Embed Size (px)

Citation preview

∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙

Toward a Sustainable Cement Industry Substudy 9: Industrial Ecology in the Cement Industry March 2002

by Bruce Vigon

with contributions from

Tiffany Brunetti, Vinay Gadkari, Scott Butner, and Jill Engel-Cox

∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙ ∙

An Independent Study Commissioned by:

World Business Council for Sustainable Development This substudy is one of 13 research investigations conducted as part of a larger project entitled, "Toward a Sustainable Cement Industry". The project was commissioned by the World Business Council for Sustainable Development as one of a series of member-sponsored projects aimed at converting sustainable development concepts into action. The report represents the independent research efforts of Battelle Memorial Institute and their subcontractors to identify critical issues for the cement industry today, and pathways forward toward a more sustainable future. While there has been considerable interactive effort and exchange of ideas with many organizations within and outside the cement industry during this project, the opinions and views expressed here are those of Battelle and its subcontractors. Battelle Battelle endeavors to produce work of the highest quality, consistent with our contract commitments. However, because of the research nature of this work, the recipients of this report shall undertake the sole responsibility for the consequence of their use or misuse of, or inability to use, any information, data or recommendation contained in this report and understand that Battelle makes no warranty or guarantee, express or implied, including without limitation warranties of fitness for a particular purpose or merchantability, for the contents of this report. Battelle does not engage in research for advertising, sales promotion, or endorsement of our clients' interests including raising investment capital or recommending investments decisions, or other publicity purposes, or for any use in litigation. The recommendations and actions toward sustainable development contained herein are based on the results of research regarding the status and future opportunities for the cement industry as a whole. Battelle has consulted with a number of organizations and individuals within the cement industry to enhance the applicability of the results. Nothing in the recommendations or their potential supportive actions is intended to promote or lead to reduced competition within the industry.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

i

Foreword Many companies around the globe are re-examining their business operations and relationships in a fundamental way. They are exploring the concept of Sustainable Development, seeking to integrate their pursuit of profitable growth with the assurance of environmental protection and quality of life for present and future generations. Based on this new perspective, some companies are beginning to make significant changes in their policies, commitments and business strategies. The study, of which this substudy is a part, represents an effort by ten major cement companies to explore how the cement industry as a whole can evolve over time to better meet the need for global sustainable development while enhancing shareholder value. The study findings include a variety of recommendations for the industry and its stakeholders to improve the sustainability of cement production. Undertaking this type of open, self-critical effort carries risks. The participating companies believe that an independent assessment of the cement industry’s current status and future opportunities will yield long-term benefits that justify the risks. The intent of the study is to share information that will help any cement company – regardless of its size, location, or current state of progress – to work constructively toward a sustainable future. The pursuit of a more sustainable cement industry requires that a number of technical, managerial, and operational issues be examined in depth. This substudy, one of 13 conducted as a part of the project, provides the basis for assessing the current status or performance and identifies areas for progress toward sustainability on a specific topic. The project report entitled Toward a Sustainable Cement Industry may be found on the project website: http://www.wbcsdcement.org.

Study Groundrules

This report was developed as part of a study managed by Battelle, and funded primarily by a group of ten cement companies designated for this collaboration as the Working Group Cement (WGC). By choice, the study boundaries were limited to activities primarily associated with cement production. Downstream activities, such as cement distribution, concrete production, and concrete products, were addressed only in a limited way. Battelle conducted this study as an independent research effort, drawing upon the knowledge and expertise of a large number of organizations and individuals both inside and outside the cement industry. The cement industry provided a large number of case studies to share practical experience. Battelle accepted the information in these case studies and in public information sources used.

The WGC companies provided supporting information and advice to assure that the report would be credible with industry audiences. To assure objectivity, a number of additional steps were taken to obtain external input and feedback. A series of six dialogues was held with stakeholder groups around the world (see Section 1.5). The World Business Council for Sustainable Development participated in all meetings and

monitored all communications between Battelle and the WGC. An Assurance Group, consisting of distinguished independent experts, reviewed both the quality

and objectivity of the study findings. External experts reviewed advanced drafts of technical substudy reports.

The geographic scope of the study was global, and the future time horizon considered was 20 years. Regional and local implementation of the study recommendations will need to be tailored to the differing states of socioeconomic and technological development.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

ii

List of Acronyms ACBFS air-cooled blast-furnace slag

AFR alternative fuels and raw materials that are inputs to cement production derived from industrial, municipal, and agricultural waste streams

BFS blast-furnace slag, a processed waste product of pig iron production

CEM I Ordinary Portland Cements (European Standard)

CEM II blended cements with 65 - 95% OPC content

CEM III blended cements with 20 - 64% OPC content

EBIT earnings before interest and taxes

EMAS Eco-Management and Audit Scheme

GBFS granulated blast-furnace slag is obtained by rapid quenching of molten blast-furnace slag in water. GBFS has latent hydraulic properties.

GGBFS ground granulated blast-furnace slag is an intermediate material for slag cements. GGBFS cannot completely substitute for clinker because the slag needs an activator to start the chemical reaction to set the concrete.

GRI Global Reporting Initiative IE Industrial ecology ISO International Organization for Standardization KPI Key Performance Indicator LCA Life Cycle Assessment NGO Non-Governmental Organization

OPC Ordinary Portland Cement consisting of approximately 95% ground clinker and 5% gypsum

SD Sustainable Development WGC Working Group Cement (ten core cement company sponsors)

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

iii

Glossary Adsorptive Physical-chemical property of a material that promotes the binding of substances to the surface

Alternative Fuels Energy containing wastes used to substitute for conventional thermal energy sources. Alternative Raw Materials Cementitious materials used as substitutes for conventional cement raw materials.

Alternative Fuels and Raw Materials (AFR) Inputs to cement production derived from industrial, municipal, and agricultural waste streams.

Binder Cohesive agent which could include cement, blended cements, and fly ash.

Blended cement* Cement with a fixed percentage of pozzolans (for example, supplements such as slag and fly ash produced by the steel and electric power industries, respectively) replacing the Portland cement clinker portion of the cement mix. Blended cement is usually understood as cement that is blended by a cement manufacturer rather than a ready-mix supplier (also referred to as composite cement).

By-Product Secondary product of an industrial process.

Cement Within the cement industry, and especially the technical domain, this term is often understood as Ordinary Portland Cement.

Clinker Decarbonized, sintered, and rapidly-cooled limestone. Clinker is an intermediate product in cement manufacturing.

Concrete A material produced by mixing binder, water, and aggregate. The fluid mass undergoes hydration to produce concrete. (Average cement content in concrete is about 15%.).

Compressive strength The maximum resistance of a material to axial compressive loading; expressed as force per unit of cross-sectional area (concrete is measured in N/mm2)

Co-processing Term used in some regions to refer to the practice of introducing AFR into cement production

Fly ash By-product with binding properties typically produced as a residue from coal-fired power plants.

Fossil fuel A general term for combustible geological deposits of carbon in reduced (organic) form and of biological origin, including coal, oil, natural gas, and oil shale.

Granulation Molten BFS is granulated by rapid quenching in water

Industrial clusters Groups of companies with the potential for exchange of materials and energy to mutual advantage

Industrial ecology Framework for improvement in the efficiency of industrial systems by imitating aspects of natural ecosystems, including the cyclical transformation of wastes to input materials.

Industrial metabolism A process in an industrial system that mimics processes in nature wherein one species’ waste provides food or energy input for another

industrial symbiosis A relationship in which organizations are able to survive and prosper because of their exchanges of materials and energy carriers

Kiln Large industrial oven for producing clinker used in manufacture of cement.

Mineral components (MIC) Cement constituents with binding properties (e.g. GGBFS, fly ash, pozzolan) which are not derived from the clinker-manufacturing process

* The International Council for Local Environmental Initiatives (ICLEI), 2001, http://www.iclei.org/about.htm.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

iv

Pozzolan A mineral admixture that acts as a supplement to standard Portland cement hydration products to create additional binder in a concrete mix.†

Pozzolanic cement Cement formulated using a specific percentage of pozzolan in place of Portland cement

Precast Concrete elements cast and cured off site; pipes, etc.

