Embed Size (px)

Citation preview

Refreshingly Sri Lanka - An Island of Retail Opportunity

Retail Intelligence I September 2013www.joneslanglasalle.com

Political stability drives economic growth

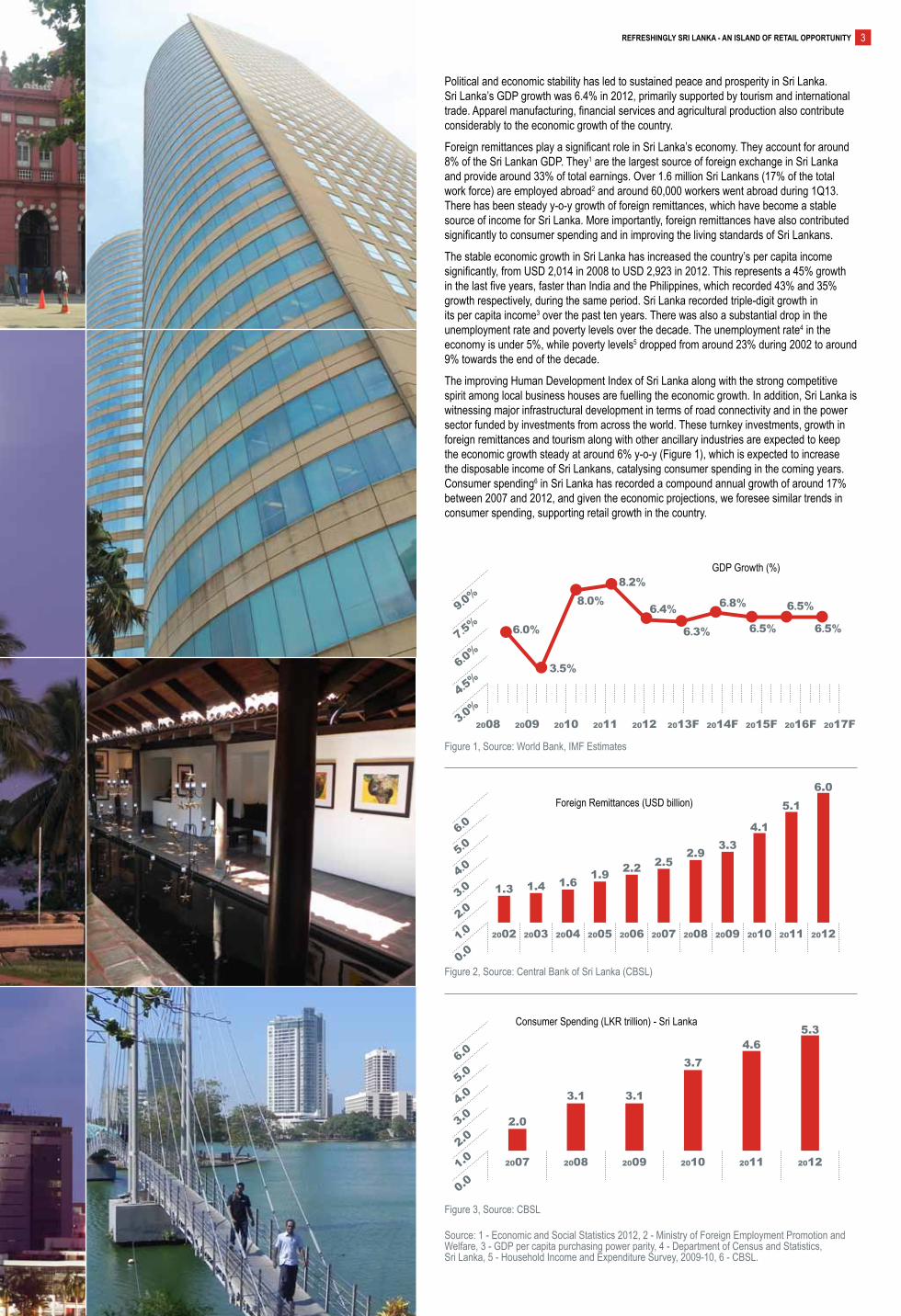

Political and economic stability has led to sustained peace and prosperity in Sri Lanka. Sri Lanka’s GDP growth was 6.4% in 2012, primarily supported by tourism and international trade. Apparel manufacturing, financial services and agricultural production also contribute considerably to the economic growth of the country.

Foreign remittances play a significant role in Sri Lanka’s economy. They account for around 8% of the Sri Lankan GDP. They1 are the largest source of foreign exchange in Sri Lanka and provide around 33% of total earnings. Over 1.6 million Sri Lankans (17% of the total work force) are employed abroad2 and around 60,000 workers went abroad during 1Q13. There has been steady y-o-y growth of foreign remittances, which have become a stable source of income for Sri Lanka. More importantly, foreign remittances have also contributed significantly to consumer spending and in improving the living standards of Sri Lankans.

The stable economic growth in Sri Lanka has increased the country’s per capita income significantly, from USD 2,014 in 2008 to USD 2,923 in 2012. This represents a 45% growth in the last five years, faster than India and the Philippines, which recorded 43% and 35% growth respectively, during the same period. Sri Lanka recorded triple-digit growth in its per capita income3 over the past ten years. There was also a substantial drop in the unemployment rate and poverty levels over the decade. The unemployment rate4 in the economy is under 5%, while poverty levels5 dropped from around 23% during 2002 to around 9% towards the end of the decade.

The improving Human Development Index of Sri Lanka along with the strong competitive spirit among local business houses are fuelling the economic growth. In addition, Sri Lanka is witnessing major infrastructural development in terms of road connectivity and in the power sector funded by investments from across the world. These turnkey investments, growth in foreign remittances and tourism along with other ancillary industries are expected to keep the economic growth steady at around 6% y-o-y (Figure 1), which is expected to increase the disposable income of Sri Lankans, catalysing consumer spending in the coming years. Consumer spending6 in Sri Lanka has recorded a compound annual growth of around 17% between 2007 and 2012, and given the economic projections, we foresee similar trends in consumer spending, supporting retail growth in the country.

Source: 1 - Economic and Social Statistics 2012, 2 - Ministry of Foreign Employment Promotion and Welfare, 3 - GDP per capita purchasing power parity, 4 - Department of Census and Statistics, Sri Lanka, 5 - Household Income and Expenditure Survey, 2009-10, 6 - CBSL.

Figure 1, Source: World Bank, IMF Estimates

4.5%6.0%7.5%

3.0%

9.0%

2008 2009 2010 2011 2012 2013F 2014F 2015F 2016F 2017F

6.0%

3.5%

8.0%8.2%

6.4%

6.3%

6.8%

6.5%

6.5%

6.5%

GDP Growth (%)

Figure 2, Source: Central Bank of Sri Lanka (CBSL)

Figure 3, Source: CBSL

Consumer Spending (LKR trillion) - Sri Lanka

1.0

0.0

2.03.04.05.06.0

2007 2008

3.1

2.0

5.34.6

3.7

3.1

2009 2010 2011 2012

Foreign Remittances (USD billion)

1.02.03.0

0.0

4.05.06.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1.3 1.4 1.61.9 2.2 2.5

2.93.3

4.1

5.16.0

RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty 3

The size of the Sri Lankan retail market is estimated at between USD 25 billion and USD 30 billion7, out of which organised players represent only 3%. However, the rising living standards of Sri Lankans are changing their spending patterns and preferences towards more quality branded goods and services. This offers growth opportunities for both global and domestic retailers in Sri Lanka.

Unlike the other emerging South and South-East Asian nations, where people prefer to save, Sri Lankans prefer to spend, as indicated by their gross domestic savings (Figure 4) being one of the lowest among South and South-East Asian countries. Sri Lanka’s spending patterns resemble Western countries, whose population demands more lifestyle products and aspirational luxury goods. As Sri Lanka’s economy is projected to grow by an average of 6.5% (Figure 1) for the next five years and per capita income is expected to increase from USD 2,923 in 2012 to USD 4,000 by 2016 (Figure 5), the nation is expected to witness steady growth in consumption. Alongside being a consumption-driven economy with changing spending patterns, we foresee strong retail growth prospects in Sri Lanka.

