Embed Size (px)

Citation preview

Master Thesis in Accounting & Management Control

Björn Bromander 870203-4839 Tony Rahm 870310-4219

Reward and compensation

in Swedish companies What linkages are there to other management

control systems?

2

Acknowledgement

As authors, we would like to express our gratitude for all people who has helped us to complete this

thesis. First and foremost we greatly appreciate the guiding and feedback that we got from our

supervisors Johan Dergård and Per-Magnus Andersson during the working process.

Furthermore, we are also thankful towards the participated companies who made this study possible

and for the helpful responses from our friends and opponents.

Lund, May 2012-05-24

Björn Bromander Tony Rahm

3

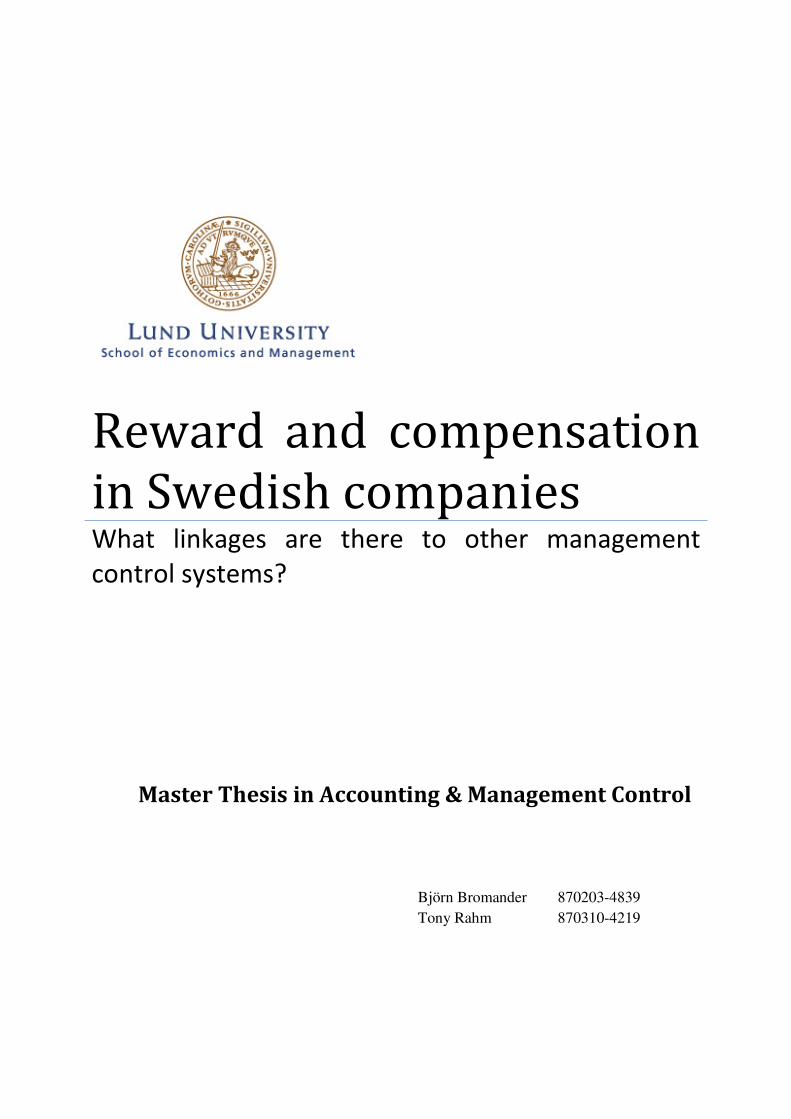

Abstract

Title: Reward and compensation in Swedish companies – what linkages are there to other management control systems? Seminar date: 30th of May, 2012 Course: Master thesis in Accounting and Management Control Authors: Björn Bromander, Tony Rahm Advisors: Per-Magnus Andersson, Johan Dergård Key words: Management control system, control package, reward and compensation, linkage, conceptual framework Purpose The aim of this paper is to describe the design of reward and compensation systems and

based on this, explain which linkages there are to other parts of the MCS package.

Methodology: In order to give an answer to the purpose of the investigation, a quantitative approach has been used were interviews with 15 Swedish have been conducted. The surveys were done by telephone and the sample aimed to represent the industries as a whole. Theoretical perspectives: The theoretical references originate from our academically studies which includes literature and previous science. A perspective of the management control system as a package is presented together with a review of conducted studies on the field of reward and compensation systems. Empirical findings: The base for the empirical findings is the 15 conducted interviews. We present the material by using tables, diagrams and other calculations. Both an overall view and a more narrowed picture of the selected questions are presented. Conclusion: The analysis in this thesis points out that there are some small linkages between reward and compensation and the other parts of the MCS package, where the linkages are strongest when it comes to performance measurements system. However, we did not find as clear and obvious connections as we had hoped for.

4

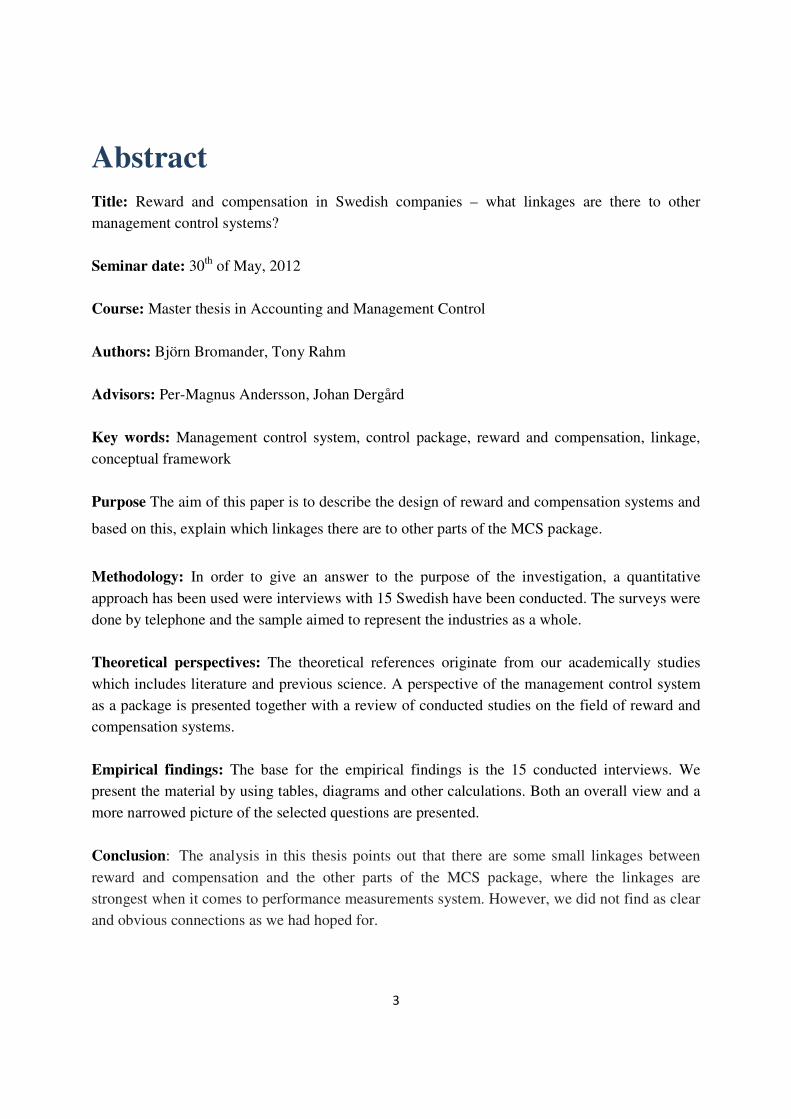

Table of content

1. Introduction ......................................................................................................................................... 6

1.1 Background .................................................................................................................................... 6

1.2 Problem discussion......................................................................................................................... 8

1.3 Purpose .......................................................................................................................................... 9

1.4 Disposition ................................................................................................................................... 10

2. Method .............................................................................................................................................. 11

2.1 Quantitative method .................................................................................................................... 11

2.2 Implementation of the study ........................................................................................................ 12

2.3 Explanatory investigation method ................................................................................................ 15

2.4 Primary and secondary data ......................................................................................................... 15

2.5 Validity and reliability ................................................................................................................... 16

2.5.1 Validity .................................................................................................................................. 16

2.5.2 Reliability............................................................................................................................... 17

3. Theoretical framework ....................................................................................................................... 18

3.1 MCSs as a package ....................................................................................................................... 18

3.1.1 Culture .................................................................................................................................. 19

3.1.2 Planning ................................................................................................................................ 20

3.1.3 Cybernetic control ................................................................................................................. 21

3.1.4 Administrative control ........................................................................................................... 22

3.1.5 Incentive systems .................................................................................................................. 22

3.1.5.1 Monetary incentives ...................................................................................................... 23

3.1.5.2 Non-monetary incentives .............................................................................................. 25

3.2 Problems regarding MCS package................................................................................................. 26

4. Empirical findings ............................................................................................................................... 27

5. Analysis .............................................................................................................................................. 31

5.1 Reward and Compensation .......................................................................................................... 31

5.2 Correlation analysis ...................................................................................................................... 34

5.2.1 Strategic planning .................................................................................................................. 34

5.2.2 Short-term planning .............................................................................................................. 35

5.2.3 Performance measurement and evaluation ........................................................................... 36

5

5.2.4 Organizational structure and management processes ............................................................ 37

5.2.5 Organization culture and values............................................................................................. 38

5.2.6 Organization and environment .............................................................................................. 39

6. Conclusion and discussion .................................................................................................................. 41

7. References ......................................................................................................................................... 43

6

1. Introduction

In the introduction section, the background and the problem discussion are described. Thereafter, we

present the problem statement followed by our purpose. Finally, a disposition is presented in order to

provide an overview of the thesis.

1.1 Background

“MCS research has provided much information about the operation of many of these systems

individually; however, at this time we know very little about how these systems are actually

configured as a package across organizations (....) A second and related theme is how the

elements within a control package relate to each other. Currently we have very little theory that

enables researchers to establish the relationships between the systems in a control package”.

(Malmi & Brown, 2008 pp. 297)

Kaplan (1984) concluded that the area of management control systems (MCSs) was narrowed and

inadequate and that the MCSs did not provide sufficient tools for managers to handle their

business in the most optimal way. Today, however, the field of MCSs has increased significantly

and the problem has more become a question of picking the most proper MCS for each and every

situation (Malmi & Granlund, 2009). The companies are offered a wide range of MCSs that can

be used to achieve their business targets including target costing, balance scorecard, total quality

management etc. The various types of MCSs that are used depend on the firms’ internal and

external conditions, which could be organizational culture, strategic planning or some other

aspect. The picture may be even more complex if companies choose to use several MCSs at the

same time. Moreover, the decision to implement different MCSs is not always guided by the

current strategy or elaborated decisions, since a manager’s background, experience, personality

and academic education often plays a crucial role for which MCS that is implemented (Nilsson et

al, 2011).

Some of the studies that have been carried out within the area of control system packages tend to

be case studies (Sandelin, 2008; Sorsanen, 2009). Even though this does not have to be a

7

drawback in itself, these studies have not been able to present a reliable picture of how different

companies actually use MCSs and how they relate to each other. A case study just gives specific

knowledge about the investigated topic together with some knowledge about the context of the

topic. Thus, problems arise if we do not possess any knowledge about how different control

systems affect or counteract each other and it cannot be proved that there exist any differences

within the MCS package that depends on e.g. company size, industry, cultural contexts etc.

(Nolin & Skarin, 2010: Axelsson et al, 2010)

Högman & Moldén (2011) have taken a more overall approach to the subject of control packages

and have studied how performance measurement systems are designed and related to other

variables in the MCSs. Results from their study indicate that companies use consistent methods

concerning control systems and performance measurements. However, the study gives no answer

to how and to what extent MCSs affect or interact with performance measurements.

In connection to the introductions of new MCSs in the companies’ organizations, there is also a

risk that companies will combine and use different MCSs without reflecting upon if these

systems work together. This in turn can lead to the fact that managers make wrong decisions for

their business. (Siverbo & Åkesson, 2009).

When it comes to in what way firms aim to match their strategy with their reward systems, Boyd

& Salamin (2001) found that companies in general are not aware of the fact that their strategy is

not always linked to the reward system. In addition to this, the formation of a reward and

compensation system that is clearly linked to the firms’ strategy has proven to be rather complex

to implement. Malmi & Brown (2008) illuminated this area even further by introducing a model

including different control categories, which try to bring attention to how control systems

interact. This model, called MCSs as a package, can be described as a control mix with the

purpose to provide a broader perspective based on reality (Nilsson et al, 2011). Furthermore,

Nilsson & Rapp (2006) give attention to the relations between different MCSs and the strategies

that are employed. Based on these articles, it appears that the interest in studying how different

MCSs interact with each other, and to view the MCSs as a package instead of individual systems,

has increased.

8

1.2 Problem discussion

The main focus in the model by Malmi & Brown has been to examine cybernetic controls and

planning and studies have indicated that companies are not regarding their MCSs as a package,

but rather use different systems for different business levels resulting in the fact that there are no

real coherence among the MCSs. (Sandt, 2009; Högman & Moldén, 2011; Axelsson et al, 2010)

Furthermore, it appears that the reward and compensation part is not examined as much as the

other parts in the model. It may be the fact that this is the most complicated part to study since it

can be difficult to get relevant information from companies.

