Embed Size (px)

Citation preview

Notes to Candidates Sitting for the 2014 or 2015 HKDSE Examinations

Turbo BAFS Elective Part A1 – Financial Accounting, 1st Edition is written in accordance with the “Business, Accounting and Financial Studies Curriculum and Assessment Guide (Secondary 4-6)” released in 2007. For candidates sitting for the 2014 or 2015 BAFS HKDSE examinations, the below table is prepared according to the supplementary notes released by the Education Bureau (EDB) in August 2013.

Chapter Section Notes Page

2G Allowances for Discounts Allowed and Discounts Received

[Deleted] 38-40

Exercise Q2.15, 2.16 [Deleted] 47

3B Capital expenditure and revenue expenditure should be included

in the syllabus 51

H Trade-in should be included in the syllabus 67

7 G Control accounts under double entry system [Deleted] 165

10E Valuation of goodwill [Deleted] 240-242

Exercise Q10.16 - 10.23 [Deleted] 250-251

11 Exercise Q11.10, 11.11 [Deleted] 272-274

12D Sale of partnership as a going concern [Deleted] 284-286

Exercise Q12.13 [Deleted] 300-301

13 ExerciseIncome tax [Refer to Appendix 1]

Q13.6 (ix) Revaluation of non-current assets [Deleted] 323

14

BIssue at discount for shares and for debenture [Deleted] 327

Issue at premium for debenture [Deleted] 327

C Issue of shares to existing shareholders [Deleted] 330-332

Exercise

All issue of shares at discount or issue of debenture at premium or discount [Deleted]

Q14.5, 14.8, 14.9 [Deleted] 334, 336-339

15

A Basis for comparison [Deleted] 341-342

BFor formulae of ratios, refer to EDB’s “Supplementary Notes for BAFS Curriculum” Appendix 1: http://334.edb.hkedcity.net/EN/supplementary_note.php

346-349

© Vision Publishing Co. Ltd 2013

Appendix 12

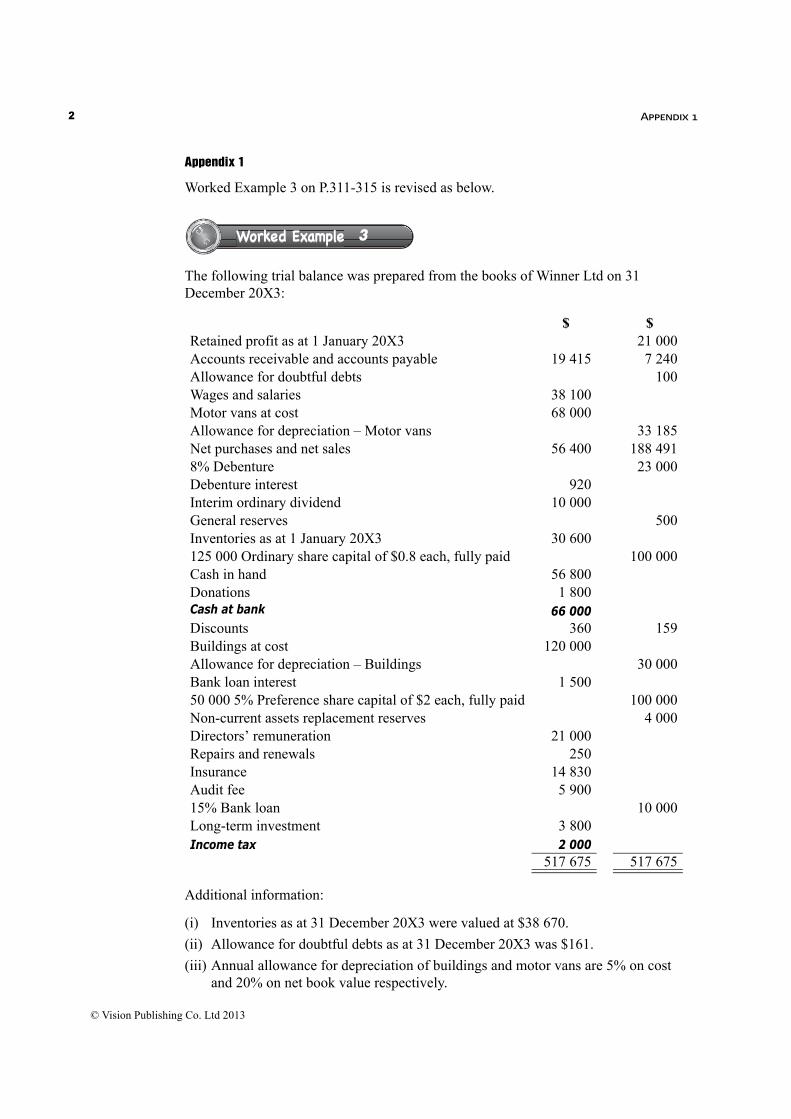

Appendix 1

Worked Example 3 on P.311-315 is revised as below.

The following trial balance was prepared from the books of Winner Ltd on 31 December 20X3:

Additional information:

(i) Inventories as at 31 December 20X3 were valued at $38 670.

(ii) Allowance for doubtful debts as at 31 December 20X3 was $161.

(iii) Annual allowance for depreciation of buildings and motor vans are 5% on cost and 20% on net book value respectively.

