Embed Size (px)

Citation preview

Schouw & Co.2015 first halfInvestor presentation

AUGUST/SEPTEMBER 2015

CEO JENS BJERG SØRENSENIR KASPER OKKELS

2015 H1 at a glance: Continued progress

revenue

5.9bnGrowth 16% // 2014H1: 5.1bnImpact from volatile raw material prices

EBIT

303m26% growth from 2014H1Positive effect from forex and raw materials

cash flow from operations

224m2014H1: 243mUnsatisfactory increase in NWC in BioMar

NIBD/EBITDA

0.1xSmall increase in NIBD y/yVery strong and solid financial position

profit from associates and JVs

47m2014H1: -7mNo PPA effect in Kramp, Xergi 8% EBIT

return on invested capital

17.0%ROIC incl. goodwill 14.1%Progress in all companies except BioMar

31.08.2015Interim Report 2015H1 2

200

220

240

260

280

300

320

340

360

380

Jan Mar May Jul Sep Nov Jan Mar May Jul

Schouw & Co. share price

C20 CAP indexed to Schouw & Co.

MidCap indexed to Schouw & Co.

2014 2015

Key figures

Revenue and income 2015H1 2014H1 2014FY

Revenue 5,888 5,064 11,784

EBITDA 494 415 1,070

- margin 8.4% 8.2% 9.1%

EBIT 303 239 708

- margin 5.1% 4.7% 6.0%

Profit after tax in associates and JVs 47 -7 28

Cash flows 2015H1 2014H1 2014FY

Cash flows from operating activities 224 243 628

Cash flows from investing activities -184 -81 -355

Of which investment in PPE -165 -95 -233

Cash flows from financing activities -116 56 -563

Invested capital and financing 2015H1 2014H1 2014FY

Working capital 2,013 1,541 1,775

Net interest bearing debt (NIBD) 134 24 44

Total equity 6,366 5,740 6,074

ROIC excl. goodwill 17.0% 18.1% 16.9%

ROIC incl. goodwill 14.1% 15.0% 14.0%

NIBD/EBITDA 0.1 0.0 0.0

30%increase in share price

in 2014

31.08.2015Interim Report 2015H1 3

21%increase in share price

in ’15H1

BioMar

Volume flat compared to 2014H1 Same total y/y volume in both Q1 and Q2 21% revenue increase due to higher raw material prices Increase in Norwegian volumes (final deliveries, contract base) Decrease in Chilean volumes (declining market, smaller fish, early harvest) Continental Europe on par despite challenges in Greece

Chile remains the key challenge Entire farming industry in financial difficulties Debtor management increasingly important Lower market share but no loss of customers Chile main reason to surge in NWC (forex, payment terms, inventory, etc.) Market volume expected to decline in next quarters

Maintaining 2015 outlook Contract base in Norway as expected (volumes and margins) Debtor risk and low volumes in Americas but positive

effect from USD exchange rate Greece seems towards a sustainable solution No effect from Chinese JV with Tongwei (but good progress) Outlook raised after Q1 following a strong first quarter

31.08.2015Interim Report 2015H1 4

RevenueLTM

EBITLTM

GuidanceRevenue 2014 8,4517m

org. 2015 ~8.5bnafter Q1 2015 ~9.0bn

EBIT 2014 434morg. 2015 360-410m

after Q1 2015 375-425m

BioMar 2015-H1 financials31.08.2015Interim Report 2015H1 5

Q2 YTDLTM 2014

2015 2014 D 2015 2014 D

Revenue 2,230 1,837 21% 4,139 3,430 21% 9,161 8,451

EBITDA 115 114 1% 201 183 10% 592 574

EBITDA% 5.1% 6.2% -17% 4.9% 5.3% -9% 6.5% 6.8%

EBIT 78 79 -1% 127 112 13% 449 434

EBIT% 3.5% 4.3% -18% 3.1% 3.3% -6% 4.9% 5.1%

Profit before tax 69 73 -5% 120 102 18% 417 398

Cash Flow from operations -96 148 NA -101 84 NA 81 266

Equity 1,929 1,665 16% 1,902

- in % of total assets 36.9% 36.4% 1% 39.3%

Inv. Capital (ex goodwill) 2,219 1,784 24% 1,931

- ROIC 21.8% 24.4% -10% 22.9%

Net Working Capital 1,260 802 57% 983

- in % of LTM revenue 13.8% 9.2% 49% 11.6%

NIBD 686 539 27% 386

- times LTM EBIDTA 1.2x 0.9x 26% 0.7x

Fibertex Personal Care

Small decline in revenue and volume Volume growth in Denmark but decline in Malaysia Lower raw material prices affects revenue negatively Positive effect from consolidation of Innowo Print Strong cash flow from operations of DKK 220m (2014H1: 100m) ROIC of 15.8% following significant lowering of NWC

Volatile raw material prices Pass-through mechanisms with some months lag About DKK +30m EBIT effect in Q1, about DKK -25m in Q2, minor effect expected in Q3 PP prices seems to have stabilized

Innovation and value-add Starting up print production in Malaysia Ongoing innovation in softer, lighter and loftier products Growing with Japanese premium diaper manufactures

Narrowing EBIT guidance Raising lower end of interval High capacity utilisation required Industry remains dynamic

31.08.2015Interim Report 2015H1 6

RevenueLTM

EBITLTM

GuidanceRevenue 2014 1,787m

2015 ~1.7bnEBIT 2014 171m

org. 2015 160-180mnew 2015 170-180m

Fibertex Personal Care 2015-H1 financials

Q2 YTDLTM 2014

2015 2014 D 2015 2014 D

Revenue 404 421 -4% 832 847 -2% 1,772 1,787

EBITDA 70 66 5% 169 136 24% 340 308

EBITDA% 17.3% 15.8% 10% 20.3% 16.1% 26% 19.2% 17.2%

EBIT 34 34 0% 98 73 35% 197 171

EBIT% 8.5% 8.1% 4% 11.8% 8.6% 37% 11.1% 9.6%

Profit before tax 29 31 -4% 94 64 46% 199 169

Cash Flow from operations 129 29 347% 220 100 119% 345 226

Equity 738 630 17% 730

- in % of total assets 41.6% 36.0% 16% 38.8%

Inv. Capital (ex goodwill) 1,225 1,195 3% 1,336

- ROIC 15.8% 12.9% 23% 14.4%

Net Working Capital 225 268 -16% 293

- in % of LTM revenue 12.7% 16.8% -24% 16.4%

NIBD 560 646 -13% 688

- times LTM EBIDTA 1.6x 2.3x -29% 2.2x

31.08.2015Interim Report 2015H1 7

Fibertex Nonwovens

Another strong quarter Growth in auto and high-value segments Substantial progress in EBIT and gross margin Effect from acquisitions, forex, scale and transformed business model One-off gain of DKK 3m following acquisition of shares in South Africa