Ready mix Concrete delivered to site in a fresh state

Setting time The time required for freshly mixed concrete to set

Slag cement Blended cement consisting of OPC and GGBFS

Special binder Custom binders not covered by standards

Sustainable development Ability to continually meet the needs of the present without compromising the ability of future generations to meet their own needs.

Thermal processing Treatment of waste materials at high temperature to render them harmless to human health or the environment

Valorization Process of assigning financial utility to a material or service; typically used in the cement industry to define waste recovery versus disposal

Workability Property of freshly mixed concrete, describing homogeneity and the ease with which the concrete can be mixed, pumped, placed, consolidated, and finished.

† The International Council for Local Environmental Initiatives (ICLEI, 2001, Cement Glossary, http://www.iclei.org/us/cement/glossary.html

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

v

Executive Summary Industrial Ecology (IE) is a concept for improving the efficiency of industrial systems by imitating aspects of natural ecosystems. At the heart of the IE concept is the idea that businesses can exchange materials or energy to mutual advantage. Within the cement industry, the use of alternative fuels and raw materials (AFR) is an example of this type of exchange. However, the relevance of IE to the cement industry extends beyond the use of AFR. The overall objective of this substudy was to characterize the potential SD consequences of adopting the concept of IE more broadly within the cement industry, including a discussion of the drivers and barriers to implementation, and technologies and tools available to increase the potential of IE. For the purposes of this study, the following definition of IE for the cement industry is offered as a practical target for realization of IE concepts:

While cement industry initiatives or involvement in IE span a range of engagements and levels of integration with other organizations in an ecosystem, the historical activities may not meet the definition of a sustainable industrial ecosystem. Cement plants addressing only specific internal goals, such as net zero fuel cost, are not working within the collaborative partnership that a true IE arrangement entails. Like most industries, the cement industry currently considers internal economic factors in decision-making related to IE. However, economics may create a barrier to implementation, particularly when large capital costs are required to make plant modifications to use new materials or fuels. Resolving conflicts between barriers and incentives is often one of the greatest challenges. Drivers for IE within the cement industry include the following: Financial Incentives: companies have a strong financial reason to investigate their cost

reductions through alternative fuels and raw materials (or extending clinker capacity to delay capital investment),

Government Support: government policy, regulations and implementation that either actively promote or do not discourage the practice,

Waste Management Infrastructure Deficiencies: the collection, transport, and disposal systems for industrial waste are lacking or the disposal capacity in landfills or incinerators is limited, and

Community Engagement: inclusion of environmental and public health activist groups in the planning and evaluation process for the fuel or raw material change is consistent with the company policy or governments have required or encouraged their involvement.

Barriers to IE implementation, apart from the absence of the above listed drivers, include: Perception of IE as Waste Disposal: the notion that IE is simply an alternative waste

disposal mechanism with little or no social benefits Environmental or Human Health Damage: evidence or perception that waste burning

causes or could cause environmental or health impacts in the local area Lack of Awareness of Market Opportunities: inability to identify and capitalize on sources

of waste in the region that could be usefully processed

Industrial Ecology is a business relationship among a set of partner organizations in which a cement company uses or provides materials and energy carriers that cannot be reused or recycled by the generating process and which otherwise would have no or little economic value as co-products. The cement company’s use or provision of these materials must correspond to the creation of system level net benefits (economic, social, and environmental) as well as benefits to the cement company.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

vi

Resistance to Products Manufactured From or Containing AFR: purchasers determination not to specify or buy products that are made with AFR or which incorporate AFR residuals

Business Operational Issues: adverse influences on product quality or output associated with use of AFR.

Currently, the cement industry does not consider the full set of trade-offs and net benefits of IE decisions. Sustainability Considerations, or decisions based on the net impact on the community and long-term viability of operations are key to the adoption of more sustainable practices. Ultimately, the objective should be to move toward a sustainable industrial ecosystem. Characteristics specified in this research for such systems include: True partnerships with active collaboration among multiple industries with sustainability

goals All participants benefit with considerations for both partners and society at large Waste management hierarchy principles apply with exceptions determined through

application of systems analysis tools Zero waste goals Quantitative benefits that are substantial enough to show improvements to the environment Innovation and tools that allow for more creative solutions and more significant benefits Location and relationship of partners is not limited to a co-located arrangement.

The industry needs a structure to allow them to realize a core role in the emerging field of IE. The cement industry is well-suited for this role as evidenced by the potential for multiple and diverse flows of resources, the potential for internal economic returns and creating social benefits. IE should be an integral part of corporate strategic planning. Company strategic goals incorporating IE need to be translated to the plant level. The framework proposed in this study would allow companies to assess their current activities, evaluate drivers, barriers, and impacts, prioritize and set goals, and develop action plans. Specific recommendations for progress toward sustainable industrial ecosystems are to: Develop an integrated IE component of corporate strategy and show how this systematic

approach has supported the identification of specific areas of improvement. Set and communicate goals for specific performance indicators for the corporation, the local

company, and individuals that reflect a true sustainable IE focus and work to align the various responsible groups to achieve success.

Provide operating companies and facilities with the necessary information and tools to fully evaluate and implement the attractive opportunities.

Obtain a more complete picture of the full range of IE opportunities regionally and locally and identify which organizations to work with to remove barriers. Consider collaborations with broker organizations acting to help introduce potential IE partners.

Build strong ecosystems by engaging with multiple partners and establishing working relationships at various levels in the partnering companies. Consider expanding into the collection, processing, and delivery of waste materials where a business case can be made and where the local infrastructure is an implementation barrier.

Establish dialogue with local and national level governments to create an objective basis for creating policies to support IE development and for evaluating IE opportunities.

Condition and educate the marketplace if the results of an IE implementation will change the product characteristics or composition.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

vii

Conduct or support research to characterize the risks and benefits of an IE opportunity for the company, plant workers, and the communities and other components of society affected. Do not rely on generic data unless it is clearly relevant and applicable.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

viii

Table of Contents 1. Introduction ......................................................................................................................... 1

1.1. Study Objectives......................................................................................................... 1 1.2. Study Scope ............................................................................................................... 1 1.3. Technical Approach .................................................................................................... 2

2. Industrial Ecology: Concept and Relevancy ........................................................................ 3 2.1. What is Industrial Ecology?......................................................................................... 3 2.2. The Relationship between Industrial Ecology and Sustainable Development.............. 4 2.3. Relevance of Industrial Ecology to the Cement Industry ............................................. 6

3. Industrial Ecology in the Cement Industry ......................................................................... 11 3.1. Drivers, Barriers, and Current Status of IE ................................................................ 11 3.2. Assessment of IE Practices in Relation to SD........................................................... 22

4. Industry Ecology in Cement Company Strategy ................................................................ 27 4.1. Need for an IE Component in Corporate Strategy..................................................... 27 4.2. Incorporating IE in Business Strategy ....................................................................... 28

5. Conclusions and Recommendations ................................................................................. 33 5.1. Relevancy of the Industrial Ecology Concept ............................................................ 33 5.2. Assessment of IE within the Cement Industry ........................................................... 33 5.3. Need for an IE Structure ........................................................................................... 34 5.4. Specific Recommendations....................................................................................... 34

6. References ....................................................................................................................... 35 Appendix A: Focused Case Studies ........................................................................................A-1 Appendix B: Alsen Cement and Salzgitter Steelworks Case Study..........................................B-1 Appendix C: Toward a Zero Emissions Society: Contributions of a Cement Plant - Case Study Taiheiyo Cement Corporation, Japan ..................................................................................... C-1 Appendix D: Self-Assessment Tool for Industrial Ecology (IE)................................................ D-1

List of Tables Table B-1: Product Properties and Environmental Impact of an OPC and Two

