Embed Size (px)

DESCRIPTION

Overview of RCOM's subsea cable business

Citation preview

PRINTING INSTRUCTIONS

CHECK TOC BEFORE PRINTING

Color/grayscale: Color (regardless of printing in b/w)

Scale to fit paper: OFF

Print hidden slides: OFF

POWERPOINT OPTIONS > ADVANCED > PRINT

Print in background: OFF

CHARTING INSTRUCTIONS

Charts in this book are created… (delete as necessary):

in Excel, pasted as a live object, then brake chart link (delete existing chart before pasting an update from Excel)

in Excel and pasted as a data linked objects (edits made directly on the slide will not be reflected in the

original Excel file)

in Excel and pasted as pictures (source location comments required for file management)

RCOM’s subsea cable business

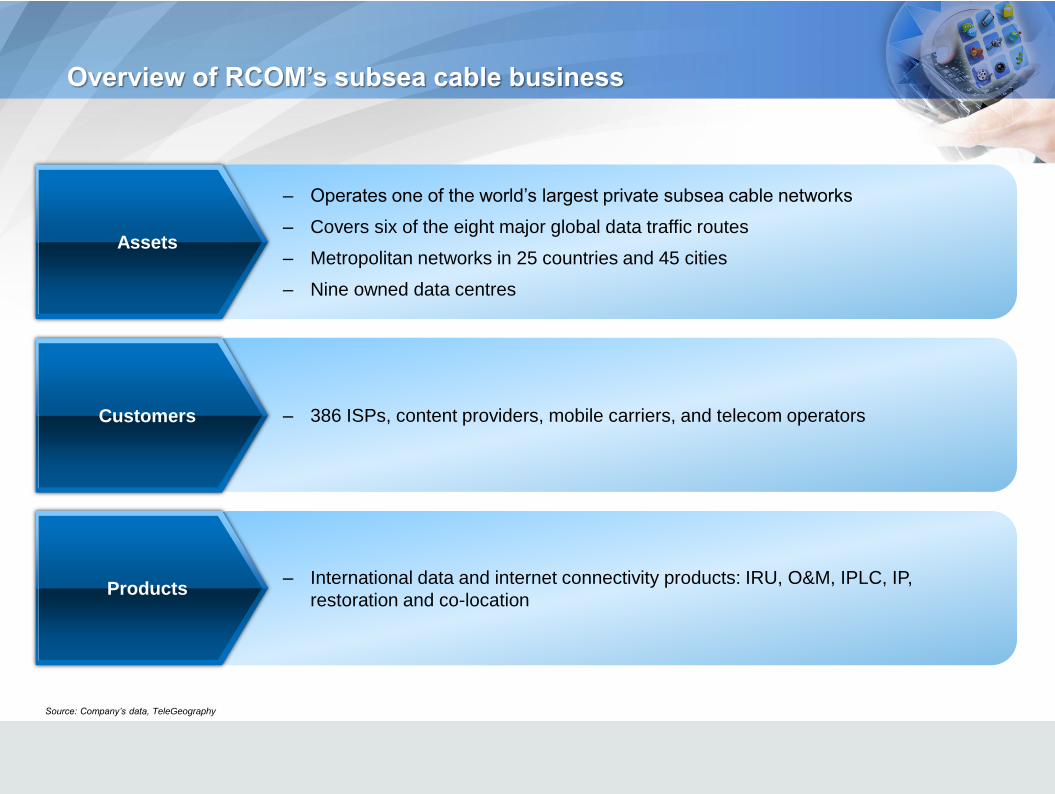

Overview of RCOM’s subsea cable business

Source: Company’s data, TeleGeography

– Operates one of the world’s largest private subsea cable networks

– Covers six of the eight major global data traffic routes

– Metropolitan networks in 25 countries and 45 cities

– Nine owned data centres

– 386 ISPs, content providers, mobile carriers, and telecom operators

– International data and internet connectivity products: IRU, O&M, IPLC, IP,

restoration and co-location

Assets

Customers

Products

Investment highlights

Presence in key markets and global reach

High entry barriers – Cost, Time, Right of Way

Significant available capacity, low incremental upgrade costs, long useful life

High quality network, Global Ethernet enabled – Low latency IP

Strong customer relationships

4x IP traffic growth expected over next 5 years

Contents

Section

1 The Global Telecommunications Infrastructure Industry 1

2 Overview of assets 8

3 Sales & customers 23

The Global Telecommunications Infrastructure Industry

Section 1

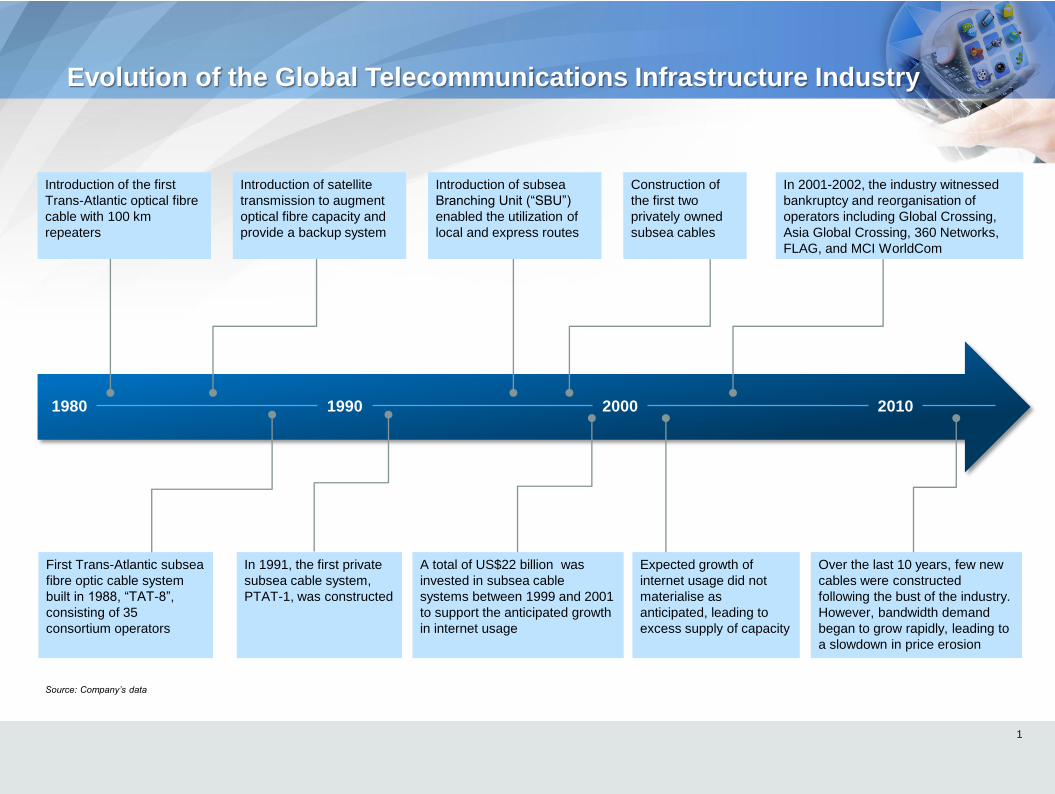

Evolution of the Global Telecommunications Infrastructure Industry

1

1980 1990 2000 2010

Source: Company’s data

Introduction of the first

Trans-Atlantic optical fibre

cable with 100 km

repeaters

Introduction of satellite

transmission to augment

optical fibre capacity and

provide a backup system

Construction of

the first two

privately owned

subsea cables

Introduction of subsea

Branching Unit (“SBU”)

enabled the utilization of

local and express routes

In 2001-2002, the industry witnessed

bankruptcy and reorganisation of

operators including Global Crossing,

Asia Global Crossing, 360 Networks,

FLAG, and MCI WorldCom

Expected growth of

internet usage did not

materialise as

anticipated, leading to

excess supply of capacity

A total of US$22 billion was

invested in subsea cable

systems between 1999 and 2001

to support the anticipated growth

in internet usage

Over the last 10 years, few new

cables were constructed

following the bust of the industry.

