Embed Size (px)

Citation preview

R I C K M U N C R I E F , C H A I R M A N & C E O

A U G U S T 6 , 2 0 1 9

WPX Delivering As Planned

2Q COMPANY HIGHLIGHTS

▪ CFFO increased 48% 1H 2019 vs. 1H 2018

▪ 2Q Delaware oil realizations of WTI plus $0.23 including Midland

basis swaps

▪ Received proceeds from Oryx II monetization

▪ Second 200 MMCF/D train came online at Delaware JV plant

SECOND HALF 2019

▪ Reaffirming existing 2019 CAPEX guidance

▪ Raising full-year oil guidance by 4% and full-year total volume

guidance by 5%

▪ Projecting free cash flow in 3Q and 4Q1

1. Free cash flow includes CFFO (excluding working capital changes) minus DC&F, non operated and midstream opportunities capital.

2

ACCELERATING RETURN OF CAPITAL

▪ Returning capital to shareholders in the form of a stock

repurchase program

▪ Initiating program to repurchase up to $400MM of shares over

the next 24 months

-$200

-$150

-$100

-$50

$0

$50

$100

$150

2016 2019E

0%

10%

20%

30%

2016 2019E

-

1

2

3

4

5

2016 2019E

3

A Lookback Since RKI Acquisition

F R E E

C A S H F L O W 2 , 3N E T L E V E R A G E 1 P R O D U C T I O N

NET

DEB

T/A

DJ.

EB

ITD

AX

$M

M

68%REDUCTION IN TRAILING

12-MONTH NET LEVERAGE SINCE 2016

$200MM+INCREASE IN FREE CASH FLOW

SINCE 2016

51%INCREASE IN PRODUCTION GROWTH

PER DEBT ADJ. SHARE SINCE 2016

1. Net debt/trailing 12-month EBITDAX. 2. 2016 free cash flow is based on cash flow from operating activities of $268 million plus net working capital changes of $82 million less capital expenditures incurred of $500 million. The capital expenditures incurred exclude $84 million of land acquisitions.3. 2019 FCST free cash flow is based on estimated CFFO less forecasted capital expenditures including operated and non-operated drilling and completions, facilities and midstream opportunities. Estimated CFFO is based on forecasted adjusted EBITDAX further adjusted for other items such as interest and stock-based compensation.4. Annual production growth that is normalized for any changes in debt or equity. This metric monitors a company’s ability to grow production responsibly in a shareholder friendly manner. Share price based on YE 2016 and held constant.

2

ESTIMATED

RANGE3

3

GROWTH PER DEBT ADJUSTED SHARE4

C L A Y G A S P A R , P R E S I D E N T & C H I E F O P E R A T I N G O F F I C E R

OPERATIONS

5.0

5.5

6.0

6.5

7.0

7.5

2018 Avg. 2Q 2019

WILLISTON 2-MILE WELL COSTS

5%

4

7

10

13

2018 Avg. 2Q 2019

Pecos State Test Benefitting Both Basins

5

WELL

CO

ST

$M

M

DELAWARE 2-MILE WELL COSTS

22%

0

4

8

12

16

20

2Q 2018 2Q 2019

WILLISTON DAYS FROM SPUD

TO RIG RELEASE (2-MILE)

31%14%

DELAWARE DAYS FROM SPUD

TO RIG RELEASE (2-MILE)

16

20

24

28

2Q 2018 2Q 2019

Applied learnings to first Williston pads

Project description

Applied learnings to first Delaware pad (CBR 41-44) Coring additional 1,240 ft in

Stateline from 2nd Bone Spring to

3rd Bone Spring bench for CBR 10

• Contiguous 806 ft core running from bottom of 3rd Bone Spring through Wolfcamp B • Equipped with microseismic geophones and external pressure & temperature

gauges • Strategically placed to monitor fracs during completion, overall well performance &

drainage through life of the well• Permanent DAS-DTS fiberoptic installation

• Lower well costs• Improved early production

2 0 1 9

• Improved completion/cluster design• Fine tuned well spacing, landing targets, and artificial lift

L O W E R C O S T S M O R E E F F I C I E N T

2 0 1 8

WELL

CO

ST

$M

M

AV

G.

