Embed Size (px)

Citation preview

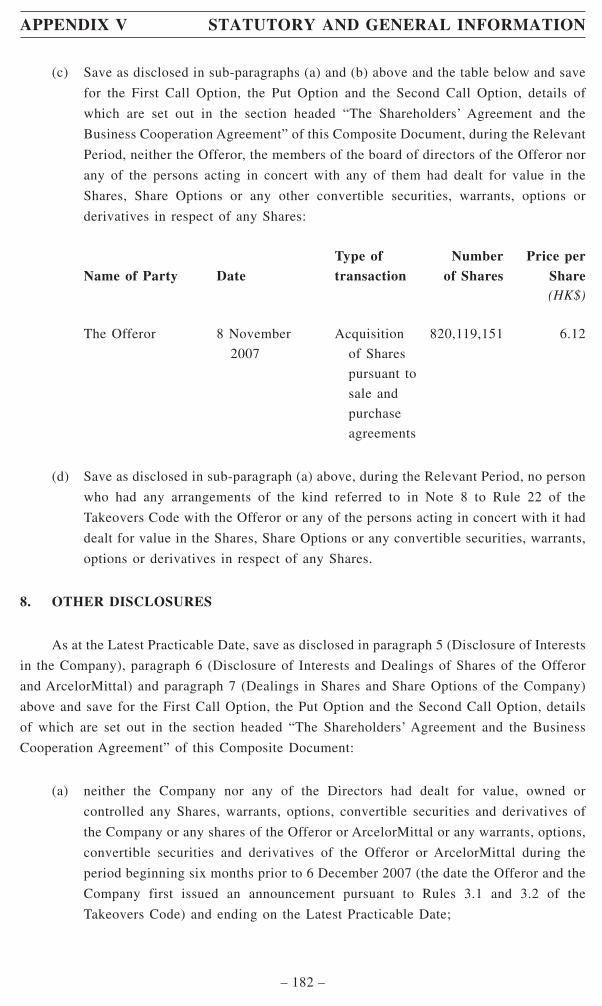

If you are in any doubt as to any aspect of this Composite Document or the Offer contained herein, you should consult a licensed securitiesdealer, or other registered institution in securities, a bank manager, solicitor, professional accountant or other professional adviser.

If you have sold or transferred all your shares in China Oriental Group Company Limited, you should at once hand this Composite Documentand the accompanying form of acceptance and transfer for the Disinterested Shares to the purchaser(s) or transferee(s) or to the bank, thelicensed securities dealer or registered institution in securities or other agent through whom the sale or transfer was effected for transmissionto the purchaser(s) or transferee(s).

The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this Composite Document, makes no representationas to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance uponthe whole or any part of the contents of this Composite Document.

(incorporated in Bermuda with limited liability)

(Stock Code 581)

COMPOSITE OFFER AND RESPONSE DOCUMENTRELATING TO

AN UNCONDITIONAL MANDATORY CASH OFFERBY ING BANK N.V. ON BEHALF OF

MITTAL STEEL HOLDINGS AG(Incorporated in Switzerland with limited liability)

TO ACQUIRE ALL THE OUTSTANDING SHARES IN THE ISSUED SHARE CAPITAL ANDCANCEL ALL SHARE OPTIONS OF

CHINA ORIENTAL GROUP COMPANY LIMITED(OTHER THAN THOSE ALREADY OWNED BY MITTAL STEEL HOLDINGS AG AND

PARTIES ACTING IN CONCERT WITH IT)

Financial Adviser toMittal Steel Holdings AG

ING Bank N.V.

Financial Adviser toChina Oriental Group Company Limited

UBS Investment Bank

Independent Financial Adviserto the Independent Board Committee, Independent Shareholders and Optionholders

of China Oriental Group Company Limited

A letter from ING containing, among other things, details of the terms of the Offer is set out on pages 9 to 27 of this Composite Document.

A letter from the Board is set out on pages 28 to 34 of this Composite Document.

A letter from the Independent Board Committee to the Independent Shareholders and Optionholders is set out on pages 35 to 37 of thisComposite Document. A letter of advice from Evolution Watterson containing its opinion and advice to the Independent Board Committee,the Independent Shareholders and Optionholders is set out on pages 38 to 61 of this Composite Document.

The procedure for acceptance and settlement of the Offer is set out in Appendix I to this Composite Document and in the accompanying formof acceptance and transfer for the Disinterested Shares and the form of acceptance and cancellation for the Share Options. Acceptances of theShare Offer in respect of the Disinterested Shares must be received by Tricor Investor Services Ltd. at 26/F, Tesbury Centre, 28 Queen’s RoadEast, Wanchai, Hong Kong by 4:00 p.m. on 4 February 2008, or such later time as the Offeror may determine and announce in accordancewith the Takeovers Code. Acceptances of the Option Offer in respect of the Share Options must be received by the Company at Suites 901-2& 10, 9/F Great Eagle Centre, 23 Harbour Road, Wanchai, Hong Kong by 4:00 p.m. on 4 February 2008 or such later time as the Offeror maydetermine and announce in accordance with the Takeovers Code.

* For identification purpose only

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

14 January 2008

Page

Expected Timetable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Letter from ING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Letter from the Board . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Letter from the Independent Board Committee . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Letter from Evolution Watterson . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

The Shareholders’ Agreement and the Business Cooperation Agreement . . . . . . . 62

Appendix I – Further Terms of the Offer . . . . . . . . . . . . . . . . . . . . . . . . 68

Appendix II – Financial Information regarding the Group . . . . . . . . . . . . 77

Appendix III – Valuation of the Put Option . . . . . . . . . . . . . . . . . . . . . . . . 143

Appendix IV – Property Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

Appendix V – Statutory and General Information . . . . . . . . . . . . . . . . . . 168

CONTENTS

– i –

Opening date of the Offer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Monday, 14 January 2008

Latest time and date for acceptance of the Offer (Note 1) . . . . . . . . .4:00 p.m. on Monday,

4 February 2008

Closing date of the Offer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Monday, 4 February 2008

Announcement in respect of the closing of the Offer and

acceptances under the Offer through the Stock Exchange’s

website and the Company’s website . . . . . . . . . . . . . . . . . . . . . . . .7:00 p.m. on Monday,

4 February 2008

Latest date for posting of remittances for the amounts

due under the Offer in respect of valid acceptances

– First Payment (Notes 2, 3) . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, 14 February 2008

– Second Payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .(Notes 2, 4)

Notes:

1. The Offer, which is unconditional in all respects, will close on Monday, 4 February 2008, unless the Offerorrevises or extends the Offer in accordance with the Takeovers Code. If the Offeror decides to extend the Offer,an announcement will be made stating either the next closing date of the Offer or that the Offer will remainopen until further notice, in which case at least 14 days’ notice in writing will be given before the Offer isclosed to those Shareholders and Optionholders who are capable of accepting, but who have not accepted, theOffer.

2. As set out in the “Letter from ING – Consideration of the Offer – The Share Offer”, accepting Shareholderscan choose any one of the following three alternatives of the consideration in respect of the Share Offer. Theconsideration for each Share held, which consists of two elements, is as follows:

Alternative 1 Alternative 2 Alternative 3

First Payment HK$6.12 HK$6.12 HK$6.12Second Payment HK$0.235 HK$0.471 HK$0.706Total HK$6.355 HK$6.591 HK$6.826

As set out in the “Letter from ING – Consideration of the Offer – The Option Offer”, accepting Optionholderscan choose any one of the following three alternatives of the consideration in respect of the Option Offer. Theconsideration for each Share Option held (with an exercise price of HK$5.24), which comprises two elements,is as follows:

Alternative 1 Alternative 2 Alternative 3

First Payment HK$0.88 HK$0.88 HK$0.88Second Payment HK$0.235 HK$0.471 HK$0.706Total HK$1.115 HK$1.351 HK$1.586

3. Remittances in respect of the First Payment payable for the Disinterested Shares and the Share Optionstendered under the Offer will be posted to the relevant Shareholders and Optionholders as soon as practicable,but in any event within ten days after the receipt by the Registrar or the Company (as the case may be) of thevalid requisite documents from the accepting Shareholders or Optionholders (as the case may be).

EXPECTED TIMETABLE

– ii –

4. Under Alternative 1, the Second Payment will be made at the same time as the First Payment to those acceptingShareholders and Optionholders who have validly chosen this alternative. Under Alternative 2, the SecondPayment will be made within ten days of the Shareholders’ Agreement becoming unconditional to thoseaccepting Shareholders and Optionholders who have validly chosen this alternative. If the Shareholders’Agreement does not become unconditional, the Second Payment will not be made to those acceptingShareholders and Optionholders who have validly chosen this alternative. Under Alternative 3, the SecondPayment will be made within ten days of the completion of the sale and purchase of the First Call OptionShares to those accepting Shareholders and Optionholders who have validly chosen this alternative. If (a) theShareholder’s Agreement does not become unconditional or (b) the sale and purchase of the First CallOption Shares is not completed, the Second Payment will not be made to those accepting Shareholdersand Optionholders who have validly chosen this alternative.

