Embed Size (px)

Citation preview

MoneyShort Run vs Long Run

Money Supply and Money DemandSlides for International Finance (KOM Chapter 15)

Alan G Isaac

American University

2012-09-21

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Preview

Defining money

Policy control of the money supply

Determinants of the demand for monetary assetsInterest rate determination

equilibrium in the money market

Exchange rate determination reduxLinking the money market and FX market

Long run effects of money supply changesprices interest rates and exchange rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money

Different groups of assets may be classified as money

Money assets that are commonly used as a means of paymentCurrency and checking accounts form a useful definition ofmoneyBank deposits in the foreign exchange market are excluded fromthis definition

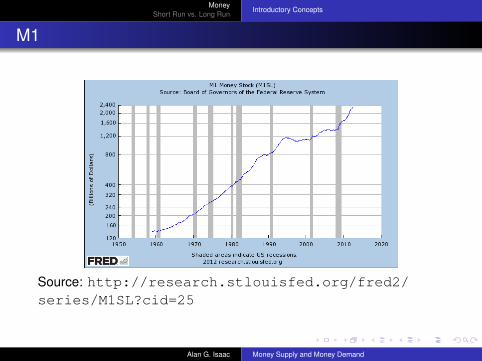

M1 currency held by public + checkable depositshttpresearchstlouisfedorgfred2categories24

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

M1

Source httpresearchstlouisfedorgfred2seriesM1SLcid=25

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

Monetary authority the institution authorized to set monetary policymost often a central bank

A monetary authority can fairly directly control

the high-powered money stock

the interbank lending rate (eg Fed funds rate)

These policy actions determine ldquothe supply of moneyrdquo (eg M1)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

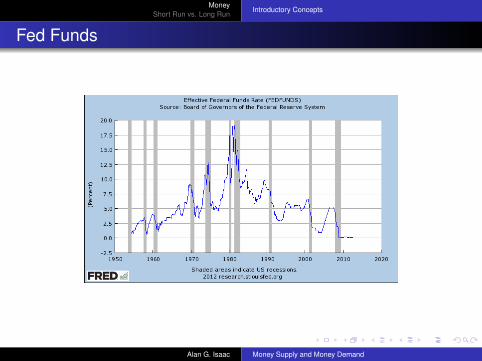

Fed Funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

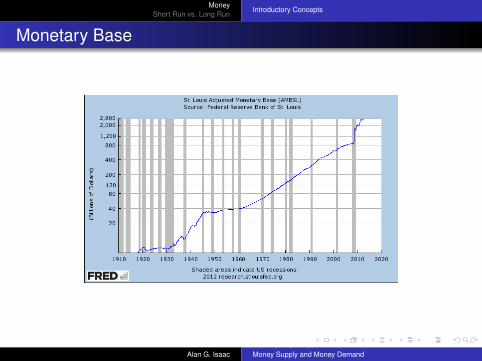

Monetary Base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

US the Federal Open Market Committee (FOMC) of the FederalReserve System (the seven members of the Board of Governorsof the Federal Reserve System plus five Fed bank presidents)

EU monetary policy defined by the Governing Council (like theFOMC includes the Executive Board of the ECB which isanalogous to the Fedrsquos Board of Governors)httpwwwecbintecborgadecisionsgovchtmlindexenhtml

JP the Policy Board of the Bank of Japanhttpwwwbojorjpenaboutorganizationpolicyboardindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

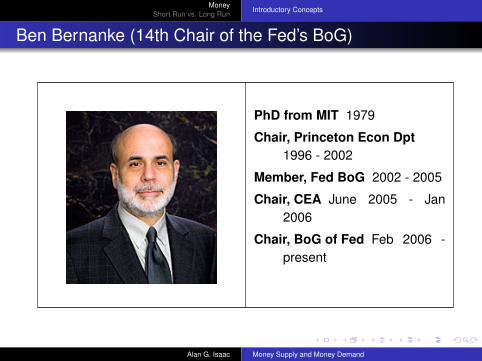

Ben Bernanke (14th Chair of the Fedrsquos BoG)

PhD from MIT 1979

Chair Princeton Econ Dpt1996 - 2002

Member Fed BoG 2002 - 2005

Chair CEA June 2005 - Jan2006

Chair BoG of Fed Feb 2006 -present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

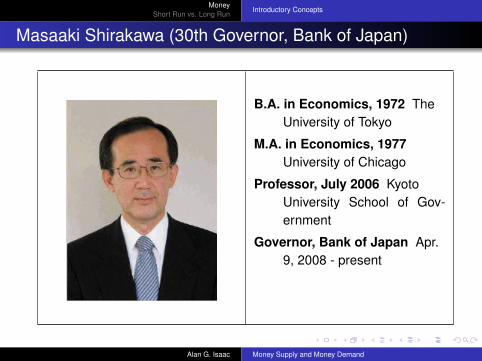

Masaaki Shirakawa (30th Governor Bank of Japan)

BA in Economics 1972 TheUniversity of Tokyo

MA in Economics 1977University of Chicago

Professor July 2006 KyotoUniversity School of Gov-ernment

Governor Bank of Japan Apr9 2008 - present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of Japan

Established 1882 the Bank of Japan Act of 1882

Reorganized 1942 Bank of Japan Act of 1942

1949 Policy Board established one of several amendments afterWorld War IIPB = highest decision-making body

Reorganized 1998 Bank of Japan Act of 1997principles independence and transparency

The BoJ has an explicit price stability goal in its bylaws

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

European Central Bank (ECB)

Figure ECB Logo

Responsible for euro area monetary policy since 1 January 1999Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Mario Draghi 3rd President of the ECB

PhD in Economics MIT 1976

University of FlorenceProfessor 1981 - 1991

World Bank Executive Director1984 - 1990

Italian Treasury Director Gen-eral 1991 - 2001

Goldman Sachs Vice-Presidentand Managing Director2002 - 2005

ECB President 2011 - present(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

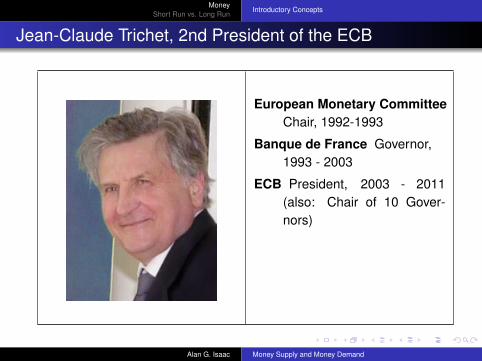

Jean-Claude Trichet 2nd President of the ECB

European Monetary CommitteeChair 1992-1993

Banque de France Governor1993 - 2003

ECB President 2003 - 2011(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Governing Council

ECB Governing Council

six members of the Executive Board plusgovernors of the national central banks of the 16 euro areacountriesthe main decision-making body of the ECB

The ECB GC formulates monetary policy for the euro areaThe ECB Governing Council usually meets twice a month at theEurotower in Frankfurt am Main Germany

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Deposit Rate

httpsdwecbeuropaeureportsdonode=100000131

httpenwikipediaorgwikiEurozoneInterest_rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

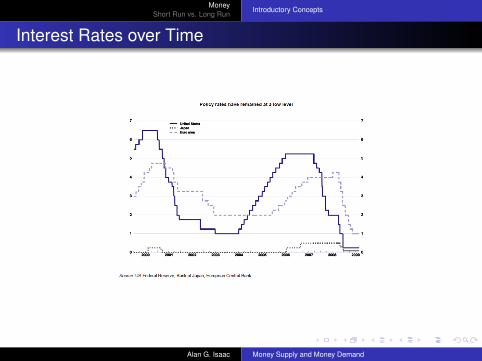

Interest Rates over Time

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Eurosystem

historical noveltysupranational monetary unionEuro launched 1 Jan 1999Physical euros since 1 Jan 2002

European Central Bank (ECB)led by Governing Council

National central banks (NCBs)EU member states that have adopted the Euro

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Supply

money supply (M) the quantity of money that circulates in aneconomyM = C + Dcurrency help by public plus checkable deposits

monetary base (MB) currency held by public + reserves of banksMB = C + Rinfluences broader measures of the money supply

eg checkable deposits (including debit card accounts)