DA

YS F

RO

M S

PU

D

AV

G.

DA

YS F

RO

M S

PU

D

Delaware Activity 2019

6

STATELINERUSTLER

BREAKS

SAND

LAKESHALEY

3RD BONE

SPRING5 1

UPPER

WOLFCAMP19 4 5 5

LOWER

WOLFCAMP1 2 4 1

Total 25 6 9 7

1 H 2 0 1 9 F I R S T S A L E S

STATELINE

RUSTLER BREAKS

SANDLAKES

HALEY

WPX ACTIVITY BY AREA 2 H 2 0 1 9 F I R S T S A L E S

S T A T E L I N E A C T I V I T Y1H: 53% 2H: 68%

R U S T L E R B R E A K S

A C T I V I T Y1H: 13% 2H: 6.5%

S A N D L A K E S A C T I V I T Y1H: 19% 2H: 6.5%

H A L E Y A C T I V I T Y1H: 15% 2H: 19%

1 H 2 0 1 9 F I R S T S A L E S

• Average lateral length of ~7,650’

• Average wells per visit ~2.1 wells

• 83% of completions were in Upper

Wolfcamp benches and 3BS

• Completed wells in 8 different benches

• 53% of activity in Stateline

2 H 2 0 1 9 F I R S T S A L E S

• Average lateral length of ~7,700’

• Average wells per visit ~2.8 wells

• 100% of completions will be in Upper

Wolfcamp benches and 3BS

• Will complete wells in 6 different benches

• 68% of activity will be in StatelineR I G C O U N T

1H: ~5.6 RIGS 2H: 5 RIGS

Upper Wolfcamp includes Wolfcamp XY and A

Lower Wolfcamp includes Wolfcamp B,C, & D

STATELINERUSTLER

BREAKS

SAND

LAKESHALEY

3RD BONE

SPRING5

UPPER

WOLFCAMP16 2 2 6

LOWER

WOLFCAMP

Total 21 2 2 6

$50.00

$52.00

$54.00

$56.00

$58.00

$60.00

$62.00

$64.00

$66.00

Apr-19 May-19 June-19

-$0.50

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

Apr-19 May-19 Jun-19

N Y M E X

WPX REALIZED PRICE INC. COMMODITY MGMT UPLIFT2

Delaware Midstream Continues to Drive Value

71. Realized prices includes basis hedges.2. Commodity management uplift represents the combination of WPX realized price and the net margin from utilizing excess capacity over production volumes.

STRONG 2Q DELAWARE

PRICE REAL IZAT IONS

$2.05$60.052Q’19 AVG. REALIZED

OIL PRICE INCLUDING BASIS HEDGES

2Q’19 AVG. REALIZED

GAS PRICE INCLUDING BASIS HEDGES

D E L A W A R E O I L D E L A W A R E G A S

$2.992Q’19 AVG. REALIZED

GAS PRICE INCLUDING BASIS HEDGES &

COMMODITY MANAGEMENT UPLIFT

0

20

40

60

80

100

120

0 10 20 30 40 50

Tho

usa

nd

s

Williston: Continued Outperformance

NORMALIZED DAYS ON PRODUCTION

CU

MU

LATI

VE O

IL (

MB

BLS

)

