Embed Size (px)

Citation preview

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 1

Financial Crises

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 2

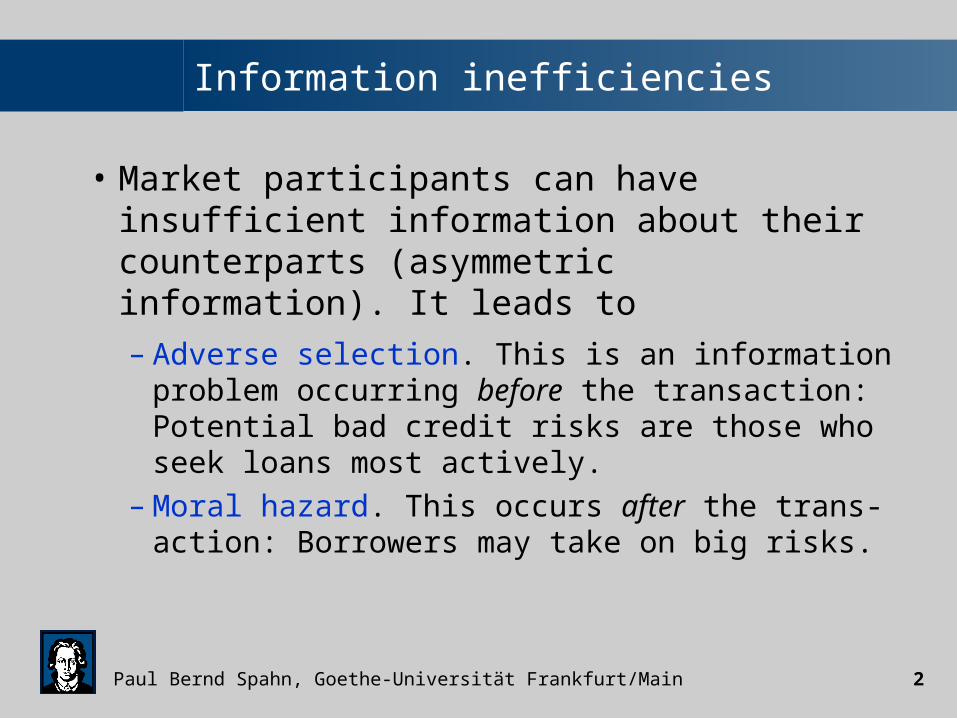

Information inefficiencies

• Market participants can have insufficient information about their counterparts (asymmetric information). It leads to

– Adverse selection. This is an information problem occurring before the transaction:Potential bad credit risks are those who seek loans most actively.

– Moral hazard. This occurs after the trans-action: Borrowers may take on big risks.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 3

Elimination of asymmetric information (1)

• A first solution to the problem is the private production and sale of information.

• There are professional rating agencies (Standard and Poor’s, Moody’s, Value Line), and you can set up costly monitoring and auditing (state verification) of the firm.

• But there is s ‘free-rider problem’ to this. If you buy a security, people my simply copy your behavior without paying for the information.

• This erodes potential extra profits, and you may not have bought the information in the first place.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 4

Elimination of asymmetric information (2)

• A second possibility could be to involve the government in regulating the market.

• The objective is to make firms reveal honest information by adhering to standard accounting practices and to disclose pertinent information.

• Government can also impose stiff criminal penalties to contain fraud.

• Government regulation may ease the asymmetric information problems, but it is difficult to eliminate them totally.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 5

Elimination of asymmetric information (3)

• A third solution is to involve financial intermediaries as experts in the production of information.

• A private loan is not traded, so others cannot watch and imitate (no free rider).

• This explains why indirect finance is more important than direct finance.

• Larger firms (because they are better known) obtain easier access to capital markets than smaller firms.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 6

Systemic instability and financial crises

• Financial crises are characterized by abrupt declines in asset prices and by insolvencies of financial and non-financial firms.

• Such crises are reoccurring in many countries. They are caused by a sharp increase in adverse selection and moral hazard problems.

• Four categories of factors trigger crises:– Increases in interest rates;– Increases in uncertainty; – Asset market effects on balance sheets; and– (Multiple) bank failures.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 7

Asset market effects on balance sheets

• Balance sheets have important repercussions on the financial system:– A deterioration (fall in stock or housing prices) of

the balance sheet reduces the ‘net worth’ of a firm.– Lenders are less willing to lend because of

reduced collateral.– This induces moral hazard because borrowers take

higher risks.– The increase in moral hazard makes lending less

attractive … this reduces economic activity.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 8

Systemic instability and financial crises

• Financial crises are characterized by abrupt declines in asset prices and by insolvencies of financial and non-financial firms.

• Such crises are reoccurring in many countries. They are caused by a sharp increase in adverse selection and moral hazard problems.

• Four categories of factors trigger crises:– Increases in interest rates;– Increases in uncertainty; – Asset market effects on balance sheets; and– (Multiple) bank failures.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 9

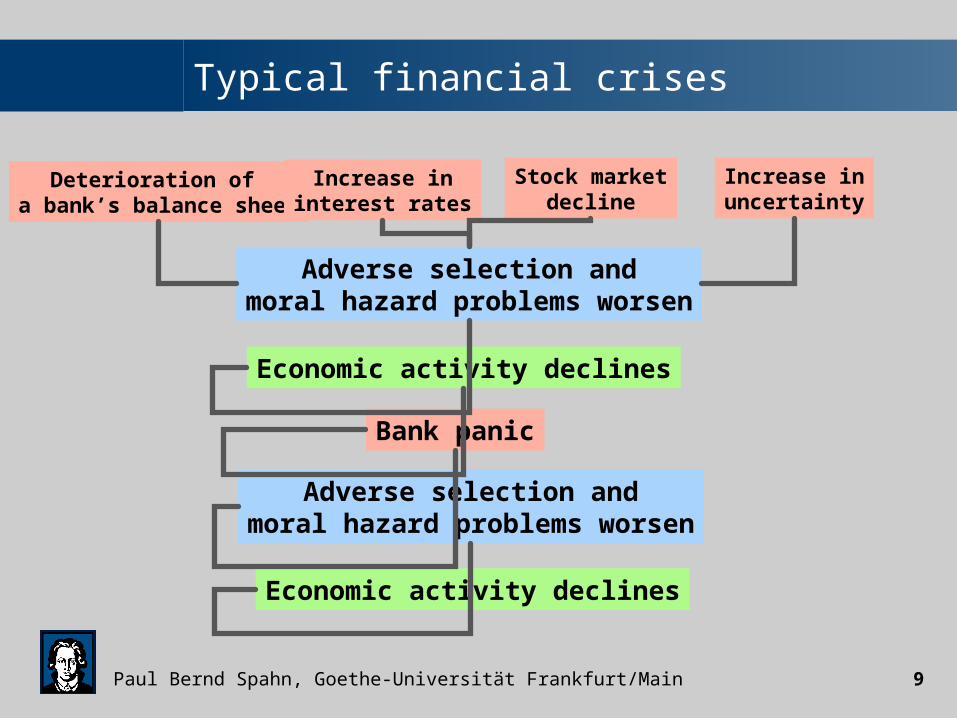

Typical financial crises

Deterioration of a bank’s balance sheet

Increase ininterest rates

Increase inuncertainty

Stock marketdecline

Adverse selection andmoral hazard problems worsen

Economic activity declines

Bank panic

Adverse selection andmoral hazard problems worsen

Economic activity declines

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 10

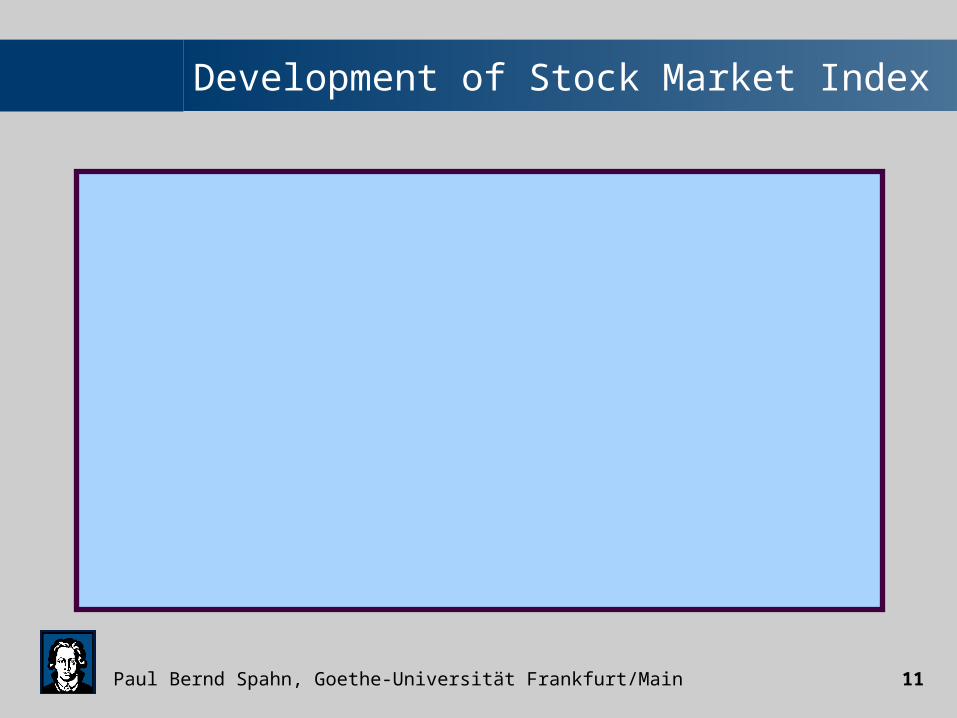

How do financial bubbles affect activity?