Sri Lanka’s retail sector is primarily driven by domestic consumption, followed by tourists’ consumption. Sri Lanka’s domestic consumption is at the nascent stage and the increase in disposable income is expected to make domestic consumption surge over the coming years. According to the latest household income and expenditure survey conducted in 2009-10, only a few Sri Lankans own computers, washing machines and other consumer durables (refer Figure 6). The introduction of liberalisation policies, including the reduction of import tariffs on automobiles and consumer durables, is expected to improve the consumption levels of these goods even further. In addition, increasing disposable income will continue to strengthen the sales of consumer durables over the coming years.

Source: 7 - A.T. Kearney 2012 Global Retail Development Index Report

Gross Domestic Savings (% of GDP)

Figure 4, Source: World Bank

15%

35%

20%

40%

25%

45%

10%

30%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011India Indonesia Malaysia Philippines Thailand Sri Lanka

Figure 5, Source: World Bank, IMF Estimates

GDP Per Capita (USD)

0

1,0002,0003,0004,0005,000

2010 2011

2,8362,400

2,9233,134 3,360

3,631 3,9334,269

4,633

2012 2013F 2014F 2015F 2016F 2017F 2018F

Figure 6, Source: CBSL Household survey 2009-10

Ownership of Household goods

10%

0%

20%30%40%50%60%70%80%90%100%

Personal Computers

VCD/DVD Players

Washing Machines

Television Refrigerators Electric Fans

Cooker Phone Motorcycle/Scooters

2006/7 2009/10

Sri Lanka’s Retail - The hidden trove

4 RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty

Sri Lanka is emerging as one of the world’s key tourist destinations and the tourism industry is one of the key drivers of Sri Lanka’s economy. According to the World Travel and Tourism Council, the tourism sector directly contributed around 4% of Sri Lanka’s GDP in 2012. Tourism offers noteworthy employment and entrepreneurial opportunities, supporting improved living standards and increasing disposable incomes. These factors in turn support retail activity from within the economy.

Western Europe contributes around 35-40% of the number of total tourists every year, while India alone consistently accounts for around 20%. Meanwhile, for 2013, the Sri Lanka Tourism Promotion Bureau (SLTPB) has set aside USD 6 million for marketing and promotional activities. Apart from focusing on India and Western Europe, SLTPB has decided to place extra focus on other Asian markets, such as China, Russia, Japan, the Middle East and South Korea. Further, in order to create awareness and to promote Sri Lanka as a tourist destination, SLTPB has been actively participating in overseas holiday fairs and organises promotional media campaigns in different targeted cities to attract international tourists.

With the Sri Lankan Tourism Development Authority (SLTDA) targeting around 2.5 million visitors by 2016, we foresee enhanced potential for the retail sector over the coming years. In general, shopping and food expenses account for more than 50% of tourist expenditure.

Figure 7, Source: Sri Lanka Tourism Development Authority (SLTDA)

Source: 8 - SLTDA, 9 - SLTDA, Annual Statistical Report 2011

On average, tourists spent 10 days8 in Sri Lanka during 2012. Assuming tourists spent an average of

two days in Colombo and given a tourist spends around USD 100 per day9, around 55% is assumed to have been spent on food and shopping. Thus, tourism is estimated

to have contributed a significant LKR 1.2 billion, which is 10.2% of Colombo’s total retail spending in

2012. Given the government’s tourism targets, we estimate that by 2016, tourism will contribute around

20% of the city’s total retail spending, gaining the spotlight in terms of retail potential. Figure 8, Source: SLTDA

Tourist Receipts (USD million)

200

0

4006008001,0001,200

2007 2008

319391

1,015839

576

333

2009 2010 2011 2012E

Figure 9, Source: SLTDA

Tourist Arrival by Region

2008200920102011

10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

America-North

Asia-South EastAsia-North East

South Asia (Ex-India)AustralasiaEurope-WestEurope-EastMiddle EastOthersIndia

Tourism to amplify retail potential

Tourist Arrivals (million)