5. Acceptance of the Offer shall be irrevocable and not capable of being withdrawn, except in the circumstancesset out in Rule 19.2 of the Takeovers Code (which is to the effect that if the Offeror is unable to comply withany of the requirements for making announcements under Rule 19 of the Takeovers Code relating to the Offer,the Executive may require that acceptors be granted a right of withdrawal, on terms acceptable to theExecutive). A further announcement will be made by the Offeror if any such right of withdrawal (as describedin this note) is available to the Shareholders and Optionholders who have accepted the Offer.

All time references contained in this Composite Document refer to Hong Kong time.

EXPECTED TIMETABLE

– iii –

In this Composite Document, the following expressions have the meanings set out below

unless the context requires otherwise.

“acting in concert” shall have the meaning set out in the Takeovers Code

“Alternative 1”, “Alternative 2”,

“Alternative 3”

the respective alternative among the three consideration

alternatives available under the Share Offer and the

Option Offer, details of which are set out in the

paragraphs headed “Letter from ING – Consideration of

the Offer – The Share Offer” and “Letter from ING –

Consideration of the Offer – The Option Offer”

“Announcement” the announcement dated 13 December 2007, jointly made

by the Offeror and China Oriental in connection with the

entering into of the Shareholders’ Agreement and the

making of the Offer

“Anti-trust Condition” ArcelorMittal having filed the anti-trust application with

the relevant departments within the Ministry of

Commerce and the State Administration for Industry and

Commerce of the PRC in charge of anti-trust review in

respect of each of the First Call Option, the Put Option

and the Second Call Option, and that no written objection

prohibiting the aforesaid has been received by

ArcelorMittal from the aforesaid departments within the

applicable anti-trust review period under the relevant

PRC anti-trust laws and guidelines as set out in the

sub-section headed “The Shareholders’ Agreement and

the Business Cooperation Agreement – PRC Approvals”

“ArcelorMittal” ArcelorMittal, a company incorporated in Luxembourg

with limited liability

“Board” the board of Directors

“Business Cooperation

Agreement”

the business cooperation agreement dated 9 November

2007 between ArcelorMittal and the Company which

governs the cooperation between the parties in respect of

certain aspects of operation of the Company, the key

terms of which will take effect upon the Shareholders’

Agreement becoming unconditional

“CCASS” the Central Clearing and Settlement System established

and operated by HKSCC

DEFINITIONS

– 1 –

“China Oriental” or the

“Company”

China Oriental Group Company Limited, a company

incorporated in Bermuda with limited liability, the shares

of which are listed on the Main Board of the Stock

Exchange with stock code 581

“Chingford” Chingford Holdings Limited, a company incorporated

under the laws of the British Virgin Islands, which holds

61,653,725 Shares, representing approximately 2.10% of

the issued share capital of the Company as at the Latest

Practicable Date. Chingford is wholly-owned by Mr. Han

“Companies Act” the Companies Act 1981 of Bermuda as in force from

time to time

“Composite Document” this composite offer and response document dated 14

January 2008

“Concert Parties” persons acting in concert with the Offeror (within the

meaning of the Takeovers Code)

“Controlling Shareholders” Mr. Han, Wellbeing and Chingford, who hold

1,320,302,849 Shares in aggregate, representing

approximately 45.07% of the issued share capital of the

Company as at the Latest Practicable Date

“Director(s)” director(s) of the Company

“Disinterested Shares” all the issued Shares and Shares that may be issued under

the Share Option Scheme other than those which are

owned by the Offeror or its Concert Parties

“EBITDA” total audited consolidated earnings before (a) interest

income and expense, (b) tax expense, (c) depreciation,

(d) amortisation, (e) extraordinary items, (f) significant

items of a non-cash nature (such as employee stock

option expenses) and (g) unrealised foreign exchange

gains or losses

“EUR” Euro, the lawful currency among participating countries

of the European Union

DEFINITIONS

– 2 –

“Evolution Watterson” Evolution Watterson Securities Limited, the independentfinancial adviser to the Independent Board Committee,the Independent Shareholders and Optionholders inrespect of the Offer and a licensed corporation under theSFO to carry on Type 1 (dealing in securities), Type 4(advising on securities) and Type 6 (advising oncorporate finance) regulated activities

“Executive” the Executive Director of the Corporate Finance Divisionof the SFC or any delegate of the Executive Director

“First Call Option” the option granted by the Controlling Shareholders toArcelorMittal to purchase the First Call Option Shares

“First Call Option Shares” such number of Shares which will result in ArcelorMittalholding in aggregate, directly or indirectly, 50.1% of thetotal number of Shares then in issue (assuming theexercise in full of all the then outstanding share optionsgranted under schemes for the issue of new Shares orother new securities of the Company)

“First Payment” first payment under Alternative 1, Alternative 2 andAlternative 3

“Form of Acceptance” the accompanying WHITE form of acceptance andtransfer in respect of the Disinterested Shares and theaccompanying YELLOW form of acceptance andcancellation for the Share Options

“GCAL” Greater China Appraisal Limited, an independent assetappraisal firm of professional valuers with registeredoffice at Room 2703, Shui On Centre, 6-8 Harbour Road,Wanchai, Hong Kong

“Group” the Company and its subsidiaries

“Hebei Jinxi” Hebei Jinxi Iron and Steel Company Limited( ), a joint stock limitedcompany incorporated in the PRC on 24 December 1999and the principal operating subsidiary of the Company.As at the Latest Practicable Date, the Company heldapproximately 97.6% equity interest in Hebei Jinxi andthe remaining approximately 2.4% equity interest washeld as to 2.2% by Tangshan City Jinxi Iron and SteelGroup Co., Ltd. ( ) and asto 0.2% by Tangshan City Qianxi Valves Factory( )

DEFINITIONS

– 3 –

“HK$” or “Hong Kong dollar” the lawful currency of Hong Kong

“HKSCC” Hong Kong Securities Clearing Company Limited

“Hong Kong” the Hong Kong Special Administrative Region of the

PRC

“Independent Board Committee” the independent board committee of China Oriental,

comprising all the non-executive Directors, being

Messrs. Yu Tung Ho, Gao Qingju and Wong Man Chung,

Francis, established to advise the Independent

Shareholders and Optionholders in respect of the Offer

“Independent Shareholders” the shareholders of the Company other than the Offeror

and its Concert Parties

“ING” ING Bank N.V., a registered institution under the SFO to

conduct Type 1 (dealing in securities), Type 4 (advising

on securities) and Type 6 (advising on corporate finance)

regulated activities

“Last Trading Day” 6 November 2007, the last full trading day for Shares

prior to the suspension of the Shares pending the release

of the Announcement

“Latest Practicable Date” 11 January 2008, being the latest practicable date prior to

the printing of this Composite Document for ascertaining

certain information referred to in this Composite

Document

“Listing Rules” the Rules Governing the Listing of Securities on The

Stock Exchange of Hong Kong Limited

“Mr. Han” Mr. Han Jingyuan, the Chairman and Chief Executive

Officer of the Company and the legal and beneficial

holder of 2,800,000 Shares, representing approximately

0.10% of the issued share capital of the Company as at

the Latest Practicable Date

“Offer” the Share Offer and the Option Offer

DEFINITIONS

– 4 –

“Offer Period” the period from 6 December 2007, being the date of the

joint announcement issued by the Offeror and the

Company, to the date when the Offer closes for

acceptances

“Offeror” Mittal Steel Holdings AG, a company incorporated under

the laws of Switzerland, which is a holder of 820,119,151

Shares, representing approximately 28.00% of the issued

share capital of the Company as at the Latest Practicable

Date

“Option Offer” the unconditional mandatory cash offer made by ING, on

behalf of the Offeror, to cancel all Share Options which

are then outstanding

“Option Offer Price” the price per Share Option payable in cash by the Offeror

on the terms of the Option Offer, details of which are set

out in the paragraph headed “Letter from ING –

Consideration of the Offer – The Option Offer” in this

Composite Document

“Optionholders” holders of the Share Options

“PRC” the People’s Republic of China, but excluding, for the

purpose of this Composite Document, Hong Kong,

Macau and Taiwan

“Put Option” the option granted by ArcelorMittal to the Controlling

Shareholders to sell the Put Option Shares which is

exercisable only after the completion of the sale and

purchase of the First Call Option Shares takes place

“Put Option Shares” the difference between: (1) the 1,320,302,849 Shares in

aggregate held by the Controlling Shareholders (as

adjusted to include any Shares representing or deriving

from those Shares as a result of an increase in,

reorganisation or reconstruction of capital and any Shares

which are issued to the Controlling Shareholders,

credited as fully-paid, in their capacity as holders of such

Shares by way of capitalisation of profits or reserves);

