Embed Size (px)

Citation preview

Procurement for Impact (P4I) and Market Shaping Progress report

16 December 2014IPC Meeting, World Bank in Washington

Stepping back: why is the Global Fund involved in Sourcing?

2

Over the last 7 years, the Board determined that the organization should play a greater role in procurement and market shaping of health products that it finances with 3 objectives1

1. Accelerate the introduction and maturation of new, more cost-effective products;

2. Ensure recipients procure the most cost-effective, WHO-recommended health products or regimens that meet the Global Fund quality assurance policies;

3. Ensure the continued availability, affordability, and innovation of products, including those for which there are not currently sustainable market conditions. through multiple approaches

1 GF/B23

The Global Fund has stepped up its sourcing and procurement strategy through a Procurement 4 Impact (P4i) transformation

One Sourcing team dedicated to fundamentally change the way we work across the supply chain to increase access to products

Earlier involvement

and closer collaboration

with manufacturers

Improving our purchasing

capability and changing our contracting

models

Optimising the international

supply chain to reduce cost and improve quality and efficiency

Better planning and

scheduling to support

continuity of supply

Delivering more products at the right time and place to more

people

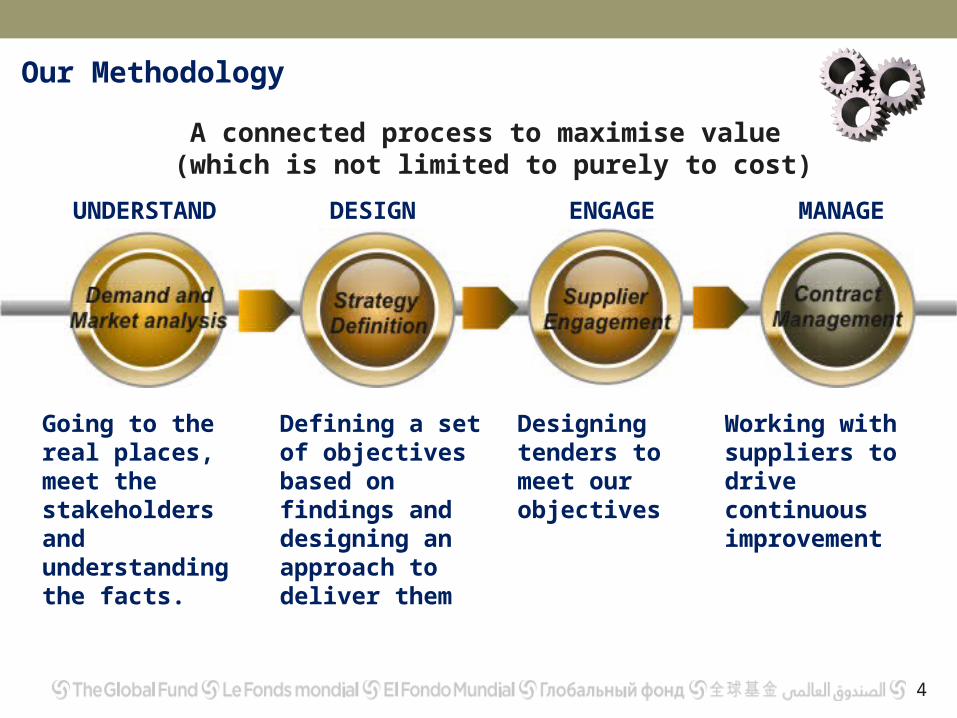

Our Methodology

4

A connected process to maximise value (which is not limited to purely to cost)

UNDERSTAND DESIGN ENGAGE MANAGE

Going to the real places, meet the stakeholders and understanding the facts.

Defining a set of objectives based on findings and designing an approach to deliver them

Designing tenders to meet our objectives

Working with suppliers to drive continuous improvement

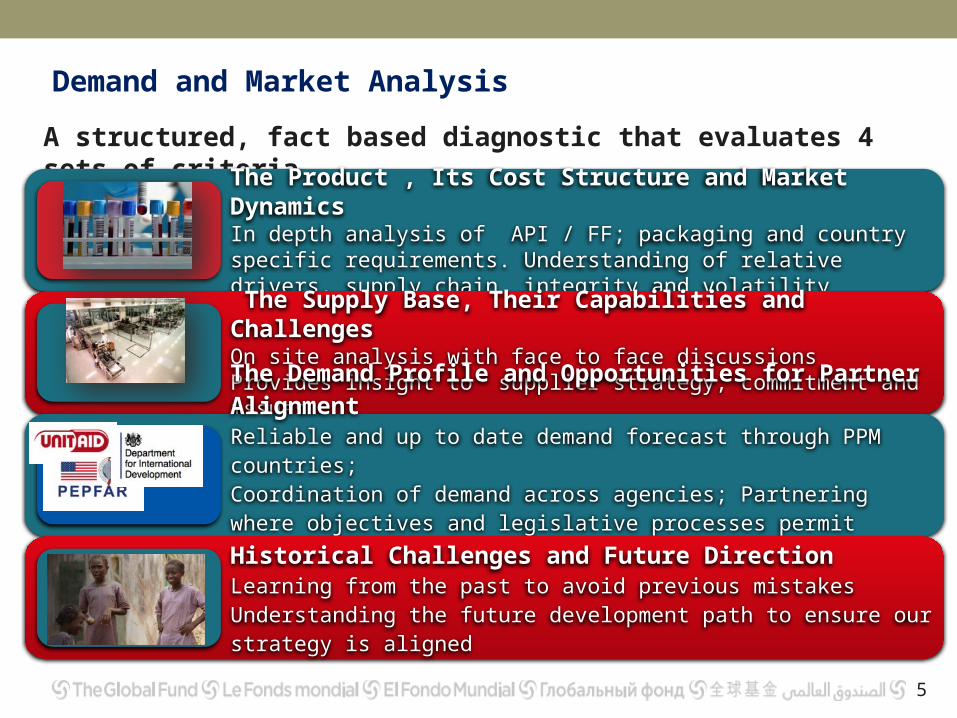

Demand and Market Analysis

5

A structured, fact based diagnostic that evaluates 4 sets of criteria

The Product , Its Cost Structure and Market DynamicsIn depth analysis of API / FF; packaging and country specific requirements. Understanding of relative drivers, supply chain integrity and volatility

The Supply Base, Their Capabilities and ChallengesOn site analysis with face to face discussions Provides insight to supplier strategy, commitment and issues

The Demand Profile and Opportunities for Partner AlignmentReliable and up to date demand forecast through PPM countries;Coordination of demand across agencies; Partnering where objectives and legislative processes permit

Historical Challenges and Future DirectionLearning from the past to avoid previous mistakesUnderstanding the future development path to ensure our strategy is aligned

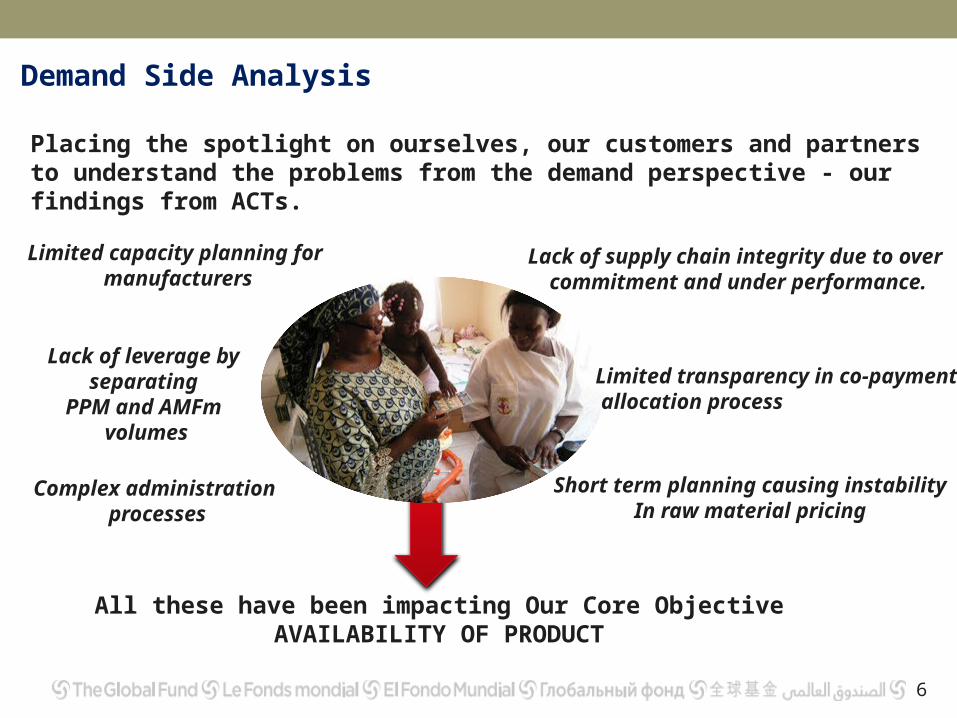

Demand Side Analysis

6

Placing the spotlight on ourselves, our customers and partners to understand the problems from the demand perspective - our findings from ACTs.

