifferent measures devised by different minds, even when based upon the same theoreticalconcepts, are never equivalent and often actually measure different constructs (Gray et al.,1964; Singer and Loomis, 1984).

The only answer to problems of this sort is the development of measures of typo-typical behaviour in work (and other) situations in such a way that reported behaviourcould be directly related to personality type, measured using the MBTI. The items mea-suring behaviour must therefore be either directly developed from the items of the MBTIor groups of items proven to be psychometrically equivalent to the latter. They must beitems which, when taken out of situational context, are strongly correlated with the scalesthe MBTI but which, with only minor adjustments, can be turned into measures of self-reported behaviour in a variety of specific situations. Such measures should reveal whetherbehaviours at work, for example, are those expected from an individuals type, and whether(typotypical) behaviours really vary across situations. Only then will it be possible to inves-tigate whether (and in whom), behavioural differences across situations are a real problem,a source of stress, or an opportunity for further self-development.

The aim of the present research has been the development of cross-situational behaviouralmeasures that can be related to personality typology, as measured using the MBTI, theKeirsey Temperament sorter and some of Eysenck’s scales. Use has been made of itemsfrom a variety of sources. A Likert-style format was used throughout, for two reasons: firstbecause attempts to measure behaviour are primarily quantitative in nature: second becausea number of workers (for example, Girelli and Stake, 1993) have demonstrated that itemsof the MBTI, when put into a Likert-style format seem to be the psychometric equals of thesame items in the original, forced-choice format.

Development of the TBI has taken 7 years. In the initial stages, 320 items were devisedand given situation-neutral, social life-related work-related and family life-related formats.Eighty items were intended to correlate strongly with each of the scales of the MBTI. Itemswere administered (in 2 questionnaires of 160 items each) to groups of more than 100subjects at the same time as the MBTI. Subjects were drawn from a wide variety of groups.Some items were original, some were modified, with consent, from the organisationalpersonality measure (OPM)—a scale devised several years ago by the management of amajor Adelaide company, based on Jungian type theory and designed to measure typotypicalbehaviours in managers (in house). All items were given a five-point Likert-style formatand randomly oriented and distributed. All four versions of all items were tested.

Scores on 172 items (when given a situation-neutral format) were found to correlate atr = .4 or better with scores on one of the scales of the MBTI. Similar correlations wereobtained, for the great majority of items, when a social life-related format was used. Cor-relations with scores on scales of the MBTI were consistently weaker when work-relatedor family life-related formats were used. This encourages us to think that there might bebehavioural differences across situations.

90 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

After this beginning, a wide variety of items were tested and three successive versions ofthe TBI were developed. The version used in the current research (TBI-4) has the followingproperties.

The TBI-4 contains 144 items, organised into three measures (A–C). The three measureshave almost identical psychometric properties. Each contains 48 items; 12 items measuringself-assessed personality-related behaviour on each of the dichotomous Jungian scales.Scores on all items had consistently correlated at r = .35 or greater (in three trials), withscores on the appropriate scale of the MBTI and correlated at r = .4 or greater on theappropriate scale of the TBI-4. Items were also selected to cover a broad range of thecharacteristics of the personality dichotomy of their scale (to be discussed in detail in alater paper). Scores on the three equivalent scales of the TBI (for example, the three scalesmeasuring extraversion–introversion), always correlated with each other at r = >.9.

The matter of zero scores was also of importance. The scores that represent an exactbalance between a pair of preferences. In the case of the MBTI, each item is forced-choiceand provides the subject with (usually) one or two points for one of an opposing pair ofpreferences: a point for extraversion, or a point for introversion perhaps. When all itemshave been answered, scores are summated—so many for extraversion, say, so many forintroversion, the smaller score is deducted from the larger and a net preference score isobtained. Zero scores – when two preferences are equal – are represented by a notional scoreof 100. In practice, because subjects have to be allocated to typological groups, individualzero scores are avoided. This is done by awarding a ‘bonus’ point for introversion, intuition,feeling and perceiving to subjects who would otherwise be typologically balanced.