The monetary authority can roughly control the money supply

US monetary authority is a central banking system FederalReserve System

The Fed can directly regulate the monetary base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Money demand the amount of money individuals and businessesare willing to hold (instead of illiquid assets)

Real money demand (L) the amount of purchasing powerindividuals and businesses are willing to hold in the form ofmoney (instead of illiquid assets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Influences on the Demand for Money

1 Expected returns rates of returns on non-monetary assets(compared to monetary assets)monetary assets pay little or no interestthe interest rate on non-monetary assets is the opportunity costof holding monetary assets ^R _L

2 Riskthe risk of holding M is largely inflation risk which reduces thepurchasing power of moneybut other assets have this risk too so this risk is not veryimportant in defining the demand for monetary assets

3 LiquidityM is the most liquid asset it is the asset with the lowest cost ofturning it into other assets or commodities

4 Prices and income ^P - ^need for M ^Y - ^need for M

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Prices and Income

A higher level of average prices means a greater need for liquidityto buy the same amount of goods and services -gt highernominal demand for money

A higher real national income (GNP) means more goods andservices are being produced and bought in transactionsincreasing the need for liquidity -gt higher real demand for money

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Aggregate money demand

real L(RY)nominal P x L(RY)

where

P is the price levelY is real national incomeR is a measure of interest rates on non-monetary assets

Aggregate demand for real monetary assets is influenced by

transactions demand (national income)

opportunity cost (interest rates)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

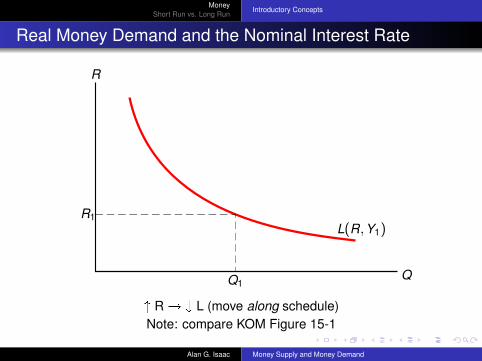

Real Money Demand and the Nominal Interest Rate

L(RY1)

QQ1

R

R1

^ R _ L (move along schedule)Note compare KOM Figure 15-1

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

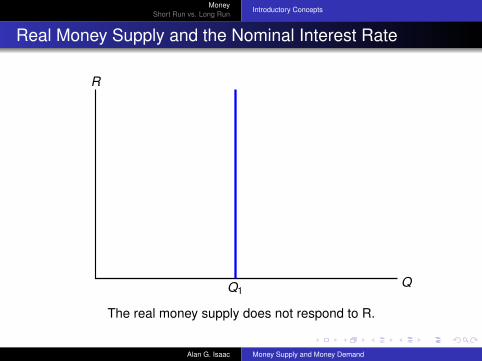

Real Money Supply and the Nominal Interest Rate

QQ1

R

The real money supply does not respond to R

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

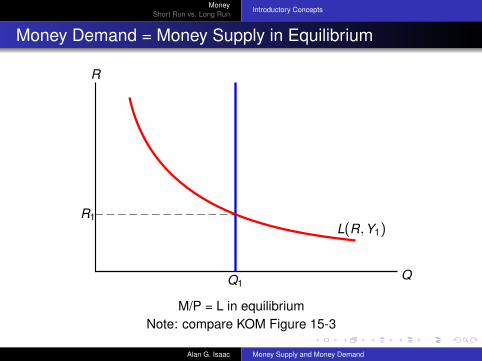

Money Demand = Money Supply in Equilibrium

L(RY1)

QQ1

R

R1

MP = L in equilibriumNote compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

The money market markets for trading monetary (very liquid) assetswhich are loosely called ldquomoneyrdquoInterest rates on monetary assets are low compared to interestrates on less liquid assets (such as bonds loans and deposits ofcurrency in the foreign exchange markets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

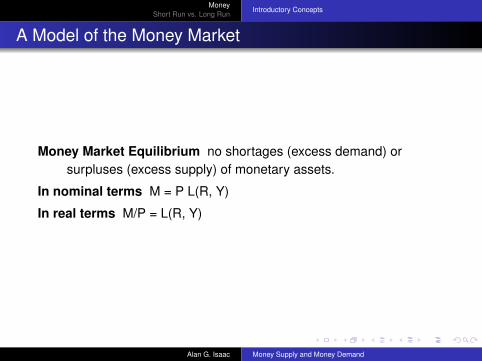

A Model of the Money Market

Money Market Equilibrium no shortages (excess demand) orsurpluses (excess supply) of monetary assets

In nominal terms M = P L(R Y)

In real terms MP = L(R Y)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

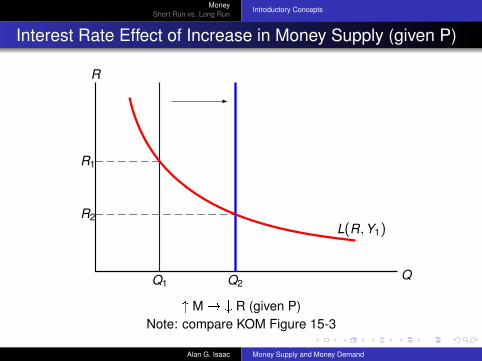

Interest Rate Effect of Increase in Money Supply (given P)

L(RY1)

QQ1 Q2

R

R1

R2

^ M _ R (given P)Note compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

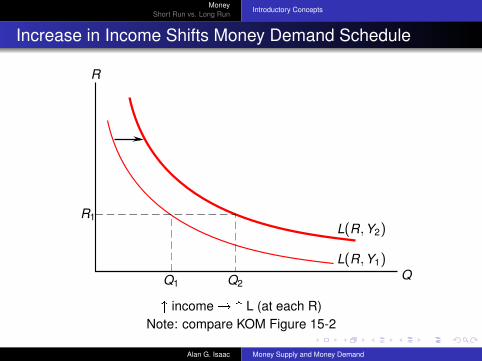

Increase in Income Shifts Money Demand Schedule

L(RY1)

L(RY2)

QQ2Q1

R

R1

^ income ^ L (at each R)Note compare KOM Figure 15-2

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

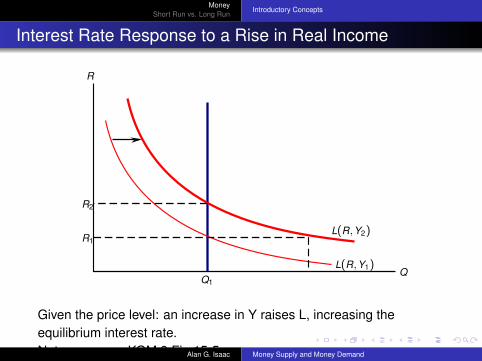

Interest Rate Response to a Rise in Real Income

R

QQ1

L(RY1)

L(RY2)R1

R2

Given the price level an increase in Y raises L increasing theequilibrium interest rateNote compare KOM 9 Fig 15-5Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

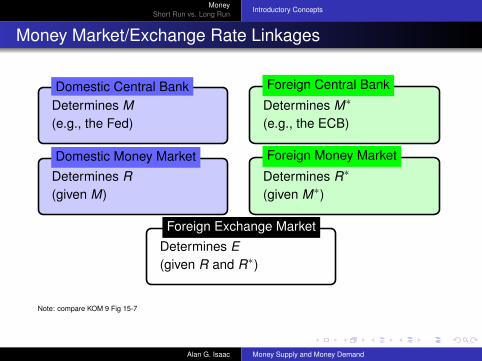

Money MarketExchange Rate Linkages

Determines M(eg the Fed)

Domestic Central BankDetermines Mlowast

(eg the ECB)

Foreign Central Bank

Determines R(given M)

Domestic Money MarketDetermines Rlowast

(given Mlowast)

Foreign Money Market

Determines E(given R and Rlowast)

Foreign Exchange Market

Note compare KOM 9 Fig 15-7

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

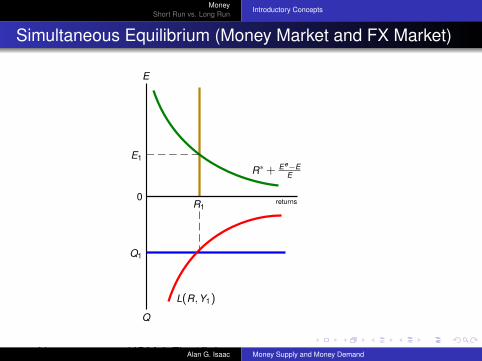

Simultaneous Equilibrium (Money Market and FX Market)