and (2) the total number of Shares acquired by

ArcelorMittal pursuant to the First Call Option

DEFINITIONS

– 5 –

“Registrar” Tricor Investor Services Ltd. at 26/F, Tesbury Centre, 28

Queen’s Road East, Wanchai, Hong Kong, being the

share registrar of China Oriental in Hong Kong for

receiving and processing acceptances of the Offer in

respect of the Disinterested Shares

“Relevant Period” the period commencing on the date falling six months

prior to the commencement date of the Offer Period and

ending on the Latest Practicable Date

“RMB” Renminbi, the lawful currency of the PRC

“Second Call Option” the option granted by the Controlling Shareholders to

ArcelorMittal to purchase the Second Call Option Shares

“Second Call Option Shares” the difference between: (1) the 1,320,302,849 Shares in

aggregate held by the Controlling Shareholders (as

adjusted to include any Shares representing or deriving

from those Shares as a result of an increase in,

reorganisation or reconstruction of capital and any Shares

which are issued to the Controlling Shareholders,

credited as fully-paid, in their capacity as holders of such

Shares by way of capitalisation of profits or reserves);

and (2) the total number of Shares acquired by

ArcelorMittal pursuant to the First Call Option and the

Put Option

“Second Payment” second payment under Alternative 1, and if conditions are

fulfilled, under Alternative 2 and Alternative 3. Further

details are set out in the paragraphs headed “Letter from

ING – Consideration of the Offer – The Share Offer” and

“Letter from ING – Consideration of the Offer – The

Option Offer” in this Composite Document

“SFC” the Securities and Futures Commission of Hong Kong

“SFO” the Securities and Futures Ordinance (Chapter 571 of the

Laws of Hong Kong)

“Share Offer” the unconditional mandatory cash offer made by ING, on

behalf of the Offeror, to acquire all the issued Shares,

other than those Shares which are owned by the Offeror

and its Concert Parties

DEFINITIONS

– 6 –

“Share Offer Price” the price per Share payable in cash by the Offeror on the

terms of the Share Offer, details of which are set out in

the paragraph headed “Letter from ING – Consideration

of the Offer – The Share Offer” in this Composite

Document

“Share Option Scheme” the share option scheme adopted by the Company on 23

June 2006 pursuant to a shareholders’ resolution passed

on 17 May 2006

“Share Options” the outstanding options granted pursuant to the Share

Option Scheme which were not yet exercised as at the

Latest Practicable Date

“Shareholders” holders of the Shares

“Shareholders’ Agreement” the shareholders’ agreement dated 9 November 2007

between the Controlling Shareholders and ArcelorMittal,

as amended by a supplemental agreement dated 12

December 2007 entered into between the Controlling

Shareholders and ArcelorMittal

“Shares” the existing issued shares of HK$0.10 each in the

Company

“Stock Exchange” The Stock Exchange of Hong Kong Limited

“Takeovers Code” the Hong Kong Code on Takeovers and Mergers as in

force from time to time

“trading day” a day on which the Stock Exchange is open for the

business of dealings in securities

“UBS” UBS AG, acting through its business group UBS

Investment Bank, a registered institution under the SFO

to conduct Type 1 (dealing in securities), Type 4

(advising on securities), Type 6 (advising on corporate

finance), Type 7 (providing automated trading services)

and Type 9 (asset management) regulated activities

“US$”, “US dollar” or “United

States dollar”

the lawful currency of the United States of America

DEFINITIONS

– 7 –

“Valin” Hunan Valin Steel Tube and Wire Company Ltd

( )

“Wellbeing” Wellbeing Holdings Limited, a company incorporated

under the laws of the British Virgin Islands with limited

liability with Registered Number 550903, which holds

1,255,849,124 Shares. Wellbeing is beneficially owned as

to approximately 60.69% by Mr. Han, who also holds

16.09% of the issued share capital of Wellbeing on trust

for the benefit of approximately 1,800 employees of

Hebei Jinxi

“%” per cent.

DEFINITIONS

– 8 –

39/F., One International Finance Centre1 Harbour View Street

Central, Hong Kong

14 January 2008

To the Shareholders and Optionholders

Dear Sir or Madam,

UNCONDITIONAL MANDATORY CASH OFFERBY ING BANK N.V. ON BEHALF OF

MITTAL STEEL HOLDINGS AGTO ACQUIRE ALL THE OUTSTANDING SHARES IN

THE ISSUED SHARE CAPITAL AND CANCEL ALL SHARE OPTIONS OFCHINA ORIENTAL GROUP COMPANY LIMITED(OTHER THAN THOSE ALREADY OWNED BY

MITTAL STEEL HOLDINGS AGAND PARTIES ACTING IN CONCERT WITH IT)

INTRODUCTION

On 13 December 2007, the Offeror and the Company jointly announced that on 9

November 2007, the Controlling Shareholders and ArcelorMittal entered into the Shareholders’

Agreement in relation to their shareholdings in and the management of the Group. Pursuant to

the Shareholders’ Agreement, the Controlling Shareholders agreed to grant to ArcelorMittal

certain rights to acquire Shares which the Controlling Shareholders currently own within a

specified period of time and ArcelorMittal agreed to grant to the Controlling Shareholders

certain rights to sell to ArcelorMittal such Shares. The key terms of the Shareholders’

Agreement are conditional upon satisfaction of the Anti-trust Condition.

As at the Latest Practicable Date, the Offeror held 820,119,151 Shares, representing

approximately 28.00% of the issued Shares while the Controlling Shareholders held

1,320,302,849 Shares, representing approximately 45.07% of the issued Shares. Accordingly,

the Offeror and the Controlling Shareholders together were interested in an aggregate of

2,140,422,000 Shares, representing approximately 73.07% of the issued share capital of the

Company as at the Latest Practicable Date.

Pursuant to a decision of the Takeovers and Mergers Panel and with reference to the joint

announcements issued by the Offeror and the Company on 6 December 2007 and 13 December

2007, the Takeovers and Mergers Panel ruled that ArcelorMittal and the Controlling

Shareholders were parties acting in concert at the time when the acquisition of approximately

28.00% of the equity interest in the Company by the Offeror was completed and accordingly,

an unconditional mandatory general offer has been triggered under Rule 26.1 of the Takeovers

Code.

LETTER FROM ING

– 9 –

As stated in the Announcement, the Offeror has a firm intention to make and extend and

shall make and extend the Offer, which shall be on the basis set out in Rule 26 of the Takeovers

Code, to acquire all the Disinterested Shares and will also make and extend to Optionholders

a comparable offer for cancellation of all Share Options which are outstanding.

This letter sets out the detailed terms of the Offer, together with the information on the

Offeror and the intentions of the Offeror regarding the Company. Further details of the Offer

are also set out in Appendix I to this Composite Document and in the accompanying form of

acceptance and transfer for the Disinterested Shares and the form of acceptance and

cancellation for the Share Options. Your attention is also drawn to the letter from the Board,

the letter from the Independent Board Committee and the letter from Evolution Watterson

contained in this Composite Document.

CONSIDERATION OF THE OFFER

The Put Option

As described in the section headed “The Shareholders’ Agreement and the Business

Cooperation Agreement” of this Composite Document, ArcelorMittal has granted to the

Controlling Shareholders an option to sell to ArcelorMittal all or part of the Put Option Shares

which is exercisable only once by the Controlling Shareholders within a 36-month period from

the completion of the sale and purchase of the First Call Option Shares. The Put Option is only

activated after the Shareholders’ Agreement becomes unconditional and the completion of the

sale and purchase of the First Call Option Shares (collectively the “Triggering Events”).