The part regarding reward and compensation includes a lot of knowledge about how different

techniques should be used and at what time. However, just a few studies have been conducted

with the aim to investigate how reward and compensation systems are working together with

other MCSs so there is a need for this kind of knowledge (Berry, 2008). It does not exist one

clear explanation why reward and compensation systems have not been studied in a wider

perspective, but there is often said to be a bias towards giving groundless credit to the reward

systems in the companies. Managers often have a self-interest of talking in favor of a reward

system even if it is not the most optimal one for the firm (Stringer, 2006). Even though

companies in all industries and during various economic periods have used reward and

compensation systems in some form as a way to manage their organization, there is still no

sufficient knowledge declaring if these reward and compensation systems are properly linked to

other management control systems. (Merchant et al, 2003) Besides this, evaluations of reward

and compensation systems have been applied very moderate leading to the fact that management

of companies do not really know if the implemented reward system actually works in reality. In

many cases the managers have no idea whether the reward and compensation system increase the

organizational performance or if it, in the worst case, even decrease the performance (Armstrong

et.al, 2011; Gerhart and Rynes, 2003).

The contexts, where the companies operate in, and the companies themselves are constantly

changing which makes it vital to study this important field of research continuously. A MCS that

is perfectly suitable for one organization may be disastrous for another. This highlights the fact

9

that management control tools and techniques need to be studied jointly and regarded in its full

contextual situation. (Malmi & Brown, 2008).

Our thesis is included in an international project which has the aim to investigate and gain

knowledge of how MCSs work as a package within Swedish organizations. Since this area is a

rather large one, we had to specify our topic and according to Rienecker & Jörgensen (2004), one

of the most essential aspects when writing a thesis is to have a clear and proper purpose that

guides and directs the work of the study. With that in mind, we believed that reward and

compensation systems and the linkages to the other parts of the MCS package within

organizations was an appropriate and interesting topic to investigate.

1.3 Purpose

The aim of this paper is to describe the design of reward and compensation systems and based on

this, explain which linkages there are to other parts of the MCS package.

10

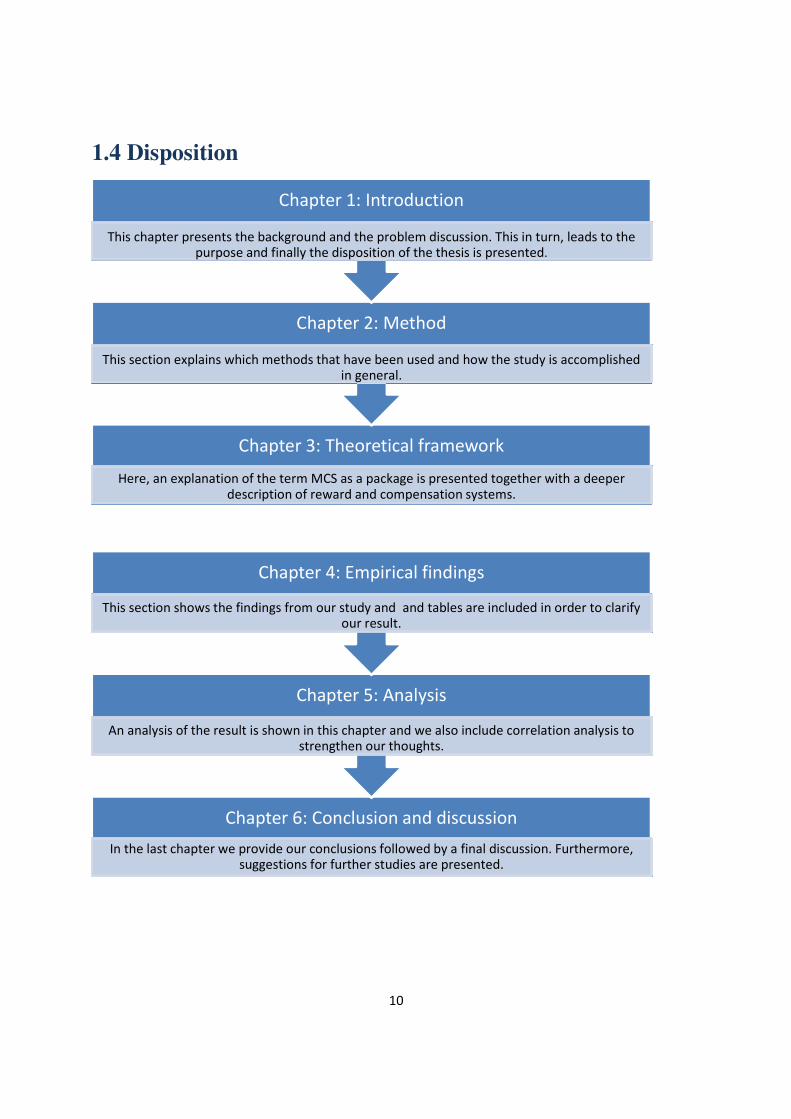

1.4 Disposition

Chapter 3: Theoretical framework

Here, an explanation of the term MCS as a package is presented together with a deeper description of reward and compensation systems.

Chapter 2: Method

This section explains which methods that have been used and how the study is accomplished in general.

Chapter 1: Introduction

This chapter presents the background and the problem discussion. This in turn, leads to the purpose and finally the disposition of the thesis is presented.

Chapter 6: Conclusion and discussion

In the last chapter we provide our conclusions followed by a final discussion. Furthermore, suggestions for further studies are presented.

Chapter 5: Analysis

An analysis of the result is shown in this chapter and we also include correlation analysis to strengthen our thoughts.

Chapter 4: Empirical findings

This section shows the findings from our study and and tables are included in order to clarify our result.

11

2. Method

This section presents which methods that have been used, followed by a detailed description of the

interview process and the working process in general. At last, we discuss the validity and reliability for our

study.

2.1 Quantitative method

Usually, there are two types of methods that are used when a study is accomplished. These are

the quantitative method and the qualitative method (Andersen, 1998). Our study has a

quantitative approach which means that we put emphasis on the broad perspective and examined

many different objects. Though, the information was not as detailed as it would have been if we

had used the qualitative approach, but on the other hand the quantitative observations are

generally more coherent and have a clearer structure. One typical example is surveys where the

answer alternatives are fixed.

The purpose of using a quantitative approach is to find some kind of linkages, averages or

something that is representative for the objects in the study. This method also tries to describe

and explain the studied area and the information is transformed to amounts and figures. Finally,

statistical analyses are accomplished. (Holme & Solvang, 1997)

Our thesis is first and foremost based on conducted several interviews including questions from a

survey which means that there is a quantitative orientation. Also, statistical analyses were

accomplished which, as we mentioned before, is a trait for the quantitative approach. Of course,

there are also some qualitative elements in our study because of the interviews, but since we

interviewed as many as 15 companies we could not examine every company as deeply as we

could have done with fewer companies. Therefore, it is obvious that the main approach of the

thesis is quantitative.

Furthermore, we thought that we would get a better result if we used a quantitative approach

instead of a qualitative, since the purpose with the thesis was to investigate the linkages between

reward and compensation systems with other parts of the companies’ MCSs. In other words, the

more companies used in the study, the more data we had for our analysis.

12

2.2 Implementation of the study

In order to get the information we needed, we used a questionnaire containing seven sections,

where each section had more or less the same size. Since we are part of a project, this

questionnaire was made in advance and handed out to us. The ones responsible for the project did

not want the questionnaire to be widely spread and it has therefore been labeled as confidential.

Most of the questions are formulated in form of scales (e.g. 1-7, where 1 is the lowest and 7 is the

highest grade) but there are also questions with different alternatives where the interviewee can

pick one or more answers. In order to apply the model by Malmi & Brown, there is a need to find

out what measures that have to be used in order to fulfill the purpose of the thesis. One way to do

this is to use the different parts from the model and as a result, a categorized structure is given

and therefore it is possible to further apply relevant variables in each part. The different sections

included in the questionnaire, except for reward and compensation included, are the following:

• Strategic planning (section A)

This part has the main aim to define the process which is taken to direct the company in the

future and include questions about what the companies do, for whom they are doing it, how the

company excels and how do they beat or avoid competition. This section is further divided into

questions like what is most essential in the strategic planning, who participate in the formation of

the strategic planning and how often it is revised.

• Short-term planning (B)

This section´s objective is to give a picture of the company’s annual planning process which

includes determining what activities should be taken in the coming twelve months and what

resources that are required for doing that. Questions like which person in the company that sets

short-term targets, how important it is to plan certain activities and how often action plans are

updated are included here

13

• Performance measurement and evaluation (C)

Accountability is seen as a crucial part here and the section is trying to establish how the

companies handle different decision-support systems. A great part of this involves both budgetary

systems and performance measurement systems. Questions in this part consist of to what extent

budgets are used, how detailed they are and what their purposes are.

• Organizational structure and management processes (E)

The direct aim with this section is to measure the internal management structure of the firm. Here

it is interesting to gain knowledge of how the management process functions, how rules and

procedures are used and what organization design is implemented. Typical questions in this part

are how the influence is balanced between the top management and the subordinates regarding

the decision process and who participates in the management teams.

• Organization culture and values (F)

The primary target for this section is to study how cultural control is used as a deliberate choice

from the management to shape the organization culture. Questions regarding promotions, skills

and technical competencies are brought up here.

• Organization and environment (G)

The last section tries to put the company in a context and establishing various variables that can

affect the use of MCSs. It also brings attention to how the company is competing, and if the

company has gone through any major changes lately.

However, since our focus was on reward and compensation systems (D), we decided to add some

more questions to this section in order to get a wider perspective and those are as follows:

- When was the reward and compensation system introduced?

- Why did you implement the reward and compensation system? Increase profit Increase sales Demand from employees

Increase innovation Recruit better competence Other reason

14

- What was the outcome of your reward and compensation system?

- Will you continue to use your reward and compensation system?

When it comes to the participating companies, we used the database “Affärsdata” where 150 of

the largest companies in Sweden from three different industries (engineering, service and

commercial) had been randomly selected. Since the service industry is the biggest industry in

Sweden followed by engineering industry and commercial industry, the sample consisted of 102

companies from the service sector, 33 from the engineering sector and finally 15 from the

commercial sector. The same proportions were used when we made our final selection regarding

which companies that were going to participate in the study. 15 companies participated in the

study which means ten were from the service industry, three from engineering and two from

commercial industry. We chose this kind of selection in order to get the right proportions for our

study and a result that was equal to reality. Naturally, we could have interviewed more than 15

companies but since we could not get in touch with more than two companies from the

commercial industry, we believed that 15 were enough in order to maintain the proportions.

We started by looking at the companies’ websites to get a brief overview of their organizations

and business areas. Consequently, this facilitated the dialogue in the interviews since we were

able to relate the questions to each company and we were also prepared to ask relevant follow-up

questions if needed. Thereafter, we contacted the companies by phone and we usually talked to

the business controller or the CFO of the companies and asked if they were interested in

participating in the study. If so, we e-mailed the questionnaire so they could read through it

before we called them a second time for the interview, which usually took about one hour to

accomplish.

After the interview process, we reviewed our findings and compared different parts of the survey

by accomplishing correlation analysis, which are compiled into tables (see Chapter 5). The reason

why we used correlation analysis was that we believed that this was an adequate method to use in

15

order to investigate if there existed some kind of linkages between reward and compensation

systems and other control systems.

2.3 Explanatory investigation method

As a researcher, there are numerous of investigation methods that can be used and how the

investigation is going to proceed depends on how much knowledge there is within the area. If

there are gaps in the knowledge, an explorative approach is suitable in order to fill those gaps.

Briefly, one can say that an explorative investigation is all about collecting or obtaining as much

knowledge as possible. If there already exists enough knowledge and this has been classified, the

investigation can instead have a descriptive approach. Another example is the explanatory

approach which differs from the two other approaches, since this one goes beyond the descriptive

and explorative approaches and tries to identify the reasons why certain phenomenon occurs. In

other words, the aim of an explanatory approach is to answer the question of why. (Patel &

Davidson, 2003)

Since the purpose of the study was to investigate connections and patterns between reward and

compensation systems and other parts in the MCS package, we thought that it was important that

we collected a lot of information. However, we strove to explain why we got certain findings and

therefore we first and foremost used an explanatory approach. Naturally, there are also

descriptive elements included since we aim to describe our findings in the analysis section.

2.4 Primary and secondary data

When writing a thesis, there are two types of data; primary data and secondary data (Andersen,

1998). Primary data can be seen as an initial source, which means that the information comes

from a person that has participated in the studied situation or event himself. Two examples of this

type of data are when the researcher conducts interviews or reads diaries. Secondary data in turn

is, precisely what it sounds like, a secondary source. This means that the information that is

provided is coming from a person that did not participate during the situation or event and this

16

information can instead be related to articles or other reports (Jacobsen, 2002). Since a big part of

our study is built on interviews we mostly used primary data for the data collection. Of course,

we also read a lot of articles and books to complement the interviews which means that there is

also secondary data included in the thesis.

