Embed Size (px)

Citation preview

OUTA Presentation to NERSA Eskom’s 2018/19 application

NOVEMBER 2017

1

TABLE OF CONTENTS q Introduction q Our Requests q Our Concerns q Declining Corporate Governance q Lack of Transparency q Regulatory Decision Making Process q Growing Inefficiencies q Recommendations q Concluding Remarks

2

3

q OUTAisaproudlySouthAfricannon-profitcivilac<onorganisa<on,supportedandfundedbythepublicwhoare passionate about improving the prosperity of ourna<on.

q OUTA was established to hold to account, those inauthority who abuse their power w.r.t. Tax Payersmoney.

INTRODUCTION

4

q TorecognisethatEskom’sprolongedtariffincreaseshaveenduredwithoutsufficientrestraintongrowinginefficiency,mismanagement,maladministra<onandcorrup<on.

q ThatNERSAinpartnershipwith(DPE,Na<onalTreasury,DPMEandDOE)assisttointroducerigorousaccountabilityofEskom’sleadershiptoacceptablelevelsofefficiency&corporategovernance.Ø ParadigmshiS(businessunusual).

q ThatNERSAdoesnotgrantapprovalforanytariffincreaseinEskom’s2018/19revenuerequirementapplica<on.

OURREQUEST

5

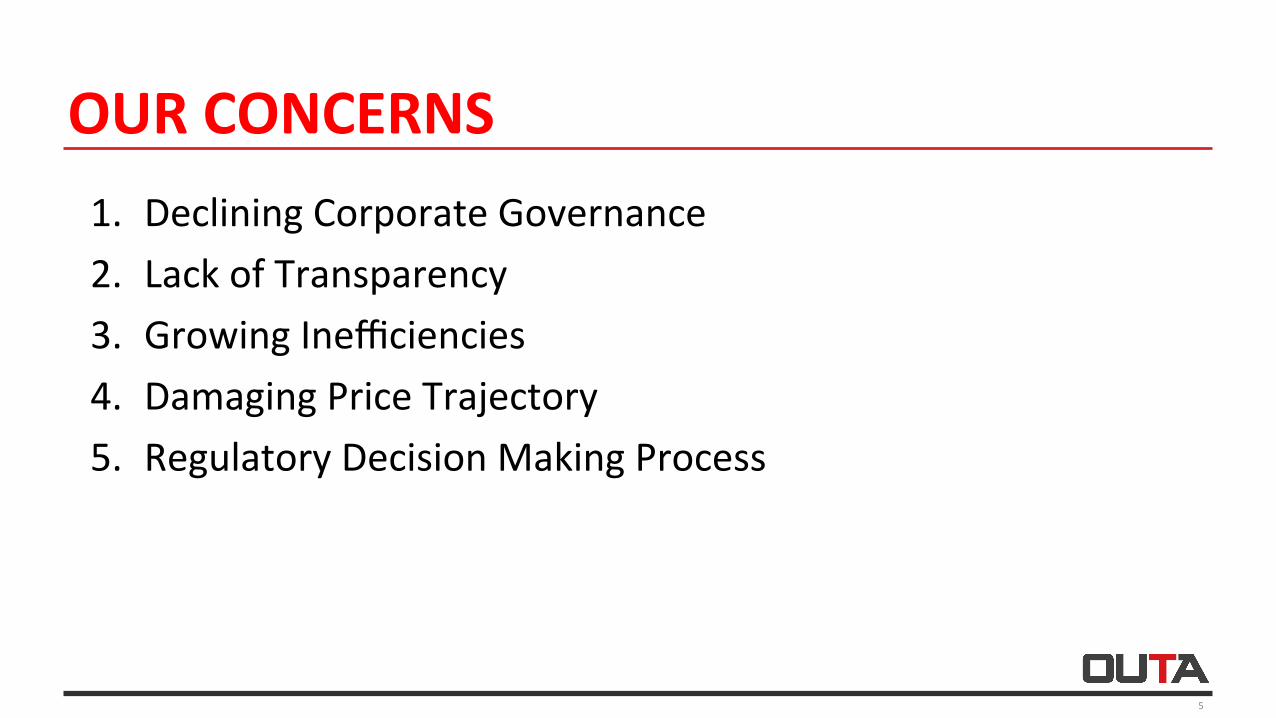

1. DecliningCorporateGovernance2. LackofTransparency3. GrowingInefficiencies4. DamagingPriceTrajectory5. RegulatoryDecisionMakingProcess

OURCONCERNS

6

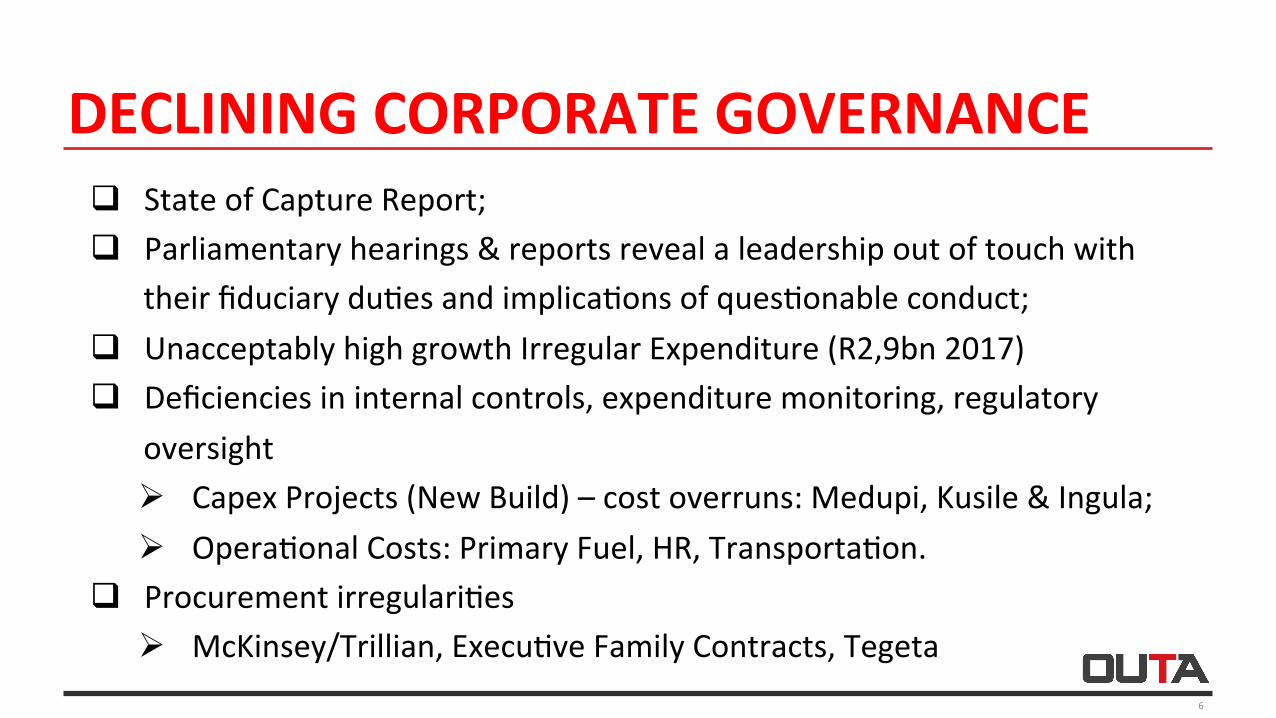

q StateofCaptureReport;q Parliamentaryhearings&reportsrevealaleadershipoutoftouchwith

theirfiduciarydu<esandimplica<onsofques<onableconduct;q UnacceptablyhighgrowthIrregularExpenditure(R2,9bn2017)q Deficienciesininternalcontrols,expendituremonitoring,regulatory

oversightØ CapexProjects(NewBuild)–costoverruns:Medupi,Kusile&Ingula;Ø Opera<onalCosts:PrimaryFuel,HR,Transporta<on.