Consolidating strong international position State-of-the-art equipment at all sites US platform contributes positively Significant long-term potential in South Africa Promising product development pipeline Proven strong ability to drive industry consolidation

2015 guidance raised for the 2nd time Effect from strong H1 (H2 always low season) Still challenges from upgrades and installation of new line Consolidation of South Africa (negative EBIT in 2015) Uncertainty about raw material prices

31.08.2015Interim Report 2015H1 8

RevenueLTM

EBITLTM

GuidanceRevenue 2014 1,048m

2015 ~1.2bnEBIT 2014 62m

org. 2015 65-75mafter Q1 2015 70-80m

new 2015 75-85m

Fibertex Nonwovens 2015-H1 financials

Q2 YTDLTM 2014

2015 2014 D 2015 2014 D

Revenue 328 267 23% 634 539 18% 1,143 1,048

EBITDA 44 31 40% 89 64 38% 153 128

EBITDA% 13.4% 11.8% 14% 14.1% 12.0% 18% 13.4% 12.2%

EBIT 25 16 59% 52 33 58% 81 62

EBIT% 7.6% 5.9% 29% 8.2% 6.1% 34% 7.1% 5.9%

Profit before tax 22 13 76% 45 27 70% 69 50

Cash Flow from operations 23 32 -29% 51 51 0% 82 82

Equity 463 331 40% 385

- in % of total assets 33.0% 33.8% -2% 32.7%

Inv. Capital (ex goodwill) 1,034 730 42% 874

- ROIC 9.4% 7.1% 33% 8.4%

Net Working Capital 349 283 23% 319

- in % of LTM revenue 30.5% 28.5% 7% 30.4%

NIBD 593 409 45% 522

- times LTM EBIDTA 3.9x 3.6x 8% 4.1x

31.08.2015Interim Report 2015H1 9

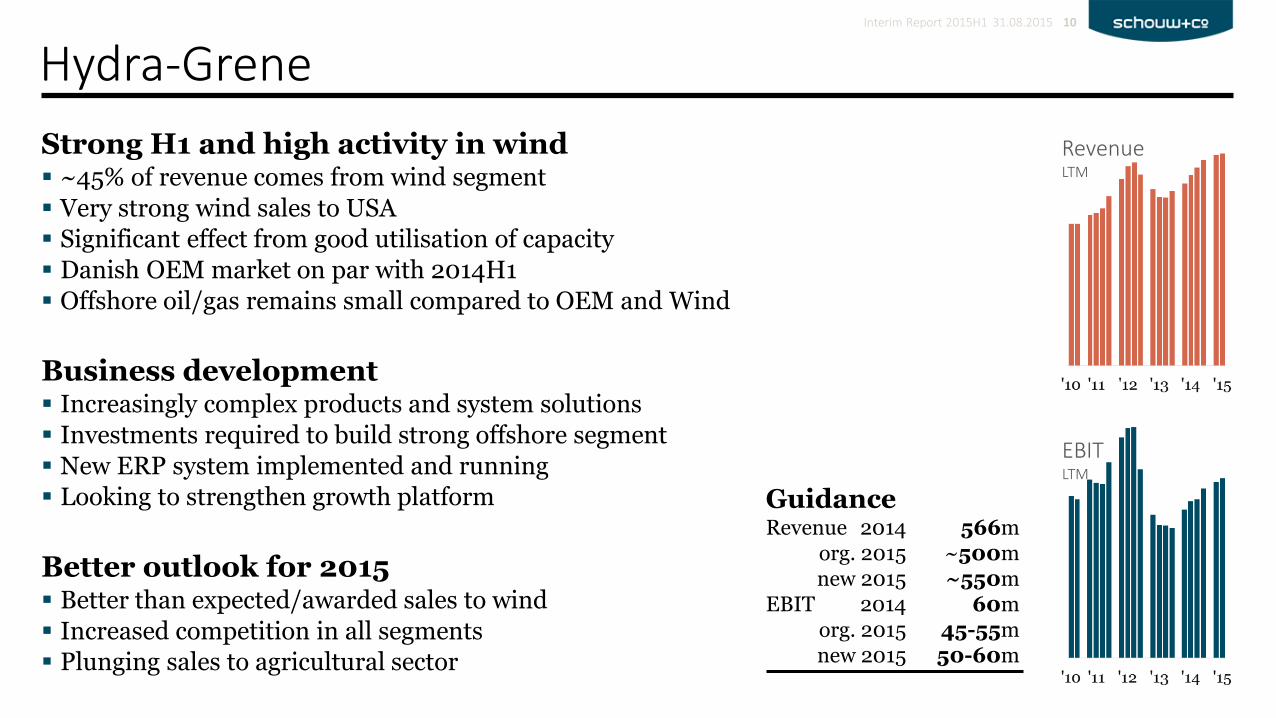

Hydra-Grene

Strong H1 and high activity in wind ~45% of revenue comes from wind segment

Very strong wind sales to USA

Significant effect from good utilisation of capacity

Danish OEM market on par with 2014H1

Offshore oil/gas remains small compared to OEM and Wind

Business development Increasingly complex products and system solutions

Investments required to build strong offshore segment

New ERP system implemented and running

Looking to strengthen growth platform

Better outlook for 2015 Better than expected/awarded sales to wind

Increased competition in all segments

Plunging sales to agricultural sector

31.08.2015Interim Report 2015H1 10

RevenueLTM

EBITLTM

GuidanceRevenue 2014 566m

org. 2015 ~500mnew 2015 ~550m

EBIT 2014 60morg. 2015 45-55mnew 2015 50-60m

Hydra-Grene 2015-H1 financials

Q2 YTDLTM 2014

2015 2014 D 2015 2014 D

Revenue 151 147 2% 299 281 7% 584 566

EBITDA 23 22 4% 43 41 5% 80 78

EBITDA% 15.2% 14.9% 2% 14.2% 14.5% -2% 13.7% 13.8%

EBIT 19 18 9% 35 32 11% 64 60