However, bandwidth demand

began to grow rapidly, leading to

a slowdown in price erosion

First Trans-Atlantic subsea

fibre optic cable system

built in 1988, “TAT-8”,

consisting of 35

consortium operators

In 1991, the first private

subsea cable system,

PTAT-1, was constructed

Source: Company’s data

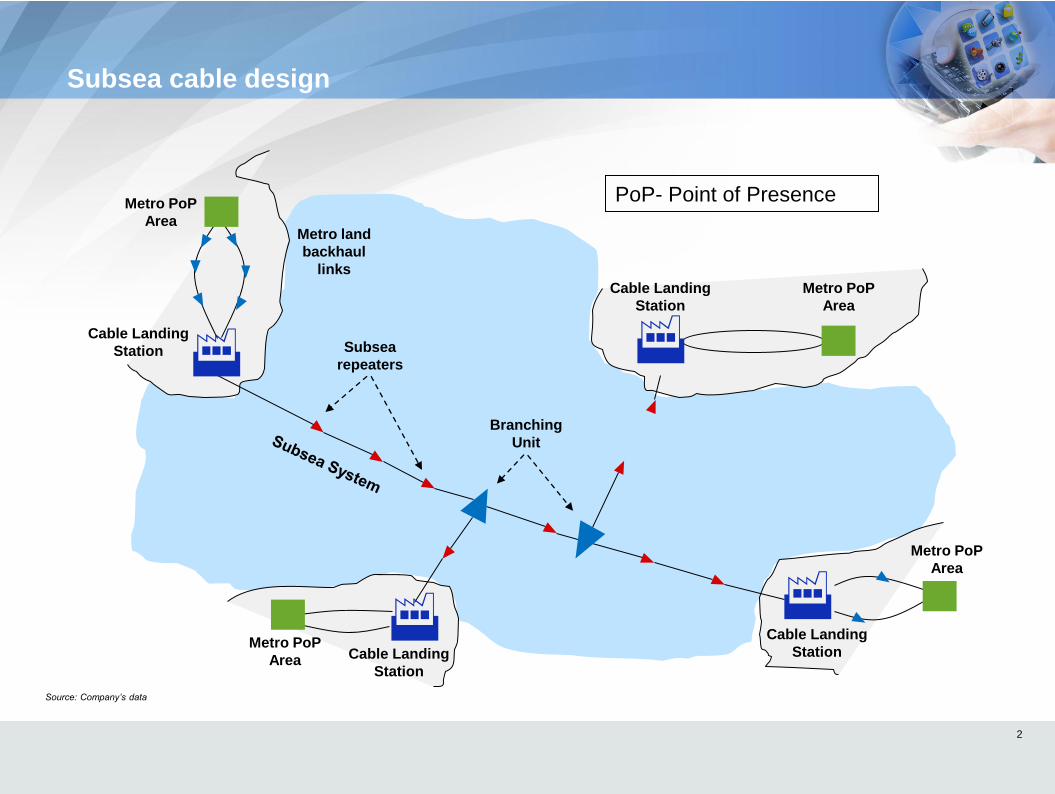

Subsea cable design

2

PoP- Point of Presence

Cable Landing

Station

Cable Landing

Station

Cable Landing

Station

Metro PoP

Area

Metro PoP

Area

Metro PoP

Area

Metro PoP

Area

Branching

Unit

Subsea

repeaters

Metro land

backhaul

links

Cable Landing

Station

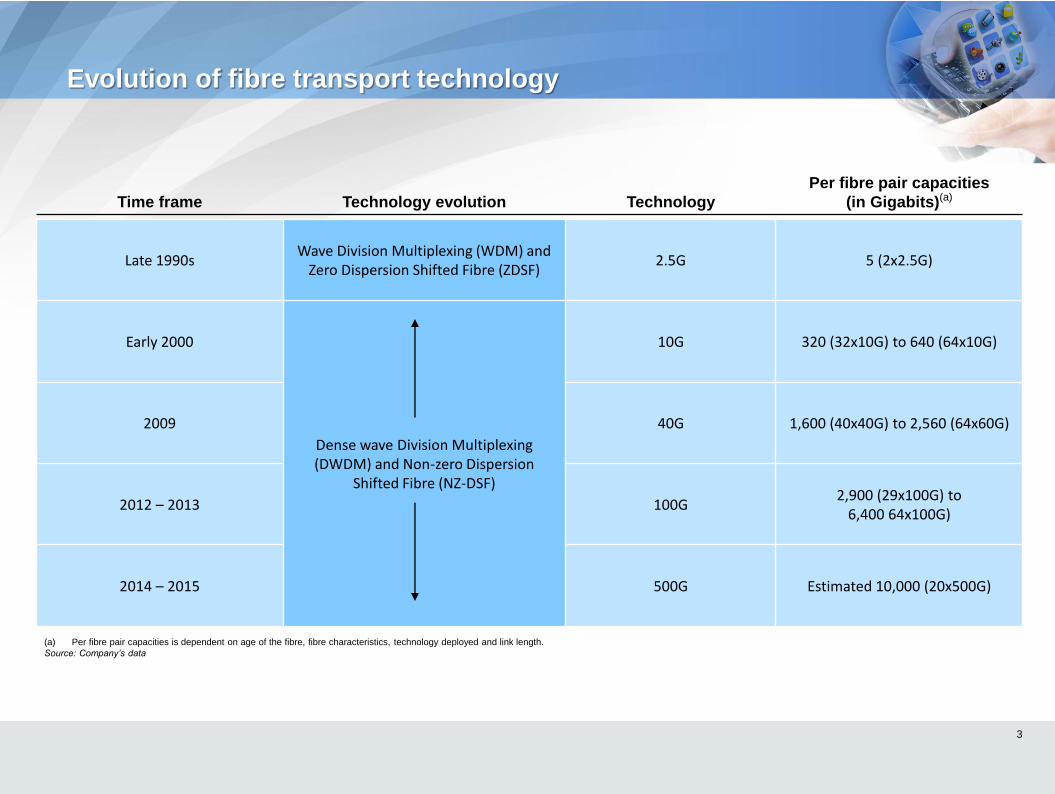

(a) Per fibre pair capacities is dependent on age of the fibre, fibre characteristics, technology deployed and link length.

Source: Company’s data

Evolution of fibre transport technology

Time frame Technology evolution Technology

Per fibre pair capacities

(in Gigabits)(a)

Late 1990s Wave Division Multiplexing (WDM) and

Zero Dispersion Shifted Fibre (ZDSF) 2.5G 5 (2x2.5G)

Early 2000

Dense wave Division Multiplexing (DWDM) and Non-zero Dispersion

Shifted Fibre (NZ-DSF)

10G 320 (32x10G) to 640 (64x10G)

2009 40G 1,600 (40x40G) to 2,560 (64x60G)

2012 – 2013 100G 2,900 (29x100G) to

6,400 64x100G)

2014 – 2015 500G Estimated 10,000 (20x500G)

3

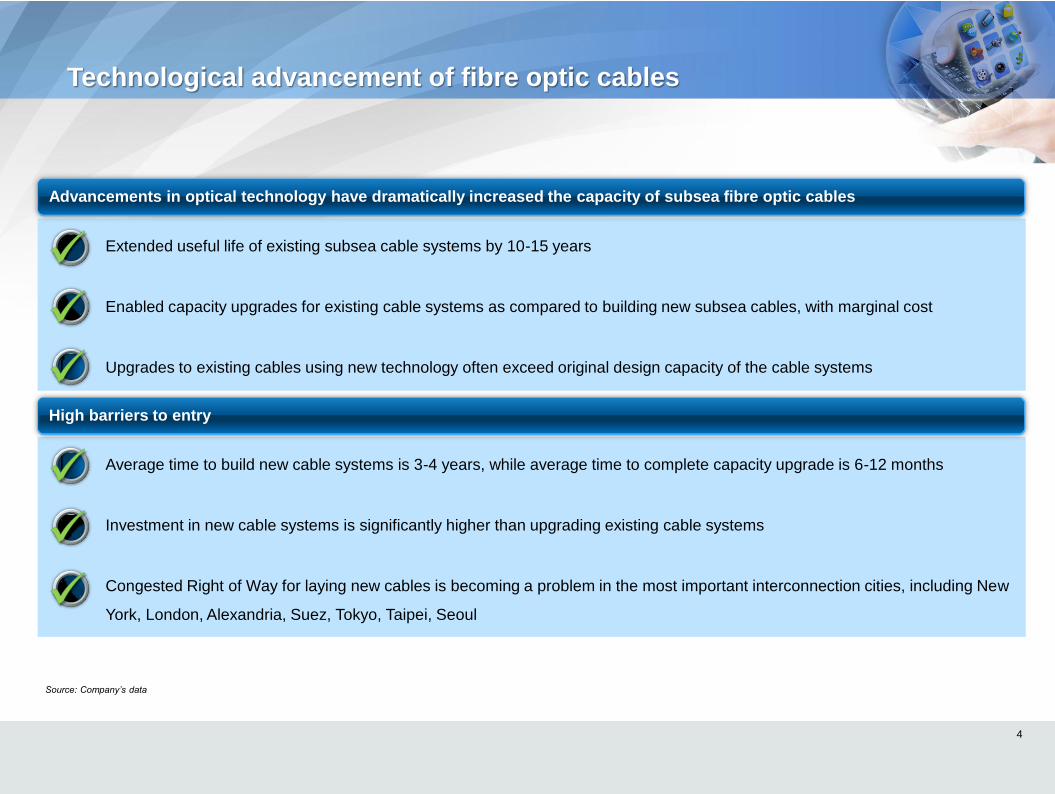

Extended useful life of existing subsea cable systems by 10-15 years

Enabled capacity upgrades for existing cable systems as compared to building new subsea cables, with marginal cost

Upgrades to existing cables using new technology often exceed original design capacity of the cable systems

The capacity upgrades often exceed the original design capacity of the system

Technological advancement of fibre optic cables

4

Source: Company’s data

Average time to build new cable systems is 3-4 years, while average time to complete capacity upgrade is 6-12 months

Investment in new cable systems is significantly higher than upgrading existing cable systems

Congested Right of Way for laying new cables is becoming a problem in the most important interconnection cities, including New

York, London, Alexandria, Suez, Tokyo, Taipei, Seoul

Advancements in optical technology have dramatically increased the capacity of subsea fibre optic cables

High barriers to entry

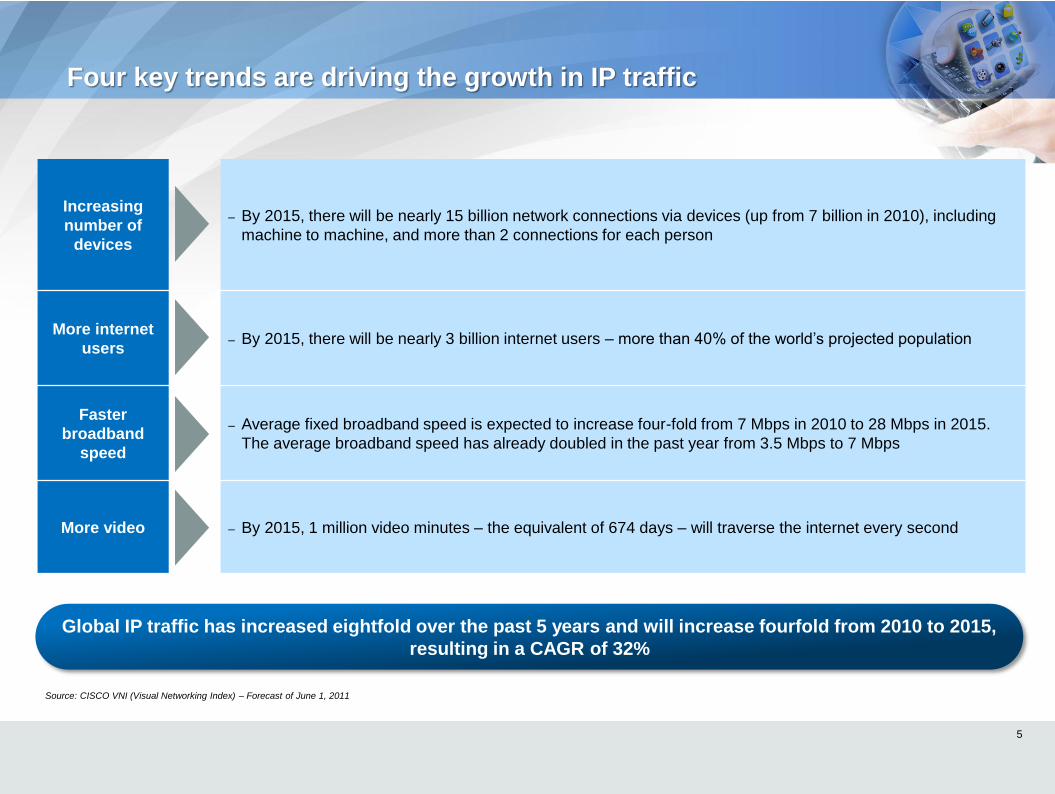

Four key trends are driving the growth in IP traffic

5

Global IP traffic has increased eightfold over the past 5 years and will increase fourfold from 2010 to 2015,

resulting in a CAGR of 32%

Increasing

number of

devices

– By 2015, there will be nearly 15 billion network connections via devices (up from 7 billion in 2010), including

machine to machine, and more than 2 connections for each person

More internet

users – By 2015, there will be nearly 3 billion internet users – more than 40% of the world’s projected population

Faster

broadband

speed

– Average fixed broadband speed is expected to increase four-fold from 7 Mbps in 2010 to 28 Mbps in 2015.

