Embed Size (px)

Citation preview

Information Classification: General

JAMES MONTIER

PARTNER AND SENIOR ASSET ALLOCATION STRATEGIST

GMO

MORNING KEYNOTE: LATE CYCLE LAMENT

Information Classification: General

LATE CYCLE LAMENT

James Montier

Information Classification: General

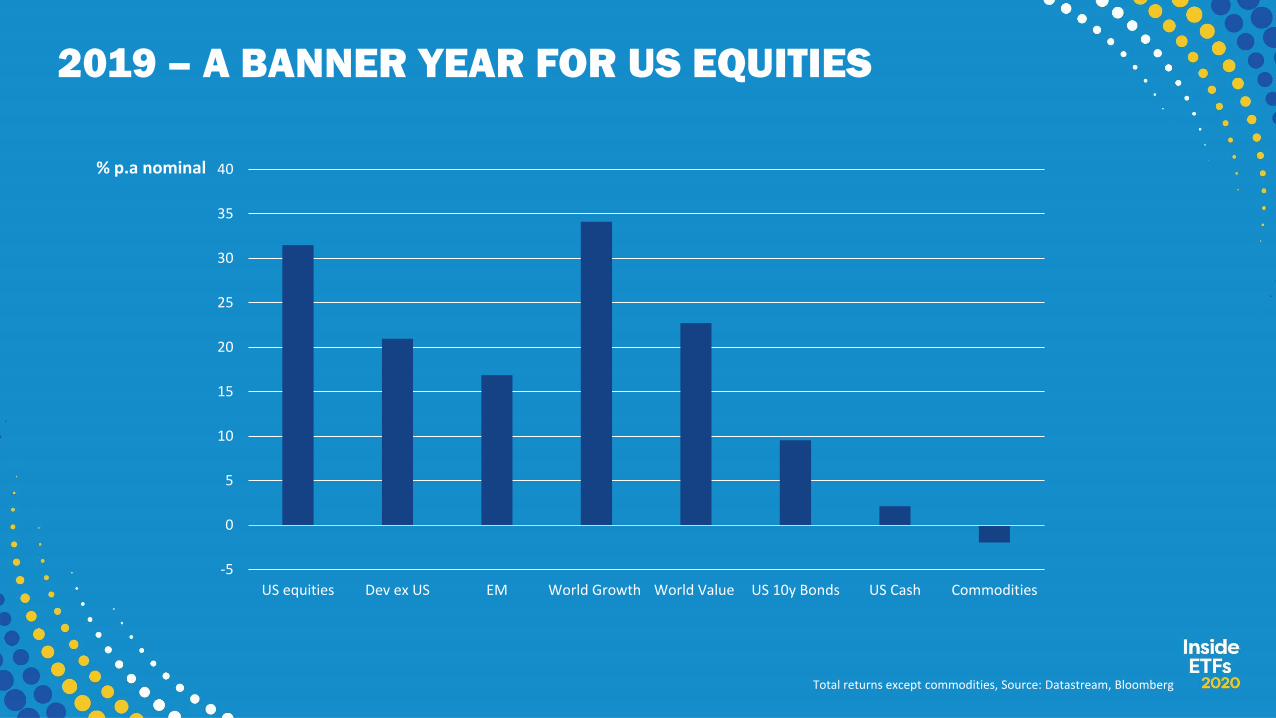

2019 – A BANNER YEAR FOR US EQUITIES

-5

0

5

10

15

20

25

30

35

40

US equities Dev ex US EM World Growth World Value US 10y Bonds US Cash Commodities

% p.a nominal

Total returns except commodities, Source: Datastream, Bloomberg

Information Classification: General

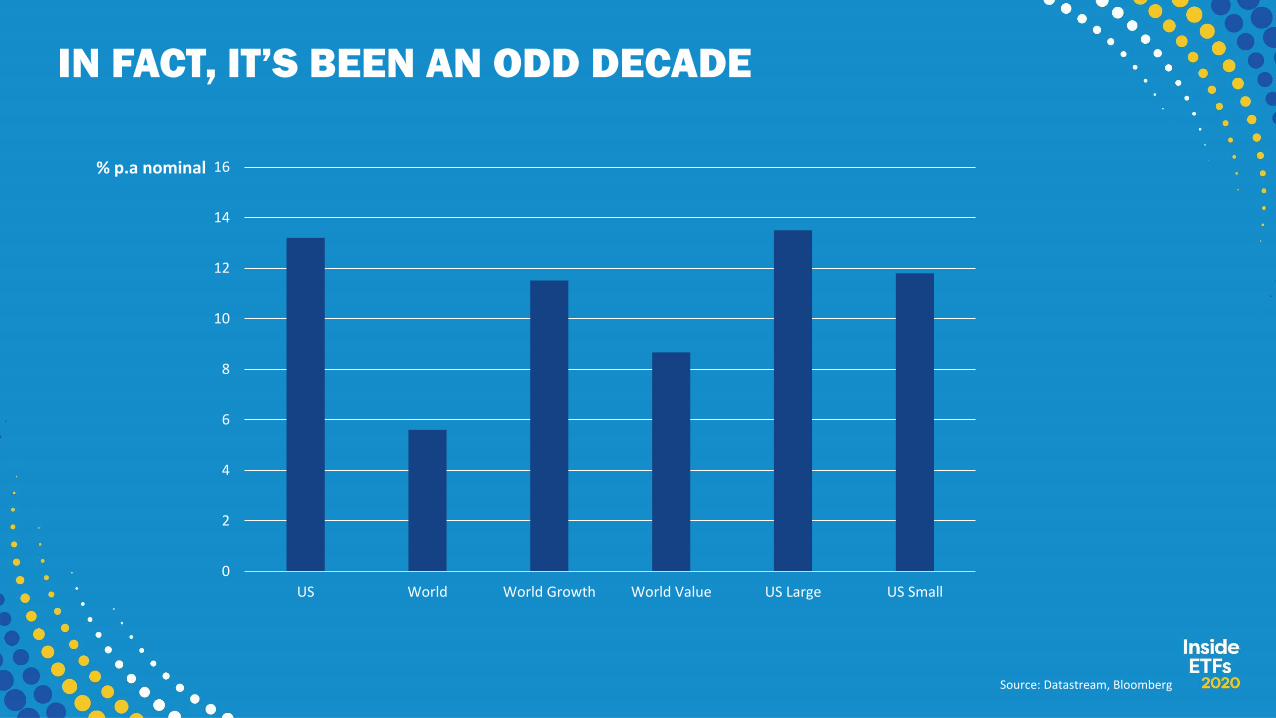

IN FACT, IT’S BEEN AN ODD DECADE

% p.a nominal

Source: Datastream, Bloomberg

0

2

4

6

8

10

12

14

16

US World World Growth World Value US Large US Small

Information Classification: General

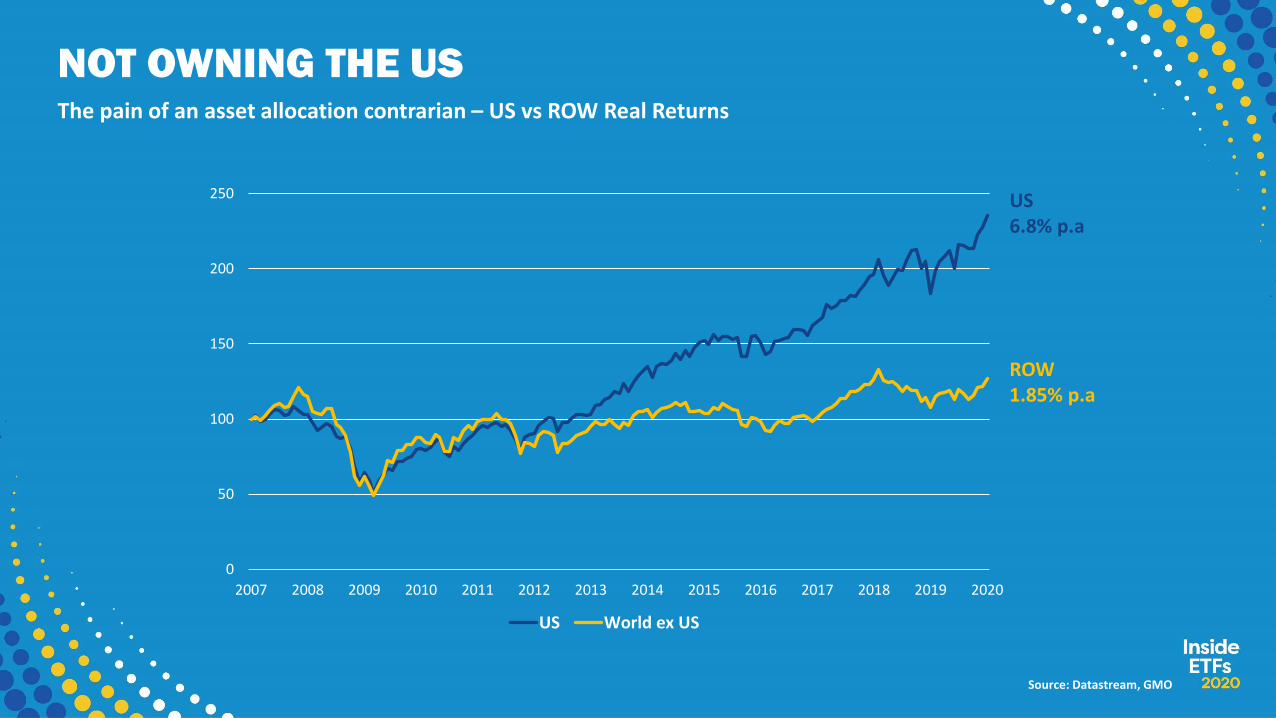

NOT OWNING THE USThe pain of an asset allocation contrarian – US vs ROW Real Returns

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

US World ex US

Source: Datastream, GMO

US6.8% p.a

ROW1.85% p.a

Information Classification: General

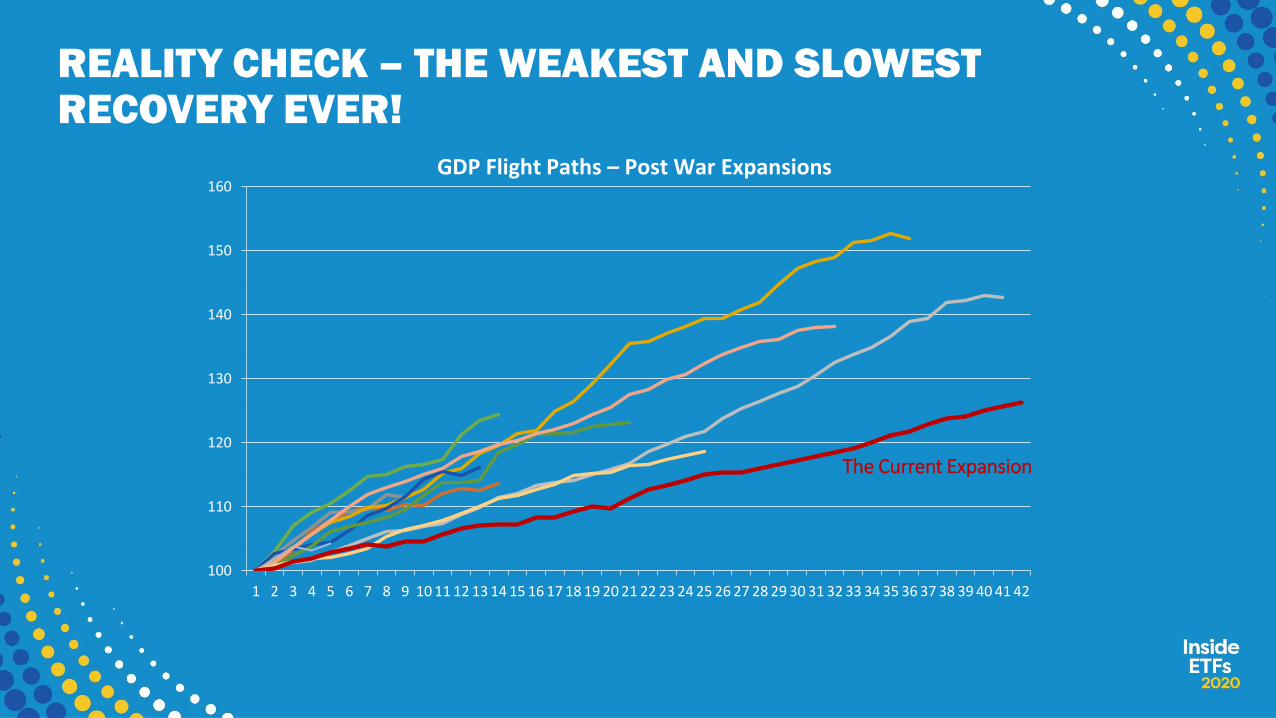

REALITY CHECK – THE WEAKEST AND SLOWEST RECOVERY EVER!