2.5 Validity and reliability

It is very important that a study is perceived as trustworthy and therefore the validity and

reliability have to be high. Validity and reliability is related to each other which means that the

researcher cannot just focus on one of them. (Patel & Davidson 2003)

2.5.1 Validity

Validity contains of two other terms; availability and relevance. The general agreement that exist

between theory and empirical findings is the same as availability, while the relevance tells you

how relevant the empirical sample is for the problem statement. (Andersen, 1998)

Availability and relevance mean that our measures actually follow our intended purpose, that the

measurements are perceived as relevant and finally that what we measure for a few objects also is

applicable for measures with more objects. (Jacobsen, 2002)

Our idea with the study was to interview companies to obtain essential information and thereafter

accomplish different measures based on this information. In order to achieve validity, we added

some questions in the survey regarding reward and compensation since this was our main

approach for the study.

It can always be discussed if we asked the right kind of questions and if we would have got a

different outcome with other questions. Also, it is important to strongly link the theoretical

purpose with the practical execution of the survey. Our intention with the survey was e.g. to find

out how the companies handled its strategic planning and therefore, we needed question like how

long the strategic planning period is, how detailed ends and means are etc.

17

2.5.2 Reliability

Reliability stresses to what extent the results from different measures are affected by

coincidences and how clear and precise the results are. In other words, the researcher has to make

sure that the measures do not contain unreliable circumstances. One can therefore state that

reliability is about how trustworthy the information is and whether repeated investigations will

lead to the same result or not. (Andersen, 1998; Bryman & Bell, 2003)

Since we accomplished interviews and talked to people with good insight in the different

companies, the reliability regarding our results and findings is enhanced. Furthermore, we have

described the whole process of the study in order to make it even more reliable.

18

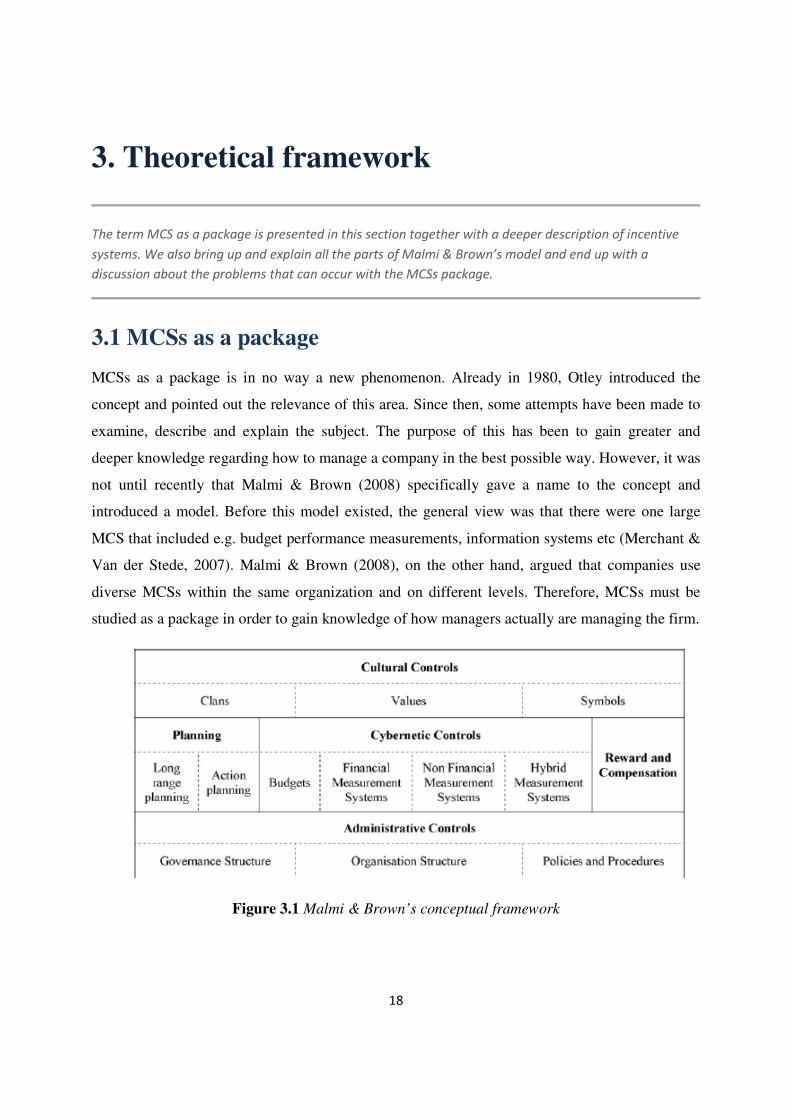

3. Theoretical framework

The term MCS as a package is presented in this section together with a deeper description of incentive

systems. We also bring up and explain all the parts of Malmi & Brown’s model and end up with a

discussion about the problems that can occur with the MCSs package.

3.1 MCSs as a package

MCSs as a package is in no way a new phenomenon. Already in 1980, Otley introduced the

concept and pointed out the relevance of this area. Since then, some attempts have been made to

examine, describe and explain the subject. The purpose of this has been to gain greater and

deeper knowledge regarding how to manage a company in the best possible way. However, it was

not until recently that Malmi & Brown (2008) specifically gave a name to the concept and

introduced a model. Before this model existed, the general view was that there were one large

MCS that included e.g. budget performance measurements, information systems etc (Merchant &

Van der Stede, 2007). Malmi & Brown (2008), on the other hand, argued that companies use

diverse MCSs within the same organization and on different levels. Therefore, MCSs must be

studied as a package in order to gain knowledge of how managers actually are managing the firm.

Figure 3.1 Malmi & Brown’s conceptual framework

19

Even if Malmi & Brown were first to introduce a conceptual framework on this area of science,

their work has its origin in several of previous conducted studies (Fisher, 1995 & 1998;

Flamholtz et al, 1985; Chenhall, 2003; Langfield-Smith, 1997). These studies, however, have not

been able to significantly increase the knowledge on the area of MCSs as a package. Therefore,

this model fills a gap in this area of business administration research. With this stated, the model

should not be regarded as a final solution on how to study MCSs as a package, but rather be seen

as a tool to encourage and stimulate continued discussion on the area. (Malmi & Brown, 2008)

Even if the model in Figure 3.1 recently has been introduced, the elements of the model are not

new. Each individual part of the MCS package has been previously investigated and examined

consistently in the literature (Malmi & Brown, 2008). Moreover, the different aspects of

contextual and environmental influences have been intensely studied which means that there

exists a great understanding regarding the various MCSs and in what context they operate, but

not in what way they affect the reward and compensation system. A situation like this tend to be

rather problematic since vital knowledge is missing on this area and MCSs, if used properly, may

be very advantageous for a company’s overall performance (Simons, 1990).

The model constructed by Malmi & Brown (2008) is, as can be observed, constructed by five

categories; cultural controls, planning, cybernetic controls, reward and compensation and

administrative controls. These are equally important parts of the package and will be described

and explained to give a clear picture of the model.

3.1.1 Culture

Culture can impose a very strong control within a company and functions as a guide for how

employees should act. It is, however, hard for a company to explicitly construct a specific culture

since it is often made up by several other factors like employees and their skills, history and

context. According to Malmi & Brown (2008), culture control is made up by three different parts

categorized as clan control, value control and symbolic control. In the concept of clan control,

phenomena like languages, everyday behavior and rituals are most frequently mentioned. Every

organization uses in some extent their own internal language, but language is also about how the

company communicates to its customers and what various stakeholders say about the company.

20

The case is that there is hardly ever an organizational culture that resembles of another

organizational culture, which has led to the fact that an organizations culture can become a

competitive advantage (David, 1990). This can be an interesting fact since if this is the case, there

should be some coherency between the organization and the planning process.

3.1.2 Planning

When it comes to achieving targets, one of the most important factors for a company is to have

some sort of goal convergence between the employees and the organization´s goals. This is

mainly done by planning and this can be undertaken in mainly two ways. Either, the planning is

directed from the HQ or the employees are directly involved in the planning process. Regardless

of how the planning is executed, it functions as a very clear guide for what is vital to focus on and

what employees should prioritize. (Papke-Shields, 2006; Spee et al, 2011)

It has been proved to be rather hard to properly examine what planning consists of (REF) and the

role planning plays in the organization. Companies are often using a wide range of planning tools

depending on the purpose and which people in the organization that are involved in the process.

(Minzberg, 1994). Moreover, the strategic planning and budget planning has in some cases

proved not to be interconnected to each other (Blumentritt, 2006).

When describing planning as a control tool it is often stated to include both strategic planning and

short-term planning. Strategic planning often expands over a time between 1-5 years whereas

short-term planning is dealing with the related time up to twelve months. When dealing with

strategic planning, one must be aware of the fact that it can be used for two different purposes.

Firstly, it can be used and implemented with the aim to declare in what activities the firm will

engage in the future. Secondly, it can be used to involve employees in a process which have the

goal to integrate the employees’ targets with the organizational targets (Malmi & Brown, 2008:

Bonn & Christodoulou, 1999).

A consequence is that strategic planning may not always be linked to financial measures or goals.

Therefore, it is essential that a distinction is made between planning as a mean to motivate the

employees and to make accurate decisions for the future. To fully understand strategic planning it

21

is also important to be aware of the fact that strategies are created and implemented by using

different techniques. The two mainly ways of distinguishing the creation of strategies is either to

use top-down approach or bottom-up approach. The first way involves the employees in the

creation of a competitive strategy, whereas the second leaves the decision to the top management

so the employees just have to implement it. Of course, there exists a wide range of mixture of

these two ways e.g. when top management set the ends and employee set the means etc

(Gundlach, 1974).

3.1.3 Cybernetic control

The cybernetic control includes different formalized methods to execute control within an

organization. The most common and frequently used technique is to use financial measurements

as budgets, target costing, activity based costing etc. Regarding the functionality of cybernetic

control, information and sharing of this information is a very essential factor (Dobre, 2007).

If the correct information is not distributed through the organization the company holds an

insufficient control system. As a consequence, the company is not using its full potential and the

cybernetic control does not support the other MCSs. (Holm, 2007; Rowe, 2010)

When describing the concept of cybernetic control, it is often seen as a process which includes

collecting, managing and presenting relevant and reliable information. This will later on be used

to correct and improve subordinates’ behavior towards the company’s objectives. Malmi and

Brown chose to divide the cybernetic control into four different measures; budgets, financial

measurements, non-financial measurements and hybrid measures. Hybrid measures include both

financial and non-financial measurements and one good example is balanced scorecard.

Moreover, depending on which cybernetic control mechanism that is used and how it is

constructed, cybernetic control can be both a very detailed or a very flexible control tool. A

company can e.g. include information from various levels within the company and at the same

time use external information from competitors for benchmarking. When companies use different

sources for information, the purpose of the cybernetic control is often very broad. It can either be

to promote learning and improvements of forthcoming activities or to reward and compensate

subordinates.

22

3.1.4 Administrative control

The aim of using administrative control is to create effective and efficient groups within the

organization, which can be done in several ways and of course differ between different

organizations. One way is to include a wide range of managers and experts when arranging

management group meetings. Another way is to have multiple ways of reporting to managers and

colleagues on different levels. The concept of administrative control can be categorized in three

explicit sub-objects; management process, organization design and rules & procedures.

Management process is stated to be of essential importance for a firm’s profitability and the

process must therefore have a clear structure. This structure regards both short-term decisions

like everyday meeting and long-term decisions like whom to employ and how to fulfill the

strategy (Brimson, 2011). When it comes to organization design, the dominant element is to

create ways of communicating and creating linkages for employee contact and relationship

building (Martin, 1992). The last concept, rules & procedures, is dealing with the more

formalized part of administrative control. Several companies use documented manuals and rules

that are written down to steer or guide the employees to execute their work so that it is in line

with the goals of the organization. These three concepts have the explicit purpose of guiding and

directing employees’ behavior so that right actions are taken place within the organization.

Empirical studies further indicate that organizations and managers actually aim to use all three

concepts, but sometimes fail to properly execute its intention (Alvesson & Karreman, 2004;

Merchant & Van der Stede, 2007).