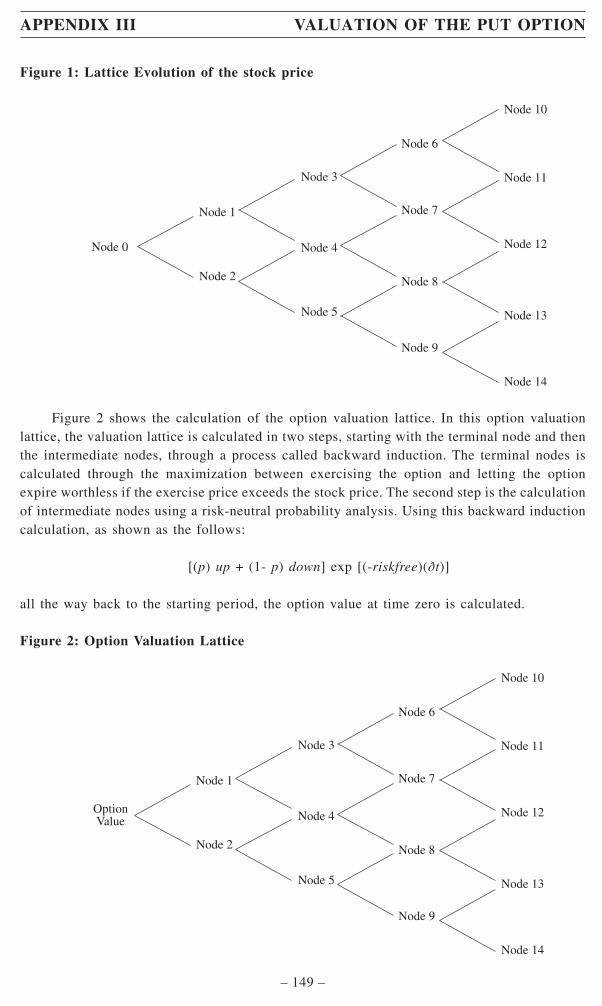

The Takeovers and Mergers Panel has determined that the Put Option constitutes a special

deal under Rule 25 of the Takeovers Code. Accordingly, the Offeror has arranged for the Put

Option to be valued by GCAL, using the Binomial option pricing model. The fair values of the

Put Option have been determined by GCAL and reported on by ING in accordance with Rule

11.1 (b) of the Takeovers Code. Full details of the Put Option valuation including the valuation

report prepared by GCAL and ING’s report on the fair values of the Put Option are set out in

Appendix III to this Composite Document.

The assumptions used by GCAL in the Binomial option pricing model before applying

any subjective probabilities of the Triggering Events include:

Date of valuation (the “Valuation

Date”)

6 December 2007

Date of the Shareholders’ Agreement

becoming unconditional (the

“Completion Date”)

3 months from the Valuation Date

LETTER FROM ING

– 10 –

Exercise period of the First Call

Option

12-month period commencing after 18 months

from the Completion Date

Date of the exercise and completion

of the First Call Option (the

“Activation Date”)

Mid-point of the exercise period of the First

Call Option (or 27 months from the Valuation

Date)

Exercise period of the Put Option At any time during the 36-month period from

the Activation Date

Share price volatility over the past 3

years

37.49%

Exercise price per Put Option Share The exercise price has been derived with

reference to the projected financial

performance and condition of the Group

contained in third party research report

Average yield of the 3-year HK$

Exchange Fund Notes over the past

3 years

3.736%

Average dividend yield over the past 3

years

2.226%

Last transacted Share price HK$6.12

Based on the above, the value of the Put Option before applying any subjective

probabilities of the Triggering Events, as computed by GCAL, is HK$0.706 per Share.

LETTER FROM ING

– 11 –

As the Put Option is only activated by the Triggering Events, various fair values of the

Put Option are derived by assigning different subjective probabilities to the Triggering Events,

as computed by GCAL, as follows:

Probabilityof the

Shareholders’Agreement

becomingunconditional

Probabilityof the

completionof the sale

andpurchase of

the FirstCall Option

Shares

Fair valueof the Put

Option perShare

Upon the completion of the Offer 50%

(note 1)

66.67%

(note 2)

HK$0.235

Upon the Shareholders’ Agreement

becoming unconditional

100% 66.67%

(note 2)

HK$0.471

Upon the Shareholders’ Agreement

becoming unconditional and the

completion of the sale and purchase

of the First Call Option Shares

100% 100% HK$0.706

Notes:

1. A subjective probability of 50% is assigned to the Shareholders’ Agreement becoming unconditional toreflect the potential uncertainties of the anti-trust clearance process such as the application of theevaluation criteria and other factors which may be considered by the regulatory authorities.

2. A subjective probability of 66.67% is assigned to the completion of the sale and purchase of the FirstCall Option Shares to reflect the risks of ArcelorMittal not exercising the First Call Option as a resultof adverse developments in the steel sector, the global economy, the capital markets and the Group.

The Share Offer

Accepting Shareholders can choose any one of the following three alternatives of the

consideration in respect of the Share Offer. The consideration for each Share held, which

consists of two elements, is as follows:

Alternative 1 Alternative 2 Alternative 3

First Payment HK$6.12 HK$6.12 HK$6.12Second Payment HK$0.235 HK$0.471 HK$0.706Total HK$6.355 HK$6.591 HK$6.826

LETTER FROM ING

– 12 –

Payment for the Share Offer

First Payment

In all three alternatives, the First Payment will be made within ten days after the receiptby the Offeror of the duly completed valid acceptances from the accepting Shareholders.

Second Payment

Under Alternative 1, the Second Payment will be made at the same time as the FirstPayment to those accepting Shareholders who have validly chosen this alternative.

Under Alternative 2, the Second Payment will be made within ten days of theShareholders’ Agreement becoming unconditional to those accepting Shareholders who havevalidly chosen this alternative. If the Shareholders’ Agreement does not becomeunconditional, the Second Payment will not be made to those accepting Shareholders whohave validly chosen this alternative.

Under Alternative 3, the Second Payment will be made within ten days of the completionof the sale and purchase of the First Call Option Shares to those accepting Shareholders whohave validly chosen this alternative. If (a) the Shareholders’ Agreement does not becomeunconditional or (b) the sale and purchase of the First Call Option Shares is notcompleted, the Second Payment will not be made to those accepting Shareholders whohave validly chosen this alternative.

In view of the fact that the Share Offer Price includes the fair value of the Put Option,the Executive considers that General Principle 1 of The Codes on Takeovers and Mergers andShare Repurchases, being all shareholders are to be treated even-handedly, is satisfied, andaccordingly, has confirmed that the Put Option will no longer constitute a special deal underRule 25 of the Takeovers Code.

Comparisons of Value

The Share Offer Price of HK$6.355 represents:

(a) a premium of approximately 17.7% over the closing price of HK$5.400 per Share asquoted on the Stock Exchange on the Last Trading Day;

(b) a premium of approximately 15.0% over the average volume weighted averageclosing price of HK$5.525 per Share based on the daily volume weighted averageclosing prices quoted on the Stock Exchange for the 5 trading days immediatelyprior to and including the Last Trading Day;

(c) a premium of approximately 16.6% over the average volume weighted averageclosing price of HK$5.449 per Share based on the daily volume weighted averageclosing prices quoted on the Stock Exchange for the 10 trading days immediatelyprior to and including the Last Trading Day;

LETTER FROM ING

– 13 –

(d) a premium of approximately 28.6% over the average volume weighted average

closing price of HK$4.943 per Share based on the daily volume weighted average

closing prices quoted on the Stock Exchange for the 30 trading days immediately

prior to and including the Last Trading Day; and

(e) a discount of approximately 0.9% to the closing price of HK$6.410 per Share as

quoted on the Stock Exchange on the Latest Practicable Date.

The Share Offer Price of HK$6.591 represents:

(a) a premium of approximately 22.1% over the closing price of HK$5.400 per Share as

quoted on the Stock Exchange on the Last Trading Day;

(b) a premium of approximately 19.3% over the average volume weighted average

closing price of HK$5.525 per Share based on the daily volume weighted average

closing prices quoted on the Stock Exchange for the 5 trading days immediately

prior to and including the Last Trading Day;

(c) a premium of approximately 21.0% over the average volume weighted average

closing price of HK$5.449 per Share based on the daily volume weighted average

closing prices quoted on the Stock Exchange for the 10 trading days immediately

prior to and including the Last Trading Day;

(d) a premium of approximately 33.3% over the average volume weighted average

closing price of HK$4.943 per Share based on the daily volume weighted average

closing prices quoted on the Stock Exchange for the 30 trading days immediately

prior to and including the Last Trading Day; and

(e) a premium of approximately 2.8% over the closing price of HK$6.410 per Share as

quoted on the Stock Exchange on the Latest Practicable Date.

The Share Offer Price of HK$6.826 represents:

(a) a premium of approximately 26.4% over the closing price of HK$5.400 per Share as

quoted on the Stock Exchange on the Last Trading Day;

(b) a premium of approximately 23.5% over the average volume weighted average

closing price of HK$5.525 per Share based on the daily volume weighted average

closing prices quoted on the Stock Exchange for the 5 trading days immediately

prior to and including the Last Trading Day;

(c) a premium of approximately 25.3% over the average volume weighted average

closing price of HK$5.449 per Share based on the daily volume weighted average

closing prices quoted on the Stock Exchange for the 10 trading days immediately

prior to and including the Last Trading Day;

LETTER FROM ING

– 14 –

(d) a premium of approximately 38.1% over the average volume weighted averageclosing price of HK$4.943 per Share based on the daily volume weighted averageclosing prices quoted on the Stock Exchange for the 30 trading days immediatelyprior to and including the Last Trading Day; and

(e) a premium of approximately 6.5% over the closing price of HK$6.410 per Share asquoted on the Stock Exchange on the Latest Practicable Date.