$ $ Retained profit as at 1 January 20X3 21 000Accounts receivable and accounts payable 19 415 7 240Allowance for doubtful debts 100Wages and salaries 38 100Motor vans at cost 68 000Allowance for depreciation – Motor vans 33 185Net purchases and net sales 56 400 188 4918% Debenture 23 000Debenture interest 920Interim ordinary dividend 10 000General reserves 500Inventories as at 1 January 20X3 30 600125 000 Ordinary share capital of $0.8 each, fully paid 100 000Cash in hand 56 800Donations 1 800Cash at bank 66 000Discounts 360 159Buildings at cost 120 000Allowance for depreciation – Buildings 30 000Bank loan interest 1 50050 000 5% Preference share capital of $2 each, fully paid 100 000Non-current assets replacement reserves 4 000Directors’ remuneration 21 000Repairs and renewals 250Insurance 14 830Audit fee 5 90015% Bank loan 10 000Long-term investment 3 800Income tax 2 000

517 675 517 675

Worked Example 3

© Vision Publishing Co. Ltd 2013

Appendix 1 3

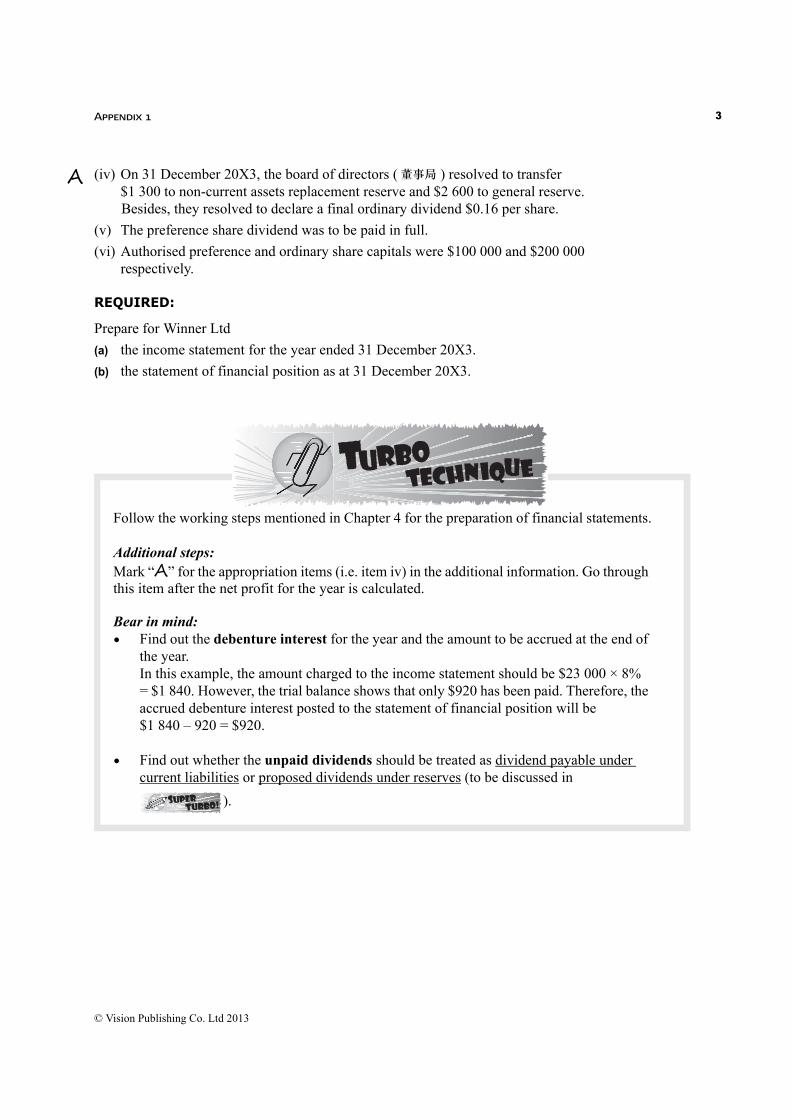

A

(iv) On 31 December 20X3, the board of directors (董事局 ) resolved to transfer $1 300 to non-current assets replacement reserve and $2 600 to general reserve. Besides, they resolved to declare a final ordinary dividend $0.16 per share.(v) The preference share dividend was to be paid in full.

(vi) Authorised preference and ordinary share capitals were $100 000 and $200 000 respectively.

REQUIRED:

Prepare for Winner Ltd

(a) the income statement for the year ended 31 December 20X3.

(b) the statement of financial position as at 31 December 20X3.

Follow the working steps mentioned in Chapter 4 for the preparation of financial statements.

Additional steps:Mark “A” for the appropriation items (i.e. item iv) in the additional information. Go through this item after the net profit for the year is calculated.

Bear in mind:Find out the debenture interest for the year and the amount to be accrued at the end of the year.In this example, the amount charged to the income statement should be $23 000 × 8% = $1 840. However, the trial balance shows that only $920 has been paid. Therefore, the accrued debenture interest posted to the statement of financial position will be $1 840 – 920 = $920.

Find out whether the unpaid dividends should be treated as dividend payable under current liabilities or proposed dividends under reserves (to be discussed in

).

