Embed Size (px)

Citation preview

Onshore, Nearshore,

Offshore: Unsure? A 2012 Czech Perspective

2 Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012

The Czech Republic

remains a target for BPO

and SSC activities.

Executive Summary

Economics

• The Czech economy faces growing risks in 2012–13

related mainly to external factors

• The heightening of the Eurozone debt crisis will keep

unemployment rates elevated

• Despite certain problems, the Czech economy is

forecasted to be healthier than most European countries

Business Environment

• Transparent business environment with a high level of

international compliance

• Attractive location for foreign investors and for SSC or

R&D projects

Labour Market

• Highly educated, skilled and multilingual labour pool

• Czech graduates often plan to connect their career path

with business service centres starting on junior positions

Real Estate

• Modern, flexible, sustainable office property market at

relatively low and stable rent levels

• Developers who understand the constantly changing

needs of occupiers

The Czech Republic

The Czech Republic is situated in the very centre of Europe and has often been referred to as the gateway between the east and west. The country is a popular tourist destination due to its cultural heritage, capital city of Prague, and the largely unspoilt countryside. The number of annual international inbound tourists oscillate around 11 - 12 million.

The Czech Republic joined the European Union on the 1st of May 2004 and as a result, opened the doors for foreign investment.

Demographics and Economics

The Czech Republic has a population of approximately 10.5 million people, with the capital city of Prague being home to 1.2 million inhabitants. The country is split into 14 regions, and for the purpose of this report we will also be covering 3 other major regional cities: Brno, Ostrava and Pilsen.

The following table shows the key economic indicators of the Czech Republic:

2010 2011 2012E 2013F

Gross Domestic Product*

2.6 1.7 -0.8 1.0

Consumer Price Index*

1.5 1.9 3.2 2.1

Nominal Wage Growth**

1.9 2.2 2.9 2.9

Household Consumption**

0.6 -0.7 -1.9 0.4

Unemployment Rate (%)*

7.3 6.7 6.9 6.9

Source: *IHS Global Insight, Aug 2012 ** Consensus Forecasts, Aug 2012 Note: Change Year on Year, E=Estimate, F=Forecast

A downturn in GDP and other Czech economic risks relate mainly to external factors, as the country is highly export dependent. With the rest of the European Union falling into recession in 2012, the Czech Republic will not avoid contagion. Indeed, the country already experienced quarter-on-quarter declines in GDP during the second half of 2011, a trend that continued in the first half of 2012. As a result of heightening Eurozone debt crisis the unemployment rates will be elevated in 2012. Still, results for the first months of 2012 were better than expected. From 2014 onwards, we can expect gradual unemployment reduction, thanks to continued inflows of foreign direct investment, further labour market reforms and improved labour mobility.

Over the longer term, moving ahead with the approval of deeper fiscal reforms in 2011–12, together with planned reforms of the pension system, represent a step in the right direction in terms of fiscal sustainability. Indeed, the country economy is healthier than most European countries.

Transport and Infrastructure

The major cities of the Czech Republic all have an excellent public transport system. Within Prague, the main means of travel are the underground (metro), trams and buses. Most office and retail developments are built very close to, or on top of metro stations. In the regional cities the transport is provided by trams, buses and trolley buses, not forgetting the inner city rail network which has recently been improved by the introduction of several train express routes, between the capital and other regional cities.

Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012 3

The Czech Republic, thanks to a great position on the transit junction between Western and Eastern Europe, represents an ideal location for Central European and European BPO and SSC activities. The Czech Republic belongs to one of those countries with the densest motorway networks in Europe. Currently there is approximately 1,200 km of motorways already in operation and another 1,000 km are in preparatory or planned phases.

All four major cities have an airport, although international routes are currently limited in the regional airports. It is expected that the importance of international airports in Brno and Ostrava will increase in the near future while Prague’s Ruzyne airport is already one of the major air travel junctions in the CEE.

All major cities and the majority of smaller cities are well catered for in terms of shopping, services and entertainment. You will find a broad range of local and international retailers occupying modern shopping centres, retail parks and factory outlets.

Business Environment Generally, there is no limit for the level of foreign participation in a Czech legal entity. Foreigners can establish both joint ventures and wholly-owned subsidiaries in the Czech Republic. For setting up a new business, applicants can submit standard forms to the relevant Commercial Register (registration court). The registration process takes five working days.

Starting 1 January 2014, civil law will be significantly changed when a new codification becomes effective, namely the new Civil Code and the Business Corporations Act.

Corporate Tax is set at 19%.