q Procurementirregulari<esØ McKinsey/Trillian,Execu<veFamilyContracts,Tegeta

DECLININGCORPORATEGOVERNANCE

7

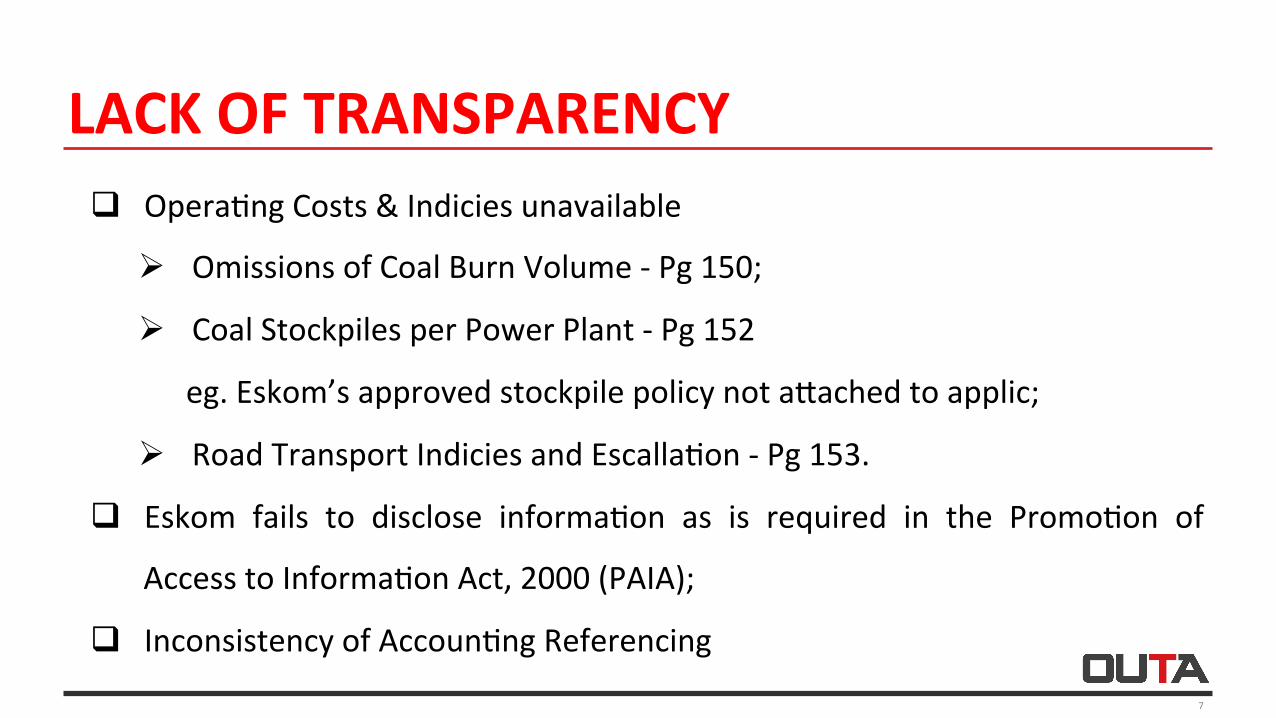

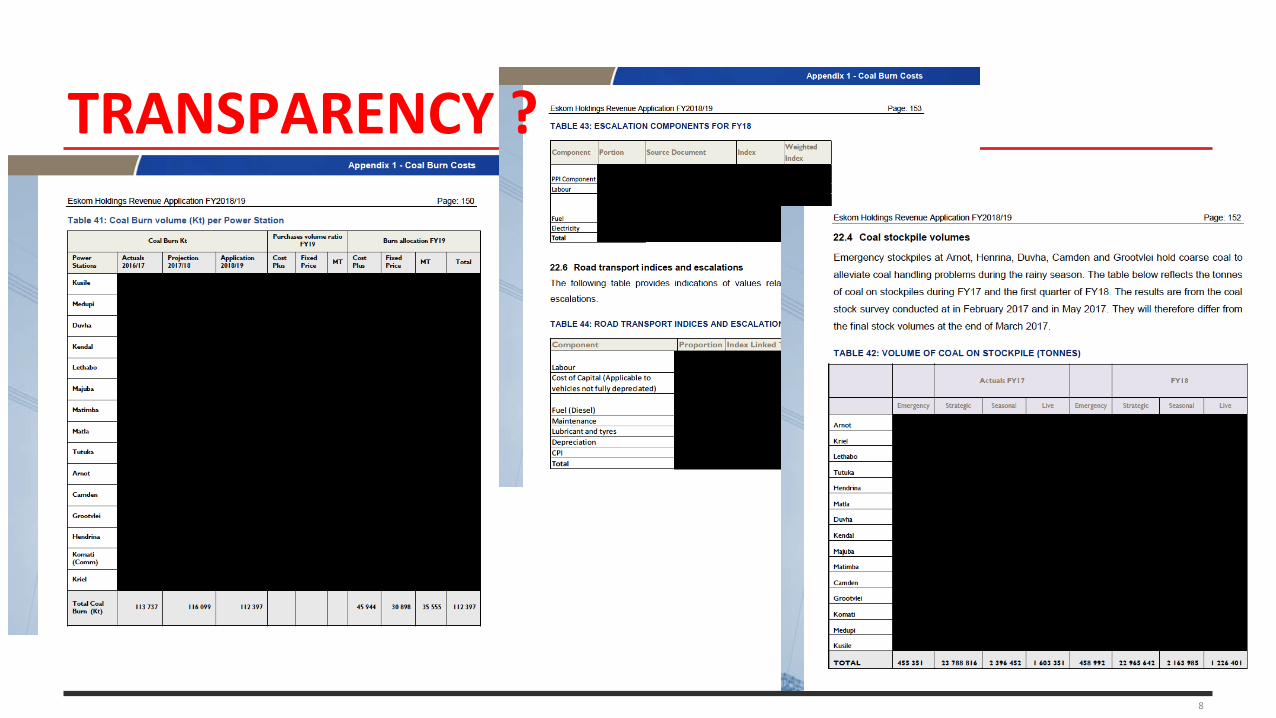

q Opera<ngCosts&IndiciesunavailableØ OmissionsofCoalBurnVolume-Pg150;

Ø CoalStockpilesperPowerPlant-Pg152

eg.Eskom’sapprovedstockpilepolicynotaiachedtoapplic;

Ø RoadTransportIndiciesandEscalla<on-Pg153.

q Eskom fails to disclose informa<on as is required in the Promo<on of

AccesstoInforma<onAct,2000(PAIA);

q InconsistencyofAccoun<ngReferencing

LACKOFTRANSPARENCY

8

TRANSPARENCY?

REGULATORY DECISION MAKING PROCESS q NERSA may use its discretion to in the application of the MYPD rules q Eskom’s lack (or inability) to provide full disclosure of material facts

hinders NERSA from making informed decision. q Is NERSA in a position to grant an increase? We believe not.

Ø NERSA cannot apply its mind objectively if not presented with relevant (and accurate) facts;

Ø Relevant facts = Accurate RAB, expenditure (coal procurement), etc

q Results in ineffective public participation (lack of transparency (incomplete /outdated information and data) – compromises integrity of the regulatory process.

9

10

q TheLegalframeworkrequiresthatEskommayonlyrecoveritscostsandearnareturnifitisan“efficientoperator”.