© Vision Publishing Co. Ltd 2013

Appendix 14

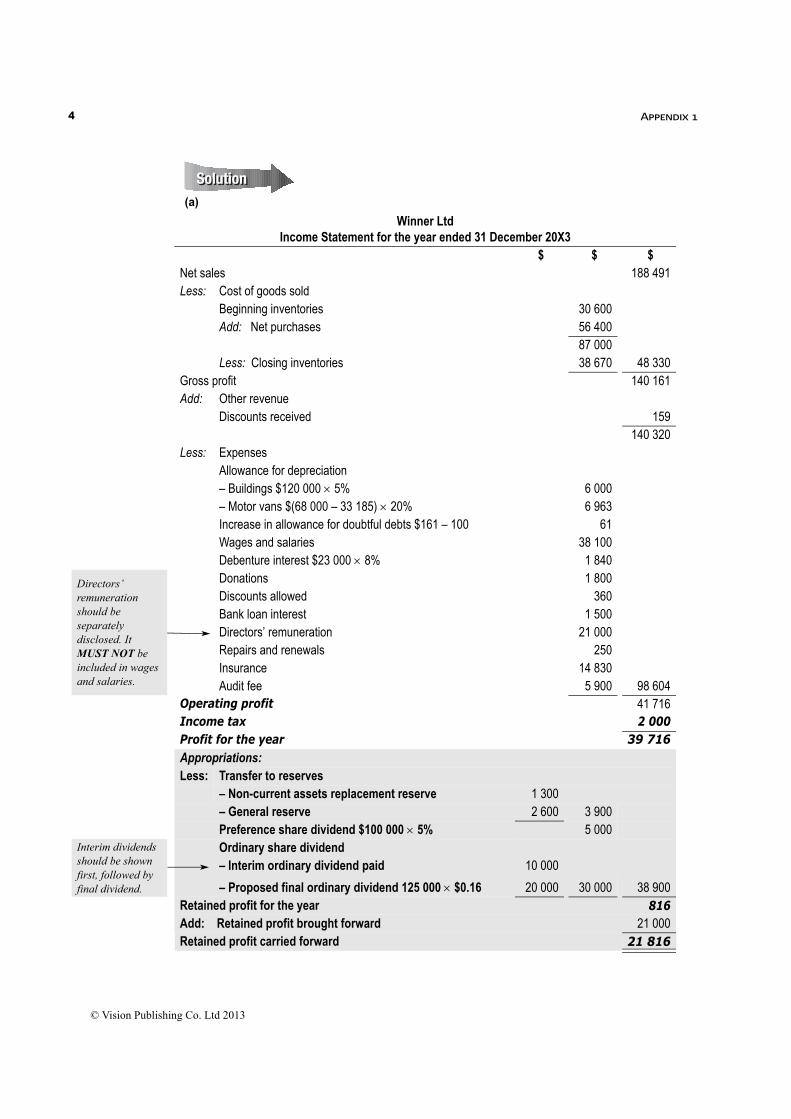

(a)

SolutionSolution

Winner LtdIncome Statement for the year ended 31 December 20X3

$ $ $ Net sales 188 491Less: Cost of goods sold

Beginning inventories 30 600Add: Net purchases 56 400

87 000Less: Closing inventories 38 670 48 330

Gross profit 140 161Add: Other revenue

Discounts received 159140 320

Less: ExpensesAllowance for depreciation– Buildings $120 000 5% 6 000– Motor vans $(68 000 – 33 185) 20% 6 963Increase in allowance for doubtful debts $161 – 100 61Wages and salaries 38 100Debenture interest $23 000 8% 1 840

Directors’ remuneration should be separately disclosed. It MUST NOT be included in wages and salaries.

Donations 1 800 Discounts allowed 360

Bank loan interest 1 500Directors’ remuneration 21 000Repairs and renewals 250Insurance 14 830Audit fee 5 900 98 604

Operating profit 41 716Income tax 2 000Profit for the year 39 716Appropriations:Less: Transfer to reserves – Non-current assets replacement reserve 1 300

– General reserve 2 600 3 900Preference share dividend $100 000 5% 5 000

Interim dividends should be shown first, followed by final dividend.

Ordinary share dividend – Interim ordinary dividend paid 10 000

– Proposed final ordinary dividend 125 000 $0.16 20 000 30 000 38 900Retained profit for the year 816Add: Retained profit brought forward 21 000Retained profit carried forward 21 816

© Vision Publishing Co. Ltd 2013

Appendix 1

©

5

Cashofirsrev(Tonex

(b)