100

110

120

130

140

150

160

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42

The Current Expansion

GDP Flight Paths – Post War Expansions

Information Classification: General

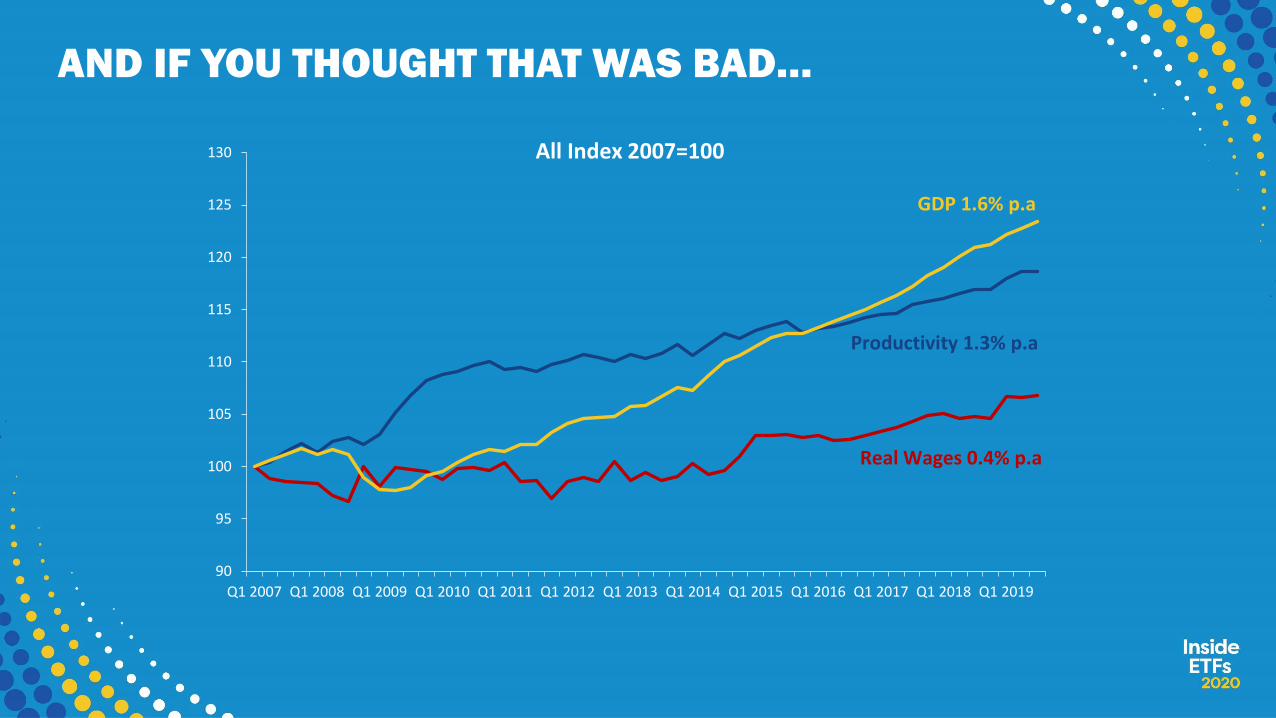

AND IF YOU THOUGHT THAT WAS BAD…

90

95

100

105

110

115

120

125

130

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018 Q1 2019

GDP 1.6% p.a

Productivity 1.3% p.a

Real Wages 0.4% p.a

All Index 2007=100

Information Classification: General

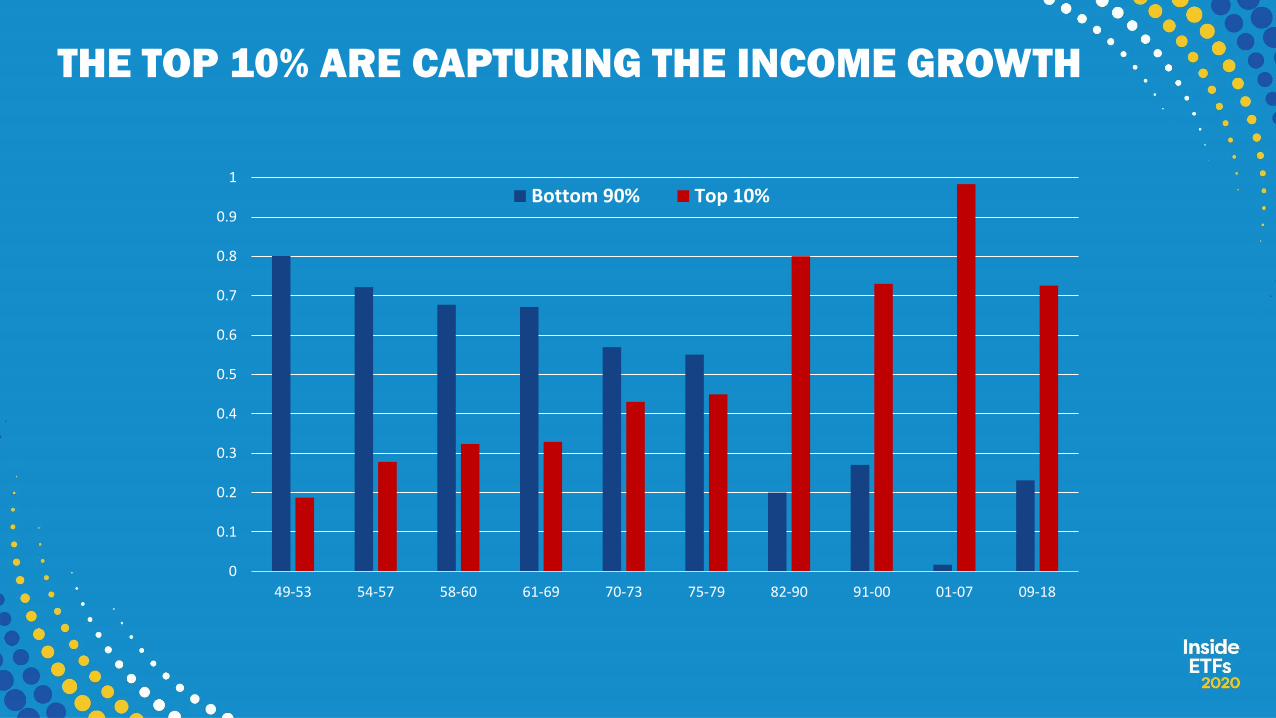

THE TOP 10% ARE CAPTURING THE INCOME GROWTH

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

49-53 54-57 58-60 61-69 70-73 75-79 82-90 91-00 01-07 09-18

Bottom 90% Top 10%

Information Classification: General

BUT SURELY EPS IS JUST FINE…

0

20

40

60

80

100

120

140

160

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018 Q1 2019

Real GDP (1.6% p.a)

Real Agg Earnings (1.3% p.a)

Real EPS (2.14% p.a)

Indexed Q1 2007 = 100

Information Classification: General

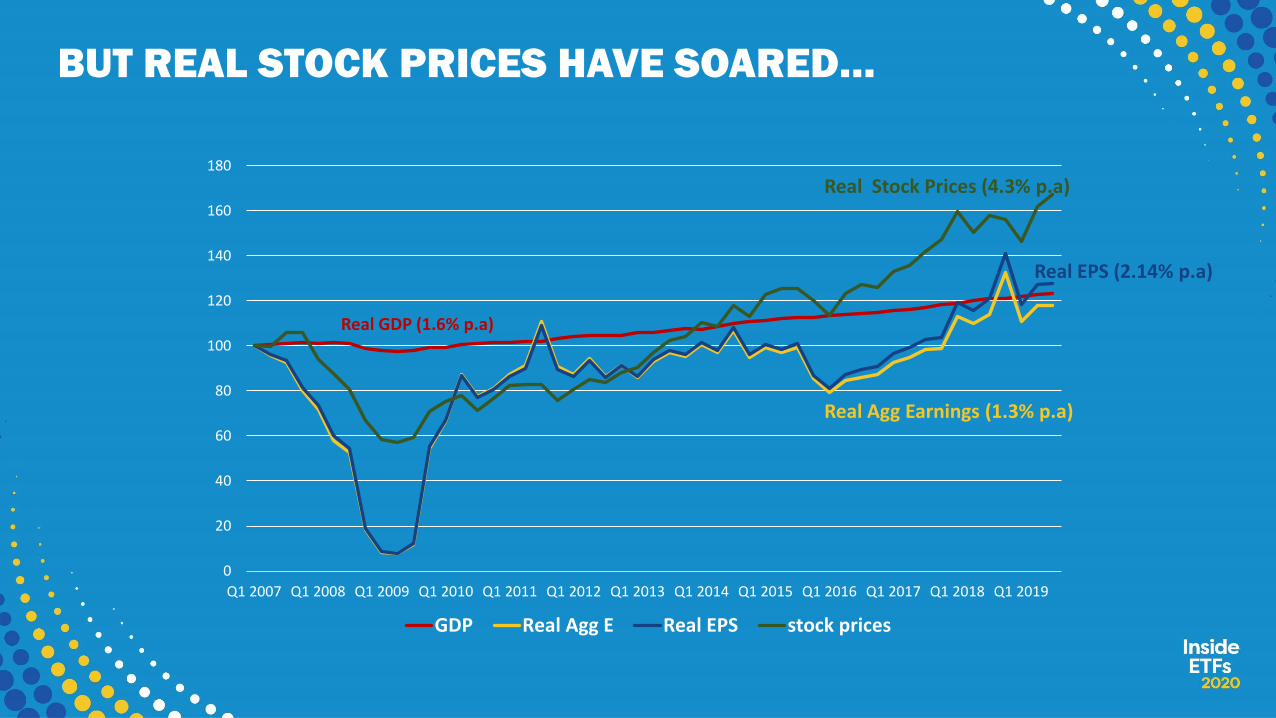

BUT REAL STOCK PRICES HAVE SOARED…

0

20

40

60

80

100

120

140

160

180

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014 Q1 2015 Q1 2016 Q1 2017 Q1 2018 Q1 2019

GDP Real Agg E Real EPS stock prices

Real GDP (1.6% p.a)

Real Agg Earnings (1.3% p.a)

Real EPS (2.14% p.a)

Real Stock Prices (4.3% p.a)

Information Classification: General

WHEN WOULD YOU RATHER BUY?