0.2

0.0

0.50.71.01.21.51.72.02.22.52.7

2002 20092003 20102004 20112005 20122006 2013F2007 2014F2008 2015F2016F

1.0

2.5

RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty 5

Colombo - The gem in the crown

gaMpaha

Colombofort

nugegoda

KADUWELA

MAHARAGAMA

Ja-ela

pettah

kolonnawa

Baseline kiribathgoda

angoda

kottawa

n

Cotta Road

Manning towntalangama

Rajagiriya

Battaramula arangala

kotte

nawala

narahenpita

Mt lavinia

Moratuwa angulana

piliyandala

Map not to scalekesbewa

Boralesgamuwa

Maharagama

Slave Island

kollupitiya

Bambalapitiya

Wellawatte

dehiwala

Ratmalana

Sri Jayawardenapura kotte

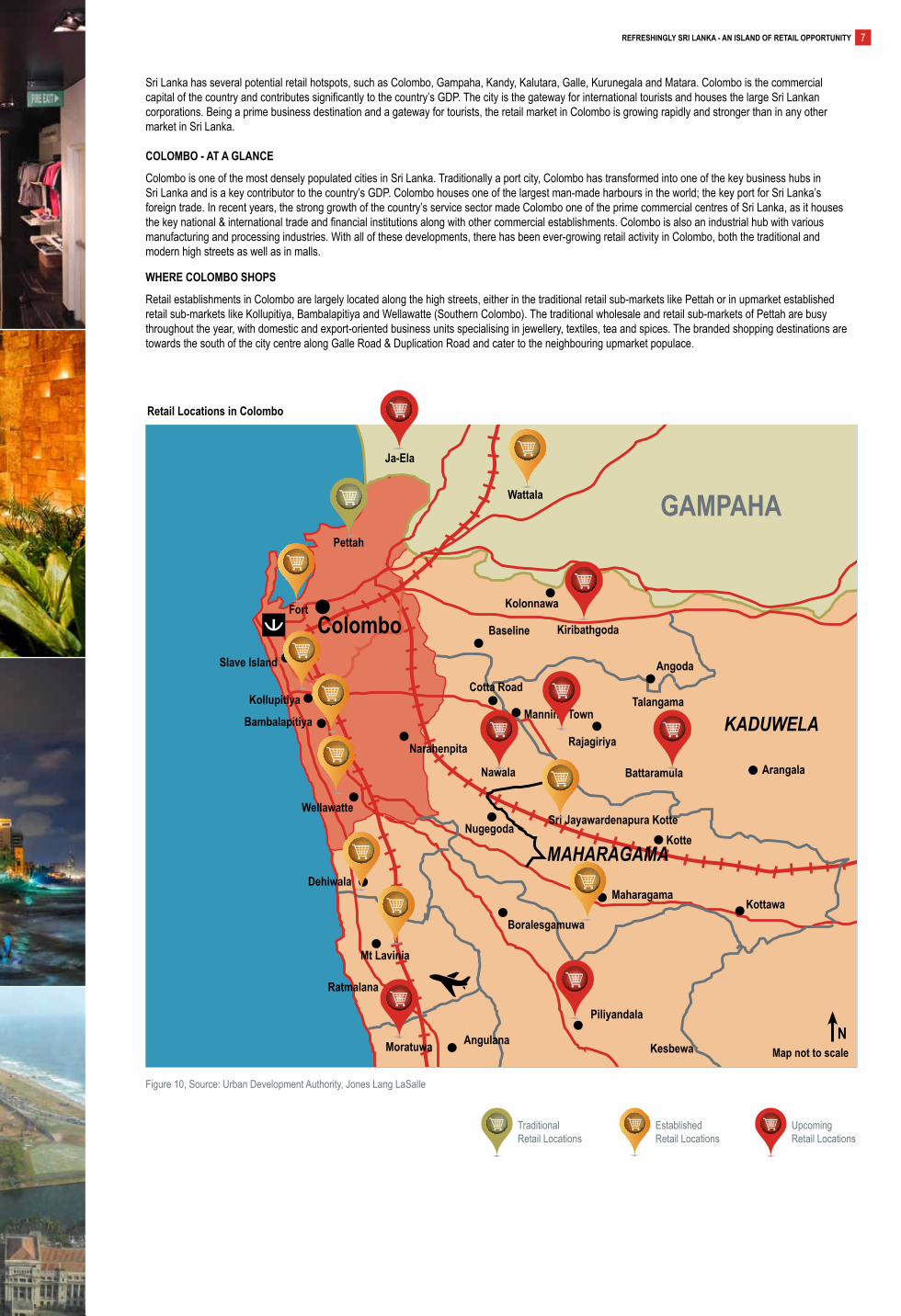

Figure 10, Source: Urban Development Authority, Jones Lang LaSalle

Retail locations in Colombo

Upcoming Retail Locations

Established Retail Locations

Traditional Retail Locations

Sri Lanka has several potential retail hotspots, such as Colombo, Gampaha, Kandy, Kalutara, Galle, Kurunegala and Matara. Colombo is the commercial capital of the country and contributes significantly to the country’s GDP. The city is the gateway for international tourists and houses the large Sri Lankan corporations. Being a prime business destination and a gateway for tourists, the retail market in Colombo is growing rapidly and stronger than in any other market in Sri Lanka.

ColoMBo - at a glanCe

Colombo is one of the most densely populated cities in Sri Lanka. Traditionally a port city, Colombo has transformed into one of the key business hubs in Sri Lanka and is a key contributor to the country’s GDP. Colombo houses one of the largest man-made harbours in the world; the key port for Sri Lanka’s foreign trade. In recent years, the strong growth of the country’s service sector made Colombo one of the prime commercial centres of Sri Lanka, as it houses the key national & international trade and financial institutions along with other commercial establishments. Colombo is also an industrial hub with various manufacturing and processing industries. With all of these developments, there has been ever-growing retail activity in Colombo, both the traditional and modern high streets as well as in malls.

WheRe ColoMBo ShopS

Retail establishments in Colombo are largely located along the high streets, either in the traditional retail sub-markets like Pettah or in upmarket established retail sub-markets like Kollupitiya, Bambalapitiya and Wellawatte (Southern Colombo). The traditional wholesale and retail sub-markets of Pettah are busy throughout the year, with domestic and export-oriented business units specialising in jewellery, textiles, tea and spices. The branded shopping destinations are towards the south of the city centre along Galle Road & Duplication Road and cater to the neighbouring upmarket populace.

Wattala

RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty 7

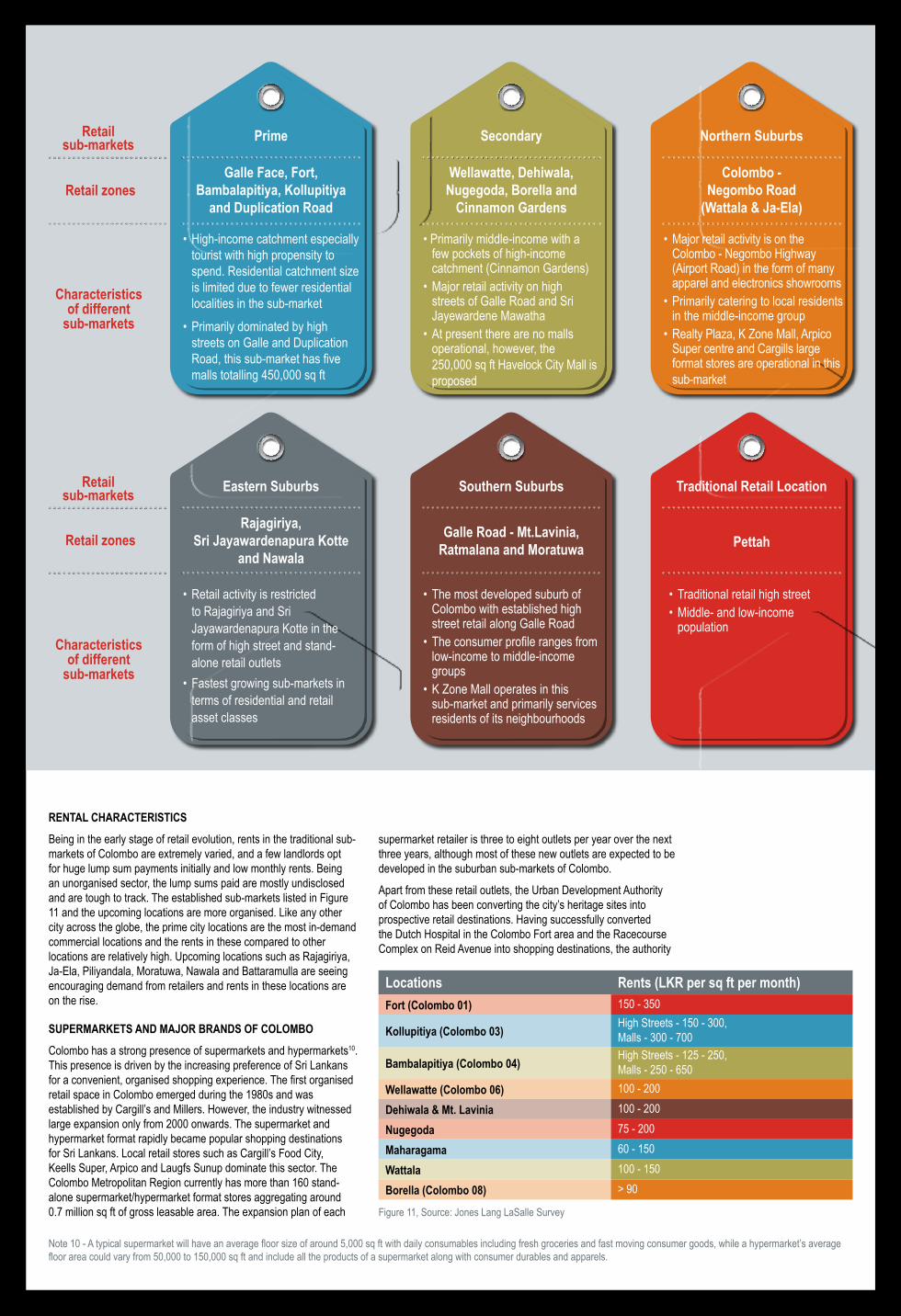

Rental ChaRaCteRIStICSBeing in the early stage of retail evolution, rents in the traditional sub-markets of Colombo are extremely varied, and a few landlords opt for huge lump sum payments initially and low monthly rents. Being an unorganised sector, the lump sums paid are mostly undisclosed and are tough to track. The established sub-markets listed in Figure 11 and the upcoming locations are more organised. Like any other city across the globe, the prime city locations are the most in-demand commercial locations and the rents in these compared to other locations are relatively high. Upcoming locations such as Rajagiriya, Ja-Ela, Piliyandala, Moratuwa, Nawala and Battaramulla are seeing encouraging demand from retailers and rents in these locations are on the rise.

SupeRMaRketS and MaJoR BRandS of ColoMBoColombo has a strong presence of supermarkets and hypermarkets10. This presence is driven by the increasing preference of Sri Lankans for a convenient, organised shopping experience. The first organised retail space in Colombo emerged during the 1980s and was established by Cargill’s and Millers. However, the industry witnessed large expansion only from 2000 onwards. The supermarket and hypermarket format rapidly became popular shopping destinations for Sri Lankans. Local retail stores such as Cargill’s Food City, Keells Super, Arpico and Laugfs Sunup dominate this sector. The Colombo Metropolitan Region currently has more than 160 stand-alone supermarket/hypermarket format stores aggregating around 0.7 million sq ft of gross leasable area. The expansion plan of each Figure 11, Source: Jones Lang LaSalle Survey

Note 10 - A typical supermarket will have an average floor size of around 5,000 sq ft with daily consumables including fresh groceries and fast moving consumer goods, while a hypermarket’s average floor area could vary from 50,000 to 150,000 sq ft and include all the products of a supermarket along with consumer durables and apparels.