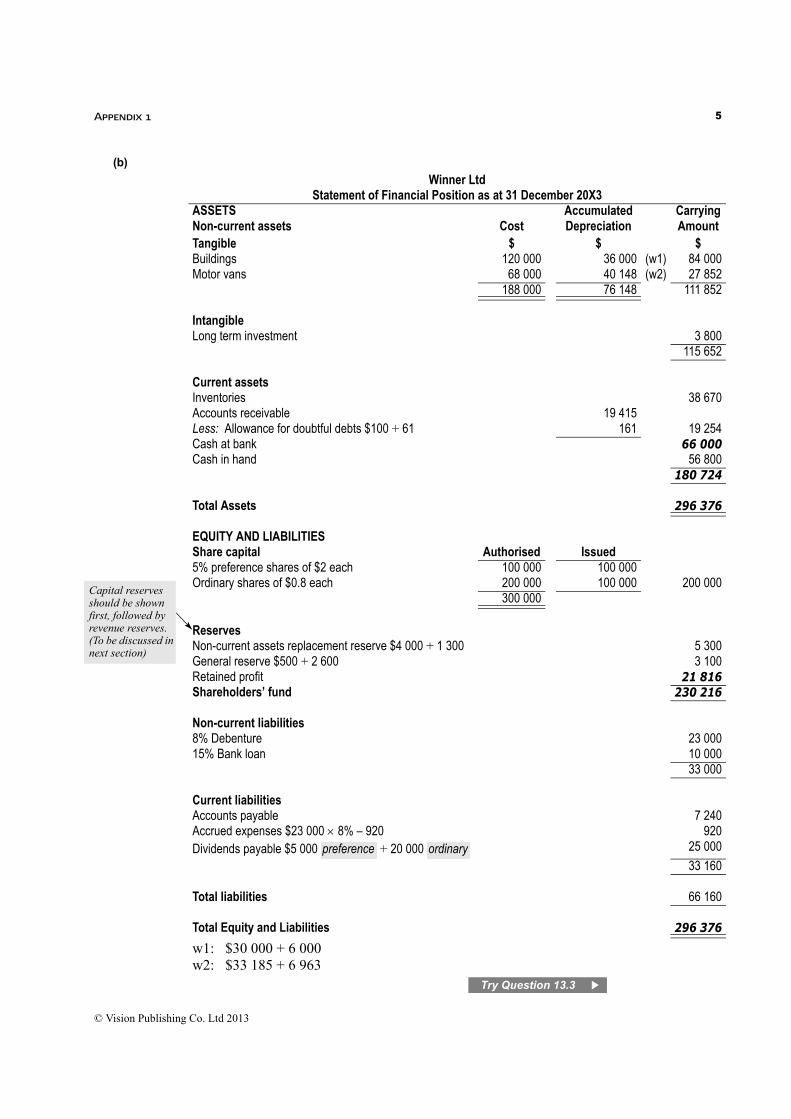

Winner LtdStatement of Financial Position as at 31 December 20X3

ASSETS Accumulated CarryingNon-current assets Cost Depreciation AmountTangible $ $ $Buildings 120 000 36 000 (w1) 84 000Motor vans 68 000 40 148 (w2) 27 852

188 000 76 148 111 852

IntangibleLong term investment 3 800

115 652

Current assetsInventories 38 670Accounts receivable 19 415Less: Allowance for doubtful debts $100 + 61 161 19 254Cash at bank 66 000Cash in hand 56 800

180 724

Total Assets 296 376

EQUITY AND LIABILITIESShare capital Authorised Issued5% preference shares of $2 each 100 000 100 000Ordinary shares of $0.8 each 200 000 100 000 200 000

300 000

ReservesNon-current assets replacement reserve $4 000 + 1 300 5 300General reserve $500 + 2 600 3 100Retained profit 21 816Shareholders’ fund 230 216

Non-current liabilities8% Debenture 23 00015% Bank loan 10 000

33 000

Current liabilitiesAccounts payable 7 240Accrued expenses $23 000 8% – 920 920Dividends payable $5 000 + 20 000 25 000

33 160

Total liabilities 66 160

Total Equity and Liabilities 296 376

w1: $30 000 + 6 000w2: $33 185 + 6 963

pital reserves uld be shown t, followed by enue reserves. be discussed in t section)

preference ordinary

Try Question 13.3

Vision Publishing Co. Ltd 2013

Appendix 16

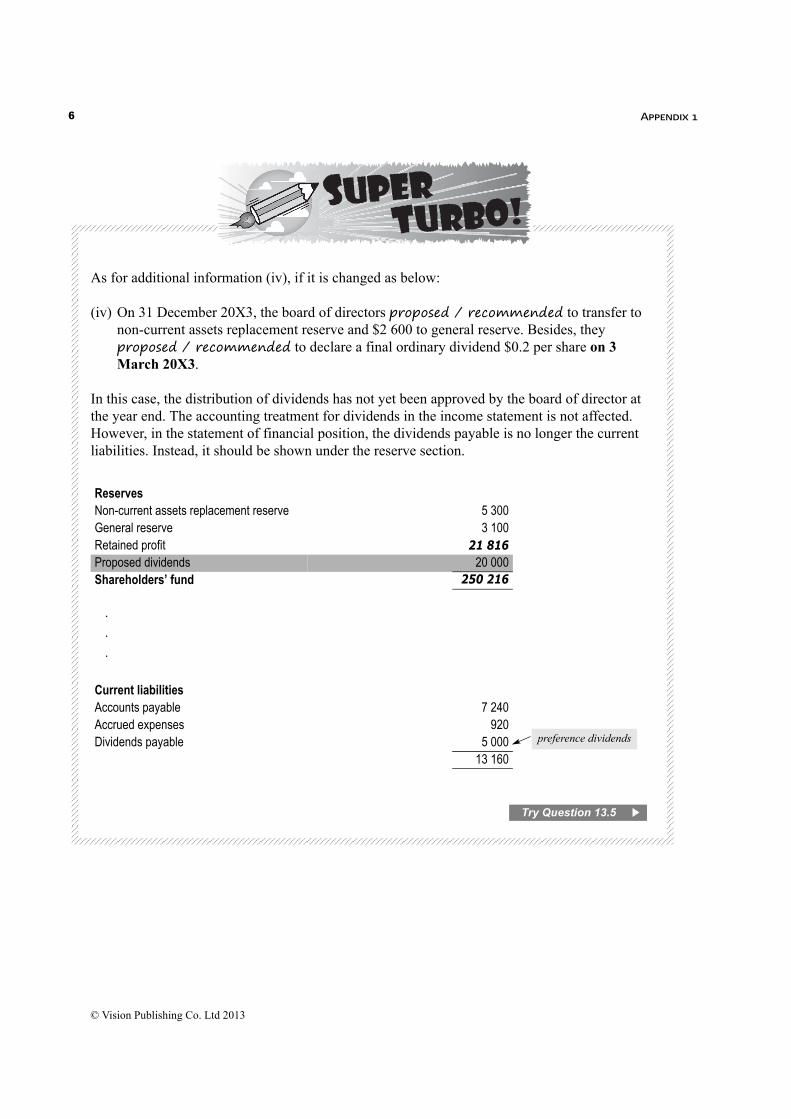

As for additional information (iv), if it is changed as below:

(iv) On 31 December 20X3, the board of directors proposed / recommended to transfer to non-current assets replacement reserve and $2 600 to general reserve. Besides, they proposed / recommended to declare a final ordinary dividend $0.2 per share on 3 March 20X3.