EBIT% 12.6% 11.9% 6% 11.8% 11.3% 5% 10.9% 10.6%

Profit before tax 17 17 2% 36 30 18% 67 61

Cash Flow from operations -5 -12 -59% 40 10 285% 89 60

Equity 176 164 8% 188

- in % of total assets 44.3% 39.0% 14% 48.0%

Inv. Capital (ex goodwill) 289 309 -6% 292

- ROIC 23.8% 22.3% 7% 22.6%

Net Working Capital 188 195 -3% 187

- in % of LTM revenue 32.2% 37.1% -13% 33.1%

NIBD 101 145 -30% 96

- times LTM EBIDTA 1.3x 1.9x -34% 1.2x

31.08.2015Interim Report 2015H1 11

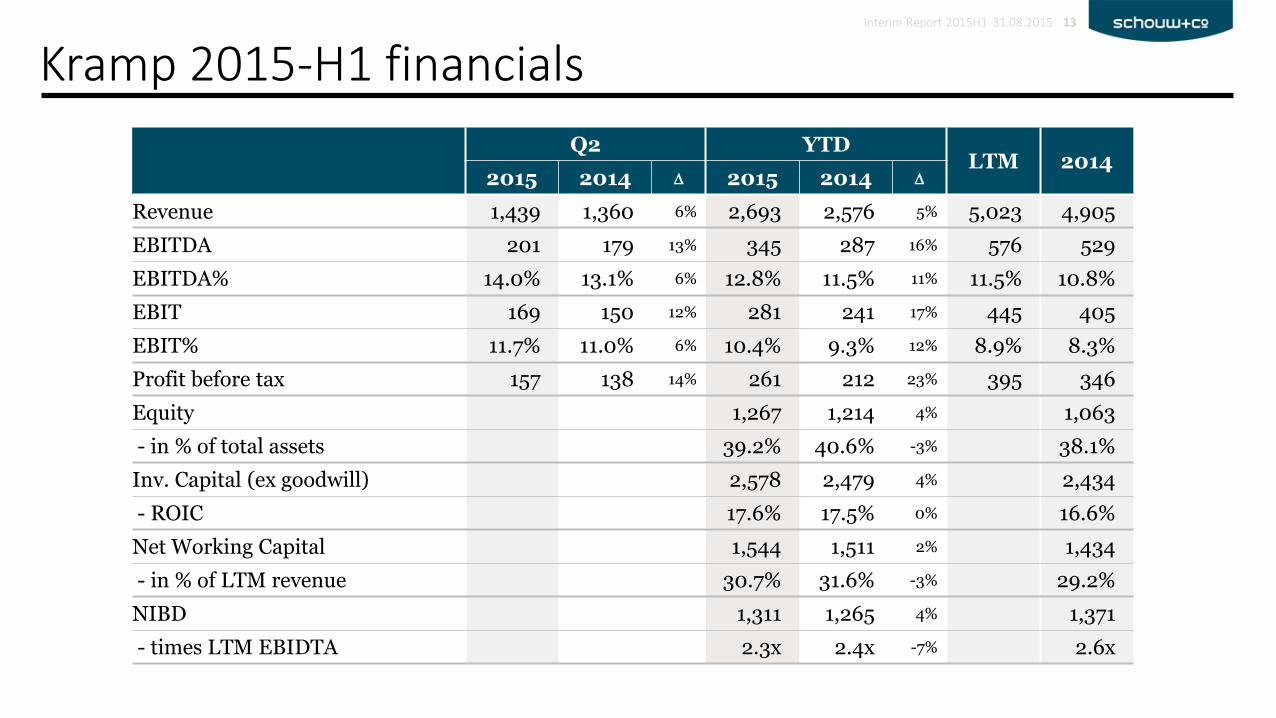

Kramp

Strong development in H1 Revenue up 4.6% and EBIT 17% driven by the big markets in PL, FR, NL

EBIT margin of 11.7% in Q2

Robust business model: high share of wearables and repair parts

Agro customers facing difficulties in selected markets

Harvesting the merger synergies Integration of Grene and Kramp progresses as planned

Expected level of synergies confirmed so far

Investments in IT required as expected

Maintaining 2015 outlook Full effect in Schouw & Co. P/L as PPA depreciations are eliminated

Disclosed 2017 revenue target of EUR 1bn requires M&Abut 13% EBITDA target remains intact

31.08.2015Interim Report 2015H1 12

GuidanceRevenue 2014 4,905m

2015 ~5.25bnEBIT 2014 405m

2015 425-450m

New warehouse in Poland

Kramp 2015-H1 financials

Q2 YTDLTM 2014

2015 2014 D 2015 2014 D

Revenue 1,439 1,360 6% 2,693 2,576 5% 5,023 4,905

EBITDA 201 179 13% 345 287 16% 576 529

EBITDA% 14.0% 13.1% 6% 12.8% 11.5% 11% 11.5% 10.8%

EBIT 169 150 12% 281 241 17% 445 405

EBIT% 11.7% 11.0% 6% 10.4% 9.3% 12% 8.9% 8.3%

Profit before tax 157 138 14% 261 212 23% 395 346

Equity 1,267 1,214 4% 1,063

- in % of total assets 39.2% 40.6% -3% 38.1%

Inv. Capital (ex goodwill) 2,578 2,479 4% 2,434

- ROIC 17.6% 17.5% 0% 16.6%

Net Working Capital 1,544 1,511 2% 1,434

- in % of LTM revenue 30.7% 31.6% -3% 29.2%

NIBD 1,311 1,265 4% 1,371

- times LTM EBIDTA 2.3x 2.4x -7% 2.6x

31.08.2015Interim Report 2015H1 13

Other activities

Xergi Significant progress in 2015

Revenue up to DKK 235m (2014H1: 86m)

EBIT margin about 8% (2014H1: loss)

Maintaining high activity level also in 2015

Effect from many years of investing in technology and markets as well as strong Danish market

Unchanged good prospects for biogas

Focus on international markets

Incuba Invest Small profit (as in 2014H1)

Properties HQ at Chr. Filtenborgs Plads in Aarhus

Two factories in Frederikshavn (Martin Prof.)