Highest and Lowest Prices

During the Relevant Period, the highest closing price of the Shares was HK$6.45 perShare as quoted on the Stock Exchange on 4 and 8 January 2008, and the lowest closing priceof the Shares was HK$2.95 per Share as quoted on the Stock Exchange on 6 July 2007.

The Option Offer

As at the Latest Practicable Date, the Company had 89,700,000 Share Options with anexercise price of HK$5.24 which were then outstanding. Share options granted pursuant to theShare Option Scheme with an exercise price of HK$1.76 have all been exercised subsequentto the issue of the Announcement and hence no offer will be made for such share options withexercise price of HK$1.76.

An unconditional cash offer is made to all Optionholders in accordance with therequirements under the Takeovers Code.

Accepting Optionholders can choose any one of the following three alternatives of theconsideration in respect of the Option Offer. The consideration for each Share Option held,which comprises two elements, is as follows:

Alternative 1 Alternative 2 Alternative 3

First Payment HK$0.88 HK$0.88 HK$0.88Second Payment HK$0.235 HK$0.471 HK$0.706Total HK$1.115 HK$1.351 HK$1.586

Payment for the Option Offer

First Payment

In all three alternatives, the First Payment will be made within ten days after the receiptby the Offeror of the duly completed valid acceptances from the accepting Optionholders.

Second Payment

Under Alternative 1, the Second Payment will be made at the same time as the FirstPayment to those accepting Optionholders who have validly chosen this alternative.

LETTER FROM ING

– 15 –

Under Alternative 2, the Second Payment will be made within ten days of the

Shareholders’ Agreement becoming unconditional to those accepting Optionholders who have

validly chosen this alternative. If the Shareholders’ Agreement does not become

unconditional, the Second Payment will not be made to those accepting Optionholders

who have validly chosen this alternative.

Under Alternative 3, the Second Payment will be made within ten days of the completion

of the sale and purchase of the First Call Option Shares to those accepting Optionholders who

have validly chosen this alternative. If (a) the Shareholders’ Agreement does not become

unconditional or (b) the sale and purchase of the First Call Option Shares is not

completed, the Second Payment will not be made to those accepting Optionholders who

have validly chosen this alternative.

By accepting the Option Offer in respect of their Share Options, the Optionholders will

agree to cancel their Share Options for the consideration set out above.

As at the Latest Practicable Date, there were 89,700,000 Share Options with an exercise

price of HK$5.24 per Share. The Option Offer Prices above represent the “see-through” price

of the Share Option, being the amount by which the consideration in respect of the Share Offer

exceeds the exercise price of that Share Option.

Total Consideration

As at the Latest Practicable Date, there were 2,929,200,000 Shares in issue and Share

Options over 89,700,000 Shares granted by the Company pursuant to the Share Option Scheme.

Save for the Share Options, there are no outstanding options, warrants, derivatives or

other securities issued by the Company that carry a right to subscribe for or which are

convertible into Shares.

Assuming none of the Share Options is exercised in accordance with the terms of the

Share Option Scheme and full acceptance of the Option Offer under Alternative 3, the Option

Offer is valued at a maximum of approximately HK$142 million. Assuming all Share Options

are exercised in full by the Optionholders, no consideration will be payable under the Option

Offer.

Assuming none of the Share Options is exercised and full acceptance of the Share Offer

and the Option Offer under Alternative 3, the total maximum cash consideration payable by the

Offeror for the Share Offer and the Option Offer would be approximately HK$5,526 million.

Assuming all of the Share Options were exercised in full and full acceptance of the Share Offer

under Alternative 3, the total maximum cash consideration payable would be approximately

HK$5,996 million.

LETTER FROM ING

– 16 –

FINANCIAL RESOURCES AVAILABLE FOR THE OFFER

The Offeror intends to finance the Offer by drawing on inter-company facilities with itsshareholder or other entities associated with it. ING, as financial adviser to the Offeror, issatisfied that sufficient financial resources are available to the Offeror to satisfy full acceptanceof the Offer. The payment of interest on, repayment of or security for any liability (contingentor otherwise) will not depend to any significant extent on the business of the Group.

UNCONDITIONALITY OF THE OFFER

The Offer is unconditional in all respects.

ISSUED SHARES AND SHARE OPTIONS OF THE COMPANY

The table below sets out the shareholding structure of the Company as at the LatestPracticable Date and after completion of the Offer:

As at theLatest Practicable Date

After completionof the Offer(1)

After completionof the Offer(2)

ShareholderNumber of

Shares% of issued

share capitalNumber of

Shares% of issued

share capitalNumber of

Shares% of issued

share capital

The Offeror 820,119,151 28.00 864,597,151 29.52 925,872,151 30.67Persons acting in concert

with the Offeror 1,320,302,849 45.07 1,320,302,849 45.07 1,320,302,849 43.73

Sub-total 2,140,422,000 73.07 2,184,900,000 74.59 2,246,175,000 74.40

Directors of the Company andits subsidiary other thanMr. Han(3) 12,000,000 0.41 12,000,000 0.41 18,000,000 0.60

Public Shareholders 776,778,000 26.52 732,300,000 25.00 754,725,000 25.00

Total 2,929,200,000 100.00 2,929,200,000 100.00 3,018,900,000 100.00

Notes:

(1) Assuming (i) all the Optionholders accept the Option Offer, (ii) directors of the Company and itssubsidiaries do not accept the Share Offer, and (iii) not more than 75% of the Shares are held by theOfferor and its Concert Parties after close of the Offer and the 25% public float is maintained by theOfferor taking appropriate steps including the selling down of its shareholding interest in the Companyafter close of the Offer.

(2) Assuming (i) all the Share Options are exercised, (ii) directors of the Company and its subsidiaries donot accept the Share Offer, and (iii) not more than 75% of the Shares are held by the Offeror and itsConcert Parties after close of the Offer and the 25% public float is maintained by the Offeror takingappropriate steps including the selling down of its shareholding interest in the Company after close ofthe Offer.

(3) Such directors are Mr. Zhu Jun, Mr. Liu Lei, Mr. Shen Xiaoling, Mr. Yu Jianshui, Mr. Gao Qingju andMr. Wong Man Chung, Francis, and two directors of a subsidiary of the Company. Other than Mr. YuJianshui (who held 2,400,000 Share Options), none of the Directors held any Share Options as at theLatest Practicable Date. In addition, 3,600,000 Share Options were held by two directors of a subsidiaryof the Company.

LETTER FROM ING

– 17 –

The table below sets out details of the Share Options as at the Latest Practicable Date:

Number ofShare Options

Date of grant ofShare Options

Exerciseprice

Exerciseperiod

89,700,000(1) 26 October 2007 HK$5.24 30 October 2007 to

25 October 2017

Note:

(1) 83,700,000 Share Options are held by employees of the Group who are not connected persons of theCompany. 6,000,000 Share Options are held by connected persons of the Company, of which 2,400,000Share Options are held by Mr. Yu Jianshui, who is an executive Director of the Company, 2,000,000Share Options are held by Mr. Feng Aimin, a director of Hebei Jinxi and 1,600,000 Share Options areheld by Mr. Pang Baoyin, a director of Hebei Jinxi. The Share Options were granted in the ordinarycourse of business of the Company.

As at the Latest Practicable Date, no other options, warrants, derivatives or other

securities have been issued by the Company that carry a right to subscribe for or which are

convertible into Shares (other than the Share Options).

FURTHER TERMS OF THE OFFER

The Shares

Acceptance of the Share Offer by any Shareholder will be deemed to constitute a warranty

by such person that all the Shares to be sold by such person under the Share Offer will be free

from all liens, charges, options, claims, equities, adverse interests, rights of pre-emption and

any other third party rights or encumbrances of any nature whatsoever and together with all

rights accruing or attaching thereto, including, without limitation, the right to receive

dividends and distribution declared, made or paid on or after 13 December 2007, being the date

of the Announcement. By accepting the Option Offer, the Optionholders will surrender and

give up the subscription rights attached to the Share Options.