The NY stock market crashed on Friday,

October 1929, initiating a persistent and long

downturn of the economy

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 11

Development of Stock Market Index

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 12

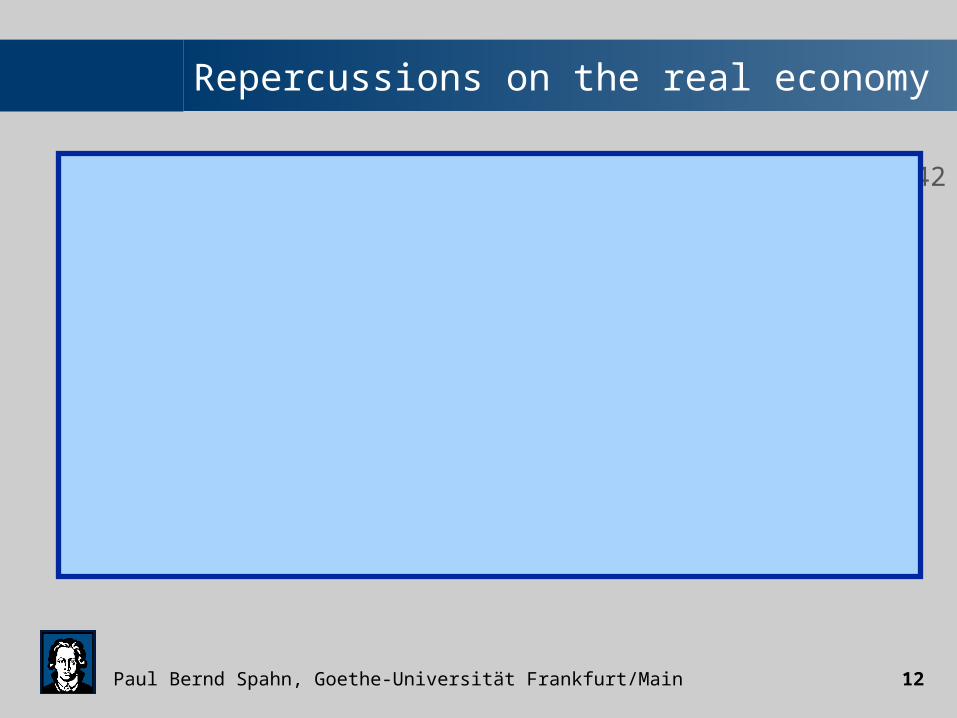

official series

Adjusted series

US Unemployment rate, 1929-1942

1930 1935 1940

25

20

15

10

5

Quelle: M.R. Darby, Three-and-a-half Million Employees Have been mislaid, Journal of political Economy,1976

Repercussions on the real economy

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 13

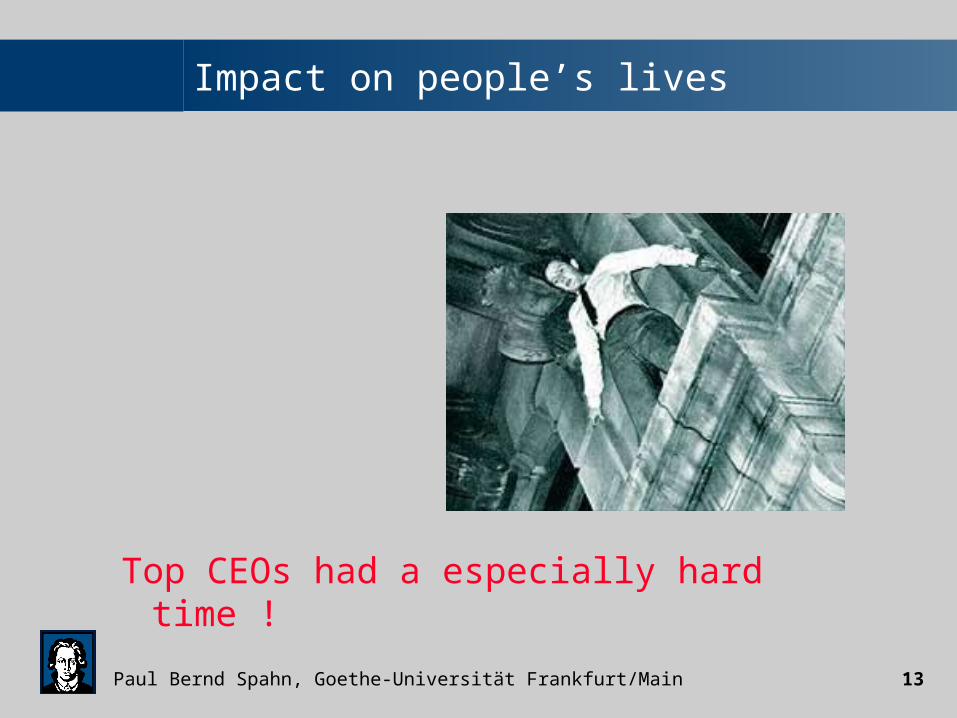

Impact on people’s lives

Top CEOs had a especially hard time !

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 14

What dragged the economy down?

• The impact was then– Increase of personal savings (and hence

a reduction of consumer spending) due to a perceived reduction of personal wealth

– Change in consumer behavior due to higher unemployment

– Credit implosion with an induced reduction of demand, notably fixed investment

– Reduction of housing investment due to prior over-investment

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 15

The Great Depression: Further problems

• And :– A general loss in consumers’ and investors’

confidence– Change in spending behavior

due to insolvencies and bankruptcies– Disintermediation due to a lack of liquidity– Negative impact on public investment

due to a fall in tax revenue– Policy failures, e.g. “strategic trade policies”

(Smoot-Hawley Act)

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 16

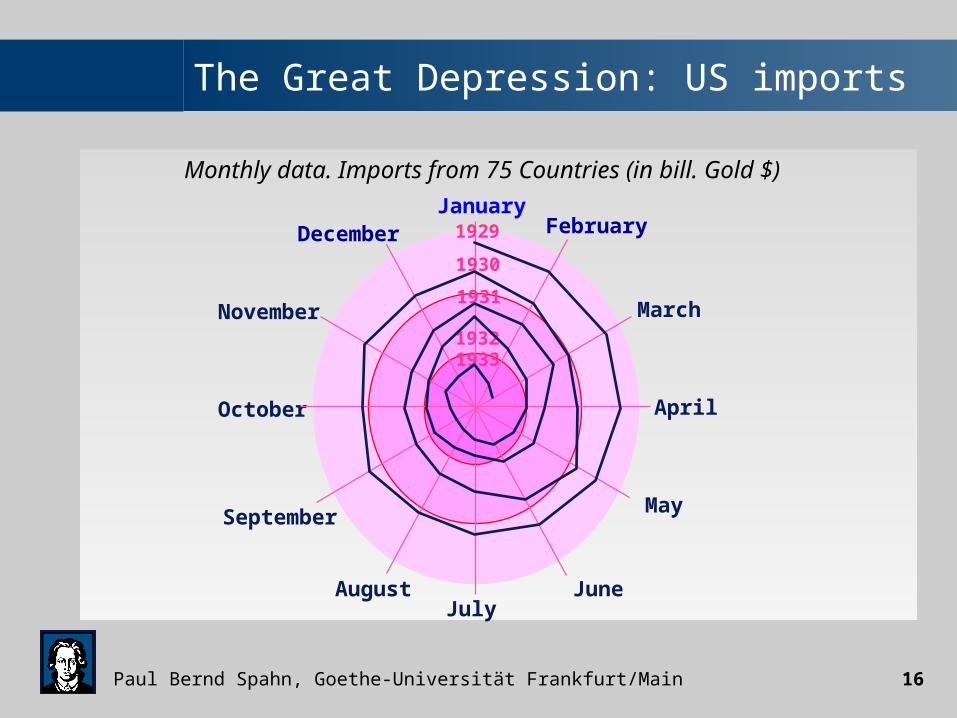

November

JanuaryFebruary

March

April

May

JuneJuly

August

September

October

Monthly data. Imports from 75 Countries (in bill. Gold $)

December 1929

1930

1931

19321933

The Great Depression: US imports

November

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 17

The central bank and systemic stability

• The health of the economy and the effectiveness of monetary policy depend on a sound financial system. Through supervising and regulating financial institutions, the ECB is better able to make policy decisions.

