Embed Size (px)

Citation preview

Chair for International Management –Liebherr / Richemont Endowed Chair

Store Brands

Research andRecent Developmentsin Switzerland and Germany

Professor Dr. Dirk Morschett

Forum in Store Brands, Universidad Complutense de Madrid Madrid, October 23, 2008

Chair for International Management –Liebherr / Richemont Endowed Chair

1

Private Label Market Share in Different European Countries (Value in %)

17,4

19,5

22,5

23,6

24,7

30,1

32,4

37,8

42,8

0% 10% 20% 30% 40% 50%

Portugal

Finland

Sweden

Spain

France

Belgium

Germany

United Kingdom

Switzerland

Source: PLMA 2006

Chair for International Management –Liebherr / Richemont Endowed Chair

2

Past Areas of Research (I) (Some Still Valid and Relevant)

Influence factors on the buying of store brands(Lauer 2001; Siemer 1999; Peters 1998)

• influence of socio-demographic consumer characteristics(e.g. Batra/Sinha 2000; Höper 1995; Rothe/Lamont 1973)

• influence of psychographic consumer characteristics(e.g. Erdem/Zhao/Valenzuela 2004; Richardson/Jain/Dick 1995; Schweiger/Koppe 1996; Meffert/Bruhn 1984)

• influence of competitive factors(e.g. Ailawadi et al. 2001; Hoch/Banerji 1993; Schmalen et al. 1996)

Findings: Store brands are more successful• the smaller the perceived quality differences within a product category• the lower functional, financial and social purchasing risk for a product• the more price sensitive the consumer• the lower the innovation intensity in a product category• the lower the promotion intensity in a product category• the larger the price distance between store brand and „national brand“

Chair for International Management –Liebherr / Richemont Endowed Chair

3

Past Areas of Research (II) (Some Still Valid and Relevant)

Effects of store brands• margins• consumer loyalty (e.g. Peters 1998, Zellekens/Horberg 1996)

• retailer image / store image (Morschett 2001; Zentes 2006; Zentes/Morschett 2004; Morschett 2006)

- studies focussing on generic private label frequently show a lowinfluence of private label on store image (e.g. Lauer 2001; Goerdt 1999; Peters 1998)

- „premium store brands“ are shown to enhance store image and consumer loyalty (Corstjens/Lal 2000; Windbergs 2007; Olbrich/Windbergs 2005)

Chair for International Management –Liebherr / Richemont Endowed Chair

4

Research Deficits and Recent Areas of Research

Combined effects of different brands in the merchandisemix insufficiently investigated

• combined effect of store brands and „national brands“• effect of store brand portfolio

- e.g. optimal structure, optimal variety

Chair for International Management –Liebherr / Richemont Endowed Chair

5Research Deficits versus Recent Developments in Store Brands in Switzerland and Germany

Highly dynamic new brand introductionSegmented store brands

• premium brands, standard brands, budget brands, eco-brands, childbrands, and many more

Upgrading of store brands• store brands as „national brands“ (Deichmann)

Linking the store brand to the retail brand (Rewe, Edeka)

Price distance store brand vs. national brand narrowsStore brands are not necessarily „lower quality“ anymore

• many of the traditional research findings are NOT valid anymore• same topics can be researched again

- socio-demographics, psychographics, …

Chair for International Management –Liebherr / Richemont Endowed Chair

6

Coop: Dynamically Segmenting Store Brand Portfolio (I: Early to late 1990s)

Chair for International Management –Liebherr / Richemont Endowed Chair

7

Coop: Dynamically Segmenting Store Brand Portfolio (II: 2002)

Chair for International Management –Liebherr / Richemont Endowed Chair

8

Coop: Dynamically Segmenting Store Brand Portfolio (III: 2004)

Chair for International Management –Liebherr / Richemont Endowed Chair

9

Coop: Dynamically Segmenting Store Brand Portfolio (IV: 2005)

Chair for International Management –Liebherr / Richemont Endowed Chair

10

Coop: Dynamically Segmenting Store Brand Portfolio (V: 2006)