The TBI has 12 items per scale, with scores of 1–5 on each. Scoring is so designed that,for each item, a strong preference for extraversion, sensing, thinking or judging (ESTJ)receives one point, a strong preference for introversion, intuition, feeling and perceiving(INFP) five points. Scores on each pair of preferences thus range from 12 to 60. Zero scoreson each scale should, in theory, be 36. However, as the purpose of the present research wasto compare typological preferences on the TBI and the MBTI, it was decided that TBI zeroscores should be taken as the average scores obtained on the four scales of the situation-neutral versions of the TBI by groups of subjects who (at the same time) achieved zeroscores (of 100) on all four scales of the MBTI.

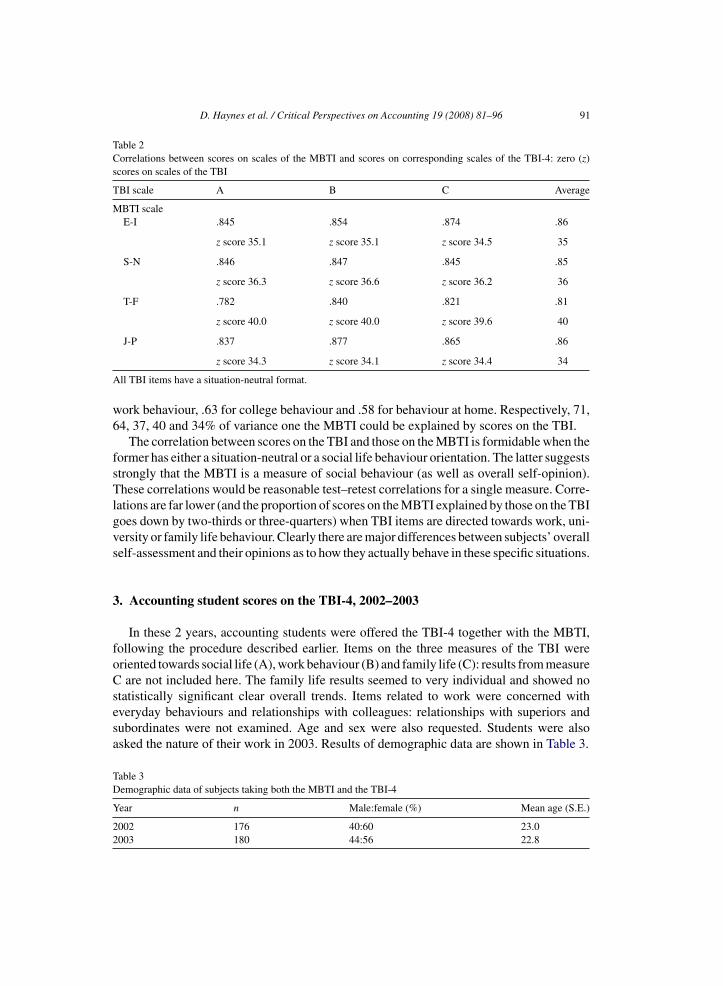

Zero scores for all the scales of the TBI-4 are shown in Table 2. Zero scores forthe equivalent scales are almost identical for all three measures (A–C). Zero scoresfor sensing-intuition are also almost precisely 36. However, zero scores of 35 forextraversion–introversion and judging–perceiving and of 40 for thinking–feeling, suggesta slight ‘drift’ on the part of subjects having zero scores on the MBTI towards extraversionand judging, a clear movement towards feeling, when given the option of relative, ratherthan absolute, preference choices. For the purposes of this paper, subjects having a scoreless than the zero score on any scale are classified as having preferences for extraversion,sensing, thinking or judging, while subjects having a zero score or above are classified ashaving a preference for introversion, intuition, feeling or perceiving.

Correlations between scores on the scales of the TBI (in a situation-neutral format) andscores on the scales of the MBTI are also shown in Table 2: zero scores are also shown. In alittle more detail, where scores on the TBI correlated at .845 overall with scores on the MBTI,equivalent figures were .80 when items were directed to measure social behaviour, .61 for

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 91

Table 2Correlations between scores on scales of the MBTI and scores on corresponding scales of the TBI-4: zero (z)scores on scales of the TBI

TBI scale A B C Average

MBTI scaleE-I .845 .854 .874 .86

z score 35.1 z score 35.1 z score 34.5 35

S-N .846 .847 .845 .85

z score 36.3 z score 36.6 z score 36.2 36

T-F .782 .840 .821 .81

z score 40.0 z score 40.0 z score 39.6 40

J-P .837 .877 .865 .86

z score 34.3 z score 34.1 z score 34.4 34

All TBI items have a situation-neutral format.

work behaviour, .63 for college behaviour and .58 for behaviour at home. Respectively, 71,64, 37, 40 and 34% of variance one the MBTI could be explained by scores on the TBI.