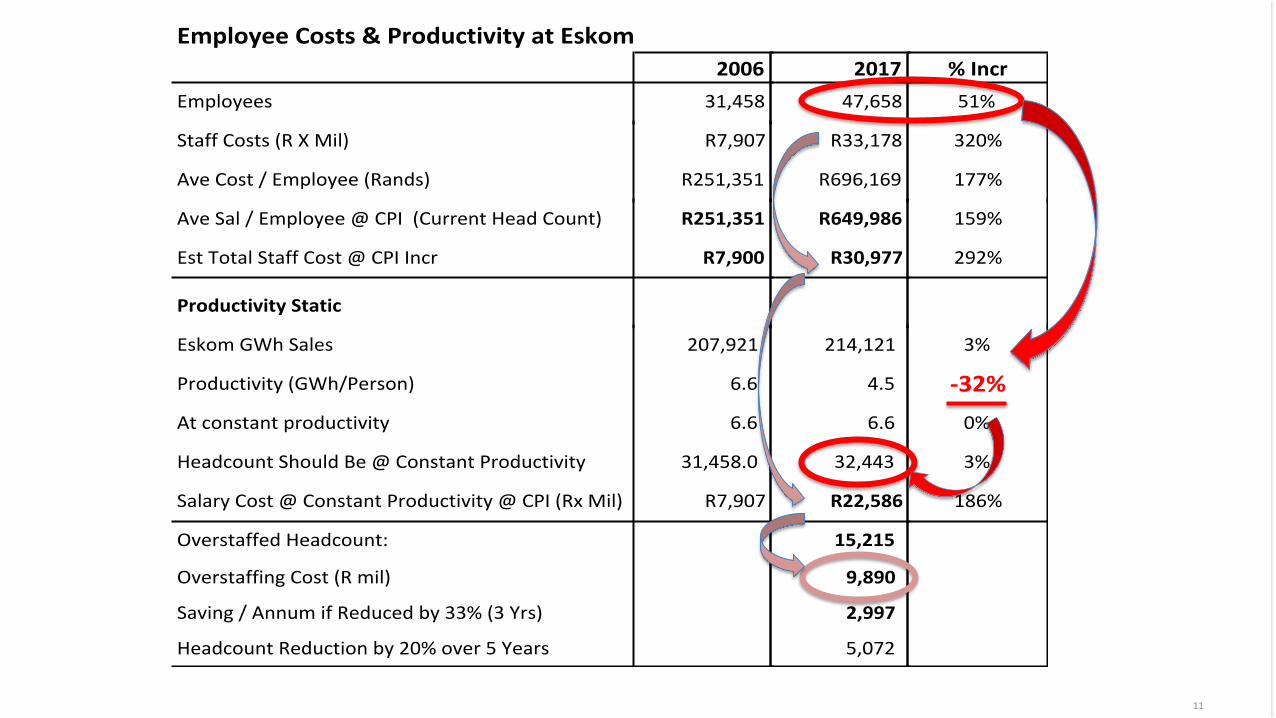

q Eskomhasbeenallowedtoincreaseitsheadcount/salarycostswellaheadofreasonableexpecta<ons,withproduc<vitydecliningby32%overpastdecade.

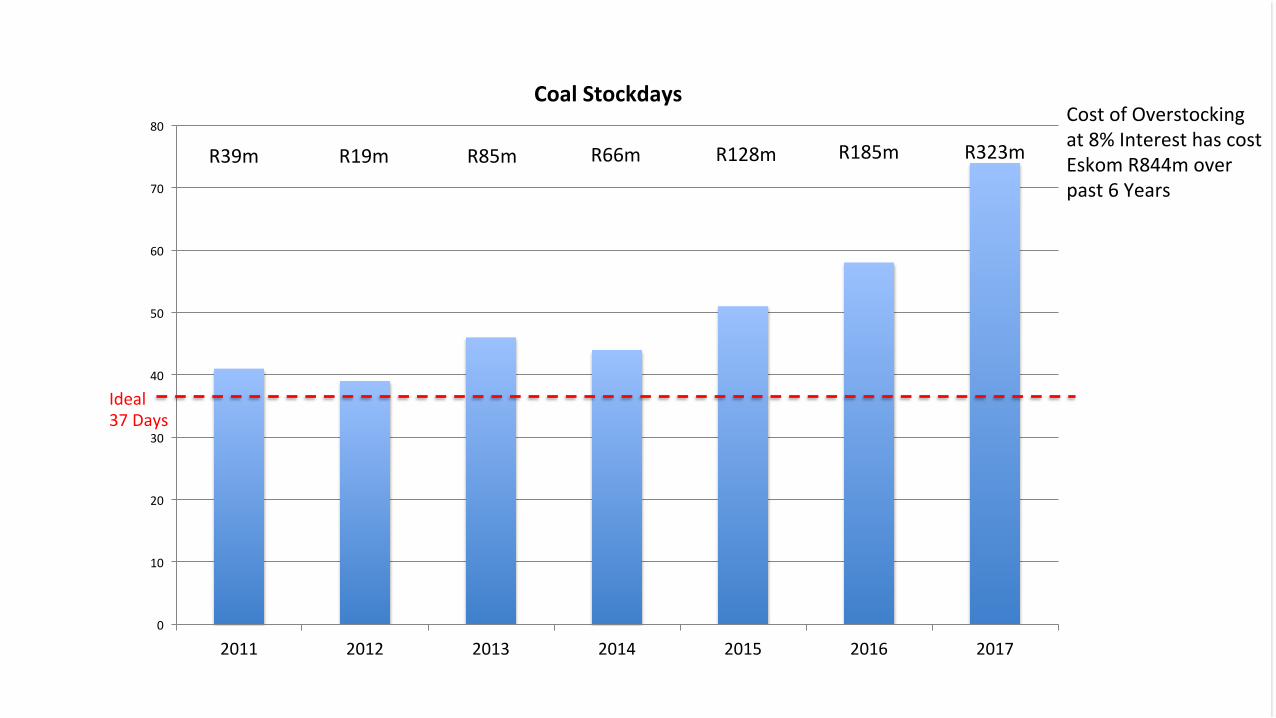

q CoalstockpileshavecostEskomalmostR1bninfinancecostsoverpast6years.

q Reportsofcoalqualityandauditprocessescompromised.

GROWINGINEFFICIENCIES

11

EmployeeCosts&ProductivityatEskom2006

Employees 31,458

201747,658

%Incr51%

StaffCosts(RXMil) R7,907

AveCost/Employee(Rands) R251,351

R33,178

R696,169

320%

177%

AveSal/Employee@CPI(CurrentHeadCount) R251,351

EstTotalStaffCost@CPIIncr R7,900

ProductivityStatic

R649,986

R30,977

159%

292%

EskomGWhSales 207,921

Productivity(GWh/Person) 6.6

Atconstantproductivity 6.6

HeadcountShouldBe@ConstantProductivity 31,458.0

SalaryCost@ConstantProductivity@CPI(RxMil) R7,907

OverstaffedHeadcount:

OverstaffingCost(Rmil)

Saving/AnnumifReducedby33%(3Yrs)