Value Added Tax (VAT) is set at a standard rate of 20% and a reduced rate of 14%.1

Repatriation of Profit - No limitations exist concerning the distribution and repatriation of profits by Czech subsidiaries to their foreign parent companies, other than the obligation of joint stock and limited liability companies to generate a mandatory reserve fund. Dividends may be subject to withholding tax unless eliminated or reduced by a treaty or EU regulations.

Taxation of Labour Cost

The personal income flat tax rate is 15%. The tax base is, however, increased by the employer’s social security and health insurance contributions. Therefore the effective tax rate is approx. 20%.2

1 An increase in both VAT rates by 1%, or the unification of VAT rates at 17.5%

from January 2013 is currently being discussed in the Czech Parliament. Source: Ernst & Young 2 As of 2015, the flat tax rate should be 19% on gross salary. Source: Ernst &

Young

Social security and health insurance contributions (34% employer’s share and 11% employees’ share) are capped at the level of EUR 48,000 p.a. for social security and EUR 72,000 p.a. for health insurance contributions.3

Incentives available for BPO, SSC and R&D investments

When assessing a site selection process for the BPO/SSC and R&D industry, public aid is always one of the most important points on the agenda. The most popular available sources of state aid for this type of investment in the Czech Republic are:

Investment incentives R&D tax relief

Investment Incentives

Investment incentives are available to investors launching or expanding:

R&D centers Strategic service centers, i.e.:

– Shared services centers – Software-development centers – High-tech repair centers

Investment incentives can be obtained in the following forms:

Corporate income tax relief for 10 years Transfer of land at a discount Job creation grants of CZK 50,000 (approx. EUR 2,000) per

employee in selected regions Training and retraining grants of 25% of eligible training

costs Cash grants on capital expenditures for R&D centers in the

case of strategic investment The key qualification conditions for SSC: creation or expansion of a SSC center creating at least 100 new jobs or 40 new jobs for software-

development centers

The key qualification conditions for R&D centers:

creation or expansion of an R&D center investment in long-term tangible and intangible assets of at

least CZK 10 mil (approx. EUR 400,000), of which at least CZK 5 mil (approx. EUR 200,000) must be invested in new machinery

creating at least 40 new jobs

3 Cancellation of cap for health insurance (9% employer's contribution and 4.5%

employee's contribution) since January 2013 is currently being discussed in the Czech Parliament. . Source: Ernst & Young

4 Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012

Strategic investment:

A strategic investment in the area of R&D centers is considered to be an investment wherein the minimum amount invested in long-term tangible and intangible assets is CZK 200 mil (approx. EUR 8 mil), of which CZK 100 mil (approx. EUR 4 mil) represents new machinery. At least 120 new jobs need to be created.

Cash grants on capital expenditures can be provided at up to 5% of the eligible costs (max. CZK 500 mil, approx. EUR 20 mil).

The maximum state aid is 30-40% (depending on the region) of either the investment costs or two-year employment costs.

Regional map of state aid intensity in 2007- 2013

Example 1

Type of investment: SSC

Level of new employment: 250 new jobs

Average gross monthly remuneration: CZK 38,000/person (approx. EUR 1,520)

Maximum level of support: 40% x (250 jobs x CZK 38,000 x 24 months) = CZK 91.2 mil (approx. EUR 3.6 mil)

Example 2

Type of investment: R&D center

Level of new employment: 150 new jobs

Value of investment: EUR 20 mil

Maximum level of support: 40% x EUR 20 mil = EUR 8 mil, of which EUR 1 mil is a cash grant on capital expenditures and EUR 7 mil is a tax holiday for 10 years

Source: Ernst & Young

R&D Tax Relief

Companies with R&D activities can apply a special deductible item in respect of R&D costs. Eligible costs are thus deducted twice – once as operating costs and, for the second time, as a special deduction. There is no condition for ownership of the

result of research and development. Therefore, companies conducting R&D activities for their customers who will become IP owners can apply the deduction.

Eligible costs include personnel costs for employees involved in project implementation (including health-insurance and social-security costs), travel costs associated with the project, depreciation of assets used in direct connection with the project and other directly related operating costs, such as the costs of materials, supplies, energy, heating, gas and telecommunications charges.