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

E

Note compare KOM 9 Fig 15-6Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

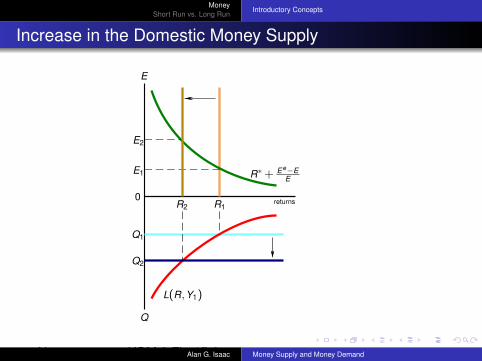

Increase in the Domestic Money Supply

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

R2

Q2

E2

E

Note compare KOM 9 Fig 15-8Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

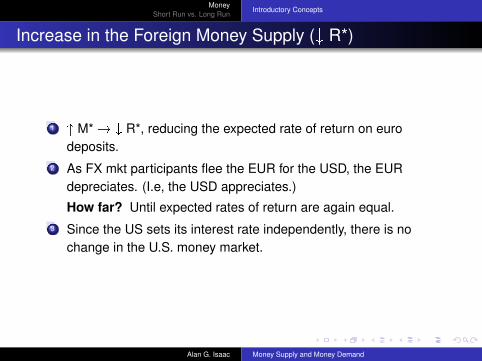

Increase in the Foreign Money Supply (_ R)

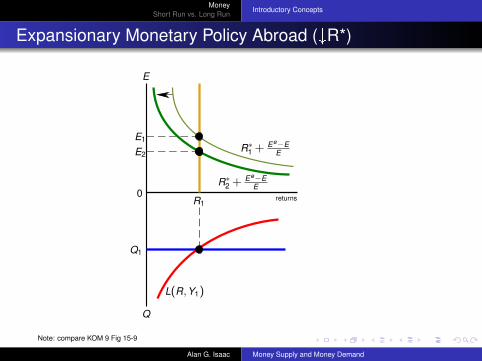

1 ^ M _ R reducing the expected rate of return on eurodeposits

2 As FX mkt participants flee the EUR for the USD the EURdepreciates (Ie the USD appreciates)

How far Until expected rates of return are again equal3 Since the US sets its interest rate independently there is no

change in the US money market

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Expansionary Monetary Policy Abroad (_R)

E2

Q

L(RY1)

Q1

R10 returns

Rlowast2 +

EeminusEE

Rlowast1 +

EeminusEE

E1

E

Note compare KOM 9 Fig 15-9

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

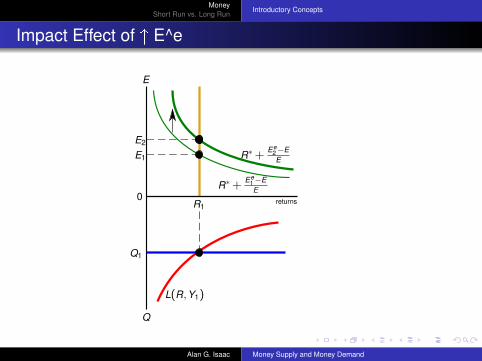

Impact Effect of ^ E^e

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+Ee

1 minusEE

Rlowast+Ee

2 minusEE

E2

E

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short Run vs Long Run

What is the long run Long enough for a change in the moneysupply to produce its full effect on the economy

Long-run neutrality of money In the long run a change in Mproduces a proportional change in all nominal stock variables(eg P E etc)In the long run a change in M does not change any real variables(eg MP EPP etc)

Long run monetary policy influences prices

Short run monetary policy influences interest rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

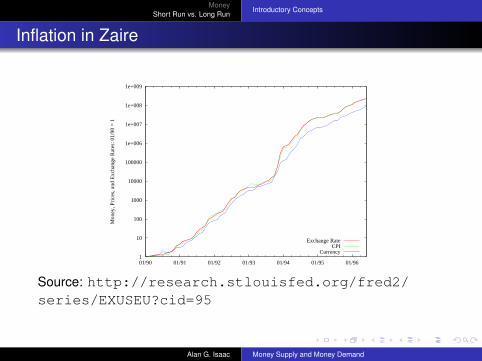

Inflation in Zaire

1

10

100

1000

10000

100000

1e+006

1e+007

1e+008

1e+009

0190 0191 0192 0193 0194 0195 0196

Mon

ey P

rice

s a

nd E

xcha

nge

Rat

es 0

190

= 1

Exchange RateCPI

Currency

Source httpresearchstlouisfedorgfred2seriesEXUSEUcid=95

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run and Short Run

Up to now have have considered short-run analysisIn the long run prices of factors of production and of output havesufficient time to adjust to market conditions

Short Run

prices do not have enough time to adjust to marketconditions

Long Run

Wages adjust to equate the demand for and supply of laborReal output (income) is determined by the economyrsquosproductive capacitymdashfactor supplies (eg the supply oflabor) and technology (Not by the quantity of money)Real interest rates depend on the supply of saved funds anddemand for these funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run (cont)

Long-run prediction for ^M

no change in Yno change in (real) interest rateno change in L(RY) the aggregate demand for realmonetary assets L(RY)proportional ^P

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

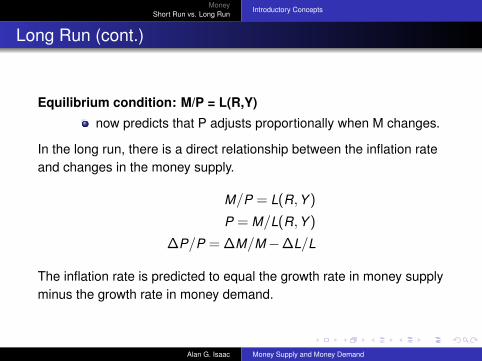

Long Run (cont)

Equilibrium condition MP = L(RY)

now predicts that P adjusts proportionally when M changes

In the long run there is a direct relationship between the inflation rateand changes in the money supply

MP = L(RY )

P = ML(RY )

∆PP = ∆MM minus∆LL

The inflation rate is predicted to equal the growth rate in money supplyminus the growth rate in money demand

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Inflation in Zaire

1

10

100

1000

10000

100000

1e+006

1e+007

1e+008

1e+009

0190 0191 0192 0193 0194 0195 0196

Mon

ey P

rice

s a

nd E

xcha

nge

Rat

es 0

190

= 1

Exchange RateCPI

Currency

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money and Prices in the Long Run

How does a change in the money supply cause prices of output andinputs to change

Excess demand for goods and services a higher quantity ofmoney supplied implies that people have more funds available topay for goods and services

To meet high demand producers hire more workers creating astrong demand for labor services or make existing employeeswork harderWages rise to attract more workers or to compensate workers forovertimePrices of output will eventually rise to compensate for higher costsAlternatively for a fixed amount of output and inputs producerscan charge higher prices and still sell all of their output due to thehigh demand

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money and Prices in the Long Run (cont)

2 Inflationary expectations

If workers expect future prices to rise due to anexpected money supply increase they will want to becompensatedAnd if producers expect the same they are more willingto raise wagesProducers will be able to match higher costs if theyexpect to raise pricesResult expectations about inflation caused by anexpected increase in the money supply causes actualinflation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

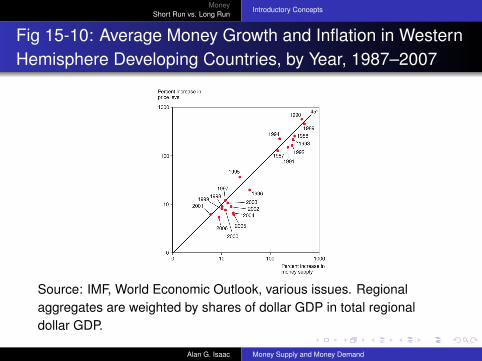

Fig 15-10 Average Money Growth and Inflation in WesternHemisphere Developing Countries by Year 1987ndash2007

Source IMF World Economic Outlook various issues Regionalaggregates are weighted by shares of dollar GDP in total regionaldollar GDP