In this case, the distribution of dividends has not yet been approved by the board of director at the year end. The accounting treatment for dividends in the income statement is not affected. However, in the statement of financial position, the dividends payable is no longer the current liabilities. Instead, it should be shown under the reserve section.

ReservesNon-current assets replacement reserve 5 300General reserve 3 100Retained profit 21 816Proposed dividends 20 000Shareholders’ fund 250 216

Current liabilitiesAccounts payable 7 240Accrued expenses 920Dividends payable 5 000

13 160

preference dividends

Try Question 13.5

© Vision Publishing Co. Ltd 2013

Appendix 2

©

7

Appendix 2 Additional Topic:

Inventory ValuationSource: Turbo LCCI Level 2 Book-keeping & Accounts, 1st Edition (K.Y. Ng, 2010)

Excellence in Principles of Accounts Book 2, 1st Edition (K.Y. Ng, 2003)

Stock should be recorded at a lower of cost or net realisable value (成本與變現值孰低法 ).

For example, if an item of goods purchased at $15 each was damaged and would be sold at $16 after the repairs cost of $3. For this item of goods, the net realisable value, i.e. $16 – $3 = $13 is lower than the cost $15. Thus, $13 should be recorded.

Normally, net realisable value should be higher than cost in order to make profit. However, the following situations may cause net value lower than cost:

Deterioration (變質 ) Damage Obsolescence (過時 ) Change in demand

Stock included in valuation must be legally possessed by the firm. Therefore, whether goods are physically or legally in the hands of customers will affect the stock valuation. The following are the two common situations:

Goods sent to customer on sale or return basisGoods have been sent to customers but the ownership still belongs to the firm until the customers show their indication of the acceptance of goods or sell it.

Goods remain on the premises of the businessGoods have been sold to customers but not yet delivered to or collected by the customers. Therefore, the goods are still on the premises of the firm.

Cost Monetary figures at which goods are bought.

Net Realisable Value (NRV)變現淨值

Saleable value – Cost necessary to make the goods saleable (e.g. repairs)

A Stock Adjustments

1 Lower of Cost or Net Realisable Value

2 Goods in Customers’ Hands

Vision Publishing Co. Ltd 2013

Appendix 28

George operates a cleaning detergents business. He carries out an annual physical stock check.

At 31 March, the stock was valued at $7 670.

Subsequently, the following were discovered:

(1) 10 bottles of concentrated foam, costing $18 each, were outdated and would be sold at $11 in total.

(2) Owing to a small fire, some packs of cleaning powder costing a total of $400 had received minor smoke damage. It was decided to sell these items at $430 after spending $50 on repackaging.

(3) On 1 March, goods costing $250 were sent on a sale or return basis to a customer. On 8 June, the customer returned all the goods to George.

(4) Cleaning detergents costing $100 was sold at a mark up of 65% on 4 March. However, they were not delivered to customers until 15 April. There cleaning detergents were included in stock sheets at 31 March.

(5) A delivery of detergents, costing $19, was made on 26 March. They remained unpaid on 31 March.

(6) One stock sheet total had been incorrectly added to $155. The correct total should have been entered as $245.

(7) Dishwashing liquid, costing a total of $87, had been deteriorated. It was decided to destroy these items.

(8) Carpet cleaner with a selling price of $120 had been omitted from the stock sheets. The mark up on this item was 50%.

(9) 4 boxes of giant laundry powder had been included at their selling price of $288. The mark up on these was 60%.

(10) 50 bottles of cleaning detergent were included in stock at $13 each. The actual cost had been $31 each.

REQUIRED:

Show the adjustment needed to correct the stock value at 31 March. Where there is no effect write No Effect.

Physical location Legal ownership (合法擁有權 )

Goods sent to customer on sale or return basis

Customers The firm

Goods remain on the premises of the business

The firm Customers

1

© Vision Publishing Co. Ltd 2013

Appendix 2

©

9

Note:

If the firm is on fire and some stock are destroyed, the firm has to find out the amount of stock loss. For the following example, it is also applicable to (適合 ) calculate the amount of stock stolen.