Slag Cements.................................................................................................................B-11 Table D-1: Self-Assessment Tool - Signal Chart Criteria ........................................................ D-1 List of Figures Figure 3-1. Potential Material and Energy Flows in a Cement Plant-Centric IE System............ 15 Figure 3-2. Waste Use Trends vs. Economic Development..................................................... 18 Figure 3-3. Flow and Quality Relationships in a Sustainable IE System ................................... 23 Figure 4-1. Proposed Process for Developing an IE Strategic Component.............................. 28 Figure 4-2. Example Signal Chart after Assessment ............................................................... 29 Figure B-1. ALSEN’s Market Penetration of Slag Cements .....................................................B-7 Figure B-2. Flow Chart of Granulation Plant ..........................................................................B-10 Figure B-3. Negative Environmental Impact of Slag Cements ...............................................B-12 Figure B-4. Positive Environmental Impact of Slag Cements.................................................B-12 Figure B-5. The Coarse Concept...........................................................................................B-13 Figure C-1. The Cement Industry at the Core of an Industrial Cluster..................................... C-3 Figure C-2. Flow Diagram of Ecocement Manufacturing Process........................................... C-7 Figure C-3. The Cement Plant Resource Recycling System................................................. C-11

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

1

1. Introduction Industrial Ecology (IE) is a concept for improving the efficiency of industrial systems by imitating aspects of natural ecosystems. It provides an objective means for making progress toward sustainable development. IE considers a range of sustainability issues including energy and resource conservation; environmental, health, and safety improvement; climate change management and land use. To employ IE as a basis for progress toward sustainable development (SD), an organization must understand the risks and benefits as well as the implementation challenges. To develop this understanding, companies must assess the business implications; the impact on organizational and plant level goals; the potential for innovative changes, community response, and the influences of supporting or constraining corporate or governmental policies. This substudy focuses on principles of IE relevant to the cement industry and includes a discussion of both the benefits and barriers to implementing a company strategy with a strong IE component. This report documents the results of one of 13 substudies under the WBCSD project Toward a Sustainable Cement Industry. Issues analyzed in the substudies are combined in an understandable way for external stakeholders by integrating particular findings and recommendations within the Triple Bottom Line of SD and the specific sustainability issues identified for the cement industry. This substudy develops actions whose primary focus is Resource Productivity. Secondary issues addressed are Emission Reduction, Ecological Stewardship, and Shareholder Value.

1.1. Study Objectives The overall objective of this substudy is to characterize the potential SD consequences of adopting the concept of IE more broadly within the cement industry. This study focuses on understanding the factors that enhance or create barriers to implementation of IE more so than the specific materials flows and energy resources that make up an industrial ecosystem. Additionally, technologies and tools that may increase the attractiveness and feasibility of IE are evaluated. Finally, this study also provides a structure for developing or enhancing an IE strategy at the corporate level.

1.2. Study Scope The substudy lays a foundation for understanding IE and related concepts for integrating the flows of mass, energy, and money of industrial systems. The substudy investigates the potential business opportunities and challenges that the cement industry faces in more widely implementing IE, including regional perspectives and priorities. In addition to characterizing existing examples of IE where the cement industry has been a partner, the substudy identifies and analyzes relevant examples from other industry sectors to understand the factors, at both the industry and regional/local levels, leading to successful implementation. The final section provides a step-by-step process for corporate cement organizations to more broadly implement IE by: Assessing the organization’s current use of IE principles Evaluating drivers, barriers, and potential consequences of current and future actions Understanding priorities for establishing a IE-oriented corporate business strategy and

developing goals, and Applying the corporate strategy to develop specific action plans at plant level to meet

organizational goals taking IE into consideration.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

2

1.3. Technical Approach This study was carried out by: describing and evaluating a number of IE concepts discussed in the literature synthesizing a definition of IE for practical realization of the concept by the cement industry

within a Sustainable Development framework characterizing the state of practice through literature reviews, interviews, and case studies developing a structured process to further enhance IE implementation within the cement

industry. Part 2 of this report describes IE and the Cement Industry and is based on literature and theories involving IE approaches. This information provides the groundwork for a workable definition of IE for the industry. The section is supported by case studies, based on the cement industry and other relevant industry examples. Part 3 gives a more detailed analysis of the potential for IE in the cement industry. This section is based on company, local, or regional data as appropriate and as available. Part 3 further discusses barriers and drivers to IE for the industry based on a review of current activities. Part 4 develops a structure for IE within a corporate strategy and identifies responses at a plant level to implement the corporate strategy. This information is based on the review of related concepts and the cement industry-specific analysis. Part 5 provides a discussion of recommendations for the industry.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

3

2. Industrial Ecology: Concept and Relevancy 2.1. What is Industrial Ecology? The term Industrial Ecology refers to the notion that industrial systems can be made more efficient by imitating selected aspects of natural ecosystems. For example, in natural ecosystems the waste from one organism (and of course, often the organism itself) becomes the food for others. Extended across the entire eco-system, this "food web" allows nutrients to be recycled continuously in an essentially closed loop. In an industrial ecosystem, this food web concept is applied to businesses, allowing materials to be recycled. In the view of industrial ecologists, such a system can help industry to be more sustainable. In this report, the term "industrial ecology" is used to suggest a perspective that views the cement industry as one "species" in a complex and interdependent collection of industries. In this context, it should be noted that while the "food web" concept is a useful one, the ecosystem analogy does not end there. Industrial ecology may be used as a way of understanding how businesses adapt to changes in the industrial ecosystem. In this way, industrial ecology can shed light on a number of important questions, including: How do industrial ecosystems

emerge? Can industrial ecosystems be

designed, or must they evolve over time? How do industries and technologies change over time? Are there predictable patterns of

succession, emergence and adaptation? How are industries affected by the introduction of new products, technologies, or regulations?

What kinds of adaptive strategies can be "borrowed" from nature to help businesses become sustainable in a constantly changing world? How do industrial ecosystems interact with the natural environment? What strategies can

businesses employ to adapt to shortages of water and other resources? Although such issues may appear to be of interest primarily to academic researchers, we believe they are central to the sustainability of the cement industry. In order to be sustainable in the most basic sense of the word, the cement industry needs to adapt and change to increasing environmental and social demands. In this report, the term "industrial ecology" is used to suggest a perspective that views the cement industry as one contributor to a complex and interdependent collection of industries. The ecological comparison provides a great opportunity for understanding adaptation strategies found in natural systems. Some of these natural examples are likely to provide insight into analogous adaptive strategies that the cement

Historical Development of Industrial Ecology

Much of the current interest in industrial ecology can be traced back to a 1989 Scientific American article by Robert Frosch and Nicolas Gallopoulos published under the unremarkable title "Strategies for Manufacturing."17 In this article, the authors introduced into popular usage many of the important concepts and terms that still comprise the core of Industrial ecology. Most importantly, the article introduced the "food chain" analogy that dominates much of today's discussion of Industrial ecology.

Central to this analogy is the observation that in natural ecosystems, organisms exist as part of a complex "food chain" in which one organism becomes the food for another. This process is repeated throughout the ecosystem to effect a continuous recycling of materials. The idea that businesses could learn to create similar kinds of "closed loops" was quite appealing in light of increasing environmental regulations, stakeholder pressures to reduce environmental emissions, and growing scarcity of natural resources, such as water and fossil fuels.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

4

Industrial Ecology: Integrating Business and Society

“Operating on a global scale brings problems at a global level. The environmental issues now facing industry are no longer focused simply on local toxic impacts – although these remain potentially serious. There are now unintended effects on the total global environment, of which global warming and ozone depletion may be only the most visible of a multitude of adverse symptoms.

The emerging environmental challenge requires a technical and management approach capable of addressing problems of global scope. By contrast, the environmental agenda of companies today is frequently driven by a list of individual issues because there is no accepted overall framework to shape comprehensive programs.

Corporate environmental agendas typically list goals such as eliminating the use of chlorofluorocarbons (CFCs), promoting recycling, increasing energy efficiency, and minimizing the production of hazardous waste. The question is whether this kind of action list goes far enough in dealing with underlying causes, or whether it is largely treating symptoms. Will it protect business against further "environmental surprises"? In its complexity, the global environmental problem-set somewhat resembles an iceberg--well-publicized environmental problems are the visible one-tenth above the surface. We still know too little about the adaptive capacity of the natural environment as a whole to predict confidently how it will react to continuing industrialization. If the iceberg suddenly rolls over, it could expose problems that the average business is quite unprepared for.