DELIVERING ON RESULTS

1

2

3

2019 WELLS OUTPERFORMING TYPE CURVE

LOWER YEAR-OVER-YEAR WELL COSTS

SETTING NEW PRODUCTION RECORDS

2019 OPERATIONS2Q 2019 WELL RESULTS

SETTING PRODUCTION RECORDS24-HOUR INITIAL PRODUCTION

MINOT GRADY 26-35HD

MINOT GRADYDELORES SAND

5,862BARRELS OF OIL EQUIVALENT PER DAY

8

K E V I N V A N N , C H I E F F I N A N C I A L O F F I C E R

FINANCIALS

2019 Updated Full-Year Guidance

10

0

10

20

30

40

50

80

90

100

110

120

1QA 2QA 3QE 4QE

2019 OIL PRODUCTION AND FIRST SALES GUIDANCE BY QUARTER

FIR

ST S

ALE

S

• RAISING FULL-YEAR PRODUCTION

GUIDANCE BY 5%

• 160 -165 MBOE/D

• RAISING FULL-YEAR OIL PRODUCTION

GUIDANCE BY 4%

• 101 -103 MBBL/D

2019 PRODUCTION GUIDANCE

MB

BL/

D

Note: Land funded with sales proceeds, excluded from FY capital guidance of $1.1-1.275B

• AS PLANNED, 55% OF FULL-YEAR

CAPITAL SPENT IN 1H 2019

• REITERATING FULL-YEAR CAPITAL

GUIDANCE

• $1,100 - $1,275MM

2019 CAPITAL GUIDANCE2019 CAPITAL GUIDANCE BY QUARTER

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

1QA 2QA 3QE 4QE

D&C Infrastructure Land Other Capex Range Guidance

$M

M

Oil Oil Range Guidance First Sales

11

2Q 2019 Results

2Q YTD

2019 2018 2019 2018

Average Daily Production

Oil (Mbbl/d) 97.9 80.8 97.0 73.3

Gas (MMcf/d) 205.9 152.2 204.1 142.3

NGLs (Mbbl/d) 27.4 18.8 26.4 16.9

Equivalent (MBOE/d) 159.6 125.0 157.4 113.9

Adjusted EBITDAX $ 339 $ 287 $ 651 $ 487

Adjusted Net Income (Loss) from Continuing Operations $ 37 $ 23 $ 59 $ 0

Capital Expenditures $ 341 $ 355 $ 766 $ 705

Note: Adjusted EBITDAX and adjusted net income are non-GAAP measures. A reconciliation to relevant GAAP measures is provided in this presentation.

21% GROWTH IN OIL VOLUMES 2Q’19 vs. 2Q’18

GROWTH IN ADJ. EBITDAX 2Q’19 vs. 2Q’18

18%

Positioned for Sustainable Value Creation

12

OUR DRIVE

OUR FOCUS

OUR PORTFOLIOPERMIAN - WILLISTON - MIDSTREAM

FINANCIAL DISCIPLINE - OIL GROWTH - VALUE CREATION

STRONG EXECUTION - CREATE OPPORTUNITIES - REMAIN DISCIPLINED

APPENDIX

2019 Full-Year Guidance

Capital Plan Production FY 2019

Oil Mbbl/d 101 – 103

Natural Gas MMcf/d 205 – 210

NGL Mbbl/d 25 – 27

Total MBOE/d 160 – 165Net Realized Price3 FY 2019

NGL – % of WTI 20% – 25%

Avg. Price Differentials2 FY 2019

Oil – WTI per barrel ($2.00) – ($3.00)

NYMEX – Nat. Gas (Mcf) ($1.25) – ($1.75)

1. Land capital is funded with proceeds from asset sales in 2019.2. Average price differentials for oil and natural gas exclude hedges, but include basis differential and revenue adjustments.3. Percentage of realized price ranges for NGLs excludes hedges, but includes basis differential and revenue adjustments.4. Rate does not reflect any potential valuation allowance or other adjustments to deferred tax assets.