The correlation between scores on the TBI and those on the MBTI is formidable when theformer has either a situation-neutral or a social life behaviour orientation. The latter suggestsstrongly that the MBTI is a measure of social behaviour (as well as overall self-opinion).These correlations would be reasonable test–retest correlations for a single measure. Corre-lations are far lower (and the proportion of scores on the MBTI explained by those on the TBIgoes down by two-thirds or three-quarters) when TBI items are directed towards work, uni-versity or family life behaviour. Clearly there are major differences between subjects’ overallself-assessment and their opinions as to how they actually behave in these specific situations.

3. Accounting student scores on the TBI-4, 2002–2003

In these 2 years, accounting students were offered the TBI-4 together with the MBTI,following the procedure described earlier. Items on the three measures of the TBI wereoriented towards social life (A), work behaviour (B) and family life (C): results from measureC are not included here. The family life results seemed to very individual and showed nostatistically significant clear overall trends. Items related to work were concerned witheveryday behaviours and relationships with colleagues: relationships with superiors andsubordinates were not examined. Age and sex were also requested. Students were alsoasked the nature of their work in 2003. Results of demographic data are shown in Table 3.

Table 3Demographic data of subjects taking both the MBTI and the TBI-4

Year n Male:female (%) Mean age (S.E.)

2002 176 40:60 23.02003 180 44:56 22.8

92 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

Table 4Typological preferences of accounting students on the MBTI and the TBI-4

Preference 2002 2003

MBTI TBI-B (work) TBI-A (social life) MBTI TBI-B (work) TBI-A (social life)

INFP 1 (2) 0 (0) 4 (7) 2 (4) 0 (0) 4 (8)INFJ 1 2 1 1 1 1INTP 5 1 6 2 1 6INTJ 4 0 2 3 1 2ISFP 4 1 3 1 1 3ISFJ 6 3 4 8 2 5ISTP 3 2 6 8 2 6ISTJ 21 (37) 16 (28) 6 (11) 21 (36) 21 (37) 7 (12)ENFP 3 (5) 3 (5) 22 (39) 5 (9) 3 (5) 22 (40)ENFJ 3 2 2 3 2 2ENTP 5 10 14 8 11 12ENTJ 3 8 2 3 8 3ESFP 5 2 11 5 2 10ESFJ 10 5 5 9 5 5ESTP 8 9 5 8 5 5ESTJ 19 (33) 36 (64) 7 (12) 14 (24) 38 (68) 6 (11)

NFP 4 (7) 3 (5) 26 (46) 7 (13) 3 (5) 27 (48)STJ 40 (70) 52 (92) 13 (23) 35 (60) 58 (105) 13 (23)SJ 56 60 22 51 66 23SP 20 13 25 21 9 24NT 17 20 24 17 20 23NF 7 7 29 11 5 30E:I 56:44 75:25 68:32 55:45 73:27 66:34S:N 76:24 74:26 47:53 71:29 75:25 47:53T:F 69:31 82:18 47:53 67:33 85:15 47:53J:P 67:33 72:28 29:71 61:39 77:23 31:69

N 176 176 176 180 180 180

Results are shown as percentiles (numbers).

Results from all subjects on the MBTI and TBI-4, measures A and B, are shown inTable 4. Results are shown as typological preferences, as detailed above.

First looking at the results using the MBTI. The most striking feature of Table 4 isin the relative proportions of subjects having STJ and NFP preferences. Subjects havingpreferences for both sensing and judging (SJs) are over 50% overall. Subjects showingpreferences for sensing and thinking with judging (STJs) are 40% in 2002 and 35% in2003, 76% in 2002 and 71% in 2003 of subjects had a preference for sensing (as againstintuition) and 69% in 2002 and 67% in 2003 of subjects showed a preference for thinking (asagainst feeling). Sixty-seven percent in 2002 and 61% in 2002 of subjects had a preferencefor judging. The number of subjects choosing the opposite typological preferences (NFP, orintuition, feeling and perceiving) is much smaller at 7% in each year. Overall, the numbersof extraverts and introverts were almost the same. The percentage of subjects in our studypreferring an STJ profile is similar to the results of the earlier studies of Booth and Winzar(1993), Jacoby (1981), Shackleton (1980), Wheeler (2001) and others.