Examples of companies which have entered the Czech Republic with BPO / SSC activities

Company City Project Started

No. of Employees

IBM Brno 2001 2600

Accenture Prague 2001 1500

DHL Prague 2004 1300

Tieto Ostrava 2005 1300

ExxonMobil Prague 2004 1100

GE Money Ostrava 2004 800

Sun Microsystems Prague 2005 600

Honeywell Prague 2006 500

SAP Prague 2004 450

HSBC Ostrava 2007 440

Johnson & Johnson Prague 2006 400

Infosys Brno 2003 400

Siemens Prague 2003 320

GTS Central Europe Holdings

Prague 2011 294

Pixmania Brno 2011 250

DSG International (Dixons Retail)

Brno 2011 230

ADP Pilsen 2005 110

Red Hat Brno 2006 100

Teradata Prague 2008 225

Slavia Capital Ostrava 2008 225

IBM Prague 2008 120

TeLogic Liberec 2008 120

AVG Technologies Brno 2008 120

Gardner Denver Brno 2011 50

FNZ (Czechia) Brno 2010 50

Source: CzechInvest, 2012

An important condition for using the deductible item is the preparation of written documentation of the research and development project describing in particular the objectives and processes.

Source: Czechinvest

Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012 5

In the case of doubt, tax authorities can be requested to provide a binding ruling that the relevant costs can be included in the special deductible item for R&D.

These companies have received support through CzechInvest and advisory companies such as Ernst & Young, who’s services support investment activities to the greatest extent possible, not only through information, consulting and after care services, but also through utilisation of EU structural funds.

Drivers of shoring activity

Despite the depth of change over the past four years, many of the original drivers of shoring remain as summarised in the following table.

Although there has been some consistency in the drivers of shoring activity - there are also signs of an evolution and growing sophistication in the way companies make location decisions. For one, the operational volatility of the last four years has seen risk mitigation move up the agenda, and become a core consideration of both location and real estate strategies. We have also seen changes in the comparative advantages of competing locations, as labour costs, currencies and growth rates fluctuate.

Driver Trend Productivity The ability to achieve greater

productivity and margin improvement through the (re)location of business functions is of growing importance

Labour The potential to access and retain appropriate labour pools and talent is becoming more challenging

Cost Cost arbitrage is a usually a key benefit, however there is growing variation in how the financial benefits of solutions are measured.

Revenue growth Increasingly shoring decisions are being linked to revenue growth, as a potential access route into new markets

Risk Management Managing supply chain and operational risk is emerging as a key driver of shoring and location decisions

Source: Jones Lang LaSalle

Labour Market The results compiled by international consulting companies indicate that the Czech Republic is a very attractive location for foreign investors and is even more interesting for SSC or R&D projects. Highly important factor is the quality of Czech workers, who are highly valued for their theoretical experience gained in high-quality educational institutions, as well as their practical experience, flexibility, ability to improvise, availability and ever growing skills.

The unemployment rate is forecasted to have decreasing trend and by the end of Quarter 2 was represented by 6.7 % for the Czech Republic.

The decrease stems from relatively strong economic outcomes. People still prefer more stable jobs and are loyal to their employer and are pretty flexible in terms of their salary demands and expectations. Attrition rate in Czech Republic within SSC / BPO is around 10-18 % and is dependent on several factors such as region, size of the company, salary package or benefits.

Based on our experience and market trends 90 % of employees in SSC/BPOs 90 % are University Graduates (60 % Msc Degree), 10 % has undertaken Postgraduate Education, 70 % are women, 98 % knows at least 1 foreign language, 40 % knows two foreign languages, 70 % has a work experience gained abroad. Czech employees are in the past 2 years more willing to travel what is connected with “national flexibility”.

