Embed Size (px)

Citation preview

OMNICHANNEL, NOT OMNISHAMBLES

Although consumers have quickly adopted digital channels for both service and sales, they aren’t abandoning traditional retail stores and call centers in their interactions with companies. Increasingly, customers expect

“omnichannel” convenience that allows them to start a journey in one channel (say, a mobile app) and end it in another (by picking up the purchase in a store).

For companies, the challenge is to provide high-quality service from end to end, regardless of where the ends might be. That was the case for a regional bank that sensed that too many customers were falling into gaps between channels.

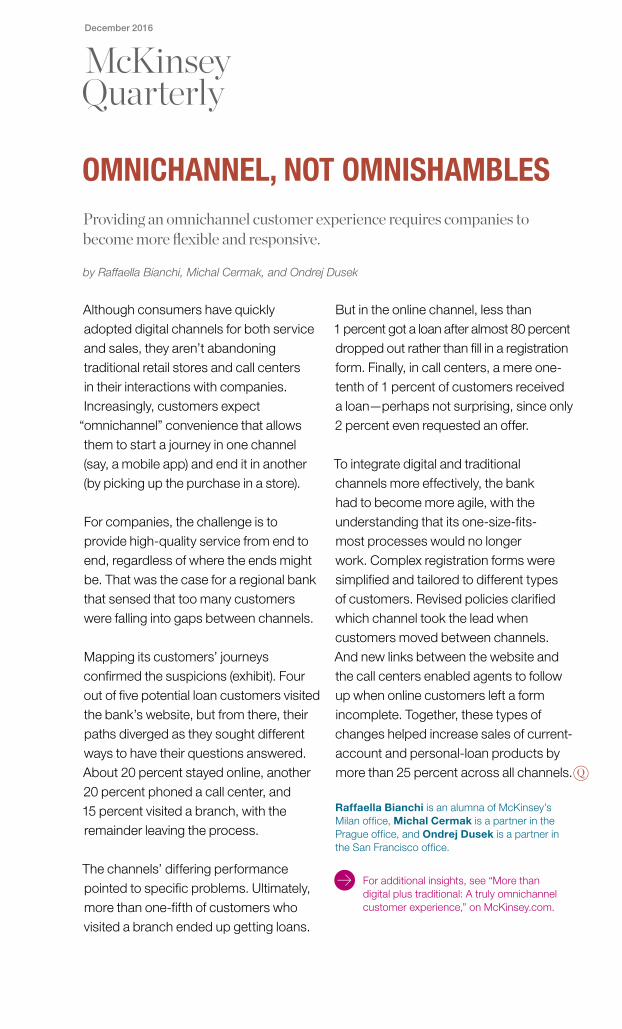

Mapping its customers’ journeys confirmed the suspicions (exhibit). Four out of five potential loan customers visited the bank’s website, but from there, their paths diverged as they sought different ways to have their questions answered. About 20 percent stayed online, another 20 percent phoned a call center, and 15 percent visited a branch, with the remainder leaving the process.

The channels’ differing performance pointed to specific problems. Ultimately, more than one-fifth of customers who visited a branch ended up getting loans.

But in the online channel, less than 1 percent got a loan after almost 80 percent dropped out rather than fill in a registration form. Finally, in call centers, a mere one-tenth of 1 percent of customers received a loan—perhaps not surprising, since only 2 percent even requested an offer.

To integrate digital and traditional channels more effectively, the bank had to become more agile, with the understanding that its one-size-fits-most processes would no longer work. Complex registration forms were simplified and tailored to different types of customers. Revised policies clarified which channel took the lead when customers moved between channels. And new links between the website and the call centers enabled agents to follow up when online customers left a form incomplete. Together, these types of changes helped increase sales of current-account and personal-loan products by more than 25 percent across all channels.

Providing an omnichannel customer experience requires companies to become more flexible and responsive.

by Raffaella Bianchi, Michal Cermak, and Ondrej Dusek

Raffaella Bianchi is an alumna of McKinsey’s Milan office, Michal Cermak is a partner in the Prague office, and Ondrej Dusek is a partner in the San Francisco office.

For additional insights, see “More than digital plus traditional: A truly omnichannel customer experience,” on McKinsey.com.

December 2016

2

Exhibit

Mapping customer flows highlights pain points.

Q1 2016OmnichannelExhibit 1 of 1

Where loan customers are lost

Average monthly customer flows for loan products by channel,1 indexed to 100,000

Gather information

100,000people

Requestoffer

Receiveoffer

Submitrequest

Request processed

Getapproval

Gather information

100,000people

Requestoffer

Receiveoffer

Submitrequest

Requestprocessed

Getapproval

97,630leave process

80% of all online customers quit before registration

98% of phone customers give up and do not bother to request offer

Only branch channel retains signi�cant percentage of customers throughout process

1,00

0 vi

sit b

ranc

h af

ter p

hone

inq

uiry

12,0

00

15,000 view registrationform online

16,0

00

22,0

0056

,000

14,500

11,00013,500

500 200 20

1003,000 1,300

6,5003,250

1,500

3,3702,370approvedloans

72,000 do web search

22,000 start onbank website

4,500phone

1,500 walk in to branch

Phone call center Online In person at branch Customers dropped out

78,000visitbankwebsite

15,000

19,50020,5004,500

1Preapproved loans excluded.

Source: Call-center data; Google Analytics; interviews; McKinsey analysis

Copyright © 2016 McKinsey & Company. All rights reserved.