• But should it intervene?

• Rescue failing banks?

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 18

Lecture 6

DETERMINANTS OF THE MONEY SUPPLY, AND THE TOOLS OF CENTRAL BANKS, Part One

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 19

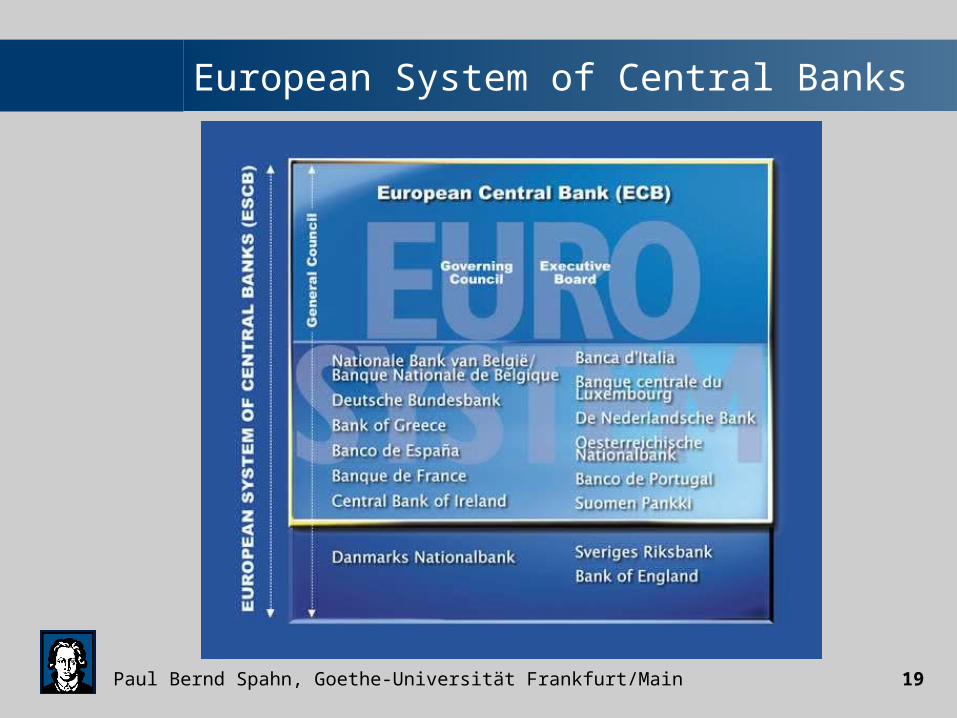

European System of Central Banks

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 20

European System of Central Banks

• The European System of Central Banks (ESCB) consists of the European Central Bank (ECB) and the national central banks of the EU Member States.

• The activities of the ESCB are carried out in accordance with the Treaty establishing the European Community (Treaty) and the Statute of the European System of Central Banks and of the European Central Bank (ESCB/ECB Statute).

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 21

Governance of the ECB

• The ESCB is governed by the decision-making bodies of the ECB. – The Governing Council of the ECB is responsible

for the formulation of monetary policy, – the Executive Board is empowered

to implement monetary policy.

• The ECB has recourse to the national central banks to carry out her operations.

• The ESCB policy operations are executed on uniform terms and conditions in all Member States.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 22

ESCB: Basic tasks

• The basic tasks by the Eurosystem are:– to define and implement the monetary policy of the

euro area;– to conduct foreign exchange operations;– to hold and manage the official foreign reserves of

the Member States; and– to promote the smooth operation of payment

systems.

• In addition, the Eurosystem contributes to the prudential supervision of credit institutions and the stability of the financial system.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 23

The US Federal Reserve System

• The formal structure of the Federal Reserve System is characterized by– a regional decentralization (there are 12

Federal Reserve Banks)– each Federal Reserve Bank is quasi-public

(partly held by government, partly by commercial banks in the district).

– all national banks chartered by the Office of the Comptroller of the Currency have to be members of the Federal Reserve System.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 24

The Federal Reserve Bank of New York

• The Federal Reserve Bank of New York has a special role (through its involvement in the bond and foreign exchange markets and through the presence of large commercial banks).

• The FRBNY is the only US Reserve Bank to be a member of the Bank for International Settlements (BIS).

• Its president assumes a chief role in the system.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 25

Governance of the Federal Reserve System

• The Fed is headed by a seven-member Board of Governors, with its influential Chairman (Alan Greespan), headquartered in Washington D.C.

• The Board of Governors is actively involved in monetary policy making.

• All governors are (voting) members of the Federal Open Market Committee (FOMC).

• In addition there are 12 (of whom 5 voting) members from district banks in the FOMC.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 26

Should central banks be independent?

• A cornerstone of the monetary constitution of the euro area is the independence of the ECB and of the NCBs (Article 108).

• There are fears that a dependent ECB– could succumb to financing large budget deficits of

the government.– could be asked to monetize too much debt, which

would entails an inflationary bias.

• Central banking also requires expertise and “should not be left to politicians”.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 27

Should central banks be independent?

• Counterarguments:– It is undemocratic to have monetary policy

controlled by a non-elected elite group.– There is no accountability in central

banking, which is a precondition for, and core element of, democratic legitimacy.

– There is need to coordinate monetary and fiscal policies.

– The ECB could pursue a policy of self-interest.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 28

Principal-agent problem

• There is a typical principal-agent relation between the Legislature and an independent institution bestowed with a public function.

• In line with the requirements of Article 113 of the Treaty, the President of the ECB presents the ECB’s Annual Report to the European Parliament at its plenary session.

• This is followed by the adoption of a European Parliament resolution, which provides a comprehensive ex post assessment of the ECB’s activities and policy conduct.

• The Chairman of the Fed reports to the US Congress.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 29

The objectives of the ESCB

• The primary objective of the ESCB, as defined in Article 105 of the Treaty, is to maintain price stability.

• Without prejudice to the primary objective, the ESCB has to support the general economic policies in the EU.

• In pursuing its objectives, the ESCB has to act in accordance with the principle of an open market economy with free competition, favoring an efficient allocation of resources.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 30