Secondary northern Suburbs

traditional Retail locationSouthern Suburbseastern Suburbs

Wellawatte, dehiwala, nugegoda, Borella and

Cinnamon gardens

Colombo - negombo Road

(Wattala & Ja-ela)

pettahgalle Road - Mt.lavinia, Ratmalana and Moratuwa

Rajagiriya, Sri Jayawardenapura kotte

and nawala

• Primarily middle-income with a few pockets of high-income catchment (Cinnamon Gardens)

• Major retail activity on high streets of Galle Road and Sri Jayewardene Mawatha

• At present there are no malls operational, however, the 250,000 sq ft Havelock City Mall is proposed

• Major retail activity is on the Colombo - Negombo Highway (Airport Road) in the form of many apparel and electronics showrooms

• Primarily catering to local residents in the middle-income group

• Realty Plaza, K Zone Mall, Arpico Super centre and Cargills large format stores are operational in this sub-market

• Traditional retail high street • Middle- and low-income

population

• The most developed suburb of Colombo with established high street retail along Galle Road

• The consumer profile ranges from low-income to middle-income groups

• K Zone Mall operates in this sub-market and primarily services residents of its neighbourhoods

• Retail activity is restricted to Rajagiriya and Sri Jayawardenapura Kotte in the form of high street and stand-alone retail outlets

• Fastest growing sub-markets in terms of residential and retail asset classes

Retail sub-markets

Retail zones

Characteristics of different

sub-markets

prime

galle face, fort, Bambalapitiya, kollupitiya

and duplication Road

• High-income catchment especially tourist with high propensity to spend. Residential catchment size is limited due to fewer residential localities in the sub-market

• Primarily dominated by high streets on Galle and Duplication Road, this sub-market has five malls totalling 450,000 sq ft

Retail sub-markets

Retail zones

Characteristics of different

sub-markets

locations Rents (lkR per sq ft per month)fort (Colombo 01) 150 - 350

kollupitiya (Colombo 03) High Streets - 150 - 300, Malls - 300 - 700

Bambalapitiya (Colombo 04) High Streets - 125 - 250, Malls - 250 - 650

Wellawatte (Colombo 06) 100 - 200

dehiwala & Mt. lavinia 100 - 200

nugegoda 75 - 200

Maharagama 60 - 150

Wattala 100 - 150

Borella (Colombo 08) > 90

supermarket retailer is three to eight outlets per year over the next three years, although most of these new outlets are expected to be developed in the suburban sub-markets of Colombo.

Apart from these retail outlets, the Urban Development Authority of Colombo has been converting the city’s heritage sites into prospective retail destinations. Having successfully converted the Dutch Hospital in the Colombo Fort area and the Racecourse Complex on Reid Avenue into shopping destinations, the authority

is working on similar lines to refurbish the Auditor-General’s Office in the Colombo Fort location and Waters Edge in Rajagirya. The Auditor-General’s Office will be partly developed as a museum along with a few retail outlets for visitors, while Waters Edge in Rajagiriya will be developed as a destination for recreation (boating) and shopping.

The garment manufacturing industry - working for some of the world’s top brands such as Abercrombie & Fitch, Gap, Marks & Spencer, Nike, H&M, Victoria’s Secret and Tommy Hilfiger - has made Sri Lankans fashion conscious. The improving living standards have increased the propensity of the local population to spend on international brands such as Levi’s, Mango and the United Colors of Benetton. Local brands such as ODEL, Hameedia and No Limit also compete aggressively in this market, while Indian brands such as Nalli Silks and Madura Garments also have presence in Colombo.

In addition to these apparel retailers, international fast food chains like KFC, McDonald’s, Domino’s Pizza & Pizza Hut and electronics dealers such as Abans, Softlogic and Singer have a strong presence in the city. The typical outlet size of these brands varies from 1,500 to 25,000 sq ft. These brands operate both through stand-alone stores and through stores in malls.

MallS In ColoMBo Colombo has eight malls at present with sizes varying from 30,000 to 250,000 sq ft. Majestic City, Liberty Plaza and Crescat Boulevard are malls that are popular with the local population and tourists alike. The built up area of these malls totals around 0.66 million sq ft with an average vacancy rate of just about 5%. In addition to the existing malls, ten other malls are planned to be developed over the next five years in Colombo. These ten new malls are expected to add more than 1.5 million sq ft of retail space to Colombo’s existing mall stock by 2018. Out of the 1.5 million sq ft, more than 0.3 million sq ft of mall space is planned to be integrated with upcoming hotel projects in the prime sub-markets of Colombo.

the RISe of MIxed-uSe developMentSMixed-use real estate developments are an integrated combination of residential, commercial, retail, cultural and institutional spaces that are fast becoming popular. Given its various advantages, such as walk to work and walk to shop options, residential development in such complexes attracts buyers helping faster sales. This gives the added advantage of a captive catchment for the retail space within and around the complex. Havelock city is one such large-scale development that is taking shape in Colombo. In addition, Krrish Square, Destiny Mall & Residency and Tata Housing will introduce large-scale residential mixed-use developments over the coming years. Similarly Shangri-La, ITC Hotels and Colombo City Centre have planned mall spaces along with their upcoming hotel projects.

the need foR luxuRy MallSThe retail spaces within or adjacent to hotels typically sell high-end luxury products. High-end and luxury product retailers generally start their flagship stores within high-end hotel complexes to tap hotel customers who generally buy such products. This trend can be seen in many branded hotels in India and across the globe. However, as the market matures, luxury brands try to reach out to the local market

existing malls

Figure 12, Source: Jones Lang LaSalle Survey

Mall name and location

Built up area (sq ft)

Start of operations Major tenants

liberty plaza at Duplication Road, Kollupitiya

110,000 1982Keells Super, Abans, Sony, Premasiri, Label Swine, Bata, Perfumerie, Lake House Bookshop, DSI

unity plaza at Galle Road, Bambalapitiya

36,000 1985 City Optical, Network Communication, PC Electronics, Leader, Photo Micro

Majestic City at Galle Road, Bambalapitiya

252,000 1997 ODEL, Hameedia, Triumph, DSI, KFC, Food City, Majestic Cinemas, Wonderworld

Crescat Boulevard at Cinnamon Grand, Galle Road

35,000 2003 Hameedia, Triumph, Levis, Reebok, Adidas, E-Mart, Keells Super, Perfumerie

Realty plaza, Ja-Ela 75,000 2007 Cinemax Cinemas

k Zone, Moratuwa 30,000 2010 Keells Super, Levis, Paris Gallery, Keko, DSI, Adidas

dutch hospital Courtyard, Fort

26,000 2011LUV SL, Colombo Jewellery, SPA Ceylon, Ministry of Crab, Heladiv Tea Club, WIP Bar, Barefoot

k Zone, Ja-Ela 100,000 2013 Keells Super, Stone n String, Samsung

and sometimes move out of star hotels, setting up outlets on high streets to improve visibility. With a very limited number of high street properties suitable for luxury brands to expand in Colombo, we see hospitality players developing mixed-use spaces including malls as a viable option to give the luxury brands the best of both worlds.

IntegRatIon to BRIng SyneRgySri Lanka’s casino industry, like other fast-growing Asia Pacific markets, provides exciting growth opportunities. Integrating casinos along the mall will also bring affluent tourist to the mall supporting increased trading volumes in the mall. Ballys Casino, Bellagio and Stardust are some of the important casinos in the city. With the success of the casino industry, players such as Crown Casino have recently planned to enter Sri Lanka’s casino market. Sri Lanka’s casino industry is largely driven by tourists from other Asian countries. these destinations attract the affluent tourist population and thus help Sri Lanka to position itself as a premier tourist destination in South Asia.