Effective defense against this uncertainty will be based on the recognition of a key principle. The ultimate driver of the global environmental crisis is industrialization, which means significant, systemic industrial change will be unavoidable if society is to eliminate the root causes of environmental damage. The resulting program of business change will have to be based in a far-sighted conceptual framework if it is to ensure the long-term viability of industrialization, and implementation will need to begin soon.

…[I]ndustrial ecology [is] the best available candidate for this needed conceptual framework. In

industry might use to define new market niches, foster increased cooperative behavior, and profit from the natural succession of industries in emerging and established economies.

2.2. The Relationship between Industrial Ecology and Sustainable Development

Some authors have claimed that IE is an essential tool for achieving sustainable development.3

Although the concepts of sustainability and IE are still fairly new, and it may be too soon to describe the ultimate linkage, it is clear that IE provides a conceptual basis for understanding some aspects of sustainability. IE is especially well suited to evaluate those aspects dealing with material and energy flows in the environment. By seeking ways to "close the loop" on material cycles, IE extends the useful lifetime of material resources and reduces the impact of their acquisition on the environment. SD implies a set of goals that typically includes the "triple bottom line" of economic prosperity, environmental stewardship, and social responsibility. IE does not explicitly address economic or social issues, but the economic and social consequences of implementing IE activities can be identified. Some proponents of IE have used the term loosely, to describe any economically beneficial use of industrial byproducts. Such an approach tends to overlook the question of whether there are some materials that should not be incorporated into products even if a market can be found for them, especially when our understanding of their fate in the environment is lacking. This substudy adopts a more strict definition that considers both economic viability and environmental implications. In the end, IE is best viewed as one of several tools that may be applied to enhance sustainable practices. It provides a powerful way to think about how businesses manage materials, adapt to change, and create value.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

5

TNS System Conditions

The TNS conditions, which are based loosely on thermodynamic principles, require that in a sustainable society, the natural world is not subject to increasing: 1. concentrations of substances extracted

from the earth's crust, 2. concentrations of substances produced by

society, or 3. degradation by physical means.

Furthermore, the final constraint states that in a sustainable society – 4. human needs are met worldwide.

Industrial Ecology and The Natural Step (TNS) In some regions of the world, interest in IE is closely linked to a program known as The Natural Step (TNS).27 The Natural Step is a philosophical framework for sustainability built largely around a set of constraints known as the "System Conditions" which must be met to achieve sustainability. TNS borrows concepts from industrial ecology (especially the concept of industrial metabolism, which concerns itself with the flow of materials and energy through the environment).6 IE and TNS have different goals but overlapping applications. The Natural Step is primarily a philosophical framework that applies selected scientific principles to support a set of guiding principles for SD. IE is a scientific framework for understanding the functioning of industrial systems (whether sustainable or not), which can be used to obtain guiding principles for sustainable industries. In practice, the two frameworks co-exist, with proponents of each framework generally recognizing value in the other system. Of the two frameworks, IE is the more powerful for evoking new insights into how industrial systems work (and consequently how they can be improved). However, many would agree that TNS is the more powerful statement of objectives for companies seeking to claim sustainability. As a worldwide movement, TNS is also useful in depicting a particular view of sustainability that is recognized among stakeholder groups. Practitioners of TNS include leading companies in a wide variety of sectors – Ikea, Volvo, Co-operative Bank, Norm Thompson Outfitters, Interface, and Electrolux.

Industrial Ecology and Zero Emissions Manufacturing Alongside IE and The Natural Step, there is one more basis for discussing sustainable manufacturing that has attracted considerable attention: Zero Emissions Manufacturing. While TNS and IE can be thought of as philosophical and scientific frameworks, respectively, Zero Emissions Manufacturing may be thought of as an engineering or design approach for translating these concepts into practical results.42 The most visible champion of this approach is the Zero Emissions Research Initiative.42

essence, industrial ecology involves designing industrial infrastructures as if they were a series of interlocking man-made ecosystems interfacing with the natural global ecosystem. Industrial ecology takes the pattern of the natural environment as a model for solving environmental problems, creating a new paradigm for the industrial system in the process. This … represents a decisive reorientation from conquering nature--which we have effectively already done--to cooperating with it. ”

— Hardin B.C. Tibbs from “Industrial Ecology: An Environmental Agenda for Industry”, Center of Excellence for Sustainable Development, 1992. http://www.sustainable.doe.gov/articles/indecol.shtml

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

6

2.3. Relevance of Industrial Ecology to the Cement Industry At the heart of the IE concept is the idea that businesses‡ can exchange materials or energy to mutual advantage (i.e., industrial symbiosis). The use of alternative fuels and raw materials (AFR) within the cement industry is an example of such an exchange. A frequently cited example is TXI's CemStarSM process, which utilizes slag from electric arc furnaces (EAF) used in steel making processed in a particular way to increase cement production and reduce emissions, at little additional cost (BCSD Gulf Coast, 1997). According to TXI, the process can increase cement production by as much as 15%. As described in a 1999 TXI press release,37 "EAF slag that once sold for $3 to $8 a ton now is converted into Portland cement that sells for an average of $70 a ton." The process has also been licensed to four cement companies and is being actively marketed in the United States and throughout the world.§ However, the relevance of IE to the cement industry extends beyond the use of AFR. IE also examines the application of ecosystems concepts to the design of so-called eco-industrial parks or estates. Some researchers have proposed using concepts from ecology to understand the system dynamics of industrial ecosystems in such parks.4 Other examples of how the industrial ecosystem metaphor offers potential benefits to the cement industry are cited below.

The Role of Cement Plants in Eco-Industria l Park Development. One of the more important applications of the IE concept has been its role in shaping the development of eco-industrial parks. The most common defining characteristic for determining what constitutes an eco-industrial park hinges upon on the co-location of industrial facilities that can exchange materials or energy to mutual advantage. Around the world, a small handful of industrial estates have emerged that appear to embody the eco-industrial park concept. Perhaps foremost among these is the Kalundborg industrial park in Denmark.15 The Kalundborg complex comprises a complex web of waste material and energy exchanges involving an electric power generating plant, an oil refinery, a pharmaceutical factory, a gypsum wallboard factory, a sulfuric acid manufacturer, cement producers, the municipality of Kalundborg, and agricultural and horticultural facilities (See Appendix A). Two characteristics of the Kalundborg example are worth stating here. One, the development of the interrelationships was not created through some overall master plan. The exchanges have evolved based on individual discussions between potential participants rather than a collaborative planning process. Two, some of the members of the complex, including the cement producer, are located outside the physical boundaries of the industrial park. Co-location is not an essential requirement of a well-functioning IE system.

‡ In this report references to businesses exchanging materials or fuels also includes flows from other organizations, such as municipalities or governmental agencies that may have or be able to use materials in these relationships. § The specific benefits of the process are dependent on the conditions at the local plant. In particular, managing the chromium content of the slag is necessary.

Expanding the IE Concept for Sustainable Development

“Industrial ecology is an evocative metaphor that has evolved into a new paradigm for environmental management. It locates human activity in a larger, environmental context and uses the natural world as a model for organizing industrial activities. To date the concepts of place and jurisdiction have been missing from industrial ecology, even though many important environmental decisions are made within local political boundaries. Planners are uniquely equipped to advance this field because they (a) study locally-open systems such as economies, and (b) link big-picture ideas to incremental decisions. In return, industrial ecology offers planners an integrative framework for describing, explaining, and solving environmental problems.”