Lack of supply chain integrity due to over commitment and under performance.

Limited transparency in co-payment allocation process

Short term planning causing instabilityIn raw material pricing

Limited capacity planning for manufacturers

Lack of leverage by separating

PPM and AMFm volumes

Complex administration processes

All these have been impacting Our Core ObjectiveAVAILABILITY OF PRODUCT

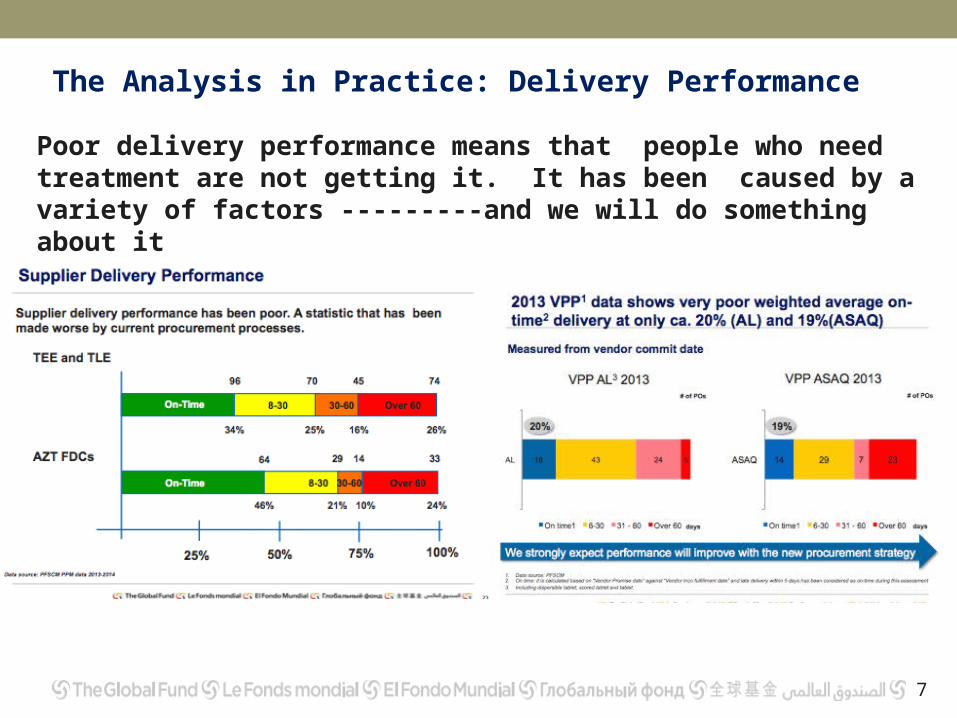

The Analysis in Practice: Delivery Performance

7

Poor delivery performance means that people who need treatment are not getting it. It has been caused by a variety of factors ---------and we will do something about it

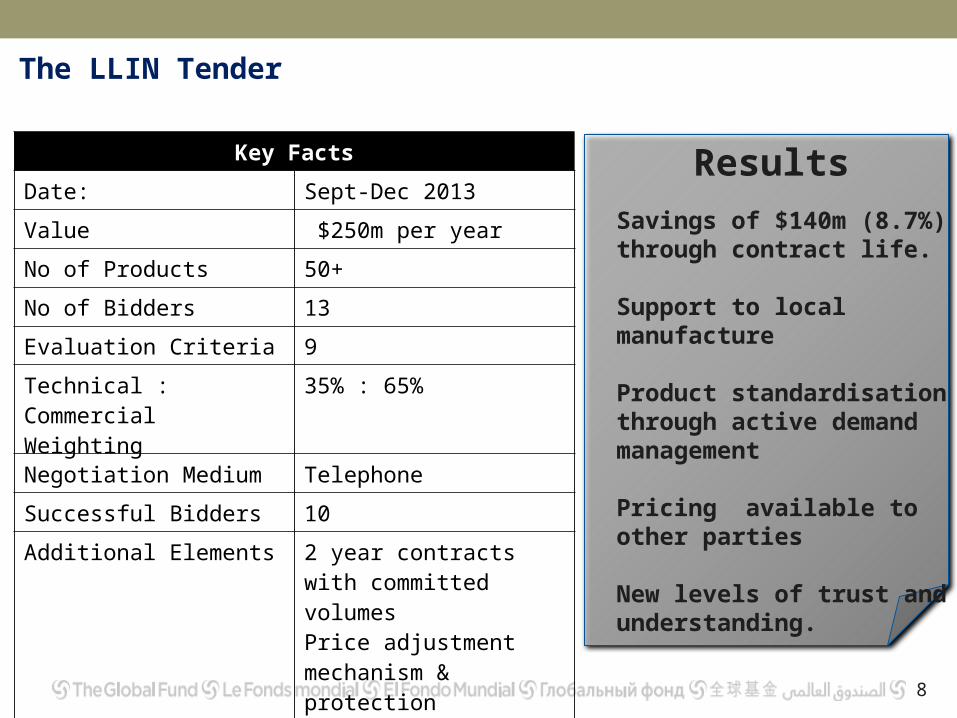

The LLIN Tender

8

ResultsKey Facts

Date: Sept-Dec 2013

Value $250m per year

No of Products 50+

No of Bidders 13

Evaluation Criteria 9

Technical : Commercial Weighting

35% : 65%

Negotiation Medium Telephone

Successful Bidders 10

Additional Elements 2 year contracts with committed volumesPrice adjustment mechanism & protection

Savings of $140m (8.7%) through contract life.

Support to local manufacture

Product standardisation through active demand management

Pricing available to other parties

New levels of trust and understanding.

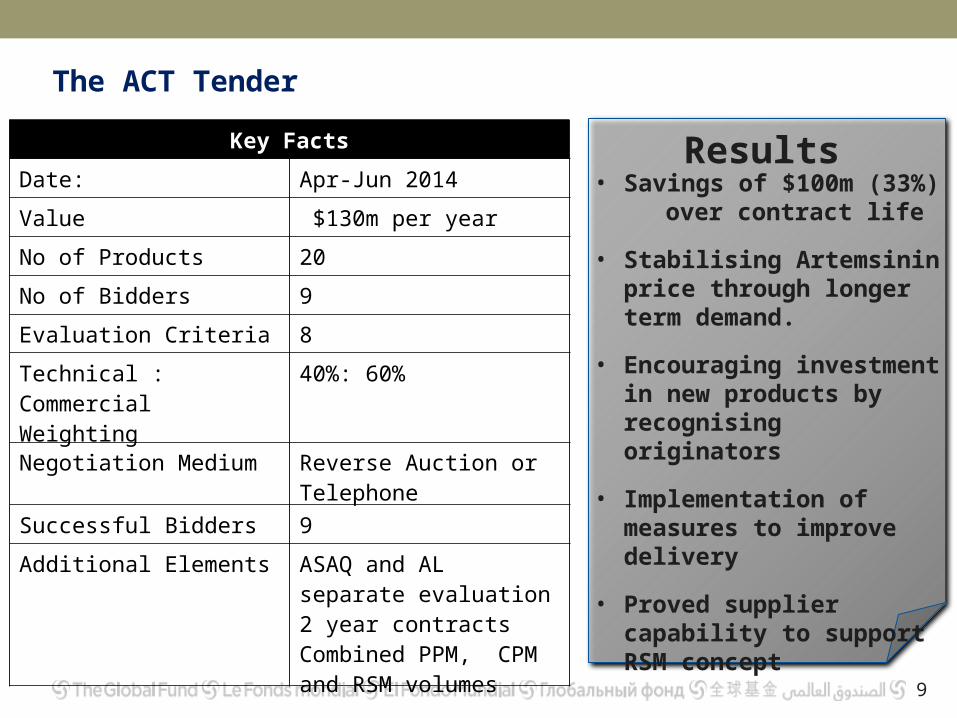

The ACT Tender

9

ResultsKey Facts

Date: Apr-Jun 2014

Value $130m per year

No of Products 20

No of Bidders 9

Evaluation Criteria 8

Technical : Commercial Weighting

40%: 60%

Negotiation Medium Reverse Auction or Telephone

Successful Bidders 9

Additional Elements ASAQ and AL separate evaluation 2 year contractsCombined PPM, CPM and RSM volumes

• Savings of $100m (33%)

over contract life

• Stabilising Artemsinin price through longer term demand.