Availability of the Offer

As the availability of the Offer to persons not resident in Hong Kong may be affected by

the laws of the relevant jurisdiction in which they are resident, persons who are citizens or

residents or nationals of a jurisdiction outside Hong Kong should inform themselves about and

observe any applicable legal or regulatory requirements and, where necessary, seek legal

advice. It is the responsibility of Shareholders and Optionholders whose addresses (as shown

on the Company’s register of members or register of holders of Share Options, as the case may

be) are outside of Hong Kong and who wish to accept the Offer to satisfy themselves as to the

full observance of the laws of the relevant jurisdiction in connection therewith (including the

obtaining of any governmental, exchange control or other consent which may be required or

the compliance with other necessary formalities and the payment of any transfer or other taxes

due in respect of such jurisdiction).

LETTER FROM ING

– 18 –

COMPULSORY ACQUISITION

The parties to the Shareholders’ Agreement have agreed that if the Offeror acquires

Shares under the Offer which will result in ArcelorMittal and any persons acting in concert

with ArcelorMittal holding more than 90% of the voting rights of the Company, none of them

will exercise any rights of compulsory acquisition under any applicable laws and regulations,

including the Companies Act and the Takeovers Code.

Accordingly, neither ArcelorMittal nor the Offeror intends to exercise the right to

compulsorily acquire any Shares outstanding after completion of the Offer.

MAINTAINING THE COMPANY’S LISTING STATUS

It is the intention of the Offeror to maintain the listing of the Company on the Main Board

of the Stock Exchange after the close of the Offer.

The Stock Exchange has stated that if, at the close of the Offer, less than 25% of the

issued Shares are held by the public, or if the Stock Exchange believes that:

(a) a false market exists or may exist in the trading of the Shares; or

(b) there are insufficient Shares in public hands to maintain an orderly market,

then it will consider exercising its discretion to suspend trading in the Shares until a level of

sufficient public float is attained. In this connection, it should be noted that upon completion

of the Offer, there may be an insufficient public float of the Shares and, therefore, trading in

the Shares may be suspended until a sufficient level of public float is attained. The parties to

the Shareholders’ Agreement have agreed that in the event that, as a result of the Offer, the

Company no longer complies with the minimum public float requirement under Rule 8.08 of

the Listing Rules, ArcelorMittal will restore the required minimum public float, if necessary,

by selling down (or procuring the Offeror to sell down) a sufficient number of Shares acquired

under the Offer. ArcelorMittal may also discuss with the Company at the relevant time whether

or not the Company would like to issue new Shares for its own capital requirements. The

provisions relating to the maintenance of public float of the Company took immediate effect

upon signing of the Shareholders’ Agreement, and are therefore not subject to the Anti-trust

Condition being satisfied.

The Offeror has undertaken to the Stock Exchange that after the closing of the Offer,

appropriate steps will be taken to ensure that sufficient public float exists in the Shares, which

may include the sell down of its shareholding interest in the Company.

LETTER FROM ING

– 19 –

INFORMATION ON THE OFFEROR AND ARCELORMITTAL

The Offeror is a company incorporated in Switzerland and is a wholly-owned subsidiaryof ArcelorMittal. The Offeror is a holding company, holding interests in companies which areengaged in the steel business.

ArcelorMittal is the world’s number one steel company, with a total crude steelproduction of 118 million tonnes, which represented approximately 10% of the world’s steeloutput in 2006.

ArcelorMittal has led the consolidation of the world’s steel industry and currentlyemploys 320,000 employees in more than 60 countries. It is today a global steelmaker with anindustrial presence in 27 countries in Europe, Asia, Africa and America, which gives the groupexposure to all the key steel markets, from emerging to mature ones.

ArcelorMittal is a leader in all major global segments, including automotive,construction, household appliances and packaging. The group engages extensively in researchand development and technology, holds sizeable captive supplies of raw materials, and operatesextensive distribution networks.

For the year ended 31 December 2006, the ArcelorMittal group reported proformaconsolidated revenue of approximately US$88.6 billion and net income of approximatelyUS$7,973 million based on financial statements prepared in accordance with the InternationalFinancial Reporting Standards.

ArcelorMittal is currently listed under the legal entity ArcelorMittal on the stockexchanges of New York, Amsterdam, Paris, Brussels and Luxembourg, and on the Spanishstock exchanges of Barcelona, Bilbao, Madrid and Valencia. As at 10 January 2008, its marketcapitalisation amounted to approximately EUR65,646 million (or equivalent to approximatelyUS$96,354 million at the exchange rate of EUR0.6813 = US$1.0).

INTENTIONS OF THE OFFEROR REGARDING THE COMPANY

Strengthening its position in the fast growing PRC market is one of the key elements inArcelorMittal’s strategy. On 8 November 2007, the Offeror purchased 820,119,151 Shares fora total consideration of HK$5,019,129,204.12, which amounted to HK$6.12 per Share.

Save as disclosed in the section headed “Issued Shares and Share Options of theCompany” of this letter, none of the Offeror and its Concert Parties owned any other Sharesas at Latest Practicable Date.

The acquisition of approximately 28.00% stake in the Company constitutes an importantstep. With this 28.00% acquisition and the Shareholders’ Agreement with the ControllingShareholders, ArcelorMittal will be better positioned to participate in the attractive growth ofthe PRC construction and infrastructure sectors in the country and develop the Company intoa leading steel manufacturer in China, in particular, as a leading producer of heavy sections,focusing on profitability, quality and sustainability.

LETTER FROM ING

– 20 –

Part of ArcelorMittal’s growth over the years has been through acquisitions and

subsequently creating value through active management of the companies acquired.

ArcelorMittal believes that it will be able to add value to the Company in areas including the

provision of technology and technical know-how, training, financial management, mergers and

acquisitions, supply chain management and marketing as well as sustainable and resource

efficient production. ArcelorMittal’s existing investments in the PRC include, among others, a

33.02% equity interest in Valin, a 12% equity interest in the Baosteel-

NipponSteel/ArcelorMittal Automotive Sheet Joint Venture and a 90% interest in Rongcheng

Chengshan Steelcord.

After the Shareholders’ Agreement becomes unconditional, the Offeror expects that

changes will be made to the composition of the Board, which will be in compliance with the

Takeovers Code and the Listing Rules. Please refer to the paragraph headed “The Shareholders’

Agreement and the Business Cooperation Agreement – The Shareholders’ Agreement –

Management of the Company” for more details.

It is the intention of the Offeror to maintain the existing business of the Group upon the

completion of the Offer. The Offeror does not intend to introduce any major changes to the

existing operating and management structure of the Group (including any redeployment of

fixed assets of the Group) or the employees of the Group as a result of the Offer.

ACCEPTANCE AND SETTLEMENT

Procedures for Acceptance

The Share Offer

For Shareholders, to accept the Share Offer in respect of your Shares, you should

complete the accompanying WHITE form of acceptance and transfer for the Disinterested

Shares in accordance with the instructions printed thereon, which instructions form part of the

terms and conditions of the Share Offer in respect of the Disinterested Shares. The completed

WHITE form of acceptance and transfer for the Disinterested Shares should then be

forwarded, together with the relevant Disinterested Share certificate(s) and/or transfer

receipt(s) and/or any document(s) of title (and/or any satisfactory indemnity or indemnities

required in respect thereof) for not less than the number of Disinterested Shares in respect of

which you intend to accept the Share Offer, by post or by hand, to the Registrar at 26/F, Tesbury

Centre, 28 Queen’s Road East, Wanchai, Hong Kong in an envelope marked “China Oriental

Share Offer” as soon as possible but in any event not later than 4:00 p.m. on Monday, 4

February 2008, or such later time as the Offeror may determine and announce in accordance

with the Takeovers Code. No acknowledgement of receipt of any form of acceptance and

transfer, share certificate(s), transfer receipt(s) or other document(s) of title (and/or any

satisfactory indemnity or indemnities required in respect thereof) will be given.

LETTER FROM ING

– 21 –

The Option Offer

For Optionholders, to accept the Option Offer in respect of your Share Options, you

should complete the accompanying YELLOW form of acceptance and cancellation for the

Share Options in accordance with the instructions printed thereon, which instructions form part

of the terms and conditions of the Option Offer in respect of the Share Options. The completed

YELLOW form of acceptance and cancellation for the Share Options should then be

forwarded, together with the relevant letter or other document evidencing the grant of the

relevant Share Options to you and/or any document(s) of title or entitlement (and/or any

satisfactory indemnity or indemnities required in respect thereof) for not less than the number

of Share Options in respect of which you intend to accept the Option Offer, by post or by hand,

to China Oriental at Suites 901-2 & 10, 9/F, Great Eagle Centre, 23 Harbour Road, Wanchai,

Hong Kong in an envelope marked “China Oriental Option Offer” as soon as possible but in

any event not later than 4:00 p.m. on Monday, 4 February 2008, or such later time as the

Offeror may determine and announce in accordance with the Takeovers Code. No

acknowledgement of receipt of any form of acceptance and cancellation, grant letter or other

document granting the Share Options or other document(s) of title or entitlement (and/or any

satisfactory indemnity or indemnities required in respect thereof) will be given.