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

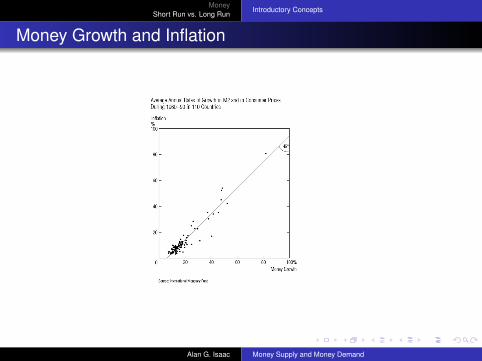

Money Growth and Inflation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of England

Governor and Company of the Bank of England

1694 established as a private institution granted a royal charter byWilliam III

1734 moved to Thread-needle Street

1931 policy making subordinated to the Treasury

1946 nationalized

1997 granted operational independence formalized in 1998 Bank ofEngland Act

Source httpwwwbankofenglandcoukabouthistoryindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

BoE Monetary Policy

Court of Directors Governor 2 Deputy Governors 9 Non-ExecutiveDirectors

Monetary Policy Committee chaired by BoE governor setsmonetary policy

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

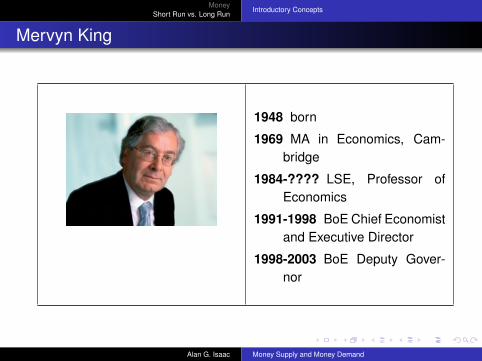

Mervyn King

1948 born

1969 MA in Economics Cam-bridge

1984- LSE Professor ofEconomics

1991-1998 BoE Chief Economistand Executive Director

1998-2003 BoE Deputy Gover-nor

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short-Run Effects of a Permanent Increase in the USMoney Supply

Combine two previous experiments

^ M (given Ee) drives down R producing a depreciation

^ Ee (given M) At each E the expected return on euro deposits risesbecause of Ee rises producing additional depreciation

Ee changes because the change in M is permanentNote Y remains exogenously fixed

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

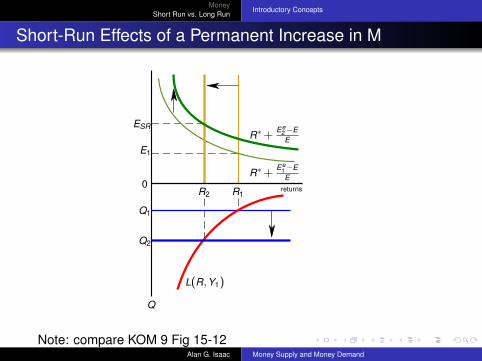

Short-Run Effects of a Permanent Increase in M

ESR

Q

L(RY1)

Q2

R20 returns

Rlowast+Ee

2 minusEE

Rlowast+Ee

1 minusEE

E1

R1

Q1

Note compare KOM 9 Fig 15-12Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long-Run Effects of a Permanent Increase in M

ESR

Q

L(RY1)

Q2

R20 returns

Rlowast+Ee

2 minusEEELR

RLR

QLR

Note compare KOM 9 Fig 15-12Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Overshooting

Permanent ^M a proportional ^E in LRBUT the dynamics involve a large iniitial depreciation and then asmaller subsequent appreciation

Permanent _M a proportional _E in LRBUT the dynamics involve a large iniitial appreciation and then asmaller subsequent depreciation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

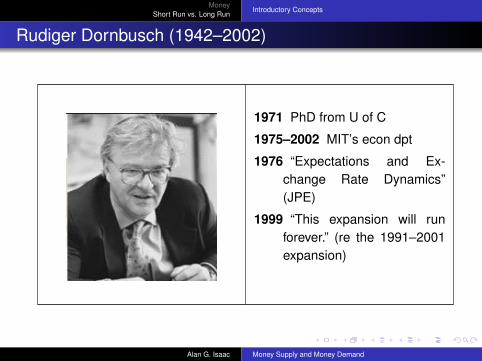

Rudiger Dornbusch (1942ndash2002)

1971 PhD from U of C

1975ndash2002 MITrsquos econ dpt

1976 ldquoExpectations and Ex-change Rate Dynamicsrdquo(JPE)

1999 ldquoThis expansion will runforeverrdquo (re the 1991ndash2001expansion)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

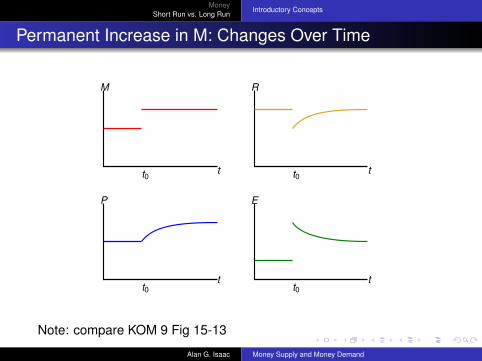

Permanent Increase in M Changes Over Time

t t

t

t0 t0

t0 t0

M

P E

R

t

Note compare KOM 9 Fig 15-13

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Exchange Rate Overshooting

We say that the exchange rate overshoots when its SR response to achange is greater than its LR response

Our model predicts exchange rate overshooting because M hasan immediate effect on R but not on P (nor expected inflation)

This overshooting prediction helps explain why exchange ratesare so volatile

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

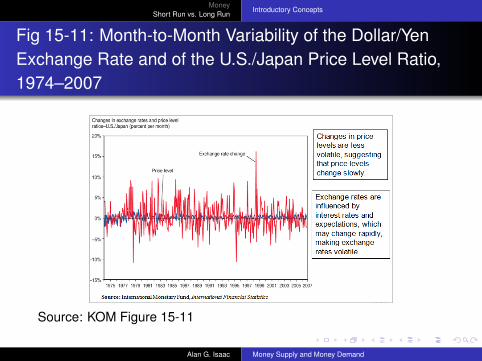

Fig 15-11 Month-to-Month Variability of the DollarYenExchange Rate and of the USJapan Price Level Ratio1974ndash2007

Source KOM Figure 15-11

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Preview

Defining money

Policy control of the money supply

Determinants of the demand for monetary assetsInterest rate determination

equilibrium in the money market

Exchange rate determination reduxLinking the money market and FX market

Long run effects of money supply changesprices interest rates and exchange rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money

Different groups of assets may be classified as money

Money assets that are commonly used as a means of paymentCurrency and checking accounts form a useful definition ofmoneyBank deposits in the foreign exchange market are excluded fromthis definition

M1 currency held by public + checkable depositshttpresearchstlouisfedorgfred2categories24

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

M1

Source httpresearchstlouisfedorgfred2seriesM1SLcid=25

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

Monetary authority the institution authorized to set monetary policymost often a central bank

A monetary authority can fairly directly control

the high-powered money stock

the interbank lending rate (eg Fed funds rate)

These policy actions determine ldquothe supply of moneyrdquo (eg M1)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fed Funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

US the Federal Open Market Committee (FOMC) of the FederalReserve System (the seven members of the Board of Governorsof the Federal Reserve System plus five Fed bank presidents)

EU monetary policy defined by the Governing Council (like theFOMC includes the Executive Board of the ECB which isanalogous to the Fedrsquos Board of Governors)httpwwwecbintecborgadecisionsgovchtmlindexenhtml

JP the Policy Board of the Bank of Japanhttpwwwbojorjpenaboutorganizationpolicyboardindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Ben Bernanke (14th Chair of the Fedrsquos BoG)

PhD from MIT 1979

Chair Princeton Econ Dpt1996 - 2002

Member Fed BoG 2002 - 2005

Chair CEA June 2005 - Jan2006

Chair BoG of Fed Feb 2006 -present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Masaaki Shirakawa (30th Governor Bank of Japan)

BA in Economics 1972 TheUniversity of Tokyo

MA in Economics 1977University of Chicago

Professor July 2006 KyotoUniversity School of Gov-ernment

Governor Bank of Japan Apr9 2008 - present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of Japan