• Encouraging investment in new products by recognising originators

• Implementation of measures to improve delivery

• Proved supplier capability to support RSM concept

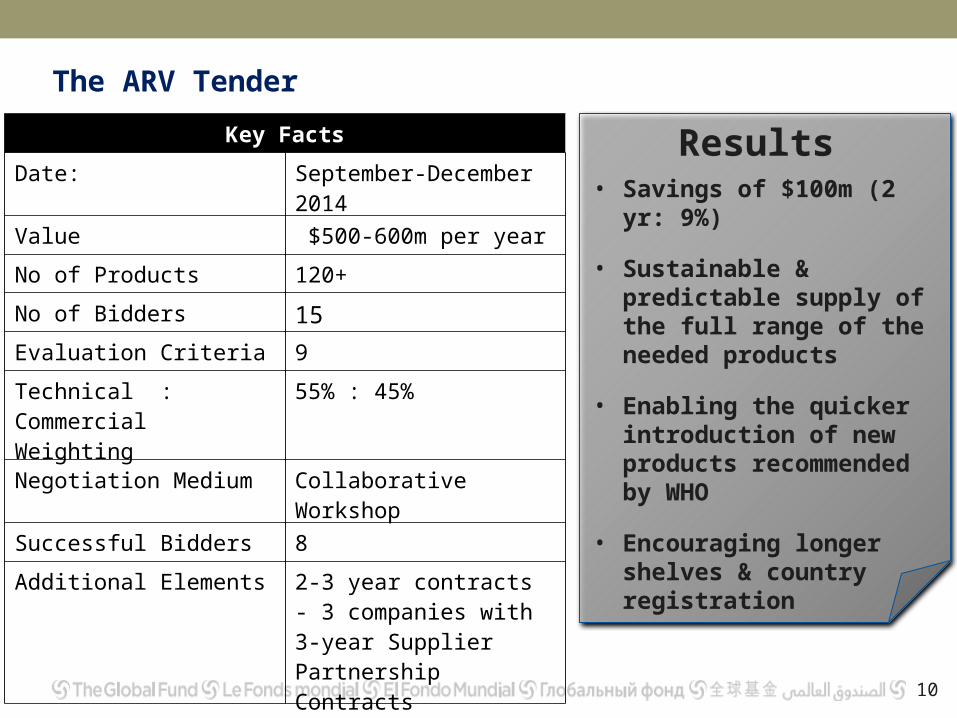

The ARV Tender

10

ResultsKey Facts

Date: September-December 2014

Value $500-600m per year

No of Products 120+

No of Bidders 15

Evaluation Criteria 9

Technical : Commercial Weighting

55% : 45%

Negotiation Medium Collaborative Workshop

Successful Bidders 8

Additional Elements 2-3 year contracts- 3 companies with 3-year Supplier Partnership Contracts

• Savings of $100m (2 yr: 9%)

• Sustainable & predictable supply of the full range of the needed products

• Enabling the quicker introduction of new products recommended by WHO

• Encouraging longer shelves & country registration

ARV MedicinesTender TGF 14-040Briefing

15 December 2014

Geneva

The ARV tender objectives are aligned to the Board’s Market Shaping Strategy.

12

These objectives will result in a new form of supplier

engagement

• Reduced lead times• Improved Delivery

Performance• Mitigate force majeure

Meeting programme needs Continued reliable supply De-risking API supply Improved processes To be customer of choice

Leveraged volumes Improved planning and

longer term contracts Use supplier expertise Collaboration to protect

reasonable margins

Sustainable supply

Competitive pricing and affordability

On-Time Delivery

Quality and Regulatory

Longer shelf life Broader country

registrations Supporting new product

introduction

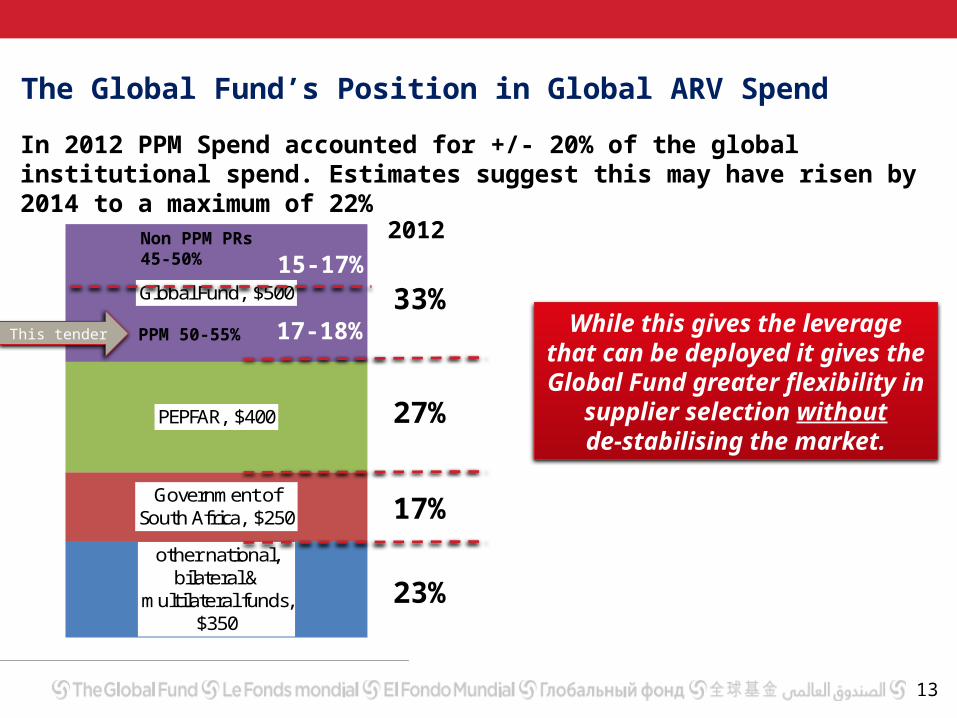

The Global Fund’s Position in Global ARV Spend

13

other national, bilateral &

multilateral funds, $350

Government of South Africa, $250

PEPFAR, $400

Global Fund, $500

Funding sources for ARVs in low and middle income countries, USD millions (2012)

PPM 50-55%

Non PPM PRs45-50%

33%

27%

17%

23%

In 2012 PPM Spend accounted for +/- 20% of the global institutional spend. Estimates suggest this may have risen by 2014 to a maximum of 22%

2012

While this gives the leverage that can be deployed it gives the Global Fund greater flexibility in

supplier selection without de-stabilising the market.

This tender 17-18%

15-17%

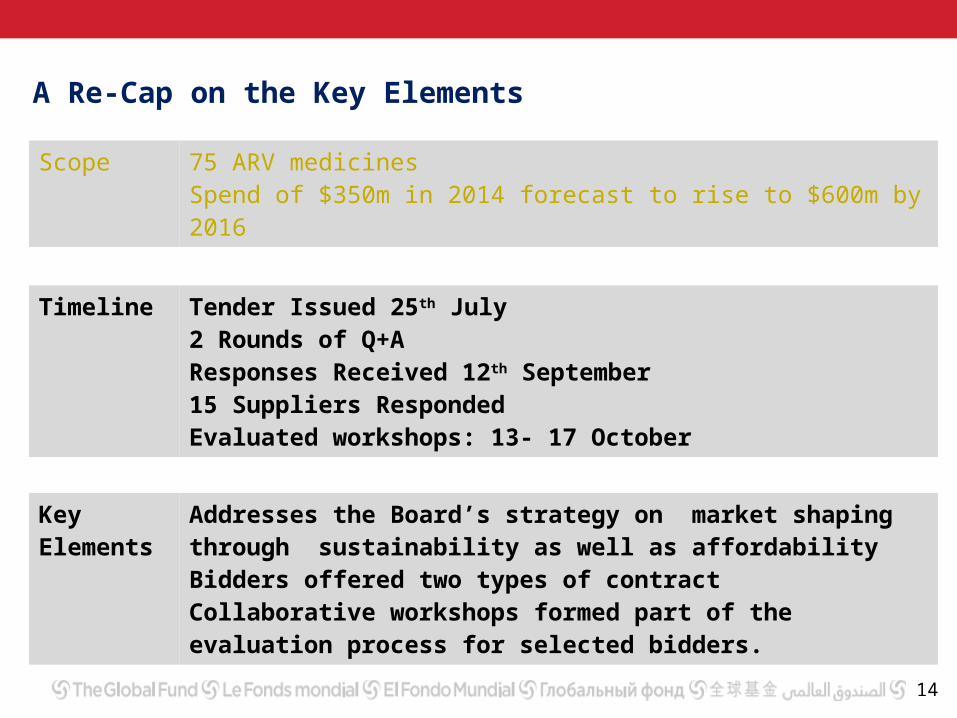

A Re-Cap on the Key Elements

14

Scope 75 ARV medicines Spend of $350m in 2014 forecast to rise to $600m by 2016

Timeline Tender Issued 25th July2 Rounds of Q+AResponses Received 12th September15 Suppliers RespondedEvaluated workshops: 13- 17 October

Key Elements

Addresses the Board’s strategy on market shaping through sustainability as well as affordabilityBidders offered two types of contractCollaborative workshops formed part of the evaluation process for selected bidders.