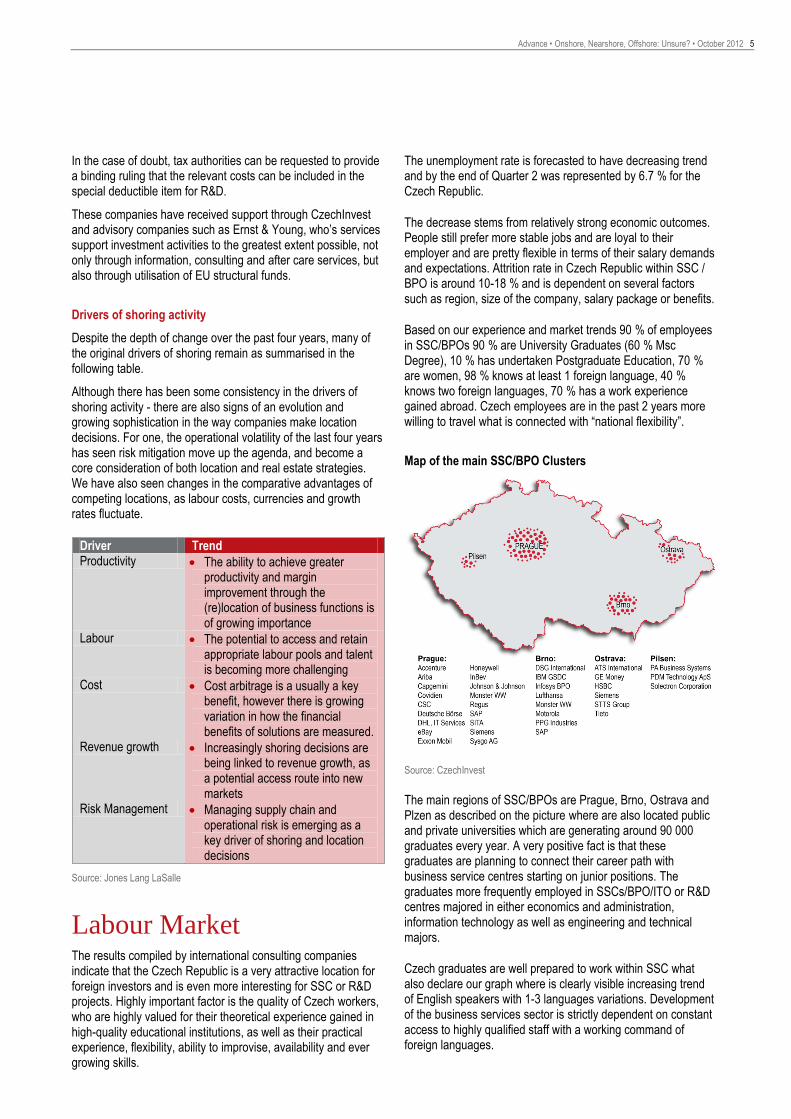

Map of the main SSC/BPO Clusters

Source: CzechInvest

The main regions of SSC/BPOs are Prague, Brno, Ostrava and Plzen as described on the picture where are also located public and private universities which are generating around 90 000 graduates every year. A very positive fact is that these graduates are planning to connect their career path with business service centres starting on junior positions. The graduates more frequently employed in SSCs/BPO/ITO or R&D centres majored in either economics and administration, information technology as well as engineering and technical majors.

Czech graduates are well prepared to work within SSC what also declare our graph where is clearly visible increasing trend of English speakers with 1-3 languages variations. Development of the business services sector is strictly dependent on constant access to highly qualified staff with a working command of foreign languages.

6 Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012

Knowledge of Foreign Languages in the Czech Republic

Source: Hays Czech Republic

Labour Costs

Key factors influencing the salary level: Required professional skills as well as sector experience;

Knowledge of foreign languages: fluency as well as popularity of the certain language (in the case of niche languages, such as Dutch or Nordics, salary expectations might increase up to 60%);

Combination of knowledge of foreign languages with required skills (e.g. combination of IT expertise with a foreign language knowledge other than English is not common);

Availability of specific skills in the local market (e.g. number of philology graduates from the local university);

Attractiveness of the market and quality of life, in case relocation of talents is required. Standards of living might also influence the attrition rate;

Market saturation and business environment within the sector;

Employer brand and recognition.

Within the knowledge based service sector average wages may vary depending on the talent pool available on the market.

Knowledge of Multiple Foreign Languages

Source: Hays Czech Republic

Situation within the R&D area

Hays Czech Republic monitors the continuing interest of candidates in companies operating in the field of R&D. This primarily concerns specialization in the sectors of information technologies, mechanical engineering and industrial automation. The following factors constitute the reasons for the growth of this field: • Investors with technologically interesting projects are entering

the Czech Republic, thus raising the sector’s prestige. • Prestigious projects are attractive not only for experienced

candidates, but also for university graduates, of whom the Czech Republic has an abundance. There is a long tradition of technical education here. The result is that the ratio of the total number of graduates to the number of graduates with a technical education is one of the highest in the world. The system of university education strongly supports cooperation with the private sector.

Comparison of Salaries (EUR) in the Business Services Sector across the CEE region

Poland Slovakia Czech Republic Hungary

F&A Processes - GL Min Max Min Max Min Max Min Max

Junior Accountant 750 950 620 900 950 1,150 750 1,100

Accountant 850 1,200 800 1,000 1,150 1,650 900 1,300

Team Leader 1,800 2,450 1,600 2,200 1,650 2,250 1,700 2,200

F&A, CS Processes (AP/AR CC)

Junior Associate 550 800 420 750 650 1,000 600 950

Associate 700 950 600 900 800 1,200 750 1,000

Team Leader 1,100 2,000 1,000 2,000 1,300 2,050 1,250 2,050

IT Processes

Junior IT Specialist 750 1,050 700 1,000 1,000 1,200 850 1,200

IT Specialist 950 1,550 900 1,400 1,100 1,650 1,100 1,450

Team Leader 1,950 2,900 1,800 2,600 1,850 2,900 1,700 2,700

Managerial level

Process Manager 2,200 3,600 1,900 3,500 1,900 3,550 2,200 4,000

SSC / BPO Director 6,000 10,000 5,200 9,000 5,500 10,000 6,000 10,000

Source: Hays Czech Republic - Note: Exchange rate: 1 EUR = 4.12 PLN; 24.61 CZK; 294.53 HUF