There are three principal phases of a bull market: the first is represented by reviving confidence in the future of business; the second is the response of stock prices to the known improvement in corporate earnings, and the third is the period when speculation is rampant – a period when stocks are advanced on hopes and expectations.

There are three principal phases of a bear market: the first represents the abandonment of the hopes upon which stocks were purchased at inflated prices; the second reflects selling due to decreased business and earnings, and the third is caused by distress selling of sound securities, regardless of their value, by those who must find a cash market for at least a portion of their assets.

– Robert Rhea, The Dow Theory, 1932

Information Classification: General

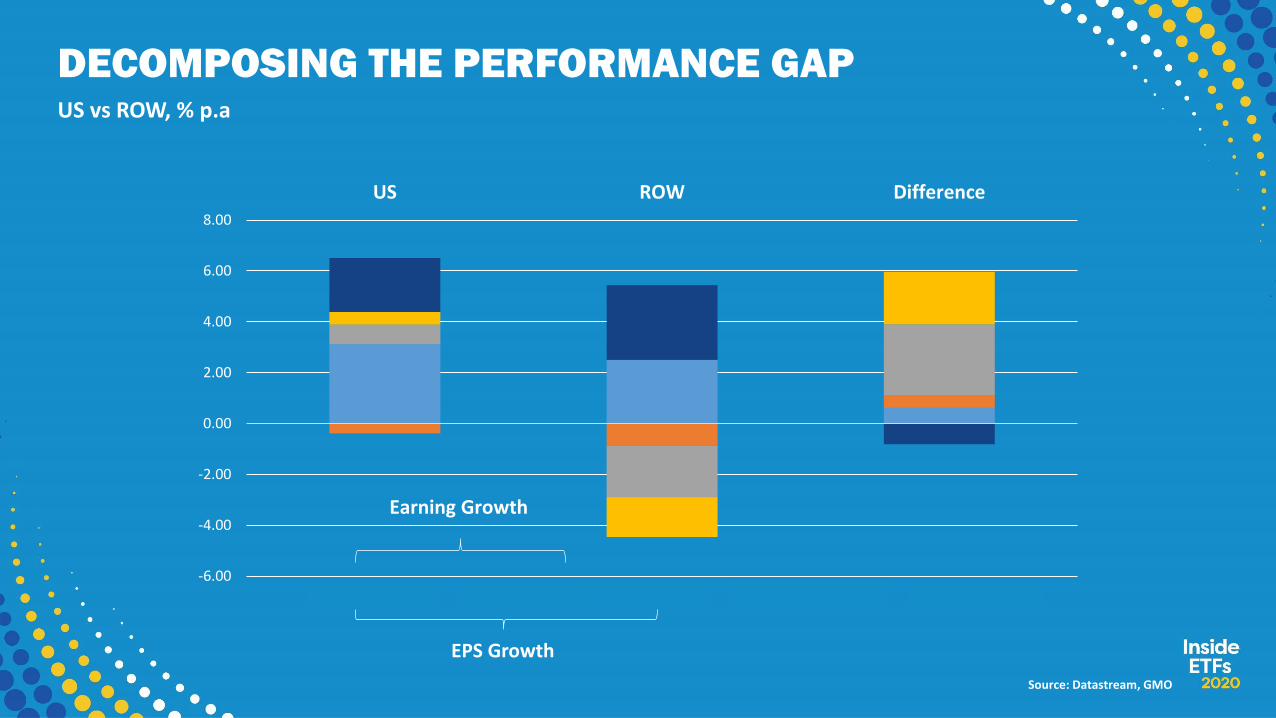

DECOMPOSING THE PERFORMANCE GAPUS vs ROW, % p.a

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

US ROW Difference

Sales growth Margin growth Buybacks Valuation Change Income

Earning Growth

EPS Growth

Source: Datastream, GMO

Information Classification: General

SHILLER PE AROUND THE WORLDAnything but the US

Source: Datastream, GMO

0

5

10

15

20

25

30

35

40

45

50

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

USWorld ex US EM

Information Classification: General

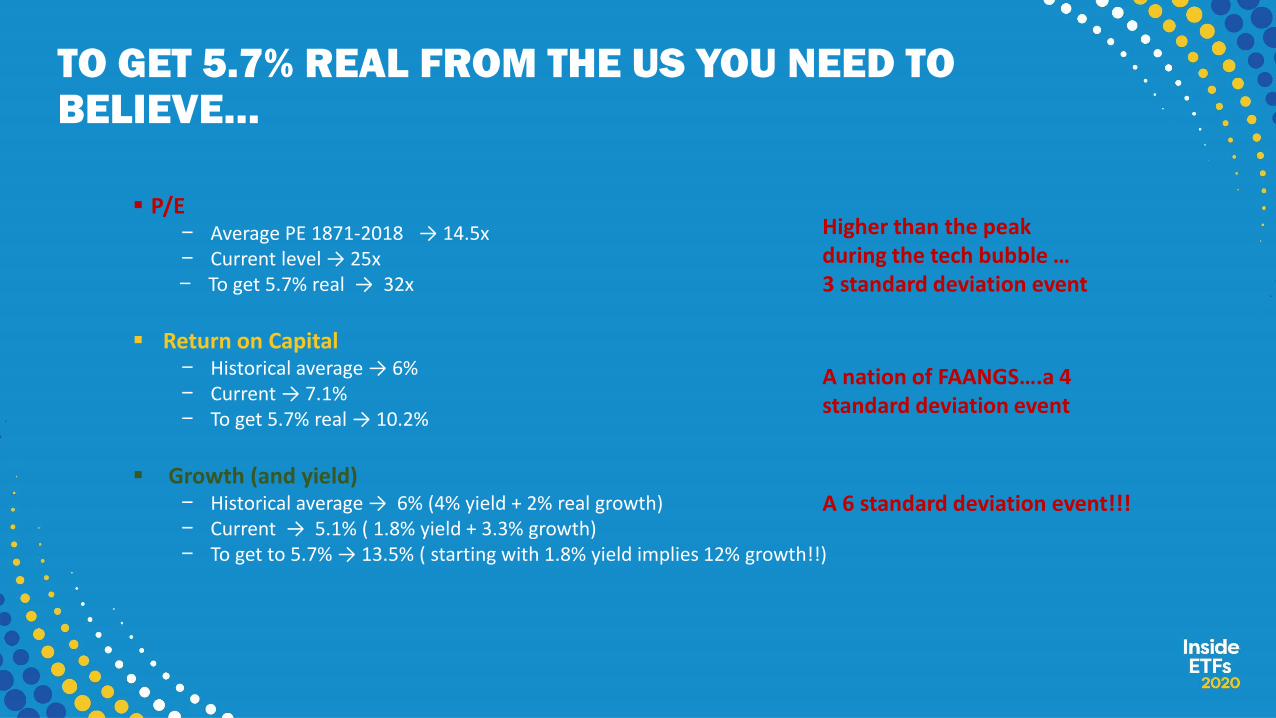

TO GET 5.7% REAL FROM THE US YOU NEED TO BELIEVE…

▪ P/E– Average PE 1871-2018 → 14.5x – Current level → 25x– To get 5.7% real → 32x

▪ Return on Capital– Historical average → 6%– Current → 7.1%– To get 5.7% real → 10.2%

▪ Growth (and yield)– Historical average → 6% (4% yield + 2% real growth)– Current → 5.1% ( 1.8% yield + 3.3% growth) – To get to 5.7% → 13.5% ( starting with 1.8% yield implies 12% growth!!)

Higher than the peak during the tech bubble …3 standard deviation event

A nation of FAANGS….a 4 standard deviation event

A 6 standard deviation event!!!