Chair for International Management –Liebherr / Richemont Endowed Chair

11

Coop: Dynamically Segmenting Store Brand Portfolio (VI: 2006-2008)

Chair for International Management –Liebherr / Richemont Endowed Chair

12

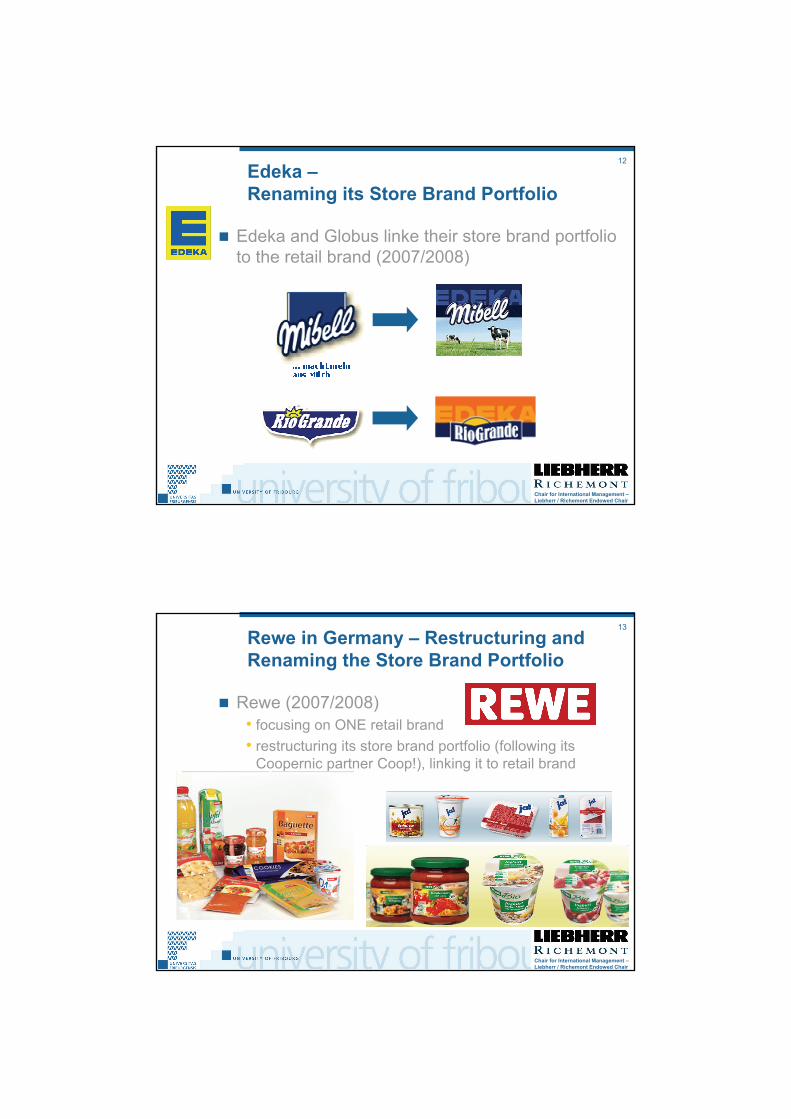

Edeka –Renaming its Store Brand Portfolio

Edeka and Globus linke their store brand portfolioto the retail brand (2007/2008)

Chair for International Management –Liebherr / Richemont Endowed Chair

13

Rewe in Germany – Restructuring and Renaming the Store Brand Portfolio

Rewe (2007/2008)• focusing on ONE retail brand• restructuring its store brand portfolio (following its

Coopernic partner Coop!), linking it to retail brand

Chair for International Management –Liebherr / Richemont Endowed Chair

14

Real – Introducing a Segmented Store Brand Portfolio

Real (Fall 2008)• Joel Saveuse (Managing Director) restructures the store

brand portfolio (following Carrefour)