Expenses FY 2019

$ per BOE

Lease & Facility Operating $6.10 – $6.30

GP&T $3.00 – $3.50

DD&A $15.00 – $16.00

G&A – Cash $2.40 – $2.60

G&A – Non-Cash $0.60 – $0.70

Exploration $1.25 – $1.50

Interest Expense $2.55 – $2.65

Production Tax 7% – 9%

Tax Provision4 21% – 25%

Capital Plan ($ in Millions) FY 2019

D&C / Facilities Capital $1,000 – $1,100

D&C Non-Operated $50 – $75

Midstream Opportunities $50 – $100

Total Development Capital $1,100 – $1,275

Land Capital1 $100

14

15

Domestic Price Realization for 2019

1. Natural gas revenue adjustments are primarily related to field compression fuel. NGL revenue adjustments include T&F and revenue sharing. Gathering deductions represent $(.25) of the oil revenue

adjustments.

2 .“Net Price” equals income statement product revenues by commodity, divided by volume.

3 .Represents the realized settlement on derivatives that occurred during each quarter.

Oil ($/bbl) Gas ($/Mcf) NGL ($/bbl)

1Q ’19 2Q’19 3Q’19 4Q ’19 1Q ’19 2Q’19 3Q’19 4Q ’19 1Q ’19 2Q’19 3Q’19 4Q ’19

Weighted-Average Sales

Price$52.35 $57.50 $2.60 $1.74 $16.81 $13.66

Revenue Adjustments1 $(0.43) $(0.08) $(1.24) $(0.86) $(2.34) $(1.45)

Net Price2 $51.92 $57.42 $1.36 $0.88 $14.47 $12.21

Realized Portion of

Derivatives3 $0.04 $(2.98) $0.42 $0.88

Net Price Including

Derivatives$51.96 $54.44 $1.78 $1.76 $14.47 $12.21

WPX Hedges Updated: August 5, 2019

1 In addition to several crude oil swaps, WPX entered into calendar monthly average(CMA) NYMEX roll swaps which provide pricing adjustments to the trade month versus the delivery month

for contract pricing. 16

Jul – Dec 2019 2020 2021

Volume/Day Average Price Volume/Day Average Price Volume/Day Average Price

Crude Oil (bbl)

Fixed Price Swaps1 60,500 $55.29 40,000 $57.48 - -

Fixed Price Calls 5,000 $54.08 - - - -

Fixed Price Collars 8,000 $50.00 - $60.19 20,000 $53.33 - $63.48 - -

Crude Oil Basis (bbl)

Midland Basis Swaps 22,000 ($1.37) 7,486 ($1.31) - -

Magellan East Houston 1,663 $4.63 - - - -

Magellan East Houston vs. Midland Swaps 5,652 $6.47 - - - -

Magellan East Houston vs. Argus LLS WTI 1,663 $0.75 - - - -

Argus LLS WTI vs. Midland WTI Swaps 1,663 $8.60 - - - -

Clearbrook Bakken 8,000 ($3.23) - - - -

Brent/WTI Spread Basis Swaps - - 5,000 $8.36 1,000 $8.00

Natural Gas (MMBtu)

Fixed Price Swaps 110,000 $3.07 - - - -

Natural Gas Basis (MMBtu)

Houston Ship Channel Basis Swaps 30,000 ($0.09) - - - -

Permian Basis Swaps 25,000 ($0.39) - - - -

West Texas Waha Basis Swaps 15,000 $2.94 60,000 ($0.79) 70,000 ($0.59)