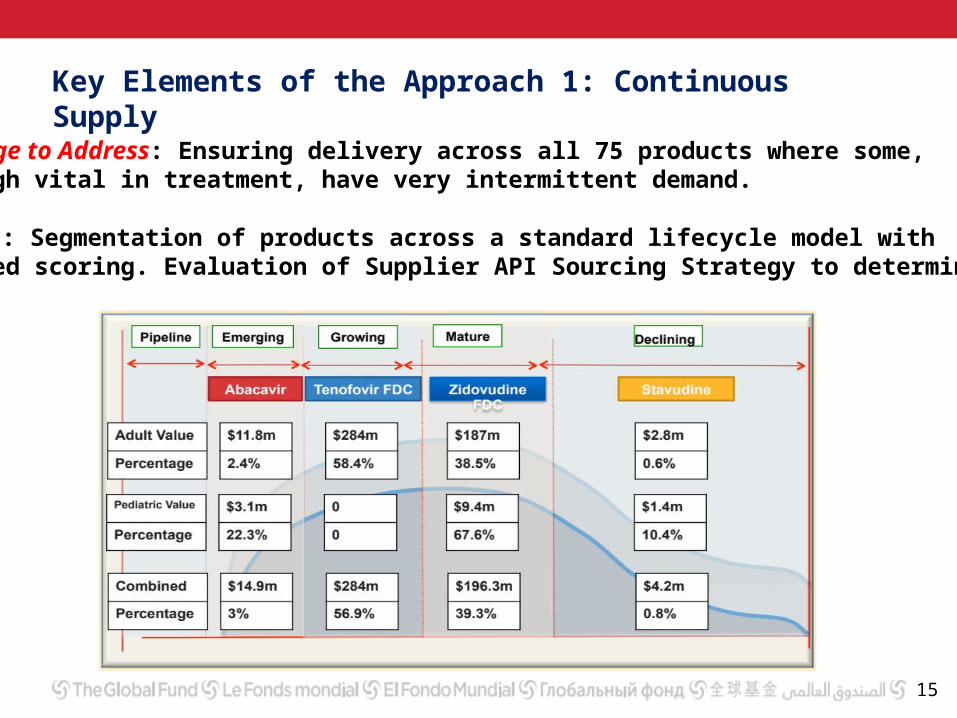

Key Elements of the Approach 1: Continuous Supply

15

Challenge to Address: Ensuring delivery across all 75 products where some, although vital in treatment, have very intermittent demand.

Solution: Segmentation of products across a standard lifecycle model withweighted scoring. Evaluation of Supplier API Sourcing Strategy to determine risk.

Key Elements of the Approach 2: Market Sustainability

16

Challenge to Address: Ensuring ongoing and new supplier participation in amarket associated with low returns.

Solution: Offer to develop long term supplier partnerships with selected suppliersbased on collaborative projects and committed product volumes over 3-5 years. Mechanism developed to support new entrants and new products from existingplayers.

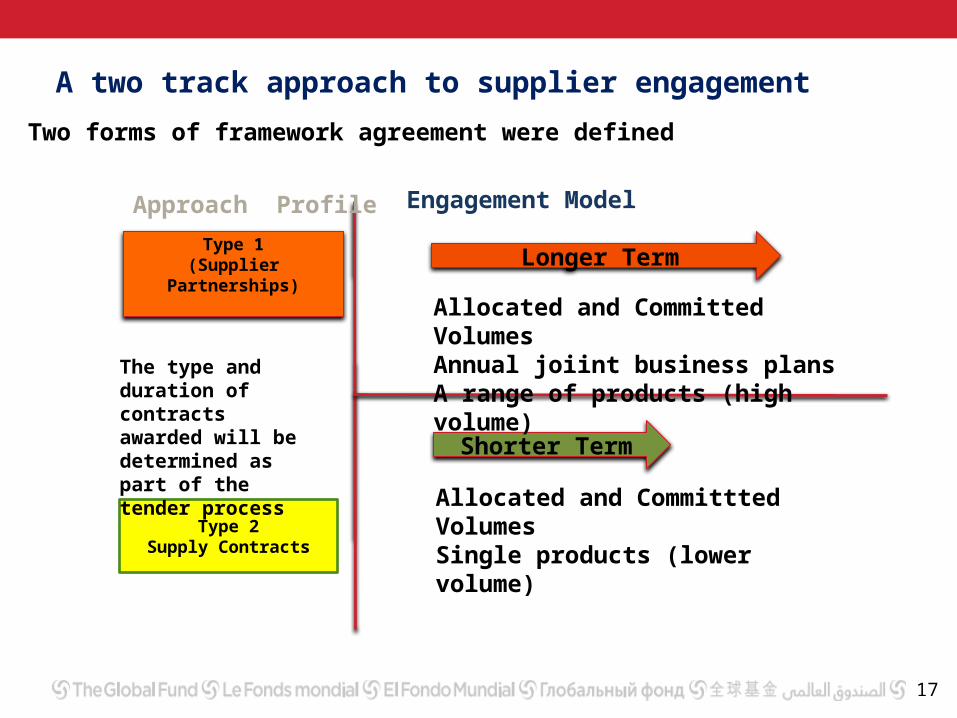

A two track approach to supplier engagement

17

Two forms of framework agreement were defined

Approach Profile Engagement Model

Longer Term

Shorter Term

Type 1(Supplier Partnerships)

Type 2Supply Contracts

The type and duration of contracts awarded will be determined as part of the tender process

Allocated and Committed VolumesAnnual joiint business plansA range of products (high volume)

Allocated and Committted VolumesSingle products (lower volume)