Established 1882 the Bank of Japan Act of 1882

Reorganized 1942 Bank of Japan Act of 1942

1949 Policy Board established one of several amendments afterWorld War IIPB = highest decision-making body

Reorganized 1998 Bank of Japan Act of 1997principles independence and transparency

The BoJ has an explicit price stability goal in its bylaws

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

European Central Bank (ECB)

Figure ECB Logo

Responsible for euro area monetary policy since 1 January 1999Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Mario Draghi 3rd President of the ECB

PhD in Economics MIT 1976

University of FlorenceProfessor 1981 - 1991

World Bank Executive Director1984 - 1990

Italian Treasury Director Gen-eral 1991 - 2001

Goldman Sachs Vice-Presidentand Managing Director2002 - 2005

ECB President 2011 - present(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Jean-Claude Trichet 2nd President of the ECB

European Monetary CommitteeChair 1992-1993

Banque de France Governor1993 - 2003

ECB President 2003 - 2011(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Governing Council

ECB Governing Council

six members of the Executive Board plusgovernors of the national central banks of the 16 euro areacountriesthe main decision-making body of the ECB

The ECB GC formulates monetary policy for the euro areaThe ECB Governing Council usually meets twice a month at theEurotower in Frankfurt am Main Germany

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Deposit Rate

httpsdwecbeuropaeureportsdonode=100000131

httpenwikipediaorgwikiEurozoneInterest_rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rates over Time

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Eurosystem

historical noveltysupranational monetary unionEuro launched 1 Jan 1999Physical euros since 1 Jan 2002

European Central Bank (ECB)led by Governing Council

National central banks (NCBs)EU member states that have adopted the Euro

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Supply

money supply (M) the quantity of money that circulates in aneconomyM = C + Dcurrency help by public plus checkable deposits

monetary base (MB) currency held by public + reserves of banksMB = C + Rinfluences broader measures of the money supply

eg checkable deposits (including debit card accounts)

The monetary authority can roughly control the money supply

US monetary authority is a central banking system FederalReserve System

The Fed can directly regulate the monetary base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Money demand the amount of money individuals and businessesare willing to hold (instead of illiquid assets)

Real money demand (L) the amount of purchasing powerindividuals and businesses are willing to hold in the form ofmoney (instead of illiquid assets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Influences on the Demand for Money

1 Expected returns rates of returns on non-monetary assets(compared to monetary assets)monetary assets pay little or no interestthe interest rate on non-monetary assets is the opportunity costof holding monetary assets ^R _L

2 Riskthe risk of holding M is largely inflation risk which reduces thepurchasing power of moneybut other assets have this risk too so this risk is not veryimportant in defining the demand for monetary assets

3 LiquidityM is the most liquid asset it is the asset with the lowest cost ofturning it into other assets or commodities

4 Prices and income ^P - ^need for M ^Y - ^need for M

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Prices and Income

A higher level of average prices means a greater need for liquidityto buy the same amount of goods and services -gt highernominal demand for money

A higher real national income (GNP) means more goods andservices are being produced and bought in transactionsincreasing the need for liquidity -gt higher real demand for money

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Aggregate money demand

real L(RY)nominal P x L(RY)

where

P is the price levelY is real national incomeR is a measure of interest rates on non-monetary assets

Aggregate demand for real monetary assets is influenced by

transactions demand (national income)

opportunity cost (interest rates)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Real Money Demand and the Nominal Interest Rate

L(RY1)

QQ1

R

R1

^ R _ L (move along schedule)Note compare KOM Figure 15-1

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Real Money Supply and the Nominal Interest Rate

QQ1

R

The real money supply does not respond to R

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand = Money Supply in Equilibrium

L(RY1)

QQ1

R

R1

MP = L in equilibriumNote compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

The money market markets for trading monetary (very liquid) assetswhich are loosely called ldquomoneyrdquoInterest rates on monetary assets are low compared to interestrates on less liquid assets (such as bonds loans and deposits ofcurrency in the foreign exchange markets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

Money Market Equilibrium no shortages (excess demand) orsurpluses (excess supply) of monetary assets

In nominal terms M = P L(R Y)

In real terms MP = L(R Y)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rate Effect of Increase in Money Supply (given P)

L(RY1)

QQ1 Q2

R

R1

R2

^ M _ R (given P)Note compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in Income Shifts Money Demand Schedule

L(RY1)

L(RY2)

QQ2Q1

R

R1

^ income ^ L (at each R)Note compare KOM Figure 15-2

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rate Response to a Rise in Real Income

R

QQ1

L(RY1)

L(RY2)R1

R2

Given the price level an increase in Y raises L increasing theequilibrium interest rateNote compare KOM 9 Fig 15-5Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money MarketExchange Rate Linkages

Determines M(eg the Fed)

Domestic Central BankDetermines Mlowast

(eg the ECB)

Foreign Central Bank

Determines R(given M)

Domestic Money MarketDetermines Rlowast

(given Mlowast)

Foreign Money Market

Determines E(given R and Rlowast)

Foreign Exchange Market

Note compare KOM 9 Fig 15-7

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Simultaneous Equilibrium (Money Market and FX Market)

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

E

Note compare KOM 9 Fig 15-6Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in the Domestic Money Supply

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

R2

Q2

E2

E

Note compare KOM 9 Fig 15-8Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in the Foreign Money Supply (_ R)

1 ^ M _ R reducing the expected rate of return on eurodeposits

2 As FX mkt participants flee the EUR for the USD the EURdepreciates (Ie the USD appreciates)

How far Until expected rates of return are again equal3 Since the US sets its interest rate independently there is no

change in the US money market

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Expansionary Monetary Policy Abroad (_R)

E2

Q

L(RY1)

Q1

R10 returns

Rlowast2 +

EeminusEE

Rlowast1 +

EeminusEE

E1

E

Note compare KOM 9 Fig 15-9

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Impact Effect of ^ E^e

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+Ee

1 minusEE

Rlowast+Ee

2 minusEE

E2

E

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short Run vs Long Run

What is the long run Long enough for a change in the moneysupply to produce its full effect on the economy

Long-run neutrality of money In the long run a change in Mproduces a proportional change in all nominal stock variables(eg P E etc)In the long run a change in M does not change any real variables(eg MP EPP etc)

Long run monetary policy influences prices

Short run monetary policy influences interest rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Inflation in Zaire

1

10

100

1000

10000

100000

1e+006

1e+007

1e+008

1e+009

0190 0191 0192 0193 0194 0195 0196

Mon

ey P

rice

s a

nd E

xcha

nge

Rat

es 0

190

= 1

Exchange RateCPI

Currency

Source httpresearchstlouisfedorgfred2seriesEXUSEUcid=95

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run and Short Run

Up to now have have considered short-run analysisIn the long run prices of factors of production and of output havesufficient time to adjust to market conditions

Short Run

prices do not have enough time to adjust to marketconditions

Long Run

Wages adjust to equate the demand for and supply of laborReal output (income) is determined by the economyrsquosproductive capacitymdashfactor supplies (eg the supply oflabor) and technology (Not by the quantity of money)Real interest rates depend on the supply of saved funds anddemand for these funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run (cont)

Long-run prediction for ^M

no change in Yno change in (real) interest rateno change in L(RY) the aggregate demand for realmonetary assets L(RY)proportional ^P

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run (cont)

Equilibrium condition MP = L(RY)

now predicts that P adjusts proportionally when M changes

In the long run there is a direct relationship between the inflation rateand changes in the money supply

MP = L(RY )

P = ML(RY )

∆PP = ∆MM minus∆LL

The inflation rate is predicted to equal the growth rate in money supplyminus the growth rate in money demand

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Inflation in Zaire

1

10

100

1000

10000

100000

1e+006

1e+007

1e+008

1e+009

0190 0191 0192 0193 0194 0195 0196

Mon

ey P

rice

s a

nd E

xcha

nge

Rat

es 0

190

= 1

Exchange RateCPI

Currency

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money and Prices in the Long Run

How does a change in the money supply cause prices of output andinputs to change

Excess demand for goods and services a higher quantity ofmoney supplied implies that people have more funds available topay for goods and services

To meet high demand producers hire more workers creating astrong demand for labor services or make existing employeeswork harderWages rise to attract more workers or to compensate workers forovertimePrices of output will eventually rise to compensate for higher costsAlternatively for a fixed amount of output and inputs producerscan charge higher prices and still sell all of their output due to thehigh demand