General

Your attention is drawn to the section headed “Further procedures for acceptance” as set

out in Appendix I to this Composite Document and in the accompanying WHITE or YELLOW

form.

Overseas Shareholders and Optionholders

Shareholders and Optionholders with registered addresses outside Hong Kong should pay

attention to the section headed “General” in Appendix I to this Composite Document.

Hong Kong Stamp Duty

Shareholder’s Hong Kong ad valorem stamp duty arising in connection with acceptance

of the Share Offer will be payable by each Shareholder at a rate of HK$1.00 for every

HK$1,000 (or part thereof) of: (i) the market value of the shares; or (ii) the consideration

payable to such person in respect of the relevant acceptance by such Shareholder, whichever

is the higher.

The Inland Revenue Department would normally accept the last closing price of the

shares on the Stock Exchange on the day of transfer as the market value of the shares

transferred for the purpose of calculating stamp duty.

LETTER FROM ING

– 22 –

The consideration payable would be the maximum amount payable under each alternative.

For a Shareholder who has chosen Alternative 1, the consideration payable for the purpose of

calculating stamp duty is HK$6.355. For a Shareholder who has chosen Alternative 2, the

consideration payable for the purpose of calculating stamp duty is HK$6.591. For a

Shareholder who has chosen Alternative 3, the consideration payable for the purpose of

calculating stamp duty is HK$6.826.

The amount of stamp duty payable will be deducted from the consideration in respect of

the First Payment due to such person on acceptance of the Share Offer. Such amounts will be

paid by the Offeror to the Hong Kong Stamp Duty Office in accordance with the Stamp Duty

Ordinance (Chapter 117 of the Laws of Hong Kong).

Shareholder should inform themselves about and observe any applicable tax requirements

and, where necessary, seek professional tax advice.

Settlement

The Share Offer

As set out in the “Letter from ING – Consideration of the Offer – The Share Offer”,

accepting Shareholders can choose any one of the three alternatives of the consideration in

respect of the Share Offer, i.e., Alternative 1, Alternative 2 or Alternative 3 as set out on page

12 of this Composite Document.

Provided that the relevant WHITE form of acceptance and transfer for the Disinterested

Shares and Disinterested Share certificate(s) and/or transfer receipt(s) and/or other

document(s) of title (and/or any satisfactory indemnity or indemnities required in respect

thereof) are valid and complete and have been received by the Registrar by no later than 4:00

p.m. on Monday, 4 February 2008 (or such later time as the Offeror may determine and

announce in accordance with the Takeovers Code), a cheque for the amount due to each of the

accepting Shareholders in respect of the First Payment (for Shareholders who choose any of the

three consideration alternatives) and the Second Payment (for Shareholders who choose

Alternative 1) of the relevant Disinterested Shares tendered by them under the Share Offer, less

seller’s ad valorem stamp duty payable by them, will be despatched to the relevant

Shareholders by ordinary post at their own risk within ten days following the date on which all

the relevant documents are received by the Registrar to render such acceptance complete and

valid.

For Shareholders who choose Alternative 2, the Second Payment will be made within ten

days of the Shareholders’ Agreement becoming unconditional to those accepting Shareholders

who have validly chosen this alternative. If the Shareholders’ Agreement does not become

unconditional, the Second Payment will not be made to those accepting Shareholders who

have validly chosen this alternative.

LETTER FROM ING

– 23 –

For Shareholders who choose Alternative 3, the Second Payment will be made within ten

days of the completion of the sale and purchase of the First Call Option Shares to those

accepting Shareholders who have validly chosen this alternative. If (a) the Shareholders’

Agreement does not become unconditional or (b) the sale and purchase of the First Call

Option Shares is not completed, the Second Payment will not be made to those accepting

Shareholders who have validly chosen this alternative.

The Option Offer

As set out in the “Letter from ING – Consideration of the Offer – The Option Offer”,

accepting Optionholders can choose any one of the three alternatives of the consideration in

respect of the Option Offer, i.e., Alternative 1, Alternative 2 or Alternative 3 as set out on page

15 of this Composite Document.

Provided that the relevant YELLOW form of acceptance and cancellation for the Share

Options and the relevant letter or other document evidencing the grant of the relevant Share

Options to the accepting Optionholder and/or other document(s) of title or entitlement (and/or

any satisfactory indemnity or indemnities required in respect thereof) are valid and complete

and have been received by China Oriental by no later than 4:00 p.m. on Monday, 4 February

2008 (or such later time as the Offeror may determine and announce in accordance with the

Takeovers Code), a cheque for the amount due to each of the accepting Optionholders in

respect of the First Payment (for Optionholders who choose any of the three consideration

alternatives) and the Second Payment (for Optionholders who choose Alternative 1) of the

relevant Share Options tendered by them under the Option Offer and agreed to be cancelled

will be despatched to the relevant Optionholders by ordinary post at their own risk within ten

days following the date on which all the relevant documents are received by China Oriental to

render such acceptance complete and valid.

For Optionholders who choose Alternative 2, the Second Payment will be made within ten

days of the Shareholders’ Agreement becoming unconditional to those accepting Optionholders

who have validly chosen this alternative. If the Shareholders’ Agreement does not become

unconditional, the Second Payment will not be made to those accepting Optionholders

who have validly chosen this alternative.

For Optionholders who choose Alternative 3, the Second Payment will be made within ten

days of the completion of the sale and purchase of the First Call Option Shares to those

accepting Optionholders who have validly chosen this alternative. If (a) the Shareholders’

Agreement does not become unconditional or (b) the sale and purchase of the First Call

Option Shares is not completed, the Second Payment will not be made to those accepting

Optionholders who have validly chosen this alternative.

LETTER FROM ING

– 24 –

Nominee registration

To ensure equality of treatment of all Shareholders, those registered Shareholders who

hold Shares as nominee for more than one beneficial owner should, as far as practicable, treat

the holding of each beneficial owner separately. In order for the beneficial owners of Shares,

whose investments are registered in nominee names, to accept the Share Offer, it is essential

that they provide instructions to their nominees of their intentions with regard to the Share

Offer.

Despatch of payment

All documents and remittances will be sent to the Shareholders and the Optionholders

through ordinary post at their own risk. These documents and remittances will be sent to them

at their respective addresses as they appear in the register of members (or the register of

holders of Share Options as the case may be), or, in the case of joint Shareholders, to the

Shareholder whose name appears first in the said register of members, unless otherwise

specified in the relevant WHITE forms of acceptance and transfer for the Disinterested Shares

completed and returned by the accepting Shareholders (or YELLOW forms of acceptance and

cancellation for the Share Options as the case may be). None of the Offeror, its Concert Parties,

ING, China Oriental, UBS, the Registrar or any of their respective directors, officers, or

associates or any other person involved in the Offer will be responsible for any loss or delay

in transmission of such documents and remittances or any other liabilities that may arise as a

result thereof.

In respect of any payment to any accepting Shareholder or Optionholder under the Offer,

each cheque representing any amount due to any such holder will be made payable to the order

of the person to whom the envelope containing the cheque is addressed, and the encashment

of the cheque shall be a good discharge to the Offeror for the monies represented by the cheque.

All cheques will be posted at the risk of the addressees and other persons entitled to the monies

represented by the cheques. On or after the day falling six months after the posting of any

cheque, the Offeror will have the right to cancel or countermand payment of such cheque which

has not been encashed or has been returned uncashed, and will place the monies represented

thereby in a deposit account (the “Deposit Account”) in the Company’s name with a licensed

bank in Hong Kong to be selected by the Company and approved by the Offeror. The Company

will hold those monies until the end of a six-year period (the “Holding Period”) commencing

from the date when the Second Payment is made, as evidenced by the posting of the relevant

cheques, to accepting Shareholders and Optionholders choosing Alternative 1, Alternative 2 or

Alternative 3, whichever is the latest. During the Holding Period, the Company will make

payments out of the sum deposited with the Deposit Account to any person who has satisfied

the Company that he is entitled to payment under the Offer and that the cheque(s) previously

sent to him has not been encashed. No payment so made by the Company will include any

interest accrued on the sum to which such person is entitled. Any payment so made by the

Company shall be a good discharge to the Offeror for the monies represented by such payment.

The Company will exercise its absolute discretion in determining whether or not it is satisfied

that any person is entitled to payment out of the Deposit Account, and a certificate issued by

LETTER FROM ING

– 25 –

the Company to the effect that a person is so entitled or not so entitled will be conclusive and

binding upon all persons claiming an interest in the monies deposited in the Deposit Account.