Small property in Aarhus rented to former Grene Industri service

31.08.2015Interim Report 2015H1 14

2015 guidance

REVENUE DKK million

2015 F

after Q2

2015 F

original

2014

actual

BioMar c. 9,000 c. 8,500 8,451

Fibertex Personal Care c. 1,700 c. 1,700 1,787

Fibertex Nonwovens c. 1,200 c. 1,200 1,048

Hydra-Grene c. 550 above 500 566

Other/eliminations - - -68

Total revenue c. 12.5bn c. 12bn 11,784

Kramp (100%) c. 5,250 c. 5,250 4,905

EBIT DKK million

2015 F

after Q2

2015 F

original

2014

actual

BioMar 375-425 360-410 434

Fibertex Personal Care 170-180 160-180 171

Fibertex Nonwovens 75-85 65-75 62

Hydra-Grene 50-60 45-55 60

Other c. -20 c. -20 -20

Total EBIT 650-730 610-700 708

Associates etc. 65-75 60-70 28

Financial items, net c. -10 c. -35 -35

Profit before tax 705-795 635-735 701

Kramp EBIT (100%) 425-450 425-450 405

31.08.2015Interim Report 2015H1 15

Upwards adjusted after Q1Upwards adjusted after Q2

Strategic goals31.08.2015Interim Report 2015H1 16

Growth Substantial growth every year

Profit Benchmark level profitability

Return ROIC > 15%, but dependent on level of risk

Leverage Comfort zone for NIBD is 1-2 times EBITDA

Payout Constant/increasing dividends and share buybacks

Portfolio A ’handful’ of big and strong businesses

AppendixSelected introductory presentation material

Merger

Grene/Kramp

Merger

NEG/Vestas

M&A activity31.08.2015Interim Report 2015H1 18

MartinEV: 500m60+40%

2000 2002 2004 2006 2008 2010 2012 2014

SchulstadEV: 2.700m

62%

FibertexEV: 660m

100%

ProvimiEV: 675m

100% (BioMar)

TharreauEV: 300m

100% (FIN)

ElopakEV: 1.200m

50%

SjøtrollEV: 1.200m

51%

Hydro-power

MartinEV: 900m

100%

Merger

Xergi

BioMarEV: 1.800m68%+32%

GreneIndustri-service

NWSEV: 150m

100% (FIN)

InnowoEV: 100m85% (FPC)

Bigger and stronger portfolio

Bigger and stronger businesses in the portfolio

Consolidating theconglomerate

Deal flow is not a target

Acquisitions and mergerspart of consolidation

and to create bigger and stronger businesses

Divestments due to no longer being best owner

Fibertex South Africa+48% (FIN)

The Schouw agenda31.08.2015Interim Report 2015H1 19

Develop big and strong businesses

Leading companies do perform better

Expand in growth markets

A global outlook is key

Constantly increase capacity

Balancing profit and growth

Maintain focus on innovation

Secure #1 positions

Think long-term

Ensuring high return on capital

Attract talent

“Results are created through people”

Conglomerate value creation31.08.2015Interim Report 2015H1 20

FOCUSED OPERATIONS TRANSFORMATION

STRUCTURE AND DEVELOP OPTIMIZE OWNERSHIP

Delivering solid performance and growthTight/optimal capital allocationOngoing efficiencyEnsure innovation

Structural and strategic initiativesDevelopment of products and servicesGeographical expansionBolt-on acquisitions

Attractive acquisitionsLong-term planningAdd Schouw DNASecure leading positions

Necessary exits with good timingParticipate in value-added consolidationsConsider mergers, JVs, minority stakesValue-creating ownership structures

minimum as benchmark ambitious plans

risk and span of control best owner philosophy

Bu

sin

ess

leve

lG

rou

p le

vel

2005Acquisition of BioMar

2007Acquisition of Provimi

2012JV in

Costa Rica

2014JV in

Turkey

2011Expansion

in Myre

2002Acquisition of Fibertex

2003 Green-field in

Malaysia

2011 Acquisitionin France

EUR +300minvestments

in cap.

2004 Acquisition

in Czech

2011 FPC and FIN

demerger

1988Acquisition

of Grene

~1990Internatio-nalisation

2009 Grene/Hydra

demerger

2010 Hydra in China

and India

~1995 A strong focus

on industry

2015-Growth andacquisitions

2013 Grene/Krampcombination

10 years of strong growth and profitable development

14 years of transformation and expansion

27 years of active and developing ownership

31.08.2015Interim Report 2015H1 21

Our mantra31.08.2015Interim Report 2015H1 22

Businesses owned by Schouw & Co. should…secure and maintain a leading position

…develop after our active ownership model

…have a long-term growth strategy

…take part in value-creating consolidations

…generate ROIC above 15%

…have visible values and a strong culture

…be prepared for change

Investment guidelines (for platform investment)

We have a long-term investment strategy and is open to attractive acquisitions and appropriate divestments of companies

We have no predetermined exit strategy for the investments we make

We want to keep and develop its businesses as long as we are the best owner

We have clear targets for return on capital and profit for all investments

Area Criteria

IndustryB2B, preference for process industry and logistics/distribution

SizeRevenue – now or short-term realizable – of more than DKK 1bn

GeographyDanish headquartered (but international focus)

OwnershipPreferable wholly owned, but open to value-creating structures

Leading position

Within top 5 in its niche/segment

Manage-ment

Strong and ambitious. No operational resources at Schouw & Co. HQ

Need for a new owner

We need to bring something to the business

Possible to be active

Plans for development and transformation

31.08.2015Interim Report 2015H1 23

Two main long-term shareholders Increase in share price and trading volume

31.08.2015Interim Report 2015H1 24

Ownership

Givesco+EE32%

Hornsylds Legat15%

Treasury shares

8%

Danish (27%) and foreign (18%)

institutional and retail investors

45%

Sole purpose is owning shares in Schouw & Co.

Administrated by the Board of Directors in Schouw & Co.

Danish active family-owned business fund with activities

within bakery, industrial equipment, food/chocolate

and hardware.