The average broadband speed has already doubled in the past year from 3.5 Mbps to 7 Mbps

More video – By 2015, 1 million video minutes – the equivalent of 674 days – will traverse the internet every second

Source: CISCO VNI (Visual Networking Index) – Forecast of June 1, 2011

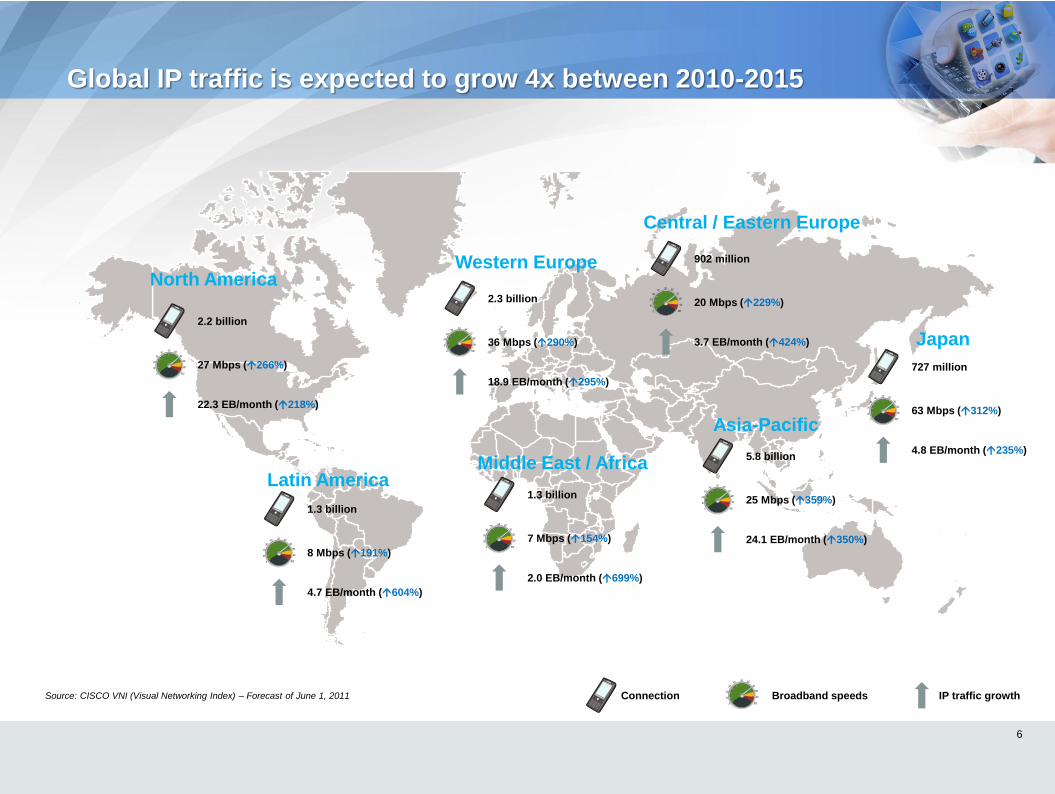

Global IP traffic is expected to grow 4x between 2010-2015

Japan

Asia-Pacific

Middle East / Africa

Central / Eastern Europe

Western Europe

Latin America

North America

2.2 billion

27 Mbps (266%)

22.3 EB/month (218%)

1.3 billion

8 Mbps (191%)

4.7 EB/month (604%)

1.3 billion

7 Mbps (154%)

2.0 EB/month (699%)

5.8 billion

25 Mbps (359%)

24.1 EB/month (350%)

727 million

63 Mbps (312%)

4.8 EB/month (235%)

902 million

20 Mbps (229%)

3.7 EB/month (424%)

2.3 billion

36 Mbps (290%)

18.9 EB/month (295%)

Connection IP traffic growth Broadband speeds

6

Source: CISCO VNI (Visual Networking Index) – Forecast of June 1, 2011

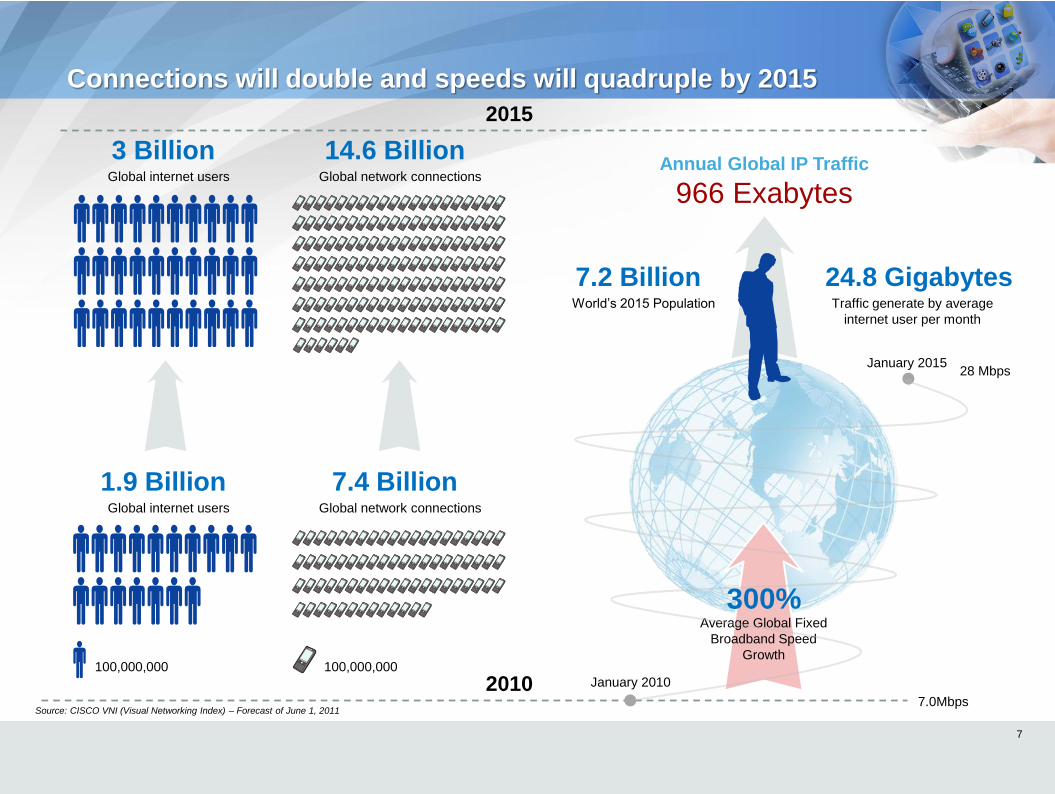

Connections will double and speeds will quadruple by 2015

3 Billion Global internet users

14.6 Billion Global network connections

1.9 Billion Global internet users

7.4 Billion Global network connections

100,000,000 100,000,000

Annual Global IP Traffic

966 Exabytes

7.2 Billion World’s 2015 Population

2015

28 Mbps

300% Average Global Fixed

Broadband Speed

Growth

7.0Mbps 2010 January 2010

January 2015

24.8 Gigabytes Traffic generate by average

internet user per month

7

Source: CISCO VNI (Visual Networking Index) – Forecast of June 1, 2011

Overview of assets

Section 2

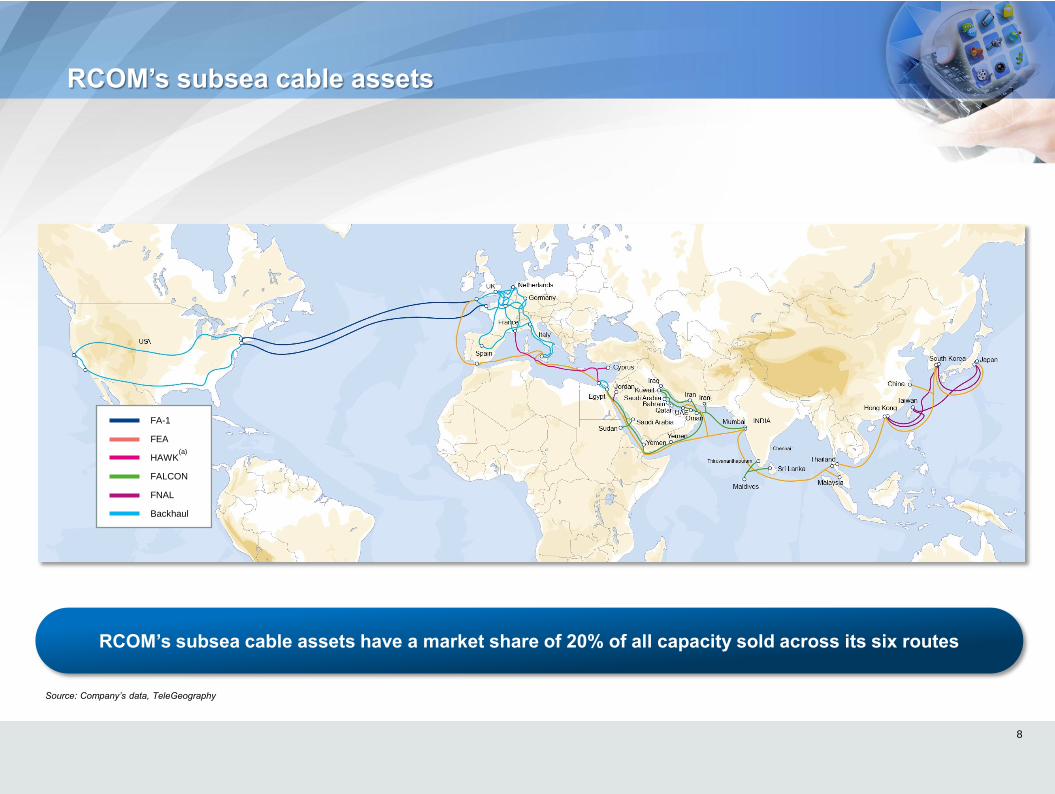

RCOM’s subsea cable assets

8

FA-1

FEA

HAWK

FALCON

FNAL

Backhaul

Source: Company’s data, TeleGeography

RCOM’s subsea cable assets have a market share of 20% of all capacity sold across its six routes

