Embed Size (px)

Citation preview

More Options, More Opportunities

CWB Organic Program

More Options, More Opportunities

Options for Marketing Organic

Wheat and Barley• Sell to an organic company that is a

handler of the CWB (they do the CWB transaction)

• Do a Producer Direct Sale (PDS) and sell to a broker, company, or processor– How to do the PDS; Why the PDS

• Marketing tools:– Producer payment options; Forward sales

More Options, More Opportunities

Selling to Companies that areagents of the CWB

• Saskatchewan Wheat Pool

• Growers International Organic Sales Inc.

• Prairie Flour Mill, Elie, MB– Compare prices; verify CWB initial and final

payments. Research other market opportunities

– ADV: reliability, track record, ease of marketing

More Options, More Opportunities

Producer Direct Selling• Producer contacts potential buyers;

before making sale verifies CWB PDS price– Obtain lists of sellers from SOD, certification

bodies, CWB– Attend trade shows: Natural Products Expo

East and West, Anaheim and Baltimore; Organic Trade Association, All Things Organic, Austin, TX; Biofach Germany; Biofach Japan

More Options, More Opportunities

Producer Direct Selling

• The CWB Producer Direct Sale:– Producer can market own grain by paying the

spread between the daily cash market price (conventional) and the CWB initial; producer then gets interim and final payments

– ie, CWB sells the grain to the farmer at the market price (conventional), farmer receives the pool price.

– Farmer guaranteed pool price plus the organic premium privately negotiated

More Options, More Opportunities

Producer Direct Selling

• PDS is designed to maintain market price structure at highest possible level– Trend towards increased niche marketing

makes floor price important to maintain price structure created and maintained by single desk selling for conventional grain• PFP, variety specific, identity preserve

– Organic returns benefit from higher conventional values

More Options, More Opportunities

How to do a PDS• Call 1-800-ASK-4-CWB; ask for organic

marketing manager

• Need permit book and PIN number

• Sale conducted over phone

• Producer faxes us:– export licence application form, final weights

• We fax sales confirmation, mail formal contract

• Shipment period is 30 days

More Options, More Opportunities

Forward Sales

• You can do a Producer Direct Sale for future delivery (beyond 30 days). The price will be based on the futures markets.

• Advisable only when you have a contracted sale, as delivery must take place or liquidated damages will be assessed

More Options, More Opportunities

PDSExample: 03 Feb 03 #1CWRS13.5 U.S.

Organic price: 367/mt 10.00/bu

PDS price: 265 7.21

Initial: 250 6.80

Up-front spread: 15 0.41

PRO: 274 7.46

Interim paymts 24 0.66

Net spread: ($9/mt) ($0.25/bu)