75 75 84 77 77 102 128 153

115 81 101 15476 0

0

180

0

100

200

300

400

2007 2008 2009 2010 2011 2012 2013 2014

Dividends paid (DKK million) Share buy-back (DKK million)

Strong historical yield

0

2.000

4.000

6.000

8.000

10.000

12.000

0

50

100

150

200

250

300

350

400

Jan2012

Mar2012

May2012

Jun2012

Aug2012

Oct2012

Dec2012

Feb2013

Apr2013

Jun2013

Aug2013

Oct2013

Dec2013

Feb2014

May2014

Jul2014

Sep2014

Nov2014

Jan2015

Trading/day (3M average) Share price

2012

+61%

2013

+49%

2014

+30%

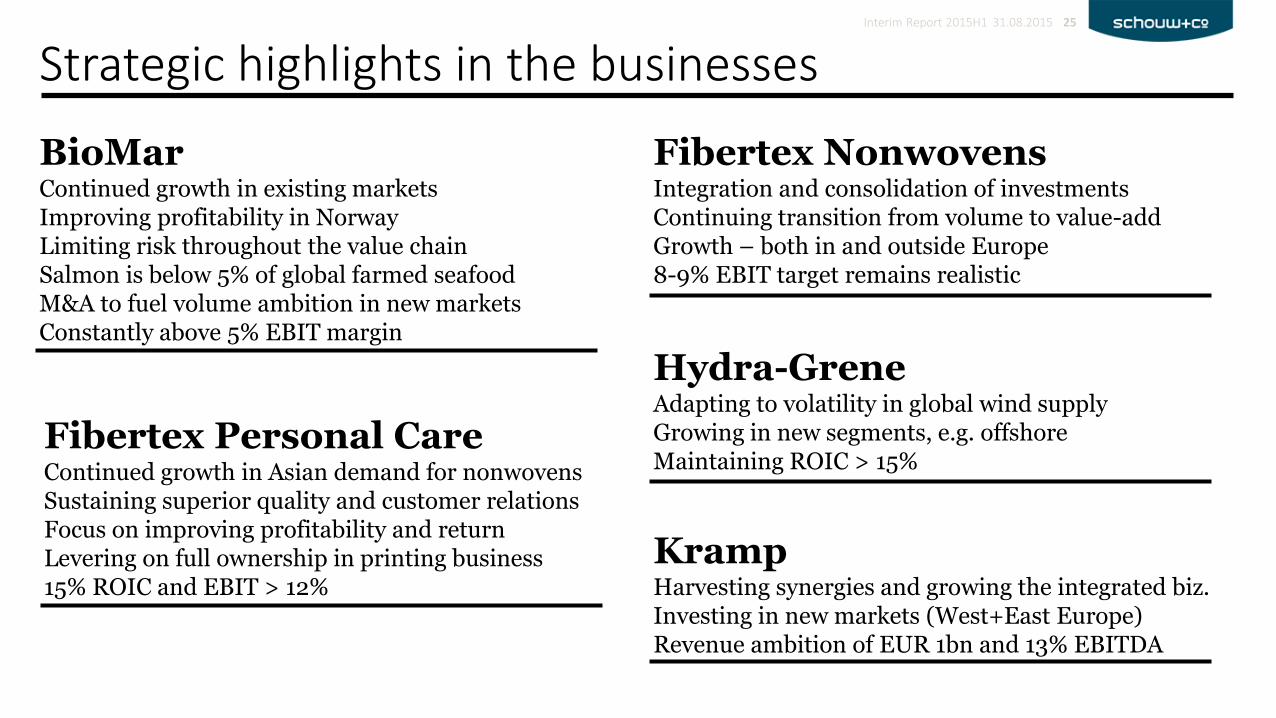

Strategic highlights in the businesses

BioMarContinued growth in existing marketsImproving profitability in NorwayLimiting risk throughout the value chainSalmon is below 5% of global farmed seafoodM&A to fuel volume ambition in new marketsConstantly above 5% EBIT margin

Fibertex Personal CareContinued growth in Asian demand for nonwovensSustaining superior quality and customer relationsFocus on improving profitability and returnLevering on full ownership in printing business15% ROIC and EBIT > 12%

Fibertex NonwovensIntegration and consolidation of investmentsContinuing transition from volume to value-addGrowth – both in and outside Europe8-9% EBIT target remains realistic

Hydra-GreneAdapting to volatility in global wind supplyGrowing in new segments, e.g. offshoreMaintaining ROIC > 15%

KrampHarvesting synergies and growing the integrated biz.Investing in new markets (West+East Europe)Revenue ambition of EUR 1bn and 13% EBITDA