Information Classification: General

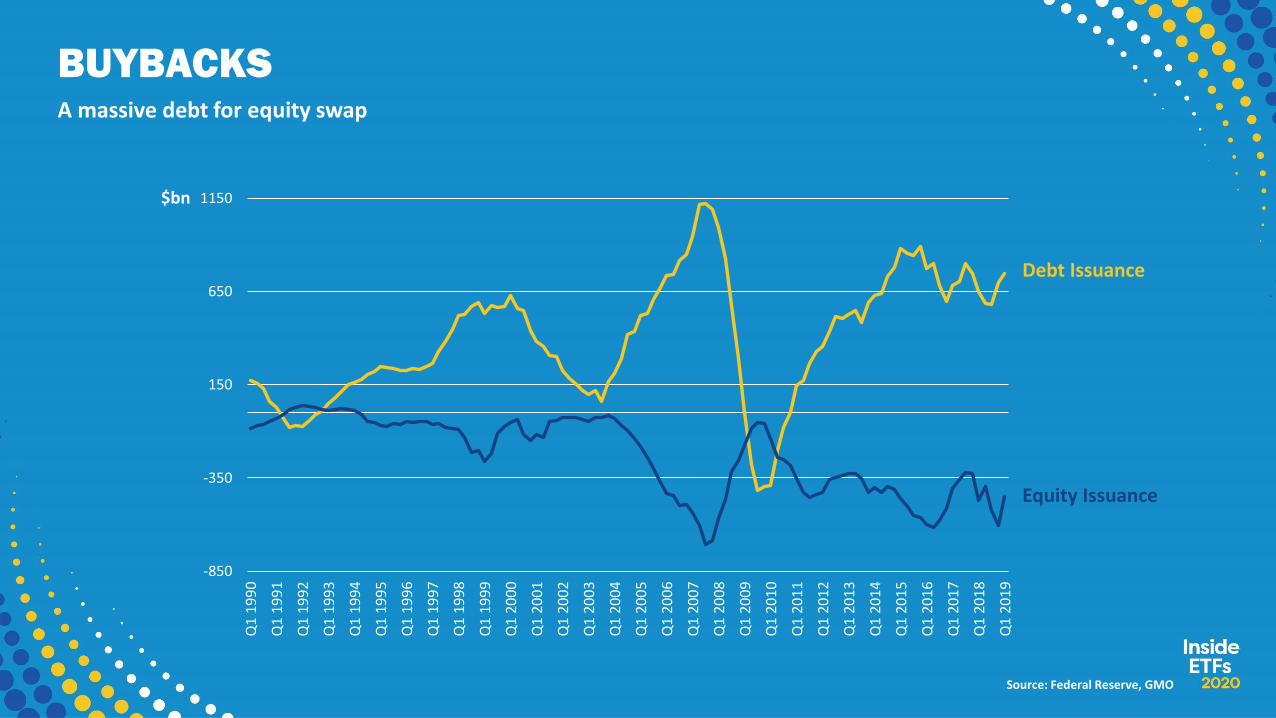

BUYBACKSA massive debt for equity swap

Source: Federal Reserve, GMO

-850

-350

150

650

1150

Q1

19

90

Q1

19

91

Q1

19

92

Q1

19

93

Q1

19

94

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

20

19

$bn

Debt Issuance

Equity Issuance

Information Classification: General

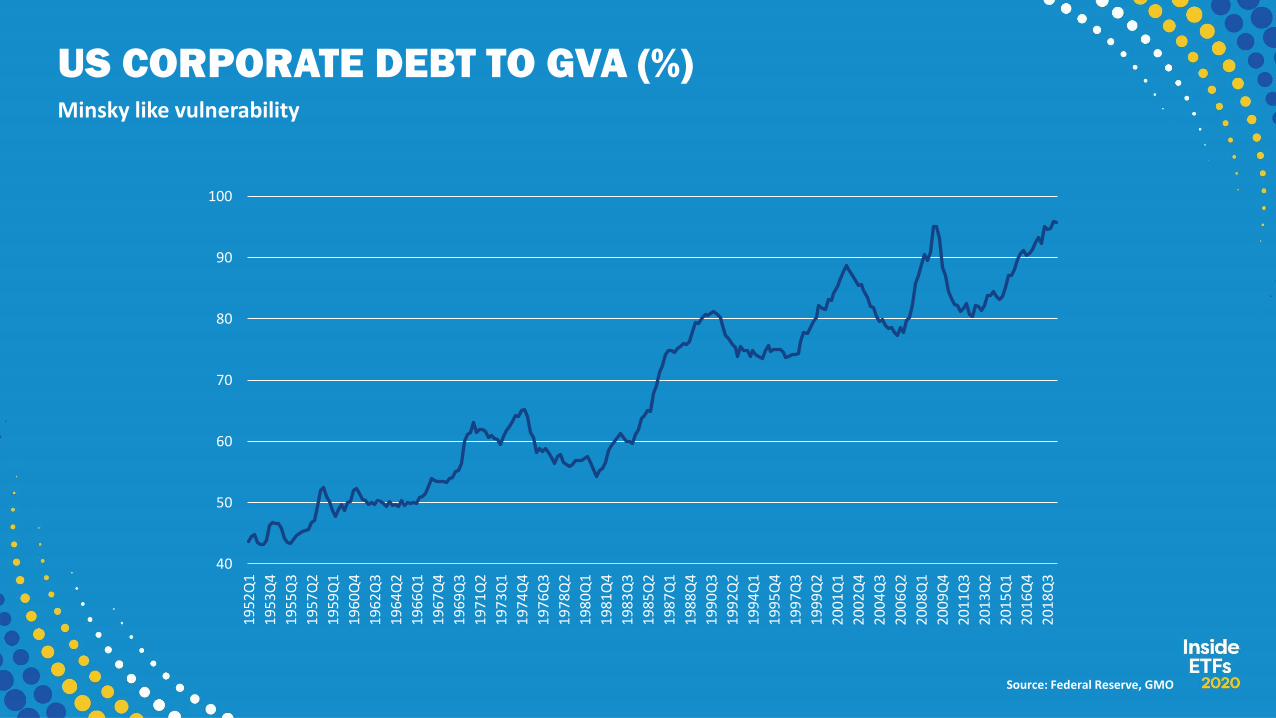

US CORPORATE DEBT TO GVA (%)Minsky like vulnerability

Source: Federal Reserve, GMO

40

50

60

70

80

90

100

19

52

Q1

19

53

Q4

19

55

Q3

19

57

Q2

19

59

Q1

19

60

Q4

19

62

Q3

19

64

Q2

19

66

Q1

19

67

Q4

19

69

Q3

19

71

Q2

19

73

Q1

19

74

Q4

19

76

Q3

19

78

Q2

19

80

Q1

19

81

Q4

19

83

Q3

19

85

Q2

19

87

Q1

19

88

Q4

19

90

Q3

19

92

Q2

19

94

Q1

19

95

Q4

19

97

Q3

19

99

Q2

20

01

Q1

20

02

Q4

20

04

Q3

20

06

Q2

20

08

Q1

20

09

Q4

20

11

Q3

20

13

Q2

20

15

Q1

20

16

Q4

20

18

Q3

Information Classification: General

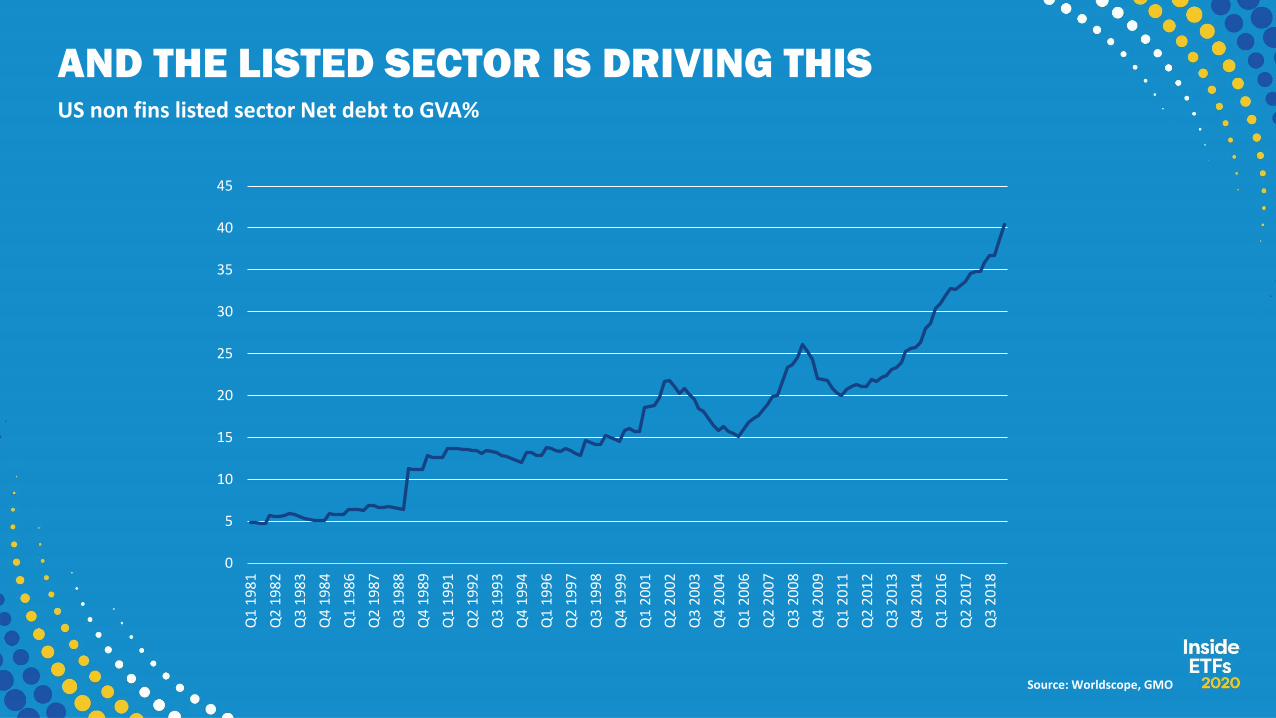

AND THE LISTED SECTOR IS DRIVING THISUS non fins listed sector Net debt to GVA%

Source: Worldscope, GMO

0

5

10

15

20

25

30

35

40

45

Q1

19

81

Q2

19

82

Q3

19

83

Q4

19

84

Q1

19

86

Q2

19

87

Q3

19

88

Q4

19

89

Q1

19

91

Q2

19

92

Q3

19

93

Q4

19

94

Q1

19

96

Q2

19

97

Q3

19

98

Q4

19

99

Q1

20

01

Q2

20

02

Q3

20

03

Q4

20

04

Q1

20

06

Q2

20

07

Q3

20

08

Q4

20

09

Q1

20

11

Q2

20

12

Q3

20

13

Q4

20

14

Q1

20

16

Q2

20

17

Q3

20

18

Information Classification: General

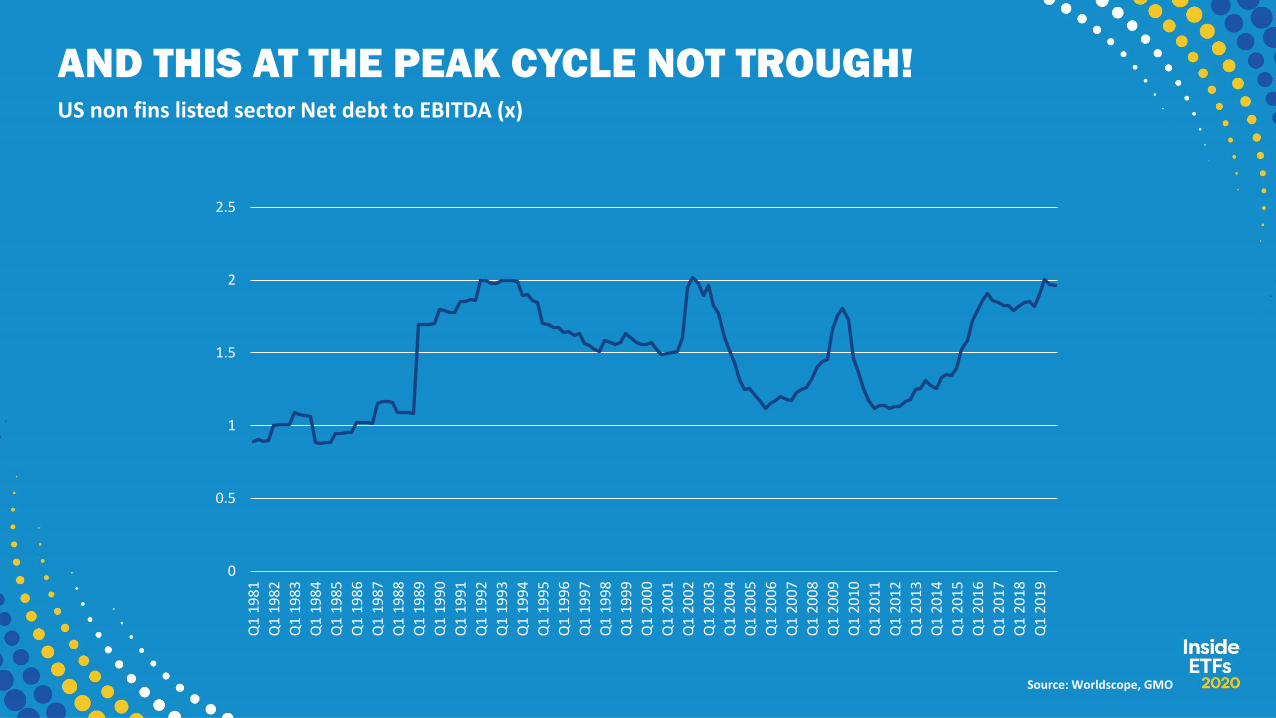

AND THIS AT THE PEAK CYCLE NOT TROUGH!US non fins listed sector Net debt to EBITDA (x)

Source: Worldscope, GMO

0

0.5

1

1.5

2

2.5

Q1

19

81

Q1

19

82

Q1

19

83

Q1

19

84

Q1

19

85

Q1

19

86

Q1

19

87

Q1

19

88

Q1

19

89

Q1

19

90

Q1

19

91

Q1

19

92

Q1

19

93

Q1

19

94

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

20

19

Information Classification: General

AND A QUARTER OF ALL FIRMS ARE MAKING LOSSES!!