3.1.5 Incentive systems

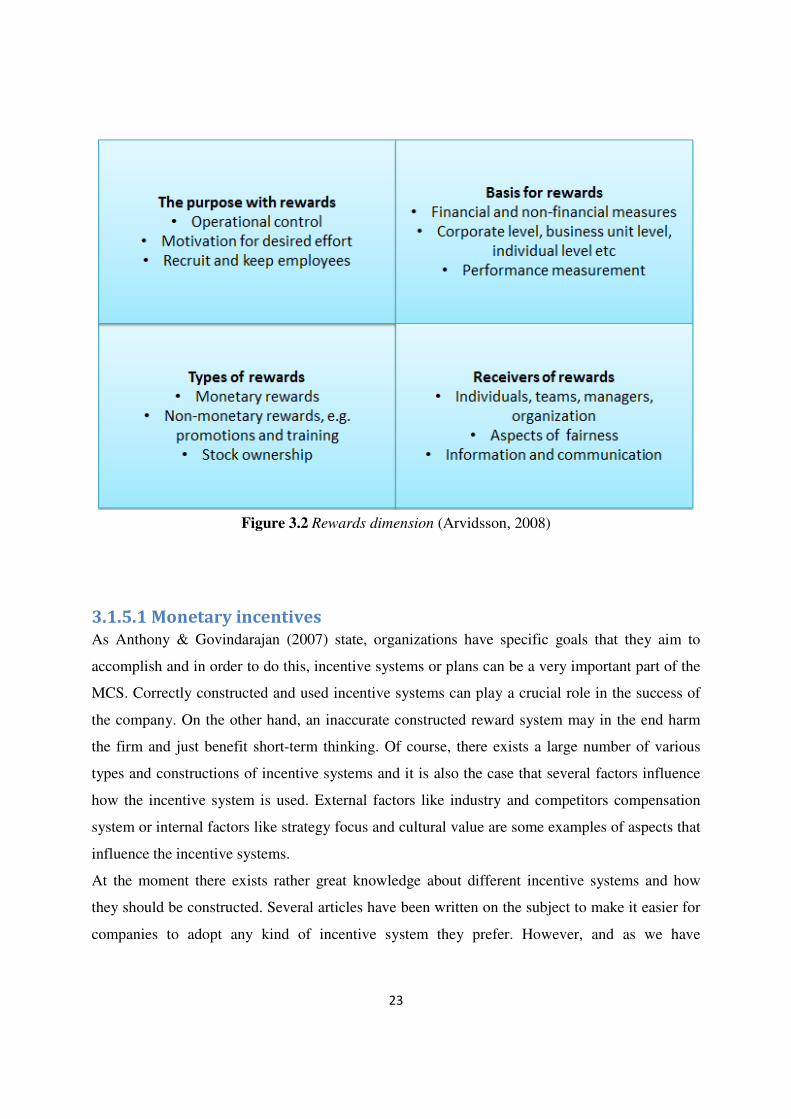

To start with, it must be stated that the concept reward and compensation equals of both incentive

systems and bonus systems. The reward and compensation systems can have different purposes,

different construction, different basis and different receivers. Some of the varieties are presented

in Figure 3.2, which include various combinations and dimensions and with this in mind it one

can see that there exist a wide range of different reward and compensation systems.

23

Figure 3.2 Rewards dimension (Arvidsson, 2008)

3.1.5.1 Monetary incentives

As Anthony & Govindarajan (2007) state, organizations have specific goals that they aim to

accomplish and in order to do this, incentive systems or plans can be a very important part of the

MCS. Correctly constructed and used incentive systems can play a crucial role in the success of

the company. On the other hand, an inaccurate constructed reward system may in the end harm

the firm and just benefit short-term thinking. Of course, there exists a large number of various

types and constructions of incentive systems and it is also the case that several factors influence

how the incentive system is used. External factors like industry and competitors compensation

system or internal factors like strategy focus and cultural value are some examples of aspects that

influence the incentive systems.

At the moment there exists rather great knowledge about different incentive systems and how

they should be constructed. Several articles have been written on the subject to make it easier for

companies to adopt any kind of incentive system they prefer. However, and as we have

24

mentioned before, almost no one have investigated how incentive systems is linked and

integrated with other parts of the MCSs. (Berry et al, 2008)

The aim of creating and using incentive systems vary and depends on the purpose of the

company. When using rewards for the employees e.g. in connection to sales, the employees are

clearly informed of what is important for the company. If companies want their employees to

perform above average, they may have to use some kind of reward systems to motivate them.

Merchant & Van der Stede (2007) discuss three different categories of management control

benefits; informational, motivational and personnel-related. Companies often want to attract high

performing employees and therefore use reward systems as a part of their personnel control

system. (Arvidsson, 2008). Furthermore, Merchant and Van der Stede (2007) express a rather

advantageous picture of incentive system stating that: “performance-dependent rewards are an

important part of the results-control contracts used to direct employees´ behaviors”.

With this in mind, the overall point of view regarding the purpose of creating invective systems is

to increase profit (Mahy, 2005). Not everyone, however, expresses the similar positive view of

rewards system but also highlight some risks. The most optimal incentive system should base the

rewards on figures that the employees have direct influence over, but to construct an incentive

system like this may be difficult since the question about who are affecting what always will

arise. A theory that is often used, when describing the problematic situation regarding rewards

systems, is the agency theory. This theory claims that a reward system must balance three factors

to accomplish a reliable system. The first factor is called incentive and consists of the fact that a

manager tries to maximize the performance metric that is measured. The second one, risk, points

out that the more uncontrollable factors included in the reward system the more risk the managers

bear. The last one, cost of measuring performance, states that there are trade-offs between

incentive and risks. It can be very costly for a company to precisely measure an employee’s

performance and therefore it has to rely on imperfect information. (Horngren et al, 2011)

The question is further complicated by the fact that there exist wide ranges of different mix of

incentive systems, e.g. individual rewards, organizational-based incentives, recognition and

external measures. Studies suggest that a mixture of those is to prefer, even though an incentive

system that contain individual rewards that are clearly linked to organizational-based incentives,

25

is regarded as a key concept for a firm´s success. (Allen & Helms, 2001; Daugherty, 2010). In the

discussion about incentive systems, cognitive theories can also be applied in order to deepen and

expand the concept. Here, the individual opinion about itself and the surroundings is a crucial

element for the understanding of motivating people. As a consequence, an incentive system must

never be generally standardized, but it must be tailor made for each employee (Arvidsson, 2008).

3.1.5.2 Non-monetary incentives

It is essential to mention that an incentive system can include other rewards than financial. One

such reward is e.g. promotion which may be the result of good work and goal convergence.

However, it is often the case that the employee does not know about this reward in advance,

which means that it is not formally included in the incentive system. (Horngren et al, 2011)

It can also be claimed that non-monetary rewards are more effective than financial rewards, since

most of the employees highly appreciate encouraging words and to be involved in the working

process. (Wiscombe, 2002). On the other hand, studies on this field that compare financial and

non-financial incentives show that financial rewards influence the performance to a greater extent

than non-financial rewards. In some studies the performance increase was twice as high when

applying financial rewards compared to the usage of non-financial rewards. It must, however, be

pointed out that financial rewards were four times more frequently studied (Condly, 2003).

Non-monetary rewards are more related to a firm’s long-term goals and ability to be profitable,

compared to financial rewards that are closely linked to short-term profit. Despite this, there has

not been that much research conducted in the area of non-monetary incentive systems. (Banker et

al, 2000). Several managers have, in addition, been rewarded based on subjective factors and

have become an essential substitute for formula based rewards. Bonuses built on subjectivity are

often said to reduce risk and to extend the tenure at the company (Gibbs et al, 2003). However, it

may be difficult to implement non-monetary rewards in the model by Malmi & Brown. The

difficulty also comprise of the fact that this incentive system consists of both explicit and implicit

instruments that tend to interrelate with each other (Gibbs et al, 2009)

As mentioned above, non-financial rewards are stated to have other objectives than financial

ones. One such objective is not directly related to increase performance but has the purpose to

26

increase work satisfaction and implement a thinking that involves the employees in the

organization to a higher extent. With this stated, it should be observed that higher work

satisfaction often also increase the performance since people who are enjoying their work tend to

outperform those who are not. (Sonawnae, 2008; Mahy, 2005; Berberian, 2008)

3.2 Problems regarding MCS package

Since the concept of MCS package contains several different aspects that are constantly changing

due to various contextual variables, it may be hard to properly investigate and eventually

formulate some kind of theory. The use of different accounting and management systems within a

firm has a direct influence on the behavior of the employee. On the contrary, employee behavior

and cultural context affect which MCS that is implemented.

The framework presented by Malmi and Brown (2008) can be seen as too broad since it includes

several different control mechanisms. As a consequence, it can be difficult to correctly

distinguish each control technique within the firms. Yet, Malmi & Brown (2008) convincingly

argued for the use of a broad model rather than using a too narrowed model that exclude

significant fact and linkages. Their reasoning is further supported by other researchers that claim

that too much attention has been given to individual control systems where the aim has been to

separately investigate these systems (Nandan, 1996: Macintosh, 1994: Whitley, 1999). The

subject which regards and examines companies’ strategies and the linkages to the other control

systems has previously been studied and the result demonstrates the difficulty of implementing

performance measurements that are accompanying the strategy. This is said to depend on the fact

that other more forceful control systems like organizational culture and context have a deeper

impact on the formation of e.g. performance measurements (Tuomela, 2005).

27

4. Empirical findings

This section displays a selection of our findings from the interview process and tables are included in

order to describe and clarify the result.

Since the questionnaire is confidential and consists of more than 200 questions we were not able

to include all of the questions and answers. However, we picked out some of the findings from

different sections of the questionnaire which we present in the tables below.

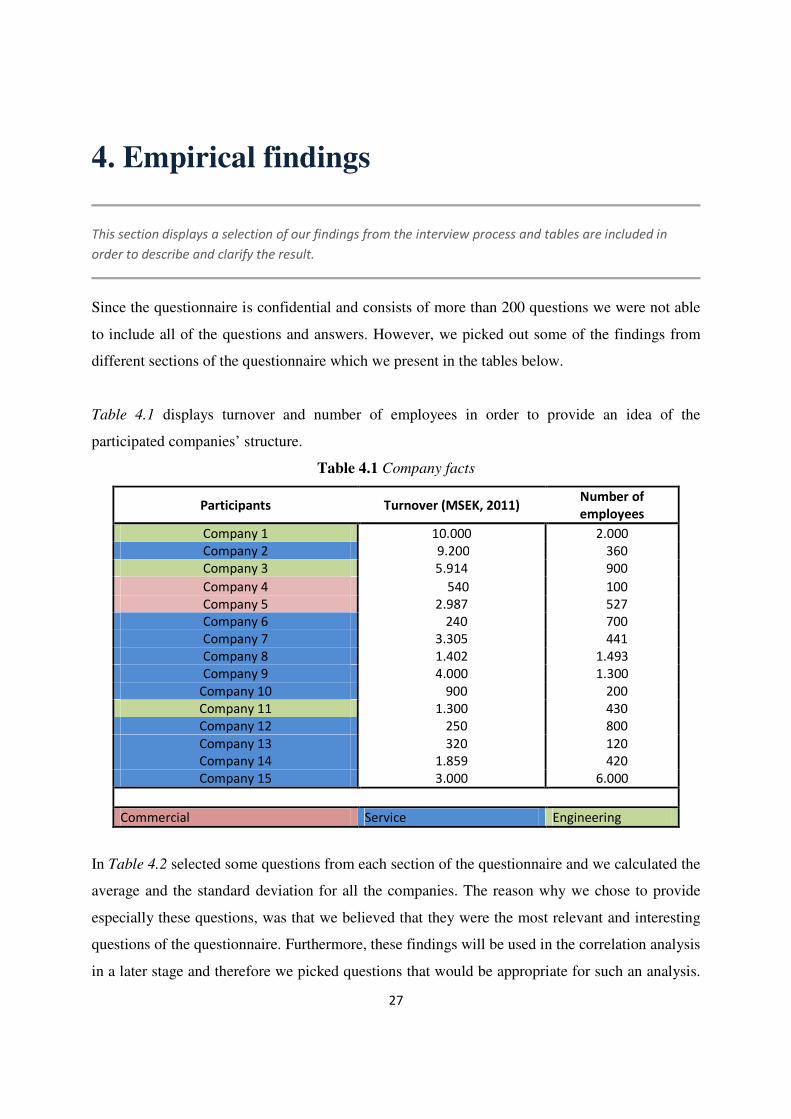

Table 4.1 displays turnover and number of employees in order to provide an idea of the

participated companies’ structure.

Table 4.1 Company facts

Participants Turnover (MSEK, 2011) Number of

employees

Company 1 10.000 2.000

Company 2 9.200 360

Company 3 5.914 900

Company 4 540 100

Company 5 2.987 527

Company 6 240 700

Company 7 3.305 441

Company 8 1.402 1.493

Company 9 4.000 1.300

Company 10 900 200

Company 11 1.300 430

Company 12 250 800

Company 13 320 120

Company 14 1.859 420

Company 15 3.000 6.000

Commercial Service Engineering

In Table 4.2 selected some questions from each section of the questionnaire and we calculated the

average and the standard deviation for all the companies. The reason why we chose to provide

especially these questions, was that we believed that they were the most relevant and interesting

questions of the questionnaire. Furthermore, these findings will be used in the correlation analysis

in a later stage and therefore we picked questions that would be appropriate for such an analysis.

28

All of the questions included in the table could be ranked from 1 to 7, except for the questions

regarding the duration of the reward and compensation systems and the size respectively. Some

interesting findings are that the participating companies value financial results high with an

average of 6,27 and that the companies use financial rewards (6,00) in a higher extent than non-

financial rewards (4,31). Furthermore, it is obvious that subordinates have not that much

influence when it comes to establishing new business (2,47) and compensation policies and

rewards (2,83). Finally, one can see that the average turnover of the companies are about 3.000

MSEK for 2011, which can be perceived as a bit misleading since the interval is between 240

MSEK and 10.000 MSEK for our interviewed companies.