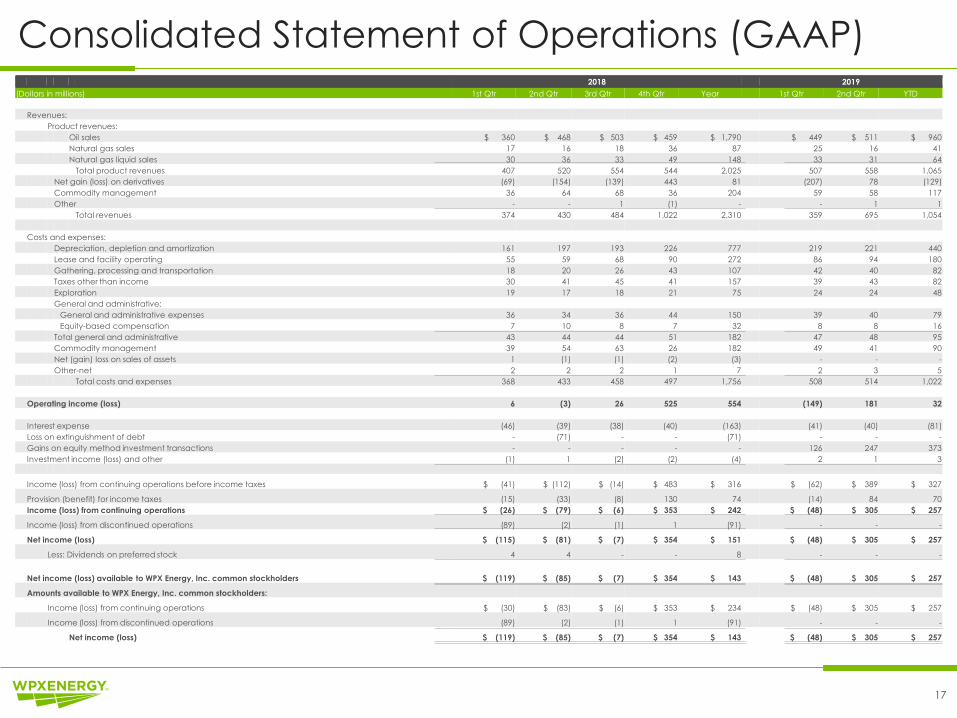

2018 2019

(Dollars in millions) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr YTD

Revenues:

Product revenues:

Oil sales $ 360 $ 468 $ 503 $ 459 $ 1,790 $ 449 $ 511 $ 960

Natural gas sales 17 16 18 36 87 25 16 41

Natural gas liquid sales 30 36 33 49 148 33 31 64

Total product revenues 407 520 554 544 2,025 507 558 1,065

Net gain (loss) on derivatives (69) (154) (139) 443 81 (207) 78 (129)

Commodity management 36 64 68 36 204 59 58 117

Other - - 1 (1) - - 1 1

Total revenues 374 430 484 1,022 2,310 359 695 1,054

Costs and expenses:

Depreciation, depletion and amortization 161 197 193 226 777 219 221 440

Lease and facility operating 55 59 68 90 272 86 94 180

Gathering, processing and transportation 18 20 26 43 107 42 40 82

Taxes other than income 30 41 45 41 157 39 43 82

Exploration 19 17 18 21 75 24 24 48

General and administrative:

General and administrative expenses 36 34 36 44 150 39 40 79

Equity-based compensation 7 10 8 7 32 8 8 16

Total general and administrative 43 44 44 51 182 47 48 95

Commodity management 39 54 63 26 182 49 41 90

Net (gain) loss on sales of assets 1 (1) (1) (2) (3) - - -

Other-net 2 2 2 1 7 2 3 5

Total costs and expenses 368 433 458 497 1,756 508 514 1,022

Operating income (loss) 6 (3) 26 525 554 (149) 181 32

Interest expense (46) (39) (38) (40) (163) (41) (40) (81)

Loss on extinguishment of debt - (71) - - (71) - - -

Gains on equity method investment transactions - - - - - 126 247 373

Investment income (loss) and other (1) 1 (2) (2) (4) 2 1 3

Income (loss) from continuing operations before income taxes $ (41) $ (112) $ (14) $ 483 $ 316 $ (62) $ 389 $ 327

Provision (benefit) for income taxes (15) (33) (8) 130 74 (14) 84 70

Income (loss) from continuing operations $ (26) $ (79) $ (6) $ 353 $ 242 $ (48) $ 305 $ 257

Income (loss) from discontinued operations (89) (2) (1) 1 (91) - - -

Net income (loss) $ (115) $ (81) $ (7) $ 354 $ 151 $ (48) $ 305 $ 257

Less: Dividends on preferred stock 4 4 - - 8 - - -

Net income (loss) available to WPX Energy, Inc. common stockholders $ (119) $ (85) $ (7) $ 354 $ 143 $ (48) $ 305 $ 257

