Embed Size (px)

Citation preview

Policy Synthesis & Strategy Development Framework

Long-Term Care Financing Advisory Committee Meeting July 23, 2009

Agenda

Looking to the Future: A brief review of the Minnesota report

Looking at the Past: Synthesizing findings from public and private financing discussions so far

Thinking about Strategies for moving forward Population-based profiles of existing and

potential coverage What is needed to support further discussion?

Committee Business

Summary of Minnesota Long-term Care Financing Study

MN Background and Process Legislated study of LTC financing options for baby boom

generation

Goal: Identify a broad array of public and private financing options

Extensive external input Series of 7 half-day policy briefings

Videoconference format with 12 viewing locations across the state 250 attendees and over 30 national and local experts provided briefings

Statewide conference Attendees voted on the most appealing options and most effective

strategies

Extensive support State inter-agency workgroup Contracted analytic and other assistance

4

MN Recommendations: Three-part strategy

Restructure public + private responsibility for LTS Affirm personal responsibility; diminish voluntary

impoverishment; incentivize individual purchasing Increase support to caregivers, prevent disability; increase “age-

friendly” communities

Expand LTS planning

Support multiple financing options (in order of preference) Partnership for Long-Term Care Life insurance used to pay for long-term care Long-term care insurance Public long-term care savings plan Health insurance that includes LTC benefits Reverse Mortgages Nursing facility benefits in Medigap policies A loan program for families Long-term care annuities (not ranked)

5

MN: Strengths and Weaknesses of Report Strengths

Broad upfront public input and buy-in Two-year timeframe Substantive analyses

quantitative fiscal evaluation and pros/cons of each option including information about eligibility, payer, administration, covered services, limitations, portability, interaction with public plans, market potential & characteristics of current users

Three-part strategy considers need to address values, change incentives, diversify mechanisms, and engage people in personal planning

Weaknesses Does not take a lifespan approach

Focuses on elders only; assumes many have the ability to plan for future care

Does not consider acuity and chronicity Does not determine expected “relative weight/role” of private

responsibility Does not discuss needs, preferences, access and availability of services Is not specific re: “most effective tools” to increase use of options 6

Policy Synthesis

Key Points: Public Financing discussions

Medicaid is the primary and most comprehensive payer for LTS

Nonetheless: Access to comprehensive community-based LTS (e.g., HCBS

waivers) is restricted by age or type of disability, acuity, and income/assets

Seniors have disparate financial access to community-based State plan LTS compared to younger people with disabilities

Many current Medicaid eligibility and coverage rules drive utilization to nursing facilities and impede Community First goals

8

Key Points: Public Financing discussions (2)

Care systems for dual eligibles are uncoordinated and result in cost-shifting between Medicaid and Medicare

Over half of individuals needing LTS are not financially eligible for public programs

Medicaid is a powerful tool forinnovations in financing LTS

9

Key Points: Private Financing discussions

Private financing is a public policy concern Counterbalances public spending Government has a role in consumer protection, consumer

education, and orchestrating incentives

Demographic changes may impact continued availability of spouse and child caregivers (a critical resource)

For many middle-income individuals, capacity to finance LTS needs out of income/wealth is not sufficient Most seniors are not poor, but cannot afford extensive use of LTS Middle-income do not have sufficient “discretionary” wealth to

use for LTS (most is in home equity)

10

Key Points: Private Financing discussions (2)

Existing financial tools are under-publicized, under-utilized and under-regulated

LTC insurance products and market need improvement

Premium affordability, rate stabilization, covered benefits, security of benefit over time, market structure, other consumer protection

NAIC model act and regulation not implemented in MA (special LTC insurance regulations)

11

Key Points: Private Financing discussions (3)

Opportunity for integrating public and private financing exists in the LTC Partnership program

MA has “quasi-Partnership”, but NAIC model required for full Partnership program

Recent national activity around new contribution program to prepare for LTS needs for subsets of population