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money and Prices in the Long Run (cont)

2 Inflationary expectations

If workers expect future prices to rise due to anexpected money supply increase they will want to becompensatedAnd if producers expect the same they are more willingto raise wagesProducers will be able to match higher costs if theyexpect to raise pricesResult expectations about inflation caused by anexpected increase in the money supply causes actualinflation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fig 15-10 Average Money Growth and Inflation in WesternHemisphere Developing Countries by Year 1987ndash2007

Source IMF World Economic Outlook various issues Regionalaggregates are weighted by shares of dollar GDP in total regionaldollar GDP

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Growth and Inflation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of England

Governor and Company of the Bank of England

1694 established as a private institution granted a royal charter byWilliam III

1734 moved to Thread-needle Street

1931 policy making subordinated to the Treasury

1946 nationalized

1997 granted operational independence formalized in 1998 Bank ofEngland Act

Source httpwwwbankofenglandcoukabouthistoryindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

BoE Monetary Policy

Court of Directors Governor 2 Deputy Governors 9 Non-ExecutiveDirectors

Monetary Policy Committee chaired by BoE governor setsmonetary policy

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Mervyn King

1948 born

1969 MA in Economics Cam-bridge

1984- LSE Professor ofEconomics

1991-1998 BoE Chief Economistand Executive Director

1998-2003 BoE Deputy Gover-nor

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short-Run Effects of a Permanent Increase in the USMoney Supply

Combine two previous experiments

^ M (given Ee) drives down R producing a depreciation

^ Ee (given M) At each E the expected return on euro deposits risesbecause of Ee rises producing additional depreciation

Ee changes because the change in M is permanentNote Y remains exogenously fixed

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short-Run Effects of a Permanent Increase in M

ESR

Q

L(RY1)

Q2

R20 returns

Rlowast+Ee

2 minusEE

Rlowast+Ee

1 minusEE

E1

R1

Q1

Note compare KOM 9 Fig 15-12Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long-Run Effects of a Permanent Increase in M

ESR

Q

L(RY1)

Q2

R20 returns

Rlowast+Ee

2 minusEEELR

RLR

QLR

Note compare KOM 9 Fig 15-12Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Overshooting

Permanent ^M a proportional ^E in LRBUT the dynamics involve a large iniitial depreciation and then asmaller subsequent appreciation

Permanent _M a proportional _E in LRBUT the dynamics involve a large iniitial appreciation and then asmaller subsequent depreciation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Rudiger Dornbusch (1942ndash2002)

1971 PhD from U of C

1975ndash2002 MITrsquos econ dpt

1976 ldquoExpectations and Ex-change Rate Dynamicsrdquo(JPE)

1999 ldquoThis expansion will runforeverrdquo (re the 1991ndash2001expansion)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Permanent Increase in M Changes Over Time

t t

t

t0 t0

t0 t0

M

P E

R

t

Note compare KOM 9 Fig 15-13

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Exchange Rate Overshooting

We say that the exchange rate overshoots when its SR response to achange is greater than its LR response

Our model predicts exchange rate overshooting because M hasan immediate effect on R but not on P (nor expected inflation)

This overshooting prediction helps explain why exchange ratesare so volatile

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fig 15-11 Month-to-Month Variability of the DollarYenExchange Rate and of the USJapan Price Level Ratio1974ndash2007

Source KOM Figure 15-11

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money

Different groups of assets may be classified as money

Money assets that are commonly used as a means of paymentCurrency and checking accounts form a useful definition ofmoneyBank deposits in the foreign exchange market are excluded fromthis definition

M1 currency held by public + checkable depositshttpresearchstlouisfedorgfred2categories24

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

M1

Source httpresearchstlouisfedorgfred2seriesM1SLcid=25

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

Monetary authority the institution authorized to set monetary policymost often a central bank

A monetary authority can fairly directly control

the high-powered money stock

the interbank lending rate (eg Fed funds rate)

These policy actions determine ldquothe supply of moneyrdquo (eg M1)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fed Funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

US the Federal Open Market Committee (FOMC) of the FederalReserve System (the seven members of the Board of Governorsof the Federal Reserve System plus five Fed bank presidents)

EU monetary policy defined by the Governing Council (like theFOMC includes the Executive Board of the ECB which isanalogous to the Fedrsquos Board of Governors)httpwwwecbintecborgadecisionsgovchtmlindexenhtml

JP the Policy Board of the Bank of Japanhttpwwwbojorjpenaboutorganizationpolicyboardindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Ben Bernanke (14th Chair of the Fedrsquos BoG)

PhD from MIT 1979

Chair Princeton Econ Dpt1996 - 2002

Member Fed BoG 2002 - 2005

Chair CEA June 2005 - Jan2006

Chair BoG of Fed Feb 2006 -present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Masaaki Shirakawa (30th Governor Bank of Japan)

BA in Economics 1972 TheUniversity of Tokyo

MA in Economics 1977University of Chicago

Professor July 2006 KyotoUniversity School of Gov-ernment

Governor Bank of Japan Apr9 2008 - present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of Japan

Established 1882 the Bank of Japan Act of 1882

Reorganized 1942 Bank of Japan Act of 1942

1949 Policy Board established one of several amendments afterWorld War IIPB = highest decision-making body

Reorganized 1998 Bank of Japan Act of 1997principles independence and transparency

The BoJ has an explicit price stability goal in its bylaws

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

European Central Bank (ECB)

Figure ECB Logo

Responsible for euro area monetary policy since 1 January 1999Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Mario Draghi 3rd President of the ECB

PhD in Economics MIT 1976

University of FlorenceProfessor 1981 - 1991

World Bank Executive Director1984 - 1990

Italian Treasury Director Gen-eral 1991 - 2001

Goldman Sachs Vice-Presidentand Managing Director2002 - 2005

ECB President 2011 - present(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Jean-Claude Trichet 2nd President of the ECB

European Monetary CommitteeChair 1992-1993

Banque de France Governor1993 - 2003

ECB President 2003 - 2011(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Governing Council

ECB Governing Council

six members of the Executive Board plusgovernors of the national central banks of the 16 euro areacountriesthe main decision-making body of the ECB

The ECB GC formulates monetary policy for the euro areaThe ECB Governing Council usually meets twice a month at theEurotower in Frankfurt am Main Germany

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Deposit Rate

httpsdwecbeuropaeureportsdonode=100000131

httpenwikipediaorgwikiEurozoneInterest_rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rates over Time

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Eurosystem

historical noveltysupranational monetary unionEuro launched 1 Jan 1999Physical euros since 1 Jan 2002

European Central Bank (ECB)led by Governing Council

National central banks (NCBs)EU member states that have adopted the Euro

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Supply

money supply (M) the quantity of money that circulates in aneconomyM = C + Dcurrency help by public plus checkable deposits

monetary base (MB) currency held by public + reserves of banksMB = C + Rinfluences broader measures of the money supply

eg checkable deposits (including debit card accounts)

The monetary authority can roughly control the money supply

US monetary authority is a central banking system FederalReserve System

The Fed can directly regulate the monetary base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Money demand the amount of money individuals and businessesare willing to hold (instead of illiquid assets)

Real money demand (L) the amount of purchasing powerindividuals and businesses are willing to hold in the form ofmoney (instead of illiquid assets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Influences on the Demand for Money

1 Expected returns rates of returns on non-monetary assets(compared to monetary assets)monetary assets pay little or no interestthe interest rate on non-monetary assets is the opportunity costof holding monetary assets ^R _L

2 Riskthe risk of holding M is largely inflation risk which reduces thepurchasing power of moneybut other assets have this risk too so this risk is not veryimportant in defining the demand for monetary assets

3 LiquidityM is the most liquid asset it is the asset with the lowest cost ofturning it into other assets or commodities

4 Prices and income ^P - ^need for M ^Y - ^need for M

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Prices and Income

A higher level of average prices means a greater need for liquidityto buy the same amount of goods and services -gt highernominal demand for money

A higher real national income (GNP) means more goods andservices are being produced and bought in transactionsincreasing the need for liquidity -gt higher real demand for money

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Aggregate money demand

real L(RY)nominal P x L(RY)

where

P is the price levelY is real national incomeR is a measure of interest rates on non-monetary assets