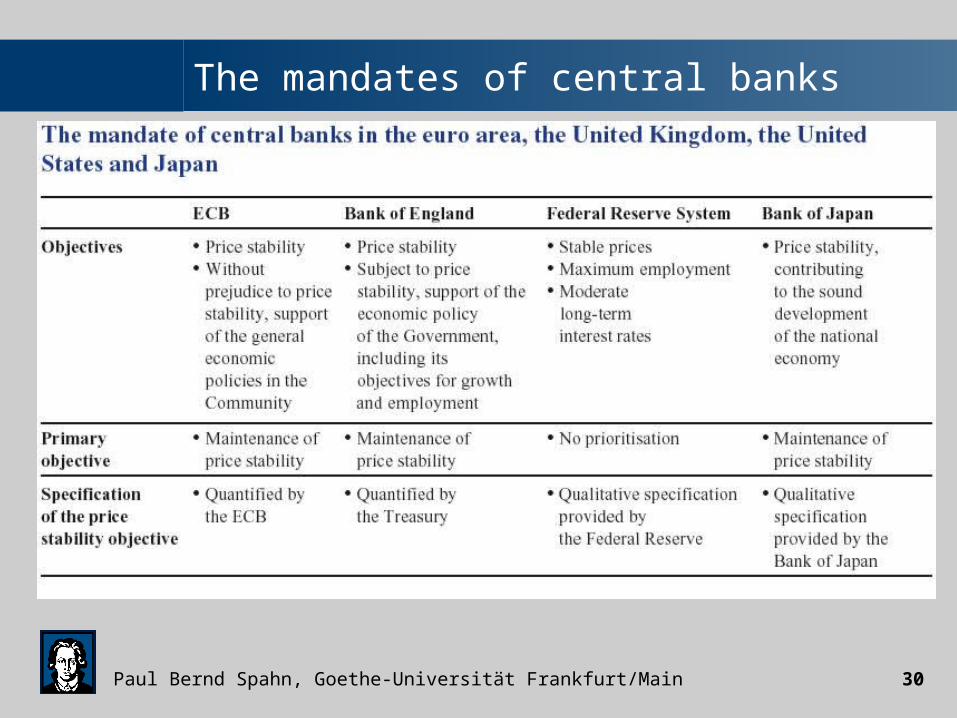

The mandates of central banks

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 31

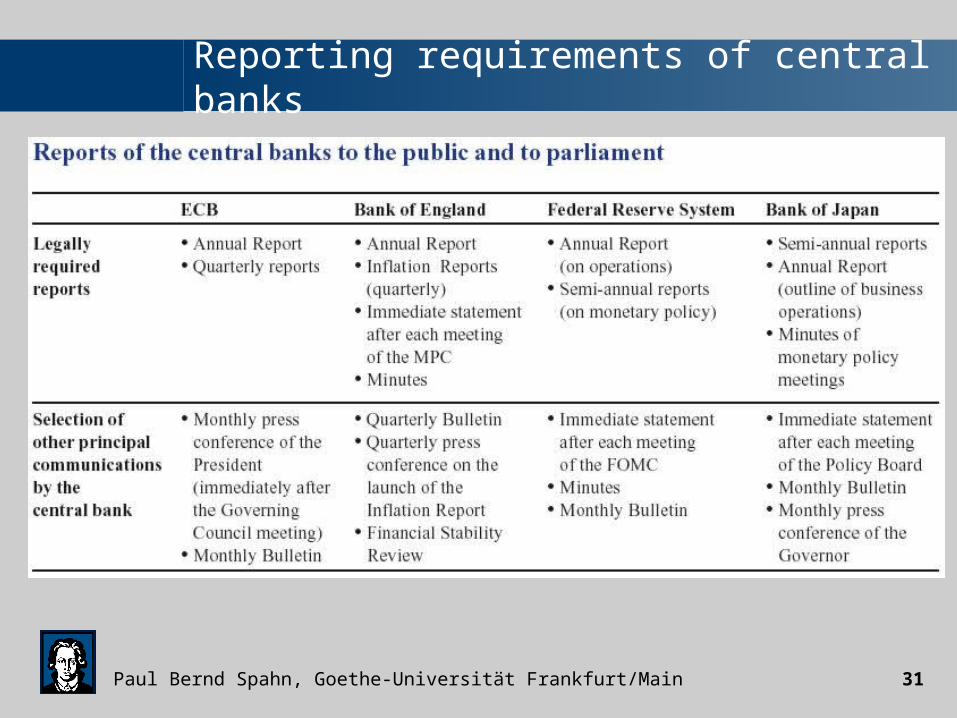

Reporting requirements of central banks

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 32

ESCB monetary policy instruments

• In order to achieve its objectives, the ESCB has at its disposal a set of monetary policy instruments.

• The ESCB

– conducts open market operations, – offers standing facilities and– requires credit institutions to hold minimum

reserves on accounts with the ESCB.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 33

Money supply process

• In order to understand the money supply process, we have to come back to the ECB’s balance sheet and the monetary base (or high-powered money).

• The assets of the CB constitute the sources of the base.

• The liabilities of the CB constitute the uses of the base.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 34

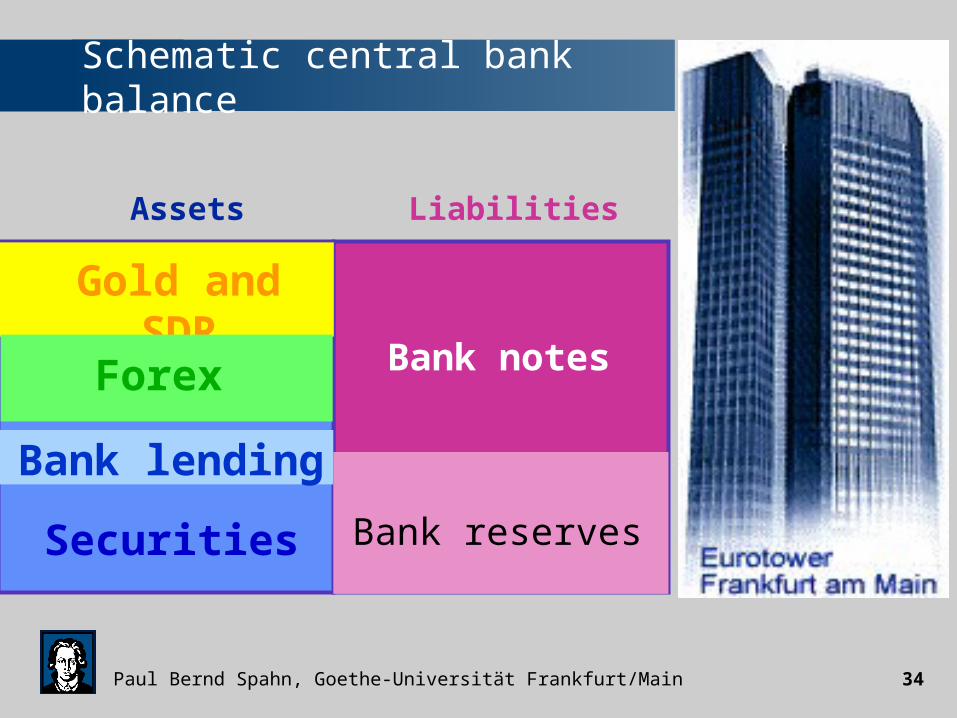

Schematic central bank balance

Assets Liabilities

Bank notes

Gold and SDR

Forex

Securities

Bank lending

Bank reserves

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 35

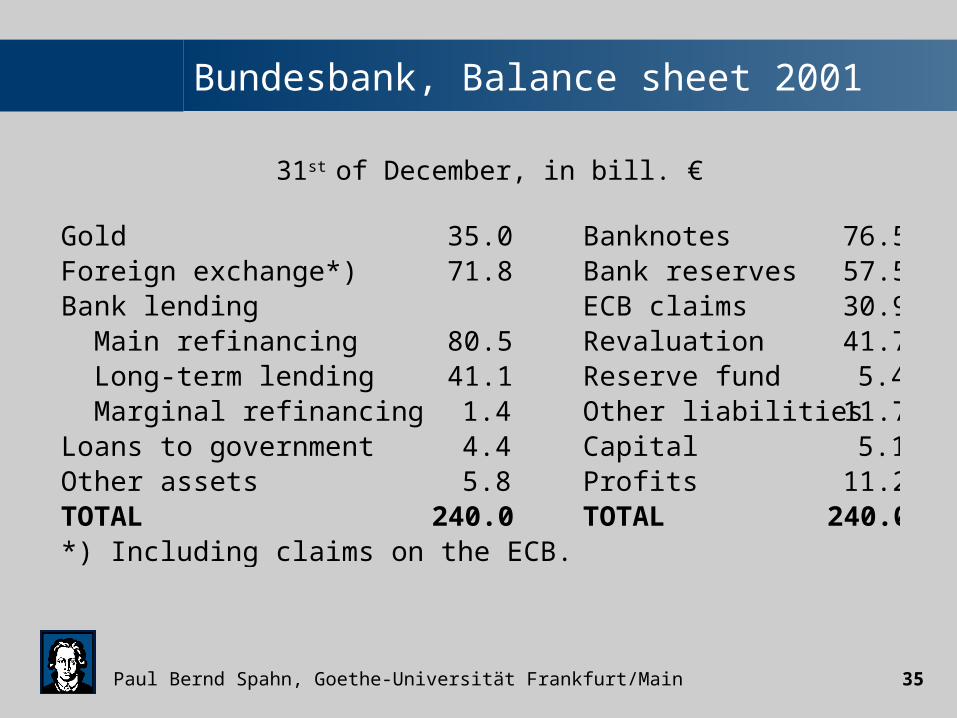

Bundesbank, Balance sheet 2001

Gold 35.0 Banknotes 76.5Foreign exchange*) 71.8 Bank reserves 57.5Bank lending ECB claims 30.9 Main refinancing 80.5 Revaluation 41.7 Long-term lending 41.1 Reserve fund 5.4 Marginal refinancing 1.4 Other liabilities 11.7Loans to government 4.4 Capital 5.1Other assets 5.8 Profits 11.2TOTAL 240.0 TOTAL 240.0*) Including claims on the ECB.

31st of December, in bill. €

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 36

The control of the monetary base

• The quantity-oriented approach to monetary policy purports that the central bank can control the monetary base.

• It is basically effected via open market operations with commercial banks.

• The ECB can control OMOs more effectively than foreign reserves, but she can also use interventions in forex markets to change the monetary base.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 37

Controlling the money supply

• Under fixed exchange rates controlling the money supply is more difficult.

• In this case the central bank has to “sterilize” inflows or outflows of foreign exchange.

• It renders interest rates endogenous, i.e. they vary in response to sterilizing interventions.