0

5

10

15

20

25

30

35

40

19

55

19

58

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

20

15

Reported Earnings by number

Economic Earnings by number

Information Classification: General

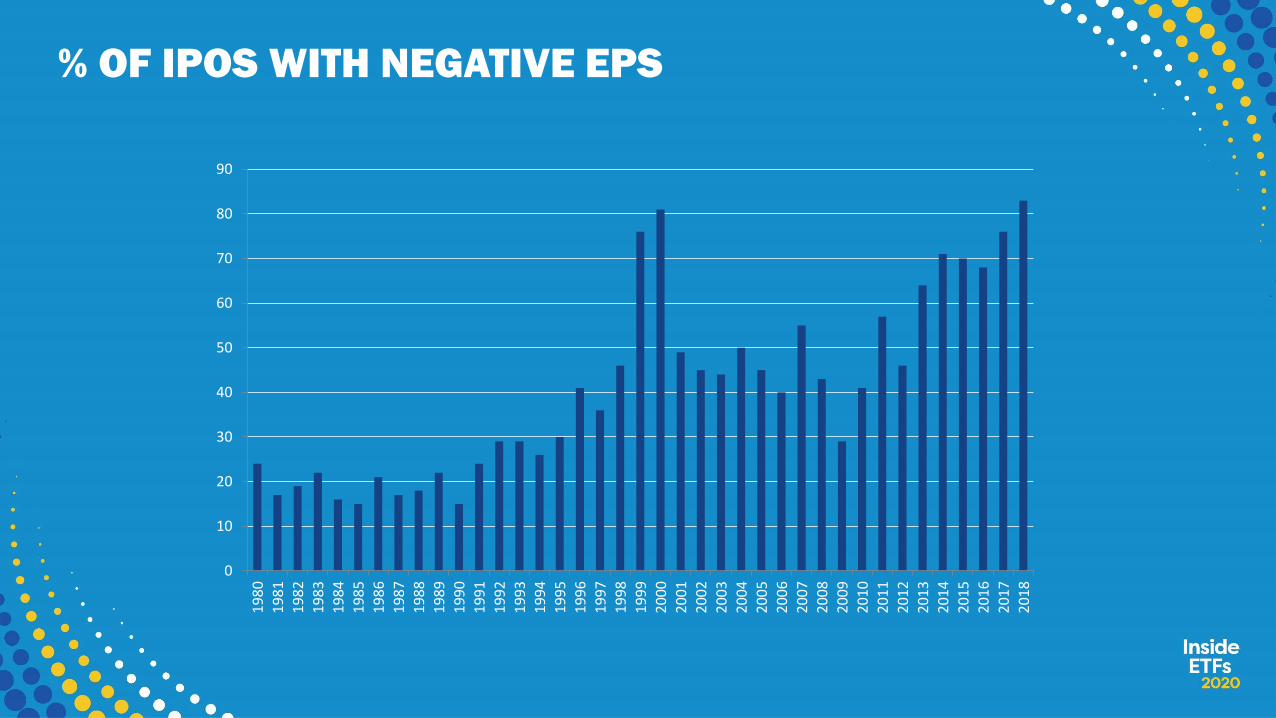

% OF IPOS WITH NEGATIVE EPS

0

10

20

30

40

50

60

70

80

90

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Information Classification: General

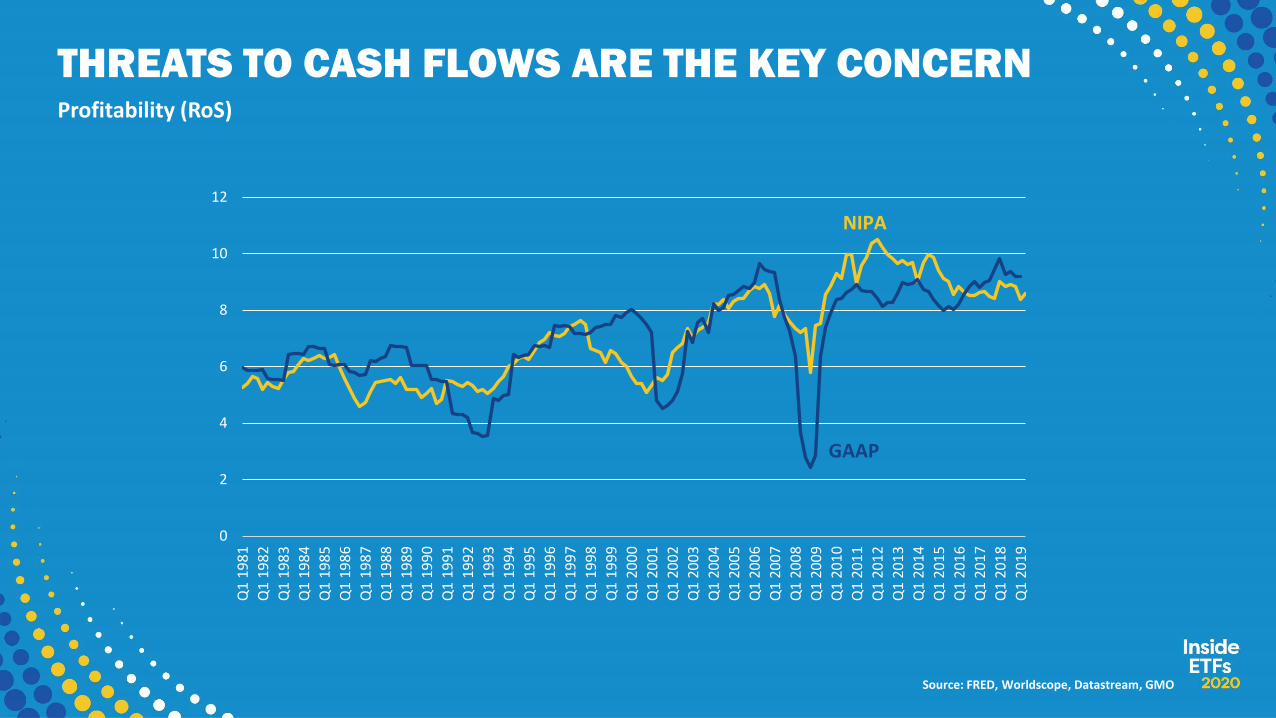

THREATS TO CASH FLOWS ARE THE KEY CONCERNProfitability (RoS)

Source: FRED, Worldscope, Datastream, GMO

0

2

4

6

8

10

12

Q1

19

81

Q1

19

82

Q1

19

83

Q1

19

84

Q1

19

85

Q1

19

86

Q1

19

87

Q1

19

88

Q1

19

89

Q1

19

90

Q1

19

91

Q1

19

92

Q1

19

93

Q1

19

94

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

20

19

GAAP

NIPA

Information Classification: General

YOU NEED TO BE DIFFERENT60/40 looks set to earn little to nothing!

% p.a

-5

0

5

10

15

20

19

52

.01

19

53

.09

19

55

.05

19

57

.01

19

58

.09

19

60

.05

19

62

.01

19

63

.09

19

65

.05

19

67

.01

19

68

.09

19

70

.05

19

72

.01

19

73

.09

19

75

.05

19

77

.01

19

78

.09

19

80

.05

19

82

.01

19

83

.09

19

85

.05

19

87

.01

19

88

.09

19

90

.05

19

92

.01

19

93

.09

19

95

.05

19

97

.01

19

98

.09

20

00

.05

20

02

.01

20

03

.09

20

05

.05

20

07

.01

20

08

.09

20

10

.05

20

12

.01

20

13

.09

20

15

.05

20

17

.01

20

18

.09

Expected return with mean reversion

Realized return to 60/40

Expected return without mean reversion

Information Classification: General

CONTRARIAN AND UNCONVENTIONALSimple but not easy

It is impossible to produce superior performance unless you do something different from the majority. If you buy the same securities everyone else is buying, you will have the same results as everyone else.

- Sir John Templeton

The central principle of investment is to go contrary to the general opinion on the grounds that if everyone agreed about its merits, the investment is inevitably too dear and therefore unattractive.

- JMK

Be fearful when others are greedy. Be greedy when others are fearful

- Warren Buffett

Information Classification: General

HURDLE 1: HUMAN NATURE

Information Classification: General

SAFER AND WARMER IN THE MIDDLE OF THE HERD

Information Classification: General

A MORE ACCURATE COMPARISON

Information Classification: General

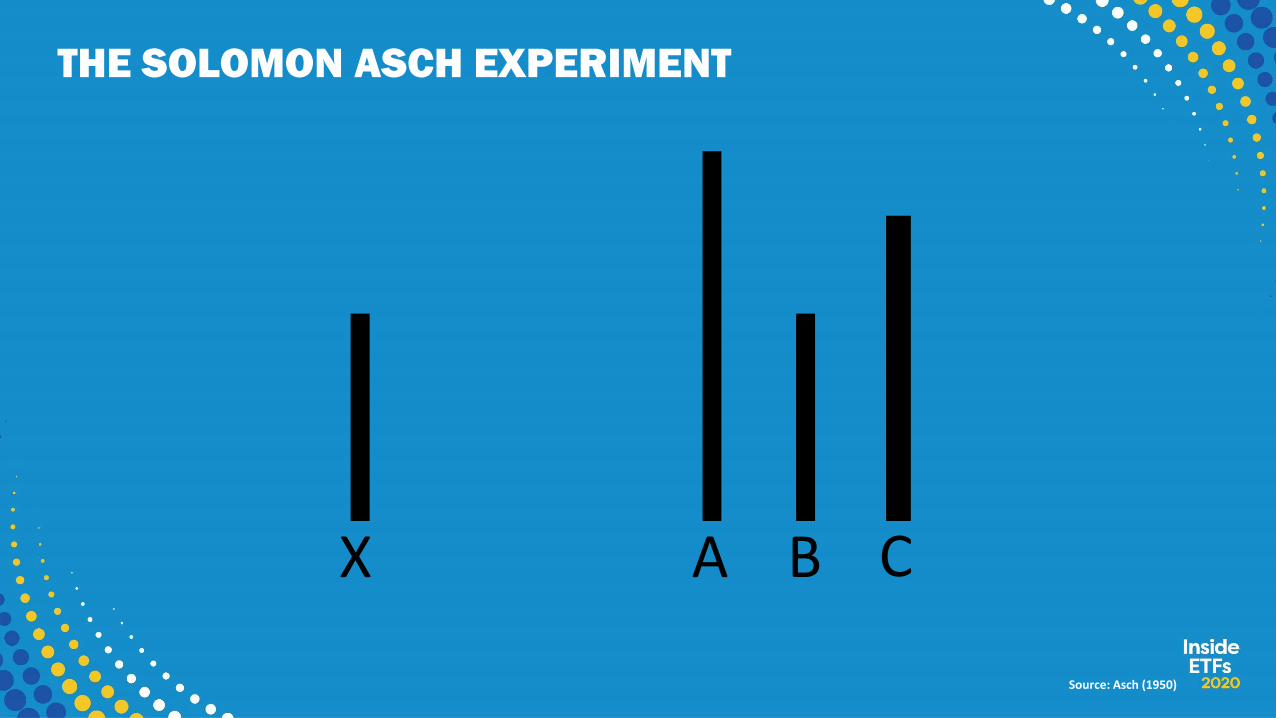

THE SOLOMON ASCH EXPERIMENT

X A B C

Source: Asch (1950)

