Embed Size (px)

Citation preview

Photo by Karl Steinbrenner

Reconciliations for a Successful Year End

June 2, 2015

Objective

Achieving successful fiscal year-end and calendar year-end reporting is done through regular reconciliation beginning on the pay-period level.

Overview

We will cover how to reconcile gross pay, taxable wages and taxes for:• Every pay period• Every month• Every quarter

Special Notes• Uncollected FICA• Prior Year Workers’ Compensation

Checks

Gross Pay, Taxable Wage & Tax Reconciliations: Every Pay Period

Every Pay Period

Reports– Report U118– Post-Certification Report 10 Compare (PAT)– Report 33 (PAT)

Every Pay Period

Report U118– Research all differences and report to SPO.– Due by closed of business on day after

certification.– Audit point for not responding.

Every Pay Period

Post-Certification Report 10 Comparison (PAT)– Helpful for researching U118 differences.– Print and keep with Certification.– Only available for 60 days.

Every Pay Period

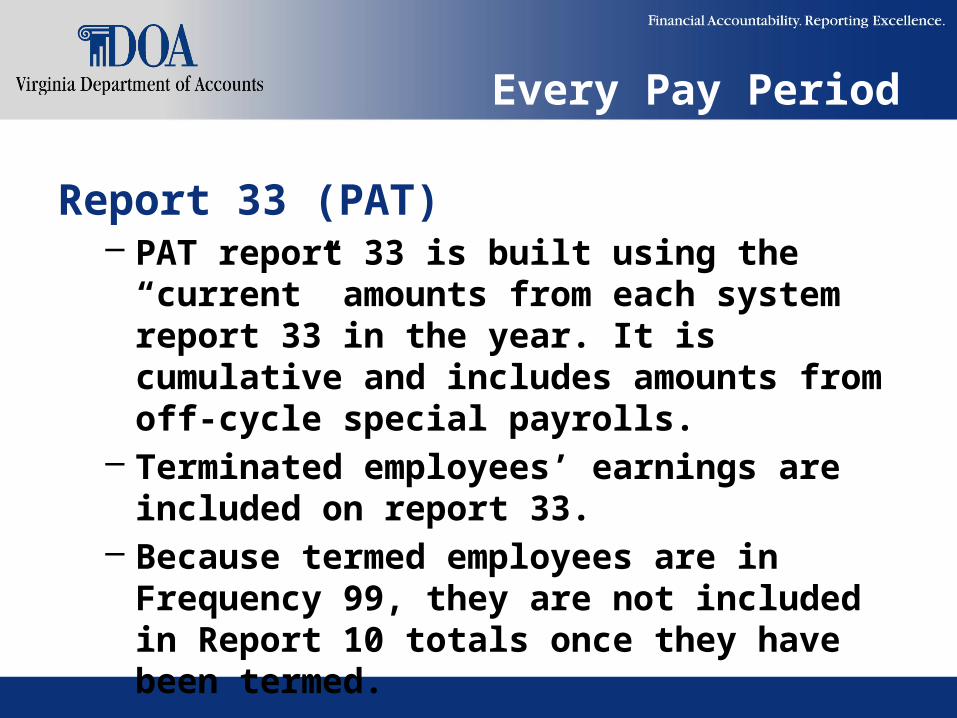

Report 33 (PAT)– PAT report 33 is built using the “current” amounts

from each system report 33 in the year. It is cumulative and includes amounts from off-cycle special payrolls.

– Terminated employees’ earnings are included on report 33.

– Because termed employees are in Frequency 99, they are not included in Report 10 totals once they have been termed.

Every Pay Period

What to check– SIT Taxable does not equal FIT Taxable

• Only valid exception, if you have non-VA SIT or dual taxation

– Employee HI Tax/Taxable does not equal Company HI Tax/Taxable

– Employee OASDI Tax/Taxable does not equal Company OASDI Tax/Taxable

Every Pay Period

How to correct– Manual pay set

• Preferred method• Regular Pay and Special Pay YTD amount

adjustments• Deduction YTD amount adjustments

Every Pay Period

How to correct, continued– Employee Masterfile Adjustment Form

• If manual payset doesn’t work– YTD Imp Life on H0BTT does not equal YTD Imp Life on

H10SA

• Submit Employee Masterfile Adjustment Form to State Payroll Operations.

• Do NOT wait until the end of the month or quarter.

Every Pay Period

How to correct, continued– Employee Masterfile Adjustment Form,

continued• How to complete: provide the amount that the field

should be; not the amount of the increase/decrease.• “Quarterly Reconciliation Forms” section of Payroll

Operations Forms page at http://www.doa.virginia.gov/Payroll/Forms/Payroll_Forms_Main.cfm

Every Pay Period

When should I reconcile?– The first business day after certification.