There is opportunity forbetter financial planning for LTS needs

12

Constructing a Strategy Development Framework

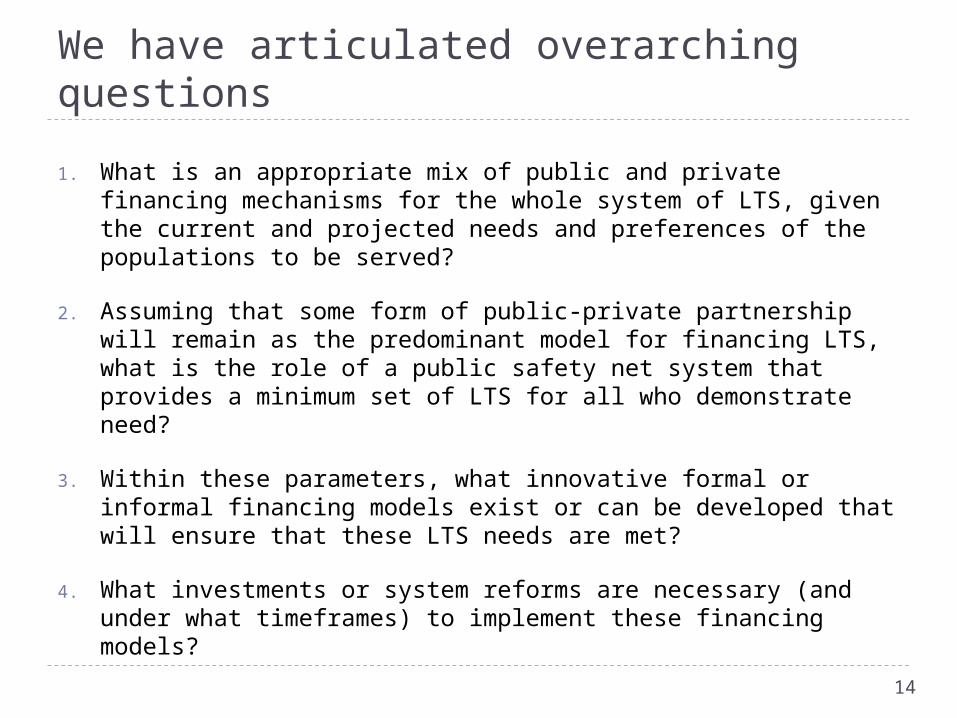

We have articulated overarching questions

1. What is an appropriate mix of public and private financing mechanisms for the whole system of LTS, given the current and projected needs and preferences of the populations to be served?

2. Assuming that some form of public-private partnership will remain as the predominant model for financing LTS, what is the role of a public safety net system that provides a minimum set of LTS for all who demonstrate need?

3. Within these parameters, what innovative formal or informal financing models exist or can be developed that will ensure that these LTS needs are met?

4. What investments or system reforms are necessary (and under what timeframes) to implement these financing models?

14

We have identified preliminary goals and high level strategies

Advisory Committee goals: Make changes in LTS financing that enhance choice and

availability, affordability, and sustainability of LTS Move from existing LTS financing system (with gaps/limitations) to

one that: Provides people with disabilities across the lifespan and with different

financial resources meaningful and affordable LTS financing alternatives

Strategies discussed to date to achieve these goals:1. Fill in gaps in public programs2. Increase private financing

Rationalize the market for LTC insurance and other private financing mechanisms so that more people participate and purchase appropriate products

Create new mechanisms to encourage contributions earlier in life3. Provide appropriate supports for unpaid informal caregivers4. Increase public awareness about need for LTS and financing