• Forex interventions will be discussed later.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 38

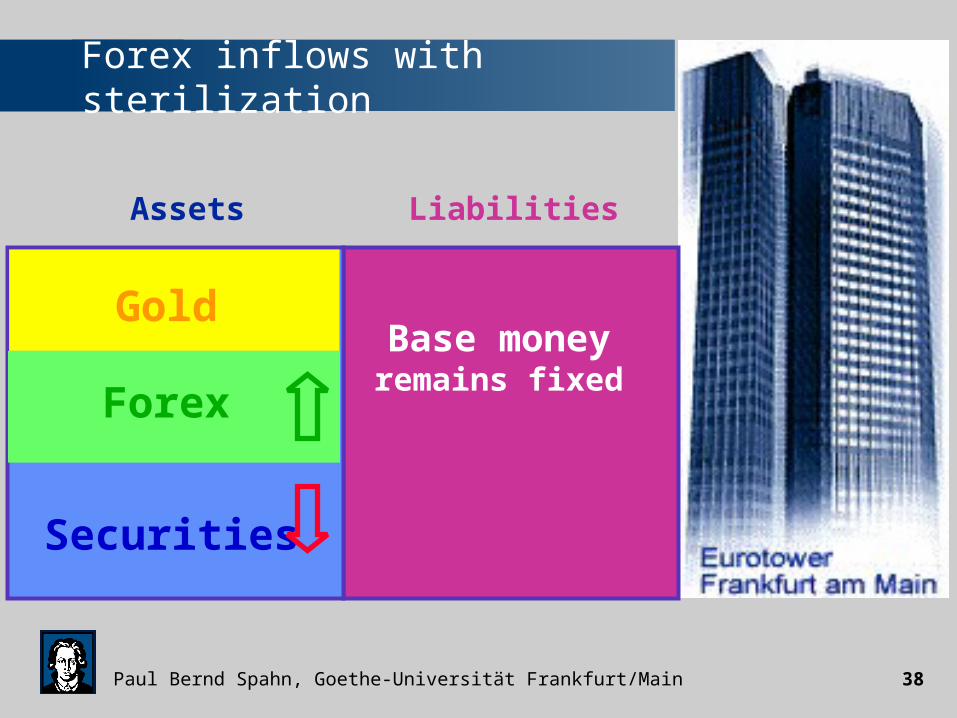

Forex inflows with sterilization

Assets Liabilities

Base money remains fixed

Gold

Forex

Securities

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 39

OMOs

• Among the OMOs, the main refinancing operations (MROs) are the most important, playing a pivotal role in steering liquidity and signaling the stance of monetary policy.

• Roughly 75% of liquidity is provided by MROs.

• MROs were conducted as fixed rate and variable rate tenders with a minimum bid rate.

• The MROs are regular, liquidity providing, reverse transactions, conducted as standard tenders, with a weekly frequency and normally a maturity of two weeks.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 40

Longer-term refinancing (LTROs)

• Longer-term refinancing operations (LTROs) are carried out through monthly standard tenders and have a maturity of three months.

• LTROs are regular open market operations executed by the Eurosystem also in the form of a reverse transaction.

• On average over the year, LTROs provide about 25% of the total refinancing of banks.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 41

Reserve requirements of banks

• The Eurosystem requires banks to hold minimum reserves equal to 2% of certain short-term liabilities. It is part of base money.

• The purpose is the stabilization of short-term interest rates and the enlargement of the structural liquidity deficit of banks.

• Reserve requirements bear interest, and must only be fulfilled on average over a one-month reserve maintenance period.

• It has a significant smoothing effect on the behavior of short-term interest rates.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 42

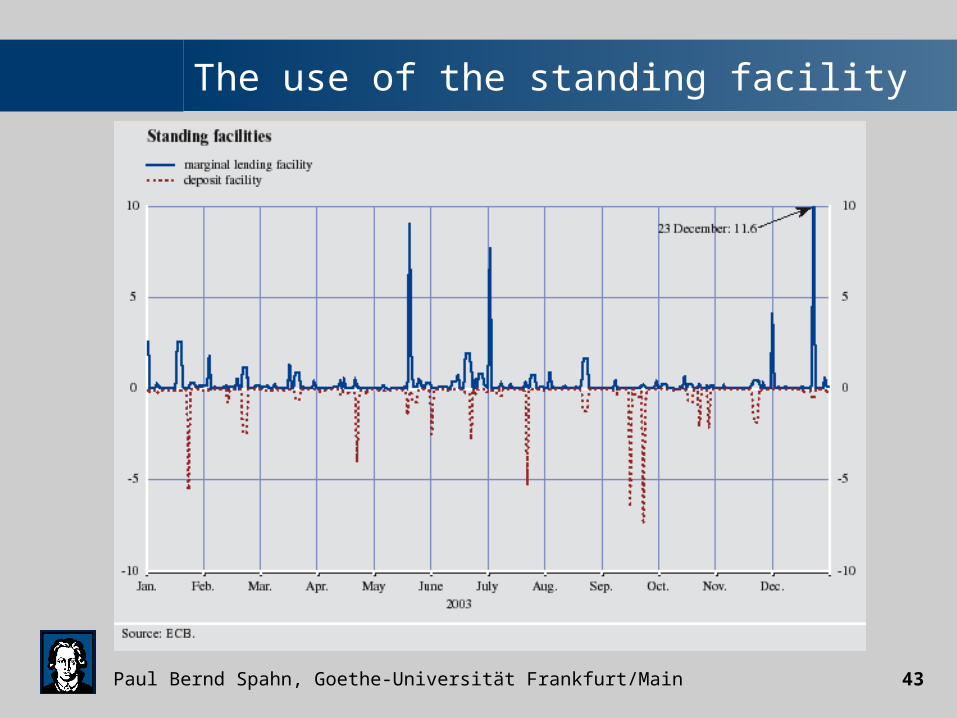

Short-term liquidity policy

• The monetary base is also affected when a central bank makes a discount loan to a bank. The ECB does not use this instrument however.

• There are two standing facilities offered by the Eurosystem– the marginal lending facility and – the deposit facility,

• These instruments provide and absorb overnight liquidity, signal the stance of monetary policy and set an upper and lower limit for the overnight market interest rate.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 43

The use of the standing facility

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 44

Key ECB interest rates

• The key ECB interest rates are at present

– the minimum bid rate on the main refinancing operations,

– the interest rate on the marginal lending facility

– and the interest rate on the deposit facility.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 45

What assets are eligible for credit operations?

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 46

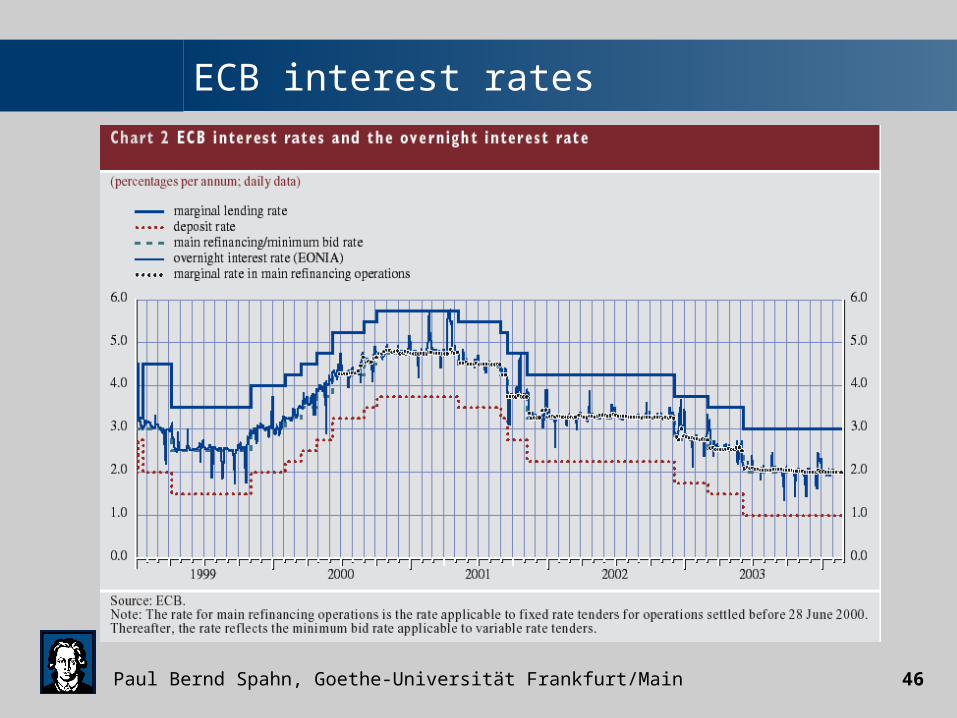

ECB interest rates

EONIA (euro overnight index average):