Information Classification: General

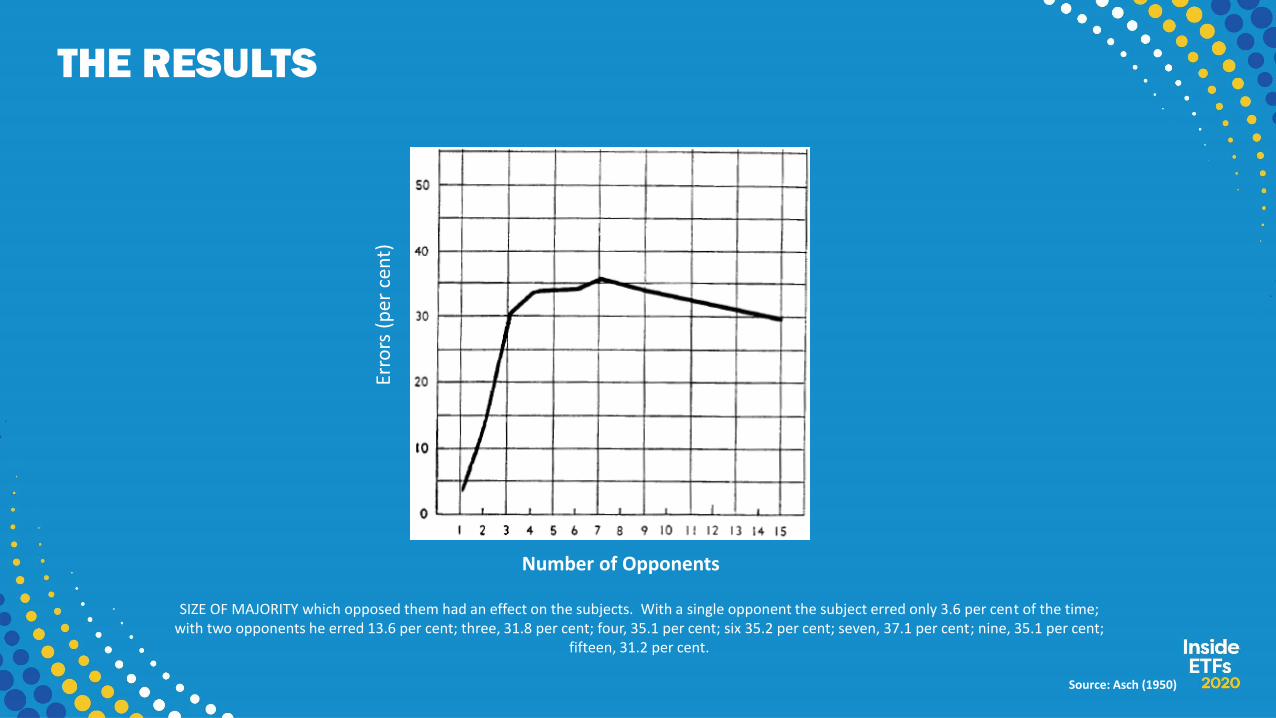

THE RESULTS

Source: Asch (1950)

Number of Opponents

Erro

rs (

per

cen

t)

SIZE OF MAJORITY which opposed them had an effect on the subjects. With a single opponent the subject erred only 3.6 per cent of the time; with two opponents he erred 13.6 per cent; three, 31.8 per cent; four, 35.1 per cent; six 35.2 per cent; seven, 37.1 per cent; nine, 35.1 per cent;

fifteen, 31.2 per cent.

Information Classification: General

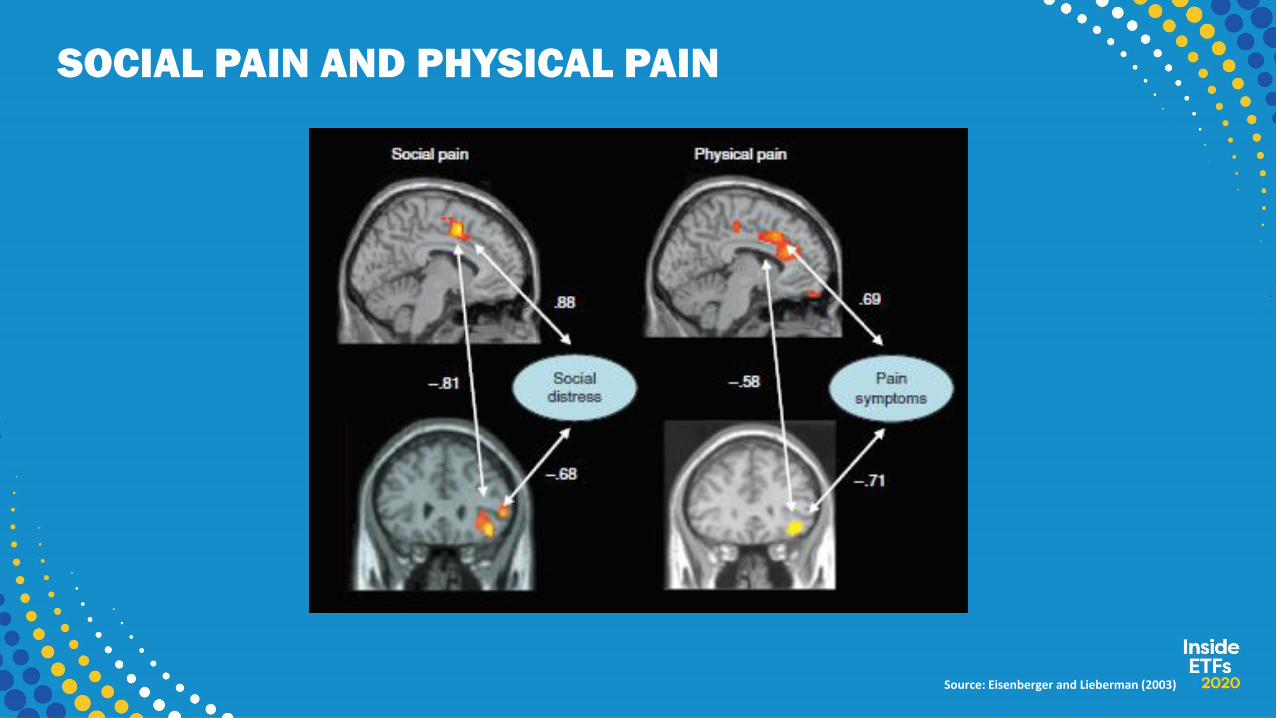

SOCIAL PAIN AND PHYSICAL PAIN

Source: Eisenberger and Lieberman (2003)

Information Classification: General

HURDLE 2: INSTITUTIONAL IMPERATIVE

Information Classification: General

KEYNES’ EDICT

Worldly wisdom teaches that It is better for reputation to fail conventionally then to

succeed unconventionally.

Information Classification: General

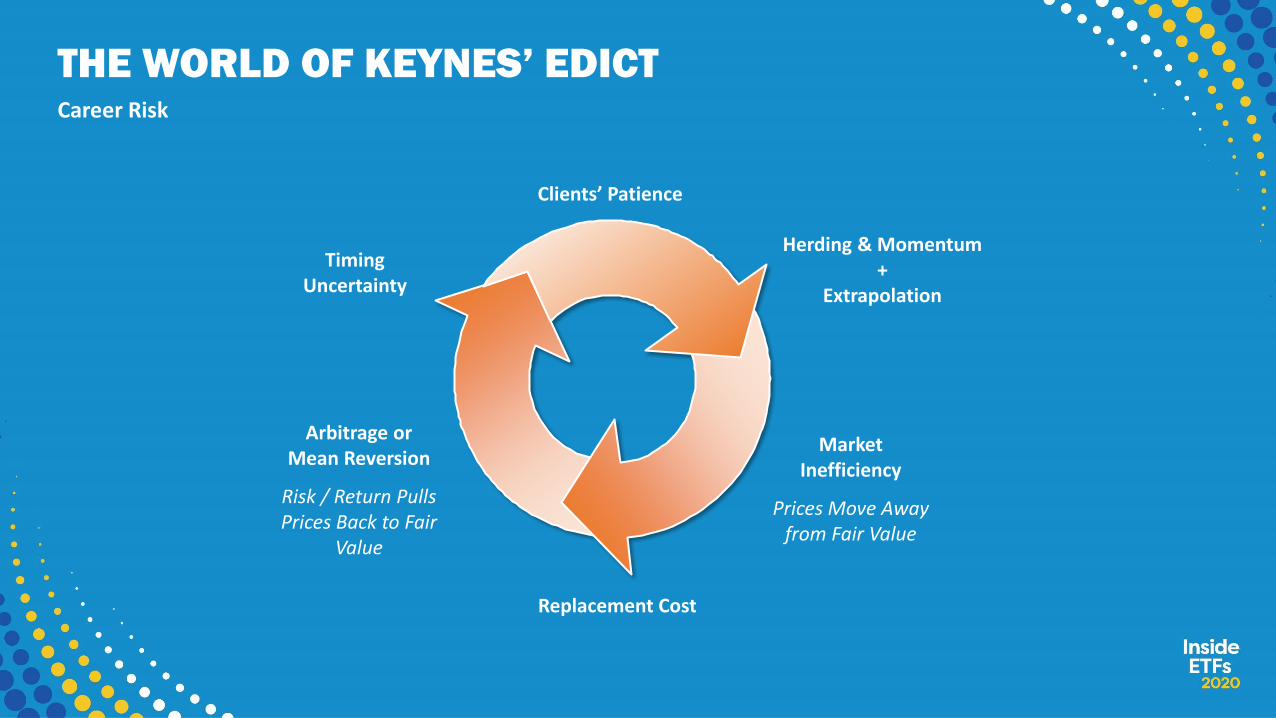

THE WORLD OF KEYNES’ EDICTCareer Risk

Market Inefficiency

Prices Move Away from Fair Value

Arbitrage or Mean Reversion

Risk / Return Pulls Prices Back to Fair

Value

Timing Uncertainty

Herding & Momentum+

Extrapolation

Clients’ Patience

Replacement Cost

Information Classification: General

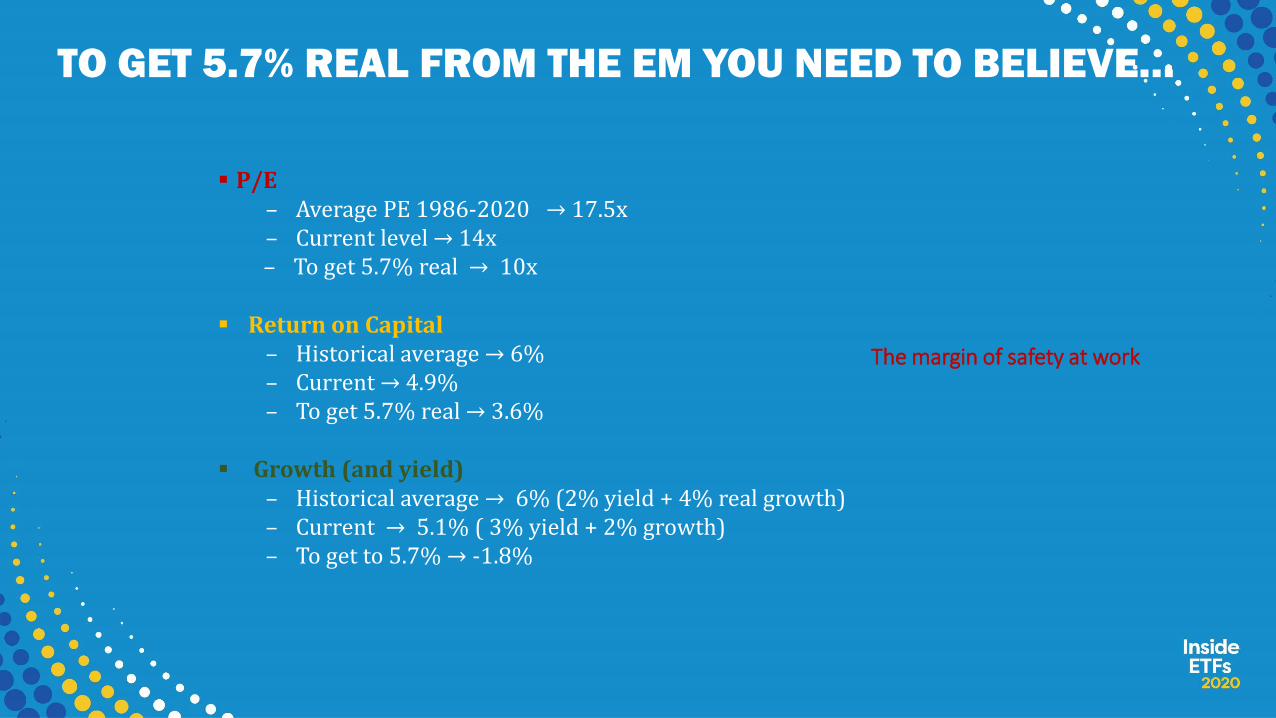

TO GET 5.7% REAL FROM THE EM YOU NEED TO BELIEVE…

▪ P/E– Average PE 1986-2020 → 17.5x – Current level → 14x– To get 5.7% real → 10x