Upon the expiration of the Holding Period, the Offeror will be released from any further

obligation to make any payment under the Offer, and the Company will accordingly transfer

to the Offeror the balance of the sums deposited with the Deposit Account together with

accrued interest, subject, if applicable, to the deduction of any interest or withholding or other

tax and any other deduction required by law as well as all costs and expenses incurred in the

transfer. The above arrangements will take effect in accordance with, and subject to, all

prohibitions and conditions, if any, imposed by law.

For accepting Shareholders and Optionholders who choose Alternative 2 or Alternative 3

among the three consideration alternatives in respect of the Share Offer and the Option Offer,

respectively, the Second Payment will not be made immediately after the completion of the

Offer. As described above, for Shareholders and Optionholders who choose Alternative 2, the

Second Payment will be made within ten days of the Shareholders’ Agreement becoming

unconditional. For Shareholders and Optionholders who choose Alternative 3, the Second

Payment will be made within ten days of the completion of the sale and purchase of the First

Call Option Shares. By accepting the Offer in respect of their Shares or Share Options as the

case may be, the accepting Shareholders and Optionholders are reminded, and specifically

agree, to immediately notify in writing the Company and the registrar of the Company from

time to time upon any changes in their addresses.

TAXATION

Shareholders and Optionholders are recommended to consult their own professional

advisers if they are in any doubt as to the taxation implications of accepting the Offer in respect

of their Shares or Share Options (as the case may be). It is emphasised that none of the Offeror,

its Concert Parties, ING, China Oriental, UBS, the Registrar or any of their respective

directors, officers or associates or any other person involved in the Offer accepts responsibility

for any taxation effects on, or liabilities of, any persons as a result of their acceptance of the

Offer.

THE SHAREHOLDERS’ AGREEMENT AND THE BUSINESS COOPERATION

AGREEMENT

The terms of the Shareholders’ Agreement and the Business Cooperation Agreement are

summarised in the section headed “The Shareholders’ Agreement and the Business Cooperation

Agreement” of this Composite Document. As described in more detail in that section, the key

terms of the Shareholders’ Agreement are conditional upon satisfaction of the Anti-trust

Condition. The key terms of the Business Cooperation Agreement will also take effect only

upon the Shareholders’ Agreement becoming unconditional.

LETTER FROM ING

– 26 –

GENERAL

Shareholders and Optionholders are advised to read carefully the letter from the

Independent Board Committee to the Independent Shareholders and the Optionholders and the

letter from Evolution Watterson to the Independent Board Committee, Independent

Shareholders and Optionholders as contained in this Composite Document before deciding

whether or not to accept the Offer.

Your attention is also drawn to the further terms of the Offer and the additional

information set out in the appendices to this Composite Document.

Yours faithfully,

On behalf of

ING Bank N.V.Malcolm E.O. Brown

Managing Director

LETTER FROM ING

– 27 –

(incorporated in Bermuda with limited liability)(Stock Code: 581)

Executive Directors:

Mr. Han Jingyuan

(Chairman and Chief Executive Officer)

Mr. Zhu Jun

Mr. Liu Lei

Mr. Shen Xiaoling

Mr. Yu Jianshui

Mr. Zhu Hao

Independent Non-executive Directors:

Mr. Gao Qingju

Mr. Yu Tung Ho

Mr. Wong Man Chung, Francis

Registered office:

Clarendon House

2 Church Street

Hamilton HM 11

Bermuda

Principal office and place of

business in Hong Kong:

Suites 901-2 & 10

9th Floor, Great Eagle Centre

23 Harbour Road

Wanchai

Hong Kong

14 January 2008

To the Independent Shareholders and Optionholders

Dear Sir or Madam,

UNCONDITIONAL MANDATORY CASH OFFERBY ING BANK N.V. ON BEHALF OF

MITTAL STEEL HOLDINGS AGTO ACQUIRE ALL THE OUTSTANDING SHARES IN

THE ISSUED SHARE CAPITAL AND CANCEL ALL SHARE OPTIONS OFCHINA ORIENTAL GROUP COMPANY LIMITED(OTHER THAN THOSE ALREADY OWNED BY

MITTAL STEEL HOLDINGS AG ANDPARTIES ACTING IN CONCERT WITH IT)

1. INTRODUCTION

Reference is made to the Announcement in which the Offeror and the Company jointlyannounced that on 8 November 2007, the Offeror completed its acquisition of approximately28.00% of the issued Shares from Ms. Chen Ningning.

* For identification purpose only

LETTER FROM THE BOARD

– 28 –

On 5 December 2007, the Takeovers and Mergers Panel came to a decision that prior to

and at the time of the Offeror’s acquisition of Ms. Chen Ningning’s approximately 28.00%

stake in the Company, ArcelorMittal and the Controlling Shareholders were parties acting in

concert and immediately following the completion of the Offeror’s acquisition of Ms. Chen

Ningning’s issued Shares, the Offeror and person acting in concert with it held an aggregate

of 2,140,422,000 Shares, representing approximately 73.07% of the issued share capital of the

Company as at the date of this Composite Document. Accordingly, the Offeror is required,

pursuant to Rule 26.1 of the Takeovers Code, to make an unconditional mandatory cash offer

to acquire all the Disinterested Shares.

The purpose of this Composite Document, of which this letter forms a part, is to provide

you with, amongst others, information relating to the Group, the Controlling Shareholders, the

Offeror and the Offer as well as setting out the letter from the Independent Board Committee

containing its recommendation and advice to the Independent Shareholders and Optionholders

in respect of the Offer and the letter from Evolution Watterson containing its advice to the

Independent Board Committee, the Independent Shareholders and the Optionholders in respect

of the Offer.

Unless the context otherwise requires, terms defined in this Composite Document shall

have the same meanings when used in this letter.

2. INDEPENDENT BOARD COMMITTEE

In accordance with Rule 2.1 and Rule 2.8 of the Takeovers Code, the Independent Board

Committee comprising all the independent non-executive Directors of the Company, namely

Mr. Yu Tung Ho, Mr. Gao Qingju and Mr. Wong Man Chung, Francis, was established to advise

the Independent Shareholders and Optionholders in respect of the Offer.

The independent non-executive Directors are independent of and have no direct or

indirect interest in the Offer other than, in the case of Mr. Gao Qingju and Mr. Wong Man

Chung, Francis, as holders of the Shares which are subject to the Share Offer. The Company,

with the approval of the Independent Board Committee, has appointed Evolution Watterson as

its independent financial adviser to advise the Independent Board Committee, the Independent

Shareholders and the Optionholders on whether the Offer is fair and reasonable so far as the

Independent Shareholders and the Optionholders are concerned and as to the actions to be

taken by them.

The full text of the letter of advice from Evolution Watterson addressed to the

Independent Board Committee, the Independent Shareholders and the Optionholders is set out

in this Composite Document. Shareholders and Optionholders are advised to read the letter of

advice from Evolution Watterson and the additional information contained in the appendices to

this Composite Document carefully before taking any action in respect of the Offer.

LETTER FROM THE BOARD

– 29 –

3. THE OFFER

ING is making the Offer, on behalf of the Offeror, on the terms and conditions set out in

this Composite Document (including, without limitation, the terms set out in Appendix I to this

Composite Document) and in the Form of Acceptance, to acquire all the Disinterested Shares

and Share Options on the following basis:

The consideration in respect of the Share Offer is as follows:

Alternative 1 Alternative 2 Alternative 3

First Payment HK$6.12 HK$6.12 HK$6.12Second Payment HK$0.235 HK$0.471 HK$0.706Total HK$6.355 HK$6.591 HK$6.826

The consideration in respect of the Option Offer is as follows:

For each Share Option held (with an exercise price of HK$5.24)

Alternative 1 Alternative 2 Alternative 3

First Payment HK$0.88 HK$0.88 HK$0.88Second Payment HK$0.235 HK$0.471 HK$0.706Total HK$1.115 HK$1.351 HK$1.586

Further details of the Offer are set out in the Letter from ING in this Composite

Document.

4. INFORMATION ON THE COMPANY

The Company is incorporated under the laws of Bermuda with limited liability. The Group

is principally engaged in the production and sale of iron and steel products in the PRC.

Wellbeing is the beneficial owner of 1,255,849,124 Shares, which represent

approximately 42.87% of the entire issued share capital in the Company. Wellbeing is

beneficially owned as to approximately 60.69% by Mr. Han and Mr. Han also holds 16.09% of

the issued share capital of Wellbeing on trust for the benefit of approximately 1,800 employees

of Hebei Jinxi, the principal subsidiary of the Company. The remainder of the issued share

capital of Wellbeing is owned by ten other individuals, all of whom are involved or were