Chair for International Management –Liebherr / Richemont Endowed Chair

15

Segm

ent d

epr

ix b

asSe

gmen

t de

prix

moy

enSe

gmen

t de

prix

hau

t(g

amm

es d

e pl

us-v

alue

)

The Store Brand Portfolio of Carrefour

Chair for International Management –Liebherr / Richemont Endowed Chair

16

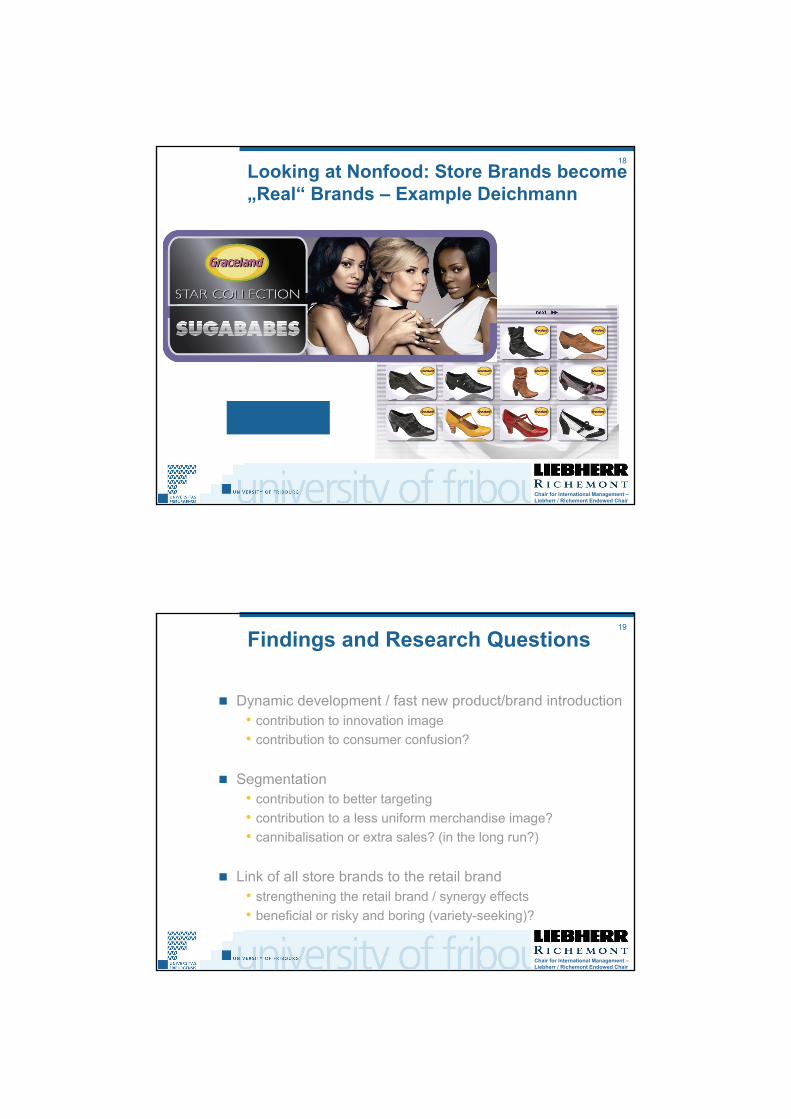

Looking at Nonfood: Store Brands become„Real“ Brands – Example Deichmann

„Brand Shoesat Deichmann“

Chair for International Management –Liebherr / Richemont Endowed Chair

17

Looking at Nonfood: Store Brands become„Real“ Brands – Example Deichmann

„Brand Shoesat Deichmann“

Chair for International Management –Liebherr / Richemont Endowed Chair

18

Looking at Nonfood: Store Brands become„Real“ Brands – Example Deichmann

Chair for International Management –Liebherr / Richemont Endowed Chair

19

Findings and Research Questions

Dynamic development / fast new product/brand introduction• contribution to innovation image• contribution to consumer confusion?

Segmentation• contribution to better targeting• contribution to a less uniform merchandise image?• cannibalisation or extra sales? (in the long run?)