Table 4.2 Selection of questions

Selection of questions Average

Standard

deviation

Weight of objectives 5,87 1,13 Extension of using quantitative ends 5,67 1,11 Importance of financial resource requirements 5,27 1,44

Importance of short-term planning when guiding and directing subordinates 5,33 1,11 Extension of basing subordinates' performance evaluation on financial measures 5,80 1,26 Importance of determine subordinate compensation 5,40 0,99 Extension of using predetermined criteria in evaluation and rewarding 5,85 1,28 Extension of financial rewarding 6,00 1,00 Extension of non-financial rewarding 4,31 1,55 Number of years since the reward and compensation system was introduced 7,57 5,07 Subordinates' influence when establishing new businesses 2,47 1,06

Subordinates' influence regarding compensation policy and rewards 2,83 1,47

Extension of leadership-based performance connected to significant rewards 4,80 1,61 Importance of values and organization culture when guiding and directing 6,07 0,70 Importance of financial results 6,27 0,88

Size, based on turnover (MSEK) 3014,47 3123,54

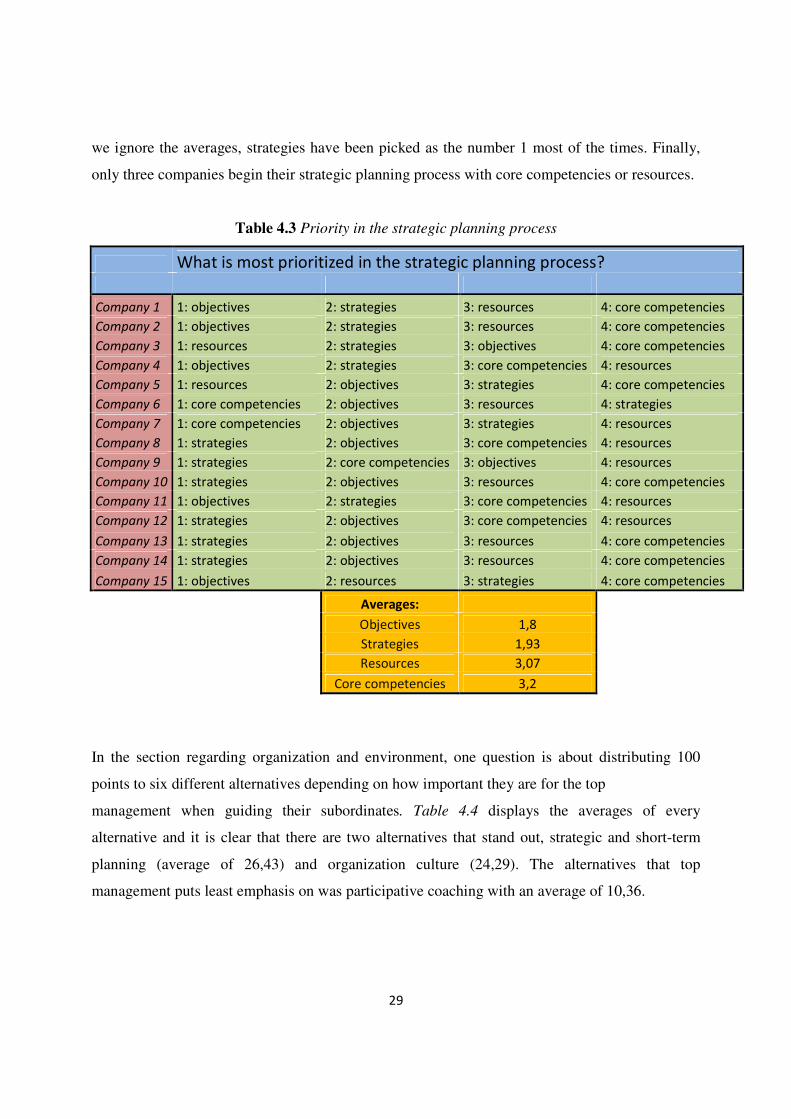

Regarding the strategic planning process, the interviewee was asked to list in which order

strategies, resources, core competencies and objectives come when making strategic plans. The

most important was marked 1 and the least important was marked 4. Table 4.3 illustrates the

findings and when looking at the result, one observes that almost every company starts their

strategic planning process with either objectives (average of 1,8) or strategies (1,93). However, if

29

we ignore the averages, strategies have been picked as the number 1 most of the times. Finally,

only three companies begin their strategic planning process with core competencies or resources.

Table 4.3 Priority in the strategic planning process

What is most prioritized in the strategic planning process?

Company 1 1: objectives 2: strategies 3: resources 4: core competencies

Company 2 1: objectives 2: strategies 3: resources 4: core competencies

Company 3 1: resources 2: strategies 3: objectives 4: core competencies

Company 4 1: objectives 2: strategies 3: core competencies 4: resources

Company 5 1: resources 2: objectives 3: strategies 4: core competencies

Company 6 1: core competencies 2: objectives 3: resources 4: strategies

Company 7 1: core competencies 2: objectives 3: strategies 4: resources

Company 8 1: strategies 2: objectives 3: core competencies 4: resources

Company 9 1: strategies 2: core competencies 3: objectives 4: resources

Company 10 1: strategies 2: objectives 3: resources 4: core competencies

Company 11 1: objectives 2: strategies 3: core competencies 4: resources

Company 12 1: strategies 2: objectives 3: core competencies 4: resources

Company 13 1: strategies 2: objectives 3: resources 4: core competencies

Company 14 1: strategies 2: objectives 3: resources 4: core competencies

Company 15 1: objectives 2: resources 3: strategies 4: core competencies

Averages:

Objectives 1,8

Strategies 1,93

Resources 3,07

Core competencies 3,2

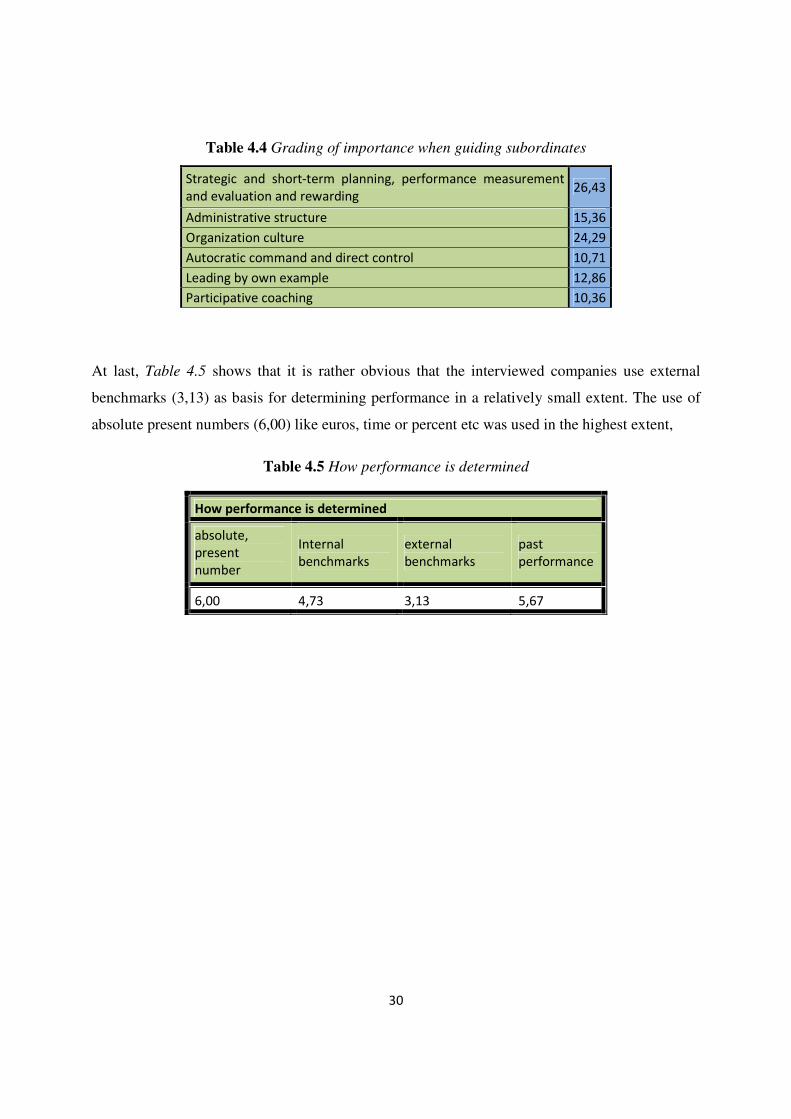

In the section regarding organization and environment, one question is about distributing 100

points to six different alternatives depending on how important they are for the top

management when guiding their subordinates. Table 4.4 displays the averages of every

alternative and it is clear that there are two alternatives that stand out, strategic and short-term

planning (average of 26,43) and organization culture (24,29). The alternatives that top

management puts least emphasis on was participative coaching with an average of 10,36.

30

Table 4.4 Grading of importance when guiding subordinates

Strategic and short-term planning, performance measurement

and evaluation and rewarding 26,43

Administrative structure 15,36

Organization culture 24,29

Autocratic command and direct control 10,71

Leading by own example 12,86

Participative coaching 10,36

At last, Table 4.5 shows that it is rather obvious that the interviewed companies use external

benchmarks (3,13) as basis for determining performance in a relatively small extent. The use of

absolute present numbers (6,00) like euros, time or percent etc was used in the highest extent,

Table 4.5 How performance is determined

How performance is determined

absolute,

present

number

Internal

benchmarks

external

benchmarks

past

performance

6,00 4,73 3,13 5,67

31

5. Analysis

In this chapter we start by making a descriptive analysis from the findings of the reward and

compensation part. Thereafter, we test the linkages between reward and compensation and the other

parts of the MCS package by using correlation analysis. Like the previous section, we provide tables in

order to strengthen our arguments.

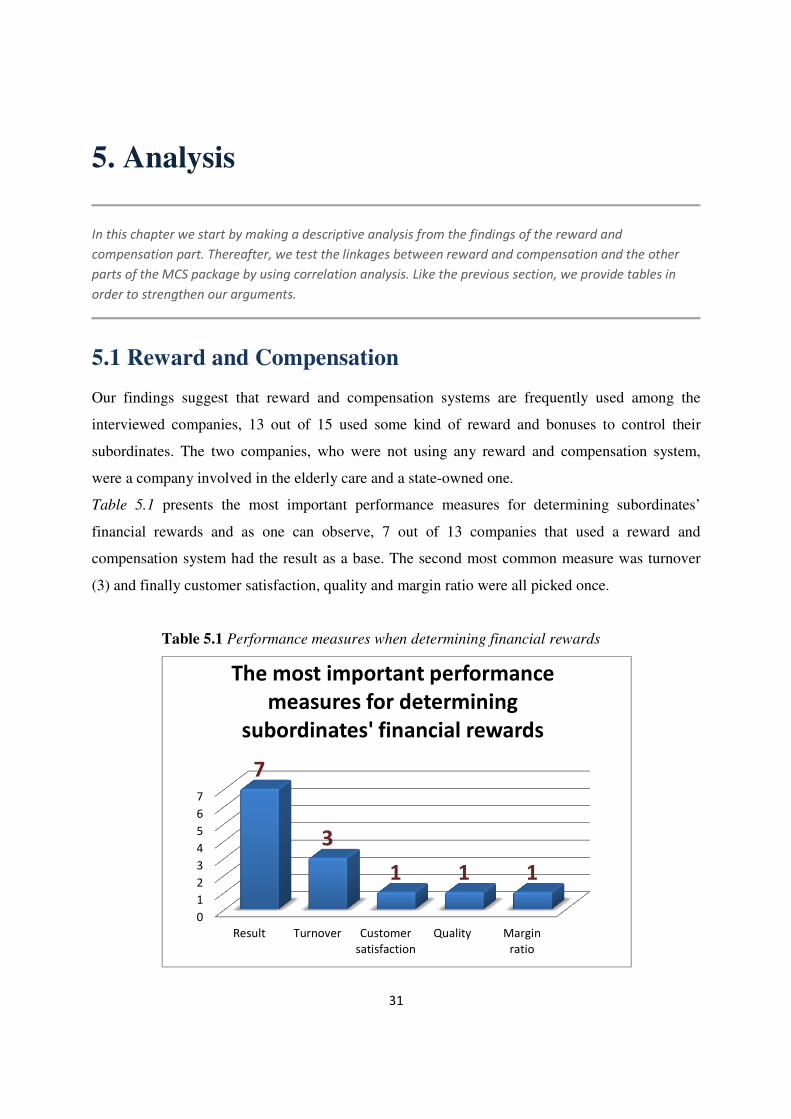

5.1 Reward and Compensation

Our findings suggest that reward and compensation systems are frequently used among the

interviewed companies, 13 out of 15 used some kind of reward and bonuses to control their

subordinates. The two companies, who were not using any reward and compensation system,

were a company involved in the elderly care and a state-owned one.

Table 5.1 presents the most important performance measures for determining subordinates’

financial rewards and as one can observe, 7 out of 13 companies that used a reward and

compensation system had the result as a base. The second most common measure was turnover

(3) and finally customer satisfaction, quality and margin ratio were all picked once.