6%

32%

23%

20%

4%

4% 3%

3% 3% 2%

No language

English

German

Russian

French

Polish

Italian

Hungarian

Spanish

Nordics

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

2006/2007 2007/2008 2008/2009 2009/2010 2010/2011

Students of 1 foreign language Students of 2 foreign languages

Students of 3 foreign languages Graduates Total

Graduates (Ba)

Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012 7

• In the last three years we have recorded growth in the number of employees who have gone abroad, e.g. to France, the UK, Germany or Switzerland, after graduating from university in a technical field. These employees possess pertinent know-how and return to the Czech Republic in management positions requiring practical experience and strong language skills. According to the Engineering and IT Division of Hays Czech Republic, we have an abundance of skilled managers in the area of R&D in the Czech Republic and the number of their future successors are also growing.

Total number of employees in R&D 75,000

R&D workers employed in the commercial sphere

33,000

Employees in university projects 22,215

Percentage of R&D workers with university education

44 %

Percentage of R&D workers with a PhD degree

26 %

Average salary of R&D workers (three year’s experience, Prague)

EUR 1745.36/ month

Number of students in technical fields in the Czech Republic

90,000

Source: Hays Czech Republic

We must also point out that potential employers are able to hire experienced, high-quality employees for a fraction of the costs common in, for example, Germany or Switzerland. Knowledge of the English language is of key importance for most foreign investors, while demand for German-speaking candidates is rising. The system of university education focused on technical fields produces a sufficient number of graduates who are flexible in terms of the locations where they are employed. Therefore, they are more available now than in the past. Hays Czech Republic records the largest group of graduates and candidates for positions in R&D centres in the regions of Prague, Brno, Liberec, Ostrava and Mladá Boleslav. The fact that the R&D field is continually growing is supported not only by the number of employees placed in such positions, but also by feedback concerning employees, who fully meet the expectations of their employers and thus help them to build a strong foundation for their business.

Statutory Employers Cost

Social security

Sickness insurance 2.3 %

Retirement / pension insurance 21.5 %

Employment insurance 1.2 %

Health security 9.0 %

Total on top of salary paid by employer 34 %

Source: Hays Czech Republic

Additional costs

Optional Benefits Costs – average annually CZK / per head

1 extra week of holidays (over 80% companies)

Based on employees´ monthly gross salary

Lunch Vouchers (over 76% companies)

6.000–12.000 (240-600 EUR) per employee annually (1 day average contribution is 40-60 (1,6-2,4 EUR)

Cafeteria / flexible benefits for culture etc. (around 30% companies)

6.000–15.000 (240-600 EUR) per employee annually

Health Care Benefits (common in organizations where expats are working)

0–24.000 (0-960 EUR)

Trainings and Development programs

5.000–40.000 (200-1600 EUR) up to seniority level

Czech standards in SSC/BPOs/CS

Optional relocation package (work permit service if necessary).

1 extra week of holidays per year.

2-6 paid sick days per year.

Contract for unlimited period of time, rarely limited contract for 1 year.

Source: Hays Czech Republic

Labour law

A trial period of up to 6 months can be agreed with so-called managerial/leading employees entitled to determine and assign tasks and give instructions to their subordinates and to organise and control their work.

The trial period of a maximum 3 months, applicable to other employees, regular staff.

Employment for an indefinite period is the most common in the Czech Republic, preferred by both parties (employer and employee).

Employment for a definite period concluded between the same contracting parties may not exceed 3 years. From the day when the first employment for a definite period is concluded, this employment term may be repeated twice only. Extended employment will be considered repeatedly concluded employment.

Previous employment for a definite period will no longer be taken into account three years after the end of the last employment for a definite period (until 12/2011 it was six months).