Malls with few recreational activities will be one such option to create a destination to stop for the tourist. Major malls across the globe integrate some recreational elements such as multiplexes, gaming arcades, bowling alleys, 3D theatres, a few amusement rides and other recreational concepts like a Scary House and a Snow House. Colombo is the gateway to Sri Lanka, yet does not have any such malls to stop. Colombo requires a few such destinations for the tourist to stop and relax. The multiplex is a common recreational facility and is available only at Majestic cinemas in Colombo. The low penetration of multiplexes in the country is largely due to the country’s low content production and restricted import of films from abroad. However, malls can still focus on other amenities to attract the tourist.

RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty 9

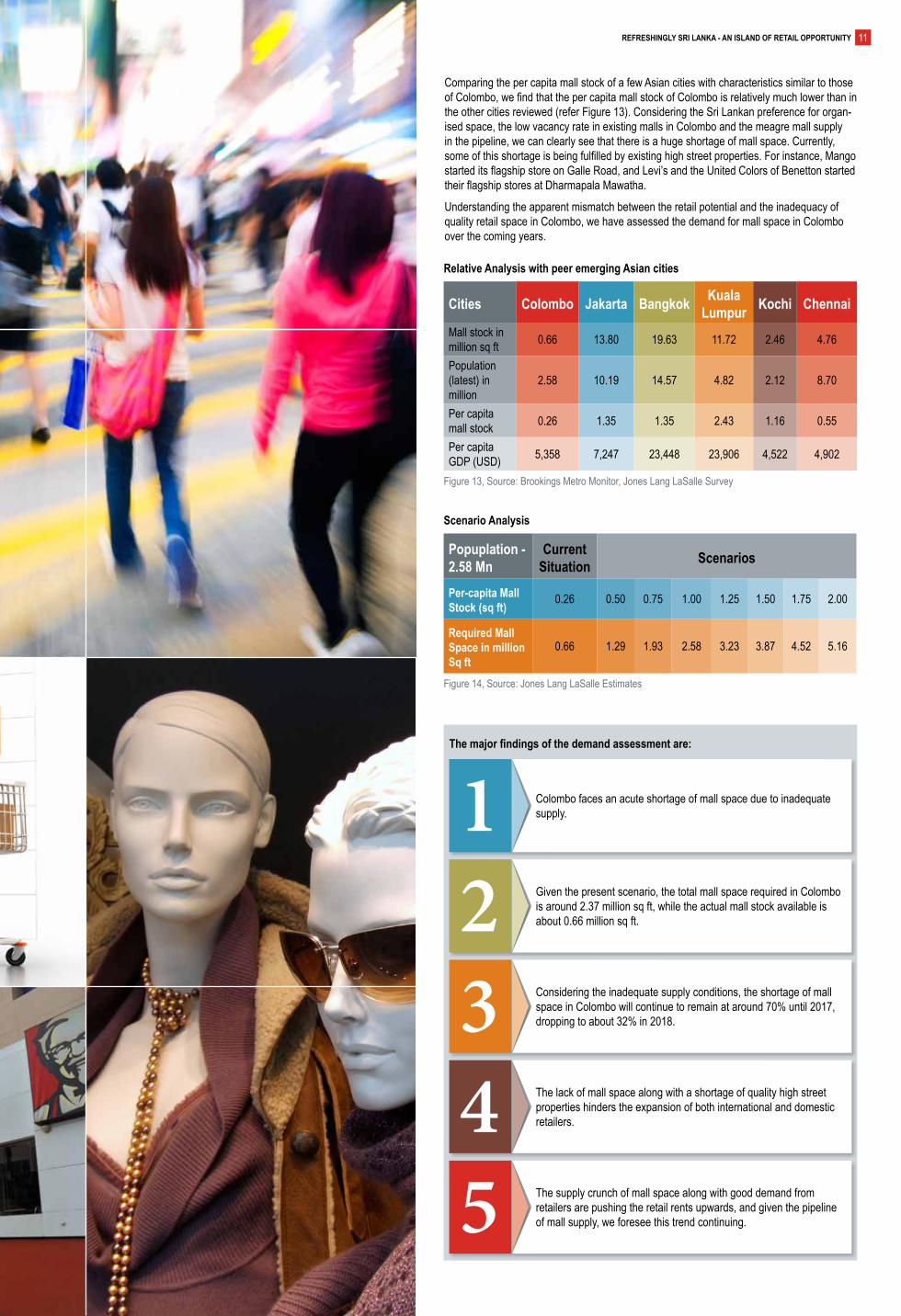

The retail sector is growing but retail realty is not keeping pace!

Comparing the per capita mall stock of a few Asian cities with characteristics similar to those of Colombo, we find that the per capita mall stock of Colombo is relatively much lower than in the other cities reviewed (refer Figure 13). Considering the Sri Lankan preference for organ-ised space, the low vacancy rate in existing malls in Colombo and the meagre mall supply in the pipeline, we can clearly see that there is a huge shortage of mall space. Currently, some of this shortage is being fulfilled by existing high street properties. For instance, Mango started its flagship store on Galle Road, and Levi’s and the United Colors of Benetton started their flagship stores at Dharmapala Mawatha.

Understanding the apparent mismatch between the retail potential and the inadequacy of quality retail space in Colombo, we have assessed the demand for mall space in Colombo over the coming years.

Cities Colombo Jakarta Bangkok kuala lumpur kochi Chennai

Mall stock in million sq ft 0.66 13.80 19.63 11.72 2.46 4.76

Population (latest) in million

2.58 10.19 14.57 4.82 2.12 8.70

Per capita mall stock 0.26 1.35 1.35 2.43 1.16 0.55

Per capita GDP (USD) 5,358 7,247 23,448 23,906 4,522 4,902

Relative analysis with peer emerging asian cities

Figure 13, Source: Brookings Metro Monitor, Jones Lang LaSalle Survey

Scenario analysis

Figure 14, Source: Jones Lang LaSalle Estimates

popuplation - 2.58 Mn

Current Situation Scenarios

per-capita Mall Stock (sq ft) 0.26 0.50 0.75 1.00 1.25 1.50 1.75 2.00

Required Mall Space in million Sq ft

0.66 1.29 1.93 2.58 3.23 3.87 4.52 5.16

Considering the inadequate supply conditions, the shortage of mall space in Colombo will continue to remain at around 70% until 2017, dropping to about 32% in 2018.3

Given the present scenario, the total mall space required in Colombo is around 2.37 million sq ft, while the actual mall stock available is about 0.66 million sq ft.2Colombo faces an acute shortage of mall space due to inadequate supply.1

The lack of mall space along with a shortage of quality high street properties hinders the expansion of both international and domestic retailers. 4The supply crunch of mall space along with good demand from retailers are pushing the retail rents upwards, and given the pipeline of mall supply, we foresee this trend continuing.5

The major findings of the demand assessment are:

RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty 11

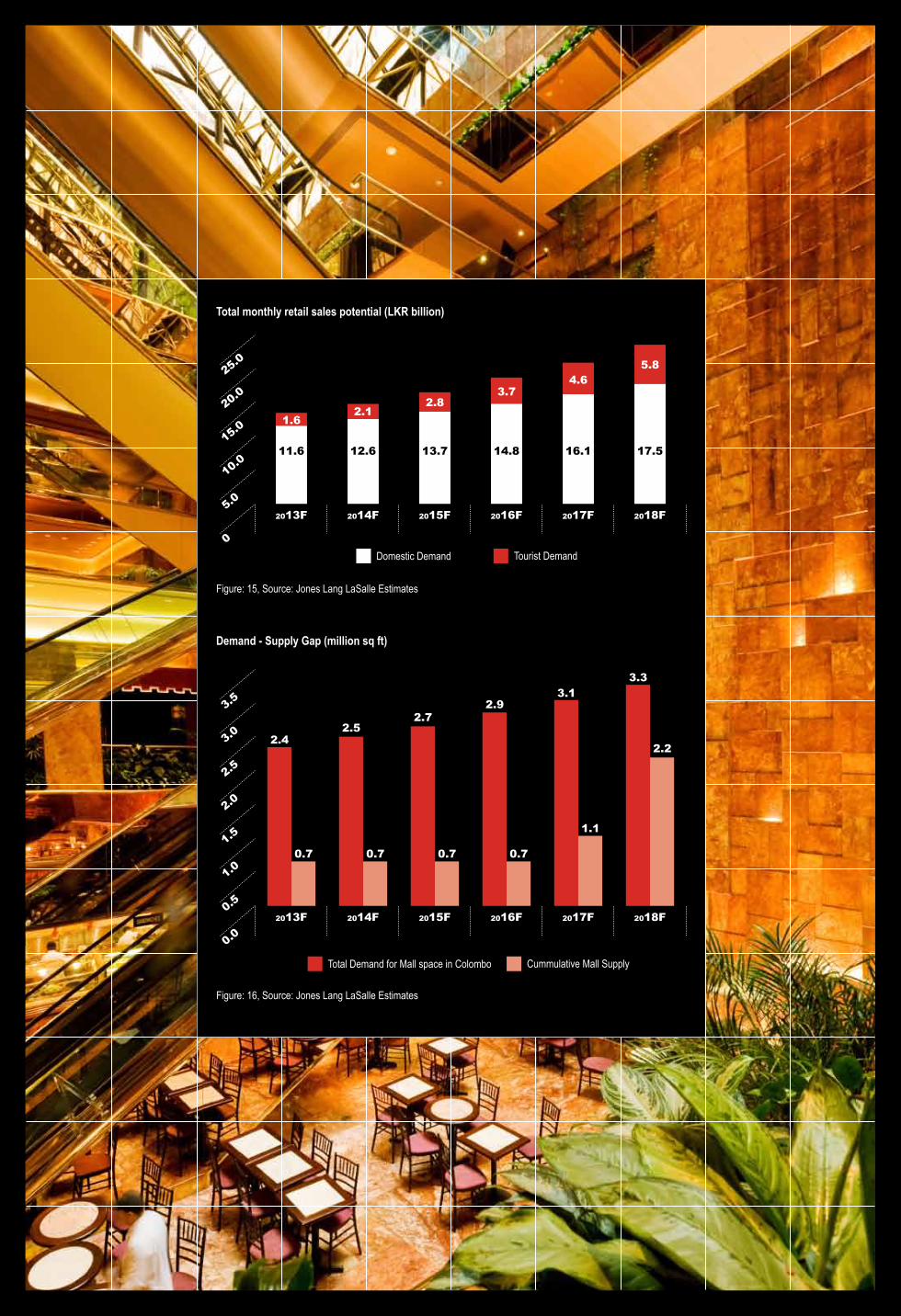

AssumpTions:• 55% of the household expenditure is spent on retail (including food

& recreation)

• 55% of tourist expenditure is spent on retail (including food)

• Mall sales is 40% of total retail sales (A+B)

upCoMIng MallS In ColoMBoThe existing shopping malls in Sri Lanka are merely larger versions of shopping centres, and very few upcoming projects are large enough to offer a complete shopping experience for shoppers. A mall should feature amenities such as a multiplex, a kids’ zone, crèche services, a games zones and a must-have food court. However, we see only a couple of upcoming malls with such capabilities (Figure 17). Most of the developers who have proposed a mall project are progressing with their projects at a slow rate and we expect some of the projects to be delayed by a year or two.

Mall Sub-Market location Completion year Bua (sq ft)liberty plaza - phase 2 CBD Kollupitiya 2014 60,000

altair CBD Beira lake 2017 40,000

Shangri-la CBD Galle face 2017 250,000

Silver needle- abans CBD Beira Lake 2017 160,000

destiny Mall CBD Slave Island 2017 30,000

havelock City Mall SBD Havelock 2018 250,000

John keells CBD Glennie Street 2018 400,000

krrish Square CBD Fort 2018 315,000

ItC hotel CBD Galle face 2018 60,000

tata Residential CBD Slave Island 2018 150,000

Figure: 17, Source: Jones Lang LaSalle Survey

estimating the demand for mall space in Colombo

Mall space demand in Colombo

(2.4 million sq ft)

Based on average monthly household expenditure & based on top 4 income

earning household deciles (similar to Sec A & B population in India)

Based on receipt per tourist per day, tourist arrivals and assuming 2

days of stay in Colombo

Total expenditure of top income earning households is calculated

Total expenditure of tourists is calculated

doMeStIC RetaIl potentIal touRISt RetaIl potentIal

Total retail sales potential from households in Colombo from top income

earning households per month (A)

Total retail sales potential from tourists in Colombo per month is

calculated (B)

Total mall sales

Based on average rent per sq ft per month in Colombo malls and

rents as % of Sales

Monthly sales per sq ftTotal high street sales

Total monthly retail sales = A + B

Figure: 15, Source: Jones Lang LaSalle Estimates

total monthly retail sales potential (lkR billion)

5.0

0

10.0

15.0

20.0

25.0

2013F 2014F 2015F 2016F 2017F 2018F

12.6

2.1

11.6

1.6

17.5

5.8

16.1

4.6

14.8

3.7

13.7

2.8

Domestic Demand Tourist Demand

Figure: 16, Source: Jones Lang LaSalle Estimates

demand - Supply gap (million sq ft)

0.5

0.0

1.0

1.5

2.0

2.5

3.0

3.5

2013F 2014F 2015F 2016F 2017F 2018F

0.7

2.4

0.7

2.5

0.7

2.7

0.7

2.9

1.1

3.1

2.2

3.3

Total Demand for Mall space in Colombo Cummulative Mall Supply

Although the per capita mall stock in Colombo is much lower than in other developing Asian cities and the city faces an acute supply crunch of mall space, it is critical to understand what kind or size of mall is sustainable in the city. To understand this, we studied a recently launched mega mall in India. The LuLu Mall is India’s largest mall and has a total built up space of more than a million sq ft.

Why koChI’S lulu Mall?In terms of tourism and foreign remittances, Sri Lanka can be compared to the Indian state of Kerala. More than 3 million Keralites work abroad and they sent around USD 11,320 million during 2012 as foreign remittances, which is similar to Sri Lanka. Sri Lanka, like Kerala, is also a preferred tourist destination and continues to witness significant retail demand from tourists. On similar lines, Kochi, the commercial capital of Kerala, is comparable to Colombo with respect to ongoing developments. Kochi had a few small mall developments similar to Colombo, until it recently recorded the completion of India’s largest mall with a total leasable area of more than a million sq ft - the LuLu Mall. Due to the similarities of Colombo and Kochi, the LuLu Mall can be an interesting case study to understand if a similar mall would be sustainable in Colombo. The mall hosts over 300 national and international brands, which have leased 90% of its space.

The mall is witnessing robust footfall, high conversion rates of around 50% even on weekdays and it is on track to become a destination mall for Keralites, besides being a prime attraction for tourists visiting Kochi.

Kochi is considered the gateway for tourists who visit Kerala, and Colombo is considered the gateway for tourists who visit Sri Lanka. Tourist demand coupled with the city’s purchasing power backed by foreign remittances is believed to be the rationale behind the construction of such a massive mall in the Tier II Indian city of Kochi. The LuLu Mall is located at the junction of NH-17, NH-47 and the Kochi bypass, which is one of the prime locations in the city and experiences heavy traffic flow. This is one of the key factors for the surging footfall in the mall. The location is very critical for the good performance of a mall. Therefore, in Colombo, a mall like this in a prime location can attract strong footfall from both the local population and tourists.

LuLu Mall has about 300 national and international retailers. In addition to this, interestingly the mall has a reserved retail space to promote local products and handicrafts, which promotes Kerala to tourists and the local population. A similar tenant mix can be replicated in the malls in Colombo, especially the idea of dedicated retail space for promoting local handicrafts, as Sri Lanka also has a vibrant tradition of handicrafts, such as handicrafts made of coconut shell, wood and local products such as tea, cinnamon and other spices. Besides being a retail attraction, the mall also employs 8,000 workers directly and 20,000 indirectly, thus stimulating local employment and the economy. A similar mall in Colombo could contribute to increased employment in the city.

The total shortage of mall space can be either aggregated to one building or scattered across many buildings throughout Colombo.