Table 5.1 Performance measures when determining financial rewards

0

1

2

3

4

5

6

7

Result Turnover Customer

satisfaction

Quality Margin

ratio

7

3

1 1 1

The most important performance

measures for determining

subordinates' financial rewards

32

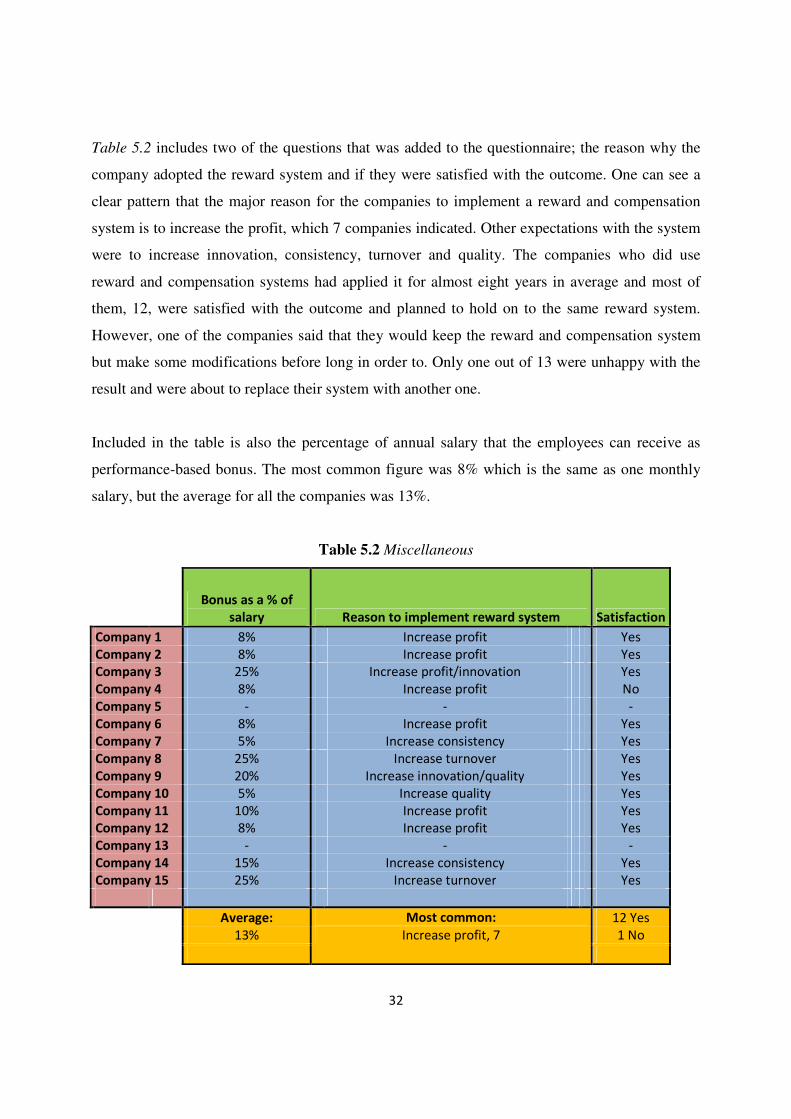

Table 5.2 includes two of the questions that was added to the questionnaire; the reason why the

company adopted the reward system and if they were satisfied with the outcome. One can see a

clear pattern that the major reason for the companies to implement a reward and compensation

system is to increase the profit, which 7 companies indicated. Other expectations with the system

were to increase innovation, consistency, turnover and quality. The companies who did use

reward and compensation systems had applied it for almost eight years in average and most of

them, 12, were satisfied with the outcome and planned to hold on to the same reward system.

However, one of the companies said that they would keep the reward and compensation system

but make some modifications before long in order to. Only one out of 13 were unhappy with the

result and were about to replace their system with another one.

Included in the table is also the percentage of annual salary that the employees can receive as

performance-based bonus. The most common figure was 8% which is the same as one monthly

salary, but the average for all the companies was 13%.

Table 5.2 Miscellaneous

Bonus as a % of

salary Reason to implement reward system Satisfaction

Company 1 8% Increase profit Yes

Company 2 8% Increase profit Yes

Company 3 25% Increase profit/innovation Yes

Company 4 8% Increase profit No

Company 5 - - -

Company 6 8% Increase profit Yes

Company 7 5% Increase consistency Yes

Company 8 25% Increase turnover Yes

Company 9 20% Increase innovation/quality Yes

Company 10 5% Increase quality Yes

Company 11 10% Increase profit Yes

Company 12 8% Increase profit Yes

Company 13 - - -

Company 14 15% Increase consistency Yes

Company 15 25% Increase turnover Yes

Average: Most common: 12 Yes

13% Increase profit, 7 1 No

33

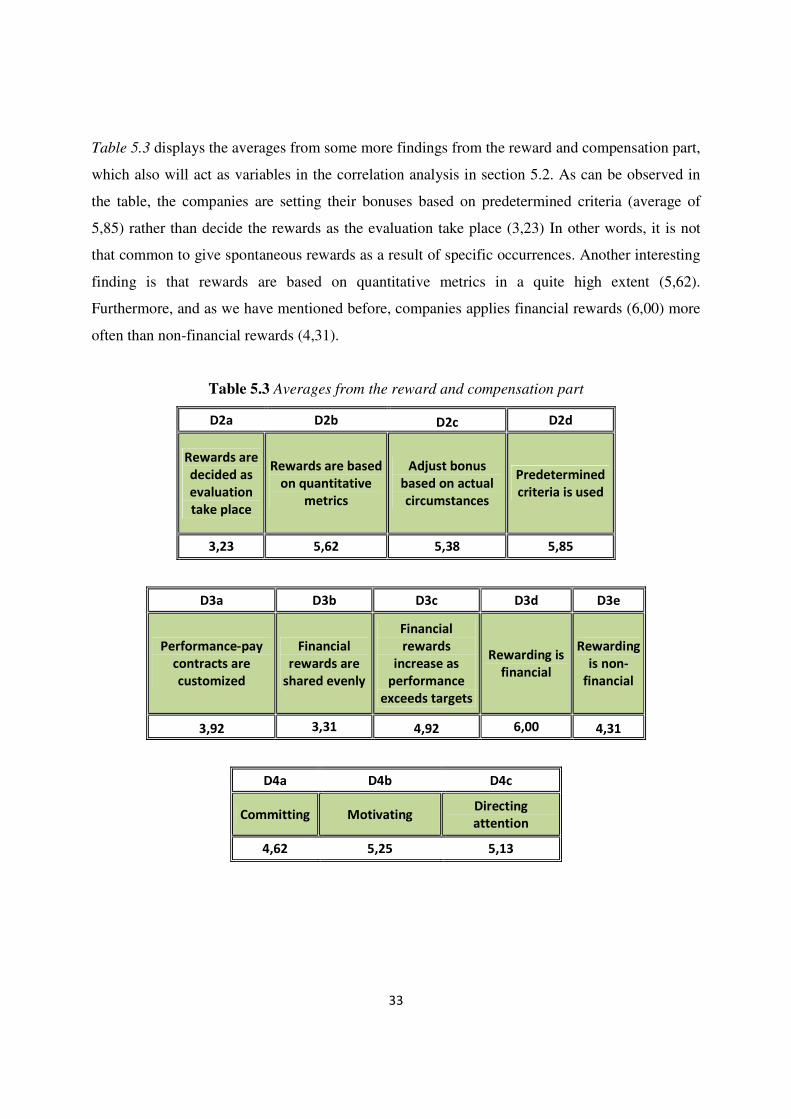

Table 5.3 displays the averages from some more findings from the reward and compensation part,

which also will act as variables in the correlation analysis in section 5.2. As can be observed in

the table, the companies are setting their bonuses based on predetermined criteria (average of

5,85) rather than decide the rewards as the evaluation take place (3,23) In other words, it is not

that common to give spontaneous rewards as a result of specific occurrences. Another interesting

finding is that rewards are based on quantitative metrics in a quite high extent (5,62).

Furthermore, and as we have mentioned before, companies applies financial rewards (6,00) more

often than non-financial rewards (4,31).

Table 5.3 Averages from the reward and compensation part

D2a D2b D2c D2d

Rewards are

decided as

evaluation

take place

Rewards are based

on quantitative

metrics

Adjust bonus

based on actual

circumstances

Predetermined

criteria is used

3,23 5,62 5,38 5,85

D3a D3b D3c D3d D3e

Performance-pay

contracts are

customized

Financial

rewards are

shared evenly

Financial

rewards

increase as

performance

exceeds targets

Rewarding is

financial

Rewarding

is non-

financial

3,92 3,31 4,92 6,00 4,31

D4a D4b D4c

Committing Motivating Directing

attention

4,62 5,25 5,13

34

5.2 Correlation analysis

As the purpose states, the aim is to describe and explain possible linkages or relations between

the reward and compensation and the other part of the MCS package. In order to further do this

we chose to use correlation analysis as a mean to investigate how different parts of the MCS

package are correlated with reward and compensation system. The scale in a correlation analysis

is between -1 and 1, where -1 means that there is a perfect negative relationship, 1 that there is a

perfect positive relationship and 0 that there is not a relationship at all (Körner, Wahlgren, 2007).

In each section we have included the numerical questions from the reward and compensation part

in the questionnaire, see Table 5.3. Also, two questions that strongly represent the respective

section are included when we accomplish the correlation analysis.

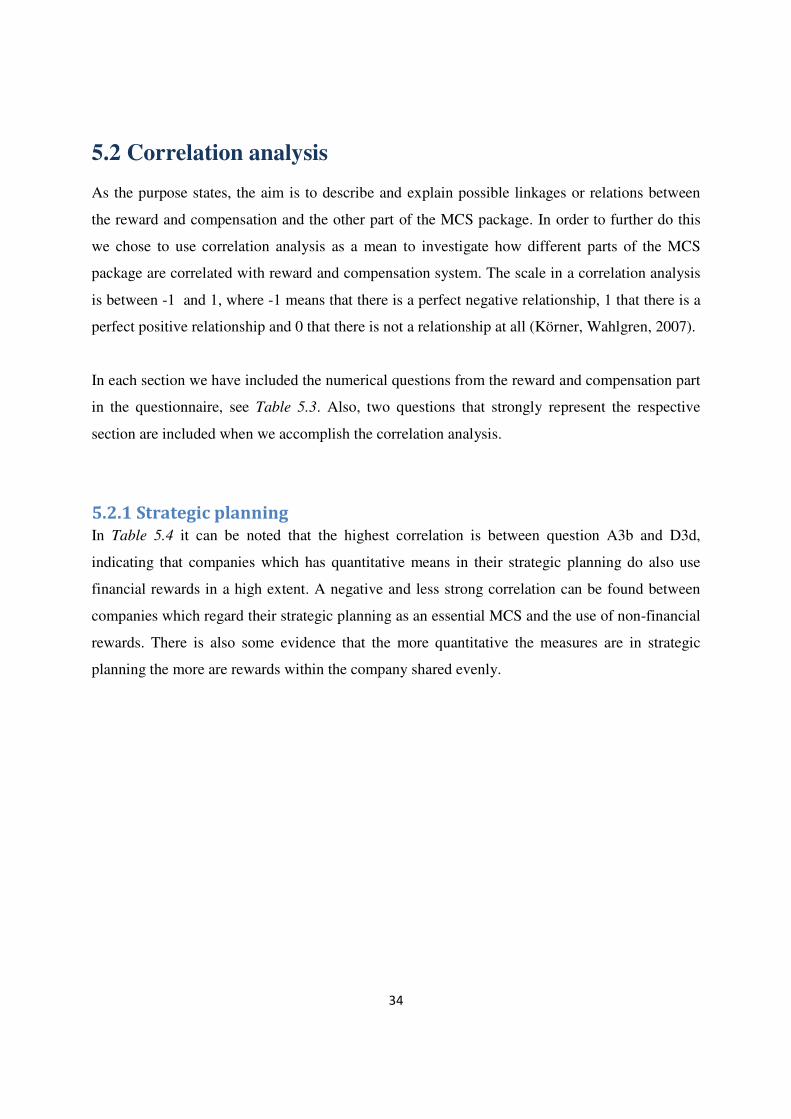

5.2.1 Strategic planning

In Table 5.4 it can be noted that the highest correlation is between question A3b and D3d,

indicating that companies which has quantitative means in their strategic planning do also use

financial rewards in a high extent. A negative and less strong correlation can be found between

companies which regard their strategic planning as an essential MCS and the use of non-financial

rewards. There is also some evidence that the more quantitative the measures are in strategic

planning the more are rewards within the company shared evenly.