Amounts available to WPX Energy, Inc. common stockholders:

Income (loss) from continuing operations $ (30) $ (83) $ (6) $ 353 $ 234 $ (48) $ 305 $ 257

Income (loss) from discontinued operations (89) (2) (1) 1 (91) - - -

Net income (loss) $ (119) $ (85) $ (7) $ 354 $ 143 $ (48) $ 305 $ 257

Consolidated Statement of Operations (GAAP)

17

2018 2019

(Dollars in millions, except per share amounts) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr YTD

Reconciliation of adjusted income (loss) from continuing operations available to common stockholders:

Income (loss) from continuing operations available to WPX Energy, Inc. common stockholders - reported $ (30) $ (83) $ (6) $ 353 $ 234 $ (48) $ 305 $ 257

Pre-tax adjustments:

Net (gains) losses on sales of assets and equity method investment transactions $ 1 $ (1) $ (1) $ (2) $ (3) $ (126) $ (247) $ (373)

Loss on extinguishment of debt $ - $ 71 $ - $ - $ 71 $ - $ - $ -

Net (gain) loss on derivatives $ 69 $ 154 $ 139 $ (443) $ (81) $ 207 $ (78) $ 129

Net cash received (paid) related to settlement of derivatives $ (55) $ (78) $ (85) $ (19) $ (237) $ 9 $ (10) $ (1)

Total pre-tax adjustments $ 15 $ 146 $ 53 $ (464) $ (250) $ 90 $ (335) $ (245)

Less tax effect for above items $ (3) $ (33) $ (13) $ 107 $ 58 $ (20) $ 76 $ 56

Impact of state deferred tax rate change $ (4) $ - $ - $ (1) $ (5) $ - $ - $ -

Impact of tax valuation allowance (annual effective tax rate method) $ - $ - $ - $ 2 $ 2 $ 1 $ (9) $ (8)

Impact of state related adjustment $ - $ - $ - $ - $ - $ (1) $ - $ (1)

Adjustment for estimated annual effective tax rate method $ - $ (7) $ (5) $ 12 $ - $ - $ - $ -

Total adjustments, after tax $ 8 $ 106 $ 35 $ (344) $ (195) $ 70 $ (268) $ (198)

Adjusted income (loss) from continuing operations availableto common stockholders $ (22) $ 23 $ 29 $ 9 $ 39 $ 22 $ 37 $ 59

Reconciliation-Adjusted Income (Loss) from Continuing Operations (Non-GAAP)

18

Reconciliation – Adjusted Diluted Income (Loss) Per Common Share

19

1. Per share impact is based on adjusted diluted weighted average shares.

2018 2019

(Dollars in millions, except per share amounts) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr YTD

Reconciliation of adjusted diluted income (loss) per common share:

Income (loss) from continuing operations - diluted earnings per share - reported $ (0.07) $ (0.21) $ (0.01) $ 0.83 $ 0.57 $ (0.11) $ 0.72 $ 0.61

Impact of adjusted diluted weighted-average shares $ - $ 0.01 $ - $ - $ - $ - $ - $ -

Pretax adjustments (1):

Net (gains) losses on sales of assets and equity method investment transactions $ - $ - $ - $ - $ (0.01) $ (0.30) $ (0.58) $ (0.88)

Loss on extinguishment of debt $ - $ 0.18 $ - $ - $ 0.17 $ - $ - $ -

Net (gain) loss on derivatives $ 0.17 $ 0.38 $ 0.33 $ (1.04) $ (0.20) $ 0.49 $ (0.19) $ 0.30

Net cash received (paid) related to settlement of derivatives $ (0.13) $ (0.20) $ (0.20) $ (0.06) $ (0.57) $ 0.02 $ (0.02) $ -

Total pretax adjustments $ 0.04 $ 0.36 $ 0.13 $ (1.10) $ (0.61) $ 0.21 $ (0.79) $ (0.58)