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 47

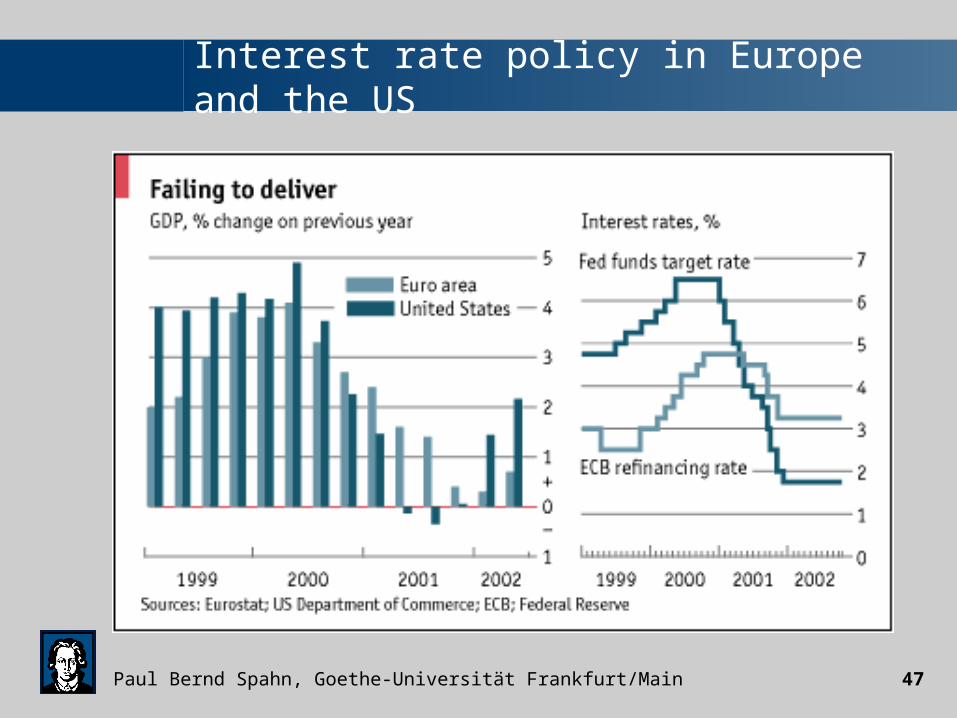

Interest rate policy in Europe and the US

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 48

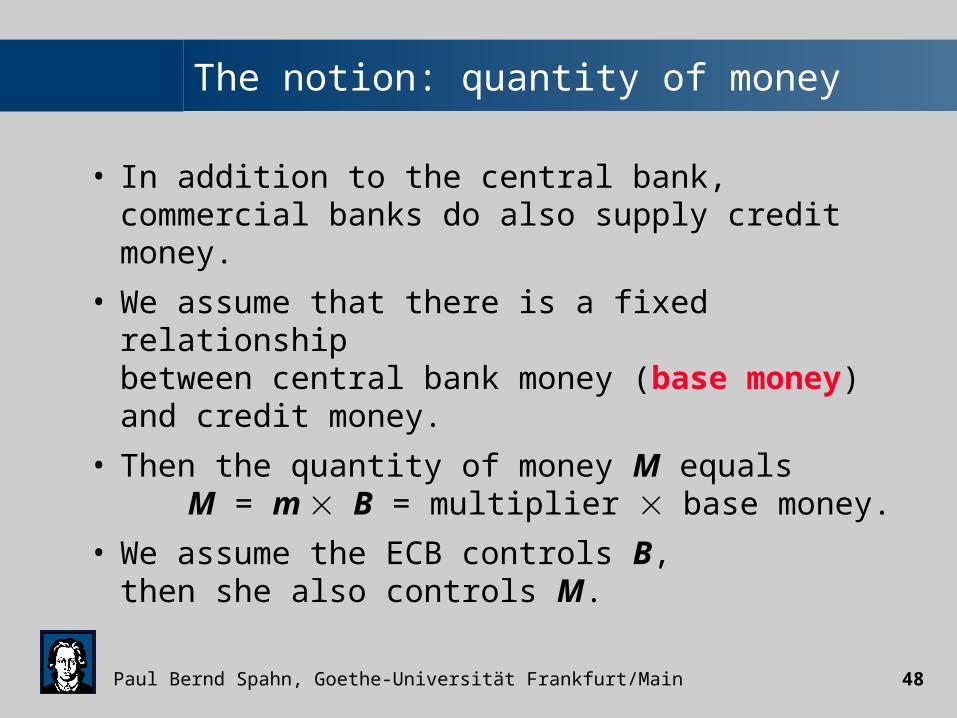

The notion: quantity of money

• In addition to the central bank, commercial banks do also supply credit money.

• We assume that there is a fixed relationshipbetween central bank money (base money) and credit money.

• Then the quantity of money M equalsM = m B = multiplier base money.

• We assume the ECB controls B, then she also controls M.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 49

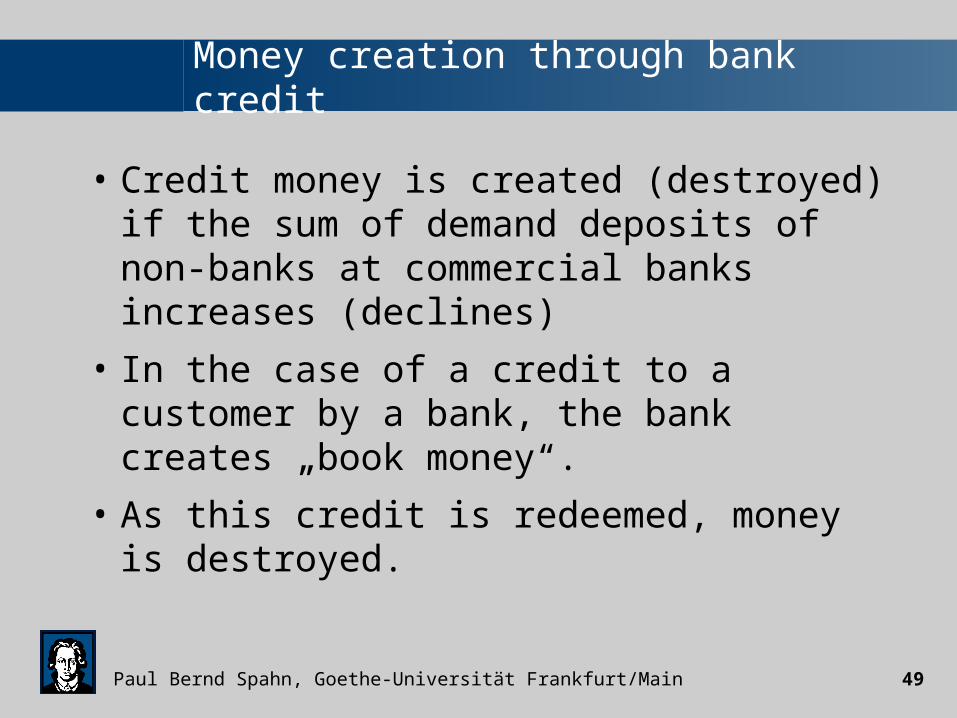

Money creation through bank credit

• Credit money is created (destroyed) if the sum of demand deposits of non-banks at commercial banks increases (declines)

• In the case of a credit to a customer by a bank, the bank creates „book money“.

• As this credit is redeemed, money is destroyed.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 50

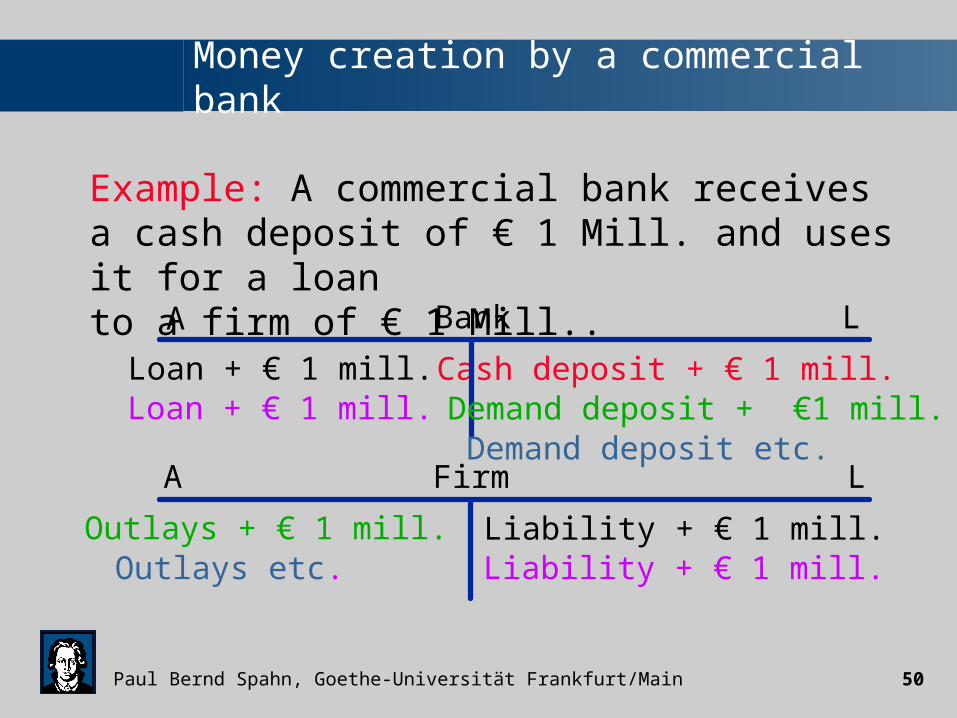

Money creation by a commercial bank

Example: A commercial bank receives a cash deposit of € 1 Mill. and uses it for a loan to a firm of € 1 Mill..