HeadcountReductionby20%over5Years

214,121

4.5

6.6

32,443

R22,586

15,215

9,890

2,997

5,072

3%

-32%0%

3%

186%

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015 2016 2017

CoalStockdays

Ideal37Days

CostofOverstockingat8%InteresthascostEskomR844moverpast6Years

R39m R19m R85m R66m R128m R185m R323m

13

R-

R100

R200

R300

R400

R500

R600

R700

R800

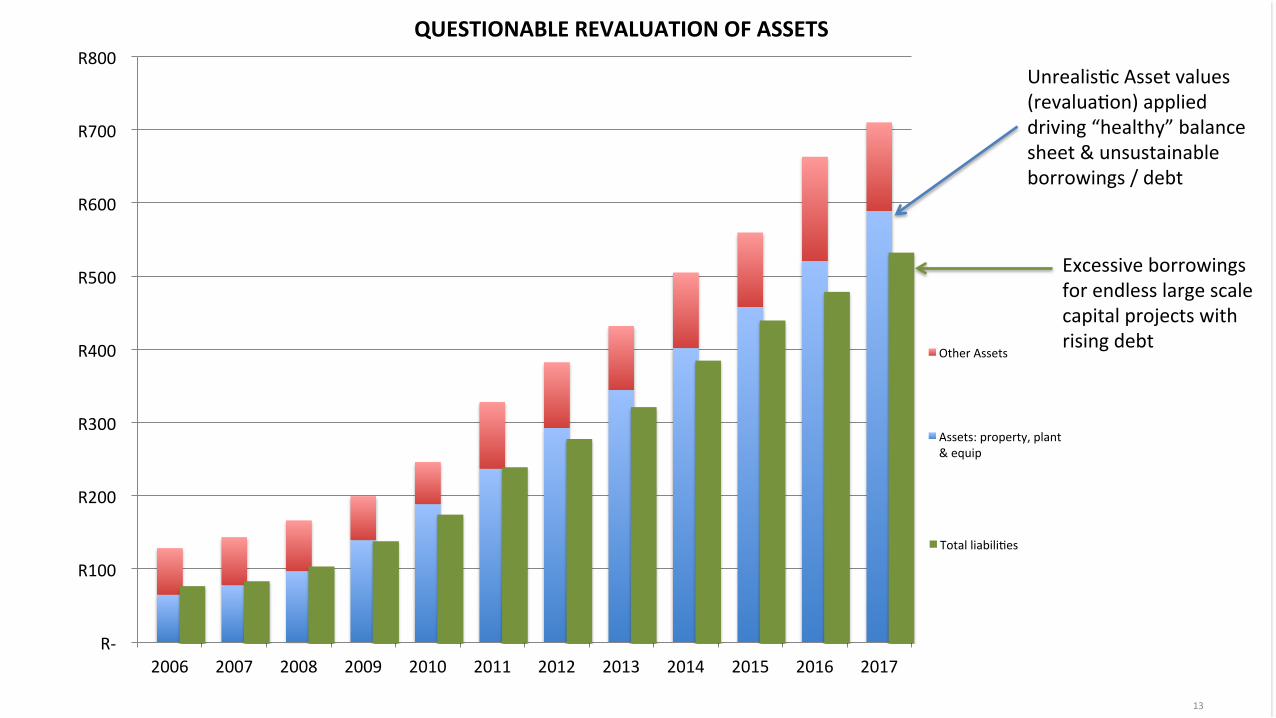

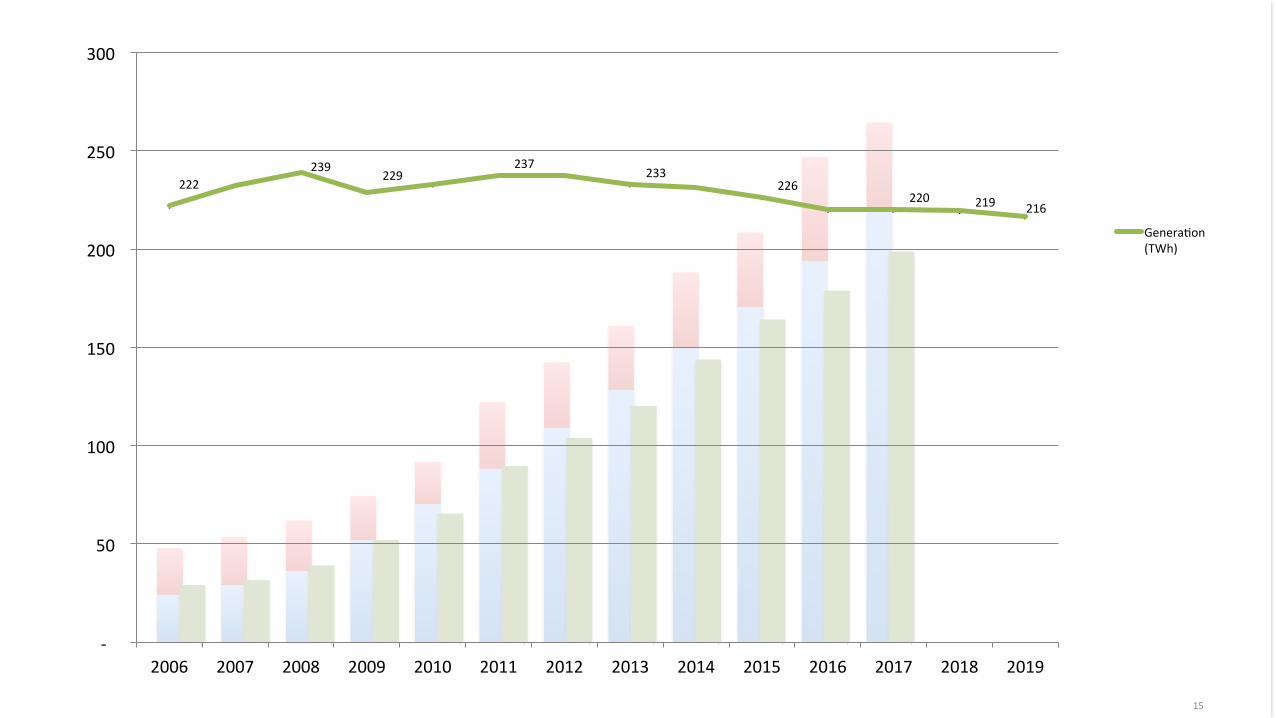

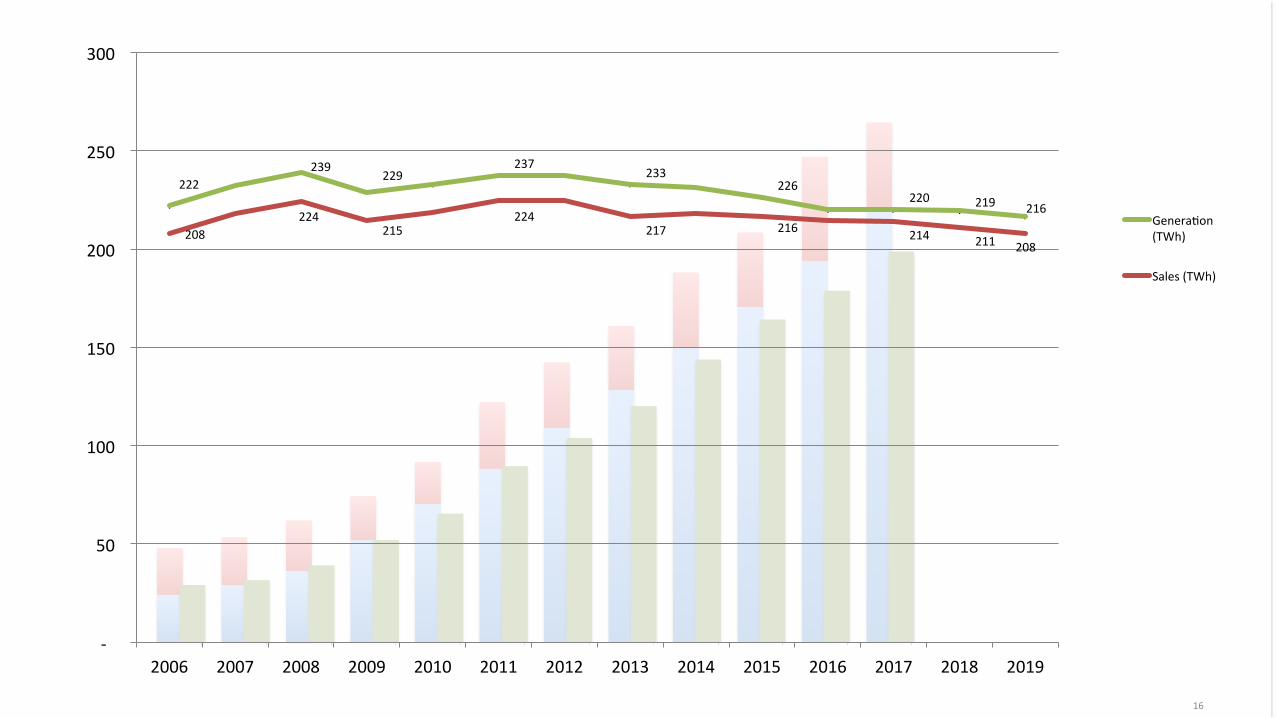

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

OtherAssets

Assets:property,plant&equip

Totalliabili<es

QUESTIONABLEREVALUATIONOFASSETS

Excessiveborrowingsforendlesslargescalecapitalprojectswithrisingdebt

Unrealis<cAssetvalues(revalua<on)applieddriving“healthy”balancesheet&unsustainableborrowings/debt