Less tax effect for above items $ (0.02) $ (0.08) $ (0.04) $ 0.26 $ 0.14 $ (0.05) $ 0.18 $ 0.13

Impact of state tax rate change $ (0.01) $ - $ - $ - $ (0.01) $ - $ - $ -

Impact of tax valuation allowance (annual effective tax rate method) $ - $ - $ - $ - $ - $ - $ (0.02) $ (0.02)

Impact of state related adjustment $ - $ - $ - $ - $ - $ - $ - $ -

Adjustment for estimated annual effective tax rate method $ - $ (0.02) $ (0.01) $ 0.03 $ - $ - $ - $ -

Total adjustments, after-tax $ 0.01 $ 0.26 $ 0.08 $ (0.81) $ (0.48) $ 0.16 $ (0.63) $ (0.47)

Adjusted diluted income (loss) per common share $ (0.06) $ 0.06 $ 0.07 $ 0.02 $ 0.09 $ 0.05 $ 0.09 $ 0.14

Reported diluted weighted-average shares (millions) 398.6 400.0 414.0 424.0 411.7 421.0 423.5 423.6

Effect of dilutive securities due to adjusted income (loss) from continuing operations available to common stockholders - 3.1 3.7 - - 2.6 - -

Adjusted diluted weighted-average shares (millions) 398.6 403.1 417.7 424.0 411.7 423.6 423.5 423.6

2018 2019

(Dollars in millions, except per share amounts) 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Year 1st Qtr 2nd Qtr YTD

Reconciliation of Adjusted EBITDAX

Net income (loss) - reported $ (115) $ (81) $ (7) $ 354 $ 151 $ (48) $ 305 $ 257

Interest expense 46 39 38 40 163 41 40 81

Provision (benefit) for income taxes (15) (33) (8) 130 74 (14) 84 70

Depreciation, depletion and amortization 161 197 193 226 777 219 221 440

Exploration expenses 19 17 18 21 75 24 24 48

EBITDAX 96 139 234 771 1,240 222 674 896

Net (gains) losses on sales of assets and equity method investment transactions 1 (1) (1) (2) (3) (126) (247) (373)

Loss on extinguishment of debt - 71 - - 71 - - -

Net (gain) loss on derivatives 69 154 139 (443) (81) 207 (78) 129

Net cash received (paid) related to settlement of derivatives (55) (78) (85) (19) (237) 9 (10) (1)

(Income) loss from discontinued operations 89 2 1 (1) 91 - - -

Adjusted EBITDAX $ 200 $ 287 $ 288 $ 306 $ 1,081 $ 312 $ 339 $ 651

Reconciliation – Adjusted EBITDAX (Non-GAAP)

20

Disclaimers

The information contained in this summary has been prepared to assist you in making your own evaluation of the Company and does not purport to contain all of the information you may consider

important in deciding whether to invest in shares of the Company’s common stock. In all cases, it is your obligation to conduct your own due diligence. All information contained herein, including any

estimates or projections, is based upon information provided by the Company. Any estimates or projections with respect to future performance have been provided to assist you in your evaluation but

should not be relied upon as an accurate representation of future results. No persons have been authorized to make any representations other than those contained in this summary, and if given or made,

such representations should not be considered as authorized.

Certain statements, estimates and financial information contained in this summary constitute forward-looking statements or information. Such forward-looking statements or information involve known and

unknown risks and uncertainties that could cause actual events or results to differ materially from the results implied or expressed in such forward-looking statements or information. While presented with

numerical specificity, certain forward-looking statements or information are based (1) upon assumptions that are inherently subject to significant business, economic, regulatory, environmental, seasonal,

competitive uncertainties, contingencies and risks including, without limitation, the ability to obtain debt and equity financings, capital costs, construction costs, well production performance, operating

costs, commodity pricing, differentials, royalty structures, field upgrading technology, and other known and unknown risks, all of which are difficult to predict and many of which are beyond the

Company's control, and (2) upon assumptions with respect to future business decisions that are subject to change.