— Clinton J. Andrews from “Putting industrial ecology into place: evolving roles for planners.” Journal of the American Planning Association, 65.4, 2000.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

7

Questions that IE hopes to answer are how the successes at Kalundborg can be replicated and whether industrial ecosystems can be designed, or are solely the result of an evolutionary process. A related question posed by the challenge of designing industrial ecosystems is whether or not all members of an industrial ecosystem are equal partners. In other words, can specific industries or industrial processes serve as an "anchor" for an industrial ecosystem? There are indications that certain types of processes or industries are well suited to becoming

"anchor" facilities around which other industries might congregate. For example, industries that provide a large amount of waste heat, or those that can serve as long-term sources or users of raw materials, appear to have the potential to serve as anchors. Cement plants show some potential for meeting these criteria in their use of alternative fuels and raw materials as well as in their ability to provide excess heat from kiln firing and recovered co-products of cement making. The excess heat could be used for other processes or to provide district heating for commercial or residential buildings.

Ecological Lessons about Adaptive Strategies for the Cement Industry Much of what is published about IE focuses on the flow of materials and energy throughout industrial systems. Such publications often depict these systems as relatively static, or unchanging with time. In real ecosystems, however, a great deal of attention is paid to understanding the dynamic aspects. As an example, such studies examine how individual species adapt over time to their environment, and how ecosystems themselves change over time. These studies also show how the living organisms themselves change the ecosystem.** Understanding these dynamic changes provides knowledge about how an ecosystem arrives at a particular state, and how it is likely to change in the future. Surprisingly, this aspect of IE gets relatively little attention even among the supporters of IE. However, using ecological analogies to understand dynamic behavior of industrial ecosystems potentially has much to offer.

** This phenomenon is known as ecological succession. It is used to describe transitions such as the progression of a forest from pioneer species to so-called "old growth" forest. Given a set of initial conditions, these successions follow a predictable sequence of stages, each reflecting a different plant and animal species composition.

Case Study: Another Successful Eco-Industrial Park

The Cajati Industrial Park in Brazil is another example of a successful Eco-Industrial Park concept. In this case the cement plant was sited to take advantage of a sub-product of another industry. Millions of tonnes of waste have been avoided during the operating period of the collaboration between the cement plant and the phosphate processing operation.

The cement plant intends to start burning alternative fuels in its kiln. The cement plant will seek to develop relations with an increasing number of industrial partners that will be able to supply it with industrial residues. The application for licensing has already been lodged and only the authorization of the environmental authority is awaited. The fact that the cement plant was born in the wake of a decision to make use of the sub-products of another industry to be used as a raw material allowed the licensing process to be simplified.

At present, the link between increased economic value, technological innovation and sustainable development is maintained through close co-operation between the two factories. A planned change in the MgO content of the dolomitic residue from the phosphate plant will allow the use of this type of residue in the manufacture of cement and provides advantages in that it will enable the production of bi-calcic phosphate for the manufacture of livestock feed. This new step will lead to a win-win-win situation, providing benefits for both companies and for the environment.

Source: Cimpor (See Appendix A)

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

8

Measuring the Benefi ts and Impacts of IE to Society One of the principles of IE relating to SD is that an opportunity to engage in a materials or fuels exchange should be analyzed with regard to its external social benefits and impacts. Cement companies need to adopt a methodology to perform these types of analyses. There are a number of candidate methods, although none have been accepted by an official international body. The detailed description and evaluation of methods is beyond the scope of this substudy, but briefly the candidates fall into two categories – those that account for external effects qualitatively or through surrogate (non-monetary) metrics and those that attempt to valorize or monetize these so-called externalities (total cost accounting or environmental accounting). Additional details on the general nature of these methods may be found in the LCA substudy and Business Case substudy reports. A specific example of use of such a methodology is described in the box below.

Case Study: An IE Example of Ecological Succession

An example of how the idea of ecological succession can be applied to cement facilities can be found by looking at the conversion of a defunct cement kiln in Stora Vika, Sweden into a large-scale composting facility.42 Taking advantage of the large capital infrastructure that was already present at the cement plant (including the kiln, docks, loading facilities, etc.), the designers of the composting facility converted the cement plant's kiln into a rotating aerobic composter, with a design capacity allowing the processing of up to 1000 metric tons per day of municipal waste. The composting facility demonstrates a number of other eco-industrial linkages, including the use of municipal wastewater to provide additional nutrients and water required for composting, and the use of carbon dioxide and heat generated by the composting operation in adjacent greenhouses.

The example above illustrates how the useful lifetime of a capital investment can be extended by redirecting its use after its original purpose is no longer served. In an industry like cement manufacture, where changes in development patterns and other factors can leave manufacturers with unused capacity, such concepts can help maximize return on capital investments.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

9

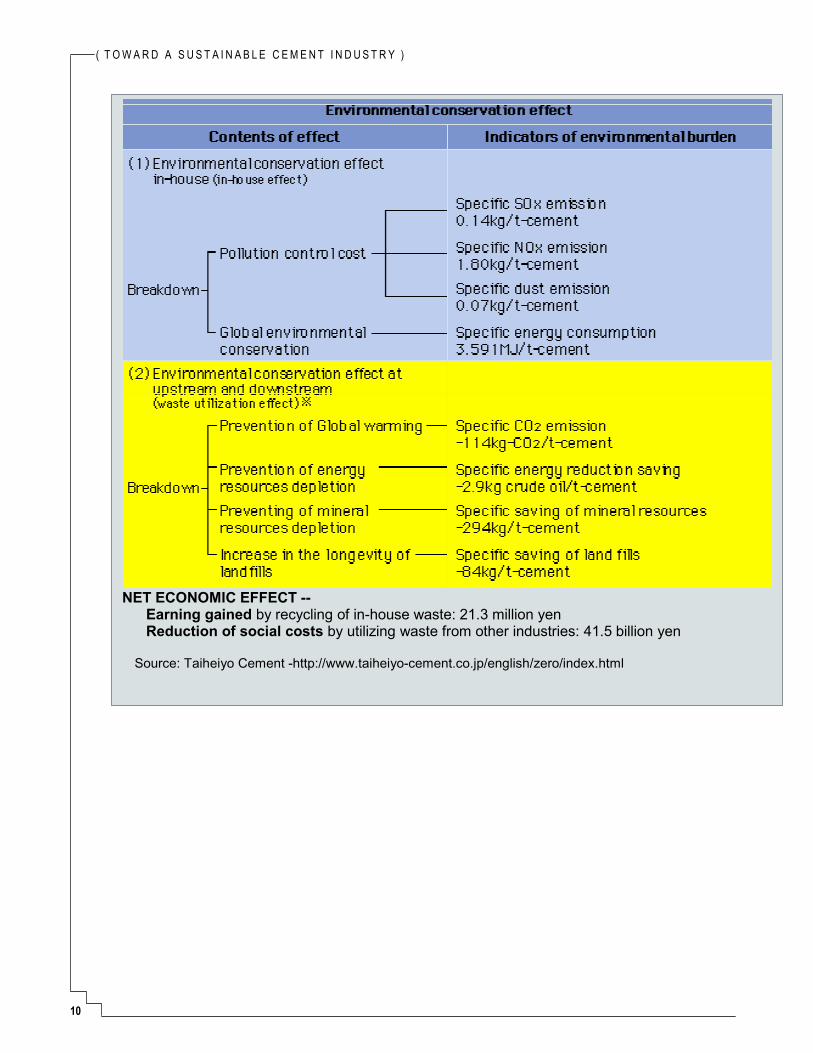

Case Study: Measuring Environmental Conservation Costs and Total Effect in Cement Production and Environmental Business

Since 1999, Taiheiyo has been studying disclosure of the costs and effects of the company's environmental conservation activities to the public as management information. The study includes participation in the ''Environmental Accounting Study Group for Administrators'' conducted by the Japanese Environment Agency. They calculated the environmental conservation costs as the reduction of social costs by using a Taiheiyo methodology that is in line with the Environment Agency Guidelines (2000 edition). The calculations summarized are from Taiheiyo's ten cement plants and groups the environmental conservation costs and effects of utilizing wastes from other industries as they influence the whole society. The external costs are included in the ''Upstream and Downstream Costs and Effects” (yellow sections). In 1999, Taiheiyo used 6.2 million tonnes of waste and by-products as AFR to produce about 24.3 million tonnes of cement. This is equivalent to about 41.5 billion yen when converted to economic value under an assumption that it is a reduction of the burden placed on society for environment and natural resources.