Link of all store brands to the retail brand• strengthening the retail brand / synergy effects• beneficial or risky and boring (variety-seeking)?

Chair for International Management –Liebherr / Richemont Endowed Chair

20

Current and Future Research Topics

Effects of store brands in isolation• consumer loyalty, retailer image, retail brand

Combined effects of different brands in the merchandise mix insufficiently investigated

• combined effect of store brands and „national brands“• effect of store brand portfolio

Open questions include• internal consistency/fit (see e.g. Morschett 2001; Morschett 2002;

Zentes/Morschett 2004; Hilt (current study))• brand differentiation, brand similarity vs. internal cannibalisation

- image transfer within the store brand portfolio• dynamic brand introduction: innovation image versus consumer confusion• store brand names: effects of using the retail brand

Chair for International Management –Liebherr / Richemont Endowed Chair

21

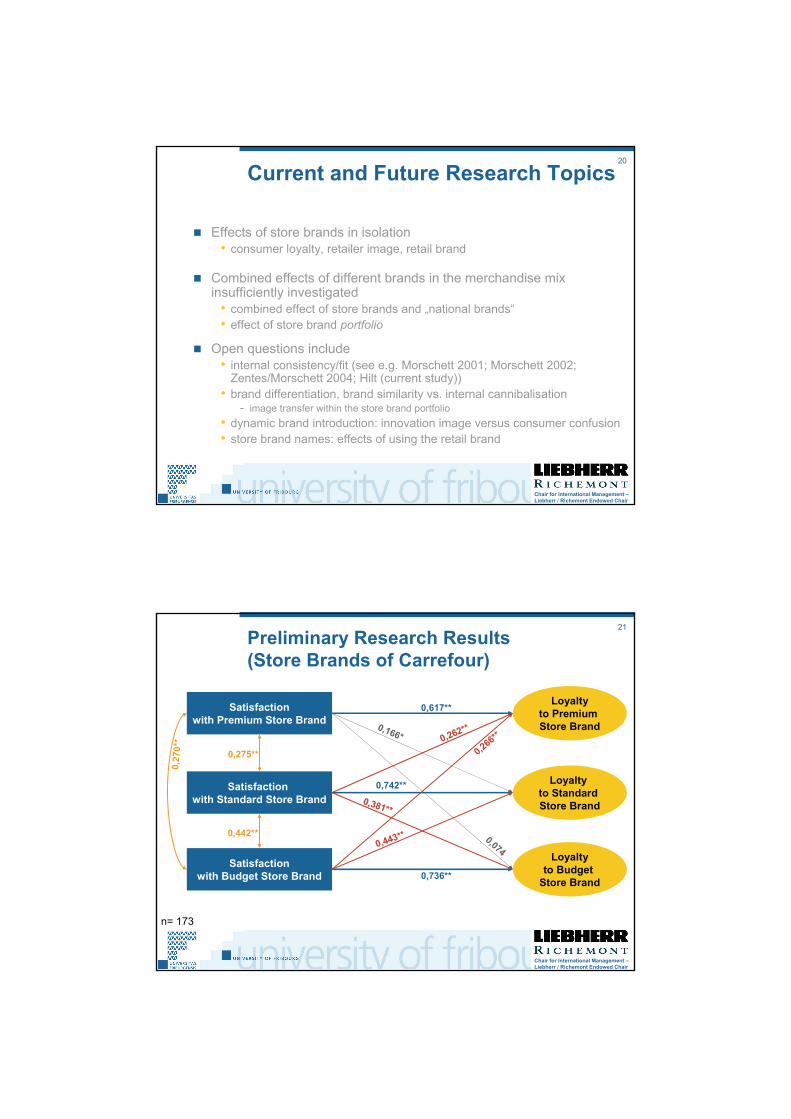

Preliminary Research Results(Store Brands of Carrefour)