35

Table 5.4 Correlation analysis for strategic planning

A

A2

How significant

different categories are

for the strategic

planning

A3b

How quantitative the

means in the strategic

planning are

D2a -0,28 -0,01

D2b -0,27 0,16

D2c -0,68 -0,17

D2d -0,17 0,46

D3a 0,05 -0,01

D3b -0,04 0,54

D3c 0,18 -0,20

D3d -0,49 0,61

D3e 0,06 0,49

D4a 0,06 0,42

D4b -0,02 0,36

D4c 0,23 0,42

D5a 0,06 0,06

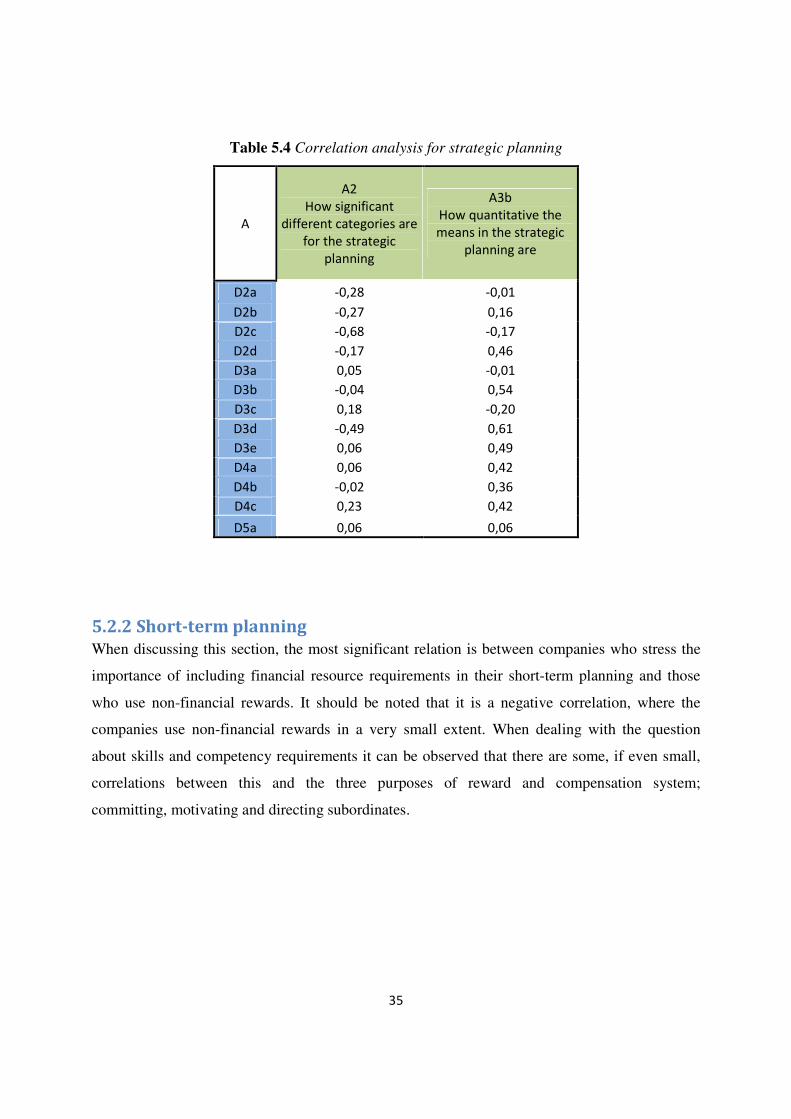

5.2.2 Short-term planning

When discussing this section, the most significant relation is between companies who stress the

importance of including financial resource requirements in their short-term planning and those

who use non-financial rewards. It should be noted that it is a negative correlation, where the

companies use non-financial rewards in a very small extent. When dealing with the question

about skills and competency requirements it can be observed that there are some, if even small,

correlations between this and the three purposes of reward and compensation system;

committing, motivating and directing subordinates.

36

Table 5.5 Correlation analysis for short-term planning

B Financial resource requirements Skills and competency

requirements

D2a -0,24 -0,33

D2b 0,37 -0,34

D2c -0,34 0,04

D2d 0,38 -0,18

D3a 0,10 -0,30

D3b -0,31 -0,18

D3c 0,20 -0,13

D3d -0,27 -0,06

D3e -0,49 0,30

D4a -0,34 0,36

D4b -0,25 0,40

D4c -0,60 0,31

D5a 0,15 0,42

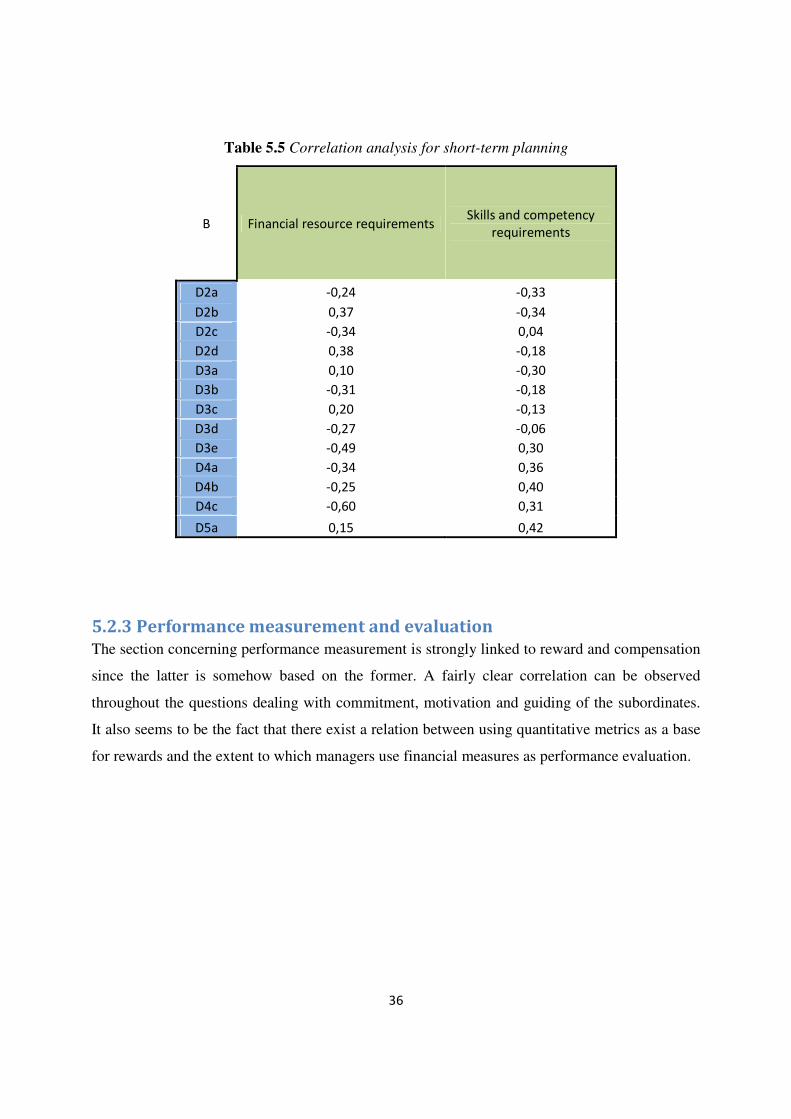

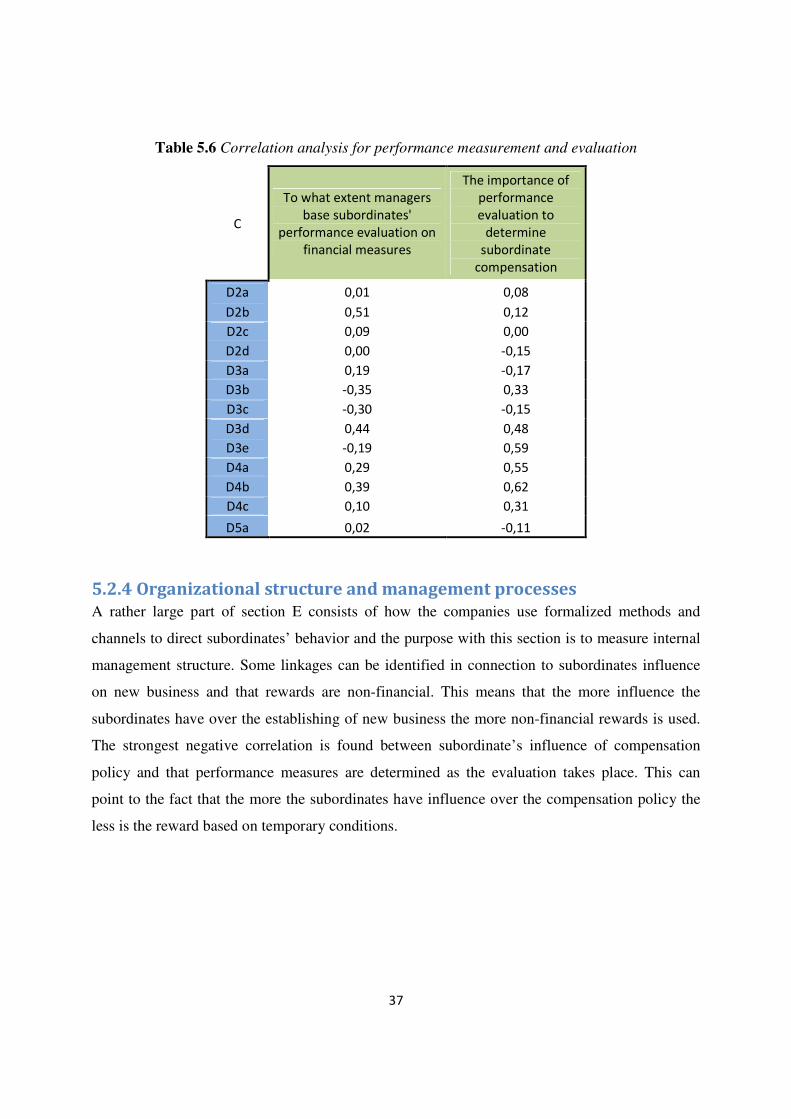

5.2.3 Performance measurement and evaluation

The section concerning performance measurement is strongly linked to reward and compensation

since the latter is somehow based on the former. A fairly clear correlation can be observed

throughout the questions dealing with commitment, motivation and guiding of the subordinates.

It also seems to be the fact that there exist a relation between using quantitative metrics as a base

for rewards and the extent to which managers use financial measures as performance evaluation.

37

Table 5.6 Correlation analysis for performance measurement and evaluation

C

To what extent managers

base subordinates'

performance evaluation on

financial measures

The importance of

performance

evaluation to

determine

subordinate

compensation

D2a 0,01 0,08

D2b 0,51 0,12

D2c 0,09 0,00

D2d 0,00 -0,15

D3a 0,19 -0,17

D3b -0,35 0,33

D3c -0,30 -0,15

D3d 0,44 0,48

D3e -0,19 0,59

D4a 0,29 0,55

D4b 0,39 0,62

D4c 0,10 0,31

D5a 0,02 -0,11

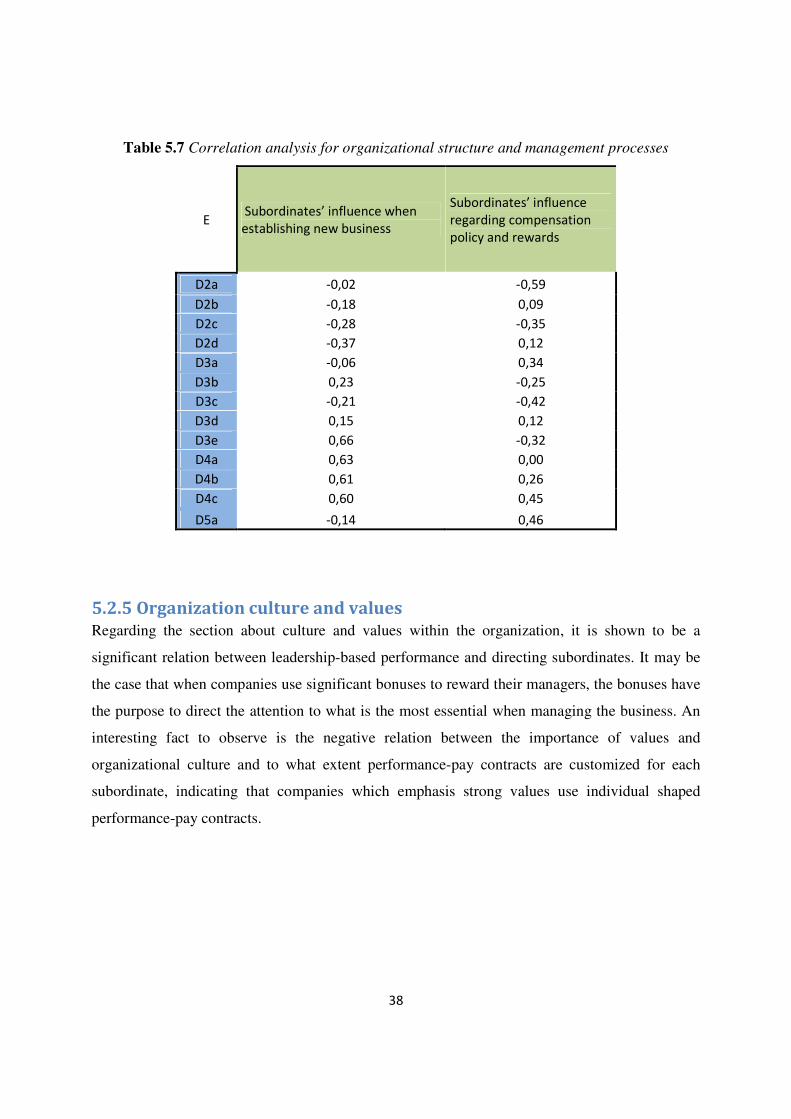

5.2.4 Organizational structure and management processes

A rather large part of section E consists of how the companies use formalized methods and

channels to direct subordinates’ behavior and the purpose with this section is to measure internal

management structure. Some linkages can be identified in connection to subordinates influence

on new business and that rewards are non-financial. This means that the more influence the

subordinates have over the establishing of new business the more non-financial rewards is used.

The strongest negative correlation is found between subordinate’s influence of compensation

policy and that performance measures are determined as the evaluation takes place. This can

point to the fact that the more the subordinates have influence over the compensation policy the

less is the reward based on temporary conditions.