Aggregate demand for real monetary assets is influenced by

transactions demand (national income)

opportunity cost (interest rates)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Real Money Demand and the Nominal Interest Rate

L(RY1)

QQ1

R

R1

^ R _ L (move along schedule)Note compare KOM Figure 15-1

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Real Money Supply and the Nominal Interest Rate

QQ1

R

The real money supply does not respond to R

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand = Money Supply in Equilibrium

L(RY1)

QQ1

R

R1

MP = L in equilibriumNote compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

The money market markets for trading monetary (very liquid) assetswhich are loosely called ldquomoneyrdquoInterest rates on monetary assets are low compared to interestrates on less liquid assets (such as bonds loans and deposits ofcurrency in the foreign exchange markets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

Money Market Equilibrium no shortages (excess demand) orsurpluses (excess supply) of monetary assets

In nominal terms M = P L(R Y)

In real terms MP = L(R Y)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rate Effect of Increase in Money Supply (given P)

L(RY1)

QQ1 Q2

R

R1

R2

^ M _ R (given P)Note compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in Income Shifts Money Demand Schedule

L(RY1)

L(RY2)

QQ2Q1

R

R1

^ income ^ L (at each R)Note compare KOM Figure 15-2

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rate Response to a Rise in Real Income

R

QQ1

L(RY1)

L(RY2)R1

R2

Given the price level an increase in Y raises L increasing theequilibrium interest rateNote compare KOM 9 Fig 15-5Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money MarketExchange Rate Linkages

Determines M(eg the Fed)

Domestic Central BankDetermines Mlowast

(eg the ECB)

Foreign Central Bank

Determines R(given M)

Domestic Money MarketDetermines Rlowast

(given Mlowast)

Foreign Money Market

Determines E(given R and Rlowast)

Foreign Exchange Market

Note compare KOM 9 Fig 15-7

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Simultaneous Equilibrium (Money Market and FX Market)

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

E

Note compare KOM 9 Fig 15-6Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in the Domestic Money Supply

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

R2

Q2

E2

E

Note compare KOM 9 Fig 15-8Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in the Foreign Money Supply (_ R)

1 ^ M _ R reducing the expected rate of return on eurodeposits

2 As FX mkt participants flee the EUR for the USD the EURdepreciates (Ie the USD appreciates)

How far Until expected rates of return are again equal3 Since the US sets its interest rate independently there is no

change in the US money market

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Expansionary Monetary Policy Abroad (_R)

E2

Q

L(RY1)

Q1

R10 returns

Rlowast2 +

EeminusEE

Rlowast1 +

EeminusEE

E1

E

Note compare KOM 9 Fig 15-9

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Impact Effect of ^ E^e

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+Ee

1 minusEE

Rlowast+Ee

2 minusEE

E2

E

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short Run vs Long Run

What is the long run Long enough for a change in the moneysupply to produce its full effect on the economy

Long-run neutrality of money In the long run a change in Mproduces a proportional change in all nominal stock variables(eg P E etc)In the long run a change in M does not change any real variables(eg MP EPP etc)

Long run monetary policy influences prices

Short run monetary policy influences interest rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Inflation in Zaire

1

10

100

1000

10000

100000

1e+006

1e+007

1e+008

1e+009

0190 0191 0192 0193 0194 0195 0196

Mon

ey P

rice

s a

nd E

xcha

nge

Rat

es 0

190

= 1

Exchange RateCPI

Currency

Source httpresearchstlouisfedorgfred2seriesEXUSEUcid=95

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run and Short Run

Up to now have have considered short-run analysisIn the long run prices of factors of production and of output havesufficient time to adjust to market conditions

Short Run

prices do not have enough time to adjust to marketconditions

Long Run

Wages adjust to equate the demand for and supply of laborReal output (income) is determined by the economyrsquosproductive capacitymdashfactor supplies (eg the supply oflabor) and technology (Not by the quantity of money)Real interest rates depend on the supply of saved funds anddemand for these funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run (cont)

Long-run prediction for ^M

no change in Yno change in (real) interest rateno change in L(RY) the aggregate demand for realmonetary assets L(RY)proportional ^P

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long Run (cont)

Equilibrium condition MP = L(RY)

now predicts that P adjusts proportionally when M changes

In the long run there is a direct relationship between the inflation rateand changes in the money supply

MP = L(RY )

P = ML(RY )

∆PP = ∆MM minus∆LL

The inflation rate is predicted to equal the growth rate in money supplyminus the growth rate in money demand

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Inflation in Zaire

1

10

100

1000

10000

100000

1e+006

1e+007

1e+008

1e+009

0190 0191 0192 0193 0194 0195 0196

Mon

ey P

rice

s a

nd E

xcha

nge

Rat

es 0

190

= 1

Exchange RateCPI

Currency

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money and Prices in the Long Run

How does a change in the money supply cause prices of output andinputs to change

Excess demand for goods and services a higher quantity ofmoney supplied implies that people have more funds available topay for goods and services

To meet high demand producers hire more workers creating astrong demand for labor services or make existing employeeswork harderWages rise to attract more workers or to compensate workers forovertimePrices of output will eventually rise to compensate for higher costsAlternatively for a fixed amount of output and inputs producerscan charge higher prices and still sell all of their output due to thehigh demand

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money and Prices in the Long Run (cont)

2 Inflationary expectations

If workers expect future prices to rise due to anexpected money supply increase they will want to becompensatedAnd if producers expect the same they are more willingto raise wagesProducers will be able to match higher costs if theyexpect to raise pricesResult expectations about inflation caused by anexpected increase in the money supply causes actualinflation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fig 15-10 Average Money Growth and Inflation in WesternHemisphere Developing Countries by Year 1987ndash2007

Source IMF World Economic Outlook various issues Regionalaggregates are weighted by shares of dollar GDP in total regionaldollar GDP

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Growth and Inflation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of England

Governor and Company of the Bank of England

1694 established as a private institution granted a royal charter byWilliam III

1734 moved to Thread-needle Street

1931 policy making subordinated to the Treasury

1946 nationalized

1997 granted operational independence formalized in 1998 Bank ofEngland Act

Source httpwwwbankofenglandcoukabouthistoryindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

BoE Monetary Policy

Court of Directors Governor 2 Deputy Governors 9 Non-ExecutiveDirectors

Monetary Policy Committee chaired by BoE governor setsmonetary policy

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Mervyn King

1948 born

1969 MA in Economics Cam-bridge

1984- LSE Professor ofEconomics

1991-1998 BoE Chief Economistand Executive Director

1998-2003 BoE Deputy Gover-nor

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short-Run Effects of a Permanent Increase in the USMoney Supply

Combine two previous experiments

^ M (given Ee) drives down R producing a depreciation

^ Ee (given M) At each E the expected return on euro deposits risesbecause of Ee rises producing additional depreciation

Ee changes because the change in M is permanentNote Y remains exogenously fixed

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short-Run Effects of a Permanent Increase in M

ESR

Q

L(RY1)

Q2

R20 returns

Rlowast+Ee

2 minusEE

Rlowast+Ee

1 minusEE

E1

R1

Q1

Note compare KOM 9 Fig 15-12Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Long-Run Effects of a Permanent Increase in M

ESR

Q

L(RY1)

Q2

R20 returns

Rlowast+Ee

2 minusEEELR

RLR

QLR

Note compare KOM 9 Fig 15-12Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Overshooting

Permanent ^M a proportional ^E in LRBUT the dynamics involve a large iniitial depreciation and then asmaller subsequent appreciation

Permanent _M a proportional _E in LRBUT the dynamics involve a large iniitial appreciation and then asmaller subsequent depreciation

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Rudiger Dornbusch (1942ndash2002)

1971 PhD from U of C

1975ndash2002 MITrsquos econ dpt

1976 ldquoExpectations and Ex-change Rate Dynamicsrdquo(JPE)

1999 ldquoThis expansion will runforeverrdquo (re the 1991ndash2001expansion)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Permanent Increase in M Changes Over Time

t t

t

t0 t0

t0 t0

M

P E

R

t

Note compare KOM 9 Fig 15-13

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Exchange Rate Overshooting

We say that the exchange rate overshoots when its SR response to achange is greater than its LR response

Our model predicts exchange rate overshooting because M hasan immediate effect on R but not on P (nor expected inflation)