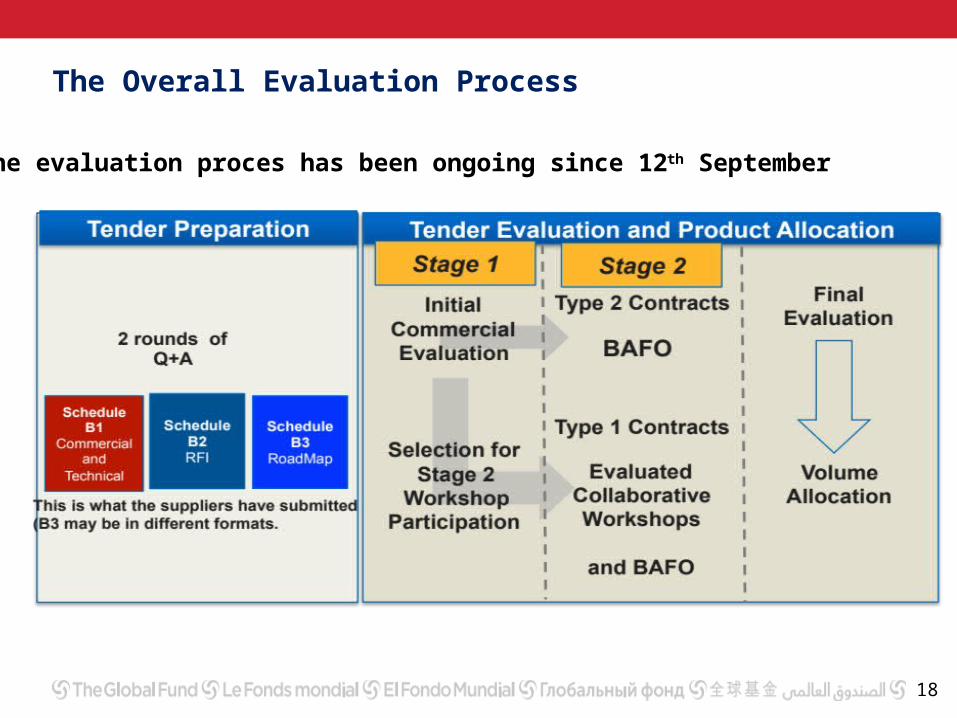

The Overall Evaluation Process

18

The evaluation proces has been ongoing since 12th September

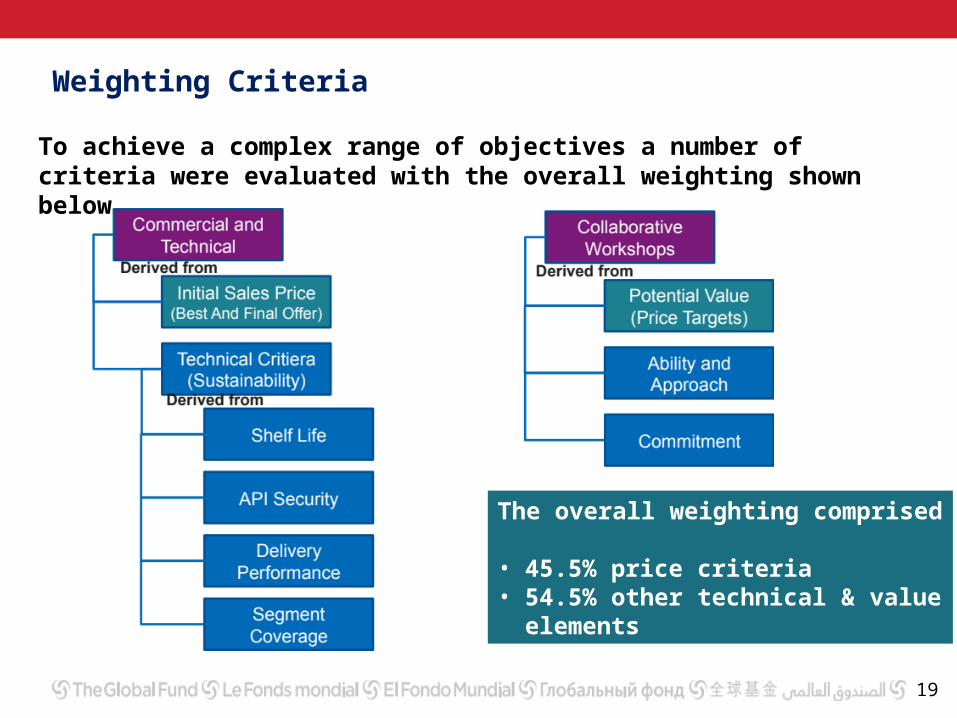

Weighting Criteria

19

To achieve a complex range of objectives a number of criteria were evaluated with the overall weighting shown below.

The overall weighting comprised • 45.5% price criteria • 54.5% other technical & value

elements

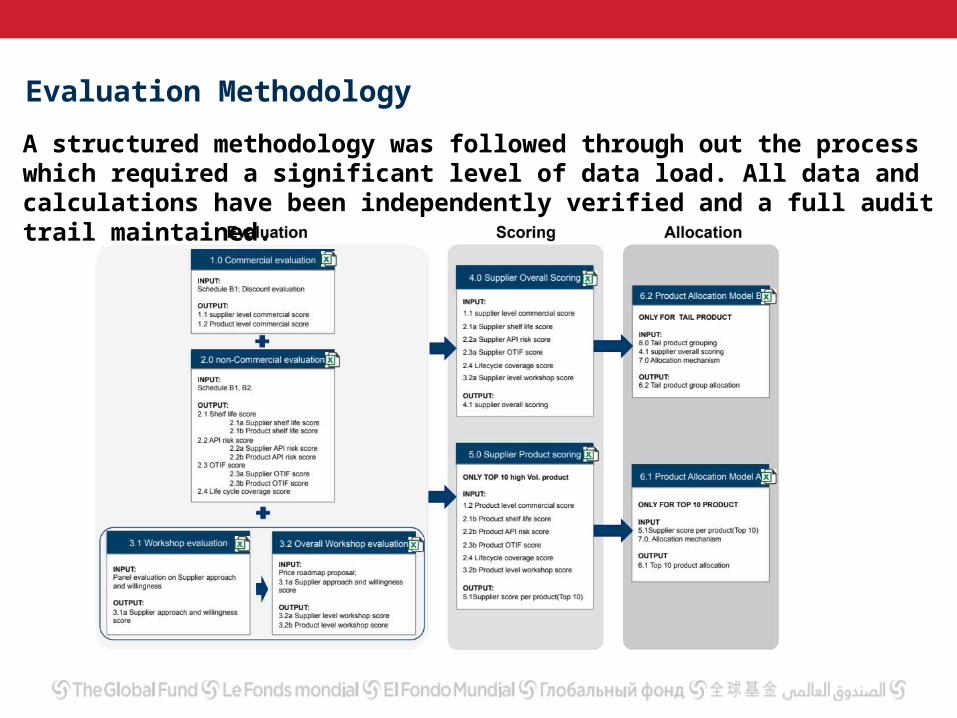

Evaluation Methodology

A structured methodology was followed through out the process which required a significant level of data load. All data and calculations have been independently verified and a full audit trail maintained.

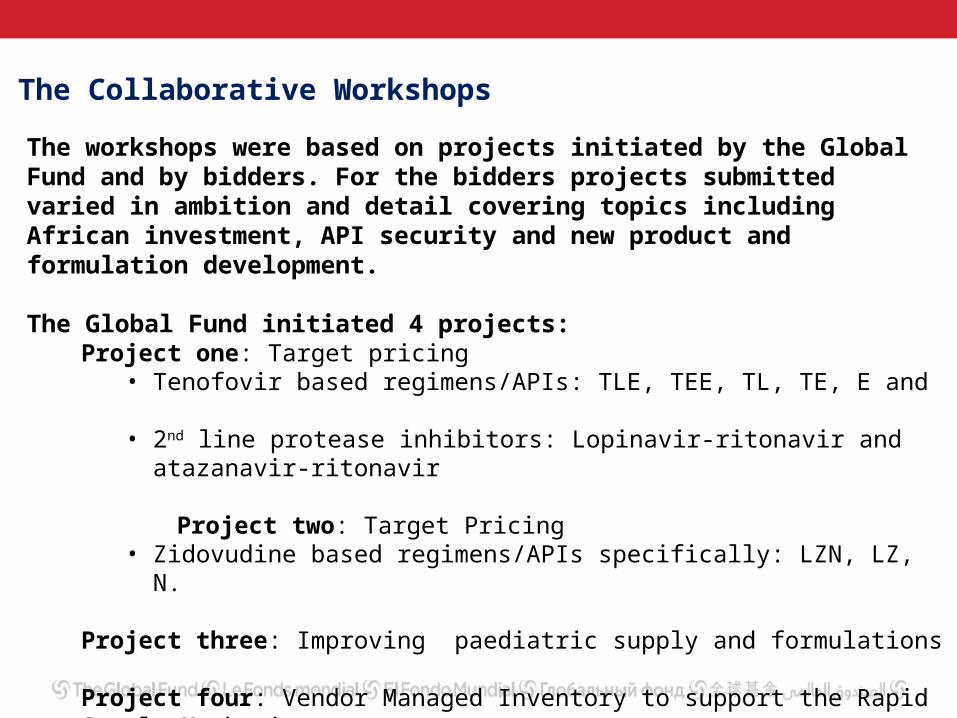

The Collaborative Workshops

The workshops were based on projects initiated by the Global Fund and by bidders. For the bidders projects submitted varied in ambition and detail covering topics including African investment, API security and new product and formulation development.

The Global Fund initiated 4 projects:

Project one: Target pricing• Tenofovir based regimens/APIs: TLE, TEE, TL, TE, E and • 2nd line protease inhibitors: Lopinavir-ritonavir and atazanavir-ritonavir

Project two: Target Pricing• Zidovudine based regimens/APIs specifically: LZN, LZ, N.

Project three: Improving paediatric supply and formulations

Project four: Vendor Managed Inventory to support the Rapid Supply Mechanism

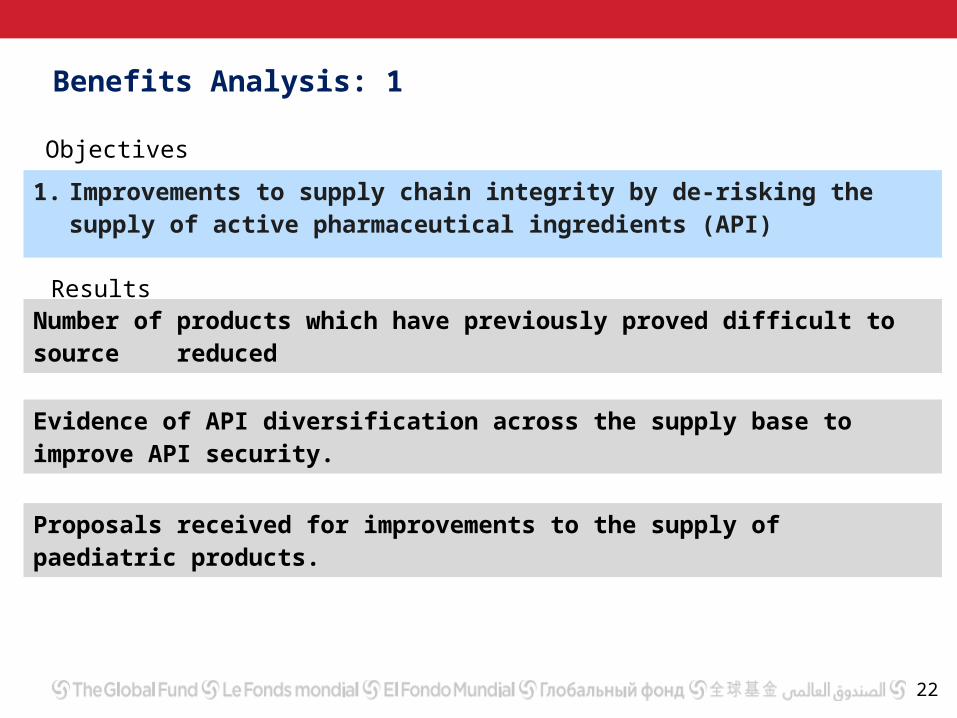

Benefits Analysis: 1

22

1. Improvements to supply chain integrity by de-risking the supply of active pharmaceutical ingredients (API)

Number of products which have previously proved difficult to source reduced

Evidence of API diversification across the supply base to improve API security.