Therefore, Colombo may or may not accommodate a LuLu Mall, depending on how these factors are addressed. However, considering the per capita mall space (Figure 14), the city has a massive shortage of mall space that a supply of good quality malls in the city could alleviate.

Figure: 18, Source: Jones Lang LaSalle Survey

1 edapally, kochi location

41.0 million sq fttotal leasable area

7 InR 55 - InR 75 per sq ft per monthanchor Rents

3 1.4 million sq fttotal Bua

6InR 200 - InR 350 per sq ft per monthvanilla Rents

9 50-55% Weekdays, 55-60% WeekendsConversion Rates

2eMke group, abu dhabi, uaedeveloper

5 March 2013Completion year

890%occupancy

LuLu Mall Quick Facts

Can Colombo accommodate a mega mall?

14 RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty

Figure 20, Source: Income and Expenditure Survey 2009-10, CBSL

Although Colombo city has significant retail potential, we also see prospective retail opportunities outside Colombo. The southern suburb locations of Colombo, such as Dehiwala, are established residential locations with a few hospitality projects, yet no malls have been planned. Similarly, the eastern suburb locations such as Rajagiriya and Battaramulla have been seeing increased residential activity amid the concentration of government offices. Moreover, with easy access to Colombo city, these locations are increasingly attracting residential developments.

Apart from these suburb locations, some of the locations listed in Figure 19 follow Colombo in terms of population density. Supported by their respective per capita income levels, we believe locations such as Gampaha, Kalutara, Kandy, Galle and Matara have significant retail potential.

Kandy is the second largest city and attracts tourists for its scenic beauty and for the Buddhist temples. Kandy City Centre, which became operational in 2008, is the only mall in this sub-market. Due to war and the economic downturn, the mall saw few takers initially, yet of late retailers’ interest has been on the rise.

Gampaha has one of the highest per capita incomes among all the cities in Sri Lanka. Realising the potentials of this district, Gampaha Development Company is coming up with couple of malls OREX City and Ward City. OREX City will become operational by the end of this year and Ward City will become operational by early 2015.

Given the government’s focus on developing infrastructure and its special interest in the Tamil-dominated Northern and Eastern provinces, including Jaffna, we can expect enhanced retail potential in these locations in the medium term.

Figure: 19, Source: Income and Expenditure Survey 2009-10, CBSL

Population density (persons/sq Km)

Kalutara

Gampaha

Colombo

KandyGalle

Matara

Jaffn

a

5,00 1,000 1,500 2,500 3,5002,000 3,000 4,000

1,634

755

664

3,822

678

726

667

Household Income & Expenditure (LKR)

Average Monthly Household Income (LKR)Average Monthly Household Expenses on Non-food (LKR)Mean Monthly Per Capita Income (LKR)

Kalutara

Gampaha

Colombo

Kandy

Galle

Matara

Jaffn

a

10000 20000 30000 50000 6000040000

18,9177,938

4,434

30,98016,846

7,533

31,37614,855

7,923

33,06316,994

8,285

35,78021,534

8,790

48,87026,589

12,300

51,07031,171

12,202

Beyond Colombo

RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty 15

ConCluSIon

Sri Lanka’s growing middle-class population, the changing spending patterns toward branded and organised retail as well as the strong growth in tourism are expected to keep retail demand upbeat over the next few years. Colombo, as the commercial capital of the country, has tremendous retail potential and it is expected to witness retail development in terms of both malls and high streets.

According to A.T. Kearney’s 2013 Global Retail Development Index, Sri Lanka’s ranking leapfrogged from 20th to 15th best country for retail investments between 2011 and 2012 and the country maintained the same ranking in 2013. Improvement in the retail investment ranking was largely due to the political and economic stability, which is significantly uplifting the living standards in the country.

Furthermore, with Sri Lanka topping the South Asian countries in terms of starting and doing business and given its fewer procedural formalities, it is logistically and legally easy for the Indian retailer to expand to Sri Lanka. The country has Free Trade Agreements with other South Asian countries, such as Pakistan and Bangladesh. Thus, entering Sri Lanka will have the added advantage of easy access to these consumer markets, which otherwise would be difficult.

Conclusion

As discussed, creating a destination mall that includes amenities such as a multiplex cinema, a gaming zone for kids and casinos, and integrating this project with a golf course or an amusement park would make such a mall a destination to stop and hence would deliver outstanding results.

The local players have built world-class supermarkets, apparel brands and electronics showrooms to an extent that the time is ripe for international stakeholders to get their foot in the market. Therefore, retailers, mall developers and investors across the globe can evaluate Sri Lanka as a potential market for expansion and explore the new opportunities.

Having detailed the untapped market potential of Sri Lanka, we recommend that stakeholders critically assess aspects such as the location of the mall or retail property, catchment size, the size of the project, the design of the project, optimal tenant and product mix, positioning of the stores and maintenance of the project. We also suggest that stakeholders carefully study other challenges and risks attached to the retail business in Sri Lanka, such as inflation, exchange rate fluctuations and stringent labour laws.

16 RefReShIngly SRI lanka - an ISland of RetaIl oppoRtunIty

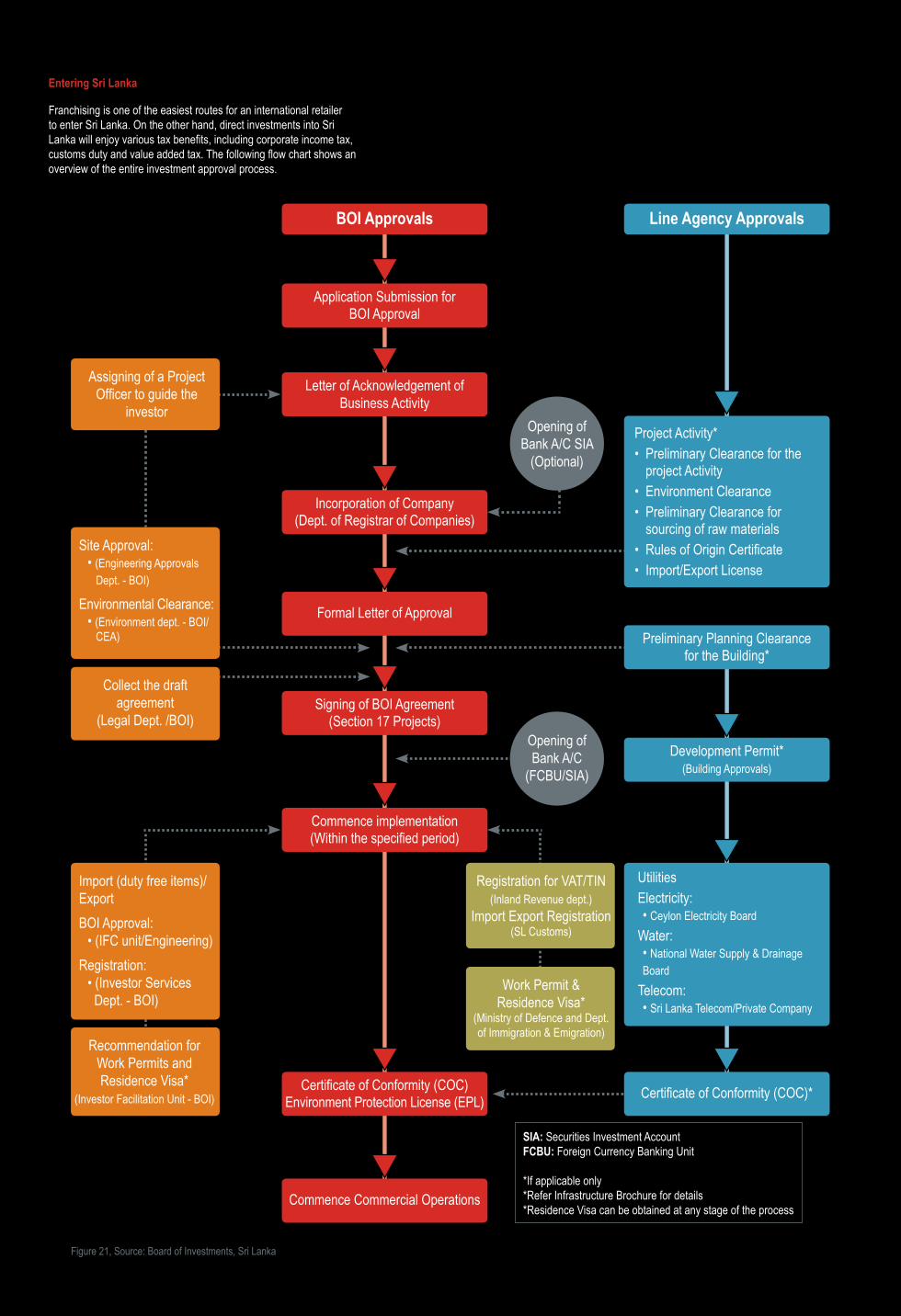

entering Sri lanka

Franchising is one of the easiest routes for an international retailer to enter Sri Lanka. On the other hand, direct investments into Sri Lanka will enjoy various tax benefits, including corporate income tax, customs duty and value added tax. The following flow chart shows an overview of the entire investment approval process.