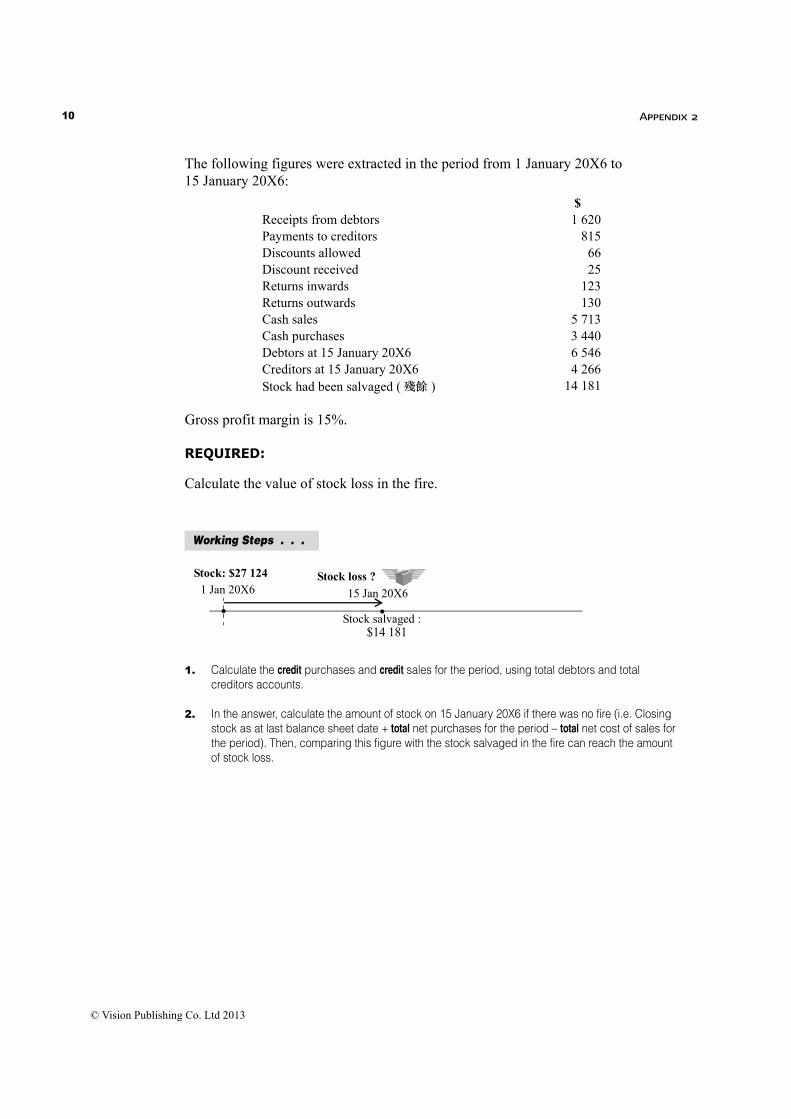

On 15 January 20X6, the warehouse of Dolls Ltd was on fire. Most of the stock was destroyed. The following figures were extracted from the final accounts of the company for the year ended 31 December 20X5:

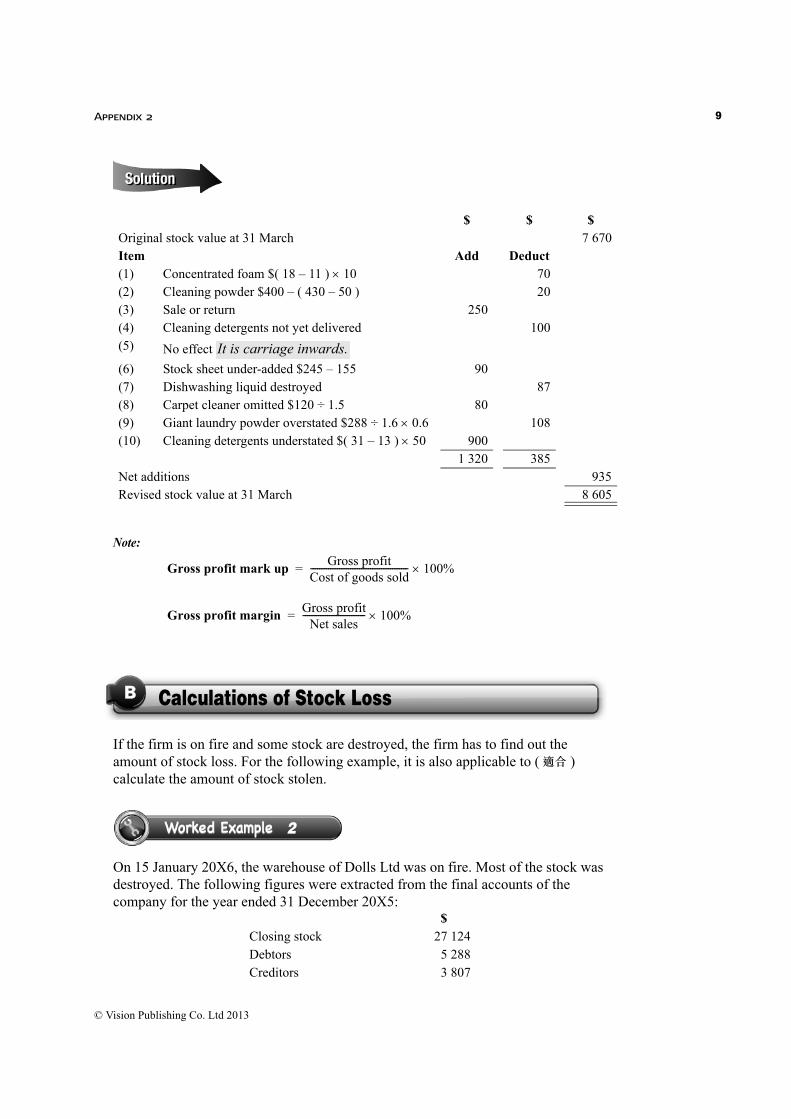

$ $ $Original stock value at 31 March 7 670Item Add Deduct(1) Concentrated foam $( 18 – 11 ) 10 70(2) Cleaning powder $400 – ( 430 – 50 ) 20(3) Sale or return 250(4) Cleaning detergents not yet delivered 100(5) No effect

(6) Stock sheet under-added $245 – 155 90(7) Dishwashing liquid destroyed 87(8) Carpet cleaner omitted $120 ÷ 1.5 80(9) Giant laundry powder overstated $288 ÷ 1.6 0.6 108(10) Cleaning detergents understated $( 31 – 13 ) 50 900

1 320 385Net additions 935Revised stock value at 31 March 8 605

$Closing stock 27 124Debtors 5 288Creditors 3 807

It is carriage inwards.