14

R-

R100

R200

R300

R400

R500

R600

R700

R800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

OtherAssets

Assets:property,plant&equip

Totalliabili<es

15

R-

R100

R200

R300

R400

R500

R600

R700

R800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

OtherAssets

Assets:property,plant&equip

Totalliabili<es

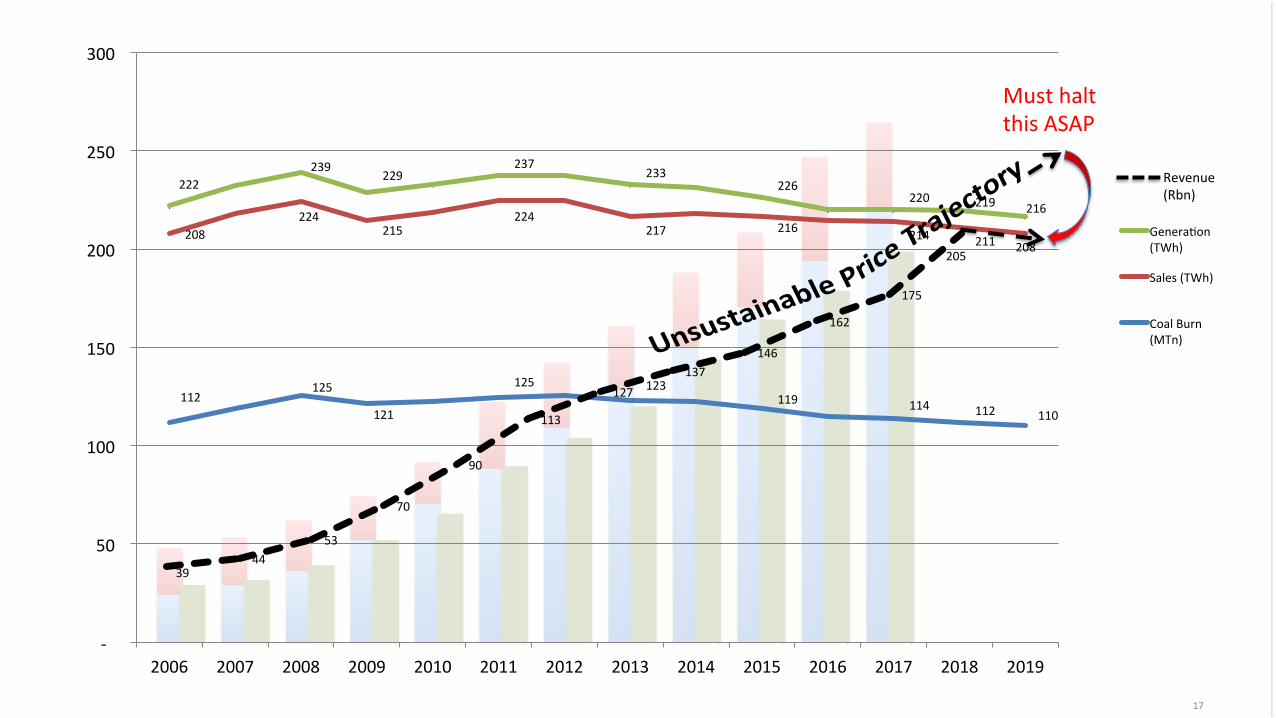

222239

229237

233226

220 219 216

-

50

100

150

200

250

300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Genera<on(TWh)

16

R-

R100

R200

R300

R400

R500

R600

R700

R800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

OtherAssets

Assets:property,plant&equip

Totalliabili<es

222239

229237

233226

220 219 216

208224

215224

217 216 214 211 208

-

50

100

150

200

250

300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Genera<on(TWh)

Sales(TWh)

17

R-

R100

R200

R300

R400

R500

R600

R700

R800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

OtherAssets

Assets:property,plant&equip

Totalliabili<es

222239

229237

233226

220 219 216

208224

215224

217 216 214 211 208

112125

121

125 123119 114 112 110

-

50

100

150

200

250

300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Genera<on(TWh)

Sales(TWh)

CoalBurn(MTn)

3944

53

70

90

113

127137

146

162

175

205

Revenue(Rbn)

MusthaltthisASAP

18

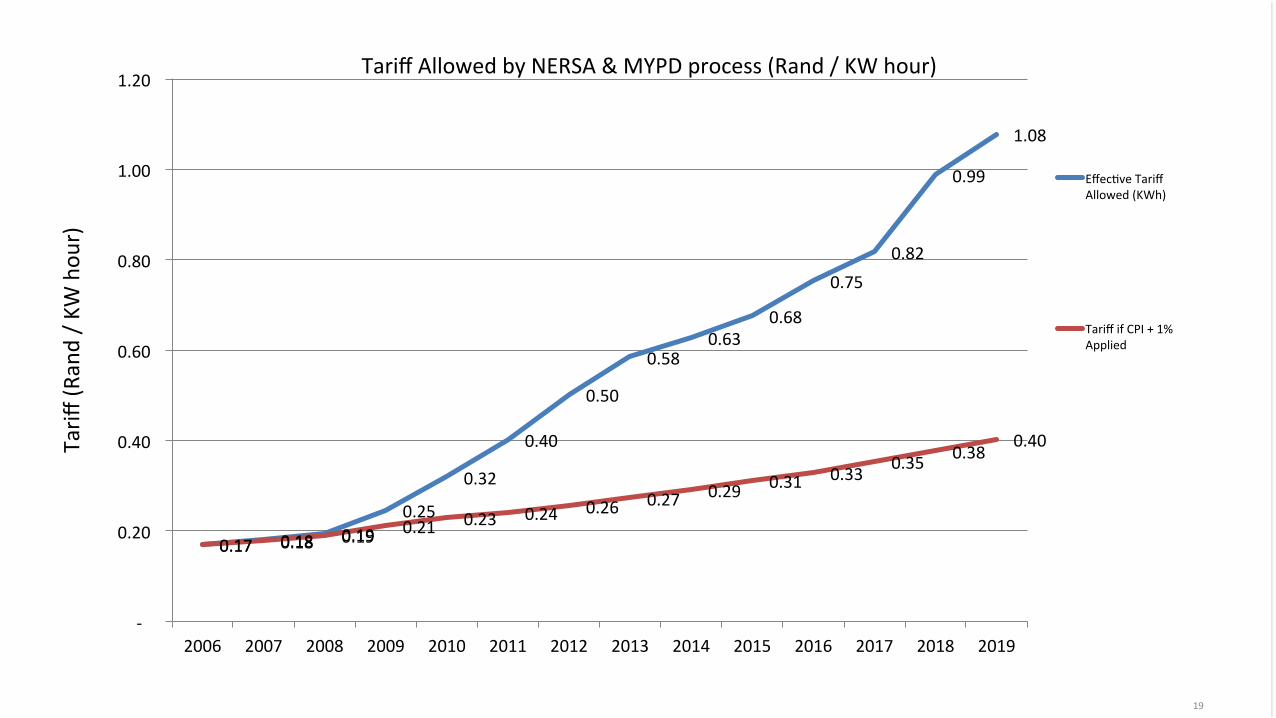

0.17 0.18 0.19 0.21 0.23 0.24 0.26 0.27 0.29 0.31 0.33 0.35 0.380.40

-

0.20

0.40

0.60

0.80

1.00

1.20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

TariffifCPI+1%Applied

TariffifCPI+1%Applied

Effec<veTariff

(Rand/K

Whou

r)