(a)

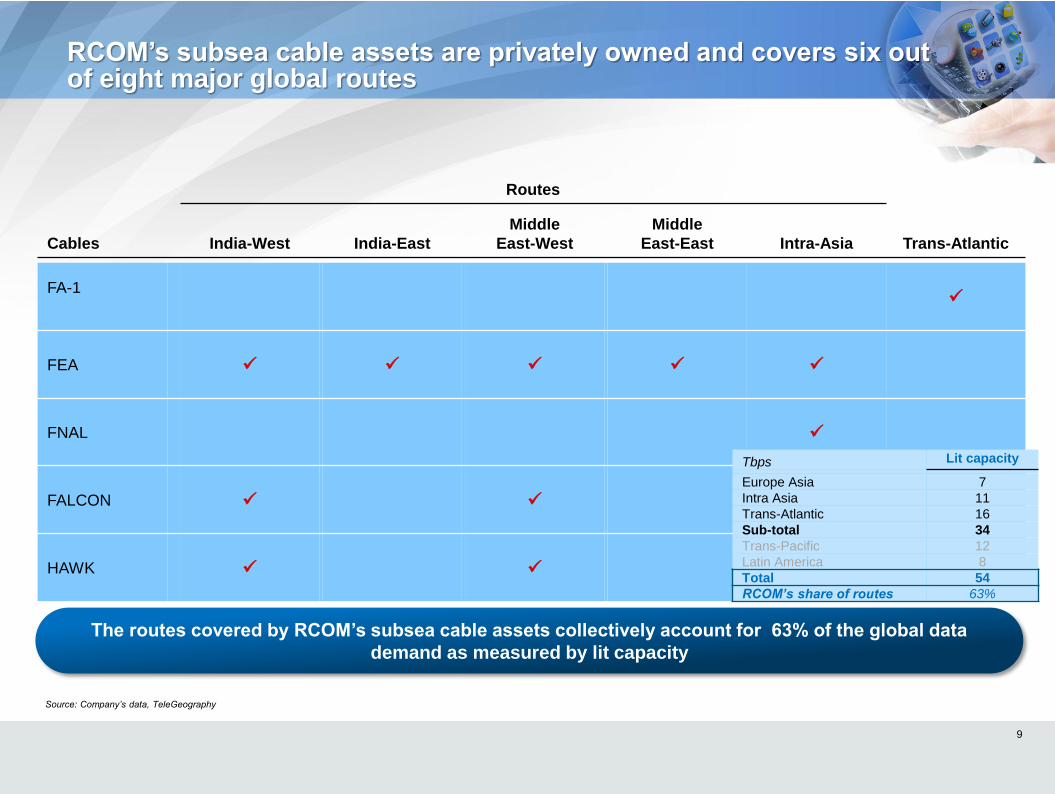

Routes

Cables

India-West India-East

Middle

East-West

Middle

East-East Intra-Asia Trans-Atlantic

FA-1

FEA

FNAL

FALCON

HAWK

RCOM’s subsea cable assets are privately owned and covers six out of eight major global routes

9

Source: Company’s data, TeleGeography

The routes covered by RCOM’s subsea cable assets collectively account for 63% of the global data

demand as measured by lit capacity

Tbps Lit capacity

Europe Asia 7

Intra Asia 11

Trans-Atlantic 16

Sub-total 34

Trans-Pacific 12

Latin America 8

Total 54

RCOM’s share of routes 63%

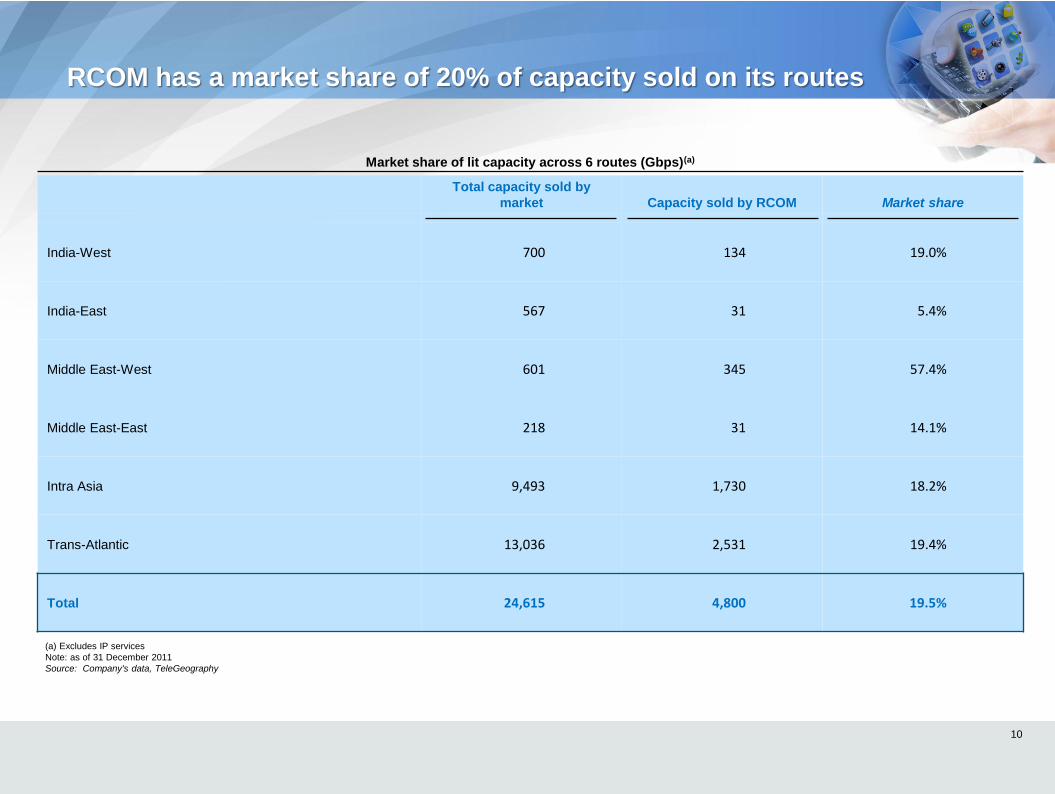

RCOM has a market share of 20% of capacity sold on its routes

Total capacity sold by

market Capacity sold by RCOM Market share

India-West 700 134 19.0%

India-East 567 31 5.4%

Middle East-West 601 345 57.4%

Middle East-East 218 31 14.1%

Intra Asia 9,493 1,730 18.2%

Trans-Atlantic 13,036 2,531 19.4%

Total 24,615 4,800 19.5%

10

(a) Excludes IP services

Note: as of 31 December 2011

Source: Company's data, TeleGeography

Market share of lit capacity across 6 routes (Gbps)(a)

Landing stations at strategic locations

Substantial remaining useful life

Significant saleable capacity

Benefit of cable assets on key routes

Wholly-owned cables with strong regional connectivity

Competitive advantages of RCOM’s cable systems

11

1

2

3

4

5

– Concurrence of all members of the consortium not required for upgrades

– Network changes, routing, and terrestrial backhaul upgrades can be done independently

– Ease of linking new landing stations to existing subsea system

– Easier to adopt new, cutting edge technology i.e. 10G to 40G to 100G

– Simpler to execute strategic deals

– Regional capacity sales, presales of capacity with future pricing

12

Wholly-owned cables with strong regional connectivity

Source: Company’s data

1

Private subsea cable operators have greater flexibility in operating cable systems

No internal price competition as private operators maintain 100% control over its inventory

Benefit of cable assets on key routes

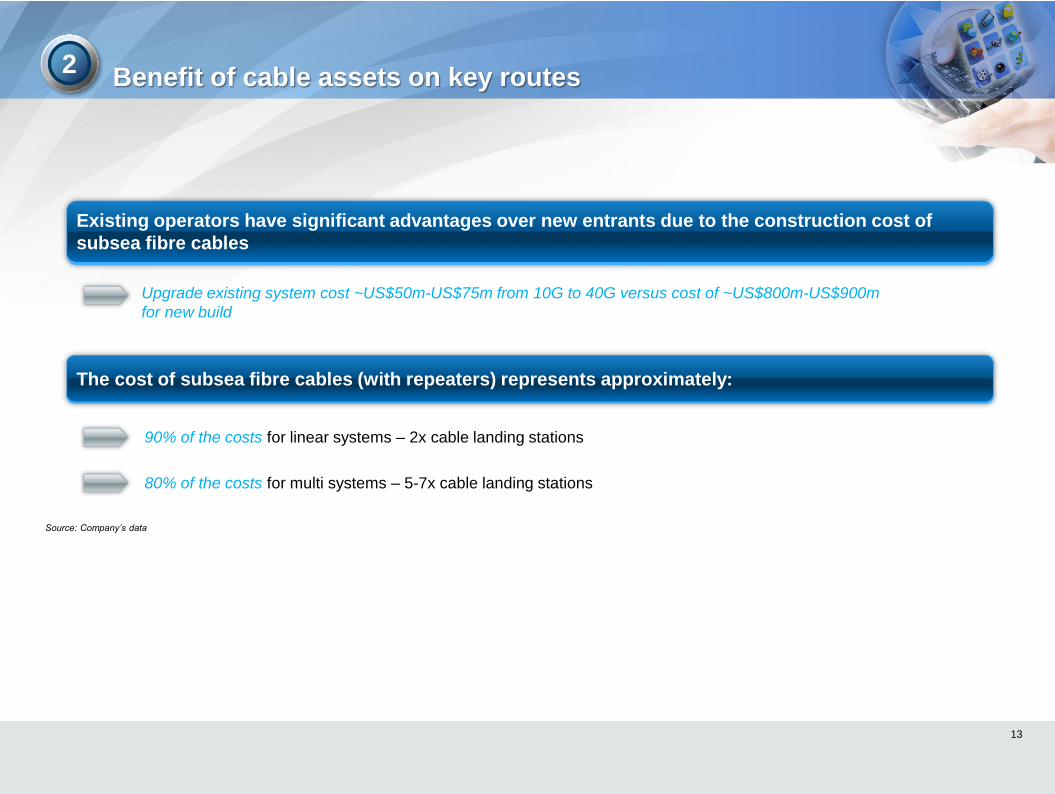

13

2

Existing operators have significant advantages over new entrants due to the construction cost of

subsea fibre cables

The cost of subsea fibre cables (with repeaters) represents approximately:

– 90% of the costs for linear systems – 2x cable landing stations

– 80% of the costs for multi systems – 5-7x cable landing stations

– Upgrade existing system cost ~US$50m-US$75m from 10G to 40G versus cost of ~US$800m-US$900m

for new build

Source: Company’s data

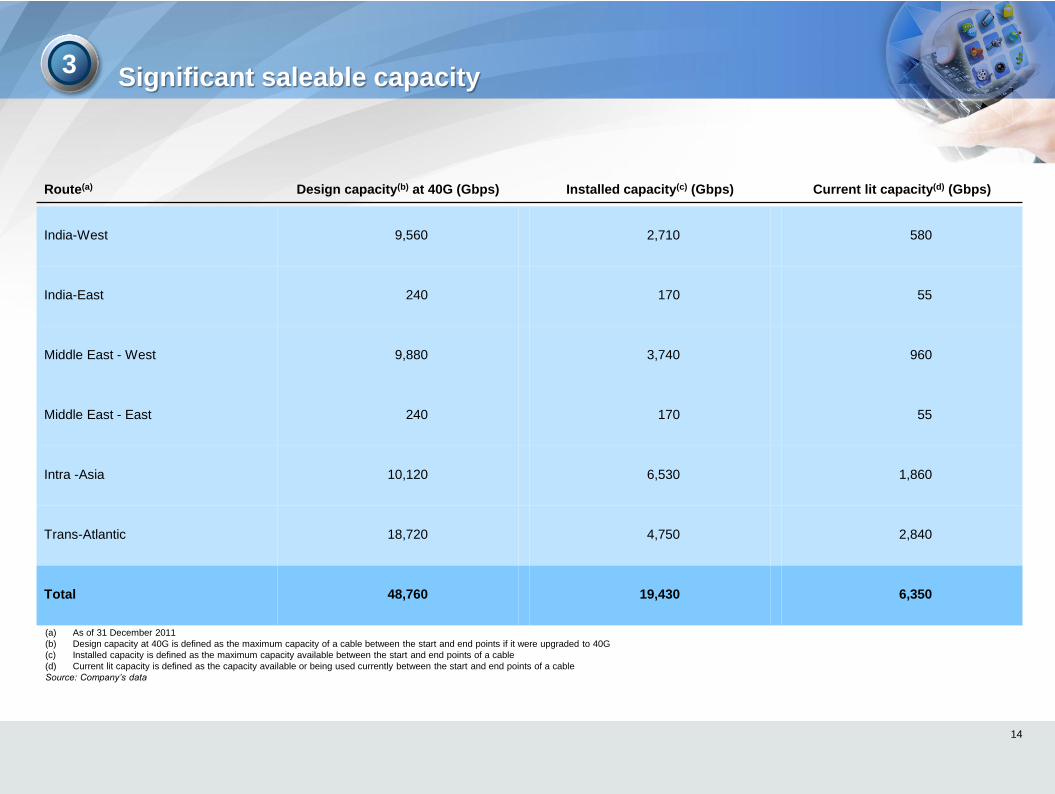

Significant saleable capacity

14

(a) As of 31 December 2011

(b) Design capacity at 40G is defined as the maximum capacity of a cable between the start and end points if it were upgraded to 40G

(c) Installed capacity is defined as the maximum capacity available between the start and end points of a cable

(d) Current lit capacity is defined as the capacity available or being used currently between the start and end points of a cable

Source: Company’s data

Route(a) Design capacity(b) at 40G (Gbps) Installed capacity(c) (Gbps) Current lit capacity(d) (Gbps)

India-West 9,560 2,710 580

India-East 240 170 55

Middle East - West 9,880 3,740 960

Middle East - East 240 170 55

Intra -Asia 10,120 6,530 1,860

Trans-Atlantic 18,720 4,750 2,840

Total 48,760 19,430 6,350

3

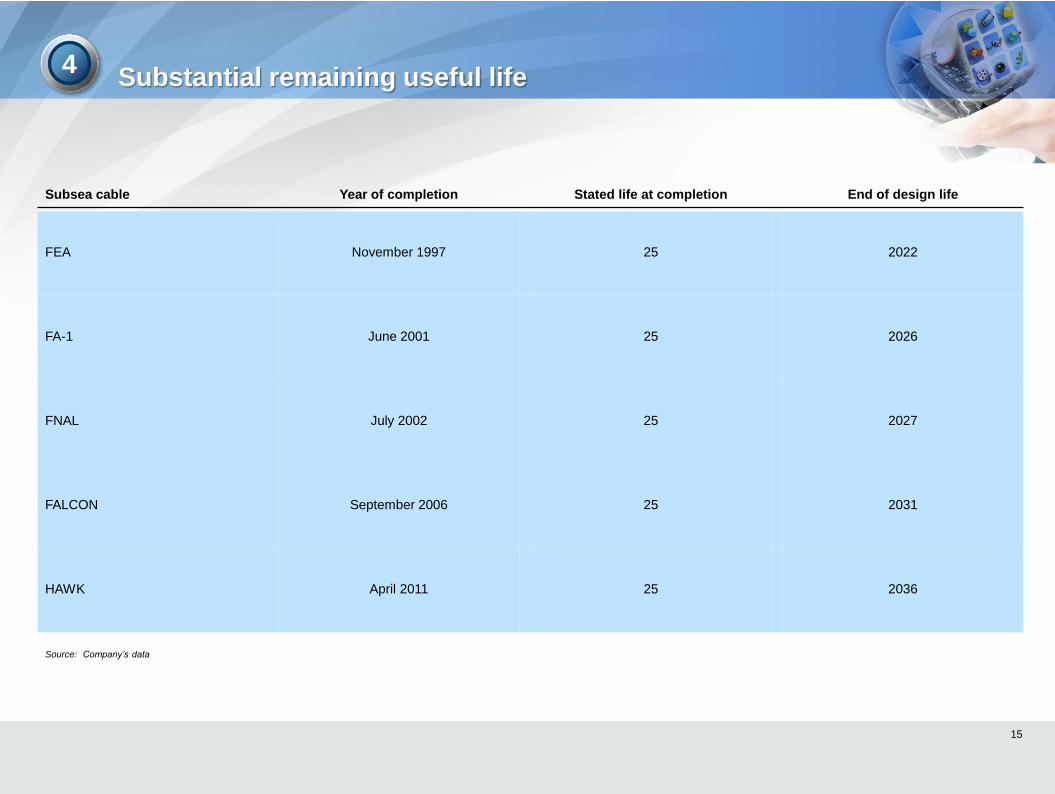

Substantial remaining useful life

15

Subsea cable Year of completion Stated life at completion End of design life

FEA November 1997 25 2022

FA-1 June 2001 25 2026

FNAL July 2002 25 2027

FALCON September 2006 25 2031

HAWK April 2011 25 2036

Source: Company’s data

4

Landing stations at strategic locations

16

5

– China – Qatar

– India – Bahrain

– Japan – Iraq

– Korea – Kuwait

– Malaysia – Yemen

– Thailand – Republic of Maldives

– Egypt – Hong Kong

– UAE – Sri Lanka

– Jordan – France

– Saudi Arabia – Cyprus

– Italy – Iran

– Spain – Sudan

– UK – US

– Taiwan – Oman

A total of 46 landing stations with 31 partners, in the following countries:

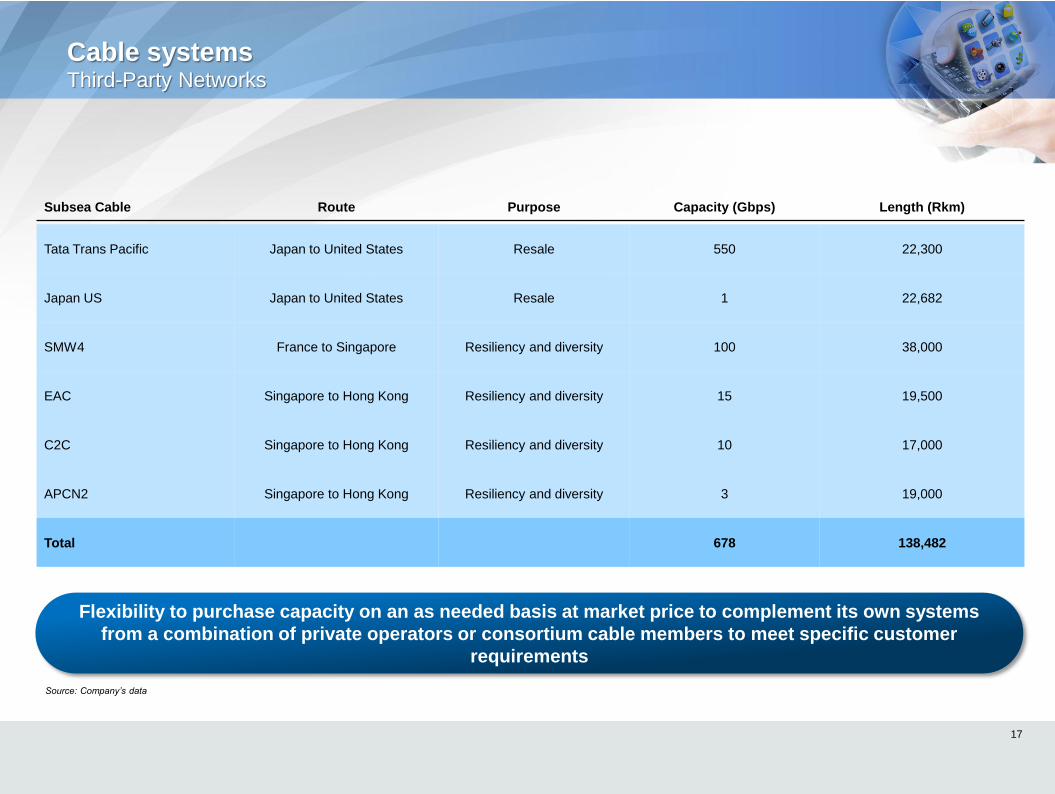

Cable systems Third-Party Networks

17

Subsea Cable Route Purpose Capacity (Gbps) Length (Rkm)