Gross Pay, Taxable Wage & Tax Reconciliations: Every Month

Every Month

Reports:– Report 33 (PAT)

• “As of composite date” = 24th of the month

– Report U092/U093

Every Month

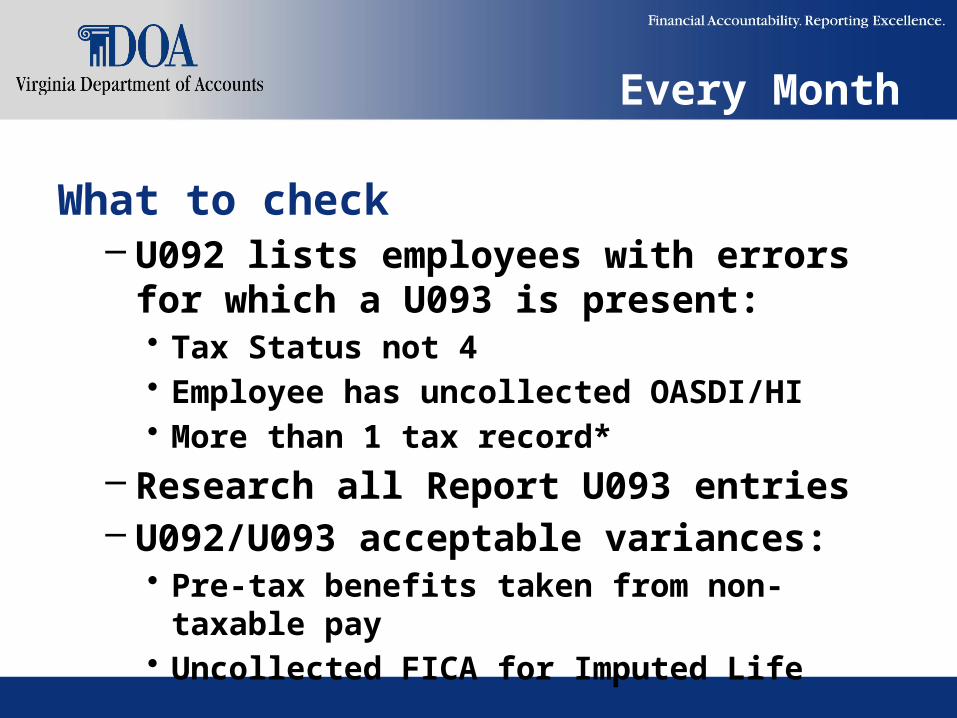

What to check– U092 lists employees with errors for which a

U093 is present:• Tax Status not 4• Employee has uncollected OASDI/HI• More than 1 tax record*

– Research all Report U093 entries– U092/U093 acceptable variances:

• Pre-tax benefits taken from non-taxable pay• Uncollected FICA for Imputed Life

Every Month

What to check, continued– Compare Report 33 YTD amounts with U092

YTD amounts

Every Month

How to correct– Manual pay set to correct

• Regular Pay and Special Pay YTD amount adjustments

• Deduction YTD amount adjustments

Every Month

How to correct, continued– Employee Masterfile Adjustment Form

• YTD Imp Life on H0BTT does not equal YTD Imp Life on H10SA (U092 will show this)

• Do NOT submit to clear Uncollected FICA caused by Imputed Life.

• Submit Employee Masterfile Adjustment Form to State Payroll Operations.

• Do NOT wait until the end of the quarter.

Every Month

When should I reconcile?– The first business day of the following month.– Report U092 and Report U093 are created

overnight the last business day of month being reported.