Proposals received for improvements to the supply of paediatric products.

Objectives

Results

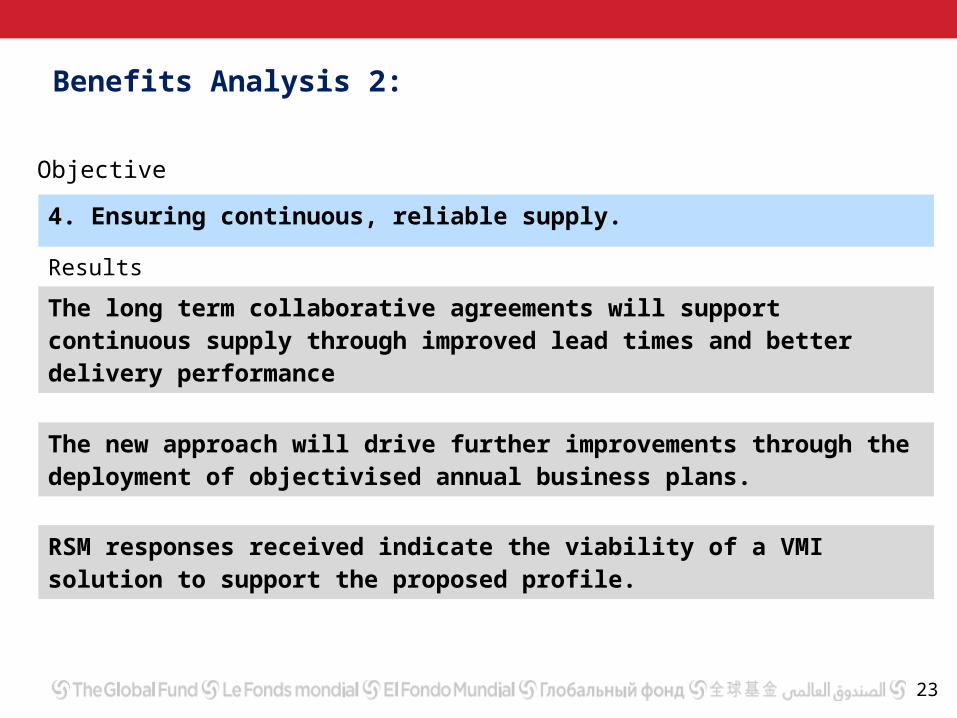

Benefits Analysis 2:

23

4. Ensuring continuous, reliable supply.

Results

The long term collaborative agreements will support continuous supply through improved lead times and better delivery performance

The new approach will drive further improvements through the deployment of objectivised annual business plans.

RSM responses received indicate the viability of a VMI solution to support the proposed profile.

Objective

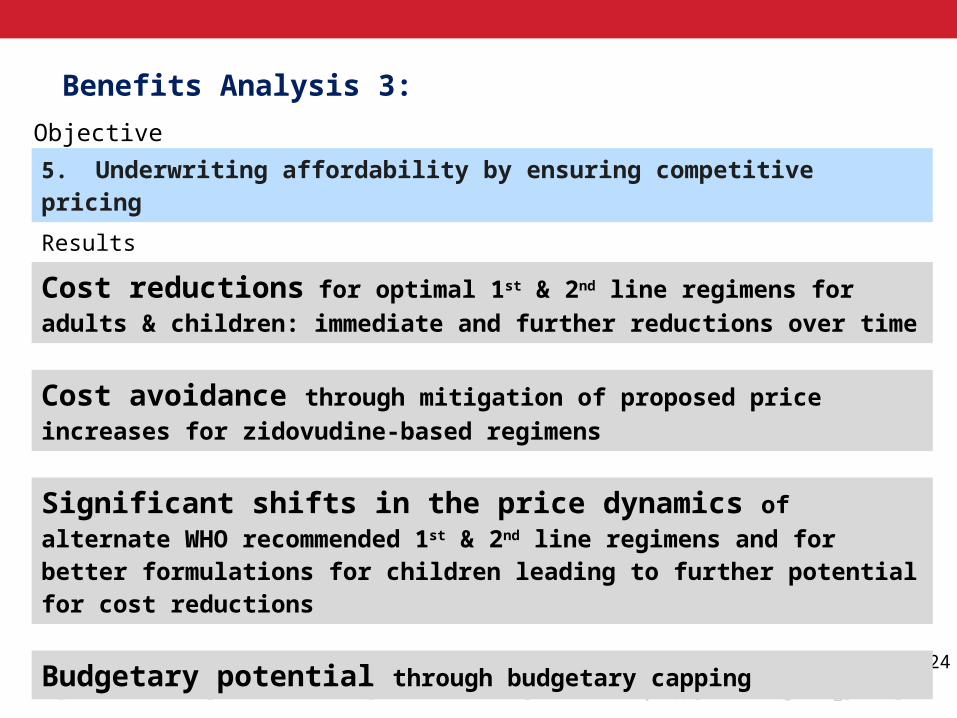

Benefits Analysis 3:

24

5. Underwriting affordability by ensuring competitive pricing

Results

Cost reductions for optimal 1st & 2nd line regimens for adults & children: immediate and further reductions over time

Cost avoidance through mitigation of proposed price increases for zidovudine-based regimens

Significant shifts in the price dynamics of alternate WHO recommended 1st & 2nd line regimens and for better formulations for children leading to further potential for cost reductions

Budgetary potential through budgetary capping

Objective

Benefits Analysis 4.

25

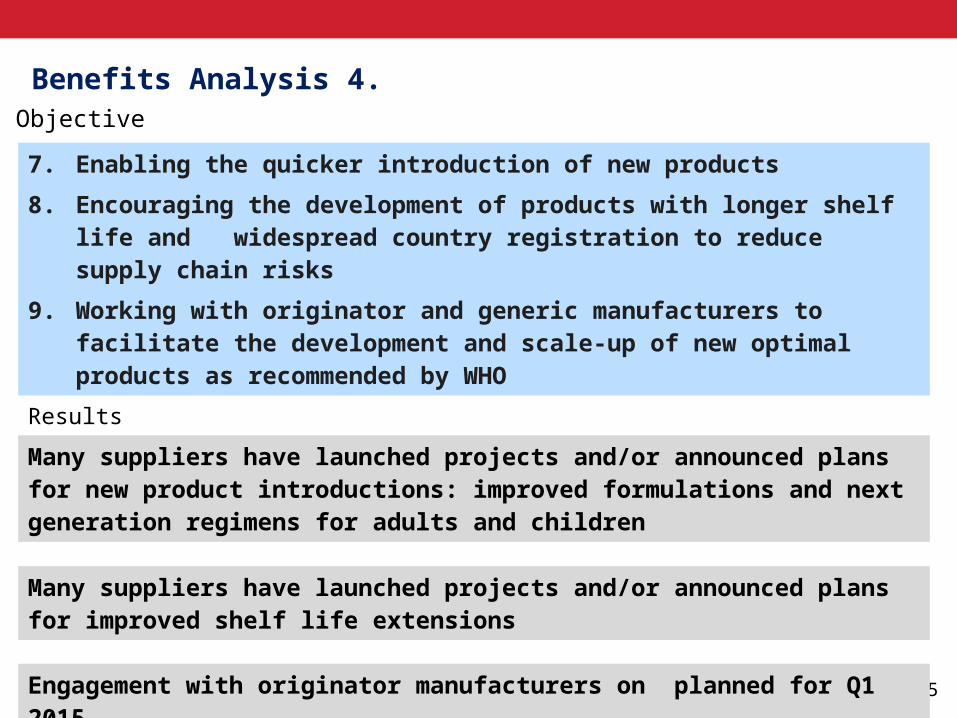

7. Enabling the quicker introduction of new products

8. Encouraging the development of products with longer shelf life and widespread country registration to reduce supply chain risks

9. Working with originator and generic manufacturers to facilitate the development and scale-up of new optimal products as recommended by WHO

Results

Many suppliers have launched projects and/or announced plans for new product introductions: improved formulations and next generation regimens for adults and children

Many suppliers have launched projects and/or announced plans for improved shelf life extensions