31.08.2015Interim Report 2015H1 25

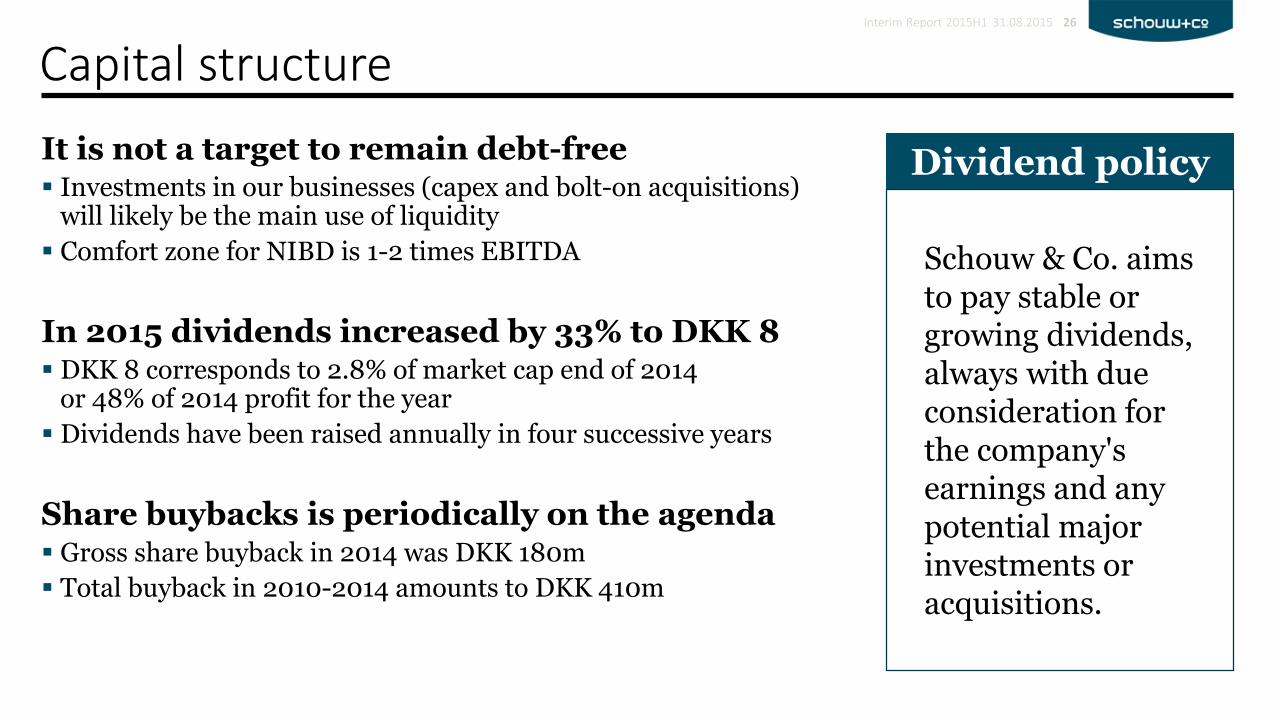

Capital structure

It is not a target to remain debt-free Investments in our businesses (capex and bolt-on acquisitions)

will likely be the main use of liquidity

Comfort zone for NIBD is 1-2 times EBITDA

In 2015 dividends increased by 33% to DKK 8 DKK 8 corresponds to 2.8% of market cap end of 2014

or 48% of 2014 profit for the year

Dividends have been raised annually in four successive years

Share buybacks is periodically on the agenda Gross share buyback in 2014 was DKK 180m

Total buyback in 2010-2014 amounts to DKK 410m

31.08.2015Interim Report 2015H1 26

Schouw & Co. aims to pay stable or growing dividends, always with due consideration for the company's earnings and any potential major investments or acquisitions.

Dividend policy

BioMar

Fish farming/feed geography31.08.2015Interim Report 2015H1 28

Atlantic salmon, trout Atlantic salmon, coho, trout, tilapia

Sea bass, sea bream, portiontrout, eel, a.o.

Shrimp, tilapia, catfish, pangasius, etc.

Market size ~2.0m tMarket growth* 5-6%Market share 20-25%

Market size ~1.4m tMarket growth* 5-6%Market share 25-30%

Market size ~0.7m tMarket growth 0-1%Market share 25-30%

Market size +10m tMarket growth 4-5%Market share -

2014 revenue DKK 4.1bn 2014 revenue DKK 2.6bn 2014 revenue DKK 1.8bn 2014 revenue N/A

Brande, Denmark Dueñas, Spain

Nersac, FranceVolos, Greece

Castro, Chile

Pargua, Chile

Myre, Norway

Karmøy, Norway Grangemouth, UK Guanacaste, Costa Rica

*Long-term market growth over the ‘salmon cycle’; flat/negative volume development in 2015

Pargua, Chile

NORTH SEA AMERICAS CONTINENTAL EUROPE ASIA

BioMar has in 2015 establisheda Joint Venture with ChineseTongwei. First step is to build a 100.000 ton factory in China.

BioMar’s strategy31.08.2015Interim Report 2015H1 29

Organisationally and geographically

Focus on current daily

business

Actively utilise competences

across BioMar units

New geographies and species

Grow organically in line with existing markets

Establish units (incl. production) in 2-4 new geographies before 2017, to the extent possible focusing on a limited number of species (< 5)

Strengthen global capabilities

More well defined structures and systems

ELEMENTS DIRECTION AND PRIORITIES

Ambitions from 2012 strategy plan31.08.2015Interim Report 2015H1 30

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Volume (1000 tons)

Sales of approx. 1.7 m tons in 2017 Approx. half through organic growth The other half in new markets (acquisitions/JV’s/green fields) 5-6% EBIT margin ROIC > 15%

‘Beyond the limits’

‘Going for Profitable Global Growth’

‘Going for Global Growth’

BioMar group strategy:

0

2

4

6

8

10

196

0

196

4

196

8

197

2

197

6

198

0

198

4

198

8

199

2

199

6

20

00

20

04

20

08

20

12

20

16

20

20

20

24

20

28

20

32

20

36

20

40

20

44

20

48

Mega-trend driven demand31.08.2015Interim Report 2015H1 31

The only sustainable way to increase the supply of fish is by fish farming.

It is not possible to increase the wild catch without environmental consequences.

Salmon is healthy

High content of vitamins and healthy fatty acids (Omega 3)

Effective growth

Low feed conversion ratio 1 kg feed gives almost 1 kg fish Fish adapts to temperature High yield (few bones and fins)