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 93

In terms of overall typologies, ISTJ was consistently the most common, followed byESTJ. The least common typological choices were INFJ, ENFJ and INFP. This is similar tothe findings of Jacoby (1981) and Wolk and Nickolai (1997). All of which suggests ratherstrongly that personality preferences in the accounting profession or the students that areentering it have not changed significantly in more than 20 years. If the profession is changingas mentioned in Section 1, then this is surely bad news for the profession, as the personality“makeup” is not changing. Particularly, perhaps, in view of the often-stated view that theprofession has a need for the ability for overview and a long-term creative approach that ismore characteristic of those with a preference for intuition.

This pattern of typological preference was even greater when the same subjects, atthe same time, took the TBI-4 as a measure of their work behaviour. Fifty-two and 58%,respectively – clearly more than one-half – preferred STJ (197 of 356 subjects overall), withabout two-thirds of these subjects overall preferring ESTJ. Only 3% (in each year) preferredNFP. Overall, nearly three-quarters of our subjects showed a preference for sensing in worksituations, while over 80% preferred thinking and about three-quarters preferred judging.All of which strongly suggests that the stereotypical image of the ‘typical’ accountant’spersonality is particularly true in a work situation. And that, therefore, intuition, the abilityto create new possibilities and human values are in very short supply there.

The results obtained when the same subjects responded to items of the TBI related tosocial life were dramatically different. The number preferring STJ drops by over three-quarters: from 52–58 to 13%. And the number preferring NFP rises by a factor of nearlynine, from 3 to 26–27%. So that, in their social life, more than twice as many of ouraccounting students prefer NFP, as against STJ. Twice as many Bill Clintons (accordingto rumour) as John Howards. This strongly suggests that the capacity for intuition, thecreation of possibilities and for values are present to a large degree, at least in potentia, inour students.

Another clear suggestion here is that personality traits, or at least behaviours that haveoften been associated with personality traits are not situation-constant. Rather, they varyvery greatly across at least the two situations we have investigated here.

To examine these suggestions in a little more detail, all 105 subjects in the 2003 samplehaving preferences for STJ at work were ‘followed up’ by examining their typologicalpreferences in social life. The results are shown in Table 5.

Table 5Social life-related typological preferences of 2003 subjects having STJ work-related preferences

Social life preferences n = 105

SFJ 12One preference change = 27STP 10

NTJ 5

NTP 19Two preference changes = 41SFP 17

NFJ 5

NFP 20 Three preference changes

STJ 17 No changes

94 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

Remarkably, only 17 of those subjects preferring STJ at work, also preferred this com-bination in social life. Sixty-one of 105 showed 2 or 3 preference changes. Note that the20 subjects who showed an NFP preference in social life, now outnumber the 17 who haveremained with an STJ orientation. A group of subjects who apparently had only two typolo-gies at work (ISTJ and ESTJ), in fact showed all 16 possible typologies in their social lives.The degree of apparent change is very great indeed. So great as to suggest only a verylimited degree of personality consistency across situations.

Two other observations should be made. First, that far more preferences for extraversionwere found using the TBI than when using the MBTI. That is, more subjects chose extraver-sion when thinking of either their social behaviours or their work-related behaviours, thanwhen giving the general self-assessment of the MBTI. The differences in percentages ofextraverts when using the social life and the work-related measures of the TBI were notgreat (and were not statistically significant) although, curiously, the work-related measureshowed more extraverts than the social life-related measure in both 2002 and 2003. Thesefindings could have a number of explanations and are the subject of ongoing research.

Second, it is apparent in Table 5 that – except for the proportions of extraverts andintroverts – the results obtained from the MBTI are generally intermediate between thoseobtained from the two measures of the TBI. This is true for almost all of the major combi-nations of preferences detailed in the lower half of the table, but also for many of the sixteenindividual typological preferences in the upper half. This would be expected of a measureintended to yield an overall self-assessment of personality, rather than a situation-specificone and it will be interesting to see if this finding is repeated when results using the MBTIare compared with results using the TBI in a wider variety of situations.