Engagement with originator manufacturers on planned for Q1 2015

Objective

Conclusion

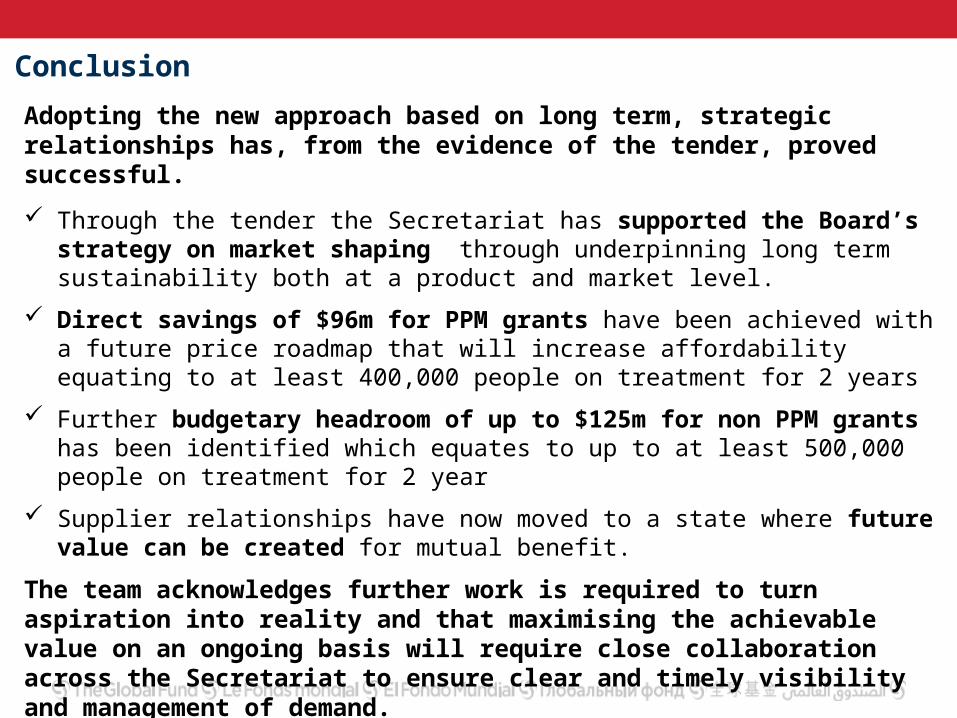

Adopting the new approach based on long term, strategic relationships has, from the evidence of the tender, proved successful.

Through the tender the Secretariat has supported the Board’s strategy on market shaping through underpinning long term sustainability both at a product and market level.

Direct savings of $96m for PPM grants have been achieved with a future price roadmap that will increase affordability equating to at least 400,000 people on treatment for 2 years

Further budgetary headroom of up to $125m for non PPM grants has been identified which equates to up to at least 500,000 people on treatment for 2 year

Supplier relationships have now moved to a state where future value can be created for mutual benefit.

The team acknowledges further work is required to turn aspiration into reality and that maximising the achievable value on an ongoing basis will require close collaboration across the Secretariat to ensure clear and timely visibility and management of demand.

Operationalising the relationships starts in January 2015

Developing a Sourcing Strategy for HIV Diagnostics

15 December 2014 Geneva

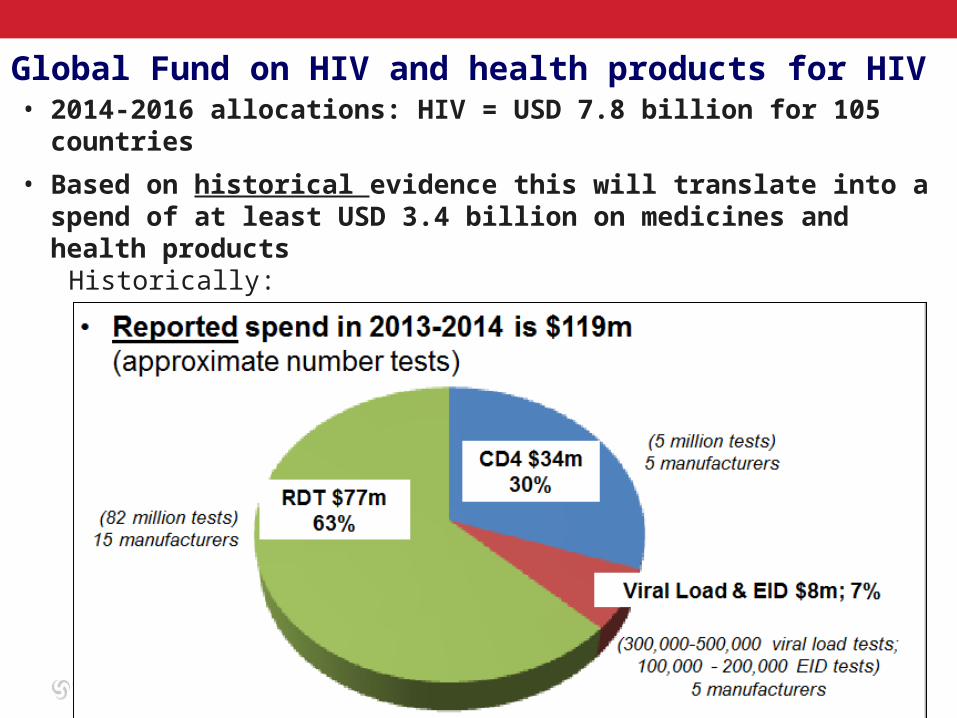

Global Fund on HIV and health products for HIV• 2014-2016 allocations: HIV = USD 7.8 billion for 105 countries

• Based on historical evidence this will translate into a spend of at least USD 3.4 billion on medicines and health products

Historically: • 80% on ARVs• 20% diagnostics, drugs of opportunistic infections; condoms etc.

Recent (Global Fund) Technical Review Panel (TRP) observations

• “Grant applicants have struggled to present a clear and prioritized concept note that explicitly explains strategic choices made in the allocation of limited resources to high-impact, cost-effective activities”

• “The TRP fully recognizes the important contribution that treatment can make to reducing both mortality and new infections. However, these gains can only be fully realized in an environment of ready and equitable access to HIV testing and treatment, strong linkages between diagnostic and ART services, quality medical care and support, appropriate regimens, high retention and good adherence”

Feedback from recipient countries and grant management teams

• Confusion on the interpretation of the WHO recommendations about CD4 and viral load

• Challenges to develop a prioritized rational and afforded plan for implementing the WHO recommendations

• Uncertainty of how DBS and “POC” will evolve and what is the right mix; should they wait?

• Need for a guidance on the process for a transparent selection and procurement of the optimal most cost-effective platforms

• National laboratory teams need empowering to be able to argue their case in funding prioritization decisions

Feedback from manufacturers

• Gaps around DBS and sample transport normative guidance• Need for & realistic country based forecasts with funding behind

them: separation of need from demand • International expectations don’t often meet country reality• Infrastructure and skills gaps need redressing• Greater focus on service levels in selection and procurement• Longer term vision in procurement and contracting • Service contracts need to be funded and purchased

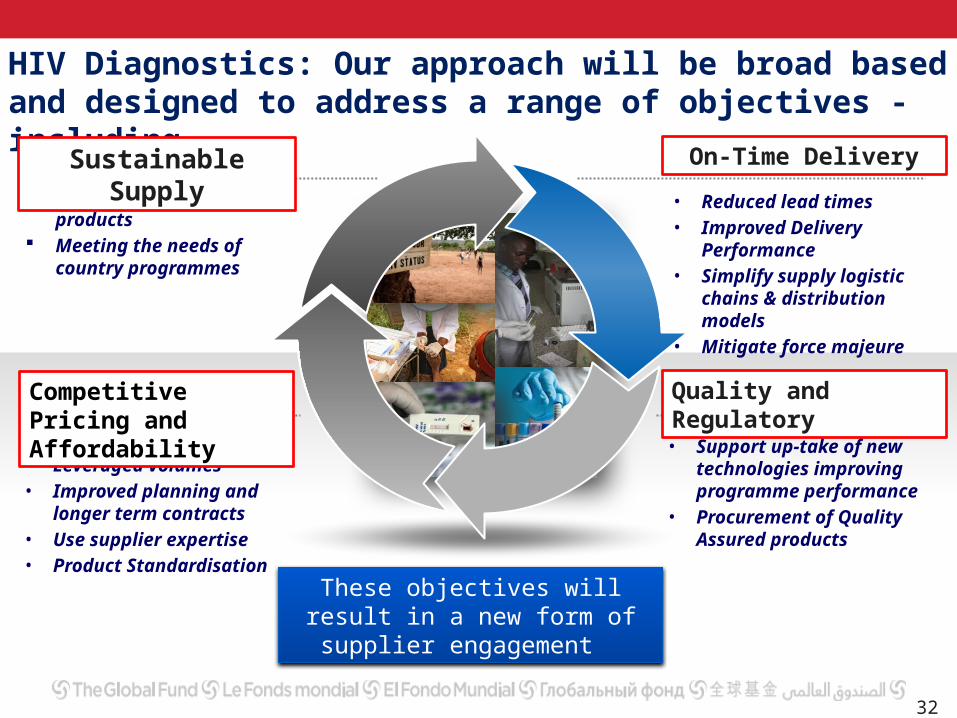

HIV Diagnostics: Our approach will be broad based and designed to address a range of objectives - including