▪ Return on Capital– Historical average → 6%– Current → 4.9%– To get 5.7% real → 3.6%

▪ Growth (and yield)– Historical average → 6% (2% yield + 4% real growth)– Current → 5.1% ( 3% yield + 2% growth) – To get to 5.7% → -1.8%

The margin of safety at work

Information Classification: General

EMERGING MARKET VALUE EVEN CHEAPERShiller PE

Source: Datastream, Bloomberg, GMO

5

10

15

20

25

30

35

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

EM

EM Value

Information Classification: General

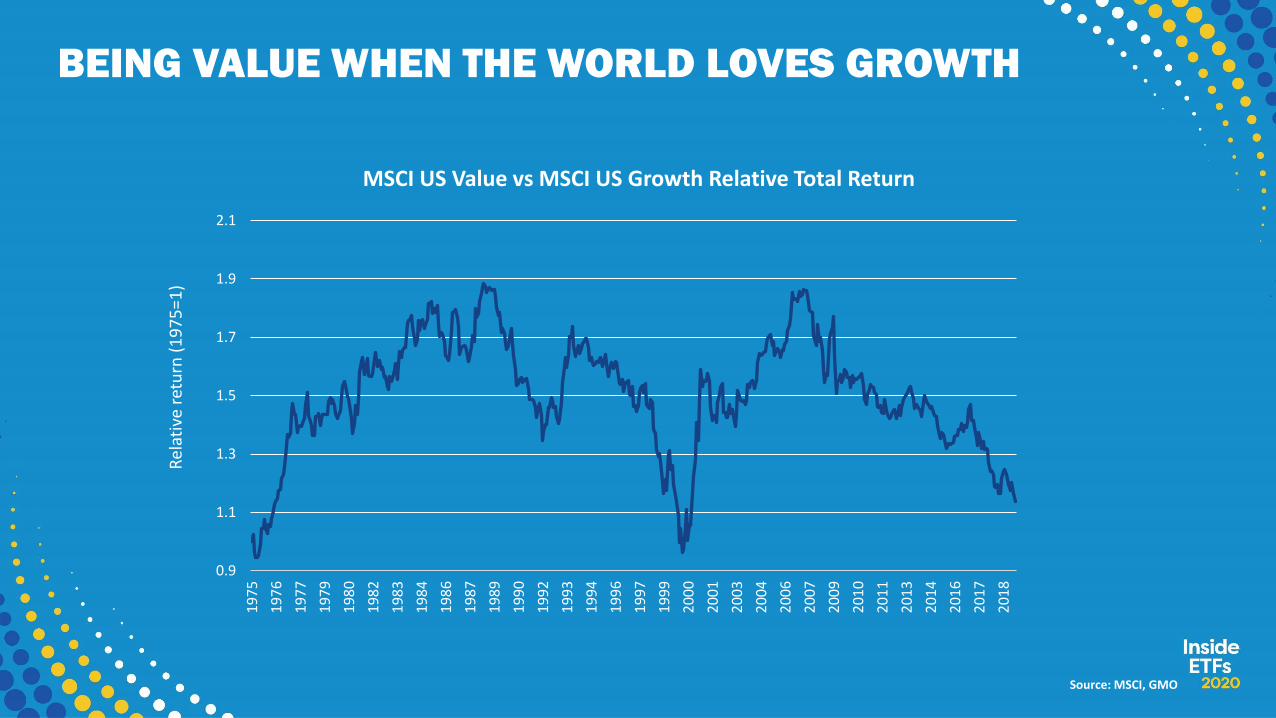

BEING VALUE WHEN THE WORLD LOVES GROWTH

Source: MSCI, GMO

0.9

1.1

1.3

1.5

1.7

1.9

2.1

19

75

19

76

19

77

19

79

19

80

19

82

19

83

19

84

19

86

19

87

19

89

19

90

19

92

19

93

19

94

19

96

19

97

19

99

20

00

20

01

20

03

20

04

20

06

20

07

20

09

20

10

20

11

20

13

20

14

20

16

20

17

20

18

Rel

ativ

e re

turn

(1

97

5=1

)MSCI US Value vs MSCI US Growth Relative Total Return

Information Classification: General

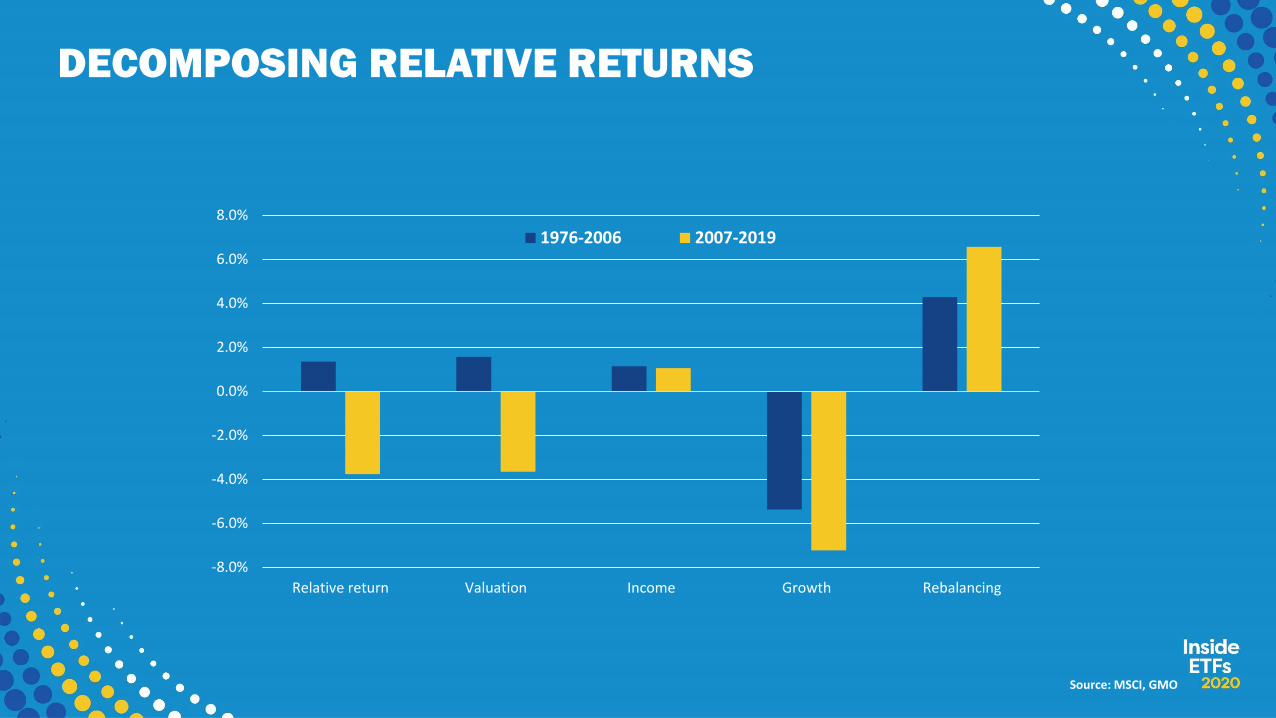

DECOMPOSING RELATIVE RETURNS

Source: MSCI, GMO

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Relative return Valuation Income Growth Rebalancing