4. Conclusion

Using the MBTI and the work-related TBI-4, the stereotypes about the personalities ofaccountants are confirmed. Personality type tests like the MBTI based on Jung’s psycho-logical type theory have been administered to many professionals including accountantsas a way of determining behaviour across situations, especially at work. From these testsaccountants have shown a strong preference towards a particular type, namely STJ. So inanswer to the question are accountants different at work than socially, the answer is yes.Using the TBI the STJ preference at work is not as strong as the MBTI would lead us tobelieve and in fact even less socially. The social life-related TBI-4 shows that accountantsprobably have the potential for a wide range of personality-related behaviours, and that, ifsuch a range is required in the profession, it can be better achieved by an education thatencourages the use of such abilities than by recruiting different students.

An understanding of personality type in various situations, and perhaps potential todevelop aspects of persona that otherwise exist in social situations, but not necessarily atwork, should assist accountants bring forth those characteristics that are required by theprofession as it seeks to change. For instance, those intuitive characteristics would assistaccountants with an overview and long-term creative approach as mentioned by the AICPA(2000) as needed by the accounting profession. Future research could explore accountantswho are for instance ENFJ socially but ISTJ at work. Can these attributes be developed for

D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96 95

work situations? Skills at, or preferences for, different types of task, for example (brain-storming, using overview, etc.). Do the apparent situation-related differences observed hereactually affect real-life behaviours?

Our results suggest that giving measures of ‘general personality’ to job or universitycourse applicants is a very unsure guide of both personality and capacity for versatility.

Finally, and perhaps most importantly, our results suggest strongly that personality, orat least behaviours often associated with personality, vary considerably across situations.

References

AICPA. CPA visioning project; 2000.American Association of Certified Public Accountants (AICPA). AICPA vision project. Available at:

http://www.aicpa.org/vision/index.htm; 1999.Amernic JH, Beechy TH. Accounting students’ performance and cognitive complexity: some empirical evidence.

The Accounting Review 1984;LIX(2):300–13.Bem DJ, Allen A. On predicting some of the people some of the time: the search for cross-situational consistencies

in behaviour. Psychological Review 1974;81:506–20.Booth P, Winzar H. Personality biases of accounting students: some implications for learning style preferences.

Accounting and Finance 1993:109–20.Boyce G. Critical accounting education: teaching and learning outside the circle. Critical Perspectives on Account-

ing 2004;15:565–86.Carver C, Scheier M. Perspectives on personality. New York: Allyn & Bacon; 1996.Craig R. Accountants unable to shake a dodgy stereotype. Canberra Times 2002:10.Costa PT, McRae RR. Trait theories of personality. In: Barone DF, Hersen M, van Hasselt J, editors. Advanced

psychology. New York: Plenum; 1998.Costa PT, McRae RR. Set like plaster? Evidence for the stability of adult personality”. In: Heatherton TF, Wein-

berger JL, editors. Can personality change? Washington: Americam Psychological Association; 1997.Costa PT, McRae RR. Personality in adulthood. A 6-year longitudinal study of self-reports and spouse ratings on

the NEO personality inventory. Journal of Personality and Social Psychology 1988;54:853–63.Costa PT, McRae RR. NEO-PI-R: professional manual. Odessa, FL: Psychological Assessment Resources; 1985.Descouzis D. Psychological types of tax preparers. Journal of Psychological Type 1989;17:36–8.Diener E, Larsen RJ. Temporal stability and cross-situational consistency of affective, behavioural and cognitive

responses. Journal of Personality and Social Psychology 1984;47:871–83.Funder DC, Colvin CR. Explorations in behavioural consistency: properties of persons, situations and behaviours.

Journal of Personality and Social Psychology 1991;60:773–94.Gardner WL, Martinko MJ. Using the Myers-Briggs type indicator to study managers: a literature review and

research agenda. Journal of Management 1996;22:45–83.Girelli SA, Stake JE. Bipolarity in Jungian type theory and the Myers-Briggs type indicator. Journal of Personality

Assessment 1993;60:290–301.Gray H, Wheelwright JH, Wheelwright JB. Jungian type survey. San Francisco: Society of Jungian Analysts of

Northern California; 1964.Harshorne H, May M. Studies in Deceit. New York: Macmillan; 1928.Harvey R. Reliability and validity. In: Hammer AL, editor. MBTI applications: a decade of research on the

Myers-Briggs type indicator. Palo Alto, CA: Consulting Psychologists Press; 1996.Jacoby PF. Psychological types and career success in the accounting profession. Research in Psychological Type

1981;16(1):125–50.Jung CG. Interviewed by John Freeman in face to face. London: BBC Television; 1960.Kreiser L, McKeon Jr JM, Post A. A personality profile of CPA’s in publis practice. The Ohio CPA Journal

1990:29–34.Kovar SE, Ott RL, Fisher DG. Personality preferences of accounting students: A longitudinal case study. Journal

of Accounting Education 2003;21:75–94.