8 Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012

Severance

Employment lasted < 1 year employee is entitled to 1x average monthly earnings

Employment lasted > 1 and < 2 years employee is entitled to 2x average monthly earnings

Employment lasted > 2 years employee is entitled to 3x average monthly earnings

Source: Hays Czech Republic

Other information

Notice period: 2 months by law, or agreement

Holidays/year: 20 days by law

Bank holidays: 13

Working hours/week: 40 (usual)

Sick Leave: 1st – 3rd day no reimbursement, 4th – 21st day reimbursed by employer, 22nd + day reimbursed by state

Source: Hays Czech Republic

Real Estate It is not just the demand for offshoring that has undergone change over the past 4 years. The supply conditions and real estate challenges posed to those companies seeking an offshore solution have also evolved. Sourcing appropriate real estate in often remote offshore locations has always been one of the challenges of the offshoring process. These challenges remain in many locations, however in some of the more mature offshoring markets such as Central and Eastern Europe the market is evolving to better meet the needs of international demand. Turnkey solutions for shared service centres are emerging in some locations, which increase speed to market and eradicate out some of the additional difficulties and risks encountered in fitting out a service centre to a suitable standard. Fit-out and specification standards are increasingly varying between locations with on the ground real estate expertise and due diligence an essential requirement for those seeking to fully mitigate risk.

Office Markets of the Czech Republic

The main office market in the Czech Republic is in the Capital city of Prague, followed by Brno, and Ostrava. About 80% of the total office stock is situated in Prague. In Brno and in Ostrava there is approximately 10% and 5% respectively.

Prague

By the end of Q2 2012 the total A and B class office stock in Prague stood slightly above 2.8 million m2 with a vacancy rate of 11.52%. Out of which, the A class office stock totalled 1 986 844 m2. Approximately, 72% of the total office stock is formed by new built projects with the largest office districts in

Prague 4 (27% of the total stock), Prague 1 (15%) and Prague 5 (15%). Altogether, almost 100,000 m2 of new office space should be delivered in Prague in 2012.

Brno and Ostrava

Brno and Ostrava are two second largest cities of the Czech Republic. Brno with its 378,575 inhabitants and Ostrava with 300,745 of inhabitants are well known locations of many international brands. In Brno and in Ostrava there are situated big universities. Therefore, in both cities we can find large educated and cheap labour force. Mainly Brno, home of technological and science universities, is recognized as a destination for technology centres, R&D centres, and back offices.

Other Regional Cities

Office stock in other regional cities is quite limited. New developments in this area are very scarce. The positive side to occupiers in these cities is a less saturated labour market with a sufficient skilled labour pool.

H1 2012 Key Office Market Indicators

City Stock m2 Vacancy Rate Prime Monthly Rent EUR / m2

Prague 2,857,200 11.50% €20 - €21

Brno 388,900 14.60% €11 - €13.5

Ostrava 161,000 19.60% €10 - €12.5

Pilsen 52,000 20.50% €9 - €11 Source: Jones Lang LaSalle Q2 2012

The Czech office markets are currently well supplied to accommodate a wide range of size requirements and have sufficient pipelines going forward to manage further expansion and new demand. It is understood that when setting up business, particularly in outsourcing or shoring, it may take one or two years to build up to full strength. In this respect, landlords and owners are flexible in managing these growth phases. Many projects are also phased, so this can work in the favour of both parties, but importantly offer occupiers expansion and growth opportunity with minimum relocation costs.

Demand

Demand for office space in the Czech Republic is relatively stable. The market gradually absorbs the volumes of office stock delievered to market prior to 2009. The average 10 year gross demand is 225,702 m2.The strongest segments from which the tenants recruit remains banking, finance and insurance sectors, manufacturing, pharmaceutical and IT sectors. With the ongoing turmoil in Europe the demand from shoring activities has slowed down. The new drivers for relocation will be green sustainable premises and new modern offices.

Supply

Some of the most successful existing or upcoming projects in the Czech Republic include: • City West by FINEP in Prague 5 • The Park by AIG Lincoln in Prague 4 • BB Centrum by Passer Invest in Prague 4 • Futurama Business Park by Immorent in Prague 8

Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012 9

• Spielberk and Axis by CTP Invest in Brno • Campus by AIG Lincoln in Brno • Nova Karolina Park by Passerinvest in Ostrava • IQ Ostrava Office Park by CTP in Ostrava • Nordica by Skanska in Ostrava • The Orchard by Red Group in Ostrava • Fabrika by Immorent in Pilsen

All of these developers plus many others on the market have a long track record of providing high quality projects. In cooperation with experienced real estate advisors, a great deal of thought has been given to the end user.

Rents

As the chart suggests, today the market is an occupiers market with tenant favourable conditions. Due to a limited pipeline of speculative development over the next few years, the market is likely to move slowly towards a landlords market, unless the conditions for speculative development become more favourable, which will accelerate the change in trend.

Optimal Timing for Occupiers in the CR 2012-2015

Market 2012 2013 2014 2015

Prague

Brno

Ostrava

Tenant-favourable market conditions

Relatively balanced between landlord and tenant market conditions Landlord favourable market conditions

The chart below indicates both the market size and average rents in main office markets of the Czech Republic. The prime rents in Prague reach up to €21 in the city centre however the average rents are much lower. In many cases the interantional tenants are more driven by the nature of the labour market in the destination city rather than by achievable rents. For many clients Prague has become an option for similar rents in non prime projects, compared to top projects in a regional city.