Gross Pay, Taxable Wage & Tax Reconciliations: Every Quarter

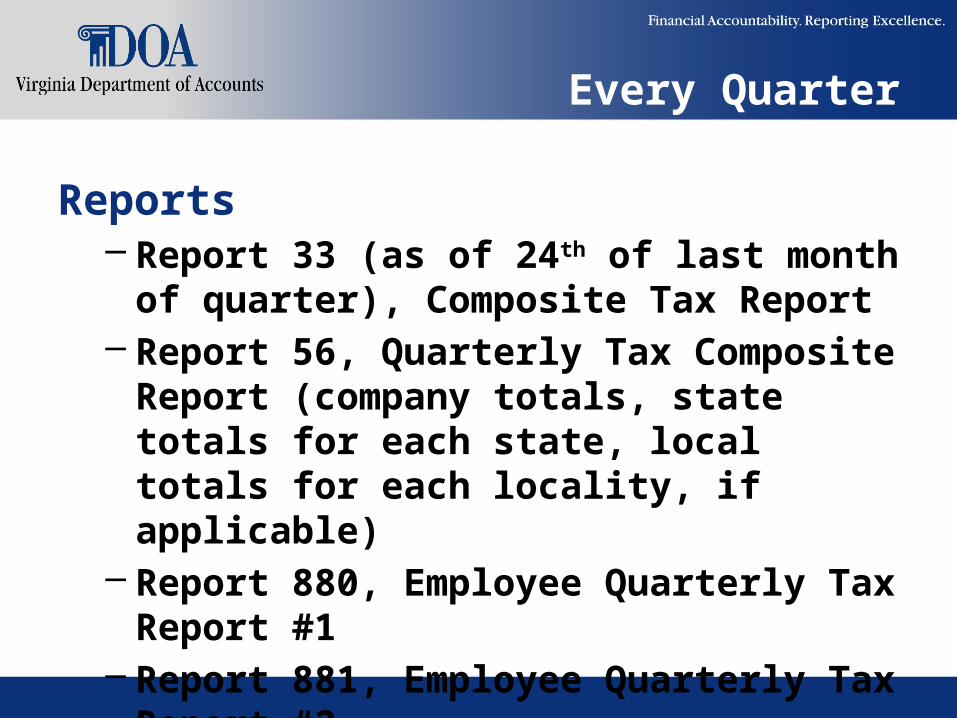

Every Quarter

Reports– Report 33 (as of 24th of last month of quarter),

Composite Tax Report– Report 56, Quarterly Tax Composite Report

(company totals, state totals for each state, local totals for each locality, if applicable)

– Report 880, Employee Quarterly Tax Report #1– Report 881, Employee Quarterly Tax Report #2

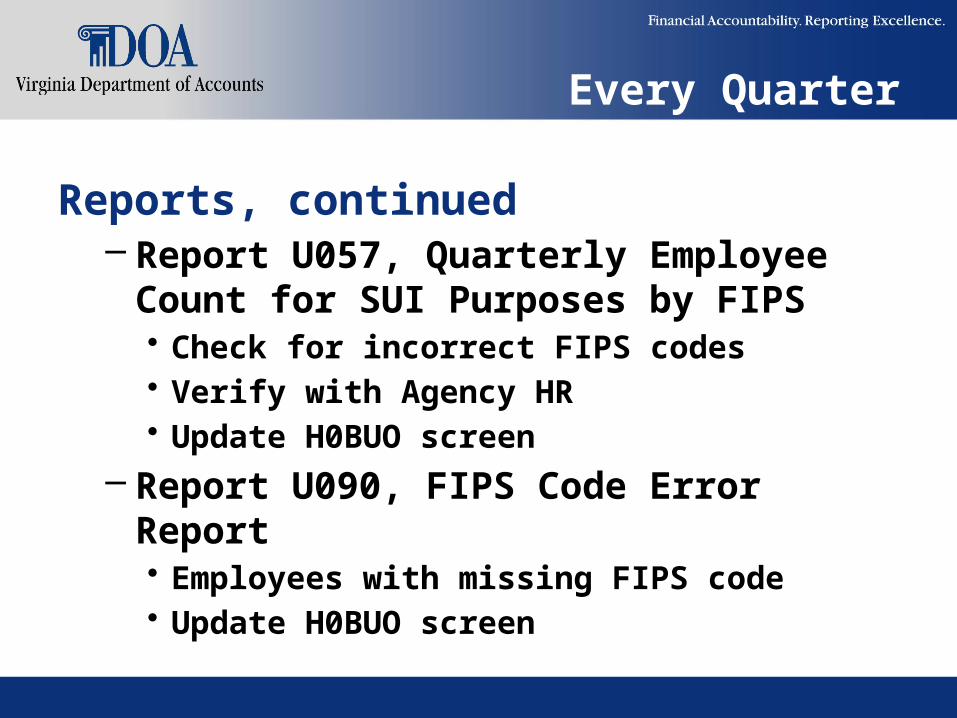

Every Quarter

Reports, continued– Report U057, Quarterly Employee Count for

SUI Purposes by FIPS• Check for incorrect FIPS codes• Verify with Agency HR• Update H0BUO screen

– Report U090, FIPS Code Error Report• Employees with missing FIPS code• Update H0BUO screen