options

15

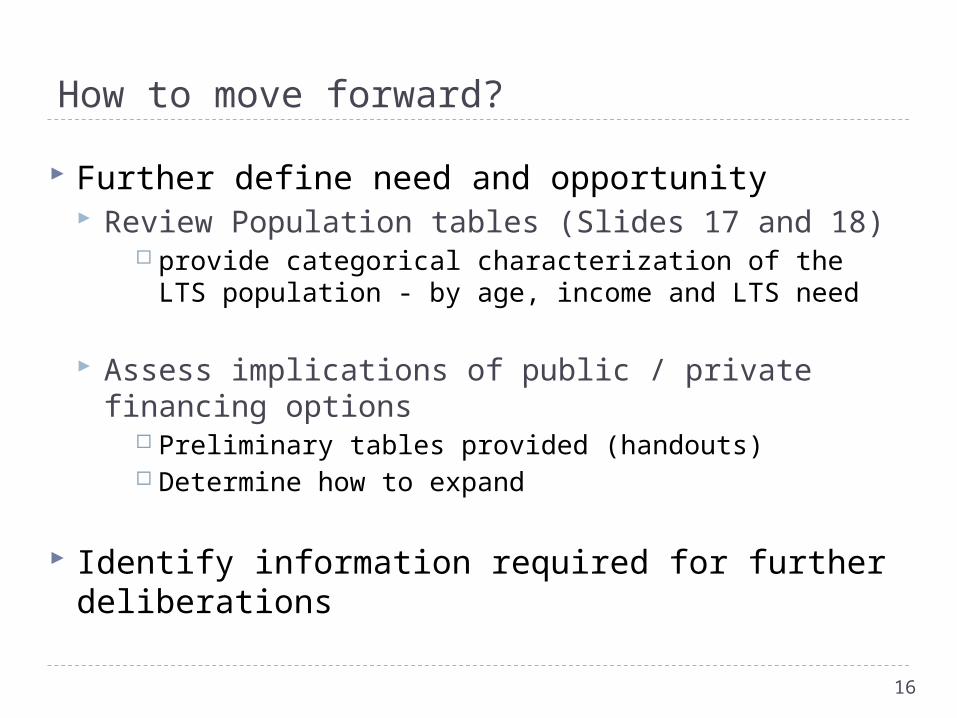

How to move forward?

Further define need and opportunity Review Population tables (Slides 17 and 18)

provide categorical characterization of the LTS population - by age, income and LTS need

Assess implications of public / private financing options

Preliminary tables provided (handouts) Determine how to expand

Identify information required for further deliberations

16

Low-income (0-199% FPL)

“Need Public Assistance”Total = 258,823 (46%)

Middle-income (200-499% FPL)

“Medicaid-bound”/“Tweeners”Total = 204,341 (36%)

Higher-income Highest (500%+ FPL) “Private Savings”

Total = 99,221 (18%)

Kids (5-18)

Adults (19-64)

Seniors (65+)

N = 9,941 (2% of total LTS)

MassHealth Standard, Autism Waiver

CommonHealth

Other state programs

Unpaid informal caregivers

New Public program ?

N = 144,718 (26%)

MassHealth Standard, MR or TBI Waiver

CommonHealth

Other state programs

Unpaid informal Caregivers

New Public program ?

N = 104,164 (19%)

MassHealth Standard, Frail Elder Waiver

Other state programs

Unpaid informal caregivers

New Public program ?

N = 7,709 (1%)

CommonHealth

Other state programs

Unpaid informal caregivers

Personal/family resources

New Contribution program ?

N = 97,437 (17%)

CommonHealth

Other state programs

Unpaid informal caregivers

Personal/family resources

LTC insurance

New Contribution program ?

N = 99,195 (18%)

MassHealth Standard via spend-down

Other state programs

Unpaid informal caregivers

Personal/family resources

LTC insurance

New Contribution program ?

New Public Program(CommonHealth-like) ?

N = 3,366 (1%)

CommonHealth

Other state programs

Unpaid informal caregivers

Personal/family resources

New Contribution program ?

N = 52,884 (9%)

CommonHealth

Other state programs

Unpaid informal caregivers

Personal/family resources

LTC insurance

New Contribution program ?

N = 42,971 (8%)

Other state programs

Unpaid informal caregivers

Personal/family resources

LTC insurance

New Contribution program ?

New Public program(CommonHealth-like ) ?

*Does not include persons who were institutionalized , in military group quarters or college dormitories, or unrelated individuals < age 15. Source: 2007 American Community Survey (ACS), US Census Bureau, tabulations by authors

MA LTS Population

Total = 562,385*

17

Legend

Existing Public (may

need improvement

s)

Existing Private (may

need improvement

s)

New Program?

People with LTS Disabilities who need assistance with Self-Care or Every Day Tasks

*Does not include persons who were: institutionalized, in military group quarters or college dormitories, or unrelated individuals < age 15. Source: 2007 American Community Survey (ACS), US Census Bureau, tabulations by authors. 18

Discussion

Committee Business

Public input process and timeframe Single centrally-located session (with breakouts) v. 3

geographically located sessions (with breakouts); October?

Additional Advisory Committee meeting When? Content?

Will send monthly e-mail (with meeting reminder) with new articles of interest sent by Committee members

November meeting moved to Thursday, November 12th

Next meeting: Thursday, September 10th , 9:00 -11:30am

Location: Ashburton Café (basement level), One Ashburton Place

Business items

21

Addendum

Hypothetical Scenarios

Hypothetical Scenario 1 – Michael(Age 19-65, low- to middle-income)

Michael is a 61 year-old divorced father of two. In 1985, Michael survived a car accident which left him paralyzed on his left side. After spending months in the hospital and rehab, he returned to work part-time. He owns a small house and lives independently, but requires the services of at least two personal care attendants (PCAs). He has ongoing medical issues and has had several bouts of severe depression.