Cash deposit + € 1 mill. Loan + € 1 mill.

Liability + € 1 mill.

Bank

Firm

A

L

L

A

Outlays + € 1 mill.

Demand deposit + €1 mill.Loan + € 1 mill.

Liability + € 1 mill. Outlays etc.

Demand deposit etc.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 51

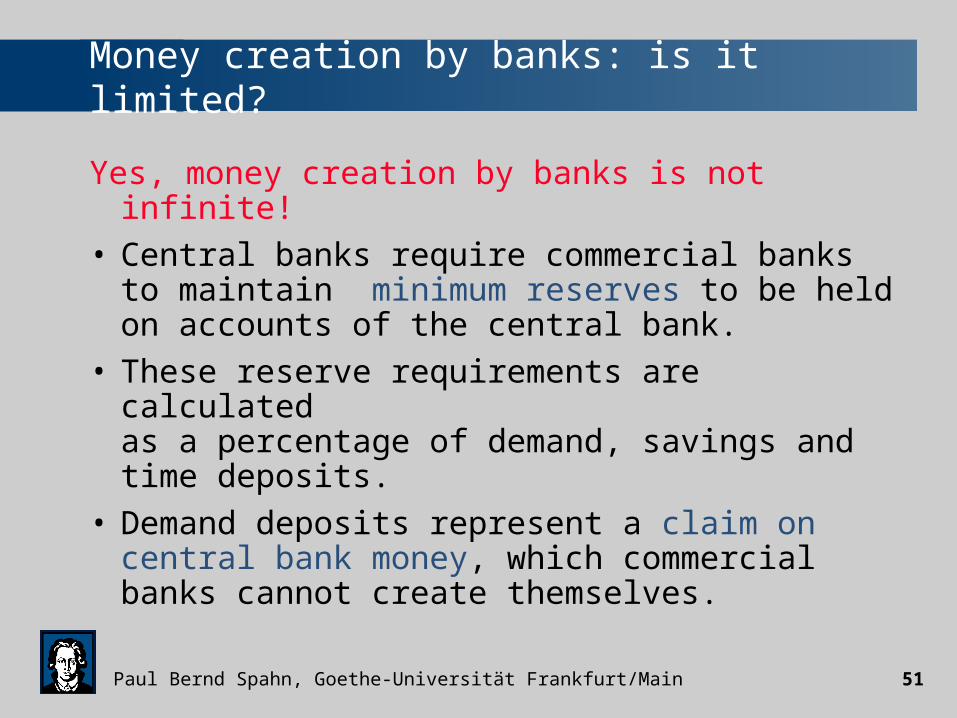

Money creation by banks: is it limited?

Yes, money creation by banks is not infinite!

• Central banks require commercial banks to maintain minimum reserves to be held on accounts of the central bank.

• These reserve requirements are calculated as a percentage of demand, savings and time deposits.

• Demand deposits represent a claim on central bank money, which commercial banks cannot create themselves.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 52

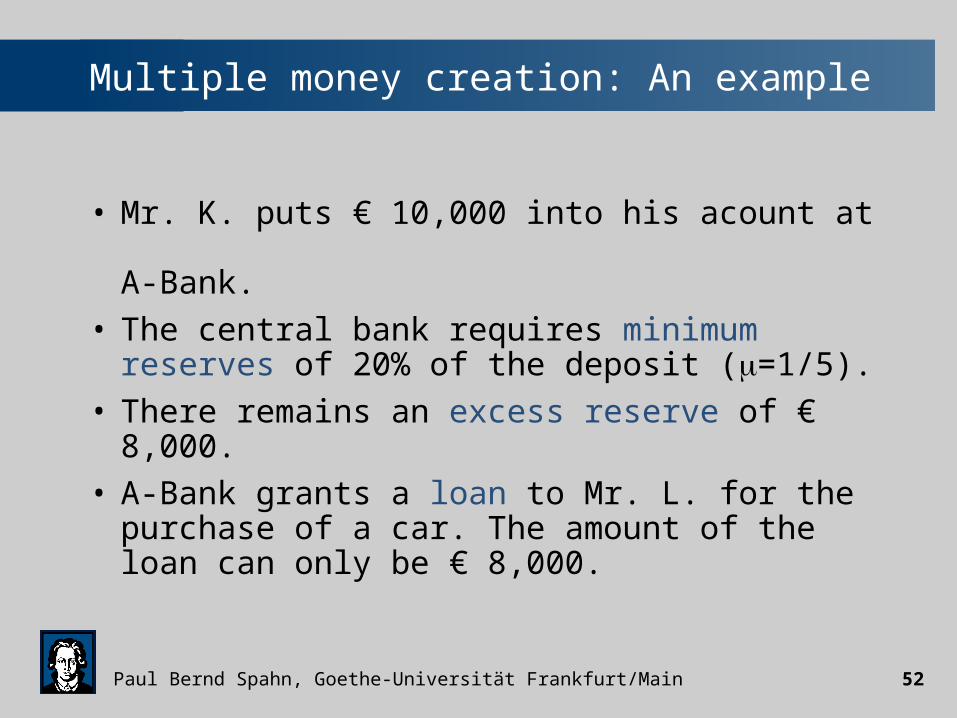

Multiple money creation: An example

• Mr. K. puts € 10,000 into his acount at A-Bank.

• The central bank requires minimum reserves of 20% of the deposit (=1/5).

• There remains an excess reserve of € 8,000.

• A-Bank grants a loan to Mr. L. for the purchase of a car. The amount of the loan can only be € 8,000.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 53

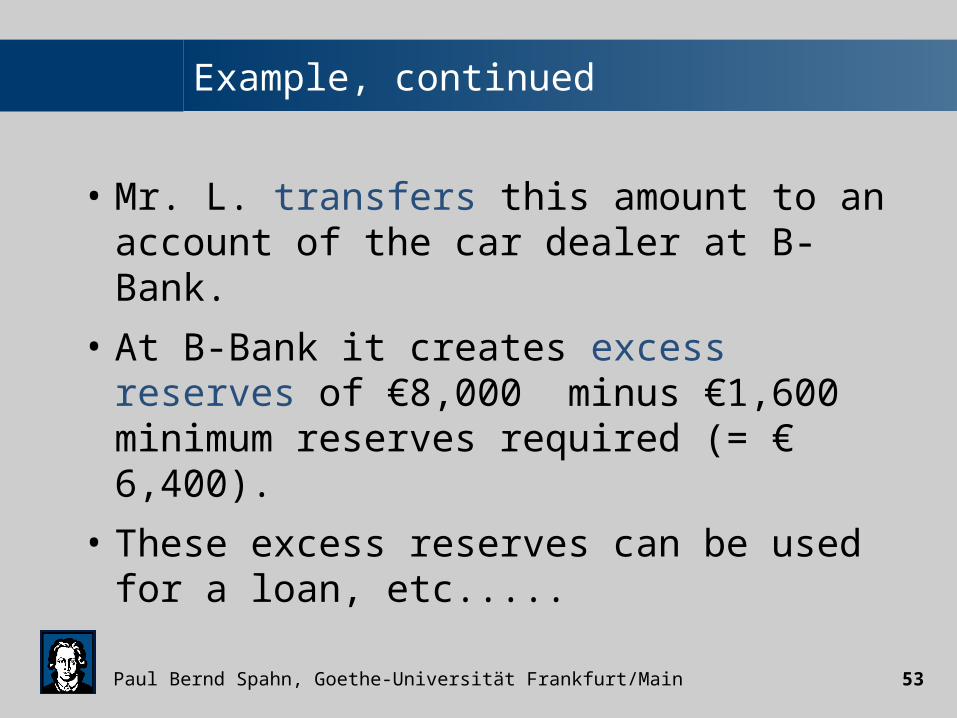

Example, continued

• Mr. L. transfers this amount to an account of the car dealer at B-Bank.