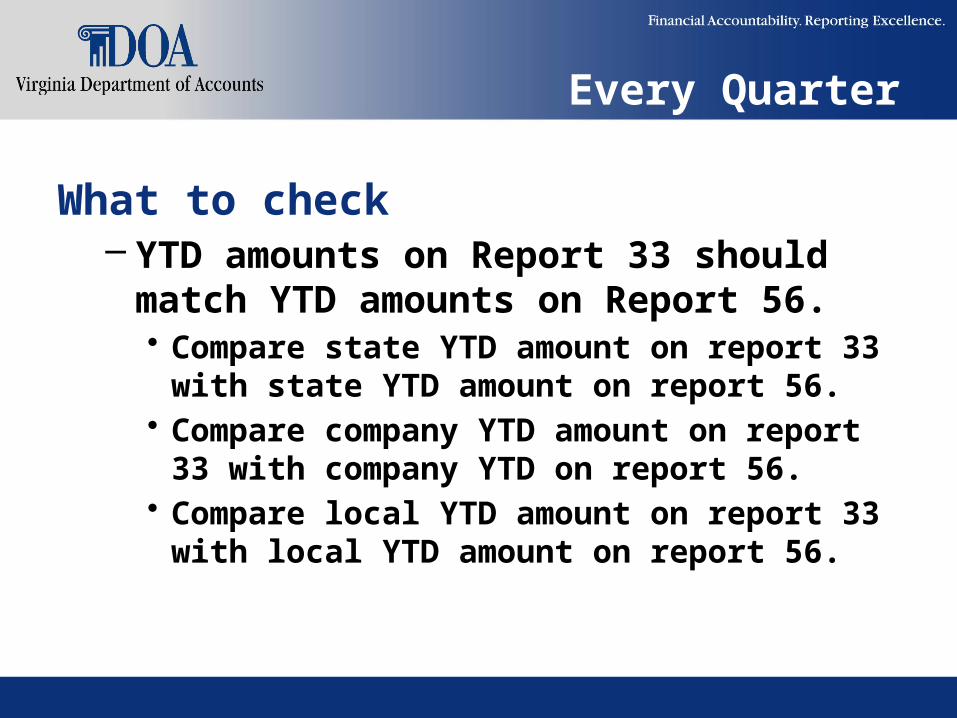

Every Quarter

What to check– YTD amounts on Report 33 should match YTD

amounts on Report 56.• Compare state YTD amount on report 33 with state

YTD amount on report 56.• Compare company YTD amount on report 33 with

company YTD on report 56.• Compare local YTD amount on report 33 with local

YTD amount on report 56.

Every Quarter

What to check, continued– Company YTD amounts on Report 56 should

match the Company YTD amounts on Report 880.

– Company YTD uncollected FICA on Report U092 should match Company YTD uncollected FICA on Report 881

Every Quarter

How to correct– Manual pay set to correct– Employee Masterfile Adjustment Form

When should I reconcile?– Second business day of month following end of

the quarter.– Quarter-end report are created overnight of

first business day of the first month of the next quarter.

Special Notes

Special Notes

Uncollected FICA (OASDI/HI) Taxes:– Imputed Life is taxable portion of the

employee’s Group Term Life Insurance benefit– In certain cases, this benefit continues despite

employee not being paid:• Military Leave without Pay• Severance/Worker Transition Act (WTA)

Special Notes

Uncollected FICA (OASDI/HI) Taxes, continued– NEVER clear uncollected FICA caused by

Imputed Life.– Doing so provides a benefit to those employees

not extended to others.

Special Notes

Workers’ Compensation– Adjust/reclassify earnings in the pay

period/calendar year of the coverage dates on the WC check.

– Checks for wages lost in a prior calendar year require issuing Form(s) W-2C for the tax year(s) affected.

– Refund OASDI/HI taxes outside of the payroll system.

Special Notes

Workers’ Compensation, continued– Workers’ Compensation checks received for

pay periods when the employee was not paid in full through VSDP and/or leave coverage:• Employee MUST BE PAID within 14 days of agency

receiving the check.• Penalty: 20% of 18-months compensation.

Special Notes

Workers’ Compensation, continued– Traditional (non-VSDP) sick plan:

• Workers’ Compensation replaces 2/3 (66 2/3%) of average weekly wage.

• First 92 days, the agency supplements 1/3 (33 1/3%) of average weekly wage.

• Special Pay 063, WC SUPP, is used for the agency supplement during the 92 days.

• Note: special pay 063 is not applicable for VSDP Workers’ Compensation claims.

Contact Us

Email: [email protected]

Director, State Payroll Operations– Voice: (804) 225-2245 or (804) 371-7800

Payroll Support Analyst/Trainer– Voice: (804) 786-1083