Michael relies on CommonHealth to pay for his medical care and PCAs. Michael is worried that when he turns 65, he will need to meet monthly spend-down criteria to obtain home care services, and this requirement will put him at risk of losing his house. “If I were in a nursing home,” he muses, “I would become severely depressed again.”

Issue: Potential solution:

23

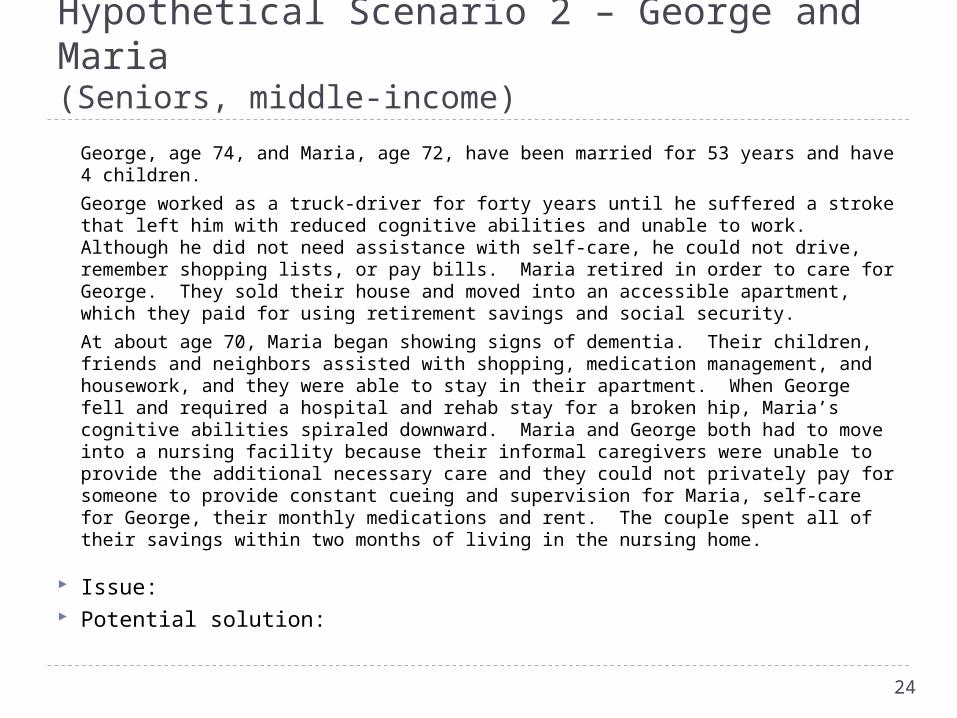

Hypothetical Scenario 2 – George and Maria(Seniors, middle-income)

George, age 74, and Maria, age 72, have been married for 53 years and have 4 children.

George worked as a truck-driver for forty years until he suffered a stroke that left him with reduced cognitive abilities and unable to work. Although he did not need assistance with self-care, he could not drive, remember shopping lists, or pay bills. Maria retired in order to care for George. They sold their house and moved into an accessible apartment, which they paid for using retirement savings and social security.

At about age 70, Maria began showing signs of dementia. Their children, friends and neighbors assisted with shopping, medication management, and housework, and they were able to stay in their apartment. When George fell and required a hospital and rehab stay for a broken hip, Maria’s cognitive abilities spiraled downward. Maria and George both had to move into a nursing facility because their informal caregivers were unable to provide the additional necessary care and they could not privately pay for someone to provide constant cueing and supervision for Maria, self-care for George, their monthly medications and rent. The couple spent all of their savings within two months of living in the nursing home.

Issue: Potential solution:

24

Hypothetical Scenario 3 – Roland and Kathy(Seniors, higher-income)

Roland, age 83, and Kathy, age 82, married in 1948 and had 3 children. After years of saving, they bought a two-family “handyman’s special”, which they fixed and continually improved over the years. Roland and Kathy loved their house and wanted more than anything to pass it on to their children.

They did their best to save their earnings as a plumber and a public school teacher and thought they had enough for a comfortable retirement. Kathy received a pension, and they received some income from the downstairs apartment.

Roland was diagnosed with a chronic and debilitating disease. He needed help walking and transferring, and Kathy couldn’t assist him by herself. The children stopped by in the mornings and evenings, and Kathy had to hire a home health aide during the day. Roland suffered third-degree burns from a cooking accident, and a visiting nurse came by every other day to perform ongoing treatment. Kathy was surprised to learn that Medicare and her medigap insurance didn’t cover these services. They were spending their savings much faster than they had planned, and they didn’t want to lose their house.

Issue: Potential solution:

25