“SAP Business Services Centre for Europe, Middle East and

Africa (SAP BSCE) has been established in 2004 in Prague as a

separate SAP legal entity with the clear purpose to become the

best-in-class shared service provider. This was to address the

trend in globalization.

As our core business at SAP was becoming global, the

administrative processes followed the globalization model.

Another important decision factor in this process was the idea to

showcase our business model embedded in our own software to

the potential but also established customer’s base considering

the move towards internal shared service. Last but not least, at

the beginning of this journey – the lower cost base in Prague

compared to the Western European levels, with its advanced

telecommunications & IT infrastructure also played an

important role in favor of Prague as the right location.

Besides political stability, a solid economic environment, and

accessibility from a logistical perspective, the availability of

qualified personnel played a key role in the location selection as

well. SAP BSCE is very well accessible from the airport as well

as from the Prague city centre, which is a positive fact for our

frequent SAP visitors.

Our current premises are very well accessible by public

transportation and that is favourable for the daily commuting of

our employees. Over the past years the centre has expanded to

today’s workforce of around 450 heads providing services in the

areas of Finance, HR, Procurement and Marketing Data

Management to all SAP legal entities in more than 70 countries.

The workforce of SAP Business Services Center for EMEA is

recruited from young professionals – mostly graduates of

universities that are located in Prague or vicinity but also from

abroad as Prague has become a multi-cultural city that is

attractive to foreign professionals as well.”

Ing. Andrea Hepnerová, MBA

Managing Director of SAP BSCE, s.r.o.

Availability of office space (Over 2,000 m2 including buildings due in 2012) and rents in the Czech Republic

Source: Jones Lang LaSalle

Availability

Large Medium Small Very Small

10 options and more 10-4 options 3-2 options 1 or less options

Size of the market (m2)

Including owner-occupiesRen

ts

€/m

2 /mon

th

6

18

16

14

12

10

8

Prague Inner City

Prague Outer City

Prague City Centre

Brno

OstravaHradec

Kralove

Pardubice

Plzen

Liberec

Usti nad

Labem

<100.000 100.000-250,000 250,000-500,000 >1,000,000500,000-1,000,000

10 Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012

Office standards When selecting an office premises, it is common practice to find many high specification features as standard, in both Prague and within new developments in the regional cities. These include, but are not limited to: • Open plan floor plates • Raised Floors with floor boxes • Suspended ceilings with 500lux lighting • A/C or Heating/Cooling system (2 or 4 pipe system) • Individual thermostatic control boxes • To use a grid of 1.35 or 1.50m (if possible) • Parking ratio 1:50 where possible plus visitor parking • Kitchenettes (or preparation for kitchenettes) • In-house management • Logo Placement on the façade or Roof • Fully operational central Reception • Presentably designed navigation panels • 24 Hour Security and Access Systems

Leasing Practice

Lease Length

The average lease length is 5 years. In terms of offices, 3-5 years are common in the city centre and 5-7 years on the outskirts. In a few cases, longer leases can be agreed..

Payment terms Rents are usually quoted in Euro and paid quarterly in advance in either Euro or CZK. Please note that in the regional cities some landlords quote rents in CZK.

Rental deposit It is common to agree on a cash deposit or bank guarantee, equal to 3 months rent.

Rent reviews Indexation is annually in line with European CPI.

Other Charges Other charges consist of Service and energy charges. (Utilities and direct consumption are paid separately) Service charges are quoted in CZK. Insurance The landlord covers costs of building insurance (recovered by service charge). The Tenant covers insurance of own premises, contents and civil liabilities.

Incentives

Incentives may be offered by the landlord. This can typically

be in the form of rent free periods or fit-out contributions.

Summary This paper has provided a short overview on the aspects of relocating a business to the Czech Republic. The paper reviewed the four principle drivers - labour, real estate and infrastructure, and business environment - that ultimately influence location choice.

Among the top global destinations for foreign direct investment and shared service centres are currently mainly emerging markets in Southeast Asia (for example India and Philippines) and in South America (Argentina). However, some European countries such as Poland and Romania remain to be very sought-after locations, particularly due to their lower labour costs and strong potential for economic growth and development.

In the current economic environment it is evident the Czech Republic can hardly compete with the economic dynamics, historically given advantage in English language skills and low labour costs of India. In that view it will be probable that the Czech Republic’s strength would rather lay in nearshore rather than offshore concept. Compared to Poland and Romania, currently two strongest competitors of the Czech Republic in the region, the advantages of the Czech Republic are predominantly the educated labour force with very good language skills, industrial tradition, long term stability, good levels of market transparency and very good infrastructure.