Note: data are a composite of ten plants.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

10

NET ECONOMIC EFFECT -- Earning gained by recycling of in-house waste: 21.3 million yen Reduction of social costs by utilizing waste from other industries: 41.5 billion yen

Source: Taiheiyo Cement -http://www.taiheiyo-cement.co.jp/english/zero/index.html

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

11

3. Industrial Ecology in the Cement Industry As the term is defined in this substudy, the cement industry’s exploration of IE began nearly 10 years ago. This history contains examples of both successes and failures based on a variety of drivers and barriers to implementation. In parallel with the industry trying to define and implement practices, governments and regulatory bodies have begun to set policies that have either facilitated or inhibited the industry from practicing IE. Experience has shown the need to consider a variety of issues, constraints, outcomes, and even the ability to maintain IE relationships. The following section provides a baseline assessment of the industry’s current practices in relation to the proposed definition of IE. The discussion includes a description of specific practices, the relationship of IE to long-term sustainability of the industry, and the long-term benefits and motivation for the industry to more widely adopt IE. The following definition of IE for the cement industry is offered as a practical target for realization of the previously discussed IE concepts:

3.1. Drivers, Barriers, and Current Status of IE Current cement industry initiatives or involvement in IE span a range of engagements and levels of integration with other organizations in an ecosystem. Following are selected examples of IE practices supported with interviews and other information collection to provide an overall picture of the state of implementation. Overall global statistics for the practice of IE within the cement industry are not available. Instead, specific issues, drivers and barriers are discussed as they affect the extent of implementation on a regional or national level. For instance, AFR (the use of alternative fuels and raw materials or co-processing as it is called in some places) may not meet the definition of a sustainable industrial ecosystem. Cement plants addressing only specific internal goals, such as net zero fuel cost, in their development of alternative sources of energy and materials are not working within the collaborative partnership that a true IE arrangement entails. Issues such as this are discussed below. The practice of IE has advanced the most when the following four drivers are collectively present: Financial Incentives: companies have a strong financial reason to investigate their cost

reductions through alternative fuels and raw materials (or extending clinker capacity to delay capital investment) Government Support: government policy, regulations and implementation that either

actively promote or do not discourage the practice Waste Management Infrastructure Deficiencies: the collection, transport, and disposal

systems for industrial waste are lacking or the disposal capacity in landfills or incinerators is limited Community Engagement: the inclusion of environmental and public health activist groups in

the planning and evaluation process for the fuel or raw material change is consistent with the company policy or governments have required or encouraged their involvement.

“Industrial Ecology is a business relationship among a set of partner organizations in which a cement company uses or provides materials and energy carriers that cannot be reused or recycled by the generating process and which otherwise would have no or little economic value as co-products. The cement company’s use or provision of these materials must correspond to the creation of system level net benefits (economic, social, and environmental) as well as benefits to the cement company.”

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

12

Barriers to IE implementation, apart from the absence of the above listed drivers, include: Perception of IE as Waste Disposal: the notion that IE is simply an alternative waste

disposal mechanism with little or no social benefits Environmental or Human Health Damage: evidence or perception that waste burning

causes or could cause environmental or health impacts in the local area Lack of Awareness of Market Opportunities: the inability to identify and capitalize on

sources of waste in the region that could be usefully processed Resistance to Products Manufactured From or Containing AFR: purchasers

determination not to specify or buy products that are made with AFR or which incorporate AFR residuals Business Operational Issues: adverse influences on product quality or output with use of

AFR Transparency with Information: sensitivity regarding sharing of process and product know-

how Availability of Analysis Tools: lack of tools for comprehensive and objective opportunity

identification. These barriers are discussed in the text in parallel with the drivers and highlighted in the text where appropriate. An additional characteristic may be needed as the industry adopts more sustainable practices: Sustainability Considerations:

decisions are based on both the net impact on the community and long-term viability of operations.

Financial Incentives Like most industries, the cement industry currently considers internal economic factors in decision-making related to IE. Cement plants are already using alternative fuels and raw materials to reduce the cost of their operations. However, economics may create a barrier to implementation, particularly when large capital costs are required to make plant modifications to use new materials or fuels. Even if the implementation investment has a short payback or return, the initial funding may not be available. In other cases, the alternative may require increased transportation, insurance, or permitting costs that make the initiative uneconomical for the cement company.

Case Study: Expanding and Educating Markets to Enhance IE Implementation

It is essential that IE opportunities address the environmental impact of cement production. But these benefits alone are insufficient to spur the industry to greater use of the concept. The challenge of producing and marketing slag cements that are competitive in price and quality and of educating customers about the new products are equally as important for success.