19

0.17 0.18 0.190.25

0.32

0.40

0.50

0.580.63

0.68

0.750.82

0.99

1.08

0.17 0.18 0.19 0.21 0.23 0.24 0.26 0.27 0.29 0.31 0.33 0.35 0.380.40

-

0.20

0.40

0.60

0.80

1.00

1.20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Effec<veTariffAllowed(KWh)

TariffifCPI+1%Applied

Tariff

(Rand/K

Whou

r)

TariffAllowedbyNERSA&MYPDprocess(Rand/KWhour)

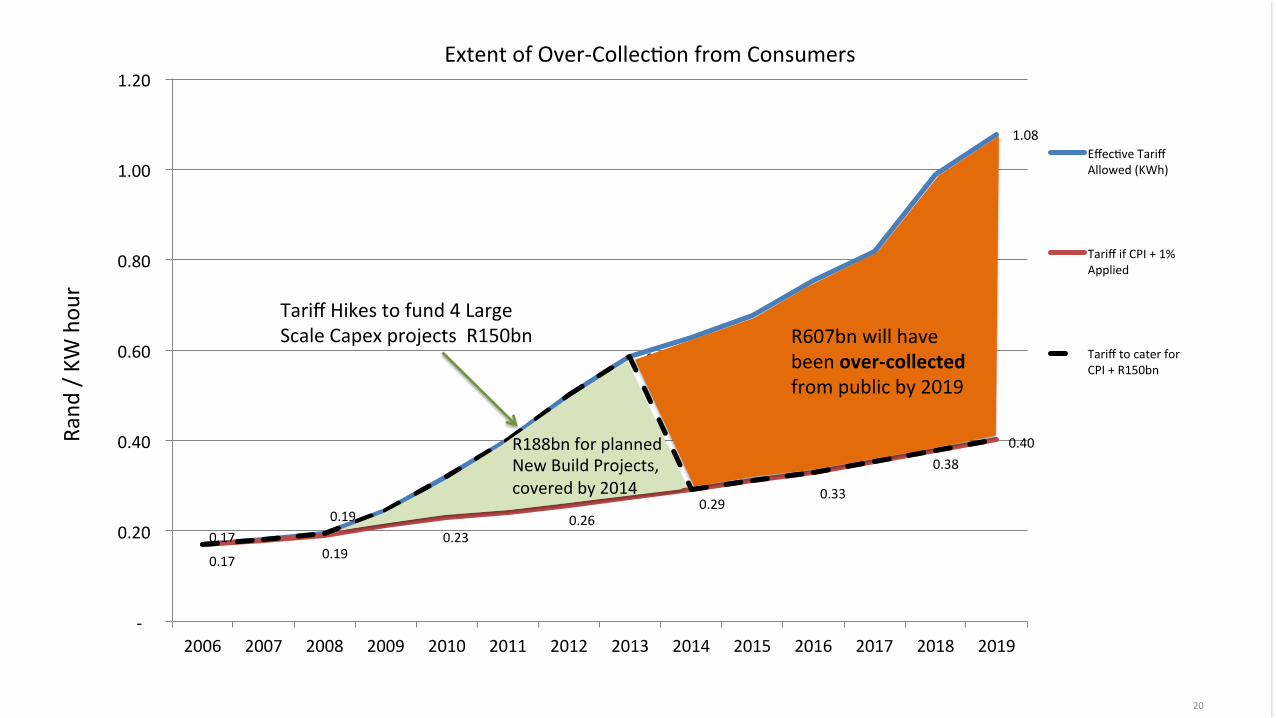

20

0.170.19 0.25

0.32

0.40

0.50

0.580.63

0.68

0.75

0.82

0.99

1.08

0.17 0.190.23

0.260.29

0.33

0.380.40

-

0.20

0.40

0.60

0.80

1.00

1.20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Effec<veTariffAllowed(KWh)

TariffifCPI+1%Applied

TarifftocaterforCPI+R150bn

TariffHikestofund4LargeScaleCapexprojectsR150bn

R188bnforplannedNewBuildProjects,coveredby2014

R607bnwillhavebeenover-collectedfrompublicby2019

Rand

/KW

hou

rExtentofOver-Collec<onfromConsumers

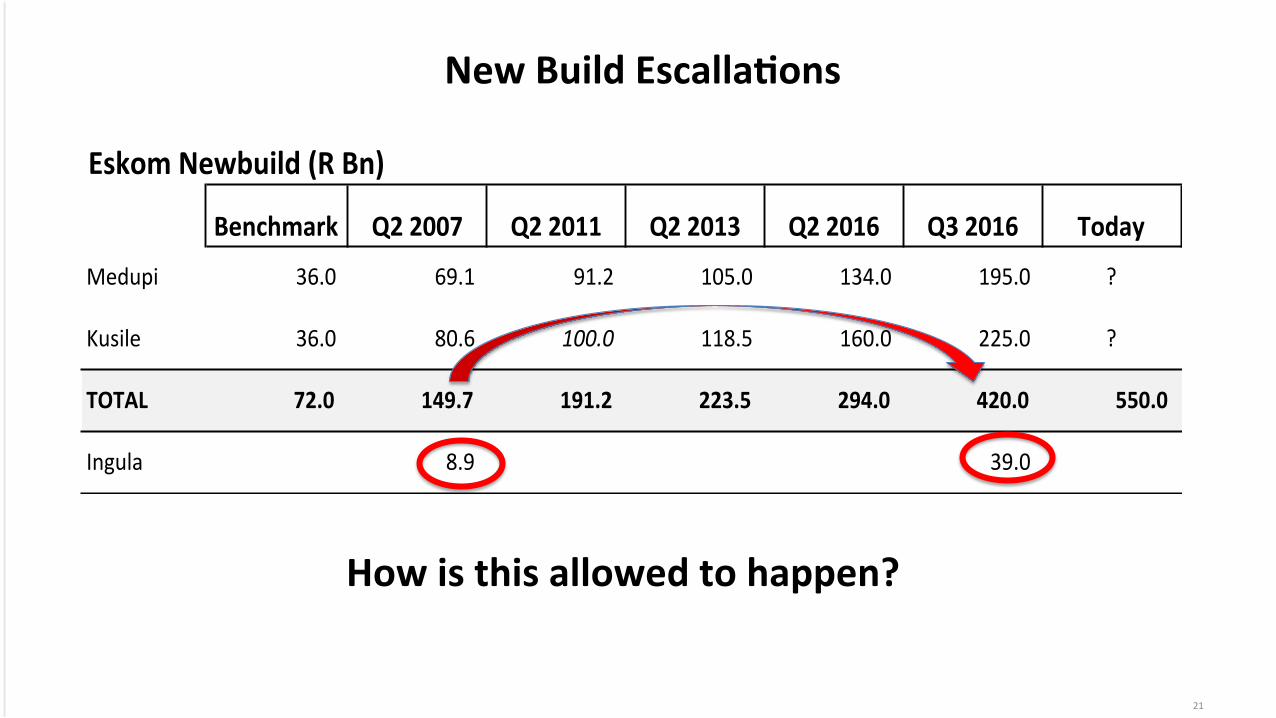

EskomNewbuild(RBn)

Benchmark Q22007 Q22011 Q22013 Q22016 Q32016 Today

Medupi 36.0 69.1 91.2 105.0 134.0 195.0 ?

Kusile 36.0 80.6 100.0 118.5 160.0 225.0 ?

TOTAL 72.0 149.7 191.2 223.5 294.0 420.0 550.0

Ingula 8.9 39.0

21

NewBuildEscallaNons

Howisthisallowedtohappen?