Stable supply

Multiple slaughtering periods and good forecasting systems

BioMarEWOSSkrettingMarine HarvestAustevoll/LerøyMultiple farmers

Africa

Asia

Population, billion

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0wild catch aquaculture

Source: FAO, 2013, farmed and wild salmonids

GLOBAL POPULATION GROWTH

GROWTH IN AQUACULTURE

Revenue 8,451mEBITDA 574m- margin 6.8%

EBIT 434m- margin 5.1%

ROIC 22.9%Employees 904

AQUACULTURE BENEFITS

FOCUSED FISH FEED PRODUCER

2014 FINANCIALS

Revenue ~9,000mEBIT 375-425m

2015 GUIDANCE

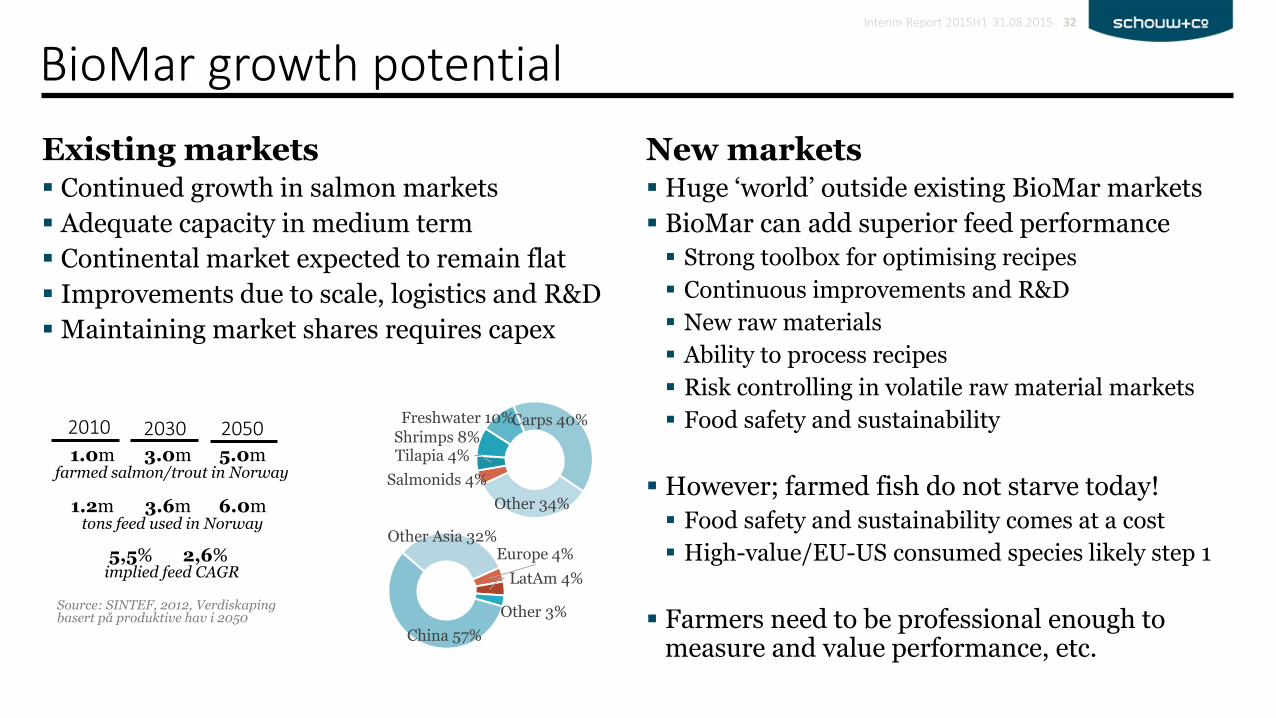

BioMar growth potential

Existing markets Continued growth in salmon markets

Adequate capacity in medium term

Continental market expected to remain flat

Improvements due to scale, logistics and R&D

Maintaining market shares requires capex

New markets Huge ‘world’ outside existing BioMar markets

BioMar can add superior feed performance

Strong toolbox for optimising recipes

Continuous improvements and R&D

New raw materials

Ability to process recipes

Risk controlling in volatile raw material markets

Food safety and sustainability

However; farmed fish do not starve today!

Food safety and sustainability comes at a cost

High-value/EU-US consumed species likely step 1

Farmers need to be professional enough to measure and value performance, etc.

31.08.2015Interim Report 2015H1 32

1.0m 3.0m 5.0mfarmed salmon/trout in Norway

1.2m 3.6m 6.0mtons feed used in Norway

5,5% 2,6%implied feed CAGR

Europe 4%

LatAm 4%

Other 3%

China 57%

Other Asia 32%

Salmonids 4%

Tilapia 4%Shrimps 8%Freshwater 10%Carps 40%

Other 34%

Source: SINTEF, 2012, Verdiskapingbasert på produktive hav i 2050

2010 2030 2050

The otherbusinesses in the portfolio

Fibertex Personal Care31.08.2015Interim Report 2015H1 34

Global top 5 producer of nonwovens for hygiene

Supplies fabrics used in baby diapers, feminine hygiene and incontinence care products

Spunbond/spunmelt technology, an integrated one-step process – from raw material to fabric

Polypropylene is the key raw material

Strong regional business

3 production lines in Denmark

4 production lines in Malaysia

Printing facilities in Germany

Growing and staying market (no alternatives)

A regional industry ∙ customers and suppliers

Simple supply chain ∙ from PP to rolls of fabric

Large investments ∙ DKK +300m for a new line

High level of competence ∙ efficiency/quality

Low margin ∙ high volume

Service and innovation makes the difference

"Preferred" partner ∙ customized activities

Core business: Spunbond for hygiene

Large customers requiring good relationship

Sensitive, small and autonomous industry

Raw materials (few suppliers, linked to oil)

One supplier of machinery (Reifenhäuser)

Customers (limited number)

Commodity products (low-margin business)

Salary and level of energy in Denmark

Radical innovations are very difficult

HIGHLIGHTS THE BUSINESS MODEL

INDUSTRY CHARACTERISTICS

Revenue 1,788mEBITDA 308m- margin 17.2%

EBIT 171m- margin 9.6%

ROIC 14.4%Employees 447

2014 FINANCIALS

Asian market continues to grow and requires significant capex

Increasing focus on value-added products (softer, bulkier, loftier and printed)