This overshooting prediction helps explain why exchange ratesare so volatile

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fig 15-11 Month-to-Month Variability of the DollarYenExchange Rate and of the USJapan Price Level Ratio1974ndash2007

Source KOM Figure 15-11

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

M1

Source httpresearchstlouisfedorgfred2seriesM1SLcid=25

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

Monetary authority the institution authorized to set monetary policymost often a central bank

A monetary authority can fairly directly control

the high-powered money stock

the interbank lending rate (eg Fed funds rate)

These policy actions determine ldquothe supply of moneyrdquo (eg M1)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Fed Funds

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Monetary Authority

US the Federal Open Market Committee (FOMC) of the FederalReserve System (the seven members of the Board of Governorsof the Federal Reserve System plus five Fed bank presidents)

EU monetary policy defined by the Governing Council (like theFOMC includes the Executive Board of the ECB which isanalogous to the Fedrsquos Board of Governors)httpwwwecbintecborgadecisionsgovchtmlindexenhtml

JP the Policy Board of the Bank of Japanhttpwwwbojorjpenaboutorganizationpolicyboardindexhtm

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Ben Bernanke (14th Chair of the Fedrsquos BoG)

PhD from MIT 1979

Chair Princeton Econ Dpt1996 - 2002

Member Fed BoG 2002 - 2005

Chair CEA June 2005 - Jan2006

Chair BoG of Fed Feb 2006 -present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Masaaki Shirakawa (30th Governor Bank of Japan)

BA in Economics 1972 TheUniversity of Tokyo

MA in Economics 1977University of Chicago

Professor July 2006 KyotoUniversity School of Gov-ernment

Governor Bank of Japan Apr9 2008 - present

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Bank of Japan

Established 1882 the Bank of Japan Act of 1882

Reorganized 1942 Bank of Japan Act of 1942

1949 Policy Board established one of several amendments afterWorld War IIPB = highest decision-making body

Reorganized 1998 Bank of Japan Act of 1997principles independence and transparency

The BoJ has an explicit price stability goal in its bylaws

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

European Central Bank (ECB)

Figure ECB Logo

Responsible for euro area monetary policy since 1 January 1999Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Mario Draghi 3rd President of the ECB

PhD in Economics MIT 1976

University of FlorenceProfessor 1981 - 1991

World Bank Executive Director1984 - 1990

Italian Treasury Director Gen-eral 1991 - 2001

Goldman Sachs Vice-Presidentand Managing Director2002 - 2005

ECB President 2011 - present(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Jean-Claude Trichet 2nd President of the ECB

European Monetary CommitteeChair 1992-1993

Banque de France Governor1993 - 2003

ECB President 2003 - 2011(also Chair of 10 Gover-nors)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Governing Council

ECB Governing Council

six members of the Executive Board plusgovernors of the national central banks of the 16 euro areacountriesthe main decision-making body of the ECB

The ECB GC formulates monetary policy for the euro areaThe ECB Governing Council usually meets twice a month at theEurotower in Frankfurt am Main Germany

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

ECB Deposit Rate

httpsdwecbeuropaeureportsdonode=100000131

httpenwikipediaorgwikiEurozoneInterest_rates

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rates over Time

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Eurosystem

historical noveltysupranational monetary unionEuro launched 1 Jan 1999Physical euros since 1 Jan 2002

European Central Bank (ECB)led by Governing Council

National central banks (NCBs)EU member states that have adopted the Euro

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Supply

money supply (M) the quantity of money that circulates in aneconomyM = C + Dcurrency help by public plus checkable deposits

monetary base (MB) currency held by public + reserves of banksMB = C + Rinfluences broader measures of the money supply

eg checkable deposits (including debit card accounts)

The monetary authority can roughly control the money supply

US monetary authority is a central banking system FederalReserve System

The Fed can directly regulate the monetary base

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Money demand the amount of money individuals and businessesare willing to hold (instead of illiquid assets)

Real money demand (L) the amount of purchasing powerindividuals and businesses are willing to hold in the form ofmoney (instead of illiquid assets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Influences on the Demand for Money

1 Expected returns rates of returns on non-monetary assets(compared to monetary assets)monetary assets pay little or no interestthe interest rate on non-monetary assets is the opportunity costof holding monetary assets ^R _L

2 Riskthe risk of holding M is largely inflation risk which reduces thepurchasing power of moneybut other assets have this risk too so this risk is not veryimportant in defining the demand for monetary assets

3 LiquidityM is the most liquid asset it is the asset with the lowest cost ofturning it into other assets or commodities

4 Prices and income ^P - ^need for M ^Y - ^need for M

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Prices and Income

A higher level of average prices means a greater need for liquidityto buy the same amount of goods and services -gt highernominal demand for money

A higher real national income (GNP) means more goods andservices are being produced and bought in transactionsincreasing the need for liquidity -gt higher real demand for money

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand

Aggregate money demand

real L(RY)nominal P x L(RY)

where

P is the price levelY is real national incomeR is a measure of interest rates on non-monetary assets

Aggregate demand for real monetary assets is influenced by

transactions demand (national income)

opportunity cost (interest rates)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Real Money Demand and the Nominal Interest Rate

L(RY1)

QQ1

R

R1

^ R _ L (move along schedule)Note compare KOM Figure 15-1

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Real Money Supply and the Nominal Interest Rate

QQ1

R

The real money supply does not respond to R

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money Demand = Money Supply in Equilibrium

L(RY1)

QQ1

R

R1

MP = L in equilibriumNote compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

The money market markets for trading monetary (very liquid) assetswhich are loosely called ldquomoneyrdquoInterest rates on monetary assets are low compared to interestrates on less liquid assets (such as bonds loans and deposits ofcurrency in the foreign exchange markets)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

A Model of the Money Market

Money Market Equilibrium no shortages (excess demand) orsurpluses (excess supply) of monetary assets

In nominal terms M = P L(R Y)

In real terms MP = L(R Y)

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rate Effect of Increase in Money Supply (given P)

L(RY1)

QQ1 Q2

R

R1

R2

^ M _ R (given P)Note compare KOM Figure 15-3

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in Income Shifts Money Demand Schedule

L(RY1)

L(RY2)

QQ2Q1

R

R1

^ income ^ L (at each R)Note compare KOM Figure 15-2

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Interest Rate Response to a Rise in Real Income

R

QQ1

L(RY1)

L(RY2)R1

R2

Given the price level an increase in Y raises L increasing theequilibrium interest rateNote compare KOM 9 Fig 15-5Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Money MarketExchange Rate Linkages

Determines M(eg the Fed)

Domestic Central BankDetermines Mlowast

(eg the ECB)

Foreign Central Bank

Determines R(given M)

Domestic Money MarketDetermines Rlowast

(given Mlowast)

Foreign Money Market

Determines E(given R and Rlowast)

Foreign Exchange Market

Note compare KOM 9 Fig 15-7

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Simultaneous Equilibrium (Money Market and FX Market)

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

E

Note compare KOM 9 Fig 15-6Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in the Domestic Money Supply

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+ EeminusEE

R2

Q2

E2

E

Note compare KOM 9 Fig 15-8Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Increase in the Foreign Money Supply (_ R)

1 ^ M _ R reducing the expected rate of return on eurodeposits

2 As FX mkt participants flee the EUR for the USD the EURdepreciates (Ie the USD appreciates)

How far Until expected rates of return are again equal3 Since the US sets its interest rate independently there is no

change in the US money market

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Expansionary Monetary Policy Abroad (_R)

E2

Q

L(RY1)

Q1

R10 returns

Rlowast2 +

EeminusEE

Rlowast1 +

EeminusEE

E1

E

Note compare KOM 9 Fig 15-9

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Impact Effect of ^ E^e

E1

Q

L(RY1)

Q1

R10 returns

Rlowast+Ee

1 minusEE

Rlowast+Ee

2 minusEE

E2

E

Alan G Isaac Money Supply and Money Demand

MoneyShort Run vs Long Run

Introductory Concepts

Short Run vs Long Run

What is the long run Long enough for a change in the moneysupply to produce its full effect on the economy

Long-run neutrality of money In the long run a change in Mproduces a proportional change in all nominal stock variables(eg P E etc)In the long run a change in M does not change any real variables(eg MP EPP etc)

Long run monetary policy influences prices