Farmer net return $358/mt $9.75/mt

More Options, More Opportunities

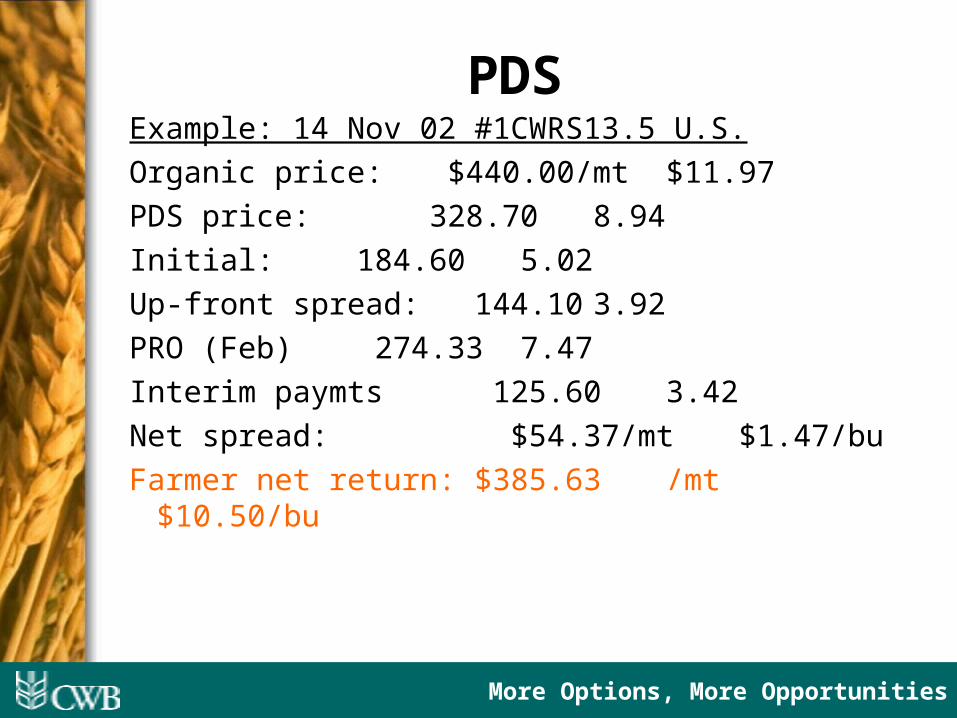

PDSExample: 14 Nov 02 #1CWRS13.5 U.S.

Organic price: $440.00/mt $11.97

PDS price: 328.70 8.94

Initial: 184.60 5.02

Up-front spread: 144.10 3.92

PRO (Feb) 274.33 7.47

Interim paymts 125.60 3.42

Net spread: $54.37/mt $1.47/bu

Farmer net return: $385.63 /mt $10.50/bu

More Options, More Opportunities

Regulations

• If a company is not a handler of the CWB, the farmer is responsible to do the PDS

• All grain sold must go through the PDS

• The farmer should do the PDS when selling to Ontario or Quebec, as well as when exporting

• Both companies and producers can be fined for marketing outside the PDS system

More Options, More Opportunities

Marketing Tools:Using Pricing Options

• Lock in a Fixed Price or

• Lock in a Basis (Spread between the CWB price--based on PRO--and the Futures Price for a specific month) then lock in a Futures Price later

Then sell to a grain company or do a PDS.

You will be paid either 2 weeks after delivery, or 2 weeks after you settle the price if already delivered.

More Options, More Opportunities

Fixed Price and Basis Options

• FPC creates certainty, pays out quickly

• Basis option allows to fix own price independent of delivery time; more flexibility

• You must deliver the grain (make a sale) before the end of the crop year--can’t carry over without liquidated damages

More Options, More Opportunities

Cash Advance Program

• You can take out a cash advance as an organic producer

• You must pay back the cash advance as you make organic deliveries; $85/mt for wheat.

More Options, More Opportunities

CWB Delivery Contracts

• As an organic producer, you do not need to sign up in advance for delivery contracts unless you plan to sell into the conventional market

• You can sign up all your tonnage; if you will not deliver the organic by end of year, call the CWB and ask for the Organic Marketing Manager, to decrease your contract

More Options, More Opportunities

U.S. Trade Action

• US. Dept. of Commerce is conducting anti-dumping/countervailing duties investigations into Canadian exports of wheat and durum

• Preliminary Determination set at Mar.3/03; potential for tariffs retroactive to Dec.3/03

• Exporters are responsible for any tariffs; petition has been for wheat tariff at 37%, durum 25%

More Options, More Opportunities

Marketing Tips

– Do market research; know what buyers are looking for and compare prices

– Grow top quality, right variety– Grow a load (or partner up)– For specialty crops, get a forward contract– Take representative samples, label well– Get the right certification– Is buyer licenced and bonded? Get references

and letter of credit; get contract; take time to negotiate

– Use Bills of lading; clean trucks

More Options, More Opportunities

Marketing Tips (cont’d)• Contracts: Get it in writing!

• Signed Purchase Order or Sales Contract

• State the product, grade, quality, percentage of FM or any other factors; Price

• Shipping date and means; From where

• Who pays costs: freight, cleaning, bagging, loading What will happen to screenings - ownership price etc.

• Payment schedule: before loading, at unload, 10 days, etc. and interest charges

• Who does the CWB buyback (PDS)?

• Who decides if product specifications are met?