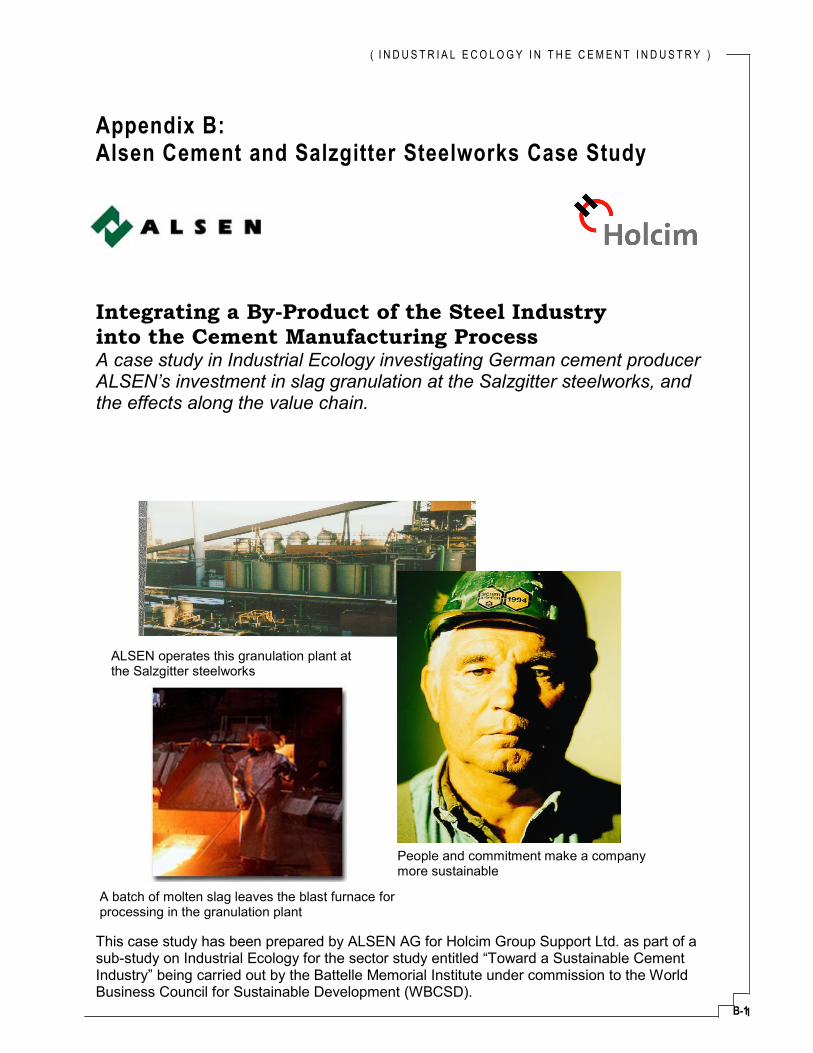

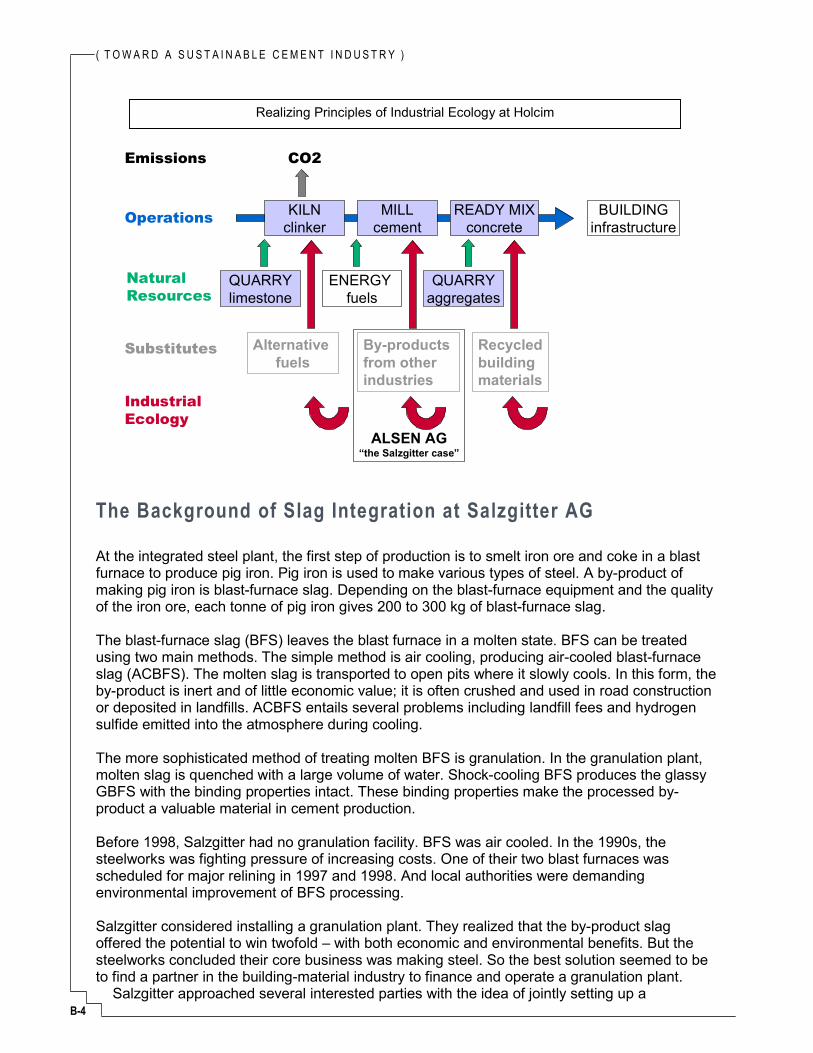

In 1996, ALSEN, a Holcim Group company, invested in a granulation plant at the Salzgitter steelworks. These two companies formally agreed to work together for at least 15 years. ALSEN is responsible for managing the entire granulation process and gets to use the blast-furnace slag. ALSEN developed new types of slag cements, nearly doubling their product range. During the shift away from ordinary Portland cement (OPC) and toward blended cements, ALSEN has been able to maintain its market share. But the sales force has experienced problems in selling slag cements. Cost-conscious customers in the building branch are not swayed by environmental arguments. This runs contrary to intuition in the environmentally conscious German market. ALSEN has developed new marketing strategies in response to these challenges.

Merely optimizing current clinker processes cannot achieve as great a contribution to environmental protection as integrating granulated blast-furnace slag can. Integration of granulated blast-furnace slag into cement manufacturing is a genuine opportunity to contribute significantly to sustainable development, but requires change along the entire value chain if the effort is to be successful.

Source: Alsen AG, 2000

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

13

Often, the greatest challenges arise when the barriers conflict equally with the incentives. This is particularly the case when an IE initiative may have economic drivers but is unsustainable when considering global environmental or local social concerns. The most significant example related to the cement industry is the use of waste as fuel. On the positive side, the use of waste as fuel provides a service to the industry generating the waste and to the community seeking to dispose of the materials. Many fuels are available at costs to the cement plant below that of conventional fuels, such as coal. On the negative side, combustion of hazardous materials is sometimes controversial with the community and employees due to their perception of risks, including increased toxic emissions, the possibility of accidental releases during transportation and handling, and increased worker exposure to chemicals. Easy availability of this treatment method (use in cement kilns) may discourage the source company from finding ways to minimize the generation of their waste through innovative source reduction techniques, in direct conflict with the waste management hierarchy. When a supplying company does begin to minimize its waste generation, interruptions may occur in the supply for the cement plant, making operations highly variable and possibly less efficient. Nevertheless, pollution prevention should in most cases be encouraged and supported, even if it adversely affects the formation or viability of an industrial ecosystem. Having multiple partners in the ecosystem provides additional flexibility and offsets the loss of one provider. Oftentimes, the facility simply does not know who in their region could be a viable partner (P. Ronsin and M. Picard, Personal Communication, 2001)††. Figure 3-1 illustrates the range of relationships that can be established to offer the company or plant manager further opportunity for identifying multiple markets. Another area of concern is the process of finding and interacting with IE partners. Once a cement plant decides to investigate potential IE projects, they need to have a process to connect with other industries that may be a source of raw materials or fuels for the cement process or industries that may have a use for cement plant-generated wastes or excess energy. Cement plants have several places to go for assistance—internal corporate headquarters, local community non-profits, and external for-profit brokers—each with their benefits and limitations. First, if the company has diverse operations, they can work through internal corporate environmental operations in order to connect with sister plants, such as a steel plant with the same parent company that has excess slag waste. Working within the same parent firm can create double savings and gives both plants a stronger commitment to succeed. The challenge is when the plants may not be located close enough to keep transportation costs economical. The second option is to meet and work with neighboring industries through local waste minimization non-profits or business organizations. This alternative option provides maximum flexibility in choosing whom to work with and keeps transportation costs to a minimum, but requires an active local business community or a dedicated non-profit acting as a facilitator. Finally, a cement plant can work with a for-profit waste broker, a company that specializes in handling industrial wastes. Some brokers provide the service of exchanging materials between compatible facilities for a fee based on the buying and selling prices. Using a broker can reduce the amount of time cement plant personnel have to spend seeking a compatible partner, can help ensure a steady supply of fuel and materials from multiple sources, and can simplify contracting to a single source. However, care must be taken to choose a reputable broker, especially when dealing with hazardous wastes, to ensure the legality of the transport, accurate labeling, analysis, and composition of incoming materials.

†† Italcementi and Lafarge representatives, respectively. Interview conducted by the substudy manager, January 2001.

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

14

In some countries the economic forces are not yet sufficiently strong to promote alternative practices. For instance, China relies on coal almost exclusively to produce its cement. Unlike some industrialized countries, China has not yet moved to burning waste and other alternative energy sources in its cement kilns, although that may become an option if coal prices continue to rise. Chinese coal prices were freed in the early 1990s and, outside of the main producing areas, are now relatively high.43 Additionally, IE often requires revealing the raw materials and fuels used in the process to the public, regulators, and the industries sharing materials and fuels. This transparency can be barrier when the process and its components are considered proprietary. Revealing them, even in a limited fashion, can be considered a risk to profitability and is yet another economic consideration.

Success with Scrap Tires

One area of success within the cement industry is in the use of scrap tires. At present in the U.S., scrap tires are classified as fuels, not as wastes. In 1998, some 38 million tires were used in cement kilns, about 15% of the 270 million new scrap tires generated that year.31 On average, kilns can replace 1.25 kg of coal for every kg of tire-derived fuel fed.30 The Scrap Tire Management Council has develop a guidance document for plant managers and operators that details information on a wide variety of operational issues relating to tires including tire characteristics as fuel, effects on cement quality, permits, and internal considerations associated with communications, customer relations, employee safety, and public relations.30 Because this guide is not produced by the cement industry and because the Council has no vested interest in promoting use in kilns above other uses, such guidance is especially powerful in enhancing the practice. This type of guidance document could be an example for other sources of AFR. From an IE perspective the expanding market for scrap tires is encouraging in that the overall beneficial use of these materials is increasing and not exclusively in the direction of combusting them for energy.

A similar type of document has been produced by the U.K. environmental agency.12 The European Commission's Landfill Directive will ban the disposal of whole tires to landfill by about 2003, and shredded tires by 2006. Some 450,000 tonnes of waste tires are generated each year in the United Kingdom. Accordingly, more reuse, material recycling and energy recovery options are needed. To this end, the use of tires as a fuel in cement kilns is an important outlet for waste tires in the U.K. The document notes that burning tires in cement kilns often has a net environmental benefit when compared to conventional fuels, which are usually coal and petroleum coke. For example, the emissions of nitrogen oxides and sulfur oxides (major pollutants) have been shown to be lower when burning tires with coal compared with coal alone.30 Also, because tires contain steel, using them as a fuel reduces the amount of iron oxide that must be added to the cement making process.