96 D. Haynes et al. / Critical Perspectives on Accounting 19 (2008) 81–96

Laribee SF. The psychological types of college accounting students. Journal of Psychological Type 1994;28:37–42.McCaulley MH. The Myers-Briggs type indicator: a measure for individuals and groups. Measurement and Eval-

uation in Counselling and Development 1990;22:181–95.McRae RR, Costa PT, Lima MP, Simoes A, Ostendorf F, Angleitner A, et al. Age differences in personality across

the adult lifespan: parallels in five cultures. Developmental Psychology 1999;35:466–77.McRae RR, Costa PT. Reinterpretation of the Myers-Briggs type indicator from the perspective of the five-factor

model of personality. Journal of Personality 1989;57:17–40.McRae RF, Costa PT. Personality in adulthood. New York: Guilford; 1990.Mohammed EKA, Lashire SH. Accounting knowledge and skills and the challenges of a global business environ-

ment. Managerial Finance 2003;29(7):3–16.Mischel W. Personality and assessment. New York: Wiley; 1968.Mischel W, Peake PK. Beyond deja vu in the search for cross-situational consistency. Psychological Review

1982;90:394–402.Monson TC, Hesley JW, Chernick L. Specifying when personality traits can and cannot predict behaviour: an

alternative to abandoning the attempt to predict single-act criteria. Journal of Personality and Social Psychology1982;43:385–99.

Myers IB. Introduction to type. 5th ed. Palo Alto, CA: Consulting Psychologists Press; 1993.Myers IB, McCaulley MH. Manual: a guide to the development and use of the Myers-Briggs type indicator. Palo

Alto, CA: Consulting Psychologists Press; 1985.Newcomb TM. Consistency of certain extravert–introvert behaviour patterns in 51 problem boys. New York:

Columbia University; 1929.Nunnally JM, Bernstein IH. Psychometric theory. 3rd ed. New York, NY: McGraw-Hill Book Company; 1994.Oswick C, Barber P. Personality type and performance in an introductory level accounting course: a research note.

Accounting Education 1998;7(3):249–54.Otte P. Do CPA’s have a unique personality: are certain personality types found more frequently in our profession?

The Michigan CPA Spring 1984:29–36.Piaget J. The moral judgement of the child. New York: The Free Press; 1965 [original work published in 1932].Pittinger DJ. The utility of the Myers-Briggs type indicator. Review of Educational Research 1993;63:467–88.Price RH, Bouffard DL. Behavioural appropriateness and situational constraint as dimensions of social behaviour.

Journal of Personality and Social Psychology 1974;30:579–86.Scarbrough DP. Psychological types and job satisfaction of accountants. Journal of Psychological Type

1993;25:3–10.Schloemer PG, Schloemer MS. The personality types and preferences of CPA firm professionals: an analysis of

changes in the profession. Accounting Horizons 1997;11(4):24–39.Shackleton V. The accountant stereotype: myth or reality? Accountancy 1980:122–3.Singer J, Loomis M. Interpretive guide for the Singer–Loomis inventory. Palo Alto, CA: Consulting Psychologists

Press; 1984.Tett RP, Gutterman HA. Situation trait relevance, trait expression and cross-situational consistency. Testing a

principle of trait activation. Journal of Research in Personality 2000;34:397–423.Wheeler P, Hunton JE, Bryant SM. Accounting information systems research opportunities using personality type

theory and the Myers-Briggs type indicator. Journal of Accounting Information Systems 2004;18(1):1–19.Wheeler P. The Myers-Briggs type indicator and applications to accounting education and research. Issues in

Accounting Education 2001;16(1):125–50.Wiggins JS. Review of the Myers-Briggs type indicator. OK Buros: Tenth Meta Measurement Yearbook; 1989. p.

537–38.Wolk C, Nickolai LA. Personality types of accounting students and faculty: comparisons and implications. Journal

of Accounting Education 1997;25(1):1–17.