• At B-Bank it creates excess reserves of €8,000 minus €1,600 minimum reserves required (= € 6,400).

• These excess reserves can be used for a loan, etc.....

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 54

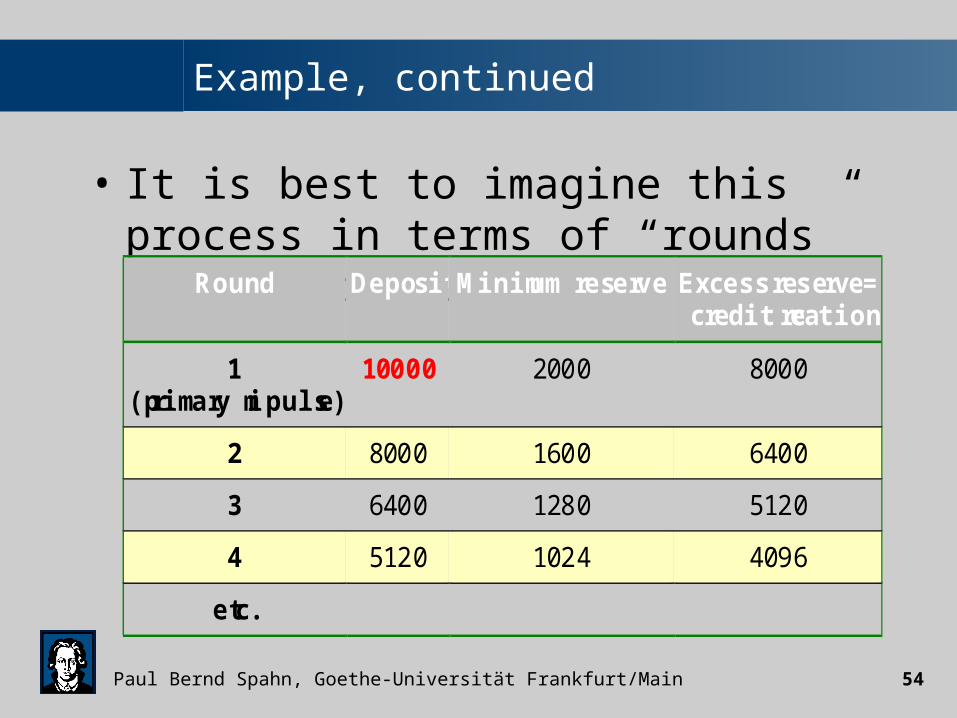

Example, continued

• It is best to imagine this process in terms of “rounds” of credit creation:

Round Deposit Minimum reserve Excess reserve=credit creation

1(primary impulse)

10000 2000 8000

2 8000 1600 6400

3 6400 1280 5120

4 5120 1024 4096

etc.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 55

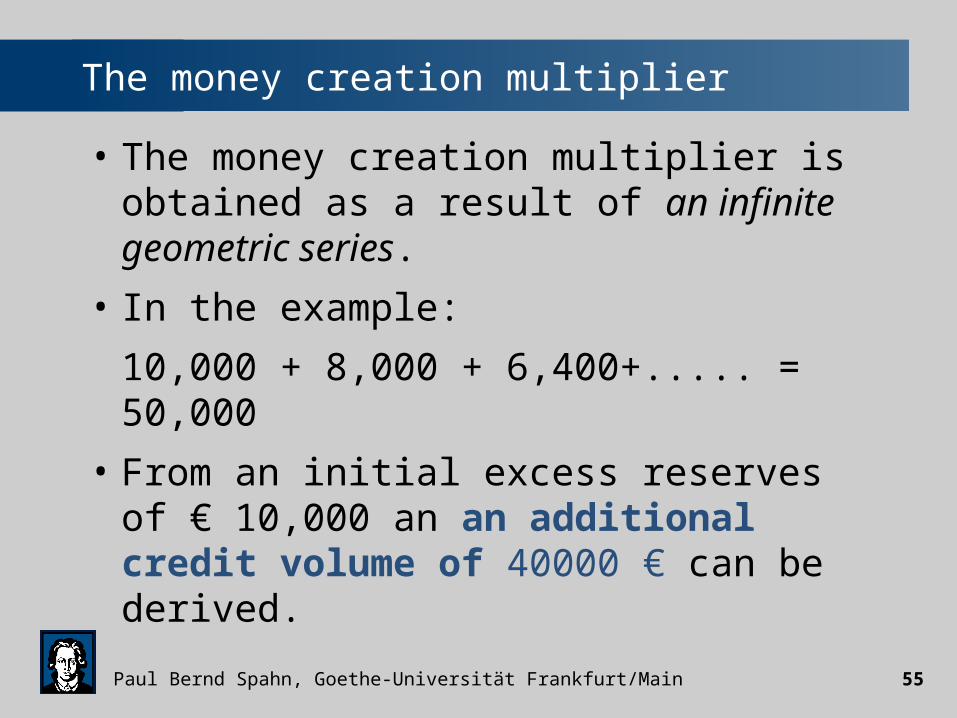

The money creation multiplier

• The money creation multiplier is obtained as a result of an infinite geometric series.

• In the example:

10,000 + 8,000 + 6,400+..... = 50,000

• From an initial excess reserves of € 10,000 an an additional credit volume of 40000 € can be derived.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 56

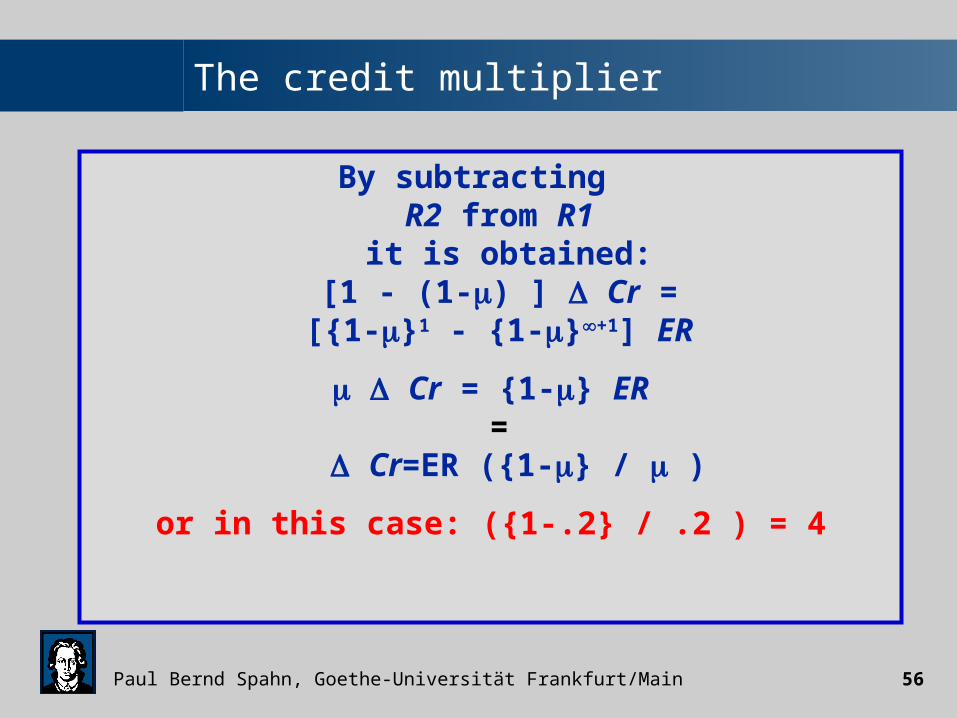

By subtracting R2 from R1

it is obtained:[1 - (1-) ] Cr =

[{1-}1 - {1-}+1] ER

Cr = {1-} ER =

Cr=ER ({1-} / )

or in this case: ({1-.2} / .2 ) = 4

The credit multiplier

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 57

Critique of the simple model

• Supply of credit must meet a demand!

• Banks do not extend their lending to the maximum because of insolvency risks.

• Lending is limited by capital adequacy ratios (Basel I and II).

• But there are refinancing possibilities– through the ESCB, and– through the interbank market.

Paul Bernd Spahn, Goethe-Universität Frankfurt/Main 58

An example: The Eurodollar market

• The Eurodollar market (better: xeno market) is an off-shore market for the US dollar (more generally: any hard currency).

• It is characterized by the absence of mandatory reserve requirements for commercial banks.

• The experience has shown that this market had avoided “credit explosion”.