Satisfactionwith Premium Store Brand

Satisfactionwith Standard Store Brand

Satisfactionwith Budget Store Brand

Loyaltyto Premium Store Brand

Loyaltyto Standard Store Brand

Loyaltyto Budget

Store Brand

n= 173

0,736**

0,742**

0,617**

0,442**

0,275**

0,27

0**

0,381**

0,443**

0,266**0,262**

0,074

0,166*

Chair for International Management –Liebherr / Richemont Endowed Chair

22

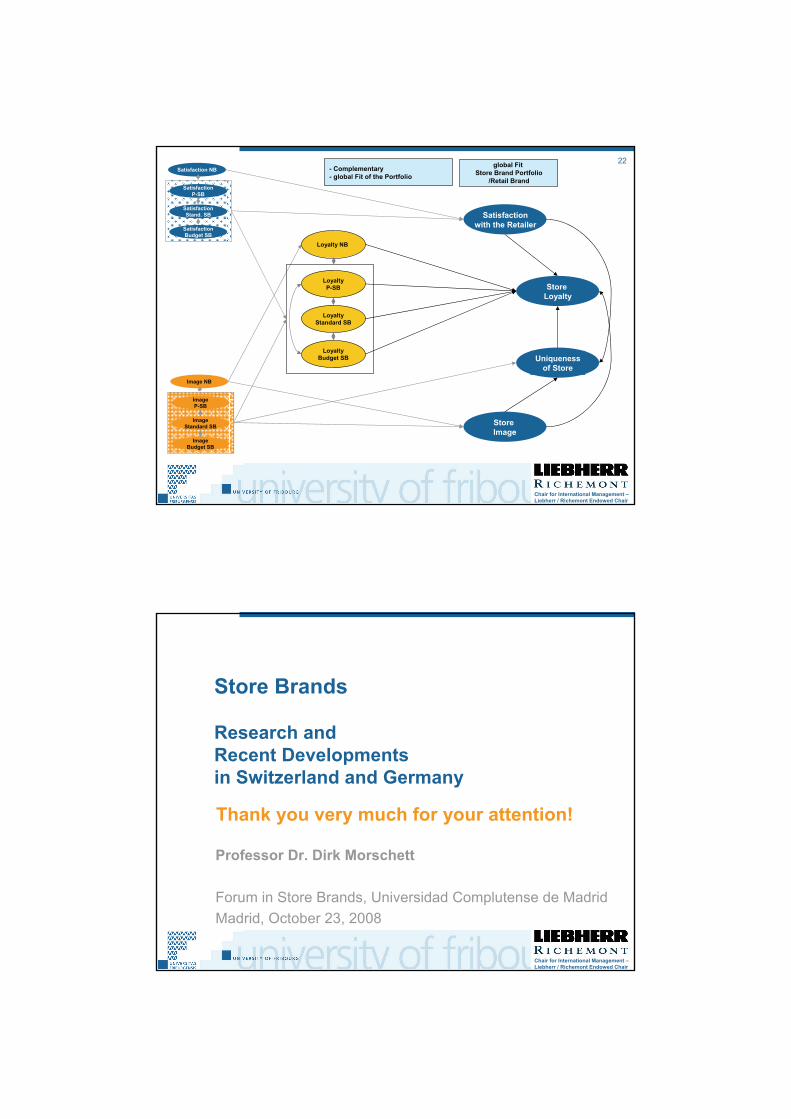

Untersuchungsmodell

ImageP-SB

ImageStandard SB

ImageBudget SB

Store Image

global Fit Store Brand Portfolio

/Retail Brand

Image NB

Uniquenessof Store

- Complementary- global Fit of the Portfolio

Satisfactionwith the Retailer

SatisfactionP-SB

SatisfactionStand. SB

SatisfactionBudget SB

Satisfaction NB

Store Loyalty

LoyaltyP-SB

LoyaltyStandard SB

LoyaltyBudget SB

Loyalty NB

Chair for International Management –Liebherr / Richemont Endowed Chair

Store Brands

Research andRecent Developmentsin Switzerland and Germany

Professor Dr. Dirk Morschett

Forum in Store Brands, Universidad Complutense de Madrid Madrid, October 23, 2008

Thank you very much for your attention!