We are convinced that the cities of the Czech Republic, from that point of view have the potential to provide a lower cost alternative to certain businesses. Prague, as the country’s capital offers very good conditions but, the labour and accommodation cost are higher than in other regions of the country. Nevertheless, some out-of-centre locations are still competitive in terms of accommodation cost and advantages of the capital city are increasing Prague’s attractivness. However, from a longer point of view we rather expect Prague to gradually establish as a centre for prime business and financial services. The other regional cities can be then split into two groups: the cities that have already attracted BPO/SSC business in the last decade and have established as important BPO/SSC centres. These include mainly Brno and Ostrava. The second group covers emerging cities represented by regional centres such as Pilsen, Hradec Králové, Pardubice, Liberec, Ústí nad Labem, Olomouc and České Budějovice. These are all university cities and as such are highly competivie in offering an educated workforce with language skills yet, at relatively lower cost. In addition, all of these cities have good infrastructure, very often including their own airport.

In summary, the conditions for setting up business in the Czech Republic, both from a labour and real estate perspective, remain very good and we expect that the potential of the country will be proven by new entrants in near future.

Advance • Onshore, Nearshore, Offshore: Unsure? • October 2012 11

Information on content providers Jones Lang LaSalle (NYSE: JLL) is a financial and professional

services firm specializing in real estate. The firm offers

integrated services delivered by expert teams worldwide to

clients seeking increased value by owning, occupying or

investing in real estate. With 2011 global revenue of $3.6 billion,

Jones Lang LaSalle serves clients in 70 countries from more

than 1,000 locations worldwide, including 200 corporate

offices. The firm is an industry leader in property and corporate

facility management services, with a portfolio of approximately

250 million square meters worldwide. LaSalle Investment

Management, the company’s investment management business,

is one of the world’s largest and most diverse in real estate with

$ 47 billion of assets under management. For further information,

please visit www.joneslanglasalle.com

Ernst & Young is a global leader in assurance, tax, transaction

and advisory services. Worldwide, our 152,000 people are united

by our shared values and an unwavering commitment to quality.

We make a difference by helping our people, our clients and our

wider communities achieve their potential. Ernst & Young refers

to the global organization of member firms of Ernst & Young

Global Limited, each of which is a separate legal entity. Ernst &

Young Global Limited, a UK company limited by guarantee, does

not provide services to clients. For more information about our

organization, please visit www.ey.com

Hays Specialist Recruitment is the world’s leading company in

recruiting qualified, professional and skilled work. Today, with

more than 40 years of recruitment experience, the Group

operates out over 245 offices in 33 countries, employing around

7800 staff worldwide across 20 specialisms. We offer tailor-

made recruitment services on permanent, contract and

temporary basis along with Executive Search, Recruitment

Process Outsourcing (RPO) and Employer Branding Solutions.

Our role is a straight forward but very important one: we power

the world of work by helping our clients find the best people they

need to develop their businesses and helping our candidates

find the best new role for themselves. Our customers benefit

from the specialist sector knowledge, extensive office network,

industry contacts and consultants experienced in recruiting staff

for various SSC/BPO centres across the CEE region. To find out

more about Hays please visit www.hays.com

Jones Lang LaSalle

Tewfik Sabongui Managing Director Jones Lang LaSalle Czech Republic +420 224 234 809 [email protected] www.joneslanglasalle.cz Petr Kareš Head of Tenant Representation Jones Lang LaSalle Czech Republic +420 224 234 809 [email protected] www.joneslanglasalle.cz Ondrej Novotný Head of Research Czech Republic Jones Lang LaSalle Czech Republic +420 224 234 809 [email protected] www.joneslanglasalle.cz

Alex Ash

Director – EMEA Location Consulting Services

Jones Lang LaSalle

UK

+44 207 852 4848

[email protected] www.joneslanglasalle.com

Content Partners

Ondrej Janecek

Partner, Tax Services

Ernst & Young

Czech Republic

+420 225 335 360

www.ey.com

Jon Hill

Managing Director

Hays Specialist Recruitment

Czech Republic & Slovakia

+420 724 352 982

www.hays.cz

October 2012 Advance publications are topic-driven white papers from Jones Lang LaSalle that focus on key real estate and business issues.

www.joneslanglasalle.cz

COPYRIGHT © JONES LANG LASALLE IP, INC. 2012. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written

consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains

no factual errors. We would like to be told of any such errors in order to correct them.