38

Table 5.7 Correlation analysis for organizational structure and management processes

E Subordinates’ influence when

establishing new business

Subordinates’ influence

regarding compensation

policy and rewards

D2a -0,02 -0,59

D2b -0,18 0,09

D2c -0,28 -0,35

D2d -0,37 0,12

D3a -0,06 0,34

D3b 0,23 -0,25

D3c -0,21 -0,42

D3d 0,15 0,12

D3e 0,66 -0,32

D4a 0,63 0,00

D4b 0,61 0,26

D4c 0,60 0,45

D5a -0,14 0,46

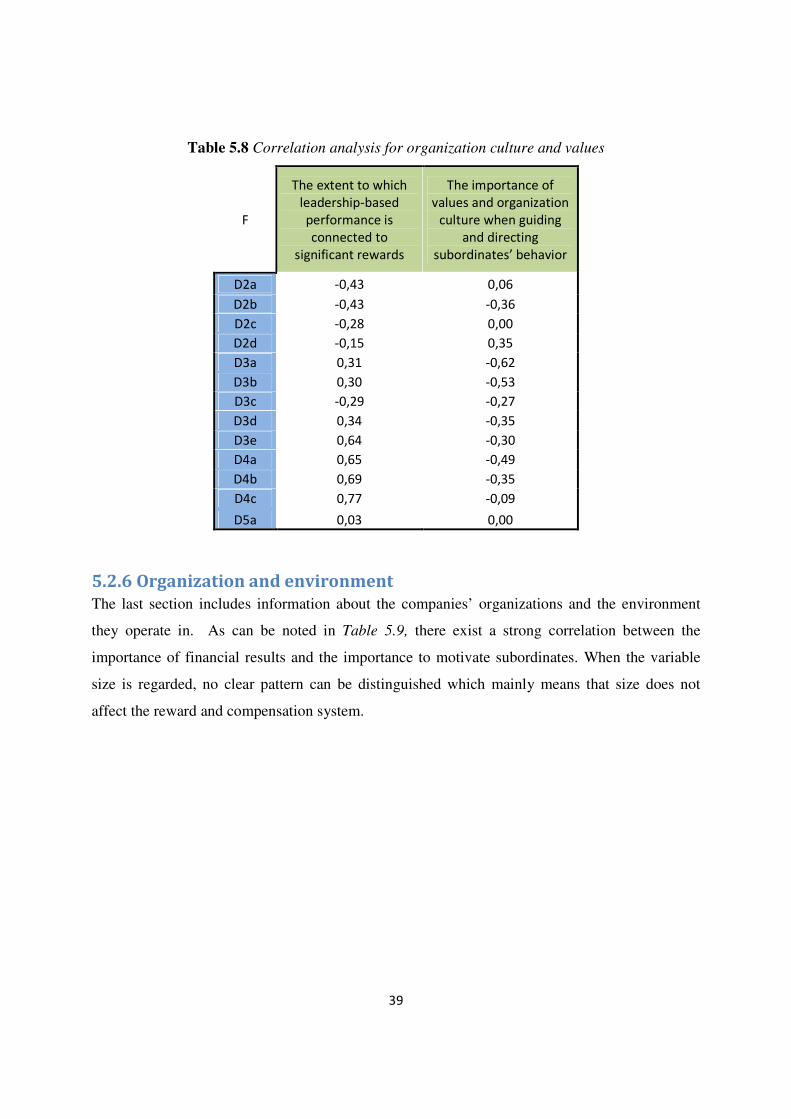

5.2.5 Organization culture and values

Regarding the section about culture and values within the organization, it is shown to be a

significant relation between leadership-based performance and directing subordinates. It may be

the case that when companies use significant bonuses to reward their managers, the bonuses have

the purpose to direct the attention to what is the most essential when managing the business. An

interesting fact to observe is the negative relation between the importance of values and

organizational culture and to what extent performance-pay contracts are customized for each

subordinate, indicating that companies which emphasis strong values use individual shaped

performance-pay contracts.

39

Table 5.8 Correlation analysis for organization culture and values

F

The extent to which

leadership-based

performance is

connected to

significant rewards

The importance of

values and organization

culture when guiding

and directing

subordinates’ behavior

D2a -0,43 0,06

D2b -0,43 -0,36

D2c -0,28 0,00

D2d -0,15 0,35

D3a 0,31 -0,62

D3b 0,30 -0,53

D3c -0,29 -0,27

D3d 0,34 -0,35

D3e 0,64 -0,30

D4a 0,65 -0,49

D4b 0,69 -0,35

D4c 0,77 -0,09

D5a 0,03 0,00

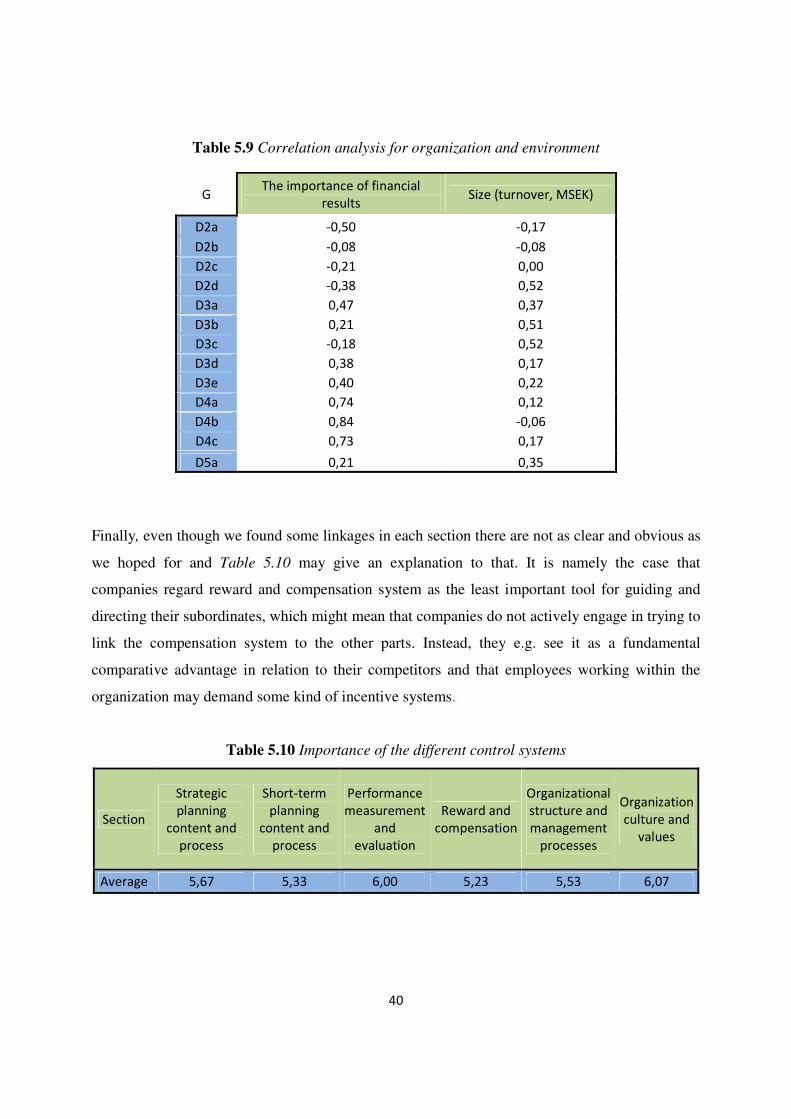

5.2.6 Organization and environment

The last section includes information about the companies’ organizations and the environment

they operate in. As can be noted in Table 5.9, there exist a strong correlation between the

importance of financial results and the importance to motivate subordinates. When the variable

size is regarded, no clear pattern can be distinguished which mainly means that size does not

affect the reward and compensation system.

40

Table 5.9 Correlation analysis for organization and environment

G The importance of financial

results Size (turnover, MSEK)

D2a -0,50 -0,17

D2b -0,08 -0,08

D2c -0,21 0,00

D2d -0,38 0,52

D3a 0,47 0,37

D3b 0,21 0,51

D3c -0,18 0,52

D3d 0,38 0,17

D3e 0,40 0,22

D4a 0,74 0,12

D4b 0,84 -0,06

D4c 0,73 0,17

D5a 0,21 0,35

Finally, even though we found some linkages in each section there are not as clear and obvious as

we hoped for and Table 5.10 may give an explanation to that. It is namely the case that

companies regard reward and compensation system as the least important tool for guiding and

directing their subordinates, which might mean that companies do not actively engage in trying to

link the compensation system to the other parts. Instead, they e.g. see it as a fundamental

comparative advantage in relation to their competitors and that employees working within the

organization may demand some kind of incentive systems.

Table 5.10 Importance of the different control systems

Section

Strategic

planning

content and

process

Short-term

planning

content and

process

Performance

measurement

and

evaluation

Reward and

compensation

Organizational

structure and

management

processes

Organization

culture and

values

Average 5,67 5,33 6,00 5,23 5,53 6,07

41

6. Conclusion and discussion

In the last chapter we provide our conclusions followed by a final discussion. Furthermore, suggestions for

further studies are presented.

When a study of this kind is conducted it is essential to question the results we got and if they are

reliable and if some generalizations can be done. With this thesis we aimed to investigate the

linkages between reward and compensation systems and other part of the management control

package. After accomplished this study, we can conclude that there are some small linkages

between reward and compensation and other parts of the MCSs. The most clear connection can

be found with the performance and measurement part, especially when it comes to financial

measures, but we still believed that we would find more clear and obvious connections. A reason

for this could be that the reward and compensation systems were quite recently introduced among

the interviewed companies. Therefore, we assume that it is rather likely that there will be more

distinctive linkages in the future.

As stated earlier, the companies used financial-reward in a greater extent than non-financial

rewards. This is, however, not completely in line with some of the literature on the area which

claims that non-monetary rewards are more effective. Our findings can therefore be discussed

and but, on the other hand, it was not our purpose to investigate the most useful reward and

compensation system. Only two companies based their rewards on non-financial figures, quality

and customer satisfaction. These companies, however, did not show any single pattern or

relations to the other MCS parts.

It is notable that the people we interviewed possess great knowledge about their firm and that

they able to answer almost all of the questions in the questionnaire. In addition to this, it can be

stated that nearly all the companies claim that they would keep their reward and compensation

systems for the foreseeable time. This may indicate that the companies are satisfied with their

reward and compensation system as a vital tool for guiding their business.

42

We are fully aware of the fact that our thesis is mainly build upon the theoretical model by Malmi

& Brown and that it may exist more theory within this area. However, it appears that this model

is seen as a guiding framework in the studying of the different parts in the MCS package.

Furthermore, a discussion has been brought up whether we could have achieved a better result if

we had used a qualitative study instead. With that kind of study, we probably would have a

deeper knowledge of every single company, but on the other hand we would not have the same

overall picture as we do have now. The aim was actually to get an overview of Swedish

companies within the area and therefore we believe that a quantitative approach was more

sufficient after all. However, we could have added more questions or modified our own questions

in order to get even better findings, since we believed that we did not got all the answers we were

aiming for.

When it comes to further research, we think that it would be appropriate to include even more

than 15 companies. It would be also be interesting to investigate this phenomenon over time since

environmental conditions are changing all the time, which means that the companies have to

adapt their organization depending on this kind of aspects

Finally, the study is, as mentioned before, focusing on finding and explaining linkages between

the reward and compensation system and the other parts of the MCS package. Another idea could

be to have a different focus and e.g. search for connections between a company’s strategic

planning and the other parts. If several studies like these where conducted, a more generalized

and reliable picture would be presented. We regard our survey as one of the contributions to gain

sufficient knowledge regarding how firms use their different MCSs.

43

7. References

Allen, R. S, Helms. M. M, 2001, Reward practices and organizational performance, Sage

publications

Alvesson, M., Karreman, D., 2004. Interfaces of control. technocratic and socio-ideological control in a global management consultancy firm. Accounting Organizations and Society 29, 423–444.

Andersen, I., 1998, Den uppenbara verkligheten: val av samhällsvetenskaplig metod, Malmö,

Studentlitteratur AB, 1th edition

Armstrong, M, Brown. D, Reilly. P, 2011, Increasing the effectiveness of reward management:

an evidence-based approach, Employee relations, Vol 33, pp 106-120

Arvidsson, P., 2008, Controllerhandboken chapter 9, Liber

Axelsson. E, Eklund. A, Larsson. E, 2010, Control package och strategi – dess samverkan i stora

svenska aktiebolag, Master thesis in accounting and management control, Lund university

Banker R. D., Potter G., Srinivasan D., 2000, An empirical investigation of an incentive plan that

includes nonfinancial performance measures, The accounting review, Vol 75, No 1, pp 65-92

Berberian. J, The impact of a non-monetary reward program on employee job satisfaction, 2008,

UMI Dissertations Publishing

Berglund M., Rapp G., 2010, The management control system package of IKEA Bäckebol,

University of Gothenburg – School of Business, Economics and Law

44

Berry. A.J, Coad. A.F, Harris. E.P, Otley. D.T, Stringer. C, 2008, Emerging themes in

management control: a review of recent literature, the British accounting revie, Vol 41, Iss 1, pp

2-20

Blumentritt. T, 2006, Intergrating strategic management and budgeting, Journal of business

strategy, Vol 27, Iss 6, pp 73-79

Bonn. I, Christodoulou. C, 1999, From strategic planning to strategic management, Long range

planning, Vol 29, Iss 4, pp 543-551

Boyd. B. K, Salamani. A, 2001, Strategic systems: a contingency model of pay system design,

Strategic management journal, Vol22, pp 777-792

Brimson. J. A, 2011, Management process principles, Journal of corporate accounting & finance,

Vol 22, No 4, pp, 83-96

Bryman. A, Bell. E, 2003, Företagsekonomiska forskningsmetoder, Liber