There can be no assurance that the results implied or expressed in such forward-looking statements or information or the underlying assumptions will be realized and that actual results of operations or

future events will not be materially different from the results implied or expressed in such forward-looking statements or information. Under no circumstances should the inclusion of the forward-looking

statements or information be regarded as a representation, undertaking, warranty or prediction by the Company or any other person with respect to the accuracy thereof or the accuracy of the

underlying assumptions, or that the Company will achieve or is likely to achieve any particular results. The forward-looking statements or information are made as of the date hereof and the Company

disclaims any intent or obligation to update publicly or to revise any of the forward-looking statements or information, whether as a result of new information, future events or otherwise. Recipients are

cautioned that forward-looking statements or information are not guarantees of future performance and, accordingly, recipients are expressly cautioned not to put undue reliance on forward-looking

statements or information due to the inherent uncertainty therein.

21

The SEC requires oil and gas companies, in filings made with the SEC, to disclose proved reserves, which are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be

estimated with reasonable certainty to be economically producible – from a given date forward, from known reservoirs, under existing economic conditions, operating methods, and governmental

regulations. The SEC permits the optional disclosure of probable and possible reserves. We have elected to use in this presentation “probable” reserves and “possible” reserves, excluding their valuation.

The SEC defines “probable” reserves as “those additional reserves that are less certain to be recovered than proved reserves but which, together with proved reserves, are as likely as not to be recovered.”

The SEC defines “possible” reserves as “those additional reserves that are less certain to be recovered than probable reserves.” The Company has applied these definitions in estimating probable and

possible reserves. Statements of reserves are only estimates and may not correspond to the ultimate quantities of oil and gas recovered. Any reserve estimates provided in this presentation that are not

specifically designated as being estimates of proved reserves may include estimated reserves not necessarily calculated in accordance with, or contemplated by, the SEC’s reserves reporting guidelines.

Investors are urged to consider closely the disclosure regarding our business that may be accessed through the SEC’s website at www.sec.gov.

The SEC’s rules prohibit us from filing resource estimates. Our resource estimations include estimates of hydrocarbon quantities for (i) new areas for which we do not have sufficient information to date to

classify as proved, probable or even possible reserves, (ii) other areas to take into account the low level of certainty of recovery of the resources and (iii) uneconomic proved, probable or possible reserves.

Resource estimates do not take into account the certainty of resource recovery and are therefore not indicative of the expected future recovery and should not be relied upon. Resource estimates might

never be recovered and are contingent on exploration success, technical improvements in drilling access, commerciality and other factors.

This presentation may include certain financial measures, including adjusted EBITDAX (earnings before interest, taxes, depreciation, depletion, amortization and exploration expenses), that are non-

GAAP financial measures as defined under the rules of the Securities and Exchange Commission.

This presentation is accompanied by a reconciliation of these non-GAAP financial measures to their nearest GAAP financial measures. Management uses these financial measures because they

are widely accepted financial indicators used by investors to compare a company’s performance. Management believes that these measures provide investors an enhanced perspective of the

operating performance of the company and aid investor understanding. Management also believes that these non-GAAP measures provide useful information regarding our ability to meet future

debt service, capital expenditures and working capital requirements. These non-GAAP financial measures should not be considered in isolation or as substitutes for a measure of performance

prepared in accordance with United States generally accepted accounting principles.

Reserves Disclaimer

WPX Non-GAAP Disclaimer

![Oct 2014 Broadcast Web... · [Web Edition 25-10-2014] Oakwood Church Springwood Road Leeds LS8 2QA Roundhay St John and Roundhay Methodist Thorner Methodist Church Main Street Thorner](https://img.pdfslide.net/doc/110x75/60a827d03d07791210652832/oct-2014-broadcast-web-web-edition-25-10-2014-oakwood-church-springwood-road.jpg)