• Method for resolving disagreements on grades, dockage, etc. CGC, independent lab

More Options, More Opportunities

Organic Production in Canada

• 2,500 farms, 150 organic processors

• 1,500 farms on Prairies

• Yr 2000: 117,000 acres wheat, 18,000 acres barley; total tonnage est. 110,600 Western Canada

• 2000: 140,000 mt of grains and oilseeds, valued at $400-$500 million

More Options, More Opportunities

Retail Market for Organic Foods in Canada

• $300-$750 million

• 80% of products imported

• Organic is 1% of total retail food sales

• Growth rate: 15% per year(Source: AAFC)

• Largest markets Vancouver, Calgary, Toronto, Montreal

• Capers (Wild Oats), Whole Foods; Loblaws brands, IGA, Safeway

More Options, More Opportunities

Canadian Organic Grain Movement

• Export Destinations: CWB sales 2001-2002Volume Sales by Destination MT % OF TOTAL

TOTAL CANADA 13 046 28

TOTAL US 9 008 19

TOTAL EU 24 250 52

TOTAL JAPAN 508 1

TOTAL 46 812

– Overseas movement mainly by container; two bulk shipments to UK 2001-2002

– Truck and rail to U.S.– Four organic elevators, GIOSI, SWP

More Options, More Opportunities

Growth Rates of Organic Sales• 2001: EU Organic food market grew 33%

(Organic Monitor)– cf conventional grocery sales growing at 3-5%

• Organic sales in 7 EU states and U.S. projected to double by 2006

• Average annual growth rates 15-25%; growth rates of manufactured food, 36%

• Fastest growing markets Germany, Italy, France, and UK

More Options, More Opportunities

2001 Organic Market Canada:Value $650 Million

Organic Market

Dairy10%

Breads & Grains14%

Beverages17%

Snack Foods3%

Condiments2%

Fruit & vegetables

41%

Packaged/Prepared Foods

12%

Meat, fish, poultry

1%

Source: Nutrition Business Journal

More Options, More Opportunities

2001 Natural Market Canada: Value $1.4 Billion

Natural & Organic Market

Dairy10%

Snack Foods5%

Condiments4%

Meat, fish, poultry

5%

Packaged/Prepared Foods

17%

Beverages19%

Breads & Grains18%

Fruit & vegetables

22%

Source: Nutrition Business Journal

More Options, More Opportunities

Total Food Market: Value $61 Billion

Total Food Market

Dairy11%

Beverages18%

Condiments4%

Meat, fish, poultry

21%Fruit & vegetables

17%

Packaged/Prepared Foods

11%Snack Foods

6%

Breads & Grains12%

Source: Nutrition Business Journal

More Options, More Opportunities

Top Growth Categories for Organics (OTA Survey)

Category 1999-2000 2000-2001Soy foods and other proteinalternatives

215% 94%

Meat, eggs, and poultry 64% 59%Canned/jarred products 51% 45%Dairy 40% 41%

Growth Rates for Grain Based FoodsCategory 1996-2000 1999-2000 2001 - 2006

Baking mixes/sweeteners 10% 13% 11%Grain products 14% 14% 18%Grain snacks and Candy 16% 14% 18%