Revenue ~1,700mEBIT 170-180m

2015 GUIDANCE

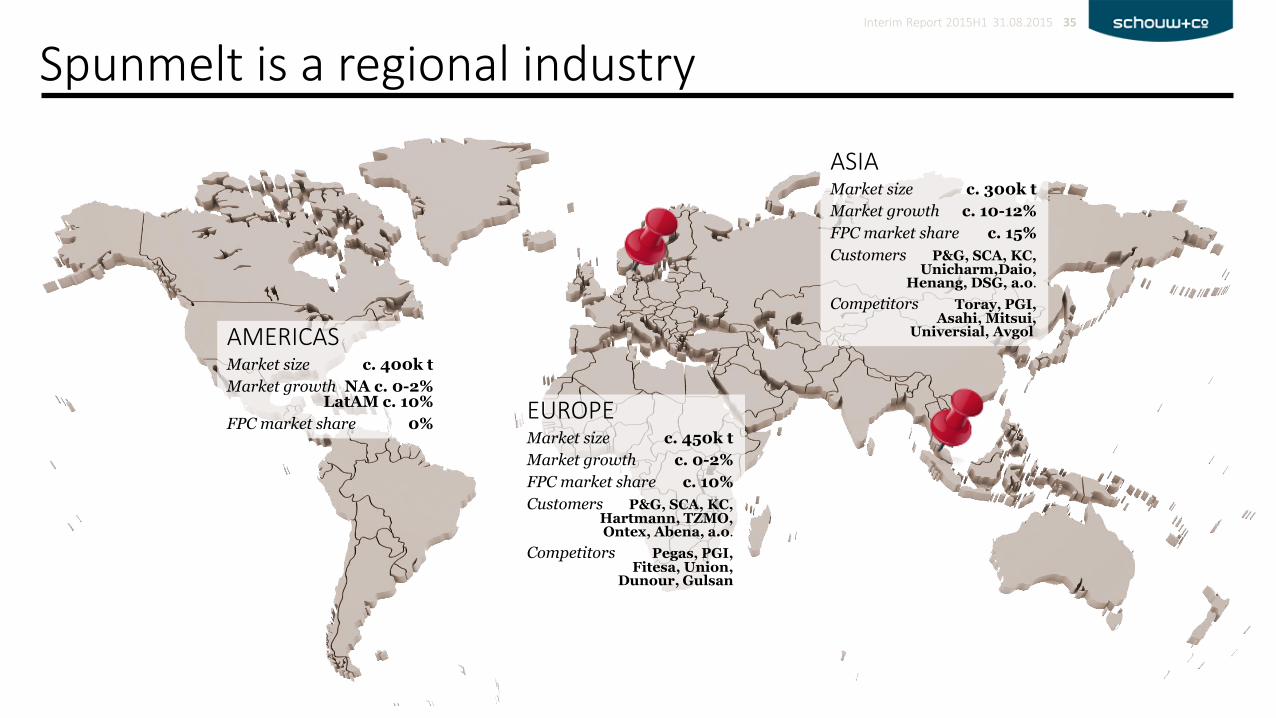

Spunmelt is a regional industry31.08.2015Interim Report 2015H1 35

EUROPEMarket size c. 450k t

Market growth c. 0-2%

FPC market share c. 10%

Customers P&G, SCA, KC,Hartmann, TZMO,Ontex, Abena, a.o.

Competitors Pegas, PGI,Fitesa, Union,

Dunour, Gulsan

ASIAMarket size c. 300k t

Market growth c. 10-12%

FPC market share c. 15%

Customers P&G, SCA, KC,Unicharm,Daio,

Henang, DSG, a.o.

Competitors Toray, PGI,Asahi, Mitsui,

Universial, AvgolAMERICASMarket size c. 400k t

Market growth NA c. 0-2%LatAM c. 10%

FPC market share 0%

Fibertex Nonwovens31.08.2015Interim Report 2015H1 36

European top supplier of industrial nonwovens

Huge versatility in product applications

Needle punching and spunlacing technology

State-of-the-art technology on all sites

Ensure critical mass / continue profit increase

Leverage on European market leader position and increase global presence

Strong competitiveness through operational improvements and state-of-the art techonology

Continue transformation; reducing dependency on volume/commodity products and growing value-added/specialty products

Building Composites

Geotextiles Concrete

About ⅓ of revenue

Infrastructure growing in emerging markets

Value added products e.g. within composites

Geotex. is commodity

Bedding Flooring

Furniture Acoustics

Hood insulation Trunk carpets

Parcel trays Wheel housing

About ⅓ of revenue

Market leader after French 2011 acquisition

Significant pipeline

Substitutes existing fabrics and part of car construction

About ⅓ of revenue

Dependent on economic cycles

Volume products

Ongoing application extension e.g. nano

16kt capacity10kt capacity 16kt capacity

7kt capacity 4kt capacity

HIGHLIGHTS AUTO

Revenue 1,048mEBITDA 128m- margin 12.2%

EBIT 62m- margin 5.9%

ROIC 8.4%Employees 547

2014 FINANCIALS

2015 will be a year of transition where new capacity will beinstalled and existingproduction lines will beupgraded.

EBIT target is 8-9%.

Revenue ~1,200mEBIT 75-85m

2015 GUIDANCE

STRATEGIC PRIORITIESCONSTRUCTION

INDUSTRIAL

Hydra-Grene31.08.2015Interim Report 2015H1 37

Leading Danish supplier of hydraulic components

Specialised trade and engineering business

Strong R&D resources taking active part in customer product development

Solid base in Danish aftermarket and OEM

Long-term growth and huge potential in the global wind turbine industry

Aftermarket customers (~25% of total revenue) Both premium and low-cost items at stock Predominantly distributed through dealers End customers within agro, lift/truck, transport

OEM customers (~25% of total revenue) Product know-how and customer support key Component distribution and own production Prod. of blocks, pipes and pump stations End customers are manufacturers of agricultural equipment, lift/trucks, boats, etc.

Hydra-Grene’s position Present in Europe, China, India and USA Strong within gear (filter blocks and systems) Total solutions in water cooling and pumps

Trends and drivers Turbine manufacturers wants fewer suppliers Established manufacturers setting the standards Increased documentation and quality More focus on aftermarket services

HIGHLIGHTS THE DANISH INDUSTRIAL BUSINESS

Revenue 566mEBITDA 78m- margin 13.8%

EBIT 60m- margin 10.6%

ROIC 22.6%Employees 230

2014 FINANCIALS

The offshore segment is gradually gainingimportance and willbecome a ‘thrid leg’.

Revenue >500mEBIT 50-60m

2015 GUIDANCE

SELECTED PRODUCTS AND BRANDS

THE GLOBAL WIND TURBINE INDUSTRY

Kramp

Leading European supplier of spare parts and accessories for the agricultural sector #1 in BeNeLux, Germany, Poland and Nordic countries

9 central warehouses covering 22 European countries

Combination of Kramp and Grene Grene wholly owned by Schouw & Co. since 1988

20% ownership in Kramp from non-cash merger between Grene and Kramp in 2013

Schouw & Co. owns 20%, management 50% and NPM Capital (Dutch long-term PE) 30%

Integration and harvesting synergies A perfect geographical match…

Expanding product ranges

Growing OEM business (partnerships)

Margin improvement through scale

Best practice (warehouse, IT, logistics)

Optimizing working capital (stockturn)

Potential annual synergies EUR 10-30m

31.08.2015Interim Report 2015H1 38

Nine distribution centers covers 22 European countries. Former Kramp in blue, former Grene in orange and Russian JV in turquoise

Revenue 4,906mEBITDA 529m- margin 10.8%

EBIT 405m- margin 8.3%

Employees 2,604

2014 FINANCIALS

Revenue ~5,250mEBIT 425-450m

2015 GUIDANCE

Contact

Investor Relations CEO/President

Kasper Okkels Jens Bjerg Sørensen

[email protected] schouw @ schouw.dk

+45 87 34 58 24 +45 86 11 22 22