1976-2006 2007-2019

Information Classification: General

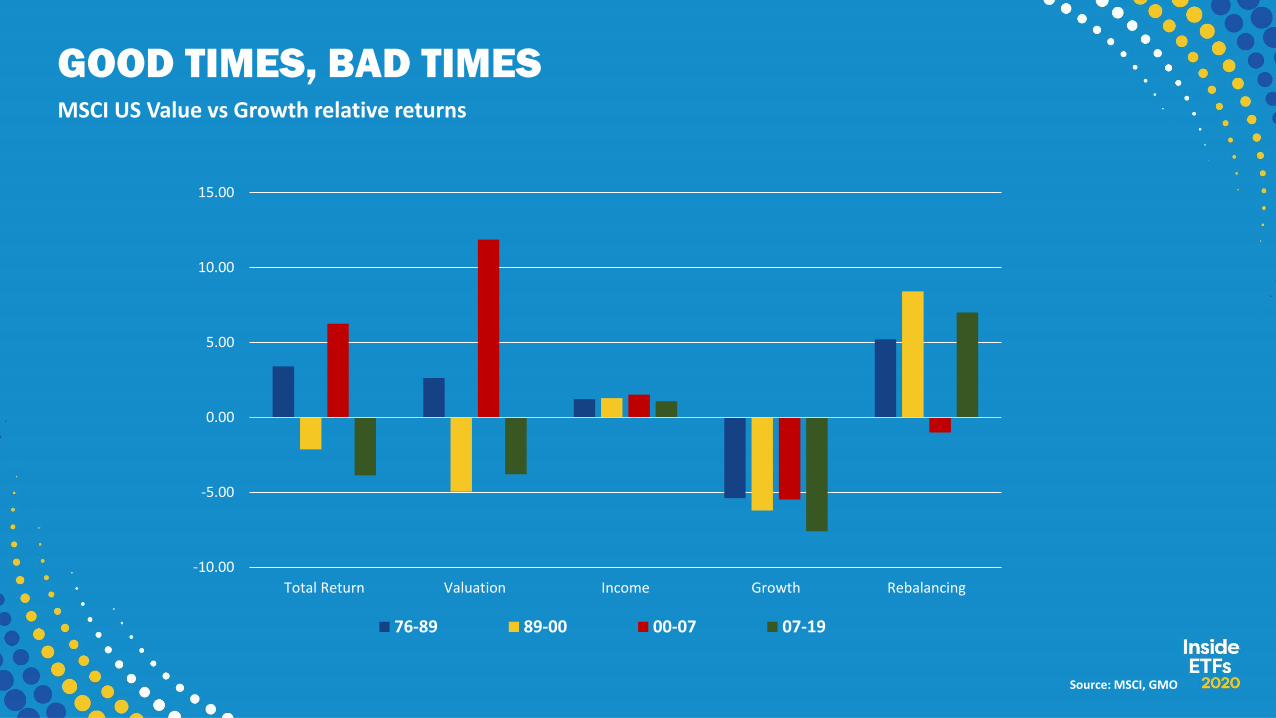

GOOD TIMES, BAD TIMES

Source: MSCI, GMO

MSCI US Value vs Growth relative returns

-10.00

-5.00

0.00

5.00

10.00

15.00

Total Return Valuation Income Growth Rebalancing

76-89 89-00 00-07 07-19

Information Classification: General

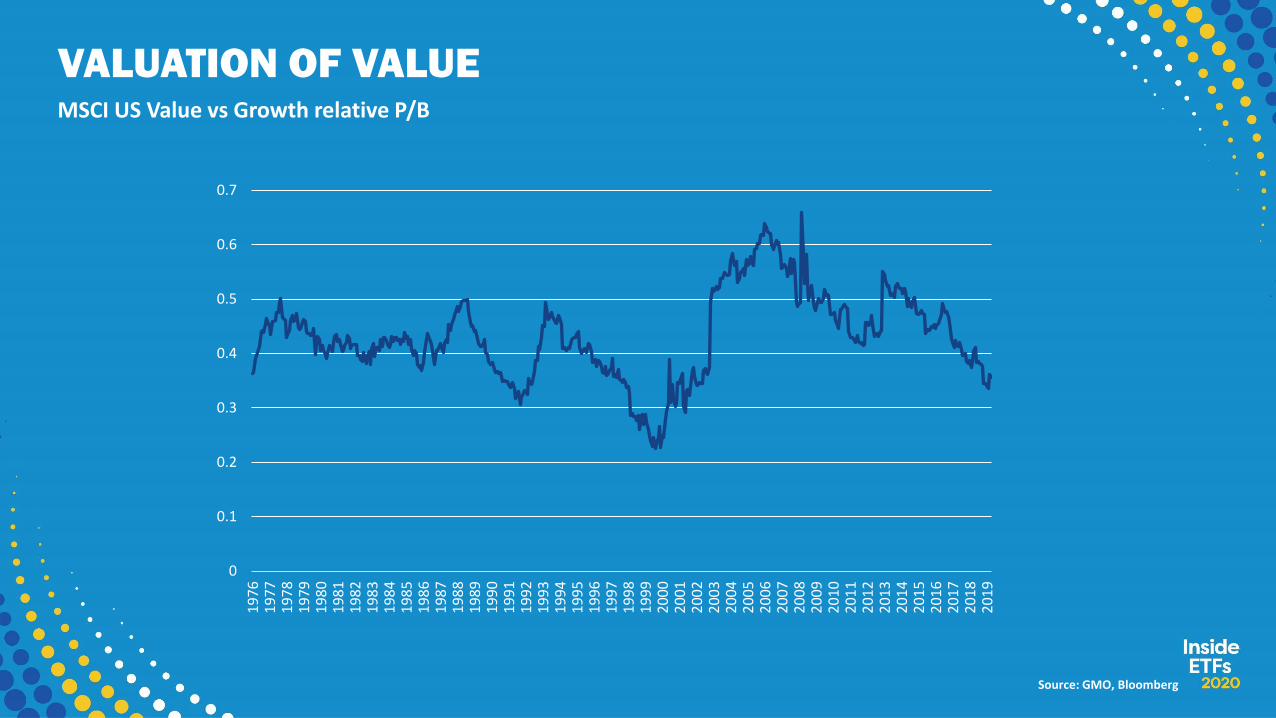

VALUATION OF VALUE

Source: GMO, Bloomberg

MSCI US Value vs Growth relative P/B

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Information Classification: General

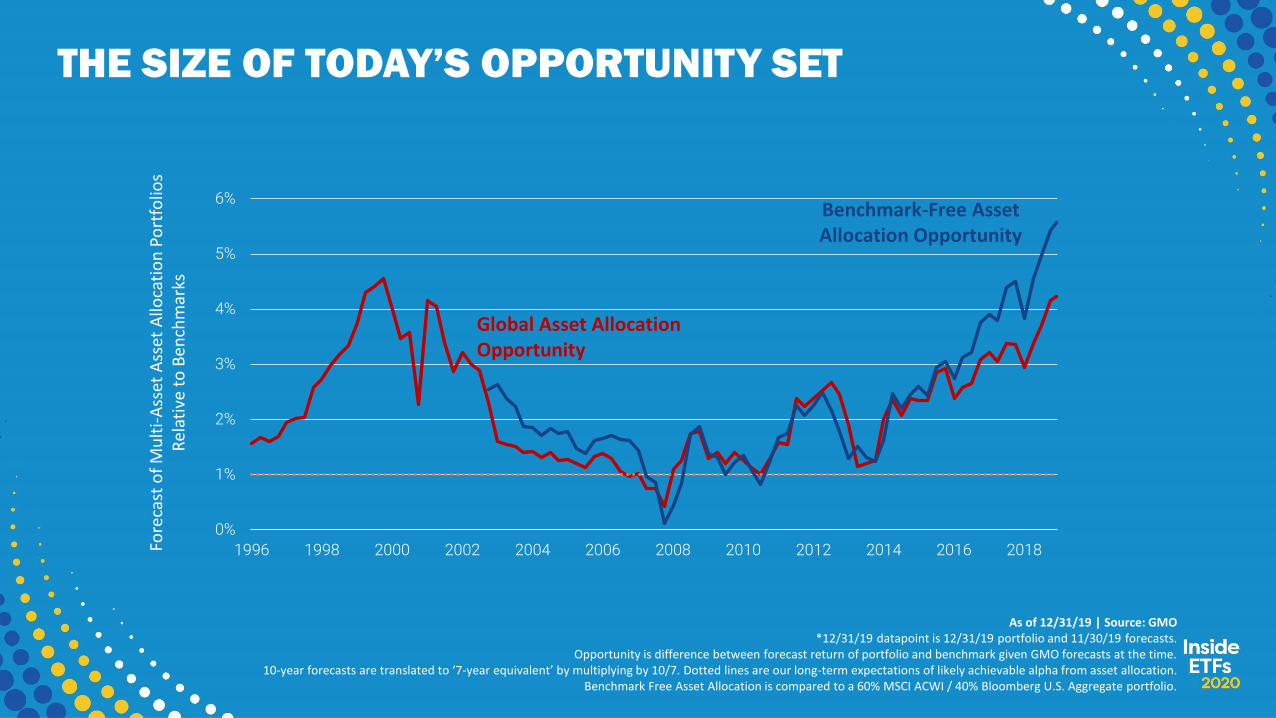

THE SIZE OF TODAY’S OPPORTUNITY SET

As of 12/31/19 | Source: GMO*12/31/19 datapoint is 12/31/19 portfolio and 11/30/19 forecasts.

Opportunity is difference between forecast return of portfolio and benchmark given GMO forecasts at the time.10-year forecasts are translated to ‘7-year equivalent’ by multiplying by 10/7. Dotted lines are our long-term expectations of likely achievable alpha from asset allocation.

Benchmark Free Asset Allocation is compared to a 60% MSCI ACWI / 40% Bloomberg U.S. Aggregate portfolio.

0%

1%

2%

3%

4%

5%

6%

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Benchmark-Free Asset Allocation Opportunity

Global Asset Allocation Opportunity

Fore

cast

of

Mu

lti-

Ass

et A

sset

Allo

cati

on

Po

rtfo

lios

Rel

ativ

e to

Ben

chm

arks

Information Classification: General

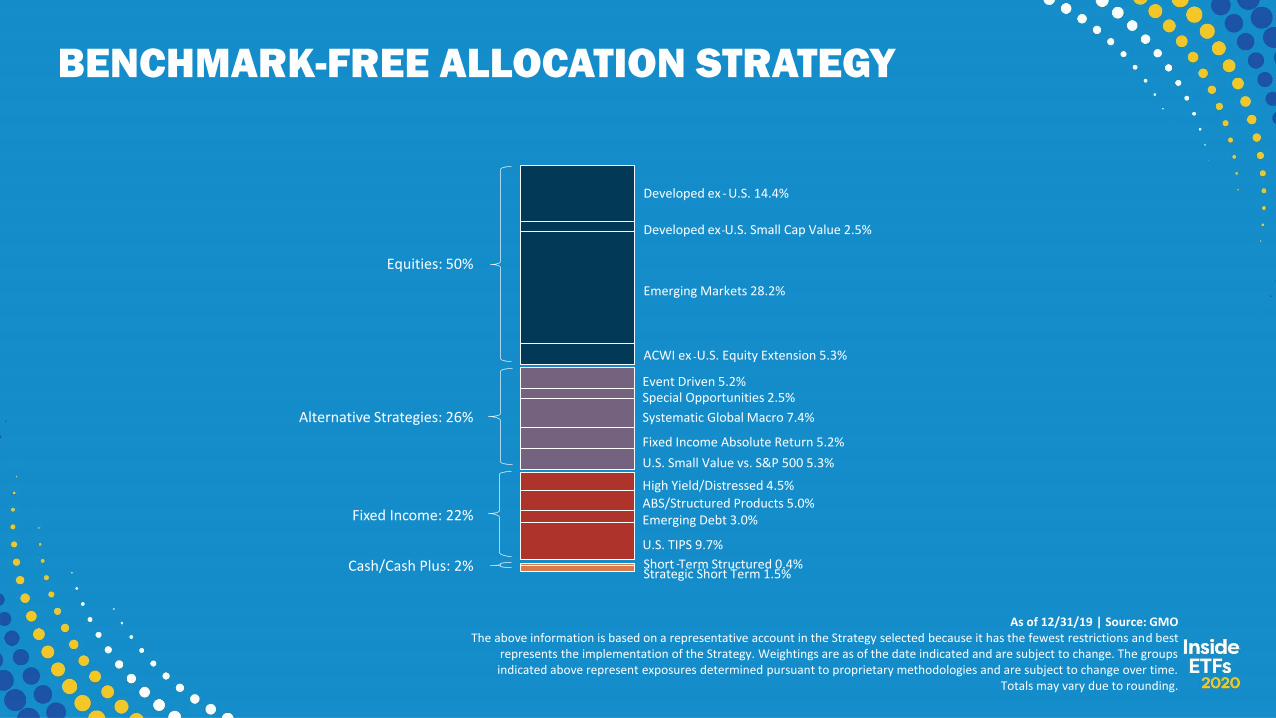

BENCHMARK-FREE ALLOCATION STRATEGY

As of 12/31/19 | Source: GMO The above information is based on a representative account in the Strategy selected because it has the fewest restrictions and best

represents the implementation of the Strategy. Weightings are as of the date indicated and are subject to change. The groups indicated above represent exposures determined pursuant to proprietary methodologies and are subject to change over time.

Totals may vary due to rounding.

Equities: 50%

Cash/Cash Plus: 2%

Fixed Income: 22%

Alternative Strategies: 26%

Developed ex

Systematic Global Macro 7.4%

Developed ex - U.S. 14.4%

Event Driven 5.2%

Emerging Markets 28.2%

Emerging Debt 3.0%ABS/Structured Products 5.0%

Fixed Income Absolute Return 5.2%

Special Opportunities 2.5%

High Yield/Distressed 4.5%

U.S. TIPS 9.7%

Short -Term Structured 0.4%Strategic Short Term 1.5%

ACWI ex -U.S. Equity Extension 5.3%

U.S. Small Value vs. S&P 500 5.3%

-U.S. Small Cap Value 2.5%