Gross profit mark upGross profit

Cost of goods sold-------------------------------------------- 100%=

Gross profit marginGross profit

Net sales---------------------------- 100%=

B Calculations of Stock Loss

2

Vision Publishing Co. Ltd 2013

Appendix 210

The following figures were extracted in the period from 1 January 20X6 to 15 January 20X6:

Gross profit margin is 15%.

REQUIRED:

Calculate the value of stock loss in the fire.

1. Calculate the credit purchases and credit sales for the period, using total debtors and total creditors accounts.

2. In the answer, calculate the amount of stock on 15 January 20X6 if there was no fire (i.e. Closing stock as at last balance sheet date + total net purchases for the period – total net cost of sales for the period). Then, comparing this figure with the stock salvaged in the fire can reach the amount of stock loss.

$Receipts from debtors 1 620Payments to creditors 815Discounts allowed 66Discount received 25Returns inwards 123Returns outwards 130Cash sales 5 713Cash purchases 3 440Debtors at 15 January 20X6 6 546Creditors at 15 January 20X6 4 266Stock had been salvaged (殘餘 ) 14 181

Working Steps . . .

15 Jan 20X61 Jan 20X6

Stock salvaged :

Stock loss ?

$14 181

Stock: $27 124

© Vision Publishing Co. Ltd 2013

Appendix 2

©

11

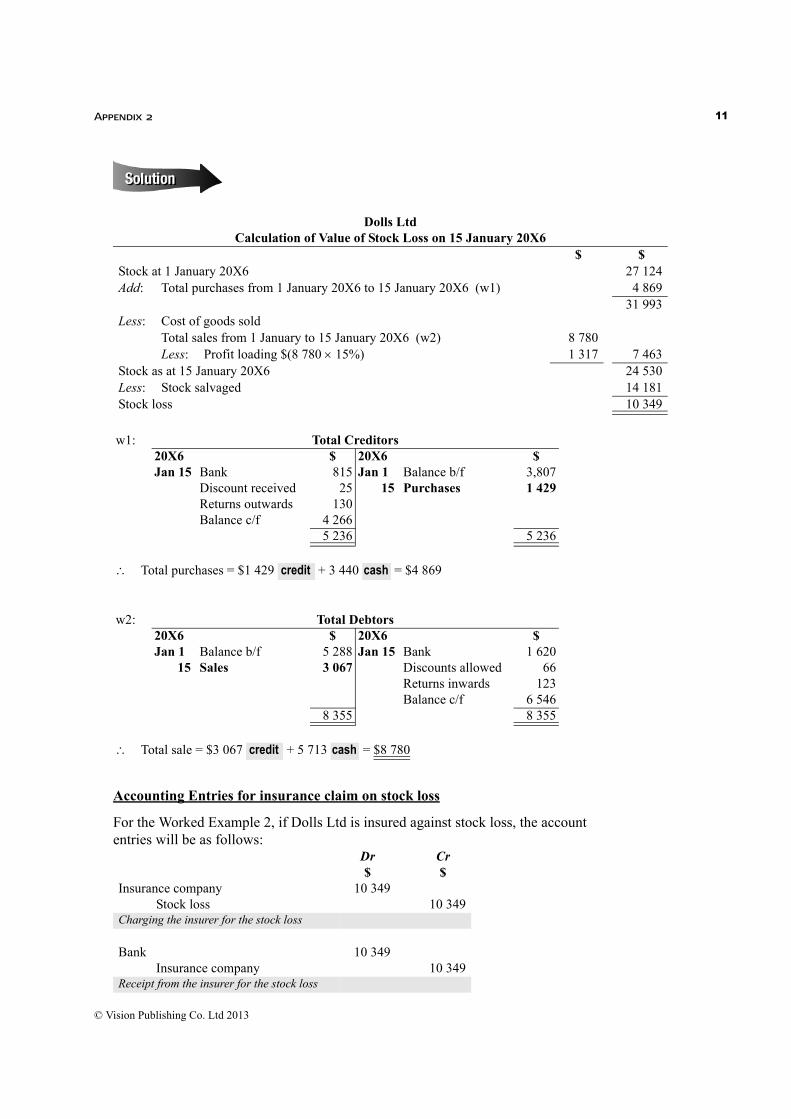

Accounting Entries for insurance claim on stock loss

For the Worked Example 2, if Dolls Ltd is insured against stock loss, the account entries will be as follows:

Dolls LtdCalculation of Value of Stock Loss on 15 January 20X6

$ $ Stock at 1 January 20X6 27 124Add: Total purchases from 1 January 20X6 to 15 January 20X6 (w1) 4 869

31 993Less: Cost of goods sold

Total sales from 1 January to 15 January 20X6 (w2) 8 780Less: Profit loading $(8 78015%) 1 317 7 463

Stock as at 15 January 20X6 24 530Less: Stock salvaged 14 181Stock loss 10 349

w1: Total Creditors20X6 $ 20X6 $Jan 15 Bank 815 Jan 1 Balance b/f 3,807

Discount received 25 15 Purchases 1 429Returns outwards 130Balance c/f 4 266

5 236 5 236

Total purchases = $1 429 + 3 440 = $4 869

w2: Total Debtors20X6 $ 20X6 $Jan 1 Balance b/f 5 288 Jan 15 Bank 1 620 15 Sales 3 067 Discounts allowed 66