Tata Trans Pacific Japan to United States Resale 550 22,300

Japan US Japan to United States Resale 1 22,682

SMW4 France to Singapore Resiliency and diversity 100 38,000

EAC Singapore to Hong Kong Resiliency and diversity 15 19,500

C2C Singapore to Hong Kong Resiliency and diversity 10 17,000

APCN2 Singapore to Hong Kong Resiliency and diversity 3 19,000

Total 678 138,482

Source: Company’s data

Flexibility to purchase capacity on an as needed basis at market price to complement its own systems

from a combination of private operators or consortium cable members to meet specific customer

requirements

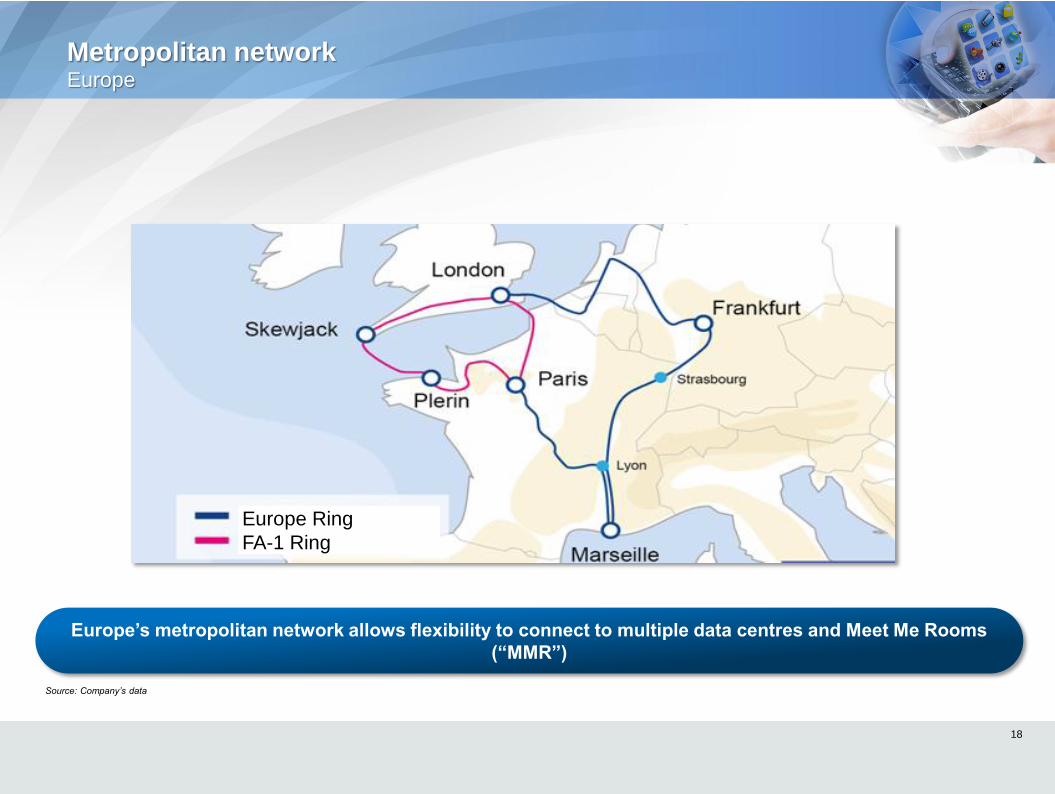

Metropolitan network Europe

18

Source: Company’s data

Europe’s metropolitan network allows flexibility to connect to multiple data centres and Meet Me Rooms

(“MMR”)

Europe Ring

FA-1 Ring

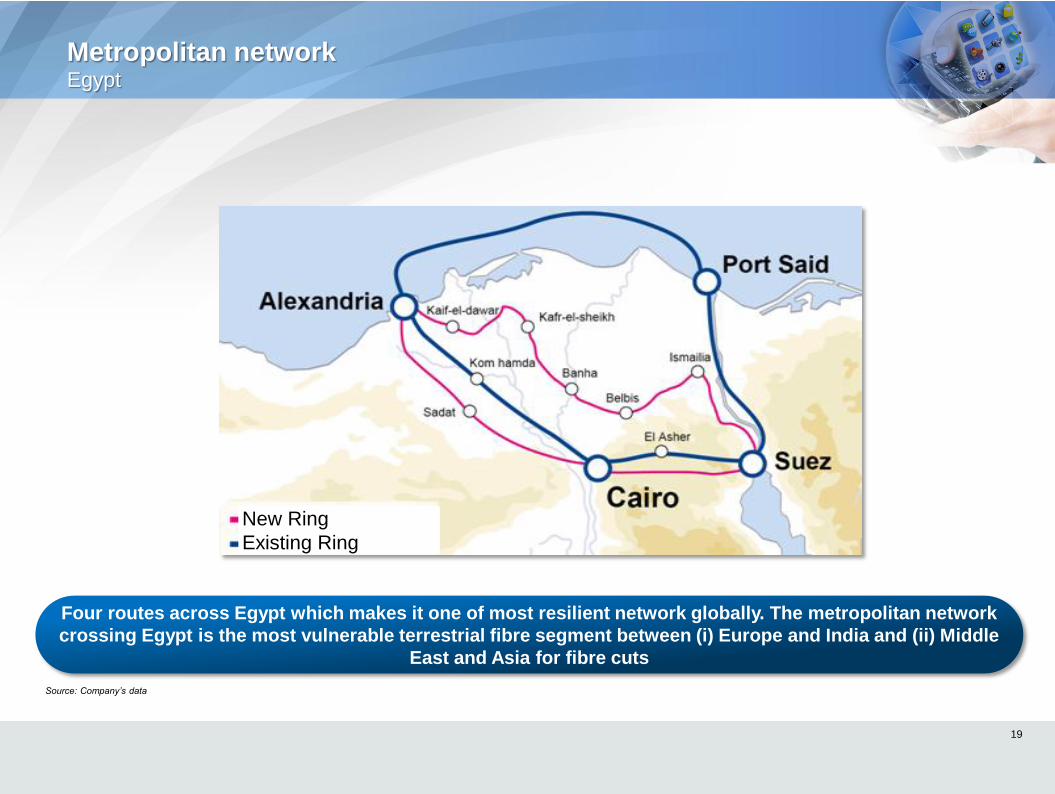

Metropolitan network Egypt

19

Source: Company’s data

Four routes across Egypt which makes it one of most resilient network globally. The metropolitan network

crossing Egypt is the most vulnerable terrestrial fibre segment between (i) Europe and India and (ii) Middle

East and Asia for fibre cuts

New Ring

Existing Ring

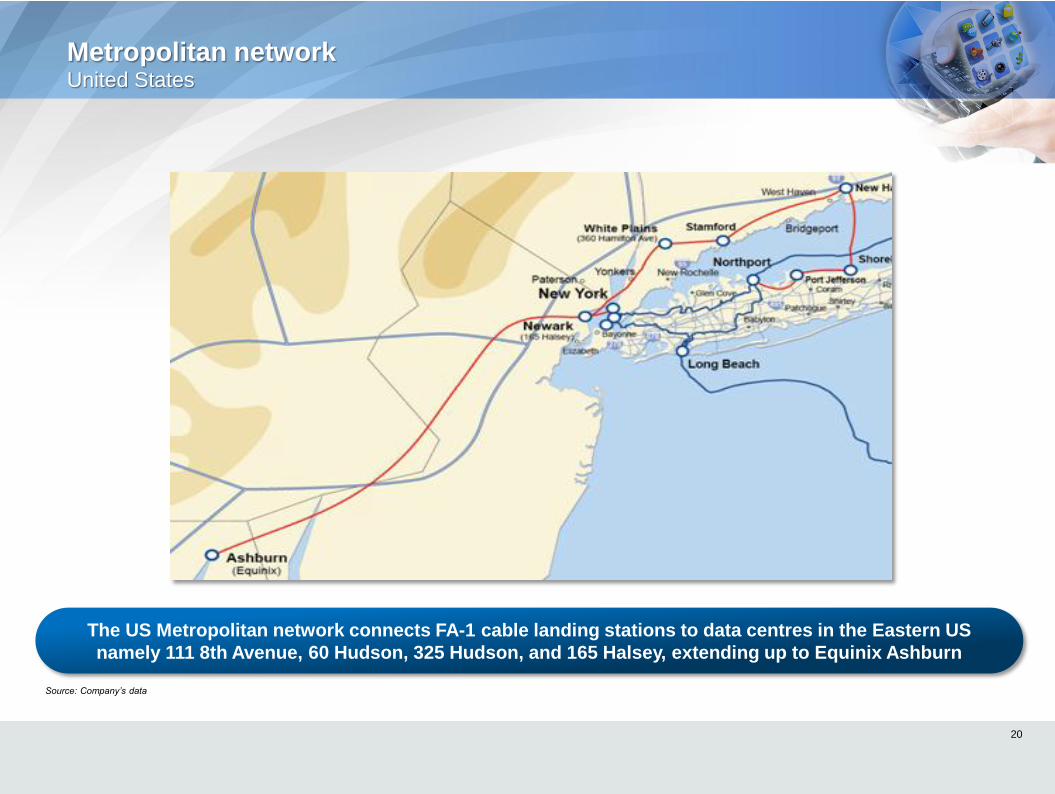

Metropolitan network United States

20

Source: Company’s data

The US Metropolitan network connects FA-1 cable landing stations to data centres in the Eastern US

namely 111 8th Avenue, 60 Hudson, 325 Hudson, and 165 Halsey, extending up to Equinix Ashburn