22

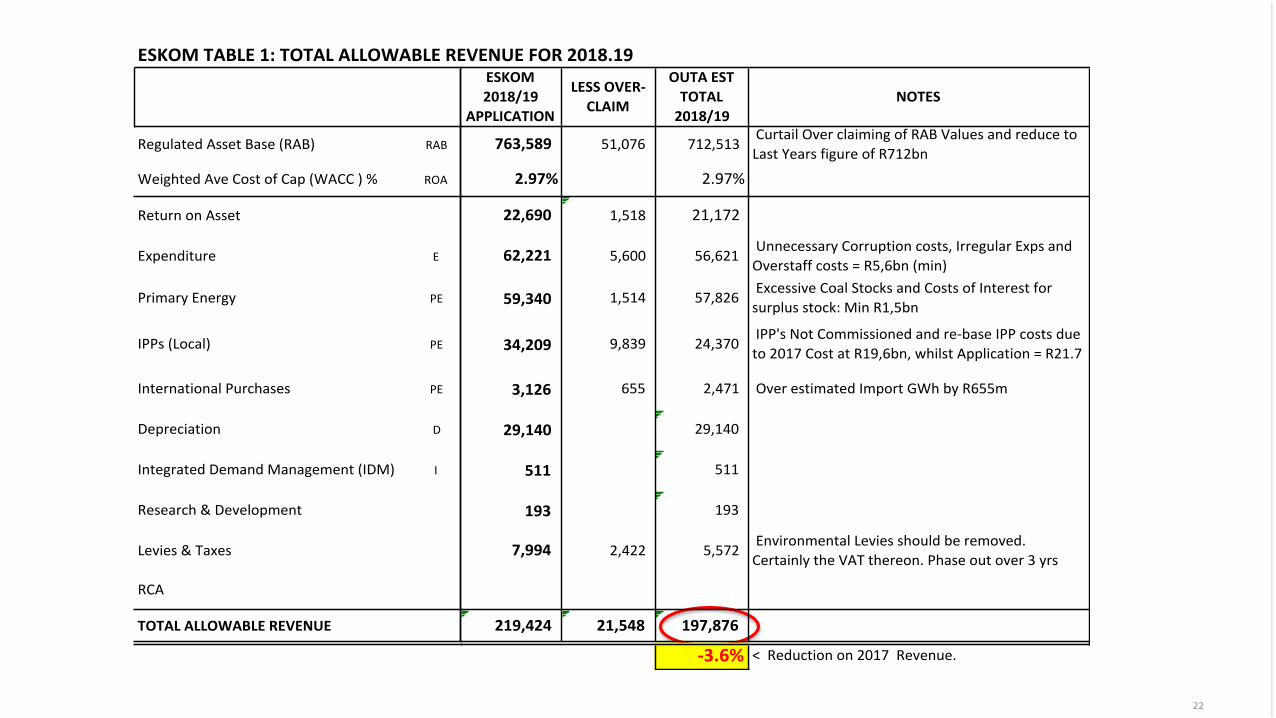

ESKOMTABLE1:TOTALALLOWABLEREVENUEFOR2018.19

RegulatedAssetBase(RAB) RAB

WeightedAveCostofCap(WACC)% ROA

ReturnonAsset

Expenditure E

PrimaryEnergy PE

IPPs(Local) PE

InternationalPurchases PE

Depreciation D

IntegratedDemandManagement(IDM) I

Research&Development

Levies&Taxes

RCA

TOTALALLOWABLEREVENUE

ESKOMTABLE1:TOTALALLOWABLEREVENUEFOR2018.19ESKOM2018/19

APPLICATION

LESSOVER-CLAIM

OUTAESTTOTAL2018/19

NOTES

763,589 51,076 712,513 CurtailOverclaimingofRABValuesandreducetoLastYearsfigureofR712bn

2.97% 2.97%

22,690 1,518 21,172

62,221 5,600 56,621 UnnecessaryCorruptioncosts,IrregularExpsandOverstaffcosts=R5,6bn(min)

59,340 1,514 57,826 ExcessiveCoalStocksandCostsofInterestforsurplusstock:MinR1,5bn

34,209 9,839 24,370 IPP'sNotCommissionedandre-baseIPPcostsdueto2017CostatR19,6bn,whilstApplication=R21.7

3,126 655 2,471 OverestimatedImportGWhbyR655m

29,140 29,140

511 511

193 193

7,994 2,422 5,572 EnvironmentalLeviesshouldberemoved.CertainlytheVATthereon.Phaseoutover3yrs

219,424 21,548 197,876

-3.6% <Reductionon2017Revenue.

23

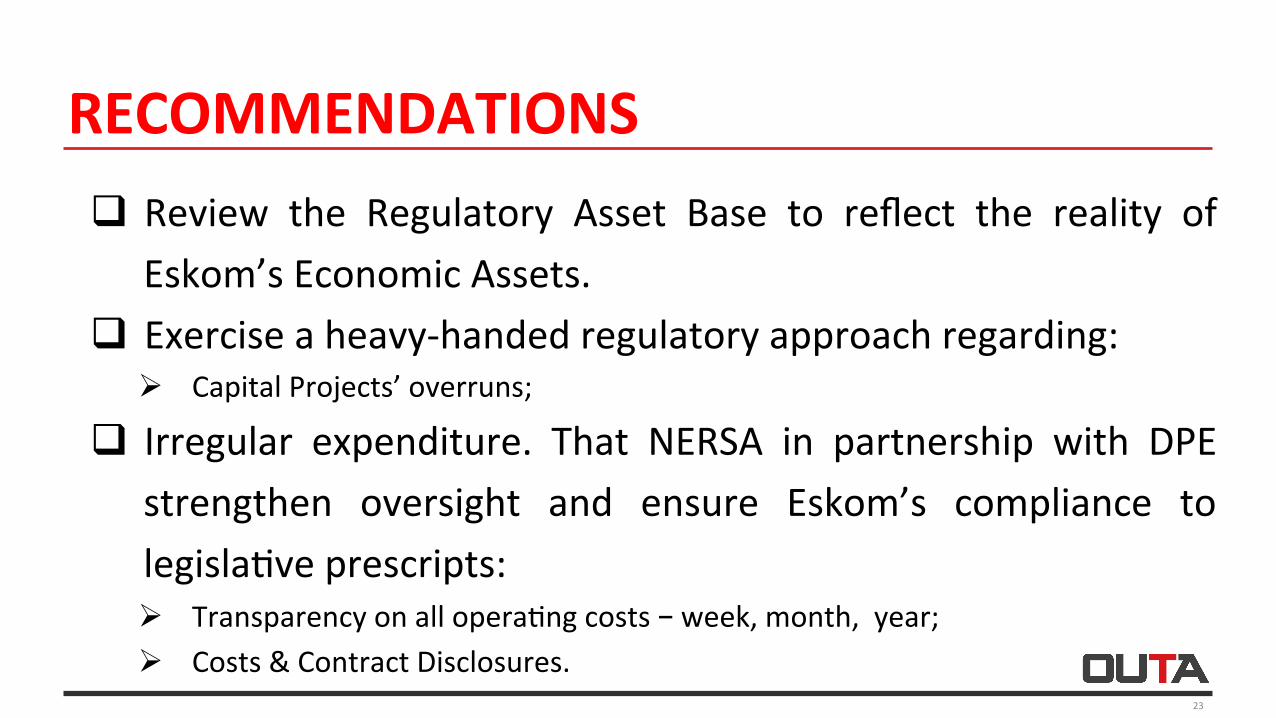

q Review the Regulatory Asset Base to reflect the reality ofEskom’sEconomicAssets.

q Exerciseaheavy-handedregulatoryapproachregarding:Ø CapitalProjects’overruns;

q Irregular expenditure. That NERSA in partnership with DPEstrengthen oversight and ensure Eskom’s compliance tolegisla<veprescripts:Ø Transparencyonallopera<ngcosts–week,month,year;Ø Costs&ContractDisclosures.