Compound Annual Growth Rate of Organic Bakery and Cereal

0%

10%

20%

30%

40%

50%

60%

Germany France UK Netherlands Sweden U.S. Overall

Per

cen

tag

e g

row

th r

ate

2000 CAGR

2005 CAGR

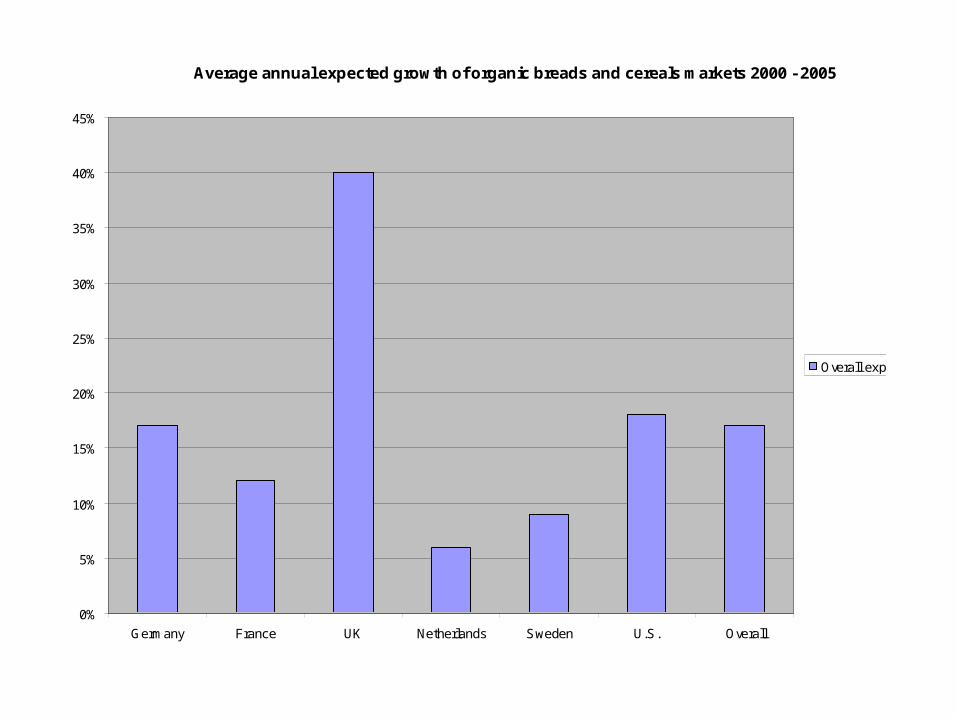

Average annual expected growth of organic breads and cereals markets 2000 - 2005

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Germany France UK Netherlands Sweden U.S. Overall

Overall expected growth

Organic Breads and Cereals as % of All Organic Categories

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

Germany France UK Netherlands Sweden U.S. Overall

% o

f o

rgan

ic c

ateg

ory

% of total 2000

% of total 2005

Change in bread category share of organic

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Germany France UK Netherlands Sweden U.S. Overall

Organic Bakery and Cereals sales 1995-2000

0

100

200

300

400

500

600

700

800

Germany France UK Netherlands Sweden U.S.

US

$ m

illio

ns

1995

1996

1997

1998

1999

2000

More Options, More Opportunities

Growth rates of conventional bread categories

– Overall bread consumption: +2.6%– White Bread -3%– Premium Bread +1.7%– Superpremium Bread +8%

– Conventional whole grains loaves, products that emphasize better health and nutrition, and higher priced artisan breads are leading in growth rates in conventional categories.

More Options, More Opportunities

Growth rates in non-organic wheat flour and

durum– Reports on conventional white and whole

wheat flour and durum consumption in the U.S. show no growth or decline, so by comparison, growth rates of organic grains categories are positive.

– In the U.S., per capita flour consumption in 2001 was 143 lbs, down from 146 lbs in 2000, and the lowes since 143 lbs in 1999.

– Overall pasta consumption in Canada is flat, and has declined in the U.S. in the last two years.

More Options, More Opportunities

The Big Players

• General Mills - Small Planet Foods, Cascadian Farm Brand, Muir Glen, Sunrise Cereal

– Organic Cheerios- “Honey Nut-Os”

• Kraft - Boca brand

• Heinz- Hain Celestial; Health Valley; Earth’s Best Baby Food; Garden of Eatin potato chips

• PepsiCo’s Quaker Oats - Mother’s Organic cereal

• Coca-Cola - Odwalla natural juice

• Kellogg Co - Kashi Co

• Mars - Seeds of Change

• ConAgra Food Ingredients - Gilroy Foods

• Chiquita; Gerber

More Options, More Opportunities

Outlook• Demand for organic foods expected to

continue to grow; many countries target 10% of total food production

• Organic movement struggling with “mainstreaming”; premiums an issue; local versus global--high energy costs of transporting food seen as unsustainable

• Organic values have had impact on conventional agriculture; research devoted to sustainability, government support

More Options, More Opportunities

Outlook

• Canadian exports threatened by Eastern Europe, China, Argentina, and “buy local” campaigns

• Organic wheat and barley consumption growing; highest rate of growth in bread/pasta categories

• Opportunities for new grain-based organic products (health bars, baby cereals, breakfast cereals, pizza, tortillas, noodles)