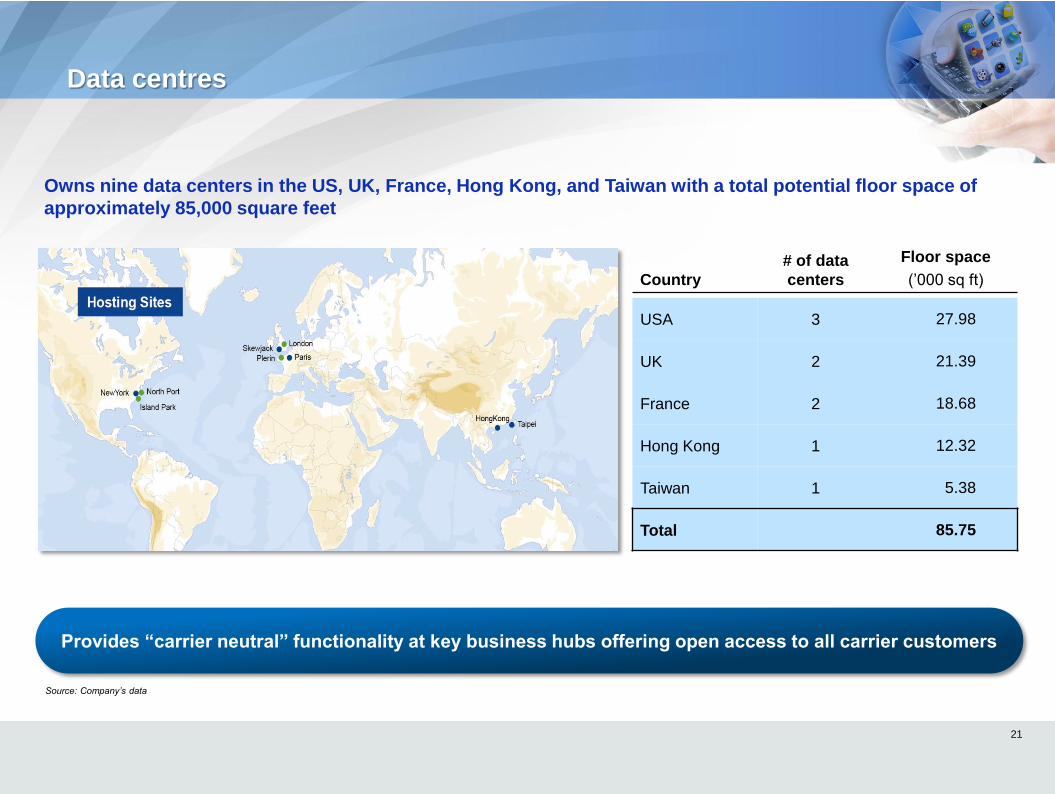

Data centres

21

Country

# of data

centers

Floor space

(’000 sq ft)

USA 3 27.98

UK 2 21.39

France 2 18.68

Hong Kong 1 12.32

Taiwan 1 5.38

Total 85.75

Source: Company’s data

Owns nine data centers in the US, UK, France, Hong Kong, and Taiwan with a total potential floor space of

approximately 85,000 square feet

Provides “carrier neutral” functionality at key business hubs offering open access to all carrier customers

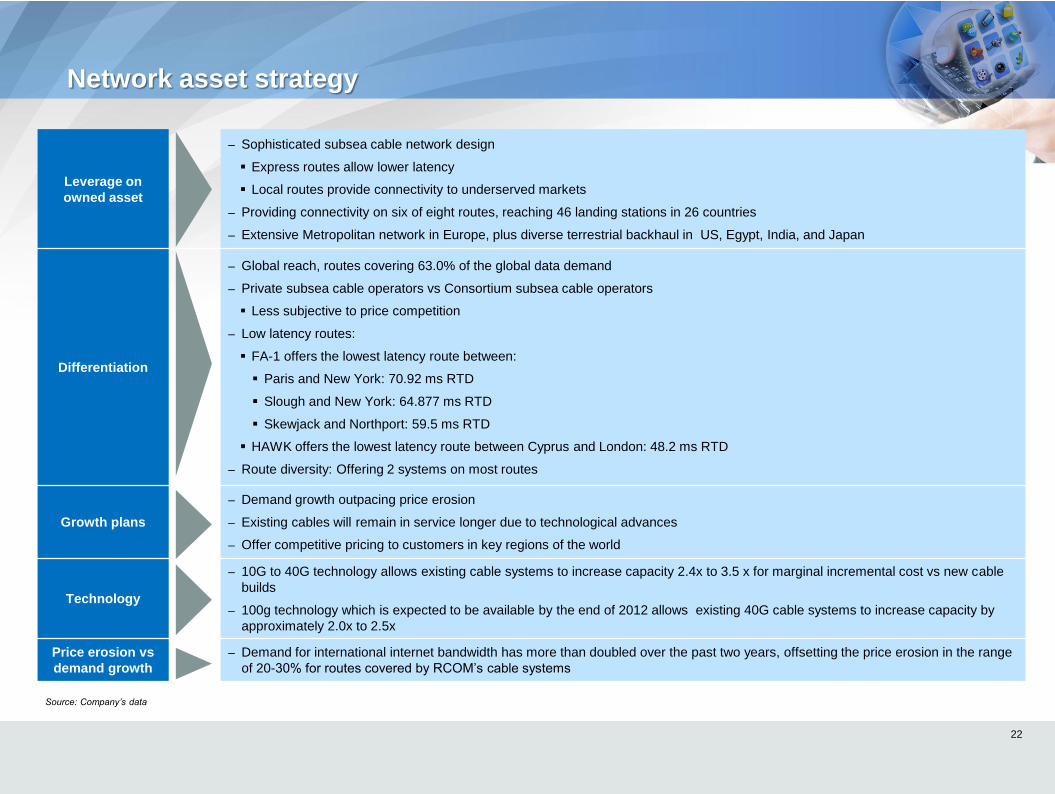

Network asset strategy

22

Leverage on

owned asset

– Sophisticated subsea cable network design

Express routes allow lower latency

Local routes provide connectivity to underserved markets

– Providing connectivity on six of eight routes, reaching 46 landing stations in 26 countries

– Extensive Metropolitan network in Europe, plus diverse terrestrial backhaul in US, Egypt, India, and Japan

Differentiation

– Global reach, routes covering 63.0% of the global data demand

– Private subsea cable operators vs Consortium subsea cable operators

Less subjective to price competition

– Low latency routes:

FA-1 offers the lowest latency route between:

Paris and New York: 70.92 ms RTD

Slough and New York: 64.877 ms RTD

Skewjack and Northport: 59.5 ms RTD

HAWK offers the lowest latency route between Cyprus and London: 48.2 ms RTD

– Route diversity: Offering 2 systems on most routes

Growth plans

– Demand growth outpacing price erosion

– Existing cables will remain in service longer due to technological advances

– Offer competitive pricing to customers in key regions of the world

Technology

– 10G to 40G technology allows existing cable systems to increase capacity 2.4x to 3.5 x for marginal incremental cost vs new cable

builds

– 100g technology which is expected to be available by the end of 2012 allows existing 40G cable systems to increase capacity by

approximately 2.0x to 2.5x

Price erosion vs

demand growth

– Demand for international internet bandwidth has more than doubled over the past two years, offsetting the price erosion in the range

of 20-30% for routes covered by RCOM’s cable systems

Source: Company’s data

Sales & customers

Section 3

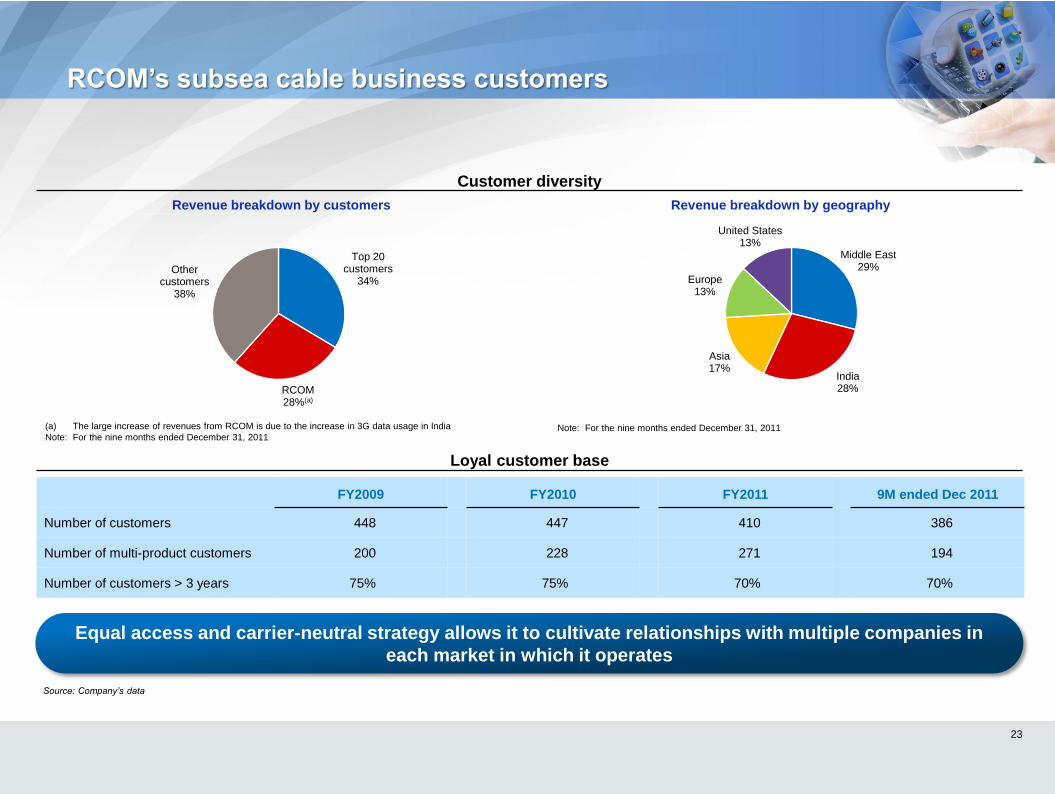

Top 20 customers

34%

RCOM 28%(a)

Other customers

38%

Middle East 29%

India 28%

Asia 17%

Europe 13%

United States 13%

RCOM’s subsea cable business customers

Customer diversity

Loyal customer base

23

Revenue breakdown by customers Revenue breakdown by geography

(a) The large increase of revenues from RCOM is due to the increase in 3G data usage in India

Note: For the nine months ended December 31, 2011 Note: For the nine months ended December 31, 2011