RECOMMENDATIONS

24

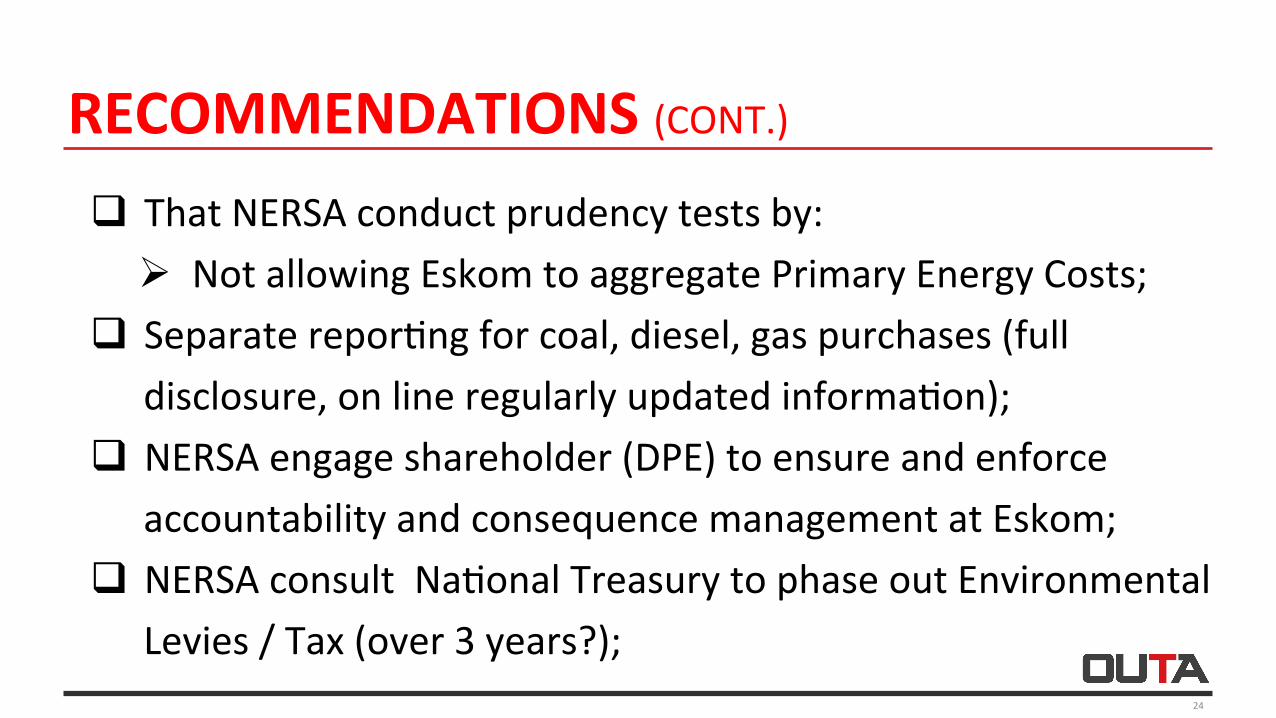

q ThatNERSAconductprudencytestsby:Ø NotallowingEskomtoaggregatePrimaryEnergyCosts;

q Separaterepor<ngforcoal,diesel,gaspurchases(fulldisclosure,onlineregularlyupdatedinforma<on);

q NERSAengageshareholder(DPE)toensureandenforceaccountabilityandconsequencemanagementatEskom;

q NERSAconsultNa<onalTreasurytophaseoutEnvironmentalLevies/Tax(over3years?);

RECOMMENDATIONS(CONT.)

25

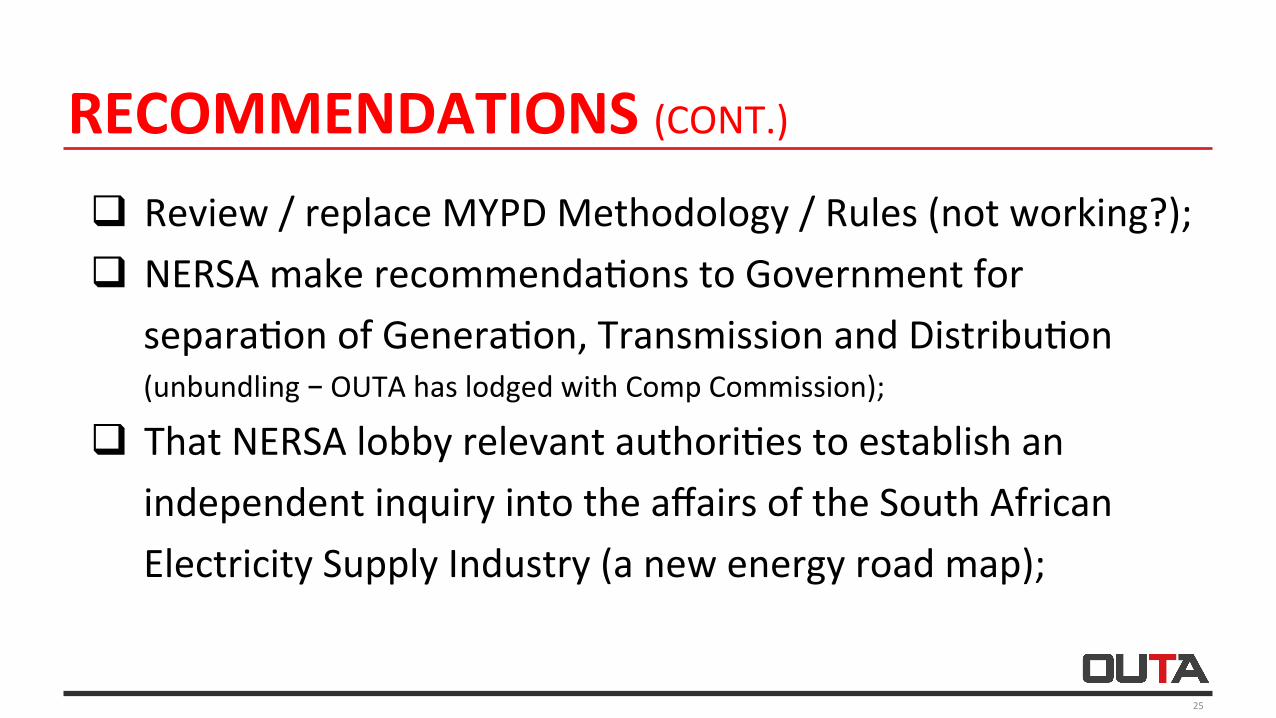

q Review/replaceMYPDMethodology/Rules(notworking?);q NERSAmakerecommenda<onstoGovernmentfor

separa<onofGenera<on,TransmissionandDistribu<on(unbundling–OUTAhaslodgedwithCompCommission);

q ThatNERSAlobbyrelevantauthori<estoestablishanindependentinquiryintotheaffairsoftheSouthAfricanElectricitySupplyIndustry(anewenergyroadmap);

RECOMMENDATIONS(CONT.)

26

q Eskomshouldsubmitausterityplanoncostreduc<onsoveraperiodof3-5years(includingpersonnelcosts):Ø Plansonhowitwilladdressthedecliningsalesversusopera<ngcosts.

q Thatthenumberofdaysforcoalstockpilesmustberegulated:Ø NERSAmustsetthebenchmark/minimumthreshold.

q Eskomtosubmitcomprehensive&<me-bounddecommissioningplanofpowerplantsandassociatedcosts.

RECOMMENDATIONS(CONT.)

CONCLUDING REMARKS q Submission of incomplete and outdated information compromises the

integrity of the regulatory process and denies the public ability to make constructive inputs/analysis of its revenue requirement application: Ø NERSA should ensure that Eskom submits ALL the required information in terms

of the MYPD Rules – to make informed decisions on the proposed tariff increase.

q NERSA should not grant approval for ANY tariff increases for the 2018/19 financial year.

q Regulatory decisions should be premised on the principle of economic realities and affordability for electricity users.

27