Returns inwards 123Balance c/f 6 546

8 355 8 355

Total sale = $3 067 + 5 713 = $8 780

credit cash

credit cash

Dr Cr$ $

Insurance company 10 349Stock loss 10 349

Charging the insurer for the stock loss

Bank 10 349Insurance company 10 349

Receipt from the insurer for the stock loss

Vision Publishing Co. Ltd 2013

Appendix 212

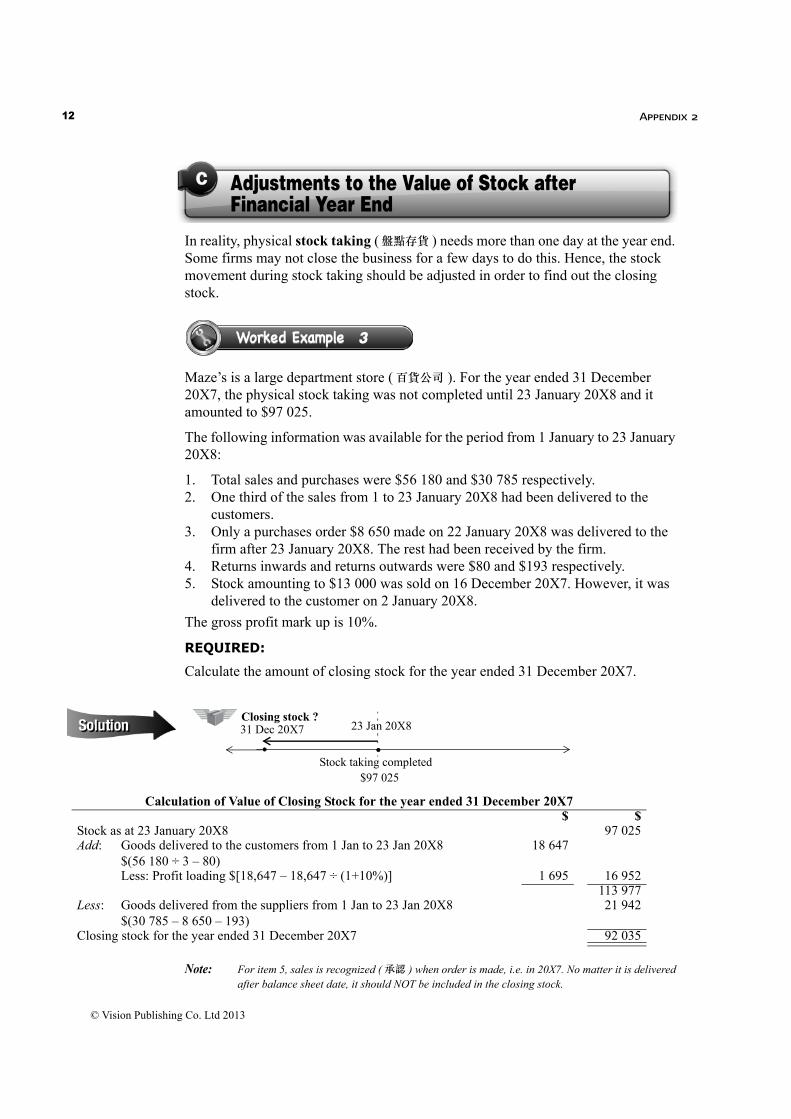

In reality, physical stock taking (盤點存貨 ) needs more than one day at the year end. Some firms may not close the business for a few days to do this. Hence, the stock movement during stock taking should be adjusted in order to find out the closing stock.

Maze’s is a large department store (百貨公司 ). For the year ended 31 December 20X7, the physical stock taking was not completed until 23 January 20X8 and it amounted to $97 025.

The following information was available for the period from 1 January to 23 January 20X8:

1. Total sales and purchases were $56 180 and $30 785 respectively. 2. One third of the sales from 1 to 23 January 20X8 had been delivered to the

customers.3. Only a purchases order $8 650 made on 22 January 20X8 was delivered to the

firm after 23 January 20X8. The rest had been received by the firm.4. Returns inwards and returns outwards were $80 and $193 respectively.5. Stock amounting to $13 000 was sold on 16 December 20X7. However, it was

delivered to the customer on 2 January 20X8.

The gross profit mark up is 10%.

REQUIRED:

Calculate the amount of closing stock for the year ended 31 December 20X7.

Note: For item 5, sales is recognized (承認 ) when order is made, i.e. in 20X7. No matter it is delivered after balance sheet date, it should NOT be included in the closing stock.

C Adjustments to the Value of Stock after Financial Year End

3

31 Dec 20X7

Stock taking completed

Closing stock ? 23 Jan 20X8

$97 025

Calculation of Value of Closing Stock for the year ended 31 December 20X7$ $

Stock as at 23 January 20X8 97 025Add: Goods delivered to the customers from 1 Jan to 23 Jan 20X8

$(56 180 ÷ 3 – 80)18 647

Less: Profit loading $[18,647 – 18,647 ÷ (1+10%)] 1 695 16 952113 977

Less: Goods delivered from the suppliers from 1 Jan to 23 Jan 20X8$(30 785 – 8 650 – 193)

21 942

Closing stock for the year ended 31 December 20X7 92 035

© Vision Publishing Co. Ltd 2013