User XP ID(login name): liawjon

File Path: \\Dbg.ads.db.com\Sng-ma-

g\ibd\sngpres\Pitchbooks\2012\12csg\IBC

A\12csg0079\Backups\12csg0079_corner

stone.xlsx

File name: 12csg0079_cornerstone.xlsx

XL Sheet name: '19'!$D$14:$E$16

Time Stamp: 23/03/2012 22:49:54

User XP ID(login name): liawjon

File Path: \\Dbg.ads.db.com\Sng-ma-

g\ibd\sngpres\Pitchbooks\2012\12csg\IBC

A\12csg0079\Backups\12csg0079_corner

stone.xlsx

File name: 12csg0079_cornerstone.xlsx

XL Sheet name: '20'!$D$11:$E$15

Time Stamp: 23/03/2012 22:52:33

Source: Company’s data

FY2009 FY2010 FY2011 9M ended Dec 2011

Number of customers 448 447 410 386

Number of multi-product customers 200 228 271 194

Number of customers > 3 years 75% 75% 70% 70%

Equal access and carrier-neutral strategy allows it to cultivate relationships with multiple companies in

each market in which it operates

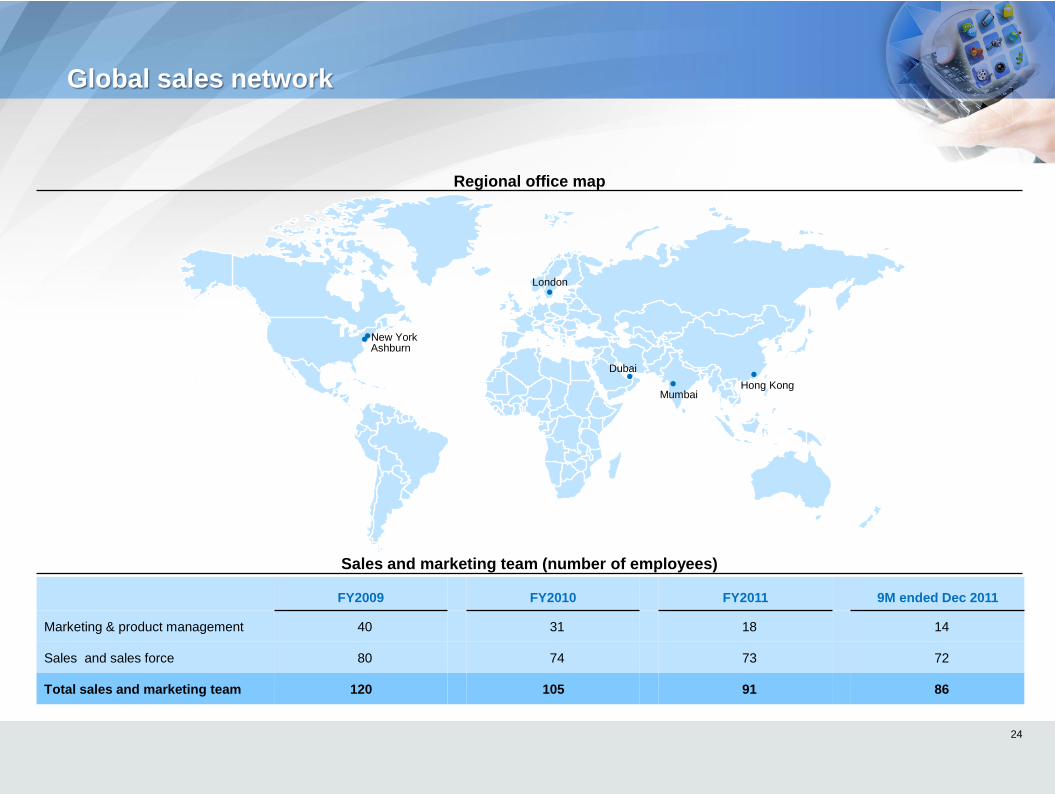

Global sales network

Regional office map

New York

Dubai

London

Hong Kong

Ashburn

24

Sales and marketing team (number of employees)

FY2009 FY2010 FY2011 9M ended Dec 2011

Marketing & product management 40 31 18 14

Sales and sales force 80 74 73 72

Total sales and marketing team 120 105 91 86

Mumbai

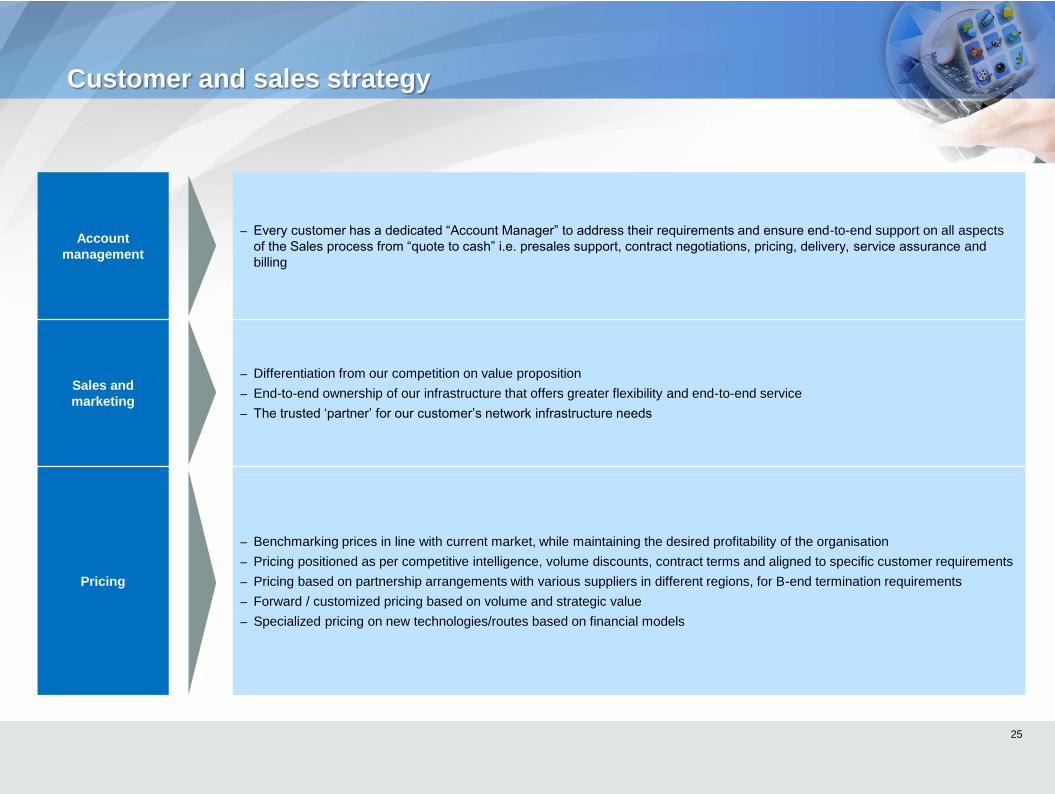

Account

management

– Every customer has a dedicated “Account Manager” to address their requirements and ensure end-to-end support on all aspects

of the Sales process from “quote to cash” i.e. presales support, contract negotiations, pricing, delivery, service assurance and

billing

Sales and

marketing

– Differentiation from our competition on value proposition

– End-to-end ownership of our infrastructure that offers greater flexibility and end-to-end service

– The trusted ‘partner’ for our customer’s network infrastructure needs

Pricing

– Benchmarking prices in line with current market, while maintaining the desired profitability of the organisation

– Pricing positioned as per competitive intelligence, volume discounts, contract terms and aligned to specific customer requirements

– Pricing based on partnership arrangements with various suppliers in different regions, for B-end termination requirements

– Forward / customized pricing based on volume and strategic value

– Specialized pricing on new technologies/routes based on financial models

Customer and sales strategy

25

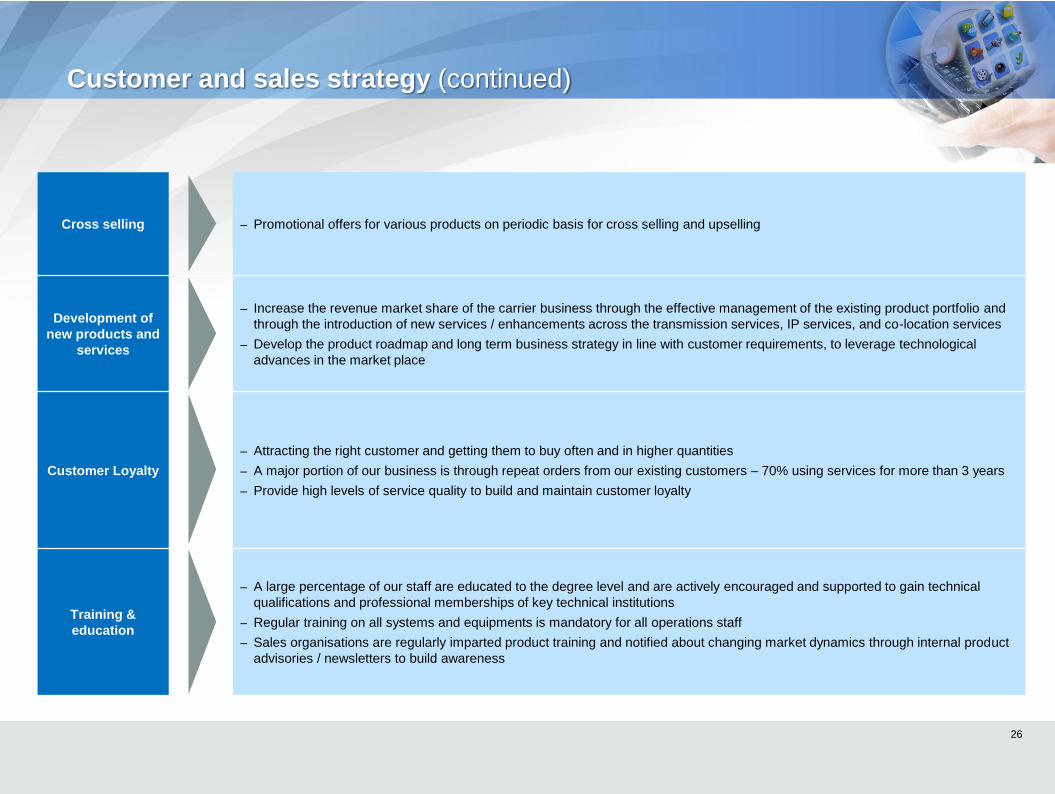

Cross selling – Promotional offers for various products on periodic basis for cross selling and upselling

Development of

new products and

services

– Increase the revenue market share of the carrier business through the effective management of the existing product portfolio and

through the introduction of new services / enhancements across the transmission services, IP services, and co-location services

– Develop the product roadmap and long term business strategy in line with customer requirements, to leverage technological

advances in the market place

Customer Loyalty

– Attracting the right customer and getting them to buy often and in higher quantities

– A major portion of our business is through repeat orders from our existing customers – 70% using services for more than 3 years

– Provide high levels of service quality to build and maintain customer loyalty

Training &

education

– A large percentage of our staff are educated to the degree level and are actively encouraged and supported to gain technical

qualifications and professional memberships of key technical institutions

– Regular training on all systems and equipments is mandatory for all operations staff

– Sales organisations are regularly imparted product training and notified about changing market dynamics through internal product

advisories / newsletters to build awareness

Customer and sales strategy (continued)

26

Investment highlights

27

Presence in key markets and global reach

High entry barriers – Cost, Time, Right of Way

Significant available capacity, low incremental upgrade costs, long useful life

High quality network, Global Ethernet enabled – Low latency IP

Strong customer relationships

4x IP traffic growth expected over next 5 years