Figure 21, Source: Board of Investments, Sri Lanka

Application Submission for BOI Approval

Project Activity*• Preliminary Clearance for the

project Activity• Environment Clearance• Preliminary Clearance for

sourcing of raw materials• Rules of Origin Certificate• Import/Export License

Assigning of a Project Officer to guide the

investor

UtilitiesElectricity: • Ceylon Electricity Board

Water: • National Water Supply & Drainage Board

Telecom: • Sri Lanka Telecom/Private Company

Letter of Acknowledgement of Business Activity

Incorporation of Company(Dept. of Registrar of Companies)

Preliminary Planning Clearance for the Building*

Development Permit*(Building Approvals)

Signing of BOI Agreement(Section 17 Projects)

Commence implementation(Within the specified period)

Certificate of Conformity (COC)Environment Protection License (EPL)

Formal Letter of Approval

Commence Commercial Operations

Certificate of Conformity (COC)*

BoI approvals line agency approvals

Site Approval: • (Engineering Approvals Dept. - BOI)

Environmental Clearance: • (Environment dept. - BOI/ CEA)

Collect the draft agreement

(Legal Dept. /BOI)

Registration for VAT/TIN (Inland Revenue dept.)

Import Export Registration (SL Customs)

Work Permit & Residence Visa*

(Ministry of Defence and Dept. of Immigration & Emigration)

Import (duty free items)/Export BOI Approval:

• (IFC unit/Engineering)Registration:

• (Investor Services Dept. - BOI)

Recommendation for Work Permits and Residence Visa*

(Investor Facilitation Unit - BOI)

Opening of Bank A/C SIA

(Optional)

Opening of Bank A/C

(FCBU/SIA)

siA: Securities Investment AccountFCBu: Foreign Currency Banking Unit

*If applicable only*Refer Infrastructure Brochure for details*Residence Visa can be obtained at any stage of the process

Shankar arumughamHead - Strategic Consulting Sri [email protected] +91 99400 66869 Sri Lanka +94 776326 888

Simon SelvarajVice PresidentStrategic [email protected] +91 98400 68451Sri Lanka +94 777985 640

ashutosh limayeHead of Research [email protected]+91 22 3985 1319

For more information about Research contact

gagan SinghCEO - Business & Chairperson - Sri Lanka [email protected] Sri Lanka +94 777 444094India +91 98111 51610

Sunil SubramanianHead - Transactions Sri [email protected]+94 775522155

For further business enquires contact

Authorsvasanth RaghunathanAssistant Manager, Research and [email protected] +91 44 3095 1063

Robin SManager, Strategic [email protected] +91 87544 04800Sri Lanka +94 774 668 757

Special Contribution & Guidance

trivita RoyAssistant Vice President Research & [email protected]+91 40 40409123

akshit ShahManagerCapital Markets Research [email protected]+91 98195 78866

Since establishing our presence, we have witnessed marked improvement in the country’s infrastructure. Sri Lanka’s economic progress has trickled down well with disposable incomes and purchasing power on the rise along with positive consumer sentiments.

Gagan SinghCEO - Business & Chairperson - Sri Lanka Operations

It’s not just international brands, even established domestic brands face challenges in identifying the right quality of retail space in Colombo. There is a desperate need for

high grade retail locations in the city.Sunil Subramanian

Head-Transactions - Sri Lanka

Asia pacific www.joneslanglasalle.com/asiapacific

australia www.joneslanglasalle.com.au

China www.joneslanglasalle.com.cn

hong kong www.joneslanglasalle.com.hk

India www.joneslanglasalle.co.in

Indonesia www.joneslanglasalle.co.id

Japan www.joneslanglasalle.co.jp

korea www.joneslanglasallekorea.co.kr

Macau www.joneslanglasalle.com.mo

new Zealand www.joneslanglasalle.co.nz

philippines www.joneslanglasalleleechiu.com.ph

Singapore www.joneslanglasalle.com.sg

Sri lanka www.joneslanglasalle.com.lk/

taiwan www.joneslanglasalle.com.tw

thailand www.joneslanglasalle.co.th

vietnam www.joneslanglasalle.com.vn

Jones Lang LaSalle Asia Pacific

COPYRIGHT @ JONES LANG LASALLE 2013. All rights reserved. The content of this publication has been compiled from the various sources acknowledged. The information is from sources we deem reliable; however, no representation or warranty is made to the accuracy thereof. This report has been produced solely as a general guide and does not constitute advice. We stress that forecasting is a problematical exercise which at best should be regarded as an indicative assessment of possibilities rather than absolute certainties.

34, East Tower, World Trade Center Echelon Square, Colombo 01 Sri Lanka tel +94 117 444 555 fax +94 117 444 556

Jones Lang LaSalle Lanka OfficeSunil Subramanian Head - Transactions Sri Lanka +94 775522155

Jones Lang LaSalle Retail, Sri Lanka

About Jones Lang LaSalleJones Lang LaSalle (NYSE:JLL) is a professional services and investment management firm offering specialized real estate services to clients seeking increased value by owning, occupying and investing in real estate. With annual revenue of $3.9 billion, Jones Lang LaSalle operates in 70 countries from more than 1,000 locations worldwide. On behalf of its clients, the firm provides management and real estate outsourcing services to a property portfolio of 2.6 billion square feet and completed $63 billion in sales, acquisitions and finance transactions in 2012. Its investment management business, LaSalle Investment Management, has $47.7 billion of real estate assets under management.Jones Lang LaSalle has over 50 years of experience in Asia Pacific, with over 25,400 employees operating in 76 offices in 14 countries across the region. The firm was named ‘Best Property Consultancy’ in nine Asia Pacific countries at the International Property Awards Asia Pacific 2012, in association with HSBC, and was named the number one real estate advisory firm in Asia Pacific in the Euromoney Real Estate Awards 2012.’

For further information, please visit our website, www.ap.joneslanglasalle.com

About Jones Lang LaSalle LankaJones Lang LaSalle Lanka is a leading professional services firm specializing in real estate in Sri Lanka. Based out of Colombo, the firm provides investors, developers, local corporates and multinational companies with a comprehensive range of services including research, analytics, project and development services, property and asset management, integrated facilities management, real estate capital markets and transactions encompassing commercial office spaces, hotels, land, industrial, retail and residential units. The Firm aims to combine local market knowledge with its access to global multinational relationships and capital sources, to provide Sri Lankan corporates, government agencies and clients with superior execution, towards transforming their real estate portfolios into efficient inventories, as well as in raising capital for real estate assets.

For further information, please visit www.joneslanglasalle.com

ashutosh limaye Head, Research and REIS [email protected] +91 98211 07054

For more information about Research

Shubhranshu pani [email protected] +91 98205 19899

pankaj Renjhen [email protected] +91 98992 18885

Jones Lang LaSalle Retail, India

deepak Bhavsar [email protected] +91 98111 74818

Jones Lang LaSalle Strategic Consulting, India

Shankar arumugham [email protected] +91 99400 66869