32

These objectives will result in a new form of supplier engagement

• Reduced lead times• Improved Delivery

Performance• Simplify supply logistic

chains & distribution models

• Mitigate force majeure

Continued supply of products

Meeting the needs of country programmes

• Leveraged volumes• Improved planning and

longer term contracts• Use supplier expertise• Product Standardisation

Sustainable Supply

Competitive Pricing and Affordability

On-Time Delivery

Quality and Regulatory

• Support up-take of new technologies improving programme performance

• Procurement of Quality Assured products

Guidance has been issued: WHO, Global Fund, UNITAID & MSF

Collaboration is good

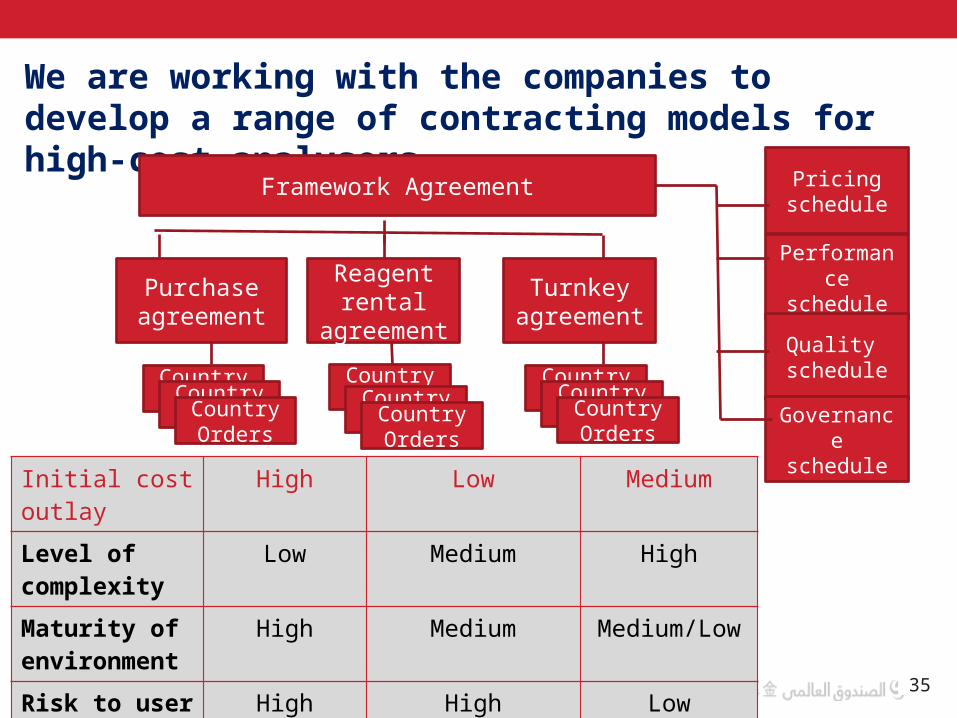

We are working with the companies to develop a range of contracting models for high-cost analysers

35

Framework Agreement Pricingschedule

Purchase agreement

Performance schedule

Quality schedule

Reagent rental

agreement

Turnkey agreement

Governanceschedule

Country OrdersCountry

OrdersCountry Orders

Country OrdersCountry

OrdersCountry Orders

Country OrdersCountry

OrdersCountry Orders

Initial cost outlay

High Low Medium

Level of complexity

Low Medium High

Maturity of environment

High Medium Medium/Low

Risk to user High High Low

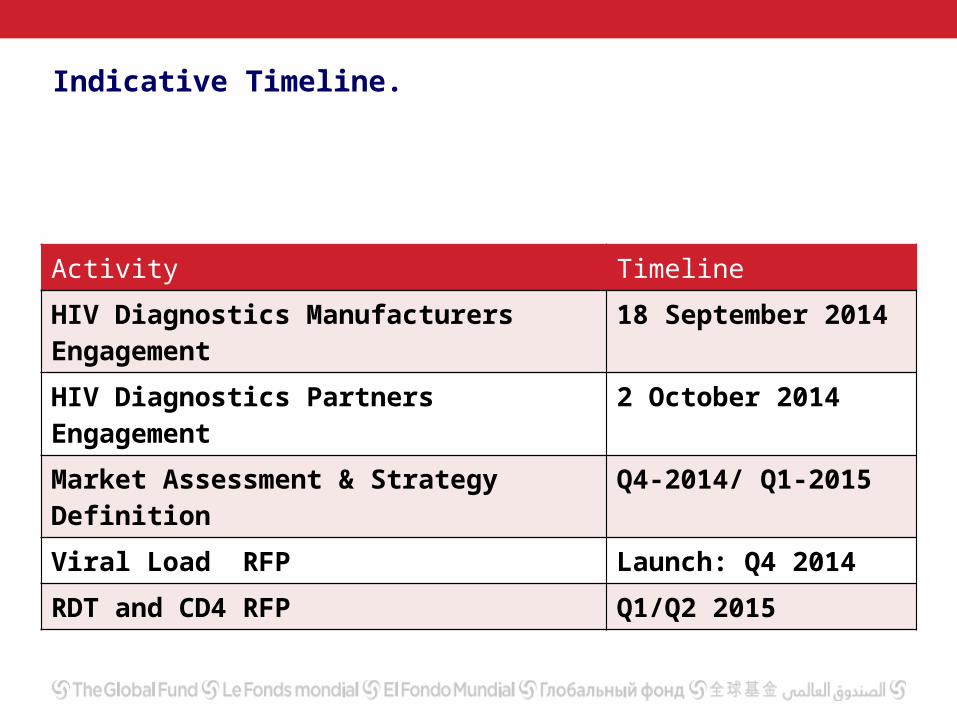

Indicative Timeline.

Activity Timeline

HIV Diagnostics Manufacturers Engagement

18 September 2014

HIV Diagnostics Partners Engagement 2 October 2014

Market Assessment & Strategy Definition Q4-2014/ Q1-2015

Viral Load RFP Launch: Q4 2014

RDT and CD4 RFP Q1/Q2 2015

37

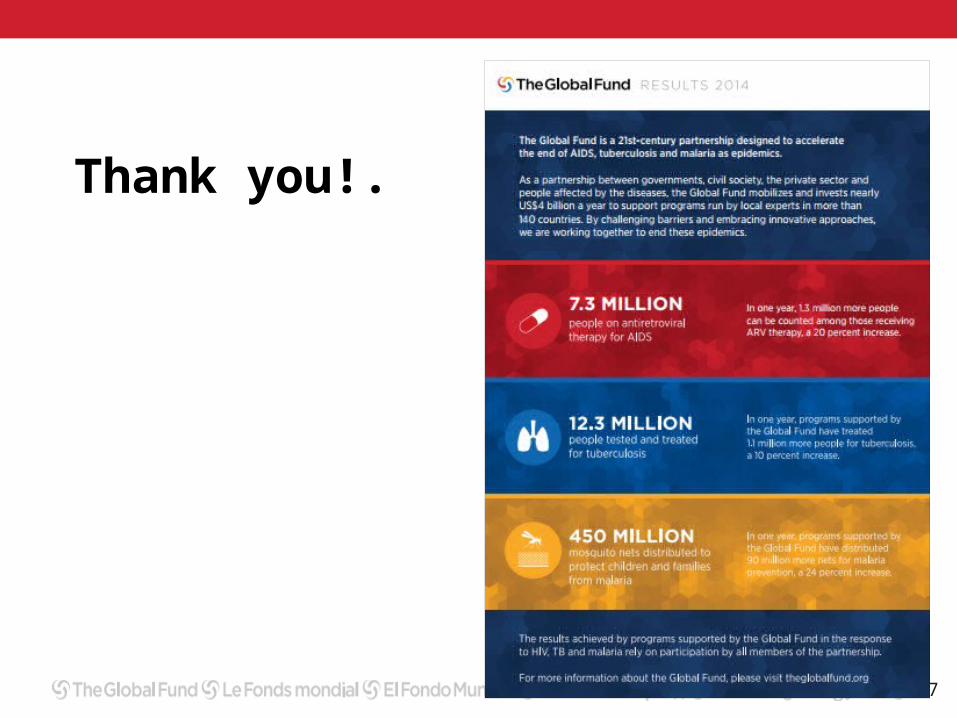

Thank you!.