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

15

Oth

er E

xcha

ngea

ble

Mat

eria

ls

alum

inum

hyd

roxi

de

slud

ge

CaF

2 slu

dge

deca

rbon

atio

n sl

udge

iro

n ox

ide

mar

ble

dust

and

scr

aps

pelle

tized

fluo

rite

pyrit

e as

h re

ctifi

catio

n sl

udge

us

ed c

atal

ysts

Mun

icip

al w

aste

fa

cilit

y H

azar

dous

was

te

faci

lity

Iron

and

stee

l Bl

ast f

urna

ce a

nd s

teel

sl

a gs

Scra

p tir

es, w

aste

wat

er

slud

ges,

MSW

inci

nera

tor a

sh

Was

te

solv

ents

Fly

ash

and

FG

D (g

ypsu

m)

Mun

icip

al

heat

ing

Was

te h

eat

Seco

ndar

y sm

elte

r

Nic

kel,

zinc

, co

pper

, lea

d,

Sust

aina

ble

Cem

ent

Faci

lity

Elec

tric

pow

er

plan

t

Non

-ferro

us

met

als

foun

dry

Silic

a fu

me,

gyp

sum

, spe

nt

pot l

iner

, sla

g (a

lum

inum

)

Roa

d co

nstru

ctio

nKi

ln d

ust

Slau

ghte

rhou

se a

nd

mea

t pro

cess

ing

Elec

tric

pow

er

plan

t

Auto

scr

ap

repr

oces

sing

Shre

dder

re

sidu

e

Mea

l, bo

ne

and

fat

Tire

dea

ler o

r m

anuf

actu

rer

Auto

man

ufac

turin

g

Foun

dry

sand

, w

aste

pai

nt

Pulp

and

pap

er

Pape

r slu

dge,

cla

y

Scra

p tir

es

Food

pro

cess

ing

and

beer

bre

win

g

Beer

slu

dge,

w

aste

filte

ring

m

ater

ial,

rice

hulls

Figu

re 3

-1 P

oten

tial M

ater

ial a

nd E

nerg

y Fl

ows

in a

Cem

ent P

lant

-Cen

tric

IE S

yste

m

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

16

Government Support Governments can either be a positive or negative force. As a positive driver they can promote the responsible use of wastes, if they have clear policies and regulations spelling out what cement companies need to do. They can constitute a barrier if their policies are unclear to the point of needing too much time or effort to comply with or if they actively discourage the practice. Regulatory issues typically become important when the alternative fuels or materials are hazardous‡‡ or have increased regulatory requirements associated with their handling or storage. Other regulatory concerns may be the re-permitting required for major process modification or changes to transportation routes. On the other hand, lower emissions as a result of an IE practice can also reduce regulatory requirements and inspections. A related area of governmental intervention is in the setting of cement standards, particularly if these standards are specific as to the allowable composition of the product. In general, an active level of engagement with governmental bodies is desirable to help set viable policies and to resolve issues with individual opportunities to implement a project (see the Policy substudy report for some specific approaches on this topic). A couple of regional examples are provided below to illustrate these principles. In Thailand, the government restricts the greater use of waste materials. Thai cement companies have begun to use waste solvents, paints, and similar energy containing wastes. However, the collection and transporting of waste is controlled by the government and cement companies cannot get as much of these materials as they actually could use. Siam Cement has established strong goals for use of alternative fuels: have a zero net fuel cost, have an overall cost reduction in producing a tonne of clinker, and improve the image of the industry through diversion and appropriate disposition of waste from

other industries.

‡‡ The term “hazardous” is used in this report to refer to materials having toxic, explosive, carcinogenic, or teratogenic properties that could cause harm to humans or other species. It does not refer to specific definitions such as the RCRA hazardous waste definition in the U.S. or the Basel Convention internationally.

Case Study: Finding Partners and Working Together

In the Rhine-Neckar industrial region of Germany, the Institute for Eco-Industrial Analysis (IUWA) facilitated the creation of the Heidelberg-Pfaffengrund Eco-Industrial Estate, designed to “explore and to exploit the economical and ecological potentials of waste-based cooperation between small to medium scale enterprises.” The participating companies were expected to contribute financially to the project as well as provide “full transparency of quantities, qualities, and costs of all kinds of waste.”

The project started with a detailed waste analysis of the 14 businesses involved, coordinated by IUWA. This led to proposals and implementation of economical and ecological closed-loop improvements that paid off investments within two years. Key aspects for success were: physical proximity of the facilities face to face contacts facilitated by IUWA dedication to transparency of waste and

material input and output information by the participants

IUWA was able to apply for grants to fund the coordination, development, and expansion of the estate. The pilot project has proven to be successful and has led to implementation on a regional level.

Source: Sterr, 2000

( I N D U S T R I A L E C O L O G Y I N T H E C E M E N T I N D U S T R Y )

17

Also, promoting the establishment of other waste management companies will in the long run lead to more competition and the increased supply of fuels (C. Dumrongsak, Personal Communication§§). The cement companies are working with the government to alleviate the processing bottleneck. External stakeholders are supporting this effort with appropriate controls and training of operators on handling and using these materials. As another example, Siam City Cement has been helping with skill training to individuals who could manage waste projects. An independent waste exchange to identify and establish IE relationships and the adoption of a national Thai standard for cement produced with alternative fuels or raw materials were proposed to increase the amount of AFR from the current 5-10% up to the 25-30% that many plants could operate with.35 The practice of IE in Brazil is still relatively underdeveloped, especially the use of alternative fuels. Progress has been made in recent years to increase the use of blended, pozzolanic, and slag cements. These now account for more than 90% of production.1 One of the primary barriers to increased practice of IE is keeping the environmental regulatory authority up to date with rapidly changing technology and emerging business practices. It is a question of demonstrating to the environmental agency that co-processing of fuels is a benefit. The industry recognizes that not enough is being done to make its case to the regulatory community. Agencies are out-dated and need motivation to be creative. Also, the regulation of industry needs to change from command and control to more collaborative approaches. (See the Public Policy substudy report for additional analysis of the impacts of alternative policy instruments.) Increased communication and information sharing with regulators is critical. In India, recent governmental requirements require the electric power utilities to develop a plan to dispose of the fly ash generated from burning coal. India's coal generally contains a high ash content of between 24-50%. However, this coal is relatively low in sulfur (0.5%) and chlorine content making the ash acceptable for use in cement manufacture. Due to the high ash content of India's coal, environmental measures are being taken by many of India's states and the cement industry is a potentially attractive 'sink'. The rule mandates establishment of a formal relationship between the cement industry and electric power plants to engage in exchange of alternative raw materials. By formalizing the need to have such capability and legal agreement, the government hopes to increase the supply of cement through blending as well as to effectively use materials that otherwise would have to be landfilled, dumped, or turned to a very low value application such as fill.*** Waste Management Infrastructure Deficiencies The establishment of an IE system provides another route for the management and beneficial use of materials that otherwise would require handling for ultimate disposal. In countries or regions that do not have well established waste management systems, the need to properly handle and dispose of such materials can serve to promote IE. Shortages in landfill space, too low a capacity in industrial incineration facilities, or bottlenecks in collection and transport can all provide a driver for a successful IE program. As long as the cement industry is not in conflict with the waste management infrastructure, such programs can be beneficial for the socially responsible management of unwanted materials (see the EHS substudy for additional discussion on this point.) This is not to say that IE should only be

§§ Siam Cement representative. Interview conducted by the substudy manager, January 2001. *** http://envfor.nic.in/legis/others/flyash.html, 1999; http://www.eia.doe.gov/emeu/cabs/india /indiach3.htm#COAL2, 1997

( T O W A R D A S U S T A I N A B L E C E M E N T I N D U S T R Y )

18